Model Selection for Generic Contextual Bandits

Abstract

We consider the problem of model selection for the general stochastic contextual bandits under the realizability assumption. We propose a successive refinement based algorithm called Adaptive Contextual Bandit (ACB), that works in phases and successively eliminates model classes that are too simple to fit the given instance. We prove that this algorithm is adaptive, i.e., the regret rate order-wise matches that of any provable contextual bandit algorithm (ex. [1]), that needs the knowledge of the true model class. The price of not knowing the correct model class turns out to be only an additive term contributing to the second order term in the regret bound. This cost possess the intuitive property that it becomes smaller as the model class becomes easier to identify, and vice-versa. We also show that a much simpler explore-then-commit (ETC) style algorithm also obtains similar regret bound, despite not knowing the true model class. However, the cost of model selection is higher in ETC as opposed to in ACB, as expected. Furthermore, for the special case of linear contextual bandits, we propose specialized algorithms that obtain sharper guarantees compared to the generic setup.

Index Terms:

Model Selection, Contextual Bandits, Linear BanditsI Introduction

The contextual Multi Armed Bandit (MAB) problem is a fundamental online learning setting capturing the exploration-exploitation trade-offs associated with sequential decision making (c.f. [2, 3]). It consists of an agent, who at each time is shown a context by nature, and subsequently makes an irrevocable decision from a set of available decisions (arms) and collects a noisy reward depending on the arm chosen and the observed context. The agent initially has no knowledge of the rewards of the various actions, and has to learn by repeated interaction over time, the mapping from the set of context and arms to rewards. The agent’s goal is to minimize regret —the expected difference between the reward collected by an oracle that knows the expected rewards of all actions under all possible observed contexts and that of the agent. The recent books of [4], [5] and the references therein provide comprehensive state-of-art on the general bandit problem.

We study the model selection question in general stochastic contextual bandits (c.f. [6], [7], [1], [8]). Practically, model selection in contextual bandits play a key role in applications such as personalized recommendation systems, which we sketch in the sequel in Section I-B. At a high-level, model selection is useful in deciding the function class (for example neural network architecture) to use to learn the mapping from contexts to rewards. Smaller function class such as a logistic regression although are easier to train and tune hyper-parameters, may fit poorly to data (high statistical bias). On the other hand, very deep neural networks although in principle can achieve high statistical accuracy, incur overheads such as complex hyper-parameter tuning and challenges of explainability. The model selection problem formalizes this trade-off and defines an optimal choice (see Section I-B).

Formally, the contextual bandit setting is described as follows. At the beginning of each round , nature sequentially chooses a context and a reward function to an agent, who then subsequently takes an action from a finite set, and obtains a reward . In the stochastic setting (the focus of the present paper), the set of contexts and reward functions are generated in an i.i.d. fashion from a distribution which is apriori unknown to the agent. At each time , conditional on the context and the action taken , the observed reward is independent of everything else, with mean , where , is an apriori unknown function. The agent is given a finite, nested family of hypothesis classes111We use the term hypothesis class and model class interchangebly, where implies . Further, there exists an optimal class , i.e., is the smallest hypothesis class containing the unknown reward function . The agent is not aware of apriori and needs to estimate it. Model selection guarantees then refers to algorithms for the agent whose regret scales in the complexity of the smallest hypothesis class ( in the above notation) containing the true model, even though the algorithm was not aware apriori.

In the case when the agent has the knowledge of but does not know , [1] recently obtain computationally efficient algorithm FALCON, that achieves regret-rate scaling as . Using realizibility, i.e., , it was shown in [1], that the stochastic contextual bandit can be reduced to an offline regression problem, which can be efficiently solved for many well known function classes beyond linear (eg. the set of all convex functions [9]). The regret of FALCON was shown to scale proportional to the square root of the complexity of the function class times , the time horizon. In the case when is a finite set, the complexity equals the logarithm of the cardinality, while if the class is infinite (either countable or uncountable), complexity is analogously defined (c.f. Section V).

The study in this paper is reliant on two assumptions: (i) Realizability (Assumption 1), —the true model belongs to at-least one of the many nested hypothesis classes, and (ii) Separation (Assumption 2) —the excess risk under any of the plausible model classes not containing the true model is strictly positive. Realizability, has been a standard assumption in stochastic contextual bandits ([10], [8], [1]), and is used in our setup to define the optimal model class that needs to be selected. The separation assumption is needed to ensure that not selecting a relizable model class leads to regret scaling linear in time. The separation assumption is analogous to that used in standard multi-armed bandits [4], where the mean reward of the best arm is strictly larger than that of the second best arm.

A negative result and the need of separability: In [11], the authors provide a negative answer to the open problem of [12], implying that it is not possible to obtain a regret which is order-wise identical to an oracle who knows the true model class . In particular, [11] shows that there always exists an instance where the regret in the smallest realizable class is (order-wise) larger than what is achievable with an oracle222The paper allows the hypothesis classes to be adversarily designed and hence in general requires a lot of exploration for model selection.. This implies that if we aim to obtain oracle-optimal regret, we should exploit certain structures in the problem. In this paper, we achieve this by the separability assumption, which comes naturally in statistical learning problems333The separability assumption restricts the amount the exploration needed, dependent on the gap or separation.. This assumption should be thought as a first step towards obtaining (oracle) optimal regret.

In parallel independent work, [13] also study model selection problem, under the same assumptions of realizability and separation that we make. They propose ModIGW algorithm that is built on FALCON and shares similarity to our algorithm ACB; both algorithms run in epochs of doubling length, where at the beginning of each epoch, an appropriate model class is selected, and the rest of the epoch consists of playing FALCON on the selected model class. In order to select the appropriate class, the nested structure of model classes along with the fact that the largest class is realizable by definition is used. The regret guarantees are similar for both ACB and ModIGW, with ModIGW having a better second order term, as they have a stronger assumption on the regression oracle. Remark 7 highlights that under the same assumption on the regression oracle, the second order term of ACB will match (order-wise) that of ModIGW. However, our proposed method, ACB can be viewed as a meta-algorithm, that uses any state-of-art contextual bandit algorithm, as a black-box (see Algorithm 2). In particular ACB works with any provable contextual bandit algorithm—a feature that ModIGW does not posses. Thus any improvement to the contextual bandit problem, automatically yields a model selection result through ACB. Moreover, our proof techniques are completely different to that of [13].

Finally in Sections VI-A and VI-B, we consider the specialized case where assumes a linear form and thus parameterized by . We note that in this setup the sparsity, naturally forms a nested hypothesis class, where denotes the class of linear functions with sparsity . So, we have and . We propose and analyze a novel algorithm, namely Adaptive Linear Bandit-Dimension (ALB-Dim), which may be thought as a variant of the generic ACB. We show that the regret of ALB-Dim scales linearly in the unknown cardinality of the support of . The regret of our algorithm matches that of an oracle who knows the support of ([14],[15]), thereby achieving model selection guarantees.

We emphasize that the setting with dimension as a measure of complexity was also studied by [14]. However, our regret bounds are stronger (by a logarithm in factor). Furthermore, our algorithmic paradigm is more broadly applicable – for eg. we can handle both the cases with finite as well as infinite arms, and obtain similar model selection regret guarantees that match the regret of an oracle that knows the true dimension. Model selection with dimension as complexity measure was also recently studied by [10], in which the classical contextual bandit ([3]) with a finite number of arms was considered. We clarify here that although our results for the finite arm setting yields a better (optimal) regret scaling with respect to the time horizon and the support of (denoted by ), our guarantee depends on a problem dependent parameter and thus not uniform over all instances. In contrast, the results of [10], although sub-optimal in and , is uniform over all problem instances. Closing this gap is an interesting future direction.

We emphasize here that our specialized algorithm, ALB-Dim does not require any (explicit) separability assumption across hypothesis classes similar to the generic case. Also, our setup here can handle the case with finite as well as infinite number of arms/actions. Moreover, we show in Sections VI-A and VI-B that the regret of ALB-Dim is independent (order-wise) of the number of actions, and hence for the finite action setup, it improves the regret of ACB by a factor of .

