Recursive Utility with Investment Gains and Losses: Existence, Uniqueness, and Convergence††thanks: We are grateful to participants at the Fifth Asian Quantitative Finance Conference in Seoul, the Second Paris-Asia Conference in Quantitative Finance in Suzhou, and the 10th World Congress of The Bachelier Finance Society in Dublin. Xue Dong He acknowledges financial support from the General Research Fund of the Research Grants Council of Hong Kong SAR (Project No. 14225916).

Abstract

We consider a generalization of the recursive utility model by adding a new component that represents utility of investment gains and losses. We also study the utility process in this generalized model with constant elasticity of intertemporal substitution and relative risk aversion degree, and with infinite time horizon. In a specific, finite-state Markovian setting, we prove that the utility process uniquely exists when the agent derives nonnegative gain-loss utility, and that it can be non-existent or non-unique otherwise. Moreover, we prove that the utility process, when it uniquely exists, can be computed by starting from any initial guess and applying the recursive equation that defines the utility process repeatedly. We then consider a portfolio selection problem with gain-loss utility and solve it by proving that the corresponding dynamic programming equation has a unique solution. Finally, we extend certain previous results to the case in which the state space is infinite.

Key words: recursive utility, gains and losses, existence and uniqueness, Markov processes, portfolio selection, dynamic programming

AMS Subject Classifications: 91G10

JEL Codes: G02, G11

1 Introduction

Barberis and Huang (2009, 2008) and Barberis et al. (2006) propose a utility specification that allows for narrow framing in a discrete-time, multiple-period setting in which an agent derives utility not only from her consumption stream but also from the investment gain and loss incurred by holding certain risky assets. The former is referred to as consumption utility, the latter as gain-loss utility. The total utility of the agent is computed based on the classical recursive utility model (Kreps and Porteus, 1978, Epstein and Zin, 1989): The total utility for the agent’s consumption and investment starting from time is the aggregation of 1) her consumption at time , 2) her gain-loss utility in the period from to , and 3) the time- certainty equivalent of her total utility for consumption and investment starting from time . In particular, when the gain-loss utility is set at zero, the model of narrow framing degenerates into the classical recursive utility model.

Just as in the classical recursive utility model, the aggregation of different components of utility in the model of narrow framing is achieved by a so-called aggregator function and the certainty equivalent is computed under the expected utility theory. The aggregator thus measures the elasticity of intertemporal substitution (EIS) and the certainty equivalent measures the relative risk aversion degree (RRAD) of the agent. As in many applications of the classical recursive utility model to portfolio selection and asset pricing, in their model of narrow framing, Barberis and Huang (2009, 2008) and Barberis et al. (2006) select a specific aggregator in which the EIS is constant and a specific certainty equivalent in which the RRAD is constant; see the exact forms in (2) and (3). Furthermore, the authors adopt an infinite-horizon setting. Both the specific choice of the aggregator and certainty equivalent and the infinite-horizon setting are known to be simple and helpful in obtaining closed-form solutions to a variety of problems.

The model of narrow framing is successful in explaining some empirical findings, such as why people are averse to small, independent gambles, even when the odds are actuarially favorable; see for instance Barberis et al. (2006). This model is further extended by De Giorgi and Legg (2012) and He and Zhou (2014) with various applications, and these authors also assume constant EIS and RRAD and adopt the infinite-horizon setting. Even with many successful applications, however, the existence and uniqueness of the agent’s (total) utility process in the model of narrow framing have not been established. Indeed, in the infinite-horizon setting, the agent’s utility is defined recursively without an end date, so its existence and uniqueness cannot be taken for granted. Surprisingly, even for the classical recursive utility, its existence and uniqueness have not been completely established; see Section 2 below.

In the present paper, we consider a generalization of the recursive utility model that adds a component of gain-loss utility and thus accommodates various models of narrow framing in the literature; see the recursive equation (4) in the following, which defines the agent’s total utility per unit of her wealth. Assuming constant EIS and RRAD, we study the existence and uniqueness of the agent’s utility process in this generalized recursive utility model in a specific Markovian setting. More precisely, we assume a Markov process and a process that is an independent sequence conditional on . Thus, models the dynamics of market states and can be interpreted as random noise. The asset returns in the period from to are assumed to be functions of , , and , so the agent’s consumption propensity, percentage investment in the assets, and utility of gains and losses per unit of investment in that period are functions of . We further assume that is irreducible and focus mainly on the case in which the state space is finite. See Section 3.1 for details of the model setting and Section 3.2 for the relevance of the setting in portfolio selection problems.

The Markovain setting here is the same as the one assumed in Hansen and Scheinkman (2012) and in a recent, independent work by Borovička and Stachurski (2019), except that we make different assumptions regarding the state space of . Both of these two works study the existence and uniqueness of the classical recursive utility with non-unitary EIS and RRAD. Compared to their works, we consider additional utility of investment gains and losses, which is motivated by the aforementioned models of narrow framing. In addition, we consider unitary EIS and RRAD as well, and also study portfolio selection problems for agents with preferences as specified by Barberis and Huang (2008). On the other hand, we focus mainly on the case of a finite state space for , while Hansen and Scheinkman (2012) consider a general state space and Borovička and Stachurski (2019) consider a compact one. See Section 2 for a detailed comparison of our results with theirs and with other related works. The finite-state setting helps us to obtain more complete results than those in Hansen and Scheinkman (2012) and Borovička and Stachurski (2019), and also makes it possible to tackle the difficulties in our analysis arising from the gain-loss utility. In addition, although the finite-state setting does not hold in many theoretical models in finance and economics,111See for instance Bansal and Yaron (2004), Hansen et al. (2008), and Schorfheide et al. (2018) for such models. it is still sufficient for many financial applications. First, finite-state Markov processes can be sufficiently flexible to describe financial data. Second, we do not impose any assumption on ; in particular, can be unbounded, so our framework accommodates the model of Barberis and Huang (2008), in which the state space for is a singleton and follows a two-dimensional normal distribution. Third, in many numerical experiments, the state space, even when assumed to be infinite in a theoretical model, is discretized to a set of finite elements; see e.g., Campbell et al. (2001).

Because of the Markovian setting, identifying the agent’s utility process is equivalent to solving the fixed point for an operator as defined by (6) in the following, and this fixed point represents the agent’s total utility divided by her consumption in the current period as a function of the market state. We prove that when a growth condition holds, for any values of the EIS and RRAD, the fixed point of the operator—or, equivalently, the agent’s utility process—uniquely exists when her gain-loss utility in each period is nonnegative. When the gain-loss utility can be negative in some states, however, the utility process can be non-existent or non-unique even in some simple settings, such as in the setting in which the EIS is less than or equal to one and the state space of is a singleton. In this case, we propose a sufficient condition under which the utility process uniquely exists, and this condition is nearly necessary.

We also prove that if the utility process uniquely exists, it can be obtained by starting from any positive utility as an initial guess and applying the recursive equation that defines the utility process repeatedly. This result is not only computationally useful but also economically important: it shows that as the number of periods in a finite-horizon model goes to infinity, the agent’s utility in that model, for any specification of the terminal utility, converges to the one in the corresponding infinite-horizon model.

We then consider a portfolio selection problem involving an agent whose preferences are represented by the model of narrow framing proposed in Barberis and Huang (2008). We prove that a consumption-investment plan is optimal if and only if it, together with the value function of the portfolio selection problem, satisfies a dynamic programming equation. Moreover, we prove that the solution to the dynamic programming equation uniquely exists and can be computed by solving the equation recursively with any initial guess. As a result, the portfolio selection problem in a finite-horizon setting approaches that in the infinite horizon setting as the number of periods in the former goes to infinity.

We also extend some of our results to the case of a non-finite state space. Assuming nonnegative gain-loss utility, we prove the existence of the utility process for non-unitary EIS and uniqueness with further conditions on the EIS and RRAD, and our results generalize those in Hansen and Scheinkman (2012).

Technically, with nonnegative gain-loss utility, the proof of existence of the utility process in the present paper follows closely the approach taken by Hansen and Scheinkman (2012) and is based on the classical Perron-Frobenius theory, although some adaption is needed due to the gain-loss utility. The proof of existence in the case of negative gain-loss utility and the proof of uniqueness in general, however, cannot follow the same approach, so we develop new methods to accomplish the proof. In addition to proving existence and uniqueness of the agent’s utility process with gain-loss utility for the first time in the literature, our results, when confined to the recursive utility model, also improve upon the existing results; see the detailed literature review provided in Section 2. Finally, the study of the portfolio selection problem and the techniques used therein are completely new.

