∎

22email: csdtc@bristol.ac.uk Copyright ©2023 Dave Cliff.

Parameterised-Response Zero-Intelligence Traders

Abstract

I introduce PRZI (Parameterised-Response Zero Intelligence), a new form of zero-intelligence (ZI) trader intended for use in simulation studies of the dynamics of continuous double auction markets. Like Gode & Sunder’s classic ZIC trader, PRZI generates quote-prices from a random distribution over some specified domain of discretely-valued allowable quote-prices. Unlike ZIC, which uses a uniform distribution to generate prices, the probability distribution in a PRZI trader is parameterised in such a way that its probability mass function (PMF) is determined by a real-valued control variable in the range that determines the strategy for that trader. When , a PRZI trader behaves identically to the ZIC strategy, with a uniform PMF; but when the PRZI trader’s PMF becomes maximally skewed to one extreme or the other of the price-range, thereby making it more or less “urgent” in the prices that it generates, biasing the quote-price distribution toward or away from the trader’s limit-price. To explore the co-evolutionary dynamics of populations of PRZI traders that dynamically adapt their strategies, I show initial results from long-term market experiments in which each trader uses a simple stochastic hill-climber algorithm to repeatedly evaluate alternative -values and choose the most profitable at any given time. In these experiments the profitability of any particular -value may be non-stationary because the profitability of one trader’s strategy at any one time can depend on the mix of strategies being played by the other traders at that time, which are each themselves continuously adapting. Results from these market experiments demonstrate that the population of traders’ strategies can exhibit rich dynamics, with periods of stability lasting over hundreds of thousands of trader interactions interspersed by occasional periods of change.

Python source-code for PRZI traders, and for the stochastic hill-climber, have been made publicly available on GitHub.

Keywords:

Zero-Intelligence Traders Continuous Double Auction Adaptive Trading Strategies Automated Trading Co-evolutionary dynamicsMSC:

MSC91–08 MSC91B26Acronyms and Abbreviations

| Characters | Expansion | First Use |

|---|---|---|

| AA | Adaptive Aggressive (adaptive trading strategy) | Section 1 |

| AF | Asymptotic Form (PMF envelope) | Section 4.1 |

| AI | Artificial Intelligence | Section 1 |

| AKA | Also Known As | Section 1 |

| ABM | Agent-Based Model | Section 1 |

| ACE | Agent-Based Computational Economics | Section 1 |

| BG | Balanced Group (experiment design) | Section 6.3 |

| BSE | Bristol Stock Exchange (simulation platform) | Section 3.2 |

| CDA | Continuous Double Auction | Section 2 |

| CDF | Cumulative Distribution Function | Section 4.2 |

| CIAO | Current Individual vs. Ancestral Opponent | Section 6.3.3 |

| GD | Gjerstad-Dickhaut (adaptive trading strategy) | Section 1 |

| GDX | GD Extended (adaptive trading strategy) | Section 1 |

| GVWY | Giveaway (nonadaptive trading strategy) | Section 1 |

| HBL | Heuristic-Based Learning (adaptive trading strategy) | Section 1 |

| IBM | International Business Machines Corp. | Section 1 |

| IID | Independent and Identically Distributed | Section 6.3.2 |

| IPRZI | Imbalance-sensitive PRZI (nonadaptive trading strategy) | Section 6.1 |

| ISHV | Imbalance-sensitive SHVR (nonadaptive trading strategy) | Section 6.1 |

| JPE | Journal of Political Economy | Section 2 |

| LOB | Limit Order Book | Section 2 |

| LOI | Line of Identity | Section 6.3 |

| LUT | Look-Up Table | Section 4.2 |

| MAB | Multi-Armed Bandit | Section 6.3.1 |

| MGD | Modified GD (adaptive trading strategy) | Section 1 |

| MI | Minimal Intelligence | Section 1 |

| ML | Machine Learning | Section 1 |

| MLOFI | Multi-Level Order-Flow Imbalance | Section 6.1 |

| NZI | Near-Zero Intelligence (nonadaptive trading strategy) | Section 6.2 |

| OD | Opinion Dynamics | Section 6.2 |

| OIM | One-in-Many (experiment design) | Section 6.3 |

| ONZI | Opinionated NZI (nonadaptive trading strategy) | Section 6.2 |

| OPRZI | Opinionated PRZI (nonadaptive trading strategy) | Section 6.2 |

| OZIC | Opinionated ZIC (nonadaptive trading strategy) | Section 6.2 |

| PMF | Probability Mass Function | Section 3.1 |

| PRSH | PRZI Stochastic Hillclimber (adaptive trading strategy) | Section 6.3 |

| PRZI | Parameterized-Response ZI (nonadaptive trading strategy) | Section 1 |

| RDA | Replicator Dynamics Analysis | Section 6.3 |

| RP | Recurrence Plot | Section 6.3.3 |

| RMS | Root Mean Square | Section 3.1 |

| RQA | Recurrence Quantification Analysis | Section 6.3.3 |

| SHVR | Shaver (nonadaptive trading strategy) | Section 1 |

| SNPR | Sniper (nonadaptive trading strategy) | Section 1 |

| ZI | Zero Intelligence (class of trader-agents) | Section 1 |

| ZIC | ZI Constrained (nonadaptive trading strategy) | Section 1 |

| ZIP | ZI Plus (adaptive trading strategy) | Section 1 |

| ZIU | ZI Unconstrained (nonadaptive trading strategy) | Section 3.1 |

Notations

| Symbol | Denotes | First Use |

|---|---|---|

| Smith’s equilibration metric | Section 3.1 | |

| The market’s tick-size | Section 3 | |

| Top-of-LOB imbalance metric | Section 6.1 | |

| Difference between minimum and maximum price on a PMF | Section 4.1 | |

| Step-size in strategy space when mapping fitness landscape | Section 6.3 | |

| Timestep duration in the BSE simulation: seconds | Section 3 | |

| Tiny threshold value to avoid divide-by-zero errors in | Section 4.2 | |

| Cumulative Distribution Function (CDF) for PRZI trader | Section 4.2 | |

| Approximation to inverse CDF, via reverse table-lookup | Section 4.2 | |

| Fitness function used in stochastic hillclimber | Section 6.3 | |

| Genesis function used in stochastic hillclimber to create | Section 6.3 | |

| Market-impact function for trader | Section 6.1 | |

| Number of different strategies held by a PRSH trader | Section 6.3 | |

| Buyer’s limit-price | Section 3 | |

| Seller’s limit-price | Section 3 | |

| Largest limit price assigned to seller at any time | Section 3 | |

| Mutation function used in stochastic hillclimber | Section 6.3 | |

| Number of buyers in the market | Section 6.3.2 | |

| Number of sellers in the market | Section 6.3.2 | |

| Number of IID repetitions of an experiment | Section 6.3 | |

| Number of discrete strategies available to choose between | Section 6.3 | |

| Number of traders in the market: | Section 6.3 | |

| Opinionated limit price | Section 6.2 | |

| Opinion value for trader | Section 6.2 | |

| Total profit/surplus extracted by the set of buyers | Section 6.3 | |

| Total profit/surplus extracted by the set of sellers | Section 6.3 | |

| Total profit/surplus extracted by all traders: | Section 6.3 | |

| Equilibrium price | Section 2 | |

| Price of the best ask on the LOB at time | Section 2 | |

| Price of the best bid on the LOB at time | Section 2 | |

| Arbitrary maximum price allowed in the market | Section 3.1 | |

| Mid-price on the LOB at time | Section 6.1 | |

| Micro-price on the LOB at time | Section 6.1 | |

| Price quoted at time by a buyer of strategy-type strat | Section 3 | |

| Price quoted at time by a seller of strategy-type strat | Section 3 | |

| Probability that random variable is equal to price | Section 4.1 | |

| PMF envelope profile function | Section 4.2 | |

| PMF for trader | Section 4.2 | |

| Equilibrium quantity | Section 2 | |

| Quantity available at price on the LOB at time | Section 6.1 | |

| Quantity available at price on the LOB at time | Section 6.1 | |

| PRZI strategy-value for trader : | Section 1 | |

| moving average of | Section 6.3.2 | |

| The set of terminal values from a population of traders | Section 6.3.2 | |

| Strategy-vector for all-PRSH market: ; | Section 6.3 | |

| Set of different -values at time for individual PRSH trader | Section 6.3 | |

| Time: | Section 2 | |

| Linear rectifier function | Section 4.2 | |

| Draws from a uniform random distribution over the range | Section 3 |

1 Introduction

In attempting to understand and predict the fine-grained dynamics of financial markets, there is a long tradition of studying simulation models of such markets. Simulation studies nicely complement the two primary alternative lines of enquiry: analysis of real market data recorded at fine-grained temporal resolution, as is studied in the branch of finance known as market microstructure; and running carefully planned experiments where human subjects interact in artificial markets under controlled laboratory conditions, i.e. experimental economics. Simulation modelling of financial markets very often involves creating agent-based models (ABMs) that populate a market mechanism with some number of trader-agents: autonomous entities that have “agency” in the sense that they are empowered to buy and/or sell items within the particular market mechanism that is being simulated. This approach, known as agent-based computational economics (ACE), has a history stretching back for more than 30 years. Over that multi-decade history, a small number of specific zero-intelligence (ZI) and/or minimal-intelligence (MI) trader-agent algorithms, i.e. precise mathematical and procedural specifications of particular trading strategies, have been frequently used for modelling various aspects of financial markets, and the convention that has emerged is to refer to each such strategy via an acronym or short sequence of letters, reminiscent of a stock-market ticker-symbol.111Notable trading strategies in this literature include (in chronological sequence): SNPR (aka Kaplan’s Sniper, as described in Rust et al., (1992)), ZIC (Zero Intelligence Constrained: Gode and Sunder, (1993)); ZIP (Zero Intelligence Plus: Cliff, (1997)); RE (Roth-Erev: Erev and Roth, (1998)); GD (Gjerstad-Dickhaut: Gjerstad and Dickhaut, (1998)); MGD (Modified GD: Tesauro and Das, (2001)); GDX (GD eXtended: Tesauro and Bredin, (2002)); HBL (Heuristic Based Learning: Gjerstad, (2003)); AA (Adaptive Aggressive: Vytelingum et al., (2008)) and IEL (Individual Evolutionary Learning: Arifovic and Ledyard, (2011)); several of which are explained in more detail later in this paper. Of these, ZIC Gode and Sunder, (1993) is notable for being both highly stochastic and extremely simple, and yet it gives surprisingly human-like market dynamics; GD Gjerstad and Dickhaut, (1998) and ZIP Cliff, (1997) were the first two strategies to be demonstrated as superior to human traders, a fact first established in a landmark paper by IBM researchers Das et al., (2001) (see also: De Luca and Cliff, 2011a ; De Luca and Cliff, 2011b ; De Luca et al., (2011)), which is now commonly pointed to as initiating the rise of algorithmic trading in real financial markets; and until very recently AA Vytelingum et al., (2008) was widely considered to be the best-performing strategy in the public domain. With the exception of SNPR Rust et al., (1992) and ZIC, all later strategies in this sequence are adaptive, using some kind of machine learning (ML) or artificial intelligence (AI) method to modify their responses over time, better-fitting their trading behavior to the specific market circumstances that they find themselves in, and details of these algorithms were often published in major AI/ML conferences and journals.

