Proof.

A Nonparametric Maximum Likelihood Approach to Mixture of Regression

Abstract

Mixture of regression models are useful for regression analysis in

heterogeneous populations where a single regression model may not be

appropriate for the entire population. We study the nonparametric

maximum likelihood estimator (NPMLE) for fitting these models. The

NPMLE is based on convex optimization and does not require prior

specification of the number of mixture components. We establish

existence of the NPMLE and prove finite-sample parametric (up to

logarithmic multiplicative factors) Hellinger error bounds for the

predicted density functions. We also provide an effective procedure

for computing the NPMLE without ad-hoc discretization and prove a

theoretical convergence rate under certain assumptions. Numerical

experiments on simulated data for both discrete and non-discrete

mixing distributions demonstrate the remarkable performances of our

approach. We also illustrate the approach on two real datasets.

Keywords: conditional gradient method, empirical Bayes, finite-sample parametric

rate, Hellinger distance, mixture of regression, nonparametric

maximum likelihood estimator (NPMLE), random coefficient

regression.

1 Introduction

Given a univariate response variable and a -dimensional regressor variable , the usual linear regression model with homoscedastic Gaussian errors assumes that the conditional distribution of given is normal with mean and variance for some and . In other words, the conditional density of is given by

where denotes the standard normal density function. In contrast, the mixture of linear regression model assumes that the conditional density of given is the mixture density

for some probability measure on and . Equivalently, given , the mixture of linear regression model can be written as

| (1) |

and denotes the standard normal distribution.

The mixture of linear regression model is a prominent mixture model in statistics and machine learning and has a long history (see, for example, Quandt (1958); De Veaux (1989); Jordan and Jacobs (1994); Faria and Soromenho (2010)). It offers a simple approach to modeling population heterogeneity which is present in many real-world applications of linear regression. For example, in pharmacokinetics, different subjects react to drug treatments differently and, in marketing, different consumers have different drivers of satisfaction. As a result, mixture of regression models have been applied in diverse fields including biology (Martin-Magniette et al. (2008)), economics (Battisti and De Vaio (2008)), engineering (Liem et al. (2015)), epidemiology (Turner (2000)), marketing (Wedel and Kamakura (2012); Sarstedt (2008)), and traffic modeling (Elhenawy et al. (2016)). Because of the assumption that the regression parameters are random, mixture of regression models are also known as random coefficient regression models (Hildreth and Houck (1968); Longford (1994); Beran and Millar (1994); Beran and Hall (1992); Beran et al. (1996)).

Suppose we observe independent observations from the model (1), i.e.,

| (2) |

where are independent with

| (3) |

If and are known, the above can be seen as a Bayesian model with parameters , and one can perform individual inference on each regression coefficient via its posterior distribution. The posterior distribution for , given the data point , will be absolutely continuous with respect to the prior and have density proportional to :

| (4) |

for subsets . This posterior distribution can be used to do individual inference on each parameter separately for . One can summarize this into point estimates for in the usual way by taking, for example, the posterior mean:

| (5) |

The subscript OB in stands for “Oracle Bayes”; Oracle here is used to refer to the fact that is typically unknown and thus known only to an Oracle.

This ability to do individual inference on the regression coefficient corresponding to each separate data point is the main attractive feature of the mixture of linear regression model. This would, of course, require knowledge of (as well as ). The goal of this paper is to study the problem of estimating from the data . We shall assume for most of the paper that is known. In practice, it is easy to estimate by using a simple cross-validation procedure as described in Subsection 4.1. If is estimated by, say, a discrete probability measure , then the posterior distribution given by (4) will be estimated by the discrete probability distribution:

| (6) |

and the posterior mean (5) will be estimated by

| (7) |

These can be used for approximate individual inference for . The subscript in stands for “Empirical Bayes”; Empirical here is used to refer to the fact that parameters and are estimated from the data.

For estimation of , most usual approaches assume a parametric form for . For example, it is popular to assume that is a discrete probability measure with a known number of atoms and estimation is then done by maximum likelihood. Likelihood maximization in this case is a non-convex optimization problem and is typically carried out via the expectation maximization (EM) algorithm (see, for example, Leisch (2004); Faria and Soromenho (2010)). In contrast with this parametric approach, we take a nonparametric approach in this paper where we do not impose any parametric assumptions on . However, like in the parametric case, we perform estimation of via maximum likelihood. We therefore follow the strategy of nonparametric maximum likelihood estimation for estimating .

Nonparametric maximum likelihood estimation for mixture models has a very long history starting with Robbins (1950) and Kiefer and Wolfowitz (1956). Book-length treatments on NPMLEs are Lindsay (1995); Groeneboom and Wellner (1992); Böhning (2000) and Schlattmann (2009). There has been renewed interest in these methods more recently (Zhang (2009); Koenker and Mizera (2014); Dicker and Zhao (2016); Saha and Guntuboyina (2020); Gu and Koenker (2020); Jagabathula et al. (2020); Deb et al. (2021); Polyanskiy and Wu (2020)). Most of these papers focus on the problem of estimating normal mixture densities with the exception of Gu and Koenker (2020) which deals with mixture of binary regression and Jagabathula et al. (2020) which deals with mixture of logit models.

Let us now describe our estimator for more precisely assuming that is known. The likelihood function in this model can be taken to be the conditional density of given and its logarithm (the log-likelihood function) is given by

| (8) |

A Nonparametric Maximum Likelihood Estimator (NPMLE) of is obtained by maximizing the log-likelihood function over a large class of probability measures on . It often makes sense to impose bounds on the support of in the maximization of the likelihood. As a result, we consider, for a given set , the estimator:

| (9) |

If no information about the support of is available, then one can either take to be the whole of or a large compact set such as a closed ball centered at the origin having a large radius.

The optimization in (9) is infinite-dimensional as is usually uncountable. However it is a convex optimization problem as the constraint set (the set of all probability measures on ) is convex and the objective function is concave in . We prove in Section 2 that exists when is compact or when satisfies a technical condition which holds when . We also provide an iterative algorithm for computing an approximate solution that is discrete. The algorithm is one of the variants of the Conditional Gradient Method (CGM) also known as the Frank-Wolfe algorithm (Frank and Wolfe (1956); Jaggi (2013)). This algorithm comes with convergence bounds which guarantee that the iterates converge to a global maximizer of the likelihood provided some conditions are satisfied. Even though these conditions seem difficult to verify in practice, we found that the algorithm works very well in a variety of simulation settings and real datasets. Our approach to computing the NPMLE based on the Conditional Gradient Method is very similar to the computational procedure of Jagabathula et al. (2020). The discrete estimate which can be written as can be used for individual inference on via (6) and (7).

