Density Sharpening: Principles and Applications to Discrete Data Analysis

Deep Mukhopadhyay

deep@unitedstatalgo.com

Abstract

This article introduces a general statistical modeling principle called “Density Sharpening” and applies it to the analysis of discrete count data. The underlying foundation is based on a new theory of nonparametric approximation and smoothing methods for discrete distributions which play a useful role in explaining and uniting a large class of applied statistical methods. The proposed modeling framework is illustrated using several real applications, from seismology to healthcare to physics.

Keywords: Density sharpening; distributions; LP-Fourier analysis; Explanatory goodness-of-fit; Jaynes’ dice problem; Compressive ; Data-efficient learning.

1 Principles of Statistical Model Building

‘Part of a meaningful quantitative analysis is to look at models and try to figure out their deficiencies and the ways in which they can be improved.’

—-Nobel Lecture by Lars Peter Hansen (2014)

Scientific investigation never happens in a vacuum. It builds upon previously accumulated knowledge instead of starting from scratch. Statistical modeling is no exception to this rule.

Suppose we are given random samples from an unknown discrete distribution . Before we jump into the statistical analysis part, the scientist provided us a hint on what might be an initial believable model for the data: ‘from my years of experience working in this field, I expect the underlying distribution to be somewhat close to .’ This information came with a disclaimer: ‘don’t take too seriously as it is only a simplified approximation of reality. Use it with caution and care.’

The general problem of statistical learning then aims to address the following questions: Whether the ‘shape of the data’ is consistent with the presumed model-0. If it is not, then what is it? How is it different from ? Revealing new hidden pattern in the data is often the most essential statistical modeling task in science and engineering. Of course, ultimately, the aim is to search for a rich class of sensible models in an automatic and faster manner, by appropriately changing the misspecified . Knowing how to change the anticipated is the first step towards scientific discovery that allows scientists to re-evaluate alternative theories to explain the data. If we succeed at this, it will provide a mechanism to build “hybrid” knowledge-data integrated models, which are far more interpretable than classical fully data-driven nonparametric models. Full development of these ideas requires a new conceptual framework and mathematical tools.

Organization. Section 2 introduces a new family of nonparametric approximation and smoothing techniques for discrete probability distributions, which is built on the principle of ‘Density Sharpening.’ Section 3 highlights the role of the proposed theoretical framework in the development of statistical methods that is rich enough to include traditional as well as contemporary statistical methods: starting from as simple as one sample Z-test for a proportion to as sophisticated as compressive chi-square, -sharp negative Binomial distribution, universal goodness-of-fit program, relative entropy estimation, Jaynes dice problem, sample-efficient learning of big distributions, etc. The paper ends with a discussion and conclusion Section 4. Additional applications and methodological details are deferred to the Supplementary Appendix to ensure the smooth flow of the main ideas.

2 Density Sharpening: Model and Mechanism

We describe a method of nonparametric approximation of discrete distribution by sharpening the initially assumed . The theory is remarkably simple, yet general enough to be vastly applicable in many areas beyond density estimation, as described in Section 3. Here is a bird’s eye view of the core mechanism, which is a three-stage process. Stage 1. Model-0 elicitation: The modeler starts a suitable by using his/her experience or subject-matter knowledge. Often a particular parametric form of is selected keeping convenience and simplicity in mind.

Stage 2. Exploratory uncertainty analysis: Assess the uncertainty of the presumed model , in a way that can explain ‘why and how’ the assumed model-0 (i.e., ) is inadequate for the data.

Stage 3. Coarse-to-Refined density: Incorporate the ‘learned’ uncertainty into to produce an improved model that will eliminate the incompatibility with the data.

The required theory is developed in the next few sections, which heavily relies on the following notation: let be a discrete variable with probability mass function , cumulative distribution function , and mid-distribution function . The associated quantile function will be denoted by for . By we mean the set of all square integrable functions with respect to the discrete measure , i.e, for a function : . The inner product of two functions and in will be denoted by . Expectation with respect to will be abbreviated as .

2.1 Learning by Comparison: -Sharp Density

We introduce a mechanism for nonparametrically estimating the density of by comparing and sharpening the presumed working model .

Definition 1 (-Sharp Density).

For a discrete random variable , we have the following universal density decomposition:

| (2.1) |

where the is defined as

| (2.2) |

The function is called ‘comparison density’ because it compares the assumed with the true and it integrates to one:

For brevity’s sake, we will often abbreviate as throughout the article.

Remark 1 (The philosophy of ‘learning by comparison’).

The density representation formula (2.1) describes a way of building a general by comparing it with the initial . The -modulated class of distributions is constructed by amending (instead of abandoning) the starting imprecise model .

Remark 2 (-sharp density).

Eq. (2.1) provides a formal statistical mechanism for sharpening the initial vague using the data-guided perturbation function . For this reason, we call the improved the ‘-sharp’ density.

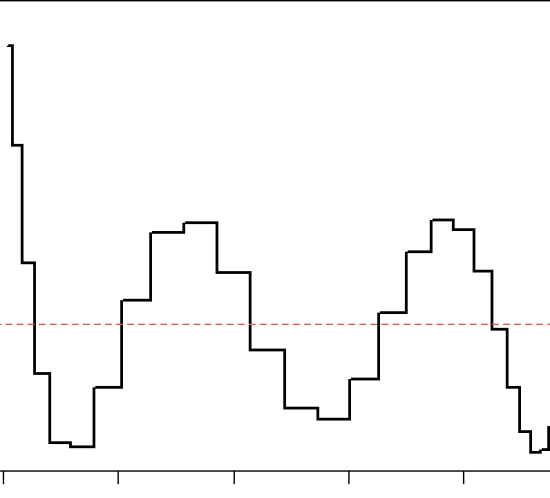

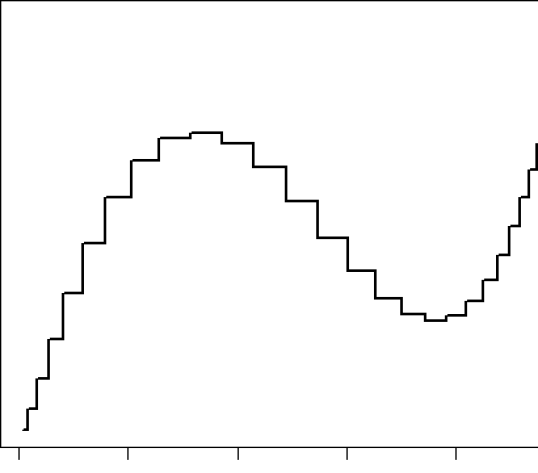

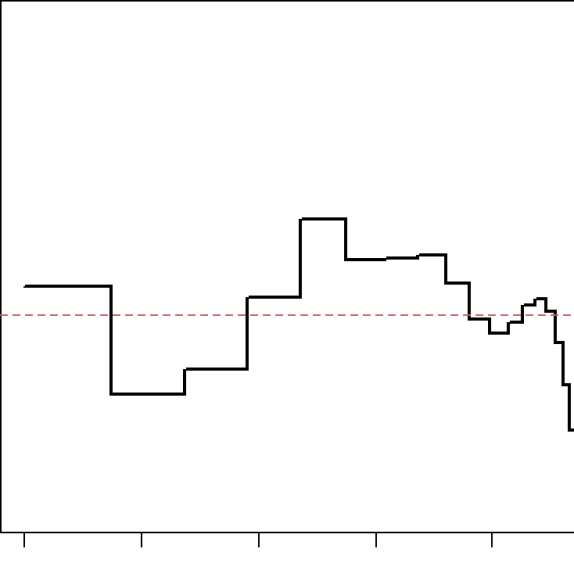

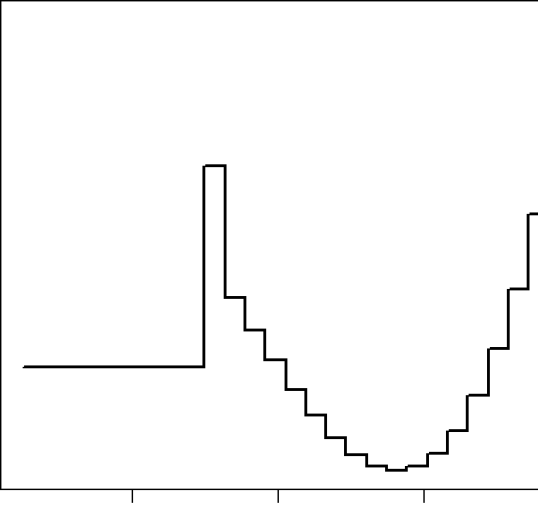

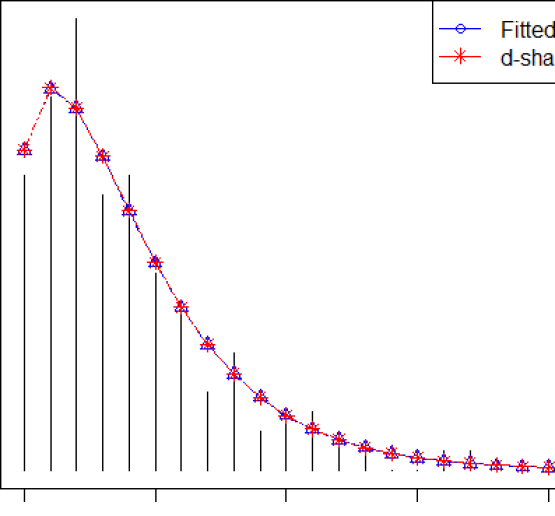

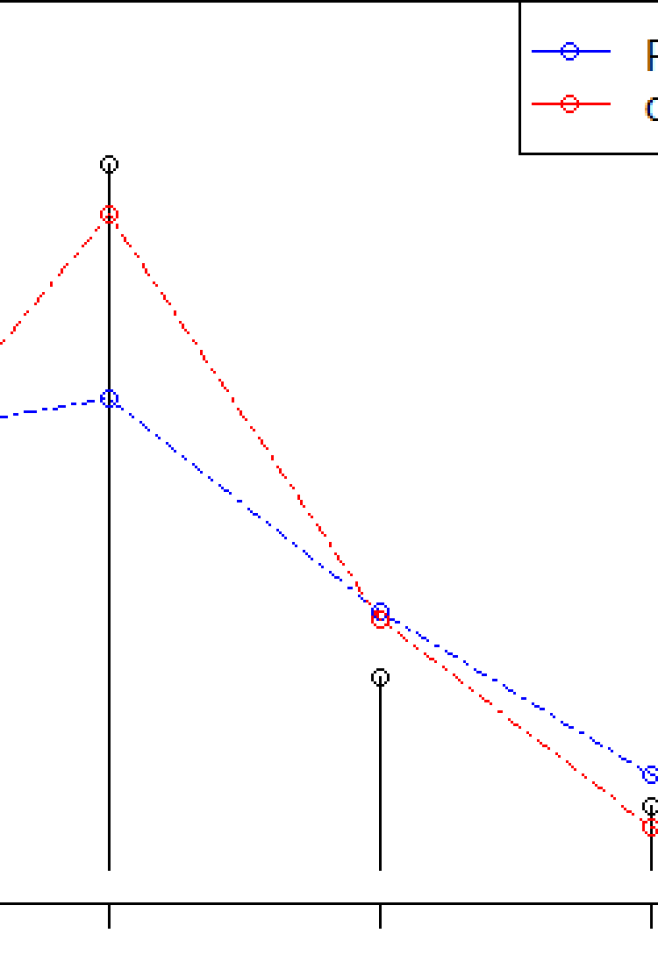

Example 1 (Earthquake Data).

