Robust exploratory mean-variance problem with drift uncertainty

Abstract

We solve a min-max problem in a robust exploratory mean-variance problem with drift uncertainty in this paper. It is verified that robust investors choose the Sharpe ratio with minimal norm in an admissible set. A reinforcement learning framework in the mean-variance problem provides an exploration-exploitation trade-off mechanism; if we additionally consider model uncertainty, the robust strategy essentially weights more on exploitation rather than exploration and thus reflects a more conservative optimization scheme. Finally, we use financial data to backtest the performance of the robust exploratory investment and find that the robust strategy can outperform the purely exploratory strategy and resist the downside risk in a bear market.

Key words: model uncertainty, exploratory mean-variance analysis, robustness, exploration and exploitation, min-max problem

1 Introduction

In this paper, we focus on an exploratory mean-variance problem with drift uncertainty. The exploratory version of the mean-variance problem mainly refers to [16] and the concept of model uncertainty stems from [7]. The classical continuous-time mean-variance problem illustrates that the optimal strategy to balance the wealth state in different assets is represented by market parameters (mean return rate , volatility matrix , interest rate ) and optimal Lagrangian multiplier . Practical implementation of the mean-variance model directly relates to the level of market parameters, whereas in real financial markets accurate values of model parameters are unknown. It is common to estimate parameters through historical market data by a variety of calibration techniques [2, 11]; however, calibration results often disperse among empirical methods. As a result, it is quite hard to pick out a consensus estimation to match most of the market scenarios.

Recently, a novel approach is intentionally designed by Wang [16, 14] to solve the mean-variance portfolio problem via a reinforcement learning framework. More specifically, investors’ decision processes are replaced by relaxed controls, and a new trade-off relationship between exploration and exploitation appears. Exploration means that investors are encouraged to explore the optimal strategy using distributional rules, and each feedback control is a classical control sampled from the distributional rule. Exploitation means that with repetitive sampling rounds, investors gradually recover the optimal strategy by sample distributions rather than unknown market parameters , then the optimization is based on the information of control samples. Accordingly, the classical mean-variance problem has converted to an exploratory mean-variance problem. For more details about exploratory problem settings, we refer readers to [15]. The critical advantage of exploratory idea is that the convergence of control samples directly guides us how to optimize the portfolio without any knowledge about the accurate value of and ; so that we are able to skip the troubles brought by calibration as well as estimation errors. [16] shows that optimal distributional rule of control is Gaussian and the value function can be solved explicitly and represented by a set of redefined parameters. At the end, optimal parameter values are trained by a reinforcement learning algorithm and feeding the real market data.

The key algorithm “ENT-MV” in [16] implicates that, even though the portfolio optimization through the reinforcement learning algorithm does not directly involve and , new parameters in “ENT-MV” algorithm to be optimized are merely recombination of original parameters and . Once the system is trained to be in its optimality, the algorithm essentially provides an “optimal” estimation of and meanwhile. The methodology behind the “ENT-MV” algorithm is nothing but replacing the traditional parameter estimation by a learning-based one so that learned parameters guarantee the optimality of the portfolio problem. However, under the viewpoint of model uncertainty, this idea suffers the same drawback as the traditional statistical estimation: the estimation is completely driven by data, while data are not always effective, or even effective past data may wrongly predict the future.

In order to fill this gap, our purpose is to add model uncertainty into the exploratory mean-variance problem and find out the robust solution under model uncertainty. Model uncertainty is intrigued by the fact that investors often fail to have a complete knowledge about the model, herein we admit the uncertainty driven by unknown parameters (drift, volatility etc.) and attempt to consider the worst-case scenarios among all potential combinations of parameters in a confidence region. Optimal solutions of portfolio problems by choosing the worst market parameters are so-called robust solutions. Model uncertainty has been considered in pricing problem since [1, 9], and it was [6] who first brought the idea into portfolio problems. Later on, [3, 4] respectively extended robust problems to continuous-time and single-period models. Other related works consider various kinds of utility functions or model settings combining with uncertainty and robust solutions, [12, 5, 7]. Notice that literatures above merely considered drift uncertainty. When volatility uncertainty is involved, we refer to [8, 10, 13] for detailed description. It is known that the drift is the main source of uncertainty because the drift is the hardest part to be estimated precisely. In order to simplify the model and consider the most crucial factor, we only discuss the drift uncertainty in the current work.

We investigate on a robust exploratory mean-variance problem in this paper. It is reasonable to suspect that parameters calibration through market data are misspecified, so we add model uncertainty to the original problem in [16]. Among all the unknown market parameters we only consider the drift uncertainty here and express it by risk premium . Our purpose is to find the “worst” in an admissible closed convex set and the “best” control distribution based on the “worst” scenario. We call it the robust solution of the exploratory mean-variance portfolio optimization problem. Our model setting inherits [14] in exploratory part and [7] in drift uncertainty part. It was proved in [14] that with an exploration term, the optimal control distribution is Gaussian and the value function can be solved explicitly. When robustness is induced, the exploratory optimization becomes a min-max problem, so we find out the saddle point which can switch the and and solve the robust value function simultaneously. In this case, the “worst” coincidentally achieves the minimal norm in its admissible set. We further discuss the effect of the robust strategy comparing with misspecified purely exploratory strategies. Due to the appearance of the exploration term, the optimal exploratory strategy should make a balance between “exploration” (trying new strategies to obtain information from a larger range) and “exploitation” (optimize the main target of reducing the terminal variance). It is interesting to notice that a merely “exploitation” targeted investor can improve the terminal variance result from the optimal exploration strategy by choosing a misspecified which is smaller than the genuine market scenario . This is essentially an adjustment of the weight between exploration and exploitation. The phenomenon also matches the behavior of a robust investor: a more conservative investor reduce his/her market viewpoint to obtain more opportunity to reduce the terminal variance and emphasize exploitation rather than exploration. We verify the variance reduction effect by a numerical simulation and test the performance of robust investment by feeding different financial data and calibrating the parameters.

The paper is organized as follows. We introduce the exploratory mean-variance problem and induce drift uncertainty into the model in Section 2. Then the robust strategy, a min-max problem’s solution and its associated saddle-point are given in Section 3. In Section 4 we discuss the effect of the robust strategy. The parameter is calibrated and the performance of the robust strategy with real market data is presented in Section 5. In Section 6 we summarize all the results in the paper. Finally, in Appendix A, we finish some technical proofs which were postponed in the previous sections.

