Signatured Deep Fictitious Play for Mean Field Games with Common Noise

Abstract

Existing deep learning methods for solving mean-field games (MFGs) with common noise fix the sampling common noise paths and then solve the corresponding MFGs. This leads to a nested-loop structure with millions of simulations of common noise paths in order to produce accurate solutions, which results in prohibitive computational cost and limits the applications to a large extent. In this paper, based on the rough path theory, we propose a novel single-loop algorithm, named signatured deep fictitious play, by which we can work with the unfixed common noise setup to avoid the nested-loop structure and reduce the computational complexity significantly. The proposed algorithm can accurately capture the effect of common uncertainty changes on mean-field equilibria without further training of neural networks, as previously needed in the existing machine learning algorithms. The efficiency is supported by three applications, including linear-quadratic MFGs, mean-field portfolio game, and mean-field game of optimal consumption and investment. Overall, we provide a new point of view from the rough path theory to solve MFGs with common noise with significantly improved efficiency and an extensive range of applications. In addition, we report the first deep learning work to deal with extended MFGs (a mean-field interaction via both the states and controls) with common noise.

1 Introduction

Stochastic differential games study the strategic interaction of rational decision-makers in an uncertain dynamical system, and have been widely applied to many areas, including social science, system science, and computer science. For realistic models, the problem usually lacks tractability and needs numerical methods. With a large number of players resulting in high-dimensional problems, conventional algorithms soon lose efficiency and one may resort to recently developed machine learning tools (Hu, 2021; Han & Hu, 2020; Han et al., 2020). On the other hand, one could utilize its limiting mean-field version, mean-field games (MFGs), to approximate the -player game for large (e.g., Han et al. (2021)). Introduced independently in Huang et al. (2006); Lasry & Lions (2007), MFGs study the decision making problem of a continuum of agents, aiming to provide asymptotic analysis of the finite player model in which players interact through their empirical distribution. In an MFG, each agent is infinitesimal, whose decision can not affect the population law. Therefore, the problem can be solved by focusing on the optimal decision of a representative agent in response to the average behavior of the entire population and a fixed-point problem (cf. equation (2.5)). The MFG model has inspired tremendous applications, not only in finance and economics, such as system risk (Carmona et al., 2015), high-frequency trading (Lachapelle et al., 2016) and crowd trading (Cardaliaguet & Lehalle, 2018), but also to population dynamics (Achdou et al., 2017; Djehiche et al., 2017; Achdou & Lasry, 2019) and sanitary vaccination (Hubert & Turinici, 2018; Elie et al., 2020a), to list a few. For a systematical introduction of MFGs, see Caines et al. (2017); Carmona & Delarue (2018a, b).

In MFGs, the random shocks to the dynamical system can be from two sources: idiosyncratic to the individual players and common to all players, i.e., decision-makers face correlated randomness. While MFGs were initially introduced with only idiosyncratic noise as seen in most of the literature, games with common noise, referred to as MFGs with common noise, have attracted significant attention recently (Lacker & Webster, 2015; Carmona et al., 2016; Ahuja, 2016; Graber, 2016). The inclusion of common noise is natural in many contexts, such as multi-agent trading in a common stock market, or systemic risk induced through inter-bank lending/borrowing. In reality, players make decisions in a common environment (e.g., trade in the same stock market). Therefore, their states are subject to correlated random shocks, which can be modeled by individual noises and a common noise. In this modeling, observing the state dynamics will be sufficient, and one does not need to observe the noises. These applications make it crucial to develop efficient and accurate algorithms for computing MFGs with common noise.

Theoretically, MFGs with common noise can be formulated as an infinite-dimensional master equation, which is the type of second-order nonlinear Hamilton-Jacobi-Bellman equation involving derivatives with respect to a probability measure. Therefore, direct simulation is infeasible due to the difficulty of discretizing the probability space. An alternative way of solving MFGs with common noise is to formulate it into a stochastic Fokker-Planck/Hamilton-Jacobi-Bellman system, which has a complicated form with common noise, forward-backward coupling, and second-order differential operators. The third kind of approaches turns it into forward backward stochastic differential equations (FBSDE) of McKean-Vlasov type (cf. Carmona & Delarue (2018b, Chapter 2)), which in general requires convexity of the Hamiltonian. For all three approaches, the common assumption is the monotonicity condition that ensures uniqueness. Regarding simulation, existing deep learning methods fix the sampling common noise paths and then solve the corresponding MFGs, which leads to a nested-loop structure with millions of simulations of common noise paths to produce accurate predictions for unseen common shock realizations. Then the computational cost becomes prohibitive and limits the applications to a large extent.

In this paper, we solve MFGs with common noise by directly parameterizing the optimal control using deep neural networks in spirit of (Han & E, 2016), and conducting a global optimization. We integrate the signature from rough path theory, and fictitious play from game theory for efficiency and accuracy, and term the algorithm Signatured Deep Fictitious Play (Sig-DFP). The proposed algorithm avoids solving the three aforementioned complicated equations (master equation, Stochastic FP/HJB, FBSDE) and does not have uniqueness issues.

Contribution. We design a novel efficient single-loop deep learning algorithm, Sig-DFP, for solving MFGs with common noise by integrating fictitious play (Brown, 1949) and Signature (Lyons et al., 2007) from rough path theory. To our best knowledge, this is the first work focusing on the common noise setting, which can address heterogeneous MFGs and heterogeneous extended MFGs, both with common noise.

We prove that the Sig-DFP algorithm can reach mean-field equilibria as both the depth of the truncated signature and the stage of the fictitious play approaching infinity, subject to the universal approximation of neural networks. We demonstrate its convergence superiority on three benchmark examples, including homogeneous MFGs, heterogeneous MFGs, and heterogeneous extended MFGs, all with common noise, and with assumptions even beyond the technical requirements in the theorems. Moreover, the algorithm has the following advantages:

1. Temporal and spacial complexity are and , compared to (for both time and space) in existing machine learning algorithms, with as the sample size, as the time discretization size, , as the dimension of common noise.

2. Easy to apply the fictitious play strategy: only need to average over linear functionals with complexity.

Related Literature. After MFGs firstly introduced by Huang et al. (2006) and Lasry & Lions (2007) under the setting of a continuum of homogeneous players but without common noise, it has been extended to many applicable settings, e.g., heterogeneous players games (Lacker & Zariphopoulou, 2019; Lacker & Soret, 2020) and major-minor players games (Huang, 2010; Nourian & Caines, 2013; Carmona & Zhu, 2016). A recent line of work studies MFGs with common noise (Carmona et al., 2015; Bensoussan et al., 2015; Ahuja, 2016; Cardaliaguet et al., 2019). Despite its theoretical progress and importance for applications, efficient numerical algorithms focusing on common noise settings are still missing. Our work will fill this gap by integrating machine learning tools with learning procedures from game theory and signature from rough path theory.

Fictitious play was firstly proposed in Brown (1949, 1951) for normal-form games, as a learning procedure for finding Nash equilibria. It has been widely used in the Economic literature, and adapted to MFGs (Cardaliaguet & Hadikhanloo, 2017; Briani & Cardaliaguet, 2018) and finite-player stochastic differential games (Hu, 2021; Han & Hu, 2020; Han et al., 2020; Xuan et al., 2021).