We are given annual counts of major earthquakes (magnitude 6 and above) for the years 1900-2006. It is available in the R package astsa. Seismic engineers routinely use negative binomial distribution for modeling earthquake frequency (Kagan and Jackson, 2000, Kagan, 2010). The best fitted negative binomial (NB) with ( and ) is shown in Fig 1, which we take as our rough initial model . From the figure, it is clearly evident that the conventional NB distribution is unable to adequately capture the shape of the earthquake count data. Model uncertainty quantification. For earthquake engineers it is of utmost importance to determine the uncertainty of the assumed NB model (Bernreuter, 1981). The problem of uncertainty quantification is the holy grail of earthquake science due to its importance in estimating risk and in making an accurate forecast of the next big earthquake. The comparison density captures the uncertainty of the assumed NB model. The left plot in Fig 1 displays the estimated for this data, which reveals the nature of deficiency of the base NB model. A robust nonparametric method of estimating from data will be discussed in the subsequent sections. But before going into the nonparametric approximation theory, we will spend some time on its interpretation.

Interpretable Exploratory learning. In our model (2.1), plays the role of a data-driven correction function, measuring the discrepancy between the initial and the unknown . Thus, the non-uniformity of immediately tells us that there’s something more in the data than what was expected in light of . In fact, the shape of reveals the nature of the most prominent deviations between the data and the presumed —which, in this case, are bimodality and presence of heavier-tail than anticipated NB distribution.

Remark 3 (Role of ).

The comparison density performs dual functions: (i) its graph acts as an exploratory diagnostic tool that exposes the unexpected, forcing decision makers (e.g., legislators, natural security agencies, local administrations) to think outside the box: what might have caused this bimodality? how can we repair the old seismic hazard forecast model so that it incorporates this new information? etc. (ii) it provides a formal process of transforming and revising an initially misspecified model into a useful one. The red curve in the right panel is obtained by multiplying (perturbing) the NB pmf with the estimated comparison density, obeying the density representation formula Eq. (2.1).

2.2 LP-Fourier Analysis

The task is to nonparametrically approximate to be able to apply the density sharpening equation (2.1). We approximate by projecting it into a space of polynomials of that are orthonormal with respect to the base measure. How to construct such a system of polynomials in a completely automatic and robust manner for any given ? In the section that follows, we discuss a universal construction.

2.2.1 Discrete LP-Basis

We describe a general theory of constructing LP-polynomials—a new class of robust polynomials that are a function of (not raw ) and are orthonormal with respect to user-specified discrete distribution .

Step 1: Define the first-order LP-basis function as standardized mid-distribution transform:

| (2.3) |

Verify that and , since and .

Step 2: Apply a weighted Gram-Schmidt procedure on to construct a higher-order LP orthogonal system with respect to measure

where is the Kronecker delta function and the highest-degree of the LP-polynomials is always less than the support size of the discrete . For example, if is binary, one can construct at most LP-basis function; see Section 3.1. Fig 2 shows the top four LP-basis functions for the earthquake data with as . Here, we have displayed them in a unit interval as a function of , denoted by . Notice the typical shape of these custom-constructed discrete orthonormal polynomials: globally nonlinear (linear, quadratic, cubic, and so on) and locally piecewise-constant with unequal step size.

Remark 4 (Role of LP-coordinate system in unification of statistical methods).

LP-bases play a unique role in statistical modeling—they provide an efficient coordinate (data-representation) system that is fundamental to developing unified statistical algorithms.

2.3 The Model

Definition 2 (LP-canonical Expansion).

Expand comparison density in the LP-orthogonal series

| (2.4) |

where the th LP-Fourier coefficient satisfies the following identity:

| (2.5) |

A change-of-basis perspective: The conventional way to represent a discrete distribution is through indicator basis (histogram representation):

| (2.6) |

where is the domain size (number of unique values) of the empirical distribution . In (2.4), we have performed a “change of basis” from the amorphous indicator-basis to a more structured LP-basis , where the expansion coefficients act as the coordinates of relative to assumed :

For that reason, one may call these coefficients the discrete LP-Fourier Transform (LPT) of relative to .

Definition 3.

denotes a class of distributions with the following representation:

| (2.7) |

obtained by replacing (2.4) into (2.1). Here stands for Density-Sharpening of using -term LP-series approximated . is a class of nonparametrically-designed parametric models that are flexible enough to capture various shapes of discrete , like multi-modality, excess-variation, long-tailed, and sharp peaks.

To estimate the unknown coefficients of the model, note the following important identity:

| (2.8) | |||||

This immediately leads to the following “weighted mean” estimator:

| (2.9) |

Using standard empirical process theory (Csörgő, 1983, Parzen, 1998) one can show that the limiting distribution of sample LP-statistic is i.i.d , under the null hypothesis . Thus one can quickly obtain a sparse estimated model by retaining only the ‘significant’ LP-coefficients, which are greater than .

2.4 LP-Maximum Entropy Analysis

To ensure non-negativity, we expand (instead of as we have done in Eq. (2.4)) in LP-Fourier series, which results in the following exponential model:

| (2.11) |

where This model is also called the maximum-entropy (maxent) comparison density model because it maximizes the entropy (flattest possible; thus promotes smoothness) under the following LP-moment constraints:

| (2.12) |

LP-moments are ‘compressed measurements’ (linear combinations of observed data; verify from (2.9)), which are sufficient statistics for the comparison density .

Definition 4 (Maxent model).

Earthquake Data Example. The estimated maxent model for the earthquake distribution is given by

| (2.14) |

whose shape is almost indistinguishable from the LP-Fourier estimated p.m.f. (2.10).

3 Applications in Statistical Modelling

We describe how the general principle of ‘density sharpening’ acts as a unified framework for the analysis of discrete data with a wide variety of applications, ranging from basic introductory methods to more advanced statistical modeling techniques.

3.1 One-sample Test of Proportion

Given samples from a binary , the one-sample proportion test is concerned with testing whether the population proportion is equal to the hypothesized proportion . We approach this problem by reformulating it in our mathematical notation:

Step 1. We start with the model

| (3.1) |

where the null model for .

Step 2. We rewrite the original hypothesis in terms of LP-parameter as .

Step 3. We derive an explicit formula for . It’s a two step process: First, we need the analytic expression of the LP-basis

| (3.2) |

We then apply formula (2.9) to deduce:

| (3.3) |

Step 4. A remarkable fact is that the test based on (3.3) exactly matches with the classical Z-test, whose null distribution is: as . This shows how the LP-theoretical device provides a transparent first-principle derivation of the one-sample proportion test, by shedding light on its genesis.

3.2 Expandable Negative Binomial Distribution

We will focus now on one important special case of maxent family of distributions (2.13), where the base measure is taken to be a negative Binomial (NB) distribution.

| (3.4) |

note that the basis functions are specially-designed LP-orthonormal polynomials associated with the base measure . We call (3.4) the th-order expandable NB distributions, denoted by XNB(m). A few practical advantages of XNB(m) distributions are: the computational ease they afford for estimating parameters; their compactly parameterizable yet shape-flexible nature; and, finally, their ability to provide explanatory insights into how is different from the standard NB distribution. Due to their simplicity and flexibility, they have the potential to be a ‘default choice’ for modeling count data. We have already seen an example of XNB-distribution in (2.14) in the context of modeling the earthquake distribution. We now turn our attention to two further real-data examples.

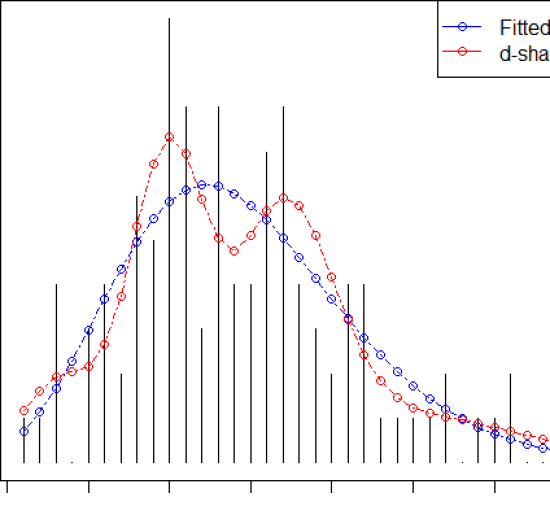

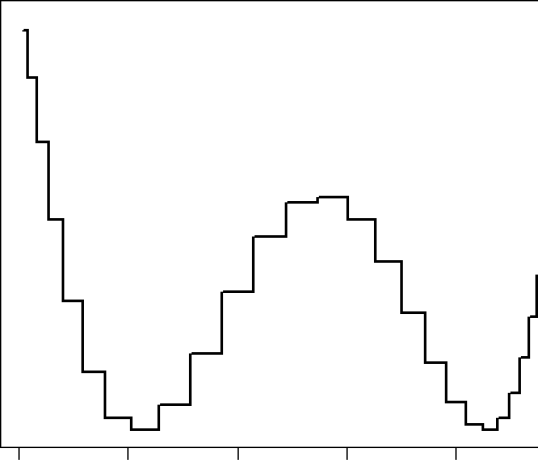

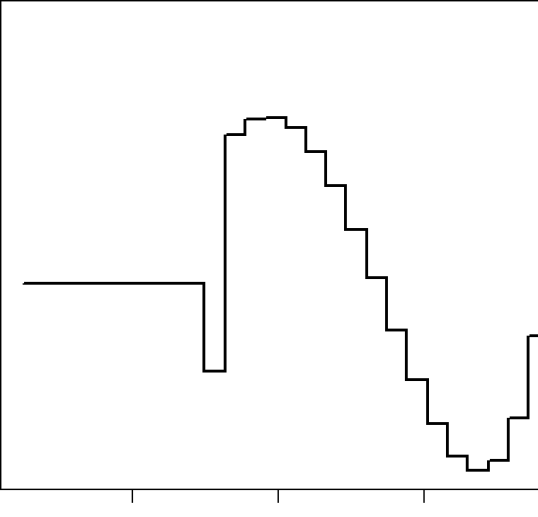

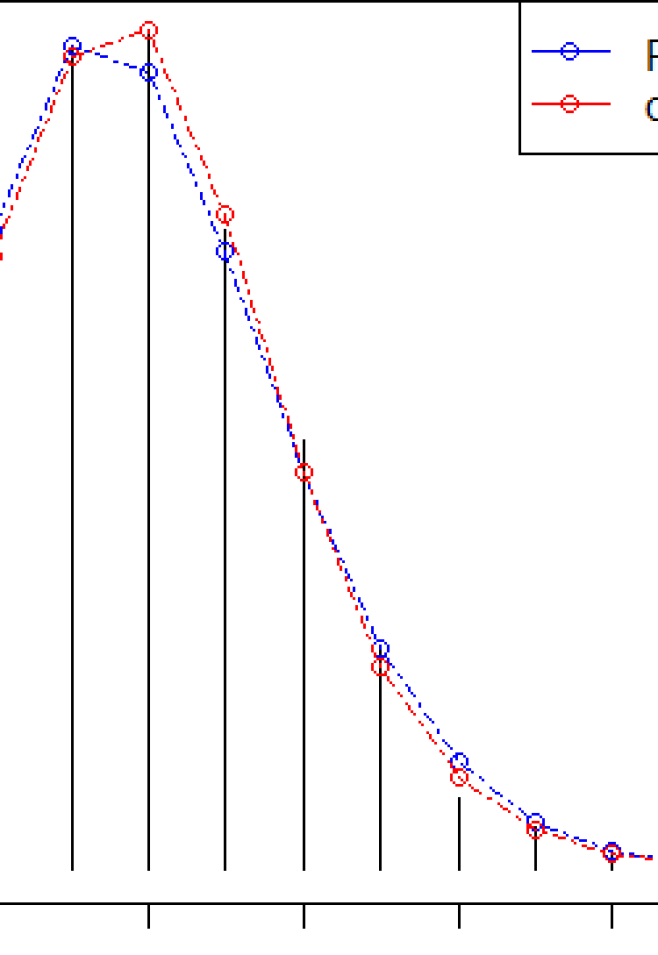

Example 2 (NMES 1988 Data).

