Statistical Enumeration of Groups by Double Cosets

In memory of Jan Saxl

Abstract

Let and be subgroups of a finite group . Pick uniformly at random. We study the distribution induced on double cosets. Three examples are treated in detail: 1) the Borel subgroup in . This leads to new theorems for Mallows measure on permutations and new insights into the LU matrix factorization. 2) The double cosets of the hyperoctahedral group inside , which leads to new applications of the Ewens’s sampling formula of mathematical genetics. 3) Finally, if and are parabolic subgroups of , the double cosets are ‘contingency tables’, studied by statisticians for the past 100 years.

keywords:

double cosets , Mallows measure , Ewens measure , contingency tables , Fisher-Yates distributionMSC:

[2010] 60B15 , 20E991 Introduction

Let be a finite group. Pick uniformly at random. What does ‘look like’? This ill-posed question can be sharpened in a variety of ways; this is the subject of ‘probabilistic group theory’ initiated by Erdős and Turan [41], [42], [43], [44]. Specializing to the symmetric group, one can ask about features of cycles, fixed points, number of cycles, longest (or shortest) cycles, and the order of [88]. The descent pattern has also been well-studied [18]. Specializing to finite groups of Lie type gives ‘random matrix theory over finite fields’ [49]. The enumerative theory of -groups is developed in [15]. The questions also make sense for compact groups and lead to the rich world of random matrix theory [4], [30], [46]. ‘Probabilistic group theory’ is used in many ways, see [39] and [87] for alternative perspectives.

This paper specializes in a different direction. Let and be subgroups of . Then splits into double cosets and one can ask about the distribution that a uniform distribution on induces on the double cosets. Three examples are treated in detail:

-

1.

If and is the lower triangular matrices (a Borel subgroup), then the Bruhat decomposition

shows that the double cosets are indexed by permutations. The induced measure on is the actively studied Mallows measure

(1) where is the number of inversions in the permutation and . The double cosets vary in size, from to . This might lead one to think that ‘most lie in the big double coset’. While this is true for large, when is fixed and is large, the double coset containing a typical corresponds to an with normal distribution centered at , with standard deviation of order . See Theorem 3.5. The descent pattern of a typical is a one dependent determinantal point process with interesting properties [17]. There has been intensive work on the Mallows measure developed in the past ten years, reviewed in Section 3.3. This past work focuses on as a parameter with . The group theory applications have and call for new theory.

-

2.

If is the symmetric group and is the hyperoctahedral group of centrally symmetric permutations (isomorphic to ), then the double cosets are indexed by partitions of and the induced measure is the celebrated Ewens’s sampling formula

(2) where is the number of parts of , if has parts of size , and . As explained in Section 4, the usual domain for is in genetics. In statistical applications, is a parameter taken with . The group theory application calls for new representations and theorems, developed here using symmetric function theory.

-

3.

If is the symmetric group and are Young subgroups corresponding to fixed partitions and of , then the double cosets are indexed by contingency tables: arrays of non-negative integer entries with row sums and column sums . If is such a table, the induced measure on double cosets is the Fisher-Yates distribution

(3) where are the row sums of and are the column sums. This measure has been well-studied in statistics because of its appearance in ‘Fisher’s Exact Test’. This is explained in Section 5. Its appearance in group theory problems suggests new questions developed here – what is the distribution of the number of zeros or the largest entry? Conversely, available tools of mathematical statistics (chi-squared approximation) answer natural group theory questions – which double coset is largest, and how large is it?

The topics above have close connections to a lifetime of work by Jan Saxl. When the parabolic subgroups are , the double cosets give Gelfand pairs. The same holds for and, roughly, Jan prove that these are the only subgroups of giving Gelfand pairs for sufficiently large. He solved similar classification problems for finite groups of Lie type. These provide open research areas for the present project.

Section 2 provides background and references for double cosets, Hecke algebras, and Gelfand pairs. Section 3 treats the Bruhat decomposition . Section 4 treats and Section 5 treats parabolic subgroups of and contingency tables. In each of these sections, open related problems are discussed.

2 Background

This section gives definitions, properties, and literature for double cosets, Hecke algebras, and Gelfand pairs.

2.1 Double cosets

Let and be subgroups of the finite group . Define an equivalence relation on by

The equivalence classes are called double cosets, written for the double coset containing and for the set of double cosets. This is a standard topic in undergraduate group theory [94], [40]. A useful development is in [20], Section 2.7. Simple properties are:

| (4) | |||

| (5) | |||

| (6) |

Despite these nice formulas, enumerating the number of double cosets can be an intractable problem. For example, when and are Young subgroups, double cosets are contingency tables with fixed row and column sums. Enumerating these is a #-P complete problem [32].

Consider the problem of determining the smallest (and largest) double coset. If , the smallest is the double coset containing (with size ). When , it is not clear. Is it the double coset containing ? Not always. Indeed, for a proper subgroup of , let be any element of not in . Let . Then , so the double coset is just a single right coset of . This has minimal possible size among double cosets . Since is not in , does not contain the identity. It can even happen that the double coset containing the identity has maximal size. This occurs, from (4) above, whenever .

For the largest size of a double coset, from 4 note that this can be at most . If this occurs if is not normal. For and different, it is not clear. For parabolic subgroups of a necessary and sufficient condition for the maximum size to be achieved is that majorizes . See [68] Section 1.3, which shows that the number of double cosets achieving the maximum is the number of matrices with row sums and column sums .

The seemingly simple problem of deciding when there is only one double coset becomes the question of factoring . This has a literature surveyed in [10].

All professional group theorists use double cosets – one of the standard proofs of the Sylow theorems is based on (5), and Mackey’s theorems about induction and restrictions are in this language. In addition, double cosets have recently been effective in computational group theory. Laue [77] uses them to enumerate all isomorphism classes of semi-direct products. Slattery [89] uses them in developing a version of coset enumeration.

2.2 Hecke algebras

With and subgroups of a finite group , consider the group algebra over a field :

This is an algebra with and . The group acts on by

The bi-invariant functions (satisfying for all ) form a sub-algebra of which is here called the Hecke algebra. Many other names are used, see [90] for history.

Hecke algebras are a mainstay of modern number theory (usually with infinite groups). They are also used by probabilists (e.g. [34]) and many stripes of algebraists. Curtis and Reiner [28] is a standard reference for the finite theory. We denote them by . Clearly the indicator functions of the double cosets form a basis for .

2.3 Gelfand pairs

For some choices of and , with , the space forms a commutative algebra (even though and are non-commutative). Examples with are or in . Of course, acts on (say with ) and commutativity of is equivalent to the representation of on being multiplicity free: Since (the trivial representation of induced up to ), Frobenius reciprocity implies that each irreducible occurring in has a 1-dimensional subspace of left -invariant functions. Let be such a function, normalized by . These are the spherical functions of the Gelfand pair . Standard theory shows that the spherical functions form a second basis for .

We will not develop this further and refer to [29] (Chapter 3F), [21], [79] for applications of Gelfand pairs in probability.

We also note that Gelfand pairs occur more generally for compact and non-compact groups. For example, is Gelfand and the spherical functions become the spherical harmonics of classical physics. For , the spherical functions are the zonal polynomials beloved of older mathematical statisticians. Gelfand pairs are even useful for large groups such as and , which are not locally compact. See [19].

Clearly, finding subgroups giving Gelfand pairs is a worthwhile project. Jan Saxl worked on classifying subgroups giving Gelfand pairs over much of his career [86], [67]. He gave definitive results for the symmetric and alternating groups and for most all the almost simple subgroups of Lie type. Alas, it turns out that if is sufficiently large, then and give the only Gelfand pairs in (at least up to subgroups of index ; e.g. is Gelfand in ).