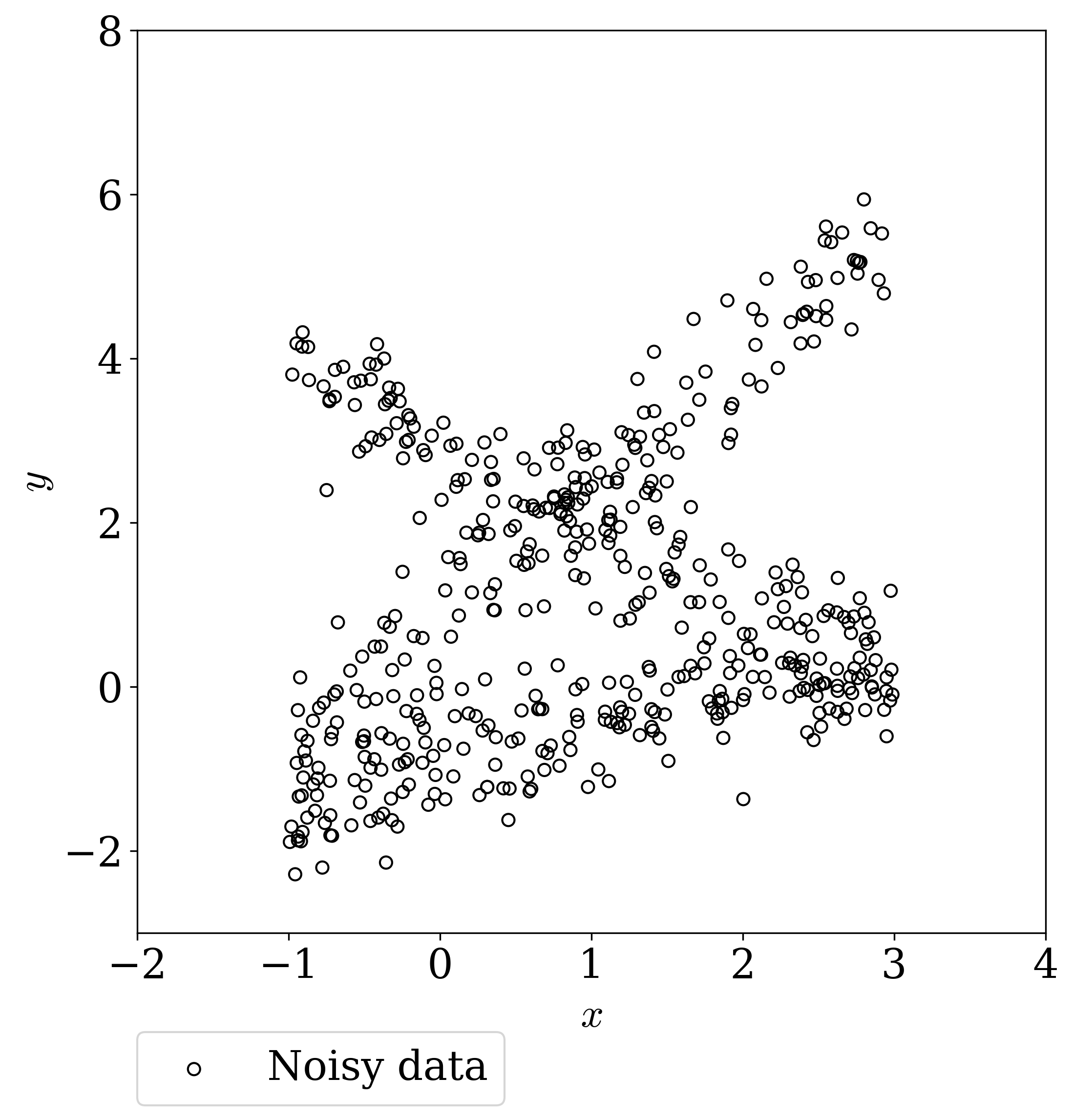

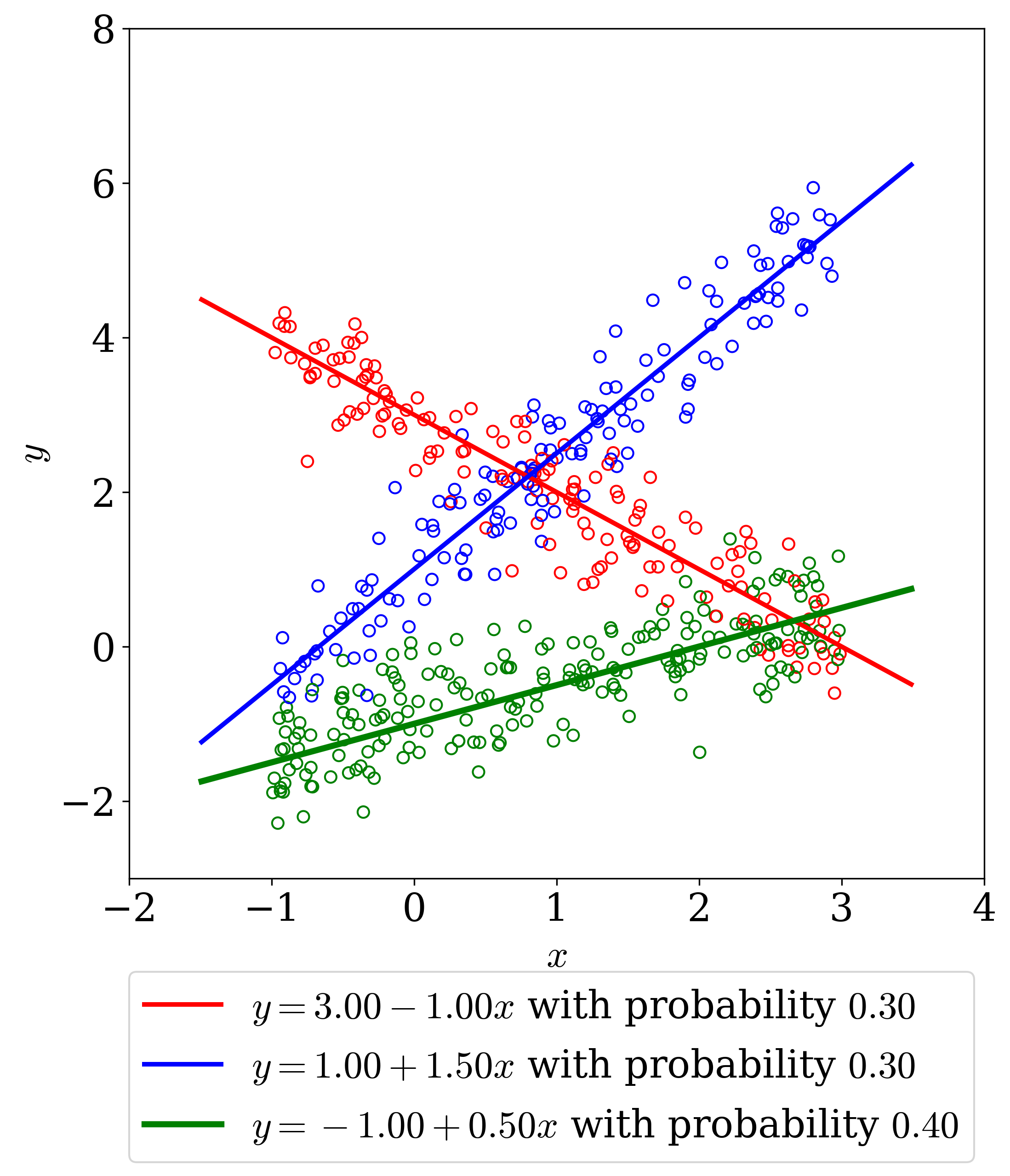

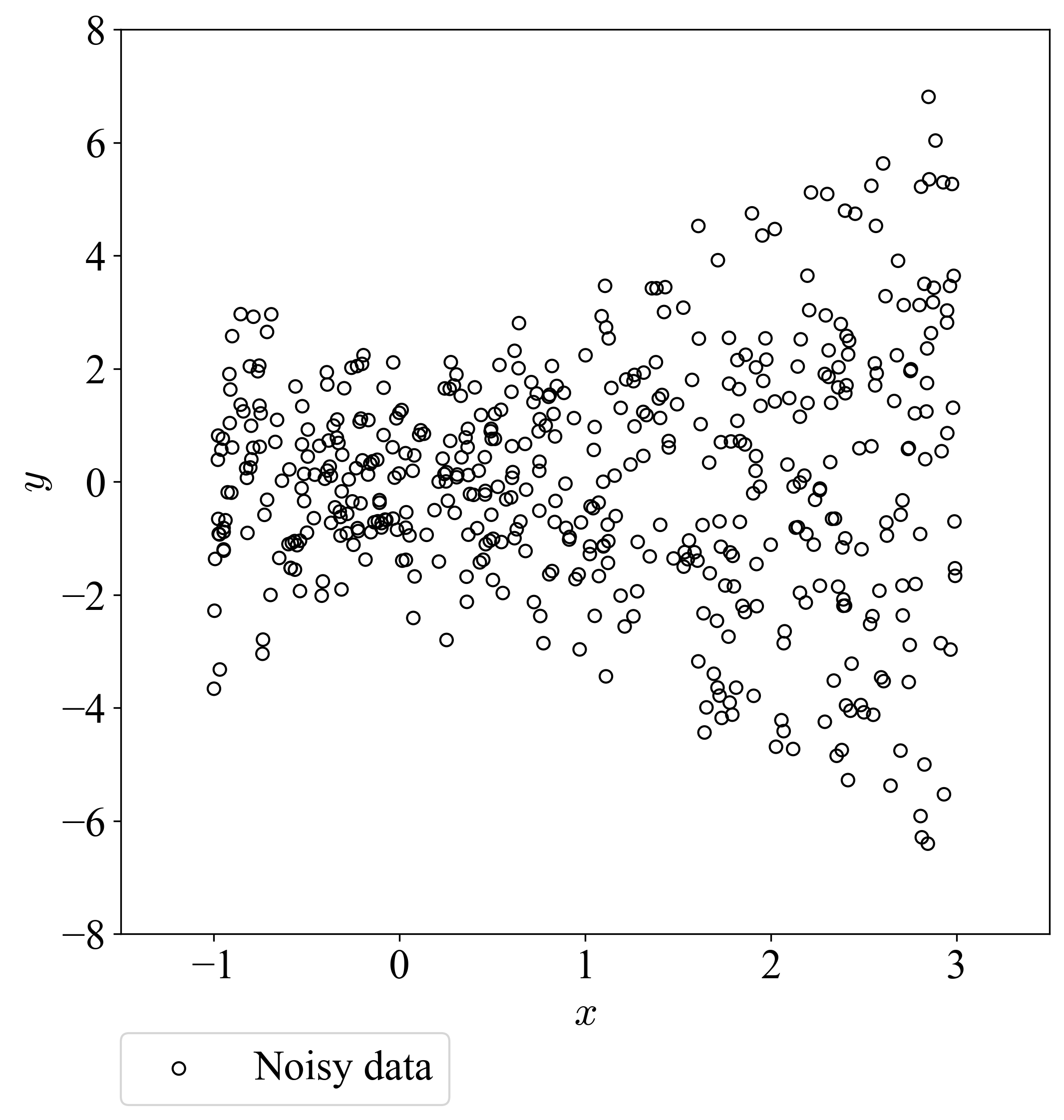

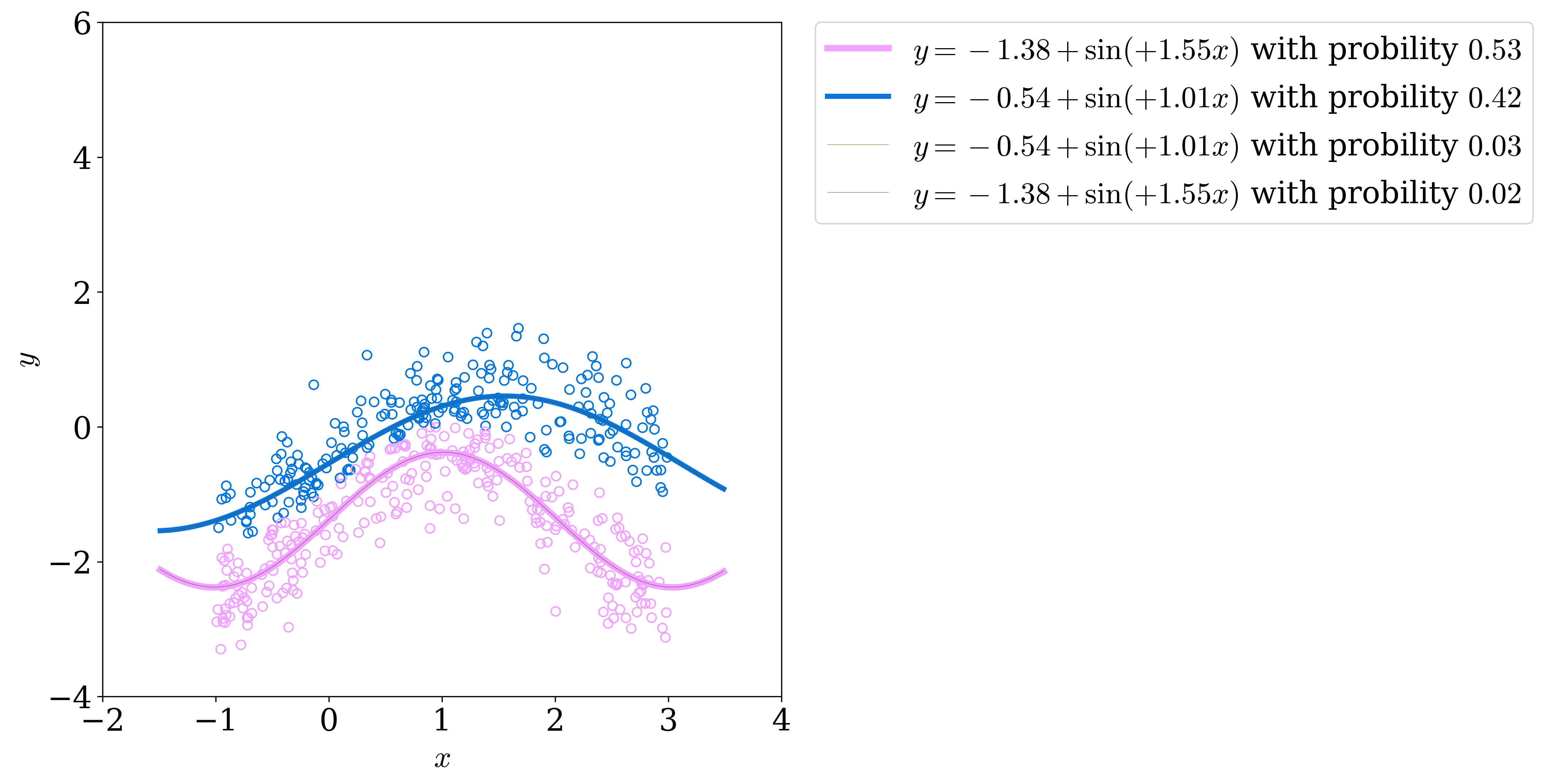

The estimator works well and does not suffer from overfitting even though it is obtained by maximization over a very large class of probability measures. To illustrate, consider the simulated dataset shown in Figure 1(a) where each data point is generated by adding () noise to one of the three lines: chosen with probabilities (the design points are independently generated from the uniform distribution on ). We visualize together with all data points in Figure 1(b), where each data point is color coded according to the line they are generated from. Of course, this color coding and the equations of the three generating lines are not part of the dataset and unavailable to the data analyst.

A common way of analyzing this dataset is to first guess that the data is generated from a three-component mixture of linear regression model by eyeballing Figure 1(a) and then fit such a mixture via the EM algorithm. In contrast, our method does not make any such parametric assumptions.