The supposed dominance of AA has recently been questioned in a series of publications Vach, (2015); Cliff, (2019); Snashall and Cliff, (2019); Rollins and Cliff, (2020); Cliff and Rollins, (2020) which demonstrated AA to have been less robust than was previously thought. Notably, Rollins and Cliff, (2020); Cliff and Rollins, (2020) report on trials where AA is tested against two novel nonadaptive algorithms that each involve no AI or ML at all: these two newcomer strategies are known as GVWY and SHVR Cliff, (2012, 2018), and each share the pared-back minimalism of Gode & Sunder’s ZIC mechanism. In the studies that have been published thus far, depending on the circumstances, it seems (surprisingly) that GVWY and SHVR can each outperform not only AA but also many of the other AI/ML-based trader-agent strategies in the set listed above. Given this surprising recent result, there is an appetite for further zero-intelligence ACE-style market-simulation studies involving GVWY and SHVR. One compelling issue to explore is the co-adaptive dynamics of markets populated by traders that can choose to play one of the three strategies from GVWY, SHVR, and ZIC, in a manner similar to that studied by Walsh et al., (2002) who employed ‘replicator dynamics’ modelling techniques borrowed from theoretical evolutionary biology to explore the co-adaptive dynamics of markets populated by traders that could choose between SNPR, ZIP, and GD.

One way of studying co-adaptive dynamics in markets where the traders can choose to either deploy GVWY, SHVR, or ZIC is to give each trader a discrete choice of one from that set of three strategies, such that at any one time any individual trader is either operating according to GVWY or SHVR or ZIC. However it is appealing to instead design experiments where the traders can continuously vary their trading strategy, exploring a potentially infinite range of differing strategies, where the space of possible strategies includes GVWY, SHVR, and ZIC; and that is the motivation for this paper. Here, I introduce a new trading strategy that has a parameterised response: that is, its trading behavior is determined by a strategy parameter : when , the trader behaves identically to ZIC; and when it behaves the same as GVWY or SHVR; but can also take on any other value in its range, such as or , which gives novel “hybrid” trading behavior part-way between ZIC and either GVWY or SHVR. As is explained in more detail later in this paper, GVWY, ZIC, and SHVR are each members of the class of zero intelligence (ZI) trading strategies, and hence I’ve named the new strategy described here as the Parameterized-Response Zero-Intelligence (PRZI) trading strategy. The acronym PRZI is pronounced like “pressie”.

To provide a zero-intelligence model trader for studying evolutionary or adaptive markets (as discussed in, for example: Friedman, (1991); Blume and Easley, (1992); Friedman, (1998); Lo, (2004, 2019); Nelson, (2020)), each PRZI trader needs some adaptation mechanism, allowing it to adjust its individual -value over time, to be better suited to the prevailing market conditions that the particular trader finds itself in. There are many potential adaptation mechanisms that could be used, but the results in this paper come – in the minimalist style of ZI traders – from a very basic adaptive algorithm (arguably, the simplest possible): a -point stochastic hill-climber, the operation of which is described in detail below, in Section 6.3. I refer to traders with this adaptation mechanism, PRZI with Stochastic Hill-climbing, as PRSH traders (pronounced “pursh”). PRSH is offered here as an absolutely minimal model of an adaptive trader – it has only a single parameter (unlike, for example, ZIP which has between 8 and 60 parameters, depending on which version is used: see Cliff, (2009)), and it does usefully adapt the value of that parameter over time (although, as discussed further below, there are many better ways of doing adaptation). Section 6.3 presents results and analysis from multiple experiments with markets populated entirely by PRSH traders – these are zero-intelligence adaptive markets, in the sense popularised by Lo Lo, (2004, 2019).

While one motivation for devising PRZI was just described: to enable explorations of co-adaptive dynamics in continuous strategy-spaces, that is not the only motivation. Two other compelling reasons for wanting a ZI-style trader with a variable response are as follows:

-

•

Recent publications Church and Cliff, (2019); Zhang and Cliff, (2021) have described methods for making these simple trader-agents exhibit a form of sensitivity to temporary imbalances between supply and demand in the marketplace, and that imbalance-sensitivity then gives rise to so-called “market impact” effects, in which the prices quoted by traders shift in the anticipated direction of future transaction prices, where the shift is anticipated from the degree of supply/demand imbalance instantaneously evident in the market. Market impact is a significant issue for traders in real markets who are looking to buy or sell an unusually large amount of some asset, and major exchange operators such as the London Stock Exchange have introduced specialised mechanisms to try to reduce the ill-effect of market impact (see e.g. Church and Cliff, (2019) for further discussion). For markets populated by ZI trader-agents to be able to exhibit impact effects, the traders need to be able to modulate their trading activity according to the direction and degree of imbalance in the market, becoming either more “urgent” or more “relaxed” in their trading: varying PRZI’s strategy-parameter implements exactly this kind of tuneable response, as is illustrated in Section 6.1.

-

•

Shiller has recently proposed Shiller, (2017, 2019) that certain economic phenomena which defy easy explanation via classical assumptions of individual economic rationality can be better understood by reference to the narratives (i.e., the stories) that economic agents tell themselves and each other about current and future economic factors. Shiller refers to this new approach as narrative economics. Noting that stories are merely externalisations of an agent’s internally-held opinions, a recent publication Lomas and Cliff, (2021) described an agent-based modelling platform for studying issues in narrative economics, in which two types of ZI traders were extended to also each include a real-valued opinion variable (the value of which could be altered by interactions with other agents, thereby modelling the way in which an agent’s opinions are shifted by the narratives it is exposed to) and adapted so that their trading strategies alter as a function of their individual opinion: this also gives rise to a need for ZI traders that can smoothly vary the nature of their trading behavior, and PRZI was designed with the intention of being used in such opinion dynamics modelling work: exploring the use of PRZI in ACE-style agent-based models is a topic of current research, discussed further in Section 6.2.

This paper is intended merely as an introduction to PRZI; it is beyond the scope of this document to provide a comprehensive and detailed literature review. Readers seeking further details of market microstructure are referred to O’Hara, (1998); Harris, (2002); Lehalle and Laruelle, (2018), and for overviews of experimental economics see for example Kagel and Roth, (1997); Smith, (2000); Plott and Smith, (2008). For reviews of ACE research, see Tesfatsion and Judd, (2006); Chen, (2011, 2018); Hommes and LeBaron, (2018); and for discussions of ZI traders in finance research, see e.g. Farmer et al., (2005); Ladley, (2012); Cartlidge et al., (2012).

2 Background: Experimental Economics

In a landmark 1962 paper Smith, (1962) published in the Journal of Political Economy (JPE), Vernon Smith described a seminal set of experiments in which human traders interacted within a continuous double auction (CDA), the mechanism embodied in most major real-world financial markets, under laboratory conditions. The introduction to Smith’s 1962 JPE paper rightly cited the earlier work of Chamberlin who had described results from an experimental market in a JPE paper published in 1948 Chamberlin, (1948). Smith’s 1962 paper, and Chamberlin’s before that, are widely regarded as marking the birth of experimental economics, and Smith’s work in this field led to him being awarded the 2002 Nobel Prize in Economics.

In the simplest case, such experimental economics work involves a market with only one type of a tradeable asset (think of it as a stock market on which only one stock is listed), and each human trader can buy or sell a specific quantity of the asset by issuing one or more quotes to the market’s central exchange. A quote would specify: the trader’s desired direction (i.e., buy or sell) for the transaction; the quantity (number of units) that the trader is seeking to transact; and the price-per-unit that they want to pay or be paid. Each trader would be given instructions, referred to here as assignments, that are private and specific to that individual trader, and each trader is told to keep these instructions secret. Some traders will be instructed to buy some quantity of the asset, paying no more than a trader-specific maximum price per unit (i.e., these traders are buyers each with a specific limit price); other traders will have been instructed to sell some quantity of the asset, accepting no less than some trader-specific minimum price per unit (so they are sellers, again each with their own limit-price). In this way, instructing some traders to be buyers and other traders to be sellers, and by varying the limit-prices in each trader’s instructions, the market’s underlying supply and demand curves could be controlled, along with that market’s competitive equilibrium price (denoted by ) and equilibrium quantity (). Smith’s 1962 paper (which reported on a sequence of experiments that he had commenced several years earlier) was notable for establishing a set of experiment methods that have since been reproduced and replicated by researchers around the world, and also for being the first empirical demonstration that CDA markets could show reliable equilibration even when populated with only very small numbers of buyers and sellers.

In many experimental economics studies, equilibration is not the only factor of interest. Another significant question is how much surplus is extracted from the market by the specific trading behaviors of the traders. In everyday language, surplus can be thought of a a seller’s profit or a buyer’s saving: if a seller has been given a limit-price of $10 per unit, but manages to agree a transaction at $15, then the $5 difference between the seller’s limit-price and the sale-price is that seller’s surplus, her profit; similarly if a buyer is given a limit-price of $10 but manages to instead buy for $8, then her saving, her surplus, is $2.

The initial experiments reported by Smith in 1962 were conducted with entirely manual issuing of assignments to traders, and with the traders simply shouting out their quote-prices in a laboratory version of an open-outcry trading-pit, a common sight on the trading floors of major exchanges for many decades prior to the arrival of automated market-trading technology. More recently, as in real financial exchanges, so in experimental economics: most experimental economics studies for the past 30 years or more have involved the human traders interacting with one another by each being sat at an individual trader-terminal (e.g. a PC running specialised trader-interface software, networked to a central exchange-server PC). The display-screen on a trader-terminal (whether in a real market or in a laboratory experiment) will often show a summary of all the currently outstanding bid-quotes received from buyers, and all the currently outstanding ask-quotes received from sellers, in a tabular form known as a Limit Order Book (LOB). Whole books have been written on the LOB (see e.g. Osterrieder, (2009); Nolte et al., (2014); Abergel et al., (2016)) but for the purposes of this paper, all we need to know is that the LOB allows all traders in the market to see the best (lowest) ask-price from a seller and the best (highest) bid-price from a buyer. In the rest of this paper I’ll use to denote the price of the best ask at time , and to denote the price of the best bid.

Any study in experimental economics where human traders interact with one another, via some market mechanism, subject to the constraints imposed by the design of the experiment, gives rise to the question of just how big a role the intelligence of the human traders plays in determining the market’s equilibration behavior. A genuinely shocking answer to that question was provided in 1993 by Gode & Sunder, also publishing in the JPE Gode and Sunder, (1993), who presented results which appeared to show that the answer was simple: zero. That is, Gode & Sunder showed that markets populated entirely by so-called zero-intelligence (ZI) traders could give rise to market dynamics, to equilibration behavior, which was statistically indistinguishable from that of human traders, when measured by the then-standard metric known as allocative efficiency, i.e. how much of the available surplus in the market was extracted by the traders. Gode & Sunder’s ZI traders manifestly have no intelligence at all, and are discussed in more detail in the next section.

3 Three ZI Trading Strategies

This section describes the three trading strategies Zero-Intelligence-Constrained (ZIC), Shaver (SHVR), and Giveaway (GVWY). As will be seen, all three of these can very reasonably be described as ZI trading strategies.

In the following text, is used to denote draws from a uniform random distribution over the range ; the integer denotes the market’s tick-size, the minimum price change allowed in the market (very often –but not always – one cent of the national currency in real financial exchanges, see e.g. Darley and Outkin, (2007); Chung et al., (2020); Chung and Chuwonganant, (2022); Cartea et al., (2022)); all prices are integer multiples of , and hence members of ; and and denotes the prices quoted by a buyer and a seller, respectively, at time , by a trader of strategy-type strat (where strat is one of a set of known strategy-types, for example strat {GD, ZIC, ZIP}). Note that a capital is used to denote a price that is (or could be, in principle) randomly generated, i.e. a random variable; and the various lower-case values are nonrandom. Time proceeds in discrete steps of , and each strategy is summarised as an equation that specifies the price that will be quoted by a trader at time on the basis of information available, the state of the market, at time . The limit-price assigned to a buyer is denoted by , and the seller’s limit-price is . The subscripted index is used where necessary to distinguish values that are specific to trader .

