On Simple Mechanisms for Dependent Items

Abstract

We study the problem of selling heterogeneous items to a single buyer, whose values for different items are dependent. Under arbitrary dependence, Hart and Nisan [30] show that no simple mechanism can achieve a non-negligible fraction of the optimal revenue even with only two items. We consider the setting where the buyer’s type is drawn from a correlated distribution that can be captured by a Markov Random Field, one of the most prominent frameworks for modeling high-dimensional distributions with structure.

If the buyer’s valuation is additive or unit-demand, we extend the result to all MRFs and show that can achieve an -fraction of the optimal revenue, where is a parameter of the MRF that is determined by how much the value of an item can be influenced by the values of the other items. We further show that the exponential dependence on is unavoidable for our approach and a polynomial dependence on is unavoidable for any approach. When the buyer has a XOS valuation, we show that achieves at least an -fraction of the optimal revenue, where is the spectral gap of the Glauber dynamics of the MRF. Note that in the special case of independently distributed items, and , and our results recover the known constant factor approximations for a XOS buyer [41]. We further extend our parametric approximation to several other well-studied dependency measures such as the Dobrushin coefficient [27] and the inverse temperature. In particular, we show that if the MRF is in the high temperature regime, is still a constant factor approximation to the optimal revenue even for a XOS buyer. Our results are based on the Duality-Framework by Cai et al. [14] and a new concentration inequality for XOS functions over dependent random variables.

1 Introduction

The design of revenue-optimal auctions for selling multiple items is a central problem in Economics and Computer Science. In the past decade, significant progress has been made, first in efficient computation of revenue-optimal auctions [18, 19, 1, 10, 2, 11, 12, 15, 13, 3, 6, 24], and then in the identification of simple auctions that achieve constant factor approximations to the optimal revenue [4, 45, 41, 14, 21, 17] under the item-independence assumptions. 333Intuitively, item-independence means that each bidder’s value for each item is independently distributed, and this definition has been suitably generalized to set value functions such as submodular or subadditive functions [41]. Despite being theoretically appealing, item-independence is an unrealistic assumption in practice. In this paper, we go beyond the item-independence assumption and study simple and approximately optimal auctions for selling dependent items.

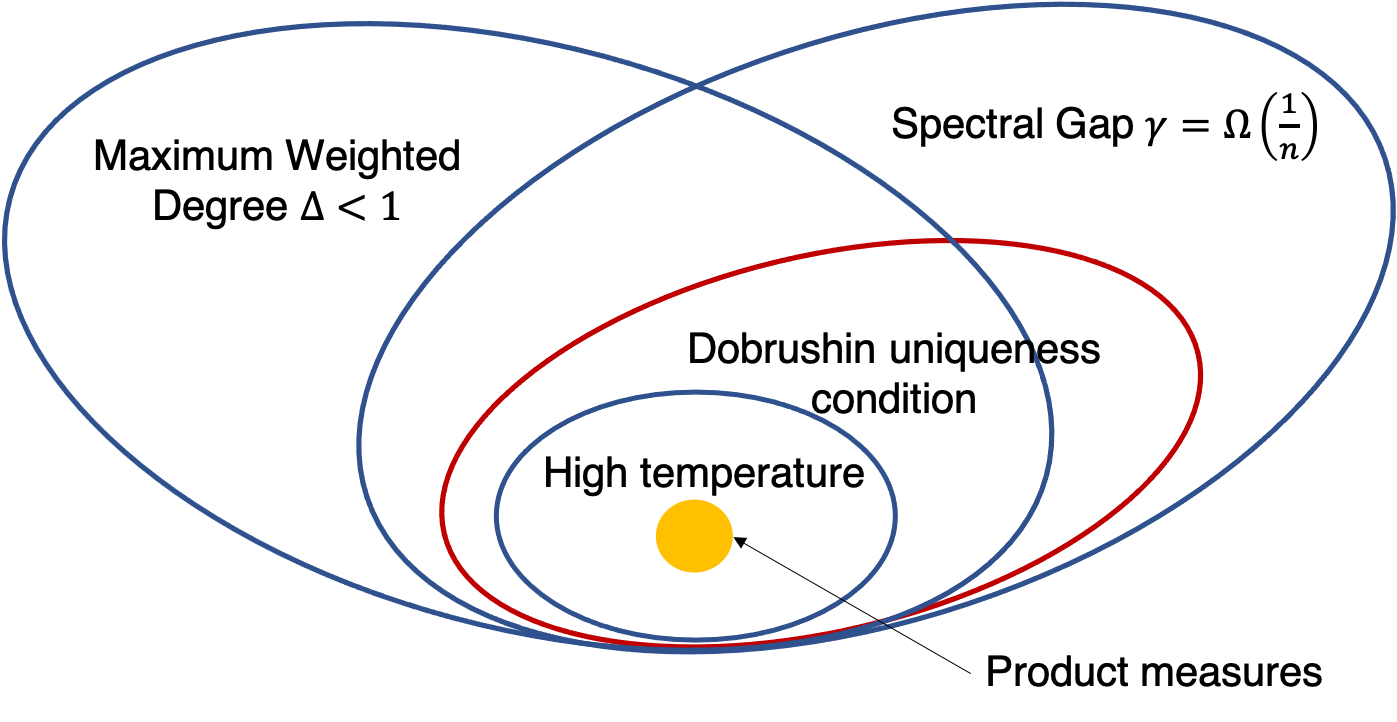

Unfortunately, strong negative results exist if we allow the items to be arbitrarily dependent [8, 30]. For example, Hart and Nisan [30] show that the revenue of the best deterministic mechanism is unboundedly smaller than the revenue of the optimal randomized mechanism even when we are only selling two correlated items to a single buyer. Since all simple mechanisms in the literature are deterministic, the result also implies that no simple mechanism that has been considered so far can provide any guarantee to the revenue for even two correlated items. Arguably, however, high-dimensional distributions that arise in practice are rarely arbitrary, as arbitrary high-dimensional distributions cannot be represented efficiently, and are known to require exponentially many samples to learn or even perform the most basic statistical tests on them; see e.g. [25] for a discussion. To overcome the curse of dimensionality, a major focus of Statistics and Machine Learning has been on identifying and exploiting the structural properties of high-dimensional distributions for succinct representation, efficient learning, and efficient statistical inference. There are several widely-studied frameworks to model the structure of dependence in high-dimensional distributions. In this work, we propose capturing the dependence between item values using one of the most prominent graphical models – Markov Random Fields (MRFs). Note that MRFs are fully general and can be used to express arbitrary high-dimensional distributions. The main advantage of MRFs is that there are several natural complexity parameters that allow the user to tune the dependence structure in the distributions represented by MRFs from product measures all the way up to arbitrary distributions. Our goal is to provide parametric approximation ratios of simple mechanisms that degrade gracefully with respect to these natural parameters.

MRFs are formally defined in Definition 2. Intuitively, a MRF can be thought of as a graph (or a hypergraph) where each node represents a random variable (or item value in our case). There is a potential function associated with each edge that captures the correlation between the two incident random variables. How does it represent a joint distribution? The probability for a particular realization or the random variables, or known as a configuration of the random field, is proportional to the exponential of the total potential of the configuration. MRF is a flexible model. For example, we can capture the degree of (positive or negative) correlations between two random variables by controlling the corresponding potential function. Here we provide a stylistic example to illustrate the suitability of MRFs for modeling buyers’ joint value distributions. Imagine that we manage a car dealership. A potential buyer is hoping to purchase one car, i.e., has a unit-demand valuation. The dealership carries various brands and types of vehicles, and will like to find the optimal way to price each car. However, it would be naïve to assume the buyer’s value for each car is independently distributed. The example in Figure 1 demonstrates how a MRF can better capture the customer’s joint value distribution for different cars.

1.1 Main Results and Techniques

We focus on the single buyer case and allow the buyer’s valuation to be as general as a XOS function (a.k.a. a fractionally subadditive function). 444The class of XOS functions is a super-class of submodular functions, and is contained in the class of subadditive functions. We consider the two most extensively studied forms of simple mechanisms: selling the items separately and selling the grand bundle. We use SRev and BRev to denote the optimal revenue obtainable by these two types of mechanisms respectively. In a sequence of papers, it was shown that is a constant factor approximation to the optimal revenue for a single additive or unit-demand buyer under the item-independence assumption [18, 4, 14]. 555More specifically, SRev denotes the optimal expected revenue achievable by any posted price mechanism. When the buyer has a unit-demand valuation, [18, 14] show that SRev is already a constant factor approximation of the optimal revenue. Our first main result extends the above approximation to any MRFs. The approximation ratio degrades with the maximum weighted degree that captures the degree of dependence among the item values.

