A Robust Approach to ARMA Factor Modeling

Abstract

This paper deals with the dynamic factor analysis problem for an ARMA process. To robustly estimate the number of factors, we construct a confidence region centered in a finite sample estimate of the underlying model which contains the true model with a prescribed probability. In this confidence region, the problem, formulated as a rank minimization of a suitable spectral density, is efficiently approximated via a trace norm convex relaxation. The latter is addressed by resorting to the Lagrange duality theory, which allows to prove the existence of solutions. Finally, a numerical algorithm to solve the dual problem is presented. The effectiveness of the proposed estimator is assessed through simulation studies both with synthetic and real data.

Index Terms:

Convex optimization, duality theory, dynamic factor analysis, nuclear norm.I Introduction

We deal with the problem of constructing a dynamical model from a high dimensional stream of data that are assumed to be noisy observations of a process depending on a small number of hidden variables. In the static case, this problem is known as factor analysis. Its origins can be traced back to the beginning of the last century and the amount of literature produced on this topic is impressive: we refer the readers to the recent papers [1, 2, 3, 4] for an overview of the literature and a rich list of references. The solution of factor analysis problems may be obtained by decomposing the covariance matrix of the observed data as the sum of a diagonal positive definite matrix (accounting for the noise covariance) and a positive semidefinite matrix whose rank must be as small as possible since it equals the number of hidden variables in the model. The main problem of this solution is that it is inherently fragile; in fact, even a minuscule variation in the covariance matrix of the observed data usually leads to a substantial variation of the number of hidden variables which is the key feature of the modelling procedure. On the other hand such a matrix must be estimated and is therefore subject to errors. To address this fragility issue, a robust method has been recently proposed, [5], that has been generalized with good results also to the dynamic framework of learning latent variable dynamic graphical models, [6].

Dynamic Factor Analysis (DFA) has been addressed much more recently, the first contribution in this field being apparently [7]. We refer to the surveys [8, 9] and to the recent paper [10] for an overview of the literature on this subject. In [11] an interesting generalization is applied to modelization of dynamical systems.

In this paper, we address the dynamic autoregressive moving average (ARMA) case with the aim of extracting, from the observed data, a model featuring a small number of hidden variables. This is important both from the point of view of the model simplicity and to uncover the structure of the mechanism generating the data. The problem may be mathematically formulated as that of decomposing the spectral density of the process generating the data as the sum of a diagonal spectral density and a low-rank one. The fragility issue in this case is even more severe. We address the problem as follows:

-

•

Given the observed data, we compute by standard methods (e.g. truncated periodogram) a raw estimate of the spectral density generating the data.

-

•

We compute a neighbourhood of that contains with prescribed probability; clearly the size of depends on the sample size.

-

•

We compute a refined estimate by imposing that it admits an additive decomposition as a diagonal spectral density and a spectral density with the lowest possible rank. To this end we set up an optimization problem that we address by resorting to duality. In particular, we prove existence of solutions and provide a numerical algorithm to compute a solution.

Our work may be cast in the rich stream of literature devoted to learning dynamic models having a topological structure describing the presence or the absence of interactions among the variables of the systems; see the former works [12, 13, 14] as well as their extensions to reciprocal processes [15, 16], sparse plus low rank graphical models [17, 18, 6], the Bayesian viewpoint proposed in [19, 20] and the case of oriented graphical models [21, 22].

The contribution of this paper is twofold; first, we propose a procedure to estimate the number of latent factors in dynamic ARMA factor models: this is the most delicate aspect of factor analysis problems; second, we derive an identification method to estimate the parameters of a factor model describing the observed data.

The outline of the paper is as follows. In Section II we introduce the DFA problem for moving average (MA) models. Section III shows that such a problem admits solution by means of duality theory, while Section IV shows how to reconstruct the solution of the primal problem from the dual one. In Section V we propose an algorithm to compute the solution of the dual problem. In Section VI we extend the previous ideas to ARMA models. Section VII presents some numerical results. Finally, in Section VIII we draw the conclusions.

I-A Notation

Given a matrix , we denote its transpose by and by the element of in the -th row and -th column. If is a square matrix, , and denote its trace, its determinant and its spectrum, respectively. The symbol stands for the Frobenius norm. For , we define their inner product as . Let be the space of real symmetric matrices of size ; if is positive definite or positive semidefinite, then we write or , respectively. We denote by the complex conjugate transpose. for denotes a function defined on the unit circle , and the dependence on is dropped if necessary. If is positive (semi-)definite we write ( ). Integrals are always defined from to with respect to the normalized Lebesgue measure .

