A Markovian Incremental Stochastic Subgradient Algorithm

Abstract

A stochastic incremental subgradient algorithm for the minimization of a sum of convex functions is introduced. The method sequentially uses partial subgradient information and the sequence of partial subgradients is determined by a general Markov chain. This makes it suitable to be used in networks where the path of information flow is stochastically selected. We prove convergence of the algorithm to a weighted objective function where the weights are given by the Cesàro limiting probability distribution of the Markov chain. Unlike previous works in the literature, the Cesàro limiting distribution is general (not necessarily uniform), allowing for general weighted objective functions and flexibility in the method. keywords: Optimization algorithms, incremental subgradient method, stochastic optimization, Markov chains.

1 Introduction

Incremental subgradient algorithms [13, 15] can be efficient tools for the minimization of a sum of convex functions . These methods use only the subgradient of a summand of the objective function at a time when updating the decision variables and, therefore, need to somehow move along all summands in order to converge to a minimizer of . Several schemes have been used for the choice of the sequence of updates, starting with the most intuitive cyclic scheme [9] going through each summand exactly once before repeating any. The cyclic scheme can be used with random permutations following each full cycle and this can be beneficial in practice. Another possibility is to choose uniformly and randomly the summand to be considered, which also seems to favor convergence speed in practice when compared to a deterministic cyclic scheme.

A common application of incremental subgradients methods is in optimization in networks. In this case each summand is processed by a network agent and, in order to avoid extra communication and processing costs and to take the network topology into consideration, it is usually necessary to impose restrictions on which summands can be selected for processing after some is processed. Usually the sequence must follow the neighborhood structure of the network, that is, summand can be followed by summand if and only if node is connected to node . Under these circumstances, the randomizations of the processing order are not practically implementable without causing an unnecessary load in the network and, instead, a Markov chain can be used in order to select the next node from all neighbors of the current one [22, 8]. Another useful application of incremental methods is in computed tomography [14, 15, 4] where the combination of fast initial convergence and computationally simple iterations is favoured over several digits accuracy.

These Markovian methods have so far been proven to converge under the hypothesis of uniformity of the limiting probability distribution of the Markov chain. In the present paper we remove this restriction and prove convergence to the minimizer of an averaged objective function where each correspond to the Cesàro limiting probability of node in the Markov chain, as intuitively should happen since will be processed with relative frequency of .

Our setup allows e.g. to consider a Markov chain for which for some indexes , so that the corresponding functions play a role in the initialization and initial steps (to speed up the method) while they do not interfere with the final solution. It is worth a mention that the Markov chain is usually constructed/designed by the user of the method, so both and the transition probabilities can be chosen at the user convenience. Not only we provide convergence results for the case of general limiting probability distributions, but our method is more general than other Markovian incremental algorithms because it allows parallel processing of certain subsets of summands of the objective function. In this sense, the proposed algorithm has similarities with the class of string-averaging incremental subgradient methods [3, 1, 17, 16] for constrained convex optimization problems. Indeed, the proposed method seems to be the first instance of Markovian string-averaging technique in the literature. Interestingly, here again, computed tomography is an application for which string-averaging is useful [3, 17, 16].

Such a general setup brings some challenges for the convergence analysis, which demanded for the development of Lemmas 1 and 2 that are unparalleled in literature. We give more details in Remark 1. Still, the main convergence result given in Theorem 1 is quite conventional and does not impose restrictive / working assumptions. For example, Theorem 1 recovers Theorem 4.3 of [22] in the context considered in that paper.

The contributions of the present paper are, therefore, threefold: (a) it is shown that Markovian incremental stochastic subgradient algorithms converge under more general conditions on the Markov chain and on the stochastic gradient error than previously established in the literature; (b) the Markovian incremental stochastic subgradient algorithms are generalized to work with many parallel Markov chains in a string-averaging scheme, and (c) theoretical analysis of global convergence under mild assumptions is presented. We analyse both diminishing and constant stepsizes. Our approach unifies different algorithms found in literature, such as the incremental (cyclic) subgradient method, Markov randomized incremental subgradient method and incremental (randomized) subgradient method [13, 22, 8]. Moreover, we also provide experimental evidence of the usefulness of the method, although with no intention of pursuing benchmarking purposes.