Parameter I: Maximum Weighted Degree .

The formal definition can be found in Definition 4. As we mentioned, a MRF can be thought of as a graph (or a hypergraph) where each node represents a random variable. The weight of an edge is related to the maximum absolute value the corresponding potential function can take and represents the “strength” of the dependence between two incident random variables. The weighted degree of a random variable is simply the sum of weights from all incident edges. If the maximum weighted degree of a MRF is small, then no random variable can depend strongly on many other random variables. Note that when the random variables are independent, and the instance constructed by Hart and Nisan [30] corresponds to a MRF with .

-

Result I:

For a single additive or unit-demand buyer whose type is generated by a MRF with maximum weighted degree , , where OPT is the optimal revenue.

The formal statement of the result is in Theorem 1 and 2. We further show that the dependence on is necessary. For any sufficiently large number , there exists a MRF with such that is no more than (Theorem 3) using a modification of the Hart-Nisan construction [30]. Although there is still an exponential gap between our upper and lower bounds, it shows that whenever Result I fails to provide a constant factor approximation (independent of the number of items), no constant factor approximation is possible without further restrictions on the dependency. We leave it as an open question to close the gap between our upper and lower bounds. The main tool we use is a generalization of the prophet inequality to the case where the rewards are sampled from a MRF (Lemma 3). The overall analysis is similar to the one used by Cai et al. [14] for the item-independent case. We show that the exponential dependence on is unavoidable for this type of analysis in Theorem 8. More specifically, a key step of the analysis involves approximating the optimal revenue in a single-dimensional setting, known as the copies setting, using SRev. Theorem 8 constructs an instance such that the optimal revenue in the copies setting is at least times larger than .

Rubinstein and Weinberg [41] show that, under the item-independence assumption, is still a constant factor approximation to the optimal revenue for a buyer whose valuation is a subadditive function. Our second main result extends their result to any MRFs when the buyer’s valuation is a XOS function. The approximation ratio depends on and the spectral gap of the Glauber Dynamics .

Parameter II: Spectral Gap of the Glauber Dynamics .

A common way to generate a sample from a high-dimensional distribution is via a Markov Chain Monte Carlo method known as the Glauber dynamics (see Definition 5). The spectral gap of the Glauber dynamics is the difference between the largest eigenvalue and the second largest eigenvalue of the transition matrix of the Glauber dynamics. It is well-known that is strictly less than for any MRFs [36], so is always strictly positive.

-

Result II:

For a single XOS buyer whose type is generated by a MRF, , where is the number of items, is the spectral gap of the Glauber Dynamics, and is the maximum weighted degree. 666Although the approximation ratio depends on , the ratio indeed improves if we increase and fix .

Some remarks are in order. First, our approximation ratio holds for any MRFs. Second, for any -dimensional random vector , the ’s are considered weakly dependent if the spectral gap . For example, when the ’s are independent, . Finally, the condition is extensively studied in probability theory. The condition is satisfied under the Dobrushin uniqueness condition (see Section 6 for details), a well-known sufficient condition that ensures weak dependency; it implies rapid mixing of the Glauber dynamics (i.e., they mix in time ); it also guarantees that polynomial functions concentrate in Ising models [29, 26].

The formal statement of Result II can be found in Theorem 4. The analysis follows the same general framework by Cai and Zhao [17]. The major new challenge is to prove that any XOS function concentrates, when is a drawn from a high-dimensional distribution . Proving concentration inequalities for non-linear functions over dependent random variables is a non-trivial task that lies at the heart of many high-dimensional statistical problems. We prove a parametric concentration inequality for XOS functions that depends on the spectral gap of the Glauber dynamics for (Lemma 13). The proof is based on a combination of the Poincaré inequality and a special property of XOS functions – the self-boundingness. We believe this concentration inequality may be of independent interest. An interesting question is whether the approximation ratio needs to depend on both and . We show that the dependence on is crucial, as no approximation can be obtained with only restriction on the spectral gap even for a single additive or unit-demand buyer (Theorem 7). 777Indeed, we prove an even stronger result that shows no finite approximation ratio is possible under only the Dobrushin uniqueness condition, which implies that (Lemma 16). We do not know whether it is possible to obtain an approximation that only depends on for a XOS buyer and leave it as an open question. 888A naïve approach is to directly bound using a function of . However, this approach can at best provide an approximation ratio that is exponential in , as could be exponential in even when is upper bounded by some absolute constant [39]. We suspect such an improvement requires proving a parametric concentration inequality for XOS functions that only depend on the maximum weighted degree , which we believe will have further applications.

Our Results under Other Weak Dependence Conditions.

There are several alternative ways to parametrize the degree of dependency in a high-dimensional distribution. We focus on two prominent ones – the Dobrushin coefficient and the inverse temperature of a MRF, and discuss how our approximation results change under these conditions. We first consider the Dobrushin coefficient and its relaxations. An important concept is the influence matrix.

Influence Matrix and the Dobrushin Condition

For any -dimensional random vector , we define the influence of variable on variable as

where denotes the conditional distribution of given . Let for each . We define the influence matrix . When the ’s are weakly dependent, the entries of should have small values. The Dobrushin Coefficient, defined as , was originally introduced by Dobrushin [27] in the study of Gibbs measures. The Dobrushin coefficient less than is known as the Dobrushin uniqueness condition, under which the Gibbs distribution has a unique equilibrium, hence the name. The condition can be viewed as a sufficient condition that guarantees weak dependence and has been extensively studied in statistical physics and probability literature (see e.g. [28, 43]). As the spectral radius of any matrix is no more than its norm, a relaxation of the Dobrushin uniqueness condition is to restrict the spectral radius of to be less than . We show that (Lemma 16), so we can replace the dependence on with in Result II when the item values are weakly dependent (Theorem 5). We also show that the dependence on is necessary. Without any restriction on , the gap between and the optimal revenue could be unbounded even under the Dobrushin uniqueness condition for an additive or unit-demand buyer (Theorem 7). Next, we consider how the approximation guarantee degrades in terms of the inverse temperature of a MRF.

Inverse Temperature of a MRF

The inverse temperature is related to both the maximum weighted degree and the Dobrushin coefficient. See Definition 3 for the formal definition. Intuitively, as the inverse temperature increases (or temperature drops), the dependence between the different random variables strengthens. When the inverse temperature is , the MRF represents a product distribution. The high temperature regime is when the inverse temperature is less than . This parameter often controls when phase transitions in the behavior of MRFs happen, and hence the name. The Dobrushin coefficient always upper bounds the inverse temperature. Recently, MRFs in the high temperature regime have been applied to model weakly dependent random variables [22].

We show that if the MRF is in the high temperature regime, then its maximum weighted degree and the spectral gap of the Glauber dynamics has value at least . As a corollary of Result II, we have

-

Result III:

For a single XOS buyer, , where is the inverse temperature.

The result states that as long as the inverse temperature is bounded away from by any constant, achieves a constant fraction of the optimal revenue. Theorem 6 contains the formal statement of the result.

Maximum Weighted Degree Maximum Weighted Degree and Spectral Gap Spectral Gap or Dobrushin Coefficient Inverse Temperature Additive or Unit-Demand UB: (Theorem 2 and 1) LB: (Theorem 3) UB: () LB: () Unbounded (Theorem 7) UB: () LB: open XOS UB: open LB: () UB: (Theorem 4) LB: () Unbounded () UB: (Theorem 6) LB: open

1.2 Related Work

Simple vs. Optimal Auctions

There has been a large body of work on multi-item auction design focusing on either approximation results under item-independence [18, 19, 1, 15, 37, 4, 45, 41, 14, 21, 17] or impossibility to approximate under arbitrary dependence [8, 30]. Two types of models have been studied for items with limited dependence. The first model considers a specific type of dependence where each item’s value is a linear combination of “independent features” [20, 5]. Unlike MRFs, this model cannot express arbitrary structure of dependence. Indeed, the values of any two items can only be positively correlated under this model. The second model considers the smoothed complexity of the problem [38]. Their result applies to arbitrary dependence structure between the item values, but only achieves an approximation ratio that is exponential in the number of items. Our paper is the first to consider a model general enough to capture arbitrary structure of dependence and obtain parametric approximation ratios that are independent of the number of items.