I-A Our Contributions

I-A1 A Successive Refinement Algorithm for General Contextual Bandit

We present Adaptive Contextual Bandit (ACB), a meta algorithm that uses FALCON as a black box and show that its regret rate matches (order-wise), FALCON’s ([1]), the state of art algorithm in contextual bandits which assumes knowledge of the true model class. ACB proceeds in epochs, with the first step in every epoch being a statistical test on the samples from the previous epoch to identify the smallest model class, followed by FALCON on this identified class in the epoch. We show that, with high probability, eventually, ACB identifies the true model class (Lemma 2), and thus its regret rate matches that of FALCON.

Cost of model selection:

The second order regret term in ACB scales as , where , is the gap (formally defined in Assumption 2) between the smallest class containing the true model and the highest model class not containing the true model. This term can be interpreted as the cost of model selection. Furthermore, as this term is inversely proportional to the gap , we see that an ‘easier’ instance ( being high), incurs lower cost of model selection than an instance with smaller . Furthermore, the model selection cost can be reduced to if is known in advance.

I-A2 An Explore-then-commit (ETC) algorithm

We propose and analyze an Explore-then-commit (ETC) algorithm that also achieves model selection, but requires knowledge of in advance has a larger second order regret compared to ACB . We show that a ETC algorithm also performs model selection, i.e., has a regret rate scaling as that of FALCON on the optimal model class. This is a conceptually simpler algorithm compared to ACB. In ETC, the model class is estimated once after a few rounds of forced exploration, and the rest of the time-horizon FALCON is played on the estimated model class. However, the cost of model selection in ETC is , which is larger than that of ACB. Nevertheless, asymptotically, a simple ETC algorithm suffices to obtain model selection.

I-A3 Improved Regret Guarantee with Linear Structure

In the special setup of stochastic linear bandits, where the reward is a linear map of the context, we propose and analyze an adaptive algorithm, namely Adaptive Linear Bandits-Dimension (ALB-Dim). First we observe that in this special case, we do not require any separability assumption. Moreover, the setup of linear bandits can include both finite as well as infinite number of actions. We show that the regret of ALB-Dim is independent of the number of actions (arms), which is an improvement over the regret of ACB. In particular, for the finite arm setup, ALB-Dim improves the regret of ACB by a factor of .

I-B Motivating example

Model selection in contextual bandits plays a key role in applications such as personalized recommendation systems, which we sketch. Consider a system (such as news recommendation) that on each day, recommends one out of possible outlets to a user. On each day, an event is realized in nature, which can be modeled as the context vector on that day. The true model function encodes the user’s preference; for example the user prefers one outlet for sports oriented articles, while another for international events. This apriori unknown to the system and needs to learn this through repeated interactions. The multiple nested hypothesis classes correspond to a variety of possible neural network architectures to learn the mapping from contexts (event of the day) to rewards (which can be engagement with the recommended item). In practice, these nested hypothesis classes range from simple logistic regression to multi-layer perceptrons [16]. Complex network architectures although has the potential for increased accuracy, incurs undesirable overheads such as requiring larger offline training to deliver accuracy gains [16], computational complexity in hyper-parameter tuning [17] and challenges of explainability in predictions [18, 19]. Model selection provides a framework to trade-off between accuracy and the overheads.

II Related work

Model selection for MAB have received increased attention in recent times owing to its applicability in a variety of large-scale settings such as recommendation systems and personalization. The special case of linear contextual bandits was studied in [20], [21] and [10], where both instance dependent and instance independent algorithms achieving model selection were given. In [20], [21], the standard OFUL algorithm of [22] is taken as a baseline and model selection procedures are proposed on top of that. In this linear bandit framework, similar to the present paper, [10] and [21] considered the family of nested hypothesis classes, with each class positing the sparsity of the unknown linear bandit parameter. In this setup, [10] proposed ModCB which uses the Exp4-IX algorithm of [23] as a base algorithm and achieves regret rate uniformly for all instances, a rate that is sub-optimal compared to the oracle that knows the true sparsity. In contrast, both our paper and [21] propose an algorithm that achieves regret rate matching that of the oracle that knows the true sparsity. The cost of model selection contributes only a constant that depends on the instance but independent of the time horizon. However, unlike ModCB, our regret guarantees are problem dependent and do not hold uniformly for all instances. A parallel line of work on linear bandits has focused on simple LASSO type algorithms under strong stochastic assumptions on the distribution of the contexts that achieve model selection guarantees [15, 24, 25, 26, 27].

A black-box model selection framework for MABs called Corral was proposed in [28], where the optimal algorithm for each hypothesis class is treated as an expert and the task of the forecaster is to have low regret with respect to the best expert (best model class). The generality of this framework has rendered it fruitful in a variety of different settings; for example [28, 29] considered unstructured MABs, which was then extended to both linear and contextual bandits and linear reinforcement learning in a series of works [30, 31] and lately to even reinforcement learning [32]. However, the price for this versatility is that the regret rates the cost of model selection is multiplicative rather than additive. In particular, for the special case of linear bandits and linear reinforcement learning, the regret scales as in time with an additional multiplicative factor of , while the regret scaling with time is strictly larger than in the general contextual bandit. Since this approach treats all the hypothesis classes as bandit arms, and work in a (restricted) partial information setting, they tend to explore a lot, yielding worse regret. On the other hand, we consider all classes at once (full information setting) and do inference, and hence explore less and obtain lower regret. Recently, the above idea of regret balancing is extended to black box optimization in the context of non-stationary Reinforcement Learning ([33]) and robust Reinforcement Learning ([34]).

| Regret Bound | Function Class | Arms | Base Algorithm | |

|---|---|---|---|---|

| [20] | , Linear | Finite | OFUL | |

| [10] | Linear | Finite | Exp4-IX | |

| [35] | Generic | Infinite | CORRAL | |

| [13] | Generic | Finite | FALCON | |

| This paper | Generic | Finite | Generic () |

Furthermore, [36] study the problem of model selection in RL with function approximation. Similar to the active-arm elimination technique employed in standard multi-armed bandit (MAB) problems [37], the authors eliminate the model classes that are dubbed misspecified, and obtain a regret of . On the other hand, our framework is quite different in the sense that we consider model selection for generic contextual bandits. Moreover, our regret scales as .

Adaptive algorithms for linear bandits have also been studied in different contexts from ours. The papers of [38, 39] consider problems where the arms have an unknown structure, and propose algorithms adapting to this structure to yield low regret. The paper [40] proposes an algorithm in the adversarial bandit setup that adapt to an unknown structure in the adversary’s loss sequence, to obtain low regret. The paper of [41] consider adaptive algorithms, when the distribution changes over time. In the context of online learning with full feedback, there have been several works addressing model selection [42, 43, 44, 45]. In the context of statistical learning, model selection has a long line of work (for eg. [46], [47], [48], [49], [50] [51]). However, the bandit feedback in our setups is much more challenging and a straightforward adaptation of algorithms developed for either statistical learning or full information to the setting with bandit feedback is not feasible.

III Problem formulation

Setup:

Let be the set of actions, and let be the set of dimensional contexts. At time , nature picks in an i.i.d fashion from an unknown distribution (see [7]), where and a context dependent . All expectation operators in this section are with respect to this i.i.d. sequence . Upon observing the context, the agent takes action , and obtains the reward of . Note that, the reward depends on the context and the action . Furthermore, it is standard ([10, 1]) to have a realizibility assumption on the conditional expectation of the reward, i.e., there exists a predictor , such that , for all and . We suppress the dependence of the reward on the context and denote the reward at time from action as .

In the contextual bandit literature ([7, 1]) it is generally assumed that the true regression function is unknown, but the function class where it belongs, is known to the learner. The price of not knowing is characterized by regret, which we define now. To set up notation, for any , we define a policy induced by the function , as 444Ties are broken arbitrarily, for example the lexicographic ordering of , for all . We define the regret over rounds defined as

Throughout this paper, we obtain high probability bounds on

IV Model selection for generic contextual bandits

In this section, we focus on the main contribution of the paper—a provable model selection guarantee for the (generic) stochastic contextual bandit problem. In contrast to the standard setting, in the model selection framework, we do not know . Instead, we are given a nested class of function classes, . Let the smallest function class where the true regressor, lies be denoted by , where .

From the above discussion, since , the regret of an adaptive contextual bandit algorithm should depend on the function class . However, we do not know , and our goal is to propose adaptive algorithms such that the regret depends on the actual problem complexity . First, let us write the realizability assumption with the nested function classes.

Assumption 1 (Realizability)

There exists , and a predictor , such that , for all and .

