Adversarial Training for Gradient Descent: Analysis Through its Continuous-time Approximation

Abstract

Adversarial training has gained great popularity as one of the most effective defenses for deep neural network and more generally for gradient-based machine learning models against adversarial perturbations on data points. This paper establishes a continuous-time approximation for the mini-max game of adversarial training. This approximation approach allows for precise and analytical comparisons between stochastic gradient descent and its adversarial training counterpart; and confirms theoretically the robustness of adversarial training from a new gradient-flow viewpoint. The analysis is then corroborated through various analytical and numerical examples.

1 Introduction

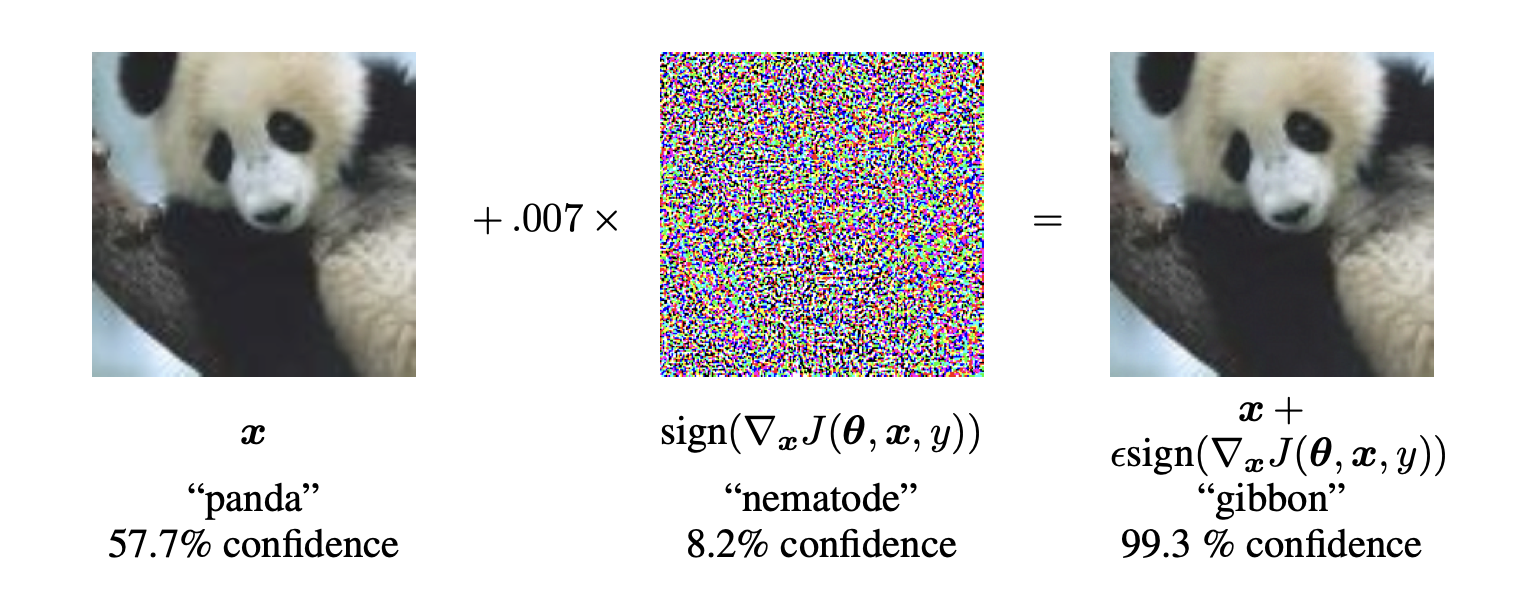

Deep neural networks and more generally gradient-based machine learning models have enjoyed substantial successes in many applications. Their performance, however, can significantly deteriorate by small and human imperceptible adversarial perturbations. Figure 1 illustrates such a well-known instance of adversarial attack which leads to blatantly identification errors [36, 17]. Such vulnerability of machine learning models raises concerns of their practicability in robustness-critical applications.

Adversarial training, proposed in [24], is one of the most promising defenses for machine learning models against adversarial perturbation. Recent empirical studies such as [9] and [2] have demonstrated its effectiveness and robustness of training neural networks in many applications. The idea of adversarial training [24] is to formulate a mini-max game between a learner who aims to improve the model performance and an adversary who is allowed to perturb the data inputs. Algorithmically speaking, in each round, the adversary generates new adversarial examples against the current neural network via projected gradient descent (PGD), the learner then responds by taking a gradient step to decrease its loss. This procedure is prescribed in Algorithm 1.

Given the popularity of adversarial training, considerable effort has been made to further improve its performance. [40] and [15] use Lipschitz regularizations for better generalization performance of trained models; [42] designs a computationally efficient variant of adversarial training based on the Pontryagin Maximum Principle from robust controls; and [43] suggests an early-stopped PGD to generate adversarial examples. To improve robustness, [25] extends the standard PGD procedure to incorporate multiple perturbation models into a single attack.

Parallel to these empirical successes, there are growing research interests in analyzing convergence and robustness of adversarial training ([24]). For instance, [39] considers quantitatively evaluating the convergence quality of adversarial examples found by the adversary, in order to ensure the convergence and the robustness; [16] and [44] study the convergence and the robustness of adversarial training on over-parameterized neural networks; [33] provides convergence analysis of adversarial training by combining techniques from robust optimal controls and inexact oracle methods from optimization; [14] investigates the non-concave landscape of the adversary for a two-layer neural network with a quadratic loss function; [41] studies the adversarially robust generalization problem via Rademacher complexity; [12] characterizes the generalization gap in terms of the number of training samples for Gaussian and Bernoulli models; and finally, [30] explores the trade-off between the robustness and the accuracy in linear models.

Given these empirical and theoretical advances, it is natural to ask: what is the difference between vanilla stochastic gradient descent and adversarial training? Is it possible to analytically quantify this difference? And, how the hyper-parameters such as perturbation step and learning rate, affect the performance of adversarial training? These are the focuses of our study in this paper.

