Iterated and exponentially weighted moving

principal component analysis

Departments of Computing and Mathematics

Imperial College London

South Kensington Campus

London SW7 2AZ, UK

paul.bilokon@imperial.ac.uk

&

DQR Ltd

3rd Floor, 120 Baker Street

London W1U 6TU, UK

df@dqr.am

Abstract

The principal component analysis (PCA) is a staple statistical and unsupervised machine learning technique in finance. The application of PCA in a financial setting is associated with several technical difficulties, such as numerical instability and nonstationarity. We attempt to resolve them by proposing two new variants of PCA: an iterated principal component analysis (IPCA) and an exponentially weighted moving principal component analysis (EWMPCA). Both variants rely on the Ogita–Aishima iteration as a crucial step.

Keywords principal component analysis PCA moving statistics rolling statistics

1 Introduction

The principal component analysis (PCA) [9, 8] invented by Pearson [11] and improved by Hotelling [6, 7] is a staple statistical and unsupervised machine learning technique in finance [1]. Its central idea is to reduce the dimensionality of a data set consisting of a large number of interrelated variables, while retaining as much as possible of the variation present in the data set. This is achieved by transforming to a new set of variables, the principal components (PCs), which are uncorrelated, and which are ordered so that the first few retain most of the variation present in all of the original variables.

