secReferences in the Online Appendix

The Shared Cost of Pursuing

Shareholder Value††thanks: We thank Pat Akey, Ghazala Azmat, Heski Bar-Isaac, Giorgia Barboni, Roland Bénabou, Claire Célerier, Clément de Chaisemartin, Vicente Cuñat, Alex Edmans, Thierry Foucault, Nickolay Gantchev, Juanita Gonzalez-Uribe, Stéphane Guibaud, Luigi Guiso, Sergei Guriev, Junnan He, Emeric Henry, Yael Hochberg, Panagiotis Koutroumpis, Nicolas Inostroza, Jean-Stéphane Mésonnier, Salvatore Nunnari, Fausto Panunzi, Naciye Sekerci, David Sraer, Jorge Tamayo, David Thesmar, Jie Yang, Noam Yuchtman, and Riccardo Zago for helpful discussions and comments, and participants at seminars and conferences taking place at Bocconi, Deakin University, Erasmus University, Florida Atlantic University, Sciences Po, Singapore Management, University, St. Gallen, and Toronto. We are grateful to Jeffrey Sonnenfeld and his team at Yale – including Joseph Delillo, Emily Gordon, Steven Tian, and Nathan Williams – for responding to our requests for clarifications regarding the database they collected on corporate sanctions against Russia. Mohammad Atif Haidry, Runpei He, Yujia Huang, Takayoshi Tokai, and Yuxuan Xu provided excellent research assistance. Fioretti and Saint-Jean thank the Einaudi Institute for Economics and Finance and the University of Toronto (Rotman) for their hospitality during their respective visits. This study received funding from a Sciences Po-McCourt Institute grant. The views expressed in this paper are those of the authors and do not necessarily reflect the views and policies of the Board of Governors or the Federal Reserve System. All errors and omissions are ours.

Abstract

We propose a portable framework to infer shareholders’ preferences and influences on firms’ prosocial decisions and the costs these decisions impose on firms and shareholders. Using quasi-experimental variations from the media coverage of firms’ annual general meetings, we find that shareholders support costly prosocial decisions, such as covid-related donations and private sanctions on Russia, if they can earn image gains from them. In contrast, shareholders that the public cannot readily associate with specific firms, like financial corporations with large portfolios, oppose them. These prosocial expenditures crowd out investments at exposed firms, reducing productivity and earnings by between 1 and 3%: pursuing the values of some shareholders comes at the cost of others, which the shareholders’ monitoring motivated by heterogeneous preferences could prevent.

JEL classifications: G32, G41, M14

Keywords: shareholder value, wealth, conflict, warm glow, reputation, exit and voice, social responsibility, charitable donations, covid, Ukraine, Russia

“[…] it is the job of the manager of a firm […] not only to […] organize production, but also to learn about the preferences of the firm’s shareholders.”

Grossman and Hart (1979)

1 Introduction

Shareholder disagreements are common but often unobserved. As shareholders try to influence managers, policies have been implemented to inform shareholders (e.g., Desai et al., 2007) and resolve conflicts by allowing them to make proposals and vote at the Annual General Meetings (AGMs) of shareholders (e.g., DeMarzo, 1993; Bouton et al., 2022). However, some shareholders can also influence managers through private channels, reducing the ability of non-connected shareholders to access managers and limiting managerial knowledge regarding shareholder preferences over firms’ decisions.

Social responsibility adds another dimension to shareholder conflicts because shareholders may disagree not only on the profitability of firms’ actions, but also on their social implications (Landier et al., 2009; Fioretti, 2022). Consider Ford Motor’s decision to convert some of its car production facilities to produce and donate medical ventilators to hospitals during the pandemic when ventilators, essential to treating patients with COVID-19, were in shortage. Due to its costs, shareholders might hold different views about the firm’s decision. Those who derive “value” from covid relief may have supported it despite smaller financial returns as their cash donations could not help hospitals procure ventilators (Hart and Zingales, 2017). Shareholders easily associated with Ford Motor could benefit further from the media coverage of the firm’s generosity, as is the case of Bill Ford, a member of the Ford family who, when interviewed by CBS, endorsed the donation of ventilators.111“[…] When we look at this crisis– as a country and said, you know, which industry is positioned to help us not only in terms of sophisticated machinery, but can do a lotta them and a lotta them quickly, the auto industry is uniquely positioned to do that” (O’Donnell, 2020). This example is illustrative as ventilator productions were economically supported by the Defense Production Act (i.e., government contracts), while this paper focuses only on voluntary donations. On the other hand, for shareholders such as US households who do not benefit from similar private returns, donations resemble taxes (Friedman, 1970). These differences in preferences raise questions about the consequences of pursuing the values of some shareholders at the cost of others.

Our main contribution is to empirically investigate the shared costs of shareholders’ influence by drawing a causal link between their preferences and the prosocial decisions of large global corporations. To overcome the main issue that we face, namely that shareholder influence is not observable, we focus on settings where a sudden emergency puts firms in an advantageous position to procure society with needed goods and services compared to what shareholders can achieve through cash donations. Exploiting the exogenous occurrence of AGMs as a shock to corporate news coverage, we find that the shareholders most likely to gain image returns from their firm’s prosocial decisions demand positive changes. In contrast, shareholders with limited opportunities to extract private gains see these demands as externalities and oppose them because the associated costs can reduce a firm’s profits and growth prospects. As a result, market capitalization and operating income drop by about one to three percentage points more at the firms most exposed to these externalities, resulting in adverse outcomes for “silent” and “unheard” shareholders. These losses come from inefficient expenses cutting current funds that would otherwise have been invested, describing a feedback loop curtailing future productivity.

Motivated by a stylized theoretical model of a contest where shareholders with different preferences about a corporate prosocial action compete to influence managers (e.g., Konrad et al., 2009), we expect that, net of prosocial inclinations, shareholders with significant shares in the firm and no private returns from its prosocial decision oppose the action if it reduces the firm’s profits. On the contrary, shareholders who can gain private returns from the prosocial action will support it if these returns exceed their losses. Also inspired by the common ownership literature (e.g., Azar et al., 2018; Backus et al., 2021), we identify the former shareholders in institutional investors – financial intermediaries such as mutual funds and banks – whom the public hardly connects with a specific firm as they own shares across many firms, and the latter shareholders in individual and family shareholders, who are synonymous with a firm.222We present robustness checks using more sophisticated association measures between a firm and its shareholders, taking advantage of the Google search data for firms and shareholders. Importantly, some of these shareholders can be past or current managers without affecting our results, as discussed below.

Our empirical framework relies on a sudden emergency where the public demands firms to take costly prosocial actions and on the exogenous variation of AGM timing across firms, which we show to heighten a firm’s media coverage, thereby increasing the media attention of its most recognizable shareholders.333We verify empirically that a firm’s media coverage increases during its AGM period (Appendix C). The International Shareholder Services (ISS), a global leader in proxy voting services, requires firms to allow 90 days between the date when shareholders receive materials about the AGM proposals and the AGM. Consider the recent pandemic as a similar emergency. The first reported US covid case occurred on January 15, 2020 (Holshue et al., 2020): since the firms with AGMs planned for the following 90 days could not move their dates by law (SEA, 1934), the increased media attention due to the AGM period is independent of the preferences of shareholders and managers toward the donations, the composition of the shareholding body and their access to managers, and the financial and operational status of a firm. These features make our approach portable across crises (or even countries) and times.

Therefore, we estimate the impact of shareholder preferences on corporate decisions as the difference in the donation rates observed by April 15, 2020, across four groups of firms: (i) the difference across treated firms (i.e., with an AGM before 90 days from the beginning of the crisis) with and without large individual (or institutional) shareholders and (ii) the same difference across control firms (i.e., with no plans for an AGM in this period). Since firms donated covid-relief cash and goods like facemasks, sanitizing gels, and software, we focus on explaining why firms donated rather than the value of the donations. At S&P 500 firms, cash donations averaged 1% of EBIT alone, a substantial cost for a firm’s shareholders but great publicity for the most visible ones.

We find that by April 15, treated S&P 500 firms are 9% more likely to donate to covid-relief if their shareholding body includes large individual shareholders before the pandemic compared to the average S&P 500 firm. In contrast, treated firms with large institutional shareholders are 15% less likely to donate compared to the average S&P 500 firm. Consumer demand for covid-related donations, managerial will, peer pressure from donating competitors, and financial returns do not explain our findings.

We validate the image-gain mechanism showing an instantaneous and sustained gap in the Google searches of the names of a firm’s individual shareholders compared to those of its institutional shareholders around the donation news date; this gap widens by about 40% in each of the ten days following a donation. Nonetheless, institutional shareholders are not necessarily against covid-related donations: several S&P 500 financial firms donated directly, but their donations negatively correlate with those of the S&P 500 firms in their portfolios. Thus, shareholders support donations only if their influence yields direct private benefits, creating an externality on other shareholders. These returns can be micro-founded as warm glow utilities (e.g., Andreoni, 1989) or reputational gains from virtue signaling (e.g., Bar-Isaac et al., 2008).

We demonstrate the portability of our framework in two ways. First, we study another focal event of the last decade, namely the decision of US multinationals to forgo their Russian investments or interrupt relationships with their Russian suppliers at the onset of the Ukrainian invasion in 2022. In this respect, we do not claim that exiting Russia was the welfare-enhancing choice, but rather that early exits could, on the one hand, receive greater media attention and, on the other, be particularly expensive for shareholders if they were not adequately planned. Our results regarding the directions of influence are consistent, with large institutional shareholders opposing exit decisions and individual shareholders supporting cutting ties with Russia. Second, we extend the scope of our influence mechanism by investigating firms’ ESG news coverage and donations over the last decade. Consistent with our previous findings, large individual shareholding is associated with fewer prosocial incidents and more donations in the AGM month, validating our usage of AGMs for identification.

