Locally sparse function-on-function regression

Abstract

In functional data analysis, functional linear regression has attracted significant attention recently. Herein, we consider the case where both the response and covariates are functions. There are two available approaches for addressing such a situation: concurrent and nonconcurrent functional models. In the former, the value of the functional response at a given domain point depends only on the value of the functional regressors evaluated at the same domain point, whereas, in the latter, the functional covariates evaluated at each point of their domain have a non-null effect on the response at any point of its domain. To balance these two extremes, we propose a locally sparse functional regression model in which the functional regression coefficient is allowed (but not forced) to be exactly zero for a subset of its domain. This is achieved using a suitable basis representation of the functional regression coefficient and exploiting an overlapping group-Lasso penalty for its estimation. We introduce efficient computational strategies based on majorization-minimization algorithms and discuss appealing theoretical properties regarding the model support and consistency of the proposed estimator. We further illustrate the empirical performance of the method through simulations and two applications related to human mortality and bidding the energy market.

Keywords: Functional data analysis; Non-concurrent functional linear model; Overlap group Lasso;

1 Introduction

The undergoing technological advancement enables the collection and storage of high-resolution data that can be modelled as smooth functions (e.g., curves or surfaces). Functional data analysis (FDA) is a branch of statistics that models such data through suitable functional counterparts of successful methods and models developed for standard Euclidean data, such as clustering, regression, and classification (Ramsay and Silverman, 2005; Horváth and Kokoszka, 2012; Hsing and Eubank, 2015). Functional regression is one of the building blocks of FDA and has received remarkable attention in theory, methods, and applications (see Morris, 2015, for a recent review).

Herein, we focus on the general case of functional regression with functional responses. We developed a model and related methods for its implementation, representing a bridge between two successful alternative models. To set up the notation, we assume that for the generic -th statistical unit , a functional response with is available along with functional covariates ( and ) and and subsets of , denoting the domains of the functional data and , respectively. The first available modelling strategy, namely, the concurrent functional linear model, assumes that the functional data are observed on the same domain, i.e., for , and the relation between the response and the predictors is given as

| (1) |

where is a functional intercept, are functional regression coefficients, and are functional zero-mean random errors. In the concurrent model, the covariates influence only through their values at the domain point . As a more general approach, the nonconcurrent functional linear model allows to entirely depend on the functional regressors, and specifically,

| (2) |

where is the kernel function determining the impact of evaluated at domain point on . The nonconcurrent model is the default choice when the response variable and the covariates do not share the same domain or, even when sharing the same domain, the value of can be assumed to depend on the functional regressors entirely and not just for their values at . The nonconcurrent model offers great flexibility, but the flexibility increases complexity, both in terms of interpretation and computation. An in-between solution, motivated by applications in which is a time domain, is represented by the so-called historical functional linear model of Malfait and Ramsay (2003). This approach restricts the domain of integration of the integral in (2) to the set leading to

| (3) |

Note that this model, for the general point , can be interpreted as a nonconcurrent model up to point . Despite providing an interesting intermediate solution, there are many situations in which the dependence through the interval is difficult to be justified.

Herein, we introduce a hybrid solution that combines the simplicity in terms of interpretation of the concurrent and historical models with the flexibility of the nonconcurrent model. Our goal is to introduce a noncconcurrent functional linear model that allows for local sparsity patterns. Specifically, we want that for with being a suitable subset of , thus inducing locally sparse Hilbert-Schmidt operators . In defining , we do not consider those regions where is zero because the kernel changes its sign or where it is tangential to the plane 0. A formal definition of used henceforth is thus

where is a ball of radius of the point and is the Lebesgue measure. Note that, although in (3) the region is fixed a priori and set equal to , we do not require any specific sparsity pattern, rather we learn it from the data, as discussed in the following sections.

Different approaches to sparsity and regularization have been used in regression models for functional data, but none of them can be readily adapted for our purpose since they are all defined in a simpler function on scalar regression setting, i.e., are scalar responses. Lee and Park (2012), for example, after representing the functional regression coefficient with a splines basis expansion, introduced a Lasso-type penalty for basis coefficients. The proposed solution has the great benefit of regularizing the estimator of the functional regression coefficients and enjoys nice asymptotic properties. However, several zeroes in the basis function coefficient do not map to a zero in the functional object represented by the basis, and thus, using this approach would not necessarily induce sparsity in the functional coefficients. James et al. (2009) proposed a model with an interpretable functional regression coefficient that can be exactly zero, flat, and different from zero, or linear in local areas of its univariate domain. This is achieved by inducing sparsity in the general -th derivative of the functional regression coefficient using a constant basis expansion and an penalization. On the surface, this solution seems intuitive and successful, but a zero on a general subregion of the regression function requires grid points that fall into the region to be simultaneously zero, which the plain regularization does not warrant in general. In addition, in our setting, the regression coefficient is not a univariate curve but a bivariate surface, and the use derivatives in two dimensions is less straightforward to apply. Lin et al. (2017) proposed a smooth and locally sparse estimator of the coefficient function based on the combination of smoothing splines with a functional smoothly clipped absolute deviation (SCAD) penalty of Fan and Li (2001). Zhou et al. (2013) proposed a two-stage sparse estimator exploiting the properties of B-spline basis expansion, where an initial estimate is obtained using a Dantzig selector (Candes et al., 2007), and the spline coefficient is later refined using a group adaptation of the SCAD penalty. The only contribution dealing with a function-on-function situation is the recent manuscript by Centofanti et al. (2020) who estimated sparse functional coefficients through a functional version of the Lasso penalty.

Our proposed solution exploits a B-spline local property similarly to Zhou et al. (2013), but directly relies on minimizing a suitable objective function, as discussed in Section 2. This objective function includes an overlapping group-Lasso penalty (Jenatton et al., 2011) that ensures the desired sparsity in . It is minimized using a fast and reliable numerical strategy proposed in Section 3. The properties of the induced estimator are discussed in Section 4. A detailed simulation study to evaluate the empirical performance of the proposed model compared to that of the state-of-the-art models is presented in Section 5. The results show that the proposed model outperforms other models in estimating both the region of sparsity and the value of the functional regression coefficient where it is different from zero. In Section 6, we specify the model in functional time-series settings and analyze two datasets related to human mortality and bidding in energy markets. Our analysis suggests that bridging between concurrent and nonconcurrent functional models results in better performance both in terms of goodness-of-fit and qualitative interpretation of the results. Section 7 concludes the paper.

2 Locally sparse functional model

Without loss of generality, we consider the case in which the functional data are centered in zero, and a single functional covariate is available for , so that for all and . We also assume that is bounded and defined on a compact domain . Thus, (2) becomes

| (4) |

The proposed locally sparse functional regression (LSFR) model relies on the introduction of a specific basis representation for the kernel and the minimization of a suitable objective function. These are described in the next two sections.

2.1 Kernel basis representation

We employ the common FDA practice of representing the functional objects using of basis expansions. Specifically, we select two bases in , e.g., and , where each is defined on , each is defined on , and the number of basis is and , respectively. Exploiting a tensor product expansion of these two, we represent the kernel in (4) as

alternatively, in matrix form as

| (5) |

where for and .

To achieve the desired sparsity property in , similarly to Zhou et al. (2013), first assume that the elements in equation (5) are B-splines (De Boor, 1978) of order . A B-spline of order is a piecewise polynomial function of degree and is defined by a set of knots, which represent the values of the domain where the polynomials meet. Based on (5), and are B-splines of order with and interior knots, respectively, and two external knots each.

Suitable zero patterns in the B-spline basis coefficients of induce sparsity of . Let and denote the knots defining the tensor product splines in (5), with and . For and let be the rectangular subset of defined as

| (6) |

Hence, to obtain for each , it is sufficient that all the coefficients with and are jointly zero. In general equals zero in the region identified by two pairs of consecutive knots if the related block of coefficients of is entirely set to zero. This suggests that should be suitably partitioned in several blocks of dimensions on which a joint sparsity penalty is induced. This is discussed further in the next section.

2.2 Sparsity-inducing norm

Consistent with the above discussion and with successful approaches in statistics and machine learning, we minimize an objective function having the following form:

| (7) |

where the first summand is a goodness-of-fit index while the second a suitable penalty.