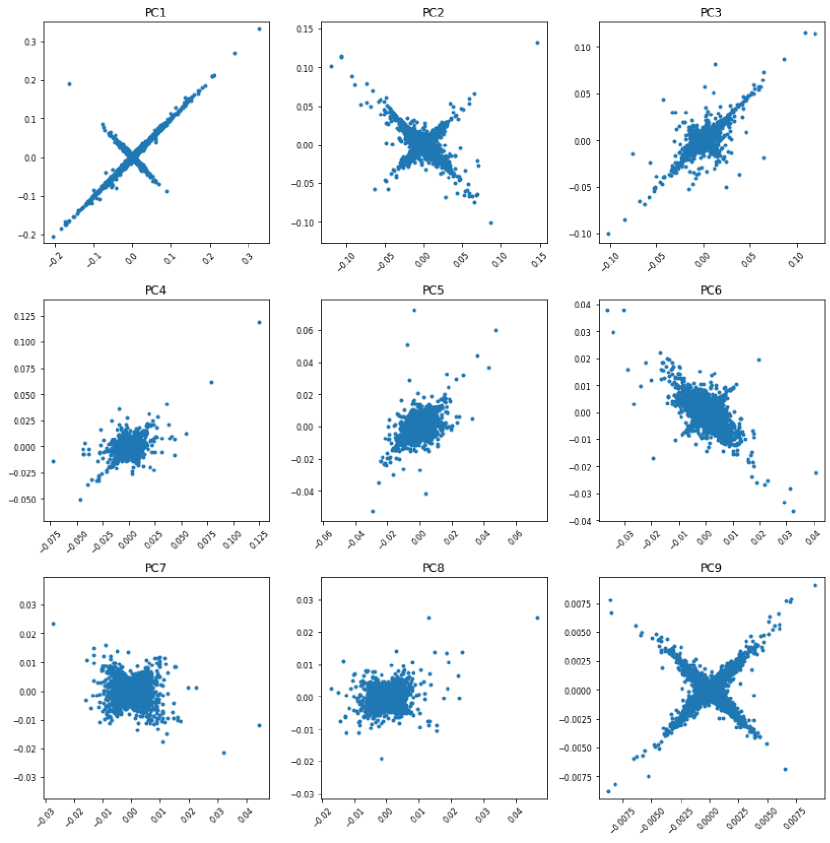

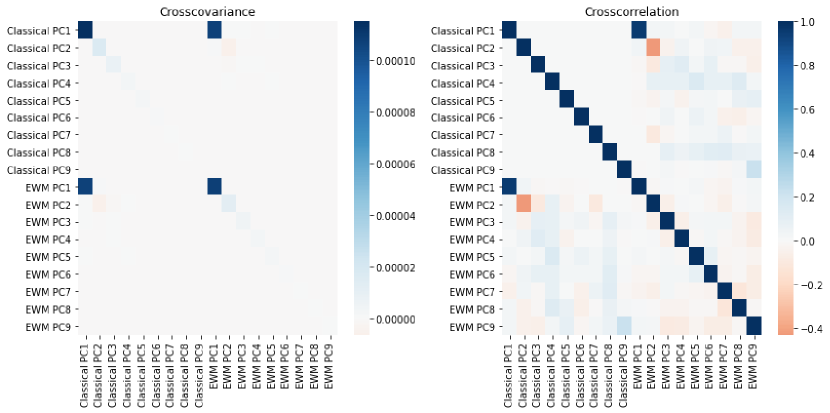

The application of PCA in a financial setting is associated with several technical difficulties. First, the entire data set may not be immediately available (it may be arriving piecewise in real time), so one is forced to work with its subsets pertaining to different time intervals. When the PCs are computed separately on each subset, the geometry of the resulting PCs may suffer from numerical artifacts, as illustrated in Figure 1. In particular, the sign of a given PC may “flip” from one subset to the next. Second, financial data are rarely stationary, and the assumption of a constant covariance matrix is rarely justified.

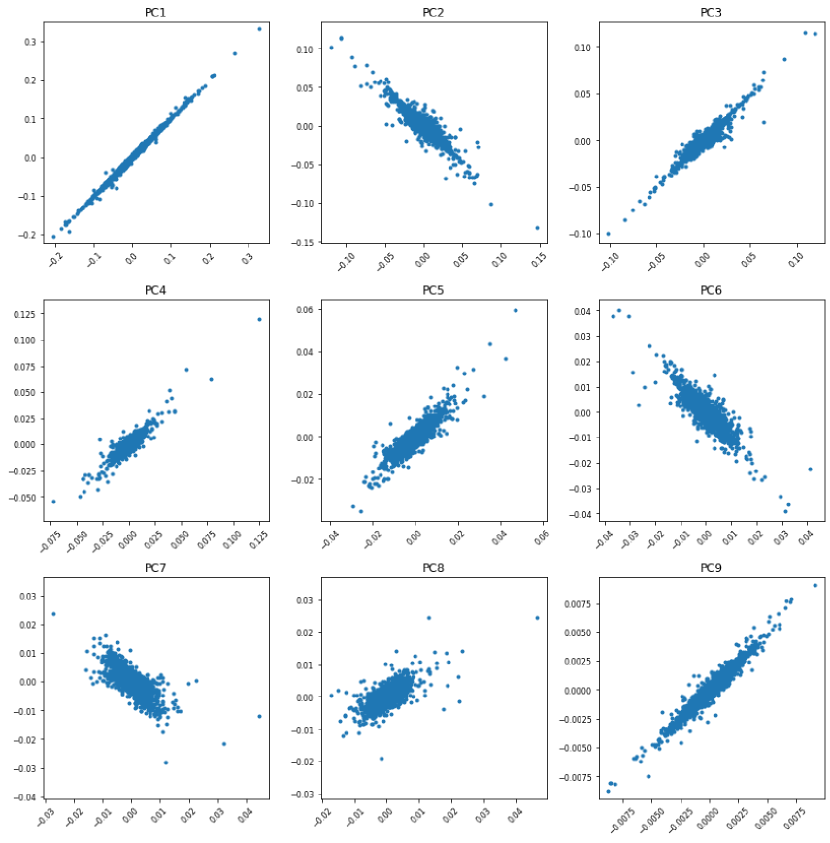

To remedy the first problem, we propose an iterated principal component analysis (IPCA): instead of computing the principal components on each arriving subset independently, we iteratively refine them from one subset to the next. To remedy the second problem, we combine the aforementioned iterative refinement with an exponentially weighted moving computation of the covariance matrix, to obtain an exponentially weighted moving principal component analysis (EWMPCA).