3 Bruhat decomposition and Mallows measure

3.1 Introduction

Let , the general linear group over a field with elements. Let be the lower triangular matrices in . Let denote the permutation group embedded in as permutation matrices. The decomposition of into double cosets is called the Bruhat decomposition [90] and has the following properties:

| (7) |

Thus, permutations index the double cosets. The size of is

where is the number of inversions of (that is, ). Dividing by , we get the induced measure

| (8) |

Example 3.1.

In , the inversions are

| 123 | 132 | 213 | 231 | 312 | 321 | |

| 0 | 1 | 1 | 2 | 2 | 3 |

and .

The measure , , is studied as the Mallows measure on in the statistical and combinatorial probability literature. A review is in Section 3.3. Much of this development is for the statistically natural case of with close to . The group theory application has for a prime and . This calls for new theorems and insights. The question of interest is

| (9) |

An initial inspection of (8) reveals the minimum and maximum values: and for , the reversal permutation. Thus, is the largest double coset. It is natural to guess that ‘maybe most elements are in ’. This turns out to not be the case.

Lemma 3.2.

| (10) |

Proof.

Using that , simple algebra gives

∎

The infinite product converges. This shows that for fixed , when is large is exponentially small. Of course, for fixed and large, tends to (only is needed).

In Section 3.2, it is shown that a uniform is contained in for with a standard normal random variable.

Let us conclude this introductory section with two applied motivations for studying this double coset decomposition.

Example 3.3 (LU decomposition of a matrix).

Consider solving with fixed in and fixed in . The standard ‘Gaussian elimination’ solution subtracts an appropriate multiple of the first row from lower rows to make the first column , then subtracts multiples of the second row to make the second column , and so on, resulting in the system

with upper triangular. This can be solved inductively for and then . This description assumes that at stage , the entry of the current triangularization is non-zero. If it is zero, a permutation (pivoting step) is made to work with the first non-zero element in column . A marvelous article by Roger Howe [66] shows in detail how this is equivalent to expressing with the number of pivoting steps being . Thus, matrices in the largest Bruhat cell require no pivots and gives the chance of various pivoting permutations.

Example 3.4 (Random generation for ).

Suppose one wants to generate independent picks from the uniform distribution on . We have had to do this in cryptography applications when . Testing conjectures for also uses random samples. One easy method is to fill in an array with independent picks from the uniform distribution on and then check if the resulting matrix is invertible (using Gaussian elimination). If is not invertible, this is simply repeated. The chance of success is approximately ( when ). Alas, this calls for a variable number of steps and made a mess in programming our crypto chip.

Igor Pak suggested a simple algorithm that works in one pass:

-

1.

Pick from .

-

2.

Pick uniformly.

-

3.

Form .

Since picking uniformly is simple, this is a fast algorithm. But how to pick from ? The following algorithm is standard:

-

1.

Place symbols down in a row sequentially, beginning with .

-

2.

If symbols have been placed, then place symbol leftmost with probability , secondmost with probability , …and th with probability .

-

3.

Continue until all symbols are placed.

The following sections develop some theorems for the Mallows distribution (8) for fixed and large. In Section 3.2, the normality of is established. Section 3.3 develops other properties along with a literature review of what is known for . The descent pattern is developed in 3.4, generalizations to other finite groups and parallel orbit decompositions (e.g. acting on ) are in Section 5.3. These sections are also filled with open research problems.

3.2 Distribution of

This section proves the limiting normality of the number of inversions under the Mallows measure defined in (8), when is fixed and is large. Thus, most are not in the largest double coset.

Theorem 3.5.

With notation as above, for any ,

The error term is uniform in .

Proof.

The argument uses the classical fact that under on , is exactly distributed as a sum of independent random variables. Let for . Write for a random variable with distribution , taking independent. Then

| (11) |

To see (11), use generating functions. Rodrigues [85] proved for any that

Take and divide both sides by to see

Under

Thus, when is large (and using that ), the law of is exponentially close to a geometric random variable with . This has and . Now, the classical central limit theorem implies the result. ∎

3.3 Simple properties of

The discussion above points to the question of: What properties of are ‘typical’ under ? We now see that with are typical, but are all such equally likely?

The distribution is studied (for general Coxeter groups) in [34]. They show (for all )

| (12) | |||

| (13) | |||

| (14) | |||

| (15) |

where in the last expression is the reversal of (e.g. ). However, there do not appear to be simple expressions for , , nor for the distribution of the number of fixed points, cycles, or other features standard in enumerative combinatorics.

There has been remarkable study of features when is close to (often ). These include

-

1.

The limiting distribution of the empirical measure was studied by Shannon Starr [92]. He shows, for ,

for any continuous function , where

Starr derives these results rigorously by considering a Gibbs measure on permutations with . This work is continued in [93], bringing in fascinating connections with statistical mechanics.

The function above is an example of a permutation limit or ‘permuton’. It figures in many of the developments below.

- 2.

-

3.

Remarkable work on statistical aspects of the Mallows model (given an observed , how do you estimate and how do such estimates behave?) is in [83]. This work treats other Mallows models of the form , for a metric on .

- 4.

- 5.

-

6.

The cycles of have limit distributions determined by [53] for .

-

7.

The length of the longest increasing subsequence under has a fascinating limit theory, see [82], [11]. See [9] for work on the longest monotone subsequence, which works for fixed and thus is relevant to the present group theory applications. This paper develops a probabilistic regenerative process for building permutations from the Mallows model that should be broadly useful for further distribution questions.

-

8.

Three further papers develop properties of the Mallows model for fixed less than (and are hence applicable to fixed greater than because of (15)). In [27], the authors study the distribution of pattern avoiding permutations for local patterns (e.g. avoiding) and related topics. A variety of techniques are used. These may well transfer to other statistics. In [54], [55] a limiting measure on permutations of the natural numbers (and ) is introduced as a limit of finite Mallows measures. As one offshoot, the limiting distribution of (and multivariate extensions) is determined. The main interest of these papers is a -analog of de Finetti’s Theorem.

3.4 Descents

In this section, is fixed. A permutation has a descent at position if . The total number of descents is . The descent set is . For example, has and descent set . Descents are a basic descriptive statistic capturing the ‘up/down’ pattern in a permutations. The distribtuion theory of is classical combinatorics going back to Euler. Descent sets also have a remarkable combinatorial structure, see [18] for an overview.

Recent work allows detailed distribution theory for and under the Mallows distribution for fixed . To describe this, let

If is random, then is a point process. The following result of Borodin, Diaconis, Fulman [18] describes many properties of this process. For further definitions and background, see [17].

Theorem 3.6.

Let , , be the Mallows measure (8).

-

(a)

The chance that a random permutation chosen from has descent set containing is

with .

-

(b)

The point process is stationary, one dependent, and determinantal with kernel where

-

(c)

The chance of finding descents in a row is . In particular, the number of descents has mean and variance

Normalized by its mean and variance, the number of descents has a limiting standard normal distribution.

Remarks

-

1.

Consider the distribution of in part (c) of Theorem 3.6. Under the uniform distribution on , has mean and variance (obtained by setting in the formula in part (c)). The distribution pushes toward . How much? The mean increase to and, as makes sense, the variance decreases. For large , the mean goes to the maximum value and the variance goes to zero.

-

2.

The paper [18] gives simple formulas for the -point correction function for general sets .

-

3.

There is an interesting alternative way to compute various moments for under the measure . Let

[91] gives

Differentiating in and setting gives the generating function of the falling factorial moments for under . Using Maple, Stanley (personal communication) computes

These give independent checks on the mean and variance reported before and an expression for the third moment. It would be a challenge to prove the central limit theorem by this route.