Furthermore, in order to identify the correct model class within the given hypothesis classes, we also require the following separability condition. The motivation of the separability comes from the following negative result.

Very recently, [11] provides a negative answer to the open problem of [12], showing that it is not possible to obtain a regret which is order-wise identical to an oracle who knows the true model class . Specifically, [11] shows that there always exists an instance where the regret in the smallest realizable class is (order-wise) larger than of an oracle.

Assumption 2 (Separability)

There exists a , such that,

The parameter is the minimum separation across the function classes. The expectation above is with respect to the randomness in contexts.

Note that the identical separability condition is also witnessed in [13]555This is equivalent to

. The above condition implies that there is a (non-zero) gap, between the regressor functions belonging to the realizable classes and non-realizable classes. Since, we have nested structure, , condition on the biggest non-realizable class, is sufficient. We emphasize that separability condition is quite standard in statistics, specially in the area of clustering ([52]), analysis of Expectation Maximization (EM) algorithm ([53, 54], understanding the behavior of Alternating Minimization (AM) algorithms ([55, 9]).

Having said that, we believe a weaker separability assumption that requires and to be separated near the optimal action only (local separability) should be sufficient—which is often the case for (offline) statistical problems. However, with finite () number of actions, it is not immediately clear how to weaken this, and model selection without (or with weak) separability is kept as an interesting future work. We also emphasize that although we require the gap assumption for theoretical analysis, our algorithm (described next) does not require any knowledge of , and adapts to the gap of the problem.

IV-A Warm Up: A simple Explore-Then-Commit (ETC) algorithm for model selection

In this section, we provide a simple model selection algorithm based on Explore-Then-Commit (ETC) novel model selection algorithm that use successive refinements over epochs. We use a simple Explore-Then-Commit (ETC) algorithm for selecting the correct function class, and then commit to it during the exploitation phase. After a round of exploration, we do a (one-time) threshold based testing to estimate the function class, and after that, exploit the estimated function class for the rest of the iterations. Here, we consider any (generic) contextual bandit algorithm along with the function class containing the true regressor . The details are provided in Algorithm 1.

As an example of , we use a provable contextual bandit algorithm, namely FALCON (stands for FAst Least-squares-regression-oracle CONtextual bandits) of [1], the details are provided in Algorithm 3.

Note that in this section, for simplicity, we continue to consider consider the setup where the function classes are finite. However, in Section V, we remove this, and work in infinite function classes.

We show that this simple strategy finds the optimal function class with high probability. We now explain the exploration and exploitation phases of this algorithm.

For the first time epochs, we do the exploration (i.e., sample randomly). Precisely, the context-reward pair is being sampled by nature in an i.i.d fashion, and the action the agent takes is chosen uniformly at random from the action set . In particular, the action is chosen independent of the context . Hence, this is a pure exploration strategy.

Based on the samples of the first rounds, we estimate the regression function for all the (hypothesis) function classes via offline regression oracle (see [1] for details) and obtain for all .

To remove dependence issues, we use the remaining samples obtained form the sampling phase. Here we actually compute the following test statistic for all hypothesis classes, namely

for all . We then perform a thresholding on . We pick the smallest index such that . We then commit to this function class for the rest time steps. Hence, in Algorithm 1, we perform one step thresholding and commit to it. We show that simple scheme obtains the correct model with high probability.

IV-B Regret Guarantee of ETC

Lemma 1 (Model Selection for ETC)

Suppose the time horizon satisfies

Then with probability at least , line in Algorithm 1 identifies the correct model class .

We now analyze the regret performance of Algorithm 1. The regret is comprised of stages; (a) exploration and (b) commit (exploitation). We have the following result.

Theorem 1

Remark 1 (Cost of Model Selection)

As seen in Theorem 1, the cost of model selection is . In the next section, we propose a successive refinement based algorithm to cut down this cost to .

Remark 2 (Matches Oracle)

Let us consider the special case when = FALCON. In the regret expression, the first term scales with . The second expression in the regret is , with high probability). So, we observe that (order-wise) the cost of model selection is no-worse than the regret of FALCON even with the knowledge of the smallest function class containing , i.e, .

IV-C Beyond ETC: Algorithm—Adaptive Contextual Bandits (ACB)

In the previous section, we saw a simple ETC type algorithm for model selection. In this section, we propose and analyze a novel model selection algorithm that use successive refinements over epochs to cut down the cost of model selection. Similar to the previous section, we consider any contextual bandit algorithm along with the function class containing the true regressor . We take as a baseline, and add a model selection phase at the beginning of each epoch. In other words, over multiple epochs, we successively refine our estimates of the proper model class where the true regressor function lies. The details are provided in Algorithm 2. Note that ACB does not require any knowledge of the separation .

As an example of , we use a provable contextual bandit algorithm, namely FALCON (stands for FAst Least-squares-regression-oracle CONtextual bandits) of [1], the details are provided in Algorithm 3.

Note that in this section, for simplicity, we continue to consider consider the setup where the function classes are finite. However, in Section V, we remove this, and work in infinite function classes.

The Base Algorithm:

We work with a generic contextual bandit algorithm, , which, upon observing context , outputs an action for the agent along with the reward . As a special case, we take the example of a contextual bandit algorithm, FALCON (see Algorithm 3), which is recently proposed and analyzed in [1]. In particular, FALCON gives provable guarantees for contextual bandits beyond linear structure. FALCON is an epoch based algorithm, and depends only on an offline regression oracle, which outputs an estimate of the regression function at the beginning of each epoch. FALCON then uses a randomization scheme, that depends on the inverse gap with respect to the estimate of the best action. Suppose that the true regressor , and the realizibility condition (Assumption 1) holds. With a proper choice of learning rate, with probability , FALCON yields a regret of . Although the above result makes sense only for the finite , an extension to the infinite is possible and was addressed in the same paper (see [1]).

Our Approach

We use successive refinement based model selection strategy along with the base algorithm . The details of our algorithm, namely Adaptive Contextual Bandits (ACB) are given in Algorithm 2. We break the time horizon into several epochs with doubling epoch length. Let be epoch instances, with , and . Before the beginning of the -th epoch, using all the data of the -th epoch, we add a model selection module, as shown in Algorithm 2 (lines 4-8).

Note that, in ACB, we feed the samples of the -th epoch to the offline regression oracle. Moreover, we split the samples in 2 equal halves. We use the first half to compute the regression estimate

via offline regression oracle. ACB then use the rest of the samples to construct the test statistics given by,

for all . We do not use the same set of samples to remove any dependence issues with and the samples .

ACB then compares the test statistics in Line of Algorithm 2 to pick the model class. Intuitively, we expect to be small for all hypothesis classes that contain . Otherwise, thanks to the separation condition in Assumption 2, we expect to be large. Realizability, i.e., Assumption 1 ensures that , the largest hypothesis class by definition contains the true model . Thus serves as an estimate of how small the excess risk of any realizable class must be. We set the threshold to be a small addition to . The additional term of in Line of Algorithm 2 is chosen so that it is not too small, but nevertheless goes to , as . In particular, we choose the threshold in ACB such that it is large enough to ensure all realizable classes have excess risk smaller than this threshold, but also not so large that it exceeds the excess risk of the non-realizable classes.

Let be function class selected by this procedure in epoch . ACB now uses the base algorithm, to obtain an action and corresponding reward . For instance, in the case of FALCON (as seen in Algorithm 3), the learner uses inverse gap randomization with properly chosen learning rate (see [1, 56, 57]) to select the action . In particular, with as the regressor function, let be the greedy action. The inverse gap randomization is defined in the following way:

where is the number of arms (actions) and is the learning rate. Finally, we sample action and henceforth observe reward .

IV-D Analysis of ACB

We now analyze the performance of the model selection procedure of Algorithm 2. We have the doubling epochs, i.e., . Without loss of generality, we simply assume . Also, assume that we are at the beginning of epoch , and hence we have the samples from epoch . So, we have total of samples, out of which, we use to construct the regression functions and the rest to obtain the testing function . Furthermore, we want the model selection procedure to succeed with probability at least , since the we want a guarantee that holds for all , and a simple application of the union bound yields that. We first show that ACB identifies the correct function class with high probability after a few epochs. We have the following Lemma.