II Identification of MA factor models

Consider the MA factor model whose order is :

| (1) |

where

, diagonal; and are normalized white Gaussian noises of dimension and , respectively, such that The aforementioned model has the following interpretation: is the process which describes the factors, with , not accessible to observation; is the factor loading transfer matrix; is the latent variable; is idiosyncratic noise. Accordingly, is a -dimensional Gaussian stationary stochastic process with power spectral density

| (2) |

where and belong to the finite dimensional space:

By construction, , where denotes the normal rank (i.e. the rank almost everywhere), and is diagonal. Therefore, represents a factor model if its spectral density can be decomposed as “low rank plus diagonal” as in (2).

Assume to collect a finite length realization of defined in (1), say where the order is known. We want to estimate the corresponding factor model, that is the decomposition in (2) as well as the number of factors . To this aim, given our data , we first compute the sample covariance lags as

Then, an estimate of is obtained by the truncated periodogram:

| (3) |

Notice that could be not positive definite for all ; in that case, we can add to the right side of Equation (3), with the constant chosen in such a way as to ensure the positivity of . On the other hand, may not admit a low rank plus diagonal decomposition. Thus, we estimate directly the two terms and of the decomposition (2) by solving the following optimization problem:

| (4) | ||||

| subject to | ||||

Here, the objective function promotes a solution for having low rank, see [17]. The first three constraints impose that and provide a genuine spectral density decomposition of type (2). The last constraint, in which is the Itakura-Saito divergence defined by

imposes that belongs to a set “centered” in the nominal spectral density and with prescribed tolerance . Notice that is uniquely determined by and . Thus, Problem (4) can be rewritten by removing :

| (5) | ||||

| subject to | ||||

II-A The Choice of

Before solving our problem, we deal with the choice of the tolerance parameter appearing in the constraint of (5).

This choice should reflect the accuracy of the estimate of .

This can be accomplished by choosing a desired probability and considering a ball of radius (in the Itakura-Saito topology)

centered in and containing the true spectrum with probability . The estimation of is not an easy task because we do not know the true power spectral density . Next, we propose a resampling-based method to estimate it.

The idea is to approximate with , and use this model to perform a resampling operation. Let

be the minimum phase spectral factor of and define the process as where is an -dimensional normalized white noise. The truncated periodogram (understood as estimator) based on a sample of the process of length is

where the subscript “” stands for resampling, as it is the means by which we perform the resampling operation. By generating a realization from (i.e. by resampling the data), we can easily obtain a realization of the random variable . Accordingly, it is possible to compute numerically such that by a standard Monte Carlo procedure. Numerical simulations show that this technique indeed provides a good estimate of .

It is worth noting that if the chosen is too large with respect to the data length , the resulting may be too generous yielding to a diagonal obeying . In this case Problem (5) admits the trivial solution and . To rule out this trivial case, in (5) must be be strictly smaller than the upper bound

where denotes the family of bounded and coercive functions defined on the unit circle and taking values in the cone of positive definite Hermitian matrices. Since must be diagonal, by denoting with and by the -th element in the diagonal of and of , respectively, we have

where is the (orthogonal projection) operator mapping a square matrix into a diagonal matrix of the same size having the same main diagonal of . Therefore, since the Itakura-Saito divergence is nonnegative, the solution corresponds to , for which . Accordingly,

| (6) |

The derivation of the aforementioned result is based on reasonings similar to [6, Section IV].

A more generous upper bound can be derived by assuming that is the spectrum of an MA process of order . However, numerical experiments showed that even in the case that is relatively small.

III Problem solution

In this section we first provide a finite dimensional matrix parametrization of Problem (5). The latter is then analyzed by resorting to the Lagrange duality theory, which allows us to prove the existence of a solution.

III-A Matricial Reparametrization of the Problem

To study Problem (5) it is convenient to introduce the following matrix parametrization for and :

| (7) | ||||

where is the so-called shift operator:

| (8) |

and are matrices in and denotes the block of in position with , so that

Moreover, denotes the vector space of matrices of the form

| (9) |

The linear mapping constructs a symmetric block-Toeplitz matrix from its first block row so that if is given by (9),

The adjoint of is the mapping defined by with

Next, the objective is to provide a more convenient formulation of Problem (5) in terms of and . To this end, we have to take into account the following points.

1) Positivity Constraints and It can been shown (see, for example, [17, Appendix A]) that, for any , if and only if there exists a matrix such that and . Therefore, we replace the conditions with , the condition with . Note that these conditions only guarantees and thus to be positive semidefinite, however we will show that this is sufficient to guarantee that at the optimum.

2) Constraint diagonal: Let denote the linear operator such that, given , is the matrix in which each off-diagonal element is equal to the corresponding element of and each diagonal element is zero. We define the “block ofd” linear operator as follows. Given , then

It is not difficult that is a self-adjoint operator, since is self-adjoint as well. Then, it is easy to see that the condition diagonal is equivalent to the condition diagonal for , that is .

