∎

Trg Dositeja Obradovića 4, 21000 Novi Sad, Serbia

22email: {svc, jasna.atanasijevic, dusan.jakovetic, natasa}@dmi.uns.ac.rs The authors acknowledge financial support of the Ministry of Education, Science and Technological Development of the Republic of Serbia (Grant No. 451-03-9/2021-14/ 200125)

Tax Evasion Risk Management Using a Hybrid Unsupervised Outlier Detection Method

Abstract

Big data methods are becoming an important tool for tax fraud detection around the world. Unsupervised learning approach is the dominant framework due to the lack of label and ground truth in corresponding data sets, although these methods suffer from lower interpretability and precision compared with supervised approaches. In contrast to prior research works, we examine the possibility of a hybrid unsupervised method for tax evasion risk management that is able to internally validate and explain outliers detected in a given tax dataset. The proposed method, HUNOD (Hybrid UNsupervised Outlier Detection) 111HUNOD is an abbreviation for “Hybrid UNsupervised Outlier Dection”, combines clustering and representation learning for robust outlier detection, additionally allowing its users to incorporate relevant domain knowledge into both constituent outlier detection approaches in order to identify outliers relevant for a given economic context. The interpretability of obtained outliers is achieved by training explainable-by-design surrogate models over internally validated outliers. The experimental evaluation of the HUNOD method is conducted on two datasets derived from the database on individual personal income tax declarations collected by the Tax Administration of Serbia. The obtained results show that the method indicates between 90% and 98% internally validated outliers depending on the clustering configuration and employed regularization mechanisms for representational learning.

Keywords:

tax evasion outlier detection unsupervised learning clustering representational learning explainable surrogate models1 Introduction

Tax evasion and tax avoidance represent a big challenge for authorities in all countries of the world. The loss from tax irregularities is estimated at 3.2% of GDP in OECD countries (Buehn and Schneider, 2016). Tax evasion reduces tax base and related public resources for provision of public goods and erodes fiscal equity. It is empirically proven that grey economy including tax evasion is higher in the countries with a lower level of per capita income (Schneider, 2005). The same literature shows that the level of tax evasion is higher in the countries where the tax system structure implies more reliance on the taxation of production factors, especially on personal income tax, than the taxation of consumption as it is easier to avoid the first type of tax.

The traditional way for improving tax compliance by tax audit is costly and limited in terms of outreach given the huge population of taxpayers and small and expensive capacity of tax controllers in tax administration. The domain knowledge, intuition and experience of tax auditors used for selection of tax payers for audit takes no advantage of rich information set registered in tax administration databases. It is also observed that the digitalization of government services is essential in tax avoidance decrease (Uyar et al., 2021). The recent evolution in data science found its vast applications in tax administrations around the world in support to traditional methods for detecting fraudulent behavior and better use of resources dedicated to tax collection. Large amounts of available tax data also enable development of mathematical models to study and understand tax fraud dynamics (Chica et al., 2021). Machine learning (ML) algorithms on administrative big data sets are increasingly being developed to improve risk management by tax authorities and help prevention and detection of tax evasion cases. However, several challenges remain that have not been completely addressed, as detailed below.

1.1 Motivation and Research Problems

The detection of tax evasion can be effectively approached by methods based on supervised ML techniques. However, those methods require large training datasets containing data instances corresponding to both verified tax evasion cases and regular (compliant) tax behaviour. As indicated in many previous studies reviewed in the related work section, such datasets are usually not available, especially in developing countries. The second problem with supervised ML approaches could be a small number of frauds identified by administrative tax controls that are recorded in the training dataset. If recorded cases are not representative of the entire population then the trained supervised model will be biased, i.e., it will have a high precision, but a low recall.

Due to the lack of availability of labelled data and ground truth that would enable supervised learning, the detection of tax evasion is usually approached by unsupervised ML methods based on anomaly detection algorithms. Compared with supervised approaches, unsupervised methods are less precise: they will not identify only tax evasion cases, but also indicate business entities with irregular and suspicious tax behaviour including also dishonest tax payers. Therefore, unsupervised methods are suitable as a decision support tool in tax evasion risk management systems enabling better prioritization of tax controls and improving efficiency of tax collection. Second, a tax evasion risk management system based on accurate unsupervised learning may lead to a more efficient use of resources when operationally treating identified risks (Sebtaoui et al., 2020).

The focus of this paper is on unsupervised ML methods for identifying suspicious tax behaviour at the level of individual business entities. Such entities can be considered as point anomalies in tax databases, so outlier detection algorithms are the most natural choice in this case. One of the main issues with outlier detection algorithms (and unsupervised machine learning in general) is the validation of obtained results (Goix, 2016). As our primary research problem, we examine the possibility of a hybrid outlier detection method that is able to internally validate identified outliers by combining outlier detection approaches based on radically different machine learning designs.

Most existing anomaly detection studies focus on devising detection models only, ignoring the capability of providing explanation of the identified anomalies (Pang et al., 2021). On the other hand, explainability is of high importance in this context, as it could be used to improve the tax collection and perhaps more importantly, provide guidance for systematic changes in taxation laws. Highly explainable features supported by the domain knowledge can be exploited to target a specific type of risky tax payers in aim to prevent dishonest fraudulent behaviour in declaring taxes. Outlier detection models with explanatory capabilities may increase both ease-of-use and usefulness of task evasion risk management systems (Wang and Lien, 2019). Thus, we investigate how to devise a tax-related outlier detection approach having strong explanatory capabilities.

Finally, it is highly desirable that ML-based fraud detection models offer a systematic way of incorporating and harnessing domain knowledge in the model, rather than adopting a black-box approach, in order to make detection models more robust and precise. Such domain knowledge incorporation should be user friendly in the sense that domain experts need to invest a low-to-moderate-effort manual work to encode prior domain knowledge in the models. Thus, the last research problem examined in this paper is how to devise a hybrid tax-related outlier detection method that can be easily enhanced with relevant domain knowledge.

1.2 Methodological Contributions

In this paper, we propose a hybrid outlier detection method based on unsupervised learning that can incorporate relevant tax-related domain knowledge. The method is abbreviated as HUNOD (Hybrid UNsupervised Outlier Detection) method from now on. The HUNOD method was developed starting from a tax dataset of individual business entities that was derived from tax declarations for all types of personal income.

The HUNOD method independently applies two unsupervised anomaly detection methods: one based on -means to detect outliers from the clustering structure of the data and another based on an autoencoder detecting anomalies according to learned latent representations of non-suspicious tax behaviour. Outliers found by the these two methods are then cross-checked in order to provide a final set of the internally-validated anomalies.

HUNOD allows for a systematic and user-friendly way of incorporating domain knowledge in the outlier detection process. A user incorporates domain knowledge by defining thresholds on relevant scoring indicators prior to learning latent representations and by weighting various data features prior to identifying clustering structures. Those numeric quantities backed by economic theory reflect common business practices related to tax legal framework (e.g. tax arbitrage across different income categories with different tax burden).

An explainable-by-design decision tree model is trained over a surrogate dataset in which data instance are labelled such that internally-validated outliers are separated from other business entities. This last step of HUNOD allows domain experts to externally validate (manually or through other means) identified anomalies. Thus, the main advantages of the proposed method are the following: domain knowledge is incorporated at the very beginning in the method to increase its accuracy, the hybrid nature of HUNOD provides internal validation of identified outliers, while its explainability capabilities support external verification of the outliers by tax experts.

1.3 Case Study

Empirical evaluation of HUNOD is conducted in cooperation with the tax authority of Serbia which has provided a depersonalised dataset of individual tax declarations for the purpose of this research. Serbia is a middle income country with GDP per capita in 2019 of 18,179 international dollars based on purchasing power parity (41% of EU-27 average) and with a relatively high level of tax avoidance. The overall level of the shadow economy (unregistered business transactions) is estimated at about 15.4% of GDP in 2017 using a perception based survey conducted in 2017 (Krstić and Radulović, 2018). The dominant form of shadow economy activity consists of undeclared labor costs, implying the entire or partial payment of salaries in cash. Tax system in Serbia is assessed as very complex and unfair. There is a large number of taxes, personal income from various sources is taxed differently. So, there are many tax breaks available (Schneider et al., 2015). Personal income taxes and contributions represent the major single source of consolidated public revenue (38% in 2020) following by the VAT (25% in 2020). Technically, most declaration and payment of both income tax and mandatory social security contributions is submitted and paid by payer of income (almost 99.9% of all declarations).

1.4 Paper Organization

The remainder of the paper is organized as follows. In Section 2 we present the related work in the area of tax fraud detection and give a short overview of methods dealing with challenges related to the anomaly detection on unlabeled data like low explanation power. We also specify in more details the novelty of the approach presented in this paper in relation to the existing works. The HUNOD method is presented in Section 3 in details. Section 4 contains a description of the dataset used for empirical testing of the method. The obtained results are presented and discussed in Section 5. Section 6 concludes the paper and outlines possible directions for further research.

2 Related Works and Our Contributions

According to the type of ML technique employed, existing ML-based methods to identify tax evasion, tax avoidance or more broadly suspicious tax behaviour can be divided in three categories: supervised, semi-supervised and unsupervised. Contrary to unsupervised methods, supervised and semi-supervised methods require training datasets in which previous cases of unwanted tax behaviour are entirely or partially indicated.

2.1 Supervised Methods

To the best of our knowledge, the first application of supervised machine learning techniques to the problem of fiscal fraud detection can be found in the work of Bonchi et al. (1999). The authors examine C5.0 algorithm for learning decision tress to build a classification model for detecting tax evasion in Italy. Other supervised machine learning approaches for detecting fraudulent tax behavior investigated in the literature include random forests (Mittal et al., 2018), rule-based classification (Basta et al., 2009) and Bayesian networks (da Silva et al., 2016).