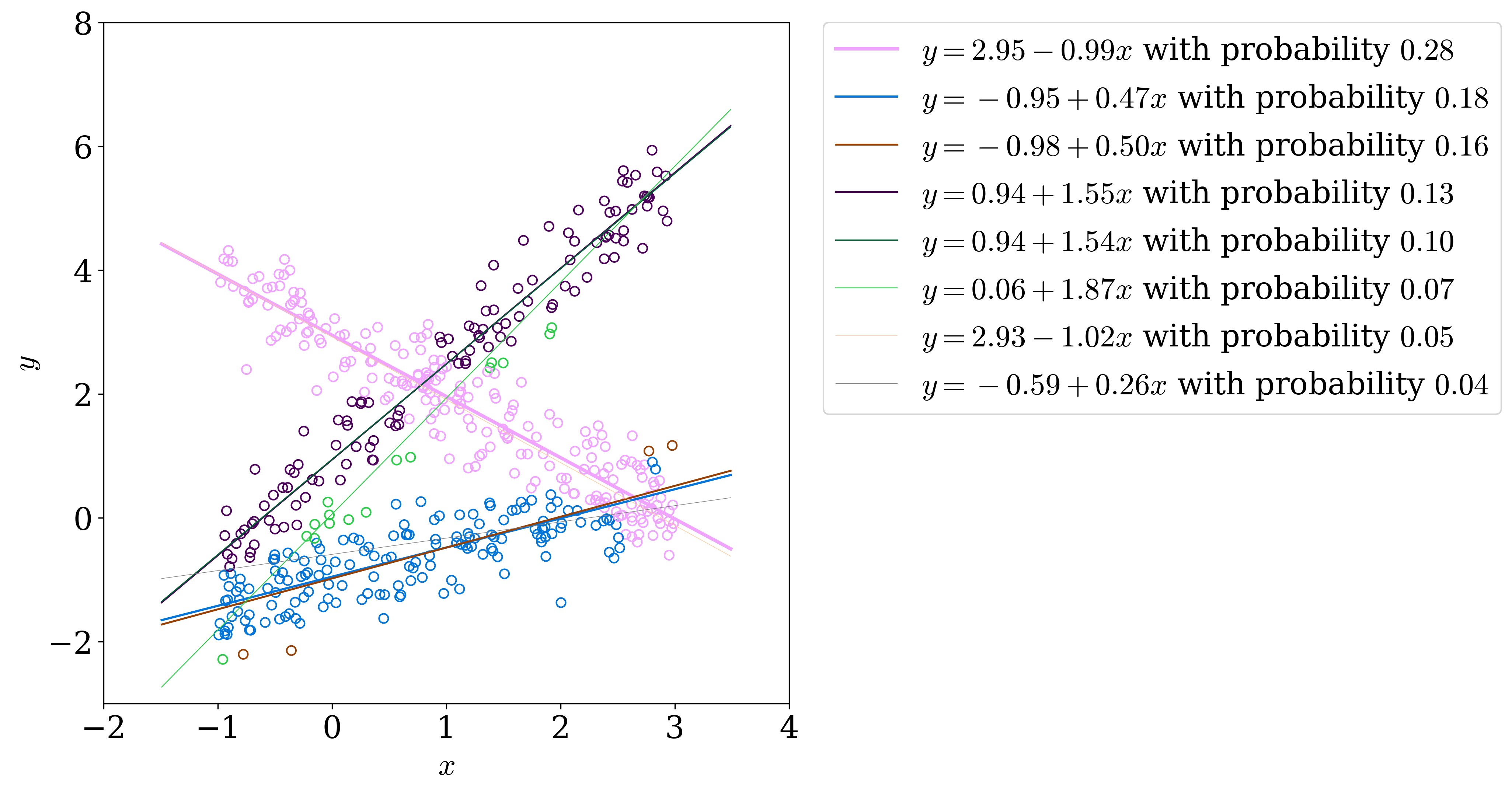

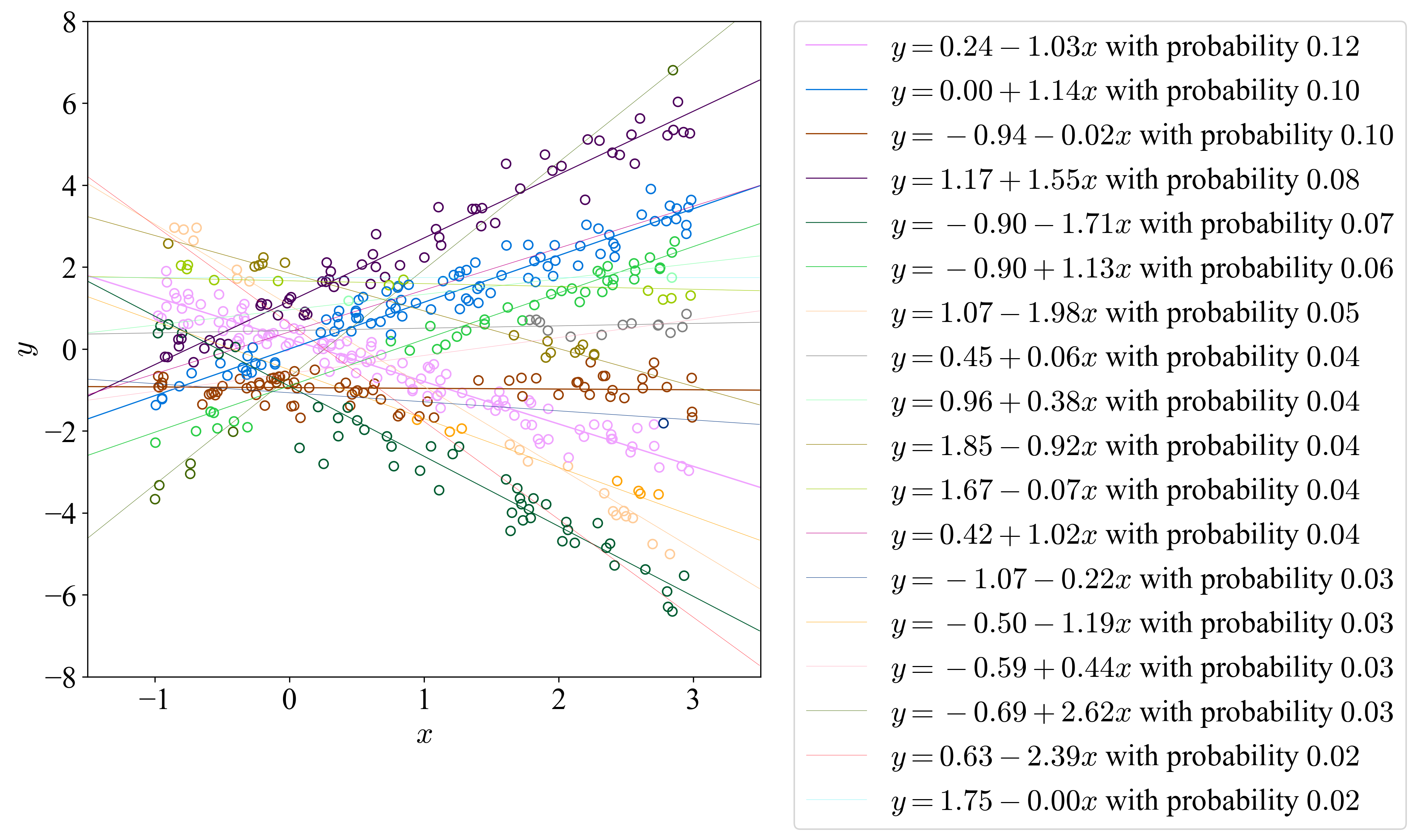

For this dataset, we applied our procedure based on the NPMLE defined in (9) with and . The value was obtained by the cross-validation method described in Subsection 4.1, and it is rather close to . We use to represent the estimate via NPMLE with the by cross-validation, to distinguish from via NPMLE with the true . Our algorithm outputted that is a discrete probability measure supported on points; the regression lines corresponding to the coefficients of these 8 support points are displayed in Figure 2 (the thickness and darkness of each line is proportional to its estimated mixing probability). We colored the 8 different lines with 8 different colors and further colored each data point with the color of the regression line corresponding to the most probable posterior line:

| (10) |

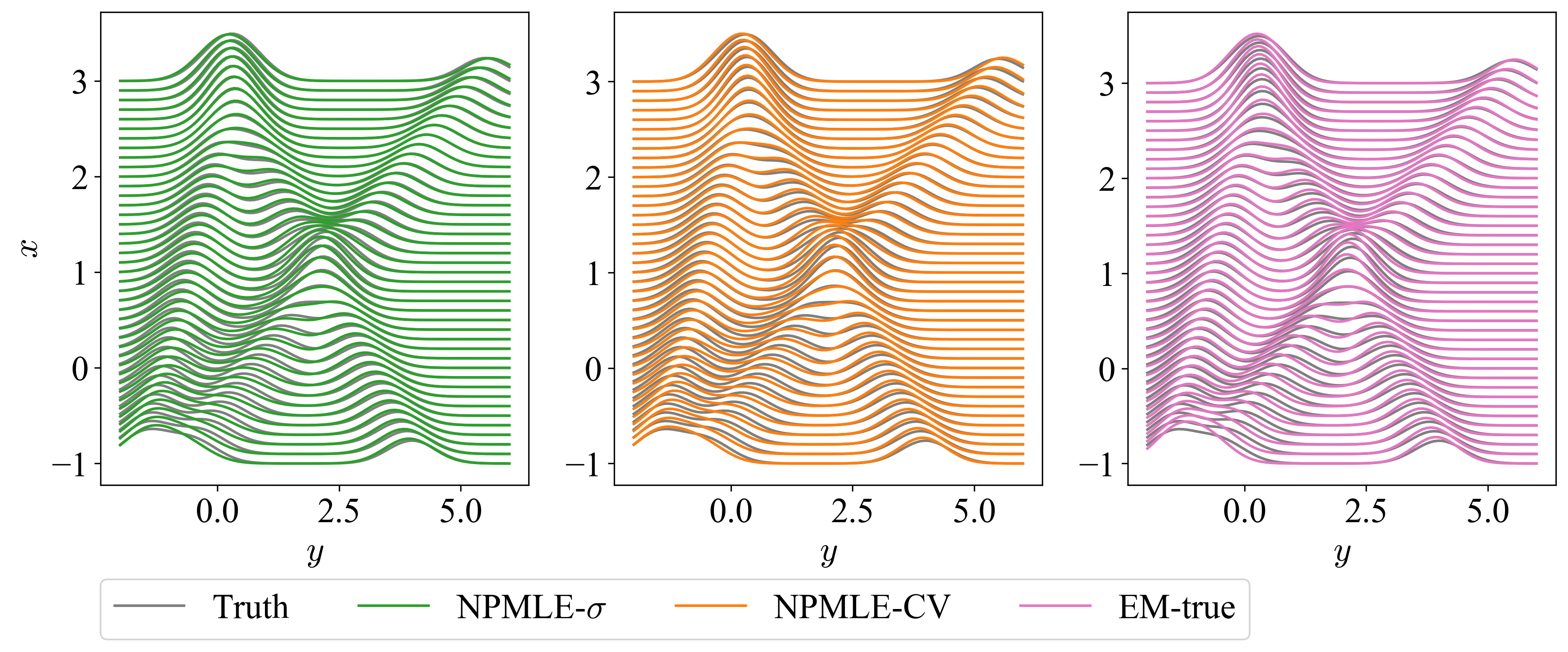

It is not surprising that the number of fitted regressions lines is larger than the true number 3 because the NPMLE is maximizing over a very large class of probability measures. However, critical structures of the three groups are recovered and, especially, each regression line with an estimated probability of at least is very close to one of the three true lines in Figure 1(b). Furthermore, the estimated conditional density function

is very close to the true conditional density function , and the accuracy is comparable to that of the density estimate given by the three-component EM algorithm initialized with true parameters:

and the estimate given by the NPMLE with the true parameter. This is depicted in Figure 3.

We have been able to prove rigorous results which show that the estimated conditional density function is a very good estimator for the true conditional density function under general conditions on and assuming that is known. These results are stated in terms of averaged squared Hellinger loss functions. For each fixed , model (1) states that the conditional distribution of the response given is which we estimate by . A natural and popular measure for comparing the discrepancy between the two densities and is the squared Hellinger distance

| (11) |

The squared Hellinger distance is a very popular loss function in density estimation (see, e.g., van de Geer (2000); Van Der Vaart and Wellner (1996)) and it has also been used in theoretical analysis of the NPMLE in Gaussian location mixture models (Ghosal and Van Der Vaart, 2001; Zhang, 2009; Saha and Guntuboyina, 2020).

The squared Hellinger distance in (11) is defined for a given . To get an overall error function, it is natural to average over . In the fixed design setting, we average over the observed design points and in the random design setting, we average with respect to the distribution of . Assuming that the set in (9) is a compact ball and that is supported on , we prove that the averaged squared Hellinger distance is, with high probability, of order up to multiplicative logarithmic factors in both the fixed design (Theorem 28) and random design (Theorem 4) settings. This proves the effectiveness of the fully nonparametric strategy of estimating : one does not need to make any parametric assumptions on and, at the same time, achieves near parametric rates for conditional density estimation (in the case where is compactly supported).

In the random design setting, we also prove that is consistent for in the sense that the Lévy-Prokhorov distance between and converges to zero in probability as . This result (Theorem 5) also requires the assumption that the set in (9) is a compact ball and that is supported on .

The remainder of this paper is organized as follows. In Section 2, we discuss the existence and computation of NPMLE. In Section 3, we present our theoretical results on the accuracy of the NPMLE. In Section 4, we provide experimental results including simulation studies and real data analysis. All these experimental results can be replicated with the code and data available at https://github.com/hanshengjiang/npmle_git. In Section 5, we argue that our methodology can also be used for the more general case of mixtures of nonlinear regression models. Proofs of all our theorems are given in Section 6.

2 Existence and Computation

2.1 Existence

We prove below that an NPMLE defined as in (9) exists, assuming that is either compact or that it satisfies a technical condition that holds when is the whole space . The following notation is used in the sequel. For a probability measure , we associate a vector by

where is defined as in (8). When is a degenerate probability measure concentrated at a point , we simply use for . Note that

Finally, we define

Theorem 1.

Suppose that is a closed subset of satisying either one of the following two conditions:

-

1.

is bounded (and hence compact).

-

2.

for every and linear subspace of (here is the projection of onto the linear subspace ).

Then, for every dataset , the optimization problem

| (12) |

admits a solution that is a probability measure supported on at most points in . Moreover the vector is unique for every maximizer and this unique vector, which we denote by , is the unique solution to the finite-dimensional optimization problem:

| (13) |

where denotes the convex hull of the set .

In the case when is compact, existence of that is asserted in the above theorem also follows from previous results in Lindsay (1983). The results in Lindsay (1983) do not apply to the case when is not compact. The second condition in Theorem 1 obviously applies to the case .

The fact that there exists a discrete NPMLE implies that we can restrict to discrete probability measures while maximizing (12). Theorem 1 also states that there exists with at most support points. In practice, NPMLEs typically have significantly smaller than support points as will be clear from the experimental results in Section 4 (see also Polyanskiy and Wu (2020) for a rigorous result in this direction in the case of univariate normal mixture models).

2.2 Computing Algorithm and Its Properties

We now discuss our algorithm for computing an (approximate) NPMLE . Our approach is very similar to the one taken by Jagabathula et al. (2020) for estimation in the mixture of logit regression model. Although (12) is a convex optimization problem, it is infinite dimensional as ranges over the class of all probability measures on . On the other hand, the problem (13) is finite dimensional and hence more tractable. Our strategy is to solve (13) approximately to obtain and then express as for some discrete probability measure . This will then be an approximate solution to (12).

In order to solve (13), it is necessary to make the constraint explicit. Existing algorithms for computing NPMLEs in mixture models rely on a priori discretization for this purpose. Specifically, they choose a set of vectors in (or in an appropriate compact subset of if is non-compact) and then approximate as

| (14) |

This leads to the following optimization problem which approximates (13):

| (15) |

This is an -dimensional convex optimization problem that can be solved in a variety of ways. One can use, for example, (a) the Vertex Direction method and the closely related Vertex Exchange Method (see, for example, Wu (1978); Lindsay (1983); Böhning (1986, 2000)), (b) the Expectation Maximization algorithm (Laird (1978); Jiang and Zhang (2009) and the, more recent, (c) algorithms based on black-box convex optimization (see Koenker and Mizera (2014)). If is a solution of the above problem, then the discrete probability measure taking the values with probabilities can be treated as an approximate NPMLE.

An obvious drawback of this approach based on (14) is the need to select an a priori discrete subset of which can be somewhat tricky to do in multiple dimensions. In contrast to these methods, the algorithm used in this paper for solving (13) does not rely on such a priori grid based discretization of .

Our algorithm uses the Conditional Gradient Method (CGM) (also known as the Frank-Wolfe algorithm) directly on (13) without any prior discretization. The CGM is an iterative algorithm for constrained convex optimization originally proposed by Frank and Wolfe (1956), and has regained attention for its efficiency in solving modern large-scale data analysis problems (Jaggi, 2013). The CGM applied to the problem (13) for maximizing subject to starts with an initial value and then generates a sequence of vectors which converge to a solution of (13) (under some conditions described later). Specifically, starting with , the iterates are generated in the following way: for each set

| (16) |

and then take

| (17) |

These two steps are repeated until a stopping criterion (described below) is satisfied. There are several variants of the CGM; the algorithm described above corresponds to the fully-corrective variant of the CGM (see, e.g., Jaggi (2013, Algorithm 4)).

For the implementation of this method, the two optimization problems (16) and (17) need to be solved. Before describing our ideas for solving (16) and (17), let us first remark that the CGM can also be applied to the discrete formulation (15) and this leads to algorithms that are very similar to the classical vertex direction and vertex exchange methods which have been historically popular approaches for approximate computation of the NPMLE in mixture models. More specifically, the vertex direction method is the line-search variant of the CGM while the vertex exchange method is the away-step variant of the CGM (these variants of the CGM are described in Jaggi (2013)) both applied to the discrete problem (15). In contrast to these approaches, our method applies the fully-corrective variant of the CGM directly to the original formulation (13).

