WEAK SIGNAL IDENTIFICATION AND INFERENCE

IN PENALIZED LIKELIHOOD MODELS

FOR CATEGORICAL RESPONSES

Yuexia Zhang, Peibei Shi, Zhongyi Zhu, Linbo Wang and Annie Qu

The University of Texas at San Antonio, Meta, Fudan University

University of Toronto and University of California, Irvine

Abstract:

Penalized likelihood models are widely used to simultaneously select variables and estimate model parameters. However, the existence of weak signals can lead to inaccurate variable selection, biased parameter estimation, and invalid inference. Thus, identifying weak signals accurately and making valid inferences are crucial in penalized likelihood models. We develop a unified approach to identify weak signals and make inferences in penalized likelihood models, including the special case when the responses are categorical. To identify weak signals, we use the estimated selection probability of each covariate as a measure of the signal strength and formulate a signal identification criterion. To construct confidence intervals, we propose a two-step inference procedure. Extensive simulation studies show that the proposed procedure outperforms several existing methods. We illustrate the proposed method by applying it to the Practice Fusion diabetes data set.Key words and phrases: adaptive lasso, de-biased method, model selection, post-selection inference

1. Introduction

In the big data era, massive data are collected with large-dimensional covariates. However, only some of the covariates might be important. To select the important variables and estimate their effects on the response variable, various penalized likelihood models have been proposed, such as the penalized least squares regression model (Tibshirani,, 1996; Zou and Hastie,, 2005; Tibshirani et al.,, 2005; Yuan and Lin,, 2006; Zou,, 2006; Zhang,, 2010), penalized logistic regression model (Park and Hastie,, 2008; Zhu and Hastie,, 2004; Wu et al.,, 2009), and penalized Poisson regression model (Lambert and Eilers,, 2005; Jia et al.,, 2019).

To achieve model selection consistency or the variable screening property for a high-dimensional problem, a common condition is the “beta-min” condition, which requires the nonzero regression coefficients to be sufficiently large (Zhao and Yu,, 2006; Huang and Xie,, 2007; Van de Geer et al.,, 2011; Tibshirani,, 2011; Zhang and Jia,, 2022). Therefore, classical methods for variable selection often focus on strong signals that satisfy such a condition. However, if the “beta-min” condition is violated, the important variables and unimportant variables may be inseparable, and the true important variables might not be selected, even if the sample size goes to infinity (Zhang,, 2013). In finite samples, the estimators shrink the true regression coefficients, owing to the penalty function. When the signal strength is weak, its coefficient is more likely to shrink to zero (Shi and Qu,, 2017; Liu et al.,, 2020). Inaccurate variable selection and biased parameter estimation could lead to a poor post-selection inference, for example, the estimation of the confidence intervals could be inaccurate. Thus, both strong and weak signals need to be considered. Identification and inference for weak signals can also help discover potentially important variables in practice. For example, in genome-wide association studies (GWAS), overlooked risk factors for a disease may be recovered by incorporating weak signals (Liu et al.,, 2020).

For linear regression models, studies have been done on weak signals. In more extreme cases, Jin et al., (2014) assumed all signals were individually weak and proposed graphlet screening for variable selection. Zhang, (2017) proposed the perturbed lasso, where signals were strengthened by adding random perturbations to the design matrix. However, these methods focused only on variable selection consistency, and did not aim to identify weak signals or provide statistical inference. For weak signal identification and inference, Shi and Qu, (2017) proposed a weak signal identification procedure in finite samples, and introduced a two-step inference method for constructing confidence intervals after signal identification. However, their derivation relies on a crucial assumption that the design matrix is orthogonal, which may not hold in practice. On the other hand, Li et al., (2019) took advantage of the correlations between covariates, detecting weak signals through the partial correlations between strong and weak signals. However, they did not study weak signal inference. Recently, Liu et al., (2020) proposed a method that combines the bootstrap lasso and a partial ridge regression for constructing confidence intervals when there are weak signals in the covariates. However, as stated in their paper, the confidence intervals of the coefficients, with magnitudes of order , may be invalid.

To the best of our knowledge, there has been little work on weak signals in likelihood-based models for categorical responses. One exception is Reangsephet et al., (2020), who proposed variable selection methods for logistic regression models with weak signals. However, they did not conduct weak signal identification or inference.

We address these gaps by developing a new unified approach to weak signal identification and inference in penalized likelihood models, including the special case when the responses are categorical. Specifically, the estimated probability of each covariate being selected by the one-step adaptive lasso estimator is used to measure the signal strength. After signal identification, a two-step inference procedure is proposed to construct the confidence intervals for the regression coefficients. The proposed method has several advantages. First, we extend the method of Shi and Qu, (2017) from linear regression models to likelihood-based models, including generalized linear models. However, our extension is not trivial. For example, in Shi and Qu, (2017), the selection probability has an explicit expression. For the proposed likelihood-based method, such an explicit expression does not exist for categorical responses. Thus, we propose a new method to estimate the selection probability. Second, in Shi and Qu, (2017), the selection probability for the covariate is an increasing function of , where is the corresponding coefficient of . Under our current general framework, such a conclusion is not necessarily true. Thus, our signal identification criterion is based directly on the estimated selection probability, in contrast to Shi and Qu, (2017). We also discuss how each signal’s selection probability is influenced by other covariates, owing to nonlinear modeling or collinearity among the covariates; in Shi and Qu, (2017), the selection probability of one covariate is independent of those of other covariates. Third, Shi and Qu, (2017) assumed that the design matrix in a linear regression model is orthogonal, whereas the proposed method relaxes this constraint. Fourth, the proposed inference method differs from that of Shi and Qu, (2017). Specifically, we construct confidence intervals for the noise variables as well, whereas their method does not. Simulation results show that our proposed two-step inference method outperforms the two-step inference method based on Shi and Qu, (2017). In particular, the proposed confidence intervals achieve accurate coverage probabilities for all signal strength levels.

The remainder of this paper is organized as follows. In Section 2, we introduce the one-step adaptive lasso estimator and derive the variable selection condition. In Section 3, we propose the weak signal identification criterion. In Section 4, we develop a two-step inference procedure for constructing confidence intervals. In Section 5, we conduct simulation studies to assess the finite-sample performance of the proposed method. In Section 6, we apply the proposed method to an analysis of diabetes data. In Section 7, we provide brief concluding remarks. We provide the technical proofs, implementation details of several methods, and some additional results in the Supplementary Material.

2 One-Step Adaptive Lasso Estimator and Variable Selection Condition

In this section, we introduce the one-step penalized likelihood estimator and derive the condition for variable selection, which we use later for weak signal identification and inference.

Let be independent and identically distributed (i.i.d.) random vectors, where is a vector of predictors and is a response variable. Assume that depends on through a linear combination , and the conditional log-likelihood of given is , where , is an unknown true location parameter, and is an unknown vector of covariate effects. Note that for a likelihood-based model, it is not always possible to eliminate the location parameter by centering the covariates and the response variable. For simplicity, assume and is fixed. Let denote the log-likelihood. Assume is the maximum likelihood estimator of ; then, . In matrix notation, we set , with and . Furthermore, denote and , where is an vector with all elements equal to one. Throughout this paper, we assume that and , for all and , which can be realized by standardizing the covariate matrix , in practice.

Assume that some components of are zero. In order to estimate the model parameters and select important variables simultaneously, we consider the penalized likelihood function , where is a penalty function controlled by the tuning parameter . One popular penalty function is derived from the adaptive lasso estimator (Zou,, 2006), where . Maximizing the penalized likelihood function is equivalent to minimizing

| (2.1) |

with respect to . According to Wang and Leng, (2007) and Zou and Li, (2008), if the log-likelihood function has first and second derivatives, then it can be approximated by a Taylor expansion. Furthermore, the objective function (2.1) can be approximated by

| (2.2) |

where is the second derivative of function . The one-step penalized likelihood estimator is .

Denote and . Let be an diagonal matrix with the th element , for . Then, . Furthermore, we assume is a continuous function of . For simplicity, denote , , , and as , , , and , respectively. By solving the equation , we obtain that

| (2.3) |

Replacing by (2.3) in (2.2), we obtain the following objective function :

| (2.4) | ||||

where and . Denote and , correspondingly.

We focus mainly on weak signal identification using the one-step adaptive lasso estimator. However, our method can be extended to other penalized likelihood estimators. Following the idea of Zou and Li, (2008), the algorithm for computing the one-step adaptive lasso estimator is as follows:

-

Step 1.

Create the working data by and , where .

-

Step 2.

Apply the coordinate descent algorithm to solve

(2.5) where , is the th element of and is the th element of .

-

Step 3.

Obtain the value of using for .

-

Step 4.

Obtain the value of as .

From the above algorithm, if , then the covariate will be selected. According to (2.5), by using the coordinate descent algorithm, we obtain that

where . Then, the condition for () is

| (2.6) |

For each and , let be the th element of . Then the variable selection condition (2.6) is equivalent to

| (2.7) |

Similarly to the proof in Zou and Li, (2008), we obtain that if the tuning parameter satisfies the conditions of and , then the one-step adaptive lasso estimator enjoys model selection consistency, and the nonzero one-step adaptive lasso estimators have the property of asymptotic normality.

3 Weak Signal Definition and Identification

3.1 Weak signal definition

Suppose a model contains both strong and weak signals. Without loss of generality, assume the covariate matrix consists of three components, that is, , where , , and represent the subsets of strong signals, weak signals, and noise variables, respectively. Following Shi and Qu, (2017), we use the selection probability of each covariate to measure the signal strength. Specifically, for any penalized model selection estimator , we define as the probability of selecting the covariate , that is, , . For the one-step adaptive lasso estimator , based on the variable selection condition (2.7), does not have an explicit form. However, in the Supplementary Material S1, we show that can be approximated by , where

| (3.1) |

Intuitively, in the derivation of the selection probability, we can omit the terms of (S2) and (S3) in the Supplementary Material S1, and simplify the calculation using asymptotic theory. Then we can relax the orthogonality assumption required in Shi and Qu, (2017). We require the following mild assumption to ensure (3.1) is valid.

Assumption 1.

For each and , , , , and is positive definite.

The condition implies that the conditional log-likelihood function of given , , is a concave function of . This is a necessary condition for the uniqueness of the maximum likelihood estimator . In addition, according to the Cauchy–Schwarz inequality, this also ensures that . The conditions of and guarantee that all expectations of random variables in (3.1) are bounded for finite . The positive-definite condition of is a necessary condition for the asymptotic normality of the maximum likelihood estimator , and ensures .

For a deeper understanding of , we first study the asymptotic properties of . When ,

Under Assumption 1, and are both positive and bounded. If , then .

These asymptotic properties of are consistent with the conclusion that the one-step adaptive lasso estimator enjoys model selection consistency if satisfies the conditions of and .

In the following, we study the finite-sample properties of . To illustrate, we first consider three special cases, where the likelihood-based model is taken as a linear regression model, a logistic regression model, and a Poisson regression model, respectively.