It is not only mathematically interesting but also economically important to study the issue of the existence and uniqueness of the utility process in the generalized recursive utility model. Our results show that with negative gain-loss utility, the utility process in the model of narrow framing is nonexistent or non-unique and thus is not well defined if the agent’s EIS is less than or equal to one. Note that in many applications of the model of narrow framing, the gain-loss utility is indeed negative and the EIS is indeed less than one; see e.g., Barberis and Huang (2009), De Giorgi and Legg (2012), and Easley and Yang (2015). Thus, our results suggest that one should use the model of narrow framing cautiously. Inspired by this observation, Guo and He (2017) propose a new preference model that allows for narrow framing, and this new model is able to accommodate negative gain-loss utility while implying a uniquely defined utility process; see the detailed discussion therein.

The remainder of the paper is organized as follows: In Section 2 we review and compare our results to the literature. In Section 3 we introduce the generalized recursive utility model and in Section 4 we prove the existence and uniqueness of the utility process in a finite-state Markovian setting. In Section 5, we consider a portfolio selection problem with narrow framing and prove the existence and uniqueness of the solution to the corresponding dynamic programming equaiton. In Section 6, we provide some extensions of the existence and uniqueness results to the non-finite-state Markovian setting. Section 7 concludes. Proofs are presented in the Appendix.

2 Literature Review

Recursive utility is a classical model for individual’s preferences with respect to discrete-time consumption streams; see Kreps and Porteus (1978) and Epstein and Zin (1989). In an infinite-horizon setting, the recursive utility of consumption stream , that is derived by an agent is represented by , , where stands for the utility of the consumption stream starting from time , i.e., , . The recursive utility process is defined recursively by

| (1) |

where stands for the certainty equivalent of random quantity conditional on the information at time and is an aggregator. There are various choices of the certainty equivalent and aggregator, but the following one, which was first proposed by Kreps and Porteus (1978), is popular due to its tractability in deriving asset pricing results (see e.g., Epstein and Zin, 1990, 1991):

| (2) | ||||

| (3) |

where stands for the expectation operator conditional on the information at time . In addition, is a discount rate, stands for the relative risk aversion degree (RRAD),222Note that any affine transformation of does not affect the certainty equivalent . In particular, in some literature takes the form so that it is increasing and thus can be directly interpreted as an utility function. The form of used in the present paper is notational simpler to use in the following analysis. and is the elasticity of intertemporal substitution (EIS); see e.g., Kreps and Porteus (1978) and Epstein and Zin (1989).

In the following, when , we set for , for , and . As a result, is well defined, takes real values, and continuous in . Similarly, when , we define and ; when , we define and . As a result, is well defined for any nonnegative random variable and increasing in . Moreover, when and with a positive probability, .

Note that in the infinite-horizon setting the recursive utility process is defined recursively without a terminal condition, so the existence and uniqueness of this process is not automatically guaranteed. In the following, we review the relevant literature. Note that when , is a trivial solution to (1), so in this case a non-trivial solution is referred to in the following discussion.

Epstein and Zin (1989) prove the existence of the recursive utility process when the aggregator is given by (2) with , assuming that consumption processes essentially have bounded growth rates.333Epstein and Zin (1989) use a different set of notations from ours: and therein correspond to and , respectively, in the present paper. In the following discussion, we follow the notation used throughout the present paper. Epstein and Zin (1989) prove the existence of the recursive utility process when , assuming that consumption processes essentially have bounded growth rates; see Theorem 3.1 and the definition of therein. Although the authors also construct a solution to the recursive equation when , this solution can be trivial; see the proof of Theorem 3.1 on pp. 964–965. Ma (1993, 1996, 1998) prove the existence and uniqueness of the recursive utility process by assuming that , the derivative of the aggregator with respect to , is bounded uniformly in and by a number that is strictly less than one.444See Assumption W4 in Ma (1993, p. 246) and Ma (1996, p. 568). In Ma (1998), the author assumes that the recursive utility for deterministic consumption flows is well defined, but this requires to be bounded by a number strictly less than one as well; see Footnote 5 of Ma (1998) and Assumption W5 in Lucas and Stokey (1984). However, this assumption does not hold for as defined in (2) for any . Balbus (2016) assumes that there exists such that for any , , and , which cannot hold for as defined in (2) for any .555See Assumption 3 therein. Note that a similar assumption is made by Le Van et al. (2008) in their study of monotone, concave operators, so their results cannot be applied here either; see condition (P1) therein. Ozaki and Streufert (1996) prove the existence and uniqueness of the recursive utility process by assuming to be uniformly bounded in and and a set of conditions to hold.666In Ozaki and Streufert (1996, Theorem D), the authors assume that and therein are finite, which is equivalent to assuming that is bounded; see pages 403–406 therein. However, these conditions are difficult to verify; see conditions N1–N12 in Ozaki and Streufert (1996, pp. 404–405); in addition, for as defined in (2), is not bounded when .

Marinacci and Montrucchio (2010) consider Thompson and Blackwell aggregators and study the existence and uniqueness of the recursive utility process with these two types of aggregator.777In a recent work, Becker and Rincon-Zapatero (2017) derive some results that are essentially the same as those in Marinacci and Montrucchio (2010). One can check that as defined in (2) satisfies properties (W-i), (W-ii), and (W-iii) in Marinacci and Montrucchio (2010, p. 1783), satisfies property (W-iv) therein if and only if , and does not satisfy property (W-v) therein for any . Thus, as defined in (2) with is a Thompson aggregator, but the case in which is neither Thompson nor Blackwell. Moreover, as defined in (3) is constant relative risk averse (CRRA), i.e., is constant in , so Theorem 3-(ii) of Marinacci and Montrucchio (2010) applies, showing that (i) the recursive utility process exists if consumption is bounded at each time (but the bound can be dependent on time) and (ii) uniqueness follows if the consumption growth rate satisfies a restrictive assumption.888The aggregator is -subhomogeneous, as defined in Marinacci and Montrucchio (2010, p. 1784), for any . Thus, Theorem 3-(ii) in Marinacci and Montrucchio (2010) implies the existence of the recursive utility process when consumption processes belong to for some weight function , which essentially means that consumption is bounded at each time; see Section 2.2 therein. To have uniqueness, one needs to further assume that satisfies . This condition, together with the condition that the consumption process is in , nearly implies that the consumption growth rate is a constant as goes to infinity; see Section 2.2 therein. The case in which , however, is not studied by Marinacci and Montrucchio (2010).999Alternatively, one can consider the following transformation: , where when and when . Then, we have for a new aggregator . However, is finite only if , and the aggregators considered in Marinacci and Montrucchio (2010) are assumed to take real values for any , so the results in Marinacci and Montrucchio (2010) do not apply to the case either, even if we perform the transformation.

Hansen and Scheinkman (2012) assume that the consumption growth rate for some function , where is a Markov process and the joint distribution of conditional on depends only on . They show that for and as defined, respectively, in (2) and (3) with and , if a growth condition on the consumption process holds, the recursive utility process exists. They also show the uniqueness of the recursive utility process when .

In the present paper, we consider a generalization of the recursive utility by adding to the recursive equation (1) a component that represents utility of investment gains and losses, and this generalization allows us to accommodate a variety of utility models with narrow framing; see Section 3 below. We then prove that the utility process in our model (i) uniquely exists and (ii) is globally attracting in that it can be obtained by starting from any initial guess and applying the recursive equation that defines the utility process repeatedly.

Our results, when refined to the case of recursive utility, generalize the above literature as well. First, in the finite-state Markovian setting, we obtain the existence and uniqueness of the utility process for any values of and under a mild growth condition on the consumption process, although no complete results have yet been obtained in the literature. Second, we also prove that the utility process is globally attracting, whereas in the aforementioned works, without uniqueness, the authors can only prove that the utility process is locally attracting in that it can be computed by starting from certain specific initial guesses only. Third, we also consider a portfolio selection problem, leading to a dynamic programming equation, and show that the solution to this equation is existent, unique, and globally attracting. Epstein and Zin (1989) consider a portfolio selection problem and show that the corresponding dynamic programming equation admits a solution, assuming certain conditions on asset returns and consumption growth rates; see Theorem 5.1 therein. After studying the existence and uniqueness of the recursive utility process, Ozaki and Streufert (1996) consider a portfolio selection problem and obtain the existence of the solution to the corresponding dynamic programming equation. Neither of these works, however, proves the uniqueness of the solution. Fourth, in a general Markovian setting, we generalize the results in Hansen and Scheinkman (2012) by proving the uniqueness of the recursive utility process in the case and in the case .