MRFs and Weakly Dependent Random Variables

There has been growing interest in understanding the behavior of weakly dependent random variables that can be captured by a MRF in the high temperature regime or under the Dobrushin uniqueness condition [29, 26, 22]. In mechanism design, Brustle et al. [9] is the first to propose modeling dependent item values using MRFs in multi-item auctions, but they focus on the sample complexity of learning nearly optimal auctions.

2 Preliminaries

Basic Notation

We consider an auction where a seller is selling heterogeneous items to a single buyer. We denote the buyer’s type as , where is the buyer’s private information about item . We use to denote the distribution of , to denote the marginal distribution of , and to denote the distribution of conditioned on . We use to denote the support of distribution , and and . Moreover, we use to denote . For any item and any and , we use to denote , to denote , to denote , and to denote . We also define and . Finally, when the buyer’s type is , her valuation for a set of items is denoted by .

We investigate the performance of simple mechanisms for several well-studied valuation classes.

Definition 1 (Valuation Classes).

We define several classes of valuations formally.

-

•

Constrained Additive: interpret as the value of item , and , where is a downward closed set system over the items specifying the feasible bundles. When , the valuation is called Additive. When contains all the singletons and the empty set, the valuation is called unit-demand.

-

•

XOS/Fractionally Subadditive: interpret as that encodes all the possible values associated with item , and .

It is well known that the class of XOS valuations contains all constrained additive valuations.

Mechanism

A mechanism is specified by an allocation rule and a payment rule. We use to denote the allocation rule, and is the probability that the buyer receives item when she reports type . We also use to denote the buyer’s payment when she reports type . We assume the buyer has quasi-linear utility. We say a mechanism is Incentive Compatible (IC) if the buyer cannot increase their expected utility by misreporting their type, and Individual Rational (IR) if the buyer has non-negative expected utility when they report their type truthfully to the mechanism.

Given , valuation function , we use to denote the expected revenue of an IC and IR mechanism . We slightly abuse notation to use to denote the optimal revenue achievable by any IC and IR mechanism under distribution .

Throughout the paper, we use the following notations for the simple mechanisms we consider.

- denotes the optimal expected revenue achievable by any posted price mechanism, and we use SRev for short if there is no ambiguity. - denotes the optimal expected revenue achievable by selling a grand bundle and we use BRev for short if there is no ambiguity.

2.1 Markov Random Fields

Definition 2 (Markov Random Fields).

A Markov Random Field (MRF) is defined by a hypergraph . Associated with every vertex is a random variable taking values in some alphabet , as well as a potential function . Associated with every hyperedge is a potential function . In terms of these potentials, we define a probability distribution associating to each vector probability satisfying: ,where denotes and denotes .

We refer the interested readers to [35, 32] and the references therein for more details about MRFs. Throughout the paper, when we say the type distribution is a MRF over a hypergraph , if , , , and there exists a collection of potential functions and so that the corresponding distribution equals to . If there are only pairwise potentials, then is a graph. We say that a random variable is generated by a MRF, if is sampled from a distribution that is represented by the MRF.

Next, we define two ways to measure the degree of dependence in a MRF.

Definition 3.

Let random variable be generated by a Markov Random Field over a hypergraph , we define the Markov influence between item and to be: . We further define the inverse temperature of the MRF as . We say random variable/type is in the high temperature regime if .

Definition 4.

Given a random variable/type generated by a Markov Random Field over a hypergraph , we define the weighted degree of item as: , and the maximum weighted degree as .

Remark 1.

Both and capture the degree of dependence between the items. Note that for any MRF , and it is possible that , where is the size of the largest hyperedge in . When is drawn from a product measure, both and are . In general, restricting and to be small ensures that the item values are only weakly dependent.

To achieve our results, we need another important concept – the Glauber dynamics. In Section 5, we relate the approximation ratio achievable by simple mechanisms to the spectral gap of the Glauber dynamics of the MRF.

Definition 5 (Glauber Dynamics).

Let be an -dimensional random vector drawn from distribution . Let be the support of . The Glauber dynamics for is a reversible Markov chain with state space . The Glauber chain moves from state as follows: an index is chosen uniformly at random from , and a new state is chosen so that (i) for all ; (ii) draw from the conditional distribution . It is not hard to verify that the Glauber dynamics is a reversible Markov chain with stationary distribution .

Remark 2.

When is the distribution that can be represented by a MRF , the Glauber dynamics has state space . The Glauber chain moves from state as follows: a vertex is chosen uniformly at random from , and a new state is chosen so that (i) for all ; (ii) for any , w.p. , in other words, sample according to the distribution conditioned on . Note that for a MRF, the Glauber dynamics is an irreiducible Markov chain, so is its only stationary distribution. The Glauber dyanamics is a standard method for generating samples from a MRF, as it does not require computing the partition function, which is often a computationally intractable task.

3 Markov Random Fields: Basic Properties and Tools

We first present some basic properties of a MRF. Roughly speaking, we show that the conditional distribution can be approximated by the corresponding marginal distribution of , and the approximation quality only depends .

Lemma 1.

Let random variable be generated by a MRF. Then for any :

and

Proof.

Note that for any , .

Clearly,

Since ,

By Law of Total Probability,

∎

Lemma 2.

Let random variable be generated by a MRF. For any and any set and set :

Prophet Inequality for MRF

Equipped with Lemma 2, we provide a generalization of the Prophet inequality when the rewards in different stages are dependent and generated by a MRF. We can think of the prophet inequality problem, as finding a good policy for a gambler in a multi-round game. At the -th round, the gambler is given the choice to accept a reward or to continue to the next round. The goal of the gambler is to find a policy that obtains high expected reward, given the distributions of the rewards at each round. Prophet inequalities have been obtained when the rewards between stages are independent [34, 42, 33] or can be expressed a a linear combination of some independent random variables [31].

Lemma 3.

Let be an -dimensional random vector generated by a MRF. There are totally rounds, and the reward of round is , where is an arbitrary function. The total reward of the prophet is . We denote by the expected of reward of the following policy – accept any reward that is at least . The following inequality holds if we choose (i.e., ),

Proof.

The proof is similar to the case when all are independent.

It is not hard to see that

We provide a lower bound on .

For every , we define the set as and as . Note that

The inequality is due to Lemma 2. Putting everything together, we know that

which is at least of the upper bound we provide for . 101010When is a discrete distribution, we may not be able to pick a such that , but it is folklore that this can be resolved by carefully picking a tie-breaking rule. We do not include the details here. ∎

4 Simple Mechanisms for a Unit-Demand or Additive Buyer under MRF

In this section, we first use the duality framework from [14, 17] to construct an upper bound of . Next, we prove that if the buyer has either unit-demand or additive valuation across the items, is a -approximation or a -approximation of , respectively.

4.1 Benchmark of the Optimal Revenue for Constrained Additive Valuations

In this section, we use the duality framework from [14, 17] to construct an upper bound of . We describe a benchmark of the optimal revenue for all constrained additive valuations. Deriving a benchmark for XOS valuations requires some extra care, and we provide details of the derivation in Section 5.1 when we study XOS valuations. We first remind the readers the partition of type space used in [14, 17].

Definition 6 (Partition of the Type Space for Constrained Additive Valuations [14, 17]).

We partition the type space into regions, where . If , we call item the favorite item of type .

To handle the dependence across the items, we introduce some new notations to specify the benchmark.

Definition 7 (Ironed Virtual Value).

Let be the type distribution. For any , we use to denote the ironed Myerson’s virtual value for distribution , to denote the ironed Myerson’s virtual value when we ironed over interval .

If is a regular distribution and ,

Moreover, always satisfies the following property:

where .

Lemma 4 (Benchmark of Optimal Revenue for Constrained Additive Valuations).

Given a distribution over the type space , and a mechanism , if the buyer’s valuation is constrained additive, then we have the following benchmark:

where .