This is a part of the US National Medical Expenditure Survey (NMES) conducted in 1987 and 1988. It is available in the R-package AER. We have observations of a discrete random variable which denotes how many times an individual, aged 66 and covered by Medicare, visited physician’s office. As displayed in the Fig. 3 boxplot, the distribution has a large support size (varies between and ), with some regions being extremely data-sparse.

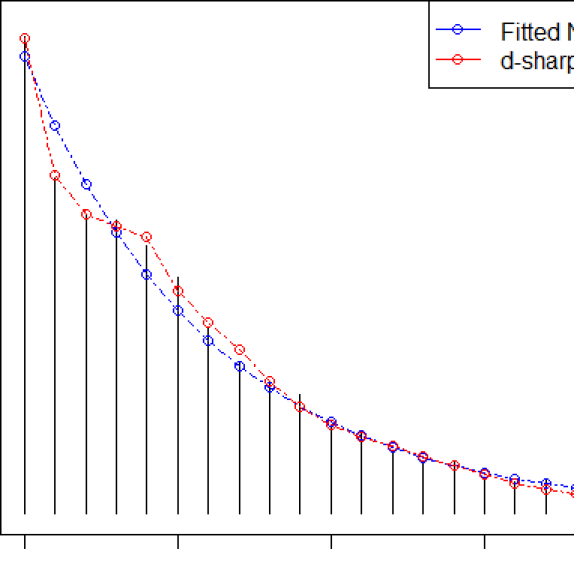

The blue curve in the top left plot shows the , where the parameters are maximum-likelihood estimates. Next, we estimate the LP-maxent , using the theory of Sec. 2.4. At this point, it is strongly advisable to pay attention to the shape . Why? Because, it efficiently extracts and exposes ‘unanticipated’ aspects in the data that cannot be explained by the initial NB distribution. The bottom-left Fig. 3 immediately reveals a few things: (i) NB underestimates the probability at ; (ii) it overestimates the probability mass around and ; (iii) there seems to be an excess probability mass (‘bump’ structure) around ; (iv) NB clearly has a shorter tail than what we see in the data—this can be seen from the sharply increasing right tail of the comparison density. To better understand the tail-behavior, we have simulated samples from and contrasted the two boxplots in the top-right panel, which strongly indicates the long-tailedness of relative to NB distribution. Any reader will agree that without the help of , even experienced eyes could have easily missed these subtle patterns. Finally, multiply by the , following eq. (3.4), to get the estimated XNB distribution—the red p.m.f curve, shown in the bottom-right panel of Fig. 3.

Example 3 (Computer Breaks Data).

We are given the number of times a DEC-20 computer broke down at Open University in each of consecutive weeks of operation, starting in late 1983. The data shows positive skewness with a slightly longer tail; see Fig. 16 in the appendix. The mechanics of XNB modeling proceed as follows: (i) We start by estimating the parameters of , which in this case are MLE-fitted (one can use any other method of estimation) . (ii) The next step is estimation of , which in this case is just the uniform distribution—none of the LP-maxent parameters were large enough to be selected. This is depicted in the left panel of supplementary Fig. 16. This graphical diagnostic indicates that the initial fits the data satisfactorily; no repairing is necessary. (iii) Accordingly, our ‘density sharpening’ principle returns the as the final model, which is simply the starting parametric model .

It is interesting to contrast our finding with Saulo et al. (2020), where the authors fit a highly specialized nonparametric discrete distribution to this data. The beauty of our approach is that it performs nonparametric correction (through ) only when it is warranted. When the reality is already simple, we don’t complicate it unnecessarily.

3.3 and Compressive-

Given a random sample of size from the unknown population distribution , chi-square goodness-of-fit statistic between the sample probabilities and the expected can be re-written as follows:

| (3.5) |

By applying Parseval’s identity on the LP-Fourier expansion of , we have the following important equality:

| (3.6) |

where is the number of unique values in our sample . This shows that chi-square information statistic is a “saturated” raw-nonparametric measure with components.

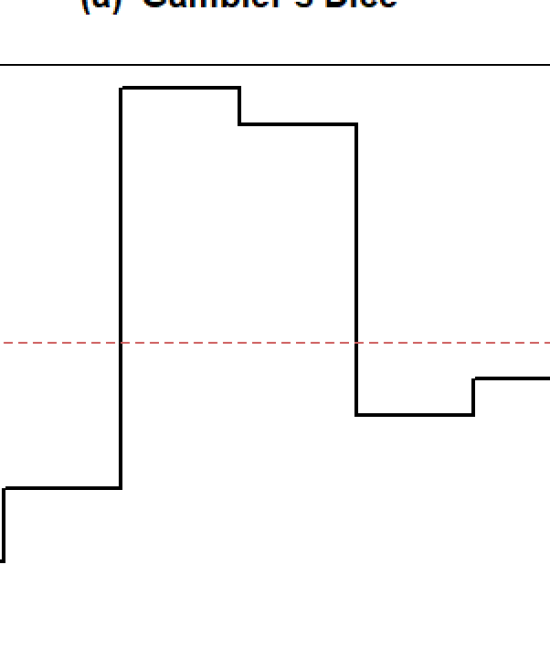

Example 4 (The Gambler’s Die).

A gambler rolls a die times and gets the following observed counts:

| Number on die | ||||||

|---|---|---|---|---|---|---|

| Observed | 4/60 | 6/60 | 17/60 | 16/60 | 8/60 | 9/60 |

| Hypothesized | 1/6 | 1/6 | 1/6 | 1/6 | 1/6 | 1/6 |

The gambler wishes to determine whether the die is fair. If it is fair, we would expect the outcomes of to are equally likely, with probability . Pearsonian chi-square and a full-rank LP-analysis, both lead to the same answer:

with the resulting -value . Note that the sum of squares of the LP-Fourier coefficients “exactly” reproduces (numerically) the Pearson’s chisquare statistic! This further verifies the mathematical fact elucidated in eq. (3.6). Conclusion: The die is loaded at 5% significance level.

Exploratory insight. Here we want to go beyond classical confirmatory analysis, with the goal to understand how the die is loaded. The answer is hidden in the shape of the comparison density . Fig. 4(a) firmly suggests that the die was loaded heavily in the middle —especially on the sides and , where it landed most frequently.

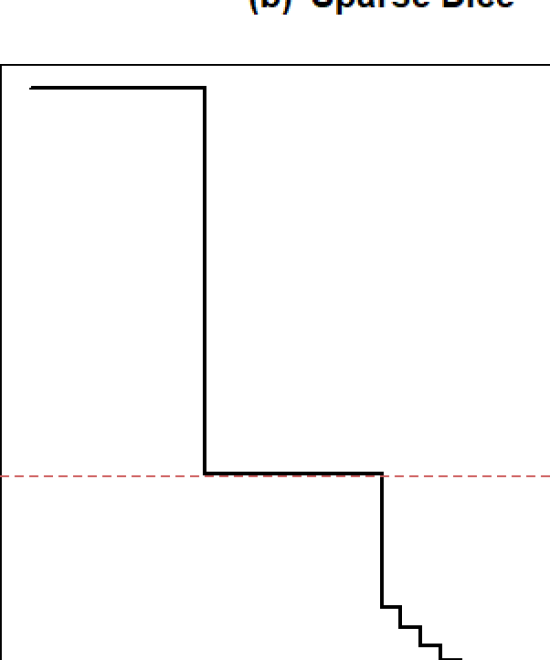

Example 5 (Sparse Dice problem).

It is an example of sparse count data with many groups. Imagine a dimensional dice is rolled times:

-

•

The hypothesized model:

-

•

The observed probabilities: .

We would like to know whether the postulated model actually reflects the data or not. If it does not, then we want to know how the hypothesized model differs from the observed probabilities.

Pearsonian chi-square111R-function chisq.test() generates the message that “Chi-squared approximation may be incorrect!.” yields value , with degrees of freedom and -value . Conclusion: there is no evidence of discrepancy at 5% level, even though there is a glaring difference between and . The legacy loses its power because of ‘inflated degrees of freedom’ for large sparse problems: Large value of increases the critical value , making it harder to detect ‘small’ but important changes.

LP-Analysis of the sparse dice problem: (i) Construct the discrete LP-polynomials that are specially-designed for the given . Appendix Fig. 14 displays the shape of those basis functions. (ii) Compute the LP-Fourier coefficients by . The Appx. figure 15 identifies the first two LP-parameters as significant components. (iii) We now compute the compressive- based on these interesting components:

| (3.7) |

and -value . Also noteworthy is the fact that compressive LP-chisquare is numerically almost same as the raw :

Remark 5 (Auto-adaptability).

LP-goodness-of-fit shows an impressive adaptability property: under the usual scenario (like in example 4) it reduces to the classical analysis, and for large-sparse problems, it automatically produces a chi-square statistic with the fewest possible degrees of freedom, which boosts its power. Our reformulation (in terms of modern LP-nonparametric language) allowed a better way of doing chi-square goodness-of-fit analysis that applies to a much broader class of applied statistics problems. In John Tukey’s (1954) words: “Do we need to find new techniques, or to use old ones better?”

Remark 6 (Ungrouped case).

What if we have ungrouped data: given a random sample of counts , check (confirm) whether the data is compatible with the hypothesised , i.e., to test the hypothesis . One way to approach this problem is to forcefully group the data points into different categories and then apply Pearson’s test on it. This is (almost) always a bad strategy, since grouping leaks information. Moreover, the arbitrariness involved in choosing the groups makes it an even less attractive option. However, our LP-divergence measure (3.6) can be applied to ungrouped data, with no trouble. The next section expands on this.

3.4 Explanatory Goodness-of-Fit

What is an explanatory goodness-of-fit? Why do we need it? This is perhaps best answered by quoting the views of John Tukey:

“What are we trying to do with goodness of fit tests? (Surely not to test whether the models fits exactly, since we know that no model fits exactly!) What then? How should we express the answer of such test?”

—John Tukey (1954)

To satisfactorily answer these questions we need to design a GOF-procedure that is simultaneously confirmatory and exploratory in nature: On the confirmatory side, it aims to develop a universal GOF statistic that is easy to use and fully automated for any user-specified discrete . One such universal GOF measure is , defined as

| (3.8) |

where the index runs over the significant components. See Appx. A.1 for more details.

On the exploratory side, the graphical visualization of comparison density provides explanations as to why is inadequate for the data (if so) and how to rectify it to reduce its incompatibility with the data. This has special significance for data-driven discovery and hypothesis generation. In particular, the non-zero LP-coefficients indicate the “main sources of discrepancies.” In the following, we illustrate this method using three real data examples, each of which contains a different degree of lack-of-fit.