The paper is organized as follows: Subsection 2.1 describes precisely the problem we are aiming to solve. Subsection 2.2 provides a complete description of the algorithm we propose; Section 3 is dedicated to the theoretical analysis; in Section 4 we examine a numerical example; final considerations are given in Section 5.

2 Proposed Algorithm

2.1 Problem formulation

We consider a network of agents that are indexed by , and we denote . The network has a static topology that is given by the directed graph , where is the set of links in the network. We have if agents and can communicate with each other. In this paper, the network goal is to solve the following optimization problem:

| (1) |

where

- (i)

-

- (ii)

-

are convex for all .

The literature on methods to solve the optimization problem (1) is very wide, so that not only incremental methods have been studied for this purpose. We can highlight, for example, distributed computation techniques [11, 23, 12, 7, 10] where each agent minimizes its own objective by exchanging information with other agents on the network. Distributed algorithms and optimization models have been studied for a long time, mainly due to potential in applications such as sensor networks [19] and distributed control [20]. One of the main disadvantages of distributed methods compared to the Markovian Incremental Stochastic Subgradient Algorithm (MISSA) that we propose here is that they require more sophisticated oracles (the minimizer instead of a stochastic subgradient) which might not always be available or be practical.

2.2 Algorithm description

The algorithm we propose in this paper, named as MISSA, is presented in this section. Consider Markov chains indexed by and we denote the index set by , so that for each we have that is a time-homogeneous Markov chain with state space and transition probabilities , where is called the transition probability matrix and is common to all Markov chains111 can be seen as a parameter of the method, to be selected by the user aiming at a desired Cesàro limiting distribution and/or transient states for accelerating the algorithm.. According to [2, Theorem 3.14], a simple re-ordering of the Markov states allow to obtain the following form for ,

| (2) |

where for each , the matrix is of dimension , is a matrix whereas is a matrix. The above structure of makes evident which states are recurrent [2]: the rows of corresponding to for a specific form a set of Markov states that are all recurrent and of same period [2]; we denote the period by and this set of Markov states by . The rows of corresponding to the matrix form a set of transient Markov states, which we denote by . Note that takes values on . As an example, consider a network composed of agents, so that , and Markov chains , whose probability matrices are given by a common matrix

In this example we have two irreducible sets of recurrent states , and a set of transient states . States in are periodic with period , while states in are of period . It is worth mentioning that is the transition probability matrix of an aperiodic Markov chain, where (where LCM means “least commom multiple”); in the example, so that gives the transition probabilities of an aperiodic chain, or equivalently we can say that the Markov chains are aperiodic. Figure 1 shows the network topology of this example.

Let us define as the initial probability distribution for , for all , i.e., . We assume that every agent is relevant to the algorithm in the sense that it is visited at infinitely many iterations with positive probability (otherwise the agent could be removed from network with no loss). Returning to the example above, this prevent us from setting, for example, because the states in would never be visited by any Markov chain. An example of valid initial distributions is , , and .

Some strong hypothesis, like the distribution converging to , are void in our setup - in fact, we do not require existence nor uniqueness of a limiting distribution for , . We resort to the limiting distribution in the sense of Cesàro [21]:

| (3) |

If we define then the definition given in (3) is equivalent to Since is aperiodic [2, Theorem 3.7, p.162], then converges, yielding and this in turn leads to

| (4) |

Now we can use equation (4) to obtain for all and any initial distribution , a Cesàro limit distribution as

| (5) |

Additionally, we define and with , and .

Summarizing the method we propose, at iteration , we compute independent subiterations by using a stochastic subgradient of and then we perform an averaging of these subiterations. It is useful to remark that although averaging is a possibility encompassed by our method, it is not mandatory. Indeed, if we recover the fully incremental method and still in this case our convergence results are novel because of the generality of the allowed Markov chain. The method Markovian Incremental Stochastic Subgradient Algorithm (MISSA) is detailed in Algorithm 1.

| (6) |

3 Convergence analysis

3.1 Assumptions

Notations: Let , then we will use the notations and . For any , is the smallest integer larger than or equal . For matrices , we use the induced norms and . We analyze the Algorithm 1 under the following assumptions.

