Abstract

These acknowledgements are surely incomplete and I apologize in advance to all those that have been ignored by these brief words. An uncountable number of people helped me through this stage and I could have never done any of this alone.

To my father, to whom this thesis is dedicated. From an early age you inspired in me the desire to solve problems, to learn, and to push the boundaries.

To my mother and my brother, for the unconditional support, the love, and the eternal companionship.

To Léon Bottou. Being advised by you is a privilige. Working with you is a constant learning experience. Your vision for what is and what will be important, enveloped with a deep curiosity and a genuine drive for understanding, helped me take shape as a researcher, and I hope to keep learning from you in the many years to come. None of this thesis would have existed without you.

To Yoshua Bengio. Few people have had a strong impact in my life as you did. After sending you a short email with a half-baked idea, you decided to take me under your wing in Montréal, and I can honestly say those months were some of the happiest I’ve ever been. The constant feeling of learning every day, being surrounded by amazing people, and at the same time being humbled and inspired by your everyday knowledge made waking up every day in the freezing weather an experience of sheer joy. Finally, it is not just your role as an academic mentor, but your human character that make working with you so rewarding: your commitment to education, to your students, and to society are a constant source of inspiration.

To David Lopez-Paz. I consider you family. Thank you for so many happy moments, for the techno, for calling me out when I need it, for teaching me about causality, for the infinite conversations, for everything. Saying all that I’m thankful for in our friendship would take more space than this thesis does. If it wasn’t for you, this thesis would also not have existed. I am so looking forward to many more years of friendship.

To Pablo Sprechmann. When you’re new to a city, finding someone that speaks not only the same language but the exact same accent, and from someone as welcoming as Pablo, makes you feel blessed. For the many many lunches, conversations, the clear advice, and your great company, thank you for making me feel at home.

To Cinjon Resnick. Thank you for your friendship and the many discussions on all aspects of life. Every time I talk to you I leave feeling motivated and ambitious. Thank you for so much love.

To Marco Vanotti. Thank you for so much laughter, for the interminable talks about life, work, what’s right and what’s wrong, and all the stupid corners of life. Thank you for allowing me to bounce all my stupid ideas with you. Thank you for so much joy.

To Ishmael Belghazi and Marcin Mocsulzki. For bouncing off crazy ideas, for complaining together about life, for sharing happiness and realizing how lucky we are to have this amazing life. For the balcony chats, for the many beers, the technical discussions, the wondering about the future, thank you for everything.

To Amar Shah. Thank you for making research fun. The many shared laughs, crashing into the corporate parties, thank you for introducing me into this research world with a smile.

To Arthur Szlam and Soumith Chintala. You guys basically taught me how to do research. From day one when I was interning as an unbearable undergrad, despite my resistance you tried to teach me how to make arguments bulletproof. What problems we should care about, and how to develop experiments to precisely prove our points. How state of the art is not what matters; that what does is identifying the core problem, validating it’s importance, solving it, and testing the solution; with targeted experiments all the way through, not just at the end. To this day I don’t know if I ever met a more brilliant person than Arthur, or a better engineer than Soumith, and I don’t know if I ever will. A quote from Arthur I received on my first year as a PhD student and I will always remember is as follows: "Never make a claim that doesn’t follow from an experiment or a theorem". The surprising importance of this phrase, given the amount of times we tend to break it in the false name of intuition, will stay with me for a very long time.

To Youngdock Choi. For the many life and math discussions. During my PhD you helped me keep the love for pure math alive. I’m sure you are going to be a great mathematician, regardless of whatever endeavour you end up doing.

To Ishaan Gulrajani, for being one of the best researchers I’ve had the priviliged of working with. I look forward to seeing you become a star soon enough.

To all my coauthors, you know who you are, I couldn’t have done any of this alone.

To my dear friends María Arone, Juan Luis Aragón, Agustín Valente, Facundo Orellana, Clementina Flores and Agostina Baiardino.

To Carlos Diuk, who taught me what Machine Learning is, and why it’s awesome.

To Federico Felguer, who inspired my love for mathematics.

To Pablo Groisman and Juan Pablo Pinasco, who taught me most of the math I knew until my PhD. Perhaps more importantly, who made me understand that pure mathematics can be an incredibly powerful tool, that can alter the way we think about most objects in the applied world, and solve otherwise unreachable problems. You made me understand what research in math really looks like, and made it be a part of my life that I so desperately adore.

To Luis Scoccola and Nacho Darago. For so many inspiring conversations, for giving me a window into the insanely large side of math that I know nothing about. For making university and learning math so much more inspiring and fun.

To Alex Lamb, for being the funniest guy in ML, a great friend, and a great researcher.

To Federico Lebrón, for showing me that unreachable things can be reachable, when I was nothing but starting to study. Thanks for the far reaching support and advice.

To Pablo Zadunaisky, for teaching us how to properly write math in the Differential Geometry class. This has been one of the most useful things I’ve learnt in the last 5 years.

To Anil Kokaram and Yao-Chung Lin, for giving me my first research project, helping me every step of the way, and teaching me how awesome applied research can be.

To my thesis committee. To Kyunghyun Cho, for uncountable discussions and providing an unachievable example of what I want to become as a junior professor. To Christina Heinze-Deml, for the friendship, for not letting me get away with half-baked arguments, and for beautiful work that inspired a large part of this thesis. To Yann LeCun, for leading this amazing lab I’m proud to be part of, and for helping me whenever I needed. To Joan Bruna, for letting me bounce ideas with you whenever I wanted, and overall being a ridiculously nice person. To Charles Blundell, for making my stay at DeepMind so much fun, for all the great advice, for giving me freedom to do whatever research I wanted, and at the same time being incredibly helpful and making me feel part of your amazing research group.

To all my amazing professors, both in Courant and in UBA. I consider myself extremely lucky to learn from such ridiculously enthusiastic and smart people. To the people that made all the online courses I took, without this I wouldn’t have been able to learn machine learning.

To the many people that helped me grow in this journey. To Christina Heinze-Deml, Alex Nowak, Alfredo Canziani, Cijo Jose, Manuel Giménez, Avital Oliver, Mike Phillips, Axel Sirota, Tom Sercu, Pablo Zivic, Oded Regev, Caglar Gulcehre, Aaron Courville, Gabriel Synnaeve, Francesco Visin, Yarin Gal, Uri Shalit, Emily Denton, Ferenc Huszar, Jake Zhao, Aditya Rahmesh, Faruk Ahmed, César Laurent, Keith Ross, Jelena Luketina, Damian Furman, Ignacio Niesz, Martín Mongi Badia, Juan Doldan, Maxi Bustos and all the rest of GARG, Andrés Campero, Jessica Forde, Facundo Sapienza, Amy Zhang, Agustín Somacal, Pedro Ortega, Felix Hill, Leopoldo Taravilse, Erin Grant, Ari Pakman, Stanisław Jastrzębski, Joseph Paul Cohen, Mathieu Germain, Federico Carnevale, Will Whitney, Maxime Oquab, Anna Klimovskaia, François Charton, Alex Pritzel, Aahlad Manas, Elman Mansimov, Zbigniew Wojna, and Matias Domingues.

To the Balinese, for welcoming me into their magical place.