3) The Low Rank Regularizer: We have

where we exploited the fact that if , and otherwise.

4) The Divergence Constraint: A convenient matrix parameterization of the Itakura-Saito divergence can be obtained by making use of the following facts.

First, since with , there exists such that . Then, by using the Jensen-Kolmogorov formula we obtain

| (10) |

which holds provided that and is coercive (i.e. is bounded away from zero on the unit circle). We need to generalize this result to spectral densities that may be singular on the unit circle. This is possible because the zeros of a rational spectral density, if any, have finite multiplicity so that the logarithm of the determinant of a rational spectral is integrable as long as the normal rank of is full.

Lemma III.1

Consider a power spectral density having full normal rank. Let be such that , , and . Then

The proof is deferred to the appendix.

A second observation in order to conveniently parameterize the Itakura-Saito divergence constraint is that, by exploiting the cyclic property of the trace,

where is defined from the expansion

as

III-B The Dual Problem

We reformulate the constrained minimization problem in (11) as an unconstrained problem by means of Duality Theory.

If we use as the multipliers associated with the constraints on the positive semi-definiteness of and , respectively;

as the multiplier associated with the constraint and

, as the multiplier associated with the Itakura-Saito divergence,

then the Lagrangian of Problem (11) is

| (12) | ||||

Note that we have not included the constraint because, as we will show later on, this condition is automatically met by the solution of the dual problem.

The dual function is defined as the infimum of over and . Thanks to the convexity of the Lagrangian, we rely on standard variational methods to characterize the minimum.

-

•

Partial minimization with respect to : depends on only through which is bounded below only if

(13) Thus, we get that

-

•

Partial minimization with respect to : The terms in are bounded below only if

(14) and are minimized if and

(15) The Lagrangian is linear in the remaining variables , for , and therefore bounded below only if

(16) Therefore, the minimization of the Lagrangian with respect to and is finite if and only if (13), (14), and (16) hold in which case

Otherwise the Lagrangian has no minimum and its infimum is .

To simplify the notation, let us define the vector space as:

since always appears in the form , we can replace it with . Then, we can formulate the dual problem for the Lagrangian (12) as

| (17) |

where

and the feasible set is given by:

Note that the constraints and are equivalent to the constraint . Thus, we can eliminate the redundant variable ; moreover, by changing the sign to the objective function and observing that , we can rewrite (17) as a minimization problem:

| (18) |

where

and the corresponding feasible set is:

III-C Existence of solutions

The aim of this section is to show that (18) admits solution. The set is not compact, as it is neither closed nor bounded. We show that we can restrict the search of the minimum of over a compact set. Then, since the objective function is continuous over (and hence over the restricted compact set), we can use Weierstrass’s Theorem to conclude that the problem does admit a minimum.

The first step consists in showing that we can restrict to a subset where with a positive constant.

Proposition III.1

Let be a sequence of elements in such that

Then, such a sequence cannot be an infimizing sequence.

The proof is essentially the same as the proof of Proposition 6.1 in [6] and it is therefore omitted.

As a consequence, minimizing the dual functional over the set is equivalent to minimize it over the set:

Next we show that we can restrict to a subset in which both and cannot diverge.

Proposition III.2

Let be a sequence of elements in such that either

or

or both. Then, such a sequence cannot be an infimizing sequence.

The above result is obtained by following arguments similar to the proof of Proposition 6.2 in [6] with a few small differences; we refer the interested reader to [23, Appendix C] for the detailed proof.

It follows from the previous proposition that there exists with such that

and such that . Therefore, the set can be further restricted to the set:

In addition, it is not possible for and to diverge while keeping the difference finite. Accordingly, we can further restrict the search for the optimal solution to a subset in which neither nor can diverge:

Proposition III.3

Let be a sequence of elements in such that

| (19) |

or

| (20) |

or both. Then, such a sequence cannot be an infimizing sequence.

The proof can be found in the appendix.

Thus, the minimization over is equivalent to the minimization over the subset:

for a certain positive constant.

Finally, we consider a sequence such that tends to be singular as . This implies that tends to zero and hence . Thus, such a sequence cannot be an infimizing sequence. Therefore, the final set is:

where and such that and

Theorem III.1

Proof:

Equivalence of the two problems has already been proven by the previous arguments. Since is closed and bounded, hence compact, and is continuous over , by the Weierstrass’s Theorem the minimum exists. ∎

IV Solution of the primal problem

In this section, after proving that the primal problem (5) and its matrix reformulation (11) are equivalent, we show how to recover the solution of the primal problem.

Let be a solution of (18) and be the corresponding solution of (11). Since is positive definite, is finite. By Lemma III.1, at the optimum must be finite as well; this implies that , may be singular at most on a set of zero measure, or, in other terms, . This observation leads to the following proposition:

Now we are ready to show how to recover the solution of the primal problem; to this aim we need the following result, see [24].