We are heavily indebted to Ogita and Aishima, who proposed an iterative refinement method for symmetric eigenvalue decomposition [10], on whose work we build.

We have used two data sets in this study. Both are derived from data supplied by FirstRate Data and both consist of hourly returns on futures. The first data set (Data Set 1) covers the period 20th August, 2007 to 4th June, 2021, both inclusive, and consists of hourly returns on equity futures: DAX (DY), E-Mini S&P 500 (ES), E-Mini S&P 500 Midcap (EW), Euro Stoxx 50 (FX), CAC40 (MX), E-Mini Nasdaq-100 (NQ), E-Mini Russell 2000 (RTY), FTSE 100 (X), Dow Mini (YM). The second data set (Data Set 2) covers the period 10th September, 2012 to 4th June, 2021, both inclusive, and consists of hourly returns on fuel futures: Brent Last Day Financial (BZ), Crude Oil WTI (CL), Natural Gas (Henry Hub) Last-day Financial (HH), NY Harbor ULSD (Heating Oil) (HO), Henry Hub Natural Gas (NG), RBOB Gasoline (RB).

2 Classical PCA

A data set of observations of features can be represented by an data matrix , whose th column, , is the vector of observations of the th feature. We seek a linear combination of the columns of matrix with maximum variance. Such linear combinations are given by , where is a vector of constants . It can be shown that must be a (unit-norm) eigenvector of the sample covariance matrix associated with the data set; more precisely, the eigenvector corresponding to the largest eigenvalue of .

The full set of eigenvectors of , corresponding to the eigenvalues sorted in decreasing order, , are the solutions to the problem of obtaining up to linear combinations , , which successively maximize variance, subject to uncorrelatedness with previous linear combinations. We call these linear combinations the principal components (PCs) of the data set.

It is standard to define PCs as the linear combinations of the centred variables , with generic element , where denotes the mean value of the observations on variable .

At the core of PCA is the eigendecomposition of the sample covariance matrix or, equivalently, the singular value decomposition (SVD) of the data matrix .

An industry-standard implementation of PCA is sklearn.decomposition.PCA in the software library scikit-learn [12]. It uses the LAPACK [2] implementation of the full SVD or a randomized truncated SVD by the method of Halko et al. [5]. When comparing our results to the classical PCA it is this implementation that we use as a benchmark.

3 The Ogita–Aishima algorithm

As is easy to see, Algorithm 1 estimates the eigenvalues of a given real symmetric matrix for a precomputed set of eigenvectors (the eigenvectors are in the columns of ).

Ogita and Aishima have proposed and analyzed an iterative refinement algorithm [10, Algorithm 1] for approximate eigenvectors of . We list this algorithm here as Algorithm 2. The authors demonstrate the monotone and quadratic convergence of the algorithm under some reasonable technical conditions.

We wrap the function ogita_aishima_step in a higher-level function that performs the number of iterations required for satisfying a sensible convergence criterion (Algorithm 3).

4 Iterated PCA

Iterated PCA (IPCA) is a straightforward extension of PCA wherein the algorithm can be fitted multiple times. Every time fit is invoked on a new data subset, that subset’s sample covariance matrix is calculated. The eigenvectors of are stored between the fits; for each new the previous eigenvectors are used as an initial guess in ogita_aishima(, , sort_by_eigenvalues=true). (At the beginning, when no initial guess is available, the eigenvectors are obtained using standard methods.)

5 Moving statistics

Let , , be a sequence of -dimensional observations. The exponentially weighted moving average for this sequence can be calculated recursively as

where is a constant parameter.

