Maximum weighted likelihood estimator for robust heavy-tail modelling of finite mixture models

Abstract

In this article, we present the maximum weighted likelihood estimator (MWLE) for robust estimations of heavy-tail finite mixture models (FMM). This is motivated by the complex distributional phenomena of insurance claim severity data, where flexible density estimation tools such as FMM are needed but MLE often produces unstable tail estimates under FMM. Under some regularity conditions, MWLE is proved to be consistent and asymptotically normal. We further prove that the tail index obtained by MWLE is consistent even if the model is misspecified, justifying the robustness of MWLE in estimating the tail part of FMM. With a probabilistic interpretation for MWLE, Generalized Expectation-Maximization (GEM) algorithm is still applicable for efficient parameter estimations. We therefore present and compare two distinctive constructions of complete data to implement the GEM algorithm. By exemplifying our approach on two simulation studies and a real motor insurance data set, we show that comparing to MLE, MWLE produces more appropriate estimations on the tail part of FMM, without much sacrificing the flexibility of FMM in capturing the body part.

Keywords: Generalized Expectation-Maximization algorithm; M-estimator; Random truncation; Regularly varying function; Multimodal distribution

1 Introduction

Modelling insurance claim sizes is not only essential in various actuarial applications including pricing and risk management, but is also very challenging due to several peculiar characteristics of claim severity distributions. Claim size distributions often exhibit multimodality for small and moderate claims, when there exists unobserved heterogeneities possibly reflected by different claim types and accident causes, or when the observed samples come from a contaminated distribution. Also, the distribution is usually heavy-tail in nature, where very large claims occur with a small but non-negligible probability. Due to the highly complex distributional characteristics, we have to admit the impossibility to perfectly capture all the distributional features using a parametric model without excessively large number of parameters (which results in over-fitting). When model misspecification is unavoidable, correct specification of the tail part is more important than finely capturing the distributional nodes of smaller claims which are rather immaterial to the insurance portfolio, because the large claims are the losses which can severely damage the portfolio. As a result, we need to specify an appropriate distributional model with a justifiable statistical inference approach which not only preserves sufficient flexibility to appropriately capture the whole severity distribution, but also puts a particular emphasis on robust estimation of the tail.

Existing actuarial loss modelling literature focus a lot on the model specifications, by introducing various distributional classes to capture the peculiar characteristics of claim severity distributions. Notable directions include extreme value distributions (EVD, see e.g. Embrechts et al. (1999)) to capture the heavy-tailedness, composite loss modelling (see e.g. Cooray and Ananda (2005), Scollnik (2007), Bakar et al. (2015) and Grün and Miljkovic (2019)) to cater for mismatch between body and tail behavior of claim severity distributions, and finite mixture model (FMM, see e.g. Lee and Lin (2010) and Miljkovic and Grün (2016)) to capture distributional multimodality. In particular, FMM is becoming an increasingly useful smooth density estimation tool in insurance claim severity modelling perspective, due to its high versatility theoretically justified by denseness theorems (Lee and Lin (2010)). The mismatch between its body and tail behavior can also be easily modelled by FMM by selecting varying distributional classes among mixture component functions (see e.g. Blostein and Miljkovic (2019) and Fung et al. (2021)), including both light-tailed and heavy-tailed distributions. In both actuarial research and practice, statistical inferences of FMM are predominantly based on maximum likelihood estimation (MLE) with the use of Expectation-Maximization (EM) algorithm.

Nonetheless, MLE would often cause tail-robustness issues where the tail part of the fitted model is very sensitive to model misspecifications – when the observations are generated from a perturbed and/or contaminated distribution. As evidenced by several empirical studies including Fung et al. (2021) and Wuthrich and Merz (2021), the estimated tail part of the FMM obtained by MLE can be unreliable and highly unstable in most practical cases. This is mainly due to the overlapping density regions between mixture components modelling small to moderate claims (body) and those modelling large claims (tail). Hence, the estimated tail distribution will be heavily influenced by some smaller claims if FMM is not able to fully explain those small claims, which is always the case in practice due to the distributional complexity of real dataset impossible to be perfectly captured even by flexible density approximation tools including FMM. Under MLE approach, FMM may fail to extrapolate well the large claims, and this would lead to serious implications to insurance pricing and risk management perspectives. It is therefore natural to question whether or not MLE is still a plausible approach in modelling actuarial claim severity data, and whether or not there exists an alternative statistical inference tool which better addresses our modelling challenges and outperforms the MLE.

Robust statistical inference methods for heavy tail distributions are relatively scarce in actuarial science literature. Notable contributions include Brazauskas and Serfling (2000), Serfling (2002), Brazauskas and Serfling (2003) and Dornheim and Brazauskas (2007) who adopt various kinds of statistical inference tools, such as quantile, trimmed mean, trimmed-M and generalized median estimators, to robustly estimate Gamma, Pareto and Log-normal distributions. Recent actuarial works study several variations of the method of moments (MoM) for robust estimations of Pareto and Log-normal loss models. Notable contributions in this direction include Brazauskas (2009), Poudyal (2021a) (trimmed moments), Zhao et al. (2018) (winsorized moments) and Poudyal (2021b) (truncated moments). Note that these research works address robustness issue against the upper outliers by reducing the influence of few extreme observations to the estimated model parameters. This outlier-robustness issue is however very different from the tail-robustness issue mentioned above as the key motivation of this paper, where the contaminations on the body part affects the tail extrapolations. Very few research works look into this “non-standard” tail-robustness issue. Notable contributions are Beran and Schell (2012) and Gong and Ling (2018) who propose a huberization of the MLE, which protects against perturbations and misspecifications in the body part of distribution, to robustly estimate the tail index of Pareto and Weibull distributions. All of the above existing approaches focus solely on one or two-parameter distributions. A general robust tail estimation strategy under multi-parameter flexible models like FMM is lacking.

Motivated by the aforementioned tail-robustness issue in insurance context, we propose a new maximum weighted likelihood estimation (MWLE) approach for robust heavy-tail modelling of FMM. Under the MWLE, an observation-dependent weight function is introduced to the log-likelihood, de-emphasizing the contributions of smaller claims and hence reducing their influence to the estimated tail part of FMM. Down-weighting small claims is also natural in insurance loss modelling perspective, as mentioned in the beginning of this section, accurate modelling of the large claims is more important than the smaller claims. To offset the bias caused by the weighting scheme, we also include an adjustment term in the weighted log-likelihood, which can be interpreted as the effects of randomly truncating the observations. With the bias adjustment term, we prove that estimated parameters under the proposed MWLE is consistent and asymptotically normal with any pre-specified choices of weight functions. Also, under some specific choices of weight functions, we will show that the MWLE tail index, which determines the tail heaviness of a distribution, is consistent, even under model misspecifications where the true model is not FMM. Therefore, MWLE can be regarded as a generalized alternative framework of Hill estimator (Hill (1975)). Furthermore, with a probabilistic interpretation of the proposed MWLE approach, it is still possible to derive a Generalized EM (GEM) algorithm to efficiently estimate parameters which maximize the weighted log-likelihood function.

Note that the proposed MWLE is different from the existing statistics papers which adopt weighting schemes for likelihood-based inference. The existing literature are mainly motivated by one of the following two aspects very different from the focus of this paper: (i) Robustness against upper and lower outliers, where related research works include e.g. Field and Smith (1994), Markatou et al. (1997), Markatou (2000), Dupuis and Morgenthaler (2002), Ahmed et al. (2005), Wong et al. (2014) and Aeberhard et al. (2021); (ii) Bringing in more relevant observations for statistical inference to increase precision while trading off some biases, studied by e.g. Wang (2001), Hu and Zidek (2002), Wang et al. (2004) and Wang et al. (2005). Note also that our proposed MWLE stems differently from the existing statistics literature in terms of mathematical technicality, since none of the above papers incorporate the truncation-based bias adjustment as included in the proposed WMLE.

The rest of this paper is structured as follows. In Section 2, we briefly revisit the class of FMM for heavy tail modelling. Section 3 introduces the proposed MWLE for robust heavy-tail modelling of FMM and explains its motivations in terms of insurance claims modelling. Section 4 explores several theoretical properties to understand and justify the proposed MWLE. After that, we present in Section 5 two types of GEM algorithms for efficient parameter estimations under the MWLE approach on FMM. In Section 6, we analyze the performance of the proposed MWLE through three empirical examples: a toy example, a simulation study and a real insurance claim severity dataset. After showing the superior performance of MWLE compared to MLE, we finally summarize our findings in Section 7 with a brief discussion how the proposed MWLE can be extended to a regression framework.

2 Finite mixture model

This section provides a very brief review on finite mixture model (FMM) which serves as a flexible density estimation tool. Suppose that there are i.i.d. claim severities with realizations . is generated by a probability distribution of with density function which is unknown. In insurance context, claim severity distribution often exhibits multimodality, which results from the unobserved heterogeneity stemming from the amalgamation of different types of claims unobserved in advance. Also, claim sizes are often heavy-tail in nature, which can be attributed to a few large losses from a portfolio of policies which usually represent the greatest part of the indemnities paid by the insurance company. The mismatch between body and tail behavior often poses difficulties to fit the data well using only a standard parametric distribution.

Motivated by the challenges of modelling insurance claim severities, we aim to model the dataset using finite mixture model (FMM). Define a class of finite mixture distributions , where is a column vector with length representing the model parameters and is the parameter space. Its density function is given by the following form:

| (2.1) |

where the parameters can alternatively be written as . Here, are the mixture probabilities for each of the components with . and are the parameters for the mixture densities and respectively.

The mixture components with densities mainly serve as modelling the multimodality for the body part of the distribution. is naturally chosen as a light-tailed distribution like Gamma, Weibull and Inverse-Gaussian. The remaining mixture component is designed to capture the large observations and hence the tail distribution can be properly extrapolated. The possible choices of heavy-tail distribution for include Log-normal, Pareto and Inverse-Gamma.