3.5 Other groups and actions

The Bruhat decomposition (7) is a special case of more general results. Bruhat showed that a classical semi-simple Lie group has a double coset of this form where is a maximal solvable subgroup of and is the Weyl group. Then Chevalley showed the construction makes sense for any field, particularly finite fields. This gives

with the length of the word in the Coxeter generators. The length generation function factors

where , the exponents of , are known. From here, one can prove the analog of Theorem 3.5. The Weyl groups have a well developed descent theory (number of positive roots sent to negative roots) and one may ask about the analog of Theorem 3.6, along with the other distribution questions above.

We want to mention two parallel developments. Louis Solomon [90] has built a beautiful parallel theory for describing the orbits of on , the set of matrices. This has been wonderfully developed by Tom Halverson and Arun Ram [57]. None of the probabilistic consequences have been worked out. There is clearly something worthwhile to do.

Second, Bob Gualnick [56] has classified the orbits of acting on the set of matrices over . Estimating the sizes and other natural questions about the orbit in the spirit of this section seems like an interesting project.

Finally, it is worth pointing out that finding ‘nice descriptions’ of double cosets is usually not possible. For example, let be the group of uni-upper triangular matrices with entries in . Let , with embedded diagonally. Describing double cosets is a well-studied wild problem in the language of quivers [52]. In [3], this was replaced by the easier problem of studying the ‘super characters’ of . This leads to nice probabilistic limit theorems. See [24], [25].

4 Hyperoctahedral double cosets and the Ewens sampling formula

4.1 Introduction

Let be the group of symmetries of an -dimensional hypercube. This is one of the classical groups generated by reflections. It can be represented as

| (16) |

with acting on the binary -tuples by permuting coordinates. Thus, . For present purposes it is useful to see as the subgroup of centrally symmetric permutations. That is, permutations with for all . For example, when we have and, as elements of , can write

The first and last values in each permutation sum to five, as do the middle two values. This representation is useful in studying perfect shuffles of a deck of cards [33].

The double coset space is a basic object of study in the statisticians world of zonal polynomials. Macdonald ([80], Section 7.1) develops this clearly, along with citations to the statistical literature, and this section follows his notation.

We begin by noting two basic facts: 1) The double cosets form a Gelfand pair. 2) The double cosets are indexed by partitions of . To see how this goes, to each permutation associate a graph with vertices and edges where joins vertices and joins vertices . Color the edges red and the edges as blue. Then, each vertex lies on exactly one red and one blue edge. This implies the components of are cycles with alternating red and blue edges, so each cycle has an even length. Dividing these cycle lengths by gives a partition of , call it .

Example 4.1.

Take and . The graph is

Here there is a cycle of length and a cycle of length , thus this corresponds to the partition .

Macdonald proves (2.1 in Section 7.2, [80]) that if and only if . Thus, the partitions of serve as double coset representatives for .

If we denote , , then

| (17) |

with and is the number of parts in , where has parts of size . For example, for , we see and . The largest double coset corresponds to the cycles in (not all cycles are in the same double coset).

To see this, let for a partition of . Note that for any , if a box from the lower right corner is moved to the right end of the top row, the result is still a partition. For example,

Lemma 4.2.

With notation above, .

Proof.

Assume the first row of has boxes and the last row has boxes. Consider . If , then . With , where is the number of parts of of length , then from to only will change. Thus,

Since is the length of the top row and is the length of the bottom row, , and the inequality follows since and .

If , then and

∎

Corollary 4.3.

For , with equality if and only if .

Remark.

It is natural to guess that is monotone in the usual partial order on partitions. This fails, for example:

Here , but . Still, inspection of special cases suggest that the partial order in the lemma can be refined.

The lemma shows that the smallest double coset in corresponds to , and the largest corresponds to the cycle .

Dividing (17) by gives the probability measure

| (18) |

This shows that is the Ewens measure for . The Ewens measure with parameter is usually described as a measure on the symmetric group with

| (19) |

If is in the conjugacy class corresponding to , then and the size of the conjucacy class is . Using this, simple calculations show (18) is (19) with .

The Ewens measure is perhaps the most well-studied non-uniform probability on because of its appearance in genetics. The survey by Harry Crane [26] gives a detailed overview of its many appearances and properties. Limit theorems for are well developed. Arratia-Barbour-Tavaré ([5], chapter 4) studies the distribution of cycles (number of cycles, longest and shortest cycles, etc. ) under . The papers of Féray [45] study exceedences, inversions, and subword patterns. A host of features display a curious property: The limiting distribution does not change with (!). For example, the structure of the descent set of an Ewens permutation matches that of a uniform permutation. An elegant, unified theory is developed in the papers of Kammoun [72], [71], [73]. More or less any natural feature of has been covered. These papers work for all so the results hold for in (19).

The following section gives more details. The final section suggests related problems.

4.2 Cycle indices and Poisson distributions

For a partition of let be the number of parts of equal to . Thus, . For , write for and introduce the generating functions:

and

The following analog of Polya’s cycle index theorem holds.

Theorem 4.4.

With notation as above,

Proof.

The proof uses symmetric function theory as in [80]. In particular, the power sum symmetric functions in variables are and, for , . A formula at the bottom of pg 307 in [80] specializes to

| (20) |

In (20), and are distinct sets of variables. We have set in Macdonald’s formula (see the discussion following the proof). Set further and replace by to get

where . Since the are free generators of the ring of symmetric functions, they may be specialized to (that is, setting ). Then the formula becomes

| (21) |

As above, the inner sum is

∎

To bring out the probabilistic content of Theorem 4.4, recall the negative binomial density with parameters assigns mass

Divide both sizes of (21) by to see

| (22) |

using the expansion . Recall the Poisson distribution on has density and moment generating function . This and (22) gives

Corollary 4.5.

Pick from and then from the uniform distribution. If has with parts equal to , then the are independent with having a Poisson distribution with parameter .

From this corollary one may prove theorems about the joint distribution of cycles exactly as in [88]. This gives analytic proofs of previously proved results. For example, for large :

-

1.

The are asymptotically independent with Poisson distributions.

-

2.

has mean asymptotic to , variance asymptotic to , and normalized by its mean and variance has a limiting normal distribution.

The distribution of smallest and largest parts are similarly determined. The calculations in this section closely match the development in [95]. This gives a very clear description of the results above from the genetics perspective.

4.3 Remarks and extensions

(a) The formula of Macdonald used in Section 4.2 involved a sequence of numbers . For a partition , define multiplicatively. Macdonald proves

At the right, the product means ‘something is independent’ and it is up to us to see what it is.

As a first example, take for all . Then, proceeding as in (22) the formula becomes

with , the cycle indicator of . This is exactly Polya’s cycle formula, see [88].

Taking gives the results of Section 4.2 and indeed suggested the project of enumerating by double cosets. Macdonald considers the five following choices for :

and shows that each gives celebrated special functions: Schur, Hall-Littlewood, Zonal, Jack, and Macdonald, respectively. We are sure that each will give rise to an interesting enumerative story, if only we could find out what is being counted. Indeed, in [50] Jason Fulman has shown that the case of enumerates -stable maximal tori in .

(b) For the cycles of the symmetric group, Polya’s formula shows that the limiting Poisson approximation is remarkably accurate. In particular, under the uniform distribution on :

-

1.

The first moments of the number of fixed points of , , are equal to the first moments of the Poisson distribution.

-

2.

More generally, the mixed moments

equal the same moments of independent Poisson variables with parameters , as long as .

Theorem 4.4 allows exact computation of the joint mixed moments of for chosen from Ewens distribution. They are not equal to the limiting moments. The moments were first computed by Watterson in [95].

(c) We mention a -analog of the results of this section which is parallel and ‘nice’. It remains to be developed. The -dimensional symplectic group is a subgroup of and is a Gelfand pair. The double cosets are nicely labeled and the enumerative facts are explicit enough that analogs of he results above should be applicable. For details, see [6].

Jimmy He ([58], [60]) worked out the convergence rates for the natural random walk on using the spherical functions. This problem was suggested to the first author by Jan Saxl as a way of tricking himself into learning some probability. The result becomes a walk on quadratic forms, and He proves a cutoff occurs.