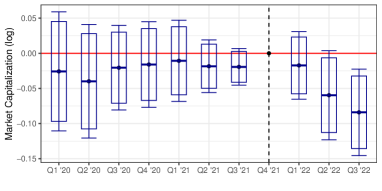

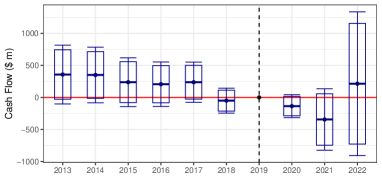

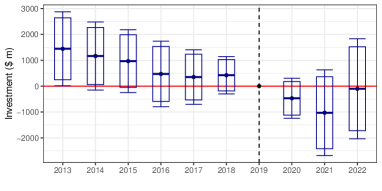

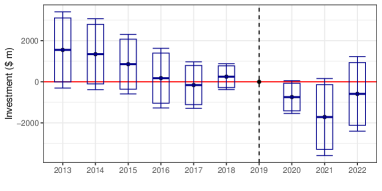

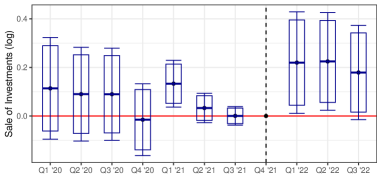

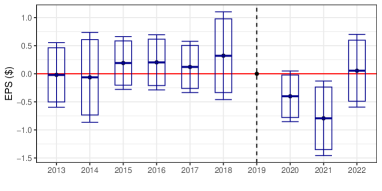

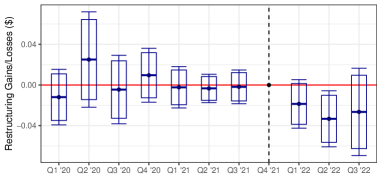

By providing goods unavailable in the markets, like sanitizing gels to hospitals or pressuring a villain state by terminating business dealings, firms had an advantage over shareholders in creating social value. As large individual shareholders benefited from these firms’ responses, pursuing their values implied high costs for the others. Using operating income and market capitalization as measures of these costs, we find that these variables dropped at the most exposed firms by between one and three percentage points. In both cases, these drops are due to increased operating costs, as revenues stayed constant across treated and control firms. Indeed, in the covid case, we find that investment dropped by about 6% in 2020 and 2021 at the most exposed firms, leading to reduced productivity that compiled over time, costing shareholders about 3% of the average earnings-per-share (EPS) in the pre-period.444The EPS loss in 2020-21 is over 8% per standard deviation of a firm’s share of individual shareholders among its shareholders with at least a 5% stake (ATE). Among the firms with large individual shareholders, an AGM at the onset of the pandemic decreased EPS by 21% (ATT), suggesting sizable costs for unheard shareholders. On the other hand, shareholders’ influence on the Russian-Ukraine crisis led treated firms to rush out of Russia, with the most exposed firms reneging 20% more investments than control firms. As a result, unheard shareholders suffered: restructuring costs in 2022 eroded 5% of the EPS at the most exposed firms. In conclusion, pursuing the values of a few shareholders costs the others both today and in the future (e.g., Bartlett and Bubb, 2023; Edmans, 2023).

Causally connecting shareholder values with the costs that its pursuit implies on other shareholders is the main novelty of this paper. These findings add to a notable literature examining firms’ objectives, which flourished in the 80s when most, if not all, firms claimed to maximize profits (e.g., Grossman and Hart, 1979; Hart, 1995) and that received renewed attention due to the recent transition toward a more sustainable economy and corporate purpose (Edmans, 2021; Rajan et al., 2022). We show that horizontal conflicts (e.g., Ashraf and Bandiera, 2018) across shareholders with misaligned preferences modulate firms’ objectives and can impact crucial strategic moves such as breaking ties with partners in a villain state. However, that shareholders (and managers) can extract private rents is not new (Shleifer and Vishny, 1997). The standard solutions are either legal protection of minority rights (La Porta et al., 2002) or the monitoring of large investors (Shleifer and Vishny, 1986; Burkart et al., 1997; Edmans, 2009). Our findings revise the latter point: minority rights are better defended at firms with several large shareholders with heterogeneous preferences than at firms with concentrated ownership around shareholders with similar preferences.

Previous works on firms’ objectives either model optimal firm’s behavior (Fioretti, 2022), exploit experimental evidence (List and Mason, 2011; Duffy et al., 2022; Hart et al., 2022), or are mainly theoretical (Bénabou and Tirole, 2006; Fleurbaey and Ponthière, 2023; Bonneton, 2023): a crucial innovation of this paper is its portable empirical framework, which allows the inference of shareholder preferences from the decisions of large corporations. Without it, we would be left to believe that shareholders did not care for covid interventions since none of the AGM proposals in 2020 at the firms in our sample discussed them. AGM proposals are indeed the standard data for studying questions related to shareholder democracy (e.g., Cuñat et al., 2012; Gantchev and Giannetti, 2021), as they come with detailed information on votes. Although a limit of our approach is that it cannot tell whether managers reacted to shareholders’ influence or their expectations, most of the influence is often exercised outside of AGM votes (Gantchev, 2013), making our framework a unique way to study unobserved influence systematically.

This paper also contributes to several recent investigations of shareholder influence through either “exit” and “voice” decisions (Hirschman, 1970; Broccardo et al., 2022; Oehmke and Opp, 2020). The empirical evidence favors voice on sustainability matters as impacting stock prices through stock sales is particularly hard and costly for investors at liquid firms like the large multinationals we survey in our paper (Berk and van Binsbergen, 2021; Saint-Jean, 2023).555Voice and exit are also studied in relation to stocks’ liquidity (Edmans et al., 2013), shareholders’ approval of key managerial decisions such as mergers (Gillan and Starks, 1998; Admati and Pfleiderer, 2009), and interactions between consumers and firms (Gans et al., 2021; Ananthakrishnan et al., 2023). A large body of literature praises the importance of institutional investors in driving the recent surge in socially responsible investment (e.g., Hartzmark and Sussman, 2019; Chen et al., 2020; Naaraayanan et al., 2021; Yegen, 2020). Our results do not conflict with these works, as factors other than image motives might be at play in other empirical settings.

Our application relates to a broader literature investigating the determinants of corporate donations (e.g., Bénabou and Tirole, 2006; List, 2011; Bonnefon et al., 2022). Related to our results, recent work by Bertrand et al. (2023) finds that, after a merger, the target firm is more likely to lobby the same politicians receiving donations from the acquiring firms (see also Bertrand et al., 2020; Cagé et al., 2021; Colonnelli et al., 2023). In the context of corporate philanthropy, giving is commonly seen as either an efficient advertising tool for profit maximization through increased consumer demand and reduced consumer price sensitivity (e.g., Navarro, 1988; Brown et al., 2006; Elfenbein et al., 2012) or worker productivity (e.g., Tonin and Vlassopoulos, 2015; Gosnell et al., 2020; List and Momeni, 2021), as insurance against reputational risks (Godfrey et al., 2009), as a way to repair sudden reputational issues (Akey et al., 2021), or as an agency problem within the firms, where managers and insiders extract private benefits to the detriment of shareholders (Jensen and Meckling, 1976; Cheng et al., 2013). Our paper reverses this agency problem by identifying the incentives different shareholders respond to and the distributional consequences of their influence.

The remainder of our paper is organized as follows. Sections 2 and 3 introduce the conceptual and empirical frameworks, respectively. Section 4 presents the main results of shareholder influence using the recent pandemic as our main testbed but also discusses its external validity using the Russia-Ukraine war and the reporting of ESG incidents and donations over the last decade. Section 5 illustrates the distributional cost of pursuing shareholder value and discusses our main contributions. Section 6 summarises our findings and concludes.

2 Conceptual Framework

A firm considers a prosocial action. The action is costly, and adopting it will decrease the firm’s profits, thereby lowering the dividends paid to each of its shareholders by . The action is also visible, and one of its two shareholders, shareholder , will enjoy image gains of due to her connection with the firm. In contrast, shareholder receives no extra benefits as the public does not associate with the firm (). Each shareholder can pressure the firm’s manager to take his or her favorite action, thereby exerting an externality on the other shareholder. The probability that shareholders’ influences result in the adoption of the prosocial action is:

| (1) |

which is increasing in the influence effort of shareholder , , and decreasing in that of shareholder , . The cost of effort to shareholder , , is convex in ’s effort level, with . The utility to shareholder is , so that ’s optimal effort sets marginal benefit equal to marginal cost, according to:

Therefore, will exert effort only if : given the expected loss , we expect shareholders to exert pressure only if they are easily associated with a firm (high ). In addition, an exogenous increase in will raise ’s equilibrium effort. As a result, in the case of strategic complementarities – namely, – shareholder will update his effort level to reduce the probability of a donation.666Strategic complementarities are rather natural in this setting and arise with simple probability distributions like (with ) or the logistic probability. Therefore, the two agents compete on influences and will set the optimal level of effort to offset each other given the dividend loss and their private returns and costs of exerting effort.

This model extends easily to a setting with shareholders where shareholder is either of type or and owns shares, with . In this case, the utility of shareholder of type becomes , where we denote the sum of the efforts of all individuals of type by . The problem yields similar first-order conditions to the problem with only two shareholders, with a caveat: under strategic complementarities, shareholders with large shares () will have the most to lose when shareholders exert more effort as exogenously increases, leading large shareholders to intensify their effort more than minority ones. Furthermore, if the public is less likely to associate minority shareholders of type with the firm, we will expect large type- shareholders to update their effort levels more than minority shareholders of the same type.

In the real world, shareholders have different effort cost functions for influence and can form different dividend expectations. Imagine that an exogenous treatment increases at some firms but not others: we expect prosocial action to be more likely at treated firms with high shares of type shareholders owning large shares (blockholders). Similarly, prosocial actions should be less likely at treated firms with larger shares of type blockholders. In what follows, we infer the externality arising from shareholder influence on observed prosocial actions through the framework displayed in Equation (1). To do this, we exploit (i) the AGM timing as an exogenous shock to some shareholders’ image gains () due to increased public scrutiny of their firm and (ii) differences in the public awareness of individual and institutional investors (i.e., financial intermediaries) to categorize shareholders of type and , respectively.

3 A Quasi-Experiment Through Crises and AGMs

Investigating the nexus between shareholder conflicts and corporate prosocial decisions requires measuring the efforts of different shareholders and observing the prosocial actions taken by the firm, as described in (1). Two issues arise. First, environmental, social, and governance (ESG) indices – standard measures of prosociality – are not an adequate dependent variable in (1) because they do not provide shareholders with image returns as they do not refer to specific and visible prosocial firms’ decisions for which a shareholder might have fought for. Second, we do not observe shareholders’ effort levels and in (1). Hence, two items are jointly required: (i) a dataset of visible prosocial actions and (ii) a device shocking only the utility of connected shareholders for some firms (i.e., in Section 2).

Crises and Annual General Meetings (AGMs) provide these two items. Widespread crises often lead the public to demand that firms take visible and costly actions. For instance, during the recent pandemic, firms contributed to the relief by donating cash and in-kind through their know-how (e.g., sanitizing gels from chemical firms or specialized software from IT firms). Similarly, the private sanctions on Russia after its recent invasion of Ukraine started even before governmental sanctions. Thus, crises fit our purposes because they provide data about visible actions firms have taken, producing item (i) above, and because they are orthogonal to firm characteristics. However, crises “shock” all shareholders at exposed firms. To get exogenous variation across shareholders, delivering item (ii) above, we take advantage of listed firms’ reporting cycles and exploit the occurrence of an AGM as a shock to the media coverage of a firm and its most connected shareholders during crises ( from Section 2).

