Ex-post implementation with interdependent values 111We are thankful to Debasis Mishra for his invaluable guidance and support. We also thank Arunava Sen and Stephen Morris for insightful comments.

Abstract

We characterize ex-post implementable allocation rules for single object auctions under quasi-linear preferences with convex interdependent value functions. We show that requiring ex-post implementability is equivalent to requiring that the allocation rule must satisfy a condition that we call eventual monotonicity (EM), which is a weakening of monotonicity, a familiar condition used to characterize dominant strategy implementation.

Keywords: ex-post implementation, interdependent value auction, eventual monotonicity, optimal auction

JEL Classification: D44

1 Introduction

We study the single object auction model when agents have interdependent values. In our model, each agent has a private signal about her value and her (ex-post) value for the object depends on the private signals of all the agents: . The only assumptions we make on the value function is that it is convex and non-decreasing in the signal . Thus, allows for a rich class of interdependence: the additive model of [3]; the max model of [1]; and the private values model in [8]. We define a new property for allocation rules that we call eventual monotonicity (EM). We show that an allocation rule is ex-post implementable (i.e., there exists a transfer rule such that the allocation rule and the transfer rule form an ex-post incentive compatible mechanism) if and only if it satisfies eventual monotonicity.

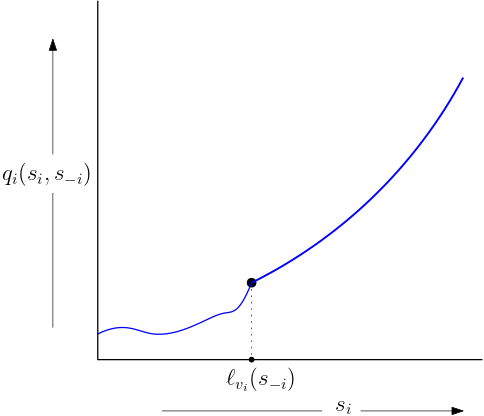

This novel property is a weakening of the monotonicity property that characterizes dominant strategy implementation [8]. Towards understanding this property, let denote the supremum of all signals of agent for which takes the same value as it does when has the lowest possible signal.444We assume that the signal space for each agent is an interval, so this supremum is also over an interval. Eventual monotonicity is then the following requirement: for any and any pair of signals for agent with , the allocation probablity of agent at is no less than the allocation probability at . This requirement captures two conditions. First, the allocation probability of agent must be increasing beyond . Two, while it does not need to be increasing below , it must be the case that the allocation probability for any type above is more than the allocation probability for any type below . See Figure 1 below for an illustration.

Extending Myerson’s monotonicity characterization to interdependent values models may be useful in solving optimal auction problems in these models with ex-post incentive compatibility as the solution concept. The interdependent values model is considered to be a model that reflects many realistic problems where agents have imperfect information about values: [7, 3, 1] contain several motivating examples.555[1] describes a setting where an agent’s signal denotes her private use. If an agent comes to know of various uses of the object, she makes the best use of it. This is captured in their max model, a common value model, given by . Our results cover their model.

Our characterization and a payment equivalence formula provide a handy method of deriving an expression for the revenue of the revenue-maximizing mechanism in terms of maximizing an objective function within the class of eventually monotone allocation rules. The tractability of deriving the exact optimal EPIC mechanism in general will depend on the form of the value functions. We show that for strictly increasing value functions, the usual Myersonian approach works. We are also able to show that the BIC and IIR inclusive posted price mechanism studied in [3], and shown to be optimal in [1], can in fact be achieved in expectation by an EPIC and EPIR mechanism using the characterization that we develop, under the condition that the object must be sold.