Lemma IV.1

Let and . If is such that

| (23) |

then .

Exploiting the constraints and , it is not difficult to see that

| (26) |

where

| (27) |

Since and in view of Lemma IV.1, . Hence, has rank at least equal to .

Since the duality gap between (11) and (18) is equal to zero, we have that , which in turn implies

| (28) |

because . Recalling that in view of (28) the matrix has rank at most equal to . Let . Then, there exists a full-row rank matrix such that

| (29) |

By (28), it follows that Let denote the matrix whose columns form a basis of . Note that the dimension of the null space of is at least because and ; also because . Rewriting the matrix as with , from (29) we obtain

| (30) |

with unknown.

In a similar fashion, by the zero duality gap between (11) and (18), the complementary slackness condition for the multiplier associated to the positive semi-definiteness of reads as which in turn implies Repeating the same reasoning as before, it can be seen that, if the dimension of the null space of is with and is a matrix whose columns form a basis of , then can be written as

| (31) |

with unknown. Plugging (31) into (30), we then obtain

| (32) |

Assume now that each block of is diagonal, namely

| (33) |

Remark 1

We can make the previous assumption without loss of generality. Indeed, let , be the solution of Problem (5) and ; , and are any matrices in such that , and . We can always consider a different matrix parametrization for , and as follows. First notice that there always exists a matrix with all diagonal blocks such that ; in other words, we can always find such that and satisfies for Now, let such that and satisfies (15). Define with . It is easy to see that and . This means that is still a solution of Problem (11) and it allows us to restrict to solutions of (11) for which (33) holds.

By applying the operator to both sides of (32) and exploiting the assumption (33), it is not difficult to obtain:

| (34) |

which is a system of linear equations in the unknowns . Notice that is given by (15). Finally, once is computed, in order to retrieve we exploit (33) and the following system of linear equations:

| (35) |

Since both the dual and the primal problem admit solution, the resulting systems of equations (33), (34) and (35) do admit solutions.

V The proposed algorithm

In this section we propose an algorithm to solve numerically the dual problem. To start with, as observed in Section IV, we rewrite (18) in a different fashion by getting rid of the slack variable . This is done by introducing a new variable defined, similarly to (27), as

| (36) |

such that, as in (26), the variable can be expressed as

| (39) |

Accordingly, the dual problem (18) can be expressed in terms of the variables , and as follows:

| (40) |

where

and the corresponding feasible set is:

We can further simplify our problem as follows. First, we observe that the constraint

| (41) |

implies

and then, by Lemma IV.1, . Now, we can easily rewrite (41) recalling the characterization of a symmetric positive semidefinite matrix using the Schur complement. To this aim, it is convenient to introduce the linear operators and that, for a given matrix construct a symmetric block-Toeplitz matrix and extract the blocks in position , and , respectively. With this notation, we have

and the constraint (41) is equivalent to require and with

In a similar fashion, the last matricial inequality constraint in can be equivalently expressed as where

Therefore, Problem (18) can be formulated as

| (42) |

where

Solving Problem (42) simultaneously for , and is not trivial because the inequality constraints and both depend on . On the other hand, once we fix the dual variable to a positive constant , the problem:

| (43) |

with

can be efficiently solved by resorting to the ADMM algorithm [25]. To this aim, we rewrite Problem (43) by introducing a new variable defined as

| (44) | ||||

| subject to |

where

and denotes the cone of symmetric positive semidefinite matrices of size . The augmented Lagrangian for (44) is:

where is the Lagrange multiplier, and is the penalty parameter. Accordingly, given the initial guesses and , the ADMM updates are:

| (45) | ||||

| (46) | ||||

Problem (45) does not admit a closed form solution, therefore we approximate the optimal solution by a gradient projection step:

where:

-

•

denotes the gradient of the augmented Lagrangian with respect to :

-

•

denotes the gradient of the augmented Lagrangian with respect to :

where the omitted argument of the operators and is intended to be equal to

-

•

denotes the projection operator onto :

-

•

denotes the projection operator onto the convex cone It is not difficult to see that

where is the projection operator onto the cone .

-

•

the step-size is determined at each step in an iterative fashion: we start by setting and we decrease it progressively of a factor with until the conditions and are met and the Armijo’s condition [26] is satisfied.

Problem (46) admits a closed form solution, which can be easily computed as:

To define the stopping criterion, we need to introduce the following quantities

which are referred to as the primal and dual residual, respectively. Notice that the omitted argument of the operators and is intended to be equal to .

Then, the algorithm stops when the following conditions are met:

where and are the desired absolute and relative tolerances.