Finally, we would like to mention a recent work by Borovička and Stachurski (2019) that was carried out independently of and simultaneously with ours. These authors study the existence and uniqueness of the recursive utility process with and as defined, respectively, in (2) and (3). Using the same Markovian setting as the one in Hansen and Scheinkman (2012) and assuming the state process to be compact, the authors prove, for the case of and , that the existence, uniqueness, and global attractingness of the recursive utility process are all equivalent to a simple condition on the spectral radius of a certain operator that is associated with the recursive equation (1). We would like to emphasize that Borovička and Stachurski (2019) and the present paper have different focuses, and the results in these two papers are largely different. First, Borovička and Stachurski (2019) derive a sufficient and necessary condition for the existence and uniqueness of the recursive utility process, whereas the literature, including the present paper, is as yet unable to prove the necessity. Furthermore, their assumption on the state space of is weaker than ours: A finite state space is always compact. We, however, prove the existence and uniqueness (i) in the case in which the state space is finite and or and (ii) in the case in which the state space can be noncompact and , and these two cases are not covered by Borovička and Stachurski (2019). In addition, our approach to proving existence and uniqueness is different from the one employed in Borovička and Stachurski (2019). Second, we consider gain-loss utility, which is largely motivated by a set of models of narrow framing in the literature, whereas Borovička and Stachurski (2019) focuses on the classical recursive utility model. Third, we also study a portfolio selection problem and the associated dynamic programming equation.

Table 1 summarizes the comparison of our results to the literature.

| Assumption | Existence | Uniqueness | Attractingness | Gain-loss | DP equation | |

| EZ89 | non-Markovian; bounded | local | existence and local attractingness for | |||

| OS96 | non-Markovian; 12 conditions | existence and local attractingness for | ||||

| MM10 | non-Markovian; bounded for existence and restrictive assumptions on for uniqueness and attractingness | global | ||||

| HS12 | General Markovian; a certain growth condition | and | global when and local otherwise | |||

| BS19 | compact-state-space Markovian; a sufficient and necessary condition | and | and | global | ||

| finite-state-space Markovian; a certain growth condition | any , | any , | global | any | existence, uniqueness, and global attractingness for any , | |

| This paper | General Markovian; a certain growth condition | or | or | global when or and local otherwise | non-negative | |

| General Markovian; certain growth condition | or | or | global when or and local otherwise | |||

3 Model and Examples

3.1 Model

Consider the following equation

| (4) |

where the aggregator and certainty equivalent are given by (2) and (3), respectively. Here, stands for a consumption propensity process (i.e., stands for the percentage of wealth that is used for consumption at time ), is a process that is used to model portfolio returns, and is used to model the utility of investment gains and losses per unit of wealth. Our goal is to establish the existence and uniqueness of the solution to this equation, which represents the agent’s total utility per unit wealth.

Following Hansen and Scheinkman (2012), we consider equation (4) in a Markovian environment. More precisely, we consider a Markov process and assume the following:

Assumption 1

-

(i)

is a Markov process and the joint distribution of conditional on depends only on .

-

(ii)

Consumption propensity and portfolio return dynamics evolve according to

for some real-valued measurable function .

-

(iii)

for some real-valued measurable function .

-

(iv)

For any state , exists.

Assumption 1-(i) is the same as Assumption 1-a) in Hansen and Scheinkman (2012); it implies that is a Markov process, and we denote its state space as . On the other hand, this assumption holds if is Markovian and , conditional on , is an independent time series. Assumptions 1-(ii) and -(iii) are parallel to Assumption 1-b) in Hansen and Scheinkman (2012), which ensure a Markovian structure in equation (4). Compared to the setting in Hansen and Scheinkman (2012), we have two additional terms, and ; the relevance of adding them to the model and the above Markovian assumption will become clear in Section 3.2. We assume the state space to be a metric space, so the measurability in Assumption 1 is with respect to Borel -algebra of .

Dividing (4) by on both sides and using the homogeneity of , we obtain

| (5) |

Thus, to solve equation (4), we only need to solve from (5). Moreover, because of Assumption 1, we restrict ourselves to Markovian solutions to (5), i.e., for some function . Then, the solution to equation (5) becomes the fixed point of operator , defined as

| (6) |

Note that represents the agent’s total utility divided by her consumption in the current period.

Denote by the space of measurable functions on , the space of nonnegative measurable functions on , i.e., , the space of nonnegative functions on that are not zero, i.e., , and the space of positive functions on , i.e., . Recalling the definitions of , , and , we can see that the domain of is contained in .

In the following, denote by the set of real numbers. For , we denote and . For any , we denote its positive part as , i.e., . For any , means and means . Any also denotes the function on that takes value in all states.

3.2 Examples

3.2.1 Recursive Utility Model

Recall the recursive utility model (1). Denote by the agent’s wealth process corresponding to a consumption strategy, i.e., a consumption process , and an investment strategy, i.e., the process of the dollar amount invested in asset , , . Then, the wealth dynamics evolve according to

where and are the gross returns of asset and the risk-free asset, respectively, in period to . Because of the homogeneity of , , and , the agent’s utility per unit wealth, , satisfies

where is the consumption propensity at time , is the percentage allocation to risky asset at time , , and

| (7) |

is the portfolio return in period to . If we denote , then solves (4) with and .

3.2.2 Models that Allow for Narrow Framing

Barberis and Huang (2009, 2008) and Barberis et al. (2006) consider a model of narrow framing: in addition to consumption utility, the agent evaluates each risky asset in a separate mental account and derives utility from the investment gain and loss in the asset. Thus, the agent’s utility process is defined recursively as follows:

| (8) |

where is a constant and stands for the utility of the gain and loss experienced by the agent for her investment in asset .

In Barberis and Huang (2009, 2008) and Barberis et al. (2006),

| (9) |

for some . Indeed, represents the preference value of the agent’s position in asset under prospect theory (Kahneman and Tversky, 1979, Tversky and Kahneman, 1992) with the reference point as the risk-free return, utility function as a piece-wise linear function in which parameter measures the loss aversion degree of the agent, and no probability weighting. Thus, captures the agent’s utility of the gain and loss for her investment in asset due to narrow framing. Later, De Giorgi and Legg (2012) generalize (9) by considering a piece-wise power utility function and nonlinear probability weighting functions. He and Zhou (2014) consider the case in which there is only one risky asset, but the reference point therein can be different from the risk-free return. All of the above variants of the model of narrow framing can be written in the form (8).101010In Barberis and Huang (2001), Barberis et al. (2001), and Li and Yang (2013) the utility of gains and losses is scaled by a power transformation of the aggregate consumption in the market, and their models take the form of (8) with a time-varying, random .

Now, define to be the agent’s utility per unit wealth in the model of narrow framing and as the consumption propensity at time . Then, solves equation (4) with and .

3.2.3 Markovian Assumption

In the following, we show that Assumption 1 is appropriate for the above examples. To this end, we consider the model of narrow framing (8) with gain-loss utility specified in (9) and assume for simplicity that . Denote

| (10) |

which stands for the utility of gains and losses per unit of investment in asset . Then, solves equation (4) with

| (11) |

Note that stands for the growth of the agent’s wealth in period to and stands for the agent’s utility of gains and losses per unit of wealth.

Suppose that the gross return rate of risky asset in period to is , , for some function and that the gross return rate of the risk-free asset in period to is , , for some function . Because, conditional on , the joint distribution of depends only on , it is natural for the agent to consider Markovian strategies only, i.e., to consider , , , , for some functions and ’s. Consequently, Assumption 1-(ii) holds. On the other hand, one can see that depends on only, so the utility of gains and losses per unit of wealth is a function of . Because the consumption propensity , we conclude that Assumption 1-(iii) holds as well.

Finally, we have

Thus, stands for consumption growth rate .

4 Existence, Uniqueness, and Convergence

In this section, we study the existence and uniqueness of the solution to (4)—that is, of the fixed point of (6)—when the state space of is finite. Thus, we impose

Assumption 2

The state space for is finite and is irreducible.

Hansen and Scheinkman (2012) consider a general Markov process when studying the solution to (1), and they implicitly assume the existence of the Perron-Frobenius eigenvalue and eigenvector of a linear operator and the stochastic stability of after a change of measure; see equation [4] and Assumption 2 therein. These assumptions hold automatically when Assumption 2 is in place; see Proposition 1 below. Their results, however, cannot be applied here because we consider utility of gains and losses in our model, and even for the case of recursive utility, they do not obtain the uniqueness for a large range of parameter values; see the detailed discussion following Theorem 1 below.

Note that we assume to be irreducible. This assumption is necessary for the existence of the stationary distribution of , which will be used in the following. Note also that we do not impose any assumptions on ; in particular, can be unbounded.

When is finite, defined by is continuous in . Indeed, fix any and consider a sequence that converges to . Denote by the set of such that and the set of such that . Define . Then decreasingly converges to 0 as , and . Consequently, for any fixed , we have

If , or if , or if , the dominated convergence theorem shows that

as , so we conclude that

If and , in which case , we have

as , so

Similarly, when and , we also have .

On the other hand, we need to show . This is trivially true when and because in this case . In the remaining cases in which , or , or , using the dominated convergence theorem, we can easily show . Thus, we conclude that .