Relation to the literature. Much of the literature on interdependent values model focuses on Bayesian incentive compatibility (BIC) and interim individual rationality (IIR). However, BIC has been criticized for its reliance on the specific priors of the agents, and hence raises questions of robustness. We use the stronger and more robust concepts of ex-post incentive compatibility (EPIC) and ex-post individual rationality (EPIR) instead. While many interesting but specific models of interdependent values have been studied, a general characterization of ex-post implementability paralleling that for private values has proved elusive, partly because of the difficulty in identifying the set of binding constraints. [6] shows that the Vickrey auction may not be ex-post implementable without the single-crossing property for the value functions 666The single-crossing property ensures that the agent with the highest signal is also the agent with the highest value, which ensures that efficient auctions produce monotonic, and hence implementable, allocation rules. Our result is orthogonal - we show that under convexity there is an exact characterization of implementable rules.. [5] demonstrates that with multidimensional types and interdependent values, there are no non-trivial (non-constant) ex-post implementable deterministic social choice functions, while [2] shows that this is not the case for private values. We fill this gap in the literature by providing a characterization of ex-post implementability in models of interdependent values.

The paper closest to ours is [9], which provides sufficient conditions under which allocation rules are ex-post implementable. Building on a result from [4], they show that under increasing differences across signals, monotonicity of the allocation rule in own signal is sufficient for ex-post implementation. However they do not provide a characterization.

The rest of the paper proceeds as follows. Section 2 specifies the setting of the problem. Section 3 builds the characterization. Section 4 explores the problem of revenue maximization, both in general and in specific models.

2 Model

Let be the set of agents. There is one good to be allocated. The agents have quasi-linear interdependent preferences for the good. Each agent receives signals from . Let be the valuation function of each agent . denotes the valuation of agent at signal profile . We assume that is convex, continuous and non-decreasing in on , for all . For every and for every , define

Since is convex, continuous, and non-decreasing, is the supremum of the interval where is constant. For instance, in the max value function studied in [1], and .

We invoke the revelation principle to focus only on direct mechanisms. Thus a mechanism in this setting is the tuple where is the allocation rule for agent and is the payment rule for agent .

Definition 1.

An allocation rule is ex-post implementable if there exists a payment rule such that the following holds :

where is the net payoff function for agent . In this case, we say that the mechanism is ex-post incentive compatible (EPIC).

3 Eventual monotonicity and ex-post implementation

Our main result characterizes ex-post implementable allocation rules. The approach we take to derive this result is fairly standard - we derive a necessary condition and then show that it also turns out to be sufficient. Here the appropriate necessary condition is a suitable modification of monotonicity.

Definition 2.

The allocation rule is eventually monotone if , and for every with , we have

Figure 1 illustrates what an EM rule might look like.

Now we are ready to state and prove our main result.

Theorem 1.

An allocation rule is ex-post implementable if and only if it is eventually monotone.

It is direct to note that EPIC is equivalent to dominant strategy incentive compatibility (DSIC) under private values, and that eventual monotonicity is just monotonocity. Hence, we obtain the standard characterization of dominant-strategy implementable rules as a corollary of the above theorem.

4 Optimal mechanisms

In this section, we assume that the signals of the agents are independent and identically distributed, each drawn from some distribution with full support on . We will first derive a condition for revenue maximization, and then explore its implications for some value functions.

Building on Theorem 1, we get the following characterization of EPIC mechanisms.

Proposition 1.

A mechanism is ex-post incentive compatible if and only if is eventually monotone and is given by 777Note that need not be differentiable with respect to everywhere, but convexity ensures that it always has a sub-gradient, which is equal to its derivative whenever the latter exists (which is almost everywhere). We write to denote the derivative of with respect to the first argument at whenever it is differentiable. Else, it is some selection from the subgradient of at .:

The following generalization of the private values version of virtual value is well-known in the literature.

Definition 3.

The virtual value of an agent at a signal profile is given by

Also, we consider rules that ensure that the agents continue to want to participate ex-post.

Definition 4.

A mechanism is ex-post individually rational (EPIR) if the following holds :

We say that a mechanism is optimal if it is EPIC and EPIR and generates more expected revenue than any other EPIC and EPIR mechanism. We then have the following formula for the revenue in an optimal mechanism.

Lemma 1.

The optimal mechanism maximizes

within the class of eventually monotone allocation rules.