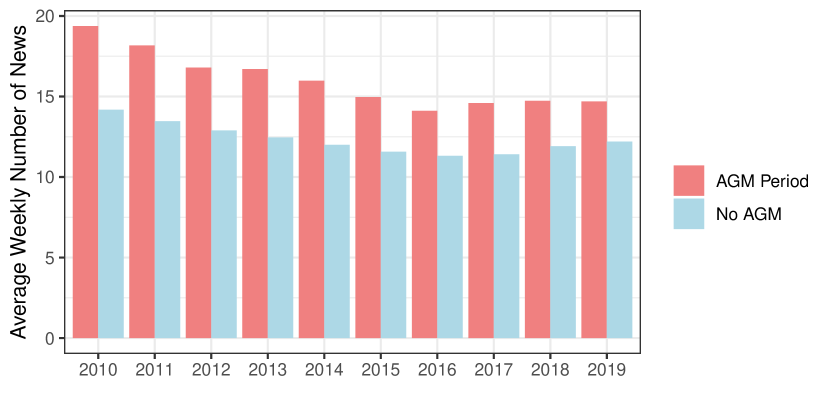

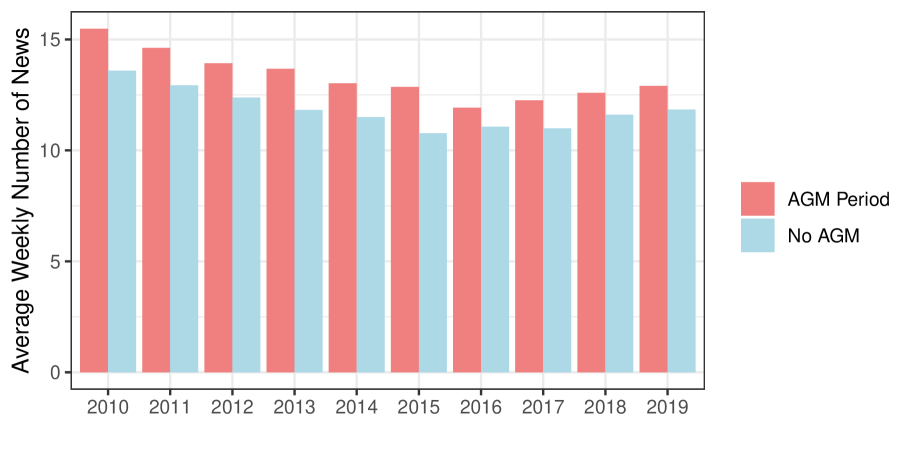

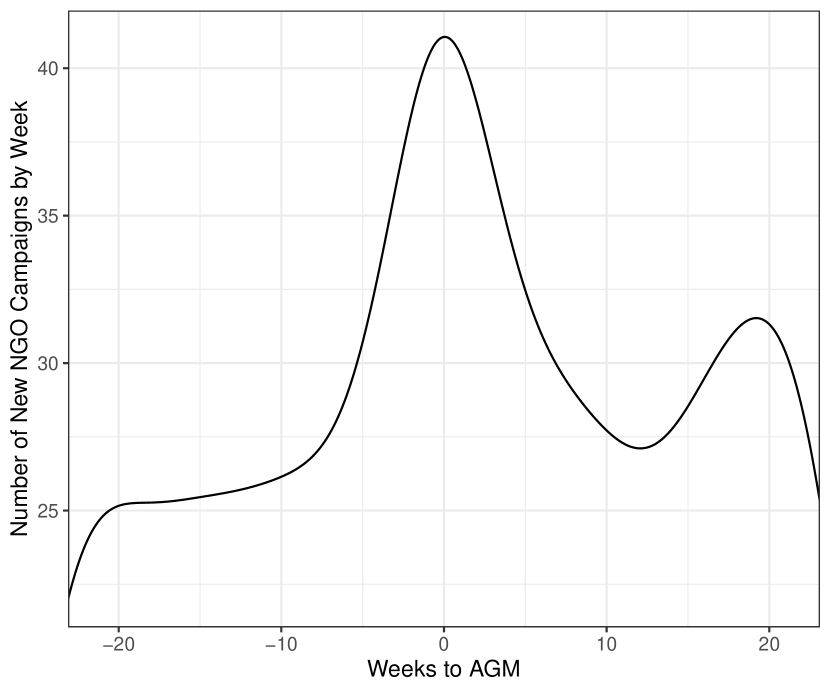

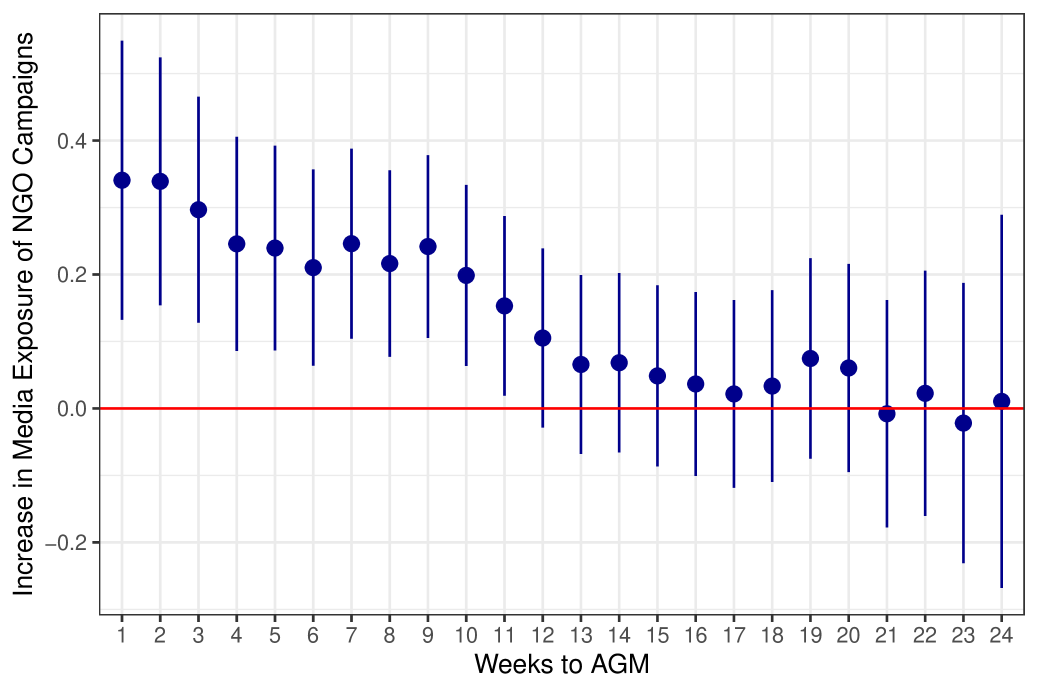

AGMs and media coverage. Appendix C provides evidence supporting the claim that AGMs bring greater media coverage by considering NGO attacks on a firm, which, as the firm itself cannot start them, are empirically easier to deal with than corporate donations that can be timed to raise a firm’s coverage. We summarize our main findings in this paragraph. First, using data for 2010-2019, Appendix Figure C2 shows that media coverage increases during an AGM period. Second, Figure C4 finds that NGOs are far more likely to start a campaign against a firm in the six weeks around the firm’s AGM date.777The NGO campaign data come from the Sigwatch database (Hatte and Koenig, 2020), which we describe in Appendix C. Third, taking the timing of NGO attacks as exogenous, Appendix Figure C4 finds that an AGM period increases news reporting of firms affected by NGO attacks up to 12 weeks away, or 90 days, from an AGM, suggesting that AGM periods trigger greater media attention, which, in turn, can impact the visibility of a firm’s shareholders.888As an illustrative example, Appendix Figure B2 reports a few media pieces featuring prominent shareholders in articles discussing the outcomes of AGM votes.

Condition for treatment. The AGM timing is exogenous to current events as its date is stable across years. A firm’s AGM is the annual gathering of its shareholders; at this meeting, managers present their annual report about the firm’s performance, and shareholders vote on previously submitted proposals. If shareholders satisfy certain criteria (see Rule 14a-8 SEA, 1934), they can submit proposals to managers at least 120 days before the release of the proxy statement based on the previous year’s AGM (Glac, 2014). Therefore, AGM dates are effectively fixed within firms over time, as shown in Panel (b) of Appendix Figure B1, which finds little variation in the AGM month for S&P 500 firms across adjacent years in 2012-2019.

Given that AGM dates hardly change over time, we consider those firms whose AGM period overlaps with the beginning of a crisis as treated. To define an AGM period, we follow the requirements of the Institutional Shareholder Service, the leading firm for proxy voting services to shareholders, which recommends no more than 90 days between the notification of the AGM proposals to shareholders and the AGM date. Therefore, since the first covid case in the US was detected on January 15, 2020 (Holshue et al., 2020), we consider as treated the firms that had an AGM in the first 90 days from January 15, and as control the remaining S&P 500 firms. Analogously, we consider as treated the firms with AGMs set within 90 days from the start of the Russian invasion of Ukraine on February 24, 2022.

Shareholder types. According to our conceptual framework (Section 2), the AGM treatment increases the private return of the shareholders that are easily associated with the firm (type shareholders), increasing their willingness to exert effort to influence managers to behave prosocially, but it also raises the opposition of the other shareholders (type ).999Other shareholder types include self-ownership, foundations, and national governments or agencies. The final outcome depends on the differential influence exerted by the various shareholders. Hence, our empirical approach needs an additional lever as the AGM treatment disregards the composition of the shareholding body.

In our empirical analysis, we label individual and family shareholders as shareholders and financial shareholders like mutual funds as shareholders . We view this distinction as the most objective way to separate shareholders based on whether the public easily links them to a firm: famous individuals, founders, and previous CEOs are included in the category, while financial shareholders like BlackRock and Vanguard invest in most S&P 500 firms (Backus et al., 2021), which detaches them from specific firms in the eyes of the public.101010We present robustness checks using more sophisticated measures of association such as Google search data of a firm and its shareholders in Section 4.3.1.

Importantly, including individuals with easy access to a firm’s managers like founders (e.g., Bill Gates) in category but not in category is inconsequential for our results because we infer the voice channel as the difference between the gap in the adoption rate of prosocial decisions between firms undergoing an AGM period with and without shareholders of type (or ) and the analogous gap among control firms (with no AGM). The first difference highlights the impacts of the AGM on the effort exerted by shareholders of type (or ), while the second difference controls for the effort of shareholders of type (or ) after the crisis (i.e., their intrinsic motivation). All idiosyncratic differences across firms, such as the cost of influence or preferences of specific shareholders, vanish by focusing on the difference among these changes at AGM-treated and at control firms as long as the crisis event we focus on and the AGM timing are unrelated to shareholders and firm characteristics. This assumption is credible in our setting, as the AGM dates were fixed before the crisis.

