Empirical Framework for Cournot Oligopoly with Private Information††thanks: We thank the editor Allan Collard-Wexler and three referees for numerous helpful suggestions that substantially improved the paper. We also thank Victor Aguirregabiria, María F. Gabrielli, Mitsuru Igami, Sung Jae Jun, Lidia Kosenkova, and Nicholas Vreugdenhil for their thoughtful comments. We are also thankful to seminar and conference participants, at the 14th GNYMA Econometrics Colloquium, 7th Alumni Conference at Universidad de San Andrés, 2018 NASM, Universidad Torcuato Di Tella, 2019 Triangle Econometrics Conference at Duke University, 2019 SEA, DC-MD-VA Econometrics Workshop 2020, UBC Econometrics Brownbag, and 2022 IIOC, for their comments.

Abstract

We propose an empirical framework for asymmetric Cournot oligopoly with private information about variable costs. First, considering a linear demand for a homogenous product with a random intercept, we characterize the Bayesian Cournot-Nash equilibrium. Then we establish the identification of the joint distribution of demand and firm-specific cost distributions. Following the identification steps, we propose a likelihood-based estimation method and apply it to the global market for crude-oil and quantify the welfare effect of private information.

We also consider extensions of the model to include product differentiation, conduct parameters, nonlinear demand, or selective entry.

JEL classification: C57, D22, D43, L13.

Keywords: Cournot Oligopoly, Private Information, Variable Costs, Identification, Crude-oil.

1 Introduction

Competition among firms is necessary for a vibrant economy, but several factors may afford market power to firms that lower competition. One such factor is their private information (e.g., Bergemann, Heumann, and Morris, 2019) about their production costs. Private information is also central for limit pricing and predation (Milgrom and Roberts, 1982a, b), collusion (Roberts, 1985), coordination (Aryal, Ciliberto, and Leyden, Forthcoming). Most empirical articles that study market power and estimate the associated welfare assume complete information and focus on getting the strategic aspect right. However, Vives (2002) shows that ignoring private information can generate a more significant error in our welfare calculation than if we had modeled the private information correctly but gotten the strategic aspect wrong. His results suggest that firms’ mutual information about each others’ costs has a more fundamental effect on welfare estimates than is typically appreciated.

Several important articles, e.g., Seim (2006); Aradillas-López (2010); de Paula and Tang (2012) and Grieco (2014), study different aspects of oligopolistic competition with private information. They, however, focus on environments with discrete actions where the source of private information is an additive “error term” in the profit function. Instead, we consider a continuous game where private information is about firms’ (possibly correlated) total variable costs. Modeling private information from the “ground up” allows us to capture the nonlinear effect of private information on firms’ profits and the resulting market efficiency and to provide an economic interpretation for the source of inefficiencies. For instance, in the Cournot oligopoly with homogenous goods that we consider here, complete cost information increases efficiency because only the most efficient firms produce, but the markup may rise with fewer firms. Using our method, one can determine which factor dominates.

Our main contribution is to develop an empirical framework for asymmetric Cournot competition with private information about their costs. To this end, we build on Vives (2002) and consider a market for a homogenous product with linear and stochastic demand, where firms are asymmetric and have private information about their marginal costs. Also, we allow for a common but unobserved (to the econometrician) market-level technology shock that shifts and induces correlation across firms’ costs.

We characterize the Bayesian Cournot-Nash equilibrium for this game and propose a constructive strategy to identify the model parameters assuming that the observed quantities and prices are equilibrium outcomes of the game. Our identification strategy uses the results that the equilibrium strategies are linear and strictly decreasing in their own cost and that demand and costs shocks are exogenous (“shifters”) independent and identically distributed across markets.

In particular, we show that the variation in observed prices and outputs identifies the demand parameters and that the variation in firms’ outputs and the monotonicity of the equilibrium strategies identify the cost distributions. Then we show that the joint variation in firms’ outputs identifies the unobserved (common) technology shock distribution.

Our identification strategy borrows some insights from the empirical literature on Bayesian games. For instance, in empirical auctions with independent private values, strict monotonicity of bidding strategies plays a central role in the identification; see, for example, Guerre, Perrigne, and Vuong (2000). See Einav and Nevo (2006), who provide the link between the classic demand and pricing literature and empirical auctions.111We also discuss how we can view our identification problem as classic identification of simultaneous equations system that determines demand and supply. Similarly, our idea of using joint variation in firms’ outputs to identify the distribution of the common technology shock is akin to the identification strategy in Krasnokutskaya (2011) for auctions with unobserved heterogeneity.

To illustrate our method, we study the monthly global market for crude-oil. We consider 20 major crude-oil-producing countries from January 1992 to December 2019. In this environment, variable costs comprise rental rates for drilling rigs, prices for steel, site preparation costs, construction costs, capital costs, and general equipment rental costs averaged across all oil fields.222While some of these costs (e.g., steel prices) may be commonly known, others (e.g., rental rates, equipment rental, and capital costs) are likely to be private information. Thus, treating the variable costs as countries’ private information is reasonable. Although we propose a semi-nonparametric identification strategy, given our small sample size (of 336 months), we make distributional assumptions and propose a maximum likelihood estimation procedure to ensure good finite-sample performance.

In our empirical exercise, we treat each oil-producing country as if it is a competitive firm in our model. This assumption is consistent with the fact that in most oil-producing countries, production decisions are centralized, and state-run companies exploit the reserves.333An exception is the U.S., where production is decentralized. We also consider an extension with conduct parameters that allows price-taking firms as a special case. However, given that we only observe the total U.S. production and our focus is on methodology, we treat the U.S. as one firm. In such cases, the estimated variable costs are an aggregate measure of costs from several oil reserves within each country. In that regard, our application is closer to Carvajal, Deb, Fenske, and Quah (2013) than to Asker, Collard-Wexler, and Loecker (2019), where the latter provides a detailed empirical analysis of the effect of heterogeneity across oil fields, within and across countries, on total efficiency. Using counterfactual exercise, we quantify the welfare effect of private information. In particular, we estimate the deadweight loss under private information at 16.3% higher than under complete information.

We also consider extensions of our model in four directions and study their identification. First, we consider differentiated products, and second, the possibility that firms do not play the (static) Bayesian Nash-Cournot equilibrium; instead, they play a conjectural variation equilibrium by allowing the firms to have different conduct parameters. Third, we consider a nonlinear demand function. Fourth, we consider Cournot oligopoly with a selective entry, where firms are symmetric and observe a signal about their cost, make a costly entry decision, and then choose their outputs after entering.

Our article contributes to several strands of research in industrial organization. First, it is related to the literature (Vives, 1984, 2002) that studies the role of private information in Cournot competition. Second, in terms of our empirical application, we complement Rosen (2006) who also studies the identification of marginal costs under incomplete information. Third, our article is also related to the literature that estimates games with private information, such as Seim (2006), Sweeting (2009), and Grieco (2014). We complement this research, but in contrast, we model the source of private information (about cost) and use it to determine the expected payoff structure, resulting in a nonseparable model that requires a new approach to identify the cost parameters. Our empirical approach is similar in spirit to Sweeting, Roberts, and Gedge (2020), where costs are firms’ private information.

We also contribute to a large and varied literature on the crude-oil industry (see, e.g., Durand-Lasserve and Pierru, 2021) by introducing private information. In so far as the oil extraction decisions involve inter-temporal tradeoffs (Hotelling, 1931; Cremer and Weitzman, 1976; Loury, 1986), our estimate of the size of private information misses these tradeoffs. Consequently, our estimate also does not incorporate any adverse effects of future oil price uncertainty on oil production (Kellogg, 2014).

While our empirical application considers the crude-oil market, our framework applies more broadly and can be used to study other industries characterized by asymmetric Cournot competition. Some of these industries may include the lysine market (de Roos, 2006), the Portland cement industry (Ryan, 2012), the ready-mix concrete industry (Hortaçsu and Syverson, 2007; Collard-Wexler, 2013), and the coffee bean market (Igami, 2015).

The rest of our paper proceeds as follows. Sections 2 and 3 describe our model and the identification strategies, respectively. Section 4 describes the data. Sections 5 provides the estimation procedure and Monte Carlo simulations. Section 6 reports our empirical findings followed by a discussion of the model and the estimates in Section 7. Section 8 concludes. The proofs of all the results stated in the main text are relegated to Appendix A, and additional estimation results to Appendix B.

In Supplementary Appendix S, we consider four extensions of our baseline model: (i) differentiated Cournot competition; (ii) possibility that firms do not play Bayesian Cournot-Nash equilibrium by allowing them to have different conduct parameters; (iii) homogenous Cournot competition with nonlinear demand; and (iv) homogenous Cournot competition with a selective entry. For each, we discuss how our empirical strategy extends to that case.