Example 6 (Spiegel Family Data).

Spiegel (1972) reported a survey data of families with five children. The numbers of families with and girls were and . As an obvious model for we choose Binomial. Estimated LP-Fourier coefficients are

| (3.9) |

with -value under the chi-square null with df . In other words, we have just shown that the comparison density is flat uniform , hence the binomial distribution is completely acceptable for this data; no further density sharpening is needed.

Remark 7.

Note that in our analysis, the prime object of interest is the shape of the estimated (because it addresses Tukey’s concern about the practical utility of goodness-of-fit), not how big or small the -value is. But if a data analyst is habituated to using a threshold -value as a basis for decision making (not a good practice), then we recommend ‘double parametric bootstrap’ (Beran, 1988) to compute the -value— admittedly a computationally demanding task. This adjusted -value takes into account the fact that the null-parameters are not given (e.g., here the binomial proportion ); they are estimated from the data.

Example 7 (Rutherford-Geiger polonium data).

Rutherford, Geiger, and Bateman (1910) presented experimental data on groups of alpha particles emitted by Polonium, a radioactive element, in 1/8 minute intervals. On the whole, time intervals were considered, in which () decays were observed. The following table summarizes the data.

| 0 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 13 | 14 |

| 57 | 203 | 383 | 525 | 532 | 408 | 273 | 139 | 45 | 27 | 10 | 4 | 1 | 1 |

In the 1910 article, Bateman showed that (appended as a note at the end of the original 1910 paper) the theoretical distribution of alpha particles observed in a small interval follows Poisson law, which we select as our model-0. The estimated model is given by

| (3.10) |

which is displayed in Fig. 18 in the Appendix. The model (3.10) indicates that there is a ‘gap’ between the theoretically predicted Poisson model and the experimental result— second-order (under‐dispersed) and third-order (less skewed) corrections are needed. To quantify the lack-of-fit, compute:

This is a borderline case, where it is important to consult subject matter specialists before choosing sides—scientific significance is as important as statistical significance. Hoaglin (1980) came to a similar conclusion using an exploratory diagnostic tool called “Poissonness plot,” shown in the Appendix Fig. 19.

Example 8 (Sparrow data).

This data composed of numbers of sparrow nests found in plots of area one hectare, the sample average being . Zar (1974) previously analyzed this dataset. We choose Poisson() as our for model. The second-order (pvalue=.03) turns out to be the only significant component, which indicates that the data exhibit less-dispersion (due to the negative sign) than postulated . Our finding is in agreement with Gürtler and Henze (2000). Finally, return the -modified under-dispersed Poisson model for the data:

which is displayed in Fig. 20 of the Appendix.

3.5 Relative Entropy and Model Uncertainty

How to quantify the uncertainty of the chosen model ? A general information-theoretic formula of model uncertainty is derived based on relative entropy between the true (unknown) and the hypothesized . Express relative entropy (also called Kullback–Leibler divergence) as a functional of maxent comparison density :

| (3.11) |

Substituting , leads to the following important formula for relative entropy in terms of LP-parameters:

| (3.12) | |||||

The second equality follows from eq. (2.8) and the last one from eq. (2.8). Based on a random sample , a nonparametric estimate of relative entropy is obtained by replacing the unknown LP-parameters in (3.12) with their sample estimates.

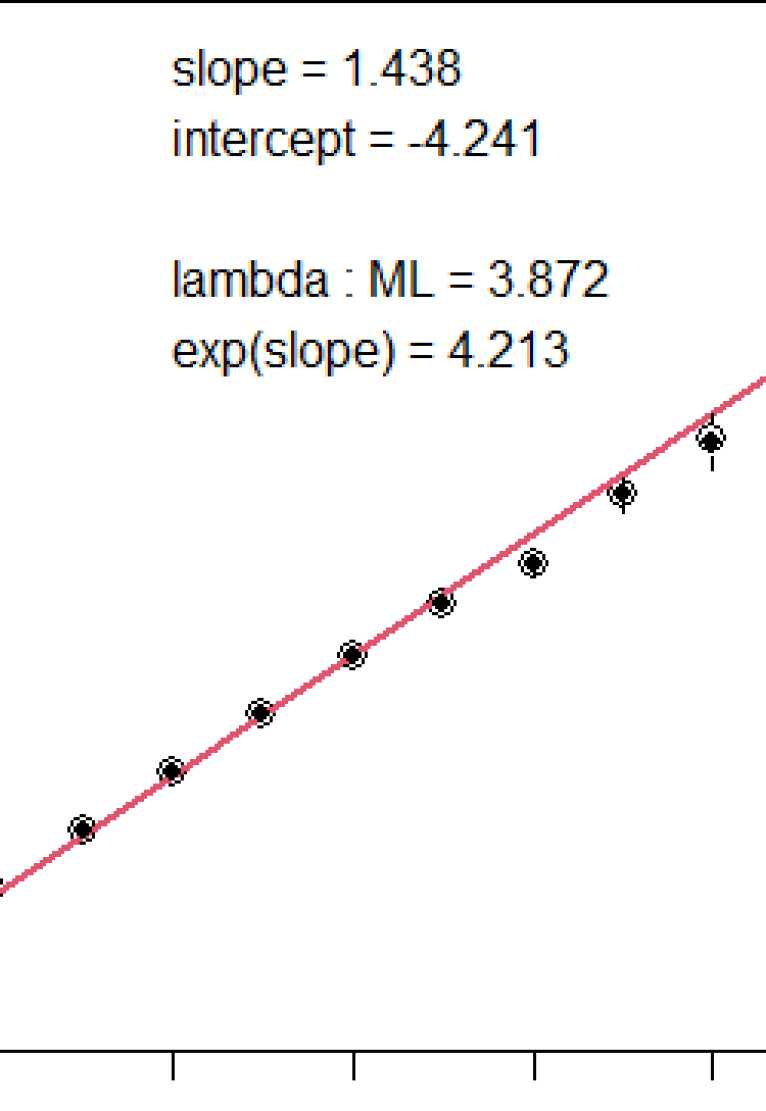

Statistical Inference. Relative entropy-based statistical inference procedure is applied to few real datasets in the context of model validation and uncertainty quantification. Estimation and Standard error: For the earthquake data, we like to quantify the uncertainty of . The estimated value of is (bootstrap standard error, based on ), indicating serious lack-of-fit of the starting NB model—which matches with our previous conclusion; see Fig. 1. Testing: For the Spiegel family data, the estimated relative entropy we get is , quite small. Naturally, we perform (parametric bootstrap-based) testing to check if . Generate samples from ; compute ; repeat, say, times; return the -value based on the bootstrap null-distribution. For this example, the -value we get is , which reaffirms that binomial distribution explains the data fairly well.

3.6 Card Shuffling Problem

Consider the following question (Aldous and Diaconis, 1986): How many times must a deck of cards be shuffled until it is close to random? To check whether a deck of cards is uniformly shuffled we use fixed point statistic, which is defined as the number of cards in the same position after a random permutation. Large values of fixed points (‘too many cards left untouched’) is an indication that the deck is not well-mixed.

Theoretically-expected distribution: One of the classical theorems in this direction is due to Pierre de Montmort (1713) who showed that the distribution of the number of fixed-points under (random permutation of is approximately .

Data and notation: Let denotes sample size and number of shuffles. Then CARD stands for a dataset , where is the number of fixed points of a -shuffled deck. By , we mean the sample distribution of fixed-point statistic after random permutations. The goal is to find the minimum value of , such that it is safe to accept , where, we should recall, the null-distribution is .

Modeling via goodness-of-fit: Fig. 5 shows a CARD dataset with and . There is a clear discrepancy between the observed probabilities and the theoretical . The estimated -sharpen Poisson is given below:

| (3.13) |

which shows that ‘first order perturbation’ (location correction) is needed: with pvalue . The positive sign of indicates that the mean of the fixed points distribution with is larger than the postulated ; more shuffling is needed to make the deck close to random. The shape of (3.13) is shown in Fig. 5.

New updated mean. A curious reader might want to know precisely how large the mean of is compared to . For a distribution , we can write an expression for the mean of () in terms of the mean of (). In this case, we have

| (3.14) | |||||

A few additional comments:

Thus far, we have verified that is not enough to produce a uniformly shuffled deck. However, we came to this conclusion based on a single sample of size . So, we generate (through computer simulation) several replications of CARD data with different .

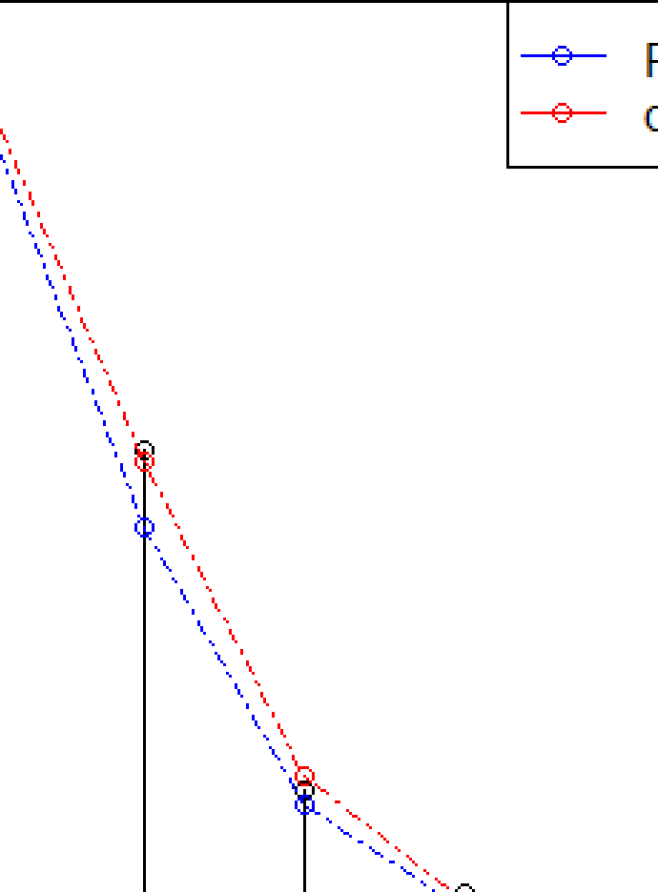

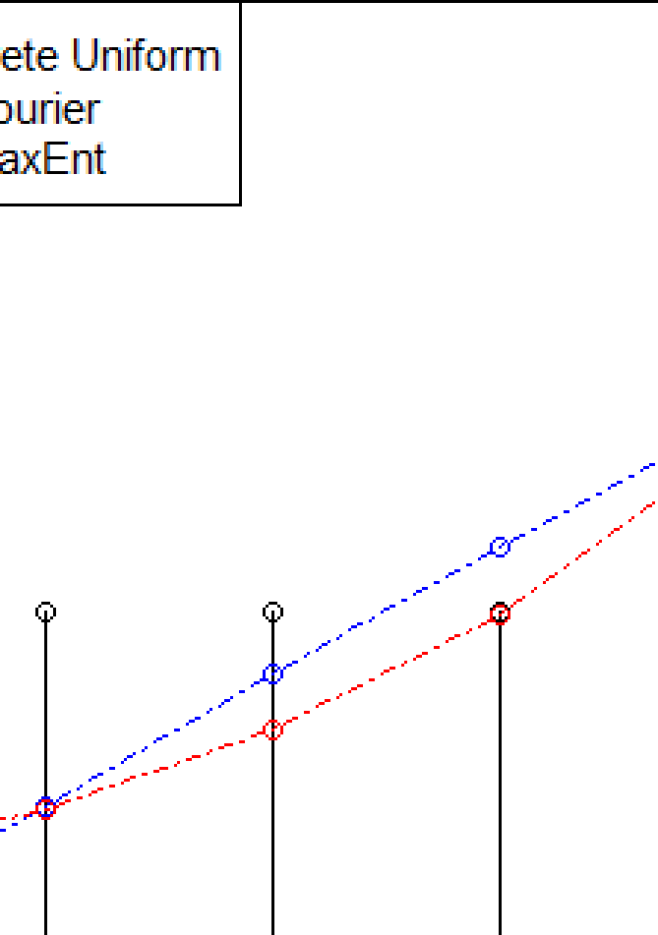

To reach a confident decision, we perform the experiment with and . The analysis was done based on datasets from each -pair. The results are summarized in appendix Fig. 21, which shows that shuffles is probably a safe bet to declare a deck to be fair—i.e., uniformly distributed.