Our work

This paper considers the mini-max game of adversarial training by alternating stochastic gradient ascent and descent. By establishing a continuous-time approximation to the training process in the form of a stochastic differential equation (SDE), it enables precise and analytical comparisons stochastic gradient descent and its adversarial training counterpart. Moreover, it confirms theoretically the robustness of adversarial training from a new gradient-flow viewpoint. This theoretical study is corroborated via several analytical and numerical examples. In the robust portfolio selection problem, it reveals an intriguing connection between adversarial training and the robust in portfolio selections, under appropriate choices of hyper-parameters such as the learning rate and the iteration steps. In the experiment with a logistic regression, it demonstrates that adversarial training leads to both increased robustness and reduced losses.

Related works

The idea of approximating discrete-time stochastic gradient algorithms (SGAs) by continuous-time SDE dynamics can be traced back to [26] and [22]. It has recently been extended to various settings of SGAs. For instance, [21] and [1] establish SDE approximations of accelerated mirror descent and asynchronous SGD, respectively; [10] designs an entropy-regularized training algorithm motivated by the SDE approximation; [11] builds the connection between SGD and variational inference by considering the evolution of training parameters; and finally, [8] studies the training process of generative adversarial networks (GANs) via a coupled SDEs system.

The formulation of adversarial training is also closely related to robust optimization [3], where the goal is to optimize the model’s worst-case performance under data uncertainty. Robust optimization has a number of applications, including financial portfolio optimization [5], [27], statistics [28], machine learning [6]) and reinforcement learning [34]). Recently, [35] and [31] investigate the empirical performance of solving robust optimization problem with adversarial training. Our study on the robust portfolio selection problem shows an intriguing connection between robust optimization with adversarial training, under proper choices of hyper-parameters.

Organization

Section 2 presents the problem set-up for adversarial training. Section 3 establishes the continuous-time SDE approximation for adversarial training, with error bound and robustness analysis, as well as discussion regarding the convergence of adversarial training via the invariant measure of the SDE. Section 4 compares the vanilla stochastic gradient descent with adversarial training from the continuous-time SDE viewpoint. Section 5 draws the connection between robust optimization and adversarial training through a robust portfolio selection problem. Section 6 is devoted to the technical proofs of main convergence results presented in Section 3. Finally, Section 7 illustrates the theoretical results in the previous sections with numerical experiments. Meanwhile, the robust portfolio optimization problem in Section 5 is solved numerically using adversarial training, and the impacts of hyper-parameters will be discussed with theoretical explanations.

Notations

The following notations will be used throughout the appendix.

-

•

For denotes the -norm over i.e., for any .

-

•

Let by a -by- real-valued matrix with the -th entry . denotes the Frobenius norm of . denotes the transpose of .

-

•

Let be an arbitrary nonempty subset of and is a function from to . We say is Lipschitz continuous if there exists some constant , such that for any ,

-

•

Let be an arbitrary nonempty subset of the set of continuously differentiable functions over some domain is denoted by for any nonnegative integer In particular when denotes the set of continuous functions.

-

•

Let be a -tuple multi-index of order where is a nonnegative integer for all then define the operator .

-

•

Fix an arbitrary . denotes a subspace of , where for any and any -tuple multi-index with there exist such that

i.e. ’s partial derivatives up to and including order have at most polynomial growth.

-

•

The Wasserstein distance between two probability measures are

-

•

For any open subset in , denotes all real-valued continuous functions on , denotes all k-times continuously differentiable functions on . Given , for any contains functions whose partial derivatives of orders in and orders in are continuous.

-

•

is defined to be of class if for all , there exists a radius such that, up to relabeling the variables, for some function on .

2 Problem Setting

Given a data set with , and a constraint set , the adversarial training problem is to find an appropriate model parameter and small perturbations to solve the following min-max optimization problem:

| (2.1) |

Here is a loss function depending on both model parameter and data , with the dimension of a given parameter space for . Meanwhile, is the perturbation on the data point within the constraint set . A common choice for is with some given and or .

One of the established approaches to compute (2.1) is by performing a gradient ascent on the perturbation parameter and a gradient descent on the model parameter . Such an alternating optimization algorithm, called projected-gradient-descent (PGD) adversarial training [24], is shown in Algorithm 1: in the inner loop, the most powerful adversarial attack to the input data batch is obtained via the multi-step projected gradient ascent; and in the outer loop, is updated by the one-step gradient descent, based on the perturbed batch of data.

Our goal is to analyze the analytical impact of adversarial perturbations. Here, we consider a more general form that incorporate variants of the original min-max problem (2.1):

| (2.2) |

where the function is the regularization term with a hyper-parameter. For instance, when the original constraint set is in the form , then the modified problem (2.2) is a Lagrange relaxation of the original problem (2.1). Moreover, is assumed to be a convex function attaining the minimum at the origin, with . This is consistent with the literature for adversarial training, including the popular regularization.

Our approach is to establish a continuous-time approximation for the discrete-time Algorithm 2, with analysis of the approximation error bound. This approximation will enable us to compare analytically the PGD with adversarial training versus its vanilla form, as well as the robustness of adversarial training.

3 Continuous-time Approximation

To establish the continuous-time SDE dynamic for adversarial training, let us first introduce some notations.

Notation

Let be the probability distribution of data on . Throughout the paper, if there is no additional specification, we assume the expectation is taken over the distribution . Let be the loss function depending on both model parameter and data . Define and to be the gradients of with respect to and , respectively. Define to be the matrix whose -th entry is .

Assumptions

Throughout this paper, we will assume for ease of exposition and with little loss of generality the same constant learning rate for both the inner and outer loops, In addition, we assume:

Assumption 3.1

The loss function satisfies the following conditions.

-

1.

.

-

2.

For any , and .

-

3.