2 Portfolio models

Assume there are risky assets in the financial market. Given a filtered probability space , we define a -dimensional -adapted Brownian motion , where ′ stands for the matrix transpose. Assume the stock market follows a geometric Brownian motion

with , where is a deterministic volatility matrix whose inverse exists, and is an -adapted random drift which brings uncertainty to the model. Let be a deterministic risk-free rate. The stock price can be rewritten in terms of a risk premium process . We transfer the model uncertainty into the uncertain risk premium for convenience although the model uncertainty stems from . An investor’s control process is randomized to present exploration and its density function is given by where stands for the set of density functions of absolutely continuous probability measures with respect to the Lebesgue measure on . In this case, a discounted self-financing wealth process with its initial wealth state has the following dynamic

| (1) |

Following the setting of [14], without model uncertainty, the classical exploratory mean-variance problem is to solve the value function

| (2) |

where is the Lagrangian multiplier under the optimal control, is the default target of the wealth expectation at maturity, is the exploration intensity and the additional term111We denote it as entropy term henceforth.

is the opposite of Shannon-entropy. Optimizing the exploration is the same as maximizing the Shannon-entropy, and thus minimizing this additional term in (2). Intuitively speaking, an larger means more exploration: in particular, reduces the minimization problem (2) into a standard mean-variance problem, where the density function of the optimal control is degenerated, and the probability measure with respect to exploration is a Dirac measure. When is very large, exploitation is negligible; we only optimize the exploration term. In this case, the optimal density function is Gaussian because Gaussian distribution family maximizes the Shannon-entropy. In general, the entropy term in (2) encourages an investor to explore among the admissible controls and diversify his/her feedback strategies. As a result, the exploratory mean-variance problem becomes a trade-off between exploitation and exploration.

The appearance of uncertainty forces investors to consider the worst case in a range of models although the optimal strategy is selected. In this case, the optimization problem becomes a min-max problem

| (3) |

The following we make the precise assumptions on parameters and give admissible sets of and for the min-max problem (3):

Hypothesis 1.

-

•

, , , for .

-

•

, , , where is the -dimensional identity matrix.

-

•

Let be a closed convex subset of ; the admissible set is the set of processes such that for all .

-

•

Let ; the admissible set is the set of processes such that for all .

Remark 1.

is closed convex and imply that all admissible are either positive or negative for all . By convention we assume that for all and if for any . This assumption is the same as the one in [7].

Our target is to solve (3) and prove a saddle point property for the problem.

3 Optimal solution to robust exploratory mean-variance problem

We derive an explicit result on a saddle point property for (3) and solve the exploratory mean-variance problem with drift uncertainty in this section. The dynamic programming argument shows that

so the HJB equation of the robust exploratory mean-variance problem is

| (4) | ||||

We split our solution into two steps. First, for any fixed specific market scenario where the model uncertainty is absent, we solve a classical exploratory mean-variance problem with a fixed drift. Then we find a “worst” scenario in the admissible set and prove that the optimal policy under the “worst” scenario is an equilibrium pair as well as the solution of (4). Two steps are presented in details in Subsection 3.1 and Subsection 3.2 respectively.

3.1 Classic exploratory solution by a HJB approach

First we consider the classical solution of the exploratory problem without model uncertainty, which follows the arguments as [14]. For any and , we define

Proposition 1 (Theorem 1 in [14]).

With any fixed , the optimal density function with respect to problem (2) is Gaussian, and the value function is obtained by

Proof.

Fix . For any fixed time , the classical exploratory problem without model uncertainty has the optimal control density function

| (5) |

which follows a high-dimensional Gaussian distribution. Assume is the Gaussian random variable whose probability density function at is . It is easy to verify that where and . More specifically, the optimal density function of the control process is

| (6) | ||||

Furthermore, the Shannon-entropy term at time is

Plug (6) back into (4) with the fixed , 222We take the following expectation of or quadratic form of under the optimal strategy’s probability measure.

We guess the solution has the form , so and it is clear to solve by ODE systems and their solutions are

Hence, the classical exploratory mean-variance problem has the following explicit solution for the value function

A simple computation derives

The wealth dynamic (1) under the optimal control distribution (6) becomes

The last equation above can be treated as an ODE for , whose solution provides the optimal Lagrangian multiplier . The value function at time 0 for the minimization problem (2) is

∎

Now we choose the worst based on the solution of . Regarding the representation formula of , it is obvious that the worst case condition is given by for each

| (7) |

where . The minimum of is attainable and it is denoted by . We note that is strictly positive because is a closed convex subset of . If is given in (7) for each , then is the solution of .

3.2 Robust solution and saddle point property

Based on the solution of classical exploratory mean-variance problem, we inherit the same model setting and define a specific control distribution by

| (8) |

Again, we assume is a Gaussian random variable whose probability density function at time is .

Theorem 2.

Proof.

For any market parameter , the wealth dynamic is

and

Apply Itó’s formula to ,

Let , , , then satisfies the ODE whose solution is

| (9) | ||||

We can use a similar argument as Proposition 1 and obtain

To compute , the entropy term is

The terminal preference term is

is the sum of the above two terms:

If the market uncertainty is achieved by , specially,

Then

Since the convexity of guarantees that for any , the first term is non-negative. Furthermore, holds true for any positive function . As a result, both two terms are non-negative so holds true for all .

So far we have

| (10) |

and actually , so all the inequalities in (10) become equalities. This directly induces that the robust exploratory mean-variance problem has the solution , and this is also the saddle point of . ∎

The solution of the robust exploratory portfolio optimization is proved to be related to a min-max problem. A saddle point pair reaches the equilibrium of the robust investor’s market opinion and his/her investment behavior. The robust investor always has a conservative attitude towards the mean-return rate and is likely to reduce the investment on risky assets. Next we will analyze the effect of adding the robustness to portfolio strategies.

4 Effect of robust strategies

Assume the genuine Sharpe ratio in risky market to be . The discounted risky asset prices follow the dynamic

Due to the model uncertainty, an investor cannot precisely estimate ; instead, a misspecified Sharpe ratio is chosen to determine his/her strategies. The robust investor further adjusts to as his/her worst-case perspective of market risk premium, as shown in Theorem 2. We have in all four mean-variance portfolio management cases to compare in the following paragraphs: a misspecified investor with neither exploration nor robustness [17]; a misspecified investor with no exploration but robustness [7]; a misspecified investor with exploration but no robustness [14]; a misspecified investor with both exploration and robustness. For simplicity, we consider the Sharpe ratio and volatility matrix are constants in this section.