Diaconis and Wang (2018) describes a Bayesian approach to this problem. In contrast, we offered a completely nonparametric solution that leverages the additional knowledge of the expected and provides more insights into the nature of discrepancies.

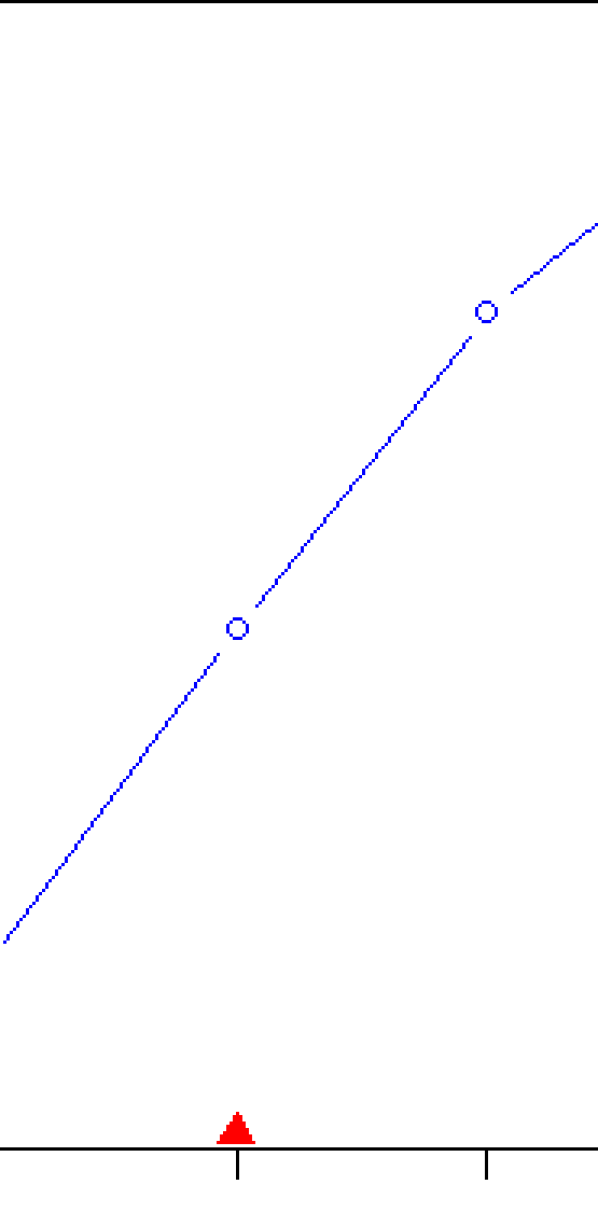

3.7 Jaynes Dice Problem

The celebrated Jaynes’ dice problem (Jaynes, 1962) is as follows: Suppose a die has been tossed times (unknown) and we are told only that the average number of the faces was —not , as we might expect from a fair die. Given this information (and nothing else), the goal is to determine probability assignment, i.e., what is the probability that the next throw will result in face , for .

Solution of Jaynes’ dice problem using density sharpening principle. The initial is selected as the discrete uniform distribution for , which reflects the null hypothesis of ‘fair’ dice. As we are given only the first-order location information (mean is ) we consider the following model:

| (3.15) |

The coefficient has to be estimated, and for that we also need to know the basis function .

Step 1. To find an explicit formula for the discrete basis , apply (2.3) with and

| (3.16) |

Step 3. Substitute the value of in eq. (3.15) to get the LP-Fourier model as

| (3.18) |

This is shown as the blue curve in Fig. 6.

Step 4. Finally, return the estimated exponential probability estimates

| (3.19) |

This is shown as the red curve in Fig. 6.

| 1/6 | 1/6 | 1/6 | 1/6 | 1/6 | 1/6 | |

| LP-Fourier | .025 | .080 | .140 | .195 | .250 | .310 |

| LP-MaxEnt | 0.054 | 0.079 | 0.114 | 0.165 | 0.240 | 0.347 |

| Jaynes’Answer | 0.054 | 0.079 | 0.114 | 0.165 | 0.240 | 0.347 |

Remark 8.

It is a quite remarkable fact that our density-sharpening principle-based probability assignment exactly matches with Jaynes’ maxent answer; see Table 3.

3.8 Compressive Learning of Big Distributions

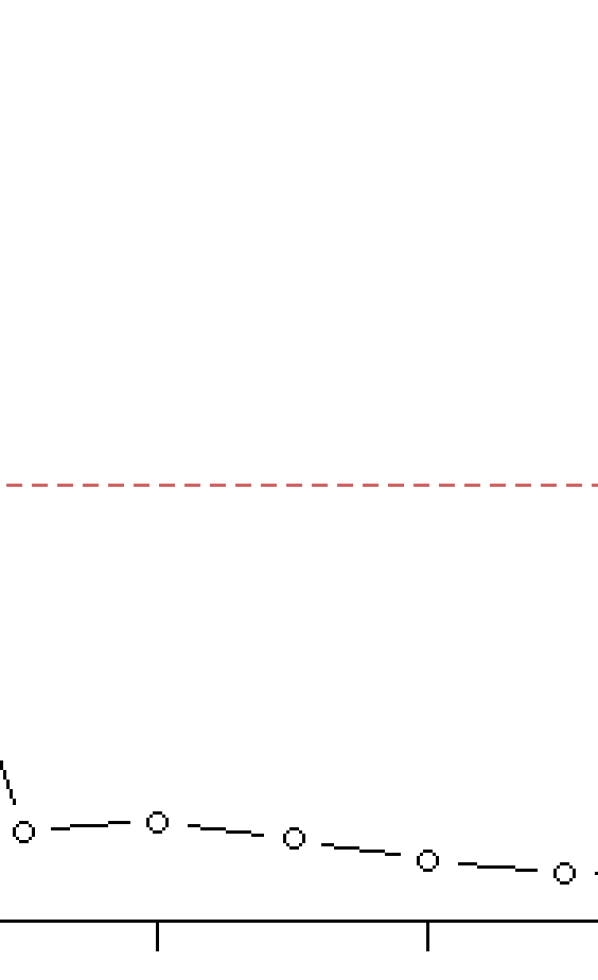

An important class of learning problem that has recently attracted researchers from various disciplines—including high-energy physics, neuroscience, theoretical computer science, and machine learning—can be viewed as a modeling problem based on samples from a distribution over large ordered domains. Let be a probability distribution over a very large domain , where . Let us look at a realistic example before discussing a general method.

Example 9 (HEP data).

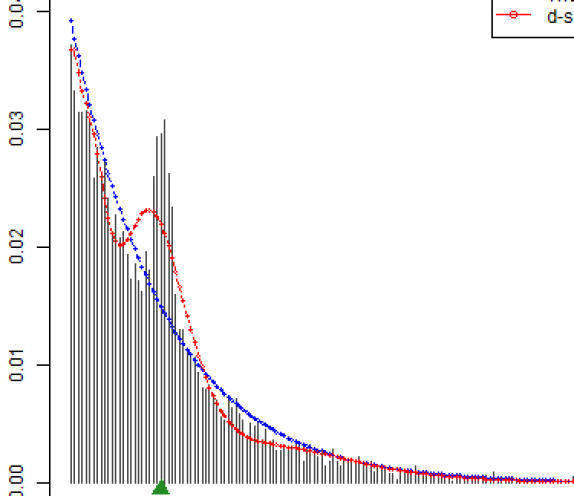

This is an example from high-energy physics222High-energy physics is not the only discipline where this kind of very large and sparse histogram-like data appears. It frequently arises in many modern scientific domains: inter-spike interval data (neuronal firing patterns); relative abundance/intensity data (mass spectrometry data); DNA methylation and ChIP-seq data (genomics); pixel histogram data (astronomical images of stars, galaxies etc); histograms of activity intensities (biosignals from wearable sensor devices, mental illnesses studies by NIMH); photometric redshift data (photo-z spectra in Cosmology), just to name a few. There is an outstanding interest in developing new computational tool that allows rapid and approximate statistical learning for big-histogram-like datasets. (HEP), motivated by the PHYSTAT 2011 Banff bump-hunting challenge task (Junk, 2011). In HEP counting experiments (e.g., in Large Hadron Collider) one observes data in the following form: samples from unknown as event counts (number of collisions) at finely binned energy-cells, which we denote by HEP. Fig. 7 displays one such data with and , with the postulated background model (dictated by the known Standard Model) as discretized exponential distribution with :

| (3.20) |

Particle physicists are interested in discovering new particles that go beyond the known Standard model described by the background model . We present a four-step algorithmic program to address the general problem of data-driven ‘Learning and Discovery.’

Phase 1. Testing. The first question a scientist would like answered is whether the data is consistent with the background-only hypothesis, i.e., . We perform the information-theoretic test described in Sec. 3.5. In particular, we choose the relative entropy-based formula given in (3.12) as our test statistic. The -value obtained using parametric bootstrap (with ) is almost zero—strongly suggesting that the data contain some surprising new information in light of the known physics model . But to figure out whether that information is actually useful for physicists, we have to dig deeper.