Now, recalling that is continuous in , we conclude that is continuous. However, we cannot apply the classical Brouwer fixed point theorem to prove the existence and uniqueness of the fixed point of . First, the domain of under consideration in the following, namely, , is not compact. Second, the Brouwer theorem does not imply uniqueness of the fixed point. Third, the Brouwer theorem does not show how to compute the fixed point; however, we will provide an easy algorithm to compute the fixed point.

4.1 Changing the Probability Measure

We follow Hansen and Scheinkman (2012) in performing a change of probability measure based on the classical Perron-Frobenius theory. To this end, consider the following operator

With Assumptions 1 and 2, this operator is well defined. Denote by the transition matrix of , i.e., , . Define matrix by , .

Proposition 1

Suppose Assumptions 1 and 2 hold.

-

(i)

Suppose . Then, there exist and such that

(12) Moreover, and are the Perron-Frobenius eigenvalue and eigenvector of , respectively.

-

(ii)

Suppose . Then, there exist and such that

(13) In addition,

where vector is the stationary distribution of .

-

(iii)

Define . Then,

Proposition 1-(i) is the same as equation [4] in Hansen and Scheinkman (2012), but Proposition 1-(ii) is new, as these authors do not consider the case .111111Note that the notations in Hansen and Scheinkman (2012) are different from ours: therein corresponds to in the present paper. Proposition 1-(iii) transforms obtained in Proposition 1-(i) and -(ii) into that is easy to use in the following. More importantly, it provides an economic interpretation for by representing it as a special form of the certainty equivalent of the consumption growth rate . This interpretation is not available in Hansen and Scheinkman (2012).

As we will see, is critical in proving the existence and uniqueness of the fixed point of . Thus, it is important to compute , i.e., to compute . When , is the Perron-Frobenius eigenvalue of , so its computation has been studied extensively in the literature; see e.g., Chanchana (2007). When , is actually the expectation of under the stationary distribution of , which is also easy to compute.

4.2 Case of Nonnegative Gain-Loss Utility

Theorem 1

Theorem 1 shows that when the state space of is finite and is nonnegative, the fixed point of in and, thus, the utility process defined by (4) uniquely exist provided that . Condition is the same as the one in Hansen and Scheinkman (2012, Proposition 6), where the authors study the existence and uniqueness of the classical recursive utility (without gain-loss utility). Thus, in a finite-state setting and in the case of recursive utility (by setting ), Theorem 1 generalizes the results in Hansen and Scheinkman (2012) because in the latter the authors do not consider the case of unitary EIS and RRAD nor prove the uniqueness when .

Note that we restrict the domain of to although is well defined on . This is because can have nonpositive fixed points. For example, when and , is a fixed point of . When , , the transition matrix of is positive, and for some , we can verify that is a fixed point of but is not in . The fixed points in these two examples, however, are not economically meaningful in representing the total utility of the agent’s consumption and investment: given a positive consumption stream and nonnegative gain-loss utility, we expect the agent’s total utility to be positive. Thus, we need to exclude such fixed points by restricting the domain of to and, by doing so, we obtain the uniqueness of the fixed point.

Theorem 1 also provides a simple algorithm to compute the fixed point: one can start from any positive function, e.g., a positive constant function, to do iteration and then obtain a sequence that eventually converges to the fixed point. This result provides another reason why nonpositive fixed points of , if they exist, are not desirable: These fixed points cannot be obtained by a recursive algorithm with any positive starting point.

In the above algorithm, one can also choose a nonnegative function, i.e., , as the initial guess, provided that for some . Such exists (i) for any if because and (ii) for any if because is irreducible and for any nonnegative, nonzero random variable when . If and , however, may not converge to the fixed point of in . For instance, suppose contains two elements, e.g., and , the transition matrix of is positive, and . Consider such that and . Note that because and that for any nonnegative random variable taking zero with a positive probability because . We then immediately obtain that and thus the limit is 0; in other words, this sequence does not converge to the fixed point of in .

The convergence of to the fixed point of for any positive is economically important: it shows that a finite-horizon model, in which the utility at the terminal time is positive, converges to the infinite-horizon model when the number of periods in the former model goes to infinity. Moreover, the utility at the terminal time in the former model is irrelevant, provided that it is positive.

4.3 Case of Negative Gain-Loss Utility

We first illustrate that when for some , can have zero, one, or multiple fixed points, depending on the parameter values.