Using machine learning to solve MFGs has also been considered, for both model-based setting (Carmona & Laurière, 2019; Ruthotto et al., 2020; Lin et al., 2020) and model-free reinforcement learning setting (Guo et al., 2019; Tiwari et al., 2019; Angiuli et al., 2020; Elie et al., 2020b), most of which did not consider common noise. Existing machine learning methods for MFGs with common noise were studied in Perrin et al. (2020), which have a nested-loop structure and require millions of simulations of common noise paths to produce accurate predictions for unseen common shock realizations.

The signature in rough path theory has been recently applied to machine learning as a feature map for sequential data. For example, Király & Oberhauser (2019); Bonnier et al. (2019); Toth & Oberhauser (2020); Min & Ichiba (2020) have used signatures in natural language processing, time series, and handwriting recognition, and Chevyrev & Oberhauser (2018); Ni et al. (2020) studied the relation between signatures and distributions of sequential data. We refer to Lyons & Qian (2002); Lyons et al. (2007) for a more detailed introduction of the signature and rough path theory.

2 Mean Field Games with Common Noise

We first introduce the following notations to precisely define MFGs with common noise. For a fixed time horizon , let and be independent - and -dimensional Brownian motions defined on a complete filtered probability space . We shall refer as the idiosyncratic noise and as the common noise of the system. Let be the filtration generated by , and be the collection of probability measures on with finite moment, i.e., if

| (2.1) |

We denote by the space of continuous -adapted stochastic flow of probability measures with the finite second moment, and by the set of all -progressively measurable -valued square-integrable processes.

Next, we introduce the concept of MFGs with common noise. Given an initial distribution , and a stochastic flow of probability measures , we consider the stochastic control

| (2.2) | |||

| (2.3) |

with . Here the representative agent controls his dynamics through a -dimensional control process , and the drift coefficient , diffusion coefficients and , running cost and terminal cost are all measurable functions, with , and .

Definition 2.1 (Mean-field equilibrium).

The control-distribution flow pair , is a mean-field equilibrium to the MFG with common noise, if solves (2.2) given the stochastic measure flow , and the conditional marginal distribution of the optimal path given the common noise coincides with the measure flow :

| (2.4) |

where is the conditional law given a filtration .

We remark that, with a continuum of agents, the measure is not affected by a single agent’s choice, and the MFG is a standard control problem plus an additional fixed-point problem. More precisely, denote by the optimal control of (2.2)–(2.3) given the stochastic measure flow , then is a fixed point of

| (2.5) |

MFGs without common noise: Note that with , (2.2)–(2.3) is a MFG without common noise, and the flow of measures becomes deterministic.

Extended MFGs: In extended mean field games, the interactions between the representative agent and the population happen via both the states and controls, thus the functions can also depend on .

3 Fictitious Play and Signatures

The Signatured Deep Fictitious Play (Sig-DFP) algorithm is built on fictitious play, and propagates conditional distributions by signatures. This section briefly introduces these two ingredients.

In the learning procedure of fictitious play, players myopically choose their best responses against the empirical distribution of others’ actions at every subsequent stage after arbitrary initial moves. When Cardaliaguet & Hadikhanloo (2017); Cardaliaguet & Lehalle (2018) extended it to mean-field settings, the empirical distribution of actions is naturally replaced by the average of distribution flows. More precisely, let be the initial guess of in (2.4), and consider the following iterative algorithm: (1) take as the given flow of measures in (2.2)–(2.3) for the -th iteration, and solve the optimal control in (2.2) denoted by ; (2) solve the controlled stochastic differential equation (SDE) (2.3) for and then infer the conditional distribution flow ; (3) average distributions and pass to the next iteration. If converges and the strategy corresponding to the limiting measure flow is admissible, then by construction, it is a fixed-point of (2.5) and thus a mean-field equilibrium.

Signatures of Paths. Let be the tensor algebra, and denote by the space of continuous mappings from to with finite -variation. For a path , define the -variation

| (3.1) |

where denotes a partition . We equip the space with the norm .

Definition 3.1 (Signature).

Let such that the following integral makes sense. The signature of , denoted by , is an element of defined by with

| (3.2) |

We denote by the truncated signature of of depth , i.e., and has the dimension .

Note that when is a semi-martingale (the case of our problems), equation (3.2) is understood in the Stratonovich sense. The following properties of the signature make it an ideal choice for our problem, with more details in Appendix A.

1. Signatures characterize paths uniquely up to the tree-like equivalence, and the equivalence is removed if at least one dimension of the path is strictly increasing (Boedihardjo et al., 2016). Therefore, we shall augment the original path with the time dimension in the algorithm, i.e., working with since characterizes paths uniquely.

2. Terms in the signature present a factorial decay property, which provides the accuracy of using a few terms in the signature (small ) to approximate a path.

3. As a feature map of sequential data, the signature has a universality detailed in the following theorem.

Theorem 3.1 (Universality, Bonnier et al. (2019)).

Let and be a continuous function in paths. For any compact set , if is a geometric rough path for any , then for any there exist and a linear functional such that

| (3.3) |

4 The Sig-DFP Algorithm

We introduce two shorthand notations: if is a path indexed by , then denotes the whole path and denotes the path between and .

4.1 Propagation of Distribution with Signatures

With the presence of common noise, existing algorithms mostly consider a nested-loop structure, with the inner one for idiosyncratic noise and the outer one for common noise . More precisely, if one works with idiosyncratic Brownian paths and common Brownian paths , then for each , one needs to simulate paths defined by (2.3) over all idiosyncratic Brownian paths and solve the problem (2.2) associated to . This requires a total of simulations of (2.3). With a sufficiently large , is approximated well by with corresponding to the trajectory . The double summation is of which is computationally expensive for large .

We shall address the aforementioned numerical difficulties by signatures. The key idea is to approximate by

| (4.1) |

where the equal sign comes from the unique characterization of signatures to the paths , and the approximation is accurate for large due to the factorial decay property of the signature. The last term is then computed by machine learning methods, e.g., by Generative Adversarial Networks (GANs). In addition, if the agents interact via some population average subject to common noise: , the approximation in (4.1) can be arbitrarily close to the true measure flow for sufficiently large . The following lemma gives a precise statement.

Lemma 4.1.

Suppose where is a measurable function. View as with continuous for some , and let be a compact set, then for any , there exist a positive integer and a linear functional , such that

| (4.2) |

Proof.

See Appendix A for details due to the page limit. ∎

With all the above preparations, we now explain how the approximation to using signatures is implemented. Given pairs of idiosyncratic and common Brownian paths and assume in (2.3) is already obtained (which will be explained in Section 4.2), we first sample the optimized state processes , producing samples . Then the linear functional in Lemma 4.1 is approximated by implementing linear regressions on with dependent variable at several time stamps , i.e.,

| (4.3) | ||||

In all experiments in Section 5, we get decent approximations of on by considering only three time stamps . Note that such a framework can also deal with multi-dimensional , where the regression coefficients become a matrix.

The choice in (4.3) is mainly motivated by Lemma 4.1 stating is a linear functional, and by the probability model underlying ordinary linear regression (OLS) which interprets that the least square minimization (4.3) gives the best prediction of restricting to linear relations. There are other benefits for choosing OLS: Once is obtained in (4.3), the prediction for unseen common paths is efficient: Moreover, it is easy to integrate with fictitious play: averaging from different iterations, commonly needed in fictitious play, now means simply averaging over . Next, we analyze the temporal and spatial complexity of using signatures and linear regression as below.