3.1 ZIC

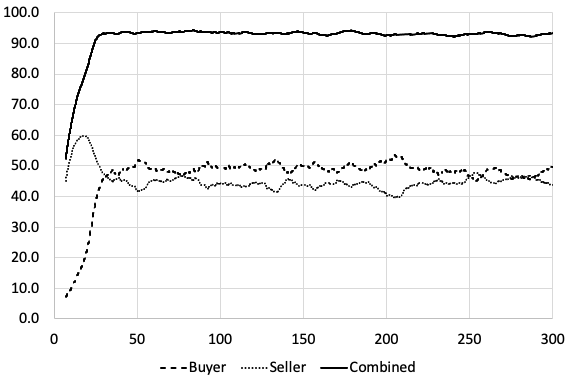

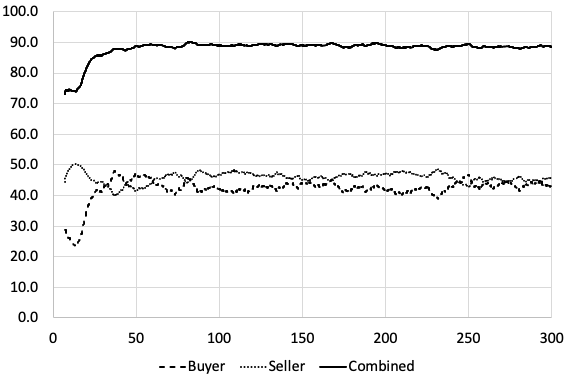

In their seminal 1993 JPE paper Gode and Sunder, (1993), Gode & Sunder presented results from three sets of experimental economics studies: in the first, groups of human traders interacted in an electronic CDA, the mechanism found in real-world financial markets, under laboratory conditions, as described above. As is commonplace in much experimental economics work, Gode & Sunder fixed the limit-quantity to one for all traders, so that transactions always involved a single unit of the asset changing hands, and hence the primary variable of interest was the transaction prices in the market. This first set of experiments established baseline data from the human traders, and Gode & Sunder recorded a key metric, , first introduced in Smith’s 1962 paper, which measures the variation of transaction prices around the market’s value, as the RMS difference between and the transaction prices over some period, i.e. is a measure of equilibration; and they also recorded the allocative efficiency for each market, which is a measure of how much of the total theoretically available surplus is actually extracted by the traders in that market.

In their second set of experiments, they replaced all the human traders with simple autonomous software agents that could electronically issue quotes to the market’s central exchange mechanism: as with the human traders in the first experiments, the software agents were each assigned a direction (buy or sell) and given a limit price for their transactions. Gode & Sunder performed two sets of experiments with these software agents: one set with a type of trader-agent that they named ZI-Unconstrained (ZIU); and another set with a modified version of the ZIU strategy, one that involved imposition of an additional constraint, and so those traders were named ZI-Constrained (ZIC). If ever a seller ZI trader issued a quote-price below the current best bid-price (i.e., in the terminology of financial markets, if the quote is for a price that crosses the spread), that seller sold its unit the buyer who had issued that best bid; and similarly if ever a ZI buyer issued a quote-price that was higher than the current best ask-price issued by a seller, the buyer would buy from that seller, because the buyer’s quote crossed the spread. (The spread is the difference between the current best ask price and the current best bid price).

ZIU traders were very basic: they generated a randomly-selected quote-price drawn from , where is an arbitrarily-chosen maximum-allowable price in the market. That is, ZIU traders were designed to ignore their limit prices. Unsurprisingly, the time-series of transaction prices in markets populated by ZIU traders looked much like random noise, and ZIU traders would often enter into loss-making deals, because they were buying at prices above their limit price or selling at prices below their limit price.

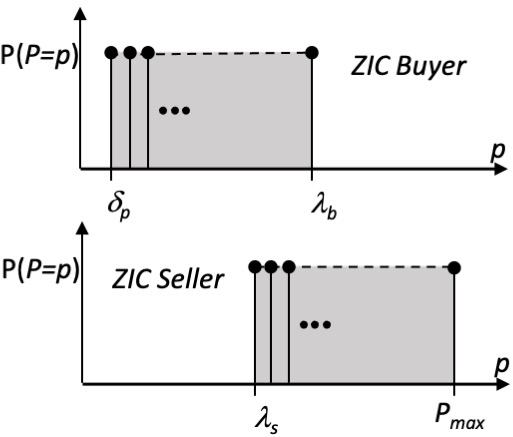

Gode & Sunder then modified the ZIU strategy, giving the ZIC strategy, by introducing a just one constraint: to not quote prices that were potentially loss-making. ZIC traders still quote random prices drawn from a uniform distribution over some range, but now there is a difference depending on whether the ZIC trader is a buyer or a seller:

| (1) |

| (2) |

That is, a ZIC buyer randomly generates its quote-prices equiprobably from , where is that buyer’s limit price; and a ZIC seller with limit-price generates its quote-prices equiprobably over the range . Surprisingly, markets populated by ZIC traders showed equilibration behaviors (as measured by Smith’s metric) and allocative effriciency scores that were virtually indistinguishable from the comparable human-populated markets. This notable result quickly became highly-cited, as it seemed to demonstrate that if there was any ‘intelligence’ in the system at all, it was in the CDA market mechanism rather than residing in the traders. Gode & Sunder were also careful to note that a different measure of surplus-extraction, called profit dispersion, was worse for ZIC traders than for human traders. .

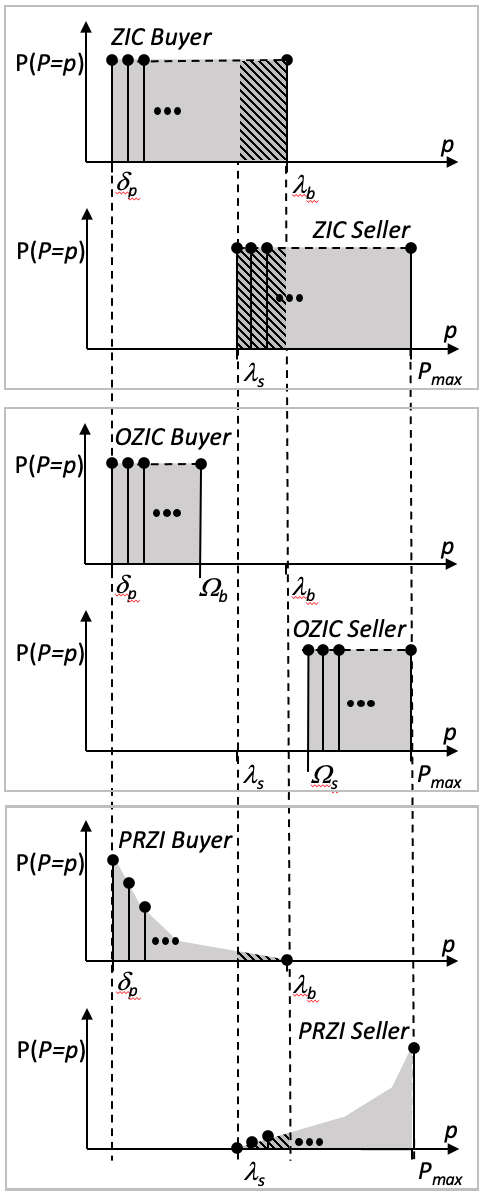

Because quote-prices in any market are quantized by that market’s tick-size , the prices quoted by a ZIC trader are samples of a discrete random variable, and the probability mass function (PMF) for that variable has a rectangular profile, because the distribution is uniform, as illustrated in Figure 1.

One problematic aspect of ZIC traders that becomes clear to anyone who actually implements them to run live in an operational market is that while ZIC buyers have a PMF domain that is bounded from below by the smallest nonzero price and bounded from above by the trader’s limit price , the PMF domain for a ZIC seller is bounded from below by its limit price but the upper bound is an arbitrary exogenous system limit , the highest price allowed in the market. In theory, might appear to be unimportant, but if its value is set to a large multiple of the largest buyer’s limit price then the ZIC sellers will spend an awful lot of their time quoting at prices , i.e. at prices that can never lead to a transaction, and so the market is flooded with unfulfillable ask-quotes, and you have to wait a long time before a ZIC seller just happens to randomly generate a plausible ask, i.e. one for which . If the only issue of interest in the market is the temporally-ordered sequence of transaction prices, this is not a problem; but if you care about the actual time intervals between successive transactions, that can be greatly affected by setting too high. Experimenters also need to be careful to ensure that is not set below the highest limit-price assignable to a seller in the market, which can be a problem in practice if the seller limit-prices are generated by an unbounded random-walk process such as geometric Brownian motion with positive drift. We’ll return to these issues, the “ problem”, in Section 4.

3.2 SHVR

Source-code for the Shaver strategy, abbreviated to SHVR, was made public in 2012 Cliff, (2012) when it was released as one of the several trader-agent strategies available in the Bristol Stock Exchange (BSE) which is a freely-available open-source simulation of a LOB-based financial exchange, written in Python. BSE was initially developed as a teaching resource, used by masters-level students studying on a Financial Technology module taught at the University of Bristol. In the years since it was first released, it has been used by hundreds of students and has increasingly also found use as a trusted and stable test-bed for exploring research questions in ACE.

Like ZIC, SHVR is minimally simple, involving no intelligence at all. Unlike ZIC, SHVR is entirely deterministic. SHVR can be explained very simply: a SHVR buyer sets its quote-price at time , denoted by , to be one tick (i.e., ) more than the current best bid , so long as that does not exceed its limit price , i.e.:

| (3) |

and similarly a SHVR seller sets its quote-price to be:

| (4) |

If the best bid or ask is undefined at time , e.g. because no quotes have yet been issued, a SHVR buyer will start with a very low , and a SHVR seller with a very high . If there is no prior trading data available in the market, the low value could be and the high value , i.e. the same lower and upper bounds as for ZIC traders; if there is prior trading data, the low and high initial values could instead be the lowest and highest prices seen in prior trading over some recent time-window.

SHVR was introduced to BSE as something of a joke, as a tongue-in-cheek approximation to a high-frequency trading algorithm. It does serve the purpose of being a minimal illustrative implementation of a trader that actually uses information available from the LOB. The surprising result (discussed in more detail in Rollins and Cliff, (2020); Cliff and Rollins, (2020)) is that if the circumstances are in its favour then SHVR can out-perform well-known strategies like ZIP or AA, which had previously been hailed as examples of AI-powered super-human robot-trader systems. And, in one further surprise, the same study that revealed SHVR can outperform ZIP and AA also revealed that an even simpler strategy, called GVWY, can do just as well as SHVR and sometimes better.

3.3 GVWY

Like SHVR, source-code for the Giveaway strategy (GVWY) was made public when the first version of BSE was released as open-source in 2012 Cliff, (2012). The correlates of Equations 3 and 4 for GVWY are as follows:

| (5) |

| (6) |

As can be seen, a GVWY trader simply sets its quote price to whatever its currently-assigned limit price is, regardless of the time. As the name implies, prima facie this trading strategy gives away any chance of surplus, because there is no difference between its quote price and its limit price: if its quote results in a transaction at that price, it yields zero surplus.

However, the spread-crossing rule (which is standard in most LOB-based markets) means that it is possible for a GVWY trader to enter into surplus-generating trades. For example, consider a situation in which a GVWY buyer has a limit price , and the current best ask is : when the GVWY buyer quotes its limit price (i.e., ), the $10 price on the quote crosses the spread and so the GVWY buyer is matched with whichever seller issued that best ask, and the transaction goes through at a price of $7, yielding a $3 surplus for the GVWY buyer (and yielding whatever surplus is arising for the seller, dependent on that seller’s value of ).