Empirical approach. Abstracting from the time dimension for simplicity, we exploit the AGM timing and the ownership structure as outlined in the previous section by translating the contest game described in (1) into:

| (2) |

The dependent variable, , features the prosocial decision taken by firm in the 90 days since the beginning of the crisis (e.g., whether it donates for covid). On the right-hand side, Ownershipf is some specific characteristics of the shareholding body of firm before the crisis, and AGMf is a dummy for whether the firm planned an AGM in the 90 days after the beginning of the crisis. To illustrate the approach, assume that Ownershipf is one for firms that have individual shareholders and zero otherwise. In this case, , the main coefficient of interest captures the difference in donation rates at AGM-treated firms with and without individual shareholders rebased by the same difference at firms without an AGM: a positive (negative) coefficient suggests that individual shareholders supported (opposed) donations. The next section extends this approach, accounting for fixed effects and the time dimension.

To study the distributional consequences of shareholder influence on other shareholders, Section 5 focuses on productivity measures and earnings per share within an intention-to-treat approach. In particular, we translate (2) into a difference-in-differences where the beginning of a crisis determines the post-period and the AGMf and Ownershipf variables determine the inclusion in the treatment. We will carefully examine the pre-trends and evaluate our results using event studies.

4 Shareholders’ Voice

Our primary focus in this section is shareholder influence at the onset of the recent covid pandemic. The first four sections present the data (Section 4.1), the estimation results (Section 4.2), and the mechanism (Sections 4.3 and 4.4). We then discuss the external validity of the voice channel that we uncover using another emergency event (the recent Russia-Ukraine conflict) and an extended period without crises in Section 4.5. Section 4.6 summarises our main findings.

4.1 Data and Balance Checks

We build a dataset on US-based S&P 500 firms collecting information from various sources. Table 1 categorizes information in different panels based on their contents. The top panel reports firms’ financial and operative characteristics, which we draw from Refinitiv, Orbis, and Compustat. The second panel considers covid exposure at a firm’s headquarters-state from Johns Hopkins University (Dong et al., 2020). The third panel focuses on the composition of a firm’s shareholding body, zooming in on the shares of individual and institutional shareholders, such as banks, mutual funds, and insurance firms. We only observe shareholders owning at least 0.1% of a firm’s equity. This panel pays particular attention to large shareholders. The fourth panel focuses on prosocial characteristics such as Refinitiv’s ESG scores and the donation data we hand-coded by sourcing news media outlets, internet searches, and company reports and websites. The last panel states that the condition for treatment is to hold the 2020 AGM before April 15, 2020. AGM dates come from the SEC’s N-PX form. Excluding non-US-headquartered S&P 500 firms leaves us with 433 firms. The financial and operational variables are as of December 2019.

| Quantiles | Average | |||||||

| 25% | 50% | 75% | Overall | Treated | Control | Diff. | p-value | |

| (1) | (2) | (3) | (4) | (5) | (6) | (5)-(6) | (8) | |

| i. Firm characteristics | ||||||||

| Revenues (bn $) | 5.16 | 10.32 | 22.44 | 27.00 | 26.84 | 28.42 | -1.60 | 0.82 |

| Share of revenues from the US (%) | 15.00 | 19.63 | 25.42 | 20.03 | 19.99 | 20.42 | -0.40 | 0.82 |

| EBIT to revenue | 0.09 | 0.16 | 0.23 | 0.16 | 0.16 | 0.13 | 0.00 | 0.14 |

| Earnings per share, EPS ($) | 2.07 | 3.91 | 6.19 | 4.78 | 4.83 | 4.41 | 0.40 | 0.44 |

| Workforce (headcount, thousands) | 8.55 | 18.80 | 55.30 | 54.00 | 53.39 | 59.81 | -6.40 | 0.63 |

| Number of branches | 9.00 | 40.00 | 171.00 | 310.52 | 310.19 | 313.42 | -3.20 | 0.98 |

| Total debt (bn $) | 3.40 | 7.18 | 16.51 | 16.02 | 16.53 | 11.78 | 4.80 | 0.13 |

| Interest expenses (m $) | 28.00 | 59.83 | 142.00 | 121.20 | 125.25 | 88.62 | 36.60 | 0.08 |

| Market capitalization (bn $) | 13.22 | 23.85 | 50.52 | 60.05 | 57.77 | 80.12 | -22.40 | 0.42 |

| Brokers’ recommendations [-2,2] | 0.32 | 0.62 | 0.87 | 0.58 | 0.58 | 0.61 | -0.00 | 0.72 |

| ii. Covid exposure | ||||||||

| Covid cases at HQ state (thousands) | 15.85 | 28.89 | 52.92 | 69.52 | 71.79 | 49.58 | 22.20 | 0.04 |

| Covid deaths at HQ state (thousands) | 0.78 | 1.27 | 2.45 | 4.70 | 4.91 | 2.85 | 2.10 | 0.02 |

| iii. Shareholding composition | ||||||||

| Individual ownership (%) | 0.00 | 0.00 | 0.09 | 1.38 | 1.37 | 1.47 | -0.10 | 0.93 |

| Institutional ownership (%) | 40.52 | 46.89 | 52.78 | 46.47 | 47.08 | 41.13 | 5.90 | 0.01 |

| - Banks (%) | 29.18 | 33.58 | 38.92 | 33.69 | 34.20 | 29.37 | 4.80 | 0.01 |

| - Mutual Funds (%) | 4.61 | 6.64 | 9.92 | 7.98 | 8.00 | 7.80 | 0.20 | 0.74 |

| - Insurance Companies (%) | 2.59 | 3.65 | 5.46 | 4.66 | 4.76 | 3.81 | 0.90 | 0.02 |

| Shares owned by individuals with 5% (%) | 0.00 | 0.00 | 0.00 | 2.31 | 2.34 | 2.12 | 0.20 | 0.90 |

| - excluding firms w/out indiv. with 5% (%) | 32.86 | 62.77 | 81.88 | 59.95 | 60.36 | 56.26 | 4.10 | 0.83 |

| Shares owned by institutions with 5% (%) | 38.48 | 51.28 | 62.55 | 49.00 | 49.87 | 41.43 | 8.40 | 0.09 |

| - excluding firms w/out inst. with 5% (%) | 42.10 | 52.73 | 63.73 | 53.44 | 53.18 | 56.31 | -3.10 | 0.50 |

| iv. Prosocial characteristics | ||||||||

| ESG scores [0,100] | 49.69 | 63.05 | 72.83 | 61.10 | 60.95 | 62.46 | -1.50 | 0.49 |

| Share of firms donating by April 15 (%) | 0.00 | 0.00 | 100.00 | 43.05 | 42.58 | 47.17 | -4.60 | 0.53 |

| Amount donated (m $) | 1.00 | 6.50 | 26.00 | 42.44 | 44.19 | 28.89 | 15.30 | 0.40 |

| Amount donated to revenue (%) | 0.01 | 0.03 | 0.11 | 0.13 | 0.13 | 0.15 | -0.00 | 0.84 |

| Amount donated to dividends (%) | 0.19 | 0.55 | 1.65 | 2.18 | 2.25 | 1.64 | 0.60 | 0.50 |

| i. Definition of the treatment group | ||||||||

| AGM date relative to April 15 | - | - | - | - | Before | After | - | - |

| Number of firms | 433 | 433 | 433 | 433 | 53 | 380 | - | - |

-

•

Note: The first three columns present summary statistics of the principal characteristics of the firms in our sample and their shareholders. The last five columns report average values for the whole sample (Column 4), for firms with an AGM before April 15, 2020 (Column 5) and for firms with an AGM after April 15, 2020 (Column 6), their differences (Column 7) and p-values (Column 8). The accounting and financial data are measured on December 31, 2019. Avg. Brokers’ Recommendations is the average of equity analysts’ investment recommendations where strong sell is -2 and strong buy is 2.

Balance checks. Columns 5 to 8 in Table 1 presents the summary statistics of the main variables for treated (firms with an AGM before April 15, 2020) and control firms (all other S&P 500 firms). The last column reports the p-values from a t-test of the difference in means: we do not detect substantial discrepancies between the two groups. The firms are very similar across their financial characteristics (e.g., debt, market capitalization, and brokers’ recommendations) and operational characteristics (e.g., revenues, EBIT, workforce, number of branches, EPS, and ESG scores). Importantly, for our analyses, despite the institutional control being 14% larger at control than at treated firms on average, treatment and control firms do not differ substantially when we focus on the shares owned by large shareholders, namely, those with more than 5%. The breakdown by type of institutional ownership indicates a statistically significant but economically negligible difference between groups, which disappears when considering only large shareholders. Finally, the share of donating firms within the two groups is approximately the same. Although most firms donate cash and in-kind, the dollar amount does not differ substantially across groups. Overall, these balance checks support the hypothesis that the AGM treatment is indeed exogenous to firms’ characteristics.

Sample size. Our sample size is comparable to other studies employing field experiments or surveys – for instance, using samples of similar size to ours, Bassi et al. (2022) quantify the importance of the rental market for production machines in carpentry, Kiss et al. (2023) study the relations between jobseekers’ skills, their beliefs, and their job search behavior, and Bandiera et al. (2013) compare individual and team incentives. However, since most S&P 500 firms hold AGMs in the summer, 53 firms have their AGMs between January 15 and April 15, 2020, or 14% of the firms without an AGM in this period, which are 380 (last panel of Table 1). This size difference creates a downward bias in the estimation of the AGM treatment effect, , in (2); as a result, our estimates should be interpreted as lower bounds of the actual effect.

