Limiting Spectral Distributions of Families of Block Matrix Ensembles

Abstract.

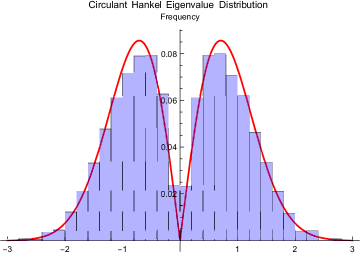

We introduce a new matrix operation on a pair of matrices, and discuss its implications on the limiting spectral distribution. In a special case, the resultant ensemble converges almost surely to the Rayleigh distribution. In proving this, we provide a novel combinatorial proof that the random matrix ensemble of circulant Hankel matrices converges almost surely to the Rayleigh distribution, using the method of moments.

Key words and phrases:

Random matrix theory, block matrices, Rayleigh distribution, method of moments, Hankel matrices2020 Mathematics Subject Classification:

60B20 (primary), 60B10 (secondary)1. Introduction

Random matrix theory was used by Eugene Wigner as a mechanism for modeling the limiting behavior of the energy distribution of heavy nuclei. The states of individual heavy nuclei are difficult to determine using the Schrödinger Equation, so instead one can examine the eigenvalues of random matrices and thereby obtain information about the statistical behavior of the system, as done in [FM09].

The techniques from nuclear physics were later abstracted to ensembles of random matrices. The motivation for choice of ensemble corresponded to the properties of physical systems. For example, this was the motivation for studying ensembles of real symmetric matrices, self-adjoint matrices, and Gaussian Orthogonal Ensembles. Given the importance of studying eigenvalues to both physics (as in [Wig51, Dys62]) and to other fields of mathematics such as analytic number theory (as in [KS99a, KS99b]), the eigenvalue distribution of the ensemble is the focus of study.

In general, it is rare to find a named, closed form limiting distribution of the eigenvalue distributions for a given ensemble of random matrices. For example, in the ensemble of Toeplitz matrices studied in [HM05] and [BDJ06], the distribution seemed to be approaching a Gaussian distribution, but there were Diophantine obstructions with the index combinatorics of the random variable entries in the matrices. These obstructions prevented the distribution from being a Gaussian distribution, and a closed form is still not known. Following these difficulties, an attempt to overcome the obstructions and increase symmetry was done by adding palindromicity, this is sufficient to guarantee almost sure convergence to the Gaussian distribution [MMS07]. Many other related ensembles have been thoroughly investigated, for example in [BBV+19, BM02, JMP10, KKM11, MSTW15, KKM11, BLM+15].

In this paper, we formulate a new matrix operation, “swirl,” based on the symmetry of the concentric even matrix ensemble. An example of a matrix in this ensemble is

Notably, the are variables drawn independently from a probability distribution with mean zero, variance one, and finite higher moments.

We chose this ensemble with the hope that by increasing symmetry we would be able to obtain a closed form for the spectral distribution of the matrices in the ensemble.

It is advantageous to understand such matrices in block matrix form, as evidenced by [BBV+19]. In this vein, we split the matrices in the concentric even ensemble into blocks or quadrants and defined the swirl operation using two input matrices, and , to create the larger block matrix of size corresponding to the concentric even matrix, where is the upper right quadrant and is the exchange matrix. That is,

| (1.1) |

In concentric even matrices, is a circulant Toeplitz matrix and is a circulant Hankel matrix. We reduce studying the circulant even ensemble to studying circulant Hankel matrices with several theorems about the behavior of in Section 3. Hankel matrices arise in a multitude of applications across fields of mathematics and physics: differential equations, functional analysis, statistics, probability theory, control theory, and more (see [BG21, Pel06, SGT82], for example). Their symmetry also makes them a heavily studied family in random matrix theory, as in [BG21, Bou21]. Circulant Hankel matrices also happen to be even centrosymmetric matrices, which have additional specialized applications in physics, for example in [DS03].

In Section 4 we characterize summands in terms of the number of repeated entries and compute the moments via combinatorial degree of freedom arguments. By these methods, we obtain a novel combinatorial proof showing that the limiting spectral distribution of the random matrix ensemble of circulant Hankel matrices converges almost surely to the symmetrized Rayleigh distribution (for an earlier proof relying on direct computation, see [BDJ06]). As we discuss in Appendix A, our methods are generally applicable to many random matrix ensembles. In particular, we have the following theorem.

Theorem 1.1.

Let be the empirical spectral measure of the circulant Hankel random matrix ensemble populated by entries from a sequence of random variables from a distribution with mean , variance , and finite higher moments. Then,

| (1.2) |

almost surely.