A VAT screening method to identify non-compliant VAT reports for further auditing checks is proposed by Wu et al. (2012). The method utilizes the Apriori algorithm for extracting association rules from a previously formed database of business entities that were involved in VAT evasion activities. The method is evaluated on non-compliant VAT reports in Taiwan in the period 2003-2004 with 3780 confirmed VAT evasion cases. The accuracy rate of identified association rules is estimated to approximately 95% using the 3-cross validation technique. The idea of using the Apriori algorithm for identifying a set of pattern characterizing fraudulent tax behavior is also explored by Matos et al. (2015) with addition of dimensionality reduction techniques (Principal Component Analysis and Singular Value Decomposition) to reduce a set of fraud indicators and create a fraud scale for ranking Brazilian taxpayers.

Both unsupervised and supervised machine learning techniques for identifying suspicious tax-related behaviour are analysed in (Castellón González and Velásquez, 2013). Two clustering techniques, self-organizing maps and neural gas, are applied to identify groups of business entities with similar tax-related behaviour in two datasets encompassing micro to small and medium to large enterprises from Chile in the period 2005-2007. Three classification learning algorithms (decision tree, neural network and Bayesian network) are then employed to construct classifiers detecting fraudulent behaviour. The evaluation showed that the examined classification techniques are able to reach the accuracy of 92% and 89% for micro to small business and medium to large enterprises, respectively. The article also summarizes machine learning practices for detecting tax evasion employed by governmental agencies that were not documented in the academic literature before.

A transfer learning method for tax evasion detection based on conditional adversarial networks is introduced in (Wei et al., 2019). The main idea is to utilize an adversarial learning to extract tax evasion features from a labeled dataset. The trained neural network is then applied to an unlabeled dataset. The transfer learning approach is tested on five tax datasets corresponding to five different Chinese regions.

Zumaya et al. (2021) analyze tax evasion on a large-scale dataset of electronic records regarding taxable transactions in Mexico by applying tools from network science and machine learning. In more detail, the authors develop network-based models and, exploring properties of network neighborhoods around known tax evaders, demonstrate that the evaders’ interaction patterns differ from those of the majority of contributors. Using this insight, the authors use deep neural networks and random forests to classify other contributors as potential suspects of tax evasion.

2.2 Semi-supervised Methods

The problem of tax evasion detection is also approached by semi-supervised and weakly-supervised learning methods. Kleanthous and Chatzis (2020) proposed a semi-supervised method for VAT audit case selection based on gated mixture variational autoencoder networks.

The method proposed by Wu et al. (2019) is based on positive and unlabeled (PU) learning techniques. PU techniques are applicable to datasets in which only a small subset of data instances is positively labeled and the rest are not annotated at all. The method by Wu et al. (2019) combines random forest to select the most relevant features, one-class probabilistic classification to assign pseudo-labels to unlabeled data instances and LightGBM as the final supervised model trained on pseudo-labeled data.

Mi et al. (2020) also explored PU learning for detecting tax evasion cases. The proposed method additionally incorporates features obtained by embedding a transaction graph into an Euclidean space.

The work by Gao et al. (2021) further improves the method by Mi et al. (2020). More concretely, the authors present PnCGCN – a novel graph embedding algorithm for transaction graphs. PnCGCN is utilized to extract network-based features prior to assigning pseudo-labels to unlabeled data instances. In the final stage, a multilayer perceptron neural network is trained on pseudo-labeled data to identify tax evasion cases.

2.3 Unsupervised Methods

The article by de Roux et al. (2018) emphasizes the importance of unsupervised machine learning methods for tax fraud detection due to intrinsic limitations of tax auditing processes. An unsupervised method for detecting under-reporting tax declaration based on spectral clustering is proposed. The probability distribution of declared tax bases is computed for each identified cluster. Suspicious tax declarations in a cluster are then identified using a quantile of the corresponding probability distribution. The method is experimentally evaluated on a dataset encompassing tax declarations of building projects in Bogota, Columbia. Spectral clustering to detect tax evaders is also explored by Mehta et al. (2020). Besides features derived from individual tax returns, in the clustering procedure, a feature derived from a graph showing business interactions among taxpayers is also included. This graph-based feature is computed by the TrustRank algorithm (a variant of the PageRank algorithm) to the constructed graph. The method is experimentally evaluated on tax declarations in India collected in the period 2017-2019.

Tian et al. (2016) introduces graph-based techniques for mining suspicious tax evasion groups in big datasets. A method for fusing a complex heterogeneous graph called Taxpayer Interest Interacted Network (TPIIN). TPIIN is enhancing a trading graph for a set of companies by investment relationships between them, influence relationships between persons and companies, and kinship relationships between persons. Suspicious tax evasion groups are then detected as subgraphs of TPIIN consisting of simple directed trails having the same start and end nodes without any trading link between intermediate nodes belonging to different trails.

A method for detecting accounting anomalies in journal entries exported from ERP (Enterprise Resource Planning) information systems is presented in (Schreyer et al., 2017). It is is based on autoencoder networks and, to the best of our knowledge, it is the first application of deep learning techniques to detect anomalies in large scale accounting data. The application of autoencoders for detecting suspicious journal entities in financial statement audits is also explored by Schultz and Tropmann-Frick (2020).

The article by Vanhoeyveld et al. (2020) investigates the applications of lightweight unsupervised outlier detection algorithms to VAT fraud detection. The two outlier detection algorithms, fixed-width anomaly detection and local outlier factor, applied to VAT declarations of ten business sectors in Belgia are analysed. The analysis of lift and hit rates of examined methods showed that simple and highly scalable outlier detection methods can be very effective when identifying outliers in sectoral VAT declarations.

2.4 Our Contributions

Previous relevant research works clearly indicate that the applicability of supervised ML approaches to detect tax evasion is conditioned by training datasets containing a significant number of confirmed tax evasion cases. Such datasets are not always available since they result from extensive and costly tax auditing processes. Thus, unsupervised and semi-supervised ML techniques (when available data contains a small number of confirmed tax evasion cases) are still dominant approaches to detect tax evasion in tax databases. Some of the proposed methods (in all three categories) rely on graph-based features derived from transaction graphs. Those methods can be applied only if data describing transactions between business entities is available.

In this paper we propose a hybrid unsupervised method to detect anomalies in tabular tax datasets without special restrictions or requirements on features describing business entities. Our method combines clustering (-means) and representational learning (autoencoders) to devise a set of internally validated outliers. As the literature review shows, both clustering and autoencoders were used in previous relevant research works as techniques to identify outliers in tax datasets. However, none of prior research proposed an unsupervised method for detecting internally validated outliers in tax datasets nor examined any kind of synergy of those two particular outlier detection approaches.

Furthermore, existing unsupervised outlier detection approaches for tax datasets do not incorporate domain knowledge into their decision models. In HUNOD, both constituent outlier detection algorithms are enhanced by relevant domain knowledge: (1) feature weights given by an economist familiar with tax related business practices that indicate feature relevance for fraudulent tax behaviour are incorporated into -means prior to identifying clusters of business entities, and (2) the training dataset for the autoencoder is formed by selecting a subset of business entities according to a scoring indicator reflecting the degree of non-suspicious tax-related behaviour.

Compared with previous autoencoder-based approaches, the inclusion of domain knowledge in HUNOD and its hybrid nature additionally improve the robustness of the HUNOD autoencoder:

-

1.

The HUNOD autoencoder is not trained on the whole dataset, but on a subset of business entities for which we can be quite confident in their regular tax-related behaviour. This has two important consequences: (1) the identified latent representations are more robust since they are learned only on negative examples, and (2) it is not necessary to define a threshold when deciding whether a test data instance is an outlier (the maximal autoencoder error on the training dataset is a natural decision boundary).

-

2.

K-means is instrumented to verify that the training dataset does not contain structural-based outliers (data instances located in small clusters).

It is also important to observe differences between HUNOD and previously proposed semi-supervised approaches based on PU learning: the HUNOD autoencoder is trained on negative examples (regular tax behaviour), whereas PU models are trained on positive examples (tax evasion cases) that are less frequent than negative examples (it is natural to expect that a model trained on bigger data would be more robust). Second, our method does not require any positive examples.

The issue of explainability of unsupervised anomaly detection techniques, although indicated in general literature as a big challenge Pang et al. (2021), was never thoroughly investigated in research works applying those techniques to tax datasets. Our HUNOD method relies on surrogate decision trees that are able not only to provide explanations for individual outliers, but also to rank features according to their power to indicate outliers.

Finally, the available empirical literature on tax fraud detection mostly focuses on VAT tax (or similar indirect tax like sales tax used in some countries) data analysis. These datasets usually cover a small number of features extractable from tax declarations for this type of tax. In our case study we apply the HUNOD method to datasets of business entities in Serbia derived from individual personal income tax declarations. To the best of our knowledge, there is no prior research on tax fraud detection using machine learning approaches to the personal income tax.

3 The HUNOD Method

The method we propose combines unsupervised clustering and representational learning algorithms additionally incorporating relevant domain knowledge into the used unsupervised algorithms and enhancing the interpretability of detected outliers by training supervised, explainable-by-design surrogate models over the results of unsupervised learning algorithms.