4.1 Misspecification and robustness without exploration

Previous literature [17, 7] have provided complete results when exploration is not involved. The optimal strategy of a misspecified investor is . It can be verified that and the optimal terminal wealth distribution under model misspecification is

We further know that : under model misspecification, the mean of the terminal wealth remains invariant; however, the variance deviates from the optimal one and . It concludes that an investor with a misspecified estimation of the Sharpe ratio will suffer from a larger terminal variance than the correct model .

A robust investor always uses a smaller Sharpe ratio (in the sense of norm) to replace his/her original estimation . A direct effect of robustness is to compare with . Fix any dimension , we split the Sharpe ratio adjustment into three cases:

-

•

: the investor overestimates the Sharpe ratio; the robust strategy enables the misspecified one to approach the genuine risk premium (though insufficiently) and reduce the terminal variance. The robust strategy is superior to the misspecified one.

-

•

: the investor underestimates the Sharpe ratio; the robustness exaggerates the deviation and thus increases the terminal variance. In this case, the robust strategy is inferior to the misspecified one.

-

•

: the investor overestimates the Sharpe ratio but overreacts during the risk premium adjustment. Whether the variance can be reduced depends on the comparison of and . Specially, if , we have .

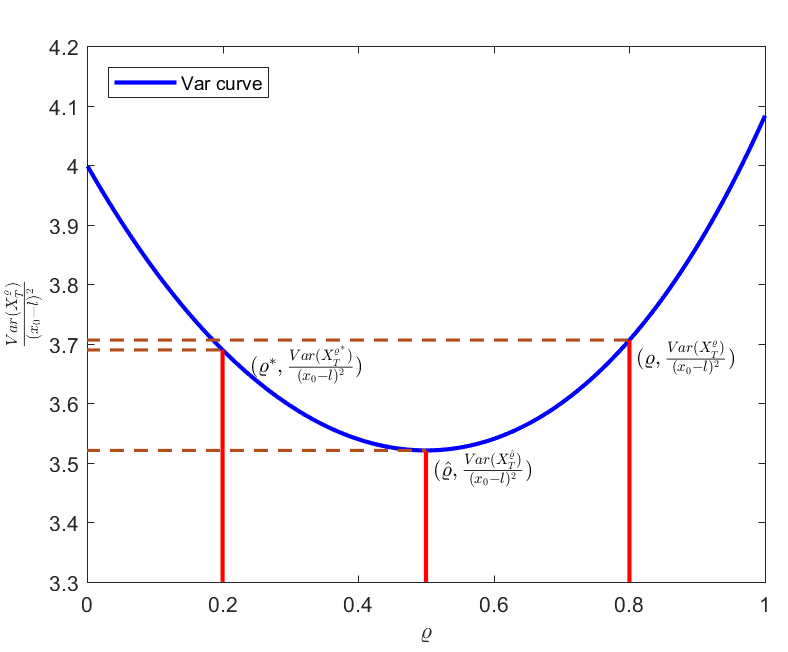

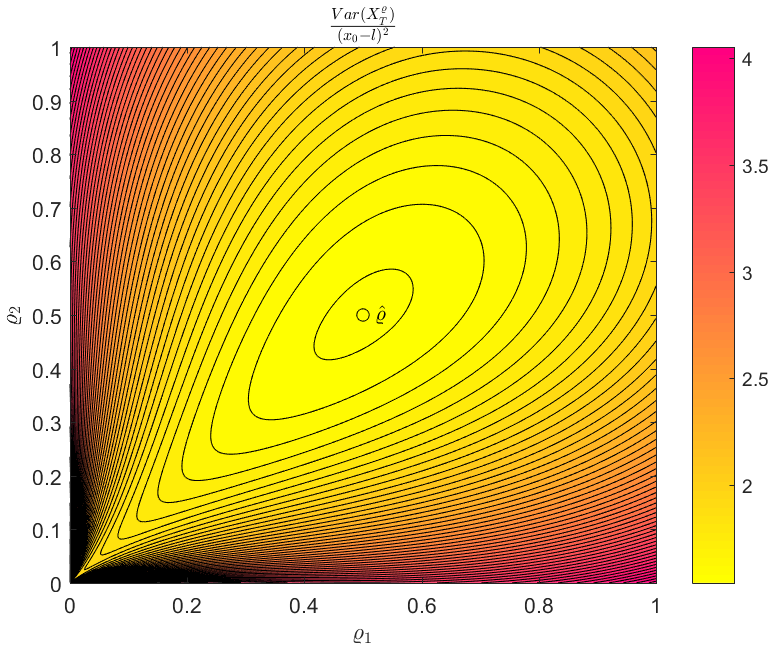

The asymmetric variance structure mentioned in the last situation is illustrated as follows. Figure 1(a) depicts the variance curve in the 1-dimension risk premium and parameters are set by , , , and the curve is plotted for . The risk premium reduction from to crosses the optimal value symmetrically, but the variance is still reduced slightly. The 2-dimensional variance contour of in the unit square with the center is shown in Figure 1(b). The variance surface reaches the basin when . When deviates from , the path from to the origin is flatter and the opposite direction is steeper. In conclusion, the variance contour (curve) leans to the side of smaller . Without any priori knowledge, reducing is more likely to reduce variance than to increase variance. The robust strategy makes sense in accordance with the asymmetric variance structure.

4.2 Misspecification and robustness with exploration

It was shown in [16] that the exploration does not affect the mean of the terminal wealth distribution, so still holds. On the other hand, the variance is adjusted as the appearance of the exploration. Assume an investor precisely estimates the market risk premium to be , the terminal variance is

| (11) | ||||

where and its solution is provided in (9). The terminal variance is increased by the term due to the exploration. If the investor selects a misspecified market scenario instead of , according to Proposition 1, the investor’s policy is given as the Gaussian distribution

| (12) |

We have the following Proposition to characterize the variance structure of , whose conclusion is slightly different from the case without exploration.

Proposition 3.

Assume the market risk premium is and an investor decides his/her strategy by a misspecified . Regard as a function of , then such that the terminal variance attains a unique global minimum at .

Proof.

Step 1. Under the misspecified risk premium , the investor’s wealth process is given by

We again represent by the term of . With the same argument as (9), has its dynamic and solution

Specially, when , the solution coincides with . The optimal Lagrangian multiplier is given by . Therefore, the variance under is

| (13) | ||||

Again, coincides with in (11) by taking limit . Furthermore, a direct computation indicates that is smooth at .