Studies on statistics and machine learning have proposed numerous approaches for the sparsity-inducing , including Lasso (Tibshirani, 1996; Efron et al., 2004). In our setting, however, Lasso would yield sparsity by treating each parameter individually, regardless of its position in , which is against our desiderata. The first extension of Lasso involving the concept of groups of coefficients is the group-Lasso reported by Yuan and Lin (2006). This approach considers a partition of all the coefficients into a certain number of (disjoint) subsets and eventually allows some of these groups to shrink to zero.

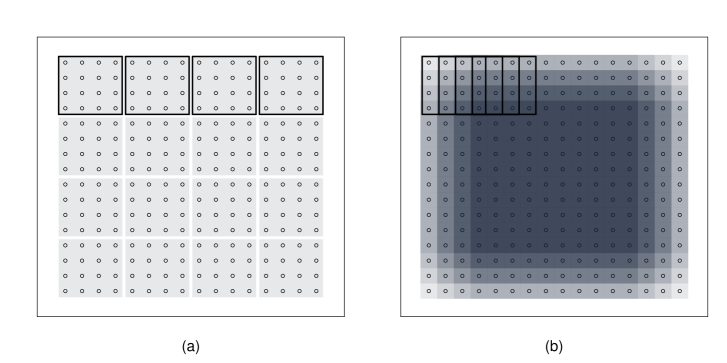

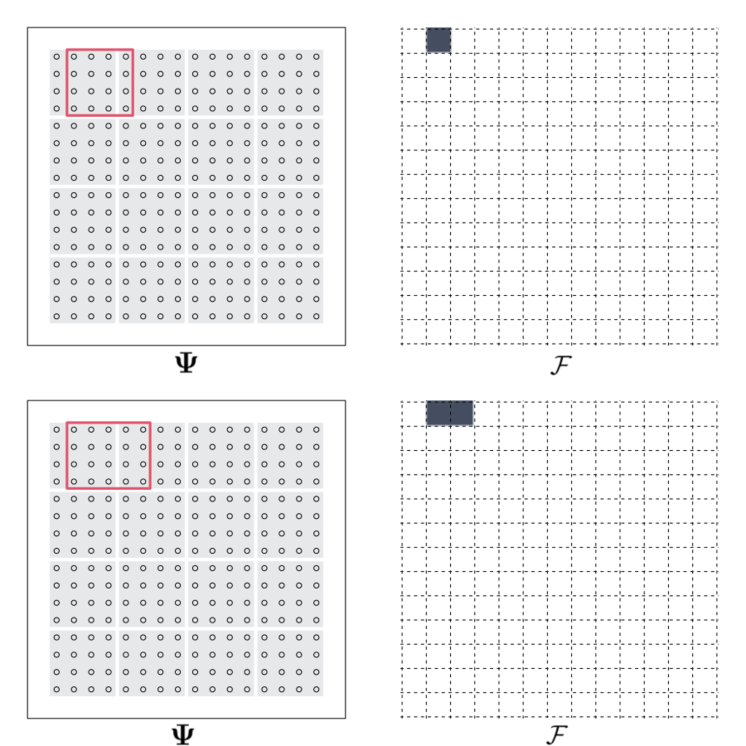

On the surface, the group-Lasso approach is a promising solution to our problem, but we discuss this in more detail in what follows considering the graphical representation of a possible grouping, coherent with the group-Lasso definition, reported in panel (a) of Figure 1. Setting all coefficients belonging to one of the tiles of panel (a) to zero will force for in a specific set . In fact, this kind of solution does not provide enough model flexibility in many respects. First, the construction requires and to be multiple of . Second, it is impossible to induce for and for belonging to neighboring sets of for any and not equal to and , respectively, where and are nonnegative integers. Third, for belonging to the union of two contiguous rectangles if and only if two consecutive and disjoint blocks of coefficients are jointly zero, leading to for each belonging to the superset . Figure 6 in the Appendix shows two examples of these key limitations of the disjoint grouping of coefficients.

To overcome these issues, instead of a disjoint partition, we define an overlapping sequence of blocks of size . Specifically, we introduce the block index with denoting the total number of blocks. Notably, there is a block for each set . The generic -th block contains the coefficients in the set

| (8) | |||||

where represents the remainder of the division . A graphical representation of this construction is shown in panel (b) of Figure 1. This overlapping group structure allows to be the union of any set in (6) by moving a block of minimum size, depending on , with steps of size one, and thus, allowing for greater flexibility in the definition of the subset , with respect to the disjoint grouping of panel (a). A precise characterization is formalized in Proposition 1, in the next section.

The above construction suggests specifying a penalty for overlapping groups of coefficients, which has attracted significant interest in the last decade. For example, Zhao et al. (2009) focused on overlapping and nested groups of coefficients motivated by modeling hierarchical relationships between predictors. More general overlapping group-Lasso penalties have been proposed by Jacob et al. (2009) and Jenatton et al. (2011), which define suitable norms for inducing a penalty that can model specific patterns for the support of the vector of coefficients—the latter being the set of coefficients different from zero. The difference between these two approaches is that Jenatton et al. (2011) introduced a penalty inducing supports that arise as intersections of a subset of suitable groups, whereas Jacob et al. (2009) introduced a penalty that induces supports that are rather the unions of a subset of the groups. Lim and Hastie (2015) exploited the construction of Jacob et al. (2009) to learn the main and pairwise interaction terms of categorical covariates in linear and logistic regression models, imposing through the overlapping group structure hierarchical regularization with a similar motivation as Zhao et al. (2009) but also proposing an efficient computational strategy.

In classical regression, the interest lies in the support of the vector of regression coefficients. Consistent with our motivations, instead, we focus on the sparsity structure of the matrix of coefficients rather than its support. Hence, we specify (7) as

| (9) |

where is a fixed penalization term, and in (7) specifies in the sum of Euclidean norms , where , and represents the Hadamard product. The index denotes the block of coefficients in , with the first blocks being consistent with (8) and the last block containing all coefficients in . Vectors of size , denoted by , contain known constants that equally balance the penalization of the coefficients in . This balancing is needed to account for the fact that the parameters close to the boundaries of the matrix appear in fewer groups than central ones, as shown by the color scaling of panel (b) of Figure 1. Specifically, the generic vector is defined as where is the selection matrix with general entry , defined as 1 if the parameter belongs to group and 0 otherwise and is the matrix with general element defined as Note that this penalty constitutes a special case of the norm defined by Jenatton et al. (2011).

3 Computation

Before describing an efficient computational strategy for our LSFR model, we introduce the empirical counterparts of the quantities described in the previous section assuming to observe a sample of response curves with on a common grid of points, i.e. . Let also be the related functional covariate observed on a possibly different but— common across —grid of points, that for simplicity and without loss of generality, we assume of length . Let be the matrix with in the rows. Let and be the and matrices defined as

Let and be the matrices obtained as and , with . Model (4) can be equivalently written in matrix form as

Applying the vectorization operator on each side of the equality above, we have

where , is the vector of coefficients of dimension , , and is the design matrix of dimension . Therefore, for a given tuning parameter , the optimization problem becomes

| (10) |

where is a diagonal matrix whose elements correspond to the elements of the vector defined in the previous section. The following result is about the uniqueness of the solution of the optimization problem in equation (10) thus leading to the uniqueness of the estimator . Its proof is reported in the Appendix.

Theorem 1.