4.1 Strictly increasing value functions

When the value functions are strictly increasing in each agent’s own signal, then it is direct to observe that EM reduces to monotonicity. In this case the optimization problem identified in Lemma 1 can be solved by the standard ironing technique of [8]. We state this observation in the following proposition:

Proposition 2.

Suppose each agent’s value function is strictly increasing in her own signal. Then, the optimal mechanism allocates the object to the agent with the highest ironed virtual value, and charges the payments that ex-post implements this allocation rule.

Note also that the case of private values is covered by this result.

4.2 Additive signals

Using the framework developed above, we derive a result for the additive signals model, which is closely related to the one studied in [3]. In this model, the value functions are given by with for all . An example of such a model is the simple additive value case - where each agent’s value for the object is the simple sum of the signals of each agent. Denote by the adjusted hazard rate of agent .

Proposition 3.

Suppose the distribution of the signals satisfies the monotone hazard rate property. Then a mechanism is optimal if and only if at every signal profile it allocates the object with probability to the agent with the lowest adjusted hazard rate if that agent’s virtual value is non-negative and does not allocate the object otherwise.

An interesting corollary of this theorem is the following: when the weights are the same for every agent (i.e. the simple additive values case) and the distribution of signals has a monotone hazard rate, the mechanism allocates the object to the agent with the highest signal. This is because the agent with the lowest adjusted hazard rate at any profile must also have the highest signal, by the monotone hazard rate assumption.

4.3 Max function

[1] derive the optimal Bayesian incentive compatible (BIC) and interim individually rational (IIR) mechanism for the maximum value function, . We use our framework to identify the optimal mechanism for this form of interdependence, under the assumption that the object must be sold.

Proposition 4.

When it is mandatory to sell the object, mechanisms that allocate the object with probability to agent at all signal profiles, for some such that , are optimal.

Each of these optimal mechanisms guarantees the same revenue in expectation as the BIC and IIR equal allocation rule of [1], which allocates with probability to each agent at every profile. Since their optimal mechanism is not ex-post IR, our result identifies an ex-post IR implementation of their mechanism.

References

- [1] Dirk Bergemann, Benjamin Brooks and Stephen Morris “Countering the winner’s curse: Optimal auction design in a common value model” In Theoretical Economics 15.4, 2020, pp. 1399–1434 DOI: https://doi.org/10.3982/TE3797

- [2] Sushil Bikhchandani “Ex post implementation in environments with private goods” In Theoretical Economics 1, 2006, pp. 369–393

- [3] Jeremy Bulow and Paul Klemperer “Prices and the Winner’s Curse” In RAND Journal of Economics 33.1, 2002, pp. 1–21 URL: https://ideas.repec.org/a/rje/randje/v33y2002ispringp1-21.html

- [4] Jacques Crémer and Richard P. McLean “Optimal Selling Strategies under Uncertainty for a Discriminating Monopolist when Demands are Interdependent” In Econometrica 53.2 [Wiley, Econometric Society], 1985, pp. 345–361 URL: http://www.jstor.org/stable/1911240

- [5] Philippe Jehiel, Moritz Meyer-ter-Vehn, Benny Moldovanu and William R. Zame “The Limits of ex post Implementation” In Econometrica 74.3, 2006, pp. 585–610 DOI: https://doi.org/10.1111/j.1468-0262.2006.00675.x

- [6] Eric Maskin “Auctions and Privatization” In Privatization J.C.B. Mohr Publisher, 1992, pp. 115–136 J.C.B. Mohr Publisher

- [7] Paul R. Milgrom and Robert J. Weber “A Theory of Auctions and Competitive Bidding” In Econometrica 50.5 [Wiley, Econometric Society], 1982, pp. 1089–1122 URL: http://www.jstor.org/stable/1911865

- [8] Roger Myerson “Optimal Auction Design” In Mathematics of Operations Research 6.1, 1981, pp. 58–73 URL: https://EconPapers.repec.org/RePEc:inm:ormoor:v:6:y:1981:i:1:p:58-73

- [9] Levent Ülkü “Implementation in an interdependent value framework” In Mathematical Social Sciences 68, 2014, pp. 64–70 DOI: https://doi.org/10.1016/j.mathsocsci.2014.01.002

Appendix A Proofs

Proof of Theorem 1.