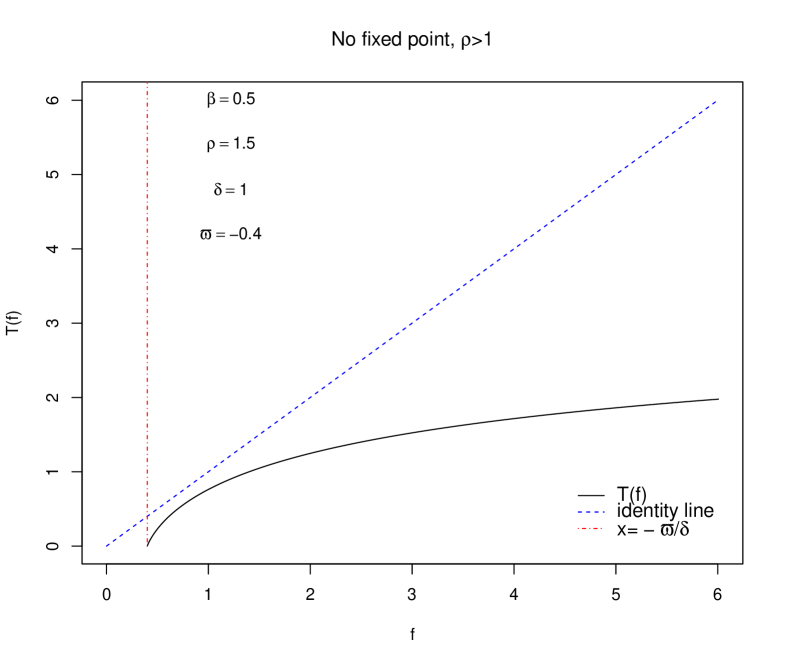

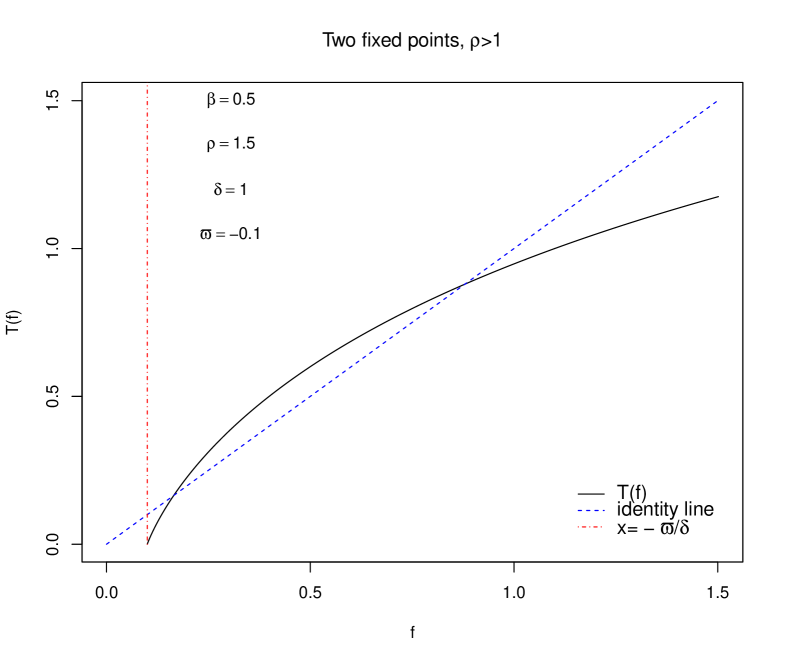

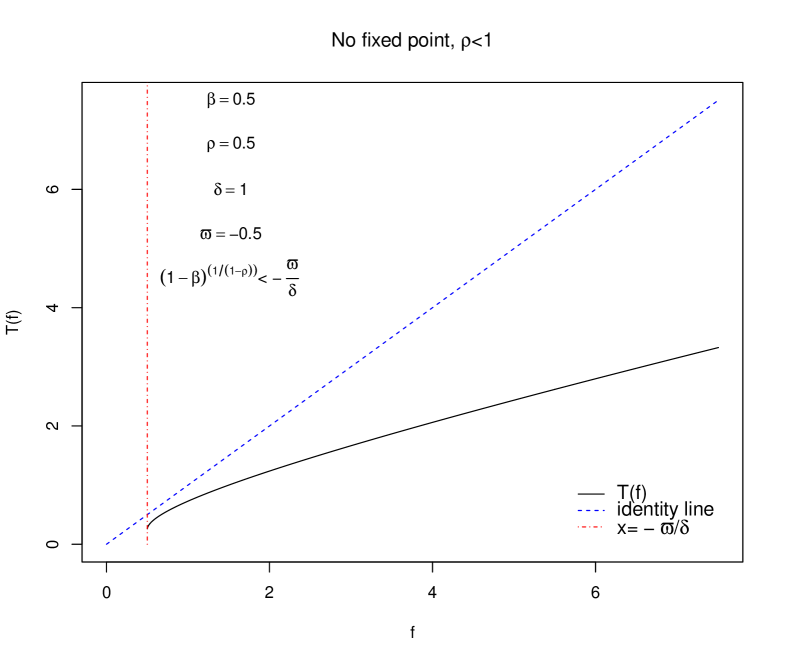

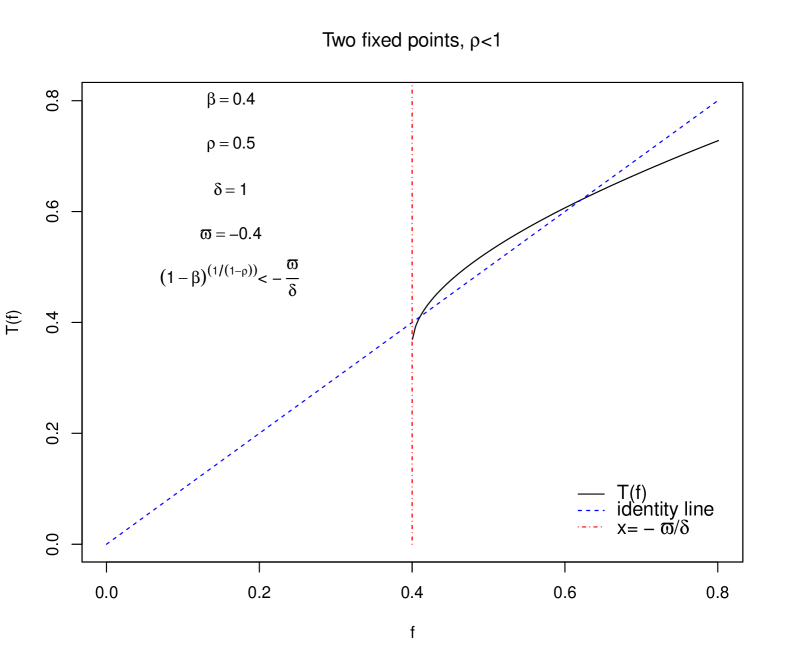

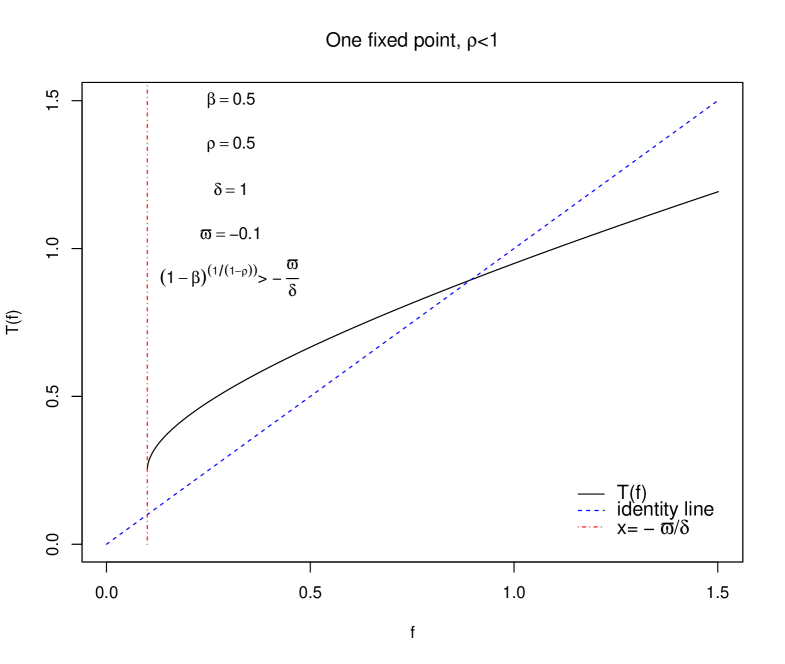

Example 1

Suppose is a singleton. Then, operator becomes a function on , and we denote this function as . In this case, defined in Proposition 1 becomes . Then, function can be written as . We assume , and Theorem 1 shows that the fixed point of in uniquely exists when . Next, we consider the case in which .

It is obvious that the domain of is . Straightforward computation yields

Moreover, is strictly increasing and concave.

We first consider the case in which . Note that in this case . Because and , we conclude that except in a very special case in which the identity line is tangent to , it is either the case in which has no fixed point or the case in which has two fixed points; see Figure 1.

Next, consider the case in which . If , we conclude, as in the case in which , that except in a very special case in which the identity line is tangent to , it is either the case in which has no fixed point or the case in which has two fixed points. If , then the fixed point exists and is unique; see Figure 2.

Note that stands for the consumption growth rate in the model of narrow framing in Section 3.2.2, so stands for the certainty equivalent of the consumption growth rate and thus is decreasing with respect to the RRAD. On the other hand, stands for the disutility of loss. We can see that with , inequality holds if is small, is large, and is small. Thus, we can conclude that the agent’s total utility is well defined when her EIS is strictly larger than one, her time discounting is large, her consumption growth rate is high, her RRAD is low, and her disutility of loss is small.

Example 1 shows that we need some conditions on model parameters in order to establish the existence and uniqueness of the fixed point of when is negative in some states.

Assumption 3

Denote

| (14) |

Assume is well defined, i.e.,

and for some .

Theorem 2

Theorem 2 shows the existence and uniqueness of the fixed point of when can go negative. Moreover, the calculation of the fixed point is easy: Start from any such that is well defined and apply repeatedly. Then, the resulting sequence converges to the fixed point. As discussed in the case of nonnegative , this algorithm implies that a finite-horizon model converges to the infinite-horizon model when the number of periods in the former goes to infinity.

Assumption 3 is crucial in order to obtain the existence and uniqueness of the fixed point of , so we discuss it in detail in the following:

(i) Note that if is well defined, we must have . However, this is insufficient to guarantee the uniqueness of the fixed point of . Indeed, in the setting of Example 1, if , is well defined and, actually, . We already showed in that example that has two fixed points, that one of them is , and that both can represent the utility process. Thus, to guarantee the uniqueness, we need further conditions, and Assumption 3 serves the purpose.

(ii) Assumption 3 implies that for some . The reverse is also true when or . Indeed, suppose for some . Then, for any such that the transition probability from to is positive, either of the conditions that and that implies

As a result, , and because of the irreducibility of , we conclude that for some .

(iii) When and for some , which can be the case if and only if and , it is possible that is well defined, for some , and the fixed point of is not unique. For instance, consider with state space such that , , , and . Then, is irreducible. Suppose . Suppose , , and . Then, one can verify that , , and . Moreover, it is straightforward to see that is a fixed point of . On the other hand, suppose and . Then, straightforward calculation shows that

where stands for the constant function taking value 1 and is the partial derivative of with respect to . Because , , and , with sufficiently small (but positive) , , and , we have , . As a result, there exists such that . Consequently, is increasing and converges because for any . It is obvious that the convergent point is a fixed point of and is different from because .

5 Portfolio Selection and Dynamic Programming Equation

5.1 Model

Consider the portfolio selection problem with narrow framing as discussed in Section 3.2.2. The agent’s total utility is given by (8), and thus her total utility per unit wealth satisfies (4) with and as given by (11). Suppose the gross return rate of risky asset in period to is for some function and the gross return rate of the risk-free asset in period to is for some function . Suppose the agent chooses consumption propensity and portfolio at time for some functions and ’s. For simplicity, we assume , and the following analysis can be performed without any additional difficulty for the case of negative . Then, the agent’s total utility per unit wealth , where is a fixed point of

with and

For any and such that and , is a fixed point of if and only if is a fixed point of , where

| (15) |

and

| (16) | ||||

| (17) |

Denote in Proposition 1 as when and therein are set to be and , respectively.

For each , consider a set and a set . Define

In view of the results obtained in Section 4, we need the following assumption:

Assumption 4

For each , , , and it is either the case in which or the case in which with is well defined, and for some .

With Assumptions 2 and 4 in place, Theorems 1 and 2 show that the fixed point of in uniquely exists for any . Thus, if the agent consumes and invests dollars in risky asset , at time , her utility is well defined. As a result, the following portfolio selection problem

| (18) |

is well defined, where

Note that for each , problem (18) is equivalent to

| (19) |

5.2 Dynamic Programming

The dynamic programming equation associated with the portfolio selection problem (19) can be derived heuristically as

| (20) |

where

| (21) | |||

| (22) |

Note that the domain of is the set of in such that for any .

Proposition 2

Proposition 2 shows that the solution to the dynamic programming equation, if it exists, must be the solution to (19).