Notation. All vectors and their concatenation with a comma are column vectors. We use boldface to denote vectors (or random vectors) and regular letters for scalars (or random variables). For generic random variables , and denote their joint cumulative distribution function (CDF) and probability density function (PDF), respectively. Further, , and denote the conditional CDF, conditional mean and conditional quantile function of given , respectively. We use for the unconditional mean and write when and are independent. We also employ the same notation for random vectors. For example, if and are random vectors each with dimension , denotes the joint CDF of the random vector . Finally, for a given vector , we write , , and . We use for a vector of ones, and for the - identity matrix.

2 Model

In this section, we present our model of Cournot oligopoly with homogeneous goods where asymmetric firms have private information about their variable costs. To this end, we extend Vives (2002) to allow for stochastic demand and a common technology shock, and then we characterize the equilibrium strategies.

Let there be markets, and in each market , let there be consumers. Each consumer , has quasi-linear preferences for an homogeneous good and in market , maximizes the net benefit function

| (1) |

where is the quantity consumed by , is the per-unit price of the product, is a (one-dimensional) demand shock that affects the consumer’s willingness to pay, and is a common utility parameter. A consumer in market takes the market price as given and chooses quantity consumed according to . Then summing the demand over consumers in market gives the inverse demand function

| (2) |

where is the total consumption and is the demand parameter.

On the supply side, let there be firms in each market that compete in quantities. And let denote the set of firms. We begin by assuming that firms are heterogeneous in their production costs. For , let denote firm ’s inefficiency parameter (or simply, firm ’s private cost) in market , and we assume that is firm ’s private information. Furthermore, we allow ’s variable cost in market to depend on ’s private cost and a cost shock common across all firms.

In particular, let ’s total variable cost of producing in market be

| (3) |

where is a cost parameter and is ’s total variable cost. Thus, firms with higher are less efficient, and have higher marginal costs, than firms with lower .

Letting , hereafter, we assume that are random vectors that satisfy the following assumption. Let and be random vectors representing the private cost shocks and the common demand and technology shocks, respectively. We begin with the following modeling assumptions.

Assumption 1.

The random vectors are IID as . Further, the distribution satisfies the next conditions.

-

(i)

The firms’ types and the common shocks are independent, i.e., . Also, the firm-specific cost shocks are mutually independent.

-

(ii)

For each , has support given by with . It also admits a PDF that is strictly positive and continuously differentiable on .

-

(iii)

The random vector has rectangular support given by with . It also admits a joint PDF that is strictly positive and continuously differentiable on .

We remark that even though Assumption 1-(i) implies that for any two firms , the total variable costs can be correlated across firms because of . We can interpret as an unobserved technology shock that shifts production costs for all the firms. Henceforth, we refer to as firm ’s private cost shock and as the common cost shock observed by all the firms. Furthermore, throughout this section, we allow the common cost shock and the demand shock to be correlated.

We have made several assumptions about the supports in light of our empirical application and model tractability. First, we assume that the demand shock has a positive lower bound, , a reasonable assumption because in Equation (1) would imply a zero demand with positive probability. Second, we follow the extant literature on games with incomplete information and assume that and have bounded support. These assumptions, together with Assumption 2 defined shortly below, ensure that firms’ ex-ante expected profit is finite and that private costs, equilibrium outputs, and market-clearing prices are nonnegative.

Thus, we can allow the upper bounds to be unbounded, as long as the private cost distribution is such that the ex-ante expected profit is finite. However, if firms’ costs are unbounded from above, firms probably will not produce anything; however, we do not observe zero production in our sample.

In the rest of this section, we present the timing of the game and derive the equilibrium strategies for which we assume that (i) the market-clearing condition holds in each market, i.e., aggregate consumption equals total output, (ii) there is no fixed cost of production, and (iii) the joint distribution is common knowledge among all firms.

Specifically, in market , nature draws and each firm observes its private cost , as well as . Then all firms simultaneously choose their outputs, and the market clears. We consider static Bayesian Cournot-Nash equilibria in pure strategies for each market. The common shocks are observed by all the firms, so they can be treated as commonly known constants when choosing the (expected) profit-maximizing output. For a given and given strategies of the opponents , where , firm chooses its quantity that maximizes its expected profit:

| (4) |

where is the total quantities produced by ’s opponents, and the expectation is with respect to ’s interim belief about its opponents’ costs is distributed as . Then the equilibrium strategy must satisfy the following first-order condition:

| (5) | |||||

where the second equality follows from Assumption 1. Thus, the equilibrium strategies are linear in private costs. We impose additional assumptions on the parameters and their supports to guarantee a unique solution with nonnegative quantities and a market-clearing price.

Assumption 2.

We have that , , and

Furthermore,

The first part of Assumption 2 is a technical requirement that ensures a nonnegative market-clearing price; see Einy, Haimanko, Moreno, and Shitovitz (2010) and Hurkens (2014) for a detailed discussion on this topic. The second part ensures that it is always profitable for every firm to produce. In particular, it implies that even when firm realizes the highest cost and demand is the lowest, it is still profitable for such a firm to choose nonnegative output. Note that Assumption 2 is automatically satisfied, e.g., when is sufficiently large in comparison with the upper boundaries . Alternatively, these boundaries can be arbitrarily large if we allow to be sufficiently large.

The following lemma, which builds on Vives (2002, Proposition 1), establishes the existence and uniqueness of the Bayesian Cournot-Nash equilibrium in strictly increasing strategies. The proof of the lemma is in Appendix A.

Lemma 1.

This lemma states that the equilibrium strategy for a firm is linear and strictly decreasing in its private cost. Each firm responds to the average cost type of its opponent, so the equilibrium may not be Pareto efficient because some firms may produce more than the socially optimal quantities. Finally, we remark that if the parameters and the shocks are scaled by some constant , then the equilibrium quantities will not be affected, but the new equilibrium price will be . Thus the observed price and quantities cannot be rationalized by two sets of structural parameters if one of them is a scaled version of the other, aiding in the identification as we study next.

3 Identification

In this section, we study the identification of our model and propose a constructive multi-step identification strategy. More specifically, we determine conditions on our model and the data under which we can use the joint CDF of the equilibrium prices and quantities , where , , for , and to uniquely determine all the model parameters. Recall that our model parameters are (i) the slope of the demand function, , (ii) the marginal CDF of the demand shock , (ii) the parameter of the cost function, , (iii) marginal distributions of private costs, , and (iv) the conditional CDF of the technological shock given , . Even though we do not know , in practice, we can consistently estimate it from the observables as , where is the market-clearing price in market , , , and is the output produced by the firms in market . Thus, the data can be interpreted as realizations of our Bayesian Cournot-Nash model over many markets.

To simplify the exposition hereafter, we do not consider additional exogenous features that can affect the costs or the demand, even though we can accommodate such features as follows. Let be observed firms’ characteristics that affect private costs and that are common knowledge among firms. We can then model for each , as well as , and build our identification strategy from the conditional distribution . Similarly, we can accommodate demand shifters such as income and demographic characteristics. To determine the limits of our identification strategy from relying solely on the game-theoretic structure, we do not consider observed firms’ characteristics in the remainder of this paper.

Before presenting the formal identification results, for intuition, we sketch the idea and discuss the identifying variations for a simplified case when there are two symmetric firms with . The market demand in period , denoted as in (2), is

| (6) |

where can be interpreted as an exogenous demand shifter. On the supply side, firm ’s first-order conditions can be written as

| (7) |

where from Lemma 1 we know . Thus, the average depends on both and because the firms observe them before they choose their productions. To express the market supply , where the superscript denotes total supply, as a function of the price and the supply shocks , we substitute in (7) and sum over the two firms, which gives us

| (8) |

Equations (6) and (8) simultaneously determine the equilibrium price and quantity under the equilibrium condition . If it is written this way, we can interpret as an exogenous demand shifter and as exogenous supply shifters, which are crucial for the identification. To wit, if we condition on being at the lowest, , the strict monotonicity of the equilibrium strategy implies that . Thus conditioning on , we can see that in Equations (6)-(8) under the equilibrium condition , and are pinned down by . Thus, as varies across , and vary, which in turn identifies the demand slope . Once we know , we can identify the demand shock (i.e., the intercept) from (6).

Next, focusing on each firm separately, we can use the fact that output decreases with its costs. If we ignore , this monotonicity of the equilibrium allows us to use the distribution of production to identify the distribution of private costs. But with , we identify the distribution of . To separately identify the distribution of from , we use a deconvolution method exploiting the fact that is common across firms.

Before we proceed, we make the following normalization assumption, important for the identification.

Assumption 3.

Both and have zero mean, i.e., and .

Assumption 3 is a technical assumption that is helpful in the identification as it is a location normalization. Essentially, is a normalization that allows us to identify the means of the private cost shocks , while is similar to the exogeneity assumption used in nonlinear models. Clearly, and imply that and must be uncorrelated.

Demand Parameters

We begin with identifying and the marginal CDF . For this purpose, consider firm and the range of its output , which is given by with (Lemma A.1). This interval can be identified from , as the support of . Strict monotonicity of the equilibrium strategy (Lemma 1) implies that ’s smallest output is associated with its highest cost and the smallest demand shock, i.e., . In other words, the event is equivalent to .

