newfloatplacement\undefine@keynewfloatname\undefine@keynewfloatfileext\undefine@keynewfloatwithin

On a Standard Method for Measuring the

Natural Rate of Interest††thanks: Without implications, I am grateful to Adrian Pagan, Paolo Giordani, Claus

Brand, Jim Stock, Jesper Lindé and Kurt Mitman for comments. I thank two

anonymous referees for remarks that helped to improve previous versions of

the paper. I am grateful to the Jan Wallander and Tom Hedelius Foundation

and the Tore Browaldh Foundation for research support.

| First Version : | October 13, 2020 |

|---|---|

| This Version (): |

)

Abstract

I show that Holston, Laubach and Williams’ (2017) implementation of Median Unbiased Estimation (MUE) cannot recover the signal-to-noise ratio of interest from their Stage 2 model. Moreover, their implementation of the structural break regressions which are used as an auxiliary model in MUE deviates from Stock and Watson’s (1998) formulation. This leads to spuriously large estimates of the signal-to-noise parameter and thereby an excessive downward trend in other factor and the natural rate. I provide a correction to the Stage 2 model specification and the implementation of the structural break regressions in MUE. This correction is quantitatively important. It results in substantially smaller point estimates of which affects the severity of the downward trend in other factor . For the US, the estimate of shrinks from to and is statistically highly insignificant. For the Euro Area, the UK and Canada, the MUE point estimates of are exactly zero. Natural rate estimates from HLW’s model using the correct Stage 2 MUE implementation are up to 100 basis points larger than originally computed.

Keywords: Natural rate of interest, Median Unbiased Estimation, Kalman

Filter, misspecified econometric models, correction to Stage 2 model.

JEL Classification: C32, E43, E52, O40.

1 Introduction

Holston, Laubach and Williams’ (2017) (simply HLW’s henceforth) estimates of the natural rate of interest have become a benchmark or reference rate — not only for policy makers at central banks — but also for asset managers and finance professionals needing to make long-term investment decisions for their clients.

One of the reasons for the model’s popularity and widespread use is its simplicity; the core of the structural model is reminiscent of a New Keynesian Policy model, albeit without a central bank reaction function (see Galí (2015) and Buncic and Melecky (2008)). Another reason is the availability of computer code that is published on the website of the Federal Reserve Bank of New York (FRBNY), which makes the non-standard estimation of the model accessible to a broader audience. The fact that the model is used to inform US policy makers about monetary policy decisions adds further to the credibility and relevance of the model.333The model can also be viewed as multivariate version of the unobserved component model of Clark (1987) (adding an inflation equation and allowing for interactions between inflation and the output gap equations), or as a multivariate filter (see Benes. et al. (2010)).

In this paper, I show that HLW’s implementation of Stock and Watson’s (1998) (SW’s) Median Unbiased Estimation (MUE) to determine the size of the signal-to-noise ratio parameter cannot recover the ratio of interest from MUE. This inability to recover the ratio of interest is due to a misspecification in HLW’s Stage 2 model formulation. I show further that the structural break regressions which are used as an auxiliary model in MUE are modified from SW’s original implementation in the simulations used to construct the look-up values in Table 3 of their paper. The misspecification in the Stage 2 model — together with the modification of the structural break regressions — leads to spuriously large estimates of the signal-to-noise ratio parameter , which affects the severity of the downward trend in other factor , and thereby the estimates of the natural rate of interest in HLW’s model.

I provide a correction to the specification of the Stage 2 model that is consistent with the signal-to-noise ratio used in the estimation of the full structural model of the natural rate, and further implement the structural break regressions in line with the simulations employed by SW to construct the MUE look-up values. The correction that I provide is quantitatively important. For the Euro Area, the UK, and Canada, the (corrected) MUE point estimates of are exactly . The downward trend in the estimates of other factor disappears entirely, with the estimates at (or very close to) zero. For the US, the point estimate shrinks from to , resulting in a much more subdued downward trend in other factor . The ensuing natural rate estimates are affected most strongly at the end of the sample period. For the US, the (corrected) estimate of is over basis points larger at approximately percentage points than from HLW’s (misspecified) implementation of . For the Euro Area, is approximately basis points larger at percentage points, instead of , while for the UK and Canada, the differences are more subtle, being respectively ( percentage points instead of ) and basis points larger ( percentage points instead of ). Estimates of trend growth remain unaffected by the proposed correction to the Stage 2 MUE implementation.

This paper is related to — but distinct from — a broader literature on estimating the natural rate of interest. For instance, Berger and Kempa (2019) use a Bayesian estimation approach to avoid pile-up at zero problems, implementing the non-centered state-space parameterisation of Frühwirth-Schnatter and Wagner (2010) for other factor to be able to test if is greater than zero.444Berger and Kempa (2019) also allow the variances of the shocks to the output gap and trend growth equations to follow integrated stochastic volatility processes, adding further a (latent) real rate cycle equation to HLW’s model, so the model is a somewhat modified version of HLW’s original set-up. They find the posterior density of to be centred at zero, suggesting no variation in other factor . Lewis and Vazquez-Grande (2018) also employ a Bayesian approach to estimate a less restrictive version of HLW’s model, ie., one that specifies trend growth and other factor to follow AR(1) processes instead of random walks. They find that should be modelled as an AR(1) process with transitory shocks, instead of following a random walk. Kiley (2020), who also uses a Bayesian estimation approach, but on a model that does not separate the natural rate into the sum of other factor and trend growth, finds that there is little information in the data to determine the process that generated the natural rate. These studies offer interesting additional results on other factor and the natural rate. The objective of the current paper is, nonetheless, to provide a correction to HLW’s Stage 2 model and MUE implementation, and to make it accessible to users of this model.555Accompanying Matlab and R code files that replicate the results presented here — together with filtered and smoothed estimates of the natural rate of interest, trend growth, other factor , and the output gap for all four countries — are available from: http://www.danielbuncic.com.

As a final remark to readers familiar with (or interested in) the original model of Laubach and Williams (2003) which first proposed MUE for the estimation of the natural rate from a structural model, the problems that I outline here with HLW’s Stage 2 model and the MUE implementation are exactly the same. This can be easily verified by expanding the matrices in Section 4.4 “The Stage 2 Model” on page 4 of the PDF file: “LW_Code_Guide.pdf” contained in the replication code zip file posted on the FRBNY website at https://www.newyorkfed.org/medialibrary/media/research/economists/williams/data/LW˙replication.zip. The vector in equation (8) only contains one lag of trend growth () and the extra parameter in the matrix, resulting in a Stage 2 output gap equation that is equivalent to HLW’s misspecified formulation shown in the right column block of (6c) below. The structural break regressions needed for MUE in Stage 2 are implemented in the same way as in HLW (see lines 109 to 114 in the R file rstar.stage2.R which prepares the and data to be called in the median.unbiased.estimator.stage2.R function implementing the structural break regressions in lines 10 to 15).

The remainder of the paper is organized as follows. Section 2 gives a brief outline of Holston et al.’s (2017) structural model of the natural rate of interest, and contrasts how Median Unbiased Estimation is implemented in SW and in HLW. Section 3 provides the empirical results. In Section 4, the study is concluded.

2 Holston et al.’s (2017) structural model and MUE

2.1 Model set-up

Holston et al.’s (2017) structural model of the natural rate takes the following form:

| Output | : | (1a) | |||||

| Inflation | : | (1b) | |||||

| Output gap | : | (1c) | |||||

| Output trend | : | (1d) | |||||

| Trend growth | : | (1e) | |||||

| Other factor | : | (1f) | |||||

where the terms , , and are lag polynomials that capture the dynamics in inflation , the output gap , and the real rate cycle , and denotes the lag operator. Output is constructed as 100 times the log of real GDP, is annualized quarter-on-quarter PCE inflation, and the real interest rate is computed as where is the federal funds rate, and expected inflation is approximated by . The natural rate of interest is defined as the sum of annualized trend growth and other factor , each of which follow first order integrated processes. The error terms in (1) are assumed to be , mutually uncorrelated, and with time-invariant standard deviations denoted by .

