Numerical approximation of hybrid Poisson-jump Ait-Sahalia-type interest rate model with delay

Abstract

While the original Ait-Sahalia interest rate model has been found considerable use as a model for describing time series evolution of interest rates, it may not possess adequate specifications to explain responses of interest rates to empirical phenomena such as volatility ’skews’ and ’smiles’, jump behaviour, market regulatory lapses, economic crisis, financial clashes, political instability, among others collectively. The aim of this paper is to propose a modified version of this model by incorporating additional features to collectively describe these empirical phenomena adequately. Moreover, due to lack of a closed-form solution to the proposed model, we employ several new truncated EM techniques to examine this model and justify the scheme within Monte Carlo framework to compute expected payoffs of some financial quantities such as a bond and a barrier option.

Key words: Stochastic interest rate model, Markovian switching, delay volatility, Poisson jump, truncated EM method, strong convergence, Monte Carlo scheme, financial products

1 Introduction

The shortcoming of the continuous-time model of Black-Scholes [1] in describing convex phenomena of implied volatility exhibited by most historical financial data led to the underlying assumption of constant volatility to be questioned. Several empirical studies have rather shown that stochastic volatility models with inherent features of past dependency are suitable models for describing convex phenomena of implied volatility against market anomalies (see, e.g., [2, 8, 9, 15]).

It has also been well known that asset prices admit jumps in response to lack of information or unexpected catastrophic news. This phenomenon typically generates price vibrations with larger quantiles than normal (see [29]). Apparently, this violates the efficient market hypothesis that all available information are reflected in current asset prices. There are several existing rich literature where the authors employed jump-diffusions models to describe jump behaviour of asset prices arising from lack of information or unexpected catastrophic news (see, e.g., [3, 4, 5, 7]).

Hybrid models driven by finite-state Markovian chains have also been increasingly employed as suitable models for modelling uncertainty in modern economic or financial systems (see, e.g.,[6, 14, 15, 16]). The hybrid models randomly switch between finite number of regimes in anticipation to unexpected abrupt structural changes in underlying economic or financial mechanisms.

The Ait-Sahalia interest rate model which is popularly used to describe time-series evolution of interest rates is driven by a strongly nonlinear stochastic differential equation

| (1) |

where and . For more extensive existing literature concerning with SDE (1), the readers, for instance, may consult [10], [11], [12] and [13] among others.

Despite of the wide applicability of SDE (1), this model may not possess inherent features to fully describe dynamical behaviours of interest rates in response to unexpected joint effects of extreme volatility, jumps, financial clashes, economic crisis among others. To help describe joint effects of these phenomena, we may specify SDE(1) as a hybrid Poisson-driven jump SDDE governed by

| (2) |

Here , is a Markov chain with finite space , and are functions of , depends on and , and denotes delay in . Moreover, , is a scalar Poisson process independent of a scalar Brownian motion , with compensated Poisson process given by , where is a jump intensity.

The SDDE (2) integrates three unique specifications under a unified framework. For instance, the delay in volatility function may capture the dynamical behaviours of implied volatility. On the other hand, the Poisson-driven term may explain tail distribution of interest rates in response to unexpected catastrophic news. The Markovian switching term may address effects of unpredictable market shocks which may arise from abrupt changes such as regulatory lapses, financial clashes, economic crisis, political instability or unobservable states of the underlying market frameworks or mechanisms.

The solution to SDDE (2) obviously cannot be found by closed-form formula. It is also obvious SDDE (2) has super-linear coefficient terms. As a result, we cannot employ the classical global Lipschitz-based techniques for numerical analysis of SDDE (2). To the best of our knowledge, there exists no relevant literature devoted to numerical analysis of system of SDDE (2) in the strong sense. This therefore calls for a need to investigate feasibility of SDDE (2) from viewpoint of applications.

In this work, we will focus on developing several new truncated EM techniques to numerically study SDDE (2). The rest of the paper is organised as follows: In section 2, we will examine the existence and uniqueness of the solution to SDDE (2) and show that the solution will always be positive. We will also establish moment bounds of the exact solution in this section. In section 3, we will define the truncated EM scheme for SDDE (2) and survey moment bounds of the numerical solutions. We will employ truncated EM techniques to establish finite time strong convergence theory in section 4. in section 5, we will also implement some numerical examples to validate efficiency of the proposed scheme. Finally, in the last section, we will justify the convergence result within a Monte Carlo scheme to value some financial products such a bond and a path-dependent barrier option.