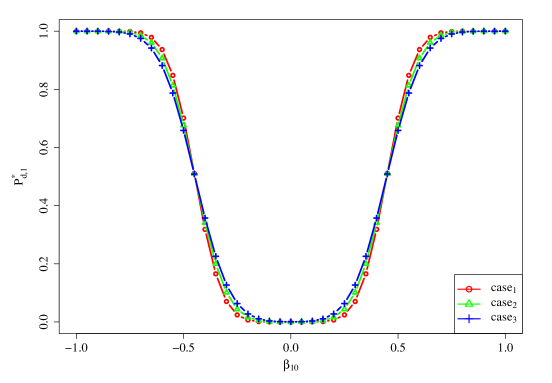

Case One: Linear regression model

We first illustrate the simplest case under the linear regression model setting. Let , where ; then, . If we assume for any , , then

Note that if the tuning parameter is replaced by , then has the same form as that in Shi and Qu, (2017), where the covariate matrix is assumed to be orthogonal. In this case, does not depend on , where stands for the components in other than . In addition, given any values in except , is a symmetric function of and increases with . Thus, both and can be used to measure the signal strength of , as shown in Shi and Qu, (2017).

However, if ; for some , , then

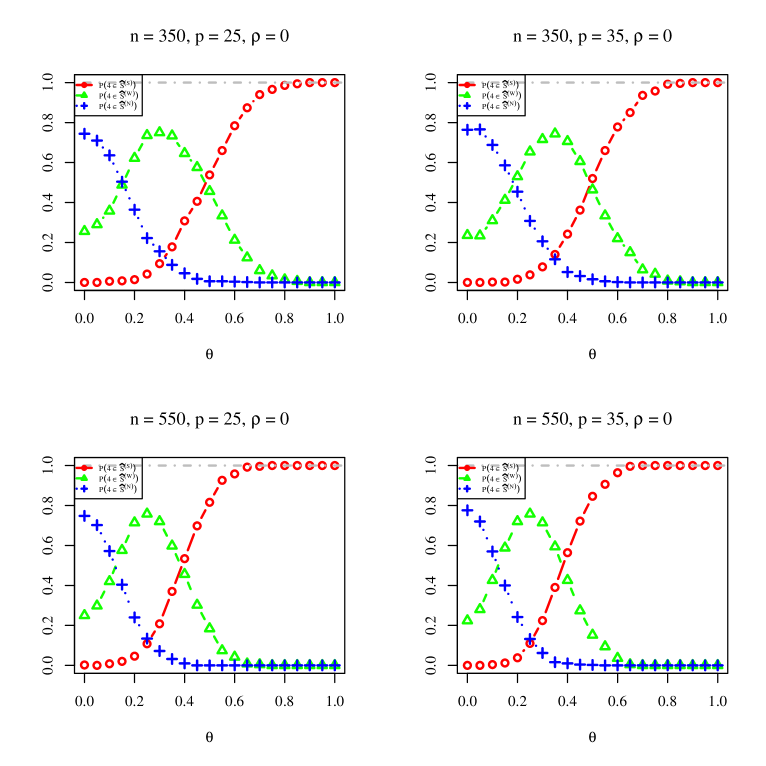

Thus, also depends on the correlations between covariates. Given any values in except , is still a symmetric function of and an increasing function of . However, under different correlation structures of , the shape of can vary with the value of . Therefore, both the value of and the correlation structure of influence the signal strength of , as illustrated in Figure 1.

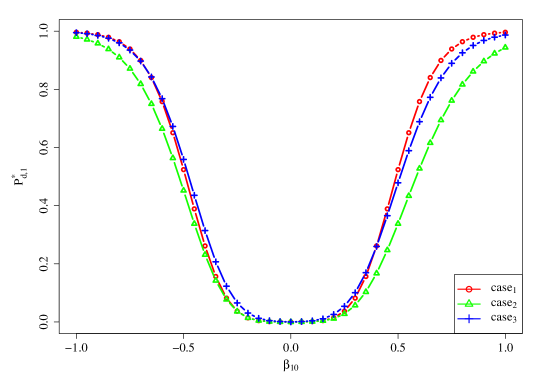

Case Two: Logistic regression model

Under the logistic regression model setting,

We obtain that in (3.1), and . Thus, not only depends on , but also depends on , the coefficients of the other covariates. This is a fundamental difference between logistic regression models and linear regression models in terms of selection probability. In contrast to linear regression models, influences through the matrix , rather than through the correlation matrix of , in logistic regression models. In addition, in the Supplementary Material S2.1, we show that is not necessarily a symmetric function of , given other values in . Thus, cannot be used to measure the signal strength of instead of , which differs from Shi and Qu, (2017).

In addition, for the logistic regression model, the range of is bounded so that can satisfy the condition , where and are some positive constants. We show that, given any values in except , is an increasing function of if , and is a decreasing function of if , where and are some bounded positive constants depending on and . Proofs of the above findings are provided in the Supplementary Material S2.2. We also illustrate these properties in Figure 2. Note that in this case, the response variable has two categories. However, it can be easily extended to the case where there are more than two categories.

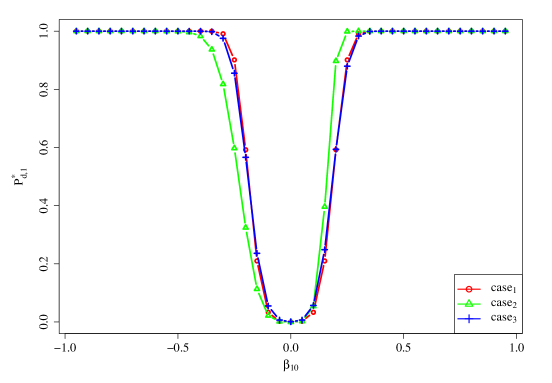

Case Three: Poisson regression model

Under the Poisson regression model setting,

where . Then, in (3.1), and . We obtain similar conclusions to those for logistic regression models, except that is influenced by through the matrix . Note that under Assumption 1, the range of is bounded. Given any other values in except , is an increasing function of if , and is a decreasing function of if , where and are some bounded positive constants. The proof for this finding is provided in the Supplementary Material S2.2. Figure 3 illustrates .

The finite-sample properties of under other likelihood-based models can be analyzed similarly. In general, is a comprehensive indicator. It shows how the selection probability of is influenced by , , , and in finite samples. Given other values in except , is not necessarily a symmetric function of or an increasing function of .

Based on the above analysis, we propose using to measure the signal strength levels directly, rather than using . Intuitively, if is close to one, then the variable is defined to be a strong signal; if is close to zero, then the variable is defined to be a noise variable; if lies between the strong and noise levels, then the variable is defined to be a weak signal. Specifically, we introduce two threshold values, and . Then the three levels of signal strength can be defined as

| (3.2) |

where , , and . Obviously, it is easier to select a stronger signal using the variable selection process than it is to select a weaker signal.

3.2 Weak signal identification

In this section, we show how to identify weak signals. Based on the analysis in Section 3.1, the approximated selection probability depends on the true parameter and the distribution of , but they are always unknown in practice. In the following, we estimate by plugging in the maximum likelihood estimator and the empirical mean of the random variables in (3.1). That is,

| (3.3) | ||||

| (3.4) |

In practice, we identify the signal strength level of based on , and introduce two threshold values and . We denote the identified subsets of strong signals, weak signals, and noise variables as , , and , respectively:

| (3.5) |

The selections of and are crucial to determining the signal type. The threshold value is selected to ensure that we can identify strong signals when the selection probabilities of signals are high. Assume is a significance level, and we choose to be larger than , so that the identified strong signals are strong. The threshold value is selected to control the false positive rate of selecting variable . Denote the false positive rate as . Then can be defined as

| (3.6) |

Thus, can be estimated based on (3.6). Because the value of is unknown in practice, we estimate it using the one-step adaptive lasso estimator . Furthermore, to make the estimated value of the false positive rate equal to based on the observed data, we take the value of as the quantile of . Because we intend to recover weak signals given finite samples, is chosen to be larger than zero. However, the value of cannot be too large, because there is a trade-off between recovering weak signals and including noise variables. In practice, if we want to recover more weak signals, we can choose a larger ; if we want to make the false positive rate lower, we can choose a smaller . In the simulation studies, we perform a sensitivity analysis for the choice of and .

4 Weak Signal Inference

In this section, we propose a two-step inference procedure for constructing confidence intervals for the regression coefficients. The procedure consists of two parts: if a covariate is identified as a strong signal, then its confidence interval is constructed based on the asymptotic theory for the nonzero one-step adaptive lasso estimator (Zou and Li,, 2008); if a covariate is identified as a weak signal or a noise variable, then we provide a confidence interval based on the following inference theory for the maximum likelihood estimator.

Similarly to the theory in Zou and Li, (2008), we can obtain the asymptotic distribution of the one-step adaptive lasso estimator. Without loss of generality, assume , where is the number of nonzero elements in . Define , then . Although the one-step adaptive lasso estimator is biased, owing to the shrinkage effect in finite samples, we can construct a de-biased confidence interval for the true coefficient based on the estimated bias and covariance matrix for , as shown in Theorem 1. The proof of Theorem 1 is given in the Supplementary Material S3.

Theorem 1.

Denote and as and , respectively. The estimators of the bias and the covariance matrix of are given by

and

respectively, where , is the sub-matrix of corresponding to , and is the sub-matrix of corresponding to .

Based on Theorem 1, if the covariate is identified as a strong signal, then the confidence interval for can be constructed as

| (4.1) |

where is the corresponding component of and is the positive square root of the corresponding diagonal component of .

If the covariate is identified as a weak signal or a noise variable, then the confidence interval for can be constructed as

| (4.2) |

where is the positive square root of the corresponding diagonal component of .

Remark 1.

Note that Shi and Qu, (2017) did not construct confidence intervals for the noise variables, whereas we do. As shown in Figure 6 in the simulation studies, this improves the coverage probabilities for the noise variables and weak signals. Using the two-step inference method based on Shi and Qu, (2017), the coverage probabilities for the noise variables tend to be lower than , and the coverage probabilities for weak signals tend to be higher than . This is because one will construct confidence intervals for the noise variables only when the noise variables are misidentified as weak signals or strong signals, in which case the estimated values of the coefficients tend to be far from the true values, leading to lower coverage probabilities; one will not construct confidence intervals for the weak signals when the weak signals are misidentified as noise variables, making the coverage probabilities of the confidence intervals higher. To solve these problems, we propose constructing confidence intervals for the identified noise variables as well. As a result, the coverage probabilities of the confidence intervals become closer to .