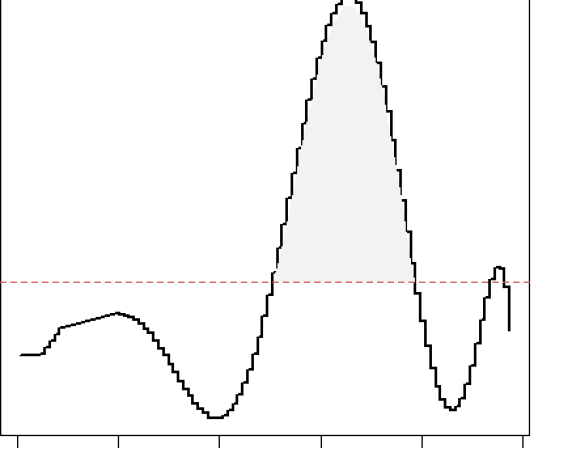

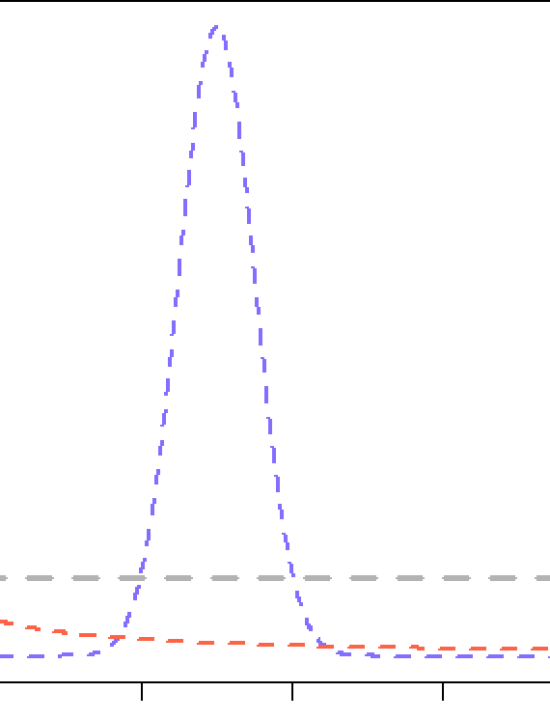

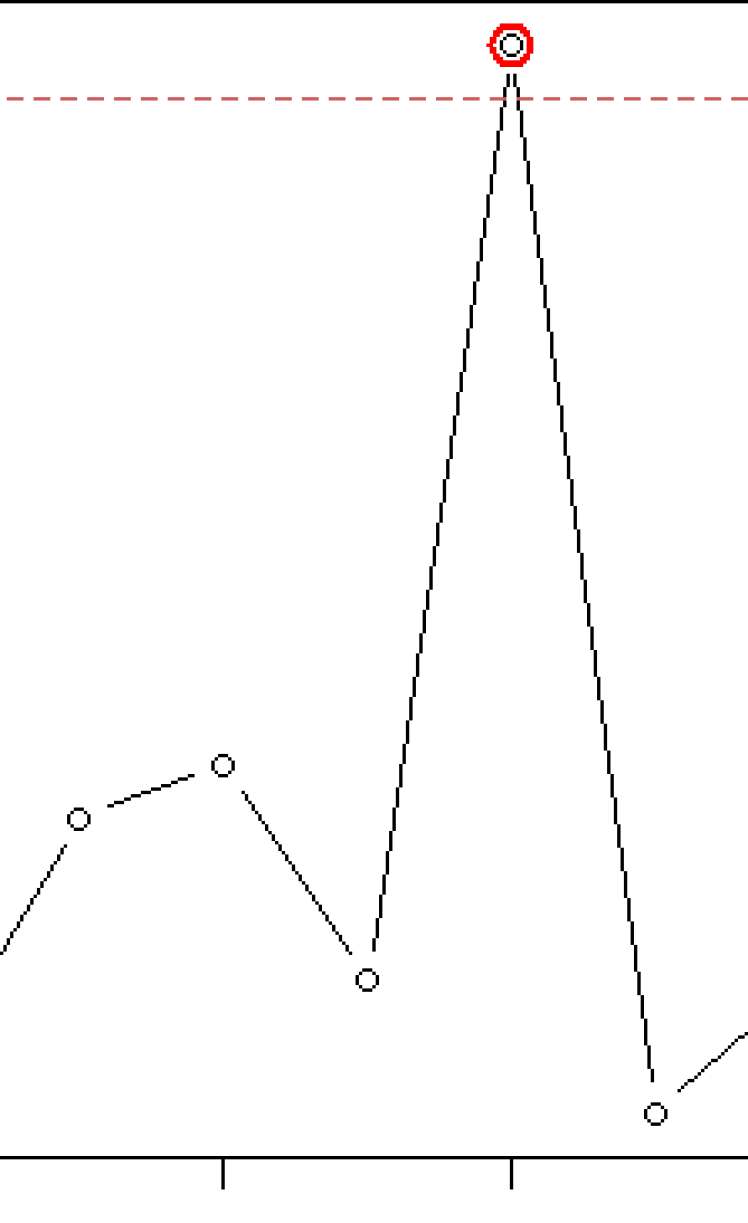

Phase 2. Exploration and Discovery. By definition, new discoveries can be made only by “contrasting” data with the existing model. This is what is achieved through . The left panel of Fig. 7 displays the estimated for the HEP-data, which compactly encodes all the structure of the data that cannot be described by the assumed .

The exploratory graphical display of reveals a few noteworthy points. Firstly, the non-uniformity of makes us skeptical about —this is completely in agreement with Phase-1 analysis. Secondly and more importantly, the shape of provides a refined understanding of the nature of new physics that is hidden in the data, which, in this case, revealed itself as a bump above the smooth background . The word ‘above’ is important because we are not interested in bumps on itself, but on , which is the unanticipated ‘excess mass.’ Hunt for new physics is the problem of bump hunting on , not on . For the HEP-data, we see a prominent bump in around , which (in the original data domain) corresponds to near 125 GeV; the green triangle in the above figure.

Remark 9 (The discovery function).

Since, encapsulates what’s new in the data by separating the unknown from the known, we also call it the “discovery function.” It is the “missing piece” that glues together the known and the unknown . It provides a graphical diagnostic tool that exposes the unexpected. These clues can guide domain-scientists to carry out more targeted follow-up studies.

Phase 3. Inference and Excess Mass Problem. Where is the interesting excess mass hiding? Is it a statistical fluke or something real? How substantial is the evidence? The real issue is: can we let the data confidently tell us where to look next for new particles? This will result in a complete paradigm shift because traditionally the HEP searches (for locating excess events) were guided by theoretical considerations only.

‘One may feel uneasy that we may therefore only find new processes if a theorist has been clever enough to propose the corresponding theory ahead of time.’

—-Glen Cowan (2007)

Interested readers may also refer to Lyons (2008) and the Nature news article by Castelvecchi (2018) for a clear exposition on the scientific importance of these issues.

Statistical Discovery: Inference Algorithm. The following are the main steps of the inference algorithm whose results are summarized in Fig. 8:

Step 1. Parametric bootstrap: To measure the natural statistical variation of under the null hypothesis: simulate samples from and estimate the comparison density. Repeat the whole process for a large number of iterations (say times) to get a bundle of comparison density curves, all of which fluctuate around the flat uniform line.

Step 2. Pointwise -value computation: At a fixed grid point , we have the following values of the test statistic

calculated from the bootstrap samples. Compute the bootstrap -value at the point by

Fig. 8 draws the curve as a function of . The discovery region is highlighted in yellow, which includes the true excess mass point GeV. This is how modern nonparametric modeling based on ‘density sharpening principle’ can convincingly guide researchers on where to look for evidence of a deeper theory of physics.

Phase 4. Sharpen Scientific-Model. Finally, the goal is to sharpen the initial scientific model to achieve a more precise description of what is loosely known or suspected. The estimated model sharpens the parametric null (3.20) to provide a nonparametrically-adjusted, parsimonious model:

| (3.21) |

where the active set along with the LP-coefficients are given in Table 4.

| 2 | 3 | 5 | 7 | 8 | |

|---|---|---|---|---|---|

| -.097 | -.090 | 0.117 | -.095 | -.060 |

Remark 10.

A few remarks:

1. The part in the square brackets of (3.21) shows how to change the prior scientific model to make it consistent with the data. Knowing the nature of the deficiency of the assumed model, is an important step towards data-driven discovery. As George Box (2001) said: “discovery usually means learning how to change the model.”

2. LP-parameterization requires only -dimensional sufficient statistics to approximately capture the shape of the distribution! The “compressiveness” of the LP-transformation—the ability to extract a low-dimensional representation—makes it less data-hungry, as demonstrated in the next section.

3. Our model (3.21) is a ‘hybrid’ between theory-driven and data-driven model, which decouples the overall density into two components: expected and unexpected .

Remark 11 (An Appeal to Physicists: Hypothesis Testing Discovery Science).

Classical statistical inference puts too much emphasis on testing, -value, standard error, and confidence intervals, etc. This ideology is reflected in the practice of high-energy physicists—which entirely revolves around antique tools of hypothesis testing, likelihood ratio, and -value. It’s time to break the shackles of outdated data analysis technology that starts with hypothesis testing and ends with a -value. George Box (2001) expressed a similar sentiment, arguing that the reason why engineering and the physical sciences rarely use statistics is: “Much of what we have been doing is adequate for testing but not adequate for discovery.”

In this section my purpose has been to introduce some modern statistical tools and concepts that can help scientists with their everyday tasks of discovery and deeper exploration of data. After all, one of the main goals of data analysis is to sharpen the scientists’ mental model by revealing the unexpected—a continuous cycle of knowledge refinement:

3.9 Data-efficient Statistical Learning

We are interested in the following statistical learning problem: Given a small handful of samples from a big probability distribution of size , how to perform time-and-storage-efficient learning? When designing such algorithms we have to keep in mind that they must be (i) data-efficient: can learn from limited sample data ; and (ii) statistically powerful: can detect “small” deviations.

Classical nonparametric methods characterize big probability distributions using high-dimensional sufficient statistics based on histogram counts , which, obviously, requires a very large sample for efficient learning. And as the required sample sizes increases, this slows down the algorithm running-time which scales with . Hence, most of the ‘legacy’ statistical algorithms (e.g., Pearson’s chi-square, Freeman-Tukey statistic, etc.) become unusable on large-scale discrete data as ‘the minimum number of data points required to obtain an acceptable answer is too large to be practical.’ Indeed, detecting sparse structure in a data-efficient manner from big distributions, such as from HEP(), is a challenging problem and requires a “new breed” of computational algorithms. There has been some impressive progress on this front by the Theoretical Computer Science community; see Appendix A.3 for a related discussion on sub-linear algorithms for big data.