Lemma 2 (Model Selection of ACB)

Proof sketch. In order select the correct function class, we first obtain upper bounds on the test statistics for model classes that includes the true regressor . We accomplish this by first carefully bounding the expectation of and then using concentration. We then obtain a lower bound on for model classes not containing via leveraging Assumption 2 (separability) along with Assumption 1. Combining the above two bounds yields the desired result.

Regret Guarantee

With the above lemma, we obtain the following regret bound for Algorithm 2.

Theorem 2

Remark 3 (Matches Oracle)

The first term of the regret scales weakly with (as ). Hence, provided , the regret scaling (with respect to ) is dominated by (in case of FALCON, this term is , with high probability). However note that this is the regret of an oracle knowing the true function class .

Remark 4 (Model selection Cost)

The first term can be interpreted as the cost of model selection and it depends on the gap . Hence, the model selection procedure only adds a term (this term is minor in the regime ) term compared to the scaling).

Remark 5 (Adaptive)

Algorithm 3 does not require knowledge of . Nevertheless, the regret guarantee adapts to the problem hardness, i.e., if is small, the regret is larger and vice-versa.

Remark 6 (Improvement from to in the model selection cost)

We emphasize that the factor in the cost of model selection term can be improved, if we have the knowledge of apriori. In that setting, instead of substituting , we substitute for all . Since the doubling epoch ensures a total of epochs, this choice of yields

with probability at least .

Remark 7 (Stronger Oracle in [13])

The cost of model selection in Theorem 2, depends on the complexity of the largest model class . Under a stronger assumption on the regression oracle (for example Assumption of [13]), the cost of model selection can only depend on as opposed to . Based on samples obtained from pure exploration for a realizable function class, we use [7] to bound the excess risk (i.e., ) as a function of . In particular, since (the largest class) is always realizable, we obtain an upper bound dependent on . On the other hand, Assumption 2 of [13] leads to an upper bound dependent on only (since they take a minimum over all realizable classes).

V Generic contextual bandits with infinite function classes

The results in Section IV hold for finite function classes, since the regret bound depends on the cardinality of the function class. However, it can be extended to the infinite function classes (see [1] for details). Exploiting the notion of the complexity of infinite function classes, this reduction is done.

Like before, we consider a nested sequence of function classes . The reward is sampled from an unknown function lying in the (smallest) function class indexed by , which is unknown. Given the function classes, our job is to find the function class , and subsequently exploit the class to obtain sub-linear regret. Let us first rewrite the separability assumption.

We assume that the function classes are compact. This, in conjunction with the extreme value theorem, it is ensured that the following minimizers exist: for , we define

for all pairs . For , we know that this minimizer is indeed . This comes directly from the realizibility assumption. Note that we require the existence of the minimizer (regression function) in order to use it for selecting actions in the contextual bandit framework (see [1])

Having defined the minimizers, we rewrite the separability assumption as following:

Assumption 3

For any , where , we have

Similar to [1], here, we are not worried about the explicit form of the regression functions . Rather, we assume the following performance guarantee of the offline regressor. For (meaning, the class containing the true regressor ), we have the following assumption.

Assumption 4

Given i.i.d data samples , the offline regression oracle returns a function , such that for , with probability at least ,

This assumption is taken from [1, Assumption 2]. As discussed in the above-mentioned paper, the quantity is a decreasing function of , e.g., . As an instance, consider the class of all linear regressors in . In that case, . For function classes with finite VC dimension (or related quantities like VC-sub graph or fat-shattering dimension; pseudo dimension in general, denoted by ), we have .

In this section, we consider:

The model-selection algorithm remains the same. For Option I, we explore for the first rounds. The first rounds are used to collect samples via pure exploration. Feeding this samples to the offline regression oracle, and focusing on the individual function classes separately, we obtain for all . Thereafter, we perform another round of pure exploration, and obtain fresh samples. Like in the finite case, we construct statistic for all .

For Option II, we collect all the samples from the previous epoch of the FALCON algorithm, split the samples, to obtain the regression estimate and similarly construct test statistic for all . In this setting, for the -th epoch, with model chosen as , we set the learning rate (similar to the FALCON algorithm of [1]) as

Similar to Algorithms 1 and 3, we choose the correct model based on a threshold on the test statistic (for Option II, it is ) and the threshold in phase is ( for Option II). We show that for all sufficiently large phase numbers, for all , , and for all , with high probability. Once this is shown, the model selection procedure follows exactly as Algorithm 1, i.e., we find the smallest index , for which . With high probability, we show that .

Regret Guarantee

We first show the guarantees for Option I, and Option II.

Theorem 3

Theorem 4

Remark 8 (Matching Oracle regret)

In both the settings, we match the regret of an oracle knowing the correct function class (see [1]). We pay a small additive price for model selection.

Remark 9

The proof of these theorems parallels exactly similar to the finite function class setting. The only difference is that instead of upper-bounding the prediction error using technical tools from [7], we use the the definition of to accomplish this.

VI Model Selection in Stochastic Linear Bandits

In the previous sections, we consider the problem of model selection for general contextual bandits. Moreover, we assumed that the function classes are separable, and leveraging that we have several provable model selection algorithms. In this section, we consider a special case of model selection for stochastic linear bandits. We observe that with this linear structure, assumption like separability across function classes is not required.

In the linear bandit settings, we consider different setup—(a) continuum (infinite) arm setting and (b) finite arm setting. We first start with the continuum arm setup.

VI-A Model Selection for Continuum (infinite) Arm Stochastic Linear bandits

VI-A1 Setup

We consider the standard stochastic linear bandit model in dimensions (see [22]), with the dimension as a measure of complexity. The setup comprises of a continuum collection of arms denoted by the set 666Our algorithm can be applied to any compact set , including the finite set as shown in Appendix X. Thus, the mean reward from any arm is , where . We assume that is sparse, where is apriori unknown to the algorithm. For each time , if an algorithm chooses an arm , the observed reward is denoted by , where is an i.i.d. sequence of mean sub-gaussian random variables with known parameter .

We consider a sequence of nested hypothesis classes, where each hypothesis class , models as a sparse vector. The goal of the forecaster is to minimize the regret, namely

where at any time , is the action recommended by an algorithm and . The regret measures the loss in reward of the forecaster with that of an oracle that knows and thus can compute at each time.

Note that, we assume that the true complexity (dimension) is initially unknown, and we seek algorithms that adapts to this unknown true dimension, rather than assume that the problem is dimensional. This is in contrast to both the standard linear bandit setup [3, 22], where there is no notion of complexity, as well as the line of work on sparse linear bandits [15], where the the true sparsity (dimension) is known, but only the set of which of the out of the coordinates is non-zero is unknown.

VI-A2 Algorithm: Adaptive Linear Bandits (Dimension) [ALB-Dim]

We present our adaptive scheme in Algorithm 4. The algorithm is parametrized by , which is given in Equation (1) in the sequel and slack . ALB-Dim proceeds in phases numbered which are non-decreasing with time. At the beginning of each phase, ALB-Dim makes an estimate of the set of non-zero coordinates of , which is kept fixed throughout the phase. Concretely, each phase is divided into two blocks:

-

1.

a regret minimization block lasting time slots777We have not optimized over the constants like and . Please refer to Remark 11 on this.,

-

2.

followed by a random exploration phase lasting time slots.

Thus, each phase lasts for a total of time slots. At the beginning of each phase , denotes the set of ‘active coordinates’, namely the estimate of the non-zero coordinates of . By notation, and at the start of phase , the algorithm assumes that is sparse. Subsequently, in the regret minimization block of phase , a fresh instance of OFUL [22] is spawned, with the dimensions restricted only to the set and probability parameter . In the random exploration phase, at each time, one of the possible arms from the set is played chosen uniformly and independently at random. At the end of each phase , ALB-Dim forms an estimate of , by solving a least squares problem using all the random exploration samples collected till the end of phase . The active coordinate set , is then the coordinates of with magnitude exceeding . The pseudo-code is provided in Algorithm 4, where, , in lines and is the total number of random-exploration samples in all phases upto and including .

VI-A3 Regret Guarantee

We first specify, how to set the input parameter , as function of . For any , denote by to be the random matrix with each row being a vector sampled uniformly and independently from the unit sphere in dimensions. Denote by , and by , to be the largest and smallest eigenvalues of . Observe that as is positive semi-definite () and almost-surely full rank, i.e., . The constant is the smallest integer such that

| (1) |

Remark 10

Theorem 5

In order to parse this result, we give the following corollary.