An outlier is a data instance that is significantly different from vast majority of other data instances. Considering the clustering structure of a dataset, outliers are data instances located in small and distant clusters. The main issue with the clustering approach to outlier detection is how to set thresholds below which a cluster is considered small and distant. With reasonable upper bounds for size and distance thresholds, a clustering algorithm such as -means yields a broad set of data points that contain all outliers, but also data points that are not outliers. In other words, a clustering-based outlier detection model can have a very high or even the perfect recall at the cost of a low precision. The second constituent component of HUNOD is an autoencoder – a representational learning (deep) neural network. The HUNOD autoencoder learns latent data representation of desirable tax behavior, i.e. it is trained on data points that are the most representative examples of compliant tax behavior selected according to the domain knowledge. Contrary to -means, the autoencoder-based outlier detection model is able to reach a high precision since it is a trained model. The precision of the autoencoder model can be verified and additionally improved by checking its results against the clustering model: false positive decisions made by the autoencoder can be accurately identified since the clustering model has a very high or perfect recall.

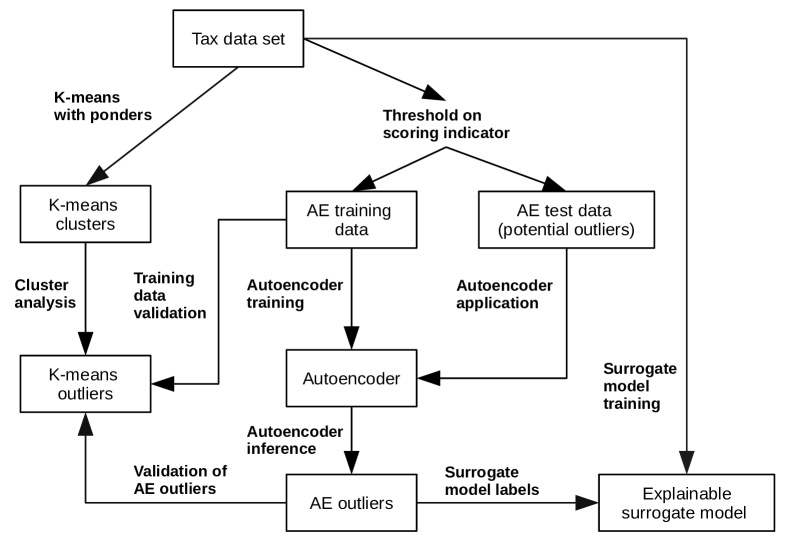

The constituent components of the method and the corresponding dataflow are schematically illustrated in Figure 1. A modification of -means incorporating relevant domain knowledge in terms of feature weights is used to detect a broad set of outliers. This part of HUNOD is described in Section 3.1. A domain-knowledge scoring indicator is then utilized to identify a subset of business entities for which we can state non-suspicious tax related behavior with a very high confidence. The instances in this subset constitute the training dataset for an autoencoder. The training dataset for the autoencoder is validated by cross-checking with outliers identified by -means with ponders. The autoencoder is then applied to all instances that are not in the training dataset to identify a narrower set of outliers. The set of outliers identified by the autoencoder is also verified against outliers detected by -means with ponders. This whole process is explained in Section 3.2. In the final step of HUNOD method the input dataset is extended by a binary feature indicating whether the corresponding instance is an outlier by the autoencoder. A decision tree is trained on this extended dataset in order to obtain the explainable surrogate model for detected outliers, Section 3.3.

Throughout this section, we assume that the input tax dataset, denoted by , is composed of instances (business entities) described by real-valued attributes or features, denoted by to , where is the total number of features. This means that present categorical features are converted into real-valued features by employing the one-hot-encoding transformation prior to the application of our hybrid outlier detection method.

3.1 -means with Ponders

The hybrid outlier detection method instruments the -means clustering algorithm (Lloyd, 1982; MacQueen, 1967) to detect a broad set of potential outliers in . For a given , the -means algorithm identifies clusters in using a previously specified distance function (e.g., the Euclidean or Manhattan distance). The algorithm starts with selecting random data points in the space of (i.e, a box of dimension bounding all instances in ) which serve as cluster centroids. Then, all instances in are assigned to the closest centroid and the centroids are recomputed according to the assignments. The previous step is repeated either a fixed number of iterations or until centroids stabilize.

The HUNOD method incorporates domain knowledge in the -means clustering by introducing ponders or feature weights. The ponders are assigned by a tax expert according to her/his assessment of feature importance for outlier detection. In our realization of the -means clustering with ponders, the distance between two instances and is computed by introducing weights to the Euclidean distance:

| (1) |

where is the weight of feature and is the value of feature for instance after feature scaling to the unit interval. The main benefit of such defined distance function is that it enables the reduction of -means with ponders to -means without ponders by simple transformations of (see Algorithm 1). Consequently, existing and verified implementations of -means can be reused when realizing -means with ponders. The -means implementation from the scikit-learn Python library (Pedregosa et al., 2011) is used in our realization.

Clusters identified by -means with ponders are then analyzed to identify outliers. In the first step, clusters are classified either as small or large, depending on the value of parameter : a cluster having less than instances is considered as small, otherwise it is large. The default value of is 5% of the total number of instances in . Clearly, potential outliers are located in small clusters that are far away from large clusters. Thus, for each small cluster we compute the outlierness score according to the following formula:

| (2) |

where is the set of large clusters and the distance between centroids is computed by (1). -means with ponders also has a parameter which is the maximal number of outliers returned by the algorithm. The default value of this parameter is 5% of the total number of instances in . The small clusters are sorted in descending order of the outlierness score. The instances from the first clusters in the sorted sequence are selected as outliers, where is the largest index such that the total number of instances in the first clusters is smaller than or equal to .

3.2 Autoencoder-based Outlier Detection

The central part of HUNOD method is the training and application of an autoencoder outlier detection. The autoencoder is a feed-forward neural network trained to reconstruct values of an input set of features at the output layer through a series of hidden layers. This implies that the number of neurons in the input layer of the autoencoder is equal to the number of neurons in its output layer. Each hidden layer contains a specified number of nodes (neurons). Each node accumulates inputs from all nodes in the previous layer that are multiplied by weights of edges connecting nodes, adds a bias value to the accumulated input and applies an activation function to the accumulated input to produce its output. Edge weights and biases are trainable model parameters. The first layers of the autoencoder represent an encoding function transforming an instance (input values) into a lower-dimensional representation, while the rest of the layers act as a decoding function transforming the obtained lower-dimensional encoding into original input values.

In common outlier detection applications, the autoencoder is trained on all instances in a given dataset, and the instances with the highest reconstruction error are selected as outliers (Hawkins et al., 2002). In our approach, the autoencoder is trained on a subset of instances in selected according to a scoring indicator derived from domain knowledge. The scoring indicator is a function computed on input features (or a subset of them) indicating the degree of non-suspicious tax related behaviour of the corresponding business entity. The details on the scoring indicators we use are presented in (Atanasijević et al., 2019). The hybrid outlier detection method trains the autoencoder on instances with high values of the scoring indicator (values above a threshold that is assigned by a tax expert). In other words, the autoencoder is trained on those business entities for which there is a high confidence that their tax related behaviour is not suspicious. Additionally, the accuracy of the training dataset is estimated by cross-checking with outliers detected by -means with ponders motivated by the fact that instances in the training dataset should not be outliers detected by some other outlier detection method.

Let denote a subset of encompassing instances whose values of the scoring indicator are above the specified threshold, the number of autoencoder layers (indexed from 1 to ), the vector of input values for layer and the vector of output values from layer . The feed-forward operation of the autoencoder for an instance from then can be recursively defined as

| (3) |

for each hidden node and layer . As above, is the value of -th feature of the instance , while is a non-linear activation function, e.g. sigmoid or rectified linear unit (ReLU) . The weights of autoencoder edges and biases are learned by minimizing a loss function considering instances in . HUNOD method uses the mean squared error (MSE) for the loss function

| (4) |

where is the reconstruction error of instance

| (5) |

The trained autoencoder is then applied to all instances in . An instance is marked as an outlier if the reconstruction error for is higher than the maximal reconstruction error on the training dataset

| (6) |

Moreover, the reconstruction error can be viewed as the outlierness score for . All outliers detected by the autoencoder are then verified against outliers identified by -means with ponders.

To prevent overfitting we include also dropout (Srivastava et al., 2014) and activation regularization (Wu et al., 2018) mechanisms into autoencoder training. Both mechanisms increase the sparsity of the autoencoder: the dropout by ignoring randomly selected neurons during training and the activation regularization by introducing an activation penalties into the loss function. With the dropout included equations (3) change to

| (7) |

where denotes any autoencoder edge, is a vector of independent Bernoulli random variables at layer , is the probability that an edge is not discarded () and represents the element-wise product operation. With the activation regularization, the loss function (4) becomes

| (8) |

where denotes the set of neurons in layer and is the regularization factor.

In HUNOD method, the Tensorflow framework (Abadi et al., 2016) is used for training the autoencoder and instrumenting it to perform outlier detection inference. The whole procedure is shown in Algorithm 2. The autoencoder is built from the Tensorflow sequential neural network model by adding the specified number of hidden layers. The default values of the regularization hyperparameters are and . The activity regularization can be excluded by setting to 0. The loss function is optimized using the Adam optimization algorithm (Kingma and Ba, 2015) in a given number of epochs (the number of forward and backward passes of through the autoencoder to optimize model parameters – edge weights and biases) and batch size (the number of instances processed to update model parameters). The default values of the autoencoder hyperparameters are and . The activition function is set to ReLU,

-

– the set of outliers detected by the autoencoder

-

– the confidence in the training dataset estimated using

-

– the confidence in estimated using

3.3 Explainable Surrogate Model

In the final step of the hybrid outlier detection method, outliers detected by the autoencoder (and cross-checked against -means with ponders) are used to extend the input dataset by an extra binary class feature . All instances identified as outliers are marked to belong to the positive class (), while other instances are assigned to the negative class (). An explainable-by-design surrogate model performing binary classification is then trained on the extended dataset. The design of the surrogate model shows common characteristics of outliers identified by the autoencoder in terms of feature values. Additionally, the surrogate model enables us to rank features according to their discriminative power to separate outliers from non-outliers.