4.2 Main Results

Before presenting the results, we provide a graphical representation of our empirical approach through an event study regressing whether firm donated (0/1) between January 15 and April 15, 2020, on weekly dummies for whether firm held its 2020 AGM in week , and industry - and state -fixed effects:111111The US Government invoked the Production Defense Act in April 2020 to economically support large transformations (e.g., Ford Motors’s medical ventilator production). Our dataset spans only voluntary donations, thereby excluding government contracts. As some industries were more likely to engage in government contracts (e.g., the car industry), we control for industries to account for potential biases from lobbying efforts, which, nevertheless, are orthogonal to our AGM timing (Bertrand et al., 2020).

| (3) |

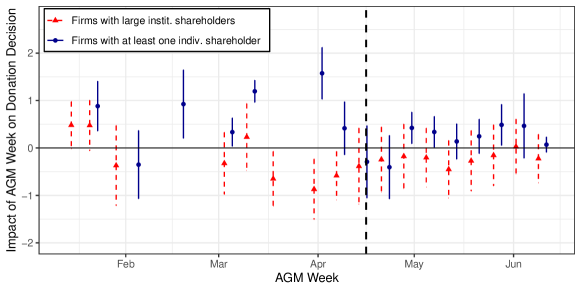

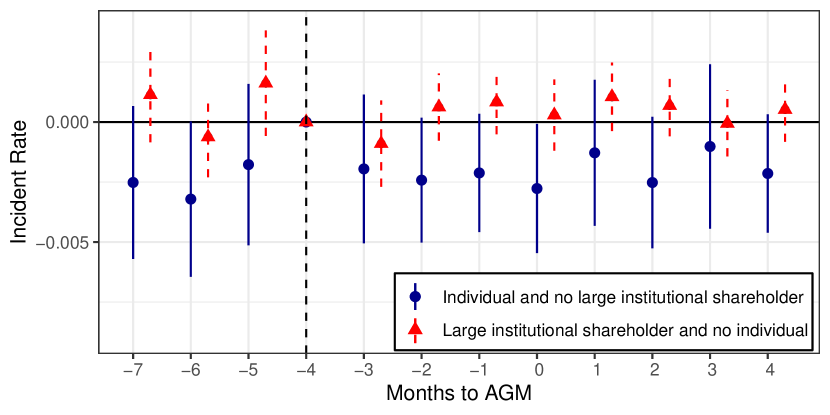

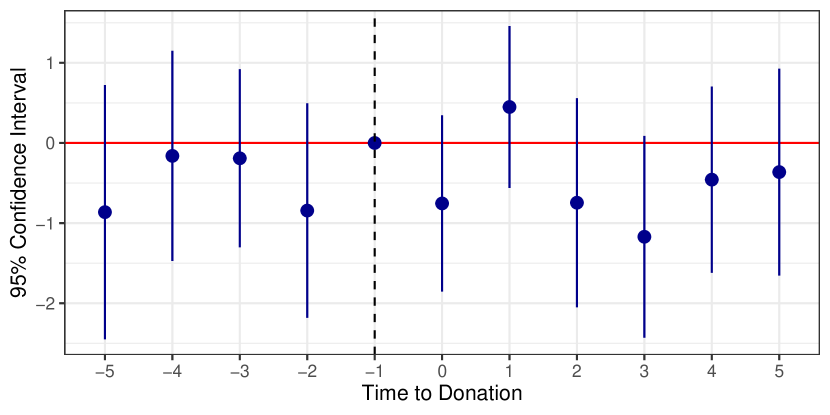

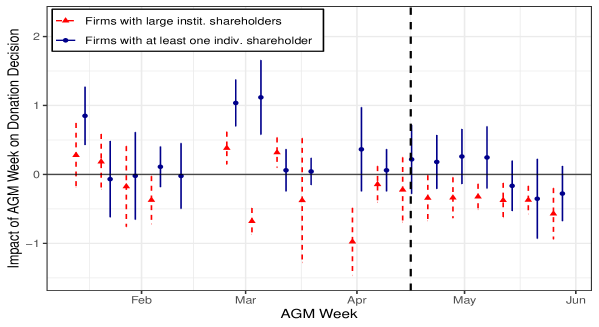

The dependent variable does not vary across weeks: a positive (negative) indicates that holding an AGM in week increases (decreases) the donation rates with respect to the reference week of June 15, 2020.121212This setup captures about 85% of the AGMs of the firms in our sample. Extending the analysis to the whole year does not affect the results. We measure donations by April 15 because the Security Exchange Commission allowed firms to change their AGM date in April, implying that the AGM treatment is no longer exogenous from shareholder preferences for firms planning an AGM for later dates.131313The SEC (2020) states that a firm “can notify shareholders of a change in the date, time, or location of its shareholder meeting without mailing additional soliciting materials or amending its proxy materials” under certain conditions. The change took place on April 7; since the seven S&P 500 firms with AGMs between April 7 and April 15 also held an AGM within less than a week from April 7, 2019, it is unlikely that these firms set their 2020 AGM dates based on shareholder preferences relative to covid donations. Panel (a) of Appendix Figure B1 shows that most AGM date changes made in the first four months of 2020 concerned only firms that held AGMs in (late) April 2019. As in most analyses below, we focus on the extensive margin rather than on the amount donated because almost all firms donated both cash and in-kind. To highlight the trade-off between shareholders that are synonymous with a firm and large institutional shareholders, Figure 1 plots the coefficients estimated through (3) on different sub-samples: firms with at least one individual shareholder (blue circles) and firms whose shareholding body is more concentrated towards large institutional shareholders (red triangles) in December 2019.

Note: The figure plots the estimated coefficients of an event study regressing whether a firm donated between January and April 2020 on dummies, indicating whether the firm held an AGM in the weeks between January 15 and June 15, 2020. The reference period is the week of June 15, 2020. Coefficients shown in circles are estimated using a sample of firms with at least one individual shareholder with at least 0.1% shares, and the triangles are from a sample of firms whose institutional blockholding (shareholders owning at least 5% a firm’s equity as of December 2019) is greater than the median at S&P 500 firms. Standard errors are clustered by industry; vertical bars denote 95% confidence intervals. The vertical dashed line is on April 15, 2020, 90 days after the first US covid case.

We note three results. First, donations are more likely at firms with individual shareholders if they hold an AGM before April 15, 2020 (dots). Second, consistent with our theory, institutional blockholders drive the decline in donation rates (triangles) as they expect dividend losses and no private returns from the donations: all else equal, the opposition to covid-donations will be more effective when institutional shareholders own more shares. Third, these two effects die out for firms that have AGMs after April 15, as shareholders at these firms have fewer incentives to influence managers: individual shareholders receive no additional image shock, which does not trigger the response of institutional shareholders.

Treatment effect. What is the effect of holding an AGM at firms with easily associable shareholders compared to the average firm? Table 2 estimates (2) by OLS, using a dependent variable that is one if firm donated by April 15 and zero otherwise as in (3) and Ownershipf defined either as the share of individual or institutional shareholders with an equity stake that, at December 2019, was either greater than 10% (Column 1 or 4), greater than 5% (Column 2 or 5), or smaller than 2% (Column 3 or 6). Ownershipf is standardized to compare coefficients across columns.141414Since S&P 500 firms have few similarly large “blockholders,” an alternative specification employing an indicator that is one if the firm has at least one shareholder of type (or ) with at least shares does not change our results qualitatively, and we omit it. Finally, standard errors are clustered at the industry level to net out potential stochastic shocks across units (Deeb and de Chaisemartin, 2019). Therefore, the treatment and control groups vary across columns. We standardize Ownershipf to compare coefficients across columns and estimate (2) with industry- and state-fixed effects.

| Whether Firm has Donated (0/1) | ||||||||||||

| (1) | (2) | (3) | (4) | (5) | (6) | |||||||

| Ownership | 0.014 | 0.018 | –0.036 | ∗ | –0.014 | –0.014 | 0.055 | ∗ | ||||

| (0.017) | (0.011) | (0.020) | (0.025) | (0.026) | (0.029) | |||||||

| AGM | 0.095 | 0.097 | 0.089 | 0.082 | 0.083 | 0.092 | ||||||

| (0.099) | (0.099) | (0.102) | (0.081) | (0.104) | (0.101) | |||||||

| Ownership AGM | 0.093 | ∗∗∗ | 0.096 | ∗∗ | –0.013 | –0.150 | ∗∗∗ | –0.021 | –0.033 | |||

| (0.021) | (0.034) | (0.042) | (0.043) | (0.066) | (0.065) | |||||||

| Ownership is defined as | Individuals | Institutional | ||||||||||

| Ownership is the share of investors owning: | ||||||||||||

| Industry fixed effects | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||

| State fixed effects | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||

| 433 | 433 | 433 | 433 | 433 | 433 | |||||||

| Adjusted R-squared | 0.1595 | 0.1599 | 0.1597 | 0.1668 | 0.1562 | 0.1657 | ||||||

| * – ; ** – ; *** – . | ||||||||||||

-

•

Note: The table presents the coefficients from OLS regressions of an indicator variable that is one if firm has donated by April 15, 2020, on covariates. Italicized variables are defined in the middle panel. The variable Ownership is the share of either individual (Columns 1-3) or institutional investors (Columns 4-6) among all investors owning at least a share of total equity, as defined in the middle panel. Institutional investors include the largest financial investors in Table 1, namely, banks, mutual funds, and insurance firms. The variable Ownership is standardized. The AGM variable is an indicator variable taking value one if the firm has an AGM before April 15, 2020, and zero otherwise. All columns include industry- and state-fixed effects. Standard errors are clustered by industry.

Focusing on the interaction term, the estimated is positive and significantly different from zero for individual blockholders (Columns 1 and 2). The coefficient estimates are large as they indicate that the probability of donating increases by more than 9% compared to the average donation rate in the data when the proportion of individual blockholders increases by one standard deviation. Minority shareholders, instead, do not seem to influence company donations (Column 3). These results confirm the predictions of the conceptual framework in Section 2, which hypothesized that prominent individual investors that are more easily associated with a firm, such as those with large equity stakes, should receive a greater pass-through of image gains from the donating firm and will exert more pressure to this end.

What about institutional investors? We focus on the three largest institutional investor types in Table 1 (banks, mutual funds, and insurance firms) and find consistent results with the predictions of the conceptual framework in Section 2. The rightmost columns of Table 2 indicate that the probability of donating decreases by approximately 15% of a standard deviation of the share of large institutional blockholders (Column 4) and a negative but insignificant effect for smaller shareholding brackets (Columns 5 and 6). Thus, the largest institutional shareholders pressure managers against donations as their large equity stakes imply they will shoulder a considerable burden from the prosocial actions.151515Table A1 reports the estimated coefficients for each of the three institutional investor types: opposing influence comes mainly from banks and insurance companies with large shares.

4.3 Mechanism

4.3.1 Do Equity-stakes Capture the Association between Shareholders and Firms?

Not all shareholders are created equal: some are easier to associate with a firm than others in ways not reflected in the equity stake. In this section, we proxy the degree of the association that the public holds between a firm and its most recognizable individual shareholders at the onset of the pandemic in 2020 through the maximum (Spearman) correlation between the Google Trends scores of a firm and that of its individual shareholders for the years 2018 and 2019.161616Google Trends scores report online searches for given keywords. We compute Google Trends scores for firms and shareholders over weekly intervals. For instance, this correlation is +0.25 for Amazon and Jeff Bezos and +0.495 for Berkshire Hathaway and Warren Buffet. Hence, we define the variable in (2) as a dummy that is equal to one if this correlation is positive and significant at the 5% level and zero otherwise, and re-estimate (2) including state- and firm-fixed effects.

The results, displayed in Appendix Table A2, are consistent with the model laid out in Section 2, which finds that donation rates are greater for treated firms with highly-associated individual investors (Column 1). In Columns 2 and 3 we run the same analysis on subsets with increasing shares of institutional shareholders: the results suggest that the influence of recognizable individual shareholders decreases with the presence of large institutional shareholders (Columns 2 and 3). The last column indicates that large institutional shareholders are responsible for this drop in donation rates, as it finds a positive treatment effect estimate when considering only firms with many but small institutional shareholders. Therefore, only large institutional shareholders actively oppose donations.