5 Simulation Studies

In this section, we conduct simulation studies to evaluate the finite-sample performance of the proposed signal identification criterion and two-step inference procedure. Consider the following logistic regression model:

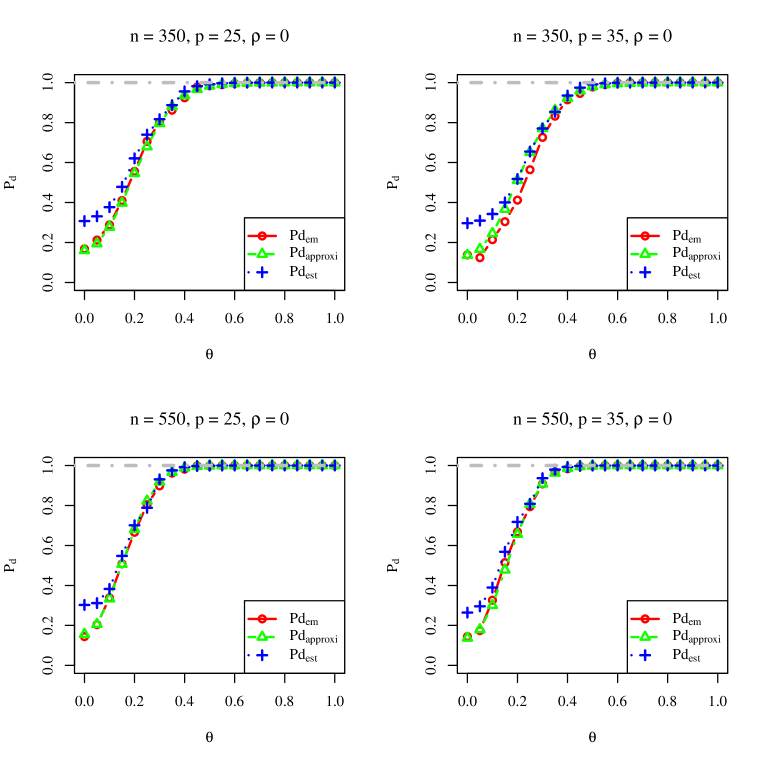

We generate the covariate vector from a multivariate normal distribution with mean zero and covariance matrix , where is a correlation matrix with the AR(1) correlation structure and . All the generated covariates are standardized by subtracting their sample means and dividing by their sample standard deviations. For each setting, we choose or , or , , , or , and . The regression coefficient vector is set to , which consists of two large coefficients , one moderate size coefficient , one varying coefficient , and zero coefficients. The coefficient ranges from zero to one, with a step size of . In each simulation setting, we repeat the simulations times. The implementation details of the one-step adaptive lasso estimators are given in the Supplementary Material S4.

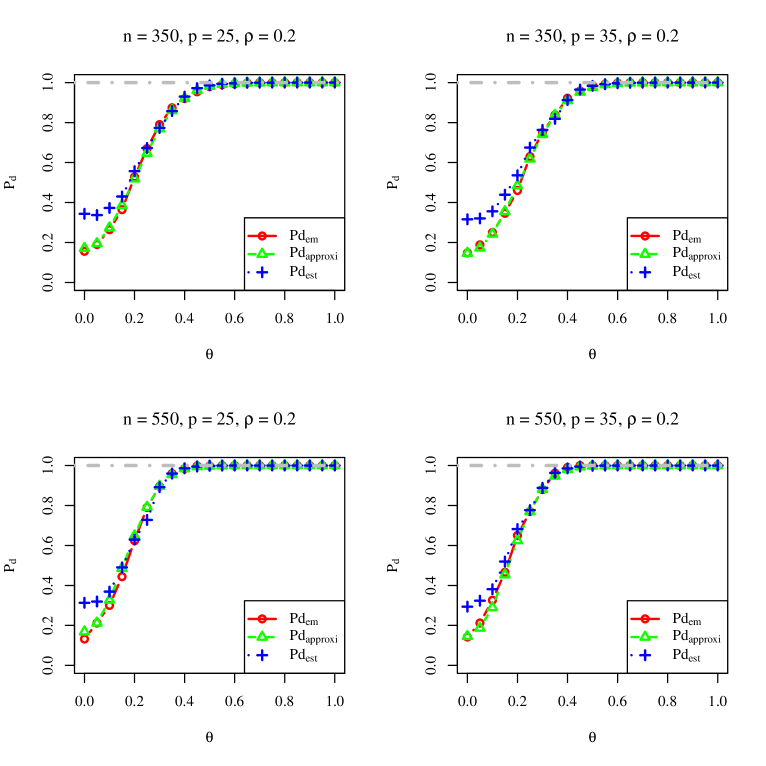

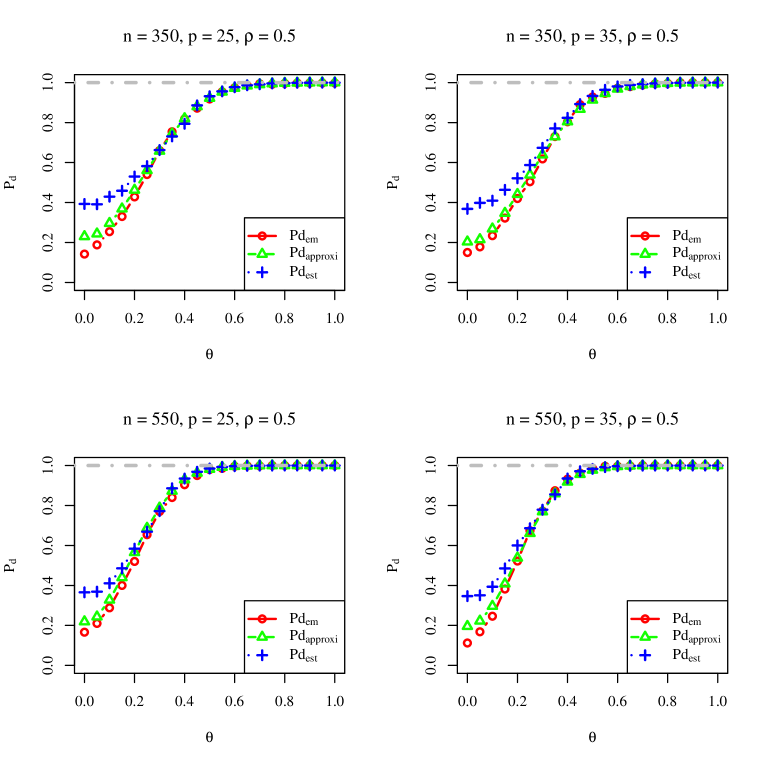

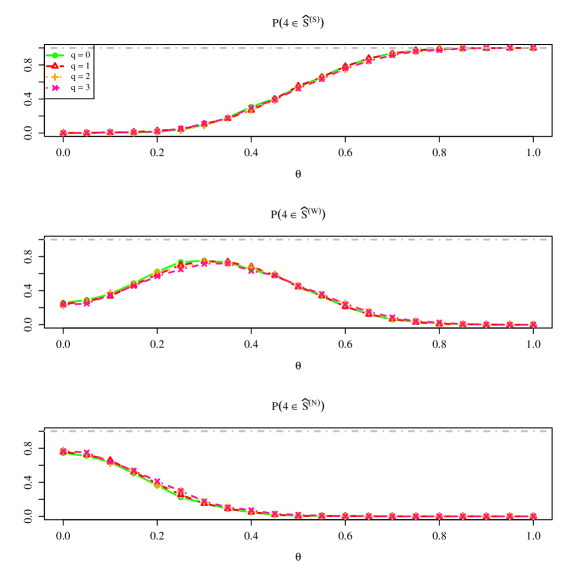

Figure 4 displays the results for different types of selection probability for when . In Figure 4, the approximated selection probability based on (3.1) is close to the empirical selection probability, indicating a small approximation error from the approximated selection probability. In addition, both the empirical selection probability and the approximated selection probability increase with , implying that a larger value of leads to a stronger signal strength. This observation supports the result in Section 3.1. Although the median of the estimated selection probabilities is not too close to the empirical selection probability when is small, the estimated selection probability still increases with the signal strength. We can still use the estimated selection probability to identify the signal strength level. The simulation results for the correlated covariates are provided in Figures S1 and S2 of the Supplementary Material S5, and the approximated selection probability is similar to the empirical selection probability. In addition, the empirical selection probability, approximated selection probability, and estimated selection probability, in general, increase with the value of . Thus, we can also identify the signal strength level based on the value of .

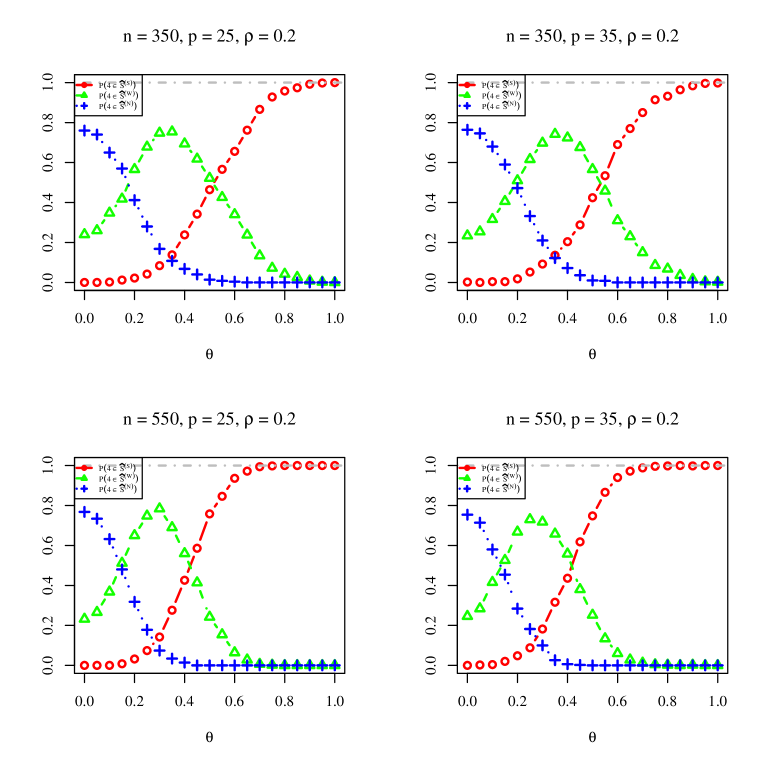

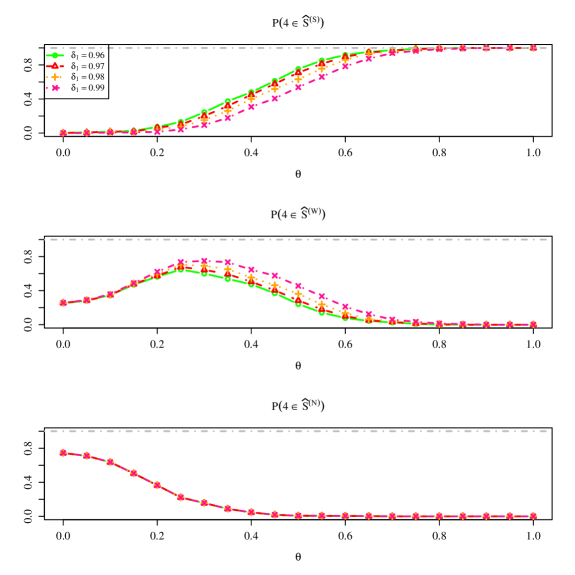

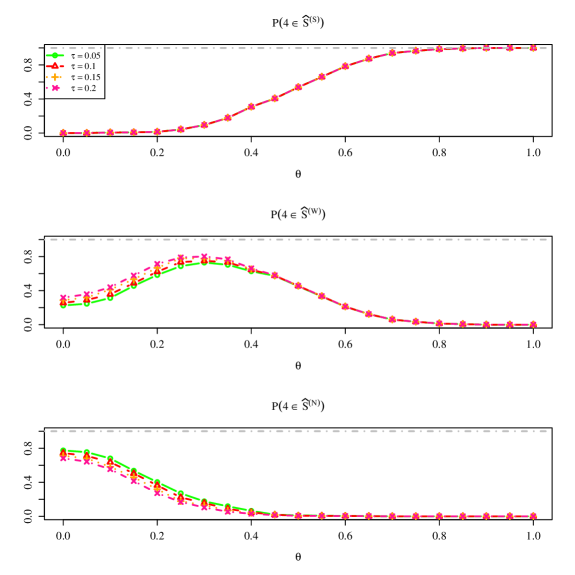

We then identify whether a covariate is a strong signal, weak signal, or noise variable based on the criterion in (3.5). For illustration, we choose to be and to be . Figure 5 represents the empirical probabilities of assigning the covariate to different signal categories as varies and . Figure 5 shows that when is close to zero, is more likely to be identified as a noise variable; when is far away from zero and one, the empirical probability of being identified as a weak signal is highest; as becomes larger, the empirical probability of being identified as a strong signal becomes more dominant, and gradually increases to one. The results for the correlated covariates are given in Figures S3 and S4 of the Supplementary Material S5, and we have similar findings. Therefore, our proposed signal identification criterion (3.5) performs well in practice.