Classic decision trees (Quinlan, 1986) are instrumented in our work as explainable surrogate models for outliers identified by the autoencoder. Each non-leaf node in the binary decision tree is a relational expression involving one feature and a constant value (e.g., where denotes a real-valued feature). Two edges emanates from each non-leaf node: the left edge is activated if the relational expression evaluates to false, otherwise the right edge is activated. The activated edge leads either to a leaf node or some other non-leaf node. Leaf nodes of the decision tree represent classes. A path from the root node to a leaf node through activated edges for a given input instance then explains how it is classified and which criteria it satisfies to be assigned to the class represented by the leaf node. In a -ary decision tree, the nodes represent features, while edges are relational expressions. Clearly, each -ary decision tree can be converted to an equivalent binary decision tree.

A decision tree for a given labeled dataset can be constructed by a recursive divide-and-conquer algorithm guided by a splitting function. For a feature and a relational expression involving , the splitting function measures the extent to which the splitting of by produces “pure” splits in terms of class frequencies (a split is pure if it contains only instances belonging to the same class). The splitting function utilizes a function measuring the purity of a dataset. Two commonly used approaches are the Gini impurity and the entropy (Suthaharan, 2016). In the binary classification setting (which is the case for our surrogate models), those two measures are defined as

| (9) |

where and are the fractions of positive and negative instances in , respectively. Clearly, Gini() = 0 or Entropy() = 0 implies that all instances in are from the same class (either positive or negative). Secondly, smaller values of both measures indicate a higher degree of purity.

The splitting function measures the change in the impurity of after splitting by , where is or a subset of obtained after applying one or more splitting operations:

| (10) |

where is a dataset impurity measure (e.g., Gini or Entropy), are instances from not satisfying , and is the fraction of instances in split , , . Now, an algorithm Binary Decision Three, BDT() for building the decision tree on can be formulated as follows:

-

•

If contains only one feature or all instances in belong to the same class then return a leaf node with the dominant class in .

-

•

Otherwise, find a relational expression leading to the highest .

-

•

Split according to to obtain and .

-

•

Make a node in the decision tree corresponding to .

-

•

Make recursive calls BDT() and BDT() to create the left and right subtree for , respectively.

Since is computed for each node in the decision tree, the importance of feature for the classification process imposed by the decision tree can be defined as the sum of values of nodes associated to normalized by the sum of values for all nodes in the tree.

The implementation of the decision learning algorithm from the Scikit-learn library (Pedregosa et al., 2011) is used in the HUNOD method to learn explainable surrogate models. The HUNOD method executes the Scikit-learn decision tree learning algorithm using its default parameters as given in the Scikit-learn library: (1) the best splits are determined by the Gini impurity measure, (2) the number of internal and leaf nodes and the maximal depth of the resulting decision tree are not bounded to some predefined values, and (3) the minimal number of instances to perform splitting is equal to 2. The Scikit-learn library is additionally utilized to evaluate the surrogate model on the training data by computing the accuracy score. The accuracy score is the number of correct classifications divided by the total number of instances on which the classification process is performed. Clearly, a reliable surrogate model must have the accuracy score on the training dataset equal to 1. In other words, the trained surrogate model has to be able to predict the same outliers as the autoencoder prior to providing explanations for particular outliers in terms of feature values.

4 Experimental Dataset

The experimental dataset is derived from the database on individual personal income tax declarations collected by the Tax Administration of Serbia. According to the ruling legal framework, the individual tax declaration for personal income is typically submitted by the payer of income. There is about 0.1% of all declarations relating to 0.001% of individuals in the observed data where an individual which is a receiver of income has submitted the tax declaration (e.g. when income is received from abroad) and these cases are not included in our experimental dataset. An individual tax declaration consists of data on payer of income ID (tax identification number, TIN), receiver of income ID (personal identification number, PID), date of income payment, date of declaration, date of payment of tax and contributions, type of income, gross amount of income, amount of paid tax and mandatory contributions for health insurance, pension insurance and unemployment insurance. Type of income refer to different types of personal income that are subject to personal income tax and mandatory contributions for social insurance. These types of income are: salary, sick leave compensations, dividend, interest, rent, authors income, temporary work assignment and one-off performance service contract. Additionally, the data on individual income payer (TIN) is accompanied with data on its sector of prevalent economic activity (NACE code), location of headquarter, date of establishment. Moreover, an individual income receiver is described by gender, age and its residency location municipality code.

In order to investigate tax fraud which is predominantly the activity performed by payer of income, the original dataset is transformed to show the business entity (TIN) level aggregated attributes on monthly level. In our experimental dataset, we observe all different TINs appearing in tax declarations along 13 months period (from March 2016 to March 2017). We excluded from the dataset public administration organizations, some non profit associations and one large state energy company which is a public monopoly. In this way we obtained the empirical dataset consisting of ca. 22 million data fields.

The final dataset covers 179,489 different business entities (TINs) which are mostly enterprises. We observe 224 different features for each TIN. Three features describe TINs status and don’t change over time. These are industry code and organization form which are represented by as many binary variables as there is different values (422 different industry codes and 24 different organizational forms) as well as the age of TIN being the difference between the year of establishment and the observed year. Other features are derived as different statistics calculated on the TIN level using original tax declaration data for each month. As these values are changing over time, each of thirteen months of the observed period represent a distinct feature. Therefore the 221 features can be observed as 17 differently defined features using the individual tax declaration data submitted by one TIN in one month each appearing as 13 different features denoted by adding YmN in the name of the feature, where Y is year and N is month number. These 17 different feature definitions aim to capture some of the relevant characteristics of TINs.

The definition of these features, though limited by the availability of data in original tax declaration, is largely motivated by the existence of some background theory so that the features can represent a good foundation for capturing risky behavior in terms of tax avoidance and tax evasion.

We can observe these 17 variables under the four categories: characteristics of the distribution of paid salaries, capital vs. labor income, overall tax and fiscal burden and characteristics of individuals that are paid by a business entity (TIN) either as employees (for which salary is paid) or as other type of contracts generating personal income. As the features may have somewhat different meaning for small business entities (e.g., micro enterprises) and large business enterprises, we divide the database into two subsets with a cutoff at 10 employees.

4.1 Salary Distribution Features

For the characteristics of the distribution of paid salaries within one business entity, we use mean, median and standard deviation of paid salary by a business entity in one month (features named average salary YmN, median salary YmN, stdev salary YmN). The rationale behind including these features is that market forces and characteristics of specific business (like technology and other industry specifics) should result in convergence of the composition and a level of salaries at the level of a business entity. Therefore, identified anomalies could indicate undeclared workers and/or underreported income of declared employees.

Next feature incorporating a domain knowledge is also related to the shape of the entity level distribution of salaries. It aims to capture the possibility for tax arbitrage and reduction of the overall fiscal burden on the business entity level. The salaries are divided into 26 bins, each bin with 10% of increase. The tax rules contain a cap on basis for mandatory social insurance (health, pension and unemployment) defined as five time average salary for the period and that amount is in the 26th bin. Thus a firm can use this rule as an opportunity to declare a few well paid individual salaries and to use these large but properly taxed salaries for cash payment of salaries of undeclared workers. We define this feature (named fraction b26r in YmN) as follows

where is the sum of salaries below the defined threshold, in our case sum of the salaries in the first 25 bins of the distribution, and is the sum of salaries in the 26th bin of the distribution, i.e. the sum of excessively large salaries.

4.2 Capital-Labor Ratio Features

Captial-labor featurs are based on the ratio , where are dividends paid to owners, or other type of owners income resulting from profit, while is the sum of paid salaries and paid profit by the same business entity in one month (feature named capital labor YmN). The economic rationale behind this feature is to capture the extensive tax arbitrage given the fact that there is a significant difference in overall fiscal burden on gross salary and paid dividend to owners. Therefore, firm owners sometimes opt for paying extensive profit (after paying a relatively low corporate income tax) and use the money to pay undeclared employees in cash. As profit is usually not distributed by regular monthly payments, unlike labor income i.e. salaries, one additional feature is calculated on the aggregated yearly level (feature capital labor 12m). On the other hand, one would expect that firms operating in a relatively competitive market and using a similar technology, should register the same capital/labor ratio which is optimal in terms of profit maximization (as described in economic theory like Solow’s growth model (Solow, 1956)).

4.3 Tax and Fiscal Burden Features

We defined three features to capture the overall effect of a potential underreporting of income by a business entity or a tax arbitrage: fiscal burden of salaries fbs YmN, tax burden of salaries tbs YmN, and overall fiscal burden of all type of income, fball YmN. The fiscal burden of salaries is calculated as the ratio of the sum of all paid duties by a business entity including tax and social contributions and the sum of gross salaries paid in the same month. This feature, also known as tax wedge, is perceived as particularly high and burdensome by employers (Schneider et al., 2015) and represent an important incentive for tax evasion with the aim to lower it. Tax burden of salaries is calculated in the same way as a previous feature but includes only paid taxes in numerator. It is worth mentioning that there is much less diversity in terms of taxing of salaries than in terms of obligatory social security regimes and therefore there is a logic to include this feature. The third feature of this type refer to overall fiscal burden on the business entity level. It is computed as where is the sum of all paid taxes and contributions by a business entity for all type of paid personal income in one month and is the sum of related gross income in the same month. This last indicator possibly captures if there is a tax arbitrage between various type of income. As already mentioned in Introduction, there is a complex and diverse set of taxation regimes with uneven rates across different types of income (Schneider et al., 2015). Although some tax arbitrage can be considered as a rational economic behavior and in line with the legal framework, an extremely low fiscal burden on the business entity level can be a reflection of an excessive arbitrage or tax evasion and can signal a tax related risky behavior by business entity.