Assumption 1.

is nonempty, convex and compact.

Assumption 1 and convexity of each over imply that the subgradients of are bounded over for each , i.e., there is such that for all and :

| (8) |

The stochastic error when computing a subgradient is denoted by . We define as the -algebra generated by , the subgradient errors and for all . In our analysis, we suppose that the second moments of the subgradient errors are bounded uniformly over the agents, conditionally on the available information until iteration (and represented by ).

Assumption 2.

There is a scalar sequence such that for all and with probability .

The main convergence result requires additional hypotheses on the bounds of the subgradient errors, which can be seen as a natural extension of the ones in [22, Theorem 4.3] to the case of periodic Markov chains.

Assumption 3.

3.2 Analysis

In the remainder of this section, we analyze the convergence of MISSA in order to solve problem (1) with a specific choice for scalars . We define for each ,

| (11) |

where is the Cesàro limit distribution given by equation (5). This means that we are establishing larger weights for the local functions associated to the agents with higher probability of use for long iterations , that is, when . As a consequence, we have that the transient states do not affect the objective function , because for all . Our main results are given in the following theorems. Define

Theorem 1.

Theorem 2.

Before we proceed to prove these theorems, we need two important auxiliary results. The first of these results shows that the averaged expected value over of any parcel , of the objective function at a given iteration becomes less dependent of the next state of the Markov chain as iterations proceed. For that, we define the vector as any row of such that the index of the row corresponds to some state in . Notice that, by the definition of in (4), all these rows are equal. With such definition, for any and ,

| (13) |

where is the vector with in the coordinate and zero in the others and denotes the -th column of .

Lemma 1.

Let k be a non-negative integer and consider another integer . Define for each , . For a given and a given , , there are positive scalars and such that, for any , we have

Proof.

For ease of notation in this proof we write (keeping fixed ):

If we note that , we can write

thus leading to

Then,

Notice that

where and are due to Lemma 5-(ii) (see Appendix). Therefore, by using (13), rearranging the terms and substituting above,

where we have used the compactness of and convexity of to guarantee the existence of such that , yielding

The fact that is a closed set of Markov states yields

hence

where . ∎

Notice that we select two iterations, namely and a previous one , and then base our argument in comparing iteration with iteration . The reason why we do so is that we need to perform the analysis on later iterations, that is, we need that both and (such as when comparing iteration against iteration in regular non-stochastic convergence analysis for subgradient methods), but this is not sufficient because the convergence in the markovian method also depends on analysing a long enough part of the chain, that is, the argument also requires in a specific way, as seen in the proof of Theorem 1.

The next lemma provides an important estimate for convergence analysis of the Algorithm 1. It gives means to establish an expected reduction in distance from the current point to any other given point with smaller objective function value as long as the stepsize is large enough, the stochastic error in subgradient computation is small and we have made sufficient passes over the Markov chain.

Lemma 2.

Proof.

Initially, due the non-expansivity of the projection , equation (7) and convexity of squared norm we have

Using the definition of subdifferential sets and remembering that , we have

and, alternatively

By Assumption 1 (and using (8)), we have

By analyzing the previous inequality over the iterates we have

By equation (14) and taking conditional expectations with respect to , we have

| (16) | ||||

For each define . Then, using Cauchy-Schwarz inequality and Assumption 1, we can estimate the second term from the right-hand side of (16), for each and , as

| (17) |

Now, we need to find an estimate for . To this end, we use (7) and non-expansivity of the projection to obtain, for each and

The law of iterated expectations, equation (6) and Assumptions 1-2 provide

| (18) |

which holds with probability . Combining (3.2) and (3.2), we can rewrite (16) as follows,

| (19) |

where in the last term we use Assumption 2. Since for any , we use again the law of iterated expectations and Assumption 2 to estimate for each and

and replacing in (3.2), we have with probability

Taking expectations, we have

| (20) |

As regards , we have for each and ,

| (21) |

Let us denote

and rewrite (3.2) as

Let us also denote

and then we have for each and ,

where the last equality follows from for all . Since , then we can write the preceding equation as