Now consider the total output of firm ’s competitors, . From Lemma A.1, we know that is continuous and is supported on . Moreover, its density is strictly positive in the interior of this set, which implies that the conditional quantile function is a well-defined and strictly increasing function. Thus, for any two distinct , from the inverse demand function (2) we obtain

So the slope parameter can be identified by subtracting the first equation from the second:

| (9) |

Note that implies and , so the denominator on the RHS of (9) is nonzero and is well defined. Heuristically, the slope of the demand function is identified by the “derivative” of the inverse demand function with respect to the equilibrium quantities produced by the other firms while holding at . The choice of and the quantiles were arbitrary, suggesting that is over-identified. Once is identified, we can recover the demand shock as and identify its CDF as for .

Cost Parameter

Next, we consider identifying the common cost parameter . In particular, we can use the variation in the output produced that can be explained by variation in across markets to identify . A high value of means the marginal cost is increasing, so even if the demand increases because increases, in equilibrium firm ’s output does respond, and vice versa. To formalize this intuition, for , let

Then, after substituting and in firm ’s equilibrium strategy (Lemma 1), we obtain the following linear expression:

| (10) |

Assumption 1 implies that , which in turn implies that the “regressor” and the “error” satisfy the orthogonality condition that allows us to identify the slope as

| (11) |

which in turn identifies the .

Distributions of Cost Shocks

In this subsection, we focus on identifying the marginal CDFs of the private cost shocks, i.e., , and the joint distribution of common shocks . Here, our identification strategy relies on the variation in firms’ output, and the equilibrium strategies are linear and strictly decrease private costs.

The intuition behind our identification approach is that all else equal, firms with higher costs choose lower quantities than firms with lower costs. So, for any two firms , if we hold firm ’s output fixed at its lowest level, , the conditional quantile of ’s output, , can be expressed as a linear function of the quantile function of because implies , while the distribution of is unaffected by independence. Then the variation in the conditional quantiles of identifies and hence .

Next, if we keep fixed, is a linear combination of the firm-specific shock and the common-cost shock . Then, once we identify , we can identify the characteristic function of using a deconvolution method, which uniquely identifies the CDF because there is a one-to-one correspondence between a CDF and a characteristic function. In the remainder of this section, we formalize these arguments.

We begin by identifying the means . After applying the law of iterated expectations to the equilibrium first-order condition (5), for any , we obtain

| (12) |

where all the parameters on the right-hand side are known or have been identified.

We are ready to state the following result that shows how we can use to identify the distributions mentioned above nonparametrically. Let denote the conditional characteristic function of given , i.e., , where and denotes the imaginary unit.

Theorem 1.

-

1.

Then, for any , is identified from the conditional distribution as

(13) -

2.

For any , we can identify the conditional characteristic function of given as

(14) which in turn identifies by uniqueness of the characteristic function.

The first part of this theorem provides a closed-form expression for in terms of , and . Our identification strategy relies essentially on the linearity and strict monotonicity of the equilibrium strategies and the independence between and . Here, note that the distribution is over-identified because when , for each , there is more than one .

The second part of Theorem 1 provides an expression for the conditional characteristic function associated with . We derive this expression from the equality

| (15) |

that follows by Lemma 1. Observe that the left-hand side is observable at this step of the identification process, while the first term on the right hand is unobservable, but its distribution is known. Thus, the distribution of can be recovered by applying deconvolution techniques usually employed in panel data, and error components models (see, e.g., Horowitz and Markatou, 1996). We note that if firms were symmetric, (15) could also be used to identify as an alternative to the first part of this theorem.

The deconvolution method identifies conditional characteristic function as a function of the data and . There is a one-to-one mapping between the conditional characteristic function and the conditional CDF, identifying ; indeed, is overidentified as in (14) is arbitrary. Formally, if the conditional PDF satisfies the regularity conditions in Shephard (1991, Theorem 3), then , we obtain

Heuristically, given , the unobserved common technological shock generates dependence between quantities produced in the same market. We can use this dependence to recover . In particular, the marginal distributions of ’s are insufficient to identify the conditional CDF because there is no unique decomposition of the sum into its common and individual components and . Finally, we can identify the joint CDF of at as

4 Data

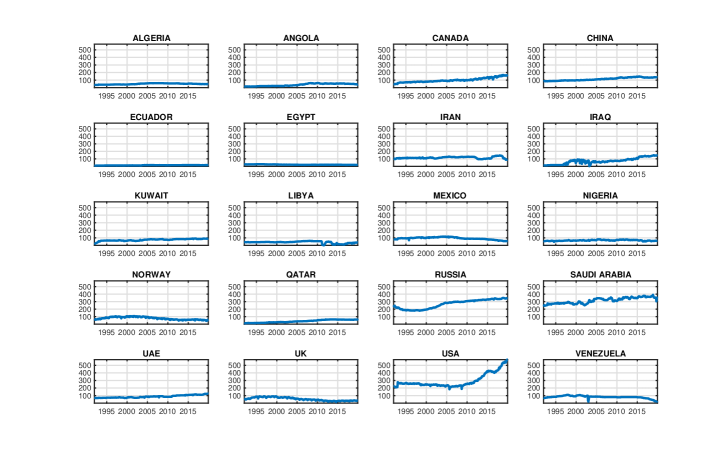

For our application, we consider the global market for crude-oil from January 1992 to December 2019. Besides being an important industry globally, crude-oil is a homogeneous product where producers compete in quantities, making it an appropriate application. The production data are available from the Monthly Energy Review published by the U.S. Energy Information Administration.444The Monthly Energy Review is available from this website https://rb.gy/rygmcz. We observe the monthly productions of 20 major oil-producing countries. We treat each country as a competing firm.

Figure 1 displays time series of monthly output data (measured in millions of barrels), while Table 1 reports summary statistics. As we can observe, all countries produce strictly positive output each month, which is consistent with the second part of Assumption 2. We may observe zero production if we consider production over a shorter period. We also see that countries differ in their productions, from Ecuador, Egypt, and Libya at the lowest end of production to Russia, Saudi Arabia, and the U.S. at the highest. These differences suggest cost asymmetry. Furthermore, the productions have a time trend, so we de-trend them first.

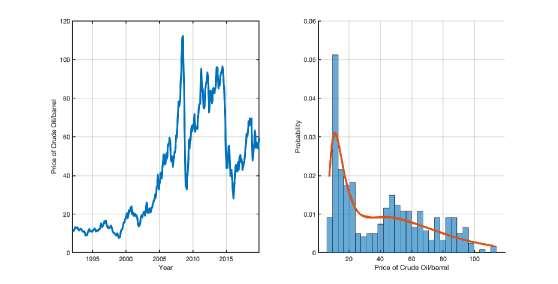

We also observe oil prices (per barrel) published by the St. Louis Federal Reserve. Figure 2 shows the time series and histogram of these prices, expressed in 2019:Q4 U.S. dollars. The prices range from $7.57 to $112.24, with a mean of $41.43 and a standard deviation of $27.71.

| Countries | Min | Mean | Std. Dev. | Max |

|---|---|---|---|---|

| Algeria | 35.85 | 49.32 | 7.2 | 59.85 |

| Angola | 14.49 | 37.8 | 15.83 | 61.5 |

| Canada | 45.51 | 99.3 | 28.69 | 171.3 |

| China | 83.76 | 113.78 | 19.25 | 149 |

| Ecuador | 8.91 | 13.963 | 2.3 | 17.1 |

| Egypt | 18.6 | 22.79 | 2.9 | 28.53 |

| Iran | 87.39 | 115.51 | 12.11 | 144.84 |

| Iraq | 1.89 | 71.43 | 38.86 | 148.98 |

| Kuwait | 17.43 | 72.88 | 12.91 | 91.26 |

| Libya | 0.6 | 40.5 | 13.5 | 59.91 |

| Mexico | 55.23 | 92.69 | 15.46 | 116.88 |

| Nigeria | 46.35 | 65.99 | 6.53 | 80.85 |

| Norway | 41.9 | 77 | 17.72 | 107.37 |

| Qatar | 9.75 | 38.4 | 17.59 | 61.92 |

| Russia | 177.8 | 266.84 | 58.62 | 349.83 |

| Saudi Arabia | 243.27 | 314.94 | 38.65 | 390.5 |

| U.A.E | 66.51 | 87.66 | 16.22 | 126.27 |

| U.K. | 16.02 | 54.64 | 21.64 | 91.8 |

| U.S.A. | 183.39 | 293.82 | 91.23 | 575.91 |

| Venezuela | 20.4 | 80.6 | 16.8 | 110.13 |

5 Estimation

In this section, we propose a MLE procedure based on observed prices and quantities . Although our identification is semi-nonparametric, we make parametric assumptions due to our sample size. In particular, we assume that the distributions of and the private costs belong to certain parametric families. Moreover, to capture the time-series nature of our data, we also allow time trends in and , . Finally, in Subsection 5 below, we provide a Monte Carlo experiment to evaluate the finite-sample performance of the proposed estimators.