5 Parabolic subgroups of

Let be a partition of (denoted ). That is, with and . The parabolic subgroup is the set of all permutations in which permute only among themselves, only among themselves, and so on. Thus,

If are the generating transpositions of , then is generated by . The group is often called a Young subgroup.

Let be a second partition of . This section studies the double cosets . These cosets are a classical object of study; they can be indexed by contingency tables: arrays of non-negative integers with row sums given be the parts of and column sums the parts of .

The mapping from to tables is easy to describe: Fix . Inspect the first positions in . Let be the number of elements from occurring in these positions, the number of elements from , …and the number of elements from . In general, is the number of elements from which occur in the positions up to .

Example 5.1.

When , , there are five possible tables:

Listed below each table is a permutation in the corresponding double coset, and the total size of the double cosest.

The mapping is bi-invariant and gives a coding of the double cosets. See [68] for further details and proof of this correspondence. Jones [70] gives a different coding.

Any double coset has a unique minimal length representative. This is easy to identify: Given , build sequentially, left to right, by putting down then … each time putting down the longest available numbers in the block, in order. Thus, in example 5.1 the shortest double coset representative is . For more details, see [13].

The measure induced on contingency tables by the uniform distribution on is

| (23) |

This is the Fisher-Yates distribution on contingency tables, a mainstay of applied statistical work in chi-squared tests of independence. The distribution can be described by a sampling without replacement problem: Suppose that an urn contains total balls of different colors, of color . To empty the urn, make sets of draws of unequal sizes. First draw balls, next , and so on until there are balls left. Create a contingency table by setting to be the number of color in the th draw.

This perspective, along with the previously defined mapping from permutations to cosets, proves that the distribution on contingency tables induced by the uniform distribution on is indeed the Fisher-Yates: Suppose a permutation represents a deck of cards labeled . Given partitions color cards with color 1, labels color and so on. From a randomly shuffled deck, draw the first cards and count the number of each color, then draw the next , and so on.

More statistical background and available distribution theory is given in the following section. These results give some answers to the question:

| (24) |

From (23),

| (25) |

However, enumerating the number of double cosets is a #-P complete problem. See [32].

When , the double cosets give a Gelfand pair with spherical functions the Hahn polynomials. The associated random walk is the Bernoulli-Laplace urn, which is perhaps the first Markov chain! (See [35].) More general partitions give interesting urn models but do not seem to admit orthogonal polynomial eigenvectors.

One final note: there has been a lot of study on the uniform distribution on the space of tables with fixed row and column sums. This was introduced with statistical motivation in [31]. The central problem has been efficient generation of such tables; enumerative theory is also natural but remains to be developed. See [32], [23], [37], [38], [8] and their references. The Fisher-Yates distribution (23) is quite different from the uniform and central to both the statistical applications and to the main pursuits of the present paper.

Section 5.1 develops statistical background and uses this to understand the size of various double cosets, Section 5.2 proves a new limit theorem for the number of zeros in . The final section discusses natural open problems.

5.1 Statistical background

Contingency tables arise whenever a population of size is classified with two discrete categories. For example, Table 1 shows 592 subjects classified by 4 levels of eye color and 4 levels of hair color.

| Black | Brown | Red | Blond | Total | |

|---|---|---|---|---|---|

| Brown | 68 | 119 | 26 | 7 | 220 |

| Blue | 20 | 84 | 17 | 94 | 215 |

| Hazel | 15 | 54 | 14 | 10 | 93 |

| Green | 5 | 29 | 14 | 16 | 64 |

| Total | 108 | 286 | 71 | 127 | 592 |

A classic task is the chi-squared test for independence. This is based in the chi-squared statistic

| (26) |

This measure how close the table is to a natural product measure on tables. In the example Table 1, .

The usual probability model for such tables considers a population of size , with each individual independently assigned into one of the cells with probability ( ). The independence model postulates

for and . A basic theorem in the subject [74] says that if is large and the statistic has a limiting distribution , i.e.

where is the chi-squared density with degrees of freedom:

| (27) |

The density has mean and variance and it is customary to compare the observed statistic with the limits and reject the null hypothesis if the statistic falls outside this interval. In the example, and the hypothesis of independence is rejected.

The great statistician R.A. Fisher suggested a different calibration: Fix the row sums, fix the column sums and look at the conditional distribution of the table given the row and column sums (under the independence model). It is an elementary calculation to show that is the Fisher-Yates distribution (23). Notice that the Fisher-Yates distribution does not depend on the ‘nuisance parameters’ . This is called Fishers exact test. There is a different line of development leading to the same distribution. This is the conditional testing approach (also due to Fisher). David Freedman and David Lane [47], [48] give details, philosophy, and history. We only add that conditional testing is a rich, difficult subject (starting with the question: what to condition on?). For discussion and extensive pointers to the literature, see [78] (Chapter 2), [36] (Section 4).

All of this said, mathematical statisticians have long considered the distribution of tables with given row and column sums under the Fisher-Yates distribution.

The following central limit theorem determines the joint limiting distribution of the table entries under the Fisher-Yates distribution. They are approximately multivariate normal. As a corollary, the statistic has the appropriate chi-squared distribution. This can be translated into estimates of the size of various double cosets, as discusses after the statement.

In the following, fix and . Let be two sequences of partitions of . Suppose there are constants with such that

| (28) |

Let be drawn from the Fisher-Yates distribution (23) and let

Theorem 5.2.

With notation as above, assuming (28), the random vector

converges in distribution to a normal distribution with mean zero and covariance matrix

for , .

The tensor product in the definition of means that covariance between the variable and the variable is given by . Note that since the final entry in each row (or column) is determined by the other entries, the covariance matrix is singular with rank .

Corollary 5.3.

A very clear proof of Theorem 5.2 and the corollary is given by Kang and Klotz [74]. They review the history, as well as survey several approaches to the proof. Their argument is a classical, skillful use of Stirling’s formula and their paper is a model of exposition.

The usual way of using these results, for a single entry in the table, gives

Any single entry of the table has a limiting normal approximation. This can also be seen through the normal approximation to the hypergeometric distribution. This is available with a Berry-Esseen error; see [62].

The limiting approximation shows that, under the Fisher-Yates distribution, most tables are concentrated around the ‘independence table’

This is rank one. While it does not have integer entries, it gives a good picture of the approximate size of a typical double coset.

To be quantitative, let us define a distance between tables with the same row and column sums:

This is the distance, familiar as total variation from probability. Since , for many tables , . The Cauchy-Schwartz inequality shows

| (29) |

Corollary 5.3 shows that, under the Fisher-Yates distribution, is typically , and thus typically is of order . A different way to say this is to divide the tables and by to get probability distributions on points. Then, for most ,

Barvinok [8] studies the question in the paragraph above under the uniform distribution on tables. In this setting, he shows that most tables are close (in a somewhat strange distance) to quite a different table .

Theorem 5.2 also gives an asymptotic approximation to the size of the double coset corresponding to the table . Call this . It is easy to see that with

for the vector corresponding to the upper left sub-matrix of (with notation as in Theorem 5.2) and the associated covariance matrix (that is, the covariances between the remaining entries of the sub-matrix). Note that removing one row and one column from removes the dependency so is full rank. This uses the local limit version of Theorem 5.2, which follows from the argument of Kang and Klotz [74]. See [22] for further details.

The asymptotics above show that the large double cosets are the ones closest to the independence table. This may be supplemented by the following non-asymptotic development.

Let and be tables with the same row and column sums. Say that (‘ majorizes ’) if the largest element in is greater than the largest element in , the sum of the two largest elements in is greater than the sum of the two largest elements in , and so on. Of course the sum of all elements in equals the sum of all elements of .

Example 5.4.