In the next section, I explain how PRZI traders have a continuously-variable strategy space that includes GVWY, ZIC, and SHVR: by setting a strategy-parameter to an appropriate value, PRZI traders will act either as one of those three ZI strategies, or as some kind of novel hybrid, intermediate between two of them; that is, a PRZI trader’s response is a parameterised version of one or more of these three ZI trading strategies, hence the name.

3.4 Summary

Table 1 summarises the three ZI strategies (GVWY, SHVR, and ZIC) that are integrated within PRZI, and also includes Gode & Sunder’s ZIU, for completeness.

| Buyer | Seller | |||

|---|---|---|---|---|

| Strategy | ||||

| GVWY | ||||

| SHVR | ||||

| ZIC | ||||

| ZIU | ||||

4 Parameterised-Response ZI Traders

4.1 Motivation

The initial motivation for developing PRZI came from a desire to give ZI traders a sense of urgency, of how keen they are to find a counterparty for a transaction. Intuitively, there is a tradeoff between time-to-transact and the expected surplus (profit or saving) on that transaction. In human-populated markets, over time, while working a trade, an individual buyer will typically announce increasing bid prices, in the hope that the better prices increase the chance of finding a counterparty seller to transact with, but each of those increases in the bid-price reduces the surplus that the transaction will generate for that buyer; the situation is the same for sellers, gradually reducing their ask prices, again in the hope that each price-cut makes it more likely that a buyer will come forward, but each cut slices away at the seller’s final profit for this transaction. In both cases, if the trader is urgent to get a deal done they can increase their chances of finding a counterparty by cutting their potential surplus, i.e. by making bigger step-changes in the prices that they’re quoting.

Lacking the intelligence of human traders, ZIC traders just issue their next quote price by drawing from a uniform distribution over a specified range of prices; for an individual ZIC trader, the change in price from one quote to the next may be positive or may be negative, and there is no control over the step-size. ZIC traders have no sense of urgency.

In contrast, a SHVR agent can be given some approximation to urgency: in Church and Cliff, (2019), SHVR was extended by applying a multiplying coefficient to the term in Equations 3 and 4, such that when the market circumstances dictate it, a value of allows SHVR to make larger step-changes in its quote prices. Work on PRZI started as a response to asking: how can we do something similar for ZIC?

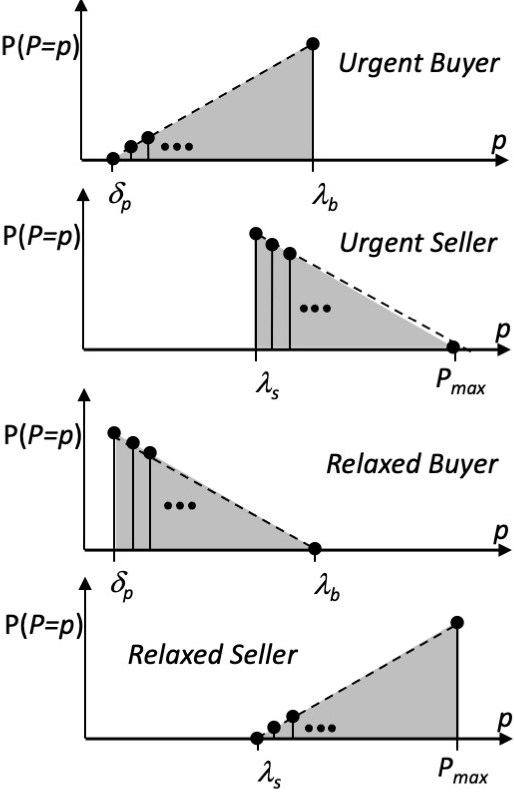

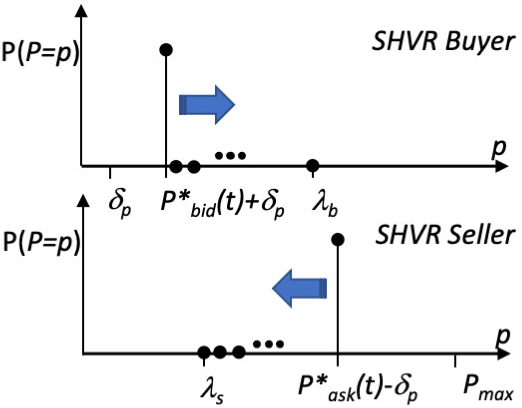

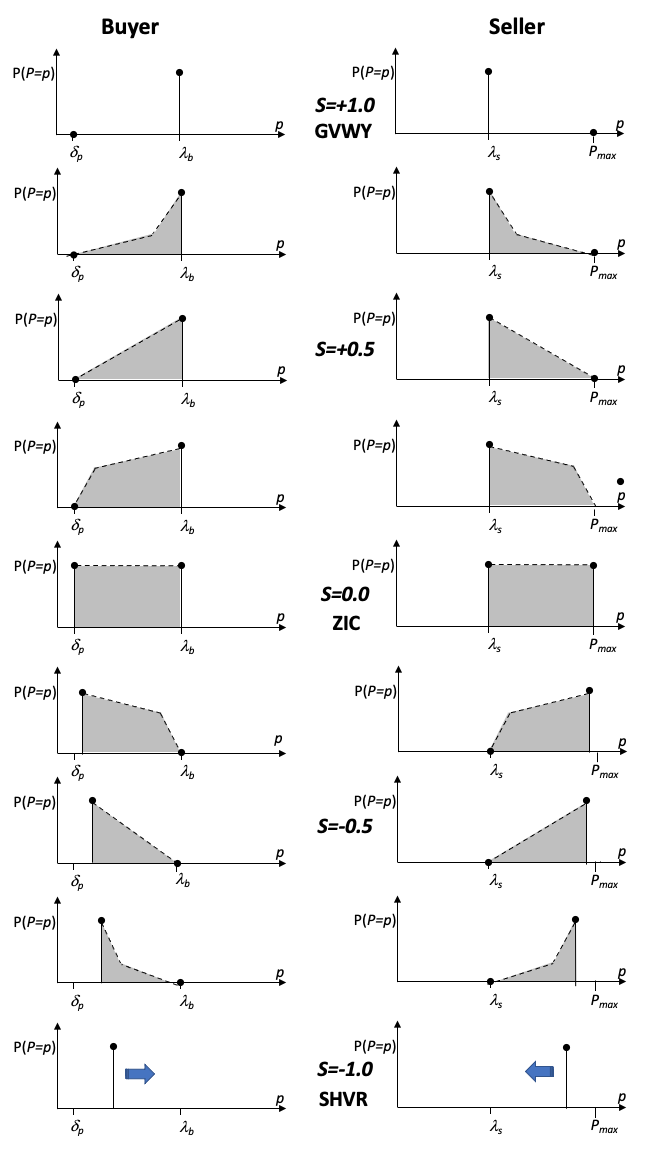

Figure 2 illustrates the reasoning underlying PRZI, when viewed as a way of making ZIC traders quote in a way that is more or less likely to lead to a transaction within any particular time-window: the rectangular PMF from the uniform distribution of the original ZIC can be replaced by a PMF that has either a right- or left-handed right-angled-triangle; depending on which way the triangle is oriented, the ZIC trader is either more or less likely to generate a quote-price that leads to a transaction. Let’s refer to these two right-triangle PMFs as the urgent and relaxed variants of ZIC.

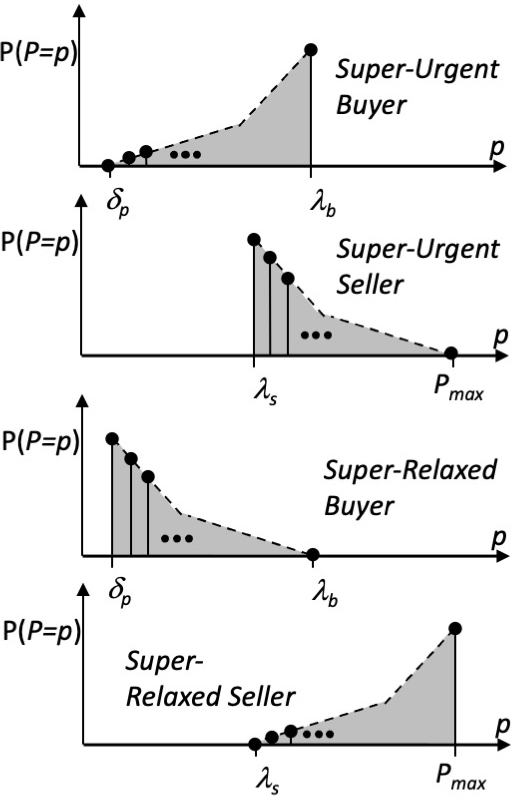

But why stop at these variants? Figure 3 illustrates two more extreme ZIC variants, where the PMF profile is nonlinear: let’s refer to these as the super-urgent and super-relaxed variants of ZIC.

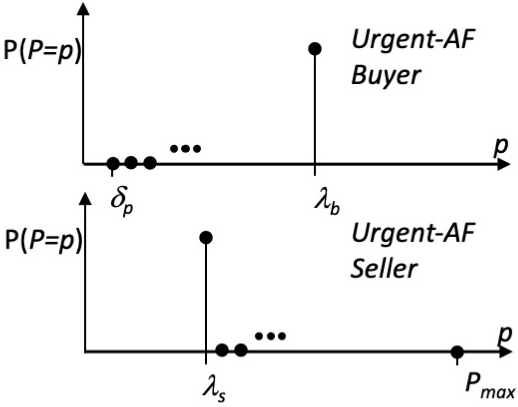

Clearly, the degree of nonlinearity in the variant-ZIC PMFs shown in Figure 3 could be made even more extreme, and eventually when the degree of curvature is at its most extreme the PMF would have only one price at nonzero probability: the price that had the highest probability in the triangular PMF. And, as there is only one price with nonzero probability, that probability must be one (i.e., 100%, total certainty). Let’s call these absolute extremes the urgent-AF and relaxed-AF (‘AF’ might stand for asymptotic form); they’re illustrated in Figures 4 and 5.

But the shapes of the urgent-AF PMFs in Figures 4 and 5 are familiar: the urgent-AF PMFs are simply a probabilistic representation of GVWY, because equations 5 and 6 can be expressed in (redundantly) probabilistic language as: with probability one, the price quoted by a GVWY trader is its current limit-price.

This then prompts the question: can a useful link be made from the relaxed-AF form of ZIC to SHVR? The PMFs of SHVR and relaxed-AF ZIC have essentially the same shape, the difference is in where they occur on the number-line of prices: SHVR as specified in Equations 3 and 4 quotes a price that is a one-tick (i.e. ) improvement on the current best price on the LOB; whereas a relaxed-AF ZIC would quote the most extreme price available, either the lowest nonzero price (i.e., ) for a buyer, or the arbitrary system maximum for a seller, neither of which is going to do anything at all to help equilibrate the market’s transaction prices. Because the relaxed-AF versions of ZIC would not equilibrate, it makes most sense to move the relaxed-AF price away from the most extreme value, and toward the best price on the LOB, as the degree of nonlinearity in the variant-ZIC PMF increases. This would mean that by the time the nonlinearity is maximally extreme, i.e. when the PMF has the -AF shape, the variant ZIC is doing the same thing as a SHVR.

And that is the motivation for creating PRZI: now all that is needed is a function that smoothly varies from the urgent-AF variant that is GVWY, on through the nonlinear super-urgent variant, on through the triangular-PMF of the urgent variant, then on to the original ZIC, then onwards to the triangular-PMF of the relaxed variant, and then on through the super-relaxed nonlinear PMF to the relaxed-AF PMF that implements SHVR: this progression is controlled by PRZI’s strategy parameter, denoted by , as illustrated in Figure 6.