We begin with the following assumption that will allow us to de-trend .

Assumption 4.

-

(i)

For each , can be expressed as where are parameters and are IID.

-

(ii)

The demand shock can be expressed as , where are parameters and is strictly stationary and ergodic.

-

(iii)

The parameters satisfy the relationship .

-

(iv)

The technology shock process is strictly stationary and ergodic.

Assumptions 4-(i) and 4-(ii) impose an additively separable time trend. Additive separability can be restrictive, but these assumptions enable us to keep the model tractable. In particular, they will allow us to express the equilibrium outputs as an additively separable function of time-trend; see Equation (25) below. Assumption 4-(iii) implies that the prices do not have a time trend; more specifically, that is strictly stationary and ergodic. In our empirical application, captures the temporary or transient cost shock facing , and the time-series components capture some persistent shocks.

By applying Assumption 4 to demand equation (2) and to the equilibrium outputs from Lemma 1, the equilibrium price and quantities can be written as

| (20) | |||||

| (25) |

where , is a vector containing the means of the de-trended private-costs, is a matrix of the form

where is a vector of ones, denotes the identity matrix of dimension , and is a vector whose element is given by

and the first element is given by .

Next, we make the following assumptions about the distribution of . However, before that, we introduce a few new notations. Let denote a truncated normal random variable. With a slight abuse of notation, for given constants , we write to denote that has the same distribution as , where stands for a Beta random variable with parameters .

Assumption 5.

-

(i)

Demand Shock: Let on with .

-

(ii)

Technology Shock: Let where and .

-

(iii)

Private Costs: For , let where and .

Thus we assume that the cost distributions belong to the Beta family. Beta densities are versatile and are widely used to model many types of uncertainties, because it can be unimodal, increasing, decreasing, or constant depending on the values of the parameters; see Johnson, Kotz, and Balakrishnan (1994). From Assumption 5-(ii), it follows that the common cost shock is supported on , so it can be negative with range. In contrast, the total de-trended marginal cost, , has support with mean . In this parametric framework, the model parameters are

To construct the estimator of , the first step is to estimate and by nonlinear least squares. Specifically, letting be a vector of constants, we set . Then let be the vector of de-trended quantities. After applying the change of variable formula to (25) and since for all , the joint PDF of can be written as

where is the joint density of Then, the estimator of is obtained by maximizing the log-likelihood function over some compact set :

Next, we can use Assumption 5 to determine the closed-form expression for . For notational simplicity, we suppress the dependence on and begin with where Assumption 5-(i) implies that is truncated-normal, and

From Assumption 5-(ii) and the change of variable formula, it follows that

where denotes the Beta density with parameter . The conditional joint density of can be written as a product of re-scaled Beta densities as follows:

The identification results in Section 3 imply that, for any two distinct parameters , we have that . If the log-likelihood function

| (26) |

is continuous at every , with probability one, then the consistency of would follow from Newey and McFadden (1994, Theorem 2.5). However, in our setting, the supports of , , and depend on two unknown boundary-parameters, and . So, the log-likelihood function in (26) is discontinuous with positive probability.

Establishing consistency of our estimator and obtaining the limiting distribution require extending Chernozhukov and Hong (2004) to allow for a nonseparable model given in (25). We remark that Chernozhukov and Hong (2004), considering an additive separable model, establish that the boundary-parameters converge at the rate of , and other regular parameters converge at the parametric rate . Given our likelihood function, we conjecture that their results apply in our setting, but the formal proof is beyond the scope of this article.

However, to evaluate the finite-sample performance of the estimator, in the following subsection, we use Monte Carlo experiments. Furthermore, to build the confidence intervals (see the application in Section 6 below), we apply the subsampling procedure (to the de-trended data) described in Politis, Romano, and Wolf (1999) Chapter 3, for stationary time series because of its robustness properties.

Monte Carlo Experiments

In this section, we present estimation results using simulated data to assess the finite-sample performance of our estimator. In light of our empirical application, we consider firms and divide them into six groups, each with a different cost distribution. In particular, for group , the private cost shocks , where is Beta distribution with parameters , see the second column of Table 2, truncated at . We assume that the firms’ groups are common knowledge and held fixed.

Let the demand and cost parameters be and , respectively. Let the demand shock to be a truncated normal random variable, i.e., on , and the common technology shock given to be, with with .

We consider two sample sizes , and for , we first draw the individual costs and the common demand and cost shocks from the distributions specified above, and then use Lemma 1 and (2) to determine the equilibrium outputs and the market-clearing price , respectively. Then we apply the estimation procedure to this sample. We repeat this procedure 500 times and, using the estimates from each round, in Table 2 we calculate the simulated bias, standard deviation (SD), and root mean squared error (RMSE), expressed as a fraction of the true parameter.

As we see, our estimation performs well. The average bias is small, and so are the SD and RMSE. Comparing the results across the two sample sizes, we see that the estimates improve with a larger sample, suggesting that our estimates will be good with .

| Parameters | True | ||||||

|---|---|---|---|---|---|---|---|

| Values | Bias | SD | RMSE | Bias | SD | RMSE | |

| Demand slope () | 0.50 | 0.0222 | 0.0038 | 0.0224 | 0.0220 | 0.0031 | 0.0222 |

| Mean of demand shock () | 300 | -0.0082 | 0.0264 | 0.0276 | -0.0092 | 0.0222 | 0.0240 |

| Variance of demand shock () | 800 | 0.0052 | 0.0369 | 0.0373 | 0.0025 | 0.0415 | 0.0415 |

| Left Truncation of demand shock () | 400 | 0.0205 | 0.0035 | 0.0208 | 0.0203 | 0.0029 | 0.0205 |

| Parameter of the cost function () | 0.03 | 0.0290 | 0.0274 | 0.0399 | 0.0325 | 0.0306 | 0.0446 |

| Type 1 cost parameter: | 0.5 | 0.0156 | 0.0135 | 0.0206 | 0.0184 | 0.0128 | 0.0224 |

| Type 1 cost parameter: | 0.2 | -0.0077 | 0.0132 | 0.0153 | -0.0117 | 0.0128 | 0.0173 |

| Type 2 cost parameter: | 0.6 | 0.0172 | 0.0141 | 0.0223 | 0.0234 | 0.0132 | 0.0268 |

| Type 2 cost parameter: | 0.2 | -0.0088 | 0.0138 | 0.0164 | -0.0114 | 0.0137 | 0.0178 |

| Type 3 cost parameter: | 0.4 | 0.0117 | 0.0154 | 0.0194 | 0.0162 | 0.0145 | 0.0217 |

| Type 3 cost parameter: | 0.1 | -0.0090 | 0.0146 | 0.0172 | -0.0147 | 0.0148 | 0.0209 |

| Type 4 cost parameter: | 0.5 | 0.0191 | 0.0145 | 0.0240 | 0.0186 | 0.0133 | 0.0229 |

| Type 4 cost parameter: | 0.3 | 0.0038 | 0.0146 | 0.0151 | 0.0022 | 0.0137 | 0.0139 |

| Type 5 cost parameter: | 0.60 | 0.0024 | 0.0168 | 0.0169 | 0.0006 | 0.0165 | 0.0165 |

| Type 5 cost parameter: | 0.7 | -0.0189 | 0.0128 | 0.0228 | -0.0203 | 0.0109 | 0.0230 |

| Type 6 cost parameter: | 0.4 | 0.0035 | 0.0185 | 0.0188 | 0.0006 | 0.0175 | 0.0175 |

| Type 6 cost parameter: | 0.3 | -0.0176 | 0.0128 | 0.0218 | -0.0198 | 0.0109 | 0.0226 |

| Parameter of the technology shock (): | 0.001 | 0.0094 | 0.0386 | 0.0397 | 0.0105 | 0.0391 | 0.0404 |

| Parameter of the technology shock (): | 0.001 | 0.0216 | 0.0400 | 0.0454 | 0.0309 | 0.0414 | 0.0516 |

| 5 | -0.0268 | 0.0040 | 0.0271 | -0.0268 | 0.0032 | 0.0270 | |

6 Estimation Results

In this section, we present the estimation results. First, we discuss the results from k-means clustering (e.g., Coates and Ng, 2012) to group countries into similar types based on the average and the standard deviation of their production. Second, we estimate the model parameters assuming that countries that belong to the same group have the same distribution of private costs: it follows from Lemma 1 that countries with the same distribution of private shocks will have symmetric strategies. Third, in a counterfactual exercise, we determine the effect of firms sharing information about their costs on consumer surplus.