Temporal Complexity: Suppose we discretize into time stamps: , and simulate paths of and . The simulation cost is of . For computing the truncated signature of depth , we use the Python package Signatory (Kidger & Lyons, 2020), yielding a complexity of where . Note that one can choose a large and reuse all sampled common noise paths for each iteration of fictitious play, thus the computation of is done only once, and is accessible in constant time for all . The linear regression111We use the Python package scikit-learn (Pedregosa et al., 2011) to do the linear regression. (or Ridge regression) takes time . Thus, the total temporal complexity is of , which is linear in given222 is usually small due to the factorial decay property of the signature. For not large, we have . . Comparing to the nested-loop algorithm, where the cost of simulating SDEs is and computing conditional distribution flows takes time , we claim that our algorithm reduced the temporal complexity by a factor of the sample size by using signatures.

Spatial Complexity: In fictitious play, one may choose to average all past flow of measures as the given measures in (2.2)–(2.3) for the current iteration. Using signatures simplifies it to average . To update it between iterations, one needs to store the current average which costs of the memory. Combining and for storing SDEs and truncated signatures, the overall spacial complexity is . The complexity of the nested-loop case is again , which we reduce by a factor of .

We conclude this section by the following remark: For the general case , though the linear regression is no longer available, the one-to-one mapping between and persists. Therefore, one can train a Generative Adversarial Network (GAN, Goodfellow et al. (2014)) for generating samples following the distribution by taking truncated signatures as part of the network inputs.

4.2 Deep Learning Algorithm

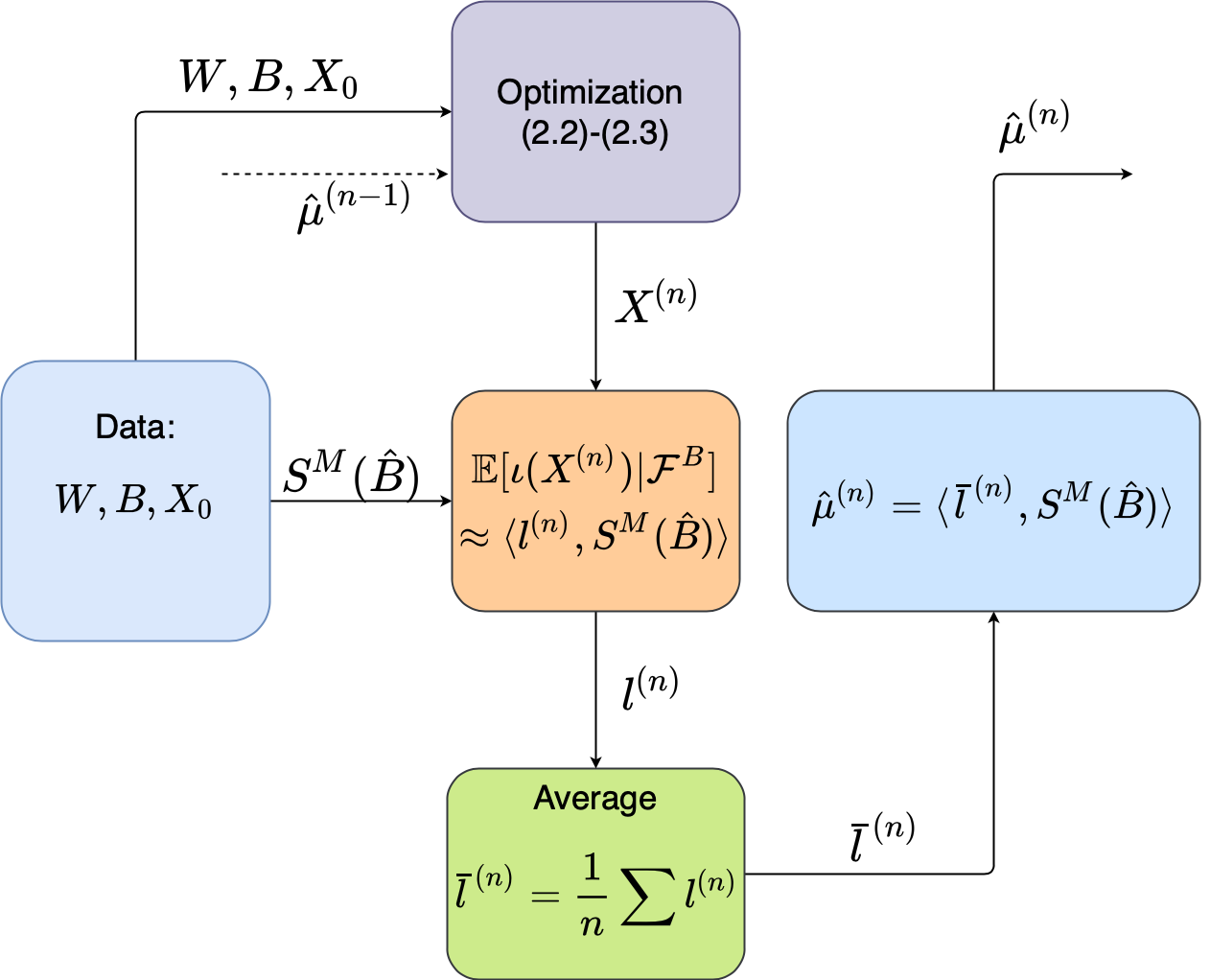

Having explained the key idea on how to approximate efficiently, we describe the Sig-DFP algorithm in this subsection. The algorithm consists of repeatedly solving (2.2)–(2.3) for a given measure flow using deep learning in the spirit of Han & E (2016), and passing the yielded to the next iteration by using signatures. The flowchart of the idea is illustrated in Figure 1. Consider a partition of , denote by the given flow of measures at stage , the stochastic optimal control problem (2.2)–(2.3) is solved by

| (4.4) | |||

| (4.5) |

where we replace the subscript by to simplify notations, and let , , . Here, we use the superscript to represent the sample path and to emphasize the stochastic measure’s dependence on the sample path of up to time . The control is then parameterized by neural networks (NNs) in the feedback form:

| (4.6) |

where denotes the NN map with parameters , and searching the infimum in (4.4) is translated into minimizing . The yielded optimizer gives , with which the optimized state process paths are simulated and its conditional law , denoted by , is approximated using signatures as described in Section 4.1. This finishes one iteration of fictitious play. Denote by the approximation of , we then pass to the next iteration via updating by averaging the coefficients in (4.3).

We summarize it in Algorithm 1, with implementation details deferred to Appendix B. Note that the simulation of and uses the equations (B.2) and (B.1) in Appendix B, respectively.

Theorem 4.1 (Convergence analysis).

Let , be the mean-field equilibrium in Definition 2.1, be the optimal control, and be the measure flow of the optimized state process after the iteration of fictitious play, and be the approximation by truncated signatures. Under Assumption C.1 and , we have

for some constants and , where denotes the 2-Wasserstein metric.

Moreover, if we consider a partition of , and define for with , then

Theorem 4.2 (Convergence in discrete time).