Notably, is the symmetrized Rayleigh distribution, with many known applications to physics (see [Sid62]).

Many block random matrix ensembles have been investigated in the past (for example, [KKM11]). Some of these have even yielded remarkably similar limiting empirical spectral distributions (see Figure 3 of [MSTW15]).

The swirl operation is very rich and lends itself to much further study. In particular, a natural next step is to study matrix ensembles determined by different choices of and . We discuss some natural next steps in Section 5.

2. Preliminaries

We characterize the distribution of the eigenvalues of several random matrix ensembles by defining a spectral measure over subfamilies of random matrices from the ensemble. Let be an element of a family of random matrices from some ensemble where the entries are drawn from a probability distribution with mean 0, variance 1, and finite higher moments.

We use the Eigenvalue Trace Lemma to relate the eigenvalues to the matrix elements.

Lemma 2.1 (Eigenvalue Trace Lemma).

Let be the eigenvalues of an matrix A. Then

| (2.1) |

Let be the number of eigenvalues of , excluding those that are trivially zero. This is derived using rank arguments and is fixed for a given and matrix structure.

Then, we define the empirical spectral measure of as the following measure.

Definition 2.2.

Let be a probability density function with mean , variance , and finite higher moments. Let be a family of matrices with entries drawn independently from . Then

| (2.2) |

where is the Dirac-delta functional, the are the nonzero eigenvalues of , and is the number of eigenvalues in that are not trivially .

Remark 2.3.

The scaling factor is derived heuristically from the Central Limit Theorem. By computing the trace of via the Eigenvalue Trace Lemma, we get

| (2.3) |

suggesting that the magnitude of the eigenvalues must be roughly each in expectation since the expectation of an entry squared is 1, by our definition of .

Via the method of moments, we will be able to understand the spectral distribution of these eigenvalues. In this instance, the convergence of the moments of the spectral distribution is enough to show the convergence of the spectral distribution. From the definition of the spectral measure in terms of the Dirac-delta functional, we may compute its moments.

Remark 2.4.

The moments of the spectral measure of are

| (2.4) |

Notice that by the Eigenvalue Trace Lemma,

Finally, we’re interested in averaging these moments over the entire family of matrices that belongs to. As is standard, we define the following.

Definition 2.5.

Let be the average of over all in our chosen family of matrices.

Our main result is that exists and that there is a universal limiting distribution for several families of matrices.

In the following work, we will calculate as a sum of terms (via the Eigenvalue Trace Lemma). We will show that some terms are negligible by showing that they are (where if, for fixed there exists such that for all .

In this paper, we investigate swirl ensembles and circulant Hankel matrices.

Definition 2.6.

An circulant Hankel matrix is defined by the link relation .

3. Swirl Matrices

3.1. Motivation

The swirl operation was inspired by radially symmetric matrices of the following form:

We refer to such matrices as “concentric even matrices.” Note that not only are the circles about the center of the matrix composed of equal entries, but also these entries are repeated in later circles such that each matrix entry appears an equal number of times. This was intentional in an effort to increase symmetry and derive a closed form limiting spectral distribution. For a matrix of this form, each entry appears exactly times ( times in each quadrant). Upon close inspection, it is apparent that the submatrix in the top right of a concentric even matrix is an circulant Toeplitz matrix (which is not necessarily symmetric). Moreover, the other three quadrants of the matrix may be generated from this circulant Toeplitz matrix via a clockwise rotation of the entries. Indeed, for an circulant Toeplitz matrix, and the exchange matrix with 1’s on the antidiagonal and zeroes elsewhere, the concentric even matrix is given by the following:

This block decomposition of the concentric even matrices motivates the following definition and the focus of this section.

Definition 3.1.

Let and be matrices. We define as the matrix where

| (3.1) |

We aim to characterize the limiting spectral distribution of . To do so, we relate to via the Eigenvalue Trace Lemma.

Remark 3.2.

Observe that

| (3.2) |

This observation vastly simplifies the computation of .

Convention 1.

We adopt a convenient shorthand notation for block matrices with four blocks which are in 3 blocks. For example, a matrix of the form with zeroes necessarily everywhere except the top right corner will be referred to as a matrix That is, is of the form

for an matrix. Define , and similarly with the indices corresponding to the block that is not necessarily zero everywhere.

Remark 3.3.

if and is of the form otherwise.

3.2. Computing

Recall the following facts:

| (3.3) |

and

| (3.4) |

for matrices and We are now ready to relate to .

Theorem 3.4.

For and both matrices, .

Proof.