Let us now describe our methods for solving (16) and (17). For (16), it is easy to see that

where

| (18) |

The above is a -dimensional non-convex optimization problem and we use available black-box optimization routines. In particular, we use the Powell conjugate direction method (Powell, 1964) from the Python scipy package (similar methods are also available in R in the packages mize and optim). These methods are iterative and require initialization. As is the case in most non-convex optimization problems, different initialization points may lead to different local maxima so we use multiple random initializations and take the solution with the highest objective function value.

In the usual vertex direction method which is basically CGM applied to the discretized formulation (15), the subproblem corresponding to (16) just involves a maximum over the finite set which can be solved exactly. However in our approach where we attempt to directly solve (13), we need to solve (18) which involves maximization over all and this necessitates using sophisticated optimization routines such as the Powell conjugate direction method.

For (17), it is easy to see that

where

| (19) |

The above is a finite dimensional convex optimization problem that can be solved using standard software such as the Rmosek package (ApS, 2019). The solution vector is usually sparse especially when is moderate or large.

The CGM comes with theoretical results (see Jaggi (2013)) that ensure converges to the global maximizer of (13) under a technical condition on the curvature of . This is the content of Theorem 2 below whose proof (provided in Section 6.2) is based on a slight modification of the arguments of Jaggi (2013, Proof of Theorem 1) and Clarkson (2010, Proof of Theorem 2.3). Theorem 2 assumes that solves (16) up to an additive error while solves (17) exactly. Allowance of an additive error while solving (16) is useful because (16) is a non-convex optimization problem and convergence to the global maximizer is usually difficult to guarantee. In contrast, it is straightforward to solve (17) to global optimality. Theorem 2 also gives an inequality (see (22)) that is potentially useful to design a stopping criterion for our algorithm.

Theorem 2.

Let us now make some remarks on the utility of Theorem 2. Inequality (21) shows that coverges to as provided

| (23) |

The sequence can be calculated during the iterates of the algorithm. Typically (this is true in all our applications), this sequence is bounded so that the first condition in (23) is satisfied. The second condition says that the Cesaro mean of converges to zero. A sufficient condition for it is

Qualitatively, this implies that the subproblem (16) need not be solved exactly and that approximately solving it up to an additive error of is enough. Precisely checking this condition is difficult however because the right hand side of (20) is typically unknown. In practice, we use multiple random initializations for the non-convex routines for solving (16) and hope that will be small.

Finally, let us state our intialization and stopping strategies for the CGM algorithm. Initialization can be arbitrary as Theorem 2 does not rely on carefully chosen . We recommend taking where

is the least squares estimator. This requires which is typically the case. Another initialization option is random initialization where one takes for some random .

For the stopping criterion, inequality (22) suggests that we can use the quantity:

to decide when to stop. Alternatively, one can opt to manually stop iterating when new iterates stop making significant increases in the log-likelihood function.

3 Theoretical Accuracy Results

In this section, we provide theoretical results on the performance of the estimator . We need to assume for these results that the set in the definition (9) of is of the form (here is the usual Euclidean norm) for some . We can always find such that as long as is compact. We assume that is actually equal to this ball for convenience. Unfortunately our results in this section do not hold when is not compact.

Our main focus is on proving rates of convergence for the accuracy of estimation of the conditional density of given . Under the model (1), the conditional density function of given is and our estimate of this conditional density is . We use the standard squared Hellinger distance (see the definition in (11)) to measure the discrepancy between the true and estimated conditional densities. This quantity is defined for each specific value . To obtain an overall loss function for evaluating the accuracy of conditional density estimation, we take the average over and this averaging is done differently in the fixed and random design settings. Let us first start with the fixed design setting where we assume that the design points are fixed (non-random). Here we take the average of over to obtain the loss function:

| (24) |

In the following theorem, we give a finite-sample bound on that holds in high probability and in expectation. The bound holds for every set of fixed design points and is parametric (i.e., of order ) up to logarithmic multiplicative factors in .

Theorem 3 (Fixed design conditional density estimation accuracy).

Consider data with where are fixed design points and are independent with having the density

| (25) |

Assume that

for some and .

Let be the estimator for defined as in (9) with . Let be defined via

| (26) |

where we use . Then there exists a constant depending only on such that

| (27) |

and

| (28) |

The error defined via (26) clearly satisfies as (keeping fixed) and thus gives the usual parametric rate for the fixed-design conditional density estimation loss up to the logarithmic multiplicative factor . Thus if the dimension is small, presents a very good estimator for in an average sense over and . This is remarkable because it implies that the NPMLE (which is obtained by likelihood maximization over a very large class of probability measures) does not suffer from overfitting.

The proof of Theorem 28 is based on empirical process arguments and is similar to the proofs of existing results on the Hellinger accuracy of the NPMLE in Gaussian mixture models in Jiang and Zhang (2009) and Saha and Guntuboyina (2020). A key ingredient in this result is a bound on the metric entropy of the function class

under a suitable metric. This metric entropy bound is stated in Theorem 7 and proved in Section 6.7.

We next consider the random design setting where we assume that are i.i.d. with (for some probability measure ) and conditional on having the density (25). In this case we take the loss function to be the average of over , i.e.,

In the following theorem, we give a finite-sample bound on that holds in high probability and in expectation. The bound is similar qualitatively to that given in Theorem 28 and is parametric up to a multiplicative factor.

Theorem 4 (Random design conditional density estimation accuracy).

in (29) is of the same order as in (26). Thus Theorem 28 and Theorem 4 give the same rate (assuming are fixed) for and respectively. Thus, in both the fixed and random design settings, the NPMLE provides a very good estimator for the true conditional density function if the dimension is small.

Theorem 4 is proved using the conclusion of Theorem 28 and an existing empirical process result (Lemma 1) which connects the random design loss to the fixed design loss.

Finally, we show that NPMLE is weakly consistent (in the random design setting) in the sense that its Lévy-Prokhorov distance to the ground truth approaches in probability as goes to infinity. The Lévy–Prokhorov metric in Theorem 5 is known to metrize the weak convergence of probability measures. We use the same assumptions as in Theorem 4 with the additional assumption that the support of contains a open set.

Theorem 5.

Consider and i.i.d. data with with and having the density (25). Assume that

for some . Further assume that the support of is contained in

for some and also that the support of contains an open set. Let , where we add subscript to denote the number of data points, be the estimator for defined as in (9) with . Then

where is the Lévy–Prokhorov metric.

4 Experimental Results

In this section, we illustrate the performance of our NPMLE approach on simulation and real data settings. All the experimental results from the paper can be replicated with the code and data available at https://github.com/hanshengjiang/npmle_git. Before describing the simulation and real data settings, let us first describe our cross validation scheme for estimating .

4.1 Cross-Validation for

We use a natural -fold cross-validation scheme where the whole dataset is randomly divided into roughly equal-sized parts . For every and a fixed value of , we obtain the estimate by computing the NPMLE on all data points excluding . Now for each data point in , the predicted conditional probability density is obtained as

Higher values of or of indicate better prediction for the data point . A reasonable cross validation is therefore

| (32) |

We estimate by the value which minimizes . We hereby denote the selected value by the cross-validation procedure as . In all our simulations with simulated dataset of size , we take . For the two real data examples with dataset sizes and , we take .

4.2 Simulation One: Discrete

The first simulation was already presented in Section 1 where was a discrete probability measure supported on three points (see Figures 1(a), 1(b), 2 and 3). Here aligned fairly well with even though had eight support points and had only three. Moreover, both and are accurate estimates of , as depicted in Figure 3.

4.3 Simulation Two: Continuous

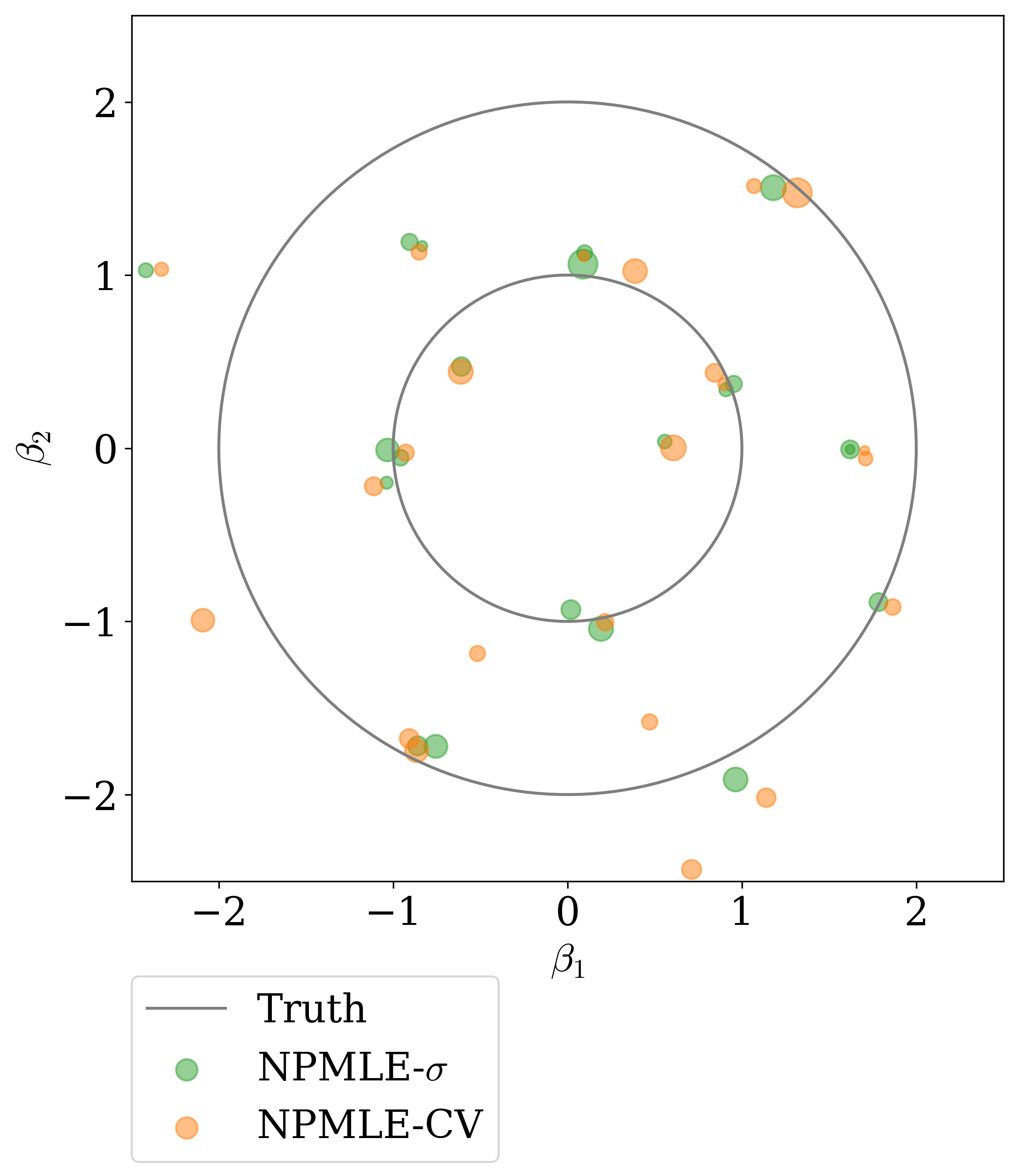

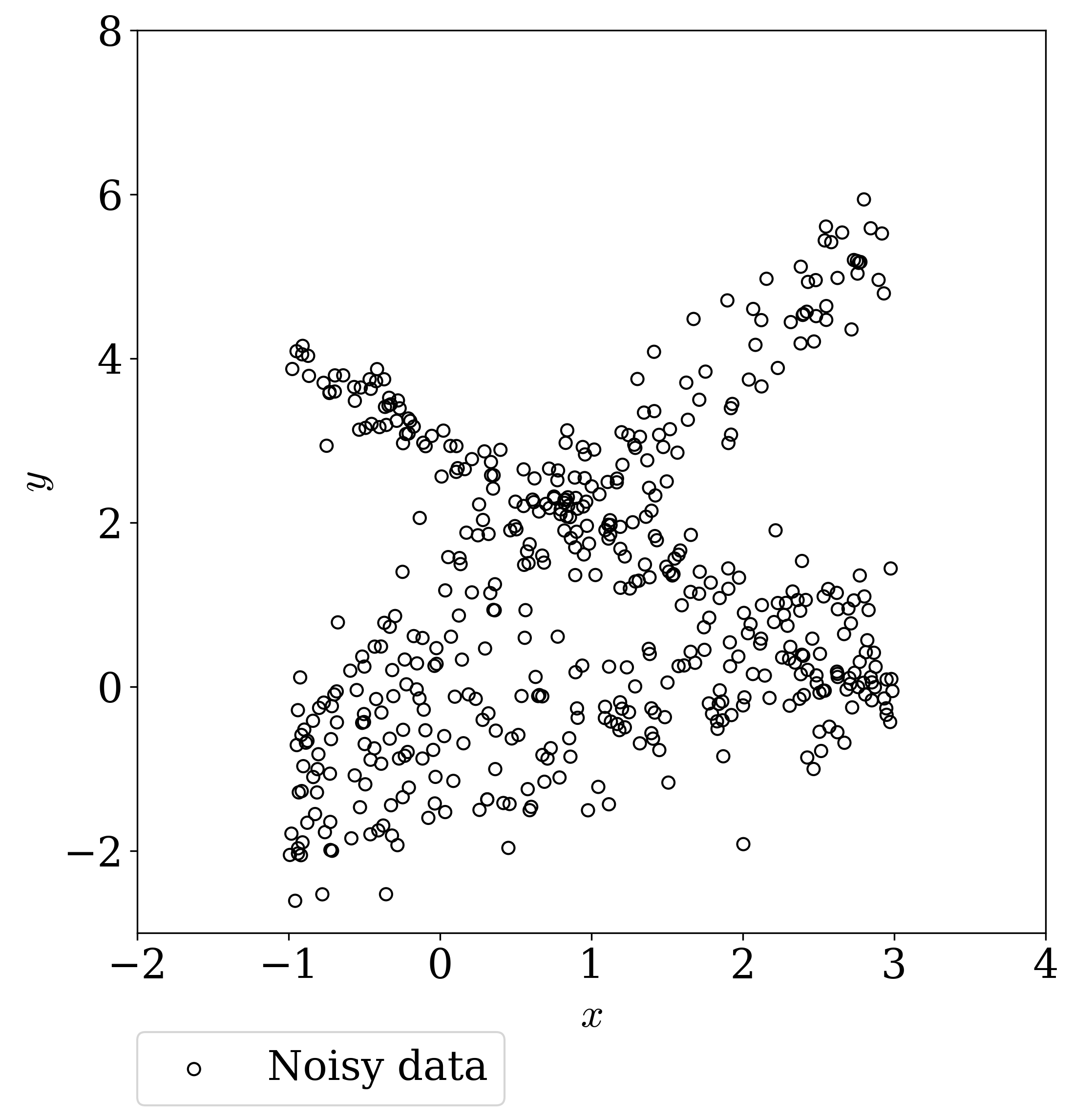

Consider the dataset showed in Figure 4(a) that is generated by our model with a continuous probability measure . Here is uniformly distributed over the two concentric circles centered at the origin with radii 1 and 2:

| (33) |

As in the previous simulation example, and the design points are independently generated from the uniform distribution on .