For any , there exists such that -almost surely,

Note that in the empirical risk minimization case [37], where the support of is a finite set, the conditions above are often trivially satisfied. Meanwhile, Assumption 3.1.2 allows us to define the following functions

| (3.1) |

| (3.2) |

Moreover, Assumption 3.1 and the dominated convergence theorem allows changing orders of expectations and derivatives such that

Hence, under Assumption 3.1, the functions , and are differentiable.

The approximation is established through a series of analysis.

3.1 Firs Step: One-step Difference in Discrete-time Update

We first focus on analyzing one step in Algorithm 2 to see how the parameter is updated from to .

Consider an inner loop starting with , then

The second equality comes from Taylor’s expansion at . Continuing this calculation, we see that any ,

| (3.3) |

Since we only keep the first order terms, terms involving higher order derivatives of are negligible by the assumption of .

Given (3.3), by Assumption 3.1 and the third order Taylor’s expansion, the update on from the outer loop is given by

| (3.4) |

In particular, given an initial model parameter and independent samples from , Algorithm 2 updates as

| (3.5) |

Now, in order to find a continuous-time approximation for , key quantities are the first and second order moments and , with the one-step difference of . The expectation here is taken over the randomness of the mini-batch samples . By direct computations,

The formal computation leads to the following lemma.

3.2 Second Step: One-step Difference in Continuous-time Approximation

Next, we will find a continuous-time stochastic process to approximate the discrete-time adversarial training dynamic (3.1).

To this end, define according to the following stochastic differential equation:

| (3.8) |

Here is a dimensional Brownian motion defined on a probability space , and the drift terms and the diffusion term in (3.8) are defined as:

| (3.9) | ||||

| (3.10) | ||||

| (3.11) | ||||

| (3.12) | ||||

Here , the ratio between the batch size and the learning rate , determines the scale of the diffusion. To ensure the well-definedness of the stochastic differential equation, we impose additionally the following smoothness conditions on , and .

Assumption 3.2

Assumption 3.2.1 is a standard assumption to guarantee that the SDE (3.8) has a unique (strong) solution. Meanwhile, Assumption 3.2.2 helps to control the growth of the solution (and its partial derivatives) of (3.8), which is crucial to the subsequent analysis of its approximation error. These assumptions are satisfied for a neural network with sufficiently smooth activation and loss functions.

As one can see, and defined in (3.10), (3.11) and (3.12) are appropriately chosen so that the dynamic (3.8) with defined in (3.10)-(3.12) indeed matches the first and second moments of the discrete-time adversarial training dynamic (3.1), as shown in the following lemma.

Lemma 3.2

Now, we will continue the error bound analysis of this approximation of by .

3.3 Step Three: Error Bound of Approximation

We now provide a rigorous proof that the SDE (3.8) is indeed the continuous-time approximation for Algorithm 2, in some appropriate analytical sense: since we are comparing a discrete-time stochastic process with a continuous-time stochastic process , it is necessary to define an appropriate notion of approximation.

Notice that the discrete-time process is adapted to the filtration generated by , which is by random sampling from the mini-batch, whereas the process is adapted to a filtration generated by an independent . Hence, it is not appropriate to compare individual sample paths. Instead, we adopt the notion of weak approximation to compare the distributions of sample paths instead of the sample paths themselves, following [23]. Recall

Definition 3.1

(Order- Weak Approximation) Let and be an integer. Set A continuous-time stochastic process is said of be an order- weak approximation of a discrete stochastic process , if for every there exists a positive constant independent of such that

The weak approximation is different from the strong approximation, where the actual sample-paths of two processes are required to be close, for example,

In contrast, weak approximation requires that the expectations of the two processes and over a sufficiently large class of test functions to be close. The test function class here includes all polynomials. In particular, it implies all moments of the two processes are close at the order of .

As pointed out in [23], one important advantage of the weak approximation is that a continuous-time process can in fact approximate a discrete-time stochastic process whose step-wise driving noise is not Gaussian, as long as appropriate moments are matched (see the following Lemma 3.3). This additional flexibility is useful as it allows the treatment of more general classes of stochastic gradient iterations, for example, asynchronous stochastic gradient descent in [1] and GAN training in [8].

The following lemma from [23] is key to show that the SDE (3.8) is a second-order weak approximation for adversarial training dynamic (3.1).

Lemma 3.3

[23] Let and Let be an integer. Let be a continuous-time stochastic process satisfying

| (3.13) |

Here is a dimensional Brownian motion, and assume , are both Lipschitz continuous. Let be a discrete-time stochastic process following

| (3.14) |

where and is a set of independent samples from some distribution , and is independent of .

Define as the continuous-time stochastic process (3.13) starting from , and as the discrete-time process (3.14) starting from . Define and . Suppose further that the following conditions hold:

-

1.

There exists a function independent of such that

for and

for all .

-

2.

For each integer , the -moment of is uniformly bounded with respect to and , i.e. there exists a independent of such that

Then, for each there exists a constant independent of such that

Note that the first condition in Lemma 3.3 is about moment matching for one-step differences, which are studied in Lemma 3.1 and Lemma 3.2 under Assumptions 3.1 and 3.2. However, Assumptions 3.1 and 3.2 are in general not sufficient to guarantee the second condition in Lemma 3.3 on the uniform moment bound for the discrete-time process. Hence, we add the the following assumption regarding the loss function .

Assumption 3.3

The loss function and its derivatives satisfy the following linear growth conditions: there exist some function , such that for any integer , and for any ,

Theorem 3.1

(Approximation) Assume Assumptions 3.1, 3.2, and 3.3. Fix an arbitrary time horizon and take the learning rate and set the number of iterations Let be the discrete-time adversarial training dynamic defined in (3.1), and be the continuous-time SDE dynamic defined in (3.8). Set . Then is an order-2 weak approximation of . That is, for each there exists a constant independent of such that

Theorem 3.1 states that the approximation error between the continuous-time SDE dynamic (3.8) and the discrete-time training dynamic is in the order of . Note that the approximation is in the sense of distribution of trained parameters, meaning this result holds for a class of neural networks from this distribution. Note also the particular order of error bound can vary depending on the specific form of continuous-time SDE dynamics, and may be further improved.