In practice, however, the non-separability of the penalty function when groups overlap, makes the optimization problem in equation (10) not straightforward. The non-separability of the overlap group-Lasso penalty function prevents the application of standard coordinate descent algorithms that cycle through the parameters and updates them either individually (as for the Lasso) or by groups (as for the group-Lasso), (see, e.g. Wu and Lange, 2008; Bach et al., 2012; Huang et al., 2012; Yang and Zou, 2015). We propose to map the optimization in equation (10) to an optimization of a fully convex and differentiable function by leveraging the Majorization-Minimization (MM, hereafter) principle firstly introduced by Ortega and Rheinboldt (1970) and developed by Hunter and Lange (2004); Lange (2010, 2016). The MM approach is a general prescription for constructing optimization algorithms that operates by creating a surrogate function that minorizes (or majorizes) the objective function. The surrogate function is then maximized (or minimized) in place of the original function. Various existing approaches in statistics and machine learning can be interpreted from the majorization-minorization point of view, including the EM algorithm (Neal and Hinton, 1999; Wu and Lange, 2010) or boosting and some variants of the variational Bayes methods (Wainwright and Jordan, 2008). Here the MM approach is employed for the purpose of delivering a quadratic function that majorizes the convex objective function in (10). The MM algorithm has been introduced within the context of and penalized regressions by Wu and Lange (2008). The authors consider both the Lasso and group-Lasso penalty and provide cyclic coordinate descent algorithms for both problems. Coordinate descent algorithms are simple, fast and stable and they usually do not require the inversion of large matrices (Hunter and Lange, 2004). However, for large dimensional models with high level of sparsity and separable penalty, the coordinate-wise gradient provide all the relevant information to update parameters and most of the parameters are never updated from their starting value of zero. Nevertheless, when the level of sparsity is either unknown or moderately low, coordinate-wise updates no longer represent the best strategy. This is exactly the framework here considered. Therefore, leveraging the supporting hyperplane paradigm (see Lange, 2016) and the Sherman–Morrison–Woodbury identity we deliver an efficient MM algorithm for our overlap group-Lasso penalty that jointly updates the non-zero regression coefficients at any iteration. Observe also that, because of the analytical form of the overlap penalty function (see Huang et al., 2012), efficient block-wise updates as in Qin et al. (2013) cannot be considered here. Our MM algorithm instead serves the purpose of delivering an efficient solution to the otpimization problem in equation (10) without imposing any specific group conformation and finds application even in more structured group-type penalties, (e.g. Bach et al., 2012; Jenatton et al., 2011).

Any MM algorithm iterates between two steps: at iteration , a majorizer function is obtained conditioning on ; the value for is obtained minimizing . As a further benefit of exploiting the MM majorization principle, the MM iterations , for possesses the decent properties driving the target function downhill.

Several paradigms can be exploited to derive a valid majorizer of the overlap group penalty term in (10), (see, e.g. Lange, 2016, for an exhaustive discussion). Here, we leverage the dominating hyperplane principle that introduces an upper bound for the strictly concave function , i.e. for any . This manoeuvres separate parameters and reduce the surrogate to a sum of linear terms and squared Euclidean norms. Consistently with this, we introduce the following surrogate function that majorizes (10) at

| (11) |

where is the value of the parameter at the -th iteration of the MM algorithm. The important consequence of this result is that solution of problem (10) can be obtained through the iterative minimization of (11), where (11) is convex and differentiable. A compact form for the minimization problem of the surrogate function of (11) is

| (12) | ||||

| (13) |

where and are constants that depend on the -th iteration:

| (14) |

The explicit solution of the minimization problem in equations (12)-(13) at the -th iteration is

| (15) |

where . The MM algorithm is described in Algorithm 1, reported in the Appendix. An important consideration in using a particular algorithm is the amount of work the computer is required to carry out in running it which is measured in terms of the number of floating-point operations (FLOPS) that are needed. The computational cost of Algorithm 1 is provided in the Appendix, at Proposition 2.

3.1 Efficient MM for the generalised ridge inversion

The MM parameters update in equation (15) suffers from two major drawbacks. First, it requires the inversion of a potentially large-dimensional ridge-type design matrix and, second, it does not exclude the pathological case where one or more of the denominators of the weights in (14) are exactly zero. The usual solution for the latter problem consists to perturb by adding a small to the -norm, (see Hunter and Lange, 2000). In what follows, instead, we rely on a different solution. Specifically, let be a diagonal matrix and define the symmetric and positive definite matrix . The computation of the MM update in equation (15) requires the inversion of the symmetric full matrix at any iteration which takes on the order of arithmetic operations (Golub and Van Loan, 2013). Since the matrix changes at any iteration performing the QR decomposition of becomes prohibitive even for moderately large values of .

Given the diagonal structure of the matrix , using the Sherman-Morrison-Woodbury matrix identity reduces the problem of inverting for a fixed to the simpler problem of computing

| (16) |

where the full matrix with can be computed without loss of generality through the spectral decomposition of . Specifically, let be such a decomposition, then . Therefore, the MM update only requires the spectral decomposition of the symmetric matrix to be computed at any iteration. However, as pointed by the following remark, as a byproduct of our procedure, we obtain the indirect solution to the problem of zeros in the surrogate penalty function.

Remark 1.

As iterations proceeds, it may happen that some of the weights associated to a sequence of zeros on the vector larger than becomes closer and closer to zero. Leveraging the Sherman-Morrison-Woodbury matrix identity prevents the weights to explode.

We can exploit the fact that in equation (15) at some iteration may become zero, i.e. , to provide a fast and efficient solution to the problem of finding the spectral decomposition of for moderately large. Let and with be a disjoint partition of the space spanned by such that , and let and be the corresponding partition of the diagonal matrix , then

Now, assume that at the -th iteration, , then , which only requires the spectral decomposition of the matrix . Additional computational considerations and results are reported in the Appendix.

4 Theoretical properties

In this section, we provide appealing theoretical properties for our LSFR model and for the related estimator of arising from (5) and (10). All the proofs are reported in the Appendix. We first describe the sparsity patterns that we can induce through our LSFR construction in the following proposition.

Proposition 1.

Let be the collection of all the sets described in (6), the power set of , and be the subset of in which . Then with and

The following two results show that the introduced model structure is sufficiently flexible to cover the two extreme situations represented by the concurrent and nonconcurrent models.

Remark 2.

Assume . Let be the subset of where in the concurrent model. Let the superset of defined as

Then .

Remark 3.

If for each then .

Remark 2 implies that for a sufficiently high number of knots in the tensor product spline expansion, the sparsity structure of a concurrent Hilbert-Schmidt operator can be well approximated by the proposed formulation. A similar property holds also for the historical model (Malfait and Ramsay, 2003). At the same time, Remark 3 trivially states that nonconcurrent model is included in our class, implying that relatively small values of the penalty parameter lead to no sparsity of .

The following two results determine interesting consistency properties, namely, that the method correctly identifies the region where the true kernel is null and vice versa. Specifically Theorem 2 assumes that the true kernel lies in the vector space generated by the tensor product and Theorem 3 relaxes this assumption. Both theorems hold under the correct model specification and when are uncorrelated Gaussian errors with variance . Both results are adaptations of the consistency results of Jenatton et al. (2011).

Before stating the results, we define the following quantities based on the assumption that there exists a true kernel . In Theorem 2 we assume that belongs to the vector space and thus that there exist a unique matrix of coefficients representing it. Furthermore, let be the set of indices of the true non-zero groups and the set of the indices of the non-zero coefficients . Let the matrix containing the columns of associated to the true non zero coefficients and its complement. Define the norm

which is the modification of the penalising norm of (9) considering the sum over the inactive groups. Let further be its dual norm. Finally let be the vector containing, for , the elements

Theorem 2.

Let be the true HS operator with where is the vector space defined by the tensor product of the two B-splines basis and both with fixed dimensions and , respectively. Let be the induced true sparsity set, i.e. for each . Define the event as

For , , , , then

The next theorem avoids the strict assumption of . The main idea is to introduce suitable approximations of and the induced and study consistency of the estimator to those approximations. Specifically, we let be the subset of of maximum Lebesgue measure belonging to the power set and define as

In what follows , and the related norm and its dual, are defined with respect to the unique associated to .

Theorem 3.

Let be the true HS operator and the true induced sparsity set, i.e. for each . Define the event as

with a positive constant. Let be the number of columns of . For , assume with

| (17) |

If and , then the probability of the event is lower bounded by

where and are positive constants.