Single-Dimensional Copies Setting:

In the analysis of unit-demand bidders with independent items [19, 14], the optimal revenue is upper bounded by the optimal revenue in the single-dimensional copies setting defined in [19]. We make use of the same technique in our analysis. There is a single item for sale, and we construct agents, where agent has value for winning the item. Notice that this is a single-dimensional setting, as each agent’s type is specified by a single number.

4.2 A Unit-Demand Buyer

In this section, we show that a simple posted price mechanism can extract fraction of the optimal revenue when the type distribution is a MRF. We first use the revenue of the Ronen’s lookahead auction [40] to upper bound the benchmark from Lemma 4. 111111 Ronen’s lookahead auction considers the setting where the seller is selling a single item to a set of buyers, whose values for the item are correlated. Ronen’s auction first identifies the highest bidder, and offers a take it or leave it price to the highest bidder to maximize the revenue conditioned on the other bidders’ types. The proof follows from the definition of Ronen’s lookahead auction and basic properties of MRF presented in Lemma 1 and 2. We postpone the proof to Appendix B.

Lemma 5.

Let the type distribution be represented by a MRF, be any IC and IR mechanism for a unit-demand buyer, and be revenue of the Ronen’s lookahead auction [40] in the Copies settings with respect to . The following inequalities hold:

Equipped with Lemma 5, we can apply the prophet inequality for MRF to show that a posted-price mechanism can obtain expected revenue that is at least . We delay the proof to Appendix B.

Theorem 1.

Let the type distribution be represented by a MRF. If the buyer’s valuation is unit-demand, then there exists a posted-price mechanism with prices that obtains expected revenue at least .

Is it possible to improve the dependence on ? In Theorem 8, we show that if we use the optimal revenue in the COPIES setting as a benchmark of the optimal revenue in the original setting, then the exponential dependence on is unavoidable.

4.3 An Additive Buyer

In this section, we show that is a approximation of the optimal revenue when the type distribution is a MRF. We denote by the revenue of Myerson’s auction for selling item only. We use to denote SRev, as the revenue collected from item only depends on the marginal distribution . We first upper bound the terms Single and Tail by . The proof follows from a combination of the standard analysis of the terms Single and Tail from [14, 17] with properties of MRFs (Lemma 2). We postpone the proof to Appendix C.

Lemma 6.

Let the type distribution be a MRF and be any IC and IR mechanism for an additive buyer. The following inequalities holds: and .

Finally, we analyze the Core. We define new random variables . Let . Note that . We first provide an upper bound on , and show that if we sell the grand bundle at an appropriate price, its revenue is close to the Core. Note that under the item-independence assumption, it is not hard to show that is upper bounded by [4, 14]. However, this analysis does not extend to the case where the buyer type is generated by a MRF. We first obtain a new upper bound of . As , we have . We further bound by using the standard analysis in [4, 14] and each covariance using properties of MRF (Lemma 2). The proof is postponed to Appendix C.

Lemma 7.

Let the type distribution be represented by a MRF. For any , . Moreover, .

In the item-independence case, the standard analysis [4, 14] applies Chebyshev’s inequality to show that the seller can sell the grand bundle at price with probability at least , which implies that Core is . As our upper bound on is a lot larger, Chebyshev’s inequality only gives a vacuous bound on the sell probability. 121212In particular, if we set the price to be for any constant and , Chebyshev’s inequality tells us that the probability that the buyer cannot afford the grand bundle is at most . However, our upper bound of will be larger than , if and is much larger than . In this case, is larger than making the bound useless. To show that selling the grand bundling is a good approximation of the Core, we set the price of the grand bundle differently and use the Paley-Zygmund inequality to prove that either the sell probability is high or the Core is within a constant factor of . The proof of Theorem 2 can be found in Appendix C.

Theorem 2.

Let the type distribution be represented by a MRF. If the buyer’s valuation is additive, then

In the following theorem, we show that the approximation ratio must have polynomial dependence on . Our proof is based on a modification of the hard instance by Hart and Nisan [30]. They construct a joint distribution over two items with support size and show that the optimal revenue is at least . Unfortunately, their construction requires to be infinite. We show how to modify their construction so that the new distribution has maximum weighted degree , and the gap between the optimal revenue and remains to be . The key is to show that under the new distribution, no type shows up too rarely, and the optimal revenue, SRev, and BRev remain roughly the same. The proof is postponed to Appendix F.

Theorem 3.

For any sufficiently large , there exists a type distribution over two items represented by a MRF such that (i) the maximum weighted degree is at most , where is an absolute constant; (ii) for an additive buyer whose type is sampled from , there exists an absolute constant such that .

5 Simple Mechanisms for a XOS Buyer

5.1 Duality Framework for XOS Valuations

The benchmark is obtained using essentially the same approach as in [17]. Suppose the buyer has a XOS valuation function . We denote by . We abuse this notation and we also define for , , where is the all vector. We summarize the benchmark for a XOS buyer in the following Lemma. More details can be found in Appendix E.

Lemma 8.

Partition the type space into regions, where

Let be the revenue of the optimal posted price mechanism that allows the buyer to purchase at most one item. Let . For any IC and IR Mechanism , we can bound its revenue by:

5.2 Approximating the Benchmark of a XOS Buyer

In this section, we show how to approximate the optimal revenue of a buyer with a XOS valuation. We first upper bound the term Single and Tail . The analysis of both terms follows from the combination of the analysis in [17] and Lemma 2.

Lemma 9.

Let the type distribution be represented by a MRF. If is an IC and IR mechanism for a buyer with a XOS valuation, then the following inequalities hold

and

where SRev is the revenue of the optimal posted price auction, in which the buyer is allowed to purchase at most one item.

5.2.1 Bounding the Core using the Poincaré Inequality

In this section, we show how to bound the Core for a XOS buyer. The Core is the expectation of the random variable . To show that bundling can achieve a good approximation of the Core, we need to upper bound the variance of . This is the main task of this section. As is not additive across the items, our method for the additive valuation (see Lemma 7) no longer applies. We provide a new approach that is based on the Poincaré Inequality and the self-boundingness of XOS functions. We first state the Poincaré Inequality.

Lemma 10 (The Poincaré Inequality (adapted from Lemma 13.12 of [36])).

Let be a reversible transition matrix on state space with stationary distribution . For any function , let

If , then

where is the spectral gap of . 131313It is well-known that the largest eigenvalue of is , and the spectral gap of is the difference between ’s largest and second largest eigenvalues. Moreover, there exists a function , such that

Next, we apply Lemma 10 to the Glauber dynamics of the MRF that generates the buyer’s type.

Lemma 11.

Let be the joint distribution of random variables and be the transition matrix of the Glauber dynamics for . For any function , we have

where is the spectral gap of . Moreover, there exists a function , such that the inequality is tight.

Remark 3.

Lemma 11 is a generalization of the well-known Efron-Stein inequality to dependent random variables. Indeed, when is a product measure, is at least and we recover the Efron-Stein inequality. As we demonstrate in Section 6, is at least under many well-studied conditions of weak dependence, such as the Dobrushin uniqueness condition.

Proof of Lemma 11: According to the definition of the Glauber dynamics, is a reversible transition matrix on state space with stationary distribution . Lemma 10 states that

| (1) |

By the definition of the Glauber dynamics, the RHS of Inequality (1) is equivalent to

The second equality is because and are two i.i.d. samples from .

Hence,

Recall that to bound the Core, we need to upper bound the variance of the random variable . By choosing to be and applying Lemma 11, we can instead upper bound the RHS of the inequality in Lemma 11. A priori, it is not clear that the RHS would be easier to bound. In the following sequence of Lemmas, we show that the RHS is indeed more amenable to analysis. We first argue that the function has a key property known as self-boundingness, using which we then upper bound the RHS by and show that SRev and BRev can approximate the Core.

Definition 8 (Self-Bounding Functions [7]).

Let be an arbitrary set and be a subset of . We say that a function is -self-bounding with some constant if there exists a collection of functions for each with , such that for each the followings hold:

-

•

for all .

-

•

.

We next argue that for a self-bounding function, the RHS of the inequality in Lemma 11 is upper bounded by its mean.

Lemma 12.

Let be the joint distribution of random variables . If is a -self-bounding function, then

Proof.