It remains to determine the optimal value for which solves Problem (42). To this aim, we exploit the following result (see [26, pp.87-88]):

Proposition V.1

If is convex in and is a convex non-empty set, then the function

| (47) |

is convex in , provided that for some . The domain of is the projection of on its -coordinates.

This result guarantees that the function

is convex in . Hence, in order to determine we can choose an initial interval of uncertainty containing , and we progressively reduce it by evaluating at two points within the interval placed symmetrically, each at distance from the midpoint. This is repeated until the width of the uncertainty interval is smaller than a certain tolerance .

Input: , ,

Output:

VI Identification of ARMA factor models

In this section we extend the proposed approach to ARMA processes. Consider the ARMA factor model:

| (48) |

where

and , and are defined analogously to (1). Notice that is a MA process of order whose spectral density admits a low rank plus diagonal decomposition. Finally, it is worth noting that it is not restrictive to assume that the autoregressive part in (48) is characterized by a scalar filter ; Indeed, any ARMA factor model can be written in the form of (48).

Assume now to collect a realization of numerosity of the process . Our aim is to estimate the factor model (48) and the number of factors . Before proceeding, the following observation needs to be made: there is an identifiability issue in the problem. Indeed, if we multiply , and by an arbitrary non-zero real number , the model remains the same. We can easily eliminate this uninteresting degree of freedom by normalizing the polynomial , so that from now on we assume .

The idea is to estimate first , and then and by preprocessing through . In more detail, the proposed solution consists of the following two steps:

-

1.

The AR dynamic estimation. Given the realization , we estimate the parameters of the filter by applying the maximum likelihood estimator proposed in [27, Section II.b]. In doing so, we are estimating an AR process whose spectral density is .

-

2.

The MA dynamic factor analysis. Let be the finite length trajectory obtained by passing through the filter the trajectory with zero initial conditions. After computing the truncated periodogram from , we solve Problem (5) with in order to recover the number of latent factors.

Although the above procedure is suboptimal, the numerical simulations showed that the resulting estimator of the number of factors performs well, see Section VII-B.

VII Numerical simulations

In this section, we test the performance of the proposed approach both for MA and ARMA factor models. In all the simulations, the parameter is computed according to the empirical procedure of Section II-A for . Then, Problem (42) is solved by applying Algorithm 1 with and In regard to the ADMM algorithm, we set , and the penalty term

VII-A Synthetic Example - MA factor models

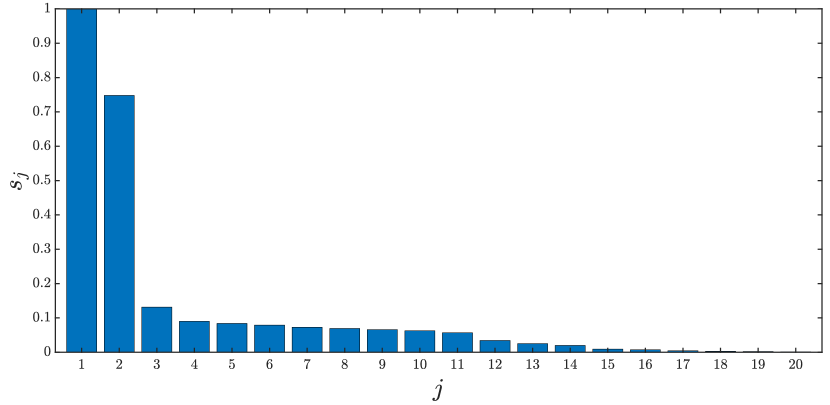

We consider an MA factor model (1) of order , with manifest variable and latent factors, computed by randomly generating the zeros of the transfer functions ’s and ’s for within the circle with center at the origin and radius on the complex plane. It is worth noting that and , that is the idiosyncratic component is not negligible with respect to the latent variable. We generate from the model a sample of length and we apply the proposed identification procedure to estimate the number of common factors. We define

where denotes the largest eigenvalue of at frequency . It is clear that represents the integral of the largest normalized singular value of over the unit circle. The quantities are plotted in Figure 1; we can notice that there is a knee point at , so that the numerical rank of is equal to and, in doing so, we can recover the exact number of common factors.

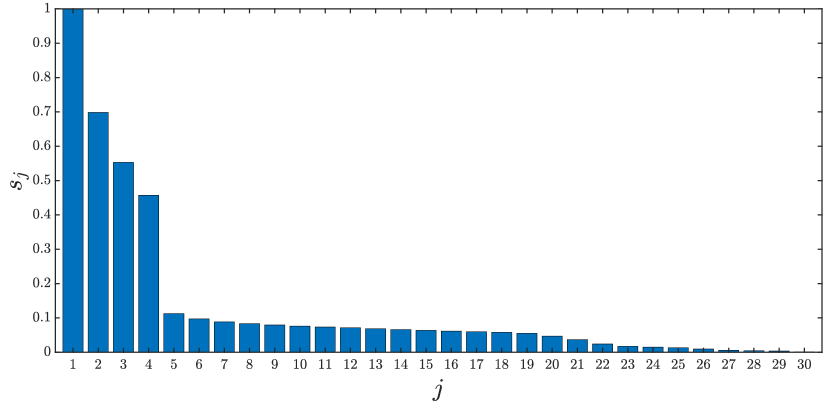

The effectiveness of the proposed estimator is also tested by considering a data sample of numerosity generated by a MA factor model with , and common factors; the integrals of the Frobenius norm of and are and respectively. As showed in Figure 2, even in this case we are able to estimate the correct number of latent variables.