4.2 Details

The various seller PMFs shown in Figure 6 have a domain that is bounded from below (the left-hand limit of the PMF) by the individual seller’s limit-price , but the upper bound on that domain, the right-hand limit of the PMF, brings us back to “the problem” discussed previously in Section 3.1. Each PRZI seller addresses this problem by determining its own private estimate of the highest plausible price, denoted by , according to the following set of heuristic criteria:

-

•

If the PRZI seller has no other information available to it (e.g., it is the start of the first session in a market experiment, and the LOB is empty) then the only available information it has is the highest limit price it has been assigned thus far, denoted by (and if it has not been assigned a limit price, it is unable to participate in the market). In this situation, the PRZI seller sets for some coefficient . Informally, this models a naive and uninformed seller making a wild guess at the highest price that the market might tolerate. Different sellers can have different values of – that is, some might guess cautiously while others might be much more optimistic.

-

•

If ever another seller issues an ask-quote at a price then seller sets . Informally, this models a seller realising that her current best guess of the highest price the market will tolerate was too low, because there is some other seller in the market who has quoted a higher price.

In principle, if reliable price information is available from an earlier market session, then that information could be used instead. However, in any one previous market session there are likely to be multiple potential candidate values (e.g: the highest ask-price quoted in that session, or the highest transaction-price in that session, or the final transaction price, or the linear-regression prediction of the next transaction price in the market, or a nonlinear prediction, and so on), and that would soon take us away from the appealing minimalism of ZI traders.

This approach, of letting each seller form its own private estimate of the highest tolerable ask-price could be criticised as merely swapping one arbitrary system parameter (the global constant ) for a bunch of new arbitrary exogenously-imposed parameters (the set of individual values, one per trader). If all we care about is minimising parameter-count, that would be a valid criticism. However, this approach has the advantage that only uses information that is locally available to an individual trader (i.e., it does not require knowledge of a system-wide constant) and it never requires manual re-calibration to the highest price in the market’s supply curve. In practice setting the values at random over a moderate range is sufficient to generate useful results: the results presented here used ; this makes it unlikely that all traders will have the same value, and the fractional exponent gives a nonlinear bias toward smaller values.

Finally note that, if introduced alone, this solution to the problem can give rise to behavioral asymmetries between PRZI buyers and sellers when , (i.e., SHVR-style strategies) because PRZI buyers still have the lower-bound of their PMF set to the system minimum price . That is, unlike the sellers, the buyers are not using some multiple of their lowest limit-price or any prices observed in the market to form their initial lowest bid-price. To illustrate the problem, consider a market populated entirely by PRZI traders all with and in which the supply and demand schedules are set such that the equilibrium price is a large multiple of relative to the number of buyers: the sellers, no longer limited by having to start their quotes at some arbitrary system maximum price, will drop their quote prices to near-equilibrium values relatively quickly, but in contrast the SHVR-style buyers will start by quoting , then , then and so on, potentially making much slower progress toward the equilibrium if that lies at, say, : there is, in this sense, also a problem. To counter this, PRZI buyers can set their in the same style that PRZI sellers set their : initially using in the absence of any other information, and using the lowest price quoted by another buyer if that quote is less than ’s initial value.222To illustrate the behavioral asymmetry that arises when the problem is not remedied in this way, in all the experiments described in Section 6.3, the PRZI buyers simply use the original ZIC-style : the strategies of the buyer population then consistently diverge from those of the sellers. This nevertheless does yield rich co-evolutionary dynamics, serving to illustrate issues in the visualization and analysis of such high-dimensional co-evolutionary systems.

As described thus far, we have a method for setting the upper limit of the PRZI seller PMF when , i.e., for the PRZI range of strategies from ZIC to GVWY. However, for the seller-case that implements SHVR, we need the upper limit of the PMF to be set such that , and we need to get there smoothly from the case where PRZI is implementing ZIC and and are set by the method just described. The simplest way of doing that is to have be a linear combination of the two. For a PRZI seller, let denote the value at , then for we use:

| (7) |

and the same form of linear combination for PRZI buyers, to pull the lower limit on the buyer PMFs progressively away from . In extremis, this approach will narrow the PMF interval to just a single discrete price, i.e. , generated with probability one.

Next, let denote the strategy-value for trader ; and let and be the bounds on trader ’s discrete-valued price-range , with and let the extent of that range be . Also define a price-range normalization function :

Then note that over the domain , the function in Equation 8 has the right profile, makes the right shapes, for the buyer PMFs that we want (as were illustrated in Figure 6):

| (8) |

where

| (9) |

and is the linear-rectifier threshold function symmetrically bounded by a cutoff constant , which also (to avoid divide-by-zero errors) clips near-zero values at for some sufficiently small value of (e.g ):

| (10) |

and then finally use:

| (11) |

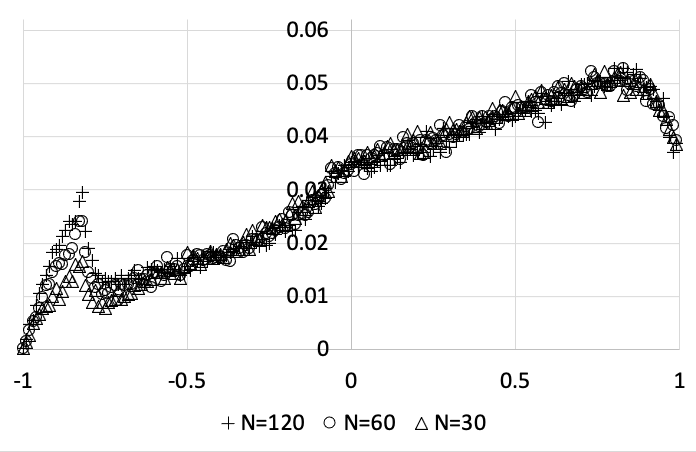

After a little trial-end-error exploration, it was found that values for the constants and give the desired shapes, i.e. similar to the qualitative PMF envelopes illustrated in Figure 6: these are illustrated in Figure 7. Also, turning the envelope into a usable PMF requires scaling and normalisation such that:

| (12) |

From this we can then compute the cumulative distribution function (CDF) for trader as which is defined over the domain as:

| (13) |

The CDF in Equation 13 maps from its domain to cumulative probabilities in the interval : for each of the discrete points in the domain, exact values of can be computed and stored in a look-up table (LUT). It is then simple to use reverse-lookup on the LUT to give an inverse CDF function such that:

| (14) |

Separate versions of need to be generated for buyers and sellers, which will be denoted by subscripted parenthetic and characters, and can then be fed samples from a uniformly distributed pseudo-random number generator to produce quote-prices for PRZI traders:

| (15) |

| (16) |

5 PRZI Implementation

A reference implementation of PRZI written in Python 3.8 has been added to the BSE sourcecode repository on GitHub Cliff, (2012). For ease of intelligibility, the implementation follows the mathematics laid out in the previous section of this paper, computing an individual LUT for each trader: this approach is conceptually simple, but is manifestly inefficient in space and in time. To illustrate this, consider the case where all traders in the market have the same value for their PRZI strategy parameter, and all sellers are assigned the same limit price and all buyers the same : in such a situation, only two LUTs are needed: one to be shared among all buyers, and another to be shared among all sellers; but the current implementation wastes time and space by blindly computing an entire LUT for each trader. A more efficient implementation could be built around compiling any one LUT for a particular instance of an triple only once, when it is first required, and storing it in some central shared key-value store or document database where the triple is the key and the LUT is the associated value or document. This would be considerably less inefficient, but would add considerably to the complexity of the code. As the Python code in BSE is intended to be simple, as an illustrative aid for non-expert programmers, the current BSE implementation does not use this approach.

6 Example Use-Cases

Section 1 listed three motivations for developing PRZI: to provide a mechanism for ZI traders to give a market-impact response; to enable ZI traders to be opinionated, thereby enabling the creation of ACE models exploring matters arising from Shiller’s notion of narrative economics; and to facilitate the study of coevolutionary dynamics in markets populated by adaptive agents that can smoothly vary their trading strategies through a continuous space. Here I briefly summarise current work-in-progress on all three of those fronts, in sequence.

6.1 PRZI as a Generator of Market-Impact Responses

In Church and Cliff, (2019) I introduced an altered version of the SHVR zero-intelligence trader strategy that is extended to be imbalance-sensitive, altering its behavior in response to instantaneous imbalances in market supply and demand, thereby giving ZI-populated ACE models in which the population of traders exhibit a market-impact effect. Market impact is here defined as the situation where the prices quoted by traders in a market shift in the direction of anticipated change in the equilibrium price, before any transactions have occurred, where the coming change in equilibrium price is anticipated because of an imbalance in the orders in the market, a sudden shift to excess demand or supply; and where it’s safe to assume that actual market transaction prices are typically close to the equilibrium price. For an extensive and insightful analysis of market impact in financial markets, see Farmer et al., (2013). As the basic SHVR was made sensitive to imbalance for the purpose of market impact, the extended SHVR was named ISHV (pronounced “eye-shave”). Here I briefly show how exactly the same mechanism developed for ISHV can be used to create an impact-sensitive version of PRZI, which I’ll refer to as IPRZI.

ISHV’s impact-sensitivity is based on the difference between the current market mid-price, denoted here by , and the current market micro-price, denoted here by , where

| (17) |

in which is the price of the best ask at time – i.e., it is the price at the top of the bid-side of the CDA market’s limit order book (LOB); is the price of the best bid at time – i.e. the price at the top of the ask side of the LOB; is the total quantity available at ; and is the total quantity available at . Equation 17 is how the micro-price is defined by Cartea et al., (2015).

When there is zero supply/demand imbalance at the top of the LOB (i.e., ), Equation 17 reduces to the equation for the market mid-price, and hence the difference between the two prices, denoted by , is zero. However if then the imbalance indicates that subsequent transaction prices are likely to increase (which should increase urgency in IPRZI buyers, and reduce it in IPRZI sellers); and if then the indication is that subsequent transaction prices are likely to fall (so IRPZI sellers should increase urgency, while buyers relax). The mapping from to IRPZI -value is achieved by giving each IPRZI trader an impact function, denoted here by , such that and . This form of IPRZI was recently implemented by my student Owen Coyne in his Masters thesis Coyne, (2021).

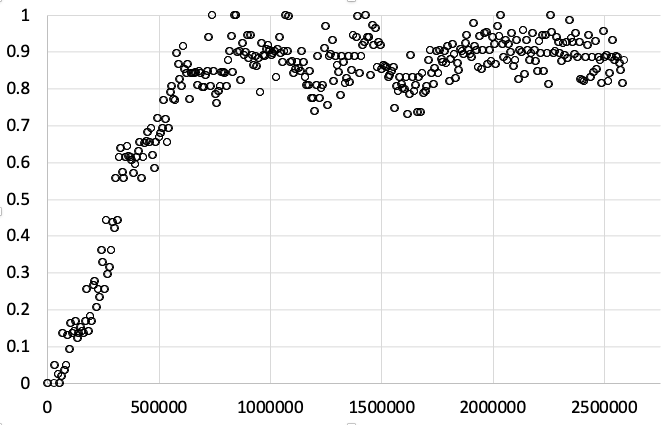

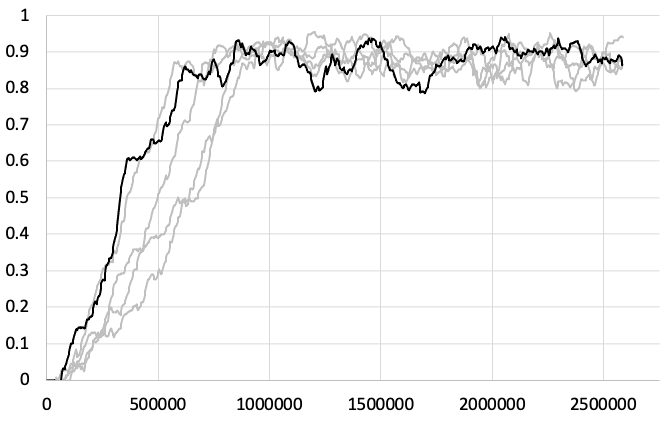

As illustration, Figure 9 shows the change in strategy of an IPRZI buyer when it reacts to a sudden change in imbalance, a sudden injection of excess demand at the top of the LOB.