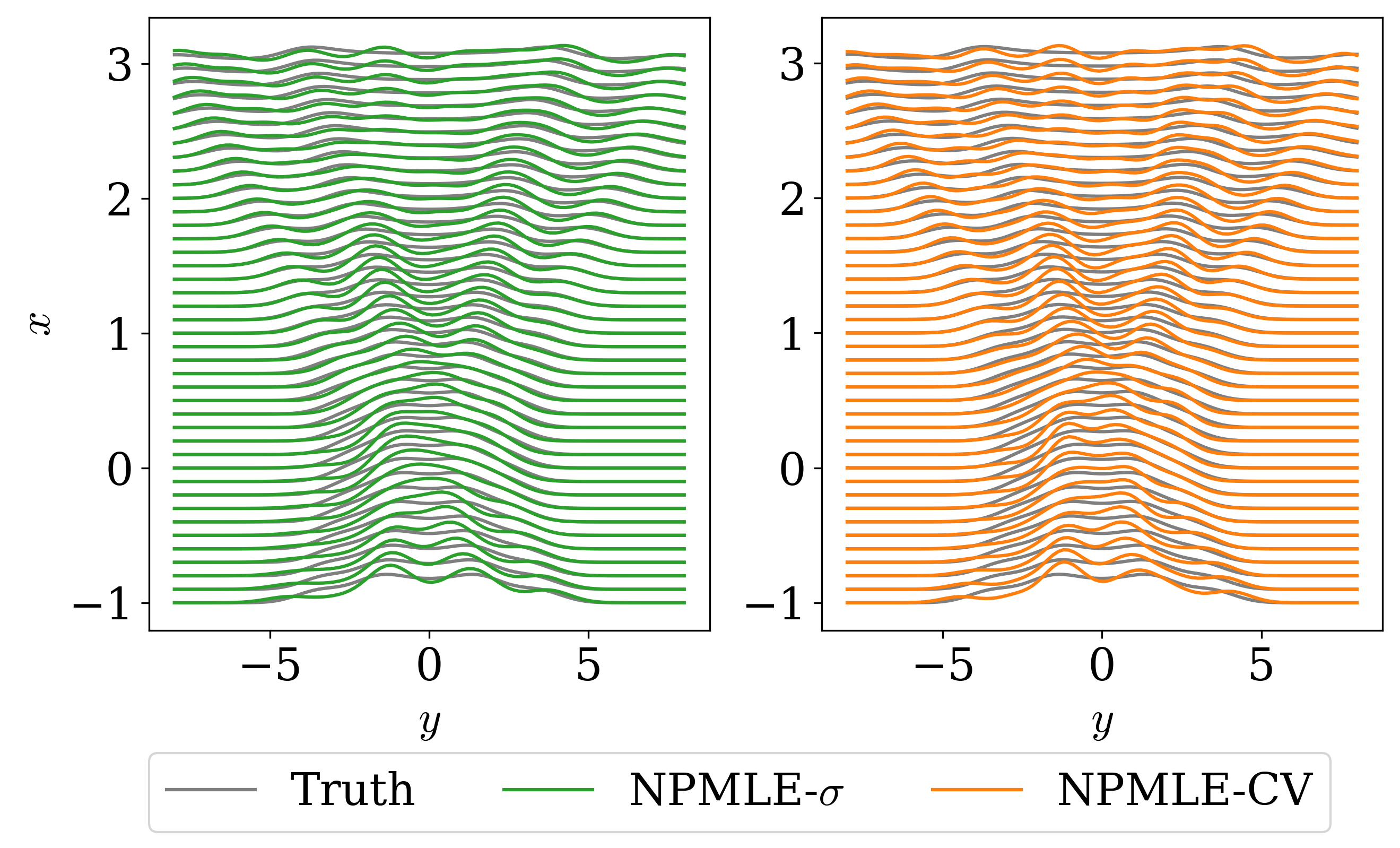

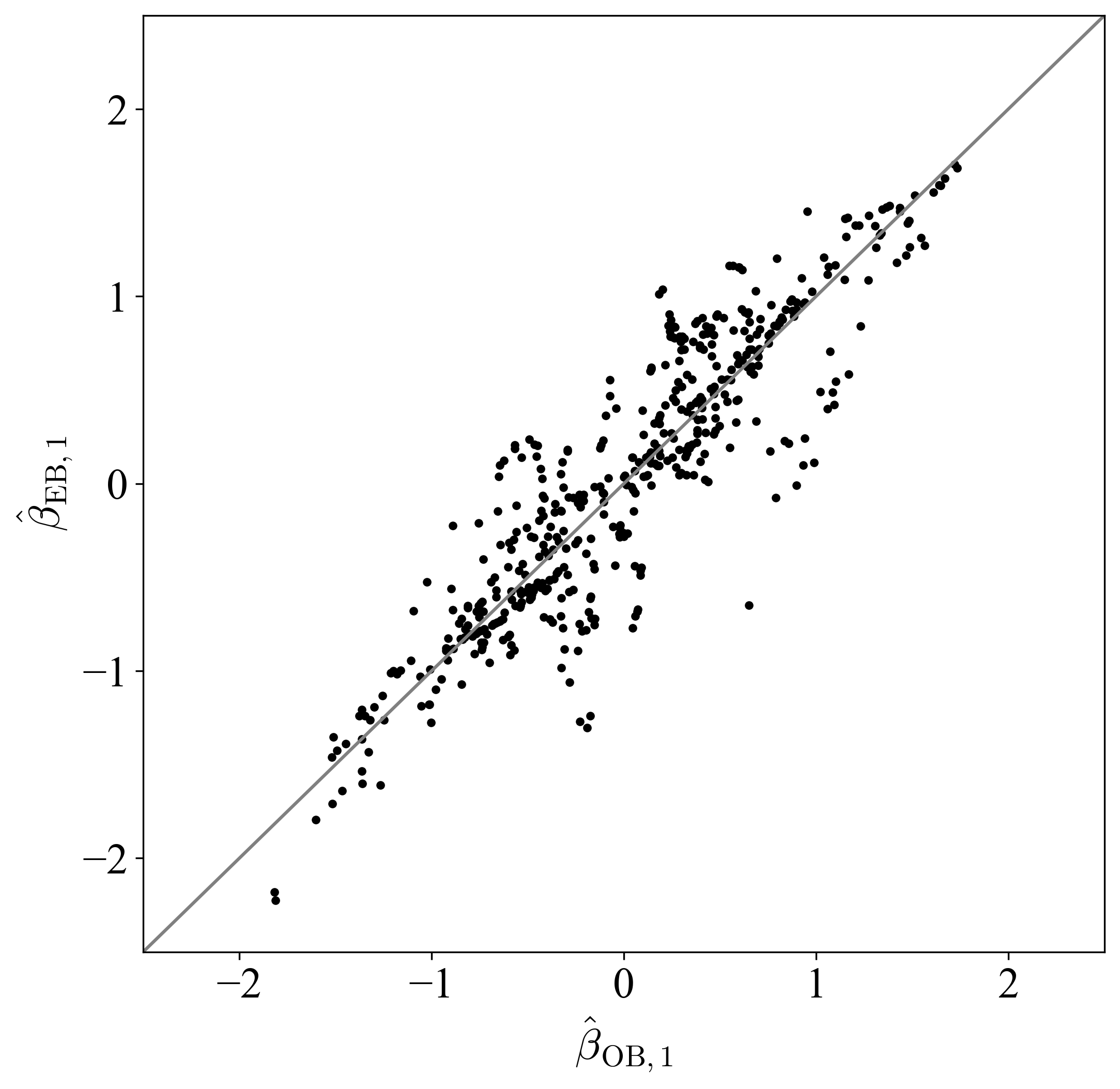

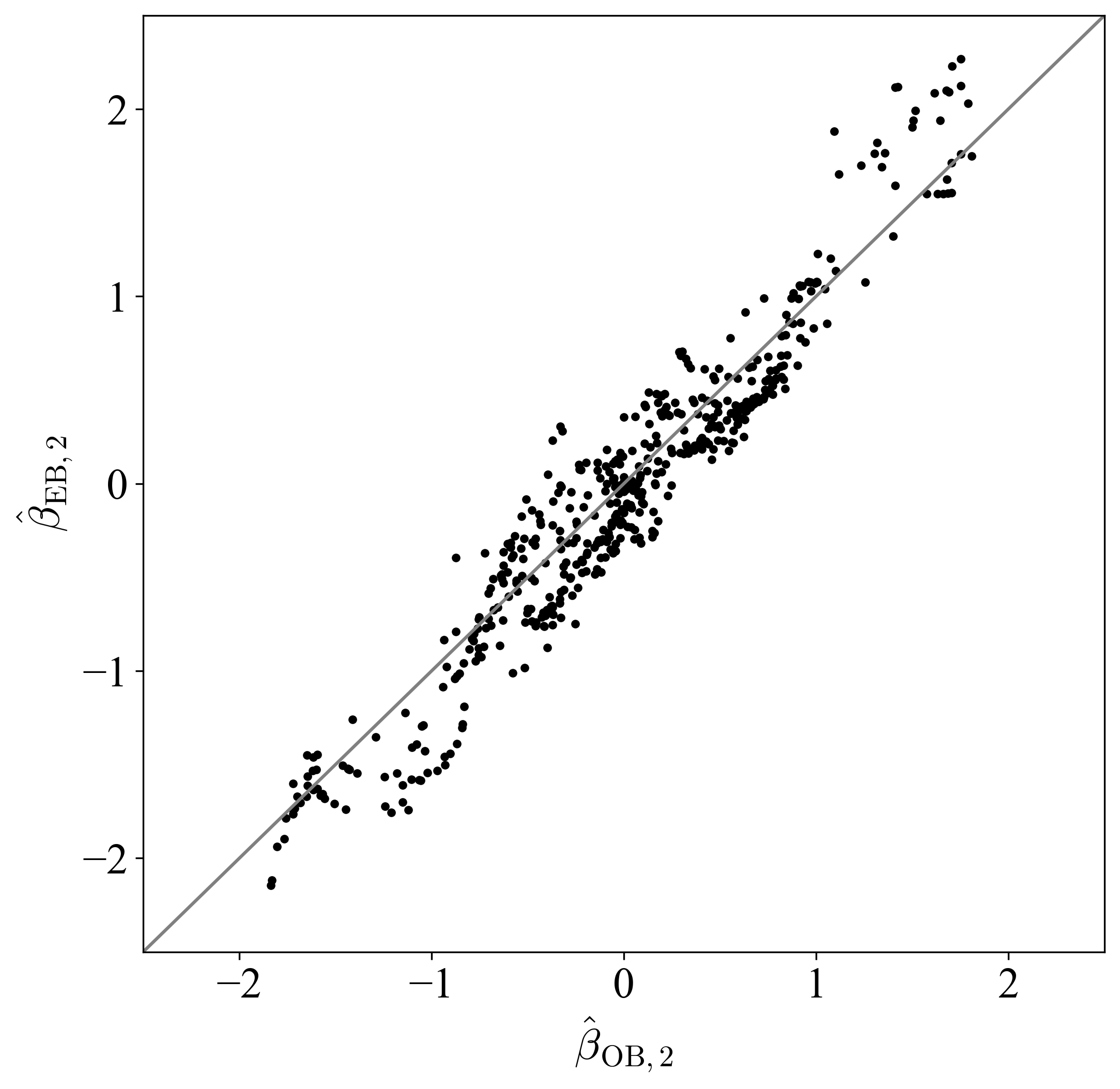

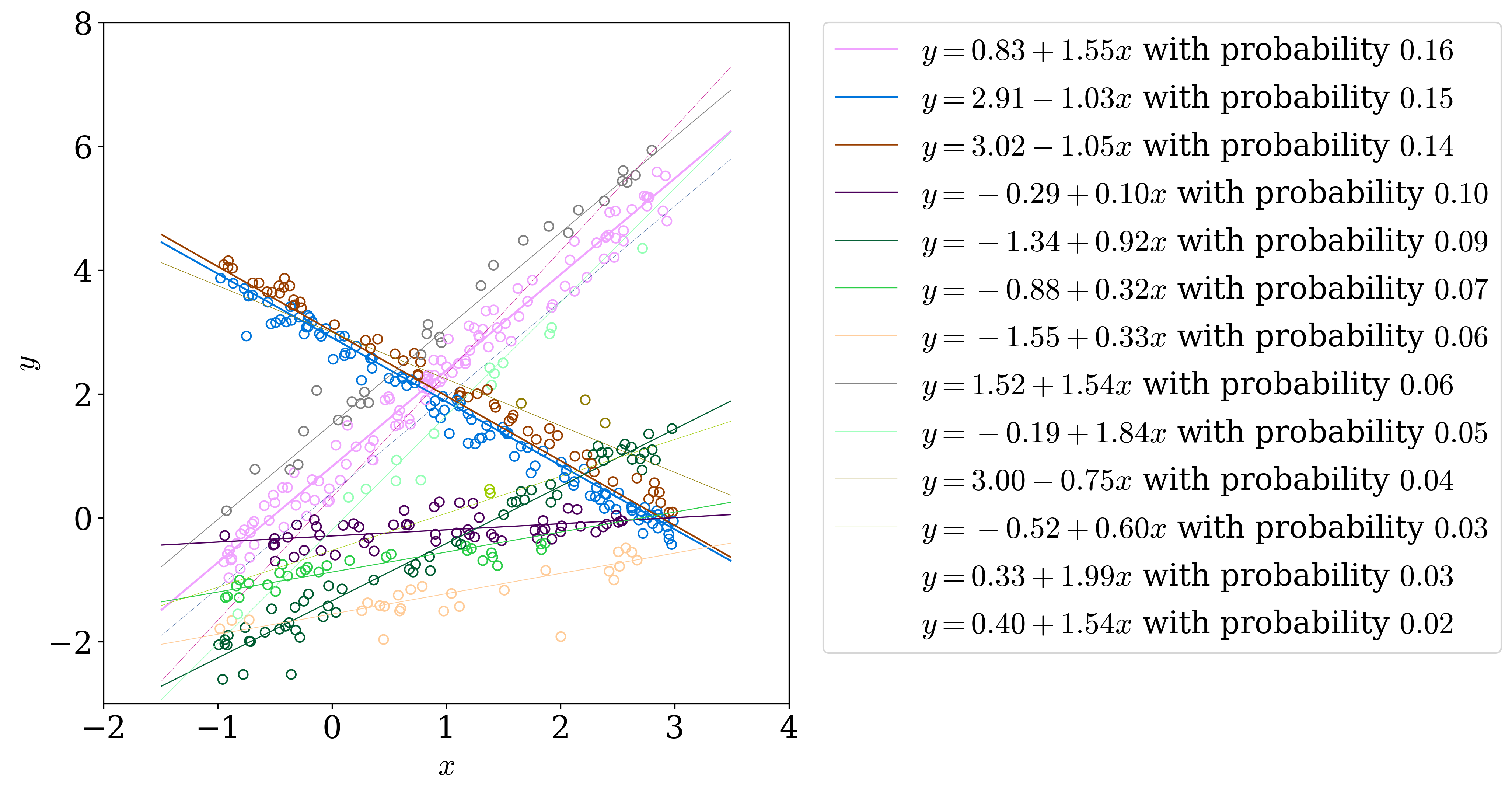

Our cross-validation procedure gave which we then used to compute (with ). Figure 5(a) plots and together (the size of each dot corresponds to the mixing probability at that point in ). Figure 4(b) plots the regression components based on the estimated , where the color coding follows the same rule as previously done in Figure 2. Since is now a continuous distribution, it is not surprising that the estimated contains many atoms. From Figure 5(a), it is clear that most of the dots corresponding to lie near one of the two circles on which is supported. It should also be clear that the the NPMLE with selected by cross-validation is close to the NPMLE with true . Figure 5(b) compares and with the truth and these are reasonably close.

As explained in Section 1, our approach produces an estimate for for each . This estimate is denoted by (defined in (7)) which should be viewed as an approximation to (defined in (5)). In Figure 6, we compare and for by plotting their two coordinates (intercept and slope) separately. That the approximation is working fairly well can easily be seen from the figure.

4.4 Simulation Three: Discrete with Heteroscedasticity

We now consider data simulated from a finite mixture of regressions model where the variances vary among the components. More specifically, we consider the regression model where the conditional distribution of given is

| (34) |

The component variances are allowed to change with . This model is actually a special case of (1) because it can be written in the form (1) for

| (35) |

for any . Here is the degenerate probability distribution concentrated on and denotes the product of the probability measures and . Also if for some , the probability measure should be interpreted as .

As a consequence, our estimation strategy should also work for the heteroscedastic model (34) and we shall demonstrate this with a simulated dataset here. We would like to note however that our theoretical results do not apply to this setting as in (35) has unbounded support. We take a setting similar to Figure 1(a) where the covariate is univariate (generated from the uniform distribution on ). The parameters are given by the three lines chosen with probabilities given by (this is exactly the same as in Figure 1(a)). The standard deviations vary with (unlike the case in Figure 1(a)) and we take these to be , . Data generated from this model is depicted in Figure 7(a).

We applied our estimation strategy to the data in Figure 7(a). Our cross-validation procedure gave , which is very close to the unknown true smallest heteroscedastic error . The result of our estimation procedure can be seen from Figure 7. As before (Figure 2), our approach leads to more lines (compared to the truth) but each fitted line is close to one of the three true lines. Also is an accurate estimate as depicted in Figure 8. This accuracy is comparable to the accuracy of and that of the estimate obtained by using the EM algorithm with three components initialized at their true values.

4.5 Real Data Example One: Music Tone Perception

We apply our method to the music tone perception data originally collected by Cohen (1980). This dataset is available, for example, in the R packages mixtools (Benaglia et al., 2009) and fpc (Hennig and Imports, 2015), and has been previously analyzed by De Veaux (1989), Viele and Tong (2002), and Yao and Song (2015). This data was collected in music experiments where a trained musician was presented with a pure fundamental tone plus a series of stretched overtones and was then asked to tune an adjustable tone to the octave above the fundamental tone. The regressor is the stretching ratio of the overtone to the fundamental tone. The response variable is the ratio of the adjusted tone to the fundamental by the musician.

At that time of Cohen (1980), there existed two conflicting music perception theories regarding the relationship between and . One theory states that the adjusted tone is constantly at ratio to the fundamental tone (), while the other theory states that the adjusted tone will be equal to the overtone ().

While existing studies are built on two-component mixture models with heteroscedastic errors, we apply our NPMLE approach without prior knowledge on number of components. Compared to data points in simulation settings, there are only data points in this real dataset, and thus we increase the number of folds in cross-validation correspondingly. We run -fold cross-valition, and the choice of by cross-validation is .