To the hundreds of coffee shops where I did so much studying and work. Here are a few of them for the interested reader: Caravane Café, La Bicicleta, Del Viento, Storyville Queen Anne, The Mill, City of Saints, Blue Bottle, SEY, Cafenation Amsterdam, Ona Café, Fortunata, Leia’s, Everyman Espresso. Augmenting this list is left for future work.

corotheo \aliascntresetthecoro \newaliascntproptheo \aliascntresettheprop \newaliascntlemmatheo \aliascntresetthelemma \newaliascntobstheo \aliascntresettheobs \newaliascntobsdeftheo \aliascntresettheobsdef \newaliascntdefitheo \aliascntresetthedefi \newaliascntassutheo \aliascntresettheassu

NEW YORK UNIVERSITY

Courant Institute of Mathematical Sciences

PhD Thesis

Out of Distribution Generalization in Machine Learning

Martin Arjovsky

Advisor: Léon Bottou

Thesis Committee:

Yoshua Bengio,

Charles Blundell,

Léon Bottou,

Joan Bruna,

Kyunghyun Cho,

Christina Heinze-Deml,

Yann LeCun.

Defense Date: 17 December 2019

A mi papá Jorge.

“Pensar es olvidar diferencias, es generalizar, abstraer.”

Jorge Luis Borges, Funes el memorioso

Chapter 1 Introduction

Why are we here? Most of us are here for a simple reason: we want to solve AI. Then what does artificial intelligence have to do with the title of this book? One way AI is modernly defined is as the study and design of rational agents [RN09]. In this sense, we describe a system as intelligent when it acts maximizing some expected notion of performance. The subfield of machine learning deals with the subset of problems and algorithms where experience is available to the agent (usually in some form of data) that can be leveraged to improve this notion of performance [MRT12]. Most often, performance is measured by how the agent acts in new and unseen situations that do not form part of its training experience. For example, an agent might be trained to perform translation from English to French, and its training experience consist of a large collection of translated UN documents. However, at evaluation time, it may be tested on new UN documents different from those it has seen. Naturally, there is a gap in performance between how the agent behaves in the training experiences it has seen, and in the new situations it is evaluated on. The ability of an agent to generalize is measured by how small this gap in performance is.

The previous paragraph hopefully has explained what generalization is in the context of machine learning, and thus in the bigger context of AI. However, what are these “Out of Distribution” words remaining in the title? As mentioned, generalization consists in reducing the gap in performance of an agent acting in seen training situations and the same agent acting in unknown test ones. However, there are many different types of unknowns. The kind of generalization commonly addressed by statistical learning is in-distribution: when the data generating process from the training examples is indistinguishable from that of the test examples. In the case described above, where the translation agent is trained on UN documents, and it is tested on new UN documents, this is an in-distribution generalization problem. If the translator is trained on a large collection of UN documents, but tested on user requested translations that are statistically different in any way (such as using certain words with different frequencies, more coloquial constructions, larger or shorter sentences), then this is not an in-distribution generalization problem. By definition, generalization problems that are not in-distribution, are called out of distribution (OOD) generalization problems, which are the topic of this book.

While in-distribution generalization has a massive importance, a large part of the intelligence we commonly attribute to humans has to do with being able to solve complex tasks in new environments or contexts [Lak+17]. These environments are typically different from the human’s previous experience, but the human is still able to leverage its knowledge to adapt and perform well in the new setting. Furthermore, humans are general purpose machines: we are not able to solve a single task, but a wide range of them. In stark contrast, current AI systems are narrow: when they are trained to perform one or a few tasks, this is all they can do, and generalization to new tasks is in general not possible [Mar18, Wel19]. The generality of humans is partly due to them being able to understand and make use of past experience in the new task [Lak+17]. For these reasons, out of distribution generalization is often discussed as being likely to have an important role in the development of general purpose intelligent machines [Lak+17, Mar18, Wel19].

Now, not all the readers of this book will want to solve AI. Some (among which the author is from time to time included) will want to solve a concrete problem of practical or industrial interest. The role of out of distribution generalization in these issues then needs to be clarified so that these readers can assess whether this document is of any interest to them. Given a problem, to answer the question of how necessary the study of OOD is to it, we have to ask two things (with a few obvious details like infrastructure aside): what kind of data is available, and what do we want to generalize to? If the data we have is of the same data generating process than the one at test, then OOD generalization is not a priori the best thing to attack the problem with. An example instance of this is when training and test data are different UN documents, or when the task involves decision making for customers, and the data at training time comes from the same type of customers that will be seen at test. However, in most real life problems, while data is abundant, it is not necessarily the right kind of data. If we are building a machine learning tool for users, and the users’ preferences vary over time, then this becomes an out of distribution generalization problem, in which we would still like to leverage the past users’ data. Furthermore, in most cases we want to build robust systems that perform well across many different settings. An example of this is building a self-driving car, where our training data might come from certain cities, and we would like to build a car that generalizes to many more cities. Often at testing time the data is perhaps of lower quality, such as images of lower resolution or noisier, or even provided by a malicious user that purposely wants to fool a sensitive machine learning system. Finally, many times we have access to massive datasets obtained by scrapping the web, such as the popular image classification datasets, and we want our models to generalize well to data provided by the particular users of our applications. All of these are out of distribution generalization problems of industrial interest.

The goal of this work is simple. We want to review, contextualize, and clarify what the current knowledge in out of distribution generalization is. As a consequence, a large part of this work will be devoted to understanding the (sometimes subtle) differences and similarities between different methods and assumptions, commonly presented in an isolated fashion. A focus will be put in ideas that are relevant to sensory nonlinear problems such as those related to AI, or modern large scale machine learning applications. Furthermore, we will devote special attention to studying the shortcomings of the different approaches, and what might be important next steps.

Out of distribution generalization is a problem unsolvable without assumptions on the task at hand. If the test data is arbitrary or unrelated to the training data, then generalization is obviously futile. Therefore, all the methods discussed make some assumption on the data. Our goal as surveyors then is to clarify what these assumptions are, how they relate to each other, and where they fall short. Our goal as researchers is to find assumptions that are 1) approximately satisfied in real problems of interest, and 2) that if they are approximately satisfied, we can obtain generalization improvements with a suitable algorithm. Assumptions that are too strong will break property 1 because they won’t be approximately realized, and assumptions that are too weak will break property 2 because they won’t have meaningful practical implications.

Hence, we embark on a quest for assumptions!

1.1 Outline

This book is split into 4 chapters, without counting this tiny introduction:

-

•

In chapter 2, we first discuss how to quantify out of distribution generalization. Then, arming ourselves with several examples, we examine the relationship between out of distribution generalization and several methods commonly employed to tackle different out of distribution tasks. Particular emphasis will be put in highlighting the assumptions underlying these methods, and showing when they do and they do not work. Along this line, an important take-off is that there is no general out of distribution machine. Some assumptions are validated on some tasks, and completely false in others, thus we will try to highlight when a particular method may be reasonable or not according to the problem at hand.

This chapter will also serve as a concise literature review on existing approaches for out of distribution generalization.

-

•

In chapter 3, we will focus on a particular class of out of distribution tasks. In these predictive tasks, as in many real problems, the difficulty in generalizing out of distribution will lie in figuring out which correlations in the data are spurious and unreliable, and which ones represent the phenomenon of interest. These tasks will often require predictors to be robust to strong changes in context, and to be able to distinguish between cause and effect.

This chapter is an extended version of [Arj+19], and as with the previous chapter, all this work has been done in collaboration with David Lopez-Paz, Léon Bottou, and Ishaan Gulrajani. In this thesis, we include a few more theoretical insights and results, particularly dealing with nonlinear predictors and sample complexity in terms of the needed number of training distributions. Furthermore, many things are rewritten to maximize clarity of exposition in a longer format, with added explanations and details making the theory more palatable.