Next, we compute the gradient of with respect to to find the minimum point. Consider two terms in separately,

The necessary condition of the exploration term to attain its minimum is

the stationary point of which is . Set the gradient of the classical variance term to be zero, i.e.

the stationary point of which is . The stationary point of is

| (14) |

(14) indicates that the stationary point of has the same direction as .

Step 2. For any given , , any rotation transformation from to where and , we have . This is because , and thus . The first term of (13) is an increasing function of ; the second term is a decreasing function of . As a result, is always suboptimal to . Thus we can simplify the minimization problem by restricting on the line and find the optimal to minimize the variance instead.

Step 3. Consider two terms in (13) again. is a strictly convex function of . Therefore its stationary point attains its global minimum. For the second term restricts on the line , is a strictly convex function of when . The proof of two functions to be strictly convex is provided in Appendix A. The stationary point (or ) attains the global minimum of the second term. is the sum of two strictly convex functions along , so it is strictly convex as well and it has a unique global minimum. The stationary point (14) attains the global minimum and is the root of

Since the two terms of has their global minimum points and respectively, the global minimum point of is a weight between its two nonnegative terms and thus . ∎

Now we consider the effect on variance reduction of the robust strategy.

Corollary 4.

For an investor taking the robust strategy to adjust his/her misspecified market viewpoint from to , where minimizes norm of in the admissible set . Fix any individual asset , then the conclusion is the same as the no exploration case in Subsection 4.1, except that the comparison object is replaced by :

-

•

: the robust strategy helps reduce the terminal variance but not sufficiently. The robust strategy is superior to the misspecified one.

-

•

: the robustness exaggerates the deviation and thus increases the terminal variance. In this case, the robust strategy is inferior to the misspecified one.

-

•

: the robust strategy overreacts during the risk premium adjustment. Whether the variance can be reduced depends on the comparison of and . Specially, if , then we have .

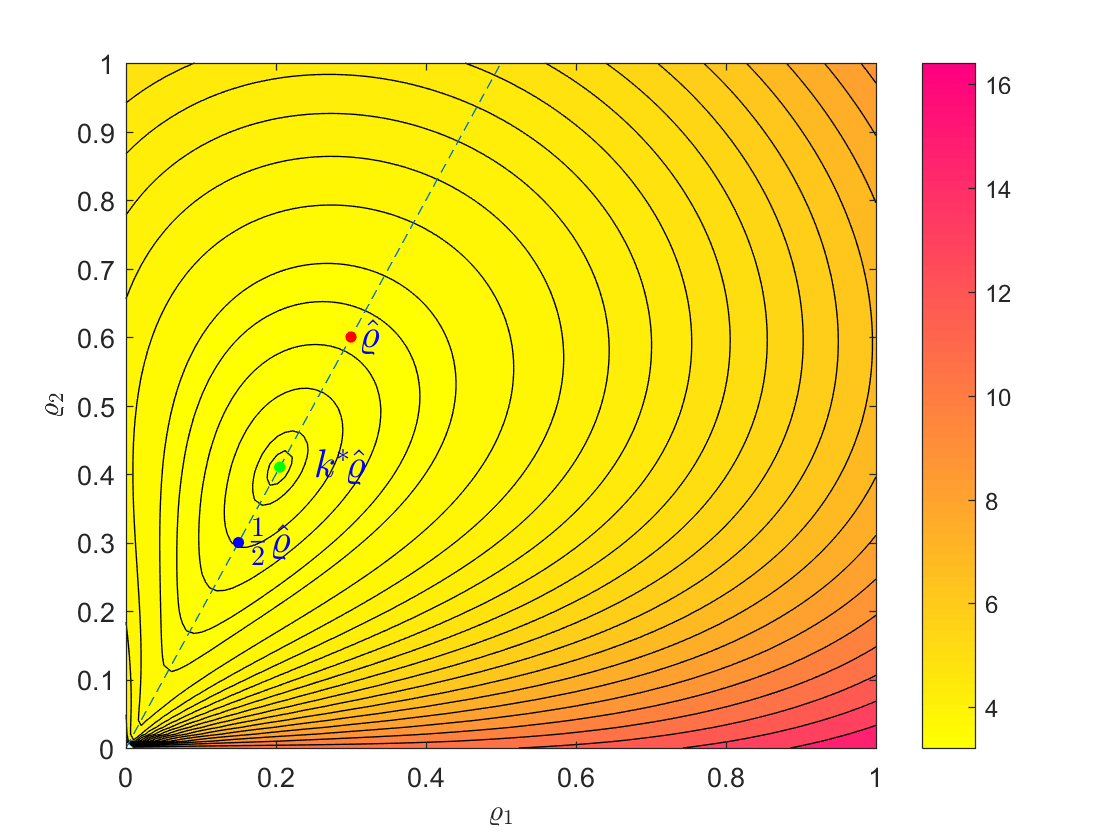

Figure 2 depicts the 2-dimensional variance contour of the exploratory mean-variance problem where the parameters are given by , , , . The red dot in Figure 2 is the optimal solution of the terminal variance term , the blue dot is the optimal solution of the additional exploratory term in the terminal variance, whereas the minimal variance point is the green dot and in this case. The dashed line going through the origin and always leads to the minimal variance direction and we can simplify the problem into merely searching this line.

Remark 2.

-

(a)

The involvement of exploration shifts the minimum point of variance from to where . This indicates that based on the precise estimation of , a minimal-variance targeted investor should be even further conservative; the market risk premium is rescaled by . This phenomenon provides a reasonable explanation why robustness makes sense: when exploration is involved, the robust strategy with has more chance to reduce the variance than with due to the change of the minimum point from to . The behavior of the robust strategy naturally matches the target of minimizing the variance.

-

(b)

We know that the value function consists of the terminal variance and the entropy term. is optimal for the value function (3) and is the minimizer of the terminal variance. The risk premium adjustment from to reduces the terminal variance but meanwhile deviates the optimality of the original problem (3). This is because is a decreasing function of in the entropy, and the entropy term increases as decreases. We know that the terminal variance minimization is the effect of exploitation, and the entropy is the effect of exploration. An investor who searches for instead of essentially focus more on exploitation rather than exploration by rebalancing the weight between them.

5 Numerical experiments and results

Having presented the theoretical formulation of the robust exploratory problem and the robust strategy against misspecification, now we focus on the real performance of the robust style investment under the exploratory background. In this section, first we simulate the wealth process (1) and compare the numerical behavior of the robust strategy against a misspecified one. Then we use the real SPX data to illustrate how robustness affects exploration and parameter calibration.