Remark that the Sig-DFP framework is flexible. We choose to solve (2.2)-(2.3) by direct parameterizing control policies for the sake of easy implementation and the possible exploration of multiple mean-field equilibria. If the equilibrium is unique, with proper conditions on the coefficients and , one can reformulate (2.2)-(2.3) into McKean-Vlasov FBSDEs or stochastic FP/HJB equations, and solve them by fictitious play and propagating the common noise using signatures.

5 Experiments

In this section, we present the performance of Sig-DFP for three examples: homogeneous, heterogeneous, and heterogeneous extended MFGs. A relative metric will be used for performance measurement, defined for progressively measurable random processes as

| (5.1) |

where is a benchmark process and is its prediction. We shall use stochastic gradient descent (SGD) optimizer for all three experiments. Training processes are done on a server with Intel Core i9-9820X (10 cores, 3.30 GHz) and RTX 2080 Ti GPU, and training time will be reported in Appendix B. Implementation codes are available at https://github.com/mmin0/SigDFP.

Data Preparation. For all three experiments, the size of both training and test data is , and the size of validation data is . We fix and discretize by . Initial states are generated independently by , with as the uniform distribution. The idiosyncratic Brownian motions and common noises are generated by antithetic variates for variance reduction, i.e., we generate the first half samples and get the other half by flipping.

Benchmarks. The examples below are carefully chosen with analytical benchmark solutions. Due to the space limit, we provide the details in Appendix D.

Linear-Quadratic MFGs. We first consider a Linear-Quadratic MFG with common noise proposed in Carmona et al. (2015), formulated as below:

| (5.2) | |||

| (5.3) |

Here is the conditional population mean, characterizes the noise correlation between agents, and are positive constants. The agents have homogeneous preferences and aim to minimize their individual costs. We assume so that the Hamiltonian is jointly convex in state and control variables, ensuring a unique mean-field equilibrium.

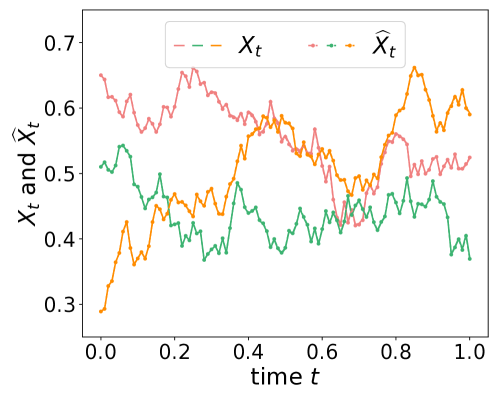

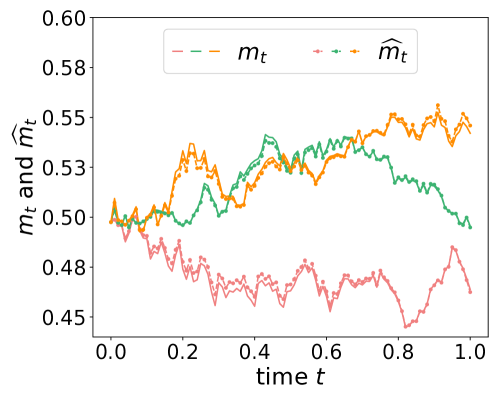

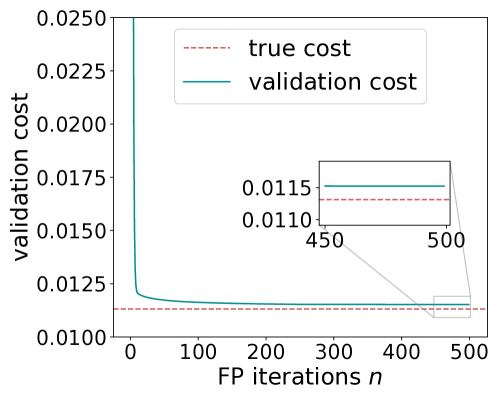

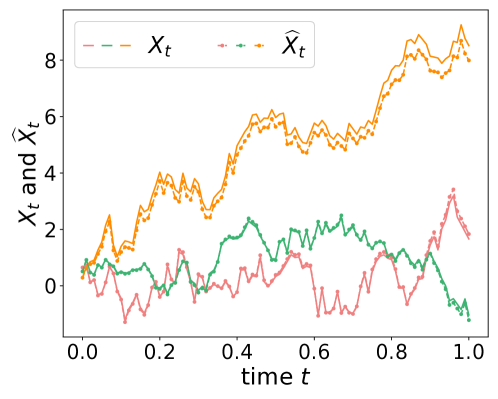

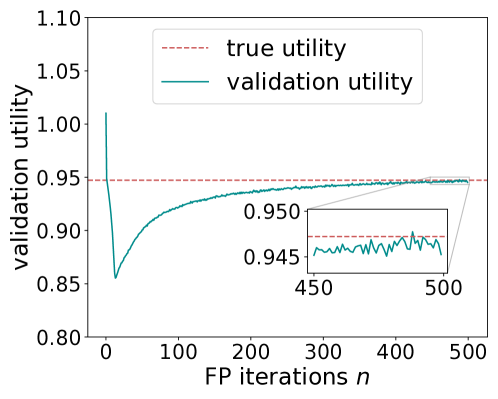

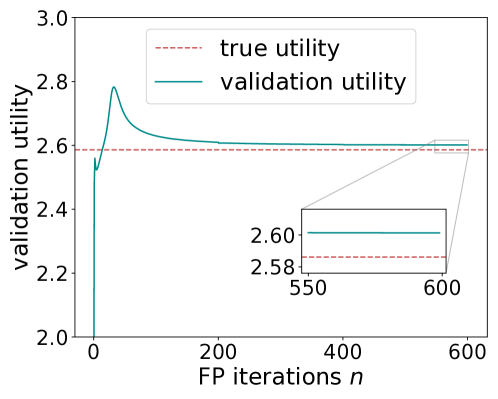

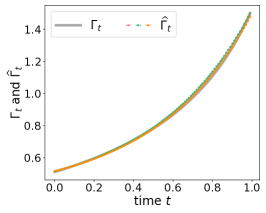

Training & Results. is a feedforward NN with two hidden layers of width 64. The truncated signature depth is chosen at . The model is trained for iterations of fictitious play. The optimized state process and its conditional mean generated by test data are shown in Figures 2a and 2b. The minimized cost after each iteration computed using validation data is given in Figure 2c, where one can see a rapid convergence to the benchmark cost. During the experiments, we notice a slow convergence speed when using the average of in (5.3). This is because the initial guess is in general far from the truth. Therefore, for the first half of iterations, we simply use the previous-step result . The learning rate is set as 0.1 for the first half and 0.01 for the second half of training. The relative errors for test data are listed in Table 1.

| SDE | Control | Equilibrium | |

|---|---|---|---|

Mean-Field Portfolio Game. Our second experiment is performed on a heterogeneous MFG proposed by Lacker & Zariphopoulou (2019), where the agent’s preference is different, characterized by a type vector which is random and drawn at time 0. They all aim to maximize their exponential utility of terminal wealth compared to the population average:

| (5.4) |

where the dynamics are

| (5.5) |

Here represents the conditional mean , and is random.