Google search data vs. shareholding data. The Google Trend correlation measure relies on a fine-tuning parameter: starting the measurement too late in time means discounting recent events, while starting it too close to our sample period could exclude some crucial past events. In addition, we find a substantial correlation between individual blockholding and the Google Trend correlation-based measure.171717The correlation between the Google Trend measure and the share of individual blockholding in the data is 0.43 (p-value ). It is instead -0.05 (p-value of 0.28) with institutional blockholding. Finally, common ownership within an industry, a phenomenon especially present across S&P 500 corporations, might bias Internet-based measures of association between a firm and its institutional investors, as a news piece affecting the whole industry is likely to mention the largest firms within an industry, which could also be shareholders in each others’ equities. For these reasons, we focus on measures of individual and institutional shareholding in the remainder of the paper.

4.3.2 The Pass-Through of Image Gains

Our conceptual framework explains shareholder influence through a different pass-through channel of image gains across investor types. Does the data support this hypothesis? To provide direct evidence of a shock to shareholders’ private returns, we examine shareholders’ media exposure around donation events. We use shareholder names as keywords and run the following OLS regression:

| (4) |

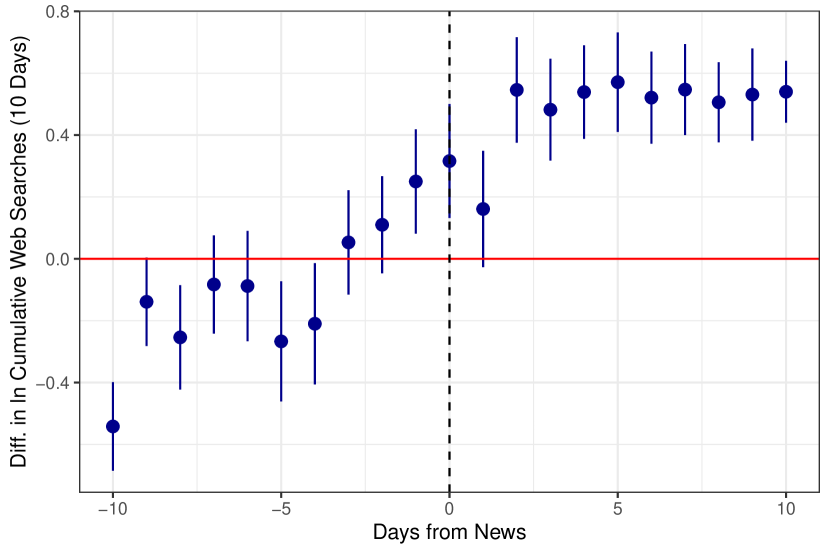

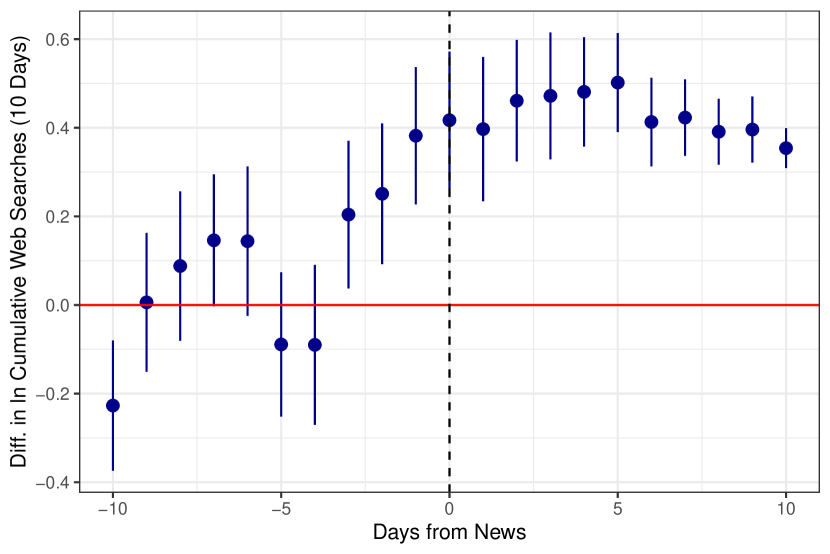

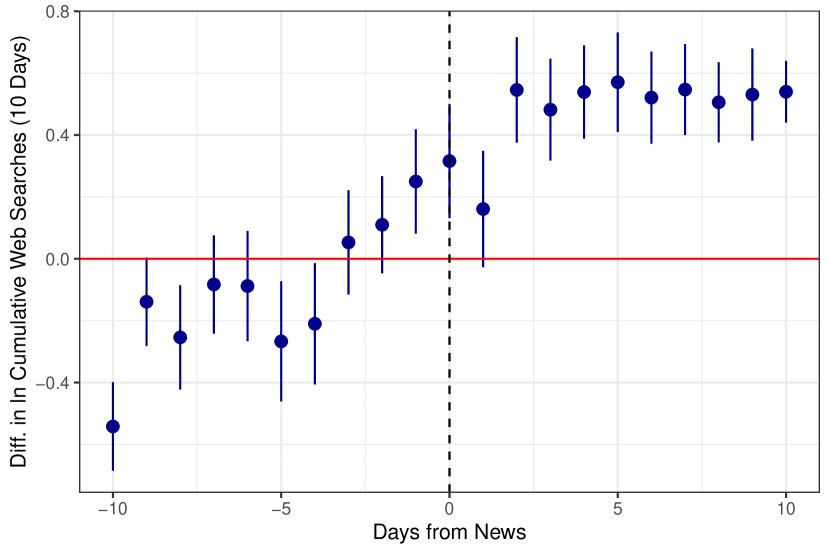

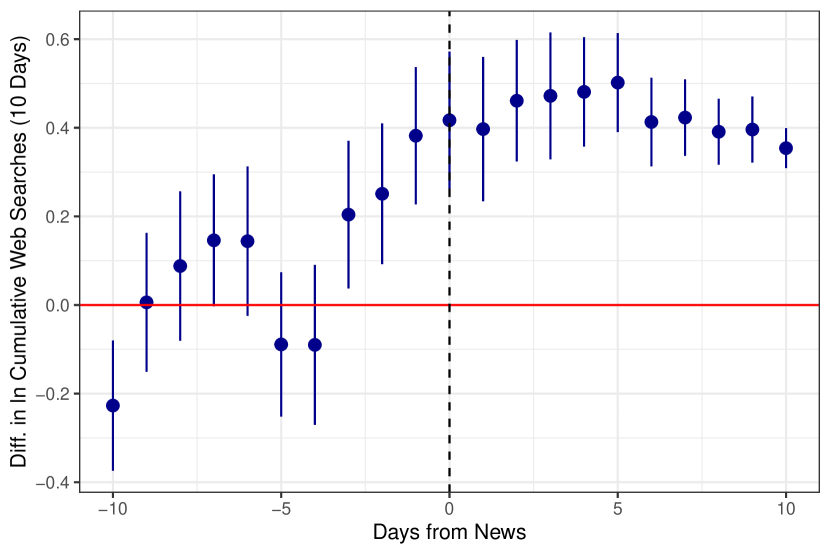

where the dependent variable is the logarithm of the cumulative Google Trends score over a ten-day period starting on day for investor in firm . On the right-hand side, the vector is a set of time dummies around the date of the donation event. We further interact these indicators with another indicator variable that is equal to one if shareholder is an individual investor and zero otherwise. We also include firm, shareholder, and time-fixed effects. We interpret the coefficient vector as the impact of donations on Google searches for nonindividual investors and as the gap in visibility between individual and nonindividual investors at each day .181818For each day, the Google Trends data return a value between 0 and 100 that indicates the frequency of Google searches for a specific keyword based on its long-run searches. Therefore, accounting for shareholder-fixed effects is necessary to compare searches across shareholders.

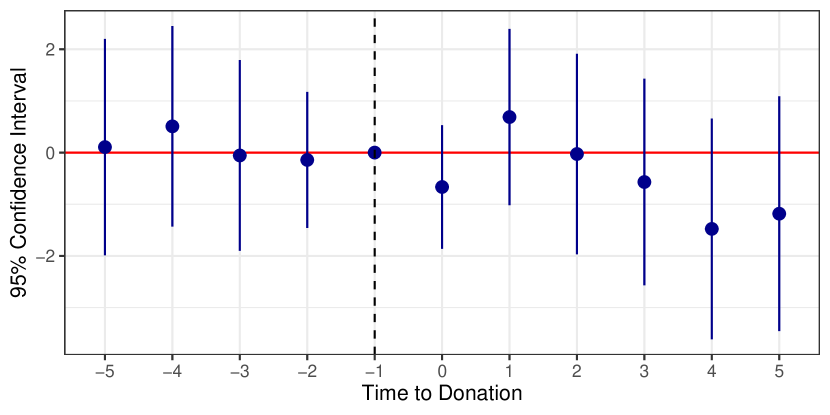

Figure 2 reports the estimated , using cumulative Google Trend scores over ten days as the dependent variable and clustering the standard errors at the firm-by-shareholder level.191919The shareholder types are banks, hedge funds, insurance companies, mutual funds, other financial companies, individual and family shareholders, government, self-ownership, and other firms. Panel (a) uses only shareholders with at least 1% of shares in December 2019. Panel (b) restricts the sample to shareholders with more than 5% of shares.202020Since our analysis finds a limited role of minority investors, we consider Google Trends data only for shareholders holding at least 1% of shares. Appendix Table LABEL:tab:google and Appendix Figure B4 show robust results to cumulating the Google Trend data over different time intervals (7, 10, and 14 days). Across both panels, cumulative Google searches are flat at around zero before the donation news is broken. In Panel (a), after the news is broken, the coefficient estimates jump to about 50% from day 3 to day 10. As we might expect, the effect is stronger in Panel (b), where the coefficient estimates are already significant two days before the news is broken.212121The coefficients cannot be directly compared across the two panels because the average number of cumulative Google searches for nonindividual shareholders is twice as high in Panel (b) than (a). Therefore, the Google search gains of individual investors are substantially higher than those of nonindividual investors, supporting our claim that image concerns create different incentives for individual and non-individual investors.

Note: Both panels report coefficient estimates from Equation 4, which reports the (log) cumulative Google Trends score (ten-day window) of shareholders’ names over dummy variables describing a ten window around a firms’ donation dates and the interaction of these dummies with an indicator function that is equal to one if the concerned shareholder is an individual or family shareholder and zero otherwise. The panels only report these interaction terms. Panel a (Panel b) includes only shareholders with more than 1% (5%) shares. The vertical bars indicate 95% confidence intervals using clustered standard errors by firms and shareholder types (bank, company, individual, financial company, government, hedge fund, insurance, mutual fund, self-ownership).