3.4 Convergence Analysis via Invariant Measure

Additionally, by studying the invariant measure of the SDE (3.8), and by adopting methodologies and notations from [38], [4], and [13], we have the convergence of the SDE under the following assumption:

Assumption 3.4

Theorem 3.2

Mathematically, Assumption 3.4.1 guarantees the existence of a unique (strong) solution to the SDE (3.8). Assumption 3.4.2 is closely related to the recurrence property of the process [4]. Assumption 3.4.3 requires to be uniformly elliptic, and is also known as the non-degenerate condition [19]. Both Assumptions 3.4.2 and 3.4.3 are standard to study invariant measures and ergodicity of SDEs, see for example, [38], [20] and [18].

These assumptions provide useful insight for algorithm designs of SGD. For instance, Assumption 3.1 requires the boundedness of the loss function’s gradient. In particular, the boundedness assumption explains analytically some well-known practices in adversarial training, including the introduction of various forms of gradient penalties; see for example, [40] and [15]. Assumption 3.4.2 suggests that the loss function and training algorithm need to be designed such that there exist strong gradient signals to keep from being extremely large; in practice, this requirement can be satisfied by adding the -regularization to . Hence, Theorem 3.2 justifies mathematically from a continuous-time viewpoint the widely-used regularization helps to stabilize the training process.

4 Comparison Between SGD and Adversarial Training

4.1 Difference in their perspective continuous-time approximations

To start, first recall that the discrete-time dynamic for SGD is

| (4.1) |

and its continuous-time SDE approximation (see for example, [23]) is

| (4.2) |

with

| (4.3) | ||||

| (4.4) | ||||

| (4.5) | ||||

Comparing the continuous time approximations (4.2) and (3.8), it is clear that (4.2) can be viewed as a special case of (3.8) by taking . The term in (3.10) differs from in (4.3) by an additional correction term , due to adversarial perturbations. Meanwhile, the term in (3.11) differs from in (4.4) by two additional terms, and , also caused by adversarial perturbations.

4.2 Gradient Flow and Robustness of Adversarial Training

These differences between adversarial training and SGD enable us to explain analytically the robustness of adversarial training from a (new) gradient-flow viewpoint.

Indeed, if (3.8) is viewed (approximately) as the negative gradient flow with respect to the function and if (4.2) is viewed (approximately) as the negative gradient flow with respect to the expected loss function , then the extra term for adversarial training exactly reflects the sensitivity of the loss function under the perturbation of data , contributing to the robustness of the trained model.

In other words, the continuous-time SDE approximation offers a new perspective to understand why using adversarial training results empirically in more robust models than simply applying SGD: adversarial training chooses to decrease the expected loss function while simultaneously improving the robustness according to the criterion , while SGD only focuses on decreasing the expected loss .

4.3 Comparison through Examples

The above analytical explanation can be corroborated in a numerical experiment with a logistic regression problem in Section 7.1. Meanwhile, more explicit comparison between the dynamic of adversarial training and its SGD counterpart can be derived in the following linear model, for which the corresponding SDE can be explicitly solved.

Let be a symmetric positive definite matrix, with its eigenvalues. Consider the loss function

| (4.6) |

and the data . In this case,

Hence, the SDE approximation (3.8) for adversarial training applied to the model (4.6) is

| (4.7) |

This linear SDE (4.7) is a multi-dimensional Ornstein-Uhlenbeck (OU) process and admits an explicit solution:

| (4.8) |

with .

By It’s isometry [19], we then deduce the dynamic of the objective function as

| (4.9) |

Meanwhile, the SDE approximation to the vanilla SGD for model (4.6) has the following dynamic [23]:

with , and

| (4.10) |

As pointed out in [23], the first term in (4.10) decays exponentially with an asymptotic rate , and the second term is induced by noise with its asymptotic value proportional to the learning rate as . This is the well-known two-phase behavior of SGD under constant learning rate: an initial descent phase induced by the deterministic gradient flow and an eventual fluctuation phase dominated by the variance of the stochastic gradients.

Now in adversarial training, the first term of the dynamic of the objective function (4.3) also decays exponentially, but with a faster asymptotic rate . This is because the gradient descent direction with respect to under this particular model (4.6) coincides with the gradient ascent direction with respect to , that is . Hence, the inner loop is accelerating the convergence of . For the second term induced by the noise, its asymptotic value is also proportional to the learning rate when .

Numerical testing

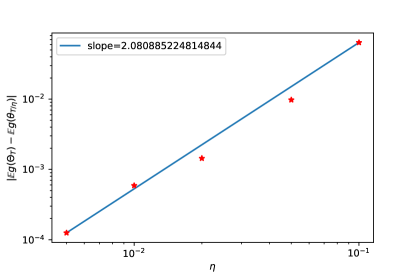

The explicit calculation for the model (4.6) enables us to verify numerically the second-order approximation result in Theorem 3.1. To see this, take the model (4.6) with a randomly generated 10-by-10 positive definite matrix , and a random initial value . The regularization (penalty) term in (2.2) is set to be , along with other parameters choices of .

As suggested by Theorem 3.1, the error with the test function is equal to the expected loss function: . The expectation of adversarial training dynamic is averaged over 1e5 runs, while the expectation of continuous-time SDE dynamic is computed via the explicit formula (4.3).

5 From Robust Optimization to Adversarial Training

In this section, we draw the connection between robust optimization [3] and adversarial training through a robust portfolio selection problem [5, 27].