-

•

In chapter 4, we discuss for different applied fields the type of out of distribution tasks that appear in practice, and how these fields have dealt with those issues in the past. This chapter is not an applications chapter of the ideas in chapter 3 (I wish it were). These are all nontrivial tasks that will likely require much research to be attacked properly, and as such we will not focus on potential solutions. Instead, we will try to focus on the particular structure that is available in each domain, and what shape the different OOD problems in these fields take.

This chapter came about from a reading group on out of distribution generalization that we ran together with Cinjon Resnick and Will Whitney at NYU. I am particularly indebted to Will Whitney for introducing us to the works in the robotics section.

-

•

In chapter 5, we lay the ground for new research areas in the context of out of distribution generalization and AI. In this chapter we will be concerned with agents interacting with the world in either an exploration or reinforcement learning setting, and how they could benefit from out of distribution generalization.

As an important note, while in my PhD I have also worked on other topics [AB17, ACB17, Gul+17, Bot+18], these are not going to be covered in this thesis. The reasons are multiple, but primarily because this is the work that I find most promising.

1.2 Definitions and Terminology

While out of distribution generalization is relevant in many aspects of machine learning, we will instantiate our exposition in the supervised learning setup, with minor important exceptions. This is in order to ground the exposition in concrete examples, and to avoid confusing notation that attempts to cover all areas of machine learning. A large proportion of the ideas discussed translate verbatim to certain situations in self-supervised learning and reinforcement learning, and the relevant parallels will be provided. Situations specific to reinforcement learning and exploration will be discussed in sections 4.1, 5.1 and 5.2, and unsupervised learning will be discussed in more detail in section 3.6.

We now introduce our notation:

-

•

Random variables such as inputs and outputs will be denoted by capital letters , and specific values will be denoted by undercaps letters .

-

•

Unless otherwise stated all vectors are column vectors. If , we will do a slight abuse of notation by denoting its corresponding row vectors as . Therefore, if , its inner product will often be written as .

-

•

The input space will be denoted by , and the space of the labels by . The space of predicted labels will be denoted as . While often , this is not always the case. For instance, in binary classification , and if denoting the estimated probability of the true label being 1, or even if contains pre-sigmoid logits.

-

•

A loss function is any function that measures the difference between a predicted label and a true label. In that sense, a loss is a function . A hypothesis or predictor is any function . In general, our goal will be to estimate from data a hypothesis such that is small in expectation under different possible test distributions.

-

•

We will often have families of probability distributions over . The indices are called environments. Given an environment , we will denote the random variables with distribution as . When taking expectations over , it is then understood that the expectation is taking under the probability distribution . Namely, we will use the symbol to mean . When the distribution of the expectation is obviously , such as if only terms appear, we often omit all subscripts and simply use .

-

•

The risk or expected loss for a given environment and hypothesis will be denoted as .

-

•

A featurizer or representation is any function . The induced random variable will be denoted . A function will be called classifier (even if the problem is not classification but, say, regression), to avoid confusion with predictors or hypothesis.

-

•

We will use the term correlation vaguely as a general way to refer to the information that one variable carries on another variable , usually a nonlinear dependence. This is done on purpose and consistent with how the machine learning field uses the term “spurious correlations” A large part of this work is itself finding useful mathematical formalizations on this term and the spurious correlations problem.

Chapter 2 Robustness and Out of Distribution Generalization

In order to judge and compare different assumptions and algorithms in the context of OOD, we first need to settle on one or a few ways to quantify how well a predictor generalizes out of distribution.

2.1 A Framework for Out of Distribution Generalization

There are many ways one could quantify out of distribution generalization. The most classical way to do so, and the one we will mostly employ, is the approach taken by distributional robustness [Wal45]. This is, we only assume that the test distribution belongs to a large, often infinite, family , and provide the natural quantification

| (2.1) |

where (as a reminder), is the risk or expected loss for environment . Assuming that the test distribution, while unknown, belongs to , definition (2.1) simply means we want to minimize the worst case over all potential test distributions.

There are many things one could question in the above definition. To begin with, one could question the need for a maximum in (2.1). If we have access to a prior distribution over potential test environments , then one could think of optimizing for the quantity . This would make perfect sense, though we find two unsurprising caveats. First of all, while prior knowledge could be available about which test environments are more likely, it is unclear how often this prior knowledge lends itself to be expressed as a probability distribution that we can easily compute. In this book we will obviously make different types of assumptions over (such as relationships between the different environments), though expressing them as an explicit would be a challenging task. Furthermore, we have the second issue that even if we have access to a that perfectly captures our prior knowledge, the different integrals and posteriors involved in minimizing would often be completely intractable. We elaborate on some of these ideas in section 2.3 and in more technical depth in Appendix D.

Another potential concern of definition (2.1) is the fact that some environments can simply be harder or more stochastic than others, and the worst case environments would dominate (2.1). Thus, could be unable to differentiate two predictors that perform equally well on the hardest environments, but one performs worse than the other in an easy environment. In that direction, one could aim to obtain a predictor minimizing (2.1) and that is Pareto-optimal for the risk of each environment across , as does [MB15]. Understanding how which algorithms lead to Pareto-optimal OOD predictors for other classes of problems is to us a potentially fruitful and largely unexplored avenue of reseearch.

In conclusion, while quantifying out of distribution generalization as in (2.1) has many caveats, it is the simplest quantity we could find that captures the relevant phenomena of OOD in most situations we’ve encountered. After all, it is simply saying we want to perform well over all possible test distributions.

What makes out of distribution generalization a hard problem is the fact that we don’t have access to samples from the test distribution . However, we must have something related to it if we hope to generalize. Therefore, we are in general going to assume that we have access to data from one or a few training distributions . We will review some cases where contains a single training distribution, though for the more ambitious tasks we strive to solve, we can easily see that this is insufficient. Thus, we will often concentrate ourselves in the multiple environments framework [PBM16], where contains more than one probability distribution. In particular, we are interested in the case where contains few distributions, and hence we will aim to obtain strong guarantees (or at least empirical performance) in the nonasymptotic case, where the number of training environments is not tending to infinity but is actually rather small (in ways we will make more precise).

As mentioned before, we are on a quest for assumptions; assumptions on our training and testing data. With the current framework, this means that we want to find valid assumptions on and such that we can make as defined by (2.1) as small as possible. In order for this to happen, and have to be related, and in general we will assume . However, this is obviously not enough, since containing some test environments which are unrelated to those in would make the problem futile. The following section provides a few concrete examples that start to elucidate what kind of properties and might have in real problems of interest.

2.2 A Few Motivating Examples

Here we provide a few out of distribution generalization problems. These tasks will serve many purposes, but primarily to motivate what the relationship between and can be, even if we can only describe it in informal terms now. Second, throughout the text they will be (perhaps simplistic) testbeds for algorithms and assumptions. In particular, we will at times be able to calculate explicitly what the predictor returned by an algorithm using would be, and how far away this predictor lies from generalizing out of distribution to .

Example 2.1.

Consider the structural equation model [Wri21]:

Defining , running the above equations as lines of code, each value defines a joint probability distribution over . By varying over , we obtain our infinite family of distributions . For high values of , the correlation between and is large, even larger than that between and . However, this correlation is spurious: for environments with different , the correlation between and can vary, and even change signs.

The first thing to see is that the only linear predictor that obtains finite under definition (2.1) in this setup is . This is because any linear predictor that assigns a nonzero weight to will have for test environments with . Interestingly enough, the predictor with optimal is also what we call the causal explanation of : it provides the correct description about how is created, and in particular about how it reacts in response to interventions on other variables.