Now we can use Lemma 1 to ensure that there are positive scalars and such that, for each

Taking expectations we have

leading to

For simplicity, let us write

| (22) | ||||

where

| (23) |

By using (11) and (1)-(i), we can rewrite (22) as

| (24) |

At this juncture we move back to the evaluation of the term . The compactness of and convexity of guarantee the existence of such that a.s.; this and statement (i) of Corollary 1 yield

or, equivalently, , so that . Next we substitute this inequality in (23) and we use statement (ii) of Corollary 1 and the fact that the same as above provides a.s., and we obtain

and from (3.2),

where we defined and . The above and equation (3.2) lead to (2), completing the proof. ∎

We can now approach the proof of our main result.

Proof of Theorem 1.

Since is compact and is convex over (therefore, also continuous), the optimal set is nonempty, compact and convex. Define and () with . Notice that for all . Therefore, we can use Lemma 2 with this particular choice for . Taking , Lemma 2 provides

| (25) |

Define and

We can rewrite the inequality (3.2) as

| (26) |

We next show that . Notice that,

because and . Due to equation (12), we have

Therefore,

| (27) |

because . Notice that for all and thus

holds for all since . Hence, for all we have

and together with inequality (3.2) we conclude that

because . Furthermore, since , there is such that and thus

because , and . By assumption (10) and noticing that , we conclude that . Denoting , and , inequality (26) provides

We can use Lemma 3 (in the surely sense) to conclude that converges to a non-negative scalar and

Since and , we have

| (28) |

The function is bounded on (because is convex over and is bounded), thus

and from Fatou’s lemma we obtain

The two preceding inequalities imply that with probability . This relation, together with the continuity of and boundedness of , implies that with probability . ∎

Proof of Theorem 2.

Notice that Lemma 2 with gives

Recall that for all and that, from Assumption 1, we know that there is for all , . Then, letting (we will soon specify ), we have

We select as a function of the scalars , , , , , and in a way to (almost) minimize the error estimate as follows. Let us define

If , then is strictly convex and has the minimizer

Notice that if is small enough, then . For , we may instead use . Notice that , therefore, . Thus,

that is

| (29) |

where .

Now, assume for contradiction that

Then, for some and , we have that for all

| (30) |

Moreover, we can also assume that is large enough such that for . Putting this and (30) in (29), we get

| (31) |

Iterating and rearranging we get

| (32) |

which is a contradiction because the right-hand side is negative for large enough . If is not sufficiently small and we have , the result is proven using and following a similar reasoning. ∎

Remark 1.

If we consider ergodic Markov chains with uniform limiting distribution (i.e., for all ) and , then Theorem 1 recovers Theorem 4.3 of [22]. However, the evaluations behind our main result are different from the ones in [22]. The use of more general Markov chains makes several passages of the convergence analysis considerably more complex in comparison with the analysis of the method with ergodic Markov chains. We had to consider some extra terms in the proof of Lemma 2 (when compared e.g. with [22, Lemma 4.2] in the simplified scenario of and ), see equation (3.2), that concerns the inclusion of recurrent periodic and transient states and all subsequent equations. Corollary 1 and Lemma 5 given in the Appendix and all related evaluations are not required in simplified scenarios.

4 Experimental results

In this section, we report the numerical results of a simple example to illustrate a possible situation we can handle when using Algorithm 1: we consider minimizing the -norm of the residual associated to the linear system . We choose a matrix () with a high degree of sparsity and a feasible set given by box constraints. The nonzero entries of are given by:

The feasible set is such that

with , and denoting the th component of , and , respectively. The vectors and were chosen as

and

In order for the optimal set to be nonempty, we set a vector and compute . We have constructed the transition probability matrix

Following the notation of (2), we can note that and we have two irreducible sets of recurrent states: and . States in are of period , while states in are aperiodic () and thus, is the transition probability matrix of an aperiodic Markov chain. We test Algorithm 1 with two Markov chains, and , with initial distributions

respectively. By using equation (11) we compute the weights :

in such a way we have a correspondence between the entries of and the rows of : the larger is the norm of the -th row of , the larger is .