Robust portfolio selection problem

Consider a capital market consisting of assets whose yearly returns are captured by the random vector The goal is to find a portfolio allocation vector in the unit simplex Since a portfolio invests a percentage of the available capital in asset for each its return is

If the full information of the return distribution is given, the problem of finding the optimal portfolio allocation can be formulated as the following single-stage stochastic program:

| (5.1) |

The objective is a weighed sum of the mean and the conditional value-at-risk (CVaR) of the portfolio loss According to the definition of CVaR in [32], we can replace CVaR in (5.1) by its formal definition and obtain an equivalent formulation:

| (5.2) |

In practice, however, instead of the full information of the return distribution , one may only have access to the empirical distribution of , where one can collect samples and obtain the empirical distribution of by In this case, instead of (2.2) where adversary attacks are added directly to data points, distributional robust optimization (DRO) (see for instance [5, 27, 29]) considers perturbations on the entire empirical distribution under the Wasserstein metric. That is, DRO studies the portfolio allocation problem (5) with the assumption that is within a Wasserstein ball around the empirical distribution , and its goal is to find the optimal portfolio allocation under the worst-case criterion:

| (5.3) | ||||

Here the Wasserstein distance between two probability measures and is

where is a nonnegative lower semicontinuous function satisfying if and only if .

Moreover, via a strong duality argument, [7] reformulates (5.3) as the following min-max problem:

| (5.4) |

Clearly, (5.4) is a special case of the general adversarial learning problem (2.2) in Section 2, where is the parameter in (2.2), corresponds to the data point , and is the perturbed data point . It is an optimization problem with a regularization term whose parameter is determined by . This regularized optimization formulation is consistent with [5] for mean-variance portfolio selection, [6] for Lasso, and [6] for logistic regression.

(5.4) can be solved by the adversarial algorithm, with the objective function as

| (5.5) |

The exact algorithm with gradient updates is detailed below in Algorithm 3.

In Section 7.2, we will apply Algorithm 3 to the robust portfolio selection problem (5.4). The perturbation power of the adversarial algorithm will be studied through experiments with different hyper-parameters, and the numerical results are shown to be consistent with the SDE approximation developed in Section 3.

6 Proofs of Key Results

Proof of Lemma 3.2

The uniqueness of the solution to the SDE (3.8) follows from the Lipschitz condition in Assumption 3.2 and the standard existence and uniqueness result for SDEs, see for instance Theorem 5.2.9 in [19].

To provide the moment estimates, let us first define the following operators for any test function , with the set of functions whose partial derivatives up to order four have at most polynomial growth:

Note that here and are real-valued functions on , while is a vector-valued function from to . By It’s formula, for any test function ,

Applying the above formula to , and yields

Taking expectations on both sides, all terms in the integral are either equal to zero or of order .Since all the integrands have at most third order derivatives in and fourth order derivatives in , by the assumption that and , all the integrands belong to . Thus, the expectation of each integrand is bounded by

| (6.1) |

for some . By the Lipschitz condition in Assumption 3.2 and standard moment estimates for SDEs, (see again Theorem 5.2.9 in [19]), (6.1) is finite.

Proof of Theorem 3.1

It suffices to check that conditions in Lemma 3.3 are satisfied by and for .

The first condition on one-step differences in Lemma 3.3 holds by Lemma 3.1 and Lemma 3.2. It remains to check the second condition on bounded moments.

Recall that for any given sampled independently from , the update in adversarial training is

| (6.3) |

By Assumption 3.3, the 2-norm of is bounded by

Define the random variable

| (6.4) |

By the independence of and the finite moment condition in Assumption 3.3, we can conclude that for any .

To simplify the notation, we now use to denote in the remainder of the proof. Now for any integer and , we have

For , by Assumption 3.3 and the fact that is independent of ,

Here the constant in the last line is independent of and , but may depend on the uniform -moment bound for , the existence of which can be justified by induction on . Hence, if we denote , we have with independent of and , which immediately implies Therefore, the second condition on bounded moments in Lemma 3.3 holds and the weak approximation result follows.

7 Numerical Examples

In this section, two numerical examples will be presented to further illustrate the theoretical results established in Section 3. More specifically,

-

•

the numerical experiment on logistic regression confirms that adversarial training, when compared with the vanilla SGD, has the added advantage of improving the robustness of the model, consistent with the gradient flow perspective discussed in Section 4.2;

-

•

the robust portfolio optimization problem (5.4) is solved numerically using adversarial training. Impact of hyper-parameters on the robustness of training will be discussed.

7.1 Logistic Regression and Robustness

In this section a logistic regression model is adopted to illustrate the robustness in adversarial training discussed in Section 4.2.

We consider the randomly generated data , where and is sampled from a multivariate Gaussian distribution given . We are to fit the data with a logistic regression model

with the cross-entropy loss function

Here are randomly generated.

Meanwhile, we choose in (2.2) to be the regularization, along with other parameters of . For simplicity, we fix the bias and only update .

Results

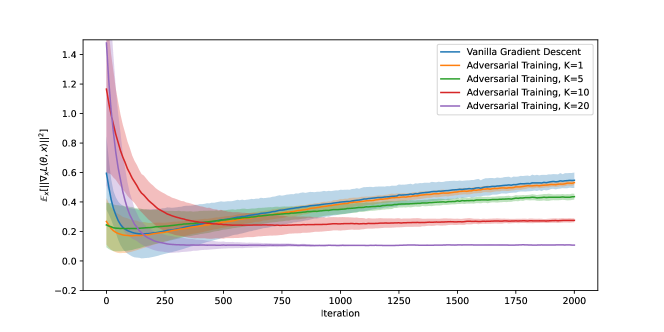

As suggested in Section 4.2, the models’ robustness in terms of for both stochastic gradient descent and adversarial learning algorithm over the training iterations is plotted in Figure 3, with means and standard deviations computed over 50 randomly initialized experiments.

Figure 3 shows how the number of perturbation steps affects the robustness of the model. When becomes larger (for example, or ), more adversarial perturbations are added to the training data, resulting in more robust models in terms of . In contrast, under vanilla gradient descent, it is observed that first decreases then increases, indicating that the model becomes increasingly sensitive hence less robust to adversarial perturbation as the training proceeds. This result is consistent with the gradient-flow viewpoint discussed in Section 4.2: updating via SGD only leads to decrease in losses, while adversarial training leads to both improvement in robustness and reduction in losses.

