On the relation of powerflow and Telegrapher’s equations: continuous and numerical Lyapunov stability

Abstract

In this contribution we analyze the exponential stability of power networks modeled with the Telegrapher’s equations as a system of balance laws on the edges. We show the equivalence of periodic solutions of these Telegrapher’s equations and solutions to the well-established powerflow equations. In addition we provide a second-order accurate numerical scheme to integrate the powerflow equations and show (up to the boundary conditions) Lyapunov stability of the scheme.

AMS subject classifications: 93D05, 65M06

Keywords: power networks, Lyapunov function, stability, numerical approximations

1 Introduction

In recent years, due to the need to restructure energy systems to incorporate more renewable energy sources renewed interest into energy-systems has sparked. In the case of electric transmission lines several mathematical approaches can be found in the literature, see for example [And15, Bie15, FR16, GHM21] for an overview. All modeling approaches rely on a graph structure where generators of electrical powers and consumers at nodes are connected by transmission lines. From a physical point of view, voltage and current are transported along the lines while power loss might occur due to resistances. In many applications, the so-called power flow equations provide a well-established tool to analyze the performance of electric transmission lines over time. Mathematically, the resulting nonlinear system of equations is typically solved via Newton’s method. Another approach to study not only the temporal resolution of power flow but also the spatial resolution in transmission lines are the spatially one-dimensional Telegrapher’s equations. These equations are a coupled system of linear hyperbolic balance laws for voltage and current. In this work, we aim to associate these two modeling approaches and therefore rigorously analyze the relation between the powerflow equations used to model power systems and the Telegrapher’s equations, that describe the underlying physics in more detail.

In terms of operation of electric transmission lines the investigation of stability issues is of great importance. Recent research in this direction include exponential stability considerations [EK17] as well as open- and closed loop problems. Open loop problems tackle questions of optimal electricity input [GKL19, GPT19, GT18], while closed loop control are concerned with feedback control [Gug14] or boundary stabilization [GPR18]. Similar to the ideas presented in [GHS16], we study the stability of the Telegrapher’s equations using the concept of Lyapunov functions [BC16]. We prove a stability result for the Telegrapher’s equations on networks with (linear) coupling conditions and show how such a solution can be thought of as a solution to the powerflow equations. In particular, we are interested in how a numerical approximation might mimic the Lyapunov stability as for example introduced in [BC16]. In contrast to the already existing literature [GH19, GHS16, GS17], where only first order schemes have been applied, we introduce a numerical scheme of second order to examine the stability. A numerical analysis shows that the proposed scheme is Lyapunov stable and can be used to numerically study power networks as the simulation results indicate.

The paper is organized as follows: In section 2 we present the physical meaning of the Telegrapher’s equation, define the network setting and prove theoretical properties concerning the Lyapunov stability. Section 3 is concerned with the derivation of the well-known powerflow equations from the Telegrapher’s equation with a particular focus on the power coupling conditions. In section 4, a numerical scheme of second order is introduced to solve the Telegrapher’s equation. The Lyapunov stability for the numerical approximation is also discussed in detail. The last section 5 deals with numerical experiments to investigate the performance of the scheme.

2 Solution structure of the Telegrapher’s equations

The Telegrapher’s equation is a system of linear hyperbolic partial differential equations (PDE) with linear source term in one space dimension and therefore often called balance law, see [GHS16, Jia05] for more details. It models the time-dependent evolution of voltage and current on a transmission line and can be written in terms of an initial-boundary value problem on a single line with and as:

| (1) | ||||

where and

| (2) |

Here, are constants depending on the line, is some time horizon and is the length of the line. The vector is composed of the voltage and the current . In the engineering literature (e.g. [MM01, §1.2.2 Lossy Transmission Lines]) the Telegrapher’s equation is usually written as

Yet another form of the Telegraper’s equation is gotten by transformation into characteristic variables :

| (3) | ||||

so that equation (1) turns into

with

| (4) |

and , . Note that the eigenvalues of are and and that in addition holds.