Moreover, any term in the expansion of

| (3.5) |

is of the form . Since trace is additive, we have that a term contributes 0 to the trace of if ; if they are not equal, the main diagonal of the matrix is all zeroes.

As such, by Remark 3.3 and the above, the nonzero summands of correspond to products where for and . There are such summands since one can choose the first indices of the matrices in the summand in ways. Then, the second indices are exactly determined by the above requirements.

Observe that the only nonzero block of a matrix in the trace expansion of is a product of matrices. By the construction of swirl, this product begins with if , and ending with if . Also observe that this product begins with an if , and ends with if . All such products will start with one of or and end with the opposite. These products will also not have consecutive repeated ’s or ’s. These properties follow from Remark 3.3 and the definition of swirl.

In order for this product of matrices to contribute to the trace, note that the first and last index of such a product must be equal (or else it will not be a diagonal entry). Thus, there must be an equal number of matrices of the form and in any contributing product. As such, each nonzero summand in the expansion of (with expressed as ) will be of the form or . Consequently, there are such nonzero contributing terms and

| (3.6) |

by the cyclic property of trace. ∎

Given that the trace of the th power of a matrix completely determines the th moment of its empirical spectral distribution, Theorem 3.4 allows us to reduce characterizing the limiting spectral distribution of ensembles to characterizing the limiting spectral distribution of matrices.

3.3. Iterating

Another interesting avenue for swirl is iterating the operation.

Definition 3.5.

Let be matrices. Let be the block matrix with ’s on the anti-diagonal and zeroes elsewhere. Note that Then, set

| (3.7) |

where is repeated times in the above.

We begin by analyzing the trace of iterated swirl matrices.

Proposition 3.6.

Fix both matrices such that and a nonnegative integer. Then

| (3.8) |

Proof.

We prove by induction. For , this follows from Theorem 3.4. Now, assume this holds for for . Then,

| (3.9) | |||

This implies

| (3.10) | |||

Now

| (3.11) | |||

Thus

| (3.12) | ||||

by induction.

Therefore,

| (3.13) |

The result then follows by induction. ∎

Remark 3.7.

Alternatively, observe that, since , is just the block matrix of repeated times. This means .

If we wish to study the moments of ensembles of such matrices, we need to understand the trace of powers of the iterated swirl matrices. We reduce this to an analysis of in the following proposition.

Proposition 3.8.

Fix to be matrices such that and and nonnegative integers. Then

| (3.14) |

Proof.

We prove by induction on . For , this follows from Theorem 3.4. Now, assume

| (3.15) |

holds for . We show it holds for . By Definition 3.5,

| (3.16) |

So,

with the last step following from Theorem 3.4.

Let . Then,

| (3.17) | |||

with the last step following from the assumption that .

Therefore

with the last step from the inductive hypothesis. The result then follows by induction. ∎

3.4. The Product of Swirl and its Transpose

If we assume that is a permutation matrix, then reduces to understanding . This is a useful quantity to understand if and are chosen such that does not necessarily have real eigenvalues.

Proposition 3.9.

Fix to be matrices with a permutation matrix. Then

| (3.18) |

Proof.

Let = . We show by induction that

| (3.19) |

For the base case consider for . We have

| (3.20) |

This yields

| (3.21) |

Expanding the transpose terms yields

| (3.22) |

Recall is a permutation matrix . Thus, we have

| (3.23) |

Now assume that the inductive hypothesis holds for ; we will show it holds for . Rewrite as . Then

| (3.24) |

by induction. Matrix multiplication yields

| (3.25) |

Simplifying we have

| (3.26) |

This completes the inductive argument.

Now calculating the trace is trivial. Note by the cyclic property of trace, . ∎

Here the limiting spectral distribution reduces to the a scaled semi-circle distribution, which is handled in [Wig58].

3.5. Limiting Spectral Distribution of Swirled Matrix Ensembles

From the previous work in this section, we can reduce the analysis of swirl matrix ensembles to the analysis of matrix product ensembles. We consider the empirical spectral measure defined in Definition 2.2. In this case, from Remark 3.7, for and both matrices, and , has the same number of trivial nonzero eigenvalues, , as . Let . Then the empirical spectral measure of is given by

| (3.27) |

From Definition 2.2 and Proposition 3.8, the th moment of the spectral distribution in this case is thus

| (3.28) |

which does not depend on . As such, the limiting spectral distribution of swirl is the same for any number of iterations, .

4. Circulant Hankel Matrices

In all the ensembles that follow, we assume that the matrices are constructed from a sequence of independently and identically distributed random variables (i.i.d.r.v.) with distribution having mean 0, variance 1, and finite higher moments. We assign elements of this sequence to matrix entries according to the symmetry of our given ensemble.