Define . We have iff . Thus, we can consider the equivalent optimization problem:

which has the same form that problem (1). In fact,

where represents the th row of . The subgradients of can be computed by the rule:

because (see, e.g., [6]), where is the sign function.

We compare the performance of Algorithm 1 with three other methods: the incremental (cyclic) subgradient method, Markov randomized incremental subgradient method and incremental (randomized) subgradient method ([13], [22] and [8]). All of them are particular cases of the Algorithm 1 when (i.e., when we use just one Markov chain), with specific transition probability matrices. Note that these methods must consider subgradients of . For ease of notation, we label the methods – Algorithm 1 (MISSA), Markov randomized incremental subgradient method, incremental (cyclic) subgradient method and incremental (randomized) subgradient method – by , , and respectively. The transition probability matrix for , denoted by , is given by , , and for all other entries. The transition probability matrix for , denoted by , is given by for all . Moreover, the initial distributions for and are and , respectively. For the method , the transition probability matrix (or all matrices in [22]), denoted by , must satisfy some assumptions that we do not consider in Algorithm 1, among them, irreducibility, aperiodicity and uniform limiting distribution. In our tests, we consider one of the suggested rules in [22] (equal probability scheme):

where is the set of neighbors of an agent . We set , , , , , and , besides an initial distribution equals to , aiming to get higher probabilities of reaching agent (the row of with larger norm) in the initial iterations.

Regarding the stochastic errors of the subgradients for the agent , we tested six different possibilities in order to study the effect of the Assumption 2 and (10) (see similar assumptions for and in [22]) on the performance of the methods. In what follows, denotes the uniform distribution in the interval and the normal distribution with zero mean and unit variance. In all cases, and , , , , are independent random variables with distributions given in Table 1.

| Tests | Description (for any and ) |

|---|---|

| Test | for all . |

| Test | for all . |

| Test | for all . |

| Test | for all . |

| Test | for all . |

| Test | for all . |

We initially present results using a diminishing stepsize rule. The initial guess was chosen as for all methods. We run all methods during iterations. The stepsizes for the algorithms , and was chosen as in Theorem 4.3 in [22] and are similar to the sequence (12) adopted for (with the exception of the periodicity ). The parameters and were tuned for each method, with and and running the methods for test (without random errors). Table 2 shows the parameters used in all tests for each method.

| Method | ||

|---|---|---|

All tests were run on a computer with an Intel(R) Core(TM) i3-4005U CPU @ 1.70GHz 4 processor and GB of RAM. We run in parallel, following the procedure of allocating a thread for each Markov chain. It is natural to expect the CPU time per iteration to be greater for than for , and . Although the subiterations in (6) are computed in parallel for (in our implementation, we use the std::thread library (C11) and the code was compiled by the g compiler of GCC – version 7.5.0) we need to compute, as we can see in (7), the average of the subiterations before calculating the projection. The average is not required for the other methods, as they only use one Markov chain, i.e., . For example, in test , the CPU time per iteration for is about e seconds, while for , and it is approximately e seconds.