In a power network setting, these equations are defined on the lines and are coupled at the nodes by some conditions. The overall aim of this work is to show that in so-called alternating current (AC) networks — which are almost all power networks in use in energy systems — the solution normally used in engineering, namely the solution to the powerflow equations, can be thought of as an exponentially stable solution of the Telegrapher’s equations defined on the power network. In an AC power network all voltages and currents that serve as boundary conditions are sinusoidal with the same angular frequency , that is, they are of the form for real and .

We start of by examining a time-periodic solution of the Telegrapher’s equations on a line with the same angular frequency as that of the boundary conditions. Therefore we write and as Fourier series in time,

| (5) | ||||

with complex-valued functions , which we call complex voltage and complex current. For the voltage and current to be real-valued, we impose

Due to the linear independence of the system the Telegrapher’s equations decompose into a decoupled family of complex linear ordinary differential equations (ODEs), indexed by , which only governs and via

| (6) | ||||

We now define

and it is easily verified, that

| (7) | ||||

solve equations (6). Here are the complex voltages at either sides of the line, which we choose as boundary conditions for now. It is also possible to prescribe the current at the end of a line as done in the network setting in subsection 2.1.

Note also that and are never zero because . Plugging these into equation (5) yields a solution to the Telegrapher’s equations. This solution will be the basis for deriving the powerflow equations in Section 3. Next, we will investigate the stability of the Telegrapher’s equation on networks.

2.1 Stability of the Telegrapher’s equations on networks

Before we can study the stability of the Telegrapher’s equations for power networks, we have to introduce the network setting and coupling conditions. Stability of similar networks has been analyzed, see e.g. [EK17, GPR18, GHS16, GS17]. Like the authors of [EK17, GPR18], we also also apply the formalism of operator semigroups to our network to show well-posedness of our problem. Similar to [EK17] we show the stability of the system without feedback control.

We discuss two different stability estimates depending on the network. The first one yields -stability for the networks we examine. The second one yields stability in but is valid only for a network with equal line parameters.

In the end we want to model power networks, that is, generators of electrical powers and consumers (loads), that are connected by transmission lines. Hence we use a directed graph as a power network model. Let therefore be a finite directed graph with vertex set and edge set . An edge consists of an interval together with edge parameters . To a vertex we assign a virtual point and for an edge starting at we identify with . For an edge ending in we identify with . The reasoning behind this identification is to interpret the graph as a subset of some , where the start and endpoints of an edge are actually the points where the vertices are located. This image is most natural for planar graphs, where can be used.

Let further where denotes the nodes with a generator and denotes the nodes with a load so that every node is either a generator or a load. Also for let be the set of edges connected to . In addition we define the function

| (8) |

which distinguishes start and end nodes of an edge.

Then we formulate the linear inhomogeneous initial-boundary-value problem (IIBVP) on the graph ,

| (IIBVP) |

with matrices and of the structure of (2) and under the conditions

| (IC) | ||||

| (CC) | ||||

| (KCg) | ||||

| (KCl) |

where (IC) is the initial condition, (CC) is a continuity condition for the voltage in the nodes, (KCg) is a coupling condition fixing the voltage at generators and (KCl) is a coupling condition fixing the current at loads. In order to show well-posedness we use the theory of operator semigroups, see [EN01] and especially [KMN03]. Therefore we introduce the following setting: As underlying Banach (and actually Hilbert) space we take

with the scalar product

| (9) |

As linear operator we take

and as its domain the space

| (10) |

In addition we choose the boundary operator

with

which maps a collection of -functions on the edges to the evaluation of line voltages at generator nodes, the differences in line voltages at load nodes and load currents, respectively. Note that is continuous on as a concatenation of the (continuous) trace operator and a finite-dimensional linear mapping.

To prove well-posedness we first verify the prerequisites of [KMN03, Assumption 3.1] in

Lemma 1.

The operator satisfies

-

(G1)

The restriction of to , namely is densely defined, closed and has non-empty resolvent set.

-

(G2)

is surjective.

-

(G3)

The combined operator

is closed.

Proof.