5 Simulation study

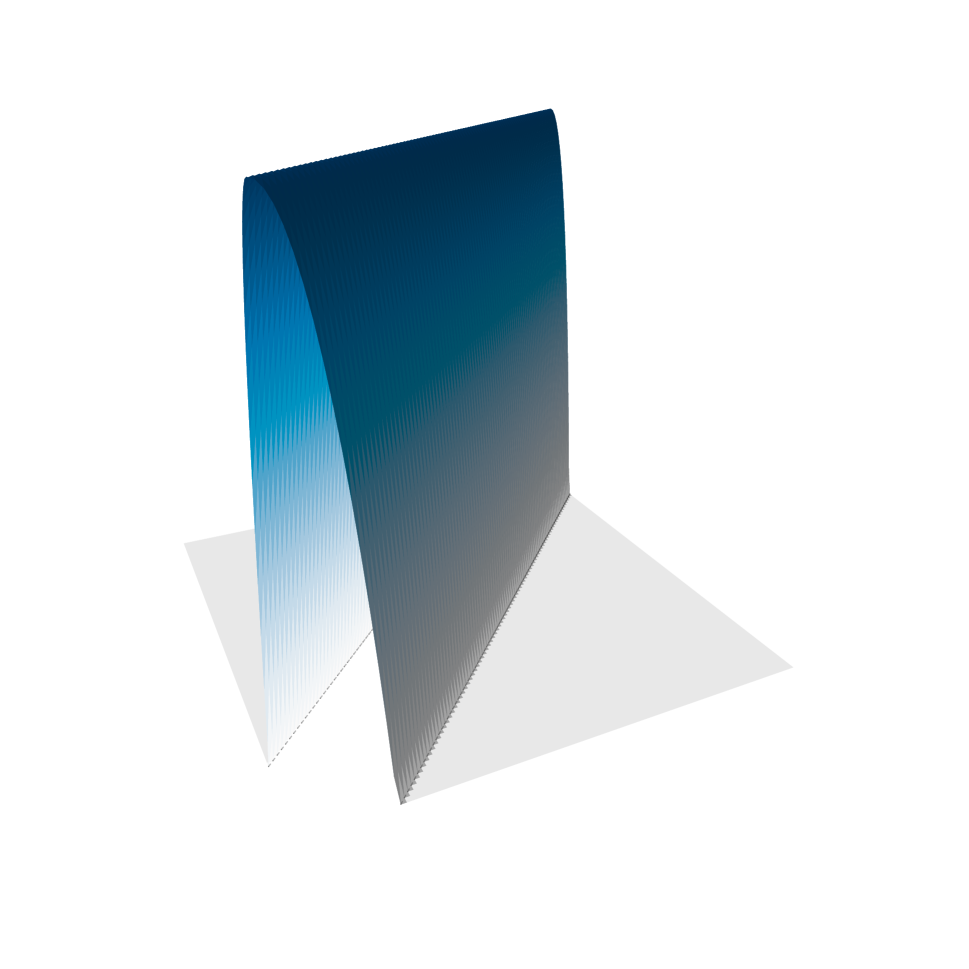

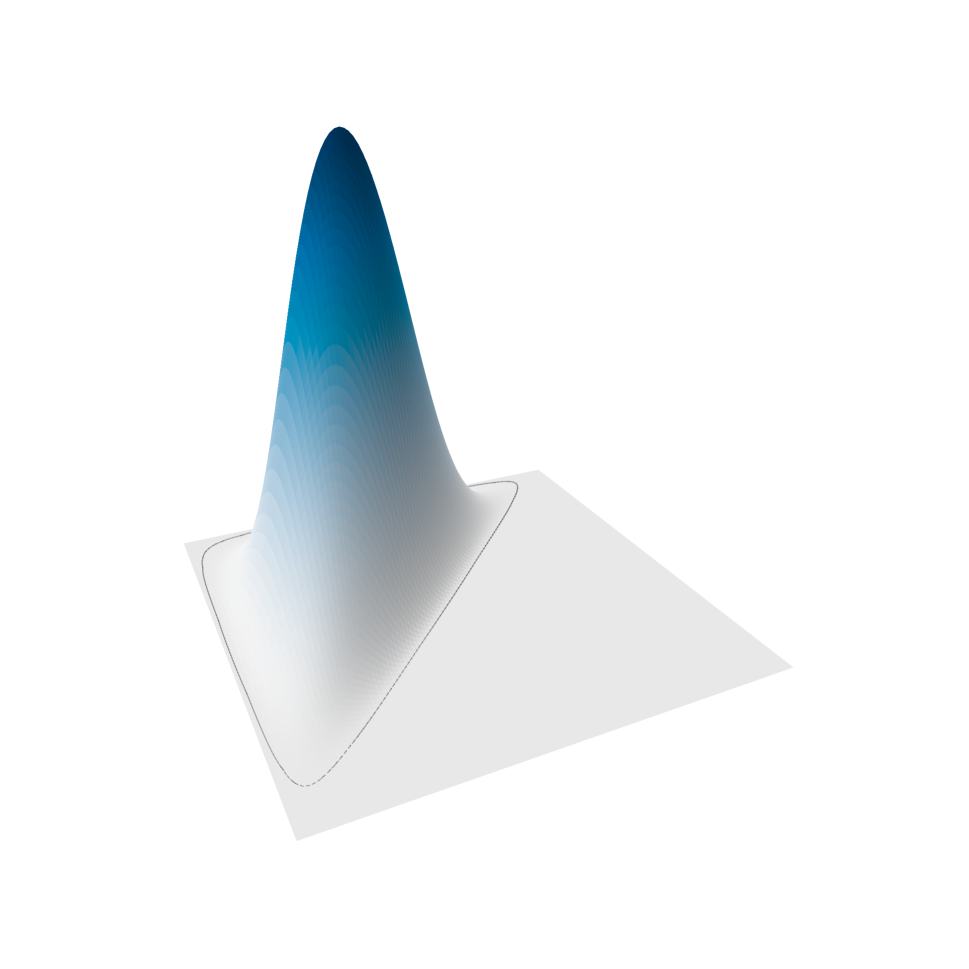

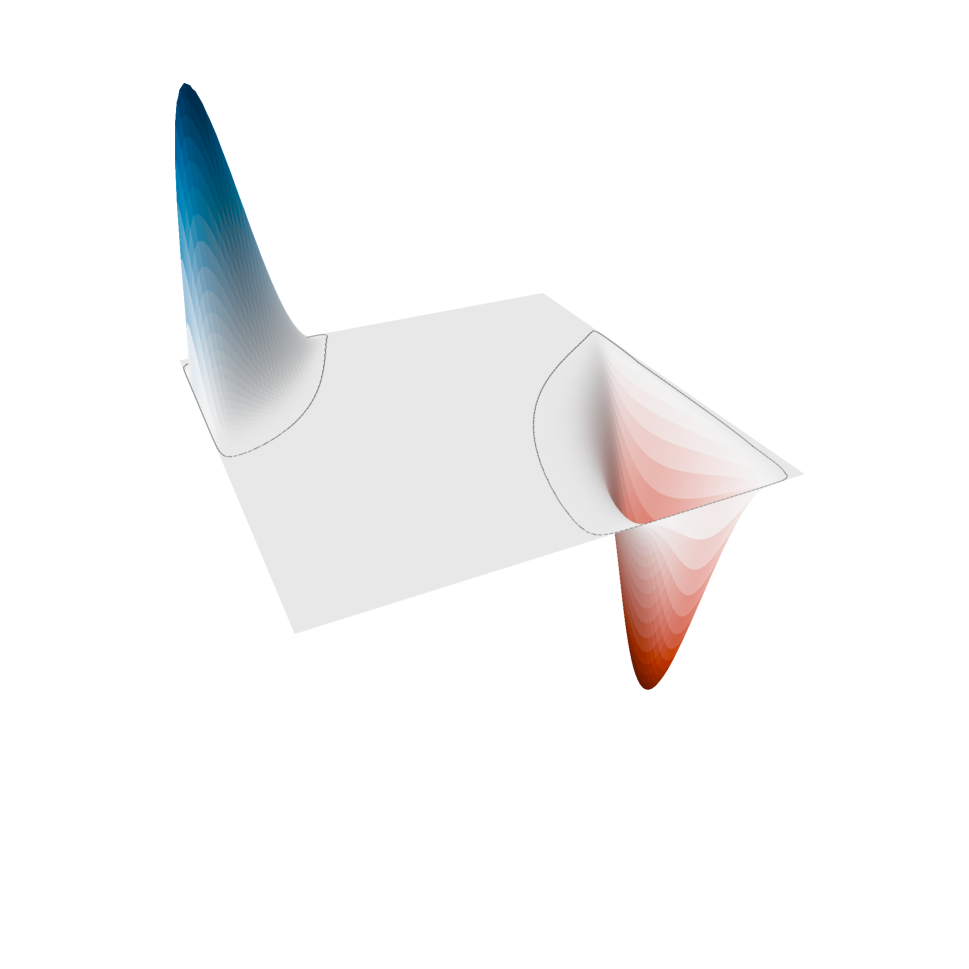

In this section we assess the empirical performance of our LSFR model by means of simulations. We generated a sample of a functional covariate from cubic B-splines basis with 15 evenly spaced knots between 0 and 1. These functional data are assumed to be observed on an equispaced grid of points and the sample size is . Conditionally on these functional covariates we generated functional responses as under four different levels of sparsity of the operator and two different signal-to-noise ratios.