3 Maximum weighted log-likelihood estimator

With the maximum likelihood estimation (MLE) approach, parameter estimations require maximizing the log-likelihood function

| (3.1) |

with respect to the parameters . Under this approach, each claim has the same relative influence to the estimated parameters, but in insurance loss modelling and ratemaking perspective, correct specification and projection of larger claims are more important than those of smaller claims. More importantly, as explained by Fung et al. (2021) and Wuthrich and Merz (2021), MLE of FMM in Equation (2.1) would fail in most practical cases due to incorrectly estimations of tail heaviness under model misspecification. Precisely, because of the overlapping region between the body parts and tail part of the distribution, the small claims may distort the estimated tail distribution if they are not fully captured by the mixture densities in the body. However, due to the highly complex multimodality characteristics of the body distribution which often appears in real insurance claim severity data, it is impossible to capture all the body distributional patterns without prohibitively large which causes over-fitting and loss of model interpretability. Therefore, it is often the case in practice that MLE of FMM would result in unstable estimates of tail distribution, causing unreliable tail extrapolation.

One way to mitigate the aforementioned model misspecification effect is to impose observation-dependent weights to the log-likelihood function, where a larger claim is assigned to a larger weight. This will reduce the influence of smaller observed values to the estimated tail parameter. For parameter estimations, we propose maximizing the weighted log-likelihood as follows instead

| (3.2) |

where is the weight of the log-likelihood function. We call the resulting parameters maximum weighted likelihood estimators (MWLE). To allow for greater relative influence of larger claims, we construct as a monotonically non-decreasing function of . In this case, we may interpret the weighted log-likelihood function as follows: First, we pretend that each claims are only observed respectively by times. However, this alone will introduce bias to a heavier estimated tail because this implies more large claims are effectively included due to the weighting effect. To remove such a bias, we pretend to model by a random truncation model instead of the original modelling distribution .

Remark 1

The proposed MWLE can be viewed as a form of M-estimator, where the optimal parameters are determined through maximizing a function. We here discuss two special cases of MWLE. (i) MLE: When , MWLE is reduced to a standard MLE; (ii) Truncated MLE: When for some threshold , then MWLE is reduced to truncated MLE introduced by Marazzi and Yohai (2004), where a hard rejection is applied to all samples smaller than .

4 Theoretical Properties

This section presents several theoretical properties of the proposed MWLE to theoretically justify the use of the proposed MWLE. Unless specified otherwise, throughout this section the estimated model parameters are obtained by maximizing the proposed weighted log-likelihood function given by Equation (3.2).

4.1 Asymptotic behavior with fixed weight function

4.1.1 Consistency and asymptotic normality

We first want to show that the proposed weighted log-likelihood approach leads to correct convergence to true model parameters as . The proof is presented in Section 2 of the supplementary materials.

Theorem 1

Suppose that . Assume that the density function satisfies a set of regularity conditions outlined in Section 1 of supplementary materials111Note that the set of regularity conditions are equivalent to those required for consistent and asymptotic normal estimations of MLE.. Then, there exists a local maximizer of the weighted log-likelihood such that

| (4.1) |

where , with and being matrices given by

| (4.2) |

and

| (4.3) |

where represents the expectation under density for any functions , and the derivative is assumed to be a column vector with length .

Remark 2

Remark 3

The above theorem suggest that for large sample size, the estimated parameters are approximately unbiased and we may approximate the variance of estimated parameters as

| (4.4) |

where and are given by and in Equations (1) and (1) except that the expectations are changed to empirical means and is changed to . Then, it is easy to construct a two-sided Wald-type confidence interval (CI) for () as

| (4.5) |

where is the estimated , is the -quantile of the standard normal distribution and is the -th element of for some matrices . For other quantities of interest (e.g. mean, VaR and CTE of claim amounts), one may apply a delta method or simulate parameters from to analytically or empirically approximate their CIs.

Next, we examine the asymptotic property of MWLE dropping the assumption that (i.e. we may misspecify the model class).

Theorem 2

Assume that the density function satisfies the same set of regularity conditions as in the previous theorem. Further assume that there is a local maximizer of

| (4.6) |

where represents the expectation under distribution for any functions . Then, there exists a local maximizer of the weighted log-likelihood such that

| (4.7) |

where , with and given by

| (4.8) |

and

| (4.9) |

As shown by the above theorem, the MWLE is still asymptotically convergent and normally distributed. As a result, it is still justifiable to evaluate the parameter uncertainties and CI of parameters in the forms of Equations (4.4) and (4.5). However, in the context of modelling heavy-tail distributions as an example, there could be an asymptotic bias on the estimated tail index. As a result, it is important to theoretically examine how the choice of weight functions influence the impacts of model misspecifications. These will be leveraged to the next subsections on the robustness studies and asymptotics under varying weight functions.

4.1.2 Robustness

It is well known that MLE is the most efficient estimator under all asymptotically unbiased estimators. Therefore, with an attempt to reduce the bias of estimated tail distribution under misspecified models through MWLE approach with , there will be a trade-off between bias regularizations and loss in efficiencies. This subsection will analyze such a trade-off, which may provide guidance to choose an appropriate weight function . In light of Theorem 1, it is easy to show the following proposition by applying delta method.

Proposition 1

Suppose that with the same set of regularity conditions as previous theorems. Define and as the MWLE and MLE respectively. Then, for some differentiable functions , the relative asymptotic efficiency (AEFF) of is given by

| (4.10) |

where is the gradient of w.r.t. , and is the inverse of Fisher information matrix under standard MLE approach.

Next, we need to quantify robustness by some statistical measures. In a theoretical setting, we follow e.g. Huber (1981), Beran and Schell (2012) and Gong and Ling (2018) to consider the case that is generated by a contamination model, given by

| (4.11) |

for some contamination distribution function . Then, the asymptotic bias can be analyzed through evaluating the influence function (IF), a column vector with length given by

| (4.12) |

where is the asymptotic estimated parameters if given by Equation (4.11) is distribution generating , contrasting to which are the true model parameters. IF can be interpreted as the infinitesimal asymptotic bias of estimated parameters by perturbing the model generating . Smaller (with being the element of IF) means a more robust estimation of under model misspecification. Our goal is to demonstrate the potential of the proposed MWLE to reduce such a bias and hence improve the robustness. We have the following proposition which derives the IF under the MWLE approach:

Proposition 2

We will show empirically how the choice of weight functions affects the AEFF and IF in Section 6.1, which will help us understand the bias-variance tradeoff of our proposed MWLE approach.

4.2 Asymptotic behavior of tail index with varying weight functions

Tail index measures the tail-heaviness of a probability distribution. Correctly specifying the tail index is a critical task of modelling insurance data with heavy-tail nature, as insurance companies often care more about large claims which are more material than small ones. In this section, we show that under some sequences of weight functions which depend on the number of observations , the estimated tail index will be consistent under the proposed MWLE even if the model class is misspecified. This result theoretically justifies how the proposed MWLE addresses the tail-robustness issue caused by model misspecification and distributional contamination, by showing that reduced influence of smaller claims through downweighting can be useful for producing a plausible tail index estimate. Also, the result may provide some theoretical guidance on selecting an appropriate weight function.

Denote be a class of regularly varying distributions with tail index , such that if and only if as for some slowly varying functions satisfying as for any . Smaller implies heavier tail. Note that regularly varying distributions include many distributions that capture heavy-tail behaviors of loss random variables and we refer the readers to Cooke et al. (2014) for more explanation on these distributions. Also define the following transformed density functions

| (4.14) |

and and are the corresponding distribution functions. We further put a bar to any function to denote its survival function (i.e. ). We then make the following assumptions:

-

A1.

with tail index .

-

A2.

for some slowly varying functions , so that . Here, is the only model parameter within that governs the tail index. Also, both and its derivative w.r.t. converges uniformly as for any fixed .

-

A3.

There exists some sequences of thresholds with as such that as .

-

A4.

as , where and for some functions .

-

A5.

The density functions and are ultimately monotone (i.e. monotone on for some ), uniformly on .

Assumptions A1 and A2 ensure that both the model generating the observations and the fitted model class are heavy tail in nature, with tail heaviness quantified by tail indices and respectively. In finite mixture context, see Section 2, A2 can be easily satisfied choosing in Equation (2.1) as any standard regularly varying distributions such as Pareto and Inverse-Gamma with compact parameter space. Assumption A3 asserts that all observations other than the extreme ones are greatly down-weighted. This assumption provides a theoretical guidance of choosing the weight function such that small to moderate claims should only be allocated by small weights, while substantial weights should be assigned only to large claims. A4 requires that the effective number of MWLE observations such that large sample theories hold. The numerator grows much slower than the denominator as a logarithm is involved. Assumption A5 is of no practical concern. Now, we have the following theorem which asserts the consistency of estimated tail index. The proof is leveraged to Section 3 of the supplementary material.

Theorem 3

Assume A1 to A5 hold for the settings under the MWLE, and the regularity conditions outlined in Section 1 of Supplementary materials are satisfied. Then, there exists a local maximizer of the weighted log-likelihood function with the estimated tail index such that as . Further, the local maximizer is unique in probability as .

Remark 4

Consider a special case where: (i) the weight functions are step functions for some sequences of ; and (ii) the fitted model class is chosen as a Generalized Pareto distribution (GPD) or equivalently Lomax distribution which will be described in Section 6 (i.e. is an FMM in Equation (2.1) with and is a GPD). Theorem 3 is then asserting the consistency of tail index obtained by excess over threshold method on GPD (Smith et al. (1987)), which has a very close connection with the consistency property of the Hill estimator (Hill (1975)) (see Section 4 of Smith et al. (1987)). Therefore, we can regard the proposed MWLE approach as a generalized framework of the Hill-type estimator by Hill (1975).

5 Parameter estimation

5.1 GEM algorithm

Since there is a probabilistic interpretation of the weighted log-likelihood given by Equation (3.2), it is feasible to construct a generalized Expectation-Maximization (GEM) algorithm for efficient parameter estimations. In this paper, we will present two distinctive approaches of complete data constructions which result to two different kinds of GEM algorithms.

5.1.1 Method 1: Hypothetical data approach

Construction of complete data

To address the challenges of optimizing directly the “observed data” weighted log-likelihood in Equation (3.2), we extend the “hypothetical complete data” method proposed by Fung et al. (2020), by defining the complete data

| (5.1) |

where is the number of missing sample points “generated” by observation , due to the probabilistic interpretation that each sample is removed with a probability of . As an auxiliary tool for efficient computations we assume that follows geometric distribution with probability mass function

| (5.2) |

and are i.i.d. variables representing the missing samples. We assume that (with realization ) is independent of and , and follows a distribution with the following density function

| (5.3) |

Further, are the latent mixture components assignment labels, where if observation belongs to the latent class and otherwise. Similarly, are the labels for missing data, where if the missing sample generated by observation belongs to the latent class, and otherwise.