For this proof we consider the basis introduced in (3), where is of the form

For (G1) we first note that the space with zero boundary conditions, i.e.,

is a subset of , which is well-known to be a dense subspace of . Then we note that is just the sum of the spatial derivative and a bounded linear operator. As is continuous on , its kernel is a closed subspace therein. Together we find that is closed, if the derivative operator is closed, which is well-known. For the non-empty resolvent set we show that is in the resolvent set of , that is is injective and its left inverse is densely-defined and bounded. The domain of is just the range of , so we show this range to be dense in . Therefore we show that the space of test functions fulfills as it is well-known that is dense in .

Let . There holds and as the zero boundary conditions essentially decouple different edges, we only consider one edge, given by . The Fourier transform of (which is well-defined as ) is given by

The operator evaluated on is given by

The matrix is invertible for all , because . Let us call this matrix . If we choose

we have . Then we get and . It remains to show that is again supported in . This is the case because of the Paley–Wiener theorem, see [Rud87, Theorem 19.3], which relates -functions supported on an interval and their Fourier transforms. Together we have . Finally using and the definition of , it is easily computed that is bounded. The injectivity of will be shown in 2.

For (G2) we note that functions, that on every edge have the form

are in and can be used to construct any value for .

For (G3) we note again that is continuous on and that is closed, hence their combination is as well. ∎

Lemma 2.

is injective.

Proof.

Here we consider again the basis, where the components of are the voltage and the current . Therefore consider an element . Such is a valid initial condition for (IIBVP) with homogeneous coupling conditions and a corresponding solution given by for all . This solution is at least once differentiable with respect to time and space. Therefore we can apply the reasoning of the following 4 to this special solution and find

As if and only if , we find that is injective. ∎

Lemma 3.

The (IIBVP) is well-posed and therefore admits a solution for and suitably smooth , .

Proof.

Following [KMN03], it remains to show that generates a strongly continuous semigroup. For this we first omit the matrices in and note that the resulting operator is skew-symmetric with respect to the scalar product (9) of . (The boundary terms arising in integration by parts vanish, because ). Then we cite [EN01, 3.24 Theorem. (Stone, 1932)] to see that generates a unitary group. We now add again, which is a bounded linear operator and use [EN01, Proposition 1.12], showing that the full operator also generates a strongly continuous semigroup. The last step of non-vanishing follows from application of the variation of constants formula [EN01, VI, Corollary 7.8], which introduces some smoothness conditions on . The exact nature of these condition is of no consequence to us but could be found by working through [KMN03] to incorporate the boundary conditions as initial conditions together with a source term. ∎

With 3 we have a -solution to (IIBVP). We now show its exponential stability using the Lyapunov function

Proposition 4.

Two solutions of the (IIBVP) with identical coupling conditions but possibly different initial conditions grow closer exponentially in the -norm.

Proof.

We take the difference of the two solutions with initial condition and examine the derivative of the Lyapunov function. As before the coupling condition for is then homogeneous.

| (11) | ||||

where the third equality stems from (CC) and the fourth from (KCg) or (KCl) depending on the node being either a load or a generator. Note that because of the homogeneous boundary conditions, for generators there holds and for loads there holds . This, together with the fact that is equivalent to the standard -scalar product, yields -stability. ∎

We have only shown -stability. Unfortunately this is all we can hope for in the relevant case of different transmission lines. In spite of this we will sketch the following result:

Proposition 5.

For a graph where all line parameters are equal: and an initial condition in (and sufficiently smooth coupling conditions) the above problem converges exponentially in the supremum norm.

5 is proved by noting that we could choose for the domain of operator in (10) without invalidating the proofs. From the coupling conditions in (IIBVP) we derive

and similarly

which means that the solution fulfills additional coupling conditions in this case. Note that these calculations are only possible because the line parameters are equal and because the coupling conditions are assumed to be differentiable. In this case, it is possible to mimic the stability proof above but for the enhanced Lyapunov function

3 From Telegrapher’s equation to powerflow equations

Now that we have established that only the coupling conditions matter, we examine periodic coupling conditions and their relation to the powerflow equations. This means the functions and in (KCg) and (KCl) shall be of the form

where quantities with a hat are prescribed at the node. A smooth solution to (IIBVP) with these coupling conditions is given by a Fourier series with coefficients of the form (7), where the coupling conditions translate to linear conditions on the complex voltage and current and for each transmission line. The correct coefficients in this expression can be calculated by solving the linear system stemming from the coupling conditions. As the system is linear, this can be done for each Fourier mode separately.