2 Mathematical preliminaries

Throughout this paper unless otherwise specified, we let be a complete probability space with filtration satisfying the usual conditions (i.e, it is increasing and right continuous while contains all -null sets). If are real numbers, then we denote and . For , denotes the space of all continuous functions with the norm . Also let and denote the space of all nonnegative continuous functions defined on . Moreover, let denote the empty set so that . For a set , denote its indication function by . For , let be a scalar Brownian motion and be a scalar Poisson process with jump intensity which is independent of the Brownian motion, defined on the above probability space. Also let , be a right-continuous Markov chain defined on the above probability space taking values in a finite state space with the generator given by

| (3) |

where . Here is the transition rate from to if while

| (4) |

We assume that the Markov chain is -adapted but independent of the Brownian motion and Poisson process . It is well known that almost every sample path of is a right-continuous step function with finite number of simple jumps in finite subinterval of . Consider the following scalar dynamics as equation of SDDE (2)

| (5) |

such that , , , and , where . For each Lyapunov function , define the jump-diffusion operator by

| (6) |

where is the diffusion operator defined by

| (7) |

with , and . Given the jump-diffusion operator, we could deduce the generalised Itô formula as

| (8) |

Consult [24] and the references therein regarding the function and the martingale measure . We impose the following standing hypotheses which will be recalled later.

Assumption 2.1.

The volatility function of SDDE (5) is Borel-measurable and bounded by a positive constant, that is

| (9) |

and .

Assumption 2.2.

For any , there exists a constant such that the volatility function of SDDE (5) satisfies

| (10) |

and .

Assumption 2.3.

The parameters of SDDE (5) obey

| (11) |

3 Analytical properties

In this section, we study the existence of pathwise uniqueness and boundness of moments of the exact solution to SDDE (5).

3.1 Global positive solution

One basic requirement of a financial model is the existence of a pathwise unique positive solution. The following lemma therefore reveals this requirement.

Lemma 3.1.

Proof.

Since the coefficient terms of SDDE (5) are locally Lipschitz continuous in , then there exists a unique positive maximal local solution for any given initial data (12), where is the explosion time (e.g., see [24]). Let be sufficiently large such that

For each integer , define the stopping time

| (13) |

Obviously, is increasing as . Set , whence a.s. In other words, to complete the proof, we need to show that

We define a -function for some by

| (14) |

From the operator (7) and by Assumption 2.1, we obtain

By the Jump-diffusion operator in (6), we now have

For and by Assumption 2.3, we observe dominates and tends to for small and for large , dominates and tends to . So there exists a constant such that

So for any arbitrary , the Itô formula gives us

It then follows

This implies and consequently, we must have

as the required assertion. The proof is thus complete. ∎

3.2 Moment boundedness

The following lemma shows the moment of the exact solution to SDDE (3) is upper bounded.

Lemma 3.2.

Proof.

For every sufficiently large integer , we define the stopping time by

We also define a Lyapunov function by . By Assumption 2.1, we apply (5) to obtain

where

Apparently, by Assumption 2.3, dominates and tends to for large . So there exists a constant such that

By the the Itô formula, we have

Applying the Fatou lemma and letting yields

and consequently, we obtain (18) as the required assertion. Moreover, by applying the operator (5) to the Lyapunov function , we compute

where Assumption 2.1 has been used and

For , we note dominates and tends to for small . Moreover, we also note dominates and tends to 0 for large . We then find a constant such that

So from the Itô formula, we can apply the Fatou lemma and let to arrive at (16). ∎

4 Numerical method

Under this section, we recall the truncated EM method and apply it for convergent approximation of SDDE (5). To start with, let also impose the following useful condition on the initial data.

Assumption 4.1.

There is a pair of constant and such that for all , the initial data satisfies

| (17) |

We also need the following lemmas (see [21]).

Lemma 4.2.

Lemma 4.3.

The truncated EM scheme for SDDE (5) is now defined in the following subsection.