Corollary 1

Remark 11

The constants in the above Theorem are not optimized. The epoch length and the threshold parameter can be chosen more carefully. For example, if we set the epoch length as and the threshold as , we obtain a worse dependence on . Furthermore, the exponent of can be made arbitrarily close to , by setting in Line of Algorithm 4, for some appropriately large constant , and increasing , for appropriately large (.

Remark 12

In this special case of linear bandits, the separability condition boils down to , which comes with the problem setup automatically, since the complexity of the problem is the number of non-zero entries of the underlying true parameter .

Discussion - The regret of an oracle algorithm that knows the true complexity scales as [14, 15], matching ALB-Dim’s regret, upto an additive constant independent of time. ALB-Dim is the first algorithm to achieve such model selection guarantees. On the other hand, standard linear bandit algorithms such as OFUL achieve a regret scaling , which is much larger compared to that of ALB-Dim, especially when , and is a constant. Numerical simulations further confirms this deduction, thereby indicating that our improvements are fundamental and not from mathematical bounds. Corollary 1 also indicates that ALB-Dim has higher regret if is lower. A small value of makes it harder to distinguish a non-zero coordinate from a zero coordinate, which is reflected in the regret scaling. Nevertheless, this only affects the second order term as a constant, and the dominant scaling term only depends on the true complexity , and not on the underlying dimension . However, the regret guarantee is not uniform over all as it depends on . Obtaining regret rates matching the oracles and that hold uniformly over all is an interesting avenue of future work.

VI-B Dimension as a Measure of Complexity - Finite Armed Setting

VI-B1 Setup

In this section, we consider the model selection problem for the setting with finitely many arms in the framework studied in [10]. At each time , the forecaster is shown a context , where is some arbitrary ‘feature space’. The set of contexts are i.i.d. with , a probability distribution over that is known to the forecaster. Subsequently, the forecaster chooses an action , where the set are the possible actions chosen by the forecaster. The forecaster then receives a reward . Here is an i.i.d. sequence of mean sub-gaussian random variables with sub-gaussian parameter that is known to the forecaster. The function888Superscript will become clear shortly is a known feature map, and is an unknown vector. The goal of the forecaster is to minimize its regret, namely , where at any time , conditional on the context , . Thus, is a random variable as is random.

To describe the model selection, we consider a sequence of dimensions and an associated set of feature maps , where for any , , is a feature map embedding into dimensions. Moreover, these feature maps are nested, namely, for all , for all and , the first coordinates of equals . The forecaster is assumed to have knowledge of these feature maps. The unknown vector is such that its first coordinates are non-zero, while the rest are . The forecaster does not know the true dimension . If this were known, than standard contextual bandit algorithms such as LinUCB [3] can guarantee a regret scaling as . In this section, we provide an algorithm in which, even when the forecaster is unaware of , the regret scales as . However, this result is non uniform over all as, we will show, depends on the minimum non-zero coordinate value in .

Model Assumptions We will require some assumptions identical to the ones stated in [10]. Let , which is known to the forecaster. The distribution is assumed to be known to the forecaster. Associated with the distribution is a matrix (where ), where we assume its minimum eigen value is strictly positive. Further, we assume that, for all , the random variable (where is random) is a sub-gaussian random variable with (known) parameter .

VI-B2 ALB-Dim Algorithm

VI-B3 Regret Guarantee

For brevity, we only state the Corollary of our main Theorem (Theorem 6) which is stated in Appendix X.

Corollary 2

Discussion - Our regret scaling matches that of an oracle that knows the true problem complexity and thus obtains a regret of . This, thus improves on the rate compared to that obtained in [10], whose regret scaling is sub-optimal compared to the oracle. On the other hand however, our regret bound depends on and is thus not uniform over all , unlike [10] that is uniform over . Thus, in general, our results are not directly comparable to that of [10]. It is an interesting future work to close the gap and in particular, obtain the regret matching that of an oracle to hold uniformly over all .

VII Conclusion

In this paper, we address the problem of model selection for generic contextual bandits. We propose and analyze a meta algorithm, that takes any provable base algorithm as blackbox and performs model selection on top. Moreover, we also analyze a much simpler algorithm based on explore and commit for model selection. Our model selection schemes rely on realizibility and separability assumptions, and remove (or weaken) them is an immediate future work. We would also like to work on model selection problems for Reinforcement Learning problems. We keep these as our future endeavors.

Acknowledgements

The authors would like to acknowledge Akshay Krishnamurthy, Dylan Foster and Haipeng Luo for insightful comments and suggestions.

Appendix

VIII Model Selection for Contextual Bandits

VIII-A Proof of Lemma 1

Since, we have samples from pure exploration, let us first show that concentrates around its expectation. We show it via a simple application of the Hoeffdings inequality.

Fix a particular . Note that is computed based on the first set of samples. Also, in the testing phase, we again sample samples, and so is independent of the second set of samples, used in constructing . Note that since we have , we may restrict the offline regression oracle to search over functions having range . This implies that, we have . Note that this restricted search assumption is justified since our goal is obtain an estimate of the reward function via regression function, and this assumption also features in [1]. So the random variable is upper-bounded by , and hence sub-Gaussian with a constant parameter. Also, note that since we are choosing an action independent of the context, the random variables are independent. Hence using Hoeffdings inequality for sub-Gaussian random variables, we have

Re-writing the above, we obtain

| (2) |

with probability at least with samples.

Note that, the conditional variance of is finite, i.e., given , , for all . Let us define999We use the notation throughout the rest of the paper. . To be concrete depends on epoch and hence makes more sense. We omit the subscript for notational simplicity. With this new notation, let us first look at the expression .

Let us look at the expression .

Case I: Realizable Class

First consider the case that , meaning that . So, for this realizable setting, we obtain the excess risk as (using [7])

So, we have, for the realizable function class,

where is an absolute constant. The second term is obtained by setting the high probability slack, as into [7, Lemma 4.1]. So, we finally have from the preceeding display and Equation (2) that

| (3) |

with probability at least .

Case II: Non-realizable class

We now consider the case when , meaning that does not lie in . We have

where the third inequality follows from the fact that given context , the distribution of in independent of (see [7, Lemma 4.1]). Hence,

where the last inequality comes from the separability assumption along with the definition of . Since the regressor , we have

and hence

Choice of Threshold

Notice from Line of Algorithm 1, that the threshold for model selection is . Thus, if the event in Equations (6) holds, then the model selection stage will succeed in identifying the correct model class if the threshold satisfies

| (7) | ||||

The first item ensures that no-non realizable class will be selected as the true model, and the second item ensures that the smallest realizable class will be selected as the true model. Thus, if the time horizon satisfies

| (8) | |||

| (9) |

then the threshold satisfies the conditions in Equations (7). It is easy to verify that for

the conditions in Equations (9) holds. Thus, Equations (6), (7) and (9) yield that, if

with probability at-least , the model selection test in Line of Algorithm 1 correctly identifies the smallest model class containing the true model.

VIII-B Proof of Theorem 1

The regret can be decomposed in stages, namely exploration and exploitation.

Since we spend time steps in exploration, and , the regret incurred in this stage

Now, at the end of the explore stage, provided Assumptions 2 and 3, we know, with probability at least , we obtain the true function class . The threshold is set in such a way that we obtain the above result. Now, we would just commit to the function class and use the contextual bandit algorithm, . We have

which proves the theorem. In the special case, where = FALCON, the regret is [1]

with probability exceeding . Combining the above expressions yield the result.

VIII-C Proof of Lemma 2

Let us first show that concentrates around its expectation. We show it via a simple application of the Hoeffdings inequality.

Fix a particular and . Note that is computed based on samples. Also, in the testing phase, we use a fresh set of samples, and so is independent of the second set of samples, used in constructing . Note that since we have , we may restrict the offline regression oracle to search over functions having range . This implies that, we have . Note that this restricted search assumption is justified since our goal is obtain an estimate of the reward function via regression function, and this assumption also features in [1]. So the random variable is upper-bounded by , and hence sub-Gaussian with a constant parameter.

Note that we are using only the samples from the previous epoch. Note that in ACB, the regression estimate actually remains fixed over an entire epoch. Hence, conditioning on the filtration consisting of (context, action, reward) triplet upto the end of the -th epoch, the random variables (a total of samples) are independent. Note that similar argument is given in [1, Section 3.1] (the FALCON algorithm) to argue the independence of the (context, action, reward) triplet, accumulated over just the previous epoch.