Finally, we obtained similar results with different samples and by changing the “true” factor model from which we generated the data.

VII-B Synthetic Example - ARMA factor models

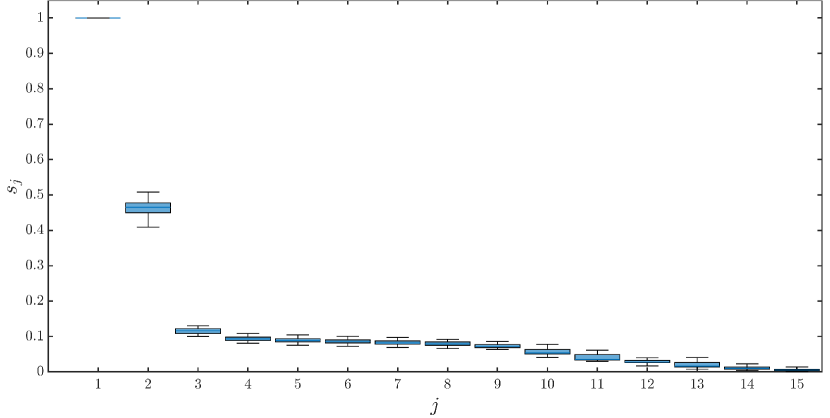

To provide empirical evidence of the estimation performance of the algorithm of Section VI, a Monte Carlo simulation study composed of 50 experiments is performed. We randomly build an ARMA factor model (48) with , , and ; without loss of generality we fix . Then, for each Monte Carlo experiment a data sequence of length is randomly generated from the model and the ARMA factor model identification procedure is performed. The boxplot of the quantities for the estimated ’s are shown in Figure 3 and it reveals that the proposed identification procedure is able to successfully recover the number of latent factors.

VII-C Smart Building Dataset

The SMLsystem is a house built in Valencia at the Universidad CEU Cardenal Herrera (CEU-UCH). It is a modular house that integrates a whole range of different technologies to improve energy efficiency, with the objective to construct a near zero-energy house. A complex monitoring system has been used in the SMLsystem: it has indoor sensors for temperature, humidity and carbon dioxide; outdoor sensors are also available for lighting measurements, wind speed, rain, sun irradiance and temperature. We refer the reader to [28] for a detailed description of the building and its monitoring system. Two datasets from the SMLsystem are available for download at the UCI Machine Learning repository http://archive.ics.uci.edu/ml. We take into account sensor signals extracted from these datasets: the indoor temperature (in ) of the dinning-room and of the room, the weather forecast temperature (in ), the carbon dioxide (in ppm) in the dinning room and in the room, the relative humidity (in %) in the dinning room and the room, the lighting in the dinning room and the room (in lx), the sun dusk, the wind (in cm/sec), the sun light (in klx) in the west, east and south facade, the sun irradiance (in dW), the outdoor temperature (in ) and finally the outdoor relative humidity (in %). The data are sampled with a period of and each sample is the mean of the last quarter, reducing in this way the signal noise. The first dataset was captured during March 2011 and has points ( days), while the second dataset has points ( days) collected in June 2011.

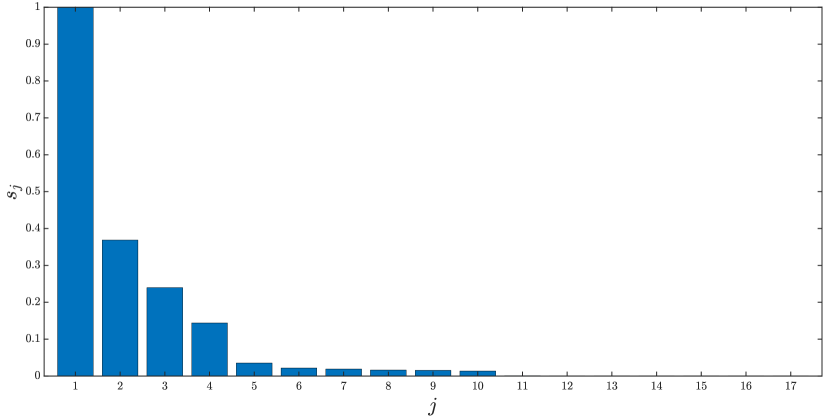

It is reasonable to expect that the variability of the considered signals may be successfully explained by a smaller number of factors. Motivated by this reason, we apply the ARMA factor model identification procedure with parameters and using the realization . As shown in Figure 4, we obtain an estimate of latent factors.