We assume that the private cost distributions are common knowledge. However, knowledge of these distributions is based on countries’ geological information (e.g., nature and size of the reserves) and extraction technologies. Thus countries may have similar technologies and thus have symmetric cost distributions.555 Countries may strategically announce their reserves or other features of their extraction technologies, say, to influence competitors’ beliefs about them. For our empirical analysis, we assume that for reasons exogenous to our model, countries know each others’ cost distributions, and those cost innovations are independent and identically distributed across months. To capture this feature, and in light of our sample size (Figure 1), we divide countries into finite groups. For instance, it is reasonable to assume that larger producers such as the U.S., Saudi Arabia, and Russia have different production costs than smaller producers such as Libya and Venezuela. Similarly, countries in similar geography are likely to have symmetric costs.

To this end, we first apply the unsupervised k-means clustering based on averages and standard deviations of the de-trended productions to classify countries with similar production. Then, given that classification, we further classify countries to belong to similar geographic areas.

We display the k-means clustering exercise results in Figure 3, which shows that we can classify countries into four groups. The classification is consistent with what we would expect from “eyeballing” Figure 1 that countries that belong to a group have similar production patterns. Given these four groups, we classify a few into smaller groups based on locations. In the end, we get six groups with the following memberships: Group 1 (Iran, Iraq, Kuwait, Qatar, and U.A.E.), Group 2 (Canada, China, Norway, U.K.), Group 3 (Mexico, Venezuela, Ecuador), Group 4 (Algeria, Angola, Egypt, Libya, and Nigeria), Group 5 (Russia and Saudi Arabia) and Group 6 (U.S.). We display the production pattern, by group, in Figure 4. Hence, countries use the type-symmetric equilibrium for estimation.

Estimates.

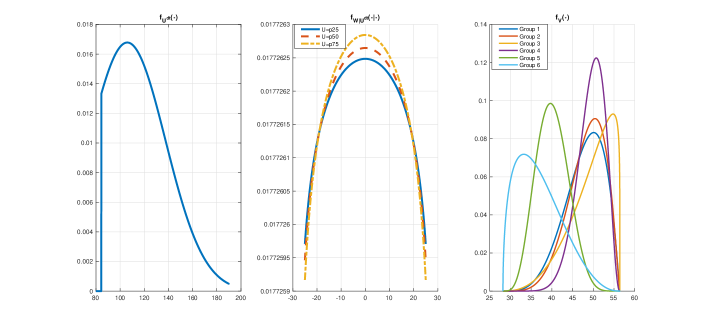

We apply our estimation method to our sample. The estimates together with their 95% confidence intervals are displayed in Table 3. To estimate the confidence interval we use subsampling method for stationary time series; see Politis, Romano, and Wolf (1999), Chapter 3.666In particular, we use a block size of , which gives us a total of 150 unique subsamples, and use Theorem 3.2.1 in the book to determine the confidence intervals. As we can see, the estimated slope parameter is , which means that the demand is downward sloping (as expected) and inelastic, and the estimated parameter of the cost function is . We estimate the mean demand shock, or the demand intercept (or the choke point) to be , and its estimated variance is , with left truncation at . Figure 5 displays the estimated densities of the demand shock, conditional density of the technology shock, and group-specific cost densities.

| Parameters | Estimates | 95% Confidence Intervals | |

|---|---|---|---|

| Demand slope () | 0.033 | [0.03, | 0.1204] |

| Mean of demand shock | 105.945 | [, | 293.713] |

| Variance of demand shock | 1,000 | [377.27, | 4,350] |

| Left truncation of demand shock | 84.443 | [84.10, | 268.036] |

| Parameter of the cost function () | [, | 0.022] | |

| Group 1 cost parameters: | 4.763 | [4.081, | 36.746] |

| Group 1 cost parameters: | 2.082 | [2.043, | 16.443] |

| Group 2 cost parameters: | 5.514 | [3.160 | 15.744] |

| Group 2 cost parameters: | 2.217 | [0.805, | 10.247] |

| Group 3 cost parameters: | 3.555 | [2.759, | 17.562] |

| Group 3 cost parameters: | 1.156 | [0.663, | 5.248] |

| Group 4 cost parameters: | 9.753 | [7.498, | 52.417] |

| Group 4 cost parameters: | 3.215 | [1.20, | 17.109] |

| Group 5 cost parameters: | 5.154 | [1.566, | 34.778] |

| Group 5 cost parameters: | 7.071 | [2.919, | 45.301] |

| Group 6 cost parameters: | 1.503 | [0.619, | 11.276] |

| Group 6 cost parameters: | 3.326 | [0.589, | 22.111] |

| Parameter of the technology shock (): | [, | ] | |

| Parameter of the technology shock (): | [, | 0.054] | |

| 28.206 | [26.247, | 77.789] | |

Regarding the individual cost parameters, the estimates suggest asymmetries across the four groups. As seen from the third and the fourth panels in Figure 5, Groups 5 and 6 are the most efficient. These orderings are consistent with the fact that the U.S. (Group 6), Saudi Arabia, and Russia (Group 5) are the largest and therefore the most efficient oil producers, while others have smaller production, which our model interprets as having higher costs.

Welfare Cost of Private Information.

Next we determine the effect of firms sharing their cost information on output, prices, and consumer surplus. We use the estimated parameters and follow Harris, Howison, and Sircar (2010) and Sarkar, Gupta, and Pal (1998) to determine equilibrium outputs and prices under complete cost information. Once we determine the outputs and price for each month , we also determine the consumer surplus. We repeat this exercise 1000 times and take an average across the simulation draws.

We find that under complete information, in many instances, countries do not produce anything: when costs are known, for some countries producing zero is the best response, and, consequently, the market efficiency increases. The outputs under complete information can be either higher or lower than those under incomplete information, depending on the cost densities. However, we find that the mean quantity under complete information is on average 7% more than under incomplete information, where the mean is taken across simulations and countries. We also find that, on average, there is a threefold increase in the variance in production across firms as we move from complete information to incomplete information. Correspondingly, the market-clearing price decreases on average by 18%, and the complete information decreases the deadweight loss (using the method in Daskin (1991)) by 16.3%.777 For each simulation, we calculate the deadweight loss built on the benchmark of the cost of the most efficient country. Then we average the deadweight loss across 1,000 simulations and compare the average under incomplete information with complete information.

7 Discussion

We have analyzed the crude-oil market using a model of static Cournot competition with private cost information to illustrate the application of our method. To this end, we have set aside several important issues about the oil industry. In this section, we briefly discuss three issues: (i) dynamics in oil extraction, (ii) non-competitive productions by the Organization of the Petroleum Exporting Countries (OPEC), and (iii) the nature of cost innovations.

Dynamics in Oil Extraction

While we have abstracted from any dynamics in the oil market, oil producers face inter-temporal tradeoffs because oil reserves are limited, and countries may allocate the production decisions over time. In such settings, production decisions are nonseparable across time. As our static model does not capture these effects, we should exercise caution in interpreting estimation results from our static model.

First and foremost, dynamics affect the interpretation of the private costs and, consequently, change the nature of the oligopolistic competition. Indeed, Loury (1986) shows that if countries have their cumulative extraction limited by the size of their initial reserves, the resource scarcity affects the Cournot oligopoly. Similarly, Cremer and Weitzman (1976) use a data structure similar to ours and show that a dynamic resource extraction model can rationalize the data and the role of OPEC producers. Our static model cannot capture these inter-temporal tradeoffs and their effects on welfare.

Furthermore, countries have strong asymmetry in terms of their cost. For instance, producing a barrel in the U.S. is more expensive than in Saudi Arabia, which explain Saudi Arabia’s oil rent and market power. Although we allow asymmetry across countries, the static model we have developed can neither capture scarcity rents nor explain the source of cost asymmetry, where scarcity rents—due to the finite reserve size and or capacity constraint—are determined by the gap between the market price and the extraction cost.

Nonetheless, extending exhaustible resource extraction problems, i.e., the so-called Hotelling problem (Hotelling, 1931), to allow private information about costs is a complex problem to solve. At the same time, there is much uncertainty in the empirical literature about the applicability of the Hotelling model (Gaudet, 2007; Anderson, Kellogg, and Salant, 2018).

Furthermore, we treat countries that own oil rigs and concessionaires as the same. In practice, however, concessionaires will likely have better information about the initial oil reserve than the owners, which affects the optimal extraction path (Martimort, Pouyet, and Ricci, 2018). How these extraction paths change with competition and the signaling effect of productions are other important but difficult questions to address. Proposing a model that captures all of these effects is beyond the scope of this paper.

Non-competitive OPEC Members

We have also assumed that all countries in our sample, including OPEC members, behave competitively.888 OPEC was founded in 1960 by Iran, Iraq, Kuwait, Saudi Arabia, and Venezuela. Later they were joined by Qatar (1961), Libya (1962), the UAE (1967), Algeria (1969), Nigeria (1971), Ecuador (1973), and Angola (2007). Although Ecuador suspended its membership in December 1992 and rejoined in October 2007, we treat it as a member in our analysis here. Thus, 12 out of 20 countries in our sample are OPEC members. As the evidence of collusion among OPEC members is mixed (Spilimbergo, 2001; Almoguera, Douglas, and Herrera, 2011; Okullo and Reynès, 2016), it is desirable to assess the robustness of our estimate of the size of private information to this assumption.