The first and the second scenario focuses on a quasi–concurrent and historical relations, respectively. The third scenario is associated to a local dependence between the dependent variable and the functional covariate with the region being the union of two non–intersecting rectangles. Finally, last scenario assumes no sparsity. Graphical representations of the kernels are showed in Figure 2.We vary the signal-to-noise ratio with

We choose and leading to coefficients in . For each combination of , , and SNR we simulated replicated datasets, leading to independent datasets.

We compare our LSFR with the results obtained minimizing (7) with Ridge, Lasso, and Elastic-net penalties (Hastie et al., 2009). Classical group-Lasso penalty has not been fitted due to its limitations discussed in Section 2.1. We expect the Ridge approach to be the best competitor in the last scenario and in general if estimation is evaluated in the non-sparse regions of the true kernels. On the other side we expect Lasso to be the best competitor in detecting the sparse regions. The Elastic-net minimization and our LSFR solution are expected to take the best of both Lasso and Ridge.

All methods depend on the choice of the tuning parameter . We run each model on a fine grid of and choose as final estimate for each method, the one minimizing the prediction error for the general estimator of , i.e.

where the sum is defined on external validation set of size 200. The range of possible depends on the specific methods and for LFSR we refer to (20) in Appendix. For all competing methods we rely on their implementation in the package glmnet (Friedman et al., 2010).

The final estimates are evaluated in both subsets of where the true function is zero or not, on a third independent test set of size 1,000. Specifically, we define two partial integrated square error measures as

| (18) |

representing the error in not estimating the sparsity of the true kernel and the estimation error when the true kernel is smooth, respectively. As a global measure, we use the integrated squared error on the whole , which can be obtained as a suitable convex combination of the previous measures, i.e.

| (19) |

| LSFR | Lasso | Ridge | Enet | |||||

|---|---|---|---|---|---|---|---|---|

| S1 | 0.18 (0.04) | 1.07 (0.20) | 0.18 (0.06) | 2.76 (0.44) | 0.66 (0.11) | 1.12 (0.22) | 0.26 (0.06) | 1.34 (0.23) |

| S2 | 0.28 (0.08) | 1.63 (0.34) | 0.31 (0.12) | 4.08 (0.67) | 0.98 (0.17) | 1.74 (0.35) | 0.42 (0.12) | 2.03 (0.40) |

| S3 | 0.14 (0.05) | 1.66 (0.36) | 0.37 (0.13) | 16.24 (2.06) | 1.02 (0.20) | 1.48 (0.31) | 0.39 (0.11) | 2.08 (0.40) |

| S4 | 0.11 (0.02) | 0.58 (0.09) | 0.08 (0.03) | 1.45 (0.24) | 0.34 (0.06) | 0.56 (0.09) | 0.14 (0.03) | 0.71 (0.11) |

| S1 | 0.04 (0.03) | 0.51 (0.14) | 0.12 (0.07) | 1.80 (0.37) | 0.52 (0.14) | 0.75 (0.18) | 0.16 (0.08) | 0.68 (0.17) |

| S2 | 0.08 (0.05) | 0.82 (0.22) | 0.23 (0.13) | 2.42 (0.47) | 0.86 (0.21) | 1.21 (0.26) | 0.30 (0.13) | 1.09 (0.25) |

| S3 | 0.08 (0.05) | 0.74 (0.21) | 0.32 (0.16) | 9.98 (2.75) | 0.96 (0.25) | 1.16 (0.26) | 0.39 (0.14) | 1.04 (0.23) |

| S4 | 0.02 (0.01) | 0.23 (0.05) | 0.04 (0.02) | 1.12 (0.22) | 0.26 (0.07) | 0.33 (0.07) | 0.06 (0.03) | 0.29 (0.06) |

| S1 | 0.26 (0.06) | 0.58 (0.11) | 0.25 (0.09) | 1.01 (0.19) | 0.86 (0.19) | 1.10 (0.16) | 0.32 (0.09) | 0.69 (0.11) |

| S2 | 0.32 (0.09) | 0.82 (0.20) | 0.32 (0.15) | 1.29 (0.27) | 1.14 (0.30) | 1.57 (0.27) | 0.40 (0.15) | 0.96 (0.20) |

| S3 | 0.25 (0.07) | 0.62 (0.14) | 0.47 (0.14) | 7.17 (1.45) | 1.18 (0.29) | 1.40 (0.20) | 0.41 (0.12) | 0.91 (0.17) |

| S4 | 0.22 (0.04) | 0.36 (0.06) | 0.21 (0.05) | 0.68 (0.13) | 0.56 (0.11) | 0.61 (0.09) | 0.27 (0.07) | 0.46 (0.08) |

| S1 | – | 0.76 (0.11) | – | 2.13 (0.26) | – | 0.93 (0.12) | – | 1.08 (0.13) |

| S2 | – | 1.07 (0.16) | – | 2.62 (0.26) | – | 1.30 (0.17) | – | 1.48 (0.17) |

| S3 | – | 1.04 (0.18) | – | 5.87 (0.81) | – | 1.10 (0.18) | – | 1.34 (0.20) |

| S4 | – | 0.42 (0.06) | – | 1.09 (0.17) | – | 0.53 (0.06) | – | 0.61 (0.08) |

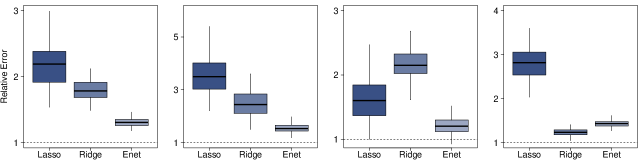

5.1 Results

Table 1 reports and for four different settings. As default setting, we consider , and . As second setting, we decrease the while keeping fixed and . In the third, we assess the effect of changing the resolution of the kernels’ basis representations letting with and . Finally, we assess the effect of a bigger sample size letting while keeping the default and . For all these settings, the performance of each method is evaluated for all the four kernels.

The proposed LSFR model exhibits good performance consistently in all settings and considering both the evaluation metrics. Specifically, our approach achieves a uniformly lower both with respect to Ridge and Elastic-net in all settings while presenting similar performance with respect to Lasso. In fact the results in terms of are broadly comparable for our LSFR and the Lasso for the estimation of the first and third kernel, while our LSFR is even slightly better in estimating the second kernel. Looking at , as expected, the performance of the Lasso and of the Ridge and Elastic-net are flipped. The proposed LSFR model, however, consistently outperforms all competing methods also in terms of .

Different values of SNR, , or and have different impacts on the results. Lowering the signal-to-noise ratio or increasing the sample size reduces —resp. increases— the errors almost proportionally among different estimation procedures. On the contrary, changing the number of basis from 20 to 40 has a relevant impact on the results. Particularly, a dramatic increase of is observed for Lasso, in all scenarios. This can be explained by the fact that using a larger number of bases is equivalent to reduce the support of each element of the basis. Consistently with this, Lasso penalizes coefficients that are much more correlated, yielding to an erratic sequence of estimated coefficients. Conversely, the larger number of bases of the third setting does not negatively affect the remaining methods including our LSFR model, but instead it allows for a potentially better identification of small sparse regions impossible to detect with a lower number of bases.

Figure 3 reports the boxplots of the global relative efficiency of the three competing methods, defined as the ratio between the three different and the achieved by our LSFR model in the default setting. All boxplots are above one, witnessing that the proposed method uniformly attains a lower . Exception made for the third scenario, Lasso is the worst method, while Elastic-net is the most flexible, as expected. Similar results can be noticed for the other simulation settings.