|

|

|

| (a) Test | (b) Test | (c) Test |

|

|

|

| (d) Test | (e) Test | (f) Test |

|

|

|

| (a) Test | (b) Test | (c) Test |

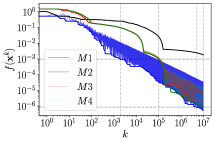

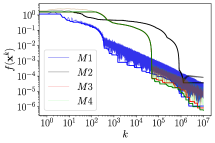

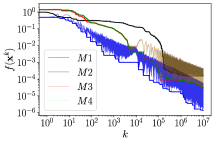

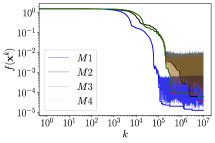

Figure 2 illustrates the behavior of for the methods , , and in tests from to by using diminishing stepsizes. For all methods, we draw a thicker line that follows the graph , representing the smallest obtained up to iteration . In Fig. 2–(a), we can notice that produces a sequence such that decreases faster in the initial iterations in comparison to the other methods. When observing a longer time horizon, and produce such that are closer to the values obtained by . Apparently, the choice of does not produce good results for . Other neighborhood schemes could be explored, or even other transition matrices (such as min–equal neighbor scheme or weighted Metropolis–Hastings scheme that also satisfy Assumption 5 in [22]). For , and , we draw a dashed horizontal line for the first occurrence of e (note that these lines are very close). For , this occurs at iteration and seconds of CPU time. For , this occurs at iteration and seconds of CPU time. For M4, this occurs at iteration and seconds of CPU time. Dashed vertical lines passing through such values of are also shown in the Fig. 2–(a). In addition, we insert a dashed horizontal line at the smallest value of obtained by during all optimization process, namely e, and a vertical dashed line in the iteration where this occurs, namely . Such solution was obtained with CPU time equal to seconds. A horizontal dashed line passing through the first occurrence of for the method is also included. This occurs with e at iteration with CPU time equal to seconds.

In Fig. 2–(b), a similar behavior occurs for the initial iterations: generates a sequence such that decreases faster in comparison to the values obtained by the other methods. However, after approximately iterations, and produce sequences with smaller values for compared to the values generated by . At the end of iterations, and reach values of slightly smaller than those produced by .

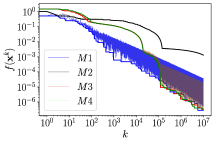

Note that tests and are perfectly compatible with what is predicted by Theorem 1 for all considered methods –. In order to explore different types of random errors, tests from to shown in Fig. 2 (c)–(f), unlike tests and , aim to visualize the behavior of incremental subgradient methods when Assumption 3 does not hold. Such situations are interesting because they can be related to practical contexts where the error does not tend to zero. Furthermore, they can be studied from the point of view of approximating the sequence to some neighborhood of when we use a constant stepsize strategy and adopt in Assumption 2. Note that tests and have the same type of error, however the error in test is one order of magnitude smaller. In this sense, the value of can be chosen smaller in test and, by Theorem 2, a better error bound can be obtained. Despite the difficulties imposed on tests and , which clearly impact the performance of the methods running with diminishing stepsizes, achieved an interesting performance being able to provide more accentuated decrease in the objective function compared to the other methods. In both cases, generates a sequence such that is decreased up to a certain number of iterations, after which the sequence produces less oscillation for and stabilizes. Such evidence suggests that MISSA benefited from the action of the Markov chains used, allowing indexes of rows of with higher norm (in the subgradient calculation) to be chosen with higher frequency over the iterations, and this might have accelerated the method.

In tests and shown in Fig. 2 (e)–(f), all methods performed better than in tests and . In test , the curve with the smallest values obtained for with the sequence generated by remains below the other curves generated by , and during the entire execution. In test , similarly to what occurred in test , has better performance in the initial iterations. After about iterations, methods and generate with smaller compared to the values obtained by . However, until the end of the execution, all three methods achieve similar values for .

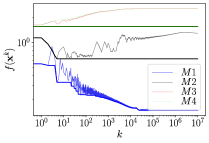

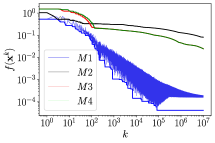

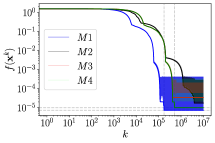

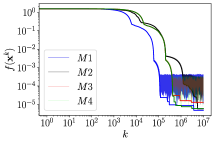

Figure 3 shows the performance of the methods during iterations using a constant stepsize in three of the tests described in Table 1, namely tests , and . We choose for each method, following the criterion of using the one that generates the best decrease for until the end of the iterations in test . In all tests, seems to approach a neighborhood of faster compared to the other methods. In test , we compare the minimum value reached by for the methods and and a dashed vertical line in the iteration where such a value occurs. For , this occurs with e at iteration and seconds of CPU time. For , this occurs with e at iteration and seconds of CPU time.