Tsai [14] proposes a similar moving statistic for the sample covariance:

One way to estimate the parameter is by using maximum likelihood (ML). For example, if , , are normally distributed, then is the value of that maximizes

In an example in Section 10.1 of [14], Tsai describes the value as being in the typical range commonly seen in practice.

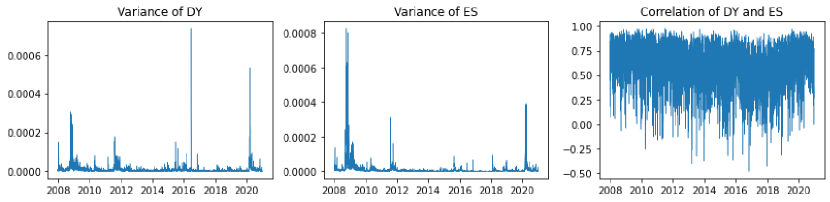

Moving statistics reveal the nonstationary nature of financial data. Consider Data Set 1 as an example. The variances of the returns on individual futures change over time and exhibit the so-called volatility clustering [4]; the correlations between pairs of futures are also time-varying (Figure 3).

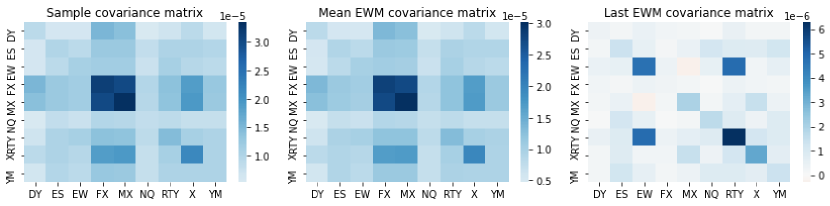

Whereas the mean exponentially weighted moving covariance matrix resembles the sample covariance matrix, individual exponentially weighted moving covariance matrices (such as the last one in our time series shown in Figure 4) may differ from it significantly.

The principal components obtained using the sample covariance matrix present an averaged picture; we need a more precise tool to work out what’s going on at each time step.

6 Exponentially weighted moving PCA

Combining ideas from the Ogita–Aishima iteration and moving statistics it is straightforward to formulate an exponentially weighted moving PCA (EWMPCA)—Algorithm 4.

must be such as to facilitate convergence. One option is to use the sample covariance matrix for the first few (say 100) observations.

As we can see from Figure 5, the EWMPCA principal components are not pairwise uncorrelated; by construction, they are uncorrelated locally, not on average. However, the pairwise correlations are low. For the most part, the EWMPCA principal components are distinct from the corresponding classical PCA principal components.

7 Economic validation

Has EWMPCA economic significance over and above that of the classical PCA? While there are many ways to explore this question, we focus on a particular approach. Avellaneda and Lee have demonstrated in [3] that PCA can be used to generate profitable trading strategies. Can EWMPCA better them?

For each component, we obtain a trading strategy, and a backtest gives us its Sharpe ratio [13]. We compute the Sharpe ratios for the strategies based on the classical PCA as well as for the strategies based on EWMPCA, while keeping all parameters equal between the two methods. The results are shown in Table 1.

| Data Set 1 | Data Set 2 | |||

|---|---|---|---|---|

| Principal component | Classical PCA | EWMPCA | Classical PCA | EWMPCA |

| PC1 | 0.65 | 0.73 | -0.32 | 0.02 |

| PC2 | 0.43 | 1.02 | -0.39 | -0.34 |

| PC3 | -0.2 | 0.89 | -0.13 | 0.48 |

| PC4 | -0.11 | -0.11 | -0.47 | 0.26 |

| PC5 | 0.5 | -0.33 | 0.3 | -0.39 |

| PC6 | -0.01 | -0.13 | 0.37 | -0.16 |

| PC7 | -0.5 | 0.04 | ||

| PC8 | -0.03 | 0.06 | ||

| PC9 | -0.08 | 0.23 | ||

We see that on both Data Set 1 and Data Set 2 Avellaneda–Lee-style statistical arbitrage strategies achieve higher maximum Sharpe ratios when used with EWMPCA as opposed to classical PCA.