Finally, note that in 50 randomly initialized experiments, SGD gets an average test accuracy of 84%, while adversarial training with gets a slightly lower average test accuracy of 78%. This finding is consistent with earlier empirical studies including [2] and [43], where adversarial training is shown to have a lower test accuracy on original samples in exchange for more robustness.

7.2 Robust Portfolio Selection

In this experiment, we apply Algorithm 3 to the robust portfolio selection problem (5.4) discussed in Section 5. The perturbation power of the adversarial algorithm is studied through experiments with different hyper-parameters.

Algorithm and numerical setup

Our experiments are based on a market with assets. Following the similar setting of Section 7.2 in [27], the return is decomposed into a systematic risk factor applied to all assets and an idiosyncratic risk factor

Perturbation power of the adversarial learning algorithm

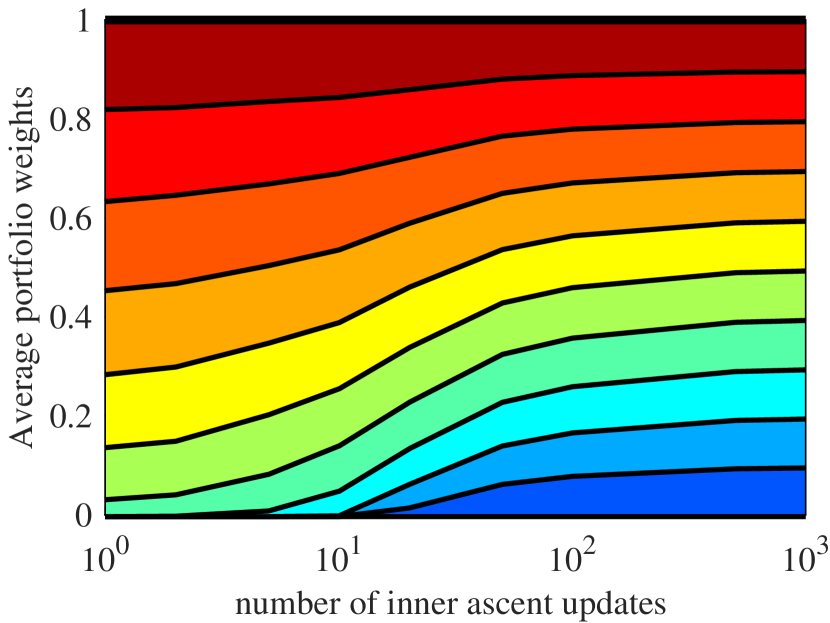

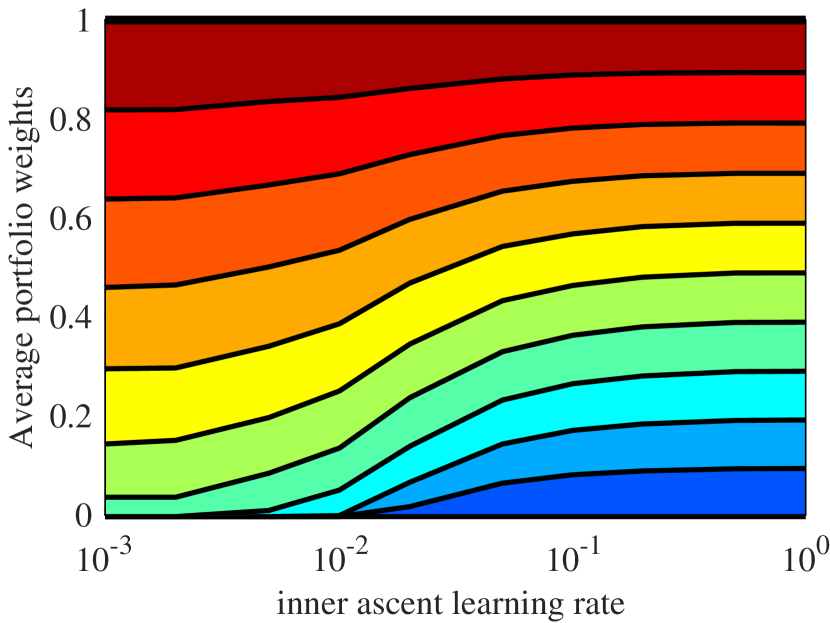

The perturbation power of the adversarial algorithm is mainly determined by two hyper-parameters: number of inner ascent updates and inner ascent learning rate . When and are small, the perturbations added to the original data are small; Consequently, assets with higher empirical returns are chosen with higher weights in the portfolio. On the other hand, for larger and , the algorithm adds more perturbations to the original data, which will lead a more conservative portfolio selection. Indeed, as observed in Figure 4, where Figure 4(a) experiments with different values and Figure 4(b) is with different , when or increases, the outcome of Algorithm 3 will converge to an equally-weighted portfolio.