Recall the following property of the variance: For any real-value random variable , . In other words, for any . Therefore, for any ,

Using this relaxation, we proceed to prove the claim.

The first inequality follows from the relaxation. The second and last inequality follow from the first and second property of a self-bounding function respectively. ∎

Lemma 13.

Let be the joint distribution of random variables and be the transition matrix of the Glauber dynamics for . For any -self-bounding function , we have

where is the spectral gap of .

Definition 8 may seem obscure at first, but many natural functions are indeed self-bounding. For example, if is and is the additive function, then is -self-bounding. We show that the function is -self-bounding and its variance is no more than . Here, we first specialize our analysis to MRFs. The main difference is that the Glauber dynamics for a MRF is irreducible, so the spectral gap is strictly positive (Lemma 12.1 of [36]). The proof is postponed to Appendix D.

Lemma 14.

Let . The function is -self-bounding and , where is the spectral gap of the transition matrix of the Glauber dynamics of the MRF that generates the buyer’s type.

Now, we show how to approximate Core using SRev and BRev.

Lemma 15.

Let the buyer’s type distribution be represented by a MRF, be the transition matrix of the Glauber dynamics of the MRF, and be the spectral gap of . We have

Proof.

According to Lemma 14, is a -self-bounding function and . If , then the statement holds. If , then . By Paley-Zygmund inequality we have that:

Therefore we have that: , which implies that the statement.

∎

Finally, we combine our analysis of Single, Tail, and Core to obtain the approximation guarantee for a XOS buyer.

Theorem 4.

Let the buyer have a XOS valuation and her type distribution be represented by a MRF. We use to denote the spectral gap of matrix – the transition matrix of the Glauber dynamics of the MRF. Then .

6 Connection to other Weak Dependence Conditions

A common way to measure the degree of dependence of a high-dimensional distribution is by considering its Dobrushin Interdependence Matrix. In this section, we show that for several natural sufficient conditions that guarantee weak dependence in the distribution, the spectral gap of the Glauber dynamics transition matrix is . We begin by defining the Dobrushin interdependence matrix.

Definition 9 (-Dobrushin Interdependence Matrix [44]).

Let be a metrical, complete and separable space. For two distributions and supported on , their -Wasserstein distance is defined as: , where is the set of valid coupling such that its marginal distributions are and .

Let be a -dimensional random vector supported on and be the conditional distribution of knowing . Define the -Dobrushin Interdependence Matrix by

and for all .

Remark 4.

captures how strong the value of affects the conditional distribution of when all other coordinates are fixed. Higher value implies stronger dependence between and . When all the coordinates of are independent, is the all zero matrix.

Dobrushin uniqueness condition:

If we choose to be the trivial metric , then is exactly the total variation distance. The influence matrix mentioned in Section 1 is exactly the Dobrushin interdependence matrix with respect to the trivial metric. To remind the audience, the Dobrushin Coefficient is defined as when is the influence matrix. If , we say satisfies the Dobrushin uniqueness condition. As is at least as large as ’s spectral radius , 141414 is the dominant eigenvalue of by the Perron-Frobenius Theorem. a weaker condition than the Dobrushin uniqueness condition is that the spectral radius is strictly less than .

We argue that even the weaker condition that implies that the spectral gap of the transition matrix of the Glauber dynamics .

Lemma 16.

Let be any metric, for any -dimensional random vector , , where is the spectral gap of the transition matrix of the Glauber dynamics for .

Proof.

By Lemma 11, there exists a function , such that

The following result by Wu [44] provides a generalization of the Efron-Stein inequality for weakly dependent random variables.

Lemma 17 (Poincaré Inequality for Weakly Dependent Random Variables - Theorem 2.1 in [44]).

Let be an -dimensional random vector drawn from distribution that is supported on . For any metric on , let be the -Dobrushin interdependence matrix for . Let be the spectral radius of . If for some fixed and , then for any square integrable function w.r.t. distribution , the following holds:

If we choose to be in Lemma 17, we have that :

Combining the two inequalities conclude the proof ∎

Combining Lemma 16 with Theorem 4, we immediately have the following Theorem. 151515A major benefit of using or the Dobrushin coefficient rather than is that these parameters are easier to estimate than given the joint distribution.

Theorem 5.

Let the buyer have a XOS valuation, her type distribution be represented by a MRF, and be the spectral radius of the -Dobrushin interdependence matrix of under some metric . If , then .

High Temperature MRFs.

Using Theorem 5, we show that when the MRF is in the high temperature regime, i.e., (see Definition 3), is a constant factor approximation to the optimal revenue. By the definition of , it clear that . Next, we show that is also an upper bound of for the trivial metric .

Lemma 18.

Let be the trivial metric . For any MRF , . Moreover, for all .

Proof.

follows the elementary fact that the spectral radius is upper bounded by the infinity norm. To prove , we first need the following definition and lemma.

Definition 10.

[22] Let be a random variable over , and denote its probability distribution. Assume on all . For any , define the log influence between and as

Lemma 19 (Adapted from Lemma 5.2 of [23]).

Let be a random variable , for any , .

We only need to prove that is no more than . Since random variable is generated by a MRF,

which is clearly no greater than .

Since for any , we have . ∎

Theorem 6.

Let the buyer’s type distribution be represented by a MRF. If the buyer’s a XOS valuation and her type is in the high temperature regime, i.e., ,

7 Impossibility Results

In this section we present some of our impossibility results. In Section 7.1, we show that the Dobrushin Uniqueness condition alone is insufficient to guarantee any multiplicative approximation of the optimal revenue using SRev and BRev. In Section 7.2 we construct a MRF such that the optimal revenue in the COPIES setting is times larger than .

7.1 Inapproximability under Only the Dobrushin Uniqueness Condition

Readers may wonder whether it is possible to prove an approximation ratio that only relies on either the spectral radius , the Dobrushin coefficient , or the spectral gap of the Glauber dynamics , but independent of the maximum weighted degree . We show that this is impossible. Indeed, we prove that for any , and any ratio , there exists a MRF with such that the ratio between the optimal revenue and is at least . Our result is based on a modification of the Hart-Nisan construction [30].

Theorem 7.

For any positive real number and any choice of , there exists a type distribution over items generated by a MRF with Dobrushin coefficient and finite inverse temperature, such that for an additive buyer whose type is sampled from , .

First we present the main building block of our construction.

Lemma 20.

Let be a correlated valuation distribution over items with Dobrushin coefficient . Let be a product distribution that has the same marginal distributions as . Then for any , we consider the distribution , that is, if we want to sample from , we can take a sample from with probability and take a sample from with probability . Distribution can be modeled as a MRF with finite inverse temperature such that , where and has Dobrushin coefficient . Furthermore, has the same marginal distribution as and .

Proof.

Assume that , where and are the marginals of . Let and . Let be the influence matrix of and be the influence matrix of . Note that the diagonal entries of and of are zero. We have that:

In the statement of the lemma, we assumed that . We can easily infer the following: . This concludes the fact that has .

Now we prove that can be modeled as a MRF with finite inverse temperature. We consider a MRF with potential functions , and . Since Distribution samples from the product distribution with probability , we have that for each , . This is true because with probability we sample from the product distribution , and with probability at least we sample the type , therefore the MRF we just described has finite inverse temperature and . In the case where the distribution is over two items, . Moreover we can easily verify that the MRF we just described has the same joint distribution as . Therefore can be modeled as a MRF with finite inverse temperature.

We now prove that . This is true because we can simply use the optimal mechanism that induces on . Since take a sample from with probability , we are guaranteed that this mechanism has revenue at least on .

The fact that has the same marginal distributions as follows from the sampling procedure. ∎

We also need the following important result from [30].

Lemma 21 (Theorem A from [30]).

For any positive number , there exists a two item correlated distribution , such that for an additive buyer whose type is sampled from , .

Proof of Theorem 7: Let be the distribution over two items that is guaranteed to exist by Lemma 21. Since is a two dimensional distribution, its Dobrushin coefficient is at most .

Apply Lemma 20 to with parameter to create another distribution which has the same marginals as but with a Dobrushin coefficient at most . Moreover, can be expressed as a MRF with finite inverse temperature. Clearly, , as one can simply achieve the RHS under distribution using the optimal mechanism designed for . Also, as the two distributions have the same marginals. Finally, . Suppose is the optimal price for the bundle, then we can set the two items separately each at price . Clearly, whenever the bundle is sold, at least one item is sold. To conclude, .