After identifying the signal strength levels, we construct the confidence intervals based on the proposed two-step inference procedure. We also compare our method with the two-step inference method based on Shi and Qu, (2017), which does not construct confidence intervals for the identified noise variables. In addition, we construct confidence intervals based on the asymptotic theory for the one-step adaptive lasso estimator, as shown in (4.1), the maximum likelihood estimation method, as shown in (4.2), the perturbation method (Minnier et al.,, 2011), the estimating equation-based method (Neykov et al.,, 2018), the standard bootstrap method (Efron and Tibshirani,, 1994), the smoothed bootstrap method (Efron,, 2014), the de-biased lasso method (Javanmard and Montanari,, 2014; Van de Geer et al.,, 2014; Zhang and Zhang,, 2014), and two different types of bootstrap de-biased lasso methods (Dezeure et al.,, 2017). The number of bootstrap resampling is set to for all bootstrap methods, and the resampling number is set to for the perturbation method. The implementation details of the estimating equation-based method and the two types of bootstrap de-biased lasso methods can be found in the Supplementary Material S4. For the method based on the asymptotic theory for the one-step adaptive lasso estimator, if a variable is not selected, then we do not construct a confidence interval for it, because the asymptotic normality is established only for the selected variables.

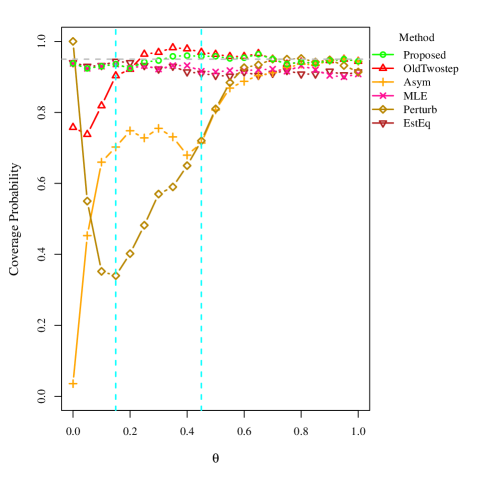

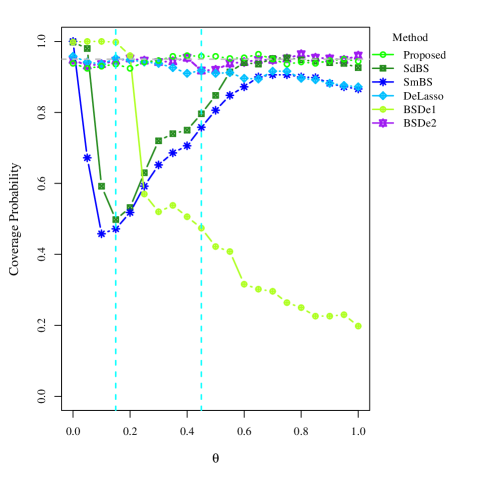

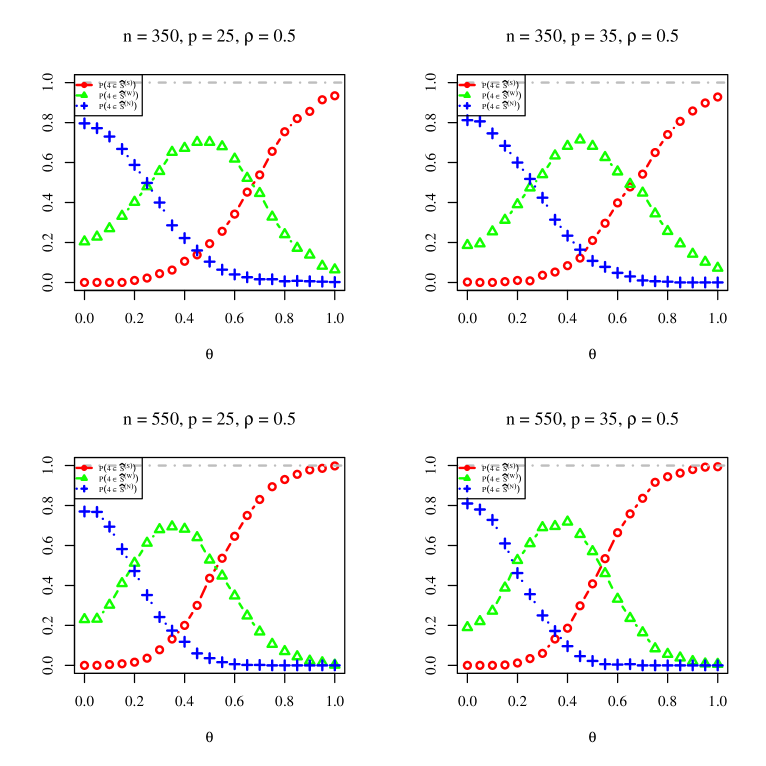

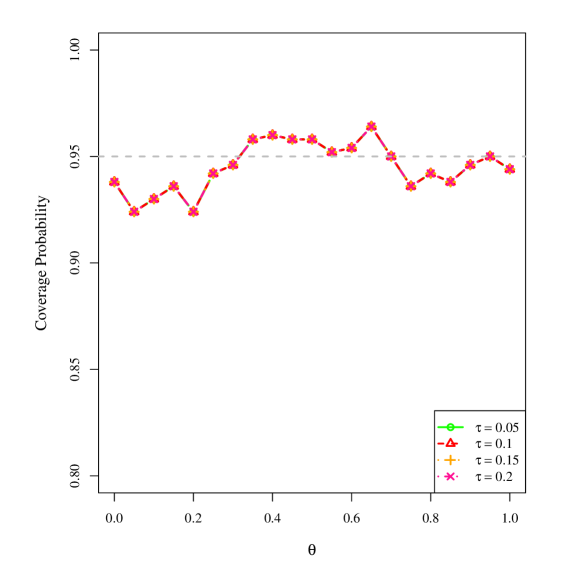

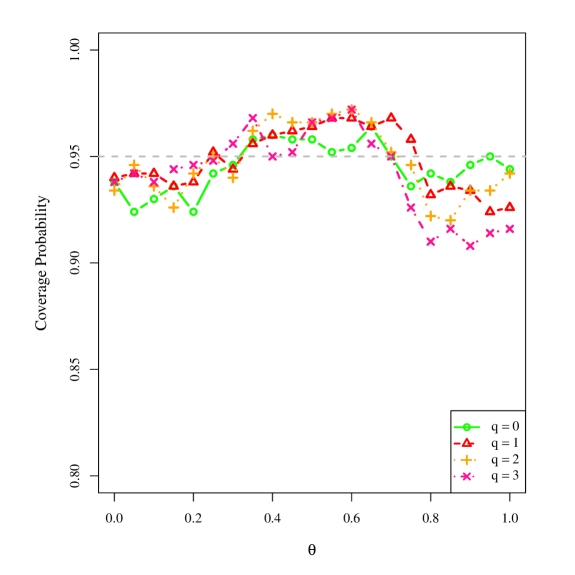

Figures 6 and 7 provide coverage probabilities of the confidence intervals as varies and . In Figures 6 and 7, the vertical line on the left shows whether is more likely to be identified as a noise variable or a weak signal, and the vertical line on the right distinguishes whether is more likely to be identified as a weak signal or a strong signal. The threshold values are obtained from Figure 5. Comparing the proposed two-step inference method with the two-step inference method based on Shi and Qu, (2017), when is small, the former outperforms the latter. When is close to zero, the coverage probability of the asymptotic method is too low and close to zero, while the perturbation method, standard bootstrap method, smoothed bootstrap method, and type-I bootstrap de-biased lasso method provide over-coverage confidence intervals, with coverage probabilities approximating to one. When the signal is weak, the asymptotic method, perturbation method, standard bootstrap method, smoothed bootstrap method, and type-I bootstrap de-biased lasso method all perform poorly, and their coverage probabilities are much lower than . In addition, the coverage probability of the estimating equation-based method is slightly lower than . When the signal is stronger, the performance of the maximum likelihood estimation method, estimating equation-based method, de-biased lasso method, and type-I bootstrap de-biased lasso method also become worse. However, the coverage probabilities of the confidence intervals for the proposed method and the type-II bootstrap de-biased lasso method are close to under all signal strength levels of .

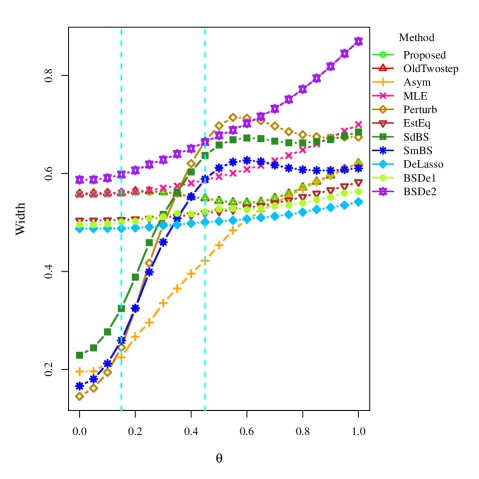

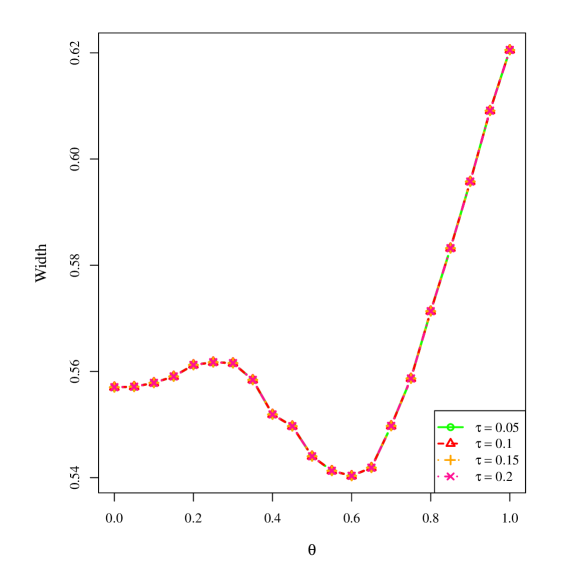

Figure 8 provides the average widths of the confidence intervals as varies and . Note that the widths of the confidence intervals for the two types of two-step inference methods are both very close, while their coverage probabilities are not similar when is small. The width of the confidence interval using the proposed method is between those of the maximum likelihood estimation method and the asymptotic method. This is not surprising, because the proposed method combines the strengths of these two methods. Although the confidence intervals based on the asymptotic method, perturbation method, standard bootstrap method, and smoothed bootstrap method are narrow when is close to zero, the coverage probabilities are not accurate, because they are either too small or too large. When the signal is strong, the widths of the confidence intervals for the perturbation method, standard bootstrap method, and smoothed bootstrap method are, in general, larger than that for the proposed method. Although the estimating equation-based method, de-biased lasso method, and type-I bootstrap de-biased lasso method have shorter confidence intervals than that of the proposed method, their coverage probabilities of the confidence intervals decrease as the signal becomes stronger. Overall, the confidence interval for the type-II bootstrap de-biased lasso method is wider than that of the proposed method.

