A Gambler that Bets Forever and the Strong Law of Large Numbers

Calvin Wooyoung Chin

Abstract.

In this expository note, we give a simple proof that a gambler repeating a game

with positive expected value never goes broke with a positive probability.

This does not immediately follow from the strong law of large numbers or

other basic facts on random walks.

Using this result, we provide an elementary proof of

the strong law of large numbers.

The ideas of the proofs come from the maximal ergodic theorem

and Birkhoff’s ergodic theorem.

A gambler that makes the same bet on a single number over and over

in a game of American roulette is bound to go broke with probability .

This has to do with the fact that the house has an edge of 5.26% in average,

and it turns out that the same is true for any other game with negative

expected value.

This general fact, sometimes called gambler’s ruin,

is a direct consequence of the strong law of large numbers.

To see this, let be i.i.d. (real-valued) random variables

with finite mean, representing the gains from the games.

For each , write , denoting

the capital of the gambler after the -th game.

The strong law of large numbers says that with

probability . If , then takes a negative value

at some point with probability , and thus so does .

This proves gambler’s ruin.

What if the game favors the gambler in the sense that ?

Is it possible that the game continues forever without the gambler going broke?

Mathematically, do we have

(1)

An argument similar to the one given above shows that stays positive

after some point with probability .

However, this does not exclude the possibility of having

before eventually remains positive.

If only takes as values, a classical approach

[1, Section 6.2]

involving difference equations yields (1).

More generally, if is bounded and , then we can use the fact

that is a martingale for some to

obtain (1); see [2, Theorem 4.8.9].

However, these methods do not easily generalize to arbitrary

with finite mean.

In this expository note, we first illustrate a proof of

(1) for arbitrary with positive mean.

The idea behind the proof is to observe that we need to show

the so-called maximal ergodic theorem [2, Lemma 6.2.2].

We then use our result to prove the strong law of large numbers.

The idea comes from the proof of Birkhoff’s ergodic theorem

[2, Theorem 6.2.1], but our proof is rather elementary.

In particular, we do not explicitly invoke advanced theorems, and

we avoid using notions such as limit superior.

Given that we obtain an interesting theorem on gambling along the way,

our exposition offers a clear and efficient approach to the strong law

of large numbers.

Let us start by proving (1) for arbitrary

with positive mean.

Theorem 1.

If , then .

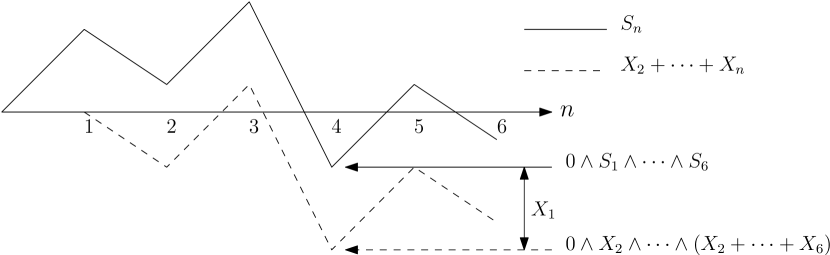

Proof.

Let us write to denote the minimum

among .

For each , we claim the following:

(2)

If , then the equality holds;

see Figure 1.

If , then the left side is ,

while the right side is nonpositive. Thus, (2) is proved.

taking the expectation of both sides of (2) yields

Letting , we have

(by dominated convergence).

Since , we have

which is equivalent to the desired conclusion.

∎

We continue on to prove the strong law of large numbers.

Theorem 2(strong law of large numbers).

We have with probability .

Proof.

We may assume that .

Given , let play the role of in

Theorem 1. Then we have

which is equivalent to

Let denote the positive probability on the left side.

If we write “eventually” to mean “for all for some ,”

then for any we have

So, and

are independent, and thus

Letting yields

Since , we have

The symmetrical argument yields

Let and be the events in the previous two displays.

On , we have .

Since

the proof is completed.

∎

References

[1] Ash, R. B. (1970). Basic Probability Theory. New York–London–Sydney: John Wiley & Sons, Inc.

[2] Durrett, R. (2019). Probability: Theory and Examples, 5th ed. Cambridge Series in Statistical and Probabilistic Mathematics, 49. Cambridge: Cambridge University Press.