5.1 Performance comparison by wealth process simulation

Given the uniform time mesh and the partition , the discrete wealth process of (1) is

| (15) |

and is sampled from the distribution (12) at . We simulate trajectories and consider the investor to choose a misspecified and the robust scenario simultaneously. The actual market risk premium drives the wealth evolution but it is unknown to the investor.

Algorithm 1 implements the simulation of the misspecified scenario and the robust strategy parallelly. Theoretically all the scenarios share the same terminal expectation , so we directly compare the behavior of different scenarios by their variances. We choose the convex admissible set to be two particular types: a cube and an elliptic. For the cube where the investor’s estimation , the robust scenario is always regarded as . Hence, the projection of in is the vertex that all dimensions choose their left endpoint respectively. For the elliptic whose center is the misspecified scenario , the projection keeps the direction invariant.

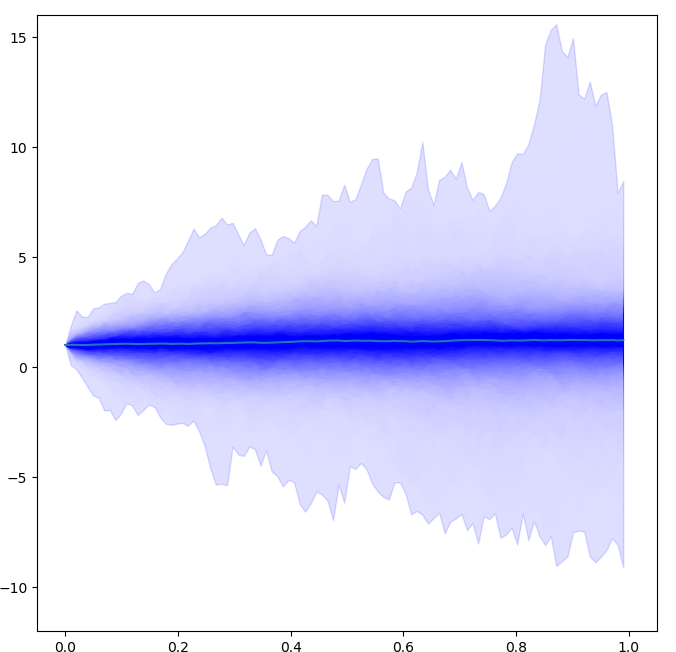

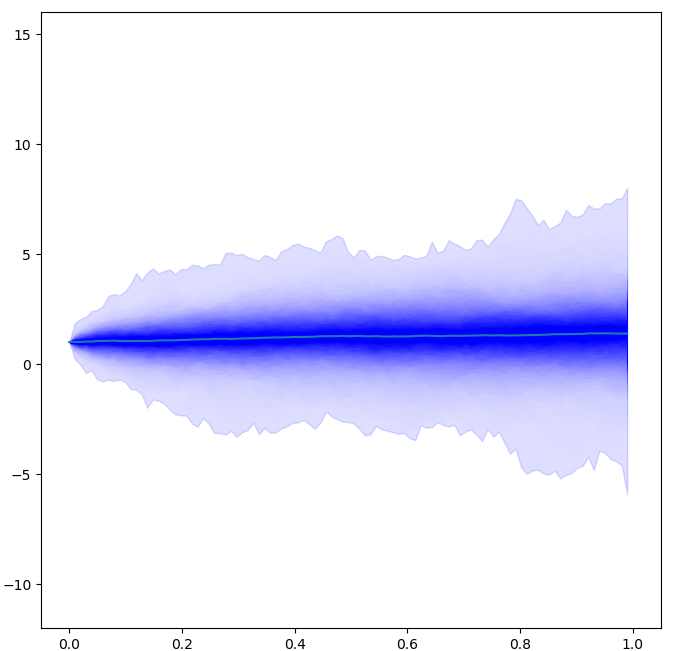

Figure 3 depicts simulated paths of wealth processes and . In these two graphs, the darker the color, the more centralized the paths. It is obvious that the robust strategy (b) has a smaller envelope than the one without robustness (a). The parameters are set by: , , , , , time mesh size and sample size . We assume the diagonal volatilities , and the correlation matrix

We can obtain the volatility matrix by taking the matrix square root of the variance matrix . It is further assumed that the correct risk premium , but an investor chooses . The robust strategy replaces by . Following Algorithm 1, the numerical values of two terminal variances are: , . In this implementation, we choose the identity risk premium among assets for convenience. Although after the robust adjustment is further from than , it indeed reduces the variance. The expectation of simulated terminal wealth converges to target in both cases, which accords to the theoretical result.

| misspecified | cube convex set | elliptic convex set | |||||

|---|---|---|---|---|---|---|---|

| robust | robust | ||||||

| [ 0.4, 0.5, 0.5 ,0.7 ] | 3.664 | 0.1 | [ 0.30, 0.40, 0.40, 0.60 ] | 3.313 | 0.2 | [ 0.330, 0.413, 0.413, 0.578 ] | 3.305 |

| 0.2 | [ 0.20, 0.30, 0.30, 0.50 ] | 3.112 | 0.4 | [ 0.261, 0.326, 0.326, 0.456 ] | 3.090 | ||

| 0.3 | [ 0.10, 0.20, 0.20, 0.40 ] | 2.909 | 0.6 | [ 0.191, 0.239, 0.239, 0.335 ] | 2.868 | ||

| 0.35 | [ 0.05, 0.15, 0.15, 0.35 ] | 2.927 | 0.8 | [ 0.122, 0.152, 0.152, 0.213 ] | 2.949 | ||

| [ 0.15, 0.15, 0.35 ,0.4 ] | 3.018 | 0.05 | [ 0.10, 0.10, 0.30, 0.35 ] | 2.937 | 0.1 | [ 0.104, 0.104, 0.243, 0.278 ] | 2.843 |

| 0.1 | [ 0.05, 0.05, 0.25, 0.3 ] | 2.958 | 0.2 | [ 0.058, 0.058, 0.136, 0.156 ] | 2.936 | ||

| 0.15 | [ 0, 0, 0.20, 0.25 ] | 2.996 | 0.3 | [ 0.013, 0.013, 0.029, 0.034 ] | 3.019 | ||

| [ 0.5, 0.4, 0.3 ,0.2 ] | 3.231 | 0.05 | [ 0.45, 0.35, 0.25, 0.15 ] | 3.218 | 0.2 | [ 0.315, 0.252, 0.189, 0.126 ] | 3.027 |

| 0.1 | [ 0.40, 0.30, 0.20, 0.10 ] | 3.071 | 0.3 | [ 0.222, 0.178, 0.133, 0.089 ] | 2.986 | ||

| 0.15 | [ 0.35, 0.25, 0.15, 0.05 ] | 3.112 | 0.4 | [ 0.130, 0.104, 0.078, 0.052 ] | 2.965 | ||

| 0.2 | [ 0.30, 0.20, 0.10, 0 ] | 3.143 | 0.5 | [ 0.037, 0.030, 0.022, 0.015 ] | 3.096 | ||