The coverage probabilities and average widths of the confidence intervals under all simulation settings are summarized in Tables S1–S4 of the Supplementary Material S5. For each simulation setting, we select three different values of , under which is identified as a noise variable, weak signal, and strong signal, respectively. In summary, the findings from the simulation setting of still hold under other simulation settings when . By comparison, the average widths of the confidence intervals for all methods decrease with the sample size and increase with the correlations between the covariates. When is not a strong signal, regardless of the correlations among covariates, the confidence intervals for the asymptotic method have relatively low coverage probabilities. When is a strong signal, if is or , the asymptotic method provides accurate confidence intervals, but if increases to , the performance of the asymptotic method deteriorates. However, the coverage probabilities of the confidence intervals for the proposed method are still close to under all simulation settings.

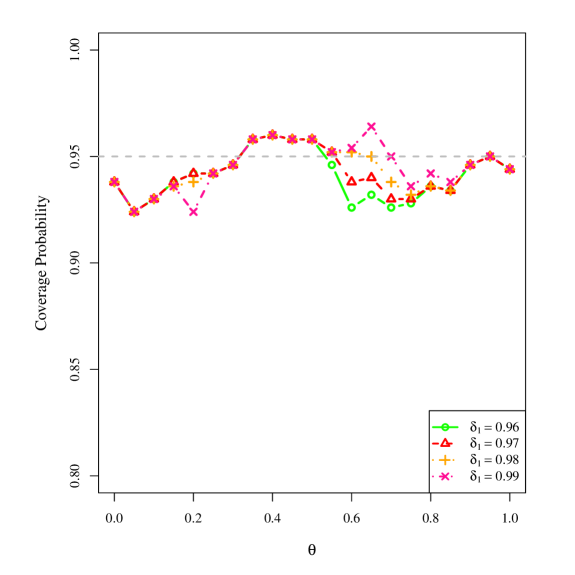

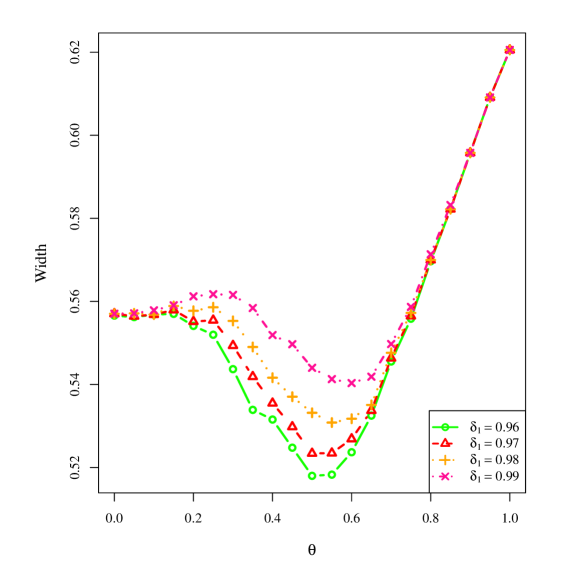

In order to see whether the performance of the proposed method is sensitive to the choice of the threshold values and , we also consider other combinations of threshold values. For example, when , we set as and choose to be , or , which is larger than . The empirical probabilities of assigning the covariate to different signal categories are shown in Figure S5 of the Supplementary Material S5. As the value of becomes larger and the value of is fixed, the empirical probability of identifying as a weak signal becomes larger, and that of identifying as a strong signal becomes smaller if is not sufficiently large. Furthermore, the empirical probability of identifying as a noise variable does not change. This is because of the proposed signal identification criterion. Figures S6–S7 in the Supplementary Material S5 show the corresponding coverage probabilities and average widths of the confidence intervals for the proposed two-step inference method. As shown, the coverage probability becomes larger as increases and is between and , and the average width becomes larger as increases and is between and . This is not surprising because when increases, the probability of using the maximum likelihood method to construct the confidence intervals becomes larger. As shown in Figures 7 and 8, when is not too large, the coverage probability and average width of the confidence interval based on the maximum likelihood method is higher than that based on the asymptotic method. However, as varies, the changes of the coverage probability and average width are not large.

We also consider another situation where is set to and is chosen to be , or . Figure S8 in the Supplementary Material S5 shows the empirical probabilities of assigning the covariate to different signal categories in this situation. Here, we find that as increases, the empirical probability of identifying as a weak signal is larger, and that of identifying as a noise variable is smaller if is not too large. The empirical probability of identifying as a strong signal remains the same. This is consistent with the proposed signal selection criterion. However, because the proposed two-step inference method uses the same confidence interval construction method for the identified noise variables and weak signals, the confidence interval does not change with the value of , as shown in Figures S9–S10 of the Supplementary Material S5.

We also examine whether the performance of the proposed method is sensitive to the total number of weak signals. We reset the regression coefficient vector to be

, where is taken to be , or . For illustration, let , be , and be . Based on the signal identification criterion, all the covariates corresponding to the coefficient are weak signals if ranges from zero to one. If the covariate is identified as a weak signal, then the total number of weak signals is ; otherwise it is . The empirical probabilities of assigning the covariate to different signal categories are shown in Figure S11 of the Supplementary Material S5, which are not sensitive to the value of . Figures S12–S13 in the Supplementary Material S5 respectively show the coverage probabilities and average widths of the confidence intervals for the proposed two-step inference method, showing that when is small, the average width increases with the value of , while the coverage probability does not change monotonously with the value of . In addition, as varies, the variations of average width and coverage probability are not large. Thus, the performance of the proposed method is quite robust to the total number of weak signals.

6 Real-Data Application

To illustrate the performance of the proposed method, we apply it to a data set in the Practice Fusion diabetes study, which was provided by Kaggle as part of the “Practice Fusion Diabetes Classification” challenge (Kaggle,, 2012). The data set consists of de-identified electronic medical records for over patients. There are a total of 9948 patients in the training data, including a binary variable indicating whether a patient is diagnosed with Type 2 diabetes mellitus (T2DM), or not. In this analysis, we aim to determine the most important risk factors for the incidence of T2DM, which can be used to identify patients with a high risk of T2DM.

We first extract predictors from the predictors selected by the first-place winner in the Kaggle competition by removing some highly correlated predictors (details can be found in https://www.kaggle.com/c/pf2012-diabetes/overview/winners). These predictors can be divided into six categories: basic information, transcript records, diagnosis information, medication information, lab result, and smoking status. Detailed information about these predictors can be found in Table S5 in the Supplementary Material S6. One outlying patient is also removed owing to inaccurate information on the predictors. All the predictors are standardized beforehand. We adopt the following logistic regression model to fit the data set:

where and .

We first obtain the one-step adaptive lasso estimates of the regression coefficients following the tuning parameter selection procedure given in the Supplementary Material S4. We then identify whether a predictor is a strong signal, weak signal, or noise variable based on criterion (3.5). Here, we choose to be and to be . From all the predictors, we identify strong signals, weak signals, and noise variables. The strong signals are all selected by the one-step adaptive lasso estimator, indicating consistency between it and our method for strong signal selection. Among the weak signals, are also selected by the one-step adaptive lasso estimator, while the other eight predictors are only identified by our method. These eight additional predictors include (1) the number of times being diagnosed with herpes zoster, hypercholesterolemia, hypertensive heart disease, respiratory infection, sleep apnea, and joint pain, respectively; (2) the number of transcripts for cardiovascular disease; and (3) the number of diagnoses per weighted year. The relationships between these eight predictors and diabetes have also been studied by other researchers. For example, Papagianni et al., (2018) reviewed studies on associations between herpes zoster and diabetes mellitus, and found that herpes zoster and T2DM were likely to coexist for the same patient.

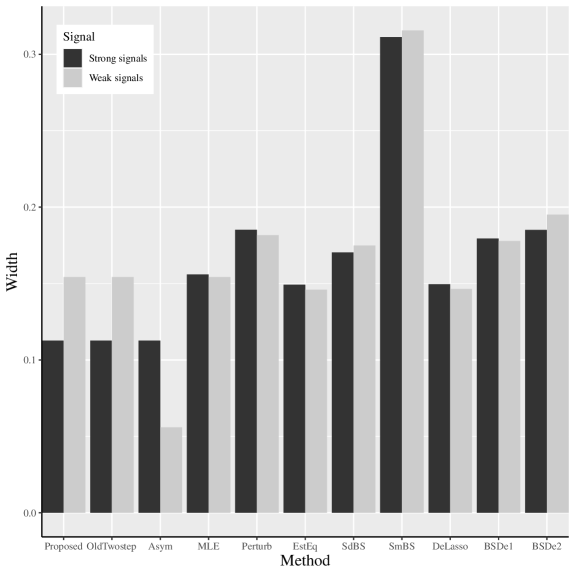

Next, we construct the confidence intervals using our two-step inference method, together with all other comparison methods in Section 5. Figure 9 shows the average widths of the confidence intervals for the strong and weak signals. For both, the widths of the confidence intervals for the two types of two-step inference methods are the same. For strong signals, the proposed method and the asymptotic method provide the shortest confidence intervals. For weak signals, the widths of the confidence intervals based on the proposed method are smaller than those based on the perturbation method, standard bootstrap method, smoothed bootstrap method, and two types of bootstrap de-biased lasso methods.

7 Conclusion

We have proposed a new unified approach for weak signal identification and inference in penalized likelihood models, including the special case when the responses are categorical. To identify weak signals, we propose using the estimated selection probability of each covariate as a measure of the signal strength, and develop a signal identification criterion based directly on the estimated selection probability. To construct confidence intervals for the regression coefficients, we propose a two-step inference procedure. Extensive simulation studies and a real-data application show that the proposed signal identification method and two-step inference procedure outperform several existing methods in finite samples.

The proposed method can be extended to a high-dimensional setting where is not fixed. One possible way is to use the de-biased lasso estimator as an initial estimator for the one-step adaptive lasso estimator, and then leverage the asymptotic properties of the de-biased lasso estimator to derive the selection probability. We can also use a penalized method to estimate the inverse of the information matrix, such as the CLIME estimator (Cai et al.,, 2011). In addition, our signal identification and inference framework can be extended to longitudinal data. For longitudinal data, we can replace the negative log-likelihood function with the generalized estimating function in the estimation. Finally, in the fields of causal inference and econometrics, there is a popular “weak instrument” problem (Chao and Swanson,, 2005; Burgess and Thompson,, 2011; Choi et al.,, 2018), which can be considered a weak signal problem. This is worth further development using our approach.

Supplementary Material

The online Supplementary Material contains six sections. Section S1 derives the approximated selection probability. Section S2 provide an additional detailed analysis of the approximated selection probability in finite samples. Section S3 contains a proof for Theorem 1. Section S4 presents the implementation details of several methods. Sections S5 and S6 provide additional simulation results and information related to the real-data application, respectively.

Acknowledgments

This work was partially supported by the National Science Foundation of the United States (DMS-1821198, DMS-1952406), National Natural Science Foundation of China (11671096, 11731011, 12071087), and Natural Sciences and Engineering Research Council of Canada (RGPIN-2019-07052, DGECR-2019-00453, RGPAS-2019-00093).

References

- Burgess and Thompson, (2011) Burgess, S. and Thompson, S. G. (2011). Bias in causal estimates from mendelian randomization studies with weak instruments. Statistics in Medicine, 30(11):1312–1323.