This version of IPRZI is the simplest to articulate, but it suffers from the vulnerability that Equation 17 is sensitive only to imbalances at the very top of the LOB – any imbalance at deeper levels of the LOB is simply ignored, and hence this is quite a fragile measure of imbalance. This is discussed at more length by Zhang and Cliff, (2021) who instead use multi-level order-flow imbalance (MLOFI) as a more robust imbalance metric. Briefly, MLOFI is a specific implementation of the novel findings of Cont et al., (2021) who used a principal component analysis of order-flow imbalance (i.e., whether the number/amount of buy orders submitted to the exchange/LOB is in balance with the number/amount of sell orders, or not) to show that taking into account multiple levels of the LOB when defining order-book supply/demand imbalance leads to higher explanatory power for the short-term predictions of market-impact price movements. It is straightforward to extend IPRZI by replacing the ISHV-like method described here with the MLOFI method developed by Zhang & Cliff, thereby making IPRZI more robustly sensitive to order imbalances: early results from exploring this approach are presented in Cliff et al., (2022).

6.2 PRZI as Opinionated Traders

Lomas & Cliff Lomas and Cliff, (2021) describe results from extending two well-known types of ZI trader, Gode & Sunder’s ZIC Gode and Sunder, (1993) and Duffy & Ünver’s NZI Duffy and Ünver, (2006), where in both cases the extension adds an opinion variable to each trader. This forms a novel intersection between work on ZI traders and work in opinion dynamics (see e.g. Krause, (2000); Meadows and Cliff, (2012, 2013). Lomas & Cliff prefix the ZIC and NZI acronyms with an O (for ‘opinionated’) to give OZIC and ONZI. As was discussed in Section 1 of this paper, Lomas & Cliff’s work was motivated by the desire to develop ZI-trader agent-based models (ABMs) in the ACE tradition that would facilitate study of Shiller’s recent notion of narrative economics Shiller, (2017, 2019); and one of the motivations for developing PRZI was to address some deficiencies in the original OZIC model.

To recap, in brief: Shiller argues that traditional economic analyses too often under-emphasise (or wholly ignore) the extent to which the buying and/or selling behavior of agents within a particular market-based system is influenced by the narratives (i.e., the stories) that the agents tell each other – and themselves – about the past, present, and future states of that market system: if the narratives that the agents are telling each other are consistent with conventional economic theory, then there is nothing much to report; but if the stories in circulation run counter to the predictions of theory, then sometimes the actual market outcomes are difficult or impossible to explain by reference only to those factors favoured in orthodox economic analyses. Shiller’s 2019 book discusses at length the extent to which the phenomenal rise in prices of cryptocurrencies such as Bitcoin is much better explained by reference to the narratives circulated and believed by the active participants in the markets for such crypto “assets” than it is by any conventional analysis or estimates of ultimate value.333Shiller’s 2019 book pre-dates the explosive rise of trading in blockchain-backed non-fungible tokens and the roller-coaster price gyrations in “meme stocks” such as GameStop (see e.g. Jakab, (2022)) and hence now seems ripe for a second edition, or at least for an epilogue to the first edition. Schiller argues for an empirical approach to studying narrative economics: gathering as much data (e.g., records of the texts of news-articles and social-media discussions) as is practicable about the narratives circulating among agents in real economic systems, and then tying analysis of these narratives to analyses of the actual market dynamics and eventual outcomes. As Kenny Lomas and I argued in Lomas and Cliff, (2021), what Shiller proposes is solely an a posteriori analysis of the roles of narratives in economics systems, but there is an alternative approach, which is to build constructive models of economic systems in which narratives are an important factor, using ZI/MI ABM/ACE methods. This can be done by recognising that what Shiller describes as narratives are nothing more than the external expressions, the verbalizations, of agents’ internally-held opinions, and hence that issues in narrative economics can be studied by developing ABMs in which the trader-agents each hold an opinion that can to some extent influence the opinion of other traders in the system, and that can in turn to some extent be influenced by the opinions of other agents that the agent interacts with; so long as each agent’s opinion then also to some extent influences its economic behavior, the overall ABM can act as a test-bed for exploring aspects of narrative economics, in much the same way as laboratory experiments involving a few tens of human subjects acting as traders in a CDA can provide genuine insights on the dynamics of real financial markets. The Lomas and Cliff, (2021) paper was our first report on extending ZI/MI traders so that they also held opinions that not only influenced their own trading behaviors but also could influence the opinions of other traders too; but, as is the case with very many exploratory first-attempts, analysis of our initial results revealed problems that needed to be addressed in further work.

Figure 10 illustrates the problem with OZIC traders that PRZI is intended to remedy: OZIC uses the value of the trader’s opinion variable to set an opinionated limit price (here denoted by ) which becomes a bound on the trader’s PMF, introducing a region on the PMF between and the trader’s original limit price in which the PMF is at the zero probability level, rather than at the positive uniform-probability level that it would be in a ZIC trader. While this does give a desirable link between the trader’s opinion and the prices that it can quote, it is too easy for the opinion-dependent ranges of zero-probability in the buyer and seller PMFs to eliminate the overlap that is required for there to be any likelihood of the randomly-generated ZIC quote-prices crossing and leading to transactions. When this happens, each side issues quotes that are unacceptable to the counterparty side, and the market simply grinds to a halt, with traders on both the buyer-side and the seller-side quoting prices that their respective counterparty side can no longer transact at.

This problem is at its most acute if the supply and demand schedules are each perfectly elastic as used e.g. by Smith, (1965) (in this case both the supply and demand curves are horizontal and flat over the range of available quantities, giving a graph of the supply and demand curves that various authors have referred to as swastika- or box- shaped: see e.g. Smith, (1994)). As illustration, consider such a perfectly elastic pair of schedules and assume the best-case overlap in buyer and seller PMFs such that all buyers have the same limit price that is set to the system maximum price ( in Lomas & Cliff’s terminology, or here) and all sellers have the same limit price that is set to the system minimum price ( in Lomas & Cliff’s terminology, or here). It is easy to prove that in these circumstances, if the market is populated entirely by OZIC traders and each trader holds a neutral opinion (i.e. have zero for their opinion value) then the buyer and seller PMFs cease to overlap for all traders; at which point – given that we’re talking about a situation in which all buyers have the same PMF and all sellers have the same PMF – transactions cease to occur.

This issue in OZIC is a consequence of what could be characterised as the binary thresholded nature of OZIC’s implementation of opinion-influenced quote-price generation: the PMF for an OZIC is starkly divided into two zones by the trader’s current value of : in one zone the PMF is a simple uniform distribution (as in ZIC) and in the other the PMF is a constant zero. PRZI’s smoothly-varying PMFs obviate this problem because they allow a graded response, with probabilities being reduced to much lower values in the OZIC “zero-zone” than in the OZIC “uniform zone” while maintaining a nonzero possibility of a transaction actually occurring.

As in Lomas & Cliff’s work, here we give PRZI traders a real-valued opinion variable, denoted here as for trader , s.t. where negative values of represent the opinion that prices are set to fall, and positive values represent the opinion that prices will rise. The linkage between and the PRZI -value is straightforward: if trader ’s opinion is that prices will rise, then if is a buyer it needs to bias its PMF toward urgency but if it is a seller then the rational thing to do when prices look set to rise is to bias the PMF toward relaxed; and if the trader’s opinion is that prices will fall, similar reasoning applies mutatis mutandis.

As should by now be obvious, we need some function that maps from trader ’s opinion to its PRZI strategy , i.e. . In the very simplest case, given that both and , the mapping can be the identity function, or the negative of the identity function, depending on whether is buyer or a seller. For a seller, the simplest is identity: ; . For a buyer, the simplest is negative identity: ; . However this fairly rapidly moves the trader’s strategy to extremes (either SHVR or GVWY) as , which may not always be desirable: instead, some nonlinear mapping resembling a logit/probit function is generally a better choice for .

The link provides between and is, as stated thus far, necessary but not entirely sufficient: it provides a linkage between a trader’s opinion and its PRZI strategy, and if this work was conducted in the manner familiar from much of the opinion dynamics (OD) literature, that would be sufficient, because a lot of research in OD has been directed at the study of shifts in opinion among a population of agents where the only factor that might change an individual’s opinion is some set of one or more interactions with one or more other agents in the population. That approach makes sense if the opinions being modelled are solely matters of individual subjective choice, such as personal religious or political views, where there is no external referent, no absolute ground truth that could prove the individual’s opinion to in fact be wrong. But in financial markets there is a ground truth: the actual dynamics of the actual market; actual prices, actual volumes. If an entire population of agents believes that the price of some asset will rise tomorrow, that can be a self-fulfilling prophecy because all traders will act in a way consistent with the collective belief (this takes us onto the well-trodden path toward sunspot equilibria Cass and Shell, (1983) and all the way back to Merton’s classic work in the 1940’s e.g. Merton, (1948)).

However if half the population believes that the price will rise while the other half believes it will fall and the next day the price does actually rise, then half the population got it wrong and may need to revise their faith in their own opinions to reduce the mismatch between their opinions and the ground truth. Given that another motivation for designing PRZI, another use-case (as discussed in Section 6.1), was to explore market-impact effects by giving PRZI traders a sensitivity to supply/demand imbalances, currently I’m working with students to explore ABMs in which the PRZI trader’s opinion-value is influenced by an appropriate mix of its OD-style interactions with other agents in the population, and its analysis of the currently observable market situation (e.g. its calculation of simple imbalance metrics such as the ISHV-style value, or MLOFI). In the spirit of ZI and minimal-intelligence modelling, a simple weighted linear combination of the two is as good a place to start as any, but this is a rich seam for further research with many alternative approaches to explore.

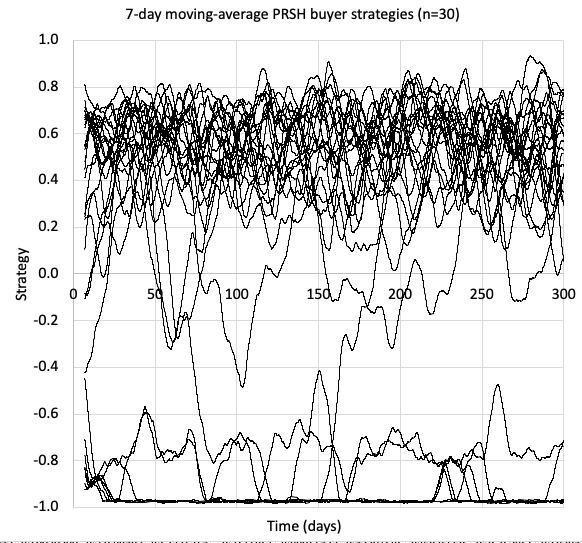

6.3 Co-evolutionary Dynamics in Markets of Adaptive PRZI Traders

The continuously-variable strategy parameter in PRZI allows for studies of co-evolutionary dynamics in markets populated entirely by adaptive ZI agents. To do this, we need to set up markets populated entirely by PRZI traders where each individual trader can alter/adapt its value in response to market conditions, always trying to fine-tune it to generate higher trading profits.