The complete data weighted log-likelihood function is then given by

| (5.4) |

which is more computationally tractable. In the following we will omit the constant term which is irrelevant for calculations.

Iterative procedures

In the iteration of the E-step, we compute the expectation of the complete data weighted log-likelihood as follows:

| (5.5) |

where , and . Also, follows in Equation (5.2) and follows in Equation (5.3). The precise expressions of the above expectations are presented in Section 4.2 of supplementary materials, under a particular specification of Gamma distribution for and Lomax distribution for . This specification will also be studied in the illustrating examples (Section 6).

In the M-step, we attempt to find the updated parameters such that . Note in Equation (5.1.1) that is linearly separable w.r.t. parameters . Therefore, the optimization can be done separately w.r.t. each subset of parameters. Details are leveraged to Section 4.3 of supplementary materials.

5.1.2 Method 2: Parameter transformation approach

Construction of complete data

Motivated by the mixture probability transformation approach adopted by e.g. Lee and Scott (2012) and Verbelen et al. (2015) for truncated data, we here rewrite the random truncation distribution in Equation (3.2) as

| (5.6) |

where are the transformed mixing weight parameters given by

| (5.7) |

As a result, the problem is reduced to maximizing the weighted log-likelihood of finite mixture of random truncated distributions. In this case, define the complete data

| (5.8) |

where are the labels where if observation belongs to the (transformed) latent mixture component and otherwise. The complete data weighted log-likelihood function is reduced to

| (5.9) |

Iterative procedures

In the iteration of the E-step, the expectation of the complete data weighted log-likelihood is:

| (5.10) |

where is provided in Section 5.2 of supplementary materials.

In the M-step, similar to Method 1 that is linearly separable w.r.t. parameters , we can maximize sequentially w.r.t. each subset of parameters. Details are presented in Section 5.3 of supplementary materials. Note that the M-step of this approach is slightly more computationally more intensive than Method 1 as the target function here involves numerical integrals.

After completing the iterative procedures, we will obtain an estimate of the transformed mixing weights instead of . One can revert Equation (5.7) to get back the estimated original mixing weights as follows:

| (5.11) |

| (5.12) |

5.2 Ascending property of the GEM algorithm

It is well known from Dempster et al. (1977) that an increase of complete data log-likelihood implies an increase of observed data log-likelihood (Equation (3.1)). This can be analogously extended to the proposed weighted log-likelihood framework where we have the following proposition. The proof is leveraged to Section 6 of the supplementary material.

Proposition 3

If the expected complete data weighted log-likelihood is increased during the iteration (i.e. ), then the observed data weighted log-likelihood is also increased (i.e. ).

5.3 Parameter Initialization, convergence acceleration and stopping criterion

Initialization of parameters is an important issue, in the sense that poor initializations may lead to slow convergence, numerical instability and even convergence to spurious local maximum. We suggest to determine the initial parameters using a modified version of clusterized method of moments (CMM) approach by Gui et al. (2018). Under this approach, we first determine a threshold which classifies observations into either body () or tail () part of the distribution. We then apply a -means clustering method to assign “body” observations with to one of the mixture components for the body, with moment matching method for each mixture components to determine the initial parameters . Moment matching technique is also applied to “tail” observations with to initialize . For details, we direct readers to Section 7 of the supplementary material.

As EM algorithm often converges slowly with small step sizes, we further apply a step lengthening procedure for every two GEM iterations to accelerate the algorithm. This is described by Jamshidian and Jennrich (1997) and its references therein as a “pure accelerator” for the EM algorithm.

The GEM algorithm is iterated until the relative change of iterated parameters is smaller than a threshold of or the maximum number of iterations of 1000 is reached.

5.4 Specification of weight function

Our proposed MWLE is rather flexible by allowing us to pre-specify any weight functions prior to fitting the GEM algorithm. The appropriate choice of depends on some decision rules beyond what statistical inference can do. In insurance loss modelling perspective, such decision rule includes the relative importance of insurance company to correctly specify the tail distribution (to evaluate some tail measures such as Value-at-risk (VaR)) compared to that of more accurately modelling the smaller attritional claims. If accurate extrapolation of huge claims are way more important than modelling the smaller claims, then one may consider to be close to zero unless is large, aligning with Assumption A3 in Section 4.2 to ensure near-consistent tail index estimations (Theorem 3). Otherwise, one may consider a flatter across .

Throughout the entire paper, we analyze the following general form of weight function

| (5.13) |

which is the distribution function of a zero-inflated Gamma distribution. The above weight function has the following characteristics:

-

•

is a non-decreasing function of , meaning that smaller observations are down-weighted.

-

•

is the minimum weight assigned to each observation.

-

•

and are the location and dispersion hyperparameters of Gamma distribution respectively. Larger means more (small to moderate) claims are under-weighted by a larger extent, while controls the shape of weight function, or how the observations are under-weighted.

-

•

If or , then the weight function is reduced to , leading to standard MLE approach.

-

•

If and , then , meaning that only observations greater than are informative in determining the estimated parameters.

Overall, smaller , larger and smaller represent greater under-weightings to more small claims, where we will expect more robust tail estimation by sacrificing more efficiencies on body estimations. In this paper, instead of quantifying decision rules to select the hyperparameters, in the subsequent sections we empirically test various (wide range) combinations of to study how these hyperparameters affect the trade-off between tail-robustness and estimation efficiency. These provide practical guidance and assessments to determine the suitable hyperparameters.

Remark 5

There are many possible ways to quantify the decision rule to select the “optimal” weight function hyperparameters. We here briefly discuss two possible ways: (1) Consider a goodness-of-fit test statistic for heavy-tailed distributions, such as the modified AD test (Ahmad et al. (1988)). Then select weight function hyperparameters which optimizes the test statistic; (2) Define an acceptable range of estimated parameter uncertainty of tail index, e.g. two times as the uncertainty obtained by MLE. Then select the hyperparameters with the greatest distortion metric (e.g. the average downweighting factor ) where the tail index uncertainty is still within the acceptable range.

5.5 Choice of model complexity

The above GEM algorithm assumes a fixed number of mixture component . However, it is important to control the model complexity by choosing an appropriate which allows enough flexibility to capture the distributional characteristics without over-fitting.

The first criterion is motivated by maximizing the expected weighted log-likelihood

| (5.14) |

where the expectation is taken on under the true model generating the observations. Without knowing the true model (in real data applications), Equation (5.14) is approximated by in Equation (3.2) with fitted model parameters . Note that it is positively biased with correction term shown by Konishi and Kitagawa (1996). This leads to a robustified AIC

| (5.15) |

Analogous and naturally, since AIC-type criteria often choose excessively complex models, we also consider the robustified BIC given by

| (5.16) |

We choose that minimizes either the RAIC or RBIC, and the -th element of can be interpreted as the effective number of parameter attributed by the parameter.

Insurance loss dataset is often characterized by very complicated and multimodal distribution on very small claims, yet it is not meaningful to capture all these small nodes by choosing an overly complex mixture distribution with large . However, the above RAIC and RBIC cannot effectively reduce those mixture components as the effective number of parameters for those capturing the smaller claims could be very small if is chosen very small over the region of small claims. To effectively remove components which excessively capture the small claims, we propose treating all parameters as “full parameters”, which results to the following truncated AIC and BIC:

| (5.17) |

| (5.18) |

Remark 6

The above TAIC and TBIC are motivated by the bias of approximating by the empirical truncated log-likelihood instead of , where is an indicator randomly discarding some observations. It can be easily shown (details in Section 8 of supplementary material) that the asymptotic bias is simply with effective number of observations . Note also that the weighted log-likelihood is asymptotically equivalent to the truncated log-likelihood , except that the former produces more accurate estimated parameters than the latter. This motivates why in TAIC and TBIC we choose to evaluate instead of .

6 Illustrating examples

In this section, we analyze the performance of our proposed MWLE approach (Equation (3.2)) on FMM given by Equation (2.1). In the following examples, we select Gamma density for the body components , a light-tailed distribution to capture the distributional multimodality of small to moderate claims, and Lomax density for the tail component to extrapolate well the tail-heaviness of larger observations. Then, Equation (2.1) becomes

| (6.1) |

where the parameter set is re-expressed as while and , and the Gamma and Lomax densities and are respectively given by

| (6.2) |

where and are the mean and dispersion parameters of Gamma distribution, while is the tail index parameter for the Lomax distribution. is scale of the Lomax distribution. Note that the above model is a regular varying distribution with the tail behavior predominately explained by the tail index . As a result, tail-robustness is highly determined by how stable and accurate the estimated tail index is.

The specifications of body and tail component functions are mainly motivated by the key characteristics of insurance claim severity distributions (multimodal distribution of small claim, existence of extremely large claims, mismatch between body and tail behavior etc.) which will be illustrated in the real insurance data application section. While we do not preclude the existence of other specifications, such as Weibull for the body and Inverse-Gamma for the tail, plausible for insurance applications, in this section we simply focus on studying Gamma-Lomax combination to focus on the scope of this paper – demonstrating the usefulness of the proposed MWLE, instead of performing distributional comparisons under FMM.

6.1 Toy example

We demonstrate how the proposed MWLE framework works through a simple toy example of one-parameter Lomax distribution (), which is a special case of Equation (6.1) with and .