- Cai et al., (2011) Cai, T., Liu, W., and Luo, X. (2011). A constrained L1 minimization approach to sparse precision matrix estimation. Journal of the American Statistical Association, 106(494):594–607.

- Chao and Swanson, (2005) Chao, J. C. and Swanson, N. R. (2005). Consistent estimation with a large number of weak instruments. Econometrica, 73(5):1673–1692.

- Choi et al., (2018) Choi, J., Gu, J., and Shen, S. (2018). Weak-instrument robust inference for two-sample instrumental variables regression. Journal of Applied Econometrics, 33(1):109–125.

- Dezeure et al., (2017) Dezeure, R., Bühlmann, P., and Zhang, C.-H. (2017). High-dimensional simultaneous inference with the bootstrap. Test, 26(4):685–719.

- Efron, (2014) Efron, B. (2014). Estimation and accuracy after model selection. Journal of the American Statistical Association, 109(507):991–1007.

- Efron and Tibshirani, (1994) Efron, B. and Tibshirani, R. J. (1994). An introduction to the bootstrap. CRC press.

- Huang and Xie, (2007) Huang, J. and Xie, H. (2007). Asymptotic oracle properties of scad-penalized least squares estimators. In Asymptotics: Particles, processes and inverse problems, pages 149–166. Institute of Mathematical Statistics.

- Javanmard and Montanari, (2014) Javanmard, A. and Montanari, A. (2014). Confidence intervals and hypothesis testing for high-dimensional regression. The Journal of Machine Learning Research, 15(1):2869–2909.

- Jia et al., (2019) Jia, J., Xie, F., and Xu, L. (2019). Sparse poisson regression with penalized weighted score function. Electronic Journal of Statistics, 13(2):2898–2920.

- Jin et al., (2014) Jin, J., Zhang, C.-H., and Zhang, Q. (2014). Optimality of graphlet screening in high dimensional variable selection. The Journal of Machine Learning Research, 15(1):2723–2772.

- Kaggle, (2012) Kaggle (2012). Practice fusion diabetes classification. data retrieved from Kaggle competition dataset, http://www.kaggle.com/c/pf2012-diabetes.

- Lambert and Eilers, (2005) Lambert, P. and Eilers, P. H. (2005). Bayesian proportional hazards model with time-varying regression coefficients: A penalized poisson regression approach. Statistics in Medicine, 24(24):3977–3989.

- Li et al., (2019) Li, Y., Hong, H. G., Ahmed, S. E., and Li, Y. (2019). Weak signals in high-dimensional regression: Detection, estimation and prediction. Applied Stochastic Models in Business and Industry, 35(2):283–298.

- Liu et al., (2020) Liu, H., Xu, X., and Li, J. J. (2020). A bootstrap lasso+ partial ridge method to construct confidence intervals for parameters in high-dimensional sparse linear models. arXiv preprint arXiv:1706.02150.

- Minnier et al., (2011) Minnier, J., Tian, L., and Cai, T. (2011). A perturbation method for inference on regularized regression estimates. Journal of the American Statistical Association, 106(496):1371–1382.

- Neykov et al., (2018) Neykov, M., Ning, Y., Liu, J. S., Liu, H., et al. (2018). A unified theory of confidence regions and testing for high-dimensional estimating equations. Statistical Science, 33(3):427–443.

- Papagianni et al., (2018) Papagianni, M., Metallidis, S., and Tziomalos, K. (2018). Herpes zoster and diabetes mellitus: a review. Diabetes Therapy, 9(2):545–550.

- Park and Hastie, (2008) Park, M. Y. and Hastie, T. (2008). Penalized logistic regression for detecting gene interactions. Biostatistics, 9(1):30–50.

- Reangsephet et al., (2020) Reangsephet, O., Lisawadi, S., and Ahmed, S. E. (2020). Weak signals in high-dimensional logistic regression models. In International Conference on Management Science and Engineering Management, pages 121–133. Springer.

- Shi and Qu, (2017) Shi, P. and Qu, A. (2017). Weak signal identification and inference in penalized model selection. The Annals of Statistics, 45(3):1214–1253.

- Tibshirani, (1996) Tibshirani, R. (1996). Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 58(1):267–288.

- Tibshirani, (2011) Tibshirani, R. (2011). Regression shrinkage and selection via the lasso: a retrospective. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 73(3):273–282.

- Tibshirani et al., (2005) Tibshirani, R., Saunders, M., Rosset, S., Zhu, J., and Knight, K. (2005). Sparsity and smoothness via the fused lasso. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 67(1):91–108.

- Van de Geer et al., (2014) Van de Geer, S., Bühlmann, P., Ritov, Y., Dezeure, R., et al. (2014). On asymptotically optimal confidence regions and tests for high-dimensional models. Annals of Statistics, 42(3):1166–1202.

- Van de Geer et al., (2011) Van de Geer, S., Bühlmann, P., and Zhou, S. (2011). The adaptive and the thresholded lasso for potentially misspecified models (and a lower bound for the lasso). Electronic Journal of Statistics, 5:688–749.

- Wang and Leng, (2007) Wang, H. and Leng, C. (2007). Unified lasso estimation by least squares approximation. Journal of the American Statistical Association, 102(479):1039–1048.

- Wu et al., (2009) Wu, T. T., Chen, Y. F., Hastie, T., Sobel, E., and Lange, K. (2009). Genome-wide association analysis by lasso penalized logistic regression. Bioinformatics, 25(6):714–721.

- Yuan and Lin, (2006) Yuan, M. and Lin, Y. (2006). Model selection and estimation in regression with grouped variables. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 68(1):49–67.

- Zhang, (2010) Zhang, C.-H. (2010). Nearly unbiased variable selection under minimax concave penalty. The Annals of Statistics, 38(2):894–942.

- Zhang and Zhang, (2014) Zhang, C.-H. and Zhang, S. S. (2014). Confidence intervals for low dimensional parameters in high dimensional linear models. Journal of the Royal Statistical Society: Series B: Statistical Methodology, pages 217–242.

- Zhang and Jia, (2022) Zhang, H. and Jia, J. (2022). Elastic-net regularized high-dimensional negative binomial regression: consistency and weak signals detection. Statistica Sinica, 32:181–207.

- Zhang, (2013) Zhang, T. (2013). Multi-stage convex relaxation for feature selection. Bernoulli, 19(5B):2277–2293.

- Zhang, (2017) Zhang, Y. (2017). Recovery of weak signal in high dimensional linear regression by data perturbation. Electronic Journal of Statistics, 11(2):3226–3250.

- Zhao and Yu, (2006) Zhao, P. and Yu, B. (2006). On model selection consistency of lasso. Journal of Machine Learning Research, 7:2541–2563.

- Zhu and Hastie, (2004) Zhu, J. and Hastie, T. (2004). Classification of gene microarrays by penalized logistic regression. Biostatistics, 5(3):427–443.

- Zou, (2006) Zou, H. (2006). The adaptive lasso and its oracle properties. Journal of the American Statistical Association, 101(476):1418–1429.

- Zou and Hastie, (2005) Zou, H. and Hastie, T. (2005). Regularization and variable selection via the elastic net. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 67(2):301–320.

- Zou and Li, (2008) Zou, H. and Li, R. (2008). One-step sparse estimates in nonconcave penalized likelihood models. Annals of Statistics, 36(4):1509–1533.

Yuexia Zhang

Department of Management Science and Statistics, The University of Texas at San Antonio, TX 78249, USA.

E-mail: yuexia.zhang@utsa.edu

Peibei Shi

Meta, Menlo Park, CA 94025, United States.

E-mail: pshi@meta.com

Zhongyi Zhu

Department of Statistics, Fudan University, Shanghai 200433, China.

E-mail: zhuzy@fudan.edu.cn

Linbo Wang

Department of Statistical Sciences, University of Toronto, ON M5S 3G3, Canada.

E-mail: linbo.wang@utoronto.ca

Annie Qu

Department of Statistics, University of California, Irvine, CA 92697, United States.

E-mail: aqu2@uci.edu

SUPPLEMENTARY MATERIALS FOR

“WEAK SIGNAL IDENTIFICATION AND INFERENCE

IN PENALIZED LIKELIHOOD MODELS

FOR CATEGORICAL RESPONSES”

Yuexia Zhang, Peibei Shi, Zhongyi Zhu, Linbo Wang and Annie Qu

The University of Texas at San Antonio, Meta, Fudan University

University of Toronto and University of California, Irvine

Abstract:

The online Supplementary Material contains six sections. Section S1 derives the approximated selection probability. Section S2 provide an additional detailed analysis of the approximated selection probability in finite samples. Section S3 contains a proof for Theorem 1. Section S4 presents the implementation details of several methods. Sections S5 and S6 provide additional simulation results and information related to the real-data application, respectively.

S1 Derivation of the Approximated Selection Probability

In Section 2 of the main paper, we have obtained the following condition for selecting the covariate , :

It is equivalent to

| (S1.1) | ||||

We consider the following three formulas respectively,

| (S1.2) |

and

| (S1.3) |

Since is the th element of , and is an diagonal matrix with the th element , then by calculation,

Since are independent and identically distributed random vectors, is a continuous function of and the maximum likelihood estimator under some regularity conditions, then by the Law of Large Numbers and Continuous Mapping Theorem, we have , and . Then

By calculation, (S1.2) equals

Because of the same reason as before, , , and . By the Central Limit Theorem, , where . Then . Furthermore, since and the number of covariates is finite, then according to the Slutsky’s Theorem, (S1.2) is .

Based on the oracle properties of , if , then . Therefore, similar to the previous proof,

| (S1.4) | ||||

If , then , where is the Fisher information matrix knowing and is an element of the matrix corresponding to . Therefore, . Furthermore,

| (S1.5) | ||||

In summary, the condition for selecting the covariate becomes

Furthermore,

| (S1.6) |

By the Central Limit Theorem, and . Therefore, the right hand side of (S1.6) can be approximated by

| (S1.7) |

S2 Additional Detailed Analysis of the Approximated Selection Probability in Finite Samples

In this selection, we provide an additional detailed analysis of finite-sample properties of the approximated selection probability and provide some plots to illustrate the finite-sample properties of under three different kinds of likelihood-based models.

S2.1 Symmetry of the approximated selection probability

In order to study given any values in except , whether is a symmetric function of or not, we need to study for any , whether is equal to . According to (S1.7),

and

Since with , and with , then one of the sufficient conditions for is that the distribution of is symmetric about zero and is independent of for any . Under this condition, we have , , and . Furthermore, .

However, this sufficient condition may not be satisfied in practice and it is easy to find a case where . So given any values in except , is not necessarily a symmetric function of .

S2.2 Monotonicity of the approximated selection probability

In order to study the monotonicity of the approximated selection probability, we need to study the first order derivative of with respect to . By calculation,

where

and

with

and

To simplify the proof, we first consider the case where follows a logistic regression model, that is,

By calculation, and . Assume , and are independent, and , . Denote as , . It is easy to show that and

Therefore,

It means that obtains a minimum value at . Furthermore, there exists two positive constant and such that for any and for any . Thus, for any and for any . In other words, is an increasing function of if and is a decreasing function of if .

Second, we consider the case where follows a Poisson regression model, that is,

where . By calculation, and . Assume , and are independent, and , . Denote as , . Then

with

and

In particular, if follows the standard normal distribution, then

Obviously, if , if and if . Thus, is an increasing function of if and is a decreasing function of if .