For the sake of comparison, we also use the Matlab function armax() of the System Identification Toolbox to compute the prediction-error method (PEM) estimate for an ARMA model with polynomials and of order 2 and diagonal from the realization .

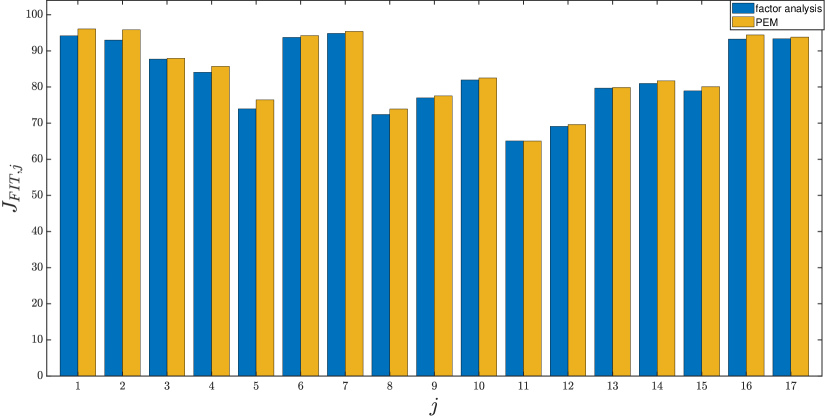

Finally, the second dataset is used in the validation step to test the prediction capability of the two estimated ARMA models. The results are summarized in Figure 5 which displays for each output channel the fit (percentage) term:

where and is the one-step ahead prediction at time computed with zero initial conditions. The figure shows that the ARMA factor model matches quite well the measurement data , reaching fit values similar to the PEM estimate. This is a remarkable result as the performances of the two approaches are essentially the same, but the factor model is parameterized by 257 coefficients, much less than the 869 coefficients of the PEM estimate.

VIII Conclusion

A procedure to estimate the number of factors and to learn ARMA factor models has been proposed. This method is based on the solution of an optimization problem whose solution has been proven to exist via dual analysis. The simulations results applying the procedure both to synthetic and real data provide evidence of a good performance.

Proof of Lemma III.1

Since with , there exists such that . The matrix is such that admits the spectral factorization where . Now, define with and let be a spectral factor of with Clearly, ; accordingly, and . Since we can exploit (10) to obtain

Then, applying the limit operator to both sides, we have

To conclude the proof, it remains to show that in the left side of the previous equation it is possible to interchange the limit and the integral operators. To this aim, we introduce the sequence where and the function . Observe that, since the interval of integration is bounded and for any , then We also define the sequence as and is a pointwise non-increasing sequence of measurable non-positive functions,

converging to from above. Hence, it satisfies all the hypotheses of Beppo-Levi’s monotone convergence theorem (applied with opposite signs), from which it immediately follows that

and consequently

| (49) |

Now, since for all ,

| (50) |

and, by plugging (50) into (49), we finally obtain

Proof of Proposition III.3

Consider a sequence in .

We first show that cannot diverge. Indeed, assume by contradiction that . Since it is a symmetric and traceless matrix, this implies

| (51) |

In view of (51), since is bounded and positive semidefinite , then has at least a negative eigenvalue for sufficiently large, so that the sequence is not in . We conclude that

As a consequence, since (which is one of the condition for the sequence to be in ), and by construction, it holds that

Then, from it follows that also the off-diagonal blocks of must be bounded , i.e.

| (52) |

Finally, by the boundedness of and by (52) we obtain that

| (53) |

which concludes the proof.

References

- [1] L. Ning, T. T. Georgiou, A. Tannenbaum, and S. P. Boyd, “Linear models based on noisy data and the Frisch scheme,” SIAM Review, vol. 57, no. 2, pp. 167–197, 2015.

- [2] D. Bertsimas, M. S. Copenhaver, and R. Mazumder, “Certifiably optimal low rank factor analysis,” Journal of Machine Learning Research, vol. 18, no. 29, pp. 1–53, 2017.

- [3] V. Ciccone, A. Ferrante, and M. Zorzi, “Learning latent variable dynamic graphical models by confidence sets selection,” Kybernetika, vol. 55, no. 4, pp. 74–754, 2019.

- [4] M. Zorzi and R. Sepulchre, “Factor analysis of moving average processes,” in European Control Conference (ECC), Linz, 2015, pp. 3579–3584.