4.4 Features Reflecting Structure of Income Receivers

The last category of features include: number of different individuals for which an entity pays salary in a given month (total employees in YmN), number of different individuals for which an entity pays any kind of income in a given month (total persons in YmN), average age of all individuals for which an entity pays any kind of income in a given month (feature named avg age in YmN) and seven similarly designed features capturing average age of different individual paid by the same business entity in a given month for different income categories. These are salaries, sick leave compensations, owners income, service contract fee, rent, author contract fee and other types of income (features named avg age salary in YmN, avg age sick leave in YmN, avg age service fee in YmN, avg age rent in YmN, avg age owner income in YmN, avg age author in YmN, avg age other in YmN).

The last set of features is interesting from tax fraud detection perspective in terms of its dynamics through 13 distinct features – one for each consecutive month of the observed period. The idea is to capture the unusual dynamics (e.g. sparce payments) which can signal a potentially fraudulent behavior. Moreover, the feature representing the average age of employees is expected to be related to the level of paid salaries (captured by the first group of features) as it is a proxy for job experience being one of two main determinants of the earning equation as evidenced by the relevant empirical and theoretical literature (Mincer, 1974; Heckman et al., 2003).

5 Results and Discussion

The HUNOD method is evaluated on two independent subsets of the experimental dataset. The first subset, denoted by , encompasses business entities with less than 10 employees. The second subset, denoted by , contains business entities having 10 or more employees. The number of instances in and are 159744 (89.57% of the total number of instances) and 18611 (10.43%), respectively.

In our experiments, -means with ponders is applied using the following pondering scheme given by a tax expert: all features associated to fiscal burden on paid gross salaries have weights equal to 10, a factor of 5 is given to all features associated to salaries and overall fiscal burden on paid gross income, while weights of other features are equal to 1.

The average of all thirteen overall fiscal burden on paid gross income (fball YmN) by business entity is instrumented as the scoring indicator to form the training dataset for the autoencoder for both and . Business entities with the average overall fiscal burden on paid gross income higher than 30% of the paid gross income can be considered non-suspicious with respect to their tax behavior and such entities are selected as training instances. The total number of training instances in is 31533 (19.74% of size), while the total number of training instances in is equal to 267 (1.43% of size).

5.1 Outliers by -means with Ponders

The first step in our experimental analysis of the hybrid outlier detection method is the evaluation of -means with ponders. The cluster structure of and datasets is examined for K taking values in {10, 15, 20, 25, 30}. For both datasets, the threshold for separating small from large clusters is set to 5% of the total number of instances. The maximal number of outliers returned by the algorithm is 1% for (larger dataset containing 159744 instances) and 5% for (smaller dataset containing 18611 instances).

Characteristics of small clusters identified by -means with ponders are summarized in Table 1. It can be observed that a majority of clusters, except for when is equal to 10, are actually small clusters. Additionally, the number of instances in small clusters increases with K. Table 1 also shows the number of small clusters containing outliers and the fraction of outliers for previously mentioned thresholds limiting the maximal number of outliers. All outliers detected in belong exactly to one small cluster for all examined values. The outlierness score of the cluster containing outliers varies between 11.68 and 11.93. The second largest outlierness score is less than 6 implying that has a small cluster very distant from other large clusters. Contrary to , outliers in are contained in more than one cluster for .

| dataset | dataset | |||||||

|---|---|---|---|---|---|---|---|---|

| K | SC | SCS [%] | SCO | Outliers [%] | SC | SCS [%] | SCO | Outliers [%] |

| 10 | 7 | 23.68 | 1 | 0.84 | 4 | 11.44 | 1 | 3.74 |

| 15 | 13 | 44.16 | 1 | 0.83 | 8 | 19.73 | 2 | 4.65 |

| 20 | 17 | 45.74 | 1 | 0.82 | 14 | 30.42 | 2 | 4.39 |

| 25 | 22 | 55.43 | 1 | 0.81 | 21 | 43.58 | 2 | 3.49 |

| 30 | 28 | 59.86 | 1 | 0.81 | 25 | 44.96 | 2 | 3.58 |

To compare outliers obtained for different values we compute the Jaccard coefficient for each pair of results. For two sets of results and this coefficient is defined as

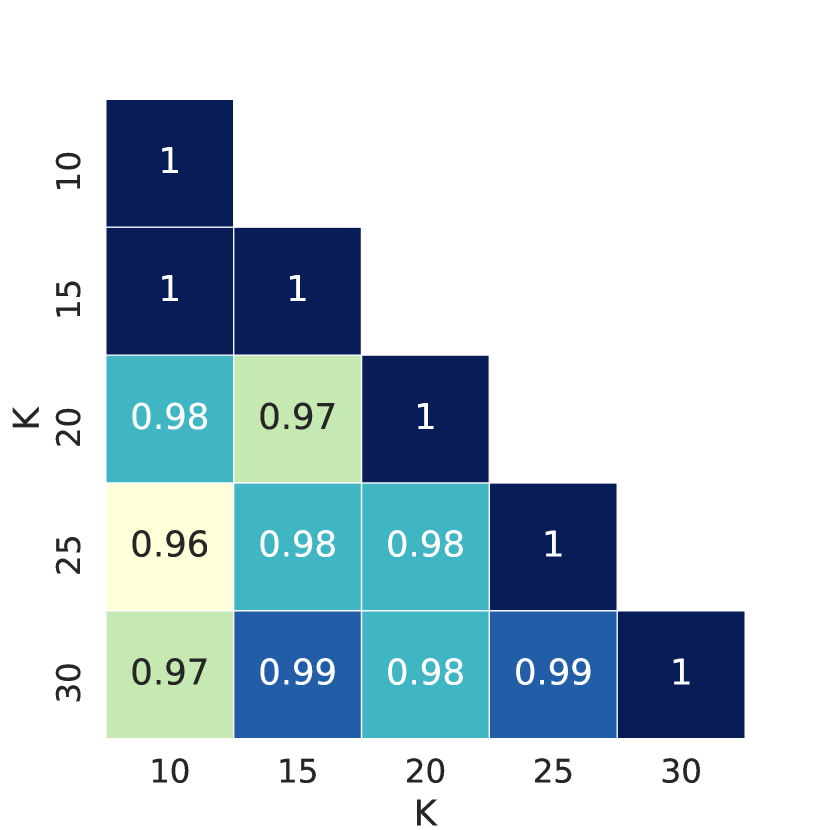

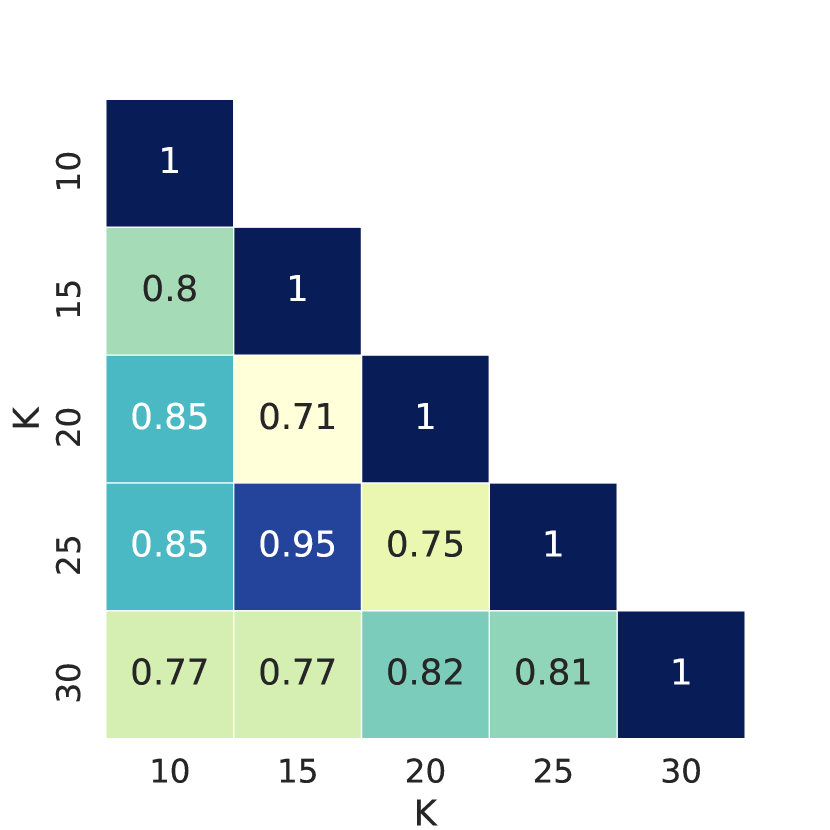

| (11) |

The obtained values of the Jaccard coefficient are shown in Figure 2. It can be seen that -means with ponders applied on identifies almost identical outliers for different values. The minimal value of the Jaccard coefficient for is 0.71 implying that -means with ponders exhibits a high degree of robustness to variations of the parameter .