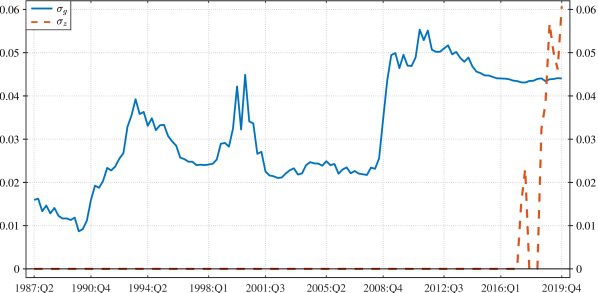

HLW argue that due to pile-up at zero problems with Maximum Likelihood Estimation (MLE) of and in (1), these estimates are ‘likely to be biased towards zero’ (Holston et al. (2017), p. S64). To avoid pile-up problems, HLW estimate and indirectly from the signal-to-noise ratios and computed in two preliminary stages (referred to as Stage 1 and Stage 2) using SW’s MUE. In the sections below, I briefly outline how MUE is implemented in SW, before describing the procedure that HLW adopt in Stage 2. This description is necessary to understand that these differences in implementation lead to very different estimates of , other factor , and ultimately the natural rate . Because I do not encounter any pile-up at zero problems with MLE of , only HLW’s Stage 2 model and implementation of MUE is described in what follows.666A referee has pointed out that MLE of in the full model in (1) may not generate pile-up at zero problems in the sample that I consider, but may well have in the sample of data used when the estimation framework was proposed in Laubach and Williams (2003), ie., with data up to 2002:Q2. In Figure 1 I plot recursive ML estimates of and from HLW’s full model in (1) with the sample ending in 1987:Q2 up to 2019:Q4, with one quarter update increments. The data were downloaded from FRED on the of May 2020. The MLE of never shrinks to zero. The MLE of does shrink to zero in every sample up to mid 2018. Although I do not have the vintage of data from their 2003 paper, estimating by MLE does not generate any pile-up at zero problems in currently available data.

2.2 Median Unbiased Estimation in SW and HLW’s Stage 2 model

Stock and Watson (1998) introduced MUE in the context of a local-level model for the estimation of US per capita trend growth, taking the form:

| (2a) | ||||

| (2b) | ||||

| (2c) | ||||

where and are two and mutually uncorrelated disturbance terms. They derived the MUE parameter of interest to be: “… times the ratio of the long-run standard deviation of to the long run standard deviation of .” (Stock and Watson (1998), p. 351, right column, top of the page, with denoting the sample size). Re-arranging, gives the following definition of the signal-to-noise ratio parameter of interest:

| (3) |

where is an AR(4) lag polynomial and denotes the long-run standard deviation. Equation (3) relates to the signal-to-noise ratio in the local-level model in (2).

In Holston et al. (2017), the signal-to-noise ratio is used in the estimation of the full model in (1). To see algebraically why in HLW’s model, assume for now that the latent cycle and trend growth variables and , as well as all the parameters , and in (1) are known. The objective is to obtain an estimate of the standard deviation of () using SW’s MUE. To do so, one needs to formulate a local-level model involving the output gap in (1c) and the equation for the latent process in (1f). This formulation is analogous to the trend growth specification in (2) and takes the following form:

| (4a) | ||||

| (4b) | ||||

where is the counterpart to the time-varying mean process in (2). The signal-to-noise ratio corresponding to (3) for the local-level model specification of the relevant equation of HLW’s model in (4) is then:

| (5) |

due to , and , since is serially uncorrelated by assumption. The last term in (5) gives HLW’s Stage 2 signal-to-noise ratio . Once has been estimated by MUE, is replaced by in the full model’s likelihood function, and is held fixed at the MUE point estimate in the estimation of the remaining parameters of the model in equation (1).

2.3 The empirical Stage 2 model in HLW and the Correct specification

In the derivation of the algebraic relationship between and in (5) it was assumed that the latent cycle and trend growth variables and , as well as all the parameters , and in (4) are known. In practice, however, these are unknown and will need to be replaced by estimates obtained from a preliminary model, called the ‘Stage 2’ model in HLW. This Stage 2 model is a restricted form of the full model in (1) and is needed to compute estimates of the unknown parameters and latent states of the empirical counterpart to the local-level model in (4). As such, the Stage 2 model should simply be defined as the full model in (1), but with excluded from the output gap relation in (1c), and the equation for in (1f) entirely removed from the model. This ‘Correct Stage 2’ model, shown in the left column block in (6) below, is consistent with the full model’s output gap definition in (1c) and yields HLW’s signal-to-noise ratio , as demonstrated algebraically in (4) and (5) above.

Instead of formulating the Stage 2 model in this way, HLW modify the output gap equation to contain only one lag of trend growth in the model and further add an intercept term, with the parameter on the lagged trend growth term not restricted to be .777The inclusion of the intercept term has been defended by HLW, arguing: ”A constant is needed in this equation because excluding it would impose a sample mean of zero for the variable , which captures the movements in the natural rate of interest not related to trend GDP growth. Such a restriction is neither implied by the model (z is a random walk and therefore the sample mean need not be zero), nor is it supported by the data.” I show in the Stage 2 estimates reported in Tables Figures and Tables, Figures and Tables, Figures and Tables and Figures and Tables that the intercept term is in fact not supported by the data (see the last column under the heading ‘Correct’). The largest increase in the log-likelihood function is for the US. With one degree of freedom, , yields an upper Chi-square value of . A constant is not needed in the correct Stage 2 model shown in the left column block of (6). For the Euro Area, the UK and Canada, the increases in the log-likelihoods are even smaller at , , and . These two different Stage 2 model specifications are contrasted in the left and right column blocks of (6) below.888The trend growth equation in (6d) is also misspecified due to instead of being included in the relation, making , that is, an MA(1) process. Due to the additional term in the (trend) equation, the covariance matrix of the error terms of the state vector will not be diagonal anymore. Since the focus here is on the output gap misspecification, I do not discuss this any further.

| Correct Stage 2 model | HLW’s (misspecified) Stage 2 model | |||||

| (6a) | ||||||

| (6b) | ||||||

| (6c) | ||||||

| (6d) | ||||||

| (6e) | ||||||

The error terms corresponding to the two output-gaps in (6c) are, respectively:

| Correct Stage 2 model | HLW’s (misspecified) Stage 2 model | |||||

| (7a) | ||||||

| (7b) | ||||||

| (7c) | ||||||

| (7d) | ||||||

To see what theoretical signal-to-noise ratio can be recovered from HLW’s (misspecified) Stage 2 model specification in the right column of (7), one needs to go through the same algebraic steps as in equations (4) and (5) above. That is, assume that and , as well as , , , , are known (or have been estimated). Then, formulating once again a local-level model analogous to (4), but now for HLW’s (misspecified) Stage 2 model, yields:

| (8a) | ||||

| (8b) | ||||

where

| (9) |

in (8a) is the (misspecified) error term corresponding to in the local-level model in (4).999Observe that so that The resulting signal-to-noise ratio is then:

| (10) |

which now requires the evaluation of the long-run standard deviation of in the denominator of (10). Even if in (9), the long-run standard deviation of will depend on due to the extra term in , giving:

| (11) |

As can be seen from (11), MUE applied to HLW’s (misspecified) Stage 2 model cannot recover the ratio of interest . Estimating the full model in (1) with replaced by in the Kalman Filter recursion that builds up the likelihood function is thus inconsistent with the signal-to-noise ratio obtained from HLW’s (misspecified) Stage 2 model.

2.4 Structural break regressions in MUE

The previous section showed algebraically that HLW’s (misspecified) Stage 2 model cannot recover the ratio of interest from MUE. I now contrast SW’s and HLW’s implementations of the structural break regressions used as the auxiliary model in MUE.