7.2 Lower Bound for the Copies Setting

In this section, we show that if the analysis uses the optimal revenue in the COPIES setting as part of the benchmark for the optimal revenue in the original setting (as in our analysis), the exponential dependence on the maximum weighted degree in the approximation ratio is unavoidable. Note that we also showed that the approximation ratio must have polynomial dependence on no matter what approach is used (Theorem 3).

Theorem 8.

For any value of and there exists a type distribution over items, such that can be represented by a MRF with only pairwise potentials and maximum weighted degree . Moreover, for an additive or unit-demand buyer, the expected optimal revenue in the COPIES settings w.r.t. can be arbitrarily close to , while .

Proof of Theorem 8: We construct the MRF in the following way. The first item has support , where is going to be defined later. Let be some tiny non-negative values, and the support of the other items’ distributions is . We consider the following node potential for the first item:

The node potentials for the other items is: for all and .

Note that and , therefore for each , we can map it to a unique . Formally, we consider a bijective function .

We define pair-wise potentials between the first item and the -th item:

It is easy to verify that for the constructed MRF.

Let be the normalizing constant so that the MRF with potentials is a valid distribution. That is . For any we have that: .

Thus for any , the marginal probability: . Note that and . Therefore the marginal distribution of the first item is an Equal Revenue Distribution, which means that the revenue of any posted price mechanism for the first item, cannot be more than . Moreover, if we choose to be sufficiently small so that , then any posted price mechanisms for the rest items has revenue less or equal than . Thus .

Now we consider the following Mechanism in the copies settings. We first collect the values for all buyers except the first one , then let the first buyer decide whether she wants to purchase the item at price . This is essentially Ronen’s lookahead auction [40]. A lower bound on the revenue of this mechanism in the COPIES settings is:

Where the last inequality follows from the definition of .

Note that if we fix and , and let , then .

Therefore as , the lower bound of the revenue of the proposed mechanisms becomes . Since we assumed that the value of the agent for each item except the first is less or equal than , then the value of the agent for all but the first item is less or equal than . This implies that if the agent buys the whole bundle at price , then she also buys the first item at price . Let be the revenue of the posted price mechanism on the first item. Since the marginal of the fist item is the Equal Revenue Distribution, then . Moreover by the argument described above, we have that . Thus .

Acknowledgement.

The authors would like to thank Jessie Huang for creating Figure 1 and to thank Costis Daskalakis for helpful discussions in the early stages of the paper.

References

- [1] Saeed Alaei. Bayesian Combinatorial Auctions: Expanding Single Buyer Mechanisms to Many Buyers. In the 52nd Annual IEEE Symposium on Foundations of Computer Science (FOCS), 2011.

- [2] Saeed Alaei, Hu Fu, Nima Haghpanah, Jason Hartline, and Azarakhsh Malekian. Bayesian Optimal Auctions via Multi- to Single-agent Reduction. In the 13th ACM Conference on Electronic Commerce (EC), 2012.

- [3] Saeed Alaei, Hu Fu, Nima Haghpanah, and Jason D. Hartline. The simple economics of approximately optimal auctions. In 54th Annual IEEE Symposium on Foundations of Computer Science, FOCS 2013, 26-29 October, 2013, Berkeley, CA, USA, pages 628–637. IEEE Computer Society, 2013.

- [4] Moshe Babaioff, Nicole Immorlica, Brendan Lucier, and S. Matthew Weinberg. A simple and approximately optimal mechanism for an additive buyer. In 55th IEEE Annual Symposium on Foundations of Computer Science, FOCS 2014, Philadelphia, PA, USA, October 18-21, 2014, pages 21–30, 2014.

- [5] MohammadHossein Bateni, Sina Dehghani, MohammadTaghi Hajiaghayi, and Saeed Seddighin. Revenue maximization for selling multiple correlated items. In Algorithms-ESA 2015, pages 95–105. Springer, 2015.

- [6] Anand Bhalgat, Sreenivas Gollapudi, and Kamesh Munagala. Optimal auctions via the multiplicative weight method. In Michael J. Kearns, R. Preston McAfee, and Éva Tardos, editors, ACM Conference on Electronic Commerce, EC ’13, Philadelphia, PA, USA, June 16-20, 2013, pages 73–90. ACM, 2013.

- [7] Stéphane Boucheron, Gábor Lugosi, and Pascal Massart. A sharp concentration inequality with applications. Random Struct. Algorithms, 16(3):277–292, 2000.

- [8] Patrick Briest, Shuchi Chawla, Robert Kleinberg, and S Matthew Weinberg. Pricing lotteries. Journal of Economic Theory, 156:144–174, 2015.

- [9] Johannes Brustle, Yang Cai, and Constantinos Daskalakis. Multi-item mechanisms without item-independence: Learnability via robustness. EC ’20, page 715–761, New York, NY, USA, 2020. Association for Computing Machinery.

- [10] Yang Cai and Constantinos Daskalakis. Extreme-Value Theorems for Optimal Multidimensional Pricing. In the 52nd Annual IEEE Symposium on Foundations of Computer Science (FOCS), 2011.

- [11] Yang Cai, Constantinos Daskalakis, and S. Matthew Weinberg. An Algorithmic Characterization of Multi-Dimensional Mechanisms. In the 44th Annual ACM Symposium on Theory of Computing (STOC), 2012.

- [12] Yang Cai, Constantinos Daskalakis, and S. Matthew Weinberg. Optimal Multi-Dimensional Mechanism Design: Reducing Revenue to Welfare Maximization. In the 53rd Annual IEEE Symposium on Foundations of Computer Science (FOCS), 2012.

- [13] Yang Cai, Constantinos Daskalakis, and S. Matthew Weinberg. Understanding Incentives: Mechanism Design becomes Algorithm Design. In the 54th Annual IEEE Symposium on Foundations of Computer Science (FOCS), 2013.

- [14] Yang Cai, Nikhil R. Devanur, and S. Matthew Weinberg. A duality based unified approach to bayesian mechanism design. In the 48th Annual ACM Symposium on Theory of Computing (STOC), 2016.

- [15] Yang Cai and Zhiyi Huang. Simple and Nearly Optimal Multi-Item Auctions. In the 24th Annual ACM-SIAM Symposium on Discrete Algorithms (SODA), 2013.

- [16] Yang Cai and Mingfei Zhao. Simple mechanisms for subadditive buyers via duality. CoRR, abs/1611.06910, 2016.

- [17] Yang Cai and Mingfei Zhao. Simple mechanisms for subadditive buyers via duality. In the 49th Annual ACM Symposium on Theory of Computing (STOC), 2017.

- [18] Shuchi Chawla, Jason D. Hartline, and Robert D. Kleinberg. Algorithmic Pricing via Virtual Valuations. In the 8th ACM Conference on Electronic Commerce (EC), 2007.

- [19] Shuchi Chawla, Jason D. Hartline, David L. Malec, and Balasubramanian Sivan. Multi-Parameter Mechanism Design and Sequential Posted Pricing. In the 42nd ACM Symposium on Theory of Computing (STOC), 2010.

- [20] Shuchi Chawla, David L. Malec, and Balasubramanian Sivan. The power of randomness in bayesian optimal mechanism design. In David C. Parkes, Chrysanthos Dellarocas, and Moshe Tennenholtz, editors, Proceedings 11th ACM Conference on Electronic Commerce (EC-2010), Cambridge, Massachusetts, USA, June 7-11, 2010, pages 149–158. ACM, 2010.

- [21] Shuchi Chawla and J. Benjamin Miller. Mechanism design for subadditive agents via an ex-ante relaxation. In Vincent Conitzer, Dirk Bergemann, and Yiling Chen, editors, Proceedings of the 2016 ACM Conference on Economics and Computation, EC ’16, Maastricht, The Netherlands, July 24-28, 2016, pages 579–596. ACM, 2016.

- [22] Yuval Dagan, Constantinos Daskalakis, Nishanth Dikkala, and Siddhartha Jayanti. Learning from weakly dependent data under dobrushin’s condition. In Alina Beygelzimer and Daniel Hsu, editors, Conference on Learning Theory, COLT 2019, 25-28 June 2019, Phoenix, AZ, USA, volume 99 of Proceedings of Machine Learning Research, pages 914–928. PMLR, 2019.