Hence using Hoeffdings inequality for sub-Gaussian random variables, we have

Note that, the conditional variance of is finite, i.e., given , , for all . Recall that , and that depends on epoch . We omit the subscript for notational simplicity. With this new notation, let us first look at the expression .

Realizable classes

Fix and consider such that . So, for this realizable setting, we obtain the excess risk as:

So, we have, for the realizable function class,

Here, the first term comes from the second moment bound of , and the second term comes by setting the high probability slack as into [7, Lemma 4.1]101010Note that for model selection, we only require this concentration result which uses a form of Freedman’s inequality. In particular, we do not require the inverse gap weighting (IGW) randomization of FALCON. For any contextual bandit algorithm, that estimates the prediction function over multiple epochs, ACB can be employed for model selection. . So, by applying Hoeffding’s inequality, we finally have (using the bound ):

with probability at least . Since we have doubling epoch, we have

where is the number of epochs and is the time horizon. From above, we obtain . Using the bound, , note that, provided

| (10) |

we have for some absolute global constant , for any ,

| (11) |

with probability at least .

Non-Realizable classes:

For the non realizable classes, we have the following calculation. For any , where , we have

where the third inequality follows from the fact that given context , the distribution of in independent of (see [7, Lemma 4.1]).

So, we have

where the last inequality comes from the separability assumption along with the assumption on the second moment. Since the regressor , we have

Now, using samples, we obtain from Hoeffding’s inequality that

with probability at least . In particular, since , there is a global constant such that, for any ,

| (12) |

holds with probability at least .

In every phase , denote by the threshold , i.e., the Model Selection parameter in Line of Algorithm 3. Now, let be the smallest value of satisfying . We have from Equations (11) and (12) and a union bound over the classes that, with probability at-least , for all phases ,

The preceding display, along with the fact that the threshold , gives that, with probability at-least and all phases ,

The second inequality follows since , by definition of . The above equations guarantee that, with probability at-least , in all phases , the model selection procedure in Line of Algorithm 3, identifies the correct class .

VIII-D Proof of Theorem 2

The above calculation shows that as soon as

the model selection procedure will succeed with high probability. Until the above condition is satisfied, we do not have any handle on the regret and hence the regret in that phase will be linear. This corresponds the first term in the regret expression. Suppose be the epoch index where the conditions of Lemma 2 hold. Lemma 2 gives that the total number of rounds till the beginning of phase is upper bounded by , where hides global absolute constants. Then, the total regret is given by

with probability exceeding , where is the number of epochs. We have

which proves the theorem.

Now, let us focus on the case where FALCON is used as the base algorithm. For the epoch, with , the regret is given by we have (see [1]):

with probability at least . So, the total regret is given by

with probability at-least . Simplifying the summation, we get

considering the leading terms. Note that, with , the epoch length doubles with . Let the length of the -th epoch is . We have

and this completes the proof of the theorem.

VIII-E Proof of Theorem 3

Case I: Realizable Class

Consider . Using calculations similar to the finite cardinality setting, we obtain

where we use the definition of , as given in Assumption 4. Hence, invoking Hoeffding’s inequality, we obtain

with probability at least . We also have (from 2-sided Hoeffding’s)

Case II: Non-realizable Class

We now consider the setting where , meaning that does not lie in . In this case, similar to above, we have

and hence

Now, with the threshold, , provided

the model selection procedure succeeds with probability at least , where we do a calculation similar to the proof of Lemma 1.

After obtaining the correct model class, the regret expression comes directly from [1] in the infinite function class setting.

VIII-F Proof of Theorem 4

For the realizable classes, we have (from Assumption 4 and converting the conditional expectation to unconditional one with probability slack as , similar to the proof of Lemma 2),

and as a result

with probability at least .

Similarly, for non-realizable classes we obtain

with probability at least .

Now, suppose we choose the threshold . Finally, we say that provided

the model selection procedure succeeds with probability exceeding

The rest of the proof follows similarly to Theorem 2, and we omit the details here.

IX Model Selection for Linear Stochastic bandits

IX-A Proof of Theorem 5

We shall need the following lemma from [58], on the behaviour of linear regression estimates.

Lemma 3

If and satisfies , and is the least-squares estimate of , using the random samples for feature, where each feature is chosen uniformly and independently on the unit sphere in dimensions, then with probability , is well defined (the least squares regression has an unique solution). Furthermore,

We shall now apply the theorem as follows. Denote by to be the estimate of at the beginning of any phase , using all the samples from random explorations in all phases less than or equal to .

Lemma 4

Suppose is set according to Equation (1). Then, for all phases ,

| (13) |

where is the estimate of obtained by solving the least squares estimate using all random exploration samples until the beginning of phase .

Proof 1

The above lemma follows directly from Lemma 3. Lemma 3 gives that if is formed by solving the least squares estimate with at-least samples, then the guarantee in Equation (13) holds. However, as , we have naturally that . The proof is concluded if we show that at the beginning of phase , the total number of random explorations performed by the algorithm exceeds . Notice that at the beginning of any phase , the total number of random explorations that have been performed is

where the last inequality holds for all .

The following corollary follows from a straightforward union bound.

Corollary 3

Proof 2

This follows from a simple union bound as follows.

We are now ready to conclude the proof of Theorem 5.

Proof 3 (Proof of Theorem 5)

We know from Corollary 3, that with probability at-least , for all phases , we have . Call this event . Now, consider the phase . Now, when event holds, then for all phases , is the correct set of non-zero coordinates of . Thus, with probability at-least , the total regret upto time can be upper bounded as follows

| (14) |

The term denotes the regret of the OFUL algorithm [22], when run with parameters , such that , and denotes the probability slack and is the time horizon. Equation (14) follows, since the total number of phases is at-most . Standard result from [22] give us that, with probability at-least , we have

Thus, we know that with probability at-least , for all phases , the regret in the exploration phase satisfies

| (15) |

In particular, for all phases , with probability at-least , we have

| (16) |

where the constant captures all the terms that only depend on , and . We can write that constant as

X ALB-Dim for Stochastic Contextual Bandits with Finite Arms

X-A ALB-Dim Algorithm for the Finite Armed Case

The algorithm given in Algorithm 5 is identical to the earlier Algorithm 4, except in Line , this algorithm uses SupLinRel of [3] as opposed to OFUL used in the previous algorithm. In practice, one could also use LinUCB of [3] in place of SupLinRel. However, we choose to present the theoretical argument using SupLinRel, as unlike LinUCB, has an explicit closed form regret bound (see [3]). The pseudocode is provided in Algorithm 5.

In phase , the SupLinRel algorithm is instantiated with input parameter denoting the time horizon, slack parameter , dimension and feature scaling . We explain the role of these input parameters. The dimension ensures that SupLinRel plays from the restricted dimension . The feature scaling implies that when a context is presented to the algorithm, the set of feature vectors, each of which is dimensional are . The constant is chosen such that

Such a constant exists since are i.i.d. and is a sub-gaussian random variable with parameter , for all . Similar idea was used in [10].

X-B Regret Guarantee for Algorithm 5

In order to specify a regret guarantee, we will need to specify the value of . We do so as before. For any , denote by and to be the maximum and minimum eigen values of the following matrix: , where the expectation is with respect to which is an i.i.d. sequence with distribution . First, given the distribution of , one can (in principle) compute and for any . Furthermore, from the assumption on , for all . Choose to be the smallest integer such that

| (17) |

As before, it is easy to see that

Furthermore, following the same reasoning as in Lemmas 4 and 3, one can verify that for all , .

Theorem 6

In order to parse the above theorem, the following corollary is presented.

Corollary 4

Proof 4 (Proof of Theorem 6)

The proof proceeds identical to that of Theorem 5. Observe from Lemmas 3 and 4, that the choice of is such that for all phases , the estimate . Thus, from an union bound, we can conclude that

Thus at this stage, with probability at-least , the following events holds.

-

•

-

•

, for all .

Call these events as . As before, let be the smallest value of the non-zero coordinate of . Denote by the phase . Thus, under the event , for all phases , the dimension , i.e., the SupLinRel is run with the correct set of dimensions.