4.1. Moments via powers of

From Theorem 3.4, studying the trace of the even concentric swirl matrices reduces to studying the trace of powers of , with the circulant Hankel matrix, the circulant Toeplitz matrix, and the exchange matrix. The matrix ensemble of circulant Hankel matrices is exceptional in its own right; its limiting spectral distribution converges almost surely to a symmetrized Rayleigh distribution (as shown in [BDJ06]). In this section, we provide a new combinatorial proof of this remarkable result. We begin by defining the empirical spectral measure for this ensemble of matrices. This measure, for the normalized eigenvalues of our matrix , is given by the following definition.

Definition 4.1.

The empirical spectral measure of a random circulant Hankel matrix is

| (4.1) |

where is the Dirac-delta functional and the are the non-zero eigenvalues of .

Remark 4.2.

The scaling factor is derived heuristically. By computing the trace of , we obtain

| (4.2) |

suggesting that the eigenvalues must be roughly each in expectation.

In order to use the method of moments, we compute the th moment for the empirical spectral distribution of a random matrix , .

Remark 4.3.

The th moment of the empirical spectral distribution of the random matrix , averaged over an ensemble, is given by

| (4.3) |

We use to denote .

This standard computation follows from the properties of the Dirac delta functional and the Eigenvalue Trace Lemma.

Proposition 4.4.

We have and .

Proof.

The first moment is immediate from . The second moment follows from substituting into the formula in Remark 4.3. ∎

In order to compute for we consider the limiting behavior of the terms in the sum combinatorially. It is useful to note the following fact.

Remark 4.5.

In , if and only if , where we index the matrix beginning at 0.

We begin by showing the odd moments of the limiting spectral distribution are all zero.

Theorem 4.6.

We have for all .

Proof.

First, we analyze via the Eigenvalue Trace Lemma. Observe that since the entries of are independent, if any are to the first power in a summand in the expansion of , the expected value of the entire summand is zero. For example,

| (4.4) |

Thus, at a minimum, the entries must be matched in pairs with at least one triple in all of the contributing terms. We bound the number of ways to construct such summands. There are at most distinct entries in a given contributing summand by this pairing argument. We can choose such entries in less than ways. Then, we can specify the matrix index of one of the terms in the summand in ways. There are at most ways to assign each factor in the summand to a particular and then the choice of one index of a matrix entry completely determines the remaining matrix indices via Remark 4.5. This implies there are at most degrees of freedom for any choice of grouping (and the number of ways to assign factors in the summand to is ). So, the number of contributing summands is . Note that each grouping of matrix entries equal to contributes

| (4.5) |

since has finite higher moments by assumption. As such, each contributing term contributes to .

Substituting into our formula from Remark 4.3, we get:

| (4.6) |

Taking the limit as , we achieve the desired result. ∎

Next, we show for all and thus , averaged over all converges to the symmetrized Rayleigh distribution.

We begin with a sample calculation showing to build intuition for the proof.

Proposition 4.7.

We have .

Proof.

Note that

| (4.7) |

where is the matrix entry of at the th row and and th column. As before, if any of the random variables in a summand is not equal to any of the others, we can write the expectation of the whole summand as a product of the expectation of the singleton term and the rest of the summand by the independence of our random variables. Since all of the random variables have mean 0, such a term contributes zero. As such, there are only two options for contributing summands: four equal matrix entries or two pairs of equal matrix entries.

- Case 1:

-

In this case, there are four summands that are all matched. That is, Up to relabeling, the first case yields the system of equations

(4.8) This implies and , leaving only two free variables. Since there are only 2 degrees of freedom in this case and each of our i.i.r.d. random variables have finite moments by assumption, terms of this kind contributes to the expectation of . Thus, by Remark 4.3, such terms contribute to the fourth moment in the limit.

Notably, the system of equations corresponds to the equation matrix

which has nullity 2. Thus, since vectors satisfying this system of equations are exactly those in the null space of this matrix, there are valid linear combinations of basis vectors of the null space, and the random variables have finite fourth moments, such terms contribute to the expectation of . This alternate linear algebraic formulation is used in our the proof of Theorem 4.11.

- Case 2:

-

In this case, all summands are paired. This case of matching the random variables into pairs has two subcases.

- Subcase 2.1:

-

Pair nonadjacent random variables, that is, . This pairing yields the following system of equations:

(4.9) This implies and . Thus there are only two degrees of freedom in this case and it does not contribute in the limit.

Note that the equation matrix corresponding to the system of equations has nullity 2, an alternative proof that this case cannot contribute.