As for the training environments, we will only assume data from two training environments

A crucial thing to note is that for both training environments in , we have that is more reliable when using it to predict than is. However, in the larger out of distribution class , there are cases where using would be catastrophical (e.g. when ). This is our first instance of a case where a predictor that is robust across can be far from robust across . However, we could use the hint that the correlation between and (while strong) changes across the training environments and thus discard , arriving to the predictor and obtaining optimal . We will study such ideas in depth in the following chapter.

Another thing to note is that since can vary all across , the distribution of and hence can shift arbitrarily large amounts across different environments, and in particular from the training ones to a potential test one. This will be a point of failure for some of the methods we’ll discuss.

Example 2.2.

As a thought experiment, consider the problem of classifying images of cows and camels [BVP18]. To address this task, we label images of both types of animals. Due to a selection bias, most pictures of cows are taken in green pastures, while most pictures of camels happen to be in deserts. After training a convolutional neural network on this dataset, we observe that the model fails to classify easy examples of images of cows when they are taken on sandy beaches. Bewildered, we later realize that our neural network successfully minimized its training error using a simple cheat: classify green landscapes as cows, and beige landscapes as camels. Here, we can consider to be a family of distributions containing pictures of cows and camels on beaches or grass in any proportion.

To solve the problem described above, we need to identify which properties of the training data describe spurious correlations (landscapes and contexts), and which properties represent the phenomenon of interest (animal shapes). For the training environments, we could assume that we have two distributions with different proportions of cows on beaches. For instance, the pictures of cows taken in the first environment may be located in green pastures 80% of the time. In the second environment, this proportion could be slightly different, say 90% of the time. These environments could arise for instance because the pictures were taken in different countries: the first environment in the UK where cows are mostly on grass, and the second environment from Goa, India, where there actually is a larger proportion of cows on beaches [McB12]. These two datasets reveal that “cow” and “green background” are linked by a strong, but varying (spurious) correlation, which should be discarded in order to generalize to new environments containing mostly pictures of cows on beaches. Learning machines which pool the data from the two environments together may still rely on the background bias when addressing the prediction task. But, we believe that all cows exhibit features that allow us to recognize them as so, regardless of their context.

This example has a peculiarity, which is that given infinite data from a single environment, training on would prefer to pick up the feature “cow shape” (which is correlated 1. with the label) rather than “green background” (which has a smaller correlation 0.9). Hence, this problem can be asymptotically solved by minimizing for any environment with sufficiently large support of . The key issue here is the assumption of sufficient data to minimize the population error , especially in the context of overparameterized models (when the number of parameters is larger than the number of datapoints). In subsection 3.6.1 will show a toy version of this cow on the beach task, which elucidates why overparameterized models tend to pick up on spurious correlations and fail to generalize OOD, even when the non-spurious ones have more predictive power in all training environments.

Example 2.3.

Consider the problem of generalizing to adversarial examples [GSS15]. In this situation, we typically have access to a dataset from a single training distribution, hence . The attacker takes a sample and performs a potentially stochastic operation on top of to obtain a test sample . The model is evaluated on the joint distribution of , which we denote . Since depends on the attack, the different types of attacks we aim to generalize to will determine the space of possible , which is . Looking for assumptions on the potential attacks and hence on is necessary, since as is widely known after the seminal paper [GSS15], simply training on tends to generalize poorly to a variety of attacks with small enough perturbations that are imperceptible to the human eye.

With these examples in mind, and refining them if need be, we are now able to begin to study different algorithms and assumptions to solve them.

2.3 Empirical Risk Minimization

The simplest method we can study is the ubiquitous Empirical Risk Minimization (ERM) principle [Vap92]. Here, ERM would minimize the average error over all environments

| (2.2) |

In example 2.1, ERM would grant a large positive coefficient to if each training environment leads to large (as is the case in example 2.1), obtaining catastrophic out of distribution generalization for test distributions with negative .

There are cases however where ERM makes a priori some sense. Indeed, ERM in certain situations is what’s known as an optimal learning principle. In an in-distribution problem, without making assumptions on the distribution, no algorithm can obtain better generalization than ERM asymptotically [Vap98]. Using this result, it is easy to see that if the distributions in are samples from a meta-distribution , then ERM is an optimal principle for minimizing the average out of distribution error . However, this has two issues already hinted at in the previous paragraph. First, ERM is optimal when test environments are sampled from the same distribution as training ones. This is not the case in example 2.1 where training environments are the two with and , and we want to generalize to worst case test environments such as . Second, even if we don’t care about worst-case OOD but the average case and with the same meta-distribution, ERM is optimal only when making no assumptions on the meta-distribution. However, all the examples mentioned in the previous section have an enormous amount of structure. In particular, in example 2.1 all environments share the same underlying data generating process, and indeed has only one degree of freedom (the varying ). In conclusion: the assumptions of ERM are in one axis too strong (assuming that training and test environments are sampled i.i.d. from a meta-distribution), and in another axis too weak (assuming no structure on this meta-distribution). However, if the reader has a problem where it is safe to assume test environments come meta-i.i.d, cares about average case OOD error, and has absolutely no other knowledge on the data, then ERM is essentially the best the reader can do.

It is important to note that ERM was never meant to be a method for out of distribution generalization. Its theory is based on having many training points i.i.d., and little knowledge about them. In OOD we will in general have few training distributions, and will have to assume some important amount of prior knowledge and structure about them. We display ERM here because it is a building block throughout all machine learning, and helps elucidate where methods fall short. The next method we study was indeed designed with out of distribution generalization in mind.

2.4 Robust Optimization

The method of this section stems from a very simple and sensible idea. Equation (2.1) asks us to minimize . Since we only have access to , from an empirical perspective it makes sense to begin by minimizing . Robust optimization [BEN09] does essentially this, it attempts to minimize the objective

| (2.3) |

where the constants serve as environment-specific baselines. Setting these baselines to zero leads to minimizing the maximum error across environments. Selecting these baselines adequately prevents noisy environments from dominating optimization. For example, [MB15] selects to maximize the minimal explained variance across environments.

At this moment, we want to stress a point. It is important to separate the notions of distributional robustness (2.1) as a goal, and robust optimization (2.3) as a method. While the method was designed to address the goal, it is not necessarily the best one. In particular, in many cases, (perhaps unsurprisingly) other algorithms can exploit the structure of and in a way that’s more successful at obtaining distributional robustness. In other words, robustness at training time does not in general imply robustness at test time. However, for specific problems, other conditions at training time may as well imply robustness at test time.

In order to understand the predictors returned by robust optimization, the following proposition will be very useful. While promising, robust learning turns out to be equivalent to minimizing a weighted average of environment training errors:

Proposition \theprop.

Given KKT differentiability and qualification conditions, there exist such that the minimizer of is a first-order stationary point of .

Proof.

See Appendix B ∎

This proposition shows that robust learning and ERM (a special case of robust learning with ) would never discover the desired predictor in example 2.1, obtaining infinite . This is because minimizing the risk of any positive mixture of environments associated to large positive ’s yields a predictor with a large positive weight on . Unfortunately, this correlation will vanish for testing environments associated to negative , and predictors trained by minimizing will fail at generalizing out of distribution. This is starting to highlight a key insight: the difference between interpolation and extrapolation. Methods based on robust optimization interpolate between training environments, and thus when correlations are large but spurious it will associate large weights averaging the correlations. To solve this task we want a method that extrapolates: noticing that the correlation varies across environments, we can aim to discard it and thus generalize to environments whose vary outside the range seen in the training environments.

2.5 Wasserstein Robustness and Adversarial Examples

Following up on example 2.3, assuming that , what assumptions do we need on the attacks (and how do they translate to asumptions on ) such that we can design an algorithm to improve generalization? Since the inception of adversarial examples, attacks are generally considered to be constrained. In particular, it is typically assumed that for some (not necessarily Euclidean) norm . This is due to the fact that in general adversarial examples are supposed to be reasonably small perturbations, almost imperceptible to the human eye.