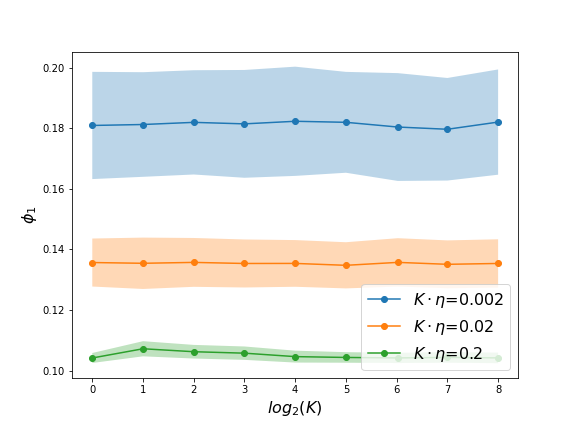

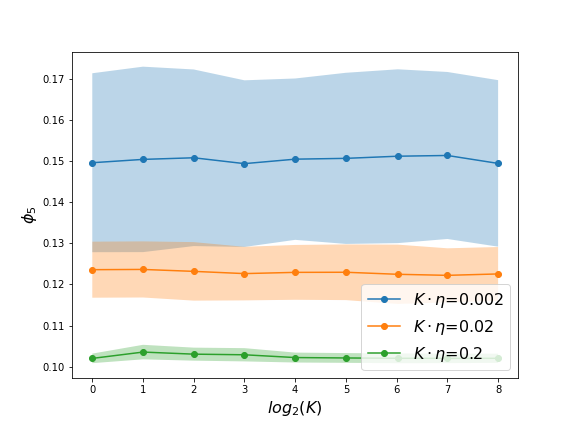

Another finding from Figure 4 is that, while keeping the product unchanged (for example, in Figure 4(a) v.s. in Figure 4(b)), Algorithm 3 yields similar portfolio selections, indicating that may be viewed as an “effective” perturbation power of the adversarial training. This observation is consistent with the SDE approximation in Theorem 3.1 and (3.3), which clearly suggests that and affect the perturbation through . This conclusion is further demonstrated in Figure 5, where three sets of experiments are conducted with and . In each set of experiments, is a fixed constant with varies from to . The portfolio compositions from adversarial training under different choices of and are compared in terms of (the weight on the first asset) in Figure 5(a), and (the weight on the fifth asset) in Figure 5(b). Means and standard deviations of and are computed over 500 simulations. Figure 5 verifies that as long as remains constant, adversarial training, Algorithm 3, produces similar portfolio compositions. Additionally, Figure 5 also indicates that larger adversarial perturbations (larger ) lead to smaller standard deviations of the training outcomes, which is a clear improvement on the robustness.

References

- An et al., [2020] An, J., Lu, J., and Ying, L. (2020). Stochastic modified equations for the asynchronous stochastic gradient descent. Information and Inference: A Journal of the IMA, 9(4):851–873.

- Athalye et al., [2018] Athalye, A., Carlini, N., and Wagner, D. (2018). Obfuscated gradients give a false sense of security: Circumventing defenses to adversarial examples. In Proceedings of the 35th International Conference on Machine Learning, volume 80 of Proceedings of Machine Learning Research, pages 274–283, Stockholmsmassan, Stockholm Sweden. PMLR.

- Ben-Tal et al., [2009] Ben-Tal, A., El Ghaoui, L., and Nemirovski, A. (2009). Robust Optimization, volume 28. Princeton university press.

- Bianca and Dogbe, [2017] Bianca, C. and Dogbe, C. (2017). On the existence and uniqueness of invariant measure for multidimensional diffusion processes. Nonlinear Studies, 24(3).

- Blanchet et al., [2021] Blanchet, J., Chen, L., and Zhou, X. Y. (2021). Distributionally robust mean-variance portfolio selection with wasserstein distances. Management Science.

- Blanchet et al., [2019] Blanchet, J., Kang, Y., and Murthy, K. (2019). Robust wasserstein profile inference and applications to machine learning. Journal of Applied Probability, 56(3):830–857.

- Blanchet and Murthy, [2019] Blanchet, J. and Murthy, K. (2019). Quantifying distributional model risk via optimal transport. Mathematics of Operations Research, 44(2):565–600.

- Cao and Guo, [2020] Cao, H. and Guo, X. (2020). Approximation and convergence of GANs training: an SDE approach. arXiv preprint arXiv:2006.02047.

- Carlini and Wagner, [2017] Carlini, N. and Wagner, D. (2017). Towards evaluating the robustness of neural networks. In 2017 IEEE Symposium on Security and Privacy, pages 39–57. IEEE.

- Chaudhari et al., [2018] Chaudhari, P., Oberman, A., Osher, S., Soatto, S., and Carlier, G. (2018). Deep relaxation: partial differential equations for optimizing deep neural networks. Research in the Mathematical Sciences, 5(3):1–30.

- Chaudhari and Soatto, [2018] Chaudhari, P. and Soatto, S. (2018). Stochastic gradient descent performs variational inference, converges to limit cycles for deep networks. In 2018 Information Theory and Applications Workshop (ITA), pages 1–10. IEEE.

- Chen et al., [2020] Chen, L., Min, Y., Zhang, M., and Karbasi, A. (2020). More data can expand the generalization gap between adversarially robust and standard models. In Proceedings of the 37th International Conference on Machine Learning, volume 119 of Proceedings of Machine Learning Research, pages 1670–1680. PMLR.

- Da Prato, [2006] Da Prato, G. (2006). An Introduction to Infinite-dimensional Analysis. Springer Science & Business Media.

- Deng et al., [2020] Deng, Z., He, H., Huang, J., and Su, W. (2020). Towards understanding the dynamics of the first-order adversaries. In Proceedings of the 37th International Conference on Machine Learning, volume 119 of Proceedings of Machine Learning Research, pages 2484–2493. PMLR.

- Farnia et al., [2019] Farnia, F., Zhang, J., and Tse, D. (2019). Generalizable adversarial training via spectral normalization. In International Conference on Learning Representations.

- Gao et al., [2019] Gao, R., Cai, T., Li, H., Hsieh, C.-J., Wang, L., and Lee, J. D. (2019). Convergence of adversarial training in overparametrized neural networks. In Advances in Neural Information Processing Systems, volume 32, pages 13029–13040. Curran Associates, Inc.

- Goodfellow et al., [2014] Goodfellow, I. J., Shlens, J., and Szegedy, C. (2014). Explaining and harnessing adversarial examples. arXiv preprint arXiv:1412.6572.

- Hong and Wang, [2019] Hong, J. and Wang, X. (2019). Invariant Measures for Stochastic Differential Equations. In Invariant Measures for Stochastic Nonlinear Schrödinger Equations, pages 31–61. Springer.

- Karatzas and Shreve, [2014] Karatzas, I. and Shreve, S. (2014). Brownian Motion and Stochastic Calculus, volume 113. springer.

- Khasminskii, [2011] Khasminskii, R. (2011). Stochastic Stability of Differential Equations, volume 66. Springer Science & Business Media.

- Krichene and Bartlett, [2017] Krichene, W. and Bartlett, P. L. (2017). Acceleration and averaging in stochastic descent dynamics. In Advances in Neural Information Processing Systems, volume 30, pages 6796–6806. Curran Associates, Inc.