Note that MUE is fundamentally an indirect estimator. A structural break test statistic is used to recover the parameter of interest, which is the signal-to-noise ratio . SW do not only provide the theory behind MUE, but also supply look-up values (Table 3 on page 354 in Stock and Watson (1998)) that convert a set of structural break test statistics into Median Unbiased estimates of (dividing by the sample size gives ). These look-up values were constructed by simulation, and are valid for the local-level model and the structural break tests as implemented in SW.101010As a reminder, the look-up table for MUE of on page 354 in Stock and Watson (1998) was constructed by simulating observations from the local-level model for increasing values of from , and then testing the observed series for a structural break in the unconditional mean as in (12), that is, without any other ‘extra regressors’. This process was repeated 5000 times. The resulting 5000 values from the structural break test statistics were then ordered, with the median of those being the MUE. When employing MUE empirically, one works the other way around and infers the value of from the structural break test statistics.

Stock and

Watson (1998) construct the structural break tests as follows.

First, the GDP growth variable in (2a) is filtered by

fitting an AR(4) model to capture the dynamics of .111111See the implementation in Stock and

Watson’s (1998) GAUSS file TST_GDP1.GSS which is

available from Mark Watson’s homepage at http://www.princeton.edu/~mwatson/ddisk/tvpci.zip, in particular, lines

39 to 66 which AR(4) filter the GDP growth data, and lines 68 to 83 which

then implement the Chow (1960) type structural break tests to the AR(4)

filtered data. Then, the AR(4) filtered series (which I denote by

below) is tested for a structural break in the

unconditional mean by running the following dummy variable regression for

each potential break point :

| (12) |

where is the estimated counterpart to the AR(4) lag polynomial in (2c), is a dummy variable that is equal to if and otherwise, and is an index (or sequence) of grid points between endpoints and .121212Stock and Watson (1998) set these endpoints at the and percentiles of the sample size , that is, and . More precisely, is computed as and as in their GAUSS code. In HLW, these are set at and , respectively. The (sequence of) statistics on the point estimates is then utilized in the computation of the following structural break test statistics:

| (13a) | ||||

| (13b) | ||||

| (13c) | ||||

where MW and EW are, respectively, Andrews and Ploberger’s (1994) mean Wald and exponential Wald tests, and QLR is Quandt’s (1960) Likelihood ratio test. SW also compute Nyblom’s (1989) statistic, which is constructed directly from the sum of squared cumulative sums of the demeaned series, and therefore does not require a structural break regression involving dummy variables as in (12).131313In our setting, Nyblom’s (1989) statistic provides a consistency check on the break test implementation, as it is not affected by how the structural break tests are implemented. Look-up Table 3 in Stock and Watson (1998) gives the mapping between the various structural break test statistics and values.

Observe how the structural break regressions in (12) are implemented. The regressand, the left-hand side variable in (12), is constructed only once outside the dummy variable regression loop and there are no other ‘extra regressors’ on the right-hand side, ie., only the break dummy is included on the right-hand side. To make this last point clear, the break regressions are not estimated as:

| (14) |

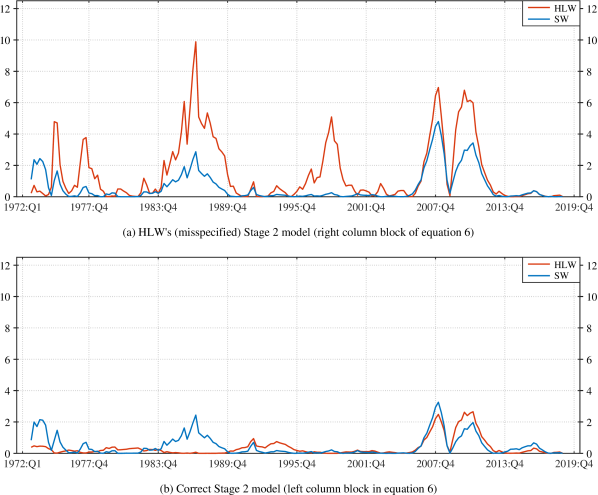

ie., with as the left-hand side variable, and extra regressors added to the right-hand side of the regression in (12). These two different forms of the break test implementations in (12) and (14) lead to vastly different sequences of statistics on . In Figure 2 I provide a visual illustration of how different the resulting sequences computed from the two versions of the structural break regressions are in the context of SW’s study on trend growth. The implementation in (14) results in a sequence that is substantially larger at values between 7 to 8, while SW’s original implementation in (12) yields estimates in the 0 to approximately 3 range. The MW, EW and QLR structural break statistics defined in (13) corresponding to the different sequences can differ by a factor of (almost) up to 10.141414Specifically, these are: and for the MW, EW and QLR tests, from the break regressions in (12) and (14), respectively. Since the break statistics are used together with the look-up values in Table 3 of SW to arrive at the MUE of , any differences in these will directly impact the estimates of .

Now HLW’s implementation of the structural break regressions is of the second form, that is, as in (14). What makes matters worse is that these structural break regressions are implemented on HLW’s (misspecified) Stage 2 model shown in the right column of (6), which spuriously amplifies the sequence of statistics even further. Specifically, HLW obtain on from the following break regression:

| (15) |

rather than from:

| (16) |

For the correct Stage 2 model, these would be:

| (17) |

and:

| (18) |

where , , , , are the corresponding estimated Stage 2 coefficients, and and are the Kalman smoothed estimates of the output gap and trend growth , respectively.

Since all Stage 2 model parameters as well as latent states have already been estimated from the full sample of data before implementing the structural break regressions needed for MUE, there is no reason not to formulate the left-hand side variable in the local-level model to be consistent with the specification in (4a) used to (theoretically) derive the signal-to-noise ratio to be . It is the variation in the unconditional mean of the left-hand side variable in (4a) that needs to be tested for a structural break, and not the variation in the mean of , conditional on . For HLW’s (misspecified) Stage 2 model, these two different break test implementations yield vastly different sequences of statistics and estimates. For the correct Stage 2 model, the differences are considerably smaller. It is precisely the combination of HLW’s (misspecified) Stage 2 model formulation together with their modified break test implementation that affects the parameter of interest and leads to the spurious downward trend in other factor . The Stage 2 model’s parameter estimates as such are not materially affected.