5.2 Outliers by Autoencoder and Surrogate Model

In the second experiment we examine outliers identified by the autoencoder and the accompanying surrogate models. The autoencoder is configured to the following parameters:

-

•

three hidden layers containing consecutively , and neurons ( denotes the total number of features),

-

•

the number of epochs is 200 with the batch size of 32 instances, and

-

•

the dropout probability is set to 0.2 and the regularization parameter

The training dataset for the autoencoder and outliers identified by it are cross-checked against outliers detected by -means for various values (the same values as in the experiment described in part 5.1).

The total number of outliers identified by the autoencoder in dataset is 155, which is 0.097% of the total number of instances in . For dataset, the number of outliers is equal to 137 (0.736% of the instances in ). Thus, the first conclusion that can be derived from this result is that the autoencoder identifies a significantly smaller number of outliers than -means with ponders. Let denotes a set of outliers revealed by -means with ponders for a fixed . Table 2 summarizes the results of the cross-check against showing two quantities:

-

1.

– the fraction of autoencoder training instances that are in , and

-

2.

– the fraction of outliers detected by the autoencoder that belong to .

In case of dataset, less than 5.5% of autoencoder training instances are in for various K values. This fraction can be considered small, especially having in mind that approximately 20% instances in constitute the training dataset for the autoencoder. For dataset, we have that less than 2.6% of instances in the dataset for training the autoencoder are -means outliers. Thus, it can be concluded that the training dataset in both cases contains a negligible number of instances that were identified as outliers by -means with ponders. This further implies that the training dataset for the autoencoder, formed according the criterion coming from the domain knowledge, can be considered valid due to a high degree of consistency with an independent outlier detection approach.

| dataset | dataset | |||

|---|---|---|---|---|

| K | ||||

| 10 | 0.053 | 0.987 | 0.015 | 0.908 |

| 15 | 0.041 | 0.987 | 0.026 | 0.931 |

| 20 | 0.055 | 0.987 | 0.022 | 0.931 |

| 25 | 0.046 | 0.987 | 0.022 | 0.908 |

| 30 | 0.041 | 0.987 | 0.022 | 0.915 |

Regarding the validation of autoencoder based outliers by -means with ponders, it can be observed that

-

1.

98.7% of autoencoder based outliers are in for dataset, and

-

2.

more than 90% of autoencoder based outliers are in for dataset.

In other words, a very large fraction of autoencoder based outliers are actually outliers identified by both independent outlier detection approaches that have nothing in common (one approach based on clustering, another on representational learning). Since -means with ponders identifies a significantly higher number of outliers than the autoencoder, it can be concluded that the autoencoder actually narrows results of -means with ponders indicating the most prominent outliers.

The obtained accuracy of the explainable surrogate model (the decision tree trained according to the labelling induced by autoencoder based outliers) computed on the training data is equal to 1 for both and datasets. This implies that the surrogate models are able to explain without errors why a particular instance is an outlier. The explanation is given by the path from the root node of the decision tree to a leaf node determined by feature values of that instance. The root node and low-depth nodes (nodes near to the root node) of the decision are the most discriminative features of detected outliers. Table 3 shows the top ten most discriminative features for and datasets together with their Gini importance scores.

| dataset | dataset | ||

|---|---|---|---|

| feature | feature | ||

| average salary in 16m4 | 0.155 | median salary in 16m8 | 0.369 |

| fraction b26r in 16m12 | 0.121 | average salary in 16m9 | 0.079 |

| fraction b26r in 16m3 | 0.080 | fraction b26r in 17m1 | 0.068 |

| total employees in 16m7 | 0.078 | stdev salary in 17m2 | 0.048 |

| total persons in 16m3 | 0.069 | fraction b26r in 17m3 | 0.047 |

| stdev salary in 16m6 | 0.045 | total persons in 16m12 | 0.044 |

| total employees in 17m1 | 0.043 | fraction b26r in 16m5 | 0.031 |

| fraction b26r in 17m2 | 0.040 | average age in 16m11 | 0.026 |

| fraction b26r in 16m5 | 0.036 | stdev salary in 16m4 | 0.021 |

| org type 14 | 0.029 | stdev salary in 17m3 | 0.020 |

The most discriminative feature for outliers in dataset is the average salary of employees in April of 2016, average salary in 16m4. The median salary in August of 2016, median salary in 16m8, is the most discriminative features for outliers in dataset. It can be observed that both lists contain a large number of b26r related features introduced as domain knowledge features. Those features represent the fraction of employees in the bin with the highest salary in Serbia. Also, there are discriminative features related to the total number of persons associated to a business entities (regular employees plus honorary and associate workers that do not have a permanent working contract, total employees in 16m7, total persons in 16m3, total employees in 17m1 ). Besides the mean and median, the standard deviation of salaries is also an important feature indicating outliers (in both datasets). The last feature in the list of top 10 features discriminating outliers (org type 14) is a binary feature indicating whether a business entity is a limited liability company. The presence of this feature in the list implies that the probability that a randomly selected LLC is an outlier is higher than the probability that a randomly selected non-LLC is an outlier for LLCs with less than 10 employees.

Thus, the list of the most discriminative features reflects a tax arbitrage behavior as expected by relying on domain knowledge, like in feature fraction b26r in YmN. In the same time, the list captures some other less straightforward features which are more likely the product of a blind ML approach (like the dummy for LLC and the feature total employees in 17m1 for L10 dataset or the feature average age in 16m11 for A10 dataset). Thanks to the blind approach, we find some features more than once i.e. in few specific time varieties. We may expect to have a high degree of correlation between time varieties of the same variable due to trend component. However, our hybrid model has probably discerned some peaks / irregularities in monthly level of payments of income as higher risk in terms of tax evasion by assigning high discriminatory power to few specific monthly varieties of some features (Table 3).

5.3 Autoencoder Structure

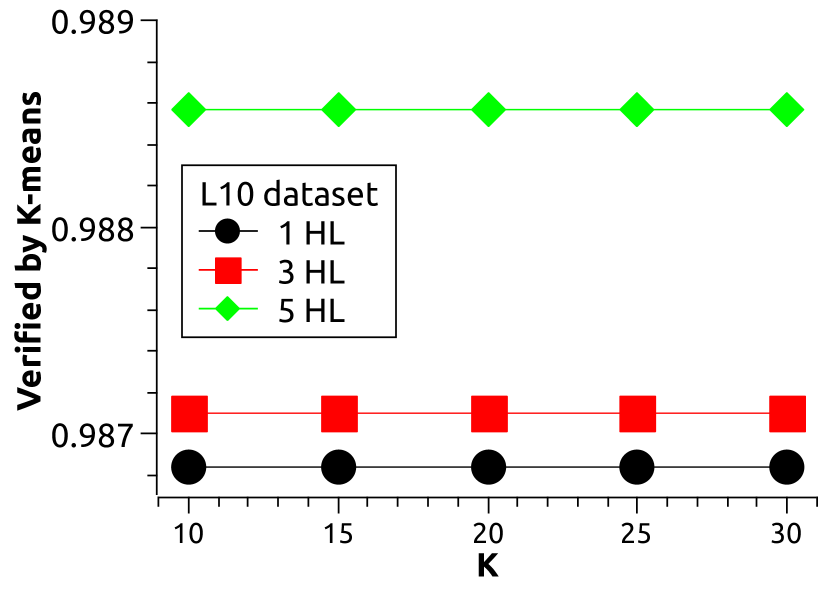

In the next experiment, we investigated the impact of the autoencoder’s structure to the resulting set of outliers. In addition to the previously examined autoencoder with three hidden layers, outliers were also detected with an autoencoder having one hidden layer and an autoencoder with five hidden layers. The autoencoder with one hidden layer contained hidden neurons. The structural configuration of the autoencoder with 5 hidden layers was , , , and hidden neurons, sequentially per layer (recall that is the number of features). The parameters describing the training process were identical as in the previous experiment.

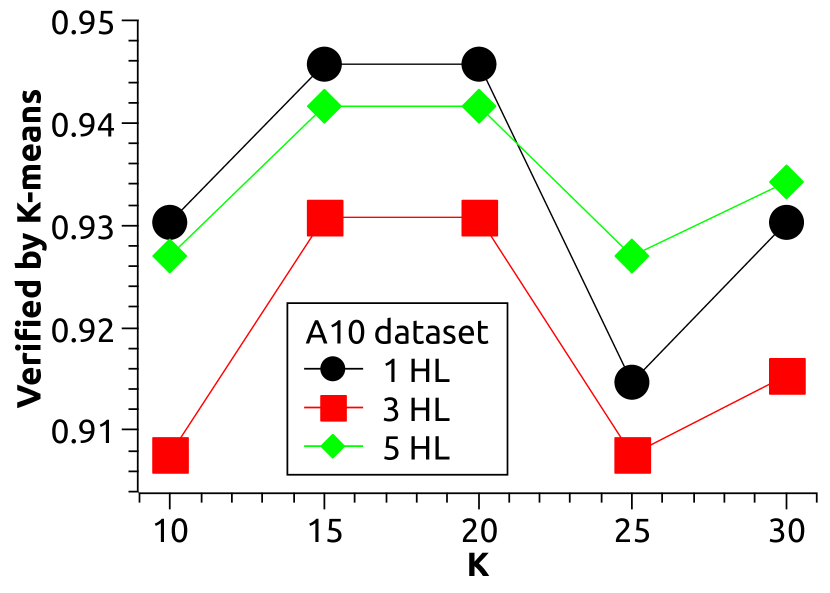

The fraction of outliers verified by -means with ponders for all three examined autoencoders is shown in Figure 3. For both datasets, the fraction of -means verified outliers is higher than 0.9 for various K values. More than 97% of outliers detected by the autoencoders in are also outliers indicated by -means with ponders. The autoencoder with 5 hidden layers has the largest fraction of -means verified outliers (98.83% for all K values), then the autoencoder with 3 hidden layers (98.71% for all K values), followed by the autoencoder with 1 hidden layer (98.68% for all K values).