The fact that means that the distributions and are close. Particularly, it means that they are close according to the Wasserstein distance, since induces a coupling between and . Therefore, with any Wasserstein distance in . Thus, , where this ball is measured in Wasserstein sense. Hence, seems like a fantastic candidate for this task. Is this enough of an assumption such that if validated in practice (which it is on this task by the above discussion), there is an algorithm with low across ? The answer is largely yes, as shown by the recent paper [SND18]. We refer the reader to this paper for the relevant details.

Is the assumption reasonable for our other examples? It doesn’t seem like it. In example 2.1, replacing by a large value will make the distribution of vary arbitrarily and hence can vary arbitrarily in Wasserstein sense. In the cow on the beach case, the test environment has a much larger proportion of cows on beaches than cows on grass, and beaches are clearly pixel far from grass. Hence the assumption is violated in there as well. This means that for these problems we will need different assumptions, and hints at the obvious fact that not all out distribution generalization problems are equal. Different tasks will require different assumptions, which will lead to different algorithms.

2.6 Robustness

We mention here for completeness another very natural out of distribution generalization problem. What differentiates this one from those in the previous section is that there is a strong negative result despite the assumption being seemingly reasonable, and in particular almost identical to that of the previous section.

The previous section studied the case where there is a single training environment , and is the -ball around with the Wasserstein distance. Does it make sense to consider a similar situation, but when the test distribution is assumed to be close to in some other distance? In particular, what if for some divergence like the Kullbach-Leibler divergence? It is important to recall that divergences measure how close to one the ratio of the densities of the two distributions are. For the above examples, this is not true in any of them. As already mentioned, can vary greatly in examples 2.1 and 2.2. For example 2.3, the distribution after the attack can have disjoint support (even if geometrically close) to the original one, and hence all divergences would be arbitrarily large. Assuming to be small would mean that the support of one of the distributions contains the other, and that the densities are similar. This is however the case when and contain the same possible examples, only one assigns slightly different probabilities to each example than the other one.

A surprising result, displayed in complete detail in [Hu+18], is that assuming is close to in any divergence brings nothing to the table when employing a classification loss. Namely, we can easily rephrase their result in our framework as showing that if then

for any two predictors . This means that we cannot expect any algorithm to bring an improvement over ERM if this type of closeness is the assumption we make. The reason for this negative result seems to be the fact that an divergence ball is in a sense too wide. It considers all possible distributions which affect the ratios of examples. Since we would have to consider increments in probability to any example, we cannot do anything better than minimize the error across all examples equally, which is what ERM does in the first place. Another way of saying this is that this assumption assumes no structure on and , in the sense that all the possible train-test shifts are considered up to a certain magnitude. This is in contrast to all examples in section 2.2, where for instance in example 2.1 we have that a change in yields a statistical change in , and example 2.3 considers test cases that are norm close (thus assuming geometric structure on the problem) to the training distribution.

2.7 Domain Adaptation

The methods of the previous two sections assume that is close to in some sense, and this is one of the reasons why they fail to address example 2.1 and example 2.2. The method that we will study in this section has a different assumption, namely that we can extract some variable by a nonlinear function, that will be useful to predict across environments, and can be identified by assuring doesn’t change across environments.

Domain adaptation [Ben+07] considers labeled data from a source environment and unlabeled data from a target environment with the goal of training a classifier that works well on . Many domain adaptation techniques, including the popular Adversarial Domain Adaptation [Gan+16, ADA], proceed by learning a feature representation such that (i) the input marginals , and (ii) the classifier on top of predicts well the labeled data from . This can be easily adapted to the multiple environment setting by looking for a such that is the same for all .

Since the distribution of doesn’t change in example 2.1, while the one of does, we can expect domain adaptation to work well in this constrained example. However, in example 2.2, the fact that the proportion of cows can change means that domain adaptation will discard this information, leading to poor prediction. We then refine slightly example 2.1 (which is meant to be a first model of example 2.2) to take into account this issue, and to see how we can fix it.

Example 2.4.

Consider the structural equation model:

The only difference between this example and example 2.1 is that we now allow (which we could think as the proportion of cows in the data) to vary. Thus, now will contain all the distributions resulting from variations in and . The training environments are now adapted to

As can be seen, the discussion of sections 2.3 and 2.4 still apply: at training time, in all environments the correlation between and is stronger than the one between to . Nonetheless, the former correlation is spurious, and using it to predict can be catastrophic at test time, while the predictor obtains optimal out of distribution error.

The main difference between example 2.4 and example 2.1 is that the distribution of now varies. This is problematic for domain adaptation, since enforcing to stay the same across environments would mean that has to be constant, thus destroying any predictive power. For a more in-depth study of these failures, we encourage the avid reader to later take a look at Appendix C where we also mathematically examine these failures and how they relate to the ideas in the next chapter.

The crucial property that has which makes it useful is indeed not that its marginal distribution stays the same, but the fact that the conditional stays the same across environments. Namely: the prediction from to doesn’t vary across environments, while that from to does, even if the latter is better at training time. We can use this idea of looking for features whose conditional doesn’t change across to discard spurious correlations like that of . This property of is what we call invariant prediction, which is the central topic of the next chapter. Our notion of invariant prediction builds directly from the foundational work of [PBM16], with similarities and differences that are made precise in section 3.1. Since we can see from just our two training environments that changes, looking for these features will filter out , use only and obtain optimal . As we will show, there is a deep and fundamental connection between this notion of invariance, causality, and certain kinds of out of distribution generalization. In particular, we will see that in many cases we can obtain out of distribution generalization by looking for features whose correlation is invariant with the label across just a few training environments.

Chapter 3 Causality, Invariance, and Generalization

This chapter studies the strong interplay between three ideas: causality, invariance, and out of distribution generalization.

The notion of causality dates back to some of the earliest years of philosophy, starting at least with the notion of karma in Hinduism [CC86]. In the Mahabharata text (dated around 400 BC), Yudhishthira and Bhishma discuss whether the course of a man has been already predestined, and the existence of free will. At one point Bhishma replicates that the future is brought into existence by human present actions given by free will, and the current circumstances that are partly set from past actions. It is karma (intent and action) that shapes the future. This idea, of actions or interventions resulting in a tangible consequence has stood tall throughout centuries until the modern mathematical theories of causality [Pea09, Rub74]. These theories formalize in different ways this century old idea that if we know the behaviour of a cause to its effect, we can predict the outcome when things change due to an action.

The notion of invariance relies upon the idea that some property of a mathematical object remains unchanged [Car03]. Any precise definition of invariance then has to determine what quantities are preserved, and across what. A particular class of invariance that we will mostly focus on is that of statistical invariance: the assumption that some statistical patterns are preserved across a series of distributions. This kind of invariance (which is still only loosely defined) has been marked as a staple of reasoning and prediction, since in order to figure out what’s going to happen we have to assume that some underlying rules of the world are going to remain invariant.

Then, why are casuality, invariance and out of distribution generalization related? Causality has often been described as having the central property of invariance under intervention [Car03]. Namely, certain statistical quantities of the joint data distribution of the cause and the effect are preserved when we change the data distribution with an intervention or action. In general, if a variable causes another one but not the other way around, intervening by changing the value of will affect the distribution of in a precise and predictable way, while changing with an action has no effect on how changes. For example, if we see as an intervention in example 2.1 as changing the value of , while many things in change, the conditional distribution remains stable and invariant. This is not true of . As we can see, these three ideas are intertwined: if there are features whose conditional distribution remains invariant, then using to predict will be reliable across different environments and allow us to obtain better out of distribution generalization. Furthermore, the idea of finding variables that cause is inherently tied to the statistical prediction from to being stable under interventions. This means that if different environments come from interventions, finding the cause is likely to help us generalize. When interventions relate to changes in context, finding the features with stable conditionals with the label will then help us generalize to changes in context.