S3 Proof for Theorem 1

According to (2.4) in the main paper, the objective function about for the one-step adaptive lasso estimator is

For , can be approximated by

where .

It can be shown easily that there exists a that is a -consistent local minimizer of and satisfies the following condition:

where and . Without loss of generality, assume and .

Note that is a consistent estimator, then

| (S3.1) | ||||

Denote as , then according to (S3.1),

| (S3.2) | ||||

where and . According to the Central Limit Theorem, , where . Furthermore, according to the Slutsky’s Theorem, the asymptotic bias of is

where . The asymptotic covariance matrix of is

If as goes to infinity, then and .

If is finite, then the bias of can not be ignored and is not necessarily equal to . Without loss of generality, assume . Then . Furthermore, the estimators of bias and covariance matrix of are given by

and

where and .

S4 Implementation Details of Several Methods

In this section, we introduce the implementation details of several methods mentioned in the main paper.

S4.1 One-step adaptive lasso estimator

To obtain the one-step adaptive lasso estimator, we use the function glmnet in R to solve (2.5). The selection of tuning parameter is important. In finite samples, if is too large, the bias of the one-step adaptive lasso estimator will be large and the coverage probability of the confidence interval constructed based on the asymptotic theory for the one-step adaptive lasso estimator will be low; if is too small, the number of false positives will be large and the width of the confidence interval will also be large. The Bayesian information criterion (BIC) and cross-validation (CV) method are two commonly used tuning parameter selection methods. Based on the simulation results, selected based on the Bayesian information criterion proposed by Wang and Leng, (2007) is much larger than the value of selected by the 5-fold cross-validation method. Denote the values of selected by these two methods as and , respectively. We choose to be as a trade-off of these two methods.

S4.2 Estimating equation-based method

In our simulation studies and real-data application, we compare the proposed method with an estimating equation-based method, which is proposed by Neykov et al., (2018) and denoted as “EstEq.” We apply their method based on Algorithm 1 in their paper. Using the same notations as in our paper, the implementation details are as follows:

-

Step 1:

Use the R functions gds and cv_gds to get the generalized Dantzig selector of the regression coefficient in a logistic regression model and denote the estimator as . That is, solve the following optimization problem to obtain an estimate :

where is the conditional log-likelihood function of given for a logistic regression model and , . The tuning parameter of the generalized Dantzig selector, , is selected by the 10-fold cross-validation method.

-

Step 2:

Calculate the inverse of , where . Denote the inverse of as . Define the projection direction for the th element of , , as , where is the th row element of . Note that in Neykov et al., (2018), the authors used the CLIME estimator to estimate the inverse of . However, in our problem, we assume and is fixed, then the inverse of can be calculated directly.

-

Step 3:

Use the R function uniroot to solve the sparse projected test function and denote the estimated value of as .

-

Step 4:

Construct a two-sided confidence interval for as

where .

S4.3 Two types of bootstrap de-biased lasso methods

Motivated by the idea of Dezeure et al., (2017), we establish two xy-paired bootstrap de-biased lasso methods, which are referred to as “the type-I bootstrap de-biased lasso method” and “the type-II bootstrap de-biased lasso method,” respectively. The bootstrap de-biased lasso method is based on the de-biased lasso method proposed by Zhang and Zhang, (2014), Van de Geer et al., (2014) and Javanmard and Montanari, (2014). Following the idea of Dezeure et al., (2017), the procedure for the type-I bootstrap de-biased lasso method is as follows:

-

(i)

Based on the original data points , calculate the lasso estimator and de-biased lasso estimator of the th element of , . Denote them as and , respectively. Calculate the standard error of the de-biased lasso estimator, .

-

(ii)

Resample with replacement from for times. For the th bootstrap sample, calculate the de-biased lasso estimator , the standard error for the de-biased lasso estimator and . Denote the -quantile of as .

-

(iii)

Construct a two-sided confidence interval for as

In addition, the procedure for the type-II bootstrap de-biased lasso method is as follows:

-

(i)

Resample with replacement from for times. For the th bootstrap sample, calculate the de-biased lasso estimator of the th element of , , which is denoted as . Denote the -quantile of as .

-

(iii)

Construct a two-sided confidence interval for as

S5 Additional Simulation Results

In this section, we present additional simulation results under the simulation settings in Section 5. Figures S1 and S2 display the results for different types of selection probability for when and , respectively. Figures S3 and S4 present the empirical probabilities of assigning the covariate to different signal categories as the value of varies when and , respectively. Tables S1–S4 show the coverage probabilities and average widths of the confidence intervals under all simulation settings. Figures S5–S7 show the simulation results for the proposed method when the threshold value varies. Figures S8–S10 show the simulation results for the proposed method when the threshold value varies. Figures S11–S13 show the simulation results for the proposed method when the total number of weak signals varies.

| Method | |||||||

|---|---|---|---|---|---|---|---|

| Proposed | 93.8 | 94.4 | 96.2 | 94.6 | 92.2 | 94.8 | |

| OldTwostep | 75.8 | 76.7 | 81.4 | 77.1 | 66.9 | 72.3 | |

| Asym | 3.6 | 3.8 | 12.7 | 4.3 | 1.4 | 4.0 | |

| MLE | 93.8 | 94.4 | 96.2 | 94.6 | 92.2 | 94.8 | |

| Perturb | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | |

| EstEq | 94.0 | 94.2 | 96.6 | 95.6 | 92.8 | 94.8 | |

| SdBS | 99.8 | 100.0 | 99.8 | 99.8 | 99.8 | 99.0 | |

| SmBS | 100.0 | 100.0 | 99.8 | 100.0 | 100.0 | 100.0 | |

| DeLasso | 95.8 | 96.0 | 98.2 | 96.4 | 95.2 | 96.4 | |

| BSDe1 | 99.8 | 100.0 | 99.8 | 100.0 | 100.0 | 100.0 | |

| BSDe2 | 94.8 | 94.4 | 96.2 | 95.4 | 91.8 | 94.4 | |

| Proposed | 94.6 | 95.2 | 92.8 | 95.2 | 96.4 | 94.6 | |

| OldTwostep | 96.9 | 96.6 | 92.0 | 98.0 | 96.7 | 92.4 | |

| Asym | 75.5 | 71.6 | 61.5 | 65.8 | 69.6 | 69.3 | |

| MLE | 92.2 | 93.4 | 92.6 | 92.4 | 92.0 | 93.6 | |

| Perturb | 57.0 | 55.0 | 52.0 | 38.8 | 49.0 | 44.0 | |

| EstEq | 92.2 | 92.6 | 93.8 | 92.6 | 91.6 | 94.2 | |

| SdBS | 72.0 | 69.6 | 62.8 | 53.0 | 61.0 | 53.4 | |

| SmBS | 65.2 | 64.6 | 59.8 | 39.8 | 49.4 | 47.8 | |

| DeLasso | 93.8 | 94.0 | 92.8 | 93.0 | 93.4 | 95.0 | |

| BSDe1 | 52.0 | 58.0 | 85.6 | 48.6 | 60.6 | 86.4 | |

| BSDe2 | 94.2 | 94.6 | 95.0 | 96.2 | 95.0 | 95.2 | |

| Proposed | 95.0 | 93.6 | 95.0 | 96.0 | 93.8 | 97.2 | |

| OldTwostep | 95.0 | 93.6 | 95.4 | 96.0 | 93.8 | 97.2 | |

| Asym | 95.0 | 93.6 | 91.6 | 96.0 | 93.8 | 92.2 | |

| MLE | 90.0 | 91.6 | 91.2 | 87.8 | 87.8 | 86.8 | |

| Perturb | 93.2 | 93.0 | 97.0 | 95.4 | 94.2 | 96.4 | |

| EstEq | 90.6 | 87.4 | 92.8 | 89.8 | 89.4 | 89.4 | |

| SdBS | 93.8 | 93.8 | 95.6 | 93.4 | 93.4 | 95.6 | |

| SmBS | 87.2 | 87.8 | 90.2 | 68.6 | 69.6 | 74.8 | |

| DeLasso | 87.6 | 87.6 | 90.4 | 90.4 | 84.2 | 89.6 | |

| BSDe1 | 23.0 | 26.0 | 34.8 | 17.8 | 15.4 | 26.4 | |

| BSDe2 | 94.8 | 95.6 | 97.4 | 94.4 | 95.0 | 95.6 | |

-

•

Note: Proposed: the proposed two-step inference method; OldTwostep: the two-step inference method based on Shi and Qu, (2017), which does not construct confidence intervals for identified noise variables; Asym: the method based on the asymptotic theory using the one-step adaptive lasso estimator; MLE: the maximum likelihood estimation method; Perturb: the perturbation method; EstEq: the estimating equation-based method; SdBS: the standard bootstrap method; SmBS: the smoothed bootstrap method; DeLasso: the de-biased lasso method; BSDe1: the type-I bootstrap de-biased lasso method; BSDe2: the type-II bootstrap de-biased lasso method.

| Method | |||||||

|---|---|---|---|---|---|---|---|

| Proposed | 95.4 | 94.8 | 95.4 | 94.6 | 94.2 | 95.8 | |

| OldTwostep | 81.7 | 77.6 | 80.0 | 75.9 | 76.4 | 78.9 | |

| Asym | 4.2 | 7.6 | 7.2 | 1.4 | 4.2 | 7.1 | |

| MLE | 95.4 | 94.8 | 95.4 | 94.6 | 94.2 | 95.8 | |

| Perturb | 99.8 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | |

| EstEq | 95.6 | 93.8 | 95.6 | 95.2 | 95.0 | 96.8 | |

| SdBS | 99.8 | 99.6 | 99.6 | 100.0 | 100.0 | 100.0 | |

| SmBS | 99.8 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | |

| DeLasso | 96.6 | 95.4 | 97.0 | 96.4 | 95.8 | 97.4 | |

| BSDe1 | 99.8 | 100.0 | 99.8 | 100.0 | 100.0 | 100.0 | |

| BSDe2 | 95.4 | 94.6 | 95.6 | 95.8 | 94.2 | 95.6 | |

| Proposed | 94.4 | 95.6 | 95.0 | 95.4 | 93.8 | 95.6 | |

| OldTwostep | 95.8 | 96.6 | 94.8 | 97.0 | 95.1 | 94.7 | |

| Asym | 69.4 | 63.8 | 68.2 | 72.3 | 69.9 | 68.5 | |

| MLE | 94.4 | 95.6 | 94.4 | 93.8 | 92.0 | 95.2 | |

| Perturb | 57.4 | 52.8 | 56.2 | 54.8 | 55.2 | 54.6 | |

| EstEq | 93.6 | 95.0 | 93.8 | 93.4 | 91.4 | 94.8 | |

| SdBS | 68.8 | 65.2 | 62.8 | 65.0 | 66.8 | 62.0 | |

| SmBS | 67.8 | 66.0 | 63.6 | 61.6 | 62.8 | 64.4 | |

| DeLasso | 93.0 | 94.8 | 94.4 | 94.0 | 93.0 | 95.8 | |

| BSDe1 | 52.8 | 57.2 | 79.2 | 49.2 | 57.4 | 79.6 | |

| BSDe2 | 94.2 | 96.4 | 94.8 | 95.2 | 96.0 | 96.0 | |

| Proposed | 94.2 | 94.4 | 93.8 | 95.0 | 95.0 | 92.2 | |

| OldTwostep | 94.2 | 94.4 | 93.8 | 95.0 | 95.0 | 92.2 | |

| Asym | 94.2 | 94.4 | 90.6 | 95.0 | 95.0 | 89.0 | |

| MLE | 93.6 | 94.4 | 92.6 | 90.4 | 89.4 | 91.2 | |

| Perturb | 90.2 | 93.0 | 97.0 | 93.8 | 94.2 | 95.8 | |

| EstEq | 92.4 | 93.0 | 90.6 | 90.4 | 92.4 | 91.6 | |

| SdBS | 91.2 | 93.8 | 96.2 | 91.8 | 91.6 | 94.2 | |

| SmBS | 88.4 | 93.8 | 94.4 | 87.0 | 86.0 | 91.2 | |

| DeLasso | 87.0 | 90.2 | 89.4 | 89.0 | 87.2 | 90.4 | |

| BSDe1 | 23.0 | 26.0 | 41.2 | 15.8 | 18.8 | 33.8 | |

| BSDe2 | 96.4 | 97.2 | 94.4 | 93.8 | 95.8 | 95.2 | |

-

•

Note: Proposed: the proposed two-step inference method; OldTwostep: the two-step inference method based on Shi and Qu, (2017), which does not construct confidence intervals for identified noise variables; Asym: the method based on the asymptotic theory using the one-step adaptive lasso estimator; MLE: the maximum likelihood estimation method; Perturb: the perturbation method; EstEq: the estimating equation-based method; SdBS: the standard bootstrap method; SmBS: the smoothed bootstrap method; DeLasso: the de-biased lasso method; BSDe1: the type-I bootstrap de-biased lasso method; BSDe2: the type-II bootstrap de-biased lasso method.