It thus remains to bound the error by summing over the phases, which is done identical to that in Theorem 5. With probability, at-least ,

where . This expression follows from Theorem in [59]. We now use this to bound each of the three terms in the display above. Notice from straightforward calculations that the first term is bounded by and the last term is bounded above by respectively. We now bound the middle term as

The first summation can be bounded as

and the second by

as

XI Numerical Experiments

In this section we will verify the theoretical findings. We concentrate on the linear contextual bandit setup. We compare ALB-Dim with the (non-adaptive) OFUL algorithm of [22] and an oracle that knows the problem complexity apriori. The oracle just runs OFUL with the known problem complexity. At each round of the learning algorithm, we sample the context vectors from a -dimensional standard Gaussian, . The additive noise to be zero-mean Gaussian random variable with variance .

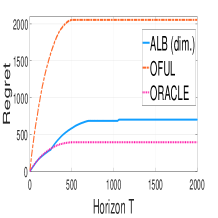

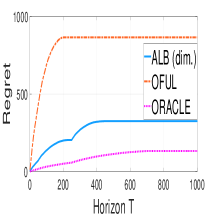

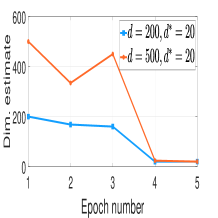

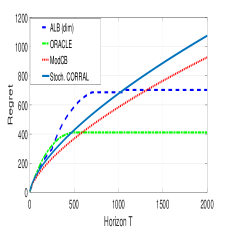

In panel (a)-(c), we compare the performance of ALB-Dim with OFUL ([22]) and an oracle who knows the true support of apriori. For computational ease, we set in simulations. We select to be -sparse, with the smallest non-zero component, . We have settings: (i) and (ii) . In panel (d) and (e), we observe a huge gap in cumulative regret between ALB-Dim and OFUL, thus showing the effectiveness of dimension adaptation. In panel (c), we plot the successive dimension refinement over epochs. We observe that within epochs, ALB-Dim finds the sparsity of .

Comparison of ALB (dim):

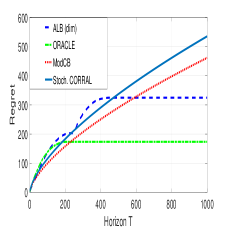

When is sparse, we compare ALB-Dim with baselines: (i) the ModCB algorithm of [10] (ii) the Stochastic Corral algorithm of [31] and (iii) an oracle which knows the support of . We select to be sparse, with dimension and . The smallest non-zero component of is . For ModCB, we use ILOVETOCONBANDITS algorithm, similar to [6]. We select the cardinality of action set as and select the sub-Gaussian parameter of the embedding as unity. In Figures 1(d) and 1(e), we observe that, the regret of ALB (dim) is better than ModCB and Stochastic Corral. The theoretical regret bound for ModCB scales as (which is much larger than the ALB-Dim algorithm we propose), and Figure 1(c), validates this. The Stochastic Corral algorithm treats the base algorithms as bandit arms (with bandit feedback), as opposed to ALB-Dim which, at each arm-pull, updates the information about all the base algorithms. Thus, (Figs , ), ALB-Dim has a superior performance compared to Stochastic Corral.

References

- [1] D. Simchi-Levi and Y. Xu, “Bypassing the monster: A faster and simpler optimal algorithm for contextual bandits under realizability,” 2020.

- [2] N. Cesa-Bianchi and G. Lugosi, Prediction, learning, and games. Cambridge university press, 2006.

- [3] W. Chu, L. Li, L. Reyzin, and R. Schapire, “Contextual bandits with linear payoff functions,” in Proceedings of the Fourteenth International Conference on Artificial Intelligence and Statistics, 2011, pp. 208–214.

- [4] T. Lattimore and C. Szepesvári, Bandit algorithms. Cambridge University Press, 2020.

- [5] A. Slivkins, “Introduction to multi-armed bandits,” arXiv preprint arXiv:1904.07272, 2019.

- [6] A. Agarwal, D. Hsu, S. Kale, J. Langford, L. Li, and R. Schapire, “Taming the monster: A fast and simple algorithm for contextual bandits,” in International Conference on Machine Learning. PMLR, 2014, pp. 1638–1646.

- [7] A. Agarwal, M. Dudík, S. Kale, J. Langford, and R. Schapire, “Contextual bandit learning with predictable rewards,” in Artificial Intelligence and Statistics. PMLR, 2012, pp. 19–26.

- [8] D. Foster and A. Rakhlin, “Beyond ucb: Optimal and efficient contextual bandits with regression oracles,” in International Conference on Machine Learning. PMLR, 2020, pp. 3199–3210.

- [9] A. Ghosh, A. Pananjady, A. Guntuboyina, and K. Ramchandran, “Max-affine regression: Parameter estimation for gaussian designs,” IEEE Transactions on Information Theory, vol. 68, no. 3, pp. 1851–1885, 2022.

- [10] D. J. Foster, A. Krishnamurthy, and H. Luo, “Model selection for contextual bandits,” in Advances in Neural Information Processing Systems, 2019, pp. 14 714–14 725.

- [11] T. V. Marinov and J. Zimmert, “The pareto frontier of model selection for general contextual bandits,” Advances in Neural Information Processing Systems, vol. 34, pp. 17 956–17 967, 2021.

- [12] D. J. Foster, A. Krishnamurthy, and H. Luo, “Open problem: Model selection for contextual bandits,” in Conference on Learning Theory. PMLR, 2020, pp. 3842–3846.

- [13] S. K. Krishnamurthy and S. Athey, “Optimal model selection in contextual bandits with many classes via offline oracles,” arXiv preprint arXiv:2106.06483, 2021.

- [14] A. Carpentier and R. Munos, “Bandit theory meets compressed sensing for high dimensional stochastic linear bandit,” in Artificial Intelligence and Statistics, 2012, pp. 190–198.

- [15] H. Bastani and M. Bayati, “Online decision making with high-dimensional covariates,” Operations Research, vol. 68, no. 1, pp. 276–294, 2020.

- [16] H.-T. Cheng, L. Koc, J. Harmsen, T. Shaked, T. Chandra, H. Aradhye, G. Anderson, G. Corrado, W. Chai, M. Ispir et al., “Wide & deep learning for recommender systems,” in Proceedings of the 1st workshop on deep learning for recommender systems, 2016, pp. 7–10.

- [17] H. Caselles-Dupré, F. Lesaint, and J. Royo-Letelier, “Word2vec applied to recommendation: Hyperparameters matter,” in Proceedings of the 12th ACM Conference on Recommender Systems, 2018, pp. 352–356.

- [18] J. McInerney, B. Lacker, S. Hansen, K. Higley, H. Bouchard, A. Gruson, and R. Mehrotra, “Explore, exploit, and explain: personalizing explainable recommendations with bandits,” in Proceedings of the 12th ACM conference on recommender systems, 2018, pp. 31–39.

- [19] K. Balog, F. Radlinski, and S. Arakelyan, “Transparent, scrutable and explainable user models for personalized recommendation,” in Proceedings of the 42nd International ACM SIGIR Conference on Research and Development in Information Retrieval, 2019, pp. 265–274.

- [20] N. S. Chatterji, V. Muthukumar, and P. L. Bartlett, “Osom: A simultaneously optimal algorithm for multi-armed and linear contextual bandits,” arXiv preprint arXiv:1905.10040, 2019.

- [21] A. Ghosh, A. Sankararaman, and R. Kannan, “Problem-complexity adaptive model selection for stochastic linear bandits,” in International Conference on Artificial Intelligence and Statistics. PMLR, 2021, pp. 1396–1404.

- [22] Y. Abbasi-Yadkori, D. Pál, and C. Szepesvári, “Improved algorithms for linear stochastic bandits,” in Advances in Neural Information Processing Systems, 2011, pp. 2312–2320.

- [23] G. Neu, “Explore no more: Improved high-probability regret bounds for non-stochastic bandits,” Advances in Neural Information Processing Systems, vol. 28, 2015.

- [24] H. Bastani, M. Bayati, and K. Khosravi, “Mostly exploration-free algorithms for contextual bandits,” Management Science, vol. 67, no. 3, pp. 1329–1349, 2021.

- [25] M.-h. Oh, G. Iyengar, and A. Zeevi, “Sparsity-agnostic lasso bandit,” arXiv preprint arXiv:2007.08477, 2020.