For tables with , there is the following ordering

Majorization is a standard partial order on vectors [81] and Harry Joe [69] has shown it is useful for contingency tables.

Proposition 5.5.

Let and be tables with the same row and column sums and the Fisher-Yates distribution. If , then

Proof.

From the definition (23), we have for a constant . This form makes it clear the right hand side is a symmetric function of the numbers . The log convexity of the Gamma function shows that it is concave. A symmetric concave function is Schur concave: That is, order-reversing for the majorization order [81]. ∎

Remark.

Joe [69] shows that, among the real-valued tables with given row and column sums, the independence table is the unique smallest table in majorization order. He further shows that if an integer valued table is, entry-wise, within of the real independence table, then is the unique smallest table with integer entries. In this case, the corresponding double coset has largest.

Example 5.6.

Fix a positive integer and consider an table with all entries equal to . This has constant row sums and column sums . It is the unique smallest table with these row and column sums, and so corresponds to the largest double coset. For , this table is

Contingency tables with fixed row and column sums form a graph with edges between tables that can be obtained by one move of the following: pick two rows and two columns . Add to the entry, to the entry, to the entry, and to the entry. This graph is connected and moves up or down in the majorization order as the table with rows and columns moves up or down. See Example 5.4 above.

5.2 Zeros in Fisher-Yates tables

In this section we will use for the row sums of a table and for the column sums. One natural feature of a contingency table is its zero entries. As shown in Section 5.1, most tables will be close to the table with entries . This has no zero entries. Therefore, zeros are a pointer to the breakdown of the independence model. In statistical applications, there is also the issue of ‘structural zeros’ – categories such as ‘pregnant males’ which would give zero entries in cross-classified data due their impossibility. See [14] for discussion. The bottom line is, professional statisticians are always on the look-out for zeros in contingency tables. This section gives a limit theorem for the number of zeros under natural hypotheses.

A simple observation which leads to the theorem is that a Fisher-Yates table is equivalent to rows of independent multinomial vectors, conditioned on the column sums: let be independent random vectors of length , with for some probabilities and . That is, are the occupancy counts generated by assigning balls to boxes, with one ball going to the th box with probability . The joint distribution for the vectors is then

| (30) |

Let be distributed as conditioned on the sums . From (30) it is clear that has the Fisher-Yates distribution (23), regardless of the choices .

This perspective allows us to use known limit results for multinomial distributions, translated to contingency tables using conditioned limit theory. For the remainder, assume that the row sums are constant, so that the are iid vectors. Let count the number of zero-entries in the vector. [63] contains limit theorems for as , with either Poisson or normal limit behavior depending on the asymptotics of and the .

Example 5.7.

Consider an table with constant column sums . The row sums are determined by . If the table is created from the counts of dropping balls in boxes, with each box equally likely, then the expected number of zero entries is

If then , and the following theorem shows that the number of zeros has a Poisson distribution under these assumptions. Indeed, it shows this for varying column sums.

Theorem 5.8.

Suppose that and fix sequences such that

Let be the number of zeros in a Fisher-Yates contingency table of size with constant row sums and column sums . Then

Proof.

Let Multinomial, with the probabilities chosen so that . Then conditioned limit theorem (Corollary 3.5 in [64]) says that if

where has no normal component, then

If is a multinomial generated by dropping balls in boxes, with probabilities , and if

then the number of empty boxes is asymptotically Poisson (e.g. Theorem 6D in [7]). Thus the condition

means that is asymptotically Poisson and so is Poisson.

∎

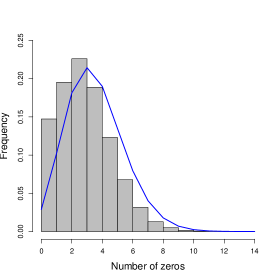

Preliminary computations indicate that Theorem 5.8 will hold with row sums that do not vary too much. Figure 1 shows the result from simulations for the number of zeros in a table with row and column sums fixed.

5.3 Further questions

It is natural to ask further questions about the distribution of natural features of the tables representing double cosets. Three that stand out:

-

1.

The positions of the zeros under the hypotheses of Theorem 5.8.

-

2.

The size and distribution of the maximum entry in the table.

-

3.

The RSK shape: Knuth’s extension of the Robinson-Schensted correspondence assigns to a table a pair of semi-standard Young tableux of the same shape. We have not seen these statistics used in statistical work. So much is known about RSK asymptotics that this may fall out easily.

- 4.

-

5.

Going further, this section has focused on enumerative probabilistic theorems for parabolic subgroups of the symmetric group. The questions make sense for parabolic subgroups of any finite Coxeter group. An enormous amount of combinatorial description is available (how does one describe double cosets?). This is wonderfully summarized in the very accessible paper [13]. In any Coxeter group, each double coset contains a unique minimal length representative. These minimal length double coset representatives can be used as identifiers for the double coset. See [61] for more on this. The focus of [13] is understanding with fixed as and vary over subsets of the generating reflections.

Acknowledgements

We thank Jason Fulman, Bob Guralnick, Jimmy He, Marty Isaacs, Slim Kammoun, Sumit Mukherjee, Arun Ram, Mehrdad Shahshahani, Richard Stanley, Nat Theim, and Chenyang Zhong for their help with this paper. MS is supported by a National Defense Science & Engineering graduate fellowship. Research supported in part by National Science Foundation grant DMS 1954042.

References

- Agresti [1992] Agresti, A., 1992. A survey of exact inference for contingency tables. Statist. Sci. 7, 131–177. URL: http://links.jstor.org.stanford.idm.oclc.org/sici?sici=0883-4237(199202)7:1<131:ASOEIF>2.0.CO;2-A&origin=MSN. with comments and a rejoinder by the author.

- Agresti [2013] Agresti, A., 2013. Categorical data analysis. Wiley Series in Probability and Statistics. third ed., Wiley-Interscience [John Wiley & Sons], Hoboken, NJ.

- Aguiar et al. [2012] Aguiar, M., André, C., Benedetti, C., Bergeron, N., Chen, Z., Diaconis, P., Hendrickson, A., Hsiao, S., Isaacs, I.M., Jedwab, A., Johnson, K., Karaali, G., Lauve, A., Le, T., Lewis, S., Li, H., Magaard, K., Marberg, E., Novelli, J.C., Pang, A., Saliola, F., Tevlin, L., Thibon, J.Y., Thiem, N., Venkateswaran, V., Vinroot, C.R., Yan, N., Zabrocki, M., 2012. Supercharacters, symmetric functions in noncommuting variables, and related Hopf algebras. Adv. Math. 229, 2310–2337. URL: https://doi-org.stanford.idm.oclc.org/10.1016/j.aim.2011.12.024, doi:10.1016/j.aim.2011.12.024.

- Anderson et al. [2010] Anderson, G.W., Guionnet, A., Zeitouni, O., 2010. An introduction to random matrices. volume 118 of Cambridge Studies in Advanced Mathematics. Cambridge University Press, Cambridge.

- Arratia et al. [2003] Arratia, R., Barbour, A.D., Tavaré, S., 2003. Logarithmic combinatorial structures: a probabilistic approach. EMS Monographs in Mathematics, European Mathematical Society (EMS), Zürich. URL: https://doi-org.stanford.idm.oclc.org/10.4171/000, doi:10.4171/000.

- Bannai et al. [1990] Bannai, E., Kawanaka, N., Song, S.Y., 1990. The character table of the Hecke algebra . J. Algebra 129, 320–366. URL: https://doi-org.stanford.idm.oclc.org/10.1016/0021-8693(90)90224-C, doi:10.1016/0021-8693(90)90224-C.

- Barbour et al. [1992] Barbour, A.D., Holst, L., Janson, S., 1992. Poisson approximation. volume 2 of Oxford Studies in Probability. The Clarendon Press, Oxford University Press, New York. Oxford Science Publications.