4.1 The truncated EM method

Let extend the volatility function and the jump term from to by setting and for . These extensions do not in any way affect above conditions and results. To define the truncated EM scheme for SDDE (5), we first choose a strictly increasing continuous function such that as and

| (20) |

Let be the inverse function of and a strictly decreasing function such that

| (21) |

Find such that and for . For a given step size , let us define the truncated functions

and

Then for , we get

and

We easily see that

| (22) |

The following lemma confirms and nicely reproduce (19).

Lemma 4.4.

Let also recall the following useful lemma.

Lemma 4.5.

Given , let for . Then is a discrete Markov chain with the one-step transition probability matrix

The discrete Markovian chain can be simulated as follows: compute the one-step transition probability matrix

Let and generate a random number which is uniformly distributed in . Define

where we set as usual. Generate independently a new random number which is again uniformly distributed in and then define

Repeating this procedure, a trajectory of can be generated.

Given the discrete Markovian chain scheme, we now form the discrete-time truncated EM scheme for SDDE (5) by first letting be arbitrarily fixed and the step size be a fraction of . Define for some positive integer . Define for , set for and then compute

| (24) |

for where and . We have two versions of the continuous-time truncated EM solutions. The first one is defined by

| (25) |

These are the continuous-time step processes and on , where is the indicator function on . The second one is the continuous-time continuous process on defined by setting for while for

| (26) |

Apparently is an Itô process on satisfying Itô differential

| (27) |

We observe , for all .

5 Numerical properties

Let now investigate the numerical properties of the truncated EM scheme. In the sequel, we let

for any , where denotes the integer part of . The following lemma affirms and are close to each other in strong sense.

5.1 Moment boundedness

Lemma 5.1.

Let Assumption 2.1 hold. Then for any fixed , we have for

| (28) |

, where denotes positive generic constants dependent only on and may change between occurrences.

Proof.

Fix any and . Then for , we derive

Recalling the characteristic function’s argument , , in [26], we note

where and are independent of and respectively. We now have

where

Moreover, for , we obtain from the Jensen inequality that

| (29) |

where . The proof is complete. ∎

The following lemma reveals the numerical solutions have upper bound.

Lemma 5.2.

Proof.

Fix any and . For , we obtain from (6) and Lemma 4.4

where

The Young inequality gives us

where . By the triangle inequality, we have for

where

We now obtain from (22) and (5.1)

| (31) |

where , and . We also have from (22)

| (32) |

We clearly observe that for and , and hence

| (33) |

So for and , we obtain from (32), Lemma 5.1, (33) and the Young’s inequality

where and . We now combine and to have

where and . Also we estimate as

where and . We combine , and to have

where

As this holds for any , we then have

The Gronwall inequality gives us

where is independent of . The proof is thus complete. ∎

5.2 Strong convergence

Lemma 5.3.

Proof.

Let be the Lyapunov function in (15). Then for , the Itô formula gives us

For , we can expand to have

where is the operator in (6), which now takes the form

with independent of and

By Assumptions 2.1 and 2.3, we can find a constant such that

| (36) |

Recalling from the definition of and , we note for

So for , we obtain from Lemma 4.2 that

Moreover, for and any , we note from (20) that

So for , we now obtain from Assumptions 2.1 and 2.2, and Lemma 4.2

Also for , we obtain from the Lyapunov function in (15) and the mean value theorem that

where . Combining , and with (36), we now have

where

and

So by Lemmas 5.1 and 5.1, we now obtain

This implies

| (37) |

For any , we may select sufficiently large such that

| (38) |

and sufficiently small of each step size such that

| (39) |

We can now combine (38) and (39) to obtain the required assertion. ∎

The following lemma shows the truncated EM scheme converges strongly in finite time.

Lemma 5.4.

Proof.