3 Empirical results

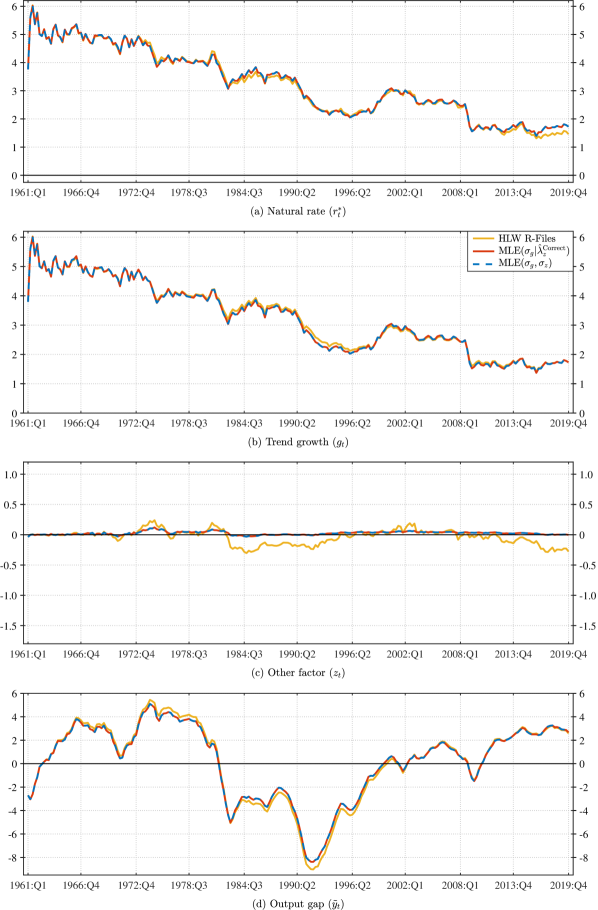

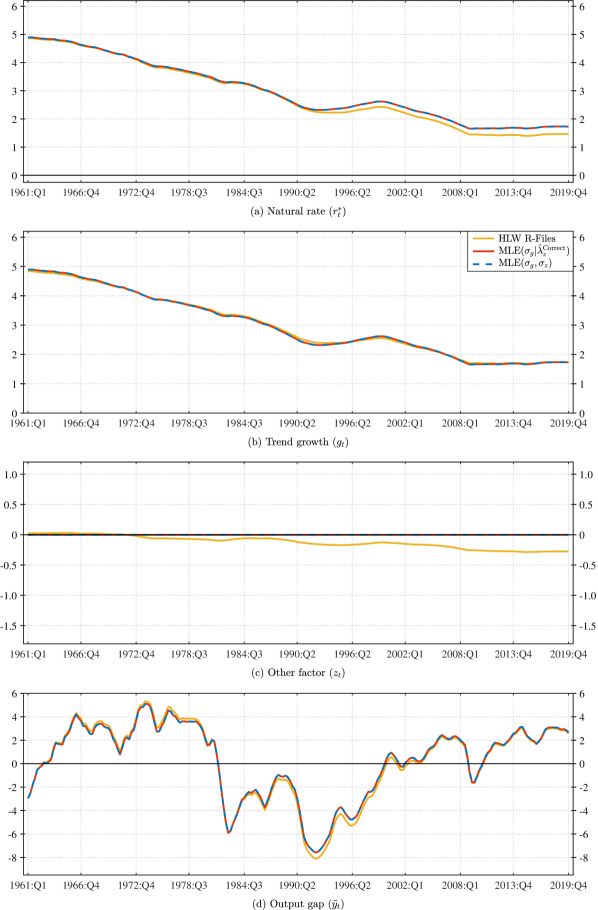

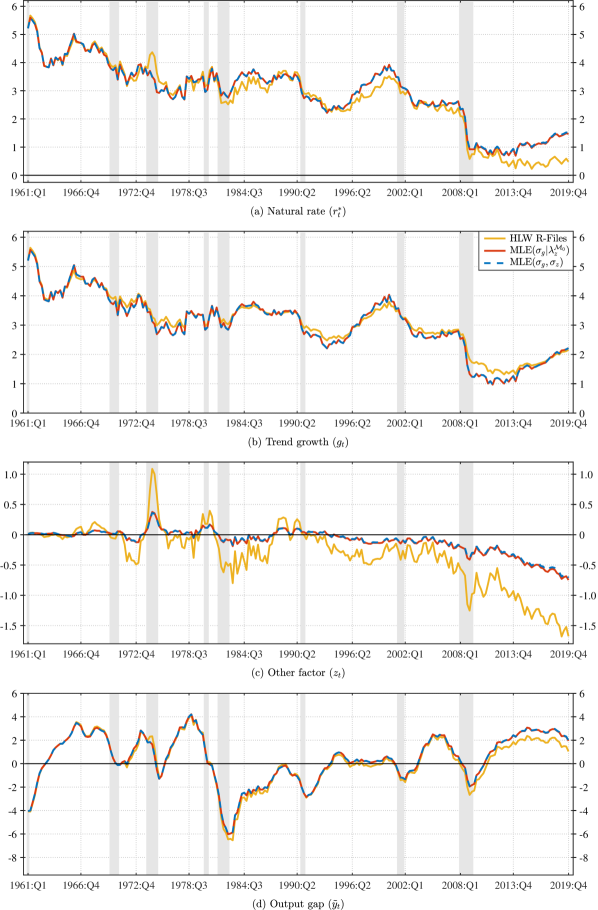

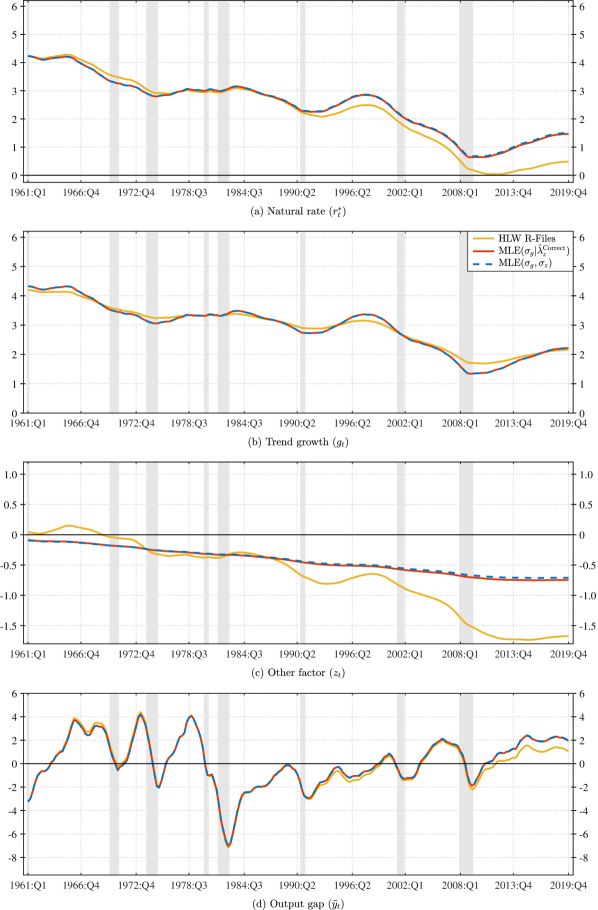

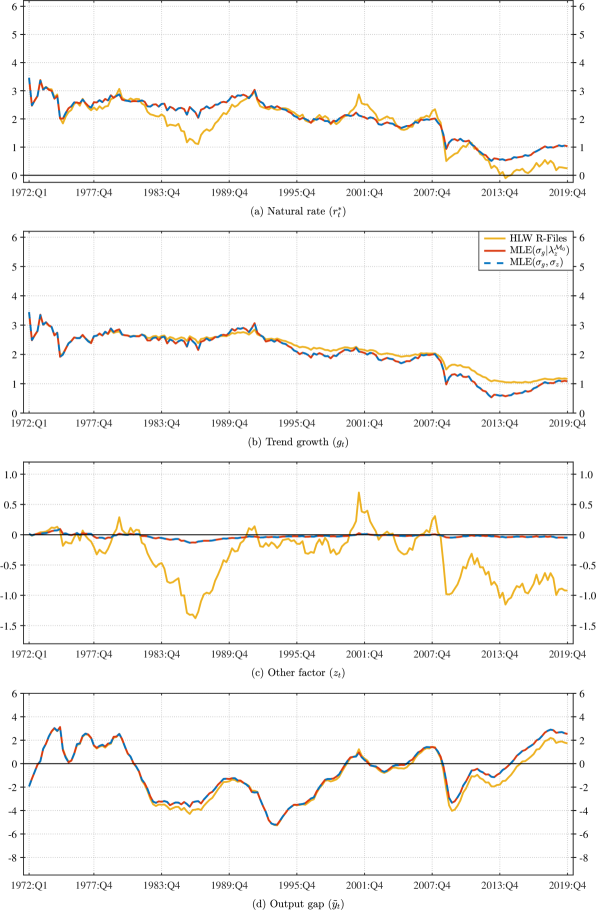

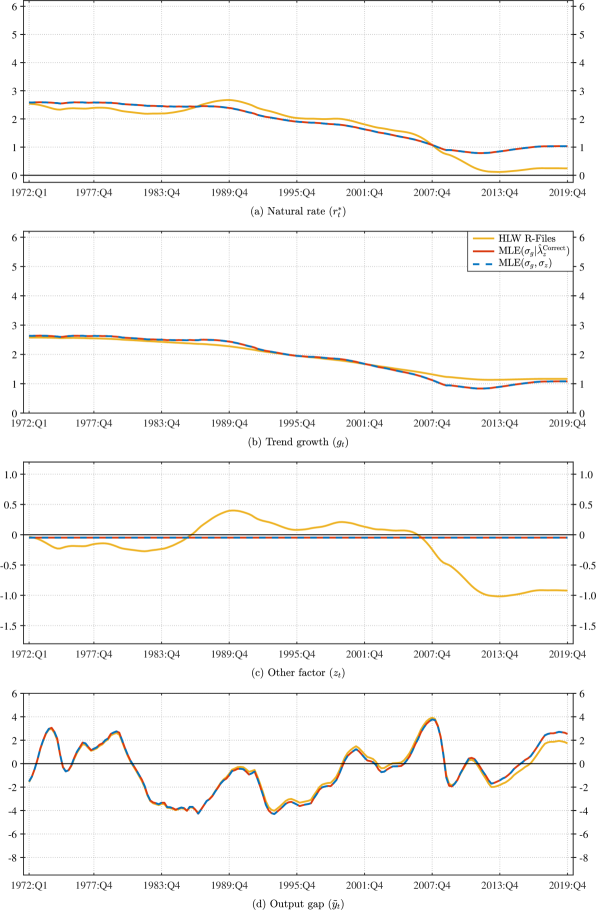

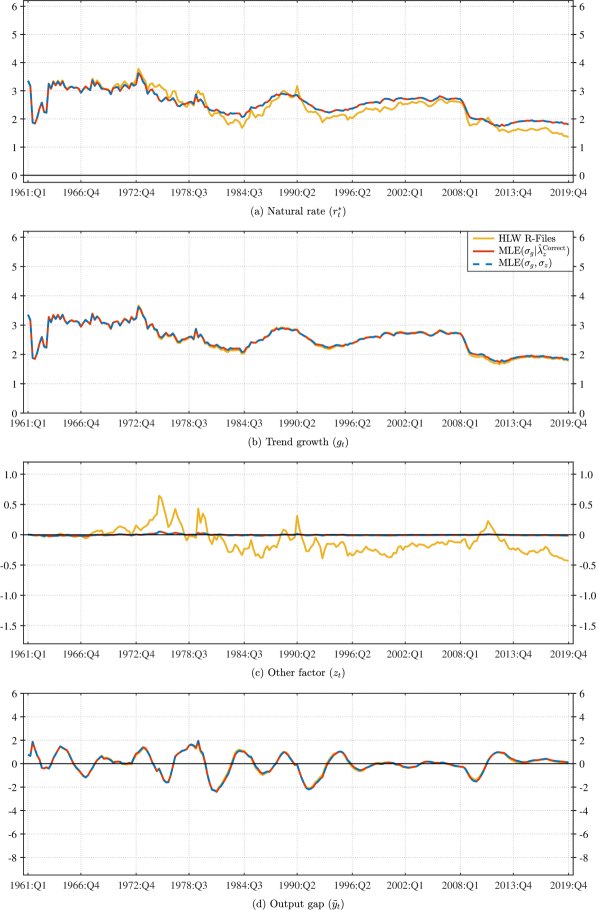

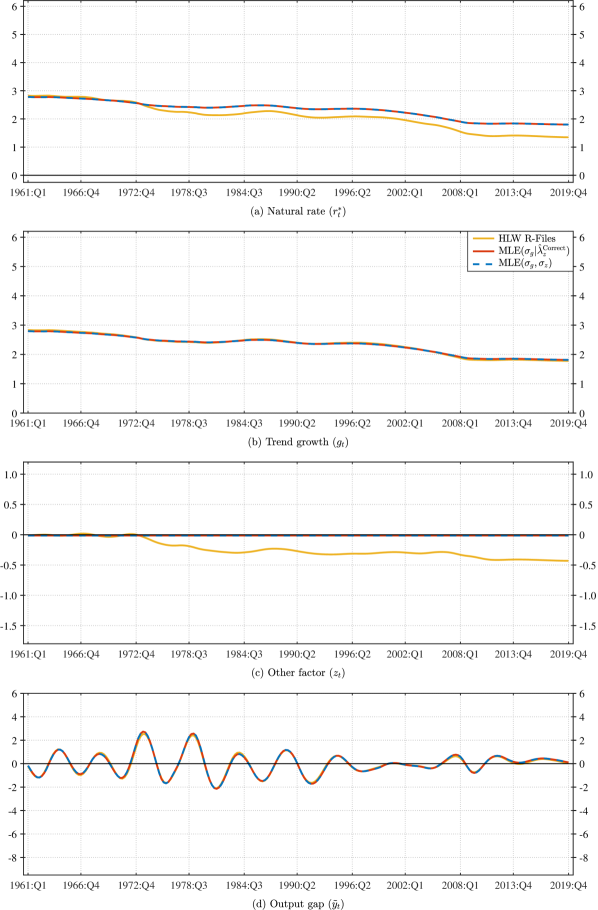

This section provides the full empirical estimation results of the correct Stage 2 model specification using the structural break test implementation as in SW. HLW’s estimates are also reported for comparison. Some results are provided as supplementary information or for reasons of completeness, and do not merit any discussion. I use the same data as described in Holston et al. (2017) (see the replication files for details) with the sample ending in 2019:Q4. Readers not interested in the Stage 2 MUE results as such can skip directly to the plots of the smoothed natural rate , trend growth , other factor , and the output gap in Figures 5, 8, 11 and 14 (filtered estimates are shown in in Figures 4, 7, 10 and 13).

In Tables Figures and Tables, Figures and Tables, Figures and Tables and Figures and Tables, the Stage 2 model parameter estimates for the US, the Euro Area, the UK and Canada are reported. The first column (‘HLW.R-File’) provides HLW’s estimates obtained from their R-Files. The second column (‘HLW()’) reports estimates from HLW’s (misspecified) Stage 2 model, but with estimated directly by MLE together with the other parameters of the model. The third column (‘Correct’) lists the estimates from the correct Stage 2 model defined in the left column block of (6), with again estimated directly by MLE. The last column (‘Correct + ’) shows the correct Stage 2 model’s estimates when an