| Method | |||||||

|---|---|---|---|---|---|---|---|

| Proposed | 55.7 | 60.0 | 78.4 | 58.2 | 62.7 | 82.1 | |

| OldTwostep | 55.9 | 60.8 | 79.7 | 58.6 | 63.2 | 82.8 | |

| Asym | 19.6 | 21.6 | 22.3 | 19.7 | 18.9 | 23.3 | |

| MLE | 55.7 | 60.0 | 78.4 | 58.2 | 62.8 | 82.1 | |

| Perturb | 14.5 | 14.7 | 17.6 | 10.3 | 11.1 | 13.9 | |

| EstEq | 50.4 | 53.9 | 70.1 | 51.1 | 54.7 | 71.0 | |

| SdBS | 22.9 | 23.6 | 27.9 | 17.2 | 17.9 | 21.7 | |

| SmBS | 16.6 | 16.8 | 19.4 | 11.4 | 11.9 | 14.3 | |

| DeLasso | 48.7 | 51.9 | 66.8 | 49.4 | 52.6 | 67.5 | |

| BSDe1 | 49.6 | 52.8 | 67.7 | 50.6 | 54.0 | 68.9 | |

| BSDe2 | 58.7 | 63.2 | 82.8 | 63.6 | 69.0 | 90.6 | |

| Proposed | 56.2 | 60.5 | 79.5 | 58.6 | 63.1 | 83.8 | |

| OldTwostep | 56.2 | 60.6 | 79.1 | 58.6 | 63.0 | 83.9 | |

| Asym | 33.5 | 34.0 | 35.0 | 30.2 | 32.8 | 35.8 | |

| MLE | 57.0 | 61.6 | 80.7 | 59.5 | 64.5 | 84.9 | |

| Perturb | 49.6 | 51.7 | 55.9 | 40.5 | 47.1 | 50.3 | |

| EstEq | 51.0 | 54.8 | 71.6 | 51.6 | 55.4 | 72.5 | |

| SdBS | 51.6 | 53.4 | 58.4 | 41.1 | 45.8 | 49.5 | |

| SmBS | 46.0 | 47.4 | 50.1 | 34.6 | 39.1 | 40.8 | |

| DeLasso | 49.4 | 52.9 | 68.3 | 49.7 | 53.2 | 68.6 | |

| BSDe1 | 51.2 | 54.9 | 70.3 | 52.7 | 56.4 | 72.5 | |

| BSDe2 | 62.8 | 67.6 | 88.0 | 68.8 | 74.8 | 98.5 | |

| Proposed | 60.9 | 63.9 | 73.4 | 62.0 | 64.9 | 75.1 | |

| OldTwostep | 60.9 | 63.9 | 73.3 | 62.0 | 64.9 | 75.1 | |

| Asym | 60.9 | 63.8 | 71.0 | 62.0 | 64.8 | 71.8 | |

| MLE | 68.6 | 73.7 | 93.7 | 72.9 | 78.1 | 100.5 | |

| Perturb | 67.4 | 70.4 | 91.6 | 71.1 | 76.1 | 103.2 | |

| EstEq | 57.4 | 61.6 | 78.9 | 57.9 | 61.6 | 79.3 | |

| SdBS | 67.6 | 70.4 | 87.4 | 67.2 | 70.4 | 86.4 | |

| SmBS | 60.8 | 63.6 | 79.7 | 57.9 | 61.0 | 75.9 | |

| DeLasso | 53.5 | 56.8 | 72.9 | 53.6 | 57.0 | 73.2 | |

| BSDe1 | 56.0 | 60.2 | 77.7 | 58.0 | 61.8 | 80.6 | |

| BSDe2 | 84.5 | 91.8 | 115.8 | 100.8 | 108.1 | 137.6 | |

-

•

Note: Proposed: the proposed two-step inference method; OldTwostep: the two-step inference method based on Shi and Qu, (2017), which does not construct confidence intervals for identified noise variables; Asym: the method based on the asymptotic theory using the one-step adaptive lasso estimator; MLE: the maximum likelihood estimation method; Perturb: the perturbation method; EstEq: the estimating equation-based method; SdBS: the standard bootstrap method; SmBS: the smoothed bootstrap method; DeLasso: the de-biased lasso method; BSDe1: the type-I bootstrap de-biased lasso method; BSDe2: the type-II bootstrap de-biased lasso method.

| Method | |||||||

|---|---|---|---|---|---|---|---|

| Proposed | 42.7 | 45.9 | 59.9 | 43.7 | 47.0 | 61.5 | |

| OldTwostep | 42.8 | 46.2 | 60.3 | 44.0 | 47.2 | 61.6 | |

| Asym | 14.8 | 15.3 | 17.0 | 13.7 | 14.7 | 17.0 | |

| MLE | 42.7 | 45.9 | 59.9 | 43.7 | 47.0 | 61.5 | |

| Perturb | 12.6 | 13.3 | 17.1 | 9.7 | 10.8 | 12.7 | |

| EstEq | 39.8 | 42.7 | 55.5 | 40.1 | 42.8 | 55.8 | |

| SdBS | 19.4 | 19.9 | 25.2 | 16.0 | 17.3 | 20.3 | |

| SmBS | 15.1 | 15.3 | 19.4 | 11.8 | 12.9 | 14.7 | |

| DeLasso | 38.6 | 41.2 | 53.2 | 38.8 | 41.4 | 53.5 | |

| BSDe1 | 38.8 | 41.4 | 53.1 | 39.1 | 41.6 | 53.6 | |

| BSDe2 | 43.0 | 46.1 | 60.3 | 44.6 | 48.0 | 62.9 | |

| Proposed | 42.7 | 46.2 | 60.6 | 43.7 | 47.2 | 62.3 | |

| OldTwostep | 42.7 | 46.2 | 60.6 | 43.7 | 47.2 | 62.0 | |

| Asym | 25.7 | 25.2 | 28.9 | 25.8 | 26.4 | 27.5 | |

| MLE | 43.4 | 46.7 | 61.2 | 44.5 | 48.0 | 62.9 | |

| Perturb | 40.7 | 41.7 | 47.7 | 39.1 | 41.2 | 46.2 | |

| EstEq | 40.2 | 43.1 | 56.3 | 40.4 | 43.3 | 56.7 | |

| SdBS | 42.4 | 43.8 | 49.8 | 40.0 | 41.7 | 47.8 | |

| SmBS | 40.2 | 41.4 | 46.0 | 37.3 | 39.0 | 43.6 | |

| DeLasso | 39.0 | 41.7 | 54.0 | 39.2 | 41.7 | 54.2 | |

| BSDe1 | 39.9 | 42.7 | 54.8 | 40.4 | 43.5 | 55.7 | |

| BSDe2 | 45.1 | 48.3 | 62.8 | 47.3 | 51.0 | 66.5 | |

| Proposed | 45.5 | 47.8 | 54.9 | 46.1 | 48.1 | 54.8 | |

| OldTwostep | 45.5 | 47.8 | 54.9 | 46.1 | 48.1 | 54.8 | |

| Asym | 45.5 | 47.8 | 53.6 | 46.1 | 48.1 | 53.6 | |

| MLE | 49.4 | 53.1 | 68.0 | 51.1 | 54.7 | 70.2 | |

| Perturb | 50.5 | 53.3 | 69.3 | 51.5 | 53.5 | 70.2 | |

| EstEq | 43.9 | 47.1 | 60.8 | 44.2 | 47.2 | 60.9 | |

| SdBS | 49.3 | 52.0 | 66.2 | 48.9 | 50.9 | 64.4 | |

| SmBS | 48.9 | 51.6 | 65.8 | 47.3 | 49.6 | 63.2 | |

| DeLasso | 41.4 | 44.2 | 56.8 | 41.6 | 43.9 | 57.2 | |

| BSDe1 | 42.9 | 45.8 | 59.2 | 43.3 | 46.7 | 60.4 | |

| BSDe2 | 54.6 | 58.6 | 74.9 | 59.0 | 63.2 | 81.5 | |

-

•

Note: Proposed: the proposed two-step inference method; OldTwostep: the two-step inference method based on Shi and Qu, (2017), which does not construct confidence intervals for identified noise variables; Asym: the method based on the asymptotic theory using the one-step adaptive lasso estimator; MLE: the maximum likelihood estimation method; Perturb: the perturbation method; EstEq: the estimating equation-based method; SdBS: the standard bootstrap method; SmBS: the smoothed bootstrap method; DeLasso: the de-biased lasso method; BSDe1: the type-I bootstrap de-biased lasso method; BSDe2: the type-II bootstrap de-biased lasso method.

S6 Additional Information in Real-data Application

Table S5 shows the candidate predictors used in the real-data application.

| Category | Predictor |

|---|---|

| Basic information | year of birth |

| gender | |

| 3 predictors indicating whether a patient is from California, Texas, New York or other states | |

| Transcript records | range of BMI |

| the median of weights | |

| the median of heights | |

| the median of systolic blood pressures | |

| the medians of Diastolic blood pressures | |

| the median of respiratory rates | |

| the median of temperatures | |

| 4 predictors corresponding to the numbers of transcripts for different physician specialties | |

| number of physicians | |

| number of transcripts with blank visit year | |

| number of visits per weighted year | |

| Diagnosis information | 69 predictors corresponding to the numbers of times being diagnosed with different diagnoses |

| number of diagnoses per weighted year | |

| number of different 3 digits diagnostics groups in the icd9 table | |

| number of different 3 digits diagnostics groups with medication | |

| Medication information | 23 predictors indicating the dose of active principle |

| number of prescriptions or the use of different medications | |

| number of medications without prescript | |

| number of active principles | |

| Lab result | 1 binary variable indicating whether a patient has any lab test or not |

| Smoking status | 1 binary variable indicating whether a patient smoked in the past |