- [5] V. Ciccone, A. Ferrante, and M. Zorzi, “Factor models with real data: A robust estimation of the number of factors,” IEEE Transactions on Automatic Control, vol. 64, no. 6, pp. 2412–2425, June 2019.

- [6] ——, “Learning latent variable dynamic graphical models by confidence sets selection,” IEEE Transactions on Automatic Control, vol. 65, no. 12, pp. 5130–5143, 2020.

- [7] J. Geweke, “The dynamic factor analysis of economic time series,” in Latent variables in socio-economic models, D. Aigner and A. Goldberger, Eds. Amsterdam: North-Holland, 1977.

- [8] M. Deistler and C. Zinner, “Modelling high-dimensional time series by generalized linear dynamic factor models: An introductory survey,” Communications in Information & Systems, vol. 7, no. 2, pp. 153–166, 2007.

- [9] J. Stock and M. Watson, “Dynamic factor models,” 2010, internal report. [Online]. Available: https://www.princeton.edu/~mwatson/papers/dfm_oup_4.pdf

- [10] G. Figá-Talamanca, S. Focardi, and M. Patacca, “Common dynamic factors for cryptocurrencies and multiple pair-trading statistical arbitrages,” Decisions in Economics and Finance, 2021.

- [11] G. Bottegal and G. Picci, “Modeling complex systems by generalized factor analysis,” IEEE Transactions on Automatic Control, vol. 60, no. 3, pp. 759–774, 2015.

- [12] J. Songsiri and L. Vandenberghe, “Topology selection in graphical models of autoregressive processes,” Journal of Machine Learning Research, vol. 11, no. Oct, pp. 2671–2705, 2010.

- [13] E. Avventi, A. Lindquist, and B. Wahlberg, “ARMA identification of graphical models,” IEEE Trans. Autom. Control, vol. 58, no. 5, pp. 1167–1178, May 2013.

- [14] S. Maanan, B. Dumitrescu, and C. Giurcăneanu, “Conditional independence graphs for multivariate autoregressive models by convex optimization: Efficient algorithms,” Signal Processing, vol. 133, pp. 122–134, 2017.

- [15] D. Alpago, M. Zorzi, and A. Ferrante, “Identification of sparse reciprocal graphical models,” IEEE Control Systems Letters, vol. 2, no. 4, pp. 659–664, Oct 2018.

- [16] ——, “A scalable strategy for the identification of latent-variable graphical models,” Submitted, 2018.

- [17] M. Zorzi and R. Sepulchre, “AR identification of latent-variable graphical models,” IEEE Transactions on Automatic Control, vol. 61, no. 9, pp. 2327–2340, Sept 2016.

- [18] S. Maanan, B. Dumitrescu, and C. Giurcăneanu, “Maximum entropy expectation-maximization algorithm for fitting latent-variable graphical models to multivariate time series,” Entropy, vol. 20, p. 76, 01 2018.

- [19] M. Zorzi, “Empirical Bayesian learning in AR graphical models,” Automatica, vol. 109, 2019.

- [20] M. Zorzi, “Autoregressive identification of Kronecker graphical models,” Automatica, vol. 119, p. 109053, 2020.

- [21] M. S. Veedu, H. Doddi, and M. V. Salapaka, “Topology learning of linear dynamical systems with latent nodes using matrix decomposition,” 2020.

- [22] M. S. Veedu and M. V. Salapaka, “Topology identification under spatially correlated noise,” 2020.

- [23] L. Falconi, “Robust factor analysis of moving average processes,” 2021, master thesis. [Online]. Available: http://tesi.cab.unipd.it/65215/

- [24] J. Songsiri, J. Dahl, and L. Vandenberghe, “Graphical models of autoregressive processes,” Convex optimization in signal processing and communications, pp. 89–116, 2010.

- [25] S. Boyd, N. Parikh, E. Chu, B. Peleato, and J. Eckstein, “Distributed optimization and statistical learning via the alternating direction method of multipliers,” Found. Trends Mach. Learn., vol. 3, no. 1, pp. 1–122, Jan. 2011. [Online]. Available: http://dx.doi.org/10.1561/2200000016

- [26] S. Boyd and L. Vandenberghe, Convex optimization. Cambridge, United Kingdom: Cambridge University Press, 2004.

- [27] F. Crescente, L. Falconi, F. Rozzi, A. Ferrante, and M. Zorzi, “Learning ar factor models,” in 2020 59th IEEE Conference on Decision and Control (CDC), 2020, pp. 274–279.

- [28] F. Zamora-Martínez, P. Romeu, P. Botella-Rocamora, and J. Pardo, “On-line learning of indoor temperature forecasting models towards energy efficiency,” Energy and Buildings, vol. 83, pp. 162 – 172, 2014. [Online]. Available: http://www.sciencedirect.com/science/article/pii/S0378778814003569