Doing this will then provides a ZI-style ABM/ACE test-bed for exploring issues in evolutionary economics – the adaptive PRZI traders are manifestly engaged in a form of evolutionary game, each adapting their strategies over time to try to maximise their local measure of fitness, a topic explored extensively (although not always using exactly that terminology) since the dawn of economics, predating even von Neumann and Morgenstern, (1944): see for example the reviews by Friedman, (1991); Blume and Easley, (1992); Friedman, (1998); Lo, (2004, 2019); Nelson, (2020).

If we were to allow only a single PRZI trader to adaptively vary its value, trying to find the best setting of relative to whatever distribution of values is present in the market (i.e., relative to the current mix of other strategies in the market) then we could say that is evolving its value of to try to find an optimum, the most profitable setting for its strategy parameter, given the unchanging set of fixed strategies that it is pitted against in the market. But when every PRZI trader in the market is simultaneously adapting its -value, the system is co-evolutionary because what is an optimal setting of the parameter for any one trader will likely depend on the -values currently chosen by many or perhaps all of the other traders in the market. That is, the profitability of is dependent not only on its own strategy value but also on many or perhaps all other values in play at any particular time, and in principle all the strategy values will be altering all the time.

A primary motivation for studying such co-evolutionary markets with adaptive PRZI traders is the desire to move beyond prior studies of markets populated by adaptive automated traders in which the “adaptation” merely involves selecting between one of typically only two or three fixed strategies (as in, e.g., Walsh et al., (2002); Vytelingum et al., (2008); Vach, (2015). The aim here is to create minimal model markets in which the space of possible ZI strategies is infinite, as a better approximation to the situation in real financial markets with high degrees of automated trading.

Prior researchers’ concentration on markets in which the traders can choose one of only two or three fixed strategies can be traced back to the sequence of publications that launched the trading strategies MGD, GDX, and AA (i.e., Tesauro and Das, (2001); Tesauro and Bredin, (2002); Vytelingum et al., (2008)), and the papers in which these strategies were shown to outperform human traders (i.e., Das et al., (2001); De Luca and Cliff, 2011a ; De Luca and Cliff, 2011b ). All of these works relied on comparing the strategy of interest with a small number of other strategies in a series of carefully devised experiments. For example, GDX was introduced in Tesauro and Bredin, (2002), and was compared only to ZIP and GD.

In aiming for a fair and informative comparison, experimenters were immediately faced with issues in design of experiments (see e.g. Montgomery, (2019)): how best to compare strategy with strategies and (and and and so on), given the finite time and compute-power available for simulation studies, and the need to control for the inherent noise in the simulated market systems.

Early comparative studies such as Das et al., (2001) limited themselves to running experiments that studied the performance of a selection of trading strategies in three fixed experiment designs: homogeneous (in which the market is populated entirely by traders of a single strategy-type); one-in-many (OIM: in which a homogeneous market was altered so that all the traders were of strategy type except one, which was of type ); and balanced-group (BG: in which there was a 50:50 split of and , balanced across buyers and sellers, with allocation of limit-prices set in such a way that for each trader of type with a limit price of there would be a corresponding trader of type also assigned a limit price of ). There were good reasons for this experiment design, and the results were informative, but they rested on only ever comparing two strategies and in markets with a total number of traders where the ratio of : was one of either : (i.e., homogeneous); or : (i.e., OIM); or : (i.e., BG). This approach left open the question of whether the performance witnessed in one of these three special cases generalised to other possible ratios, other relative proportions of the two strategies in the market.

A method by which that open question could be resolved was developed by Walsh et al., (2002) who borrowed the technique of replicator dynamics analysis (RDA) from evolutionary game theory (see e.g. Maynard Smith, (1982)). In a typical RDA, the population of traders is initiated with some particular ratio of the strategies being compared, and the traders are allowed to interact in the market as per usual, but every now and again an individual trader will be selected via some stochastic process and will be allowed to mutate its current strategy to one of the other available strategies if that new strategy appears to be more profitable than . In this way, given enough time, the market system can be started with any possible ratio of the strategies, and in principle it can evolve from that starting point through other system state-vectors (i.e., other ratios of the strategies) to any other possible ratio of those strategies. However in practice the nature of the evolutionary trajectories of the system, i.e. the paths traced by the time-series of state-vectors of the system, will be determined by the profitability of the various strategies that are in play: some points in the state-space (i.e., some particular ratios of strategies) will be unprofitable repellors, with the evolutionary system evolving away from them; others will be profitable attractors, with the system converging towards them; and if the system converges to a stable attractor then it’s at an equilibrium point, or potentially on a repeating sequence of equilibrium points, i.e. a limit cycle. Walsh et al’s 2002 paper showed the results of RDA for market systems in which , comparing the trading strategies GD, SNPR, and ZIP, and visualised the evolutionary dynamics as plots of the two-dimensional unit simplex, an equilateral triangular plane with a three-variable barycentric coordinate frame.

Similar plots of the evolutionary dynamics on the 2D unit simplex were subsequently used by other authors when comparing trading strategies: see e.g. Vytelingum et al., (2008); Vach, (2015), and those authors also limited themselves to studies in which the traders in the market could switch between one of only different discrete strategies. And, in this strand of research, three-way comparisons seem to then have become the method of choice primarily because evolutionary trajectories through state-space, and the location and nature of any attractors and repellors on the space, is readily renderable as a 2D simplex when dealing with a system, but rapidly gets very difficult, to the point of impracticability, as soon as . Higher-dimensional simplices are mathematically well-defined, but very difficult to visualise: the four-variable simplex is a 3D volume, a tetrahedron; and more generally the -variable simplex is an -dimensional volume – so if we wanted to study the evolutionary dynamics of a six-strategy system, we would need to find a way of usefully rendering projections of the 5-D simplex, or we need to find alternative methods of visualisation and analysis.

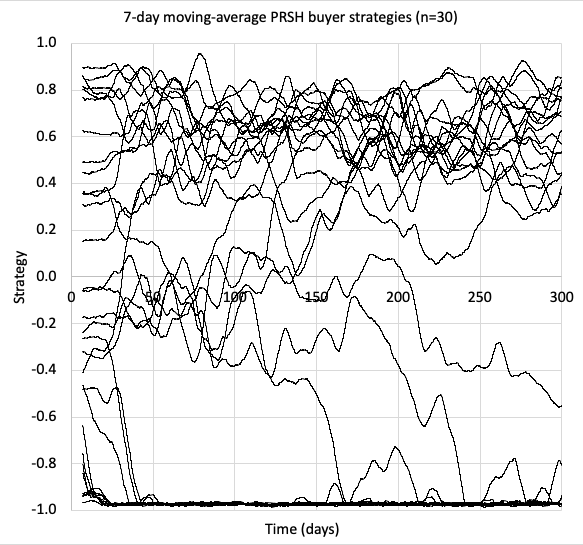

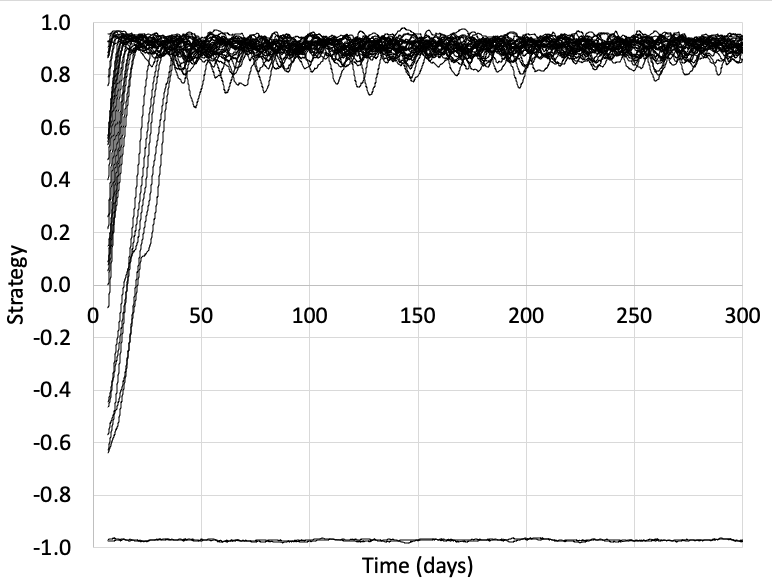

However, as first shown by Vach, (2015) and later confirmed in more detailed studies by Snashall and Cliff, (2019); Rollins and Cliff, (2020) and Cliff and Rollins, (2020), when the complete state-space of all possible ratios of discrete strategies is exhaustively explored, the dominance hierarchies indicated by the simple OIM/BG analyses are sometimes overturned. That is, if strategy outperformed strategy in both the and the tests, that would usually be taken as evidence that generally outperformed , that was “dominant” in that sense; but actually if markets were set up with some ratio of : other than the OIM or BG ratios, then in those markets would dominate – that is, the direction of the dominance relationship between and can often depend on the ratio of :, their relative proportions of the overall population. Furthermore, while might dominate in two-strategy experiments (i.e., where ), plausibly would dominate in experiments where values of : the indications are that as yet there is no single master-strategy that dominates all others in all situations; what strategy is best will depend on the specific circumstances.