- [26] K. Ariu, K. Abe, and A. Proutière, “Thresholded lasso bandit,” arXiv preprint arXiv:2010.11994, 2020.

- [27] W. Li, A. Barik, and J. Honorio, “A simple unified framework for high dimensional bandit problems,” arXiv preprint arXiv:2102.09626, 2021.

- [28] A. Agarwal, H. Luo, B. Neyshabur, and R. E. Schapire, “Corralling a band of bandit algorithms,” in Conference on Learning Theory. PMLR, 2017, pp. 12–38.

- [29] R. Arora, T. V. Marinov, and M. Mohri, “Corralling stochastic bandit algorithms,” in International Conference on Artificial Intelligence and Statistics. PMLR, 2021, pp. 2116–2124.

- [30] A. Pacchiano, C. Dann, C. Gentile, and P. Bartlett, “Regret bound balancing and elimination for model selection in bandits and rl,” arXiv preprint arXiv:2012.13045, 2020.

- [31] A. Pacchiano, M. Phan, Y. Abbasi Yadkori, A. Rao, J. Zimmert, T. Lattimore, and C. Szepesvari, “Model selection in contextual stochastic bandit problems,” in Advances in Neural Information Processing Systems, H. Larochelle, M. Ranzato, R. Hadsell, M. F. Balcan, and H. Lin, Eds., vol. 33. Curran Associates, Inc., 2020, pp. 10 328–10 337.

- [32] J. Lee, A. Pacchiano, V. Muthukumar, W. Kong, and E. Brunskill, “Online model selection for reinforcement learning with function approximation,” in International Conference on Artificial Intelligence and Statistics. PMLR, 2021, pp. 3340–3348.

- [33] C.-Y. Wei and H. Luo, “Non-stationary reinforcement learning without prior knowledge: An optimal black-box approach,” in Conference on Learning Theory. PMLR, 2021, pp. 4300–4354.

- [34] C.-Y. Wei, C. Dann, and J. Zimmert, “A model selection approach for corruption robust reinforcement learning,” in International Conference on Algorithmic Learning Theory. PMLR, 2022, pp. 1043–1096.

- [35] A. Pacchiano, M. Phan, Y. Abbasi-Yadkori, A. Rao, J. Zimmert, T. Lattimore, and C. Szepesvari, “Model selection in contextual stochastic bandit problems,” arXiv preprint arXiv:2003.01704, 2020.

- [36] J. N. Lee, A. Pacchiano, V. Muthukumar, W. Kong, and E. Brunskill, “Online model selection for reinforcement learning with function approximation,” CoRR, vol. abs/2011.09750, 2020. [Online]. Available: https://arxiv.org/abs/2011.09750

- [37] E. Even-Dar, S. Mannor, and Y. Mansour, “Action elimination and stopping conditions for the multi-armed bandit and reinforcement learning problems,” Journal of Machine Learning Research, vol. 7, no. 39, pp. 1079–1105, 2006. [Online]. Available: http://jmlr.org/papers/v7/evendar06a.html

- [38] A. Locatelli and A. Carpentier, “Adaptivity to smoothness in x-armed bandits,” in Conference on Learning Theory, 2018, pp. 1463–1492.

- [39] A. Krishnamurthy, Z. S. Wu, and V. Syrgkanis, “Semiparametric contextual bandits,” arXiv preprint arXiv:1803.04204, 2018.

- [40] T. Lykouris, K. Sridharan, and É. Tardos, “Small-loss bounds for online learning with partial information,” arXiv preprint arXiv:1711.03639, 2017.

- [41] P. Auer, P. Gajane, and R. Ortner, “Adaptively tracking the best arm with an unknown number of distribution changes,” in European Workshop on Reinforcement Learning, vol. 14, 2018, p. 375.

- [42] H. Luo and R. E. Schapire, “Achieving all with no parameters: Adanormalhedge,” in Conference on Learning Theory, 2015, pp. 1286–1304.

- [43] B. McMahan and J. Abernethy, “Minimax optimal algorithms for unconstrained linear optimization,” in Advances in Neural Information Processing Systems, 2013, pp. 2724–2732.

- [44] F. Orabona, “Simultaneous model selection and optimization through parameter-free stochastic learning,” in Advances in Neural Information Processing Systems, 2014, pp. 1116–1124.

- [45] A. Cutkosky and K. Boahen, “Online learning without prior information,” arXiv preprint arXiv:1703.02629, 2017.

- [46] V. Vapnik, Estimation of dependences based on empirical data. Springer Science & Business Media, 2006.

- [47] L. Birgé, P. Massart et al., “Minimum contrast estimators on sieves: exponential bounds and rates of convergence,” Bernoulli, vol. 4, no. 3, pp. 329–375, 1998.

- [48] G. Lugosi, A. B. Nobel et al., “Adaptive model selection using empirical complexities,” The Annals of Statistics, vol. 27, no. 6, pp. 1830–1864, 1999.

- [49] S. Arlot, P. L. Bartlett et al., “Margin-adaptive model selection in statistical learning,” Bernoulli, vol. 17, no. 2, pp. 687–713, 2011.

- [50] V. Cherkassky, “Model complexity control and statistical learning theory,” Natural computing, vol. 1, no. 1, pp. 109–133, 2002.

- [51] L. Devroye, L. Györfi, and G. Lugosi, A probabilistic theory of pattern recognition. Springer Science & Business Media, 2013, vol. 31.

- [52] Y. Lu and H. H. Zhou, “Statistical and computational guarantees of lloyd’s algorithm and its variants,” arXiv preprint arXiv:1612.02099, 2016.

- [53] J. Kwon and C. Caramanis, “The em algorithm gives sample-optimality for learning mixtures of well-separated gaussians,” in Conference on Learning Theory. PMLR, 2020, pp. 2425–2487.

- [54] S. Balakrishnan, M. J. Wainwright, B. Yu et al., “Statistical guarantees for the em algorithm: From population to sample-based analysis,” Annals of Statistics, vol. 45, no. 1, pp. 77–120, 2017.

- [55] X. Yi, C. Caramanis, and S. Sanghavi, “Solving a mixture of many random linear equations by tensor decomposition and alternating minimization,” CoRR, vol. abs/1608.05749, 2016. [Online]. Available: http://arxiv.org/abs/1608.05749

- [56] D. Foster and A. Rakhlin, “Beyond UCB: Optimal and efficient contextual bandits with regression oracles,” in Proceedings of the 37th International Conference on Machine Learning, ser. Proceedings of Machine Learning Research, H. D. III and A. Singh, Eds., vol. 119. PMLR, 13–18 Jul 2020, pp. 3199–3210. [Online]. Available: http://proceedings.mlr.press/v119/foster20a.html

- [57] R. Sen, A. Rakhlin, L. Ying, R. Kidambi, D. Foster, D. Hill, and I. Dhillon, “Top- extreme contextual bandits with arm hierarchy,” arXiv preprint arXiv:2102.07800, 2021.

- [58] M. Krikheli and A. Leshem, “Finite sample performance of linear least squares estimators under sub-gaussian martingale difference noise,” in 2018 IEEE International Conference on Acoustics, Speech and Signal Processing (ICASSP). IEEE, 2018, pp. 4444–4448.

- [59] P. Auer, “Using confidence bounds for exploitation-exploration trade-offs,” Journal of Machine Learning Research, vol. 3, no. Nov, pp. 397–422, 2002.

| Avishek Ghosh (Ph.D UC Berkeley, 2021) is an Assistant Professor at the department of Systems and Control Engg. and The Centre for Machine Intelligence and Data Science at IIT Bombay. Previously, he was an HDSI (Data Science) Post-doctoral fellow at the University of California, San Diego. Prior to this, he completed my PhD from the Electrical Engg. and Computer Sciences (EECS) department of UC Berkeley, advised by Prof. Kannan Ramchandran and Prof. Aditya Guntuboyina. His research interests are broadly in Theoretical Machine Learning, including Federated Learning and multi-agent Reinforcement/Bandit Learning. In particular, Avishek is interested in theoretically understanding challenges in multi-agent systems, and competition/collaboration across agents. Before coming to Berkeley, Avishek completed his masters degree from Indian Institute of Science (IISc), Bangalore (at the Electrical Communication Engg. Dept) and prior Avishek completed his bachelors degree from Jadavpur University, in the dept. of Electronics and Telecommunication Engineering. |