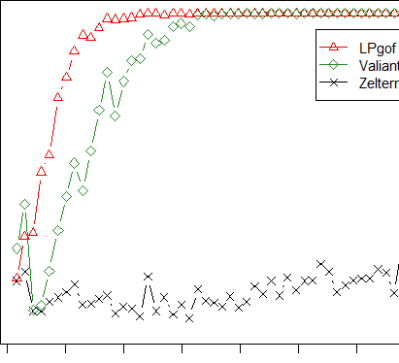

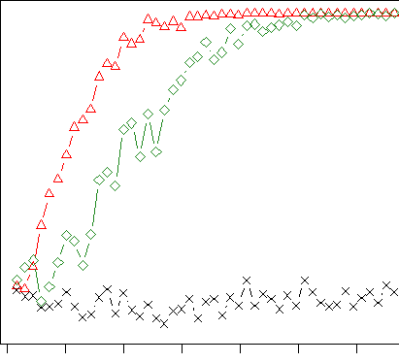

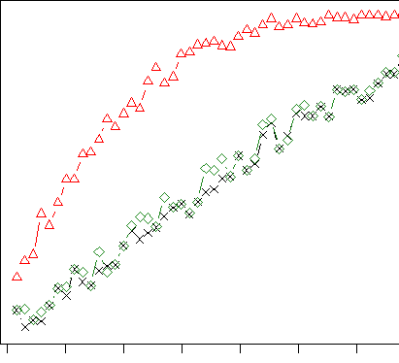

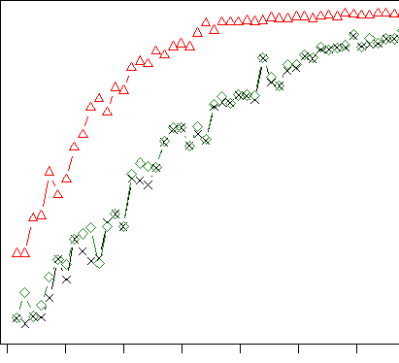

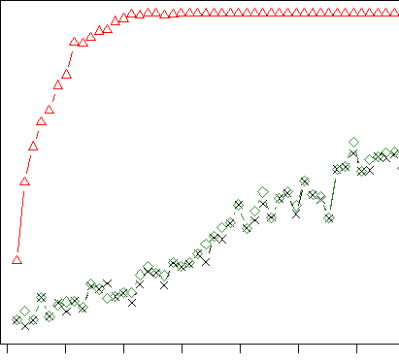

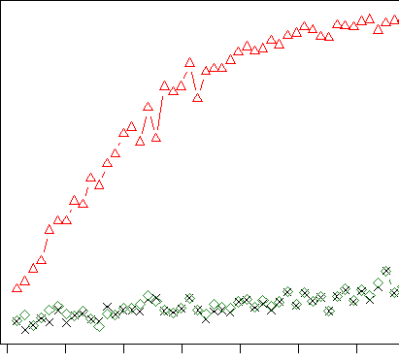

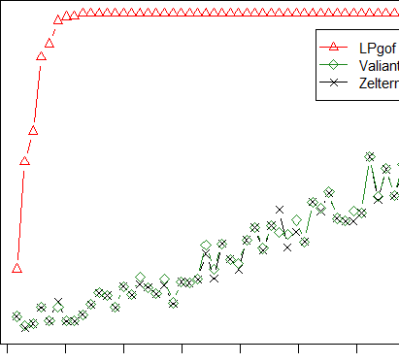

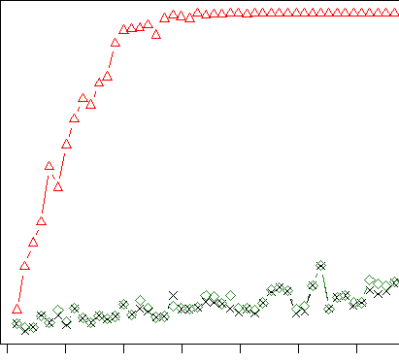

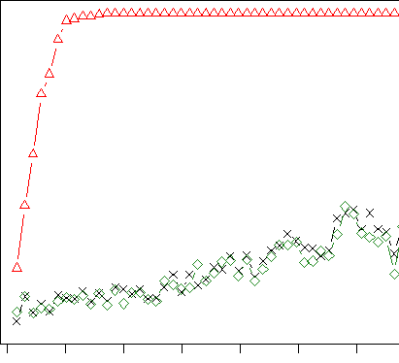

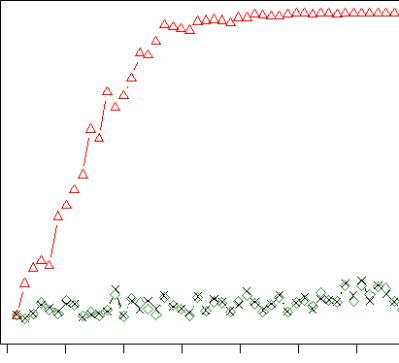

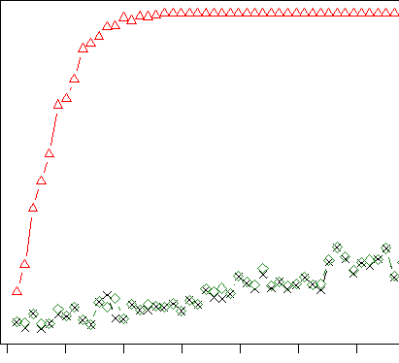

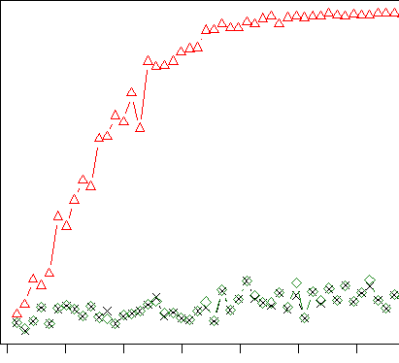

HEP Data Example. We generate HEP() data for varying sample size . We used null simulated data sets to estimate the 95% rejection cutoffs for all methods at the significance level , and used simulated data sets from alternative to approximate the power, as displayed in Fig. 10. We compared our LPgof method (3.8) with two state-of-the-art algorithms (proposed by theoretical computer scientists): (i) Valiant and Valiant (2017) and (ii) Acharya et al. (2015)—interestingly, this exact test has been proposed earlier by Zelterman (1987), which in Statistics literature is known as Zelterman’s D-statistic333‘Those who ignore Statistics are condemned to reinvent it’—Brad Efron.. Conclusion: LPgof requires 50% less data to reach the correct conclusion with power 1.

Empirical Power Comparisons. We compare the power of different methods under six different settings, as described in the Figs 10 description, and will not repeat this here. The overall conclusion is pretty clear: LPgof emerged as the most powerful data-efficient test—it can detect new discoveries quickly and more reliably. The prime reason for achieving this level of performance is fully attributable to the good sparsity (energy compaction) property of “LP-domain data analysis.” The specially-designed discrete LP-transformation basis provides an efficient coordinate system that requires far fewer parameters than the size of the distribution to capture the essential information. For additional examples see Figs. 22 and 23 of the Appendix.

3.10 Discovery-source Separation Problem

“At this scale it is not possible to keep all the data (the LHC produces up to a Petabyte of data per second) and it is essential to have efficient data-filtering mechanisms so that we can separate the wheat from the chaff.”

— Bob Jones, Project Leader at CERN.

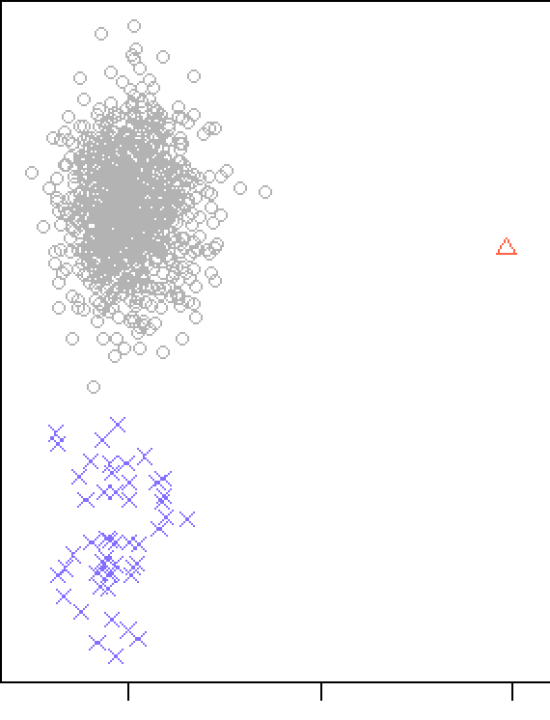

Imagine a typical scenario, where massive experimental data are distributed across thousands of different computation units (say, servers). Each data source has its own ‘personal’ distribution over a large domain of size , from which, we only have access to samples. Thus, the observed data can be summarized as a collection of highly noisy and sparse empirical distributions . Suppose we are given such sparsely-sampled empirical distributions from , from , and from a mixture of , where denotes the increments of the cdf of . Shapes of these three source-distributions are shown in the left of Fig. 12.

Discovery-source Separation (DSS). The goal here is to design algorithms that can quickly filter out the ‘interesting’ data sources, having potential for a new physics discovery. A more ambitious goal would be to classify different data sources based on their ‘nature’ of discoverability.

Algorithm. It consists of two main steps: Step 1. LP-Fourier Transform Matrix: Define the LP-transform matrix by

| (3.22) |

for and .

Step 2. DSS-plot: Perform the singular value decomposition (SVD) of , where are the elements of the singular vector matrix , and , . DSS-plot is the two-dimensional graph in the right panel of Fig 12 (b), which is formed using the points , for by taking the top two dominant singular vectors. Different data sources are shown as points, which captures the heterogeneity in terms of discoverability.

Interpretation: DSS-plot displays and compares a large number of (empirical) distributions by embedding them in 2D Euclidean space. The cluster of points (data sources) that are near to the origin are the ones with background distribution. The distance from the origin

can be interpreted as the “degree of newness” of that dataset. The DSS-plot successfully separates different sources based on the statistical nature of their signal components. Researchers (like Bob Jones) can use this tool to quickly identify interesting data sets for careful investigation.

4 Discussion

Compared to the rich and well-developed tools for continuous data modeling problems, many companion discrete data modeling problems are still quite challenging. This was the main motivation for undertaking this research, which aimed at developing a widely-applicable general theory of discrete data modeling. This paper makes three broad contributions to the field of nonparametric statistical modeling:

1) Model-Sharpening Principle: We have introduced a new principle of statistical model building, called ‘Density-Sharpening,’ which performs three tasks in one step: model verification, model exploration, and model rectification. This was the guiding principle behind our systematic theory of discrete data modeling. As future work, we plan to explore how model-sharpening principle can help developing ‘auto-adaptable’ machine-learning models.

2) Model: We have introduced a new class of nonparametric discrete probability model and robust estimation techniques that has the capability to leverage researchers’ vague (misspecified) prior knowledge. It comes with novel exploratory graphical methods for ‘discovering’ new knowledge from the data that investigators neither knew nor expected.

3) Unified Statistical Framework: Our modern nonparametric treatment of the analysis of discrete data is shown to be rich enough to subsume a large class of statistical learning methods as a special case. This inclusivity of the general theory has some serious implications: Firstly, from a theoretical angle, it deepens our understanding of the ties between different statistical methods. Secondly, it simplifies practice by developing unified algorithms with expanded capabilities. And finally, it is also expected to be beneficial for modernizing Statistics curriculum in a way that is applicable to small- as well as large-scale problems.

Supplementary Appendix

The supplementary material includes additional theoretical and algorithmic details.

References

- Acharya et al. (2015) Acharya, J., C. Daskalakis, and G. C. Kamath (2015). Optimal testing for properties of distributions. In Advances in Neural Information Processing Systems, pp. 3591–3599.

- Aldous and Diaconis (1986) Aldous, D. and P. Diaconis (1986). Shuffling cards and stopping times. The American Mathematical Monthly 93(5), 333–348.

- Beran (1988) Beran, R. (1988). Prepivoting test statistics: a bootstrap view of asymptotic refinements. Journal of the American Statistical Association 83(403), 687–697.

- Bernreuter (1981) Bernreuter, D. (1981). Seismic hazard analysis application of methodology, results, and sensitivity studies. volume 4. Technical report, Lawrence Livermore National Lab., CA.

- Box (2001) Box, G. (2001). Statistics for discovery. Journal of Applied Statistics 28(3), 285–299.

- Castelvecchi (2018) Castelvecchi, D. (2018). LHC physicists embrace brute-force approach to particle hunt. Nature 560(7718), 293–295.

- Cowan (2007) Cowan, G. (2007). The small-n problem in high energy physics. In Statistical Challenges in Modern Astronomy IV ASP Conference Series; Edited by G. Jogesh Babu and Eric D. Feigelson., Volume 371, pp. 75.

- Csörgő (1983) Csörgő, M. (1983). Quantile processes with statistical applications. SIAM.

- de Montmort (1713) de Montmort, P. R. (1713). Essay d’analyse sur les jeux de hazard. Jacques Quillau, Paris. Reprinted 1980 by Chelsea, New York.