The Fourier mode of the current at the ends of a line can be expressed as

We see that the ingoing end behaves differently from the outgoing end, because of an overall minus sign in the second component. This is natural in the PDE setting as the sign of the current marks the direction of flow. By using and , we can transform the system into

This makes the transmission line invariant under switching orientation and positive currents mean currents leaving the node into the transmission line. A further benefit is that we can omit the function from equation (8). With this we come back to the whole network. By the continuity condition on the voltage, i.e. (CC), we do not need voltage Fourier modes for every transmission line, but only for each vertex. Therefore we introduce the variables as the th voltage Fourier mode at vertex .

This is different for the current. For a transmission between node and node we define the current leaving node in direction as

where , and now depend on the transmission line.

The net current at node is then just the sum of all current leaving that node,

| (12) |

where we set if node and are not connected. These equations are then combined for the whole network, i.e.,

| (13) |

where are the vectors of net current and voltage at each node and is the so-called admittance matrix. One can set up admittance matrices for different power networks, where not every edge is a transmission line. Yet in our case is given as

An admittance matrix is invertible, whenever not all of its row sums are zero (see [KP18, Theorem 1]). This is usually the case here, but we remark that it is possible to find a set of line parameters for which is singular.

That means the coupling conditions in the time periodic setting are usually solvable if all nodes are loads. If there are generator nodes, (13) can be reduced by inserting the values of and shifting them to the other side by altering . Concretely, we define the vector by

and

Then, we strike all lines (and columns respectively) from and that correspond to generator nodes and arrive at a new equation

in which is usually111Again by carefully choosing line parameters it is possible to make the resulting singular. still invertible and only load nodes are left. Therefore apart from pathological counter-examples the coupling conditions,

| (14) | ||||

which are again linear in the complex voltages, are solvable by functions defined by equations (5) through (7).

3.1 Power coupling conditions

In power networks we usually want to satisfy a power demand instead of a current demand.

Electric power at a node is given by the product of voltage and the net current,

One way to replace the linear coupling conditions (14) would be to prescribe at every load node. In the case where and are Fourier polynomials, that is there is , such that for , this yields equations for just as many unknown voltage Fourier modes222Up to now these are complex equations for complex Fourier modes but assuming yields real equations for as many real unknowns.. So depending on the concrete values of the system might be solvable. Unfortunately, except for small examples it is hard to decide a priori whether a given set of power coupling conditions is feasible, see for example [Jer+20].

The mixing of different Fourier modes can make the resulting coupling conditions quite cumbersome. Luckily in applications a strong simplification is done: It is assumed that all inputs are sinusoidal, meaning that the only non-vanishing Fourier modes are those for .

We use to express and define , similarly and find for the power

This suggests to define the so-called complex apparent power , its real part, the real power and its imaginary part, the reactive power , so that at the node it holds:

To define the powerflow equations we use the admittance matrix from (12):

of which we write the real and imaginary part as

For the complex apparent power this means

For every node we then find the nonlinear system of equations

which are the so-called powerflow equations.

The coupling conditions for our network problem are then usually chosen as follows:

-

•

All load nodes prescribe and .

-

•

All generators (with one exception) prescribe and .

-

•

The last generator, known as the slack bus, prescribes and .

These conditions lead to a system of nonlinear equations with two equations for each node to determine the two nodal variables and . For more information, we refer to [FR16, And15].

Unfortunately it is unclear how the system of powerflow equations can be transformed back into the PDE setting as it has an inherently periodic time dependence. Therefore, in order to examine the stability properties of the system in the following section, we will treat nodal voltages and currents only as linear coupling conditions in (IIBVP). We prescribe the net current at load nodes and the voltage at generators. The justification for this is, that “voltage is pushed” (set by the voltage source) and “current is pulled” (drawn by the load).