To us, neither causality nor invariance will ever be the goal. They will be but tools to attack out of distribution generalization. We acknowledge that this is perhaps not what the reader wants, and finding the causal structures governing the data seems like a worthy goal by itself. To that reader we assure you that (to some extent), that goal will be satisfied, as a strong part of this chapter will end up showing that in certain circumstances invariance, causality, and out of distribution generalization are indeed equivalent. This might seem strange at first, but really it’s unsurprising after a certain closer look. After all, we won’t be able to predict how will react to interventions on the variables we don’t know are causes or effects of . Perhaps unsurprisingly, causality will often be equivalent to a precise statistical invariance, since being useful to predict across when contains all distributions arising from interventions means that certain conditional distributions from to have to be preserved. However, a central point of this chapter is that even when no traditional notion of causality is mathematically defined (such as a causal graph between observed variables), invariance will be a statistically testable quantity that enables generalization. And in cases when causality makes sense, these three notions are often equivalent.

This last point makes us wonder whether we need to redefine what causality is. It is clear that our notions of causality such as graphs between observed variables are not very useful for many situations of interest (what even is a graph between pixels?). Since invariance is equivalent to causality in some settings when both are clearly defined, and invariance keeps the fundamental generalization properties we would expect from causation when the latter is undefined, we could consider empowering the formalization of cause and effect from an invariance point of view. We take a stab at this epistemological qualm in section 3.4.

For now, let’s make these ambitions more concrete and try to solve example 2.4 by studying which statistical patterns are preserved across environments.

3.1 Invariance and Generalization

As mentioned before, the peculiarity that the optimal OOD predictor for example 2.4 has is that it uses only the feature , which has a stable correlation with across environments. A more precise way of saying this is that is preserved for all . How then can we find these features that have stable correlations with the label? The following observation comes to aide. In general, conditional expectations from to can be written as the optimal predictor minimizing the prediction error from to .

Observation / Definition \theobsdef (Invariant Prediction).

Let follow a joint distribution , for . Then, the two following statements are equivalent:

-

A.

For all in the intersection of the supports , we have

-

B.

There is a classifier that is simultaneously optimal for all risks, i.e.

where can be either the cross-entropy or mean-squared error losses.

Furthermore, in the case where is discrete (as in classification), we can replace item (A) with

If either item (A) or (B) are satisfied, we say that leads to an invariant predictor across . If , and is the classifier in item (B), we will also say leads to the invariant predictor across .

This leads to the following simple idea. To predict from , we can look at optimal least-squares predictors for environments :

-

•

regress from , to obtain and ,

-

•

regress from , to obtain and ,

-

•

regress from , to obtain and .

The regression using is our first example of an invariant correlation: this is the only regression whose coefficients do not depend on the environment . Conversely, the second and third regressions exhibit coefficients that vary from environment to environment. This shows that we can identify the optimal predictor by looking at subsets of variables for which the least square predictor is the same across environments. This is similar to what the seminal paper [PBM16], our main source of inspiration, does. There, the authors define invariant prediction for a subset of variables as those that have the same residual distributions (the distributions of ) across environments. While this is in general not equivalent to our notion of matching or , for the problems of causality they study the two notions do coincide. Algorithmically the authors look for subsets of variables which have the same regression residual variances across environments. However, the method of [PBM16] (titled Invariant Causal Prediction, or ICP for short) has three significant drawbacks. First, looking for subsets of variables in a -dimensional setup has computational cost . Second, hypothesis testing for regression residuals inherently dooms recovering any useful predictor in the presence of mild model mispecification. While these two qualms are important, it is the third drawback that will matter the most for us.

The third issue of ICP is that in the perceptual problems related to AI, such as example 2.2, looking at subsets of variables makes very little sense. We cannot expect a fixed subset of pixels to have invariant correlations with the label across images and datasets (since the relevant objects can appear in different pixels for different images). This becomes even more odd when looking at the causality interpretation of example 2.4: in this case is the only causal parent of , but what even is a causal graph between pixels? In problems related to AI, causality and invariance must operate at a latent variable level: algorithms have to learn features (potentially nonlinear, as in the work of [CPE15, HM17]) of the inputs which themselves have stable correlations with the label.

The following theorem starts to formalize why looking for features with invariant correlations may be a good idea. The theorem says that obtaining features with invariant prediction across and low error across is enough to guarantee out of distribution generalization, i.e. low error across .

Theorem 3.1.

Let be a representation function, and a classifier. Let’s assume that for some constant (which is trivially satisfied when is the cross entropy or mean squared error if the features and targets are bounded). Then, if satisfies:

-

A.

Approximate invariant prediction:

for , where is the total variation distance.

-

B.

Low training error.111This is a stronger condition than simply bounding training error as in the conclusion of the theorem, since we’re stating that for all features, at training time the features are well correlated with the label. This could be replaced by standard training error, but we would have to take into account the fact that some examples are harder than others (i.e. can have different variances for different values of ), and the test distribution can include a larger proportion of harder examples. This is perfectly fine, and indeed it’s good that the framework allows for detailing generalization errors when distributions have different dificulties, but we opted for this exposition simply because the corrresponding result is easier to understand. Let be such that:

for all .

Then we have the following simple bound on the test error for any

Proof.

See Appendix B ∎

The condition of invariance across is a priori unverifiable and unatainable without assumptions, since we don’t have access to . What this theorem does is split our work in two: in section 3.2, we provide an algorithm that gives invariance across and low error across . Then, section section 3.3 studies assumptions and theorems that showcase when invariance across implies invariance across . Together with Theorem 3.1, this means that our algorithm will be able to provide out of distribution generalization in these settings.

3.2 Invariant Risk Minimization

To discover these invariances from empirical data, we introduce Invariant Risk Minimization (IRM), a learning paradigm to estimate data representations eliciting invariant predictors across multiple environments. In this section, we have two goals in mind for the data representation : we want it to be useful to predict well, and elicit an invariant predictor across . Mathematically, we phrase these goals as the constrained optimization problem:

| (IRM) | ||||||

| subject to |

This is a challenging, bi-leveled optimization problem, since each constraint calls an inner optimization routine. So, we instantiate (IRM) into the practical version: (IRMv1) where becomes the entire invariant predictor, is a scalar and fixed “dummy” classifier, the gradient norm penalty is used to measure the optimality of the dummy classifier at each environment , and is a regularizer balancing between predictive power (an ERM term), and the invariance of the predictor .

3.2.1 From (IRM) to (IRMv1)

This section is a voyage circumventing the subtle optimization issues lurking behind the idealistic objective (IRM), to arrive to the efficient proposal (IRMv1).

Phrasing the constraints as a penalty

We translate the hard constraints in (IRM) into the penalized loss

| (3.1) |

where , the function measures how close is to minimizing , and is a hyper-parameter balancing predictive power and invariance. In practice, we would like to be differentiable with respect to and . Next, we consider linear classifiers to propose one alternative.