Theorem 3

Suppose that Assumptions 2 and 4 hold, , and that for each , is compact and is closed relative to (i.e., for some closed set ).

-

(i)

Suppose for any . Then, the fixed point of in uniquely exists, converges to the fixed point of in for any , and there exists such that is a maximizer of (21) for each .

-

(ii)

Suppose for some and some , and define

(23) Then, is in the domain of . Assume that there exists such that . Then, the fixed point of in uniquely exists, converges to the fixed point of in for any in the domain of , and there exists such that is a maximizer of (21) for each .

Theorem 3 shows the existence and uniqueness of the solution to the dynamic programming equation and the existence of corresponding maximizer . Note that we assume , the feasible set of percentage investment in the risky assets, to be compact and , the feasible set of percentage consumption, to be a closed set relative to ; in particular, can be . Note also that is implied by Assumption 4 when and are compact for all .121212Indeed, in this case, is compact. Because the eigenvalue of a matrix is continuous in and because under the stationary distribution of is continuous in , for any implies that . When for some and some , we impose an additional assumption: there exists such that , and the following Proposition shows that this assumption can be easily satisfied.131313The condition in Proposition 3-(iii) stipulates that the gain-loss utility is nonnegative for certain investment strategies and in certain states . It holds particularly when zero investment in the risky assets (i.e., ) is allowed.

Proposition 3

Theorem 3 also shows that starting from any that is positive when for any or any in the domain of in other cases, by applying the dynamic programming equation repeatedly, one eventually obtains the solution to the equation. This result shows that the optimal consumption and portfolio in a finite-horizon model converges to those in the infinite-horizon model when the number of periods in the former goes to infinity.

Note that is strictly concave in for each and and that is strictly concave in for any given . Thus, for each and , the maximization problem in the right-hand side of the dynamic programming equation (20), i.e., the problem in (21), can be solved easily. As a result, can be easily computed, and once we find the fixed point of , the optimal control can also be solved easily.

Finally, when for some and some , equation (23) provides a simple choice of in the domain of , which can be easily computed. Note that is convex in and is concave in for any , so the maximization in and can be computed easily.

5.3 Verification of Assumptions

There are two crucial assumptions to verify in order to apply Proposition 2 and Theorem 3: (i) and (ii) for any such that for some , for some . In this subsection, we provide sufficient conditions for these two assumptions.

Proposition 4

Because is concave in , its maximization and minimization with respect to can be computed easily, and thus conditions (24) and (25) can be verified.

Proposition 5

Suppose , , and the transition matrix of is positive. Then, the left-hand side of (26) is 0 for any that makes for certain , so (26) does not hold. This is not surprising because the analysis in Section 4.3 shows that it is difficult to define the agent’s total utility when the utility for investment gain and loss is negative. Condition (26), however, is useful and can be verified when . Indeed, a sufficient condition is given by (27), where the left-hand side of the inequality therein is concave in and thus its minimum with respect to can be computed easily.

Note that (27) cannot be satisfied if —that is, when the agent chooses to consume very little.141414Intuitively, suppose , , and in a market state , the agent derives negative gain-loss utility, i.e., . Suppose the agent consumes little in this state, i.e., , . Then, one can compute that in state and, consequently, the certainty equivalent of is nearly 0. As a result, it is impossible that this certainty equivalent plus is larger than 0 in state , so is not even well defined. This, however, does not undermine our portfolio selection results. First, when the gain-loss utility is always nonnegative, in particular when the agent’s preferences are modeled by recursive utility, we only need to verify , so the conditions in Proposition 5 are irrelevant. Second, it is reasonable for us to focus on strategies that satisfy because other strategies generate too much disutility of losses and thus should not be preferred.

5.4 A Numerical Example

We consider a market with a risky stock and a risk-free asset, and we can regard the stock as the market portfolio. Set the length of each period to be one year. To construct the return of the stock, we assume that the stock pays a dividend every year and that the dividend growth rates are i.i.d. and follow the distribution as given in Table 2.

| State | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

|---|---|---|---|---|---|---|---|---|---|

| Outcome | 0.976 | 0.993 | 1.002 | 1.011 | 1.019 | 1.028 | 1.037 | 1.045 | 1.054 |

| Probability | 0.03 | 0.03 | 0.10 | 0.16 | 0.24 | 0.19 | 0.13 | 0.09 | 0.03 |

We assume that the market is governed by a two-state Markovian process that takes values in . We assume the price-dividend ratio at time to be and the risk-free gross return rate in period to to be ; i.e., both are functions of . As a result, the gross return rate of the stock in period to is

where refers to the dividend growth rate in period to .

We assume the transition matrix of to be

We also set the risk-free total return rate and the price-dividend ratio to be

respectively, so that the mean and volatility of the stock return under the stationary distribution of are 6% and , respectively, and, consequently, the equity premium is 3%.

We set the loss aversion degree , so , which measures the gain-loss utility, is

where . Finally, we set , , , and .

Consider the feasible set and , . With the help of Propositions 4 and 5, we can verify that all assumptions in Theorem 3 hold.151515Here, we set the lower bound of to be a positive number in order to have for any . Then, we apply this theorem to calculate the optimal consumption and portfolio and the value function, and the results are as follows:

6 When the State Space is Not Finite

In this section, we study the existence and uniqueness of the solution to (4), i.e., the fixed point of , when the state space of is not finite. We consider only the case in which is nonnegative for two reasons. First, when is negative, by imposing a similar condition to Assumption 3, we can prove that the fixed point of exists, but we do not have uniqueness, so we chose not to present the results here. Second, a new model of narrow framing that is proposed by Guo and He (2017) represents a special case of (4) with .

Proposition 6

Suppose Assumption 1 holds, , and . Suppose that the results in Proposition 1-(i) and -(ii) hold and recall defined therein. When , denote as the probability measure that is obtained by a change of measure using the Radon-Nikodym density , and, when , simply refers to the original probability measure. Denote as the expectation operator corresponding to . For each , denote space when equipped with the norm under the stationary distribution of under as . Define operator on by

where , and define . Then, is a fixed point of in if and only if is a fixed point of in the same space. Moreover, with the assumptions that and that the stationary distribution of under exists, the following results hold:

-

(i)

If and , then is a contraction mapping in and its unique fixed point is positive.

-

(ii)

If and for some , then the limit of exists, belongs to , and is the minimum fixed point of in .

-

(iii)

If and , then is a fixed point of in if and only if is a fixed point of the following operator in the same space:

Moreover, if , then is a contraction mapping in , and its unique fixed point is positive.

Propositions 6-(i) and -(ii) are completely parallel to Proposition 6 in Hansen and Scheinkman (2012): When and is nonnegative, if (i) , , and in Proposition 1 are well defined and and (ii) the stationary distribution of exists after a specific change of measure, then the fixed point of exists. Moreover, when , the fixed point is unique. Our proof is also analogous to that in Hansen and Scheinkman (2012). Note that just as in Hansen and Scheinkman (2012), in general we are unable to prove uniqueness when . Following Hansen and Scheinkman (2012), we do not discuss here the issue of when the results in Proposition 1 hold and when the stationary distribution of under exists. For sufficient conditions, one can refer to Assumption 7.2 in Hansen and Scheinkman (2009) and Proposition 9.2 in Ethier and Kurtz (2009).

When , we also prove uniqueness in the recursive utility model, namely, in the case ; see Proposition 6-(iii). This result generalizes those in Hansen and Scheinkman (2012, Proposition 6) nontrivially.

Proposition 7

Suppose Assumption 1 holds and the stationary distribution of exists. Suppose and . Then, is a fixed point of in if and only if is a fixed point of in , where

| (28) | ||||

Denote equipped with the norm under the stationary distribution of as , and assume there exists such that . Then, is a contraction mapping on and thus the fixed point of uniquely exists in .

Proposition 7 shows the existence and uniqueness of the fixed point of when , provided that has a stationary distribution and is nonnegative.

Finally, we show that the solution to (4) uniquely exists when even in a non-Markovian setting.

Proposition 8

Suppose , , and . Then, is a positive solution to (4) if and only if is a fixed point of

| (29) |

Moreover, if there exist and , the space of -adapted processes with norm , such that , then is a contraction mapping on and thus the fixed point of on this space uniquely exists.

7 Conclusion

We considered a generalization of the recursive utility model that adds a component of gain-loss utility and thus accommodates a variety of models of narrow framing encountered in the literature. Assuming constant EIS and RRAD, we studied the existence and uniqueness of the agent’s utility process in this generalized model.

We assumed a Markovian setting: the asset returns in the period from to are assumed to be functions of , , and , so the agent’s consumption propensity, percentage investment, and utility of gains and losses per unit of investment for the assets in that period are functions of , where is a Markov process that represents market states and is an independent sequence conditional on and thus represents random noise. We further assumed that is irreducible and that its state space is finite.