4 Numercial scheme

We aim to mimic the behavior of the analytical solution of (IIBVP) by a numerical approximation. We will first treat a single line, define the numerical scheme there and then prescribe numerical boundary conditions.

We approximate a solution of (1) by an approximation and compute the discrete solution via a splitting scheme. The numerical approximation is based on equation (3), where

is diagonal. The balance law is split into an ODE part

| (15) |

and a PDE part

| (16) |

Therefore we choose the discretization , , , and

Further, we define the lattice constant as

As splitting we use Strang splitting (see [LeV02, 17.4 Strang splitting]), meaning we make a half-step of equation (15), a full step of (16) and another half-step of (15).

Equation (15) is a linear ODE with constant coefficients, so we can solve it exactly up to machine precision with only constant computational costs by setting the ODE scheme to

As Strang splitting is of second order, we cannot hope to get higher accuracy and therefore choose a scheme for the conservation law (16) which is at most second order, namely a flux-limited Lax-Wendroff scheme (explained for example in [LeV02, 6.12 TVD limiters]) that for a single component is given for right and left moving waves as:

where is the wave speed and we define as usual

As limiter we choose the minmod-limiter,

which will become important for the numerical Lyapunov stability. As with any explicit finite volume scheme a necessary condition for stability is the CFL condition

| (17) |

which relates the lattice constant and the wave speed. The quantity is also called the CFL number.

We write the scheme (although it is not linear) as

so that the full split scheme can be written as

Having defined the scheme we come to the two main properties of it. We will now prove that the scheme is

-

•

total-variation-diminising and

-

•

Lyapunov stable.

As numerical Lyapunov function we choose

| (18) |

which is just the squared discrete -norm of the solution and hence corresponds directly to the analytical Lyapunov function.

As definition of total variation in two dimensions we choose the sum of the componentwise total variations:

| (19) |

Now we are able to discuss the following results:

Proposition 6.

The ODE-scheme (15) is Lyapunov stable and total-variation-diminishing.

For the proof we need a short lemma.

Lemma 7.

There holds

-

1.

The matrix has the structure

(20) -

2.

Its eigenvalues are given by , and fulfill .

-

3.

There holds .

Proof.

Consider the base change matrix

Note that a matrix fulfills

if and only if has the form (20). Therefore there holds . But commutes with change of basis and therefore

proving 1. The eigenvalues of can be computed from (20) and are . So they are also given by where are the eigenvalues of . Assertation 2 follows because . Lastly . ∎

Next we come to the

Proof of 6.

On the PDE side we find similar results.

Proposition 8.

The PDE-scheme is Lyapunov stable and total-variation-diminishing.

Proof.

For the claim of TVD we note that the total variation (19) is given as the sum of the variations in both components. As the PDE-scheme does not mix the components, it is overall total variation diminishing, if it is TVD each of its components. The TVD property of the minmod-limiter for the scalar case is a standard result found e.g. in [LeV02, 6.12 TVD Limiters].

The Lyapunov function (18) is also given as a sum of the components, namely the sum of the -norms squared. Therefore we examine -stability of the PDE-scheme for the linear advection equation (which is one component of (16)), given by

| (21) |

with the wave speed . The pair

is an entropy-entropy-flux pair for (21). According to [Tad87, Theorem 4.1] there is an entropy-conserving three-point scheme for this entropy. This scheme turns out to be the so-called naive scheme with numerical flux

and numerical viscosity

Now according to [Tad87, Theorem 5.2] a scheme with viscosity is entropy-stable if

for all . The viscosity of the minmod scheme is given by

because of the CFL condition (17) and . ∎

4.1 Coupling conditions

Now that we have established the stability of the scheme in the interior of the transmission line, we need to define the coupling conditions. Therefore we consider a node with a set of transmission lines, that all start at it and reformulate the combined Telegrapher’s equations on all these lines. We define the vector and the matrices

and also

which leads to the PDE

For line we define . If the node is a load with prescribed current , we have the following conditions:

To reformulate them we define the matrices

which yields the conditions333Note that is invertible, as its determinant is given by and . for the ghost cell values :

| (22) |

Note that , so for no energy is injected at the node. We still must choose and will do so by linear extrapolation. In principle one should use stable extrapolation (see [BMZ15]) to guard against non-smooth solutions but this seems to be unnecessary with high enough and .