Figure 9 shows the fitted result together with original data points. Similar to our simulation plots, the thickness and darkness of each line in Figure 9 are proportional to the mixing probability of the corresponding component. While there are more than two components in Figure 9, two major components account for most of the mixing probabilities, and all other components occupy very low probabilities. Compared to the two-component modeling in Viele and Tong (2002), the fitted result in Figure 9 attains a considerably higher log-likelihood of 175.50 whereas the highest log-likelihood in Viele and Tong (2002) is 145.52 (our choices of are rather close). We would like to mention again that the NPMLE approach does not use the prior knowledge of two music theories. Yet, the algorithm is able to identify two major components, which are very close to the conjectural regression functions and respectively.

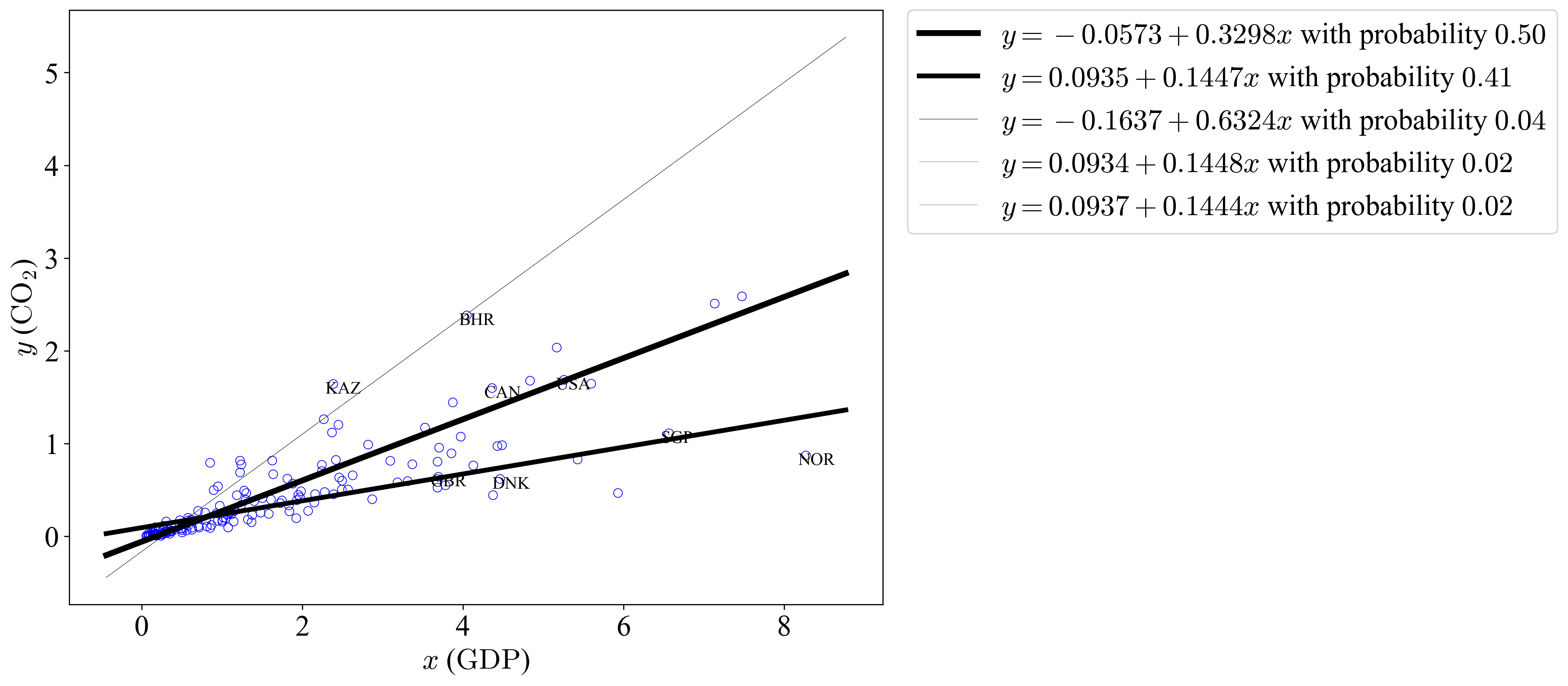

4.6 Real Data Example Two: CO2-GDP

Although it seems reasonable to assume a two-component structure in the aforementioned music dataset given the side information of two music perception theories, many real datasets do not come with such a clear structure, and the number of components is unknown. In this example, we apply our NPMLE approach to a real dataset in this latter category.

CO2 is a greenhouse gas primarily produced from fossil fuel consumption. Increased CO2 emissions are generally considered to be responsible for global warming. GDP is a measure that reflects a country’s economic wellbeing. Human activities that lead to high GDP often correspond with high CO2 emissions. Considering both the economy and the environment, it is desirable for countries to achieve high GDP per capita while maintaining low CO2 per capita. Therefore, the correlation of CO2 and GDP attracts considerable attention. We retrieve per capita data of 159 countries in year 2015 from Roser (2021). We set the CO2 emissions per capita (in 10 tons) as the response variable , and set the GDP per capita (in 10,000 USD) as the regressor . A value of is selected by -fold cross-validation. Previously, the CO2-GDP relationship has been modeled with mixture of linear regression models with a pre-specified number of components in Hurn et al. (2003) and Huang and Yao (2012).

Figure 10 shows the fitted result together with original data points. For certain countries, the country’s circle marker in Figure 10 is annotated with its three-digit country code. The thickness and darkness of each line in Figure 10 are proportional to the mixing probability of the corresponding linear regression component. In Figure 10, there are several fitted linear regression components, but only two of them take most of the mixing probabilities. We now take a closer took at these linear regression components in Figure 10. All five components share similar intercepts, which are all close to , but the slopes differ. The component with the highest mixing probability has a medium slope value, and countries near this component include Canada, United States, etc. The component with the highest slope value has a very low mixing probability, and countries near this component include Bahrain, Kazakhstan, etc. The component with the lowest slope value has a relative high mixing probability, and countries near this component include Great Britain, Denmark, Norway, etc. Interestingly, countries in the same component seem to be geographically close, or similarly rich in fossil fuel resources. The fitted result indicates the 159 countries can be effectively categorized to several groups in terms of CO2 emissions and GDP growth relationship. The identification of such subgroups can help to illustrate potential developing paths of lower GDP countries, which was pointed out in Hurn et al. (2003).

5 Extension to Mixture of Nonlinear Regression

In this section, we argue that the NPMLE approach can also be applied to the more general case of mixtures of nonlinear regression models. Here the conditional distribution of given is given by the density

| (36) |

where represents a possibly nonlinear regression function parametrized by a -dimensional parameter . The covariate , as before, has dimension . The dimensions (of ) and (of ) are not necessarily equal.