- [23] Yuval Dagan, Constantinos Daskalakis, Nishanth Dikkala, and Siddhartha Jayanti. Learning from weakly dependent data under dobrushin’s condition. CoRR, abs/1906.09247, 2019.

- [24] Constantinos Daskalakis, Nikhil R. Devanur, and S. Matthew Weinberg. Revenue maximization and ex-post budget constraints. In Tim Roughgarden, Michal Feldman, and Michael Schwarz, editors, Proceedings of the Sixteenth ACM Conference on Economics and Computation, EC ’15, Portland, OR, USA, June 15-19, 2015, pages 433–447. ACM, 2015.

- [25] Constantinos Daskalakis, Nishanth Dikkala, and Gautam Kamath. Testing ising models. In Proceedings of the Twenty-Ninth Annual ACM-SIAM Symposium on Discrete Algorithms, pages 1989–2007. Society for Industrial and Applied Mathematics, 2018.

- [26] Constantinos Daskalakis, Nishanth Dikkala, and Gautam Kamath. Testing ising models. IEEE Transactions on Information Theory, 65(11):6829–6852, 2019.

- [27] PL Dobruschin. The description of a random field by means of conditional probabilities and conditions of its regularity. Theory of Probability & Its Applications, 13(2):197–224, 1968.

- [28] RL Dobrushin and SB Shlosman. Completely analytical interactions: constructive description. Journal of Statistical Physics, 46(5-6):983–1014, 1987.

- [29] Reza Gheissari, Eyal Lubetzky, Yuval Peres, et al. Concentration inequalities for polynomials of contracting ising models. Electronic Communications in Probability, 23, 2018.

- [30] Sergiu Hart and Noam Nisan. Selling multiple correlated goods: Revenue maximization and menu-size complexity. Journal of Economic Theory, 183:991 – 1029, 2019.

- [31] Nicole Immorlica, Sahil Singla, and Bo Waggoner. Prophet inequalities with linear correlations and augmentations. In Péter Biró, Jason Hartline, Michael Ostrovsky, and Ariel D. Procaccia, editors, EC ’20: The 21st ACM Conference on Economics and Computation, Virtual Event, Hungary, July 13-17, 2020, pages 159–185. ACM, 2020.

- [32] Ross Kindermann and Laurie Snell. Markov random fields and their applications, volume 1. American Mathematical Society, 1980.

- [33] Robert Kleinberg and S. Matthew Weinberg. Matroid Prophet Inequalities. In the 44th Annual ACM Symposium on Theory of Computing (STOC), 2012.

- [34] Ulrich Krengel and Louis Sucheston. On semiamarts, amarts, and processes with finite value. Probability on Banach spaces, 4:197–266, 1978.

- [35] Steffen L. Lauritzen. Graphical Models. Oxford University Press, 1996.

- [36] David A. Levin, Yuval Peres, and Elizabeth L. Wilmer. Markov chains and mixing times. American Mathematical Soc., Providence, 2009.

- [37] Xinye Li and Andrew Chi-Chih Yao. On revenue maximization for selling multiple independently distributed items. Proceedings of the National Academy of Sciences, 110(28):11232–11237, 2013.

- [38] Alexandros Psomas, Ariel Schvartzman, and S Matthew Weinberg. Smoothed analysis of multi-item auctions with correlated values. In Proceedings of the 2019 ACM Conference on Economics and Computation, pages 417–418, 2019.

- [39] Dana Randall. Slow mixing of glauber dynamics via topological obstructions. In Symposium on Discrete Algorithms: Proceedings of the seventeenth annual ACM-SIAM symposium on Discrete algorithm, volume 22, pages 870–879, 2006.

- [40] Amir Ronen. On approximating optimal auctions. In Michael P. Wellman and Yoav Shoham, editors, Proceedings 3rd ACM Conference on Electronic Commerce (EC-2001), Tampa, Florida, USA, October 14-17, 2001, pages 11–17. ACM, 2001.

- [41] Aviad Rubinstein and S. Matthew Weinberg. Simple mechanisms for a subadditive buyer and applications to revenue monotonicity. In Proceedings of the Sixteenth ACM Conference on Economics and Computation, EC ’15, Portland, OR, USA, June 15-19, 2015, pages 377–394, 2015.

- [42] Ester Samuel-Cahn et al. Comparison of threshold stop rules and maximum for independent nonnegative random variables. the Annals of Probability, 12(4):1213–1216, 1984.

- [43] Daniel W Stroock and Boguslaw Zegarlinski. The logarithmic sobolev inequality for discrete spin systems on a lattice. Communications in Mathematical Physics, 149(1):175–193, 1992.

- [44] Liming Wu. Poincaré and transportation inequalities for gibbs measures under the dobrushin uniqueness condition. Ann. Probab., 34(5):1960–1989, 09 2006.

- [45] Andrew Chi-Chih Yao. An n-to-1 bidder reduction for multi-item auctions and its applications. In SODA, 2015.

Appendix A Missing Details of the Duality-base Benchmark

We provide the necessary information to derive the benchmark for XOS valuations in Appendix E. Deriving a benchmark for a constrained additive valuation is a simpler task. We summarize the benchmark for a constrained additive valuation in Definition 11.

Definition 11.

The duality framework provide the following bound:

Lemma 22.

We can bound Non-Favorite by Core and Tail. More specifically,

Proof.

∎

Appendix B Missing Proofs from Section 4.2

Proof of Lemma 5:

For the term Single we have that:

| (2) |

According to Definition 7, , which is exactly the revenue of Ronen’s auction when bidder has the highest value and the other bidders have value . This completes the proof that .

As the buyer has unit-demand valuation, the Non-Favorite term is at most the revenue of the second price auction in the Copies settings. The second price auction can be viewed as a special case Ronen’s mechanism, in which the price is always set to be the same as the second highest bid. Hence, .

Recall that:

Due to Lemma 2,

Proof of Theorem 1: Let . We let price . We first provide a lower bound of the revenue of the posted-price mechanism under the prices .

For each item , let denote the event and denote the event . Clearly, the buyer buys item in event , so the revenue of the posted-price mechanism is at least

Note that and . Hence, the RHS of the inequality above is lower bounded by

The inequality is due to the union bound. By Lemma 3, the lower bound is at least . Combining this conclusion with Lemma 5, the revenue of the posted-price mechanism is at least .

Appendix C Missing Proofs from Section 4.3

Proof of Lemma 6:

The first equality is due to the definition of (Definition 7). The second inequality follows from Lemma 2. The third and last inequalities follow from the definition of and .

Similarly, we can bound the term Tail.

First, note that . Therefore

The second inequality is due to Lemma 2. The third inequality follows from the union bound. The fourth and sixth inequalities hold because and .

Proof of Lemma 7: We have that:

The inequality follows from Lemma 2. Therefore, .

Note that .

Using Lemma 9 from [14], we can bound by . Hence,

Proof of Theorem 2: First we present the Paley-Zygmund inequality. For a non-negative random variable , Paley-Zygmund inequality implies that for we have that:

By the Paley-Zygmund inequality and Lemma 7, we derive the following inequality:

| (3) |

If , then according to Lemma 6,

Otherwise, Equation (3) implies that

Therefore, if we sell the grand bundle at price , it will be sold with probability at least . Thus .

Combining everything, we have

Appendix D Missing Proofs from Section 5

Proof of Lemma 9:

We use to denote SRev. We remind the readers that we use to denote SRev, which is the revenue of the optimal posted price auction, in which we only allow the buyer to purchase at most one item.

We note that Single term in the XOS case, is the same as the the Single term in the Unit-Demand case in Section 4.2, if we consider that the buyer has valuation for the -th item. In section 4.2, using Lemma 5 we proved that . Therefore it is enough to prove that there exists a posted price mechanism that allows the buyer to only pick her favorite item such that its revenue is at least . A corollary of Theorem 1 is that there exists a posted price Mechanism such that , which concludes the proof for the term Single.

Next, we consider the term Tail. We remind the readers that is a cutoff we use to separate the and the term. The reason we chose this specific value is that we can bound the sum of the marginal probability that any item has value greater or equal than .