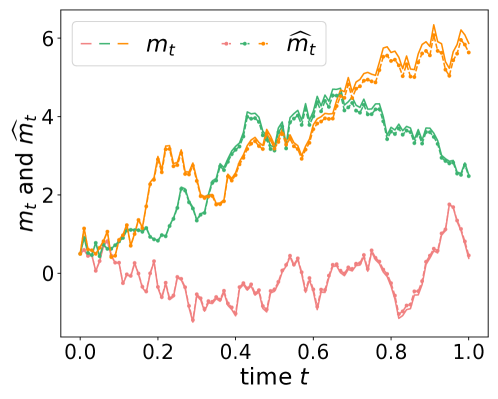

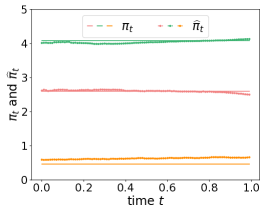

Training & Results. We use truncated signatures of depth and a feedforward NN with 4 hidden layers333Since agents are heterogeneous characterized by their type vectors , takes as inputs. Hidden neurons in each layer are (64, 32, 32, 16). to approximate . We train our model with 500 iterations of fictitious play. The learning rate starts at and is reduced by a factor of every 200 rounds. The relative errors evaluated under test data are listed in Table 2. Figure 3 compares and to their approximations, and plots the maximized utilities.

| SDE | Invest | Equilibrium | |

|---|---|---|---|

Mean-Field Game of Optimal Consumption and Investment. Our last experiment considers an extended heterogeneous MFG proposed by Lacker & Soret (2020), where agents interact via both states and controls. The setup is similar to Lacker & Zariphopoulou (2019) except for including consumption and using power utilities. More precisely, each agent is characterized by a type vector , and the optimization problem reads

| (5.6) |

where , , follows

| (5.7) |

and . Here and are the mean-field interactions from consumption and wealth.

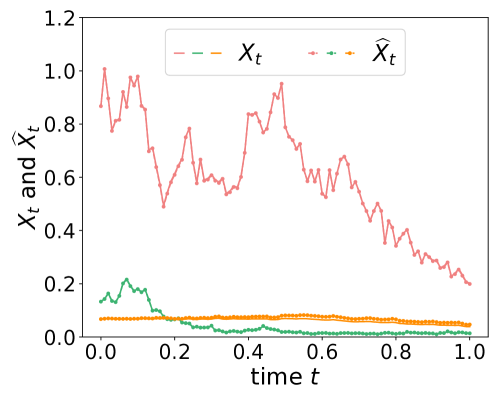

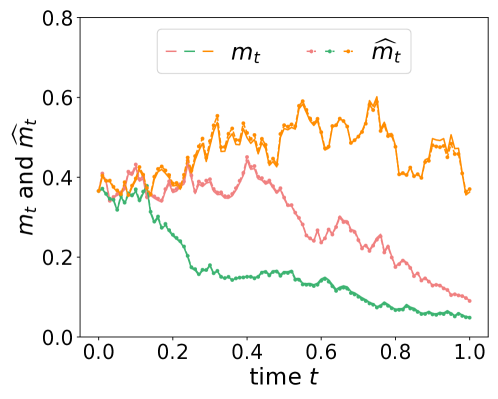

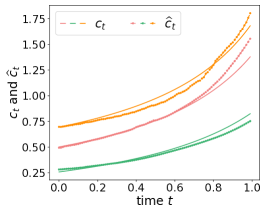

Training & Results. For this experiment, we use truncated signatures of depth . The optimal controls are parameterized by two neural networks and , each with three hidden layers.444Due to the nature of heterogeneous extended MFG, both and take as inputs. Hidden neurons in each layer are (64, 64, 64). Due to the extended mean-field interaction term , we will propagate two conditional distribution flows, i.e., two linear functionals during each iteration of fictitious play. Instead of estimating directly, we estimate by , and then take exponential to get . To ensure the non-negativity condition of , we evolve according to (D.4) and then take exponential to get . For optimal consumption, is used to predicted and thus gives the predicted . With 600 iterations of fictitious play and a learning rate of 0.1 decaying by a factor of 5 for every 200 iterations, the relative errors for test data are listed in Table 3. Figure 4 compares and to their approximations, and plots the maximized utilities. Plots of , , are provided in Appendix E.

| Invest | Consumption | |||

|---|---|---|---|---|

Comparison with the nested algorithm. We run both Sig-DFP and the nested algorithm for the training data size of (INP, CNP), where INP means the number of individual noise paths and CNP means the number of common noise paths. From the comparisons of running time, memory, and relative errors in Tables 4 and 5, one can see that the accuracy is mainly affected by the size of (INP, CNP) used for training the neural network. Sig-DFP has the advantage of reducing memory request and running time, which allows it to use a larger size of data, e.g., (INP, CNP), to produce much better accuracy. The quadratic growth of memory in the nested algorithm, evidenced by the first three columns of data in Tables 4 (least squares growth rate ), makes us unable to run the nested algorithm beyond in our current computing environment due to its high demand for memory.

| (INP, CNP) | |||||

|---|---|---|---|---|---|

| Nested Algorithm | NA | NA | |||

| Sig-DFP |

| (INP, CNP) | |||||

|---|---|---|---|---|---|

| Nested Algorithm | NA | NA | |||

| Sig-DFP |

| (, Depth ) | ||||||||

| Running Time (hours) |

Comparisons of running time for different signature depth and dimension . We choose the data size (INP, CNP) and compare the running time for different ’s in Table 6. Choosing yield the relative errors of controls as , , and for , respectively. Note that, compared to , taking improves the accuracy significantly but not . This is because the curves of and are approximately either linear or quadratic in , as shown in Figure 5 in Appendix E after taking a logarithm, which implies that the signatures of depth will be sufficient to produce good accuracy. We remark that Sig-DFP has no difficulty computing high-dimensional problems, evidenced by the running time of cases in Table 6. We focus on one-dimensional problems since, to our best knowledge, the closed-form non-trivial solutions only exist in one-dimensional cases, which can serve as the benchmark solutions. More details about are given in Appendix F.

6 Conclusion

In this paper, we propose a novel single-loop algorithm, named signatured deep fictitious play, for solving mean-field games (MFGs) with common noise. We incorporate signature from rough path theory into the strategy of deep fictitious play (Hu, 2021; Han & Hu, 2020; Han et al., 2020), and avoid the nested-loop structure in existing machine learning methods, which reduces the computational cost significantly. Analysis of the complexity and convergence for the proposed algorithm is provided. The effectiveness of the algorithm is justified by three applications, and in particular, we report the first deep learning work to deal with extended MFGs with common noise. In the future, we shall study deep learning algorithms for MFGs with common noise in more general settings (Hu & Zariphopoulou, 2021).

Acknowledgement

R.H. was partially supported by NSF grant DMS-1953035, the Faculty Career Development Award and the Research Assistance Program Award, University of California, Santa Barbara. M.M. and R.H. are grateful to the reviewers for their valuable and constructive comments.

References

- Achdou & Lasry (2019) Achdou, Y. and Lasry, J.-M. Mean field games for modeling crowd motion. In Contributions to partial differential equations and applications, pp. 17–42. Springer, 2019.

- Achdou et al. (2017) Achdou, Y., Bardi, M., and Cirant, M. Mean field games models of segregation. Mathematical Models and Methods in Applied Sciences, 27(01):75–113, 2017.

- Ahuja (2015) Ahuja, S. Mean Field Games with Common Noise. PhD thesis, Stanford University, 2015.