additional intercept term is added to the model.151515Values in round brackets are implied from the Stage 1 signal-to-noise ratio relation . As can be seen, the MLE of in the Stage 2 model does not shrink to zero for any of the estimates and is in fact larger than the one obtained from MUE for three of the four series. The Stage 1 model is thus not needed as an auxiliary model to estimate — at least not for this data set. Further, all intercept terms () in the correct Stage 2 model are (highly) insignificant, indicating that the correct Stage 2 auxiliary model does not need to be formulated with an intercept term.

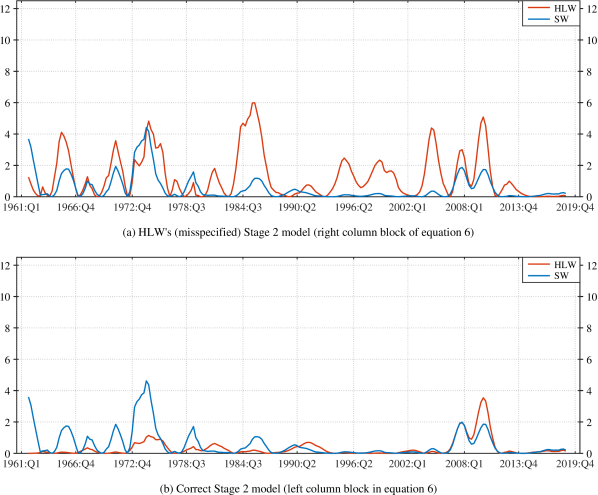

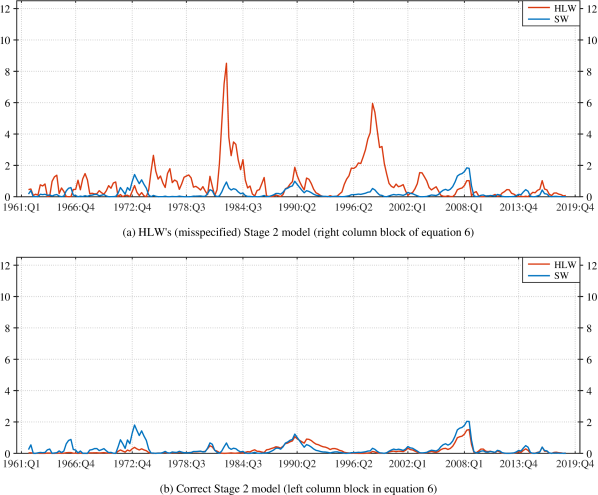

Figures 3, 6, 9 and 12 plot the sequences of statistics from the dummy variable regressions of HLW’s (misspecified) Stage 2 model (top Panel (a)) and the correct Stage 2 model (bottom Panel (b)) for both implementations of the structural break regressions denoted by HLW (red line) and SW (blue line) as defined in equations (15) to (18). These plots show that HLW’s implementation of the structural break regression leads to vastly larger sequences of statistics for the misspecified Stage 2 model shown in the top Panels (a), most notably so for the US, the Euro Area, and Canada. For the same implementations of the break tests applied to the correct Stage 2 model shown in the bottom Panels (b), the differences in the statistics are more subdued, with both implementations suggesting rather low values. Note here that the purpose of showing this comparison is to highlight the fact that it is the combination of HLW’s (misspecified) Stage 2 model and their implementation of the structural break regression in (15) that leads to the excessively large statistics.