We proved that the utility process uniquely exists for any values of the EIS and RRAD when the gain-loss utility is nonnegative. We then illustrated by an example that when the state space of is a singleton and the EIS is less than or equal to one, the utility process is either non-existent or non-unique if the gain-loss utility is negative. We then proposed a sufficient condition under which the utility process uniquely exists when the gain-loss utility is negative, and this condition is nearly necessary. We also proved that if the utility process uniquely exists, it can be computed by starting from any initial guess and applying the recursive equation that defines the utility process repeatedly.

We then considered a portfolio selection problem with narrow framing and proved that a consumption and portfolio plan is optimal if and only if it, together with the value function of the portfolio selection problem, satisfies a dynamic programming equation. Moreover, we proved that the solution to the dynamic programming equation uniquely exists and can be computed by solving the equation recursively with any starting point.

Finally, we extended some of the previous results to the setting of non-finite state spaces.

Appendix A Proofs

Proof.

Proof of Proposition 1 We first consider (i). Because of Assumption 1-(i), we have

Because is irreducible and is positive, we conclude that is also irreducible. Thus, we have (12), where and are the Perron-Frobenius eigenvalue and eigenvector of , respectively, and , ; see e.g., Meyer (2000, p. 673).

Next, we consider (ii). It is straightforward to see that (13) is equivalent to

| (30) |

where denotes the vector of and denotes the vector of all ones. Because is an irreducible stochastic matrix, the kernel of , where is the identity mapping, is the linear space spanned by the left-Perron-Frobenius eigenvector of , namely, by the stationary distribution of . As a result, the range of is the space of all vectors that are orthogonal to . By the definition of , is orthogonal to and thus is in the range of . As a result, there exists such that (30) holds. Moreover, by multiplying the stationary distribution on both sides of (30), we can see that is uniquely determined.

Finally, we prove (iii). We first consider the case in which . Because is the Perron-Frobenius eigenvalue of , according to the max-min version of the Collatz-Wielandt formula (Meyer, 2000, p. 673), we have

Moreover, it is straightforward to see that the maximum in the above formula is attained when is chosen to be the Perron-Frobenius eigenvector of . Because the eigenvector lies in , we conclude that can be replaced with in the above formula. Now, recalling and setting , we conclude that when ,

| (31) |

Similarly, according to the min-max version of the Collatz-Wielandt formula (Meyer, 2000, p. 669),161616The formula therein is presented for postive matrices, but it also holds for irreducible nonnegative matrices because the Perron-Frobenius eigenvectors for these matrices are positive; see for instance Meyer (2000, p. 673). we have

Recalling and setting , we conclude that (31) also holds when .

Finally, we show that (31) also holds when . For each , denote

As a result, . Taking expectation on both sides under the stationary distribution of and recalling that is derived in part (ii) of the proof, we conclude that , which implies . Therefore, we conclude

| (32) |

On the other hand, recall defined in part (ii) of the proof. Then, and (30) can be written as

Combining the above with (32), we immediately conclude that

Therefore, (31) holds.

Proof.

Proof of Theorem 1 For ease of exposition, the proof is divided into two parts.

Part One: existence and uniqueness of the fixed point

In the first part of the proof, we show the existence and uniqueness of the fixed point of in . The proof of the case in which follows exactly the same line as in Hansen and Scheinkman (2012), but some adaptation is needed to accommodate the gain-loss utility, so we sketch the proof in the following. For the case in which , the proof of the existence mimics the idea of Hansen and Scheinkman (2012), but the proof of the uniqueness and the global attractingness of the fixed point is completely new because they are not proved in Hansen and Scheinkman (2012). In addition, Hansen and Scheinkman (2012) did not consider the case or the case either.

Observe that is well-defined for any and that is increasing. We first note from Proposition 1-(i) that when , with , , and as defined in Proposition 1, we can define and show that and . As a result, we can define a new measure by using as the Radon-Nikodym density. Note that is still an irreducible Markov process under . Denote the corresponding expectation as . Then,

As a result, we obtain

| (33) | ||||

After careful calculation, one can conclude from Proposition 1-(ii) that (33) holds for the case as well, with replaced by . Therefore, in the following, we will use (33) regardless of the value of , and stands for when . Using (33) and the homogeneity of , we obtain

| (34) |

We first consider the case in which . In this case, denoting , we conclude that is a fixed point of in if and only if is a fixed point of in , where is an operator on defined as

| (35) | ||||

with .

It is easy to see that is an increasing mapping from into . Consider function for some . It is straightforward to see that . Consequently, for any . As a result, for any and , we have

When , is a convex power function, so we conclude from the above inequality that

which implies

Recall that is an irreducible Markov chain under measure , so it has a unique stationary distribution. Taking expectation on both sides of the inequality under this stationary distribution, and noting that the marginal distributions of and are the same, we conclude

| (36) |

Because , is a contraction mapping on with norm . Consequently, for any , the limit of exists and is the unique fixed point of in . Moreover, because , the fixed point must lie in . As a result, has a unique fixed point in .

When , we consider the following operator:

| (37) | ||||

Because is either a concave power function or a logarithmic function when , we have for any nonnegative random variable . As a result, for any , and in particular for . One can see that both and are increasing sequences, and that the former is dominated by the latter. On the other hand, following the same proof as in the case in which , we can show that is a contraction mapping from into . As a result, converges, and so does . Consequently, the limit of is a fixed point of and lies in , and thus the fixed point of in exists. We then show the uniqueness of the fixed point of in when . For the sake of contradiction, suppose there are two distinct fixed points and in . Without loss of generality, we assume for some . Define and denote the corresponding minimum value as . Because is finite and ’s are positive, is well defined and . Define . Then, and . Denote as the identity mapping. Then, for each , we have

where the inequality is the case because and and the last equality is the case because is a fixed point of . In particular, we have . On the other hand, because is increasing and , we have , where the equality is the case because is a fixed point of . Speficially, . Thus, we have a contradiction, so the fixed point of must be unique.

Next, we consider the case in which . In this case,

Because is finite, there exists such that

| (38) |

It is straightforward to verify that for such , . Because is increasing, is an increasing sequence. On the other hand, because and is finite, there exists such that . Consequently, , so the limit of exists and is a fixed point of in . Using the same proof as the one in the case in which and , we can show that the fixed point of in is unique.

Part Two: computation of the fixed point.

In the second part of the proof, we show that converges to the fixed point of for any . Denote the fixed point as .

Because , , and is finite, there exists such that and . Then,

where the inequality is the case because and and the equality is the case because is the fixed point of . Consequently, is a decreasing sequence. Similarly, is an increasing sequence. Moreover, because is increasing. As a result, both and converge in , and the convergent points are fixed points of . Because the fixed point of is unique, both and converge to this fixed point, namely to . By the squeeze theorem, also converges to .

Proof.

Proof of Theorem 2. Define operator on by

It is obvious that for any . According to Assumption 3, sequence is increasing. Consequently, , and thus is also an increasing sequence and dominates . By Assumption 3, for some . As a result, for sufficiently large , and thus converges to the fixed point of in according to Theorem 1. Consequently, the limit of exists, is a fixed point of , and is strictly larger than point-wisely.

Next, we show the uniqueness of the fixed point of . We first note that for any fixed point of , we have . Because for some , must be strictly larger than point-wisely. Now, for the sake of contradiction, suppose that we have two distinct fixed points and . We already showed that , . Without loss of generality, we assume for some . Define

and denote the corresponding minimum value as . Because is finite, must exist and . Define . Then, one can verify that and . Because is well defined, so is . Recall that for some . Because is increasing and concave, so is . Denote as the identity mapping. Then, for any ,

where the first inequality is the case due to the concavity of and the equality is the case because is a fixed point of . Thus, . On the other hand, because is increasing and is a fixed point of . In particular, , which is a contradiction.

Finally, we show that for any such that is well defined, converges to the fixed point of . We first note that and that is well defined according to Assumption 3. As a result, is well defined for any . Recall that for some , so . Thus, in the following, we assume without loss of generality.

Denote as the unique fixed point of , and recall that we already showed that . Because is finite, there must exist such that , i.e., . Then,

where the equality is the case because is the fixed point, the first inequality is the case because is increasing, and the second inequality is the case because is concave. Applying on both sides of the above inequality, we conclude that for any , which implies

On the other hand, we have . Because converges to , the squeeze theorem shows that converges to as well.

Proof.

Now, suppose is a solution to (20) and consider any . Then, we have , which implies that is well defined due to Assumption 4. Moreover, by (20) we have . Consequently, is a decreasing sequence and so is . By Theorem 1, its limit is the fixed point of , i.e., . Thus, .

If there exists such that is a maximizer of (21) for each , then . From the uniqueness of the fixed point of , we conclude that . As a result, and are a maximizer and the optimal value, respectively, of (19).

Proof.