For the mimmod scheme we need a second ghost cell . In principle it should be possible to use the time derivative of the coupling condition as in [BHH16] or [BK14], but in our setting it is much easier to simply use a first order extrapolation through the first couple of inner cell values and the newly-computed boundary value from (22).

Contrary, the generator coupling conditions are easier to determine as they essentially decouple different lines. When we prescribe the voltage at a node, this acts as a regular boundary condition for each attached line and can be treated as such. Alternatively we can write the generator coupling conditions similar to equation (22),

| (23) |

Regarding the stability of coupling conditions (22) and (23) we make the following remark.

Remark 9.

We note that any numerical entropy production at the nodes is countered by the decay in the ODE part, whenever and are great enough. Unfortunately we suppose that these coupling conditions are unstable if and are small enough. A rigorous analysis will be subject of future work.

5 Numerical examples

For the computations we wrote a package444The package is free software and be used and modified by anyone. It can be found under https://bitbucket.org/efokken/telegraph_numerics for the Julia programming language555see https://julialang.org/ (see [Bez+17]).

We will treat two examples, in which we compare exact periodic solutions, that correspond to powerflow solutions and numerical solutions computed with the splitting scheme from section 4. In addition we consider the behavior of the numerical Lyapunov function.

As we compare the splitting scheme to the powerflow solution, the coupling conditions in the node are given by sinusoidal functions, namely by

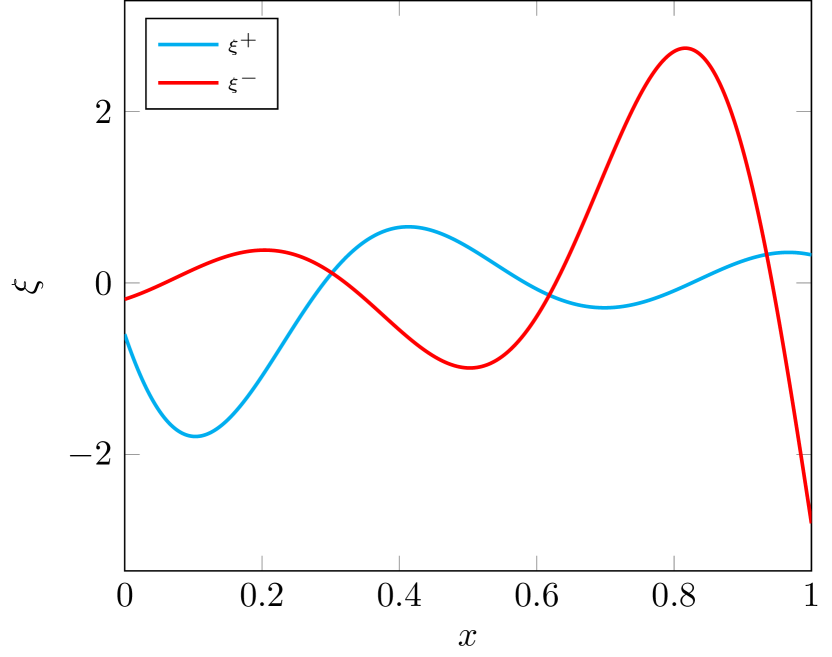

Therefore we provide only the quantity and for each node and of course for the whole network. The first example under consideration is a single transmission line between two nodes, one of which supplies voltage, while the other draws current.

The parameters of this network are given in 1(a) and the parameters of the periodic solution in 1(b).