Choosing a penalty for linear classifiers

Consider learning an invariant predictor , where is a linear-least squares regression, and is a nonlinear data representation. In the sequel, all vectors , are column vectors. By the normal equations, and given a fixed data representation , we can write as:

| (3.2) |

where we assumed invertibility. This analytic expression would suggest a simple discrepancy between two linear least-squares classifiers:

| (3.3) |

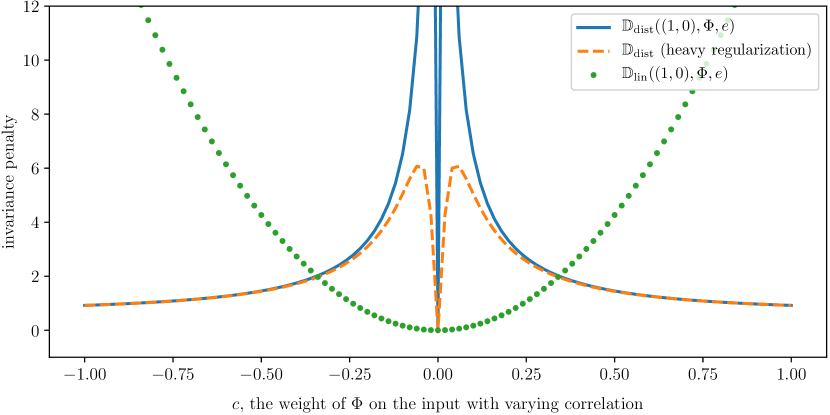

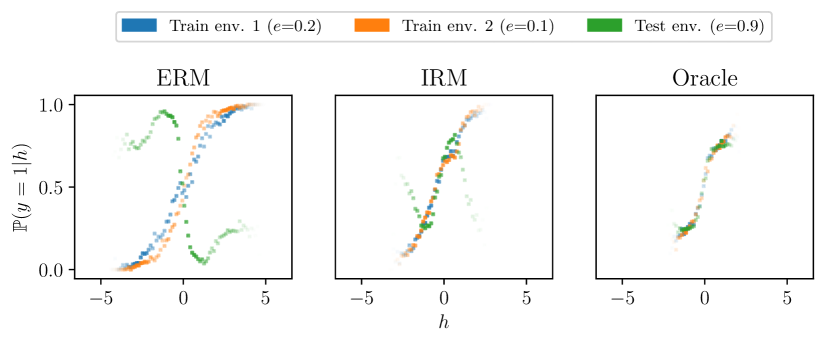

Figure 3.1 uses example 2.1 to show why is a poor discrepancy. The blue curve shows (3.3) as we vary the coefficient for a linear data representation , and . The coefficient controls how much the representation depends on the variable , responsible for the spurious correlations in example 2.1. We observe that (3.3) is discontinuous at , the value eliciting the invariant predictor. This happens because when approaches zero without being exactly zero, the least-squares rule (3.2) compensates this change by creating vectors whose second coefficient grows to infinity. This causes a second problem, the penalty approaching zero as . The orange curve shows that adding severe regularization to the least-squares regression does not fix these numerical problems.

To circumvent these issues, we can undo the matrix inversion in (3.2) to construct:

| (3.4) |

which measures how much the classifier violates the normal equations. The green curve in Figure 3.1 shows as we vary , when setting . The penalty is smooth (it is a polynomial on both and ), and achieves an easy-to-reach minimum at —the data representation eliciting the invariant predictor. Furthermore, if and only if . As a word of caution, we note that the penalty is non-convex for general .

Fixing the linear classifier

Even when minimizing (3.1) over using , we encounter one issue. When considering a pair , it is possible to let tend to zero without impacting the ERM term, by letting tend to zero. This problem arises because (3.1) is severely over-parametrized [Zha+17]. In particular, for any invertible mapping , we can re-write our invariant predictor as

This means that we can re-parametrize our invariant predictor as to give any non-zero value of our choosing. Thus, we may restrict our search to the data representations for which all the environment optimal classifiers are equal to the same fixed vector . In words, we are relaxing our recipe for invariance into finding a data representation such that the optimal classifier, on top of that data representation, is “” for all environments. This turns (3.1) into a relaxed version of IRM, where optimization only happens over :

| (3.5) |

As , solutions of (3.5) tend to solutions of (IRM) for linear .

Scalar fixed classifiers are sufficient to monitor invariance

Perhaps surprisingly, the previous section suggests that would be a valid choice for our fixed classifier. In this case, only the first component of the data representation would matter! We illustrate this apparent paradox by providing a complete characterization for the case of linear invariant predictors. In the following theorem, matrix parametrizes the data representation function, vector the simultaneously optimal classifier, and the predictor .

Theorem 3.2.

For all , let be convex differentiable cost functions. A vector can be written , where , and where simultaneously minimize for all , if and only if for all . Furthermore, the matrices for which such a decomposition exists are those whose nullspace is orthogonal to and contains all the .

Proof.

See Appendix B ∎

So, any linear invariant predictor can be decomposed as linear data representations of different ranks. In particular, we can restrict our search to matrices and let be the fixed scalar . This translates (3.5) into:

| (3.6) |

section 3.3 shows that the existence of decompositions with high-rank data representation matrices are key to out-of-distribution generalization, regardless of whether we restrict IRM to search for rank-1 .

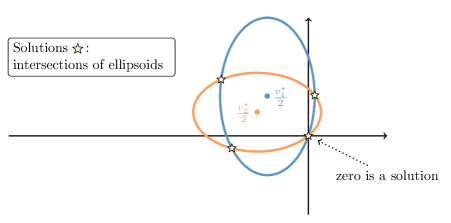

Geometrically, each orthogonality condition in Theorem 3.2 defines a -dimensional manifold in . Their intersection is itself a manifold of dimension greater than , where is the number of environments. When using the squared loss, each condition is a quadratic equation whose solutions form an ellipsoid in . Figure 3.2 shows how their intersection is composed of multiple connected components, one of which contains the trivial solution . This shows that (3.6) remains nonconvex, and therefore sensitive to initialization.

Extending to general losses and multivariate outputs

Continuing from (3.6), we obtain our final algorithm (IRMv1) by realizing that the invariance penalty (3.4), introduced for the least-squares case, can be written as a general function of the risk, namely , where is again a possibly nonlinear data representation. This expression measures the optimality of the fixed scalar classifier for any convex loss, such as the cross-entropy. If the target space returned by has multiple outputs, we multiply all of them by the fixed scalar classifier .

3.2.2 Implementation details

When estimating the objective (IRMv1) using mini-batches for stochastic gradient descent, one can obtain an unbiased estimate of the squared gradient norm as

where and are two random mini-batches of size from environment , and is a loss function.

3.2.3 About nonlinear invariances

How restrictive is it to assume that the invariant optimal classifier is linear? One may argue that given a sufficiently flexible data representation , it is possible to write any invariant predictor as . However, enforcing a linear invariance may grant non-invariant predictors a penalty equal to zero. For instance, the null data representation admits any as optimal amongst all the linear classifiers for all environments. But, the elicited predictor is not invariant in cases where . Such null predictor would be discarded by the ERM term in the IRM objective. In general, minimizing the ERM term will drive so that is optimal amongst all predictors, even if is linear.

From an algorithmic point of view, learning nonlinear invariances is more complicated as well. Let be a subset of functions from to . We say that a penalty enforces -invariance if implies that . Namely, the penalty is 0 implies that is optimal among all the classifiers in . The penalty in (IRMv1) then enforces linear-invariance, or -invariance when is the set of linear classifiers. The way (IRMv1) achieves this by attaining , and this only means if the loss is convex. When is the set of linear classifiers and the loss is the MSE or cross-entropy, this is verified and then the penalty enforces that , i.e. linear invariance. However, if contains nonlinear classifiers, then is in general not a convex function of , which means that the gradient penalty of (IRMv1) would only make a saddle point, of which there can be many meaningless ones [Dau+14, MNG17]. Therefore, figuring out algorithms that enforce -invariance for families containing nonlinear classifiers is a completely open research problem.