- Barvinok [2010] Barvinok, A., 2010. What does a random contingency table look like? Combin. Probab. Comput. 19, 517–539. URL: https://doi-org.stanford.idm.oclc.org/10.1017/S0963548310000039, doi:10.1017/S0963548310000039.

- Basu et al. [2017] Basu, R., Bhatnagar, N., et al., 2017. Limit theorems for longest monotone subsequences in random mallows permutations, in: Annales de l’Institut Henri Poincaré, Probabilités et Statistiques, Institut Henri Poincaré. pp. 1934–1951.

- Baumeister [1997] Baumeister, B., 1997. Factorizations of primitive permutation groups. J. Algebra 194, 631–653. URL: https://doi-org.stanford.idm.oclc.org/10.1006/jabr.1997.7027, doi:10.1006/jabr.1997.7027.

- Bhatnagar and Peled [2015] Bhatnagar, N., Peled, R., 2015. Lengths of monotone subsequences in a Mallows permutation. Probab. Theory Related Fields 161, 719–780. URL: https://doi-org.stanford.idm.oclc.org/10.1007/s00440-014-0559-7, doi:10.1007/s00440-014-0559-7.

- Bhattacharya and Mukherjee [2017] Bhattacharya, B.B., Mukherjee, S., 2017. Degree sequence of random permutation graphs. Ann. Appl. Probab. 27, 439–484. URL: https://doi-org.stanford.idm.oclc.org/10.1214/16-AAP1207, doi:10.1214/16-AAP1207.

- Billey et al. [2018] Billey, S.C., Konvalinka, M., Petersen, T.K., Slofstra, W., Tenner, B.E., 2018. Parabolic double cosets in Coxeter groups. Electron. J. Combin. 25, Paper No. 1.23, 66. URL: https://doi-org.stanford.idm.oclc.org/10.37236/6741, doi:10.37236/6741.

- Bishop et al. [2007] Bishop, Y.M.M., Fienberg, S.E., Holland, P.W., 2007. Discrete multivariate analysis: theory and practice. Springer, New York. With the collaboration of Richard J. Light and Frederick Mosteller, Reprint of the 1975 original.

- Blackburn et al. [2007] Blackburn, S.R., Neumann, P.M., Venkataraman, G., 2007. Enumeration of finite groups. volume 173 of Cambridge Tracts in Mathematics. Cambridge University Press, Cambridge. URL: https://doi-org.stanford.idm.oclc.org/10.1017/CBO9780511542756, doi:10.1017/CBO9780511542756.

- Borga [2020] Borga, J., 2020. Local convergence for permutations and local limits for uniform -avoiding permutations with . Probab. Theory Related Fields 176, 449–531. URL: https://doi-org.stanford.idm.oclc.org/10.1007/s00440-019-00922-4, doi:10.1007/s00440-019-00922-4.

- Borodin [2011] Borodin, A., 2011. Determinantal point processes, in: The Oxford handbook of random matrix theory. Oxford Univ. Press, Oxford, pp. 231–249.

- Borodin et al. [2010] Borodin, A., Diaconis, P., Fulman, J., 2010. On adding a list of numbers (and other one-dependent determinantal processes). Bull. Amer. Math. Soc. (N.S.) 47, 639–670. URL: https://doi-org.stanford.idm.oclc.org/10.1090/S0273-0979-2010-01306-9, doi:10.1090/S0273-0979-2010-01306-9.

- Borodin and Olshanski [2017] Borodin, A., Olshanski, G., 2017. Representations of the infinite symmetric group. volume 160 of Cambridge Studies in Advanced Mathematics. Cambridge University Press, Cambridge. URL: https://doi-org.stanford.idm.oclc.org/10.1017/CBO9781316798577, doi:10.1017/CBO9781316798577.

- Carter [1993] Carter, R.W., 1993. Finite groups of Lie type. Wiley Classics Library, John Wiley & Sons, Ltd., Chichester. Conjugacy classes and complex characters, Reprint of the 1985 original, A Wiley-Interscience Publication.

- Ceccherini-Silberstein et al. [2008] Ceccherini-Silberstein, T., Scarabotti, F., Tolli, F., 2008. Harmonic analysis on finite groups. volume 108 of Cambridge Studies in Advanced Mathematics. Cambridge University Press, Cambridge. URL: https://doi-org.stanford.idm.oclc.org/10.1017/CBO9780511619823, doi:10.1017/CBO9780511619823. representation theory, Gelfand pairs and Markov chains.

- Chaganty and Sethuraman [1985] Chaganty, N.R., Sethuraman, J., 1985. Large deviation local limit theorems for arbitrary sequences of random variables. The Annals of Probability , 97–114.

- Chen et al. [2005] Chen, Y., Diaconis, P., Holmes, S.P., Liu, J.S., 2005. Sequential Monte Carlo methods for statistical analysis of tables. J. Amer. Statist. Assoc. 100, 109–120. URL: https://doi-org.stanford.idm.oclc.org/10.1198/016214504000001303, doi:10.1198/016214504000001303.

- Chern et al. [2014] Chern, B., Diaconis, P., Kane, D.M., Rhoades, R.C., 2014. Closed expressions for averages of set partition statistics. Res. Math. Sci. 1, Art. 2, 32. URL: https://doi-org.stanford.idm.oclc.org/10.1186/2197-9847-1-2, doi:10.1186/2197-9847-1-2.

- Chern et al. [2015] Chern, B., Diaconis, P., Kane, D.M., Rhoades, R.C., 2015. Central limit theorems for some set partition statistics. Adv. in Appl. Math. 70, 92–105. URL: https://doi-org.stanford.idm.oclc.org/10.1016/j.aam.2015.06.008, doi:10.1016/j.aam.2015.06.008.

- Crane [2016] Crane, H., 2016. The ubiquitous Ewens sampling formula. Statist. Sci. 31, 1–19. URL: https://doi-org.stanford.idm.oclc.org/10.1214/15-STS529, doi:10.1214/15-STS529.

- Crane et al. [2018] Crane, H., DeSalvo, S., Elizalde, S., 2018. The probability of avoiding consecutive patterns in the Mallows distribution. Random Structures Algorithms 53, 417–447. URL: https://doi-org.stanford.idm.oclc.org/10.1002/rsa.20776, doi:10.1002/rsa.20776.

- Curtis and Reiner [2006] Curtis, C.W., Reiner, I., 2006. Representation theory of finite groups and associative algebras. AMS Chelsea Publishing, Providence, RI. URL: https://doi-org.stanford.idm.oclc.org/10.1090/chel/356, doi:10.1090/chel/356. reprint of the 1962 original.

- Diaconis [1988] Diaconis, P., 1988. Group representations in probability and statistics. volume 11 of Institute of Mathematical Statistics Lecture Notes—Monograph Series. Institute of Mathematical Statistics, Hayward, CA.

- Diaconis [2003] Diaconis, P., 2003. Patterns in eigenvalues: the 70th Josiah Willard Gibbs lecture. Bull. Amer. Math. Soc. (N.S.) 40, 155–178. URL: https://doi-org.stanford.idm.oclc.org/10.1090/S0273-0979-03-00975-3, doi:10.1090/S0273-0979-03-00975-3.

- Diaconis and Efron [1985] Diaconis, P., Efron, B., 1985. Testing for independence in a two-way table: new interpretations of the chi-square statistic. Ann. Statist. 13, 845–913. URL: https://doi-org.stanford.idm.oclc.org/10.1214/aos/1176349634, doi:10.1214/aos/1176349634. with discussions and with a reply by the authors.

- Diaconis and Gangolli [1995] Diaconis, P., Gangolli, A., 1995. Rectangular arrays with fixed margins, in: Discrete probability and algorithms (Minneapolis, MN, 1993). Springer, New York. volume 72 of IMA Vol. Math. Appl., pp. 15–41. URL: https://doi-org.stanford.idm.oclc.org/10.1007/978-1-4612-0801-3_3, doi:10.1007/978-1-4612-0801-3_3.