- Subcase 2.2:

-

Pair adjacent random variables. For example, and . Note that there are two such pairings. Up to relabeling, this pairing yields the following system of equations:

(4.10) This implies only , yielding 3 degrees of freedom. Thus, the terms in this case contribute in the limit. Fixing , there is a unique choice for and choices for both and , yielding choices total after iterating over all and both choices of pairing orientation.

Substituting into Remark 4.3, we then get that this case contributes precisely to in the limit and , since this is the only contributing case.

∎

We see that only a select few of the summands in the computation of even moments contribute in the limit. We formalize this observation in the following lemmas.

Lemma 4.8.

For even moments , where , the only contributing summands in the trace expansion are those where for all .

Proof.

Consider any summand in , , where

| (4.11) |

and each . Now, if any , the expectation of the summand is 0. So, we may assume each . If there is at least one factor in the summand with , there are less than degrees of freedom of terms with such groupings—there are at most ways to choose the and an additional ways to fix a matrix index in some term (which then induces a constant in number of possible arrangements).

Each such term contributes

| (4.12) |

to , as desired. ∎

Remark 4.9.

For the following arguments, consider an index “even” if its subscript is even. Similarly define odd indices. For example, consider

| (4.13) |

We view as the “odd” indices and as the “even” indices.

Lemma 4.10.

The pairings of odd indices to even indices contribute to .

Proof.

Consider the system of equations resultant in this case. Each relation can be assumed to be of the general form

| (4.14) |

for even and odd. Note in particular that all even indices arise on the left hand side of such relations as the first term and all odds similarly as the first term on the right hand side. Since in such relations each index is added to the subsequent index, every index appears in a sum exactly once on both sides of the equations.

Interpret these equations as row vectors with ones in the entries corresponding to the indices on the left hand side of the relations and negative ones to those on the right hand, as in Proposition 4.7. Now, from the above observation, the sum of these row vectors is 0. This implies they are linearly dependent. This means the matrix given by this system of equations has nullity at least . Note that vectors in the null space are exactly solutions to

| (4.15) |

for the matrix of these row vectors. This implies we have degrees of freedom in this case. From Remark 4.9, we thus have exactly degrees of freedom, so these pairings contribute exactly their constant term to in the limit.

To count the number of odd-even pairings, we choose an odd and an even index to pair in ways. Then we repeat until there are no indices left to pair, yielding . However, we introduced an arbitrary ordering on the pairs in this process, so we correct by dividing by , yielding as desired. Note that, given the choice of a single index and pairings, every index is determined uniquely (regardless of the modulo ). ∎

Now we complete the proof by showing that the other pairings of indices do not contribute in the limit.

Theorem 4.11.

.

Proof.

From Lemma 4.10, it suffices to show that any arrangement of pairs including an odd-odd or even-even index matching will not contribute. One way to do so is to show that the row vectors corresponding to the resultant system of equations are all linearly independent and thus the rank of the corresponding matrix is , implying a nullity of and less than degrees of freedom. Note that there being an odd-odd index pairing implies that there must be an even-even index pairing.

- Step 1:

-

We will show that if there is an odd-odd index pairing then the equations corresponding to even-odd index pairings are linearly independent as row vectors.

Fix a relation given by such an even-odd index pairing. Each side of each relation of the form can be conceptualized as as a “first” index (matched index) plus a “second” index. For the sake of consistency, when converting such relations into row vectors (by moving all the terms to a single side), we negate the side with the odd first index. In order to show linear independence of the even-odd row vectors, it suffices to show that no nonempty linear combination of them sums to 0.

Note that each index appears at most twice amongst the odd-even pair relations. In particular, if we fix

(4.16) to be in our linear combination, with even, this yields a row vector of the form

with the ’s in the and st positions and the ’s in the st and th positions and all other positions (note the indices range from to ).

Crucially, in order to form a linear combination of even-odd vectors summing to 0, we must nullify each index in the sum. Each index appears at most once as a first and a second index. Given our signing convention, even indices are positive as first indices and negative as second indices. Odds indices are negative as first indices and positive as second indices. Note that, since each index occurs at most once as a first index and a second index, the two expressions cannot be exactly equal. In order to cancel out the positive contribution of to the th column, we need to add the term including as a second index. However, we then must cancel out the contribution of as a first index by including it as a second index. To do that, we must include as a first index. As such we see that in order to cancel out the contribution of each necessary term, we need to include every term as both a first and second index. However, by assumption, there is an odd-odd index. Therefore, not every index has a row vector corresponding to it as a first and second index. Thus, we cannot cancel out the contribution to every column and there is no nonempty linear combination of vectors corresponding to the even-odd pair expressions that equals 0. We conclude that these row vectors are linearly independent.