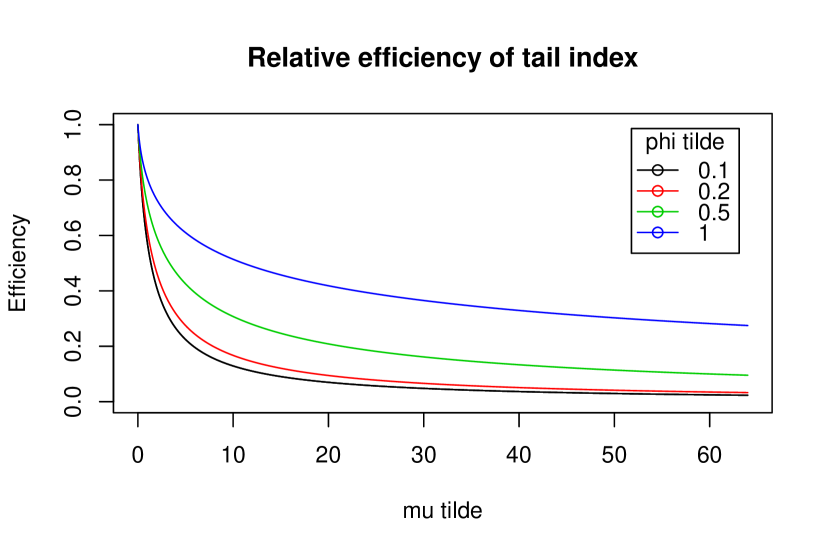

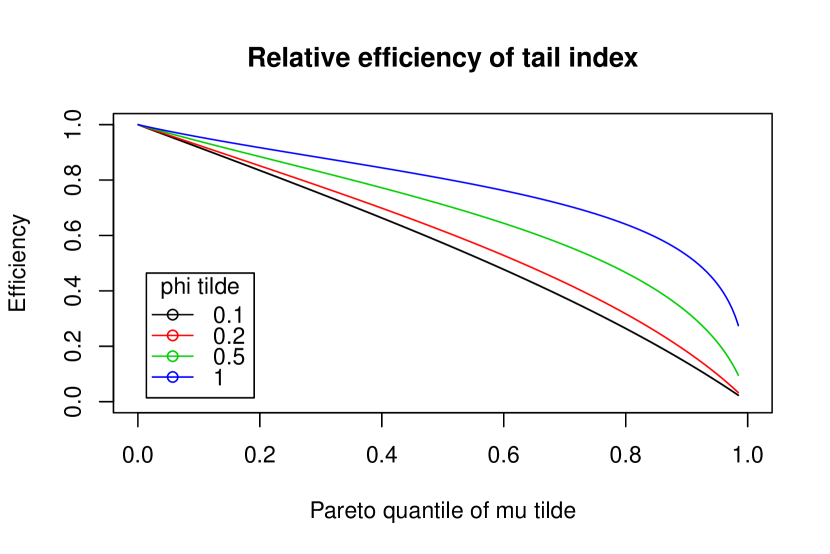

Consider the first case where the true model is a Lomax with . For the weight function for the MWLE, we consider the form of Equation (5.13) with for simplicity. We will test across a wide range of and across . Figure 1 presents how the choices of these hyperparameters affect the AEFF. Starting from when which is equivalent to standard MLE, the AEFF decrease monotonically as increases. This is intuitive because under-weighting smaller observations with MWLE means effectively discarding some observed information, leading to larger parameter uncertainties compared to MLE. Since the MLE estimated tail index is unbiased under the true model, there is obviously no benefit of using the proposed MWLE to fit the true model.

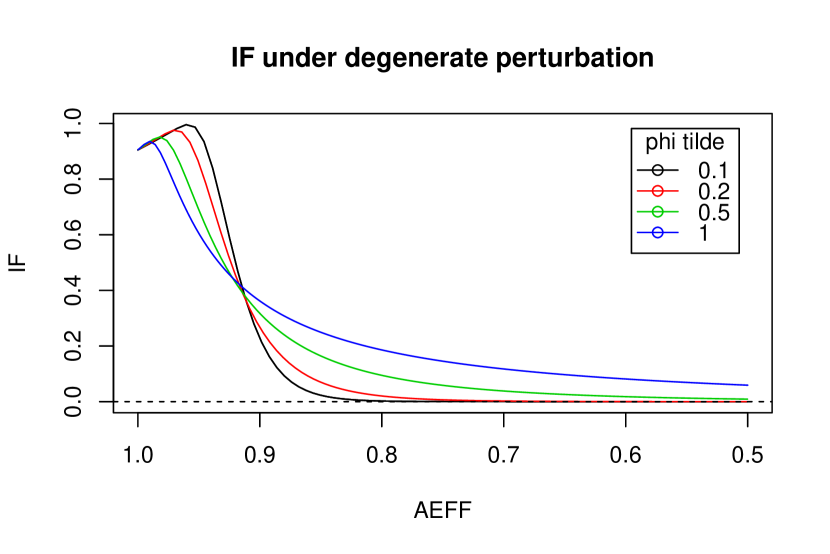

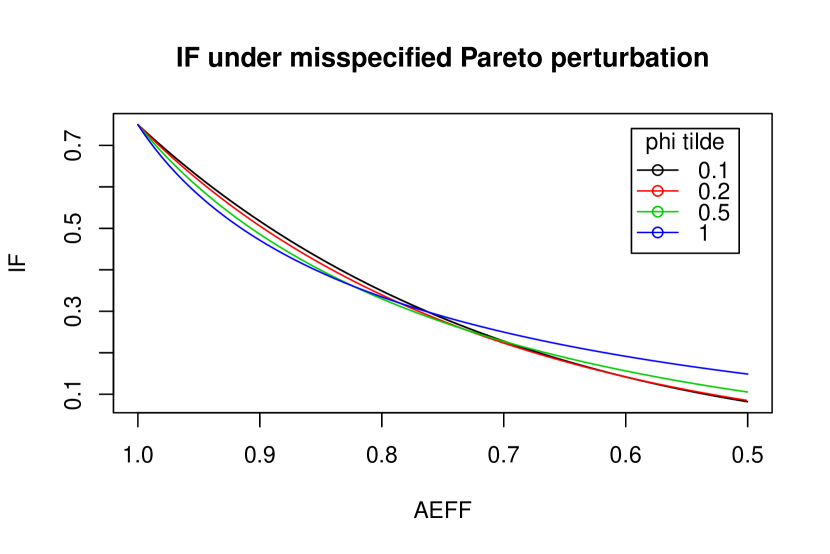

Now, consider the second case where the true model is perturbed by the contamination function , as presented in Equation (4.11). In this demonstration example, we consider two following two choices for the contamination function :

-

•

Degenerate perturbation: One-point distribution on

-

•

Pareto perturbation: Lomax distribution with tail index

Note that the contamination function is relatively lighter tailed and hence it would not affect the tail behavior of the perturbed distribution. In Figure 2, we present the IF as a function of the AEFF (determined as a function of chosen ) under the two choices of . We find that as the AEFF reduces (by choosing a larger ), the IF would shrink towards zero. This reflects that a more robust estimation of tail index can be achieved using the proposed MWLE approach by trading off some efficiencies.

6.2 Simulation studies

6.2.1 Simulation settings

We here simulate claims (the sample size is motivated by the size of a typical insurance portfolio) from the aforementioned -Gamma Lomax distribution for each of the following two parameter settings with :

-

•

Model 1: , , , and .

-

•

Model 2: , , , and .

We also consider the zero-inflated Gamma distribution given by Equation (5.13) as the weight function, with , and , where is the empirical quantile of the data with . Recall that the choice of implies that and hence the MWLE is equivalent to standard MLE. For each combinations of models and weight function hyperparameters, the simulations of sample points are repeated by 100 times to enable thorough analysis of the results using the proposed weighted log-likelihood approach under various settings. Each simulated sample is then fitted to the -Gamma Lomax mixture in Equation (6.1) with . Note that for simplicity, in the simulation studies we do not examine the choice of as outlined by Section 5.5. As a result, we have the following research goals in the simulation studies:

-

•

Under Model 1, the data is fitted to the true class of models. Hence, we empirically verify the consistencies of estimating model parameters (Theorem 1) using the MWLE. We also study how the selection of weight function hyperparameters affect the estimated parameter uncertainties. Further, we compare the computational efficiency of the two kinds of proposed GEM algorithms.

-

•

Under Model 2, the data is fitted to a misspecified class of models. Hence, we demonstrate how this would distort the estimation of the tail under the MLE, and study how the proposed MWLE produces a more robust tail estimation.

6.2.2 Results of fitting Model 1 (true model)

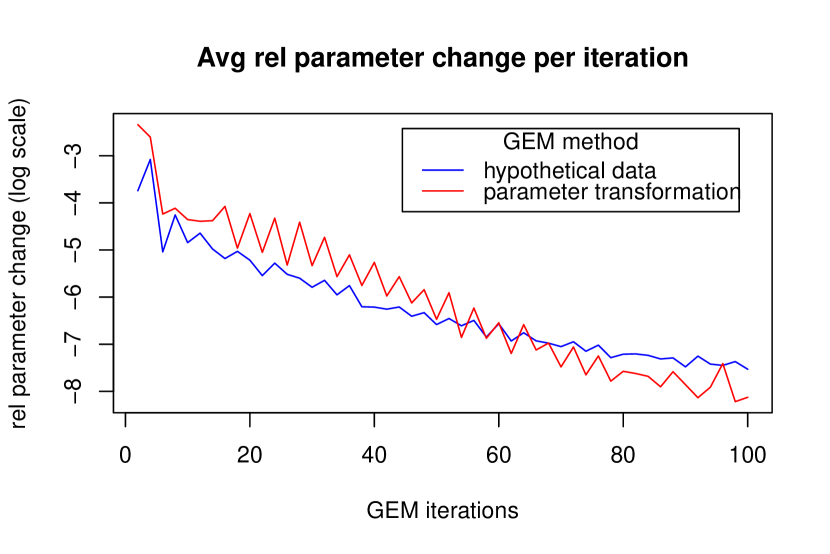

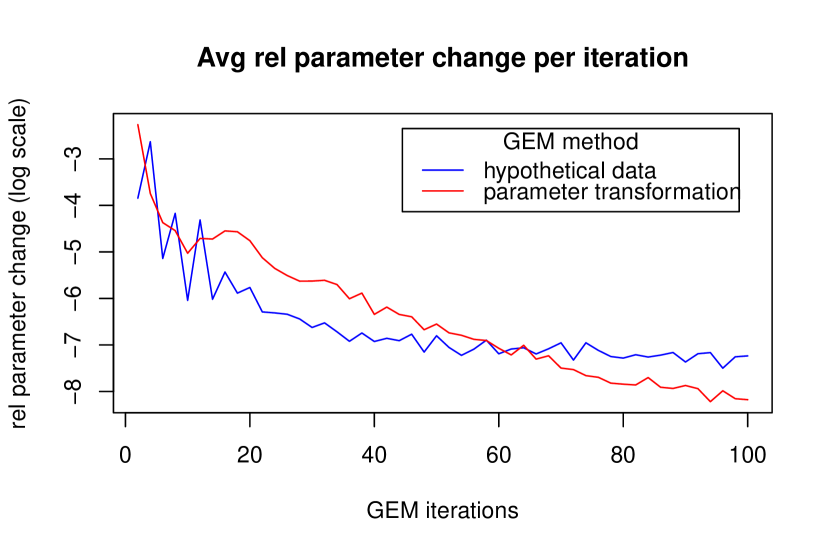

Considering the case where we fit the true class of model to the data generated by Model 1, we first compare the computational efficiencies between the two construction methods of the GEM algorithm as presented by Section 5.1. In general, around 100 iterations are needed under parameter transformation approach (Method 2), as compared to at least 300 iterations under hypothetical data approach (Method 1), revealing relatively faster convergences under Method 2. Figure 3 plots the relative change of iterated parameters versus the GEM iteration under two example choices of weight function hyperparameters, where the division operator is applied element-wise to the vector of parameters. It is apparent that the curve drops much faster under Method 2 than Method 1, confirming faster convergence under Method 2. The main reason is that the construction of hypothetical missing observations under Method 1 will generally effectively reduce the learning rates of the optimization algorithms. As both methods produce very similar estimated parameters while Method 2 is more computationally efficient, from now on we only present the results produced by the GEM algorithm under Method 2.