6 Applications

6.1 Swedish Mortality

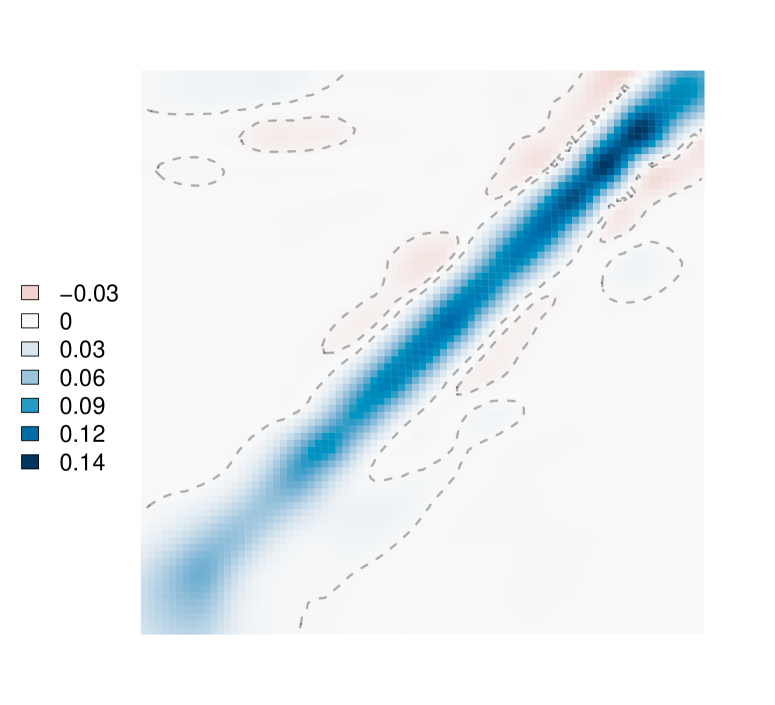

We apply the proposed LSFR model to the well-known Swedish Mortality dataset, available from the Human Mortality Database and considered one of the most reliable dataset on long-term longitudinal mortality. We focus on the analysis of the log-hazard rate functions of the Swedish female population between the years 1751 and 1894. The goal of our analysis is to model the log-hazard function at a specific calendar year by using the log-hazard function at previous year . The log-hazard rate for year and age is computed as the logarithm of the ratio between women born on year who died at age and women born on year still alive at age . An underlying autoregressive linear relation between and is assumed and specifically

The estimated kernel can be interpreted as the influence of the log-hazard rate at year and age on the log-hazard rate at year and age . Existing studies (Ramsay et al., 2009; Chiou and Muller, 2009) show that the hazard function at year and age is mainly influenced by the hazard function at the previous year at age , resembling a quasi–concurrent relation. However, none of these studies reports the total absence of relation when and are far away and the corresponding estimated surfaces exhibit nonvanishing fluctuations even near the boundaries of their bivariate domains.

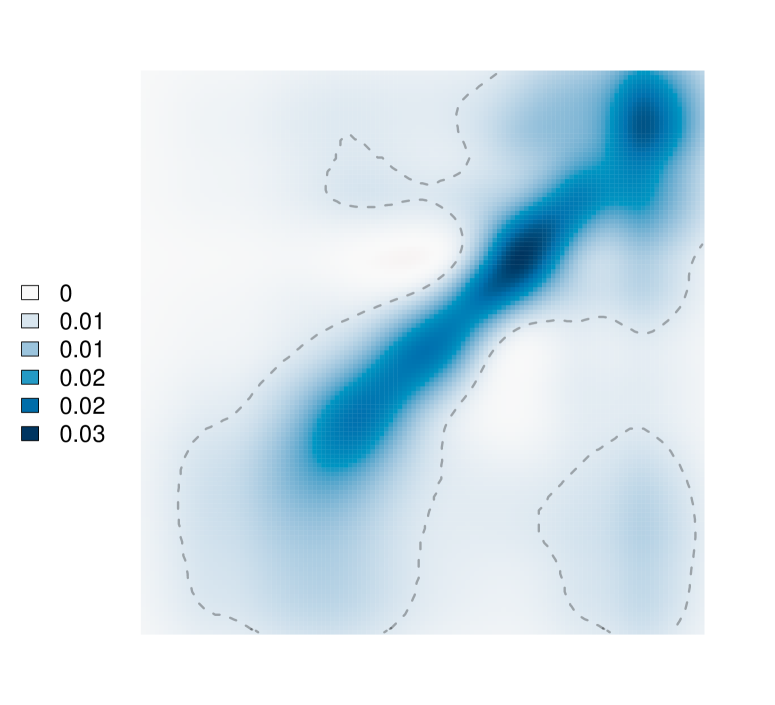

We implement the proposed locally sparse estimator by minimizing the objective (10) with , basis functions on each dimension and we select the optimal value of by means of cross–validation. Perspective and contour plots of the estimated kernel are depicted in Figure 4.

Our estimate shows a marked positive diagonal confirming the positive influence on the log-hazard rate at age of the previous year’s curve evaluated on a neighborhood of . At the same time, the flat zero regions outside the diagonal suggest that there is no influence of the curves evaluated at distant ages. Our estimate is more regular than previous approaches and its qualitative interpretation sharper and easier. Refer, for example, to Figure 10.11 of Ramsay et al. (2009).

This result witnesses the practical relevance of adopting the proposed approach. Indeed, the resulting estimates, while being reminiscent of a concurrent model—inheriting its ease of interpretation—it gives further insights and improves the fit, representing the desired intermediate solution between the concurrent and nonconcurrent models.

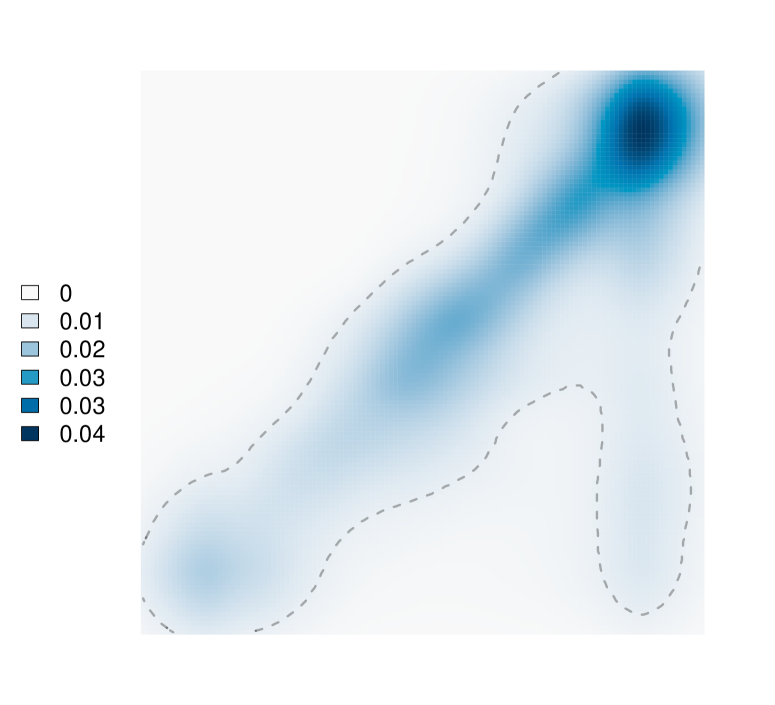

6.2 Italian Gas Market

As second illustrative example, we focus on the Italian natural gas data first analyzed by Canale and Vantini (2016) by means of a concurrent functional time series regression fitted under a Ridge-like penalty. Data consists on 375 pairs of demand and supply curves related to the Italian gas trading platform in 2012. Details on how the curves are constructed from the original bids can be found in Canale and Vantini (2016). The domain of the demand and supply curves represent the quantity and the price of the natural gas, respectively. The demand (resp. supply) curves are subject to equality and inequality constraints at the two edges of the domain and are monotonically increasing (resp. decreasing). Consistently with the so-called transform/back-transform method (Ramsay and Silverman, 2005) we map the actual monotone and bounded curves using the logH transformation introduced by Canale and Vantini (2016) and fit a LSFR autoregressive model to the transformed data similarly to the previous section. Specifically, let be the demand (resp. supply) curve at day . We let

and then model transformed demand (resp. supply) curve at day with a first-order autoregressive linear model as done in Section 6.1. We set and basis functions and select via cross-validation, in the previous application. Two models for the demand and supply series are fitted separately.