- Step 2:

-

We will show that the row vectors corresponding to odd-odd pairs of indices cannot be part of any nonempty linear combination of row vectors summing to zero (the proof follows for even-even pairs as well).

Suppose indices and are paired for odd and . The corresponding row vector is of the form

with ’s in the th and st indices and ’s in the th and st indices. As before, to cancel out the contribution of , we need to appear as a second index and contribute negatively. As a result, must appear as a first index and contribute negatively. Then we need to appear as a second index and contribute positively to cancel out that contribution. This requires to appear as a first index and contribute positively. However, this implies that all first odd indices must contribute positively and all first even indices must contribute negatively to achieve total cancellation. We know this cannot be the case as there is an odd-odd pair and one of the first odd indices must thus contribute negatively. As such, odd-odd and even-even pairs cannot be a part of linear combinations of the row vectors summing to 0.

We conclude that a linearly dependent family of row vectors must be a subset of the even-odd pair row vectors if it exists. However, from Step 1, this is impossible. So, all of the row vectors are linearly independent. Thus, if there are odd-odd or even-even index pairs, the rank of the matrix is and the nullity is . Since the nullity of this matrix is a upper bound on the degrees of freedom in this case, such pairings will not contribute in the limit. The only remaining pairings are all odd-even. From Lemma 4.10 we conclude .

∎

We use in Theorem 4.12 that the moments of the limiting spectral distribution of the Circulant Hankel ensemble are the same as the moments of a symmetrized Rayleigh distribution. More broadly, a Rayleigh distribution is a Weibull distribution with fixed parameters. For our purposes, denote the Weibull distribution with scale parameter and shape parameter by the following:

| (4.17) |

for and otherwise. As our eigenvalue distributions are symmetric, we symmetrize the distribution by replacing with and dividing through by 2 to retain

| (4.18) |

This symmetrization notably has no effect on the even moments of the distribution and zeroes all the odd moments.

The th moment of a Weibull distribution is given by

| (4.19) |

When this distribution is Rayleigh, i.e., and , the th moment for even is then .

Theorem 4.12.

Let denote an infinite sequence of values drawn from a distribution with mean , variance , and finite higher moments. As the limiting spectral measure of the circulant Hankel random matrix ensemble converges almost surely to the limiting spectral distribution given by the ’s, the symmetrized Rayleigh distribution:

| (4.20) |

Proof.

This follows by the exact same argumentation as in Section 6 of [HM05] with plus rather than minus modulo . ∎

We may then conclude that the limiting spectral distribution of iterated swirl ensembles on circulant Toeplitz and an exchange matrix also converges almost surely to a symmetrized Rayleigh distribution.

Corollary 4.13.

Let for the exchange matrix and a random circulant Toeplitz matrix. As , the limiting spectral measure of this ensemble converges almost surely to a symmetrized Rayleigh distribution.

Proof.

From the observation that trivially has half of its rows repeated, has only nontrivial, nonzero eigenvalues. The empirical spectral measure of the matrix is thus given by the following equation:

| (4.21) |

See Definition 2.2 for the derivation of the scaling factor. From Theorem 3.4, the th moment of the limiting spectral distribution of this ensemble equals

| (4.22) |

As such, the th moment in this case is exactly the th moment of the limiting spectral distribution of . The result then follows from Theorem 4.12. ∎

Remark 4.14.

Note that, for an ensemble such that has no repeated rows, would not have the same limiting spectral distribution as . Indeed, its moments would be times the moments of the limiting spectral distribution of . In the case of a Weibull distribution, this would only increase the scaling parameter of the Weibull distribution by a factor of .

5. Future Work

The obvious next step is to study broader matrix ensembles related to . A good starting point is ensembles with , due to the following theorem of Tao and Yasuda [TY02].

Theorem 5.1 (Tao-Yasuda [TY02], 2002).

Let and be real symmetric matrices with .

-

•

if and only if the spectrum of equals the spectrum of up to sign.

-

•

if and only if the spectrum of equals the spectrum of multiplied by .

In particular, if we choose ensembles and such that and are real symmetric matrices, and , then has all real eigenvalues.

Another interesting direction is study the even powers of non-symmetric swirl ensembles. Proposition 3.9 provides a useful starting point for such investigations.

Finally, given that circulant Toeplitz and circulant Hankel matrices yield rare named, closed form limiting spectral distributions, it seems likely that they possess some intrinsic, special properties. Inspired by the work of [BB18, BB11, BHS11, MSTW15] on matrices with patterns governed by link functions, we investigated circulant matrices with link functions along different diagonals, but found the results disappointingly uninteresting. These results are summarized in Appendix A.