In Tables Figures and Tables, Figures and Tables, Figures and Tables and Figures and Tables, the structural break statistics corresponding to the sequences of statistics and the resulting MUEs of are reported. The tables are arranged in two column blocks, showing the output from HLW’s implementation of the structural break regressions on the left and SW’s implementation on the right, respectively. The tables are further split into a top and a bottom part. In the top part of the tables, the estimates together with confidence intervals are reported, with the bottom part showing the respective structural break test statistics and values in parenthesis. The column headings are the same as in the tables showing the Stage 2 estimates, that is, ‘HLW.R-File’, ‘HLW()’ and ‘Correct’ (excluding the ‘Correct ’ column). The reason for reporting the results of ‘HLW()’ under HLW’s implementation of the structural break tests provided in the left column block is to highlight how different the MW, EW and QLR break statistics as well as MUEs of are from Nyblom’s (1989) test. Nyblom’s (1989) statistic is (highly) insignificant for all four countries, with values between and , resulting in MUEs of that are exactly zero.161616A value of exactly zero for is obtained whenever the structural break test statistic is smaller than the entries corresponding to in the first row of Table 3 in Stock and Watson’s (1998) look-up values, which is 0.118 for Nyblom’s (1989) test. The MW, EW and QLR tests, on the other hand, suggest (sizeable) non-zero point estimates of , although the corresponding 90% confidence intervals indicate that these are not statistically different from zero (HLW do not report confidence intervals on the MUE’s of ). Under SW’s implementation of the structural break tests (right block), the tests indicate an exactly zero point estimate of for the US when implemented on HLW’s version of the Stage 2 model (see the results under the heading ‘HLW’ in the right column block).

The parameter estimates of the full model in (1) are reported in Tables Figures and Tables, Figures and Tables, Figures and Tables and Figures and Tables. The first column under the heading (‘HLW.R-File’) lists again the estimates from HLW’s R-Files as reference values. The second column (‘MLE()’) shows estimates when conditioning on the ‘Correct’ Stage 2 MUE of (from EW’s structural break test) and estimating directly by MLE together with the other parameters of the full model in (1). In the last column (‘MLE()’), all parameters of the full model (including and ) are estimated by MLE (without using the Stage 2 model’s estimate). The following results stand out. First, as in the Stage 2 model, the MLEs of in the full model in (1) do not shrink to zero and are again larger than their MUE based counterparts (the UK estimate being the exception). For the US, they are larger; for the Euro Area, even larger. Second, the MLE and MUE based estimates of are similar when conditioning on the correct MUE of (), that is, when is computed from the correct Stage 2 model and when implementing the structural break regressions as in SW. For instance, for the US, the (non-zero) ML estimate of is , while the MUE estimate implied from the relation is . For the Euro Area, the UK and Canada, both, the MLE and MUE based point estimates of are zero.

The above results should not come as a surprise and are in line with the findings in Stock and Watson (1998). As a reminder, SW examine two different ML estimators; one estimates the initial condition of the state vector (referred to as MPLE in SW — see Section 3.2 on pages 352 to 354 in Stock and Watson (1998) for details), the second one (MMLE) does not, and uses instead a diffuse prior. SW show that these two MLEs have very different pile-up at zero frequencies (see Table 1 on page 353 in SW). In the extreme case considered in SW’s simulations where the true value of is actually 0, the MLE that does not estimate the initial condition leads to an (at most) 16 percentage point larger pile-up at zero frequency than MUE. MUE has a pile-up frequency of when is 0. When the true value is 6 (this corresponds to a which is close to the empirical estimate of for the US), the difference in pile-up frequencies drops to 9 percentage points. Now HLW do not estimate the initial condition of the state vector and use rather tightly specified priors instead.171717This is discussed in more detail in Sections 3 and 4 in Buncic (2021). Getting a non-zero MLE point estimate for the US, and exactly zero estimates for the Euro Area, the UK and Canada from both, MLE and MUE, is thus entirely consistent with SW’s simulation results.

Lastly, Kalman Filter and Smoother based estimates of the natural rate , annualized trend growth , other factor , and the output gap are shown in Figures 4, 7, 10 and 13, and in Figures 5, 8, 11 and 14, respectively. Estimates of other factor from the correct Stage 2 model implementation are substantially different to HLW’s estimates, particularly so for the US and the Euro Area, and somewhat less for the UK and Canada. For the UK and Canada, the estimates are essentially a horizontal line at 0, and are just below zero for the Euro Area. For the US, the estimate of still shows a visible downward trend over the full sample period. Nevertheless, relative to HLW’s estimate, it is more subdued, particulary since the global financial crisis. The difference in these estimates is strongest at the end of the sample in 2019:Q4. Trend growth estimates are essentially unchanged from HLW for the Euro Area, the UK, Canada, and show a small drop in trend growth following the financial crisis for the US. Due to the large impact of HLW’s Stage 2 procedure on the estimates of other factor , the natural rate is estimated to be over 100 basis points larger for the US at the end of 2019:Q4 from the correct Stage 2 model implementation. For the Euro Area, this estimate is nearly 80 basis points larger, and for the UK and Canada, circa 45 and 27 basis points. The magnitude of the natural rate is thus sizeably underestimated by HLW’s Stage 2 MUE procedure.

4 Conclusion

This paper shows that Holston et al.’s (2017) implementation of Stock and Watson’s (1998) Median Unbiased Estimation to determine the size of the signal-to-noise ratio cannot recover the ratio of interest from MUE. This inability to recover the ratio of interest is due to a misspecification in HLW’s Stage 2 model formulation. The paper shows further that the structural break regressions which are used as an auxiliary model in MUE are modified from SW’s original implementation. The misspecification in the Stage 2 model — together with the modification of the structural break regressions — leads to spuriously large estimates of the signal-to-noise ratio , which affects the severity of the downward trend in other factor , and thereby the estimates of the natural rate .

The paper provides a correction to the specification of the Stage 2 model which is consistent with the required signal-to-noise ratio , and further implements the structural break regressions following the format of SW’s original formulation to be compatible with the construction of the look-up table values provided on page 354 in Stock and Watson (1998). This correction is quantitatively important. For the Euro Area, the UK, and Canada, the (corrected) MUE point estimates of are exactly . The downward trend in the estimates of other factor disappears entirely, with the estimate resembling a horizontal line centered at (or very close to) zero. For the US, the point estimate shrinks from to , resulting in a much more subdued downward trend in other factor .

The effects of HLW’s Stage 2 MUE implementation on the estimates of the natural rate are strongest at the end of the sample period (here, in 2019:Q4); arguably when they are most needed for policy analysis. For the US, the estimate of is over basis points larger at approximately percentage points, than from HLW’s (misspecified) implementation of . For the Euro Area, is approximately basis points larger at percentage points, instead of , while for the UK and Canada, the differences are more subtle, being ( percentage points instead of ) and basis points larger ( percentage points instead of ). Estimates of trend growth — the second factor that determines the natural rate of interest — remain unchanged by the proposed correction to the Stage 2 MUE implementation.

References

- Andrews and Ploberger (1994) Andrews, Donald W. K. and Werner Ploberger (1994): “Optimal Tests when a Nuisance Parameter is Present only under the Alternative,” Econometrica, 62(6), 1383–1414.

- Benes. et al. (2010) Benes., J., K. Clinton, R. Garcia-Saltos, M. Johnson, D. Laxton, P. Manchev and Troy Matheson (2010): “Estimating Potential Output with a Multivariate Filter,” IMF Working Paper No. 10/285, International Monetary Fund. Available from: https://www.imf.org/external/pubs/ft/wp/2010/wp10285.pdf.

- Berger and Kempa (2019) Berger, Tino and Bernd Kempa (2019): “Testing for time variation in the natural rate of interest,” Journal of Applied Econometrics, 34(5), 836–842.