In contrast to dataset, the fraction of -means verified outliers in dataset depends on . However, the differences in the number of -means verified outliers for different values are less than 3.1%. Small differences are also present for different autoencoders for a fixed (less than 3%; for = 15 and = 20 less than 1.5%). The autoencoder with one hidden layer has the highest fraction of -means verified outliers for . For larger values the autoencoder with 5 hidden layers exhibits the highest degree of agreement with -means with ponders.

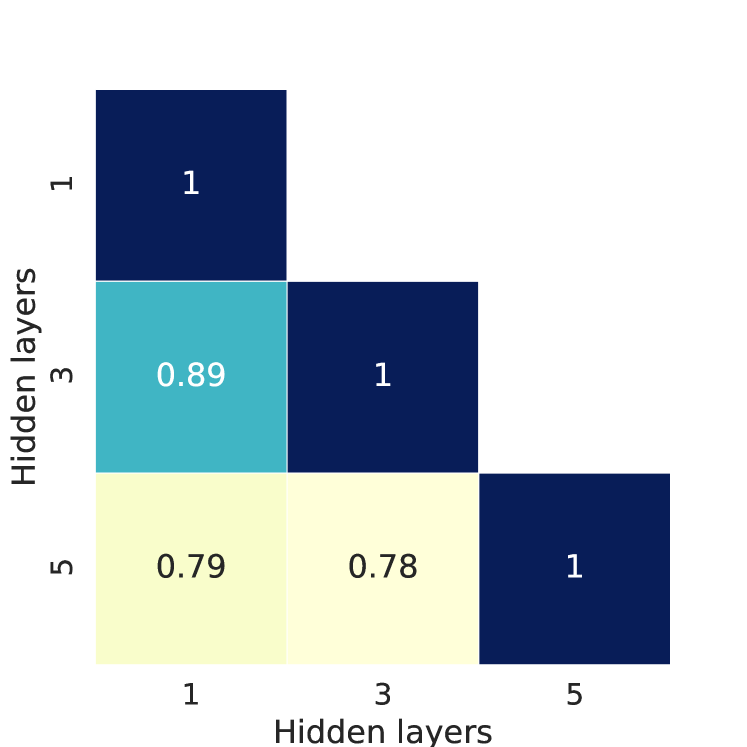

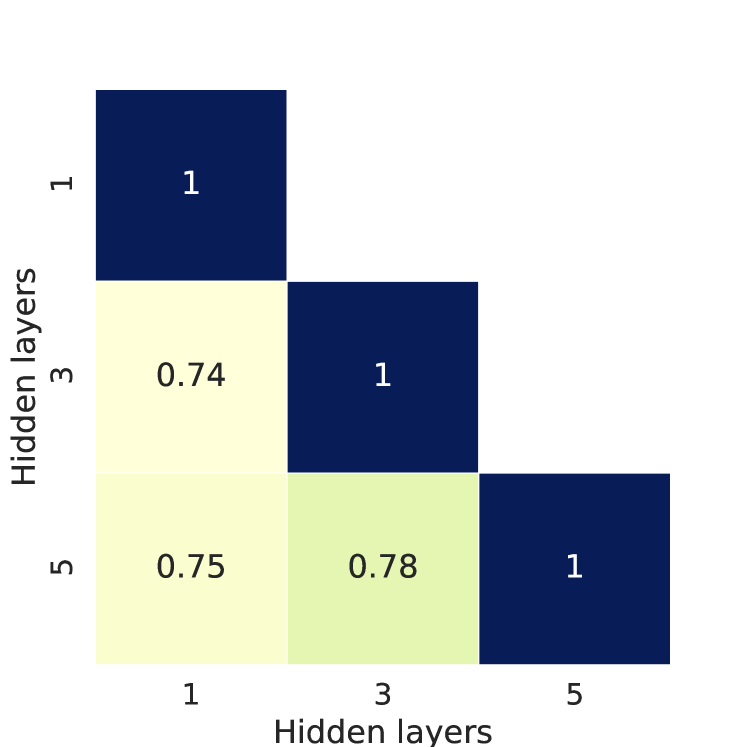

Figure 4 shows the overlap between outlier sets measured by the Jaccard coefficient for each pair of examined autoencoders. It can be seen that the lowest overlap is 0.75 implying a high degree of agreement in outliers detected by structurally different autoencoders. Taking into account a high fraction of -means verified outliers for structurally diverse autoencoders and a high degree of their mutual agreement, it can be concluded that the hybrid method is robust to variations in the structure of the autoencoder.

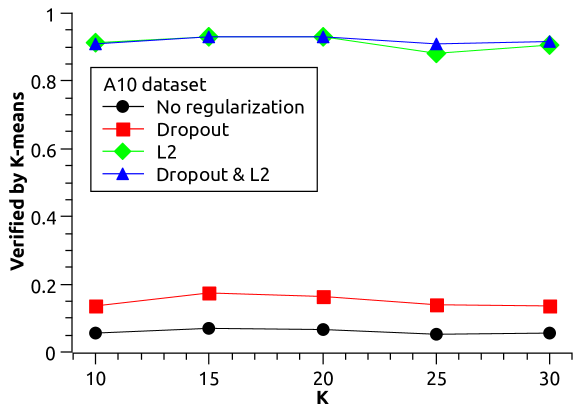

5.4 Impact of Regularization

In the last experiment we analyzed the impact of two regularization mechanisms aimed to prevent autoencoder overfitting and make it more robust to unknown instances. Here we give the results obtained for the autoencoder with 3 hidden layers. The results for the autoencoders with 1 and 5 hidden layers are very similar to those presented and discussed in this section and hence omitted here.

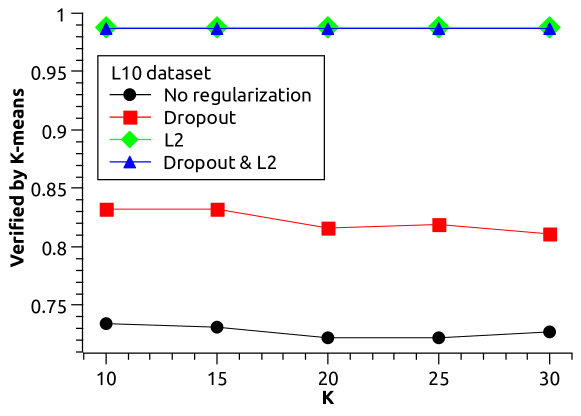

Figure 5 shows the fraction of -means verified outliers in dataset for four autoencoders: the autoencoder trained with both regularization mechanism (this autoencoder was examined in two previous experiments), the autoencoder trained using the activity regularization without dropout, the autoencoder trained using dropout without the activity regularization and the autoencoder trained without regularization mechanisms. It can be observed that the fraction of -means verified outliers significantly drops down if the activity regularization is turned off. The autoencoder trained with both regularization mechanisms behaves in the same way the autoencoder trained only using activity regularization achieving more than 98% -means verified outliers. On the other hand, the autoencoder trained only with dropout has less than 85% of -means verified outliers, while the autoencoder without regularization identifies less than 75% of -means verified outliers.

The importance of using the activity regularization when training the autoencoder is even more evident on dataset (Figure 6). On this dataset, the fraction of -means verified outliers drops from more than 90% to less than 20% when the activity regularization is deactivated. The fraction of -means verified outliers is less than 10% when both regularization mechanisms are excluded. Summarizing up the results obtained in this experiment, it can be concluded that the regularization mechanism leads to autoencoders with a high degree of consistency with -means with ponders significantly narrowing its result to outliers indicated by two independent outlier detection approaches.

5.5 Comparison to Alternative Outlier Detection Approaches

To additionally demonstrate the effectiveness of HUNOD, we compare it with eight widely used outlier detection algorithms. The following alternative outlier detection approaches provided by scikit-learn (Pedregosa et al., 2011) and PyOD (Zhao et al., 2019) libraries are considered in our comparative analysis:

-

1.

SVM – outlier detection by one-class support vector machines,

-

2.

LOF – outlier identification based on local outlier factor,

-

3.

IF – isolation forest algorithm,

-

4.

EE – elliptic envelope algorithm,

-

5.

PCA – outlier detection based on principal component analysis,

-

6.

HBOD – histogram-based outlier detection,

-

7.

ABOD – angle-based outlier detection, and

-

8.

KNN – outlier detection by the -nearest neighbors algorithm.

All considered alternatives identify outliers by computing an outlierness score to each data instance in a dataset. Then, the instances are sorted by the outlierness score and the top results are returned as outliers, where is a threshold specified by the user. Thus, we apply the alternative algorithms by setting to the number of outliers identified by the HUNOD autoencoder. Then, we check identified outliers against -means with ponders for different values of . Specifically for KNN and ABOD, outliers are identified with the same value of parameter that is used by -means with ponders. The hyperparameters of other algorithms are set to their default values (as specified by scikit-learn or PyOD).

Having in mind that -means with ponders has a high recall, the fraction of outliers identified by an alternative method that are also outliers indicated by -means with ponders can be considered as a measure of relative precision of (relative to -means with ponders). If has a low value of the relative precision with respect to a model having high recall then it can be definitely stated that exhibits a poor outlier detection performance.