We leave for future work several questions related to this issue. Are there non-invariant predictors that would not be discarded by either the ERM or the invariance term in IRM? What are the benefits of enforcing non-linear invariances belonging to larger hypothesis classes ? How can we construct invariance penalties for non-linear invariances?

3.3 Generalizing with Invariance

The introduced IRM principle promotes low error and invariance across training environments . As mentioned before in Theorem 3.1, this is one of the two pieces needed to achieve out of distribution generalization (i.e. low error across ). The missing piece is assumptions and theorems showing when and how invariance across can imply invariance across . So far, we have omitted how different environments should relate to enable out-of-distribution generalization via invariance. The answer to this question is rooted in the theory of causation. However, causality (at least the traditional techniques for causality) will just be our starting point.

In general, we will need two things for invariance across to imply invariance across and to obtain from it low out of distribution error.

-

A.

We will need an underlying unknown invariance to exist. We cannot expect to obtain a low error invariant solution across if there is none.

-

B.

We will need to provide sufficient coverage. This will mean that we will need training environments to be sufficiently diverse, we should have enough of them, and they should respect the underlying invariance (e.g. by having and the above condition).

This chapter is interested in how to formalize these assumptions in different ways, studying when they are satisfied in relevant situations, and how we can leverage them appropriately. In particular, item B can be instantiated in many different ways, and as we will see, this can lead to drastically different sample complexities in terms of the needed number of environments.

The causality literature provides us with a well studied instance of practical interest where these two conditions can be expressed in very clear terms. More precisely, our starting point will be the ideas in the seminal work of [PBM16]. However, we will rapidly depart from the causality language and express everything purely in invariance terms. This is not simply a change in syntax: by doing this we will be able to express everything in purely statistical terms, and quickly build from that to generalize the theory and ideas to nonlinear predictors which work on perceptual inputs, and where all causality and invariance operates at a latent variable level. The central idea at play is that causality, invariance, and out of distribution generalization are equivalent when data satisfies a causal graph. However, invariance can be phrased in purely statistical terms and still allow for out of distribution generalization in a far broader range of settings.

3.3.1 Causal graphs: a starting point for invariance and generalization

We begin by assuming that the data from all the environments share the same underlying Structural Equation Model, or SEM [Wri21, Pea09]:

Definition \thedefi.

A Structural Equation Model (SEM) governing the random vector is a set of structural equations:

where are called the parents of , and the are independent noise random variables. We say that “ causes ” if . We call causal graph of to the graph obtained by drawing i) one node for each , and ii) one edge from to if . We assume acyclic causal graphs.

By running the structural equations of a SEM according to the topological ordering of its causal graph, we can draw samples from the observational distribution . In addition, we can manipulate (intervene) a unique SEM in different ways, indexed by , to obtain different but related SEMs .

Definition \thedefi.

Consider a SEM . An intervention on consists of replacing one or several of its structural equations to obtain an intervened SEM , with structural equations:

The variable is intervened if or .

Similarly, by running the structural equations of the intervened SEM , we can draw samples from the interventional distribution . For instance, we may consider example 2.1 and intervene on , by holding it constant to zero, thus replacing the structural equation of by . Admitting a slight abuse of notation, each intervention generates a new environment with interventional distribution . Valid interventions , those that do not destroy too much information about the target variable , form the set of all environments .

Prior work [PBM16] considered valid interventions as those that do not change the structural equation of , since arbitrary interventions on this equation render prediction impossible. In this work, we also allow changes in the noise variance of , since varying noise levels appear in real problems, and these do not affect the optimal prediction rule. We formalize this as follows.

Definition \thedefi.

Consider a SEM governing the random vector , and the learning goal of predicting from . Then, the set of all environments indexes all the interventional distributions obtainable by valid interventions . An intervention is valid as long as (i) the causal graph remains acyclic, (ii) , and (iii) remains within a finite range.

Condition (ii) can be replaced with assuming that the causal graph stays the same, and one can intervene in the variables not containing . This is akin to saying that the underlying causal structure of the world remains unchanged, while we are able to take actions that affect independently (in the probabilistic sense) some of the variables. However, we found that assumption (while many times reasonable) to be slightly restrictive, since it wouldn’t allow for, say, adding an arrow from a variable to another one . In particular, this could be the case when there’s an intervention of the type “let me copy the value of one variable and input it in another one” (since this would add dependences between the variables), for example by rerouting the flow of a fluid from one city to another.

Condition (iii) can be waived if one takes into account environment specific baselines into the definition of , similar to those appearing in the robust learning objective . We leave this direction for additional quantifications of out-of-distribution generalization for future work.

The previous definitions establish fundamental links between causation and invariance. Namely, finding the causal parents of , finding an invariant predictor across , and generalizing out of distribution across are equivalent. More precisely, one can show that a predictor is invariant across if and only if it attains optimal , and if and only if it uses only the direct causal parents of to predict, that is, . We state and prove this result in Theorem A.1 for the case where we assume the causal graph stays the same and the arrow of is unchanged. The extension to the setup of subsection 3.3.1 is straightforward.

An important comment at this point is that the equivalence, which means that the causal explanation is the only invariant predictor acoss , is only true when allowing all possible interventions that don’t affect . If instead one where to only allow a subset of all possible interventions, this would result in a smaller (in the inclusion sense) , and hence a larger set of invariant predictors, of which the causal one would be one of potentially many more.

The rest of this section follows on these ideas to showcase how invariance across training environments can enable out-of-distribution generalization across all environments.

3.3.2 Generalization theory for IRM

As mentioned before, by Theorem 3.1, two pieces are needed to achieve out of distribution generalization (i.e. low error across ). The first one, privided by IRM, is low error and invariance across . We now examine the remaining condition towards low error across . Namely, under which conditions does invariance across training environments imply invariance across all environments ? We explore this question for linear IRM first.

Our starting point to answer this question is the theory of Invariant Causal Prediction (ICP) [PBM16, Theorem 2]. There, the authors prove that ICP recovers the target invariance as long as the data (i) is Gaussian, (ii) satisfies a linear SEM, and (iii) is obtained by certain types of interventions. Theorem 3.3 shows that IRM learns such invariances even when these three assumptions fail to hold. In particular, we allow for non-Gaussian data, dealing with observations produced as a linear transformation of the variables with stable and spurious correlations, and do not require specific types of interventions or the existence of a causal graph.

Before showing Theorem 3.3, we need to make our assumptions precise. To learn useful invariances, one must require some degree of diversity across training environments. On the one hand, extracting two random subsets of examples from a large dataset does not lead to diverse environments, as both subsets would follow the same distribution. On the other hand, splitting a large dataset by conditioning on arbitrary variables can generate diverse environments, but may introduce spurious correlations and destroy the invariance of interest [PBM16, Section 3.3]. Therefore, we will require sets of training environments containing sufficient diversity and satisfying an underlying invariance. We say that a set of training environments satisfying these conditions lie in a linear general position.

Assumption \theassu.

A set of training environments lie in a linear general position of degree if for some , and for all non-zero :

Terms are defined in Theorem 3.3. Intuitively, the assumption of linear general position limits the extent to which the training environments are co-linear. Each new environment laying in linear general position will remove one degree of freedom in the space of invariant solutions. Fortunately, Theorem A.2 shows that the set of cross-products not satisfying a linear general position has measure zero. Using the assumption of linear general position, we can show that the invariances that IRM learns across training environments transfer to all environments.