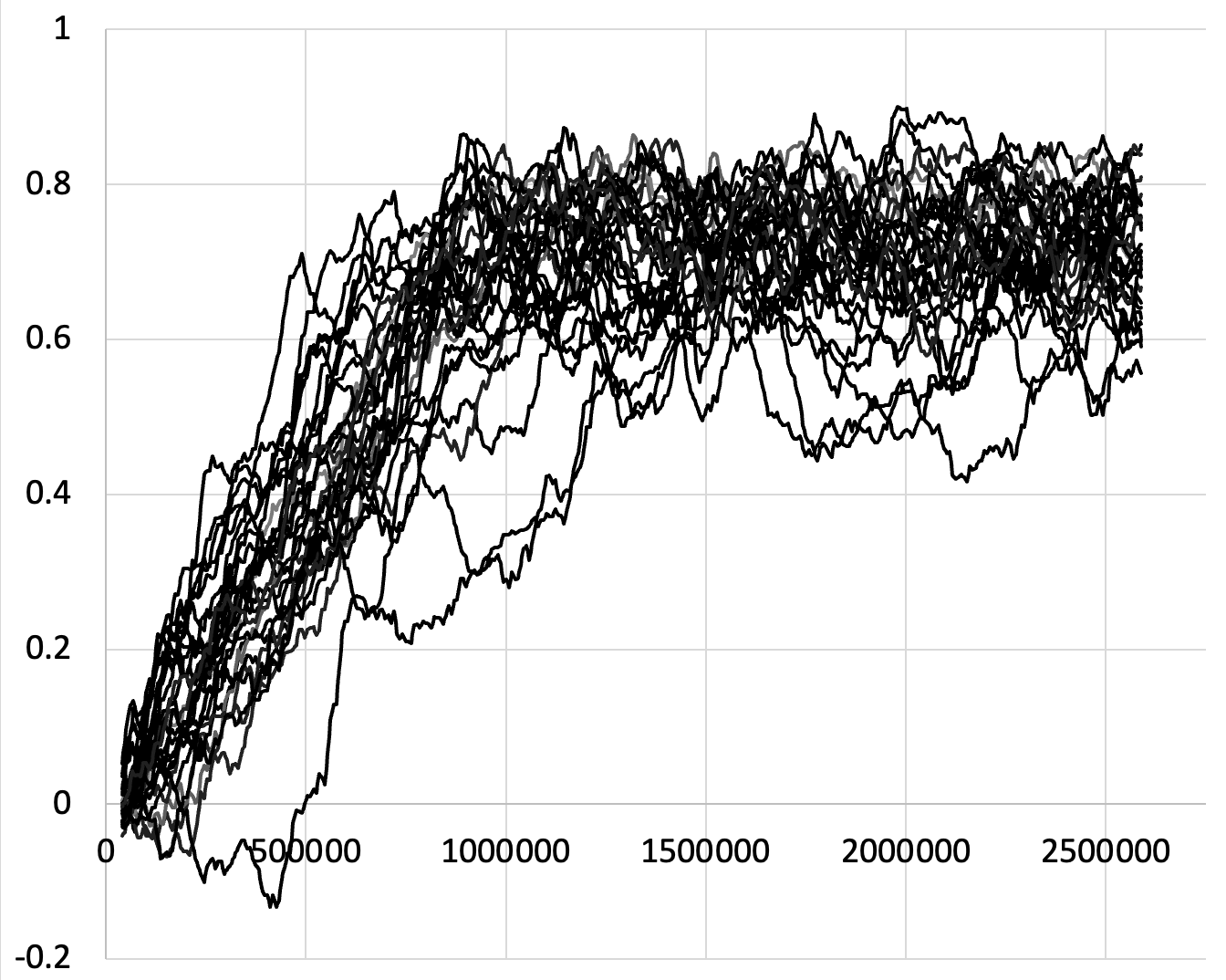

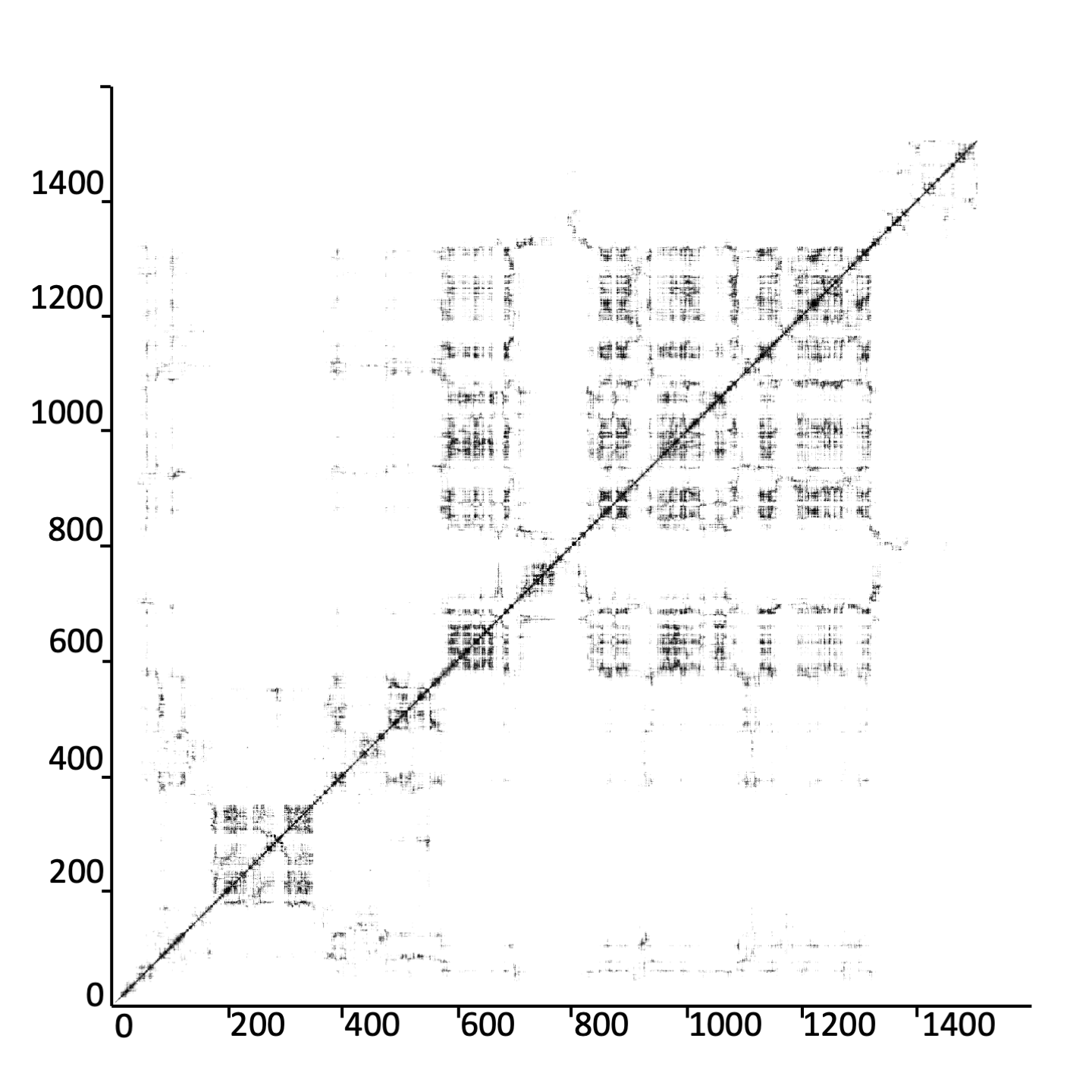

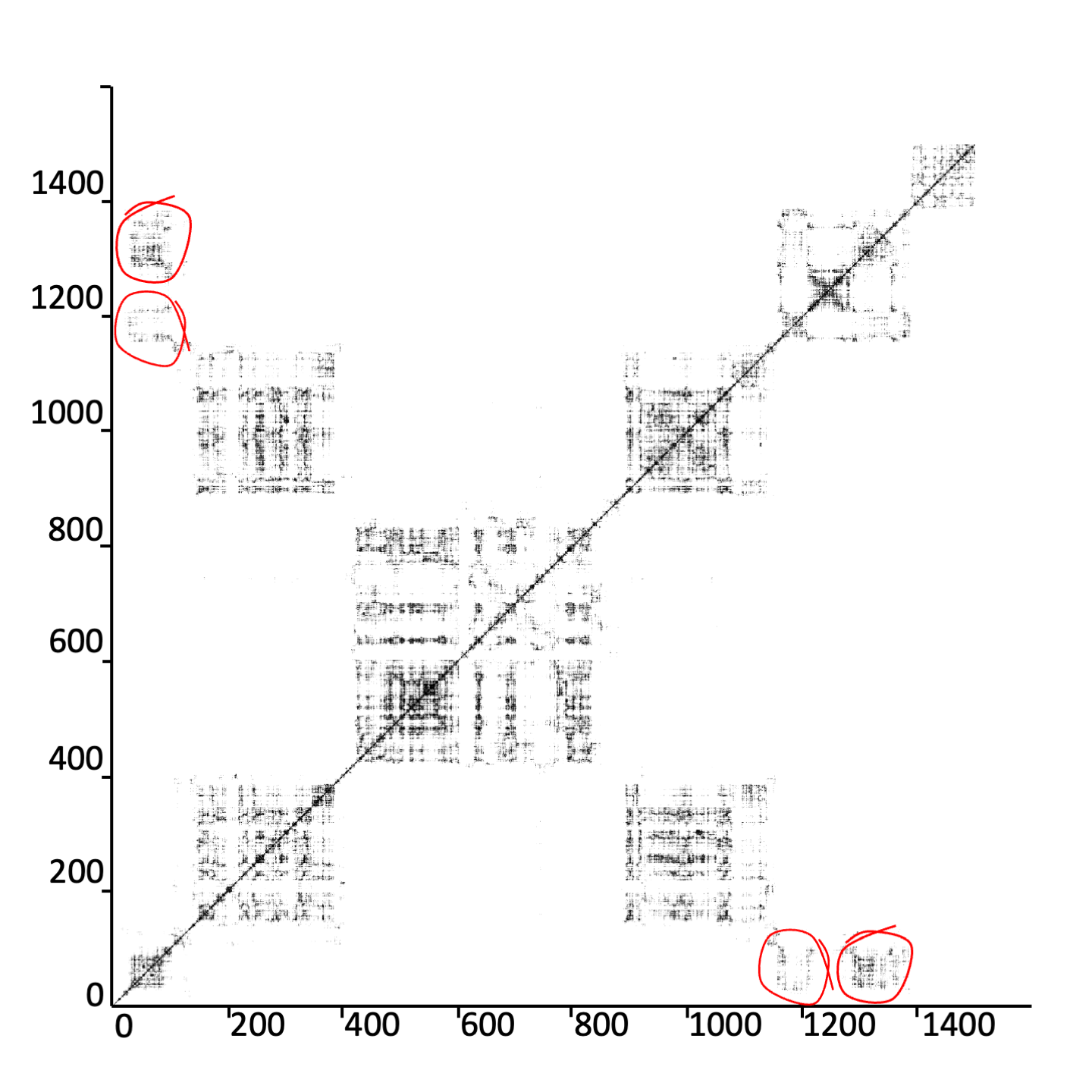

By populating a model market entirely with adaptive PRZI traders we create a minimal test-bed for exploring issues of market efficiency and stability in situations where all traders are simultaneously co-evolving in an infinite continuous space of strategies. The state at time of such a market with traders in it can be characterised as an -dimensional vector of -values, denoted by , identifying a single point in the -dimensional hypercube that is the space of all possible system states, and that point will move over time as the traders each adapt their values. We can attempt to identify attractors and repellors in this hypercube, but we will need new visualisation techniques: we’ll need to leave simplices behind.

There are many ways in which a PRZI trader could be made to dynamically adapt its -value in response to market conditions. Here, in the spirit of minimalism associated with studies of ZI traders, I use a crude and simple stochastic hill-climbing algorithm, of the sort that might be found as an introductory illustrative straw-man sketch in the opening chapter of a book on machine learning. To keep with the tradition of naming ZI/MI trading algorithms with short acronyms, I’ve named this PRZI Stochastic Hill-Climber as PRSH (pronounced “pursh”). PRSH is defined in Section 6.3.1, and then some illustrative baseline results from experiments in which a single PRSH trader adapting in markets where all other traders are playing fixed strategies are presented in Section 6.3.2. After that, Section 6.3.3 shows results from experiments in which all traders are PRSH, and hence in which the market is maximally co-evolutionary. The Python source-code for PRSH has been released as free-to-use open-source, in BSE (see Cliff, (2012)) to enable other researchers to replicate and extend the preliminary results shown here.

6.3.1 PRSH: a minimal PRZI Stochastic Hill-Climber

At any time , a PRSH trader has a set of strategies that was created at time and that consists of different PRZI strategy values to (i.e., ). Although is continuous in this model, alterations to happen only occasionally. After an initialisation step in which the strategies are each assigned a value via a genesis function , PRSH enters into an infinite loop: let denote the time at which a new iteration of the loop is initiated; in each cycle of the loop a PRSH trader first evaluates each of its strategies in turn, trading with each of them as the sole exclusive strategy for at least a minimum period of time , such that all have been evaluated by time ; after that, it ranks the strategies by some performance or fitness metric , and copies the top-ranked strategy (the elite) at time into ; it then creates new ‘mutants’ of , via a stochastic mutation function , and this set of new strategies then replaces the old , becoming , at which point it loops back for the next iteration (and hence in that next iteration the value is what was in the prior iteration).

This definition leaves the experimenter free to decide certain key details when implementing PRSH:

-

•

The choice of and of together determine the speed of adaptation: PRSH will generate a new at most once every seconds: i.e., is the minimum time-period between successive mutations, where each mutation is an adaptive step on the underlying fitness landscape. If you want a PRSH to make adaptive steps on the fitness landscape in the course of an experiment, that experiment needs to run for seconds.

-

•