Our estimation strategy can be extended to the problem of estimating from independent observations drawn from the above model. Assuming that is supported on for a known constant , we estimate by the NPMLE defined via

| (37) |

The existence of in (37) when is compact follows from the same argument as in the proof of Theorem 1. Our computational algorithm from Subsection 2.2 based on the CGM can be used with little modification (basically must now be replaced by ) to compute the above estimator . We initialize the CGM with where is a random point in . The cross validation procedure to choose also works analogously as before.

We have found that our estimation strategy works well for estimation under the model (36) for several different nonlinear functions including polynomials, exponentials and trigonometric functions. As illustration, consider the data shown in Figure 11(a). These are 500 points generated independently from the model (36) with

The probability measure is given by and is given by .

In other words, the true regression function equals one of the two nonlinear functions and with equal probability. These two functions are also plotted in Figure 11(a) and the individual data points are colored according to the function which generated them. These colors (and the curves corresponding to the true functions) are of course not available to the data analyst. While applying our method to this dataset, we make the assumption that the component regression functions are known to be of the form but we do not know the values of .

The results of applying our method to the data in Figure 11(a) are shown in Figures 11(b) and 11. We took in (37) to be . was estimated by and the fitted had four components. Our method estimated 4 regression components but two of them are very close (up to rounding errors) to and the other two are very close to . These are, in turn, quite closely aligned with the true regression functions and . The estimated probabilities of these two components were and respectively (while the true probabilities were equal to ). Figure 11 shows that the estimated density function

is an accurate estimator for

and the accuracy is compared to that of our estimator computed with known to be its true value.

It would be of interest to extend the theoretical results of Section 3. We do not know how to do this for a large class of nonlinear functions . Let us just remark here that it is straightforward to extend Theorem 28 to the case where is a polynomial in . This leads to the following theorem.

Theorem 6.

Consider data with where are fixed design points and are independent with having the density (36) with . Assume that, for every , the function is a polynomial of degree at most . Assume that for some and that is a positive quantity such that

| (38) |

Then inequalities (27) and (28) hold with replaced by

| (39) |

The rate given in (39) has the same qualitative behavior as the rates of Theorem 28 and Theorem 4. Specifically it is assuming that are all fixed. Theorem 28 can be viewed as a special case of Theorem 39 with , , and . Also (defined in (38)) can be taken as any value that is at least because, by the Cauchy-Schwarz inequality,

Under the assumption in Theorem 28, one can thus take in (39) and this yields the conclusion of Theorem 28.

6 Proofs

6.1 Proof of Theorem 1

The notation for , and introduced at the beginning of Subsection 2.1 will be used in the proof below.

Proof of Theorem 1.

The objective function in the optimization problem (12) only depends on through the vector . As a result, (12) is equivalent to

| (40) |

where denotes the element of the vector and

The set need not be compact in general. We claim that

| (41) |

where denotes closure and denotes convex hull. This claim will be proved later. The set is compact because is compact (as is bounded) and as the convex hull of a compact set in Euclidean space is compact (see, for example, (Bertsekas et al., 2003, Proposition 1.3.2)). Therefore a solution exists for the optimization problem

| (42) |

Further the solution is unique as the objective function is strictly concave. Moreover lies in the boundary of the set because otherwise would have to be zero which is impossible. As a result, by the the Carathéodory theorem (see, for example, (Silvey, 1980, Appendix 2)), can be written as a convex combination of at most points in i.e., for some , and with . We now claim that under the assumptions on given in the statement of Theorem 1, for every , there exists such that

| (43) |

Assuming the validity of this claim (which will be proved later), there exists for which

| (44) |

Now if for some and , we would have having a higher objective value compared to (note that all components of are all strictly positive for every ) which would contradict the fact that is the unique solution to (42). We thus have for all which implies, by (44), that for every . This obviously implies that so that . Also

As a result which shows that is the unique solution to (40) and this completes the proof of Theorem 1. We only need to prove the two claims (41) and (43).

For (41), take where is a probability measure on . By Parthasarathy (2005, Theorem 6.3), there exist discrete probability measures with finite supports converging weakly to as and this implies for . As a result, as . This implies that

because each . To complete the proof of (41), it is enough to show that

| (45) |

For (45), first note that which implies . is convex, and is the smallest convex set that contains , so

For the other inclusion, observe that, as noted earlier, is compact so that

We next prove (43). Fix . If is compact, then is also compact so that which means that for some and this proves (43). So let us assume that is not necessarily compact and that the second assumption in the statement of Theorem 1 holds.

Let and let be the linear subspace of spanned by (recall that are the observed covariate vectors). Because , we can write for some sequence in . For , let denote the projection of onto so that for all and all . Also by our assumption on , we have . We will show that is bounded.

For , thus is bounded and exists. Since , is also bounded. Take an orthonormal basis of as . For any , since is spanned by , is a linear combination of . Therefore, as a linear combination of , is bounded (noting that the linear combination coefficients do not depend on ). Because

it follows that is also bounded. Now we can take a convergent subsequence of . The limit of the subsequence, denoted by , also belongs to because is assumed to be closed. For , . Let denote the atomic likelihood vector with respect to , then for all . This proves (43) and thereby completes the proof of Theorem 1. ∎

6.2 Proof of Theorem 2

Proof of Theorem 2.

Fix . By definition of and the fact that solves (17), we have

| (46) |

By (20), we have

| (47) |

Using concavity of , we get

| (48) |

Combining the above three inequalities, we obtain

which is equivalent to

| (49) |

We shall prove

| (50) |

where the product term on the right hand side should be interpreted as 1 for . (50) immediately implies (21) because

We use induction on to prove (50). Taking in (49) and noting that , we get

which proves (50) for . Assume that (50) is true for . Using (50) for in (49), we get

6.3 Proof of Theorem 28

The proof of Theorem 28 given below uses the notion of covering numbers and metric entropy which are defined as follows. Let be a subset of a metric space with metric . For , we say that a set is an -covering of if . The smallest possible cardinality of an -covering of is known as the -covering number of under the metric and this is denoted by . The logarithm of is called the -metric entropy of under . When is a subset of and the metric is the usual Euclidean metric on , we shall denote by simply .

The proof of Theorem 28 given below is based on ideas similar to those used in Jiang and Zhang (2009) and Saha and Guntuboyina (2020). A key ingredient is the metric entropy result stated as Theorem 7. Theorem 7 is stated for the more general case of possibly nonlinear regression functions . We take while applying Theorem 7 in the proof below.

Proof of Theorem 28.

Let so that contains all the design points . Let

| (51) |

where . Let be the pseudometric on given by

Theorem 7, which will be crucially used in this proof, gives an upper bound on the -covering number of under the pseudometric . For a fixed , let be an -covering set of under where . This ensures

| (52) |

For a fixed sequence and , let us now bound (the precise form for will be given later in the proof; it will equal a constant multiple of ).

We define a set . Let be composed of all index for which there exists satisfying

| (53) |

Let be such that (such a clearly exists because form an -covering set of ). Now if , then and consequently which implies that

Therefore, we have

where the first inequality follows from the fact that maximizes the likelihood. We thus get

where we used the union bound in the second line and Markov’s inequality (followed by the independence of ) in the third line. For each ,

where we used the inequality in the second line, and the last equality follows from the fact that has density . The simple inequality now gives, for each ,

As a result, we deduce

As we have assumed that for every ,

we obtain

We have thus proved

which gives (note that )

| (54) |

We now use the metric entropy result in Theorem 7 to bound . Setting and in Theorem 7, we get

where and is defined in (69). It is clear that for the linear model, and (note that we have made the assumption ). The Euclidean covering number is bounded in the following way. It is well-known that

and consequently

This and the fact that lead to

| (55) |

where absorbs a coefficient in the last line. Using the above in (54), we obtain

We shall now take and so that

| (56) |

This will ensure that, for ,

| (57) |

To satisfy (56), we first take (so that ). The quantity will then have to satisfy the two inequalities:

| (58) |

and

| (59) |

It is now elementary to check that (58) is satisfied whenever

and (59) is satisfied whenever

where we used the notation .

We may now assume . It is then easy to see that both the above inequalities and consequently both (58) and (59) are satisfied whenever

Using and absorbing all the -dependent constants in , we deduce that inequality (57) holds for where is defined in (26). This completes the proof of (27) (note that can be bounded by by taking larger than 4).

6.4 Proof of Theorem 4

The proof of Theorem 4 uses the following result from the theory of empirical processes which follows from van de Geer (2000, Proof of Lemma 5.16).

Lemma 1.

Suppose are independently distributed according to a probability distribution and suppose is a class of functions on the support of that are uniformly bounded by 1. Then

| (60) |

provided satisfies

| (61) |

Here denotes the -bracketing number of in the metric defined as the smallest number of pairs of functions satisfying and the property that every is sandwiched between one such pair (i.e., for some ).

Proof of Theorem 4.

We shall use Lemma 1 with equal to the class of all functions

on the set as ranges over the class of all probability measures on . Note that the function above is uniformly bounded by 1. The key to the application of Lemma 1 is to bound and for this, we use the inequality:

| (62) |

where is as in (51),

and is the metric on the set . To prove (62), let and let be an -covering set of under the -metric on . This means that for every probability measure on , there exists such that

which implies that for all . As a result

lies in the interval

where . The squared distance between the two end points of the above interval equals

| (63) |

Because for all , we can bound (63) by

and this proves (62).

The quantity is bounded from above by a finite constant depending only on and because of the following argument.

For , we use the trivial inequality

and for , we use

which is true because (note that )

We thus get

for a universal positive constant .

Using (55), the covering number is bounded by

for a positive constant depending on alone. Inequality (62) then gives

where .

6.5 Proof of Theorem 5

The proof of Theorem 5 relies on Theorem 4. It also uses the following lemma whose proof is similar to Beran and Millar (1994, Proof of Proposition 2.2). We recall that the mixture of linear regression model under random design can be expressed as

| (64) |

Let denote the joint distribution of under the above model. We use to denote an NPMLE given data points. Let denote the Lévy–Prokhorov metric, which is known to metrize the weak convergence of probability measures.

Lemma 2.

Assume the support of contains an open set, if

where denotes a sequence of probability measures such that , then

Proof of Lemma 2.

Because is supported on a compact ball, is tight, and has a subsequence converging weakly (Theorem 3.10.3 in Durrett (2019)). Let denote the limiting probability measure of the weakly convergent subsequence, then

Meanwhile, the weak convergence of to implies

for all and . Combining the above two equations, we get

The Fourier inversion theorem now gives,

| (65) |

Both sides of equation (65) are bounded and thus analytic as function of . Furthermore, since the support of is assumed to contain an open set, (65) holds for all . Alternatively, by viewing as the argument of characteristic functions, (65) shows that and have the same characteristic functions and thus .

Therefore, we have shown that every weakly convergent subsequence of weakly converges to . Suppose that does not converge weakly to , then there exists , for every there exists such that . It is clear that any subsequence of cannot converge weakly to . However, following the same argument before, is tight and contains a weakly convergent subsequence converging to leading to a contradiction. This completes the proof of Lemma 2. ∎

We are now ready to prove Theorem 5.

Proof of Theorem 5.

Based on (30) in Theorem 4, converges to in probability. We first notice that is exactly the Hellinger distance between and . Since convergence under Hellinger distance is stronger then weak convergence, we have

in probability. We now invoke a classic probability result (Theorem 2.3.2 in Durrett (2019)): given random variables and , in probability if and only if for every subsequence , there is a further subsequence converges almost surely to . Consider the random sequences and , for any subsequence , there is a further subsequence

that converges to almost surely because in probability and consequently almost surely because of Lemma 2. Thus we have shown that in probability.

∎

6.6 Proof of Theorem 39

Proof of Theorem 39.

Theorem 39 follows same arguments as in the proof of Theorem 28. As in the proof of Theorem 28, (54) can be deduced to obtain

where . Setting and in Theorem 7, we get

where is as in (38). In the proof of Theorem 28, we could set and use but now, we need to keep both and here. Again, we use the well-known bound on the Euclidean covering number that and set , which leads to

We then take and so that

| (66) |

is taken (as in the proof of Theorem 28) to be . It is elementary to check that (66) holds when satisfies both

and

We further simplify the conditions for and absorb constants into , the crucial condition for becomes (assuming and noting that )

We then take as a upper bound of as below

The remainder follows the same argument as in Theorem 28. ∎

6.7 Metric Entropy Result: Theorem 7 and its proof

In this section, we prove our metric entropy results, and these results provide key ingredients for the proof of Theorem 28 and Theorem 4. The main theorem of this section is Theorem 7. We work here under a more general setting than linear regression functions. Specifically, we use the function to represent the mean of the response given and so that the conditional density function of given is

Let denote an arbitrary compact set in and

| (67) |

The goal of this section is to prove an upper bound on the covering number of under the metric :

| (68) |

for an arbitrary set of -values. For each , let be defined as

| (69) |

so that

Theorem 7.

Suppose that, for every , the function is a polynomial function of degree at most . Then there exists a constant depending only on such that for every , we have

| (70) |

where .

We prove Theorem 7 by modifying appropriately the proof of the metric entropy results for Gaussian location mixtures in Zhang (2009) (see also Ghosal and Van Der Vaart (2007) and Saha and Guntuboyina (2020)). Actually Theorem 7 can be seen as a generalization of metric entropy results for Gaussian location mixtures. Indeed, in the special case when , , , and (for some ), the class becomes

and inequality (70) gives that the -metric entropy of under the metric on is bounded by

for all . This is essentially Zhang (2009, inequality (5.8)).