- Diaconis et al. [1983] Diaconis, P., Graham, R.L., Kantor, W.M., 1983. The mathematics of perfect shuffles. Adv. in Appl. Math. 4, 175–196. URL: https://doi-org.stanford.idm.oclc.org/10.1016/0196-8858(83)90009-X, doi:10.1016/0196-8858(83)90009-X.

- Diaconis and Ram [2000] Diaconis, P., Ram, A., 2000. Analysis of systematic scan Metropolis algorithms using Iwahori-Hecke algebra techniques. Michigan Math. J. 48, 157–190. URL: https://doi-org.stanford.idm.oclc.org/10.1307/mmj/1030132713, doi:10.1307/mmj/1030132713. dedicated to William Fulton on the occasion of his 60th birthday.

- Diaconis and Shahshahani [1987] Diaconis, P., Shahshahani, M., 1987. Time to reach stationarity in the Bernoulli-Laplace diffusion model. SIAM J. Math. Anal. 18, 208–218. URL: https://doi-org.stanford.idm.oclc.org/10.1137/0518016, doi:10.1137/0518016.

- Diaconis et al. [1998] Diaconis, P., Sturmfels, B., et al., 1998. Algebraic algorithms for sampling from conditional distributions. Annals of statistics 26, 363–397.

- Dittmer [2019] Dittmer, S., 2019. Counting linear extensions and contingency tables. Ph.D. thesis. UCLA.

- Dittmer et al. [2020] Dittmer, S., Lyu, H., Pak, I., 2020. Phase transition in random contingency tables with non-uniform margins. Trans. Amer. Math. Soc. 373, 8313–8338. URL: https://doi-org.stanford.idm.oclc.org/10.1090/tran/8094, doi:10.1090/tran/8094.

- Dixon [2002] Dixon, J.D., 2002. Probabilistic group theory. Mathematical Reports of the Academy of Sciences 24, 1–15.

- Dummit and Foote [2004] Dummit, D.S., Foote, R.M., 2004. Abstract algebra. Third ed., John Wiley & Sons, Inc., Hoboken, NJ.

- Erdős and Turán [1965] Erdős, P., Turán, P., 1965. On some problems of a statistical group-theory. I. Z. Wahrscheinlichkeitstheorie und Verw. Gebiete 4, 175–186 (1965). URL: https://doi-org.stanford.idm.oclc.org/10.1007/BF00536750, doi:10.1007/BF00536750.

- Erdős and Turán [1967a] Erdős, P., Turán, P., 1967a. On some problems of a statistical group-theory. II. Acta math. Acad. Sci. Hungar. 18, 151–163. URL: https://doi-org.stanford.idm.oclc.org/10.1007/BF02020968, doi:10.1007/BF02020968.

- Erdős and Turán [1967b] Erdős, P., Turán, P., 1967b. On some problems of a statistical group-theory. III. Acta Math. Acad. Sci. Hungar. 18, 309–320. URL: https://doi-org.stanford.idm.oclc.org/10.1007/BF02280290, doi:10.1007/BF02280290.

- Erdős and Turán [1968] Erdős, P., Turán, P., 1968. On some problems of a statistical group-theory. IV. Acta Math. Acad. Sci. Hungar. 19, 413–435. URL: https://doi-org.stanford.idm.oclc.org/10.1007/BF01894517, doi:10.1007/BF01894517.

- Féray [2013] Féray, V., 2013. Asymptotic behavior of some statistics in Ewens random permutations. Electron. J. Probab. 18, no. 76, 32. URL: https://doi-org.stanford.idm.oclc.org/10.1214/EJP.v18-2496, doi:10.1214/EJP.v18-2496.

- Forrester [2010] Forrester, P.J., 2010. Log-gases and random matrices. volume 34 of London Mathematical Society Monographs Series. Princeton University Press, Princeton, NJ. URL: https://doi-org.stanford.idm.oclc.org/10.1515/9781400835416, doi:10.1515/9781400835416.

- Freedman and Lane [1983a] Freedman, D., Lane, D., 1983a. A nonstochastic interpretation of reported significance levels. Journal of Business & Economic Statistics 1, 292–298.

- Freedman and Lane [1983b] Freedman, D.A., Lane, D., 1983b. Significance testing in a nonstochastic setting. A festschrift for Erich L. Lehmann , 185–208.

- Fulman [2002] Fulman, J., 2002. Random matrix theory over finite fields. Bull. Amer. Math. Soc. (N.S.) 39, 51–85. URL: https://doi-org.stanford.idm.oclc.org/10.1090/S0273-0979-01-00920-X, doi:10.1090/S0273-0979-01-00920-X.

- Fulman [2016] Fulman, J., 2016. A generating function approach to counting theorems for square-free polynomials and maximal tori. Ann. Comb. 20, 587–599. URL: https://doi-org.stanford.idm.oclc.org/10.1007/s00026-016-0310-4, doi:10.1007/s00026-016-0310-4.

- Fulman et al. [2019] Fulman, J., Kim, G.B., Lee, S., 2019. Central limit theorem for peaks of a random permutation in a fixed conjugacy class of . arXiv preprint arXiv:1902.00978 .

- Gabriel and Roĭter [1992] Gabriel, P., Roĭter, A.V., 1992. Representations of finite-dimensional algebras, in: Algebra, VIII. Springer, Berlin. volume 73 of Encyclopaedia Math. Sci., pp. 1–177. With a chapter by B. Keller.

- Gladkich et al. [2018] Gladkich, A., Peled, R., et al., 2018. On the cycle structure of mallows permutations. The Annals of Probability 46, 1114–1169.

- Gnedin and Olshanski [2010] Gnedin, A., Olshanski, G., 2010. -exchangeability via quasi-invariance. Ann. Probab. 38, 2103–2135. URL: https://doi-org.stanford.idm.oclc.org/10.1214/10-AOP536, doi:10.1214/10-AOP536.

- Gnedin and Olshanski [2012] Gnedin, A., Olshanski, G., 2012. The two-sided infinite extension of the Mallows model for random permutations. Adv. in Appl. Math. 48, 615–639. URL: https://doi-org.stanford.idm.oclc.org/10.1016/j.aam.2012.01.001, doi:10.1016/j.aam.2012.01.001.

- Guralnick [2020] Guralnick, R.M., 2020. On the singular value decomposition over finite fields and orbits of gu x gu. arXiv:1805.06999.

- Halverson and Ram [2001] Halverson, T., Ram, A., 2001. -rook monoid algebras, Hecke algebras, and Schur-Weyl duality. Zap. Nauchn. Sem. S.-Peterburg. Otdel. Mat. Inst. Steklov. (POMI) 283, 224--250, 262--263. URL: https://doi-org.stanford.idm.oclc.org/10.1023/B:JOTH.0000024623.99412.13, doi:10.1023/B:JOTH.0000024623.99412.13.

- He [2019] He, J., 2019. A characteristic map for the symmetric space of symplectic forms over a finite field. arXiv:1906.05966.

- He [2020a] He, J., 2020a. A central limit theorem for descents of a mallows permutation and its inverse. arXiv:2005.09802.

- He [2020b] He, J., 2020b. Random walk on the symplectic forms over a finite field. Algebraic Combinatorics 3, 1165--1181.

- He [2007] He, X., 2007. Minimal length elements in some double cosets of Coxeter groups. Adv. Math. 215, 469--503. URL: https://doi-org.stanford.idm.oclc.org/10.1016/j.aim.2007.04.005, doi:10.1016/j.aim.2007.04.005.

- Höglund [1978] Höglund, T., 1978. Sampling from a finite population. a remainder term estimate. Scandinavian Journal of Statistics , 69--71.