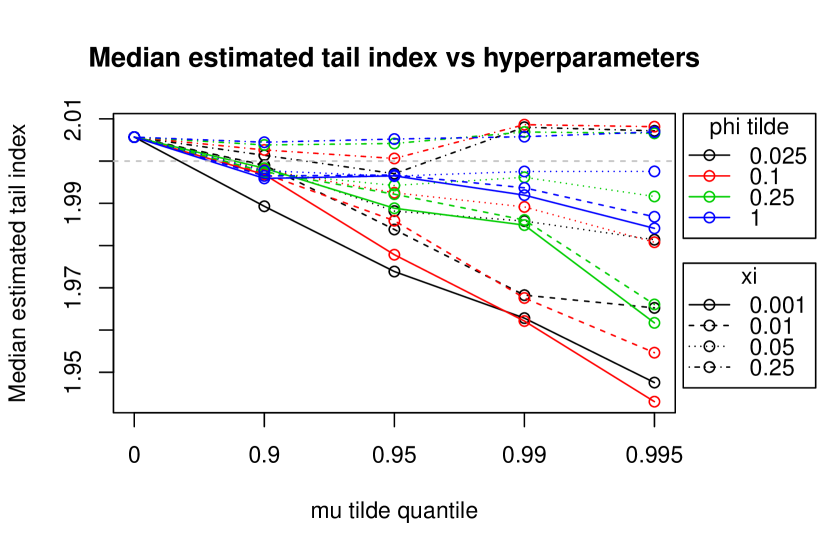

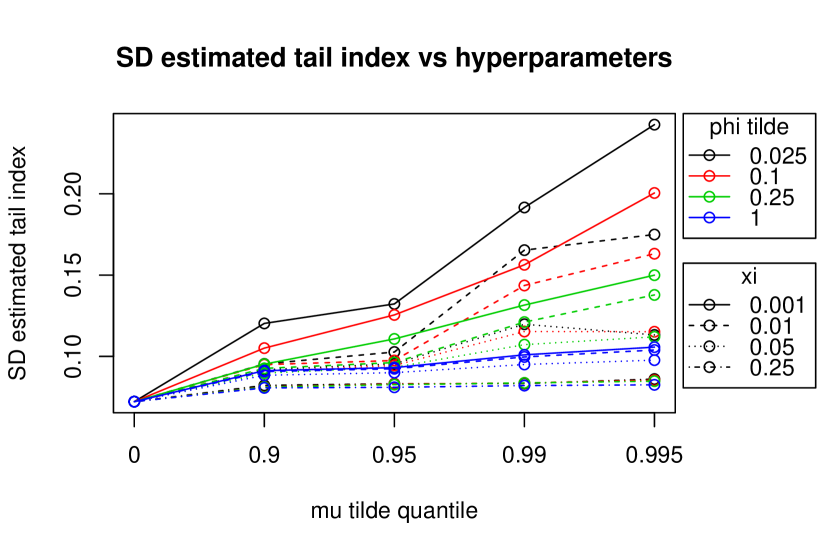

Figure 4 demonstrates the how the biasedness and uncertainty of the estimated tail index differ among various choices of weight functions and their corresponding hyperparameters . From the left panel, the median estimated parameters are very close to the true model parameters (differ by less than 1-2%) under most settings of the weight functions, except for few extreme cases where both and are chosen to be very small. This empirically justifies the asymptotic unbiasedness of the MWLE. As expected from the right panel, the uncertainties of MLE parameters are the smallest, verifying that MLE is the asymptotically most efficient estimator among all unbiased estimators if we are fitting the correct model class. The parameter uncertainties generally slightly increase as we choose larger to de-emphasize the impacts of smaller observations. In some extreme cases where and very small and is very large, the standard error can grow dramatically, reflecting that a lot of information are effectively discarded.

Similarly in Figure 5 where the biasedness and uncertainty of an estimated mean parameter from the body distribution are displayed, we observe that the proposed MWLE approach behaves properly for fitting the body distribution unless when and are both chosen to be extremely small (in those cases, the estimated body parameters would become unstable with inflated uncertainties). Hence, these extreme choices of hyperparameters are deemed to be inappropriate.

6.2.3 Results of fitting Model 2 (misspecified model)

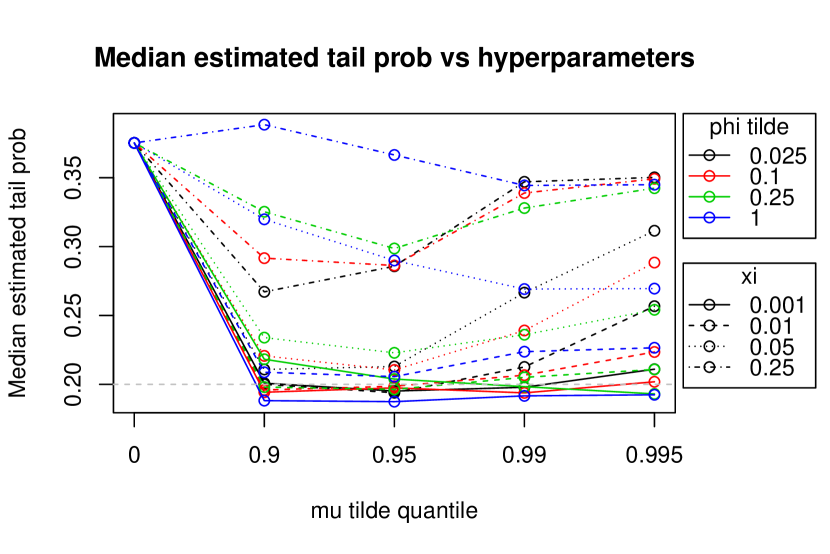

We now turn to the case where we fit a misspecified model (with ) to the simulated data generated from Model 2 (with ). The left panels of Figures 6 and 7 examine how the robustness of the estimated tail index and tail probability differs among different choices of hyperparameters . From the left panel, the MLE of the tail index is around which largely over-estimates the true tail index , indicating that the heavy-tailedness of the true distribution is under-extrapolated. On the other hand, with the incorporation of weight functions to under-weight the smaller claims, the biases of the MWLE of are greatly reduced compared to that of the MLE under most choices of weight function hyperparameters. In particular, the bias reduction for tail index is more effective using smaller (i.e. ). This is intuitive as smaller means smaller claims are under-weighted by a larger extent, reducing the impacts of smaller claims on the tail index estimations. Similarly from the right panel, the proposed MWLE approach effectively reduces the bias of the estimated tail probability .

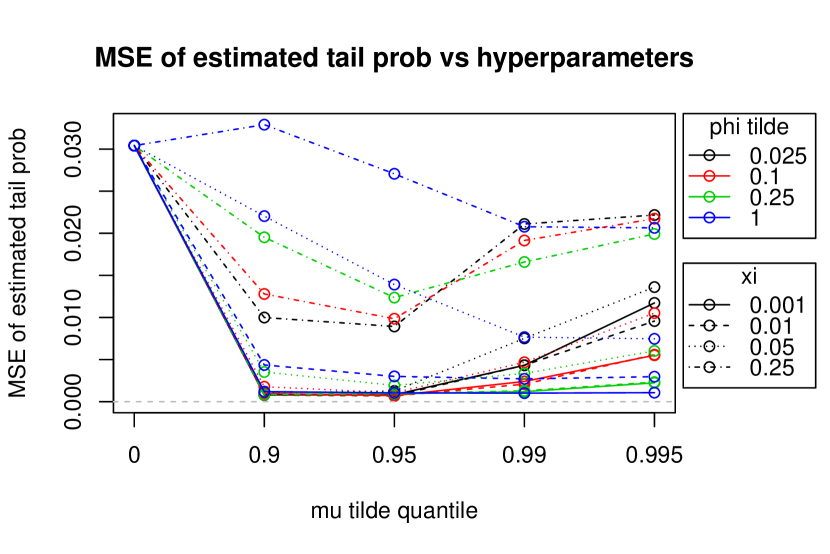

The analysis of bias-variance trade-off is also conducted through computing the mean-squared errors (MSE) of both estimated tail index and tail probability . From the right panels of Figures 6 and 7, as evidenced by smaller MSEs under most choices of weight function hyperparameters, MWLE is much more preferable than MLE approach even after accounting for the increased parameter uncertainties through down-weighting the importance of smaller claims.

6.2.4 Summary remark on the choice of weight function hyperparameters

From the above two simulation studies, we find that under a wide range of choices of weight function hyperparameters, the proposed MWLE not only produces plausible model estimations under true model (Model 1), but is also effective in mitigating the bias of tail estimation inherited from model misspecifications (Model 2).

Among the three hyperparameters , the choice of minimum weight hyperparameter plays a particularly vital role on the bias-variance trade-off of the estimated parameters. Under misspecified model (Model 2), smaller (i.e. ) is more effective in reducing the biases of both estimated tail index and tail probability . However, as evidenced by the results produced under the true model (Model 1), the estimated parameters of the body distributions (i.e. and ) may become prohibitively unstable if is chosen to be extremely small (i.e. ) such that smaller observations are effectively almost fully discarded. It is therefore important to compare parameter uncertainties of MWLE to that of MLE, and select/ consider only the weight function hyperparameters where the corresponding MWLE parameter uncertainties are within an acceptable range (i.e. not too off from the MLE parameter uncertainties). Overall, the choices of between 0.01 and 0.05 are deemed to be suitable.