5 Conclusions

In this paper, we have introduced a new method for minimizing a weighted sum of convex functions based on incremental subgradient algorithms with subgradients chosen through Markov chains. No special condition is imposed on the Markov chain, allowing for transient states and periodicity, which makes MISSA flexible enough as to contain other methods, as the incremental cyclic subgradient method and the other methods considered in Section IV. This paves the way for exploring new situations that might benefit incremental methods. Certain large-scale optimization problems can be addressed with the method we have presented, especially taking advantage of the flexibility of parallel processing. Future work may move toward exploring the inclusion of transient states in the construction of the transition probability matrix and using them over a given time horizon (which is established through their own transition probabilities) in order to accelerate the convergence without changing the objective function . Also interesting is to investigate how theoretical convergence rates can be optimized and how to build more efficient Markov chains for incremental methods.

Acknowledgment

This work was supported by CNPq Grant 310877/2017-2, CNPq-Universal 421486/2016-3, FAPESP 2017/20934-9 and FAPESP-CEPID 2013/07375-0.

Appendix A Preliminary results

In this appendix we collect preliminary claims used in the convergence analysis and, when necessary, their proofs.

Lemma 3.

(Robbins-Siegmund, [18] - Lemma 11, p.50) Let be a probability space and a sequence of sub- algebras of . Let , and be non-negative random sequences and let be a deterministic sequence. Suppose that , and

holds with probability 1. Then, with probability 1, the sequence converges to a non-negative random variable and .

Proposition 1.

Let and consider the linear system . If for a given initial condition the sequence converges to zero, then there exist , such that

Proof.

Consider the subset of comprised of all initial conditions such that the solution of the linear system converges to zero. is a vector subspace because the system is linear, and it is -invariant because the system is time-invariant so its solution starting from any such converges to zero. Let us “restrict” into by constructing a (possibly) lower dimensional linear mapping such that for all . The linear system , , constructed in this way is asymptotically stable. From the equivalence between asymptotic and exponential stability given in [5, Theorem 8.4] we have that there exist positive constants and such that

This yields

for all . ∎

Lemma 4.

Consider an aperiodic finite state space Markov chain and let be the limiting distribution for a given initial distribution . Then, there exist such that for any initial distribution we have that converges exponentially to in the sense that

where .

Proof.

The existence of for aperiodic Markov chains with finitely many states follow directly from the computation of via Theorem 5.3.2 and Corollary 2.11 in [2]: We shall write to emphasize the dependence on the initial distribution. Then, we have that as , and since , Proposition 1 (taking ) provides

where may depend on (notice that the result in Proposition 1 does not depend on the choice of the norm). We want to obtain a bound that is independent of choice of . For that, let be the canonical basis of . Again, Proposition 1 ensures that there are such that

| (33) |

where are parameters linked with the initial distribution . Further, since and , then we have for any

Therefore, by the previous equality and equation (33), we have

Since was taken arbitrarily, the result follows taking and . ∎

Corollary 1.

There exist and such that

(i) and

(ii) .

Proof.

Lemma 4 applies to because the -step chain is aperiodic. The limiting probability of a transient state is always zero, that is, , and Lemma 4 establishes that convergence is exponentially fast (with uniform parameters and ), which leads to (i). Similarly, converges exponentially fast to a limiting constant , and , and some algebra leads to (ii). ∎

We point out that the Markov chain with transition probability matrix is an aperiodic chain [2, Theorem 3.7] and in this case can be computed via Theorem 5.3.2 and Corollary 2.11 in [2].

Lemma 5.

Consider a time-homogeneous Markov chain with finite state space and probability transition matrix . Let be the period of this chain, with , , and . Then, there exist such that

- (i)

-

;

- (ii)

-

for all with .

Proof.

(i) We denote and thus

as and by noticing that , we can apply Proposition 1 and Lemma 4 and obtain geometric convergence for the sequence for any . By observing that is the -th row of the matrix and is the -th row of , then is the -th row of the matrix . Bringing this and Lemma 4 together yields

where and . The result follows by noticing that .

(ii) It is sufficient note that

where we use (i) and for all . ∎

References

- [1] Yair Censor and Alexander J Zaslavski. String-averaging projected subgradient methods for constrained minimization. Optimization Methods & Software, 29(3):658–670, 2014.

- [2] E. Cinlar. Introduction to Stochastic Processes. Dover Books on Mathematics Series. Dover Publications, Incorporated, 2013.