- Diaconis and Wang (2018) Diaconis, P. and G. Wang (2018). Bayesian goodness of fit tests: a conversation for david mumford. Annals of Mathematical Sciences and Applications (arXiv:1803.11251).

- Gürtler and Henze (2000) Gürtler, N. and N. Henze (2000). Recent and classical goodness-of-fit tests for the poisson distribution. Journal of Statistical Planning and Inference 90(2), 207–225.

- Hansen (2014) Hansen, L. P. (2014). Nobel lecture: Uncertainty outside and inside economic models. Journal of Political Economy 122(5), 945–987.

- Hoaglin (1980) Hoaglin, D. C. (1980). A poissonness plot. The American Statistician 34(3), 146–149.

- Jaynes (1962) Jaynes, E. T. (1962). Information theory and statistical mechanics (notes by the lecturer). Statistical Physics 3, Lectures from Brandeis Summer Institute 1962. New York: WA Benjamin, Inc.

- Junk (2011) Junk, T. R. (2011). Banff Challenge 2. Proceedings of the PHYSTAT 2011 Workshop and Fermi National Accelerator Laboratory Report.

- Kagan (2010) Kagan, Y. Y. (2010). Statistical distributions of earthquake numbers: consequence of branching process. Geophysical Journal International 180(3), 1313–1328.

- Kagan and Jackson (2000) Kagan, Y. Y. and D. D. Jackson (2000). Probabilistic forecasting of earthquakes. Geophysical Journal International 143(2), 438–453.

- Lyons (2008) Lyons, L. (2008). Open statistical issues in particle physics. The Annals of Applied Statistics, 887–915.

- Parzen (1998) Parzen, E. (1998). Statistical methods mining, two sample data analysis, comparison distributions, and quantile limit theorems. In B. Szyszkowicz (Ed.), Asymptotic Methods in Probability and Statistics, pp. 611–617. Amsterdam: North-Holland.

- Rutherford et al. (1910) Rutherford, E., H. Geiger, and H. Bateman (1910). The probability variations in the distribution of particles. The London, Edinburgh, and Dublin Philosophical Magazine and Journal of Science 20(118), 698–707.

- Saulo et al. (2020) Saulo, H., R. Vila, L. Paiva, and N. Balakrishnan (2020). On a family of discrete log-symmetric distributions. arXiv preprint arXiv:2005.09744.

- Spiegel (1972) Spiegel, M. R. (1972). Statistics. McGraw-Hill.

- Tukey (1954) Tukey, J. W. (1954). Unsolved problems of experimental statistics. Journal of the American Statistical Association 49(268), 706–731.

- Valiant and Valiant (2017) Valiant, G. and P. Valiant (2017). An automatic inequality prover and instance optimal identity testing. SIAM Journal on Computing 46(1), 429–455.

- Zar (1974) Zar, J. H. (1974). Biostatistical analysis. Prentice Hall, Englewood Cliffs, N.J.

- Zelterman (1987) Zelterman, D. (1987). Goodness-of-fit tests for large sparse multinomial distributions. Journal of the American Statistical Association 82(398), 624–629.

5 Appendix

It consists of four sections.

A.1 Goodness-of-fit Methods: Automatic verses Manual

Traditional GOF methods, mainly inspired by Lancaster (1953), construct orthonormal polynomials on a case-by-case basis for each parametric discrete distribution . This is generally done by solving the heavy-duty Emerson recurrence (Emerson, 1968, Best and Rayner, 1999a, 2003a) relation, which could be quite complicated for non-standard distributions. Few concrete examples: The proposal of Best and Rayner (1997) for testing Binomial distribution is based on Krawtchouk polynomial; Best and Rayner (2003b) develop test for geometric distribution using Meixner orthonormal polynomials; Best and Rayner (1999b) construct Poisson GOF method based on Poisson-Charlier orthonormal polynomials; For a theory of classical (distribution-specific) orthonormal polynomials refer to Chihara (2011).

The problem with this line of thinking is that it makes the whole procedure hard to automate and generalize, which may turn off practitioners.

Instead of bookkeeping a long list of esoteric polynomials for each parametric distribution, we want to devise a universal mechanism that works for any arbitrary —which will make it easy to use and compute. This is achieved in Section 3.4 of our paper by employing LP-orthonormal polynomial bases. Its universality (3.8) lies in the fact that, unlike traditional methods, we have the ability to construct discrete orthonormal polynomials (Sec. 2.2) of the user-specified in a completely automatic and robust manner.

A.2 LPdiscrete: A Unified Algorithm

We summarize some of the key steps of our generic discrete data modeling approach, which starts with data and an approximate (misspecified) working model .

LPdiscrete: Algorithm Based on ‘Density-Sharpening’ Principle

1. Input: Discrete sample distribution and the assumed reference model . The corresponding cdfs are denoted by and . 2. Compute the first-order LP-basis by standardizing mid-distribution transform

3. Apply weighted Gram-Schmidt procedure on to construct empirical orthonormal polynomials with respect to measure

Define the Unit LP-bases , .

4. Estimate the discrete LP-Fourier transform coefficients of with respect to

They are the coordinates of the true unknown distribution relative to

5. Sparse LP-transform. Identify the ‘significant’ non-zero LP-coefficients with . A more sophisticated method: identify indices using AIC (or BIC) model selection criterion applied to arranged in decreasing magnitude

Choose to maximize . Store the selected indicates in the set . 6. Compute the lack-of-fit of the assumed model

7. Since is the inner product of comparison density with LP-basis , they are the coefficient of the orthogonal expansion of in LP-polynomial bases. Thus, the estimated LP-Fourier comparison density is given by:

8. Construct MaxEnt comparison density model based on selected LP-sufficient statistics

9. Estimate the relative entropy using the LP-parameter-based formula:

This quantifies the uncertainty that surrounds the initial tentative model . 10. Exploratory uncertainty analysis. The graphical visualization of plays a central role in data-driven knowledge discovery. It conveys the missing knowledge that was not anticipated by the a-priori assumed —tool for detecting the unexpected. It also provides insights as to how to change the misspecified to get a better model that fits the data well. The purpose of this exploratory interface is to encourages interactive data analysis and visual reasoning. 11. Model amendment via density-sharpening: Construct a class of reasonable models in the neighborhood of the reference model

for either use LP-Fourier canonical estimate or the LP-maxent estimate. The bottom line: Density-sharpening provides a systematic statistical model developmental process, describing how a relatively simple model can evolved into a more mature model when it comes in contact with new data. The is not a conventional nonparametric model, it is a ‘hybrid’ model that supplements domain-knowledge with data-knowledge.

A.3 Sub-linear Algorithms for Detecting Sparse Structure

The problem of developing ‘efficient’ algorithms for detecting sparse structure in big discrete distributions has recently attracted lots of attention from the Theoretical Computer Science (TCS) community. By ‘efficient’ we mean algorithms that require less data to correctly detect the presence of signals. We call an algorithm sub-linear if the sample complexity () is sub-linear in size of the domain ().

Some interesting new ideas and results recently appeared in the Theoretical Computer Science (TCS) literature under the banner of ‘Sub-linear Algorithms for Big data,’ ‘Big data Property testing,’ etc; see, for example, Canonne (2015), Indyk et al. (2012), Valiant and Valiant (2011), Rubinfeld (2012), Diakonikolas (2016), Orlitsky et al. (2003), Orlitsky and Suresh (2015), Jiao et al. (2015). They promise to give 20th-century pioneering statistical modeling ideas a 21st-century makeover with new ideas from TCS. They deserve the credit for asking the right question. However, all of these methods are too specialized and develops “new tricks” for each new related learning problem, which makes them practically inconvenient. This paper presents a more systematic and adaptable strategy, which starts with the following question (the holy grail of data analysis): How to find an efficient coordinate system adapted to the given data sets sitting on a high-dimensional discrete domain to deliver time and sample efficient computation? Section 3.9 of the main paper, performed an extensive numerical comparison of the power of different methods. Here we perform six further experiments. The detailed settings and results are summarized in Fig. 23, which further re-establish the power of LP-domain statistical learning for detecting sparse structure in big discrete distributions.

A.4 Additional Figures

Some figures of the main article have been moved to the Appendix to save space.

References

- Best and Rayner (1997) Best, D. and J. Rayner (1997). Goodness of fit for the binomial distribution. Australian Journal of Statistics 39(3), 355–364.

- Best and Rayner (1999a) Best, D. and J. Rayner (1999a). Goodness of fit for the poisson distribution. Statistics & probability letters 44(3), 259–265.

- Best and Rayner (1999b) Best, D. and J. Rayner (1999b). Goodness of fit for the poisson distribution. Statistics & probability letters 44(3), 259–265.

- Best and Rayner (2003a) Best, D. and J. Rayner (2003a). Tests of fit for the geometric distribution. Communications in Statistics-Simulation and Computation 32(4), 1065–1078.

- Best and Rayner (2003b) Best, D. and J. Rayner (2003b). Tests of fit for the geometric distribution. Communications in Statistics-Simulation and Computation 32(4), 1065–1078.

- Canonne (2015) Canonne, C. L. (2015). A survey on distribution testing: Your data is big. but is it blue? Electronic Colloquium on Computational Complexity (ECCC) 22(63).

- Chihara (2011) Chihara, T. S. (2011). An introduction to orthogonal polynomials. Courier Corporation.

- Diakonikolas (2016) Diakonikolas, I. (2016). Learning structured distributions. Handbook of Big Data, 267.

- Emerson (1968) Emerson, P. L. (1968). Numerical construction of orthogonal polynomials from a general recurrence formula. Biometrics, 695–701.

- Hoaglin (1980) Hoaglin, D. C. (1980). A poissonness plot. The American Statistician 34(3), 146–149.

- Hoaglin and Tukey (1985) Hoaglin, D. C. and J. W. Tukey (1985). Checking the shape of discrete distributions. Exploring Data Tables, Trends and Shapes, 345–416.

- Indyk et al. (2012) Indyk, P., R. Levi, and R. Rubinfeld (2012). Approximating and testing k-histogram distributions in sub-linear time. Proceedings of the 31st symposium on Principles of Database Systems, 15–22.

- Jiao et al. (2015) Jiao, J., K. Venkat, Y. Han, and T. Weissman (2015). Minimax estimation of functionals of discrete distributions. Information Theory, IEEE Transactions on 61(5), 2835–2885.

- Lancaster (1953) Lancaster, H. (1953). A reconciliation of , considered from metrical and enumerative aspects. Sankhyā: The Indian Journal of Statistics (1933-1960) 13(1/2), 1–10.

- Orlitsky et al. (2003) Orlitsky, A., N. P. Santhanam, and J. Zhang (2003). Always good turing: Asymptotically optimal probability estimation. Science 302(5644), 427–431.

- Orlitsky and Suresh (2015) Orlitsky, A. and A. T. Suresh (2015). Competitive distribution estimation: Why is good-turing good. Advances in Neural Information Processing Systems, 2134–2142.

- Rubinfeld (2012) Rubinfeld, R. (2012). Taming big probability distributions. XRDS: Crossroads, The ACM Magazine for Students 19(1), 24–28.

- Valiant and Valiant (2011) Valiant, G. and P. Valiant (2011). Estimating the unseen: an n/log (n)-sample estimator for entropy and support size, shown optimal via new clts. Proceedings of the forty-third annual ACM symposium on Theory of computing, 685–694.