To this end, we consider a variation of our model in which OPEC members choose their (possibly coordinated) productions for reasons that are exogenous to the model before the nonmembers. In particular, we estimate a model where OPEC moves first and chooses its quantity. Then other countries compete á la Cournot conditional on the OPEC choice.

Two remarks are noteworthy. First, while conceptually straightforward, developing an equilibrium model of Stackelberg competition with private cost information where the “leader” is a cartel is complex and beyond the scope of our article, not least because such a model must incorporate adverse selection (Roberts, 1985; Athey and Bagwell, 2001) and the signaling effect of OPEC’s production on others’ beliefs. Second, without an equilibrium notion to rationalize OPEC choices, we cannot estimate the cost parameters of OPEC members. Nonetheless, as our objective is to assess the robustness of our welfare estimate with respect to the OPEC behavior, our model is reasonable because, given its additive separability, we can compare the welfare using only the nonmember productions.

In particular, relying on the linearity and additive separability of the demand, we can separate the production between OPEC members and nonmembers and express it as

| (27) |

where denotes the set of OPEC members and is the new random demand intercept. From Eq. (27) and after appropriately adapting Assumptions 1 and 2 to , we can show that the equilibrium characterization in Lemma 1 still applies to the nonmembers in , as long as the total OPEC output is exogenous. Consequently, we can nonparametrically identify , , and the cost distributions for firms in . Since we observe , we can also identify the conditional distribution from .

| Parameters | Estimates | 95% Confidence Intervals | |

|---|---|---|---|

| Demand slope () | 0.027 | [0.02, | 0.05] |

| Mean of demand shock | 60.029 | [2.02, | 101.79] |

| Variance of demand shock | 532.026 | [255.477, | 1,630.167] |

| Left truncation of demand shock | 70.22 | [55.755, | 135.647] |

| Left truncation of demand shock | 39.283 | [31.533, | 75.01] |

| Parameter of the cost function () | 0.028 | [, | 0.038] |

| Group 2 cost parameters: | 5.798 | [4.272 | 11.389] |

| Group 2 cost parameters: | 2.088 | [1.824, | 4.752] |

| Group 3 cost parameters: | 7.851 | [3.072, | 20.74] |

| Group 3 cost parameters: | 2.627 | [1.705, | 5.356] |

| Group 4 cost parameters: | 12.048 | [5.023, | 22.164] |

| Group 4 cost parameters: | 2.652 | [1.212, | 4.283] |

| Group 5 cost parameters: | 16.22 | [3.712, | 18.602] |

| Group 5 cost parameters: | 24.456 | [12.412, | 24.839] |

| Group 6 cost parameters: | 3.173 | [1.972, | 6.965] |

| Group 6 cost parameters: | 4.33 | [3.015, | 12.728] |

| Parameter of the technology shock (): | [, | ] | |

| Parameter of the technology shock (): | [, | ] | |

| 42.935 | [30.379, | 75.01] | |

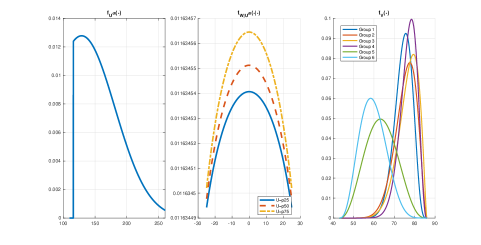

We present the estimation results in Table 4, which is comparable to Table 3. To make the comparison easy, we keep the same group numbering after removing the OPEC members. For instance, all countries except Egypt in Group 4 are OPEC members. So, the “new” Group 4 in Table 4 includes only Egypt. Likewise, Group 1 is excluded because all the countries in that group are OPEC members.

We find the estimates are reasonably similar even though now we have a smaller sample size. We have also obtained that the average output under complete information has a 9% higher mean and 60% higher variance than under incomplete information. Correspondingly, the market-clearing price decreases on average, while the deadweight loss decreases by 15.1%.

Thus, the estimate is similar to the one obtained previously, although here, we use the information only from non-OPEC members to quantify the size of private information and that welfare variation captures only the cost of private information for non-OPEC countries. Although we should exercise caution and not interpret these estimates to mean that OPEC does not affect market efficiency Asker, Collard-Wexler, and Loecker (2019). These results only suggest that the cost of private information outside or inside OPEC are of similar magnitude since including OPEC before or considering only non-OPEC countries here gives similar estimates.

Nature of Cost Innovations

So far, we have assumed that country-specific shocks are independent and identically distributed (i.i.d.) across for every . Regarding the independence condition, even though we allow auto-correlation in observed quantities induced by , we may still have some auto-correlation in when studying the global crude-oil market. Some country-specific structural changes might make this i.i.d. assumption unrealistic. Below, we discuss how we can adapt our framework to capture these two features.

First, month-to-month cost innovations may be associated with common changes in input costs across the industry, for instance, when all countries hire from a common set of offshore drilling rigs or comparable pools of oil workers. As we mentioned, some of these common shocks can be captured by the time-series components (Assumption 4) and common cost shock , but we may still miss some correlation left. One way to capture this dependence is to use the U.S. Bureau of Labor Statistic’s PPI for oil and gas drilling (PCU213111213111P) as a deflator. The estimates using the new deflator are in Appendix B. We estimate deadweight loss under incomplete information becomes 12.9% larger than under complete information.

Second, our framework allows for asymmetric distributions in private costs shocks, so publicly known country-specific shocks can be captured by changing the functional form of the corresponding distributions. For instance, if there is a war in Libya, we can consider Libya as a separate group with two cost distributions: and another distribution with higher mean to capture higher costs during wartime. If these distributions satisfy Assumption 1 and are common knowledge, then there will be two equilibria: one before and another after the war. Moreover, our identification strategies will still apply if we observe when country-specific shocks occur.

To estimate the new model, we would need to introduce observed within-country heterogeneity by adapting Assumption 5-(iii) and modifying Eq. (26) accordingly. For instance, we can continue to assume Assumption 5-(iii) holds so that the two Beta distributions can be modeled with four parameters parameters . Then, we can write the log-likelihood function as

where is equal to one during the Libyan war periods and zero otherwise. If the war permanently affects costs, then we can set from the start of the war.

Similarly, the shale-oil revolution may be the reason behind the increase in U.S. production over the last decade; see Figure 4. However, the deposits behind it (e.g., tight oil formations) are different from conventional oil deposits previously exploited, requiring different extraction technologies with different costs than before. We can follow the same procedure outlined above to capture these changes, modeling the U.S. with two different cost distributions and adapting the above log-likelihood function accordingly.

Third, some innovations might simultaneously impact countries with similar deposits, i.e., countries with similar oil types, sizes, operators, extraction technologies, and locations. In other words, innovations may affect multiple countries, but not all of them. Our model can still be adapted to capture such changes in costs, as long as those changes are publicly observed. In particular, we can define groups based on deposits’ observables (e.g., type of the oil, location) instead of productions and geographic locations, as we have done above. Although such modification does not affect the identification results because, in practice, one has a finite sample, there is a tradeoff between the number of groups and the variance of the estimators.

8 Conclusion

We have developed a model of Cournot competition with private information about (possibly asymmetric) costs. We have specified that the inverse demand function is linear in total quantity with stochastic intercept (or choke price). We have also allowed for an unobserved market characteristic that affects the costs of all firms. In this context, we have first characterized the equilibrium strategies and established the semi-nonparametric identification of the model’s parameters. The identification and estimation strategies exploited the strictly monotonic relationship between a firm’s output and unobserved shocks. In sum, we rely on the optimality conditions, functional form assumptions about demand, and the assumptions that firms have correct mutual beliefs for the identification. We applied our method using crude-oil production data to quantify private information’s role. Finally, we extended our analysis to consider several extensions.

There are several avenues for future research. First, and as we discussed earlier, we abstracted from any dynamics in the oil market. However, understanding the role of private information in dynamic Cournot competition is important. Although there has been substantial development on this topic (Bonatti, Cisternas, and Toikka, 2017), its application to an empirical setting, say, by adopting and extending the method in Bajari, Benkard, and Levin (2007), is still open. Furthermore, an extension of such a model to a resource extraction problem with asymmetric information between countries and their concessionaire, in the spirit of Martimort, Pouyet, and Ricci (2018), is yet another topic for future research.

Second, we may consider the possibility that firms have imprecise beliefs about the cost distribution of their competitors. For example, in the context of the crude-oil market, knowledge about cost distributions is based on geological information (e.g., nature and size of the reserves), which is either private or when public, comes with its uncertainty given the incentives of each country to use these announcements for strategic purposes. There are at least three ways to model this feature. We can follow the approach in Aryal, Grundl, Kim, and Zhu (2018) for auctions and model firms with multiple priors, or allow non-equilibrium beliefs (Aguirregabiria and Magesan, 2020), or like Magnolfi and Roncoroni (Forthcoming), use Bayes Correlated Equilibrium (Bergemann and Morris, 2016).