Proof of Theorem 3. We first derive some properties for . Because is compact for each , we immediately conclude that for any fixed , there exists such that and for all . Moreover, is continuous and increasing in . Consequently, in its domain, is increasing and satisfies

| (39) |

where we set for for convenience.

Define for . Then, for each , is continuous in , where is the closure of in and thus is a compact set. We then conclude from (39) and from the continuity of in that is continuous in its domain.

For any , straightforward calculation yields

One can see that is positive (respectively negative) when is sufficiently close to 0 (respectively close to 1). For each , because is close relative to , is uniquely attained by certain , and

| (40) |

where , , and . As a result, for each such that , there exists such that , i.e., the maximum in (39) is attained by .

The remaining proof of the theorem is divided into three parts.

Part One: existence of the fixed point

We prove the existence of the fixed point of in this part. We first consider the case in which there exists such that for some .

Recall as defined in Assumption 3, i.e., for each , and recall

By Assumption 4, for each , is well defined. Because , i.e., , for each , we conclude that is well defined for any , so is in the domain of . Moreover, because for any and such that is well defined, we conclude that for any . As a result, . Now, define , . Becuase is increasing, is an increasing sequence.

Because for some and some , Assumption 4 yields that for some . On the other hand,

which implies . Repeating the the above calculation, we conclude that . As a result, , showing that . Also recall that it is assumed that for some .

Now, we show that is bounded from above and thus its limit exists. The above shows that without loss of generality, we can assume and for all . Then, for each , there exists such that

which implies . Because , according to Theorems 1 and 2, converges to , the fixed point of , as goes to infinity. Consequently, , i.e., . Thus, we only need to show that is bounded. When , we have , where the first inequality is the case because and the second one is the case because . Thus, in the following, we only need to consider the case in which .

Recall , , , and in Proposition 1, and denote them as , , , and , respectively, when is replaced by . Define

and . Then, straightforward calculation yields that for , and are, respectively, the Perron-Frobenius eigenvalue and eigenvector of the operator . For , with , we have

In the following, when , we always identify , Perron-Frobenius eigenvector of , to the one that has unitary norm. When , by the proof of Proposition 1, is the solution to , where , is the identify matrix, and is the transition matrix of . We identify to be the one that is orthogonal to the kernel of , which must be uniquely determined. Moreover, is linear in , so there exists a constant such that for all , where stands for the Euclidean norm.

Now, we prove the boundedness of for the case in which and . Recalling that is the fixed point of , we conclude from (34) that

where stands for the norms of functions on . Consequently, recalling the relation , we have

where . With , we have for any , so

As a result,

| (41) |

We first recall that . In addition, because and is compact for any . Thus, by (41), to prove that is bounded, we only need to show that is uniformly bounded from above by a constant and from below by another positive constant. Because is the Perron-Frobenius eigenvector of with unitary norm, its entries must be bounded by 1. Thus, we only need to prove that is uniformly bounded from below by a positive constant. Equivalently, denoting as the ratio of the maximum entry of divided by the minimum entry of , we only need to prove that is bounded.

Recall that for all and that is of finite elements, so there exists such that , for all and all . Recall the definition of . Then, the bound in (40) yields that there exists such that , for all and all . Recall and , and denote the matrix representing as . Then, we have

where . Because is irreducible, there exists such that is positive. Consequently, because and , we conclude that is positive. Note that and are, respectively, the Perron-Frobenius eigenvalue and eigenvector of , so171717For a positive matrix , denote its Perron-Frobenius eigenvalue and eigenvector as and , respectively, and denote the maximum and lowest entries of as and , respectively. Then, the Collatz-Wielandt formula shows that the eigenvalue . On the other hand, from the identity , we conclude that . Thus, we conclude .

Because and thus for all and all and because is compact for each , it is straightforward to see that and . Consequently, we have , and thus

Next, we consider the case in which and . Following the same calculation as above, we conclude that

and we only need to show that is uniformly bounded. Recalling that for some and all , that is a probability distribution on and thus the sum of its entries is equal to 1, that is compact for all , and that for some and all and , we immediately conclude that is uniformly bounded.

Next, we consider the case in which . The same calculation as above shows that

is uniformly bounded from above by a positive constant , and is uniformly bounded from below by a positive constant and bounded from above by a positive constant . When , recall that is the Perron-Frobenius eigenvalue , and that we already proved that for some positive constants and . Consequently,

Therefore, there exists such that . When , , where , where the expectation is taken under the stationary probability of . Recalling (16), we immediately conclude that

Because there exists such that for all and because is compact for all , we immediately conclude that and thus that for certain constant . Then, for any , we have

Recalling that , we immediately conclude that , and thus are uniformly bounded in .

We have proved that the limit of exists and must be in . Then, by the continuity of , the limit must be a fixed point of in .

Next, we consider the case in which for any . In this case, for any , is well defined. Moreover, we have , so is an increasing sequence. On the one hand, the sequence is in because . On the other hand, following the same proof as in the previous case, we can show that this sequence is bounded from above. As a result, this sequence converges and the convergent point is a fixed point of in .

Part Two: uniqueness of the fixed point

Consider any fixed point of in . If for any , then we have , so there exists such that solves the maximization problem in (21) for each . If for some and some , we have where is as defined in (23). Consequently, there exists such that

Therefore, there also exists such that solves the maximization problem in (21) for each . Now, Proposition 2 yields that must be the optimal value of (19), and thus the fixed point of in is unique.

Part Three: computing the fixed point

Denote the unique fixed point of as . We first consider the case in which for any . Note that for any , because is finite, there exists such that . Because for all and ,

Therefore, is a decreasing sequence. Similarly, is an increasing sequence. Moreover, because is increasing. As a result, both and converge in and the convergent points are fixed points of in . Because the fixed point of in is unique, both and converge to this fixed point, i.e., to . By the squeeze theorem, converges to as well.

Next, we consider the case in which for some and some . In this case, for any in the domain of , we have

As a result, , . On the other hand, consider the following operator:

where is defined by replacing in with . We already showed that has a unique fixed point in , and we denote this fixed point as . Because is finite, there exists such that . Then,

where the first inequality is the case because is increasing, the second inequality is the case because dominates , the third inequality is the case because and for all , and the equality is the case because is the fixed point of . As a result, is a decreasing sequence and dominates , and thus it dominates as well. We already showed that converges to , so must converge in , and the convergent point is a fixed point of in . Because the fixed point of in is unique, we conclude that converges to as well. By the squeeze theorem, we conclude that converges to .

Proof.

Proof of Proposition 3 Suppose . In the proof of Theorem 3, we already showed that for sufficiently large . Then, we must have because

and because in the case .

In the following, we assume , denote , and, for the sake of contradiction, we assume that for any there exists such that for some . Because is of finite elements, there exists such that is true for infinitely many and thus true for any due to the monotonicity of in . Denote the set of such as . For any , we have

for any . Now, consider such that is reachable from certain , i.e., . We claim that is a constant in . For the sake of contradiction, suppose for certain . Then, because is reachable from and because , we conclude from the definition of in (22) that and, consequently, , which is a contradiction. Denote by the union of the set of such as above and , and the above analysis shows that is a constant in for any . The same argument as above then shows that for any that is reachable from certain , is also constant in . Because is irreducible, we can eventually show that is constant in for any . This implies that

| (42) |

We further claim that

| (43) |

For the sake of contradiction, suppose there exists such that . Then, because is positive, we have

| (44) |

Combining (42) and (44) and noting that because the latter value is nonnegative, we arrive at a contradiction.

Now, if for certain , then (43) cannot hold, so we must have for sufficiently large . On the other hand, suppose there exists such that for any . Then, because is closed relative to , there exists such that . Consequently, (43) implies that for a given feasible ,

By the definition of , we have for any , so we have for any . Because of (43), we conclude for any , so Assumption 4 implies that for certain . Consequently, we have

which is a contradiction.

Proof.

Proof of Proposition 4 For each fixed , Proposition 1-(iii) and (16) yields that

| (45) |

By considering , we immediately conclude that

| (46) |

On the other hand, for any , there exists such that . Consequently,

where the second inequality is the case because for any . Consequently, we conclude

| (47) |

The conclusion of the proposition then follows from (46) and (47).

Proof.

Proof of Proposition 5 For fixed , the monotonicity of in yields that if and only if

Straightforward calculation shows that the above is equivalent to

Because is concave in for any , one can see that, for the above to hold for any , it is sufficient to have (26).

Proof.

Proof of Proposition 6. Following the proof of Theorem 1, we can show that is a fixed point of in if and only if is a fixed point of in . In addition, when , inequality (36) holds for any . As a result, because , this inequality implies that for any . Moreover, because , is a contraction mapping on and thus admits a unique fixed point. In particular, is an increasing sequence converging to the fixed point. Because , we conclude that the fixed point must be positive.

When , define