Figure 5 reports the contour plots of the estimated kernels. Similarly to Section 6.1, both estimates present marked positive diagonals while the influence of the curve at time on the curve at time vanishes if we move far away from the diagonal. The qualitative interpretation is clear: the price of a given quantity for day mainly depends on the price of the demand curve in a neighborhood of the same quantity.

Also in this practical case we stress the usefulness of the proposed approach and its ability to lie between the concurrent and nonconcurrent approaches.

7 Discussion

Motivated by the current gap between the concurrent and nonconcurrent models, we introduced a model for function-on-function regression which allows for local sparsity patterns, exploiting some of the properties of B-spline basis and a specifically tailored overlap group-Lasso penalization. The proposed MM algorithm directly tackles the minimization arising from such a group-Lasso penalty, but it is also amenable to generalizations beyond the specific group structure motivated by our model and, furthermore, beyond the FDA context. The empirical assessment through simulation and applications to real datasets, provides evidence of improved estimation accuracy with respect to standard competitors and straightforward and effortless interpretability of the results. The latter is of substantial interest when dealing with infinite dimensional objects as in FDA.

Despite we focused on the case of a single functional covariate, the extension of our modelling framework to covariates is straightforward. At the same time, our approach can be specified also in the simpler case when the ’s are scalar responses.

References

- Bach et al. (2012) Bach, F., Jenatton, R., Mairal, J. and Obozinski, G. (2012) Optimization with sparsity-inducing penalties. Foundations and Trends® in Machine Learning, 4, 1–106.

- Canale and Vantini (2016) Canale, A. and Vantini, S. (2016) Constrained functional time series: Applications to the italian gas market. International Journal of Forecasting, 32, 1340–1351.

- Candes et al. (2007) Candes, E., Tao, T. et al. (2007) The dantzig selector: Statistical estimation when p is much larger than n. The annals of Statistics, 35, 2313–2351.

- Centofanti et al. (2020) Centofanti, F., Fontana, M., Lepore, A. and Vantini, S. (2020) Smooth lasso estimator for the function-on-function linear regression model. arXiv, 1–31.

- Chiou and Muller (2009) Chiou, J.-M. and Muller, H.-G. (2009) Modeling hazard rates as functional data for the analysis of cohort lifetables and mortality forecasting. Journal of the American Statistical Association, 104, 572–585.

- De Boor (1978) De Boor, C. (1978) A practical guide to splines, vol. 27. Springer-Verlag New York.

- Efron et al. (2004) Efron, B., Hastie, T., Johnstone, I., Tibshirani, R. et al. (2004) Least angle regression. The Annals of statistics, 32, 407–499.

- Fan and Li (2001) Fan, J. and Li, R. (2001) Variable selection via nonconcave penalized likelihood and its oracle properties. Journal of the American statistical Association, 96, 1348–1360.

- Friedman et al. (2010) Friedman, J. H., Hastie, T. and Tibshirani, R. (2010) Regularization paths for generalized linear models via coordinate descent. Journal of Statistical Software, 33, 1–22.

- Golub and Uhlig (2009) Golub, G. and Uhlig, F. (2009) The algorithm: 50 years later its genesis by John Francis and Vera Kublanovskaya and subsequent developments. IMA J. Numer. Anal., 29, 467–485.

- Golub and Van Loan (2013) Golub, G. H. and Van Loan, C. F. (2013) Matrix computations. Johns Hopkins Studies in the Mathematical Sciences. Johns Hopkins University Press, Baltimore, MD, fourth edn.

- Hastie et al. (2009) Hastie, T., Tibshirani, R. and Friedman, J. (2009) The Elements of Statistical Learning: Data Mining, Inference, and Prediction, Second Edition. Springer Series in Statistics. Springer New York.

- Horváth and Kokoszka (2012) Horváth, L. and Kokoszka, P. (2012) Inference for Functional Data with Applications. Springer Series in Statistics. Springer New York.

- Hsing and Eubank (2015) Hsing, T. and Eubank, R. (2015) Theoretical foundations of functional data analysis, with an introduction to linear operators. John Wiley & Sons.

- Huang et al. (2012) Huang, J., Breheny, P. and Ma, S. (2012) A selective review of group selection in high-dimensional models. Statist. Sci., 27, 481–499.

- Hunter and Lange (2000) Hunter, D. R. and Lange, K. (2000) Quantile regression via an MM algorithm. J. Comput. Graph. Statist., 9, 60–77.

- Hunter and Lange (2004) — (2004) A tutorial on MM algorithms. Amer. Statist., 58, 30–37.

- Jacob et al. (2009) Jacob, L., Obozinski, G. and Vert, J.-P. (2009) Group lasso with overlap and graph lasso. In Proceedings of the 26th annual international conference on machine learning, 433–440.

- James et al. (2009) James, G. M., Wang, J., Zhu, J. et al. (2009) Functional linear regression that’s interpretable. The Annals of Statistics, 37, 2083–2108.

- Jenatton et al. (2011) Jenatton, R., Audibert, J.-Y. and Bach, F. (2011) Structured variable selection with sparsity-inducing norms. The Journal of Machine Learning Research, 12, 2777–2824.

- Lange (2010) Lange, K. (2010) Numerical analysis for statisticians. Springer, New York.

- Lange (2016) — (2016) MM optimization algorithms. Society for Industrial and Applied Mathematics, Philadelphia, PA.

- Lee and Park (2012) Lee, E. R. and Park, B. U. (2012) Sparse estimation in functional linear regression. Journal of Multivariate Analysis, 105, 1–17.

- Lim and Hastie (2015) Lim, M. and Hastie, T. (2015) Learning interactions via hierarchical group-lasso regularization. Journal of Computational and Graphical Statistics, 24, 627–654.

- Lin et al. (2017) Lin, Z., Cao, J., Wang, L. and Wang, H. (2017) Locally sparse estimator for functional linear regression models. Journal of Computational and Graphical Statistics, 26, 306–318.

- Malfait and Ramsay (2003) Malfait, N. and Ramsay, J. O. (2003) The historical functional linear model. Canadian Journal of Statistics, 31, 115–128.

- McLachlan and Krishnan (2008) McLachlan, G. J. and Krishnan, T. (2008) The EM algorithm and extensions. Wiley Series in Probability and Statistics. Wiley-Interscience, John Wiley & Sons, Hoboken, NJ, second edn.

- Morris (2015) Morris, J. S. (2015) Functional regression. Annual Review of Statistics and Its Application, 2, 321–359.

- Neal and Hinton (1999) Neal, R. M. and Hinton, G. E. (1999) A View of the EM Algorithm That Justifies Incremental, Sparse, and Other Variants, 355–368. Cambridge, MA, USA: MIT Press.

- Ortega and Rheinboldt (1970) Ortega, J. M. and Rheinboldt, W. C. (1970) Iterative Solution of Nonlinear Equations in Several Variables. USA: Society for Industrial and Applied Mathematics.

- Polak (1987) Polak, E. (1987) On the mathematical foundations of nondifferentiable optimization in engineering design. SIAM Rev., 29, 21–89.

- Qin et al. (2013) Qin, Z., Scheinberg, K. and Goldfarb, D. (2013) Efficient block-coordinate descent algorithms for the group Lasso. Math. Program. Comput., 5, 143–169.

- Ramsay et al. (2009) Ramsay, J. O., Hooker, G. and Graves, S. (2009) Functional data analysis with R and Matlab. New York: Springer.

- Ramsay and Silverman (2005) Ramsay, J. O. and Silverman, B. W. (2005) Functional data analysis. New York: Springer.

- Tibshirani (1996) Tibshirani, R. (1996) Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society: Series B (Methodological), 58, 267–288.

- Trefethen and Bau (1997) Trefethen, L. N. and Bau, III, D. (1997) Numerical linear algebra. Society for Industrial and Applied Mathematics (SIAM), Philadelphia, PA.