Table 4 shows the fraction of outliers identified by the alternative methods on that are also indicated as outliers by -means with ponders for different values (the same as values used in Section 5.2). It can be seen that LOF, PCA and ABOD have a very low relative precision on . SVM, EE, HBOD and KNN reach a moderate level of relative precision that is significantly lower than the relative precision of the HUNOD autoencoder (the precision of the HUNOD autoencoder on is equal to 0.987, please see Table 2). The highest relative precision on is achieved by IF, ranging between 0.981 (slightly lower than the HUNOD autoencoder) and 1.0 (slightly higher than the HUNOD autoencoder), i.e. the HUNOD autoencoder and IF identify nearly the same set of outliers.

| SVM | LOF | IF | EE | PCA | HBOD | KNN | ABOD | |

|---|---|---|---|---|---|---|---|---|

| 10 | 0.549 | 0.013 | 0.981 | 0.690 | 0.116 | 0.439 | 0.794 | 0.006 |

| 15 | 0.542 | 0.045 | 0.994 | 0.695 | 0.116 | 0.413 | 0.794 | 0.032 |

| 20 | 0.542 | 0.006 | 1.000 | 0.712 | 0.116 | 0.439 | 0.800 | 0.006 |

| 25 | 0.542 | 0.019 | 0.994 | 0.800 | 0.123 | 0.484 | 0.826 | 0.019 |

| 30 | 0.490 | 0.013 | 0.987 | 0.779 | 0.116 | 0.445 | 0.545 | 0.019 |

The relative precision of the alternative methods on dataset is given in Table 5. Similarly as for , LOF, PCA and ABOD have a very low values of the relative precision. EE, HBOD and KNN also show poor outlier detection performance on with significantly lower values of the relative precision than on . SVM and IF exhibit a moderate degree of consistency with -means with ponders with the relative precision between 0.382 and 0.788. This level of relative precision is significantly lower than the relative precision of the HUNOD autoencoder which is in the range [0.908, 0.931]. Thus, it can be concluded that the HUNOD autoencoder gives more precise results than the examined alternative outlier detection methods.

| SVM | LOF | IF | EE | PCA | HBOD | KNN | ABOD | |

|---|---|---|---|---|---|---|---|---|

| 10 | 0.412 | 0.000 | 0.788 | 0.168 | 0.102 | 0.255 | 0.219 | 0.095 |

| 15 | 0.434 | 0.000 | 0.796 | 0.139 | 0.102 | 0.241 | 0.190 | 0.162 |

| 20 | 0.404 | 0.015 | 0.511 | 0.109 | 0.102 | 0.350 | 0.204 | 0.184 |

| 25 | 0.382 | 0.015 | 0.507 | 0.080 | 0.095 | 0.299 | 0.146 | 0.190 |

| 30 | 0.382 | 0.022 | 0.650 | 0.058 | 0.109 | 0.299 | 0.153 | 0.175 |

6 Conclusions and Future Work

In this paper, we proposed a novel approach for tax fraud risk management based on a hybrid machine learning-based approach that possesses several favorable features. First, the proposed method allows to incorporate the relevant domain knowledge into the model in a user friendly way, through setting of ponders (weights) of the different data features from a pre-defined set of a few candidate ponders. Second, the method offers an explainable decision tree model based on which domain experts can verify (manually or through another way) the anomalous entities that the ML model outputs. Hence, the proposed method allows for domain expert validation of the ML-declared anomalies. Finally, the method demostrates strong robustness in terms of anomaly validation due to its hybrid nature. Namely, anomalies obtained by two idependent anomaly detection methods (-means and autoencoder) are cross-checked in order to devise the final set of internally-validated anomalies.

The experimental evaluation of the method shows that there is a very good embedding of outliers detected by the HUNOD autoencoder into much larger set of outliers detected by -means with ponders. Given that these two outlier detection approaches are based on radically different machine learning designs and that the set of outliers detected by the autoencoder is significantly smaller and yet contained in the set of outlier detected by -means to a very large degree, we conclude that the autoencoder actually refines the results of -means indicating the most prominent outliers. Our experimental analysis also showed that the HUNOD autoencoder exhibits a higher degree of consistency with -means than eight other alternative outlier detection algorithms. Since -means exhibits a high recall, this result also suggests that the HUNOD autoencoder is a more precise outlier detection model than the examined alternatives.

The results of cross-checking and the results obtained by the decision tree further strengthen our initial idea that the integration of domain knowledge improves the ML approach significantly and offers the level of explainability not typical for ML methods. The features pondering appears to influence the results of -means significantly while the most discriminative features are both expert-designed as the features aimed to capture the possible tax arbitrage as well as features without particular economic interpretation. Furthermore, the tests performed with different autoencoder structure and regularization parameters indicate that the HUNOD method is rather robust and that the regularization plays an important role in the method.

The presented method designed for tax fraud detection related to the personal income is contributing to the literature on tax fraud detection using big data methods where the prevailing literature is dealing with models for VAT evasion detection. The further research could consist in additional development of the proposed hybrid model while the underlying dataset used for definition of features could be improved to encompass the relevant data related to the business entities (TINs) and individual persons from existing administrative and statistical data registries such as business financial statements, individual occupation, education level and length of working service. The dataset could be also complemented with VAT and profit tax for each business entity.

Acknowledgements.

The authors would like to thank to Olivera Radiša-Pavlović for her help during the preparation of experimental data and Nataša Krklec-Jerinkić for proof-reading an initial version of this article and giving us valuable comments and suggestions how to improve it. The authors are also grateful to anonymous reviewers for their constructive and helpful comments and suggestions. This research is supported by Ministry of Education, Science and Technological Development and Tax Administration of Republic of Serbia. The authors acknowledge financial support of the Ministry of Education, Science and Technological Development of the Republic of Serbia (Grant No. 451-03-9/2021-14/ 200125)References

- Abadi et al. (2016) Abadi M, Barham P, Chen J, Chen Z, Davis A, Dean J, Devin M, Ghemawat S, Irving G, Isard M, Kudlur M, Levenberg J, Monga R, Moore S, Murray DG, Steiner B, Tucker P, Vasudevan V, Warden P, Wicke M, Yu Y, Zheng X (2016) Tensorflow: A system for large-scale machine learning. In: Proceedings of the 12th USENIX Conference on Operating Systems Design and Implementation, USENIX Association, USA, OSDI’16, p 265–283

- Atanasijević et al. (2019) Atanasijević J, Jakovetić D, Krejić N, Krklec-Jerinkić N, Marković D (2019) Using big data analytics to improve efficiency of tax collection in the tax Administration of the Republic of Serbia. Ekonomika preduzeća 67:115–130, DOI 10.5937/EkoPre1808115A

- Basta et al. (2009) Basta S, Fassetti F, Guarascio M, Manco G, Giannotti F, Pedreschi D, Spinsanti L, Papi G, Pisani S (2009) High quality true-positive prediction for fiscal fraud detection. In: Proceedings of the 2009 IEEE International Conference on Data Mining Workshops, IEEE Computer Society, USA, ICDMW ’09, p 7–12, DOI 10.1109/ICDMW.2009.59

- Bonchi et al. (1999) Bonchi F, Giannotti F, Mainetto G, Pedreschi D (1999) Using data mining techniques in fiscal fraud detection. In: Mohania M, Tjoa AM (eds) Data Warehousing and Knowledge Discovery, Springer Berlin Heidelberg, Berlin, Heidelberg, pp 369–376

- Buehn and Schneider (2016) Buehn A, Schneider F (2016) Size and Development of Tax Evasion in 38 OECD Coutries: What do we (not) know? Journal of Economics and Political Economy 3(1):1–11

- Castellón González and Velásquez (2013) Castellón González P, Velásquez JD (2013) Characterization and detection of taxpayers with false invoices using data mining techniques. Expert Systems with Applications 40(5):1427–1436, DOI 10.1016/j.eswa.2012.08.051

- Chica et al. (2021) Chica M, Hernandez JM, Manrique-de Lara-Penate C, Chiong R (2021) An evolutionary game model for understanding fraud in consumption taxes [research frontier]. IEEE Computational Intelligence Magazine 16(2):62–76, DOI 10.1109/MCI.2021.3061878

- Gao et al. (2021) Gao Y, Shi B, Dong B, Wang Y, Mi L, Zheng Q (2021) Tax evasion detection with fbne-pu algorithm based on pncgcn and pu learning. IEEE Transactions on Knowledge and Data Engineering (In print), DOI 10.1109/TKDE.2021.3090075

- Goix (2016) Goix N (2016) How to evaluate the quality of unsupervised anomaly detection algorithms? CoRR abs/1607.01152, URL http://arxiv.org/abs/1607.01152, 1607.01152

- Hawkins et al. (2002) Hawkins S, He H, Williams GJ, Baxter RA (2002) Outlier detection using replicator neural networks. In: Proceedings of the 4th International Conference on Data Warehousing and Knowledge Discovery, Springer-Verlag, Berlin, Heidelberg, DaWaK 2000, p 170–180

- Heckman et al. (2003) Heckman JJ, Lochner LJ, Todd PE (2003) Fifty Years of Mincer Earnings Regressions. NBER Working Papers 9732, National Bureau of Economic Research, Inc, URL https://ideas.repec.org/p/nbr/nberwo/9732.html

- Kingma and Ba (2015) Kingma DP, Ba J (2015) Adam: A method for stochastic optimization. In: Bengio Y, LeCun Y (eds) 3rd International Conference on Learning Representations, ICLR 2015, San Diego, CA, USA, May 7-9, 2015, Conference Track Proceedings, URL http://arxiv.org/abs/1412.6980