6.3 Real data analysis

6.3.1 Data description and background

In this section, we study an insurance claim severity dataset kindly provided by a major insurance company operating in Greece. It consists of 64,923 motor third-party liability (MTPL) insurance policies with non-zero property claims for underwriting years 2013 to 2017. This dataset is also analyzed by Fung et al. (2021) using a mixture composite model, with an emphasis on selecting various policyholder characteristics (explanatory variables) which significantly influence the claim severities. The empirical claim severity distribution exhibits several peculiar characteristics including multimodality and tail-heaviness. The excessive number of distributional nodes for small claims reflects the possibility of distributional contamination, which cannot be and should not be perfectly captured and over-fitted by parametric models like FMM. Preliminary analyses also suggest that the estimated tail index is around 1.3 to 1.4, but note that these are only rough and subjective estimates. The details of preliminary data analysis are provided in Section 9 of the supplementary materials. The key goals of this real data analysis are as follows:

-

1.

Illustrate that MLE of FMM would produce highly unstable and unrobust estimates to the tail part of the claim severity distribution. This confirms that tail-robustness is an important research problem in real insurance claim severity modelling which needs to be properly addressed.

-

2.

Demonstrate how the proposed MWLE approach leads to superior fittings to the tail and more reliable estimates of tail index as compared to MLE, without much sacrificing its ability to adequately capture the body.

To avoid diverging the focus of this paper, in this analysis we solely examine the distributional fitting of the claim sizes without considering the explanatory variables. Note however that the proposed MWLE can be extended to a regression framework, with the discussions being leveraged to Section 7.

6.3.2 Fitting results

The claim severity dataset is fitted to the mixture Gamma-Lomax distribution with density given by Equation 6.1 under the proposed MWLE approach. The fitting performances will be examined thoroughly across different number of Gamma (body) mixture components and various choices of weight function hyperparameters (, and ). The MWLE fitted parameters are also compared to the standard MLE across various .

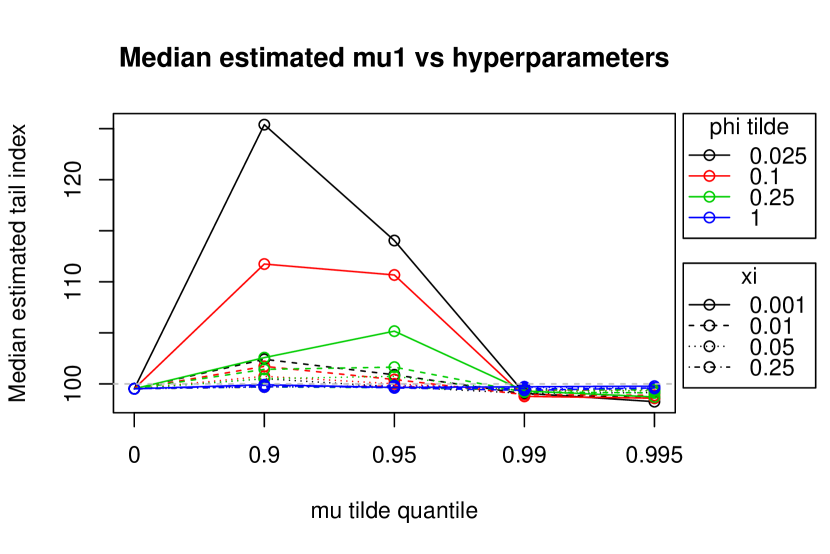

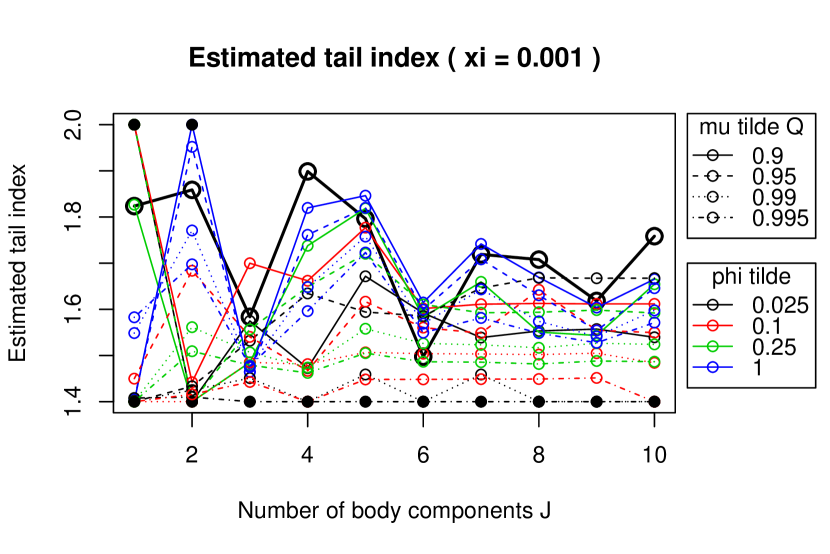

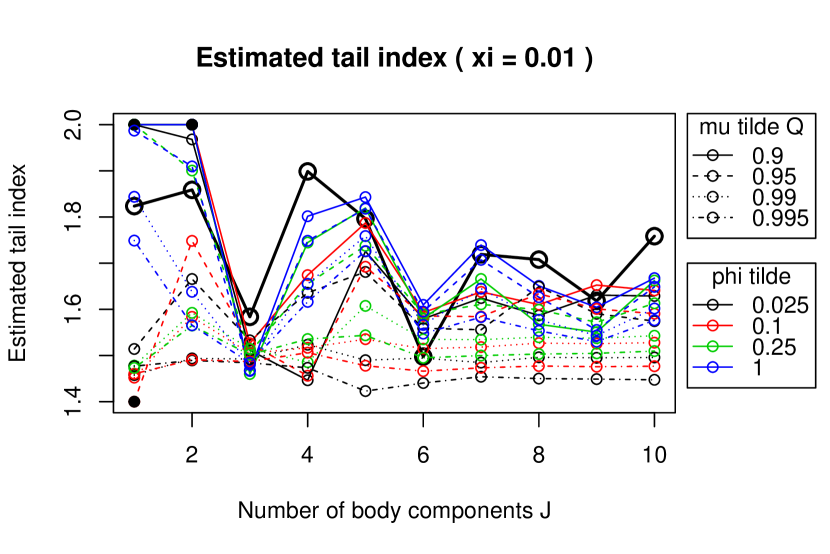

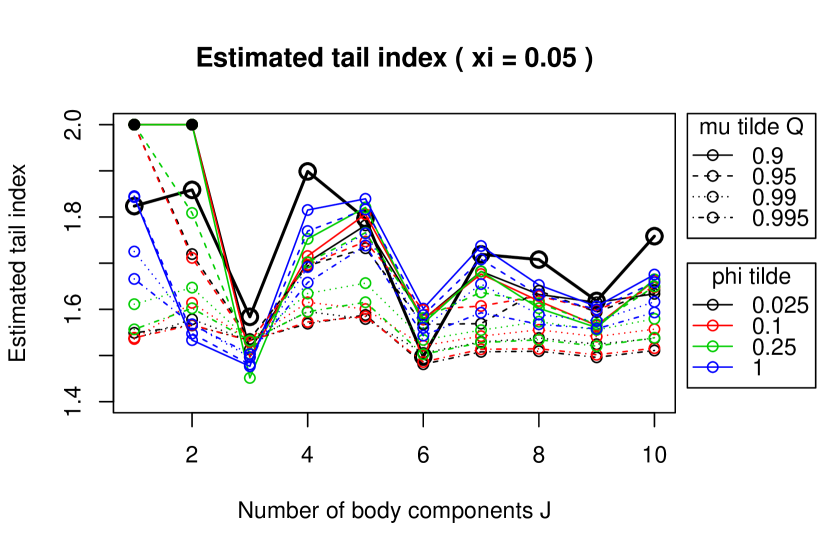

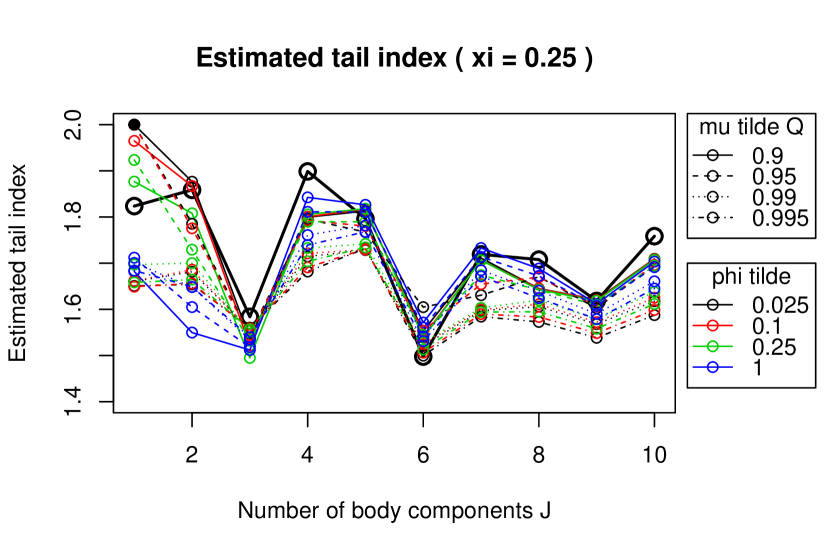

We first present in Figure 8 the fitted tail index versus the number of body components under all combinations of selected weight function hyperparameters. Each of the four sub-figures corresponds to a particular choice of . The black thick trends for each sub-figure are the MLE estimated tail indexes for comparison purpose. The MLE tail indexes are rather unstable as evidenced by great fluctuations across different number of body components , showing that MLE may not be reliable in extrapolating the heavy-tailedness of complex claim distributions. For instance, with a slight change of model specification from to , the estimated tail index largely drops from about 1.8 to 1.5. This is rather unnatural because the change from to should only reflect a slight change in specifying the body. The large drop of the estimated tail index reflects that the Lomax tail part of FMM is not specialized in extrapolating the tail-heaviness of the distribution, but instead is very sensitive to the small claims and the model specifications of the body part. Therefore, we conclude that the mixture Gamma-Lomax FMM is not achieving its modelling purpose under the MLE.

On the other hand, looking individually at each path under MWLE, we find that the estimated is much more stable across different under most choices of weight function hyperparameters, especially when . Also, the estimated MWLE is in general smaller than the obtained by MLE, moving closer to the values roughly determined by the preliminary data analysis in Section 6.3.1. Note in the figure that there are a few black solid dots, which appear when the estimated under MWLE is outside the range of the plots. These unstable estimates of are rare and only occur under one the following two situations: (i) is chosen be very small (i.e. ) in the sense that the models would severely under-fit the distributional complexity of the dataset; (ii) extreme choices of weight function hyperparameters (very small and ) aligned to the results of the simulation studies.