- Wainwright and Jordan (2008) Wainwright, M. J. and Jordan, M. I. (2008) Graphical models, exponential families, and variational inference. Foundations and Trends® in Machine Learning, 1, 1–305.

- Watkins (2011) Watkins, D. S. (2011) Francis’s algorithm. Amer. Math. Monthly, 118, 387–403.

- Wu and Lange (2008) Wu, T. T. and Lange, K. (2008) Coordinate descent algorithms for lasso penalized regression. Ann. Appl. Stat., 2, 224–244.

- Wu and Lange (2010) — (2010) The MM alternative to EM. Statist. Sci., 25, 492–505.

- Yang and Zou (2015) Yang, Y. and Zou, H. (2015) A fast unified algorithm for solving group-lasso penalize learning problems. Stat. Comput., 25, 1129–1141.

- Yuan and Lin (2006) Yuan, M. and Lin, Y. (2006) Model selection and estimation in regression with grouped variables. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 68, 49–67.

- Zhao et al. (2009) Zhao, P., Rocha, G., Yu, B. et al. (2009) The composite absolute penalties family for grouped and hierarchical variable selection. The Annals of Statistics, 37, 3468–3497.

- Zhou et al. (2013) Zhou, J., Wang, N.-Y. and Wang, N. (2013) Functional linear model with zero-value coefficient function at sub-regions. Statistica Sinica, 23, 25.

Appendix

Examples of group-Lasso not allowed sparsity patterns

Additional computational results

In this Section we provide additional results concerning the MM algorithm introduced in Section 3. We first introduce the MM algorithm 1, then we provide the exact computational costs and we conclude the section by considering the problem of finding the minimum value of for which all the coefficients are equal to zero.

Proposition 2.

Proof.

The exact computational cost is

-

-

to compute and to compute and to compute , in the initialization step, totalling ;

-

-

to compute and to compute , totalling ;

- -

-

-

to compute ;

-

-

to compute , totalling ;

-

-

to compute , totalling ,

totalling . ∎

It is worth noting that the leading element of the computational cost is cubic in which is assumed to be less than . Moreover, leveraging the Shermann-Morrison-Woodbury formula has the further benefit that, as the MM algorithm iterates, the columns of the design matrix that correspond to groups of coefficients that have been previously set to zero are discarded.

The next proposition provides the minimum value of the tuning parameter for which all the coefficients in the minimization problem in Equation (10) are equal to zero.

Proposition 3.

For the overlap group-Lasso problem in equation (10) the smallest at which all coefficients are equal to zero is

| (20) |

where denotes the -th column vector of the matrix and denotes the -th diagonal element of the matrix .

Proof.

The objective function of the overlap group-Lasso in equation (10) can be decomposed into the sum of three terms:

| (21) |

having subdifferential

| (22) |

where is the subdifferential of the OG penalty term

| (23) | ||||

Since the objective function is convex the first order optimality condition and Theorem 1 ensure the existence of a unique fulfilling the condition . Plugging we get from which we obtain the equivalent condition and is the dual variable satisfying if and if for . Therefore , which completes the proof. ∎

Algorithm convergence properties

The following propositions state the local and global convergence properties of the MM algorithm. In what follows, let be the objective function to be minimized and be the majorizing function at the current -iteration, where is the estimate of the parameter at the -iteration. Moreover, let denote the mimimizer of at iteration . Following Lange (2010) we provide conditions for local and global convergence of the MM algorithm for proving the local and global convergence of the MM sequence delivered by the MM algorithm introduced in Section 3.

The following proposition (adapted from Lange, 2010, Proposition 15.3.2) provides the conditions for local convergence of any MM sequence.

Proposition 4.

Since the majorizing function is strictly convex, if the Hessian of the surrogate function is invertible, then the proposed MM algorithm is locally attracted to a local minimum at a linear rate equal to the spectral radius of , where denotes the identity matrix of dimension .

Proof.

The mapping function in equation (15) is differentiable and the surrogate function is strictly convex. Moreover, the second derivative of is invertible for any . By Proposition 15.3.1 in Lange (2010) it is then sufficient to show that all the eigenvalues of the differential lie in the half-open interval . All the eigenvalues of the can be determined as stationary points of the Rayleight quotient . Moreover, strict convexity of both and implies that and are positive definite (see Polak, 1987) and therefore for any non null vector of length one. Positive semi-definiteness of also implies . ∎

The convergence rate is usually used to characterize the convergence behavior of an iterative algorithm. It is well known that the convergence rate of an MM algorithm is, in general, linear. If converges to some optimal point of and is continuous, then is a fixed point and . By Taylor expansion, where is the matrix rate of convergence. The spectral radius of is usually defined as the local convergence rate of the sequence (see, e.g. Lange, 2010; McLachlan and Krishnan, 2008). The following proposition provides conditions for global convergence of the MM algorithm.

Proposition 5.

If is coercive, the subset of parameter domain is compact and all stationary points of are isolated. The majorizing function is strictly convex and differentiable in both and , then the MM sequence convergence to the stationary point of . Moreover, since is strictly convex, then the limiting point of is the minimum.

Proof.

For any fixed , the objective function is convex with one bounded local minimizer (see Proposition 1), which implies that is coercive, (see Lange, 2010, 2016). The convexity of further implies that is Lipschitz continuous on each compact subset of (i.e. locally Lipschitz continuous). It follows that the gradient of exists for almost all . Moreover, by the Liapunov theorem (Lange, 2010, Proposition 15.4.1) the set of clustering points generated by the sequence , for , is contained in the set of stationary points of . Then, according to (Lange, 2010, Proposition 8.2.1), is a connected set since any closed subset of a compact set is also compact. The condition that all stationary points of are isolated easily implies that the number of stationary points in the compact set can only be finite and since the cluster set is a connected subset of a finite set , reduces to a singleton. ∎

Proofs of Section 4

Remark 2.

∎

Theorem 1.

Using Proposition 1 of Jenatton et al. (2011) and noting that the -th element of the second sum in (10) is the norm of all the coefficients , the minimization in (10) leads to a unique set of coefficients . Since and the knots defining the bases and are fixed each B-spline basis represents a vector space of piecewise polynomials. Since their tensor product also generates a vector space, the elements of the tensor product basis are also linearly independent and so the coefficients of any given kernel in this vector space are uniquely determined. Thus, the estimator obtained by the minimization of (10) is unique. ∎

Theorem 2.

We first note that if , there exists a unique true and thus the event is equivalent to consistently estimate the non-zero patterns in . To show this, it is sufficient to rely on Theorem 6 of Jenatton et al. (2011). The rest of the proof consists in noting that the conditions required by Theorem 6 of Jenatton et al. (2011) are satisfied under our set of assumptions. ∎

Theorem 3.

We study the consistency of with respect to exploiting its representation through the vector space and using the results of Theorem 7 of Jenatton et al. (2011). Eventually the consistency of with respect to the true is obtained letting the number of B-splines basis to grow with since if both and are increasing we have that the event approaches and . Note that for any we also have since is a subset of . Thus the correct estimation of automatically leads to

Despite correctly estimating , however, it may happen that for for subregions of a finite number of sets in (6) of Lebesgue measure . Since is bounded we can conclude that a correct estimation of the non zero patterns in would also lead to

Hence, similarly to Theorem 2 we focus on the consistent estimation of the non-zero patterns in . To this end, we exploit Theorem 7 of Jenatton et al. (2011) and show how the conditions required therein translate to our settings. We first sightly rewrite the minimization in (10) as

| (24) |

where is obtained dividing each column of by its standard deviation. Consistently with this operation we are intrinsically rescaling and thus the final estimator is multiplied through the Hadamart product for the inverse of which is the vector containing the standard deviations of . To maintain the penalization consistent with our settings, the weights inside the norm are also redefined as . With this operation, the minimization is conducted on a matrix such that has unit diagonal. In addition, let be the minimum eigenvalue of the matrix . From condition (17) the number of nonzero coefficients in is strictly less than and then is positive definite and .

Hence, defining the constants and consistently with Jenatton et al. (2011) all the requirements of their Theorem 7 are satisfied. Hence the proof. ∎