Appendix A Appendix: Proofs

This section provides the proofs of Lemma 1 and Theorem 1. The proof of the latter relies on an auxiliary lemma provided in Section A.2 together with its proof and a brief discussion on its testable implications.

A.1 Proof of Lemma 1

Existence of the equilibrium strategies follows immediately by checking that satisfy the first-order conditions (5), as well as the second-order conditions, which is trivial because by Assumption 2. Observe also that such strategies are nonnegative due to the second part of this assumption.

To establish uniqueness, let be equilibrium strategies and fix . By (5), the former must satisfy

for each ; note that depends only on and . Thus, in vector notation, we can write

| (A.1) |

where is matrix that has zeros in the main diagonal and ones outside, is a vector of ones, and . Expression (A.1) can be rewritten as

| (A.2) |

where denotes the identity matrix of dimension . To complete the proof, it suffices to show that the matrix on the left-hand side is invertible. To do so, write

and note that the desired result is obtained from the Sherman-Morrison formula because ; see Sec. 2.7.1. in Press, Teukolsky, Vetterling, and Flannery (2007) ∎

A.2 An Auxiliary Lemma

The next auxiliary lemma establishes smoothness conditions on the distributions of quantities, as well as on certain conditional distributions. These results will be employed in the proof of Theorem 1 below.

Lemma A.1.

-

1.

has support . It also admits a PDF that is strictly positive and continuously differentiable on the interior of this set.

-

2.

The supports of conditional CDFs and are given by and , respectively. Furthermore, and admit conditional PDFs and that are strictly positive and continuously differentiable on and , respectively.

Before proceeding to the proof of this lemma, we highlight that this lemma can be of interest by itself as it provides testable implications of our model. Specifically, the first part of Lemma A.1 establishes that is a continuous random variable supported on an interval. This result follows that is a linear combination of and . As an example of a model whose equilibrium outputs are not continuous, consider a static (or dynamic) Cournot model with entry and exit. In such a model, a potential entrant first decides whether to pay a fixed cost to enter and, upon entry, choose the optimal quantity. If the fixed entry cost is sufficiently high and we observe the set of all potential entrants, then some firms do not enter with a positive probability. As a result, we would observe that the outputs of some firms are equal to zero, and therefore the distribution of these outputs would have a mass point at zero. Similarly, an incumbent might exit, which means the outputs would have a mass point at zero.

The second part of Lemma A.1 states that, for any , is a continuous random variable when we condition on . This prediction does not hold, e.g., under complete information, because the equilibrium strategy for a firm is given by

where stands for the average type (see Vives, 2002, Proposition 1).999Note that these quantities can be negative without further restrictions on the parameter values. See Section 2 in Harris, Howison, and Sircar (2010) for a discussion on the complete-information Cournot equilibrium with non-identical marginal costs. Unlike with in Lemma 1, the firm ’s strategy depends on its type and also on its competitors type in a strictly monotonic way and thus

| (A.3) |

where and . In other words, under complete information, firm produces at the lowest level when its costs are the highest and its competitors’ costs are at the lowest. As a result, letting be firm ’s equilibrium output under complete information, we have that implies with probability one. Thus, becomes a degenerated random variable after conditioning on , so cannot be rationalized by a Cournot model with complete information.

Proof of Lemma A.1.

For the first part, by the transformation formula and , observe that for and , where and

Thus,

| (A.4) |

Now pick . Observe that there exists a nonempty open neighborhood and such that Thus, since is bounded away from zero on , we obtain

As has been arbitrarily chosen, from this inequality we can conclude that the support of is and that is strictly positive on . Moreover, by Assumption 1 and expression (A.4), it follows that is continuously differentiable on this set.

For the second part, to simplify the exposition and without loss of generality, we prove the statement for and . The conditional CDF can be expressed as and that the boundaries of its (conditional) support are given by

Now let be a matrix of the form and write where , , and each has been defined in the previous subsection. Since is nonsingular and are mutually independent, by the transformation formula and monotonicity of the equilibrium strategies (Lemma 1), we have

for . Thus, the conditional PDF can be obtained by integrating out the utmost right-hand side with respect to the first elements of . Then it follows by standard arguments that is strictly positive and continuously differentiable on . Finally, the desired results regarding and can be obtained by noting that ∎

A.3 Proof of Theorem 1

We start with the identification of . Note that for any by strict monotonicity of firm ’s equilibrium strategy (Lemma 1). Further, we have that by Assumption 1, so we can write , where we use the fact that the events and are equivalent. Using Lemma 1, we can express the conditional quantile function of given as

| (A.5) |

for all , where , , and have been identified in (9), (11), and (12), respectively. As and are independent by Assumption 1, the unconditional quantile function of satisfies . Hence, after rearranging (A.5), we get (13).

Regarding the second statement, note that Lemma 1 implies

Now consider any and write

Assumption 1 implies that , so, the second term on the right-hand side becomes

Then, using , we get

The desired result follows by recalling that , being an identified object. ∎

Appendix B Cost Innovation.

Here, we present the estimation results that uses BLS’s PPI for oil and gas drilling (PCU213111213111P) as the price deflator as discussed in Section 7 under “Nature of Cost Innovations.”

| Parameters | Estimates | 95% Confidence Intervals |

|---|---|---|

| Demand slope () | 0.05 | [0.5, 0.19] |

| Mean of demand shock | 128.937 | [] |

| Variance of demand shock | 2,722.666 | [] |

| Left truncation of demand shock | 115.987 | [] |

| Parameter of the cost function () | [] | |

| Group 1 cost parameters: | 13.832 | [] |

| Group 1 cost parameters: | 5.064 | [] |

| Group 2 cost parameters: | 9.01 | [] |

| Group 2 cost parameters: | 2.927 | [] |

| Group 3 cost parameters: | 8.853 | [] |

| Group 3 cost parameters: | 2.417 | [] |

| Group 4 cost parameters: | 13.888 | [] |

| Group 4 cost parameters: | 3.731 | [] |

| Group 5 cost parameters: | 3.619 | [] |

| Group 5 cost parameters: | 3.967 | [] |

| Group 6 cost parameters: | 3.92 | [] |

| Group 6 cost parameters: | 6.233 | [] |

| Parameter of the technology shock (): | [] | |

| Parameter of the technology shock (): | [] | |

| 42.975 | [] |

References

- (1)

- Aguirregabiria and Magesan (2020) Aguirregabiria, V., and A. Magesan (2020): “Identification and Estimation of Dynamic Games When Players’ Beliefs Are Not in Equilibrium,” Review of Economic Studies, 87, 582–625.

- Almoguera, Douglas, and Herrera (2011) Almoguera, P. A., C. C. Douglas, and A. M. Herrera (2011): “Testing for the Cartel in OPEC: Non-Cooperative Collusion or Just Non-Cooperative?,” Oxford Review of Economic Policy, 27(1), 144–168.

- Anderson, Kellogg, and Salant (2018) Anderson, S. T., R. Kellogg, and S. W. Salant (2018): “Hotelling under Pressure,” Journal of Political Economy, 126(3), 984–1026.

- Aradillas-López (2010) Aradillas-López, A. (2010): “Semiparametric Estimation of a Simultaneous Game with Incomplete Information,” Journal of Econometrics, 157, 409–431.

- Armantier, Florens, and Richard (2008) Armantier, O., J.-P. Florens, and J.-F. Richard (2008): “Approximation of Nash Equilibria in Bayesian Games,” Journal of Applied Econometrics, 23(7), 965–981.

- Aryal, Ciliberto, and Leyden (Forthcoming) Aryal, G., F. Ciliberto, and B. T. Leyden (Forthcoming): “Coordinated Capacity Reductions and Public Communication in the Airline Industry,” Review of Economic Studies.

- Aryal, Grundl, Kim, and Zhu (2018) Aryal, G., S. Grundl, D.-H. Kim, and Y. Zhu (2018): “Empirical Relevance of Ambiguity in First Price Auctions,” Journal of Econometrics, 204(2), 189–206.

- Asker, Collard-Wexler, and Loecker (2019) Asker, J., A. Collard-Wexler, and J. D. Loecker (2019): “(Mis)Allocation, Market Power, and Global Oil Extraction,” American Economic Review, 109(4), 1568–1615.

- Athey (2001) Athey, S. (2001): “Single Crossing Properties and the Existence of Pure Strategy Equilibria in Games of Incomplete Information,” Econometrica, 69(4), 861–889.

- Athey and Bagwell (2001) Athey, S., and K. Bagwell (2001): “Optimal Collusion with Private Information,” RAND Journal of Economics, 32(2), 428–465.

- Bajari, Benkard, and Levin (2007) Bajari, P., C. L. Benkard, and J. Levin (2007): “Estimating Dynamic Models of Imperfect Competition,” Econometrica, 75(5), 1331–1370.