For , we obtain from (5) and (4.1) that

| (42) |

where

By the Hölder and elementary inequalities, we compute

where

It is clear from the definition of the truncated function that for So by Lemma 4.2,

Let be the integer part of . Then

with now set to be . We now have from (22)

| (43) |

where we use the fact that and are conditionally independent with respect to the algebra generated by in the last step. By the Markov property, we compute

| (44) |

where . By Lemma 5.2, we note

This implies

and consequently

Substituting this into yields

We then combine and to obtain

where

Also by the Hölder and Burkholder-Davis Gundy inequalities, we have

where

where is a positive constant. For , we note from (20) that and . So we now have

where

By Assumption 2.2, we obtain

Also as before, we compute

where is the usual integer part of with set to be . By elementary inequality,

We note from (5.2) that

By Assumption 2.1, we have

This means by Assumption 2.1, we have

and hence,

Inserting this into yields

We obtain from and

Moreover, by Assumption 2.1 and Lemma 4.2

Combining and , we have

where

Furthermore, by elementary inequality

where

By the Doob martingale inequality and martingale isometry, we have

where

and is a positive constant. By Lemma 4.2,

We also compute

where , as usual, is the integer part of with set to be . By Lemma 5.2 and (5.2)

where . Consequently, we have

and then,

| (45) |

We substitute this into to get

It then follows from and that

By the the Hölder inequality,

where

So by Lemma 4.2,

Apparently, we see from (45) that

This implies

We now have from and

We then combine and to have

where

Substituting , and into (42), we get

It then follows that

where

By elementary inequality, Assumption 4.1 and Lemma 5.1

So by Lemma 5.2 and noting that , we now have

where and . The Gronwall inequality gives us

as the required result in (40). where . By letting , we get (41). ∎

The strong convergence theorem of the truncated approximate solutions is as follows.

Theorem 5.5.

Proof.

Here, we only prove the theorem for . As for , it follows directly from the case of and the Hölder inequality. Let , and , be the same as before. Set

For any arbitrarily , the Young inequality gives us

| (48) |

So for , Lemmas 3.2 and 5.2 give us

| (49) |

| (50) |

Also by Lemma 5.4,

| (51) |

Substituting (5.2), (50) and (51) into (5.2) yields

Given , we can select so that

| (52) |

Similarly, for any given , there exists so that for , we may select to have

| (53) |

and select such that for

| (54) |

Finally, we may select sufficiently small for such that

| (55) |

Combining (52), (53), (54) and (55), we get

as the required result in (46). By Lemma 5.1, we also get (47) by setting . ∎

6 Numerical simulations

Let us now implement the truncated EM (TEM) scheme for SDDE (2). To illustrate the strong result established in Theorem 5.5, we compare the scheme with the backward EM (BEM) scheme. For justification regarding the choice of BEM scheme and its limitation, we refer the reader to consult [21]. Now consider the following form of SDDE (2)

| (56) |

on with initial values and , where is a Markovian chain defined on the state with the generator given by

| (57) |

Moreover, let

| (58) |

| (59) |

and

| (60) |

. The volatility process is a sigmoid-type function defined as follows:

for ,

and for ,

| (61) |

. Obviously, all the assumptions imposed on are met(see [21]). We clearly see

We can now set with inverse .