More simulation results are presented in Table 1. This time we keep the parameters the same as those in last experiment except and larger sample size . The investor will apply different and use different convex set to describe the robust scenarios. In the cube type, is the distance from to endpoints so . According to Table 1, in most cases robustness reduces the variance. Furthermore, there is more mistake tolerance to adopt an underestimated risk premium than an overestimated one. Finally, the elliptic convex type is more sensitive than the cube type, and possibly approaches the basin of the variance surface even though the direction of is far from .

5.2 Performance test by real market data

Lastly, we consider the performance of the robust exploratory mean-variance portfolio optimization in a real market test. In order to discuss the behavior of robust/exploratory strategies in different market patterns, we choose two benchmarks separately: SPX daily data in US market (bull) and SSE Composite index daily data in Chinese market (bear) among last 15 years, see Figure 4.

The risk free rate is chosen to be for price discounting. For convenience, we assume all the parameters to be calibrated are constants and only 1 risky asset to be invested.

In each case, we split the stock price series into three parts: first 7 years to be train data, next 3 years to be valid data and last 3 years to be test data. We clip each data series with 1-year length successively and collect them to generate the data pool. The investment period is fixed to be . SPX data has trading days per year in average while the number in SSE composite index is . Unknown market parameters , and are calibrated through training data and validation data. Finally we input the calibrated parameters into the test data and observe the investment performance.

Our calibration method as well as the portfolio optimization are based on the minimization problem (2) and the optimal strategy distribution (12). The loss function of the minimization problem contains two terms: the terminal variance and the exploration loss equals to The terminal variance is a function of and the exploration loss is a function of .

Since the exploration loss is an increasing function of , it is ineffective to recover the volatility level of the real data by minimizing the exploratory value function (2). Instead, we estimate by computing the historical volatility

where is the market price at day in -length rolling window. Then we train the parameter by the stochastic gradient descend scheme and update the optimal Lagrangian multiplier by , where is the exponentially decaying learning rate defined by .

We further set the hyper-parameters by: batch size , training steps , initial wealth , target terminal wealth , exploration intensity . should be chosen properly so that it is able to keep balance between the terminal variance loss and the exploration loss.