- Bergemann, Heumann, and Morris (2019) Bergemann, D., T. Heumann, and S. Morris (2019): “Information, Market Power and Price Volatility,” Working Paper.

- Bergemann and Morris (2016) Bergemann, D., and S. Morris (2016): “Bayes Correlated Equilibrium and the Comparison of Information Structures in Games,” Theoretical Economics, 11, 487–522.

- Bonatti, Cisternas, and Toikka (2017) Bonatti, A., G. Cisternas, and J. Toikka (2017): “Dynamic Oligopoly with Incomplete Information,” Review of Economic Studies, 84, 503–546.

- Bresnahan (1989) Bresnahan, T. (1989): “Empirical Studies for Industries with Market Power,” in Handbook of Industrial Organization, ed. by R. Schmalensee, and R. Willig, vol. 2, chap. 17, pp. 1011–1057. Elsevier.

- Carvajal, Deb, Fenske, and Quah (2013) Carvajal, A., R. Deb, J. Fenske, and J. K.-H. Quah (2013): “Revealed Preference Tests of the Cournot Model,” Econometrica, 81(6), 2351–2379.

- Chernozhukov and Hong (2004) Chernozhukov, V., and H. Hong (2004): “Likelihood Estimation and Inference in a Class of Nonregular Econometric Models,” Econometrica, 72(5), 1445–1480.

- Coates and Ng (2012) Coates, A., and A. Y. Ng (2012): “Learning Feature Representations with K-means,” in Neural Networks: Tricks of the Trade, Reloaded, ed. by G. Montavon, G. Orr, and K.-R. Müller, LNCS 7700. Springer.

- Collard-Wexler (2013) Collard-Wexler, A. (2013): “Demand Fluctuations in the Ready-Mix Concrete Industry,” Econometrica, 81(3), 1003–1037.

- Cremer and Weitzman (1976) Cremer, J., and M. L. Weitzman (1976): “OPEC and the Monopoly Price of World Oil,” European Economic Review, 8, 155–164.

- Daskin (1991) Daskin, A. J. (1991): “Deadweight Loss in Oligopoly: A New Approach,” Southern Economic Journal, 58(1), 171–185.

- de Paula and Tang (2012) de Paula, Á., and X. Tang (2012): “Inference of Signs of Interaction Effects in Simultaneous Games with Incomplete Information,” Econometrica, 80, 143–172.

- de Roos (2006) de Roos, N. (2006): “Examining Models of Collusion: The Market for Lysine,” International Journal of Industrial Organization, 24(6), 1083–1107.

- Durand-Lasserve and Pierru (2021) Durand-Lasserve, O., and A. Pierru (2021): “Modeling World Oil Market Questions: An Economic Perspective,” Energy Policy, 159, 112606.

- Einav and Nevo (2006) Einav, L., and A. Nevo (2006): “Empirical Models of Imperfect Competition: A Discussion,” CSIO Working Paper Number 0087.

- Einy, Haimanko, Moreno, and Shitovitz (2010) Einy, E., O. Haimanko, D. Moreno, and B. Shitovitz (2010): “On the Existence of Bayesian Cournot Equilibrium,” Games and Economic Behavior, 68(1), 77–94.

- Gaudet (2007) Gaudet, G. (2007): “Natural Resource Economics under the Rule of Hotelling,” Canadian Journal of Economics, 40(4), 1033–1059.

- Genesove and Mullin (1998) Genesove, D., and W. P. Mullin (1998): “Testing Static Oligopoly Models: Conduct and Cost in the Sugar Industry, 1890-1914,” RAND Journal of Economics, 29(2), 355–377.

- Gentry and Li (2014) Gentry, M., and T. Li (2014): “Identification in Auctions with Selective Entry,” Econometrica, 82(1), 315–344.

- Grieco (2014) Grieco, P. L. E. (2014): “Discrete Games with Flexible Information Structures: An Application to Local Grocery Markets,” RAND Journal of Economics, 45(2), 303–340.

- Guerre, Perrigne, and Vuong (2000) Guerre, E., I. Perrigne, and Q. Vuong (2000): “Optimal Nonparametric Estimation of First-Price Auctions,” Econometrica, 68(3), 525–574.

- Harris, Howison, and Sircar (2010) Harris, C., S. Howison, and R. Sircar (2010): “Games with Exhaustible Resources,” SIAM Journal on Applied Mathematics, 70(7/8), 2556–2581.

- Horowitz and Markatou (1996) Horowitz, J. L., and M. Markatou (1996): “Semiparametric Estimation of Regression Models for Panel Data,” Review of Economic Studies, 63(1), 145–168.

- Hortaçsu and Syverson (2007) Hortaçsu, A., and C. Syverson (2007): “Cementing Relationships: Vertical Integration, Foreclosure, Productivity, and Prices,” Journal of Political Economy, 115(2), 250–301.

- Hotelling (1931) Hotelling, H. (1931): “The Economics of Exhaustible Resources,” Journal of Political Economy, 39(2), 137–275.

- Hurkens (2014) Hurkens, S. (2014): “Bayesian Nash Equilibrium in ‘Linear’ Cournot Models with Private Information about Costs,” International Journal of Economic Theory, 10(2), 203–217.

- Igami (2015) Igami, M. (2015): “Market Power in International Commodity Trade: The Case of Coffee,” Journal of Industrial Economics, 63(2), 225–248.

- Johnson, Kotz, and Balakrishnan (1994) Johnson, N. L., S. Kotz, and N. Balakrishnan (1994): Continuous Univariate Distributions, vol. 1. Wiley Series, 2 edn.

- Kellogg (2014) Kellogg, R. (2014): “The Effect of Uncertainty on Investment: Evidence from Texas Oil Drilling,” American Economic Review, 104(6), 1698–1734.

- Krasnokutskaya (2011) Krasnokutskaya, E. (2011): “Identification and Estimation of Auction Models with Unobserved Heterogeneity,” Review of Economic Studies, 78(1), 293–327.

- Loury (1986) Loury, G. C. (1986): “A Theory of ’Oil’Igopoly: Cournot Equilibrium in Exhaustible Resource Markets with Fixed Supplies,” International Economic Review, 27(2), 285–301.

- Magnolfi and Roncoroni (Forthcoming) Magnolfi, L., and C. Roncoroni (Forthcoming): “Estimation of Discrete Games with Weak Assumptions on Information,” Review of Economic Studies.

- Martimort, Pouyet, and Ricci (2018) Martimort, D., J. Pouyet, and F. Ricci (2018): “Extracting Information or Resource? The Hotelling Rule Revisited under Asymmetric Information,” RAND Journal of Economics, 49(2), 311–347.

- Milgrom and Roberts (1982a) Milgrom, P., and J. Roberts (1982a): “Limit Procing and Entry under Incomplete Information: An Equilibroum Analysis,” Econometrica, 50(2), 443–460.

- Milgrom and Roberts (1982b) (1982b): “Predation, Reputation, and Entry Deterrence,” Journal of Economic Theory, 27, 280–312.

- Newey and McFadden (1994) Newey, W. K., and D. McFadden (1994): “Large Sample Estimation and Hypothesis Testing,” in Handbook of Econometrics, ed. by R. F. Engle, and D. McFadden, vol. 4, chap. 36, pp. 2111–2245. Elsevier.

- Okullo and Reynès (2016) Okullo, S. J., and F. Reynès (2016): “Imperfect Cartelization in OPEC,” Energy Economics, 60, 333–344.

- Politis, Romano, and Wolf (1999) Politis, D. N., J. P. Romano, and M. Wolf (1999): Subsampling, Statistics. Springer-Verlag, New York.

- Press, Teukolsky, Vetterling, and Flannery (2007) Press, W. H., S. A. Teukolsky, W. T. Vetterling, and B. P. Flannery (2007): Numerical Recipes: The Art of Scientific Computing. Cambridge Uni. Press, 3rd edn.

- Roberts (1985) Roberts, K. (1985): “Cartel Behaviour and Adverse Selection,” Journal of Industrial Economics, 33(4), 401–413.

- Rosen (2006) Rosen, A. (2006): “Identification and Estimation of Firms’ Marginal Cost Functions with Incomplete Knowledge of Strategic Behavior,” Working Paper.

- Ryan (2012) Ryan, S. P. (2012): “The Costs of Environmental Regulation in a Concentrated Industry,” Econometrica, 80(3), 1019–1061.

- Sarkar, Gupta, and Pal (1998) Sarkar, J., B. Gupta, and D. Pal (1998): “A Geometric Solution of a Cournot Oligopoly with Nonidentifical Firms,” Journal of Economic Education, 29(2), 118–126.

- Seim (2006) Seim, K. (2006): “An Empirical Model of Firm Entry with Endogenous Product Type-Choices,” RAND Journal of Economics, 37(3), 619–640.

- Shephard (1991) Shephard, N. G. (1991): “From Characteristic Function to Distribution Function: A Simple Framework for the Theory,” Econometric Theory, 7(4), 519–529.