6.1 Numerical results

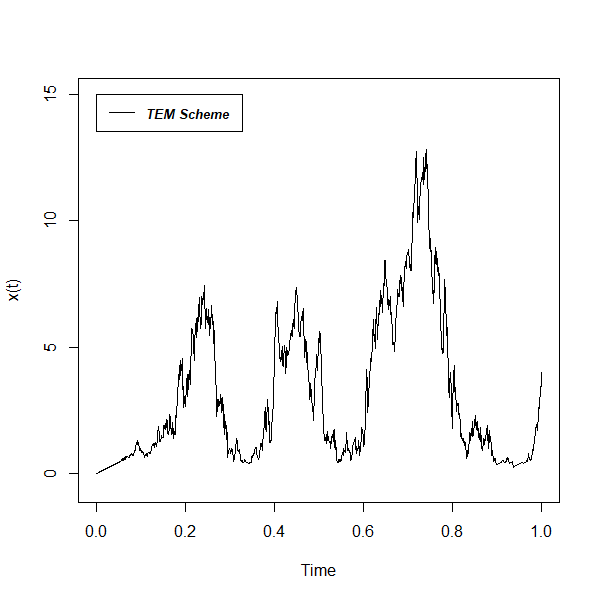

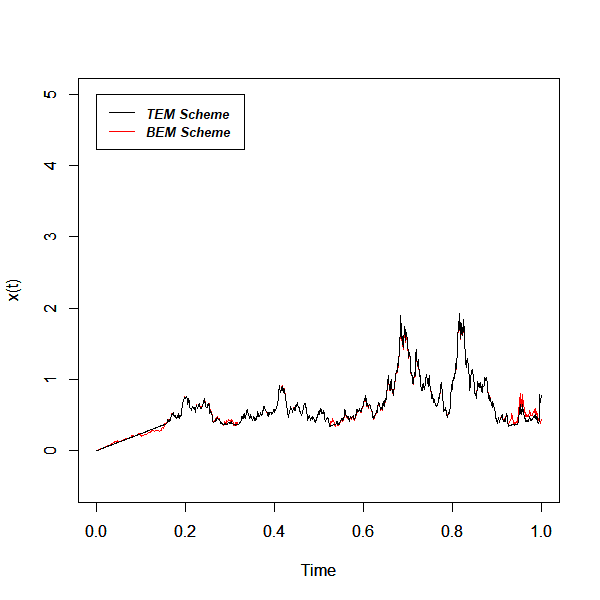

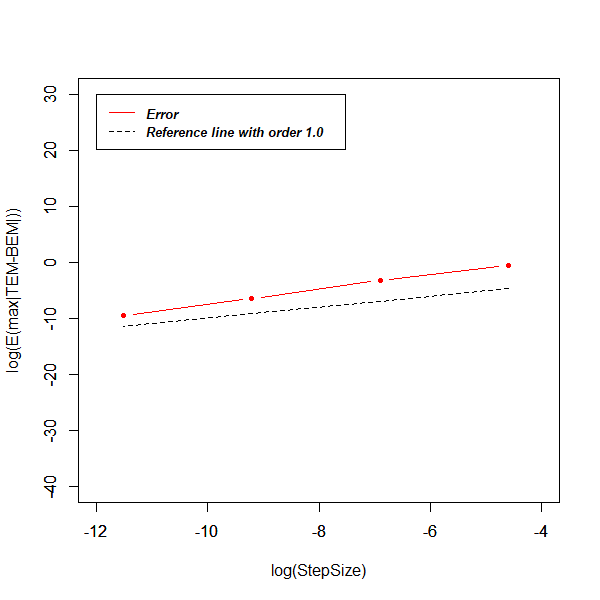

By selecting and step size , we obtain Monte Carlo simulated sample path of to SDDE (56) at terminal time in Figure 1 using the TEM scheme. The strong convergence between TEM and BEM numerical solutions is shown in Figure 2. In Figure 3, we observe the strong order to be approximately one half although this result is not yet proved theoretically. Do note that Figure 2 and Figure 3 were obtained without the drift term (see [21]).

7 Applications in finance

In this section, we justify Theorem 5.5 for Monte Carlo valuation of a bond and a barrier option.

7.1 A bond

7.2 A barrier option

Acknowledgements

The author would like to express his sincere gratitude to his supervisor, Prof. Mao Xuerong and also thank University of Strathclyde for the doctoral scholarship.

References

- [1] Black, F. and Scholes, M., 1973. The pricing of options and corporate liabilities. Journal of political economy, 81(3), pp.637-654.

- [2] Mao, X. and Sabanis, S., 2013. Delay geometric Brownian motion in financial option valuation. Stochastics An International Journal of Probability and Stochastic Processes, 85(2), pp.295-320.

- [3] Merton, R.C., 1976. Option pricing when underlying stock returns are discontinuous. Journal of financial economics, 3(1-2), pp.125-144.

- [4] Lin, B.H. and Yeh, S.K., 1999. Jump-Diffusion Interest Rate Process: An Empirical Examination. Journal of Business Finance and Accounting, 26(7-8), pp.967-995.

- [5] Kou, S.G., 2002. A jump-diffusion model for option pricing. Management science, 48(8), pp.1086-1101.

- [6] Elliott, R.J., Chan, L. and Siu, T.K., 2013. Option valuation under a regime-switching constant elasticity of variance process. Applied Mathematics and Computation, 219(9), pp.4434-4443.

- [7] Wu, F., Mao, X. and Chen, K., 2008. Strong convergence of Monte Carlo simulations of the mean-reverting square root process with jump. Applied Mathematics and Computation, 206(1), pp.494-505.