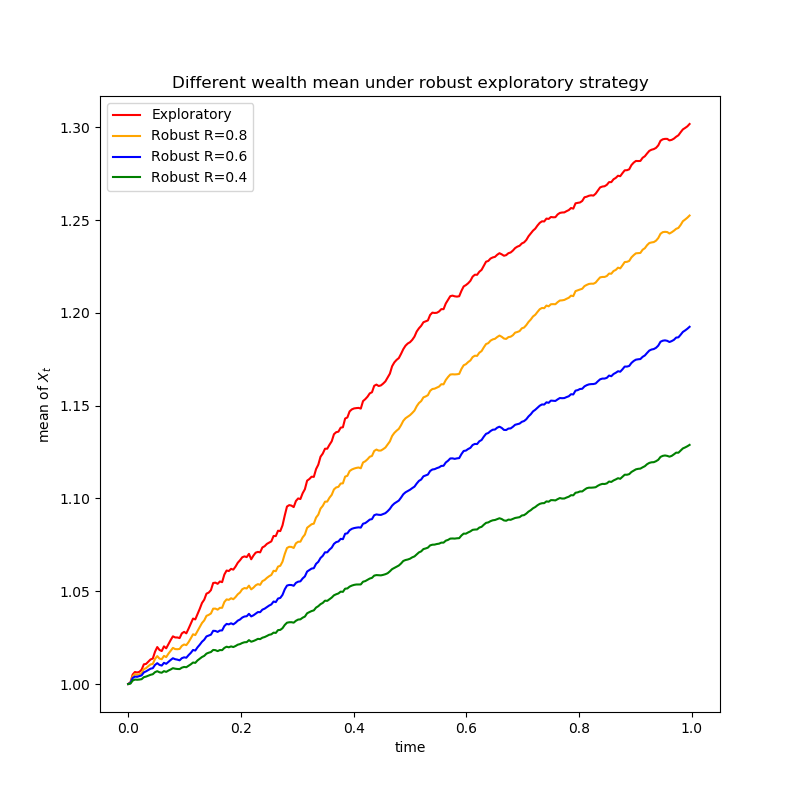

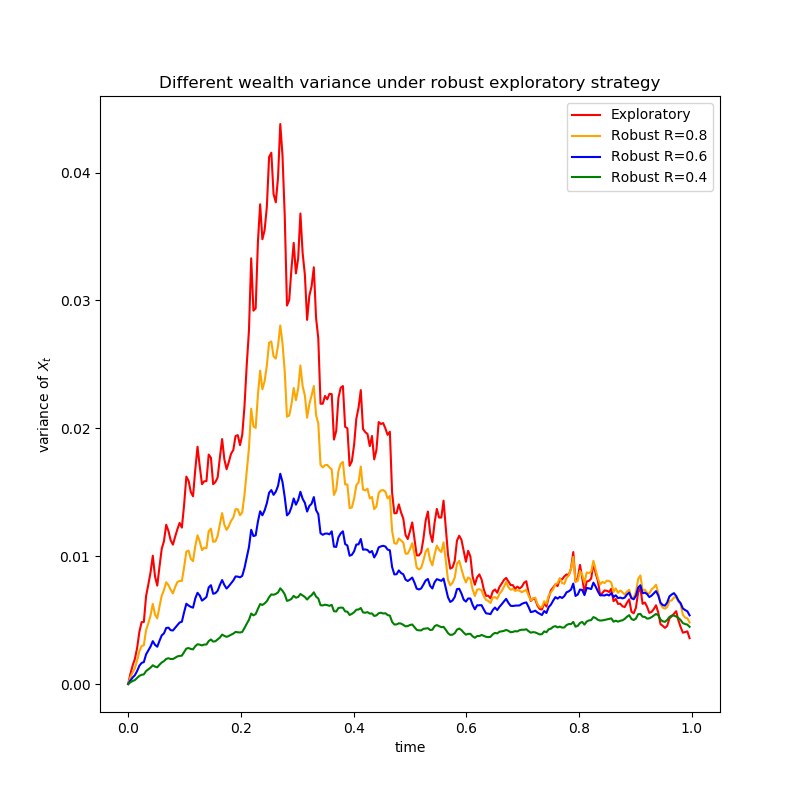

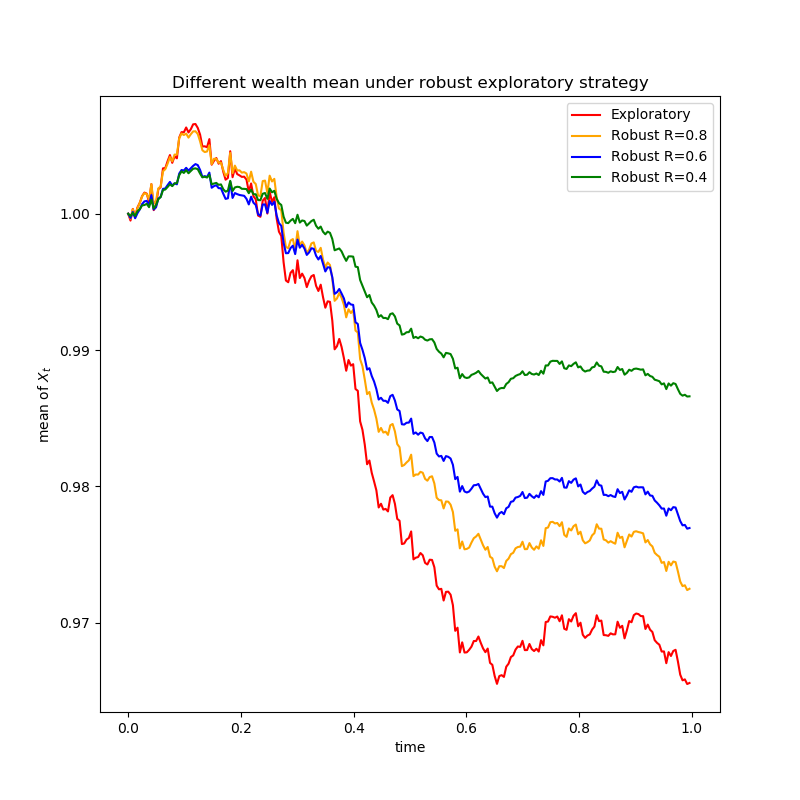

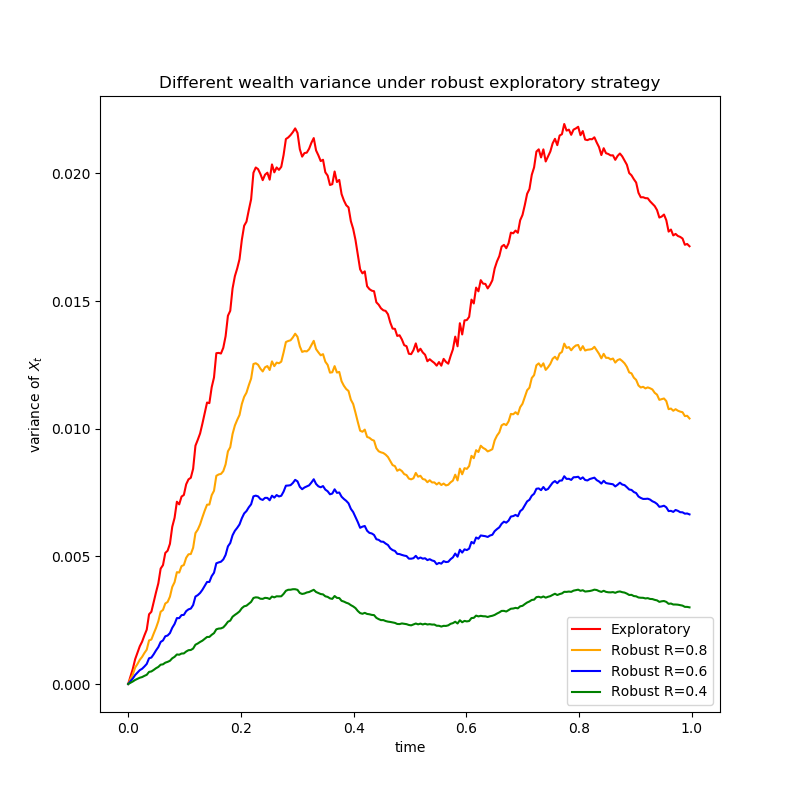

Algorithm 2 provides the performance test based on two real market data. Under the background of model uncertainty, it is suspected that the value estimated from market data is still misspecified. A robust investor further cuts down the estimated value of to for his/her own market viewpoint where respectively. The key point is to compare the numerical results of different strategies (robust and no robust) in different market patterns (bull and bear). The investment performances are shown in Table 2, Figure 5 and Figure 6.

| benchmark | SPX | SSE | ||||||

| calibration | ||||||||

| results | 1.104 | 2.025e-1 | 1.236e-1 | 1.418 | 1.220e-1 | 2.982e-1 | 1.721e-1 | 3.066 |

| strategies | Robust exploratory | exploratory | Robust exploratory | exploratory | ||||

| R | 0.4 | 0.6 | 0.8 | 1.0 | 0.4 | 0.6 | 0.8 | 1.0 |

| 4.416e-1 | 6.623e-1 | 8.832e-1 | 1.104 | 4.881e-2 | 7.321e-2 | 9.762e-2 | 1.220e-1 | |

| test loss | 2.237e-1 | 2.053e-1 | 2.028e-1 | 2.156e-1 | -3.529 | -3.525 | -3.521 | -3.514 |

| test mean | 1.126 | 1.193 | 1.252 | 1.301 | 9.866e-1 | 9.769e-1 | 9.725e-1 | 9.656e-1 |

| test variance | 4.285e-3 | 5.230e-3 | 4.499e-3 | 3.419e-3 | 3.002e-3 | 6.644e-3 | 1.040e-2 | 1.715e-2 |

In the Chinese market, both valid region and test region basically go through the bear market, so the optimality of investment strategy under train data does not completely transfer to the test region. Despite following the optimal exploratory strategies, the market misspecification leads to negative profit in mean. In this situation, robustness helps reduce both the risk and the profit loss simultaneously. As a result, in both mean and variance, the robust strategy outperforms the purely exploratory strategy. On the contrary, the US market has gone through a remarkable long run bull. The robust strategy seems to be too conservative to adapt to the US market because in both mean and variance it underperforms the purely exploratory strategy.