- Ahuja (2016) Ahuja, S. Wellposedness of mean field games with common noise under a weak monotonicity condition. SIAM Journal on Control and Optimization, 54(1):30–48, 2016.

- Angiuli et al. (2020) Angiuli, A., Fouque, J.-P., and Laurière, M. Unified reinforcement Q-learning for mean field game and control problems. arXiv preprint arXiv:2006.13912, 2020.

- Bensoussan et al. (2015) Bensoussan, A., Frehse, J., and Yam, S. C. P. The master equation in mean field theory. Journal de Mathématiques Pures et Appliquées, 103(6):1441–1474, 2015.

- Boedihardjo et al. (2016) Boedihardjo, H., Geng, X., Lyons, T., and Yang, D. The signature of a rough path: uniqueness. Advances in Mathematics, 293:720–737, 2016.

- Bonnier et al. (2019) Bonnier, P., Kidger, P., Arribas, I. P., Salvi, C., and Lyons, T. Deep signature transforms. In Advances in Neural Information Processing Systems 32 (NeurIPS), 2019.

- Briani & Cardaliaguet (2018) Briani, A. and Cardaliaguet, P. Stable solutions in potential mean field game systems. Nonlinear Differential Equations and Applications NoDEA, 25(1):1–26, 2018.

- Brown (1949) Brown, G. W. Some notes on computation of games solutions. Technical report, RAND CORP SANTA MONICA CA, 1949.

- Brown (1951) Brown, G. W. Iterative solution of games by fictitious play. Activity analysis of production and allocation, 13(1):374–376, 1951.

- Caines et al. (2017) Caines, P. E., Huang, M., and Malhamé, R. P. Mean field games. In Handbook of Dynamic Game Theory, pp. 1–28. Springer, 2017.

- Cardaliaguet & Hadikhanloo (2017) Cardaliaguet, P. and Hadikhanloo, S. Learning in mean field games: the fictitious play. ESAIM: Control, Optimisation and Calculus of Variations, 23(2):569–591, 2017.

- Cardaliaguet & Lehalle (2018) Cardaliaguet, P. and Lehalle, C.-A. Mean field game of controls and an application to trade crowding. Mathematics and Financial Economics, 12(3):335–363, 2018.

- Cardaliaguet et al. (2019) Cardaliaguet, P., Delarue, F., Lasry, J.-M., and Lions, P.-L. The Master Equation and the Convergence Problem in Mean Field Games:(AMS-201), volume 201. Princeton University Press, 2019.

- Carmona & Delarue (2018a) Carmona, R. and Delarue, F. Probabilistic Theory of Mean Field Games with Applications I. Springer, 2018a.

- Carmona & Delarue (2018b) Carmona, R. and Delarue, F. Probabilistic Theory of Mean Field Games with Applications II. Springer, 2018b.

- Carmona & Laurière (2019) Carmona, R. and Laurière, M. Convergence analysis of machine learning algorithms for the numerical solution of mean field control and games: II–the finite horizon case. arXiv preprint arXiv:1908.01613, 2019.

- Carmona & Zhu (2016) Carmona, R. and Zhu, X. A probabilistic approach to mean field games with major and minor players. Annals of Applied Probability, 26(3):1535–1580, 2016.

- Carmona et al. (2015) Carmona, R., Fouque, J.-P., and Sun, L.-H. Mean field games and systemic risk. Communications in Mathematical Sciences, 13(4):911–933, 2015.

- Carmona et al. (2016) Carmona, R., Delarue, F., and Lacker, D. Mean field games with common noise. Annals of Probability, 44(6):3740–3803, 2016.

- Chevyrev & Oberhauser (2018) Chevyrev, I. and Oberhauser, H. Signature moments to characterize laws of stochastic processes. arXiv preprint arXiv:1810.10971, 2018.

- Djehiche et al. (2017) Djehiche, B., Tcheukam, A., and Tembine, H. A mean-field game of evacuation in multilevel building. IEEE Transactions on Automatic Control, 62(10):5154–5169, 2017.

- Elie et al. (2020a) Elie, R., Hubert, E., and Turinici, G. Contact rate epidemic control of COVID-19: an equilibrium view. Mathematical Modelling of Natural Phenomena, 15:35, 2020a.

- Elie et al. (2020b) Elie, R., Pérolat, J., Laurière, M., Geist, M., and Pietquin, O. On the convergence of model free learning in mean field games. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 34, pp. 7143–7150, 2020b.

- Friz & Victoir (2010) Friz, P. K. and Victoir, N. B. Multidimensional stochastic processes as rough paths: theory and applications, volume 120. Cambridge University Press, 2010.

- Goodfellow et al. (2014) Goodfellow, I. J., Pouget-Abadie, J., Mirza, M., Xu, B., Warde-Farley, D., Ozair, S., Courville, A., and Bengio, Y. Generative adversarial nets. In Advances in Neural Information Processing Systems 27 (NIPS), 2014.

- Graber (2016) Graber, P. J. Linear quadratic mean field type control and mean field games with common noise, with application to production of an exhaustible resource. Applied Mathematics & Optimization, 74(3):459–486, 2016.

- Guo et al. (2019) Guo, X., Hu, A., Xu, R., and Zhang, J. Learning mean-field games. In Advances in Neural Information Processing Systems 32 (NeurIPS), 2019.

- Han & E (2016) Han, J. and E, W. Deep learning approximation for stochastic control problems. Deep Reinforcement Learning Workshop, NIPS, 2016.

- Han & Hu (2020) Han, J. and Hu, R. Deep fictitious play for finding Markovian Nash equilibrium in multi-agent games. In Mathematical and Scientific Machine Learning (MSML), volume 107, pp. 221–245. PMLR, 2020.

- Han et al. (2020) Han, J., Hu, R., and Long, J. Convergence of deep fictitious play for stochastic differential games. arXiv preprint arXiv:2008.05519, 2020.

- Han et al. (2021) Han, J., Hu, R., and Long, J. A class of dimensionality-free metrics for the convergence of empirical measures. arXiv preprint arXiv:2104.12036, 2021.

- Hu (2021) Hu, R. Deep fictitious play for stochastic differential games. Communications in Mathematical Sciences, 19(2):325–353, 2021.

- Hu & Zariphopoulou (2021) Hu, R. and Zariphopoulou, T. N-player and mean-field games in Itô-diffusion markets with competitive or homophilous interaction. arXiv preprint arXiv:2106.00581, 2021.

- Huang (2010) Huang, M. Large-population LQG games involving a major player: the Nash certainty equivalence principle. SIAM Journal on Control and Optimization, 48(5):3318–3353, 2010.

- Huang et al. (2006) Huang, M., Malhamé, R. P., and Caines, P. E. Large population stochastic dynamic games: closed-loop mckean-vlasov systems and the nash certainty equivalence principle. Communications in Information & Systems, 6(3):221–252, 2006.

- Hubert & Turinici (2018) Hubert, E. and Turinici, G. Nash-MFG equilibrium in a SIR model with time dependent newborn vaccination. Ricerche di matematica, 67(1):227–246, 2018.

- Kidger & Lyons (2020) Kidger, P. and Lyons, T. Signatory: differentiable computations of the signature and logsignature transforms, on both CPU and GPU. arXiv preprint arXiv:2001.00706, 2020.