The optimal choice of is tricky as evidenced by the excessive number of small distributional nodes for very small claim sizes described in Section 6.3.1, which should not be over-emphasized or excessively modelled as these very small claims are almost irrelevant for pricing and risk management. However, both AIC and BIC decrease slowly and steadily for MLE models as increases. The optimal in this case goes way beyond . Under the proposed MWLE approach with various choices of weight function hyperparameters, the same model selection problem exists using RAIC and RBIC, with the reasons already explained in Section 5.5. On the other hand, using TAIC and TBIC (especially for TBIC), a majority selections of weight function hyperparameters lead to an optimal , aligning with the heuristic arguments by Fung et al. (2021) that is enough for capturing all the distributional nodes except for the very small claims which are smoothly approximated by a single mixture component.

To better understand how the use of proposed MWLE affects the estimations of all parameters (not just the tail index but also parameters affecting the body distributions such as ), we showcase in Table 1 all the estimated parameters and their standard errors (based on Equation (4.4)) using MWLE under two distinguishable example choices of hyperparameters (MWLE 1: ; MWLE 2: ) as compared to MLE parameters with , the optimal number of body components under TBIC for both MWLE 1 and MWLE 2. Note that the two selected examples are for demonstration purpose – generally the following findings and conclusions are also valid for other choices of weight function hyperparameters under the proposed MWLE.

We first observe that the estimated parameters influencing the body (i.e. , and ) under MWLE are very close to those under MLE, even if the smaller claims are greatly down-weighted. MWLE generally results to larger parameter uncertainties as compared with MLE – reflecting a bias-variance trade-off, but these standard errors are of the same order of magnitude and are still relatively immaterial compared to the estimates as the sample size is large.

Comparing between the above two MWLE examples, we further notice that the parameter uncertainties under MWLE 1 are greater than those under MWLE 2. This is expected because the influences of smaller claims are down-weighted more under MWLE 1 than those under MWLE 2 (as reflected by smaller minimum weight hyperparameter chosen under MWLE 1). On the other hand, the estimated tail index under MWLE 1 is slightly closer to the heuristic values (i.e. 1.3 to 1.4) than MWLE 2. These may also reflect the bias-variance trade-off among various choices of weight function hyperparameters.

| MWLE 1 | MWLE 2 | MLE | ||||

| Estimates | Std. Error | Estimates | Std. Error | Estimates | Std. Error | |

| 0.3787 | 0.0053 | 0.3829 | 0.0031 | 0.3878 | 0.0022 | |

| 0.0380 | 0.0036 | 0.0404 | 0.0021 | 0.0444 | 0.0014 | |

| 0.1117 | 0.0024 | 0.1134 | 0.0020 | 0.1161 | 0.0017 | |

| 0.0221 | 0.0059 | 0.0192 | 0.0021 | 0.0153 | 0.0008 | |

| 0.2173 | 0.0036 | 0.2163 | 0.0022 | 0.2130 | 0.0019 | |

| 1,303.21 | 50.30 | 1,322.10 | 16.70 | 1,348.68 | 11.11 | |

| 9,171.42 | 145.83 | 9,165.92 | 64.64 | 9,165.36 | 49.38 | |

| 27,590.46 | 125.68 | 27,571.75 | 64.36 | 27,538.88 | 52.41 | |

| 317,274.90 | 2,410.93 | 323,827.70 | 2,159.37 | 322,872.40 | 2,372.68 | |

| 89,007.07 | 170.41 | 88,979.12 | 112.01 | 88,895.92 | 99.20 | |

| 0.9945 | 0.0175 | 0.9996 | 0.0121 | 1.0062 | 0.0113 | |

| 0.0264 | 0.0089 | 0.0284 | 0.0030 | 0.0324 | 0.0020 | |

| 0.0154 | 0.0015 | 0.0158 | 0.0007 | 0.0164 | 0.0005 | |

| 0.0472 | 0.0033 | 0.0333 | 0.0025 | 0.0186 | 0.0020 | |

| 0.0127 | 0.0007 | 0.0126 | 0.0003 | 0.0122 | 0.0002 | |

| 1.5353 | 0.0707 | 1.6153 | 0.0586 | 1.7963 | 0.0471 | |

| 62,637.42 | 7,829.79 | 73,604.51 | 6,630.65 | 101,107.20 | 5,088.29 | |

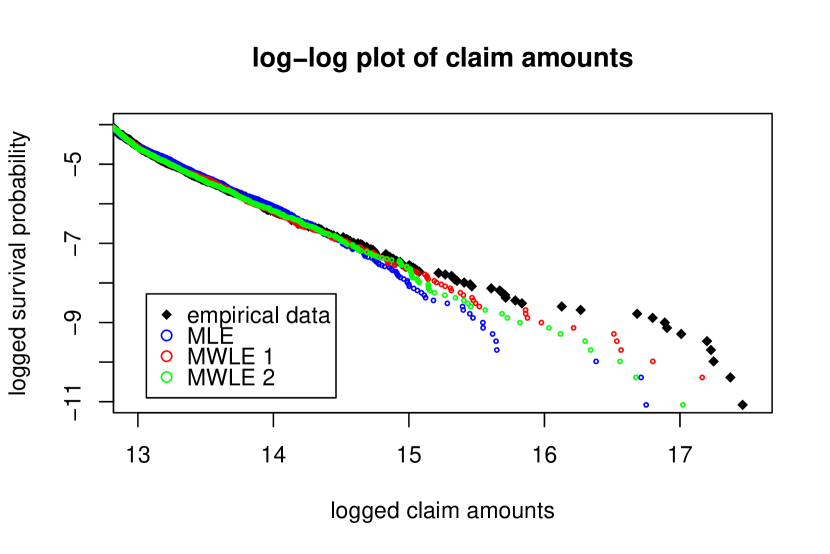

The Q-Q plot in Figure 9 suggests that the fitting results are satisfactory under both MWLE and MLE except for the very immaterial claims (i.e. ). Note however that due to the log-scale nature of the Q-Q plot, it is hard to examine from the plot how well the fitted models extrapolate the tail-heaviness of the claim severity data. To examine the tail behavior of the fitted models, we present the log-log plot in the left panel of Figure 10, with the axis shifted to include large claims only. We observe that for extreme claims (i.e. claim amounts greater than about 0.5 millions, or ), the logged survival probability produced by MLE fitted model diverges quite significantly from that of empirical observations. Such a divergence can effectively be mitigated by using MWLE with either of the hyperparameter settings.

We further compute the value-at-risk (VaR) and conditional tail expectation (CTE) at security level (denoted as and respectively) from the fitted models, and compare them to the empirical values from the severity data (denoted as and respectively). The results are summarized in Table 2. Both MLE and MWLE produce plausible estimates of VaR and CTE up to security levels of 95% and 75% respectively, reflecting the ability of both approaches in capturing the body part of severity distribution. Nonetheless, the MLE fitted model shows significant divergences of VaR and CTE from the empirical data at higher security levels. In particular, the 99%-CTE and 99.5%-CTE are largely underestimated by the MLE approach. Such a divergence is effectively reduced by the proposed MWLE approach where superior fittings to the tail are obtained. Further, MWLE 1 seems to perform slightly better than MWLE 2 in terms of tail fitting, as reflected by smaller underestimations of CTEs at high security levels. This provides a plausible trade-off to the increased parameter uncertainties under MWLE 1 as previously mentioned.

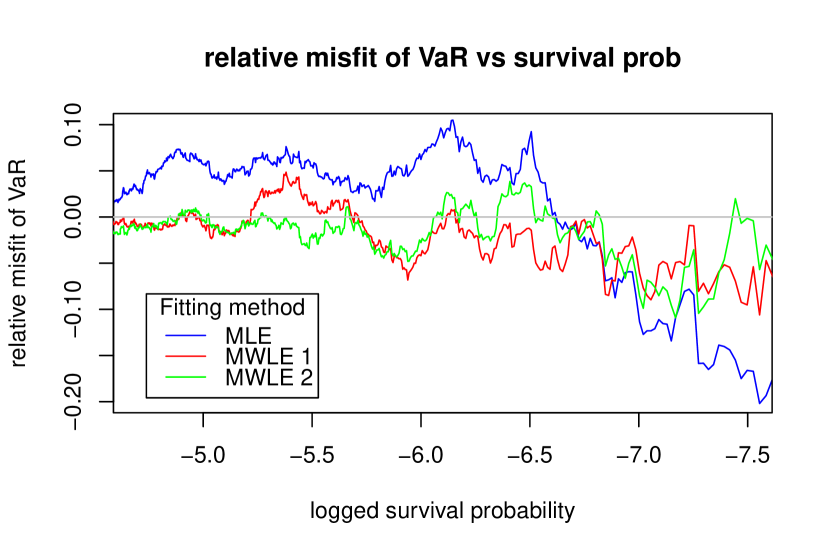

To visualize the results, we further plot the relative misfit of VaR, given by , versus the log survival probability , equivalent to the range of security level from 99% to 99.95%, in the right panel of Figure 10. We observe that the MLE fitted model over-estimates the VaR of large claims (security level between 99% to 99.8%) but then largely under-extrapolates the extreme claims (security level beyond 99.8%). This issue is well mitigated by the MWLE where the misfits of VaR are smaller in both regions. Therefore, we conclude that the proposed MWLE effectively improves the goodness-of-fit on the tail part of distribution (as compared to the MLE) without much sacrificing its flexibly to adequately capture the body part.

| VaR (’000) | CTE (’000) | |||||||||

| Level | MLE | MWLE 1 | MWLE 2 | Empirical | Level | MLE | MWLE 1 | MWLE 2 | Empirical | |

| 50% | 21 | 21 | 21 | 21 | 0% | 109 | 112 | 111 | 116 | |

| 75% | 83 | 82 | 82 | 82 | 50% | 174 | 180 | 177 | 187 | |

| 95% | 190 | 191 | 187 | 182 | 75% | 468 | 505 | 489 | 536 | |

| 99% | 461 | 450 | 445 | 452 | 90% | 1,140 | 1,326 | 1,242 | 1,498 | |

| 99.5% | 719 | 693 | 674 | 676 | 95% | 1,711 | 2,115 | 1,948 | 2,455 | |

| 99.75% | 1,149 | 1,031 | 1,046 | 1,075 | 99% | 2,533 | 3,379 | 3,063 | 4,057 | |

| 99.95% | 2,787 | 3,163 | 3,220 | 3,348 | 99.5% | 5,956 | 10,243 | 8,572 | 13,329 | |

7 Discussions

In this paper, we introduce a maximum weighted log-likelihood estimation (MWLE) approach to robustly estimate the tail part of finite mixture models (FMM) while preserving the capability of FMM to flexibly capture the complex distributional phenomena from the body part. Asymptotic theories justify the unbiasedness and robustness of the proposed estimator. In computational aspect, the applicability of EM-based algorithm for efficient estimation of parameters makes the proposed MWLE distinctive compared to the existing literature on weighted likelihood approach. Through several simulation studies and real data analyses, we empirically confirm that the proposed MWLE approach is more appropriate in specifying the tail part of the distribution compared to MLE, and at the same time it still preserves the flexibility of FMM in fitting the smaller observations.