4.3.3 Donate Directly or Through the Financial Footprint?

Do financial investors openly oppose covid-related donations? To address this question and to understand the tradeoff faced by institutional investors, we compare the donation decisions of financial corporations in the S&P 500 (e.g., BlackRock and Bank of America) with those of the S&P 500 firms in their investment portfolios.222222We focus on only S&P 500 firms that invested in other S&P 500 firms due to data availability. However, we expect our result to hold more broadly because it should be more difficult to influence the management of an S&P 500 corporation than that of a smaller one, other things being equal. More specifically, we analyze the correlation between two vectors: a vector of donation decisions and a vector of donation shares. The vector of donation decisions is a list of binary dummies, one for each of the 37 financial corporations in our data, indicating whether a corporation donated by April 15, 2020 (19 of them donated). The second vector reports the share of firms in the portfolio of a financial shareholder that also donated. A positive correlation between these two variables suggests an alignment in donation intents between investors and firms, while a negative correlation points to a misalignment. We exploit variation in the AGM treatment statuses of the firms in an investor’s portfolio to causally infer whether a donating investor pushes or refrains the firms in their portfolio from donating.

| Spearman Correlations | |||

|---|---|---|---|

| Minimum | Simple | Weighted | Weighted Avg. |

| Equity Share | Average | Average | AGM |

| Considered | [p-values] | [p-values] | [p-values] |

| (1) | (2) | (3) | (4) |

| 0% | 0.442 | -0.062 | -0.211 |

| (Avg. = 222) | [0.007] | [0.721] | [0.238] |

| 1% | 0.064 | 0.079 | -0.093 |

| (Avg. = 100) | [0.751] | [0.696] | [0.705] |

| 2% | -0.230 | 0.077 | -0.439 |

| (Avg. = 57) | [0.280] | [0.721] | [0.089] |

| 3% | -0.105 | 0.180 | -0.617 |

| (Avg. = 48) | [0.643] | [0.423] | [0.077] |

| 4% | -0.112 | 0.060 | -0.878 |

| (Avg. = 42) | [0.630] | [0.795] | [0.021] |

| 5% | 0.124 | 0.275 | -0.289 |

| (Avg. = 35) | [0.637] | [0.285] | [0.638] |

-

•

Note: This table shows a negative correlation between large institutional investors such as financial firms in the S&P 500 Index and the firms in their portfolio that had their AGMs before April 15, 2020. The negative correlation indicates that financial investors opposed COVID-19-related donations in their footprints. The table computes the Spearman correlation between whether a financial firm donates and the share of donations at the firms in its portfolio. In each row, we vary the minimum share % that a firm must have in another firm to be considered an investment according to the percentages reported in the first column. Column 1 also reports the average number of S&P500 firms in the portfolio of a financial investor in parenthesis. Column 2 computes the total donations of the firms that financial firm has invested in using simple averages (i.e., , where is the number of investments of firm ), Column 3 computes weighted average with weights equal to the equity shares (i.e., ), and column 4 considers only investments that got an AGM in the period under consideration (i.e., ). p-values testing whether the Spearman correlation is equal to zero are reported in square brackets.

Focusing first on Column 3 of Table 3, we find that the correlation coefficient between a firm’s corporate giving and the giving within its footprint is positive and even increases across rows, as we raise the minimum shareholding threshold from 0% to 5%. However, no coefficient is statistically significant. This trend may be driven by a few donating firms with larger shares receiving larger weights. Column 2 removes this effect by focusing on simple averages: the correlations are smaller and negative when the minimum shareholding threshold is 2%, 3%, or 4%. Moving to the last column, where we consider only firms with an AGM meeting, we effectively focus on firms whose shareholders might be under the spotlight due to the AGM periods and for which institutional investors might need to pressure managers to prevent individual investors from capturing private rents. As the minimum share threshold increases across rows, the estimated correlation coefficient becomes more negative and statistically significant, approaching for larger thresholds.

These results suggest that, as we tilt the balance of influence from individual to institutional shareholders, the latter shareholders do not necessarily oppose all donations, as they donate themselves. They oppose donations at treated firms in their footprint as they do not yield any image gain but (potentially) cost them lower earnings, as we will see in Section 5.

4.4 Alternative Mechanisms

Intensity of the pandemic. Firms could respond to the need for the donation rather than shareholder pressures. Our empirical approach could miss it if, although unlikely, it is correlated with the AGM treatment. To account for this, we exploit covid cumulative cases and deaths at a firm’s headquarters state under the assumption that the severity of the pandemic will provide shareholders with greater incentives to donate even without the AGM treatment. To this end, we modify (2) as follows:

| (5) | ||||

where the dependent variable, , is equal to one if firm has publicly committed to donating by day and zero otherwise. The main coefficient of interest is , which captures the interaction between the cumulative covid rate at firm ’s headquarters state, , the fraction of equity owned by the reference blockholder, , which varies across specifications, and the AGM treatment, . We use headquarter-state covid rates because Appendix Figure B3 shows a clear spatial pattern across these two variables, with covid-related donations being more likely as the pandemic heightens. Finally, and are firm- and day-fixed effects, and the standard errors are clustered at the firm level.

The first three columns of Appendix Table LABEL:tab:reg-results-large-shareholders present the results when individual shareholders are the reference category, with and standardized to facilitate comparisons across columns with different -blockholding percentages, covid cases (Panel a) and deaths (Panel b). Although the table indicates that one standard deviation in covid rates increases donation rates by about 1%-2%, such an increase is towered by the AGM treatment effect at firms with greater shares of large individual shareholders, , which is estimated between 10 and 20 times larger. In contrast, the treatment effect estimates when the focal blockholder in (2) varies across banks, mutual funds, and insurers are negative (Columns 4 to 12) , consistent with the previous results, and the unconditional effect of covid rates is again negligible.232323We replicate the analysis using cumulative national covid cases and deaths at the national level instead of at the headquarters-state level as they could be more salient than headquarters-state rates for large financial investors. The results, which we omit because of space constraints, are consistent with those presented thus far, with the only difference being that the estimates for individual and family shareholders are now close to zero. Hence, prominent individual shareholders seem to react to local covid rates rather than national rates. This result aligns well with the image concern mechanism we uncover if these large individual shareholders live or conduct their businesses close to their firms and care for local information (see also Bordalo et al., 2022a).

Financial motives. Abnormal returns do not explain covid-related donations. To compute abnormal returns, we predict daily stock returns using the Fama-French three factors, namely, daily market returns (, proxied by the S&P 500 Index), daily returns on a portfolio of “small minus big stocks” (, from Kenneth French’s website), and daily returns on a portfolio of stocks with “high minus low” book-to-market value ratios (, also from French’s website). We retrieve the betas () of those three portfolios for the stocks in our sample from CRSP. Then, stock ’s abnormal return () on day is given by the difference between the actual excess return of the stock over the risk-free rate () and the prediction of the 3-factor model, as We then plug the realized in the following event study:

where the left-hand side refers to either firm ’s abnormal return () or its cumulative abnormal return (CAR) on day . The regression includes firm- and date-fixed effects. Appendix Figure B5 displays the estimates of . Panel (a) shows no abnormal returns before the news is broken, while the abnormal returns are actually negative (although not significant) right after it. Panel (b) reports the CAR over five days, showing a negative drop after the news date.242424We find similar results for the CAR over longer horizons (Appendix Table A4). In summary, we find a negative but transient effect of the news on firms’ financial returns.

Consumer pressure. We exploit exogenous variation in a firm’s exposure to covid through its branches to assess whether consumers pressured firms to donate. Using the Orbis database, we compute the weighted cumulative averages of covid cases and deaths using the number of branches a firm has in each state as weights. We denote the standardized versions of these two new variables by and estimate the following linear probability model:

| (6) | ||||

where is the reported number of branches as of December 2019.252525The distribution of the number of branches for S&P 500 firms ranges from 0 to 13,582 with a median of 40 branches; since we do not know whether a branch is a shop or a factory, it is fair to assume that firms with more branches are more exposed to final consumers than firms with few branches. The results show a null effect of covid exposure (Appendix Table A3).

Managerial freedom and competition. We proxy managerial freedom with the share of a firm’s equity owned by the firm itself and study the probability of observing a donation by time using (5), where we set equal to one if firm owns more than the median amount of its own shares, and zero otherwise. Since the AGM period provides an opportunity for managers to present their achievements, we use the difference between the treated and control firms to estimate the causal impact of managerial’s private or image returns on donations. Although the salience of a donation in a period of crisis can help managers of underperforming firms (Akey et al., 2021; Bordalo et al., 2022b), the results indicate that managers aligned with financial investors in opposing donations potentially because if the donations are costly, as we will see in Section 5, managers might see their compensation decrease (Appendix Table A5).

We also study whether firms donated in response to past covid-related donations of a firm’s direct competitors by also controlling in (5) for a variable that is one if at least one S&P 500 firm in the industry of the focal firm has donated in the previous week and zero otherwise.262626We consider competitors’ donations in the past week to single out a firms’ response to their donations. We obtain similar results using different lags. Our results, presented in Appendix Table A6, show a limited role of competition while the treatment effect coefficients are very similar to those from Table LABEL:tab:reg-results-large-shareholders. Overall, these findings are in line with other studies suggesting that managers are under pressure to report positive corporate results during AGM periods (Dimitrov and Jain, 2011): large donations can jeopardize a firm’s financial position during a time of distress, potentially also affecting managerial compensation.

Missing observations in Orbis. This section has focused on a sample of firms without missing financial and ownership information in Orbis to ensure consistency across the empirical exercises. We replicate our main results – the evidence of influence by individual and institutional shareholders (Figure 1 and Table 2) and by financial shareholders within their portfolio (Table 3) – in Appendix Section D using Refinitiv’s consolidated ownership data, a slightly larger dataset, that provides historical shareholding information but, unlike Orbis, lacks self-ownership data. Across analyses, not only the signs but also the magnitude of the coefficients stays almost unchanged.

4.5 Shareholder Influence Beyond the Pandemic

Does shareholders’ influence through voice extend beyond pandemic periods? We test external validity over time and crises by focusing on another time of crisis, the recent Russian invasion of Ukraine in Section 4.5.1 and by using various measures of prosociality over the last decade in Section 4.5.2.

4.5.1 Shareholder Influence and the Russian Invasion of Ukraine in 2022

On February 24, 2022, the President of the Russian Federation, Vladimir Putin, launched the so-called “special military operation,” which started with the invasion of Ukraine and quickly escalated to a war that is still ongoing at the time of writing. Soon after that, media scrutiny of multinational corporations intensified as the public questioned the Western firms that continued to conduct business in the attacking country, Russia. As a result, many firms decided to limit their exposure to Russian consumers and businesses, with several exiting Russia altogether. In this section, we study whether a differential pass-through of image gains to individual and institutional shareholders was a factor in these decisions without discussing whether exiting was or was not the socially optimal decision. That is, we view rushed exits as consequential, costly decisions with a significant media impact that could boost the image of synonymous shareholders while costing the others substantially as firms need to pay relocation costs (e.g., suddenly seeking new suppliers and consumers than for planned exits).