- Király & Oberhauser (2019) Király, F. J. and Oberhauser, H. Kernels for sequentially ordered data. Journal of Machine Learning Research, 20(31):1–45, 2019.

- Lachapelle et al. (2016) Lachapelle, A., Lasry, J.-M., Lehalle, C.-A., and Lions, P.-L. Efficiency of the price formation process in presence of high frequency participants: a mean field game analysis. Mathematics and Financial Economics, 10(3):223–262, 2016.

- Lacker & Soret (2020) Lacker, D. and Soret, A. Many-player games of optimal consumption and investment under relative performance criteria. Mathematics and Financial Economics, 14(2):263–281, 2020.

- Lacker & Webster (2015) Lacker, D. and Webster, K. Translation invariant mean field games with common noise. Electronic Communications in Probability, 20, 2015.

- Lacker & Zariphopoulou (2019) Lacker, D. and Zariphopoulou, T. Mean field and n-agent games for optimal investment under relative performance criteria. Mathematical Finance, 29(4):1003–1038, 2019.

- Lasry & Lions (2007) Lasry, J.-M. and Lions, P.-L. Mean field games. Japanese Journal of Mathematics, 2(1):229–260, 2007.

- Lin et al. (2020) Lin, A. T., Fung, S. W., Li, W., Nurbekyan, L., and Osher, S. J. APAC-Net: Alternating the population and agent control via two neural networks to solve high-dimensional stochastic mean field games. arXiv preprint arXiv:2002.10113, 2020.

- Lyons & Qian (2002) Lyons, T. and Qian, Z. System control and rough paths. Oxford University Press, 2002.

- Lyons et al. (2007) Lyons, T. J., Caruana, M., and Lévy, T. Differential equations driven by rough paths. Springer, 2007.

- Min & Ichiba (2020) Min, M. and Ichiba, T. Convolutional signature for sequential data. arXiv preprint arXiv:2009.06719, 2020.

- Ni et al. (2020) Ni, H., Szpruch, L., Wiese, M., Liao, S., and Xiao, B. Conditional Sig-Wasserstein GANs for time series generation. arXiv preprint arXiv:2006.05421, 2020.

- Nourian & Caines (2013) Nourian, M. and Caines, P. E. -Nash mean field game theory for nonlinear stochastic dynamical systems with major and minor agents. SIAM Journal on Control and Optimization, 51(4):3302–3331, 2013.

- Pedregosa et al. (2011) Pedregosa, F., Varoquaux, G., Gramfort, A., Michel, V., Thirion, B., Grisel, O., Blondel, M., Prettenhofer, P., Weiss, R., Dubourg, V., Vanderplas, J., Passos, A., Cournapeau, D., Brucher, M., Perrot, M., and Duchesnay, E. Scikit-learn: Machine learning in Python. Journal of Machine Learning Research, 12:2825–2830, 2011.

- Perrin et al. (2020) Perrin, S., Pérolat, J., Laurière, M., Geist, M., Elie, R., and Pietquin, O. Fictitious play for mean field games: Continuous time analysis and applications. In Advances in Neural Information Processing Systems 33 (NeurIPS), 2020.

- Ruthotto et al. (2020) Ruthotto, L., Osher, S. J., Li, W., Nurbekyan, L., and Fung, S. W. A machine learning framework for solving high-dimensional mean field game and mean field control problems. Proceedings of the National Academy of Sciences, 117(17):9183–9193, 2020.

- Tiwari et al. (2019) Tiwari, N., Ghosh, A., and Aggarwal, V. Reinforcement learning for mean field game. arXiv preprint arXiv:1905.13357, 2019.

- Toth & Oberhauser (2020) Toth, C. and Oberhauser, H. Bayesian learning from sequential data using gaussian processes with signature covariances. In Proceedings of the 37th International Conference on Machine Learning (ICML), volume 119, pp. 9548–9560. PMLR, 2020.

- Xuan et al. (2021) Xuan, Y., Blkin, R., Han, J., Hu, R., and Ceniceros, H. D. Optimal policies for a pandemic: A stochastic game approach and a deep learning algorithm. In Mathematical and Scientific Machine Learning (MSML), 2021. Accepted.

Appendix A Preliminaries on Rough Path Theory and Signatures

In this appendix, we shall follow Lyons & Qian (2002); Lyons et al. (2007); Friz & Victoir (2010) and briefly introduce rough path theory and signatures. We will also give the proof of Lemma 4.1 using the factorial decay property of signatures. Denote by the simplex , and by the truncated tensor algebra.

Definition A.1 (Multiplicative Functional).

Let , with as an integer. For each , denotes the image of under the mapping , and we write

The function is called a multiplicative functional of degree in if for all and

| (A.1) |

which is called Chen’s identity.

Rough paths will be defined as a multiplicative functional with extra regularization conditions.

Definition A.2 (Control).

A control function on is a continuous non-negative function on the simplex which is supper-additive in the sense that

It is easy to see that for any control . In the following, we use the notation , where is the Gamma function and x is a positive real number.

Definition A.3.

Let be a real number and be an integer. Denote as a control and as a multiplicative functional. Then we say that has finite -variation on controlled by if

| (A.2) |

where is the tensor norm induced by the norm on . We will call that has finite -variation in short if there exists a control such that (A.2) is satisfied.

Note that in (A.2), is a constant depending only on . We are now ready to define the rough paths.

Definition A.4 (Rough Path).

Let be a real number. A -rough path in is a multiplicative functional of degree with finite -variation. The space of -rough paths is denoted by .

Given a continuous path with bounded -variation, one can construct a -rough path with for any . In particular, truncated siganture is a -rough path. The following fundamental theorem of rough paths allows us to make extension of a -rough path,

Theorem A.1 (Extension Theorem, Lyons & Qian (2002)).

Let be a real number and an integer. Denote as a multiplicative functional with finite -variation controlled be a control . Assume that , then there exists a unique extension of to a multiplicative functional which possesses finite -variation.

More precisely, for every , there exists a unique continuous function such that

is a multiplicative functional with finite -variation controlled by . By this we mean that

| (A.3) |

Signature can be seen as an extension of rough path, and its factorial decay property follows by (A.3). The control function is related to -variation of path. Given that , is a -rough path and one candidate for its control function is

| (A.4) |

where the norm is the tensor norm induced by Euclidean norm in .

Let , and be a -rough path. We call a -geometric rough path if is in the closure of under -variation metric, where -variation metric is given by

| (A.5) |

Proof of Lemma 4.1.

By constructing the iterated integral in Stratonovich sense, is the signature of a -geometric rough path (Friz & Victoir, 2010), and thus it characterizes uniquely. Therefore, conditional distribution can be written as .

By Theorem 3.3, for any there exits such that

| (A.6) |

Since where the first norm is functional norm and second is tensor norm and . By the compactness of , and (A.3), (A.4), admits a convergent uniform norm over and goes to as . Then for large enough,

| (A.7) |

For , we extend path to space by defining

Then , by Chen’s identity (A.1), and . Denote . Thus is also compact.

| (A.8) |

where the second equality is due to the construction of and the last inequality is by (A.7). ∎

Appendix B Details of Implementing the Sig-DFP Algorithm

The simulation of and follows

| (B.1) | |||

| (B.2) |

where is computed by with obtained from the previous round of fictitious play. Then is calculated by regressing on , and we update for . The algorithm starts with a random initialization to produce .