- Li et al., [2017] Li, Q., Tai, C., and E, W. (2017). Stochastic modified equations and adaptive stochastic gradient algorithms. In Proceedings of the 34th International Conference on Machine Learning, volume 70 of Proceedings of Machine Learning Research, pages 2101–2110, International Convention Centre, Sydney, Australia. PMLR.

- Li et al., [2019] Li, Q., Tai, C., and E, W. (2019). Stochastic modified equations and dynamics of stochastic gradient algorithms I: Mathematical foundations. Journal of Machine Learning Research, 20(40):1–47.

- Madry et al., [2018] Madry, A., Makelov, A., Schmidt, L., Tsipras, D., and Vladu, A. (2018). Towards deep learning models resistant to adversarial attacks. In International Conference on Learning Representations.

- Maini et al., [2020] Maini, P., Wong, E., and Kolter, Z. (2020). Adversarial robustness against the union of multiple perturbation models. In Proceedings of the 37th International Conference on Machine Learning, volume 119 of Proceedings of Machine Learning Research, pages 6640–6650. PMLR.

- Mandt et al., [2015] Mandt, S., Hoffman, M. D., and Blei, D. M. (2015). Continuous-time limit of stochastic gradient descent revisited. In OPT Workshop, Advances in Neural Information Processing Systems.

- Mohajerin Esfahani and Kuhn, [2018] Mohajerin Esfahani, P. and Kuhn, D. (2018). Data-driven distributionally robust optimization using the wasserstein metric: performance guarantees and tractable reformulations. Mathematical Programming, 171(1).

- Nguyen et al., [2020] Nguyen, V. A., Zhang, X., Blanchet, J., and Georghiou, A. (2020). Distributionally robust parametric maximum likelihood estimation. Advances in Neural Information Processing Systems, 33:7922–7932.

- Pflug and Wozabal, [2007] Pflug, G. and Wozabal, D. (2007). Ambiguity in portfolio selection. Quantitative Finance, 7(4):435–442.

- Raghunathan et al., [2020] Raghunathan, A., Xie, S. M., Yang, F., Duchi, J., and Liang, P. (2020). Understanding and mitigating the tradeoff between robustness and accuracy. In Proceedings of the 37th International Conference on Machine Learning, volume 119 of Proceedings of Machine Learning Research, pages 7909–7919. PMLR.

- Ren and Majumdar, [2022] Ren, A. Z. and Majumdar, A. (2022). Distributionally robust policy learning via adversarial environment generation. IEEE Robotics and Automation Letters, 7(2):1379–1386.

- Rockafellar and Uryasev, [2000] Rockafellar, R. T. and Uryasev, S. (2000). Optimization of conditional value-at-risk. Journal of Risk, 2(3).

- Seidman et al., [2020] Seidman, J. H., Fazlyab, M., Preciado, V. M., and Pappas, G. J. (2020). Robust deep learning as optimal control: Insights and convergence guarantees. In Proceedings of the 2nd Conference on Learning for Dynamics and Control, volume 120 of Proceedings of Machine Learning Research, pages 884–893, The Cloud. PMLR.

- Si et al., [2020] Si, N., Zhang, F., Zhou, Z., and Blanchet, J. (2020). Distributional robust batch contextual bandits. arXiv preprint arXiv:2006.05630.

- Sinha et al., [2017] Sinha, A., Namkoong, H., Volpi, R., and Duchi, J. (2017). Certifying some distributional robustness with principled adversarial training. arXiv preprint arXiv:1710.10571.

- Szegedy et al., [2013] Szegedy, C., Zaremba, W., Sutskever, I., Bruna, J., Erhan, D., Goodfellow, I., and Fergus, R. (2013). Intriguing properties of neural networks. arXiv preprint arXiv:1312.6199.

- Vapnik, [1991] Vapnik, V. (1991). Principles of risk minimization for learning theory. In Advances in Neural Information Processing Systems, volume 4, pages 831–838. Morgan Kaufmann Publishers Inc.

- Veretennikov, [1988] Veretennikov, A. Y. (1988). Bounds for the mixing rate in the theory of stochastic equations. Theory of Probability & Its Applications, 32(2):273–281.

- Wang et al., [2019] Wang, Y., Ma, X., Bailey, J., Yi, J., Zhou, B., and Gu, Q. (2019). On the convergence and robustness of adversarial training. In Proceedings of the 36th International Conference on Machine Learning, volume 97 of Proceedings of Machine Learning Research, pages 6586–6595. PMLR.

- Yan et al., [2018] Yan, Z., Guo, Y., and Zhang, C. (2018). Deep defense: Training dnns with improved adversarial robustness. In Advances in Neural Information Processing Systems, volume 31, pages 419–428. Curran Associates, Inc.

- Yin et al., [2019] Yin, D., Kannan, R., and Bartlett, P. (2019). Rademacher complexity for adversarially robust generalization. In Proceedings of the 36th International Conference on Machine Learning, volume 97 of Proceedings of Machine Learning Research, pages 7085–7094. PMLR.

- Zhang et al., [2019] Zhang, D., Zhang, T., Lu, Y., Zhu, Z., and Dong, B. (2019). You Only Propagate Once: Accelerating adversarial training via maximal principle. In Advances in Neural Information Processing Systems, volume 32, pages 227–238. Curran Associates, Inc.

- [43] Zhang, J., Xu, X., Han, B., Niu, G., Cui, L., Sugiyama, M., and Kankanhalli, M. (2020a). Attacks which do not kill training make adversarial learning stronger. In Proceedings of the 37th International Conference on Machine Learning, volume 119 of Proceedings of Machine Learning Research, pages 11278–11287. PMLR.

- [44] Zhang, Y., Plevrakis, O., Du, S. S., Li, X., Song, Z., and Arora, S. (2020b). Over-parameterized adversarial training: An analysis overcoming the curse of dimensionality. arXiv preprint arXiv:2002.06668.