The proof of Theorem 7 crucially relies on Lemma 72 (moment matching accuracy) and Lemma 74 (approximation by discrete mixtures) which are given next. Lemma 72 follows almost directly from the corresponding result for Gaussian location mixtures (see Jiang and Zhang (2009, Lemma 1) or Saha and Guntuboyina (2020, Lemma D.2)) but Lemma 74 requires additional arguments.

Lemma 3.

Fix a pair and let be a subset of such that

for some and where

and

Let and be two probability measures on such that for some and all integers , we have

| (71) |

Then

| (72) |

Proof of Lemma 72.

Lemma 4.

Let be a probability measure supported on . For every , there exists a discrete probability measure supported on at most

| (73) |

points in such that

| (74) |

Proof of Lemma 74.

Let us introduce a pseudometric on as

| (75) |

Fix and let denote the -covering number of under the pseudometric . Let denote balls of radius (with respect to ) within whose union is equal to . We define and for . Let and consider the following collection of -dimensional vectors:

By standard results, it follows that is the convex hull of

This follows, for example, from Parthasarathy (2005, Theorem 6.3) and the fact that is closed. Notice that both and lie in the Euclidean space of dimension . By Carathéodory’s theorem, any vector in can be written as a convex combination of at most elements in . This implies that for every probability measure on , there exists a discrete measure which is supported on a discrete subset of of cardinality at most such that

| (76) |

Fix and . We shall prove the bound (74) for by using Lemma 72. First note that since is contained in , the sets cover . Let so that

We shall prove below that

| (77) |

which will enable us to apply Lemma 72 with . To see (77), note that for each fixed , there exists such that , i.e., . As the diameter of (under the metric ) is at most , it follows that for every . Consequently,

This proves (77). In order to apply Lemma 72, we need to check that inequalty (71) holds. This basically follows from (76) and the fact that is assumed to be a polynomial function of the components of with degree (this will ensure that the terms being integrated on both sides of (71) are polynomials of components of with degree up to ). Lemma 72 can thus be applied (with and ), which gives

Because , we have and

where we used the simple fact that . This proves (74). It remains to prove that the cardinality of the support of is at most (73). As we have already seen that the cardinality of the support of is at most , we only need to show that is at most the Euclidean covering number . For this, note that by definition of , we have

for every . This gives

| (78) |

which completes the proof of Lemma 74. ∎

Proof of Theorem 7.

Fix a probability measure that is supported on . By Lemma 74, for each fixed , there exists a probability measure supported on such that

and such that the cardinality of the support of is at most where is given by (73).

Now let . Let be an -covering of under the pseudometric (defined in (75)), where (via (78))

| (79) |

Also let be a -covering of the probability simplex under the -metric where . We can write for some and . Since form an -covering of , we can find (not necessarily distinct) elements from such that . Letting , we have

for every and . Also since is a -covering of under the metric, there exist from such that . Denote , then for every and any , we have

Combining three inequalities together, we have

| (80) |

for all and . We now take so that . The right hand side of (80) is bounded by

Therefore, as varies, the collection of functions forms an -covering of under the metric . It remains to bound the cardinality of this collection which equals . Thus

By Stirling’s formula,

By (79) and (73), we have so that . Also is the -covering number of under the -metric which implies, by a well known result, that . We thus get

By and , we get

| (81) |

for a universal constant . It also follows from (73) that

This, combined with (81), completes the proof of Theorem 7. ∎

References

- ApS (2019) ApS, M. (2019). The R to MOSEK Optimization Interface. R package version 1.3.5.

- Battisti and De Vaio (2008) Battisti, M. and G. De Vaio (2008). A spatially filtered mixture of -convergence regressions for EU regions, 1980–2002. Empirical Economics 34(1), 105–121.

- Benaglia et al. (2009) Benaglia, T., D. Chauveau, D. R. Hunter, and D. Young (2009). mixtools: An R package for analyzing finite mixture models. Journal of Statistical Software 32(6), 1–29.

- Beran et al. (1996) Beran, R., A. Feuerverger, and P. Hall (1996). On nonparametric estimation of intercept and slope distributions in random coefficient regression. The Annals of Statistics 24(6), 2569–2592.

- Beran and Hall (1992) Beran, R. and P. Hall (1992). Estimating coefficient distributions in random coefficient regressions. The Annals of Statistics 20(4), 1970–1984.

- Beran and Millar (1994) Beran, R. and P. W. Millar (1994). Minimum distance estimation in random coefficient regression models. The Annals of Statistics, 1976–1992.

- Bertsekas et al. (2003) Bertsekas, D. P., A. Nedi, and A. E. Ozdaglar (2003). Convex analysis and optimization. Athena Scientific.

- Böhning (1986) Böhning, D. (1986). A vertex-exchange-method in d-optimal design theory. Metrika 33(1), 337–347.

- Böhning (2000) Böhning, D. (2000). Computer-assisted analysis of mixtures and applications. Taylor & Francis Group.

- Clarkson (2010) Clarkson, K. L. (2010). Coresets, sparse greedy approximation, and the frank-wolfe algorithm. ACM Transactions on Algorithms (TALG) 6(4), 1–30.

- Cohen (1980) Cohen, E. (1980). Inharmonic tone perception. Ph. D. Dissertation, Stanford University.

- De Veaux (1989) De Veaux, R. D. (1989). Mixtures of linear regressions. Computational Statistics & Data Analysis 8(3), 227–245.

- Deb et al. (2021) Deb, N., S. Saha, A. Guntuboyina, and B. Sen (2021). Two-component mixture model in the presence of covariates. Journal of the American Statistical Association, 1–15.

- Dicker and Zhao (2016) Dicker, L. H. and S. D. Zhao (2016). High-dimensional classification via nonparametric empirical bayes and maximum likelihood inference. Biometrika 103(1), 21–34.

- Durrett (2019) Durrett, R. (2019). Probability: theory and examples, Volume 49. Cambridge university press.

- Elhenawy et al. (2016) Elhenawy, M., H. Rakha, and H. Chen (2016). An automatic traffic congestion identification algorithm based on mixture of linear regressions. In Smart cities, green technologies, and intelligent transport systems, pp. 242–256. Springer.

- Faria and Soromenho (2010) Faria, S. and G. Soromenho (2010). Fitting mixtures of linear regressions. Journal of Statistical Computation and Simulation 80(2), 201–225.

- Frank and Wolfe (1956) Frank, M. and P. Wolfe (1956). An algorithm for quadratic programming. Naval research logistics quarterly 3(1-2), 95–110.

- Ghosal and Van Der Vaart (2007) Ghosal, S. and A. Van Der Vaart (2007). Posterior convergence rates of dirichlet mixtures at smooth densities. The Annals of Statistics 35(2), 697–723.

- Ghosal and Van Der Vaart (2001) Ghosal, S. and A. W. Van Der Vaart (2001). Entropies and rates of convergence for maximum likelihood and bayes estimation for mixtures of normal densities. The Annals of Statistics 29(5), 1233–1263.

- Groeneboom and Wellner (1992) Groeneboom, P. and J. A. Wellner (1992). Information bounds and nonparametric maximum likelihood estimation, Volume 19. Springer Science & Business Media.

- Gu and Koenker (2020) Gu, J. and R. Koenker (2020). Nonparametric maximum likelihood methods for binary response models with random coefficients. Journal of the American Statistical Association, 1–20.

- Hennig and Imports (2015) Hennig, C. and M. Imports (2015). Package ‘fpc’. Flexible Procedures for Clustering.

- Hildreth and Houck (1968) Hildreth, C. and J. P. Houck (1968). Some estimators for a linear model with random coefficients. Journal of the American Statistical Association 63(322), 584–595.

- Huang and Yao (2012) Huang, M. and W. Yao (2012). Mixture of regression models with varying mixing proportions: a semiparametric approach. Journal of the American Statistical Association 107(498), 711–724.

- Hurn et al. (2003) Hurn, M., A. Justel, and C. P. Robert (2003). Estimating mixtures of regressions. Journal of computational and graphical statistics 12(1), 55–79.

- Jagabathula et al. (2020) Jagabathula, S., L. Subramanian, and A. Venkataraman (2020). A conditional gradient approach for nonparametric estimation of mixing distributions. Management Science 66(8), 3635–3656.

- Jaggi (2013) Jaggi, M. (2013). Revisiting frank-wolfe: Projection-free sparse convex optimization. In Proceedings of The 30th International Conference on Machine Learning, Volume 28, pp. 427–435.

- Jiang and Zhang (2009) Jiang, W. and C.-H. Zhang (2009). General maximum likelihood empirical bayes estimation of normal means. The Annals of Statistics 37(4), 1647–1684.

- Jordan and Jacobs (1994) Jordan, M. I. and R. A. Jacobs (1994). Hierarchical mixtures of experts and the EM algorithm. Neural computation 6(2), 181–214.

- Kiefer and Wolfowitz (1956) Kiefer, J. and J. Wolfowitz (1956). Consistency of the maximum likelihood estimator in the presence of infinitely many incidental parameters. The Annals of Mathematical Statistics, 887–906.

- Koenker and Mizera (2014) Koenker, R. and I. Mizera (2014). Convex optimization, shape constraints, compound decisions, and empirical bayes rules. Journal of the American Statistical Association 109(506), 674–685.

- Laird (1978) Laird, N. (1978). Nonparametric maximum likelihood estimation of a mixing distribution. Journal of the American Statistical Association 73(364), 805–811.

- Leisch (2004) Leisch, F. (2004). Flexmix: A general framework for finite mixture models and latent class regression in R. Journal of Statistical Software 11.

- Liem et al. (2015) Liem, R. P., C. A. Mader, and J. R. Martins (2015). Surrogate models and mixtures of experts in aerodynamic performance prediction for aircraft mission analysis. Aerospace Science and Technology 43, 126–151.

- Lindsay (1983) Lindsay, B. G. (1983). The geometry of mixture likelihoods: a general theory. The Annals of Statistics, 86–94.

- Lindsay (1995) Lindsay, B. G. (1995). Mixture models: theory, geometry and applications. In NSF-CBMS regional conference series in probability and statistics, pp. i–163. JSTOR.

- Longford (1994) Longford, N. T. (1994). Random coefficient models. In International Encyclopedia of Statistical Science.

- Martin-Magniette et al. (2008) Martin-Magniette, M.-L., T. Mary-Huard, C. Bérard, and S. Robin (2008). Chipmix: mixture model of regressions for two-color chip–chip analysis. Bioinformatics 24(16), i181–i186.

- Parthasarathy (2005) Parthasarathy, K. R. (2005). Probability measures on metric spaces, Volume 352. American Mathematical Soc.

- Polyanskiy and Wu (2020) Polyanskiy, Y. and Y. Wu (2020). Self-regularizing property of nonparametric maximum likelihood estimator in mixture models. arXiv preprint arXiv:2008.08244.

- Powell (1964) Powell, M. J. (1964). An efficient method for finding the minimum of a function of several variables without calculating derivatives. The computer journal 7(2), 155–162.

- Quandt (1958) Quandt, R. E. (1958). The estimation of the parameters of a linear regression system obeying two separate regimes. Journal of the american statistical association 53(284), 873–880.

- Robbins (1950) Robbins, H. (1950). A generalization of the method of maximum likelihood-estimating a mixing distribution. In Annals of Mathematical Statistics, Volume 21, pp. 314–315. IMS BUSINESS OFFICE-SUITE 7, 3401 INVESTMENT BLVD, HAYWARD, CA 94545: INST MATHEMATICAL STATISTICS.

- Roser (2021) Roser, M. (Accessed in March 2021). Economic growth. Published online at OurWorldInData.org. Data Source: Global Carbon Project; BP; Maddison; UNWPP.

- Saha and Guntuboyina (2020) Saha, S. and A. Guntuboyina (2020). On the nonparametric maximum likelihood estimator for gaussian location mixture densities with application to gaussian denoising. Annals of Statistics 48(2), 738–762.

- Sarstedt (2008) Sarstedt, M. (2008). Market segmentation with mixture regression models: Understanding measures that guide model selection. Journal of Targeting, Measurement and Analysis for Marketing 16(3), 228–246.

- Schlattmann (2009) Schlattmann, P. (2009). Medical applications of finite mixture models. Springer.

- Silvey (1980) Silvey, S. (1980). Optimal design: an introduction to the theory for parameter estimation, Volume 1. Springer Science & Business Media.

- Turner (2000) Turner, T. R. (2000). Estimating the propagation rate of a viral infection of potato plants via mixtures of regressions. Journal of the Royal Statistical Society: Series C (Applied Statistics) 49(3), 371–384.

- van de Geer (2000) van de Geer, S. (2000). Empirical Processes in M-estimation. Cambridge university press.

- Van Der Vaart and Wellner (1996) Van Der Vaart, A. W. and J. A. Wellner (1996). Weak convergence and empirical processes. Springer.

- Viele and Tong (2002) Viele, K. and B. Tong (2002). Modeling with mixtures of linear regressions. Statistics and Computing 12(4), 315–330.

- Wedel and Kamakura (2012) Wedel, M. and W. A. Kamakura (2012). Market segmentation: Conceptual and methodological foundations, Volume 8. Springer Science & Business Media.

- Wu (1978) Wu, C.-F. (1978). Some algorithmic aspects of the theory of optimal designs. The Annals of Statistics, 1286–1301.

- Yao and Song (2015) Yao, W. and W. Song (2015). Mixtures of linear regression with measurement errors. Communications in Statistics-Theory and Methods 44(8), 1602–1614.

- Zhang (2009) Zhang, C.-H. (2009). Generalized maximum likelihood estimation of normal mixture densities. Statistica Sinica, 1297–1318.