- Buncic (2021) Buncic, Daniel (2021): “Econometric Issues with Laubach and Williams Estimates of the Natural Rate of Interest,” Sveriges Riksbank Working Paper No. 397, Sveriges Riksbank. Available from: https://www.riksbank.se/globalassets/media/rapporter/working-papers/2019/no.-397-econometric-issues-with-laubach-and-williams-estimates-of-the-natural-rate-of-interest2.pdf.

- Buncic and Melecky (2008) Buncic, Daniel and Martin Melecky (2008): “An Estimated New Keynesian Policy Model for Australia,” The Economic Record, 84(264), 1–16.

- Chow (1960) Chow, Gregory C. (1960): “Tests of Equality between Sets of Coefficients in two Linear Regressions,” Econometrica, 28(3), 591–605.

- Clark (1987) Clark, Peter K. (1987): “The Cyclical Component of U.S. Economic Activity,” Quarterly Journal of Economics, 102(4), 797–814.

- Frühwirth-Schnatter and Wagner (2010) Frühwirth-Schnatter, Sylvia and Helga Wagner (2010): “Stochastic model specification search for Gaussian and partial non-Gaussian state space models,” Journal of Econometrics, 154(1), 85–100.

- Galí (2015) Galí, Jordi (2015): Monetary policy, inflation, and the business cycle: an introduction to the new Keynesian framework and its applications, 2nd Edition, Princeton University Press.

- Holston et al. (2017) Holston, Kathryn, Thomas Laubach and John C. Williams (2017): “Measuring the Natural Rate of Interest: International Trends and Determinants,” Journal of International Economics, 108(Supplement 1), S59–S75.

- Kiley (2020) Kiley, Michael T. (2020): “What Can the Data Tell us about the Equilibrium Real Interest Rate,” International Journal of Central Banking, 16(3), 181–209.

- Laubach and Williams (2003) Laubach, Thomas and John C. Williams (2003): “Measuring the Natural Rate of Interest,” Review of Economics and Statistics, 85(4), 1063–1070.

- Lewis and Vazquez-Grande (2018) Lewis, Kurt F. and Francisco Vazquez-Grande (2018): “Measuring the natural rate of interest: A note on transitory shocks,” Journal of Applied Econometrics, 34(3), 425–436.

- Nyblom (1989) Nyblom, Jukka (1989): “Testing for the Constancy of Parameters over Time,” Journal of the American Statistical Association, 84(405), 223–230.

- Quandt (1960) Quandt, Richard E. (1960): “Tests of the Hypothesis that a Linear Regression System obeys two Separate Regimes,” Journal of the American Statistical Association, 55(290), 324–330.

- Stock and Watson (1998) Stock, James H. and Mark W. Watson (1998): “Median Unbiased Estimation of Coefficient Variance in a Time-Varying Parameter Model,” Journal of the American Statistical Association, 93(441), 349–358.

Figures and Tables

| HLW.R-File | HLW | Correct | Correct | |

| — | ||||

| — | — | |||

| (implied) | ) | |||

| (implied) | ) | ) | ) |

Log-likelihood -534.57461094 -534.37024579 -535.95791031 -535.57316476

Notes: This table reports parameter estimates of the various Stage 2 models. The first column (‘HLW.R-File’) lists the estimates obtained from Holston et al.’s (2017) R-Files, where is fixed at the first stage estimate and is implied from the Stage 1 signal-to-noise ratio . The second column (‘HLW()’) shows estimates of the same model, but with computed by MLE together with the other parameters of HLW’s (misspecified) Stage 2 model shown in the right column block of (6). The third column (‘Correct’) provides estimates of the correct Stage 2 model defined in the left column block of (6), where is again estimated directly by MLE. The last column (‘Correct + ’) shows estimates of the correct Stage 2 model when an additional intercept term is added to the specification. Values in round brackets give the implied values of or from the relation when either or are estimated.

Corresponding structural break test statistics (values in parenthesis) — 0.037097 (0.9450) 0.170077 (0.3350) 0.049609 (0.8750) 0.037097 (0.9450) 0.170077 (0.3350) MW 2.747739 3.850795 (0.0150) 1.159557 (0.2850) 0.326527 (0.8150) 0.251819 (0.8900) 0.977255 (0.3550) EW 2.553645 3.184074 (0.0100) 0.775920 (0.2800) 0.199023 (0.7900) 0.148746 (0.8750) 0.681178 (0.3250) QLR 12.398151 13.725281 (0.0050) 6.156285 (0.1450) 2.759496 (0.5900) 2.185052 (0.7200) 5.613296 (0.1850)

Notes: This table reports the Stage 2 MUEs of and corresponding structural break statistics computed from the correct Stage 2 model and HLW’s (misspecified) Stage 2 model defined in the left and right columns of (6), respectively. The table is split into a left and right block corresponding to the two different implementations of the structural break regressions for each of the Stage 2 models defined in equations (15) to (18). The left block shows HLW’s implementation of the structural break regressions. The right block shows SW’s implementation. The table is further split into a top and bottom half. The top half shows the MUEs of . The bottom half lists the corresponding structural break test statistics. The results under (‘HLW.R-File’) report estimates obtained from Holston et al.’s (2017) R-Files for HLW’s (misspecified) Stage 2 model. The (‘HLW()’) column lists estimates of the same model but with estimated directly by MLE rather than from the first Stage . Results under the heading (‘Correct’) are for the correct Stage 2 model, where is again estimated directly by MLE. The table lists results for all four structural break tests, namely, Nyblom’s (1989) , MW, EW and QLR tests. Values in square brackets in the top part of the table are lower and upper confidence intervals (CIs). Values in parenthesis in the bottom part are values corresponding to SW’s structural break tests. Both, the CIs as well as the values, were obtained from Stock and Watson’s (1998) GAUSS files.

Log-likelihood -536.48377160 -535.97760443 -535.97718006

Notes: This table reports the Stage 3 estimates. The first column (‘HLW.R-File’) gives the estimates from Holston et al.’s (2017) R-Files. The second column (‘MLE’) shows estimates of from the correct Stage 2 model and SW’s implementation of the structural break regressions in (18) (based on the EW structural break test), where is again estimated by MLE. The last column (‘MLE’) reports estimates where all parameters, including , are computed directly by MLE. Values in round brackets give the implied or values constructed from the signal-to-noise ratios and .

Log-likelihood -422.30013304 -421.13354157 -421.17804744 -421.13660601

Notes: This table reports parameter estimates of the various Stage 2 models. The first column (‘HLW.R-File’) lists the estimates obtained from Holston et al.’s (2017) R-Files, where is fixed at the first stage estimate and is implied from the Stage 1 signal-to-noise ratio . The second column (‘HLW()’) shows estimates of the same model, but with computed by MLE together with the other parameters of HLW’s (misspecified) Stage 2 model shown in the right column block of (6). The third column (‘Correct’) provides estimates of the correct Stage 2 model defined in the left column block of (6), where is again estimated directly by MLE. The last column (‘Correct + ’) shows estimates of the correct Stage 2 model when an additional intercept term is added to the specification. Values in round brackets give the implied values of or from the relation when either or are estimated.