Lemma 23.

We have that:

Proof.

We can lower bound as the sum of the following disjoint events:

Using Lemma 2 with sets and , we have that:

Note that . This is true because if we set the price of every item at , then if any item is bought with probability greater than , we have revenue greater than , a contradiction. Moreover . By these observations, we can conclude that:

which implies that .

∎

Now we are going to bound the term Tail.

For any fixed , using Lemma 2 on sets and we have that:

We consider the mechanism that posts price at each item except item , and allows the buyer to get her favorite item. The expected revenue of this mechanisms is exactly , which is at most . This implies that:

Where the last inequality follows from Lemma 23.

Proof of Lemma 14: Define , where . When , . When , . Additionally, and . Since is a XOS function, there exists non-negative numbers such that and . Therefore, .

Combining Lemma 11, 12, and the fact that is -self-bounding, we derive the stated upper bound of the variance of .

Appendix E Missing Details of the Revenue Benchmark for a XOS Buyer

Similar to [17], we are going to apply the duality framework on a relaxed version of the valuation function.

Definition 12 (Relaxed Valuation (Definition 5 from [16])).

We define the relaxed subadditive valuation the following way:

The reason that we consider the relaxed valuation function is because that is “additive” across the favorite item and the rest of the items, and this “additivity” plays a crucial role in obtaining an analyzable dual. Due to the non-monotonicity of the optimal revenue in multi-item auctions, it is not clear that the optimal revenue w.r.t. the relaxed valuation is higher than the original optimal revenue. The following Lemma shows that the optimal revenue under is not too much smaller than the original optimal revenue, so it suffices to apply the Cai-Devanur-Weinberg duality [14, 17] on the relaxed valuation .

Lemma 24 (Lemma 2 from [16]).

We define by the probability that the buyer with type receives exactly the set in Mechanism . Then:

where is the optimal revenue under the relaxed valuation

Now we are going to show how to upper bound the with terms similar to the ones we studied in the cases where the valuation function was additive.

Lemma 25 (Theorem 1 and Lemma 33 from [16]).

For a Mechanism and a flow that satisfied the partial specification (See Figure 3 from [16]), we have that:

Where is the virtual valuation function, defined as:

For , we set . So we have that:

The following lemma provides a way to set a flow that satisfies the partial specifications (See Figure 3 from [16]).

Lemma 26 (Adapted Claim 1 from [16]).

There exists a flow that satisfies the partial specifications (See Figure 3 by [16]) such that:

Where by we denote the ironed virtual value of , when is sampled from .

Proof.

First we are going to describe how to set a flow that satisfies the partial specification requirements such that for it holds that , where by we denote the non-ironed virtual value of , when is sampled from . Then the way to set a flow that satisfies the partial specifications such that for it holds that is similar to the ironing procedure of Section 4 by [14].

For any two types , only if there exists such that , and . Let , and , we define . Note that only if . For any and , we set to be equal to fraction of the total in flow at . We note that for any type , the sum of fractions of flows that it pushes to other types is at most one:

Therefore if , we can dump any remaining flow in the sink. It is clear that this flow satisfies the partial specifications.

Moreover for any , the total in flow of is:

Therefore we have that:

Therefore, is equal to the non-ironed virtual valuation of , when is sampled from .

∎

Lemma 27 (Adapted version of Theorem 2 from [17]).

We further decompose the term the following way:

We note that in the case where the buyer is XOS, we chose as the value that separates the and the term. We sum up in the following lemma.

Appendix F Lower Bound: Polynomial Dependence on

In this section, we prove that for sufficiently large values , there exists an type distribution represented by a MRF with maximum weighted degree , such that the optimal revenue is at least times the maximum revenue achieved by simple mechanisms.

To prove this statement, we first modify the construction of Hart and Nisan [30], where they prove the following Theorem. We present a high-level idea of the proofs in this section.

Lemma 28 (Theorem C from [30]).

There exists a two item correlated distribution and a constant , such that for any , when a buyer with additive valuation is sampled from , .

Their construction, relies on the following lemma.

Lemma 29 (Proposition 7.5. from [30]).

Let and be two sequences of points, such that . For we define:

For any , there exists a sequence in such that and for each , . Moreover, if we set for all , then .

Their construction is developed inductively, by placing points on “shells” of fixed radius. More specifically, in the -th shell, whose radius is , they place points so that the angle between any pair of points in the same shell is . They observed that for all points (except ), , since and . In their proof, they only needed a lower bound for each , but we also need an upper bound. Lemma 30 provides us with that bound.

Lemma 30.

In the construction of the set of points in Proposition 7.5 in [30], if:

-

•

we place the first point of each shell in the same line that passes through the origin

-

•

for the -th shell, whose radius is , and any point in that shell (except the first point of that shell), there exists another point in that shell such that the angle between them is ,

then if we consider , for each point that is in the -th shell, we have that .

Proof.

First we note that there is no restriction that prevents us from placing the first point of each shell in the same line. This is because different shells, have different radius so there is no way two points coincide. It is also trivial to ensure that the for point in the -th shell, which is not the first point in the shell, there exists a point in the -th shell such that the angle between them is . We note that the only assumption about the set of points that was made in the proof of Proposition 7.5 in [30] (Lemma 29), was that for the -th shell, the points are placed in a semicircle of the radius we described above and that the angle between any pair of points is . Therefore the result of Lemma 29 applies to this point set too.

Now we are going to prove that for the first point in the -th shell, it holds that . Let be the first point of the shell and be the first point of the -th shell, then , where the first equality holds because point and point lie in the same line that passes through the origin. Since the results of Lemma 29 holds here, we have that .

Next, we deal with the case where point is not the first point of the -th shell. In the proof of Proposition 7.5 in [30], they noted that for two points that have angle between them, it holds that . We note that for , we can similarly prove that using the Taylor expansion of . For any point that is not the first point in the shell, there is another point such that the two point have an angle . Since , we can conclude that . Finally, since the -th shell contains points, if point belongs to the -th shell, then . Hence, . ∎

Lemma 31 (Modified version of Theorem C from [30]).

For any sufficiently large , there exists a two item correlated distribution with support and an absolute constant such that . Moreover, when a buyer with additive valuation is sampled from , then there exists another absolute constant such that .

Proof.

Given any sequences and and a target value , Proposition 7.1 in [30] constructs the following distribution : (i) Construct a sequence of positive numbers that increases fast enough, so that (a) is increasing, where and (b) ; (ii) The buyer has type with probability . Proposition 7.1 shows that for any choice of that satisfies property (a) and (b) in step (1) of the construction, the corresponding distribution has .

If we choose and for all as in Lemma 30 and that satisfies property and , it is not hard to verify that . Hence, the gap between and is as stated in the claim. The problem with this construction is that we cannot lower bound the probability that the rarest type shows up, as and can be very close to each other. To fix this issue, we modify the construction by replacing property (a) with a strengthened property (a*) for all , where is an absolute constant that will be determined later.

We first argue that if (a*) is satisfied, then the rarest type shows with sufficiently large probability. More specifically, type shows up with probability

Next, we argue that for the sequences and as described in Lemma 30, there exists a sequence that satisfies (a*) and (b). Note that

By the definition of , each point is placed in a shell of radius at least , so and . Since , , which implies that . According to Lemma 30, if belongs to the -th shell, so . Hence, there exists two positive absolute constants and such that . For the rest of the proof, we take to be . If we choose such that to be for all , for some absolute constant . As the construction above satisfies both property (a*) and (b), we have

for the induced distribution .

∎

Proof of Theorem 3: By Lemma 31, there exists a type distribution and constants such that and when a buyer has an additive valuation sampled from , then .

Using Lemma 20 on with parameters , we get a MRF , such that its maximum weighted degree is bounded by for sufficiently large . Moreover .

Since the marginal distributions of and are the same, we have that . We now prove that . Let be the optimal revenue when we only sell the first item, and to be the optimal revenue when we only sell the second item. We can easily see that . Since , we can conclude that .

At this moment, we prove that . Let be the price induced by the optimal grand bundle mechanism. The revenue achieved by posting each item at price is a lower bound on . Moreover, if we sell each item at price , then we are guaranteed to achieve at least half the revenue induced by and our claim holds.

Thus , which concludes the proof.