In conclusion, whether robustness makes sense is most likely related to the financial market background. Compared with exploratory strategy, robustness takes advantage in bear market and disadvantage in bull market. A conservative investor adopts the robust strategy rather than a pure exploratory one in order to resist the downside risk, even though he will potentially miss the high profit in uptrend market.

6 Conclusion

The robust exploratory mean-variance analysis was investigated in this paper. Based on the previous work of exploratory mean-variance problem, we inherited the exploratory wealth dynamic setting but further assumed there is model uncertainty in drift. Under the background of misspecification, a robust investor who always considers the worst scenario should seek for the sharpe ratio with minimal norm in the specific admissible set as his/her market perspective, and this is also a saddle-point of the min-max problem. Theoretically, an investment under a misspecified deviates the target of minimizing the terminal variance, while the robust viewpoint has more opportunity to reduce the deviation than to exaggerate it. Market parameter calibration in exploratory mean-variance optimization is based on the balance between exploration and exploitation. It can be justified that a robust investor’s behavior is equivalent to transferring additional weight from exploration to exploitation. Finally, financial data backtests show that robustness outperforms the pure exploration and helps resist the downside risk in a bear market, while it underperforms in a bull market.

Appendix A The proof of convexity in Proposition 3

Lemma 5.

Let and be smooth and convex functions. Assume and on . Assume also satisfies either or is invertible. Then is strictly convex.

Proof.

Compute the Hessian matrix of :

With the assumptions on and , we have, for arbitrary ,

Then is also positive definite, which implies is strictly convex. ∎

Theorem 6.

The function is a strictly convex function of .

Proof.

Let where and is fixed. Let when and when . Then is invertible and . We also have the derivative of

Let , has the critical point , and attains the global minimum. So for all , together with we have is strictly increasing. The second order derivative of is given by

Again let . Then , which imply is strictly. Together with , we have when , and when . Then when , and as well, so is strictly convex. Applying Lemma 5, is strictly convex. ∎

Lemma 7.

Let and be smooth functions. Assume and on . Assume also on . Then is strictly convex.

Proof.

The strict convexity of function implies

whereas and . Then and thus is strictly convex. ∎

Theorem 8.

The function is a strictly convex function of on .

Proof.

It is equivalent to prove is a strictly convex function on . Choosing , then . Denote its second order derivative by

| (16) |

We note that can be decomposed as , where and . We can consider the two terms separately. For , we have on

| (17) | ||||

so is an increasing function on . Therefore, is the lower bound of and is the upper bound of on . We further define . Then the second term can be represented by

| (18) | ||||

| (19) | ||||

thus and are strictly decreasing on , , , on , is strictly decreasing, and on . In order to satisfy conditioning on when , it suffices to prove that , which is, on . We let , its derivative is . It is known that for any , so the second term in is positive on . We then define and claim that on . According to (19), the claim is equivalent to

| (20) |

It is convenient to do the change of variable and thus the left hand side of (20) becomes

Next, we compute the derivatives of and we have on

Together with , we have on and thus the claim on holds. Therefore, on . Together with , we have . It implies that on and thus defined in (16) is positive on . According to Lemma 7, we conclude that is strictly convex and the proof is completed. The graph of function are plotted in Figure 7 (b). ∎

Remark 3.

has second order derivative

and . However, it is rather tedious to prove on . Instead, we plot the graph of in Figure 7 (a).

References

- [1] M. Avellaneda, A. Levy, and A. Parás, Pricing and hedging derivative securities in markets with uncertain volatilities, Applied Mathematical Finance, 2 (1995), pp. 73–88.

- [2] H. Berestycki, J. Busca, and Florent, Asymptotics and calibration of local volatility models, Quantitative Finance, 2 (2002), pp. 61–69.

- [3] Z. Chen and L. Epstein, Ambiguity, risk and asset returns in continuous time, Econometrica, 70 (2002), pp. 1403–1443.

- [4] D.Goldfarb and G.Iyengar, Robust portfolio selection problems, Mathematics of Operations Research, 28 (2003), pp. 1–200.

- [5] A. Gundel, Robust utility maximization for complete and incomplete market models, Finance and Stochastics, 9 (2005), pp. 151–176.

- [6] L. Hansen and T. J.Sargent, Robust control and model uncertainty, American Economic Review, 91 (2001), pp. 60–66.

- [7] H. Jin and X. Zhou, Continuous-time portfolio selection under ambiguity, Mathematical Control and Related Fields, 5 (2015), pp. 475–488.

- [8] Q. Lin and F. Riedel, Optimal consumption and portfolio choice with ambiguity, Economic Theory, 71 (2021), pp. 1189–1202.

- [9] T. Lyons, Uncertain volatility and the risk free synthesis of derivatives, Applied Mathematical Finance, 2 (1995), pp. 117–133.

- [10] A. Matoussi, D. Possamaí, and C. Zhou, Robust utility maximization in non-dominated models with 2bsdes: the uncertainty volatility model, Mathematical Finance, 25 (2012), pp. 258–287.

- [11] R. C. Merton, On estimating the expected return on the market: An exploratory investigation, Journal of Financial Economics, 8 (1980), pp. 323–361.

- [12] C. Skiadas, Robust control and recursive utility, Finance and Stochastics, 7 (2003), pp. 475–489.

- [13] R. Tevzadze, T. Toronjadze, and T. Uzunashvili, Robust utility maximization for a diffusion market model with misspecified coefficients, Finance and Stochastics, 17 (2013), pp. 535–563.

- [14] H. Wang, Large scale continuous-time mean-variance portfolio allocation via reinforcement learning, arXiv:1907.11718v2, (2019).

- [15] H. Wang, T. Zariphopoulou, and X. Zhou, Reinforcement learning in continuous time and space: A stochastic control approach, Journal of Machine Learning Research, 21 (2020), pp. 1–34.

- [16] H. Wang and X. Zhou, Continuous-time mean-variance portfolio selection: A reinforcement learning framework, Mathematical Finance, 30 (2020), pp. 1273–1308.

- [17] X. Zhou and D. Li, Continuous-time mean variance portoflio selection: A stochastic lq framework, Applied Mathematics and Optimization, 42 (2000), pp. 19–33.