- [3] Elias S. Helou, Yair Censor, Tai-Been Chen, I-Liang Chern, Álvaro R. De Pierro, Ming Jiang, and Henry H.-S. Lu. String-averaging expectation-maximization for maximum likelihood estimation in emission tomography. Inverse Problems, 30(5):055003, 2014.

- [4] Gabor T Herman. Fundamentals of computerized tomography: image reconstruction from projections. Advances in Computer Vision and Pattern Recognition. Springer-Verlag London, 2009.

- [5] J.P. Hespanha. Linear Systems Theory. Princeton University Press, 2009.

- [6] Jean-Baptiste Hiriart-Urruty and Claude Lemaréchal. Convex Analysis and Minimization Algorithms I. Fundamentals., volume 305 of A Series of Comprehensive Studies in Mathematics. Springer-Verlag, Berlin, 1993.

- [7] D. Jakovetić, J. Xavier, and J. M. F. Moura. Fast distributed gradient methods. IEEE Transactions on Automatic Control, 59(5):1131–1146, May 2014.

- [8] Bjorn Johansson, Maben Rabi, and Mikael Johansson. A randomized incremental subgradient method for distributed optimization in networked systems. SIAM Journal on Optimization, 20(3):1157–1170, 2010.

- [9] V M Kibardin. Decomposition into functions in the minimization problem. Avtomatika i Telemekhanika, (9):66–79, 1979.

- [10] A. Nedić and A. Olshevsky. Distributed optimization over time-varying directed graphs. IEEE Transactions on Automatic Control, 60(3):601–615, March 2015.

- [11] A. Nedić and A. Ozdaglar. Distributed subgradient methods for multi-agent optimization. IEEE Transactions on Automatic Control, 54(1):48–61, Jan 2009.

- [12] A. Nedić, A. Ozdaglar, and P. A. Parrilo. Constrained consensus and optimization in multi-agent networks. IEEE Transactions on Automatic Control, 55(4):922–938, April 2010.

- [13] Angelia Nedić and Dimitri P Bertsekas. Incremental subgradient methods for nondifferentiable optimization. SIAM Journal on Optimization, 12(1):109–138, 2001.

- [14] Elias Salomão Helou Neto and Alvaro Rodolfo De Pierro. Convergence results for scaled gradient algorithms in positron emission tomography. Inverse problems, 21:1905, 2005.

- [15] Elias Salomão Helou Neto and Álvaro Rodolfo De Pierro. Incremental subgradients for constrained convex optimization: a unified framework and new methods. SIAM Journal on Optimization, 20(3):1547–1572, 2009.

- [16] R. M. Oliveira, E. S. Helou, and E. F. Costa. String-averaging incremental stochastic subgradient algorithms. Optimization Methods and Software, 34(3):665–692, 2019.

- [17] Rafael M Oliveira, Elias S Helou, and Eduardo F Costa. String-averaging incremental subgradients for constrained convex optimization with applications to reconstruction of tomographic images. Inverse Problems, 32(11):115014, 2016.

- [18] Boris T Polyak. Introduction to optimization. 1987. Optimization Software, Inc, New York.

- [19] M. Rabbat and R. Nowak. Distributed optimization in sensor networks. In Third International Symposium on Information Processing in Sensor Networks, 2004. IPSN 2004, pages 20–27, April 2004.

- [20] S. S. Ram, V. V. Veeravalli, and A. Nedic. Distributed non-autonomous power control through distributed convex optimization. In IEEE INFOCOM 2009, pages 3001–3005, April 2009.

- [21] Dieter Spreen. On some properties of the cesàro limit of a stochastic matrix. Linear Algebra and its Applications, 41:81–91, 1981.

- [22] S Sundhar Ram, A Nedić, and Venugopal V Veeravalli. Incremental stochastic subgradient algorithms for convex optimization. SIAM Journal on Optimization, 20(2):691–717, 2009.

- [23] S Sundhar Ram, A Nedić, and Venugopal V Veeravalli. Distributed stochastic subgradient projection algorithms for convex optimization. Journal of optimization theory and applications, 147(3):516–545, 2010.