Another advantage of the MWLE not yet mentioned throughout this paper is its extensibility. First, it is obvious that the proposed MWLE is not restricted to FMM but it is also applicable to any continuous or discrete distributions. Second, MWLE can be easily extended to regression settings, which is crucial for insurance pricing perspective as insurance companies often determine different premiums across policyholders based on individual attributes (e.g. age, geographical location and past claim history). In regression settings, we define as the covariates vectors for each of the observations. Then, the weighted log-likelihood function in Equation (3.2) is then re-expressed as

| (7.1) |

for some regression models with density function . Obviously, the asymptotic properties still hold subject further to some regularity conditions on covariates . For parameter estimations using the GEM algorithm, only the hypothetical data approach (Method 1, which converge slower than Method 2 in Section 6) works, because the transformed mixing probabilities in Equation (5.7) under Method 2 are assumed to be homogeneous across all observations. We leave all theoretical details with more empirical studies and applications to the future research direction.

References

- Aeberhard et al. [2021] W. H. Aeberhard, E. Cantoni, G. Marra, and R. Radice. Robust fitting for generalized additive models for location, scale and shape. Statistics and Computing, 31(1):1–16, 2021.

- Ahmad et al. [1988] M. I. Ahmad, C. Sinclair, and B. Spurr. Assessment of flood frequency models using empirical distribution function statistics. Water Resources Research, 24(8):1323–1328, 1988.

- Ahmed et al. [2005] E. S. Ahmed, A. I. Volodin, and A. A. Hussein. Robust weighted likelihood estimation of exponential parameters. IEEE Transactions on reliability, 54(3):389–395, 2005.

- Bakar et al. [2015] S. A. Bakar, N. A. Hamzah, M. Maghsoudi, and S. Nadarajah. Modeling loss data using composite models. Insurance: Mathematics and Economics, 61:146–154, 2015.

- Beran and Schell [2012] J. Beran and D. Schell. On robust tail index estimation. Computational Statistics & Data Analysis, 56(11):3430–3443, 2012.

- Blostein and Miljkovic [2019] M. Blostein and T. Miljkovic. On modeling left-truncated loss data using mixtures of distributions. Insurance: Mathematics and Economics, 85:35 – 46, 2019.

- Brazauskas [2009] V. Brazauskas. Robust and efficient fitting of loss models: diagnostic tools and insights. North American Actuarial Journal, 13(3):356–369, 2009.

- Brazauskas and Serfling [2000] V. Brazauskas and R. Serfling. Robust and efficient estimation of the tail index of a single-parameter pareto distribution. North American Actuarial Journal, 4(4):12–27, 2000.

- Brazauskas and Serfling [2003] V. Brazauskas and R. Serfling. Favorable estimators for fitting pareto models: A study using goodness-of-fit measures with actual data. ASTIN Bulletin: The Journal of the IAA, 33(2):365–381, 2003.

- Cooke et al. [2014] R. M. Cooke, D. Nieboer, and J. Misiewicz. Fat-tailed distributions: Data, diagnostics and dependence, volume 1. John Wiley & Sons, 2014.

- Cooray and Ananda [2005] K. Cooray and M. M. Ananda. Modeling actuarial data with a composite lognormal-pareto model. Scandinavian Actuarial Journal, 2005(5):321–334, 2005.

- Dempster et al. [1977] A. P. Dempster, N. M. Laird, and D. B. Rubin. Maximum likelihood from incomplete data via the em algorithm. Journal of the Royal Statistical Society: Series B (Methodological), 39(1):1–22, 1977.

- Dornheim and Brazauskas [2007] H. Dornheim and V. Brazauskas. Robust and efficient methods for credibility when claims are approximately gamma-distributed. North American Actuarial Journal, 11(3):138–158, 2007.

- Dupuis and Morgenthaler [2002] D. J. Dupuis and S. Morgenthaler. Robust weighted likelihood estimators with an application to bivariate extreme value problems. Canadian Journal of Statistics, 30(1):17–36, 2002.

- Embrechts et al. [1999] P. Embrechts, S. I. Resnick, and G. Samorodnitsky. Extreme value theory as a risk management tool. North American Actuarial Journal, 3(2):30–41, 1999.

- Field and Smith [1994] C. Field and B. Smith. Robust estimation: A weighted maximum likelihood approach. International Statistical Review/Revue Internationale de Statistique, pages 405–424, 1994.

- Fung et al. [2020] T. C. Fung, A. L. Badescu, and X. S. Lin. Fitting censored and truncated regression data using the mixture of experts models. 2020. Available in SSRN: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3740061.

- Fung et al. [2021] T. C. Fung, G. Tzougas, and M. Wuthrich. Mixture composite regression models with multi-type feature selection. arXiv preprint arXiv:2103.07200, 2021.

- Gong and Ling [2018] C. Gong and C. Ling. Robust estimations for the tail index of Weibull-type distribution. Risks, 6(4):119, 2018.

- Grün and Miljkovic [2019] B. Grün and T. Miljkovic. Extending composite loss models using a general framework of advanced computational tools. Scandinavian Actuarial Journal, 2019(8):642–660, 2019.

- Gui et al. [2018] W. Gui, R. Huang, and X. S. Lin. Fitting the Erlang mixture model to data via a gem-cmm algorithm. Journal of Computational and Applied Mathematics, 343:189–205, 2018.

- Hill [1975] B. M. Hill. A simple general approach to inference about the tail of a distribution. The annals of statistics, pages 1163–1174, 1975.

- Hu and Zidek [2002] F. Hu and J. V. Zidek. The weighted likelihood. Canadian Journal of Statistics, 30(3):347–371, 2002.

- Huber [1981] P. J. Huber. Robust statistics. Wiley, New York, 1981.

- Jamshidian and Jennrich [1997] M. Jamshidian and R. I. Jennrich. Acceleration of the EM algorithm by using quasi-newton methods. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 59(3):569–587, 1997.

- Konishi and Kitagawa [1996] S. Konishi and G. Kitagawa. Generalised information criteria in model selection. Biometrika, 83(4):875–890, 1996.

- Lee and Scott [2012] G. Lee and C. Scott. EM algorithms for multivariate gaussian mixture models with truncated and censored data. Computational Statistics & Data Analysis, 56(9):2816–2829, 2012.

- Lee and Lin [2010] S. C. Lee and X. S. Lin. Modeling and evaluating insurance losses via mixtures of Erlang distributions. North American Actuarial Journal, 14(1):107–130, 2010.

- Marazzi and Yohai [2004] A. Marazzi and V. J. Yohai. Adaptively truncated maximum likelihood regression with asymmetric errors. Journal of statistical planning and inference, 122(1-2):271–291, 2004.

- Markatou [2000] M. Markatou. Mixture models, robustness, and the weighted likelihood methodology. Biometrics, 56(2):483–486, 2000.

- Markatou et al. [1997] M. Markatou, A. Basu, and B. Lindsay. Weighted likelihood estimating equations: The discrete case with applications to logistic regression. Journal of Statistical Planning and Inference, 57(2):215–232, 1997.

- McLachlan and Peel [2004] G. McLachlan and D. Peel. Finite Mixture Models. John Wiley & Sons, 2004.

- Miljkovic and Grün [2016] T. Miljkovic and B. Grün. Modeling loss data using mixtures of distributions. Insurance: Mathematics and Economics, 70:387 – 396, 2016. ISSN 0167-6687.

- Poudyal [2021a] C. Poudyal. Robust estimation of loss models for lognormal insurance payment severity data. ASTIN Bulletin: The Journal of the IAA, 51(2):475–507, 2021a.

- Poudyal [2021b] C. Poudyal. Truncated, censored, and actuarial payment-type moments for robust fitting of a single-parameter pareto distribution. Journal of Computational and Applied Mathematics, 388:113310, 2021b.

- Scollnik [2007] D. P. Scollnik. On composite lognormal-pareto models. Scandinavian Actuarial Journal, 2007(1):20–33, 2007.

- Serfling [2002] R. Serfling. Efficient and robust fitting of lognormal distributions. North American Actuarial Journal, 6(4):95–109, 2002.

- Smith et al. [1987] R. L. Smith et al. Estimating tails of probability distributions. The annals of Statistics, 15(3):1174–1207, 1987.

- Verbelen et al. [2015] R. Verbelen, L. Gong, K. Antonio, A. Badescu, and S. Lin. Fitting mixtures of Erlangs to censored and truncated data using the em algorithm. ASTIN Bulletin, 45(3):729–758, 2015.

- Wang [2001] S. X. Wang. Maximum weighted likelihood estimation. PhD thesis, University of British Columbia, 2001.

- Wang et al. [2004] X. Wang, C. van Eeden, and J. V. Zidek. Asymptotic properties of maximum weighted likelihood estimators. Journal of Statistical Planning and Inference, 119(1):37–54, 2004.

- Wang et al. [2005] X. Wang, J. V. Zidek, et al. Selecting likelihood weights by cross-validation. The Annals of Statistics, 33(2):463–500, 2005.

- Wong et al. [2014] R. K. Wong, F. Yao, and T. C. Lee. Robust estimation for generalized additive models. Journal of Computational and Graphical Statistics, 23(1):270–289, 2014.

- Wuthrich and Merz [2021] M. V. Wuthrich and M. Merz. Statistical foundations of actuarial learning and its applications. Available at SSRN, 2021.

- Zhao et al. [2018] Q. Zhao, V. Brazauskas, and J. Ghorai. Robust and efficient fitting of severity models and the method of winsorized moments. ASTIN Bulletin: The Journal of the IAA, 48(1):275–309, 2018.