- [8] Wu, F., Mao, X. and Chen, K., 2009. The Cox–Ingersoll–Ross model with delay and strong convergence of its Euler–Maruyama approximate solutions. Applied Numerical Mathematics, 59(10), pp.2641-2658.

- [9] Lee, M.K. and Kim, J.H., 2016. A delayed stochastic volatility correction to the constant elasticity of variance model. Acta Mathematicae Applicatae Sinica, English Series, 32(3), pp.611-622.

- [10] Ait-Sahalia, Y., 1996. Testing continuous-time models of the spot interest rate. The review of financial studies, 9(2), pp.385-426.

- [11] Cheng, S.R., 2009. Highly nonlinear model in finance and convergence of Monte Carlo simulations. Journal of Mathematical Analysis and Applications, 353(2), pp.531-543.

- [12] Szpruch, L., Mao, X., Higham, D.J. and Pan, J., 2011. Numerical simulation of a strongly nonlinear Ait-Sahalia-type interest rate model. BIT Numerical Mathematics, 51(2), pp.405-425.

- [13] Dung, N.T., 2016. Tail probabilities of solutions to a generalized Ait-Sahalia interest rate model. Statistics and Probability Letters, 112, pp.98-104.

- [14] Hamilton, J.D., 1988. Rational-expectations econometric analysis of changes in regime: An investigation of the term structure of interest rates. Journal of Economic Dynamics and Control, 12(2-3), pp.385-423.

- [15] Ratanov, N., 2016. Option pricing under jump-diffusion processes with regime switching. Methodology and Computing in Applied Probability, 18(3), pp.829-845.

- [16] Bollen, N.P., Gray, S.F. and Whaley, R.E., 2000. Regime switching in foreign exchange rates:: Evidence from currency option prices. Journal of Econometrics, 94(1-2), pp.239-276.

- [17] Hutzenthaler, M., Jentzen, A. and Kloeden, P.E., 2012. Strong convergence of an explicit numerical method for SDEs with nonglobally Lipschitz continuous coefficients. The Annals of Applied Probability, 22(4), pp.1611-1641.

- [18] Wang, X. and Gan, S., 2013. The tamed Milstein method for commutative stochastic differential equations with non-globally Lipschitz continuous coefficients. Journal of Difference Equations and Applications, 19(3), pp.466-490.

- [19] Liu, W. and Mao, X., 2013. Strong convergence of the stopped Euler–Maruyama method for nonlinear stochastic differential equations. Applied Mathematics and Computation, 223, pp.389-400.

- [20] Mao, X., 2015. The truncated Euler–Maruyama method for stochastic differential equations. Journal of Computational and Applied Mathematics, 290, pp.370-384.

- [21] Coffie, Emmanuel. and Mao, X., 2021. Truncated EM numerical method for generalised Ait-Sahalia-type interest rate model with delay. Journal of Computational and Applied Mathematics, 383, p.113137.

- [22] Mao, X. and Yuan, C., 2006. Stochastic differential equations with Markovian switching. Imperial college press.

- [23] Mao, X., 2007. Stochastic differential equations and applications. 2nd ed. Chichester: Horwood Publishing Limited.

- [24] Yuan, C. and Mao, X., 2010. Stability of stochastic delay hybrid systems with jumps. European journal of control, 16(6), pp.595-608.

- [25] Higham, D.J. and Mao, X., 2005. Convergence of Monte Carlo simulations involving the mean-reverting square root process. Journal of Computational Finance, 8(3), pp.35-61.

- [26] Bao, J., Böttcher, B., Mao, X. and Yuan, C., 2011. Convergence rate of numerical solutions to SFDEs with jumps. Journal of Computational and Applied Mathematics, 236(2), pp.119-131.

- [27] Deng, S., Fei, W., Liu, W. and Mao, X., 2019. The truncated EM method for stochastic differential equations with Poisson jumps. Journal of Computational and Applied Mathematics, 355, pp.232-257.

- [28] Coffie, E., 2021. Delay stochastic interest rate model with jump and strong convergence in Monte Carlo simulations. arXiv preprint arXiv:2103.07651.

- [29] Benth, F.E., 2003. Option theory with stochastic analysis: an introduction to mathematical finance. Berlin: Springer Science and Business Media.

- [30] Oksendal, B., 2013. Stochastic differential equations: an introduction with applications. Springer Science and Business Media.