Linear-Quadratic MFGs. We set to be a feed-forward NN with two hidden layers of width 64. The signature depth is chosen at . This model is trained for iterations of fictitious play. Note that fictitious play has a slow convergence speed since our initial guess is far from the truth. Therefore, we only apply averaging over distributions (or linear functions) during the second half iteration. We set the learning rate as for the first half iterations and for the second half. The minibatch size is , and hence .

Mean-field Portfolio Game. We consider signature depth and use a fully connected neural network with four hidden layers to estimate . Since different players are characterized by their type vectors , takes as inputs. Hidden neurons in each layer are (64, 32, 32, 16). We train our model with rounds fictitious play. The learning rate starts at and is reduced by a factor of after every 200 rounds. The minibatch size is , and hence .

Mean-field Game of Optimal Consumption and Investment. In this example, signature depth is . The optimal controls are estimated by two neural networks and , each with three hidden layers. Due the nature of heterogeneous extended MFG, both and take as the inputs. Hidden layers in each network have width (64, 64, 64). We will propagate two conditional distribution flows, i.e., two linear functionals during each round fictitious play. Instead of estimating directly, we estimate by , , and then take the exponential to get . To ensure the non-negativity condition, we evolve according to (D.4), use to predicted , and then take exponential to get . We use rounds fictitious play training, learning rate 0.1 decaying by a factor of 5 for every 200 rounds, the minibatch size , and hence .

The training time for all three experiments with sample size is given in Table 7.

| LQ-MFG | |||

|---|---|---|---|

| MF Portfolio | |||

| MFG with Consump. |

Appendix C Proof of Theorems 4.1 and 4.2

We first list all main assumptions on that will be used to prove Theorem 4.1. Let be the Euclidean norm and be the same constant for all assumptions below.

Assumption C.1.

We make assumptions A1-A3 and B1-B3 as follows.

-

A1.

(Lipschitz) exist and are -Lipschitz continuous in uniformly in , i.e., for any , ,

The drift coefficient in (2.3) takes the form

where , and are measurable functions and bounded by . The diffusion coefficients and are uncontrolled and -Lipschitz in uniformly in :

-

A2.

(Growth) satisfy a linear growth condition, i.e., for any , ,

In addition satisfy a quadratic growth condition in :

-

A3.

(Convexity) is convex in and is convex jointly in with strict convexity in , i.e., for any ,

and there exist a constant such that for any , , ,

-

B1.

(Lipschitz in ) are Lipschitz continuous in uniformly in , i.e., there exists a constant such that

for all , , where is the 2-Wasserstein distance.

-

B2.

(Separable in ) is of the form

where is assumed to be convex in and strictly convex in , and is assumed to be convex in .

-

B3.

(Weak monotonicity) For all , and with marginals respectively,

Note that Assumption C.1 extends conditions A and B in Ahuja (2015) by considering general drift coefficient and non-constant diffusion coefficients and .

Our proof of Theorem 4.1 uses the probabilistic approach. To this end, we define the Hamiltonian by

Denote by the minimizer of the Hamiltonian which is unique due to Assumptions A1 and A3:

| (C.1) |

By the Lipschitz property of in and the boundedness of , is Lipschitz in . Let be the Hamiltonian, with obtained in (C.1),

| (C.2) |

Under Assumptions A1-A3, with the stochastic maximum principle, the problem (2.2)-(2.3) is equivalent to solve the following FBSDE, given ,

| (C.3) | ||||

Moreover, the optimal control is given by

| (C.4) |

for any solution to FBSDE (C.3).

The next theorem describes the McKean-Vlasov FBSDE for finding the mean-field equilibrium (cf. Definition 2.1).

Theorem C.1 (Theorem 2.2.8, Ahuja (2015)).

Theorem C.2.

Proof.

The results generalize Theorem 3.1.3, Proposition 3.1.4 and Theorem 3.1.6 in Ahuja (2015) to the multi-dimensional case and with Lipschitz SDE coefficients . The original proofs rely on Theorem 3.1.1 and Theorem 3.1.2 under Assumption H in Ahuja (2015). With the additional conditions on in our setting, Assumption H of Ahuja (2015) still holds. We omit the details because they essentially parallel the corresponding derivations in Ahuja (2015). ∎

Now we are ready to prove Theorem 4.1.

Proof of Theorem 4.1.

The proof uses the estimate (C.7) repeatedly. We first observe that, for and , one has

| (C.8) |

Then we define a map by

| (C.9) |

where is the optimal controlled process in FBSDE (C.3) given . Combining (C.8) and (C.7) gives

| (C.10) |

Thus, for sufficiently small , is a contraction map. By definition, defined in (C.6) is a fixed point of : . Let be the initial guess of , and be the resulted flow of measures of given which is the approximation of by truncated signatures. So the measure flows are generated by

| (C.11) |

where corresponds to the map , and corresponds to the truncated signature approximation. Therefore, with (C.10) and the assumption in Theorem 4.1, and denoting by , we deduce that

With sufficiently small , one has . To estimate , we observe that

| (C.12) |

where is the solution to FBSDE (C.3) given , and can be viewed as the solution to FBSDE (C.3) given . Then using the Lipschitz property of in and (C.7) again produces

Therefore, we obtain the desired result. ∎

Next we give the proof to Theorem 4.2.

Proof of Theorem 4.2.

Consider a partition of , and define for with , then by following the line of the proof to Theorem 4.1, one only needs an additional estimate on to complete the proof. Noticing that solves (2.3) with and satisfies (4.5) with , one can obtain the estimate by following Lemma 14 in Carmona & Laurière (2019) with . ∎

Appendix D Benchmark Solutions

This appendix summarizes the analytical solutions to the three examples in Section 5, which are used to benchmark our algorithm’s performance.

Linear-Quadratic MFGs.

The analytical solution is provided in Carmona et al. (2015):

| (D.1) | |||

| (D.2) |

where is a deterministic function solving the Riccati equation:

with the solution given by

Here , , and the minimized expected cost is with

Mean-field Portfolio Game

Given the type vector , the analytical solution provided in Lacker & Zariphopoulou (2019) is summarized below

where and . Note that, since the type vector is random representing the heterogenuity of agents in this mean-field game, is a random strategy. The maximized expected utility of this game is given by , with

Note that Figure 3(c) plots the absolute value of .

Mean-field Game of Optimal Consumption and Investment

Note that the expression of , and the maximized expected utility are not given in Lacker & Soret (2020). For completeness, we give their derivations below. Since in (D.3) doesn’t depend on the common noise , admits a unique formula for all agents

To obtain the formula for , we first deduce by Itô’s formula that

| (D.4) |

from which we easily get

and . The maximized expected utility of this game is given by , with

and is defined by

Note that, to ensure the positiveness of required by using the power utility, the trajectories of are obtained by simulating via (D.4) then taking the exponential.

Appendix E Plots of , , for Mean-Field Game of Optimal Consumption and Investment

Appendix F Experiment setup for the high-dimensional case

To test the performance of Sig-DFP in high dimensions, we implement a toy experiment on the mean-field game of optimal consumption and investment with the common noise of dimension . Specifically, we modify the term in (5.7) to be in high dimensions, i.e., now follows

where , is a -dimensional Brownian motion, and . We use the same hyperparameters for training and provide the running time in Table 6.