8 Implementation

The code behind this paper is publicly available on GitHub: https://github.com/sydx/xpca

The repository contains a general-purpose Python library, xpca.py, and the notebooks that were used to produce the figures in this paper.

A few notes on the implementation are in order. The class IPCA implements the iterated PCA algorithm. It has been modelled on sklearn.decomposition.PCA, so that IPCA can be a drop-in replacement for the former. However, no attempt to achieve industrial-grade performance has been made; in particular, the functions estimate_eigenvalues, ogita_aishima_step, and ogita_aishima could benefit from further optimization.

The class EWMPCA, as the name suggests, implements the EWMPCA algorithm. It can be used in two modes (and the modes can be interleaved):

-

•

the online mode, where the method add is applied to a single observation and returns the corresponding observation transformed to the principal component space;

-

•

the batch mode, where the method add_all is applied to a matrix whose rows are -dimensional observations; the result is, then, a matrix of principal components.

References

- AA [21] Irene Aldridge and Marco Avellaneda. Big Data Science in Finance. Wiley, 2021.

- ABB+ [99] E. Anderson, Z. Bai, C. Bischof, S. Blackford, J. Demmel, J. Dongarra, J. Du Croz, A. Greenbaum, S. Hammarling, A. McKenney, and D. Sorensen. LAPACK Users’ Guide. Society for Industrial and Applied Mathematics, Philadelphia, PA, 3rd edition, 1999.

- AL [10] Marco Avellaneda and Jeong-Hyun Lee. Statistical arbitrage in the US equities market. Quantitative Finance, 10(7):761–782, August 2010.

- Con [07] Rama Cont. Long Memory in Economics, chapter Volatility Clustering in Financial Markets: Empirical Facts and Agent–Based Models, pages 289–309. Springer, 2007.

- HMT [11] N. Halko, P. G. Martinsson, and J. A. Tropp. Finding structure with randomness: Probabilistic algorithms for constructing approximate matrix decompositions. SIAM Review, 53(2):217–288, January 2011.

- Hot [33] Harold Hotelling. Analysis of a complex of statistical variables into principal components. Journal of Educational Psychology, 24(6 and 7):417–441 and 498–520, 1933.

- Hot [36] Harold Hotelling. Relations between two sets of variates. Biometrika, 28(3/4):321, December 1936.

- JC [16] Ian T. Jolliffe and Jorge Cadima. Principal component analysis: a review and recent developments. Philosophical Transactions of the Royal Society A: Mathematical, Physical and Engineering Sciences, 374(2065):20150202, April 2016.

- Jol [02] I.T. Jolliffe. Principal Component Analysis. Springer, 2nd edition, 2002.

- OA [18] Takeshi Ogita and Kensuke Aishima. Iterative refinement for symmetric eigenvalue decomposition. Japan Journal of Industrial and Applied Mathematics, 35:1007–1035, 2018.

- Pea [01] Karl Pearson. On lines and planes of closest fit to systems of points in space. Philosophical Magazine, 2(11):559–572, 1901.

- PVG+ [11] F. Pedregosa, G. Varoquaux, A. Gramfort, V. Michel, B. Thirion, O. Grisel, M. Blondel, P. Prettenhofer, R. Weiss, V. Dubourg, J. Vanderplas, A. Passos, D. Cournapeau, M. Brucher, M. Perrot, and E. Duchesnay. Scikit-learn: Machine learning in Python. Journal of Machine Learning Research, 12:2825–2830, 2011.

- Sha [94] William F. Sharpe. The Sharpe ratio. The Journal of Portfolio Management, 21(1):49–58, October 1994.

- Tsa [10] Ruey S. Tsay. Analysis of Financial Time Series. Wiley Series in Probability and Statistics. Wiley, 2010.