Appendix A

When computing the moments of the limiting empirical spectral measures of our ensembles we converted our problem of finding degrees of freedom of contributing summands in the trace to a problem of calculating the nullity of a matrix. As a specific example, we can calculate the th moment of the Hankel ensemble by looking at set partitions of and calculating the rank of matrices of the form

| (A.1) |

where is the identity matrix, is a permutation matrix, and is a matrix with in the diagonal and to the right of the diagonal. The matrix is written below as an example.

| (A.2) |

The permutation matrix corresponds to the particular matchings of indices in the summand corresponding to equal matrix entries. The nullity of the matrix gives the degrees of freedom of assignments of entries to groups that contribute in the case . Iterating over all set partitions and substituting into the formula in Definition 2.4, we can easily show certain configurations do not contribute in the limit.

We generalize by considering matrices which are constant along certain circulant lines/diagonals. We call these -ensembles. Formally, an matrix is in the -ensemble if

| (A.3) |

An example of a matrix within the (1,2)-ensemble is:

| (A.4) |

Note how the equivalent entries, denoted here by entries of the same value, are spaced apart by row movements and column movements. This creates the appearance of a matrix where every rows, the entries are horizontally permuted by columns. From this, we obtain the idea of slope as we describe the relationship between equivalent entries in -ensemble patterns. This generalization is the idea of a polynomial link function in the literature, except now modulo (see [BB18, BB11, BHS11, MSTW15]).

However, this generalization is insufficient if we intend to study symmetric matrices. Thus, we strengthen our condition to

| (A.5) |

This allows us to generalize the special behavior of both circulant Hankel and circulant Toeplitz matrices.

Below we is a matrix that belonging to the -ensemble

These represent the circulant Hankel matrices. Moreover, matrices from the -ensemble are of the form

These represent the circulant Toeplitz matrices.

Inspired by the fact that both the circulant Hankel and circulant Toeplitz matrices admitted, we generalize the structure of these matrices in the hopes of finding a broader class of matrices with limiting empirical spectral distributions given by named probability distributions. To this end, notice how the elements of the aforementioned families cascade through the matrix with ”slope” . It is this notion of slope which we wish to generalize, and will be made more concrete in what follows.

With this change in parameters, the same pattern of equivalent entries being rows and columns away persists, and the main observable change is in the number of equivalence classes of matrix entries that appear.

The elements at the indices generated by and form a group:

| (A.6) |

Notice that is a normal subgroup of . We want to understand the number of cosets associated to as this will give us the number of unique elements within an matrix with the aforementioned rule.

In the simplest cases we get the matrices we studied in the main portion of the paper. When and both equal , the resultant ensemble is Hankel, with the number of cosets increasing as increases. It is this positive slope that reflects the symmetry of the matrix that is lacking in the ciruclant Toeplitz. Likewise, if and are units with opposite signs, i.e., and , the resulting matrices are all Toeplitz. Similarly, the number of cosets increases consistently with . The number of cosets is important to consider because it indicates the amount of variation within the matrix, the more cosets there are, the fewer zero eigenvalues appear.

Now, as we vary and , new patterns arise in the family of matrices and consequently the number of cosets. This variance is a function of the positioning of equivalent entries. With these new and values, the spacing between the placement of the entries changes, and there are some very interesting patterns to the numbers of cosets and the qualities of symmetry. However, among all these patterns, it appears that the only ones that remain symmetric are circulant Hankel. Besides those, we continue to observe circulant Toeplitz matrices appearing at certain intervals and numbers of cosets.

For coprime to and , we observe that when

| (A.7) |

where is the index of in , the matrices yielded are circulant Toeplitz. Alternatively, when

| (A.8) |

the matrices yielded are circulant Hankel.

However, we found that whenever we consider matrices from the -ensemble with , then the limiting spectral distribution is uninteresting. This is because the number of cosets for a matrix in this ensemble appears bounded by a constant times . Indeed, the matrix becomes a block matrix with many repetitions of a much smaller matrix, deferring its spectral distribution to that smaller matrix ensemble. When and are units (up to sign), we find computationally that the number of cosets is proportional to , which is just . Because the number of cosets is proportional to , the number of eigenvalues grows as we increase the size of the matrix. However, in the other case, number of nonzero eigenvalues is fixed, preventing a new distribution from arising.

References

- [BB11] Sayan Banerjee and Arup Bose. Noncrossing partitions, catalan words, and the semicircle law. Journal of Theoretical Probability, 26(2):386–409, 2011.