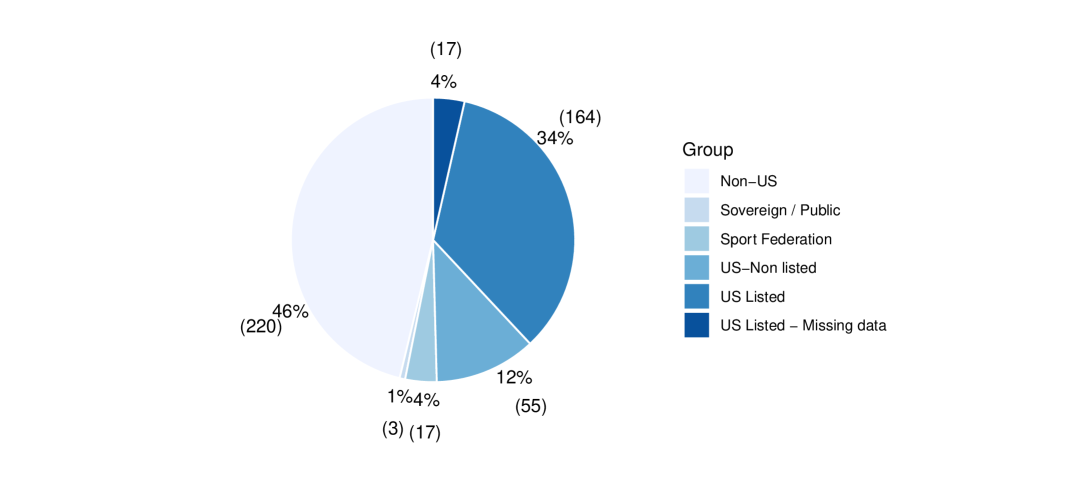

Using the same approach outlined in Section 4.1, we test shareholders’ influence on exiting decisions. Once again, we take advantage of the SEC rules and exploit the occurrence of AGMs as exogenous shocks to firms’ scrutiny. To this end, we use a novel dataset that records the actions taken by international corporations vis-à-vis Russia (Sonnenfeld et al., 2022). Through this dataset, we observe the set of US-listed firms that publicly announced actions by March 23, 2022 – a month from the beginning of the conflict (164 firms).272727We focus on US-listed firms because the SEC rules apply to US firms. The emphasis is on the first month of conflict because the firms that took action in this period are most likely the most exposed to the Russian market. Focusing on this period also allows us to exclude actions dictated by the ensuing Western sanctions. The vast majority of these firms are in the S&P 500 index and span various sectors of the economy. Online Appendix E describes the data in detail and shows that industries are similarly represented across treated and control firms. These decisions vary from exiting the country to limiting current and future investments or continuing business as usual. In particular, 51 of the 164 firms in the dataset decided to leave the Russian market. We study this radical decision because of its visibility and salience to the public. Moreover, exiting Russia goes beyond the intention of international sanctions in the first month of conflict, and thus, it was not forced by regulations.

Using (2), we identify shareholders’ voice on whether to leave Russia by setting the dependent variable, , to one if firm announced its exit during the first month of conflict and zero otherwise. The regressors are instead, , which is equal to one if held an AGM in the three-month period starting on February 24, 2022, and zero otherwise, and which is equal to one if firm has either a shareholder of the reference type, either an individual or an institutional shareholder depending on the specification, owning more than the median share of the reference shareholder in the data. We set shareholding data at January 2022 to avoid contamination from shareholder sales. We also include several control variables such as industry fixed effects, broker recommendations, information about geographic sources of revenues, and financial standing at the end of 2021. We provide more information on the covariates and show balance tests in Appendix E.

Table 4 reports the results: Columns 1 to 3 refer to individual blockholders, while Columns 4 to 6 refer to institutional blockholders. As in the previous tables, we vary the blockholding thresholds as described in the middle panel: the magnitude of the treatment effect, , increases for higher thresholds. Consistent with previous results, the presence of prominent individual shareholders positively correlates with exits, while the presence of similarly large institutional investors pushes firms’ decisions in the opposite direction.

| Exited Russia in the Frist Month of Conflict (0/1) | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | |||||||

| AGM | –0.067 | –0.080 | –0.094 | 0.144 | 0.035 | 0.043 | ||||||

| (0.090) | (0.087) | (0.090) | (0.115) | (0.116) | (0.111) | |||||||

| Above Median Blockholding | –0.547 | ∗∗∗ | –0.542 | ∗∗∗ | –0.428 | ∗∗∗ | 0.116 | 0.070 | 0.148 | |||

| (0.181) | (0.145) | (0.128) | (0.132) | (0.134) | (0.137) | |||||||

| AGM Above Median Blockholding | 0.705 | ∗∗∗ | 0.316 | 0.263 | –0.341 | ∗∗ | –0.152 | –0.188 | ||||

| (0.254) | (0.244) | (0.175) | (0.165) | (0.160) | (0.159) | |||||||

| Above Median Blockholding (0/1) defined for: | Individual | Institutional | ||||||||||

| Threshold to be considered a blockholder: | 10% | 5% | 2% | 10% | 5% | 2% | ||||||

| Controls | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||

| Sector fixed effects | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||

| 138 | 138 | 138 | 138 | 138 | 138 | |||||||

| Adjusted R-squared | 0.2762 | 0.2923 | 0.2879 | 0.2642 | 0.2320 | 0.2372 | ||||||

| * – ; ** – ; *** – . | ||||||||||||

-

•

Note: The table presents the coefficients from OLS regressions of an indicator that is one if firm has exited Russia by March 23, 2022, and zero otherwise on covariates. The regressions only exploit cross-section variation across firms at March 23, 2022. Italicized variables are defined in the middle panel. Above Median Blockholding is one if firm has more blockholders of the reference category than the median S&P 500 firm and zero otherwise. The reference category and the blockholding thresholds are defined in the middle panel. Control variables include the share of revenues that come from activities in the US and Canada, the exposure to Russia, brokers’ recommendations, CEO age, and net income. Market capitalization, revenues, and net income are highly correlated; controlling for any of these two variables instead of net income does not change the results qualitatively. For models where individual investors are the reference category (Columns 1 to 3), we also include a dummy equal to 1 for above-median institutional ownership. This variable is necessary to control whether institutional investors are heavily invested in a firm, as this channel could reduce the voice of individual and family shareholders. This variable would have been unnecessary if we could have exploited firm-fixed effects. All columns include sector-fixed effects. Robust standard errors in parenthesis.

Robustness checks. In Online Appendix E.2, we perform several tests of these empirical findings. First, we show that the negative coefficient for institutional investors is mainly driven by mutual funds and banks and only partially depends on the influence of insurance company shareholders – a finding that is consistent with those in Table LABEL:tab:reg-results-large-shareholders. The results also remain unchanged by modifying equation 2 to show simultaneous treatment effects by individual and institutional blockholders through the AGM treatment or whether firms that decide for business as usual are included in the analysis. In addition, we obtain similar results when we include all US S&P 500 firms while assuming that the S&P 500 firms not surveyed by Sonnenfeld et al. (2022) took no action against Russia. Finally,exit decisions are not merely determined by the size of the firm, as measured by market capitalization or net income in 2021, indicating scope for shareholder influence.

Impacts on supply chains. Online Appendix E.3 examines supply chains. Drawing from Factset, which provides information on supply relationships between US and Russian firms, we let the dependent variable in (2), , be one if firm reduced ties with Russia after February 24 and zero otherwise. Despite the size of the dataset, which covers only 102 firms with supply chains in Russia before February 24, 2022, we find that large individual shareholders indeed demanded to cut Russian suppliers.

4.5.2 Shareholder Influence Beyond Crises

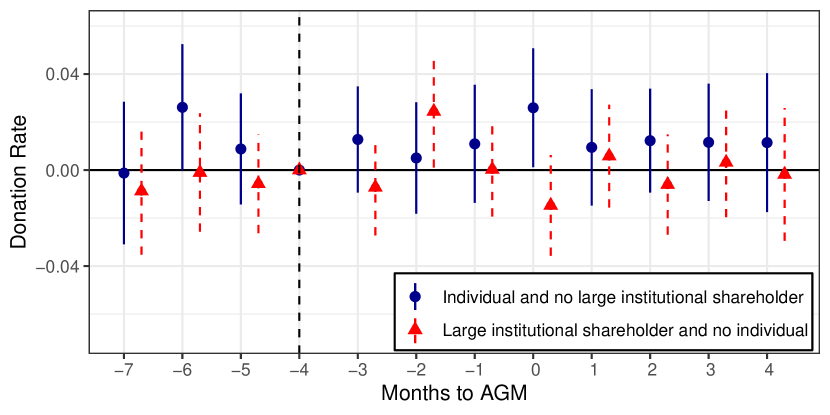

Is shareholder influence on prosocial matters only limited to crisis events? We examine this question by studying firms’ ESG-related news coverage and donations during AGM periods across firms with different shares of individual shareholders. We expect the change in these variables to be only temporary because shareholders’ reputation gains should be limited to the AGM period if they drive influence.

Data. ESG-related news data come from RepRisk for 2011-2021. RepRisk screens over 80,000 media, regulatory, and commercial documents daily in fifteen different languages for adverse ESG issues called “incidents.” We focus on incidents because favorable news may come from greenwashing. Charitable donation data comes from Ravenpack, which similarly gathers news about millions of entities worldwide and identifies news about donations made by US corporations between 2011 and 2021. We merge this data with historical shareholding information from Refinitiv to get the firms’ shareholder compositions over the period. Finally, we source AGM dates from ISS. The resulting ESG-incident dataset covers 642 firms over eight years. The average firm had 772 ESG incidents in this period, of which 651 pertained to the social (“S”) category. The donation dataset spans 988 firms over 11 years, 760 of which made at least one donation for a total of 4,439 donations. The firms in the resulting datasets account for over 90% of the market capitalization of the original Ravenpack and RepRisk datasets (Appendix F describes the sample selection).

Methodology. Once again, we exploit the exogeneity of the dates of AGMs to test whether the presence of individual blockholders is associated with prosociality. Exploiting the fact that shareholders have until 120 days before the date of the release of the proxy statement of the previous AGM to submit proposals for the current AGM, we distinguish two periods: a pre-period, during which formal proposals can be cast, and a post-period, during which shareholders can engage only informally with managers and board members. We also consider two groups of firms based on their level of individual and institutional blockholders. To operationalize this analysis, we need to overcome two issues: (i) AGM dates vary across firms within a year, and (ii) firms have AGMs every year – i.e., repeated treatment. To address the first concern, we modify the calendar time of each firm so that the third month before its AGM date coincides with month 0. The pre-period starts in month -4 and ends in month 0, while the post-period lasts from period 0 to 7. Thus, a year still consists of 12 months and starts seven months before the AGM date for all firms. To address the second challenge, we stack all our yearly difference-in-differences analyses over the years as proposed in Cengiz et al. (2019). We focus on the following event study regression:

| (7) |