Corresponding structural break test statistics (values in parenthesis) — 0.067682 (0.7650) 0.068424 (0.7600) 0.097108 (0.5950) 0.067682 (0.7650) 0.068424 (0.7600) MW 1.493978 1.270378 (0.2500) 0.351069 (0.7900) 0.622436 (0.5450) 0.454903 (0.6850) 0.455205 (0.6850) EW 1.525650 1.090316 (0.1750) 0.226251 (0.7500) 0.474062 (0.4550) 0.300121 (0.6400) 0.292027 (0.6500) QLR 9.882686 8.878605 (0.0450) 2.652280 (0.6150) 4.796794 (0.2650) 3.454149 (0.4500) 3.257853 (0.4900)

Notes: This table reports the Stage 2 MUEs of and corresponding structural break statistics computed from the correct Stage 2 model and HLW’s (misspecified) Stage 2 model defined in the left and right columns of (6), respectively. The table is split into a left and right block corresponding to the two different implementations of the structural break regressions for each of the Stage 2 models defined in equations (15) to (18). The left block shows HLW’s implementation of the structural break regressions. The right block shows SW’s implementation. The table is further split into a top and bottom half. The top half shows the MUEs of . The bottom half lists the corresponding structural break test statistics. The results under (‘HLW.R-File’) report estimates obtained from Holston et al.’s (2017) R-Files for HLW’s (misspecified) Stage 2 model. The (‘HLW()’) column lists estimates of the same model but with estimated directly by MLE rather than from the first Stage . Results under the heading (‘Correct’) are for the correct Stage 2 model, where is again estimated directly by MLE. The table lists results for all four structural break tests, namely, Nyblom’s (1989) , MW, EW and QLR tests. Values in square brackets in the top part of the table are lower and upper confidence intervals (CIs). Values in parenthesis in the bottom part are values corresponding to SW’s structural break tests. Both, the CIs as well as the values, were obtained from Stock and Watson’s (1998) GAUSS files.

Log-likelihood -422.87276090 -421.23654260 -421.23654260

Notes: This table reports the Stage 3 estimates. The first column (‘HLW.R-File’) gives the estimates from Holston et al.’s (2017) R-Files. The second column (‘MLE’) shows estimates of from the correct Stage 2 model and SW’s implementation of the structural break regressions in (18) (based on the EW structural break test), where is again estimated by MLE. The last column (‘MLE’) reports estimates where all parameters, including , are computed directly by MLE. Values in round brackets give the implied or values constructed from the signal-to-noise ratios and .

Log-likelihood -877.75517435 -877.74815473 -877.76354886 -877.74887189

Notes: This table reports parameter estimates of the various Stage 2 models. The first column (‘HLW.R-File’) lists the estimates obtained from Holston et al.’s (2017) R-Files, where is fixed at the first stage estimate and is implied from the Stage 1 signal-to-noise ratio . The second column (‘HLW()’) shows estimates of the same model, but with computed by MLE together with the other parameters of HLW’s (misspecified) Stage 2 model shown in the right column block of (6). The third column (‘Correct’) provides estimates of the correct Stage 2 model defined in the left column block of (6), where is again estimated directly by MLE. The last column (‘Correct + ’) shows estimates of the correct Stage 2 model when an additional intercept term is added to the specification. Values in round brackets give the implied values of or from the relation when either or are estimated.

Corresponding structural break test statistics (values in parenthesis) — 0.080184 (0.6900) 0.081772 (0.6800) 0.079305 (0.6900) 0.080184 (0.6900) 0.081772 (0.6800) MW 1.295177 1.319085 (0.2400) 0.309463 (0.8300) 0.540538 (0.6100) 0.546107 (0.6050) 0.555764 (0.6000) EW 0.984618 1.021807 (0.1900) 0.210029 (0.7750) 0.392172 (0.5350) 0.397701 (0.5300) 0.409986 (0.5150) QLR 5.993069 6.261263 (0.1400) 3.541260 (0.4350) 4.408113 (0.3050) 4.476559 (0.2950) 4.619930 (0.2800)

Notes: This table reports the Stage 2 MUEs of and corresponding structural break statistics computed from the correct Stage 2 model and HLW’s (misspecified) Stage 2 model defined in the left and right columns of (6), respectively. The table is split into a left and right block corresponding to the two different implementations of the structural break regressions for each of the Stage 2 models defined in equations (15) to (18). The left block shows HLW’s implementation of the structural break regressions. The right block shows SW’s implementation. The table is further split into a top and bottom half. The top half shows the MUEs of . The bottom half lists the corresponding structural break test statistics. The results under (‘HLW.R-File’) report estimates obtained from Holston et al.’s (2017) R-Files for HLW’s (misspecified) Stage 2 model. The (‘HLW()’) column lists estimates of the same model but with estimated directly by MLE rather than from the first Stage . Results under the heading (‘Correct’) are for the correct Stage 2 model, where is again estimated directly by MLE. The table lists results for all four structural break tests, namely, Nyblom’s (1989) , MW, EW and QLR tests. Values in square brackets in the top part of the table are lower and upper confidence intervals (CIs). Values in parenthesis in the bottom part are values corresponding to SW’s structural break tests. Both, the CIs as well as the values, were obtained from Stock and Watson’s (1998) GAUSS files.

Log-likelihood -877.97896968 -877.77522874 -877.77522874

Notes: This table reports the Stage 3 estimates. The first column (‘HLW.R-File’) gives the estimates from Holston et al.’s (2017) R-Files. The second column (‘MLE’) shows estimates of from the correct Stage 2 model and SW’s implementation of the structural break regressions in (18) (based on the EW structural break test), where is again estimated by MLE. The last column (‘MLE’) reports estimates where all parameters, including , are computed directly by MLE. Values in round brackets give the implied or values constructed from the signal-to-noise ratios and .

Log-likelihood -679.90156186 -679.87545118 -679.94373632 -679.94347472

Notes: This table reports parameter estimates of the various Stage 2 models. The first column (‘HLW.R-File’) lists the estimates obtained from Holston et al.’s (2017) R-Files, where is fixed at the first stage estimate and is implied from the Stage 1 signal-to-noise ratio . The second column (‘HLW()’) shows estimates of the same model, but with computed by MLE together with the other parameters of HLW’s (misspecified) Stage 2 model shown in the right column block of (6). The third column (‘Correct’) provides estimates of the correct Stage 2 model defined in the left column block of (6), where is again estimated directly by MLE. The last column (‘Correct + ’) shows estimates of the correct Stage 2 model when an additional intercept term is added to the specification. Values in round brackets give the implied values of or from the relation when either or are estimated.

Corresponding structural break test statistics (values in parenthesis) — 0.037529 (0.9450) 0.048128 (0.8850) 0.038851 (0.9350) 0.037529 (0.9450) 0.048128 (0.8850) MW 0.833493 0.824762 (0.4200) 0.182530 (0.9550) 0.221949 (0.9200) 0.214878 (0.9250) 0.278728 (0.8650) EW 0.801254 0.761333 (0.2900) 0.101482 (0.9500) 0.126872 (0.9100) 0.122280 (0.9200) 0.161823 (0.8550) QLR 8.513039 8.272703 (0.0550) 1.514397 (0.8850) 1.842522 (0.8050) 1.793354 (0.8200) 2.040637 (0.7600)

Notes: This table reports the Stage 2 MUEs of and corresponding structural break statistics computed from the correct Stage 2 model and HLW’s (misspecified) Stage 2 model defined in the left and right columns of (6), respectively. The table is split into a left and right block corresponding to the two different implementations of the structural break regressions for each of the Stage 2 models defined in equations (15) to (18). The left block shows HLW’s implementation of the structural break regressions. The right block shows SW’s implementation. The table is further split into a top and bottom half. The top half shows the MUEs of . The bottom half lists the corresponding structural break test statistics. The results under (‘HLW.R-File’) report estimates obtained from Holston et al.’s (2017) R-Files for HLW’s (misspecified) Stage 2 model. The (‘HLW()’) column lists estimates of the same model but with estimated directly by MLE rather than from the first Stage . Results under the heading (‘Correct’) are for the correct Stage 2 model, where is again estimated directly by MLE. The table lists results for all four structural break tests, namely, Nyblom’s (1989) , MW, EW and QLR tests. Values in square brackets in the top part of the table are lower and upper confidence intervals (CIs). Values in parenthesis in the bottom part are values corresponding to SW’s structural break tests. Both, the CIs as well as the values, were obtained from Stock and Watson’s (1998) GAUSS files.

Log-likelihood -680.25212417 -680.00345718 -680.00345718

Notes: This table reports the Stage 3 estimates. The first column (‘HLW.R-File’) gives the estimates from Holston et al.’s (2017) R-Files. The second column (‘MLE’) shows estimates of from the correct Stage 2 model and SW’s implementation of the structural break regressions in (18) (based on the EW structural break test), where is again estimated by MLE. The last column (‘MLE’) reports estimates where all parameters, including , are computed directly by MLE. Values in round brackets give the implied or values constructed from the signal-to-noise ratios and .