- Holst [1979] Holst, L., 1979. A unified approach to limit theorems for urn models. J. Appl. Probab. 16, 154--162. URL: https://doi-org.stanford.idm.oclc.org/10.2307/3213383, doi:10.2307/3213383.

- Holst [1981] Holst, L., 1981. Some conditional limit theorems in exponential families. Ann. Probab. 9, 818--830. URL: http://links.jstor.org.stanford.idm.oclc.org/sici?sici=0091-1798(198110)9:5<818:SCLTIE>2.0.CO;2-D&origin=MSN.

- Hoppen et al. [2013] Hoppen, C., Kohayakawa, Y., Moreira, C.G., Ráth, B., Menezes Sampaio, R., 2013. Limits of permutation sequences. J. Combin. Theory Ser. B 103, 93--113. URL: https://doi-org.stanford.idm.oclc.org/10.1016/j.jctb.2012.09.003, doi:10.1016/j.jctb.2012.09.003.

- Howe [1992] Howe, R., 1992. A century of Lie theory, in: American Mathematical Society centennial publications, Vol. II (Providence, RI, 1988). Amer. Math. Soc., Providence, RI, pp. 101--320.

- Inglis et al. [1986] Inglis, N.F.J., Liebeck, M.W., Saxl, J., 1986. Multiplicity-free permutation representations of finite linear groups. Math. Z. 192, 329--337. URL: https://doi-org.stanford.idm.oclc.org/10.1007/BF01164008, doi:10.1007/BF01164008.

- James and Kerber [2009] James, G., Kerber, A., 2009. The representation theory of the symmetric group, cambridge u. Press, Cambridge .

- Joe [1985] Joe, H., 1985. An ordering of dependence for contingency tables. Linear algebra and its applications 70, 89--103.

- Jones [1996] Jones, A.R., 1996. A combinatorial approach to the double cosets of the symmetric group with respect to Young subgroups. European J. Combin. 17, 647--655. URL: https://doi-org.stanford.idm.oclc.org/10.1006/eujc.1996.0056, doi:10.1006/eujc.1996.0056.

- Kammoun [2020a] Kammoun, M.S., 2020a. On the longest common subsequence of conjugation invariant random permutations. The Electronic Journal of Combinatorics , 4--10.

- Kammoun [2020b] Kammoun, M.S., 2020b. Universality for random permutations and some other groups. arXiv:2012.05845.

- Kammoun et al. [2018] Kammoun, M.S., et al., 2018. Monotonous subsequences and the descent process of invariant random permutations. Electronic Journal of Probability 23.

- Kang and Klotz [1998] Kang, S.h., Klotz, J., 1998. Limiting conditional distribution for tests of independence in the two way table. Comm. Statist. Theory Methods 27, 2075--2082. URL: https://doi-org.stanford.idm.oclc.org/10.1080/03610929808832210, doi:10.1080/03610929808832210.

- Kim and Lee [2020] Kim, G.B., Lee, S., 2020. Central limit theorem for descents in conjugacy classes of . J. Combin. Theory Ser. A 169, 105123, 13. URL: https://doi-org.stanford.idm.oclc.org/10.1016/j.jcta.2019.105123, doi:10.1016/j.jcta.2019.105123.

- Lancaster [1969] Lancaster, H.O., 1969. The chi-squared distribution. John Wiley & Sons, Inc., New York-London-Sydney.

- Laue [1982] Laue, R., 1982. Computing double coset representatives for the generation of solvable groups, in: Computer algebra (Marseille, 1982). Springer, Berlin-New York. volume 144 of Lecture Notes in Comput. Sci., pp. 65--70.

- Lehmann and Romano [2006] Lehmann, E.L., Romano, J.P., 2006. Testing statistical hypotheses. Springer Science & Business Media.

- Letac [1981] Letac, G., 1981. Problèmes classiques de probabilité sur un couple de Gelfand, in: Analytical methods in probability theory (Oberwolfach, 1980). Springer, Berlin-New York. volume 861 of Lecture Notes in Math., pp. 93--120.

- Macdonald [1998] Macdonald, I.G., 1998. Symmetric functions and Hall polynomials. Oxford university press.

- Marshall et al. [1979] Marshall, A.W., Olkin, I., Arnold, B.C., 1979. Inequalities: theory of majorization and its applications. volume 143. Springer.

- Mueller and Starr [2013] Mueller, C., Starr, S., 2013. The length of the longest increasing subsequence of a random Mallows permutation. J. Theoret. Probab. 26, 514--540. URL: https://doi-org.stanford.idm.oclc.org/10.1007/s10959-011-0364-5, doi:10.1007/s10959-011-0364-5.

- Mukherjee [2016a] Mukherjee, S., 2016a. Estimation in exponential families on permutations. Ann. Statist. 44, 853--875. URL: https://doi-org.stanford.idm.oclc.org/10.1214/15-AOS1389, doi:10.1214/15-AOS1389.

- Mukherjee [2016b] Mukherjee, S., 2016b. Fixed points and cycle structure of random permutations. Electron. J. Probab. 21, 1–--18. URL: https://doi-org.stanford.idm.oclc.org/10.1214/16-EJP4622, doi:10.1214/16-EJP4622.

- Rodrigues [1839] Rodrigues, O., 1839. Note sur les inversions, ou dérangements produits dans les permutations. J. de Math 4, 236--240.

- Saxl [1981] Saxl, J., 1981. On multiplicity-free permutation representations, in: Finite geometries and designs (Proc. Conf., Chelwood Gate, 1980), Cambridge Univ. Press, Cambridge-New York. pp. 337--353.

- Shalev [1999] Shalev, A., 1999. Probabilistic group theory. London Mathematical Society Lecture Note Series , 648--678.

- Shepp and Lloyd [1966] Shepp, L.A., Lloyd, S.P., 1966. Ordered cycle lengths in a random permutation. Trans. Amer. Math. Soc. 121, 340--357. URL: https://doi-org.stanford.idm.oclc.org/10.2307/1994483, doi:10.2307/1994483.

- Slattery [2001] Slattery, M.C., 2001. Computing double cosets in soluble groups. J. Symbolic Comput. 31, 179--192. URL: https://doi-org.stanford.idm.oclc.org/10.1006/jsco.1999.1005, doi:10.1006/jsco.1999.1005. computational algebra and number theory (Milwaukee, WI, 1996).

- Solomon [1990] Solomon, L., 1990. The Bruhat decomposition, Tits system and Iwahori ring for the monoid of matrices over a finite field. Geom. Dedicata 36, 15--49. URL: https://doi-org.stanford.idm.oclc.org/10.1007/BF00181463, doi:10.1007/BF00181463.

- Stanley [1986] Stanley, R.P., 1986. What is enumerative combinatorics?, in: Enumerative combinatorics. Springer, pp. 1--63.

- Starr [2009] Starr, S., 2009. Thermodynamic limit for the Mallows model on . J. Math. Phys. 50, 095208, 15. URL: https://doi-org.stanford.idm.oclc.org/10.1063/1.3156746, doi:10.1063/1.3156746.

- Starr and Walters [2018] Starr, S., Walters, M., 2018. Phase uniqueness for the Mallows measure on permutations. J. Math. Phys. 59, 063301, 28. URL: https://doi-org.stanford.idm.oclc.org/10.1063/1.5017924, doi:10.1063/1.5017924.

- Suzuki [1982] Suzuki, M., 1982. Group theory. I. volume 247 of Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences]. Springer-Verlag, Berlin-New York. Translated from the Japanese by the author.

- Watterson [1976] Watterson, G.A., 1976. The stationary distribution of the infinitely-many neutral alleles diffusion model. J. Appl. Probability 13, 639--651. URL: https://doi-org.stanford.idm.oclc.org/10.1017/s0021900200104309, doi:10.1017/s0021900200104309.