Suppose is ex-post implementable. Then, there exists a payment rule such that is EPIC. Let . EPIC implies

and

Adding these two together,

| (1) |

Let . Then . Hence by 1, we must have

Thus, must be eventually monotone.

For the converse, suppose is eventually monotone. Let be given by

Fix , and consider . We need to prove that the following quantity is non-negative.

Let us proceed by taking cases.

Case:

Case:

Case:

Case:

Case:

Case:

Thus we have ex post incentive compatibility of , and hence is ex-post implementable. ∎

Proof of Proposition 1.

Let be an EPIC mechanism. We already know from Theorem 1 that must be eventually monotone. So all we need to show is that the payments take the form specified in the hypothesis.

Let denote the utility of agent from . Since the value functions are convex, it is reasonable to expect that the net payoff functions are convex. This is indeed the case.

Claim 1.

For each , is convex in .

Proof of Claim 1.

Consider any . Let , where . By convexity of . By incentive compatibility,

| (2) |

| (3) |

where the last inequality follows from convexity of . ∎

The next step of the proof uses the convexity of to establish the relationship between and .

Claim 2.

Given ex-post incentive compatibility, almost everywhere.

Proof of Claim 2.

By convexity of and , they are not differentiable at most in a pair of measure subsets. Since their union will continue to be measure , we must have that and are together differentiable almost everywhere.

Let be an interior point where and are both differentiable and let . By incentive compatibility,

| (4) |

| (5) |

Rewriting 5, we get,

| (6) |

∎

We use the fundamental theorem of calculus to derive what must look like.

Claim 3.

The payment rule must be of the form

Proof of Claim 3.

From Claim 2 and using the fundamental theorem of calculus888Specifically, the fundamental theorem of Lebesgue integral calculus for absolutely continuous functions.,

which gives us the required equality. ∎

For the converse, suppose is eventually monotone and the payments formula take the form specified. The proof of the converse of Theorem 1 shows that is EPIC, and hence we are done.

∎

Proof of Lemma 1.

As is standard in the case of private values, in this setting as well IR reduces to ensuring IR of the lowest type.

Claim 4.

Given ex-post incentive compatibility, a mechanism is individually rational if and only if

Changing the order of integration, we can write,

Thus, expected revenue is

The second term in the above expression is non-positive under EPIR. Thus, in order to maximize revenue we must set . As a result, the optimal mechanism maximizes the first term, which reduces to:

∎

Proof of Proposition 3.

If we were to pointwise maximize the revenue, we would not allocate the object at signal profiles where the virtual value of each agent is negative. At other profiles, note that the virtual value of agent is . Thus,

The first term above is unchanged given a fixed total probability of allocation. Again pointwise maximizing, we can allocate with probability 1 to the agent with the lowest adjusted hazard rate and maximize the entire term at a given signal profile.

Since the hazard rate is monotone non-increasing, once an agent starts winning by having the lowest adjusted hazard rate, she continues to win at higher signals. Thus this pointwise-maximizing allocation rule also turns out to be non-decreasing, and hence the maximizer within the class of non-decreasing allocation rules. ∎

Proof of Proposition 4.

We invoke the optimality of the inclusive posted price under must-sell shown by Bergemann Brooks Morris (2019). For this we first show that ex post incentive compatibility is sufficient for interim incentive compatibility.

EPIC means , , ,

Now, we show that ex post individual rationality is sufficient for interim individual rationality.

EPIR means , , ,

Since the allocation rule , is monotone and hence eventually monotone, it is ex-post implementable. The corresponding payments are,

For agent such that

and for all

Thus the tuple is both EPIC and EPIR, and hence IIR and IIC.

We now show that in expectation, this payment scheme gives the same revenue as the inclusive posted price mechansim in Bergemann Brooks Morris (2019).

The expression for expected revenue is

Changing the order of summation,

It is direct to show that any mechanism in the class of mechanisms identified in this theorem has the same revenue as the equal sharing mechanism, and hence we are done.

∎