- [BB18] Arup Bose and Anirban Basak. Balanced toeplitz and hankel matrices. Patterned Random Matrices, page 131–142, 2018.

- [BBV+19] Keller Blackwell, Neelima Borade, Charles VI, Noah Luntzlara, Renyuan Ma, Steven Miller, Mengxi Wang, and Wanqiao Xu. Distribution of eigenvalues of random real symmetric block matrices. 2019.

- [BDJ06] Włodzimierz Bryc, Amir Dembo, and Tiefeng Jiang. Spectral measure of large random hankel, markov and toeplitz matrices. The Annals of Probability, 34(1), 2006.

- [BG21] Eugene Bogomolny and Olivier Giraud. Statistical properties of structured random matrices. Phys. Rev. E, 103:042213, 2021.

- [BHS11] Arup Bose, Rajat Subhra Hazra, and Koushik Saha. Convergence of joint moments for independent random patterned matrices. The Annals of Probability, 39(4), 2011.

- [BLM+15] Olivia Beckwith, Victor Luo, Steven J Miller, Karen Shen, and Nicholas Triantafillou. Distribution of eigenvalues of weighted structured matrix ensembles. Integers, 15:A21, 2015.

- [BM02] Arup Bose and Joydip Mitra. Limiting spectral distribution of a special circulant. Statistics & Probability Letters, 60(1):111–120, 2002.

- [Bou21] A. Bourget. Spectral distribution of families of hankel matrices. Linear Algebra and its Applications, 624:103–120, 2021.

- [DS03] F. Diele and I. Sgura. Centrosymmetric isospectral flows and some inverse eigenvalue problems. Linear Algebra and its Applications, 366:199–214, 2003.

- [Dys62] Freeman J. Dyson. The threefold way. algebraic structure of symmetry groups and ensembles in quantum mechanics. Journal of Mathematical Physics, 3(6):1199–1215, 1962.

- [FM09] Frank Firk and Steven Miller. Nuclei, primes and the random matrix connection. Symmetry, 1, 2009.

- [HM05] Christopher Hammond and Steven J. Miller. Distribution of eigenvalues for the ensemble of real symmetric toeplitz matrices. Journal of Theoretical Probability, 18(3):537–566, 2005.

- [JMP10] Steven Jackson, Steven Miller, and Thuy Pham. Distribution of eigenvalues of highly palindromic toeplitz matrices. Journal of Theoretical Probability, 25, 2010.

- [KKM11] Murat Koloğlu, Gene S. Kopp, and Steven J. Miller. The limiting spectral measure for ensembles of symmetric block circulant matrices. Journal of Theoretical Probability, 26(4):1020–1060, 2011.

- [KS99a] Nicholas Katz and Peter Sarnak. Random matrices, frobenius eigenvalues, and monodromy. Colloquium Publications, 1999.

- [KS99b] Nicholas M. Katz and Peter Sarnak. Zeroes of zeta functions and symmetry. Bulletin of the American Mathematical Society, 36(01):1–27, 1999.

- [MMS07] Ada Massey, Steven J. Miller, and John Sinsheimer. Distribution of eigenvalues of real symmetric palindromic toeplitz matrices and circulant matrices. Journal of Theoretical Probability, 20(3):637–662, 2007.

- [MSTW15] Steven J. Miller, Kirk Swanson, Kimsy Tor, and Karl Winsor. Limiting spectral measures for random matrix ensembles with a polynomial link function. Random Matrices: Theory and Applications, 04(02), 2015.

- [Pel06] V. Peller. Hankel operators and their applications. IEEE Transactions on Automatic Control, 51:383–385, 2006.

- [SGT82] Iohvidov Iosif Semënovič., Israel Gohberg, and Gerard Philip Antoine. Thijsse. Hankel and Toeplitz matrices and forms: algebraic theory. Birkhäuser, 1982.

- [Sid62] M M Siddiqui. Some problems connected with rayleigh distributions. Journal of Research of the National Bureau of Standards, Section D: Radio Propagation, 66D(2):167, 1962.

- [TY02] David Tao and Mark Yasuda. A Spectral Characterization of Generalized Real Symmetric Centrosymmetric and Generalized Real Symmetric Skew-Centrosymmetric Matrices. SIAM Journal on Matrix Analysis and Applications, 2002.

- [Wig51] Eugene P. Wigner. On the statistical distribution of the widths and spacings of nuclear resonance levels. Mathematical Proceedings of the Cambridge Philosophical Society, 47(4):790–798, 1951.

- [Wig58] Eugene P. Wigner. On the distribution of the roots of certain symmetric matrices. The Annals of Mathematics, 67(2):325, 1958.