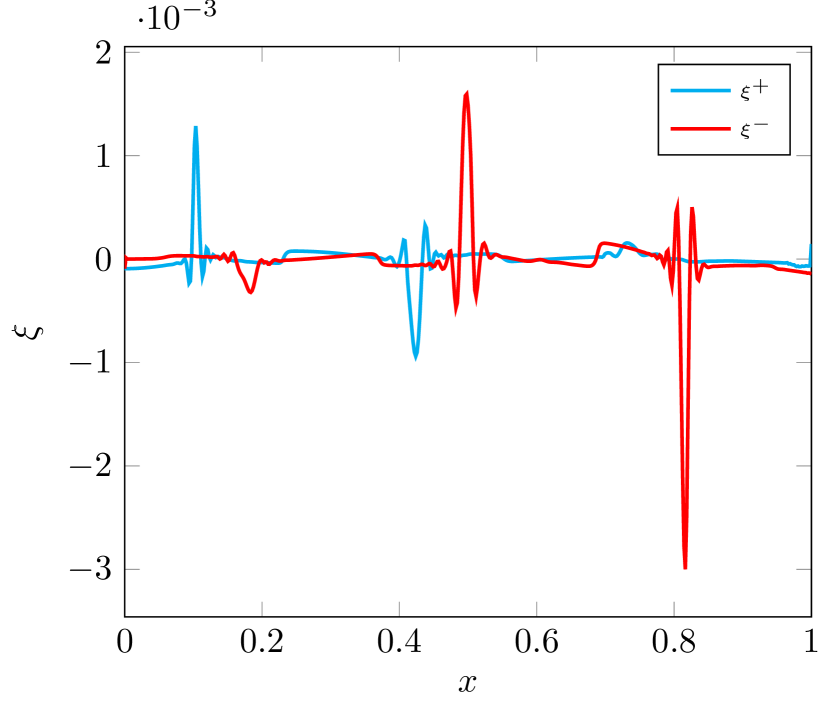

We integrate this problem from to with space discretization . As CFL number we choose . The numerical solution at can be found in 1(a). To compute the error we first provide the analytical solution expressed in . The analytical solution on every line is given by

where are taken from equation (7) (with ). As voltages at the ends of the line we take the solution to the linear system (14). With these we compute the analytical expressions for as

on every line. For an analytical solution and a numerical solution the maximal error of the numerical solution on a network over a time is then given by

| (24) |

where is again the set of edges and is the number of spatial steps on edge and is the total number of time steps. Here, is just the analytical solution evaluated at cell centers.

The time-dependent error over the whole line at time is shown in 1(b) for illustrating its usual appearance. The spikes in the error chart come from the minmod-scheme and lie exactly at the extrema of the solution. We remark that the boundary conditions are not introduce no further error.

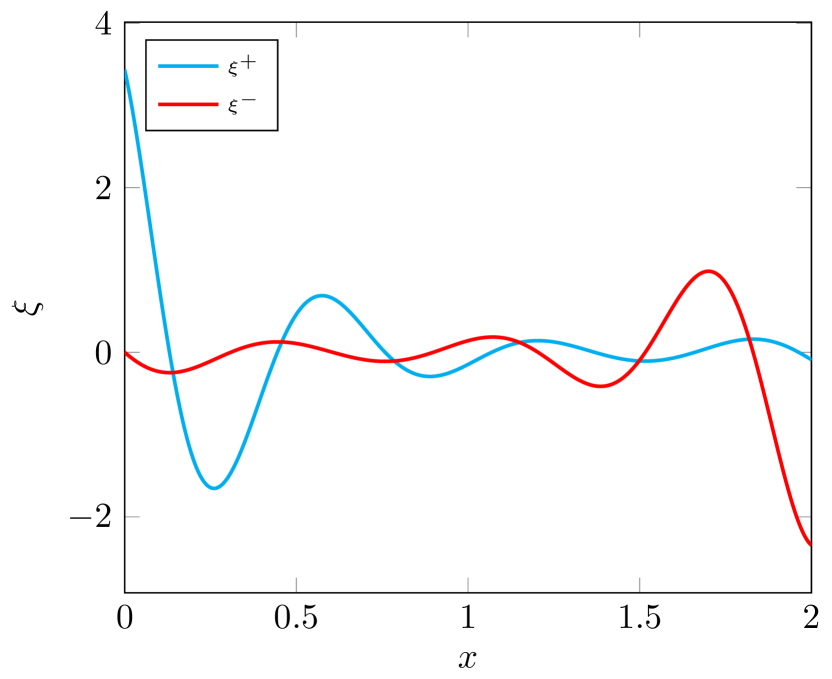

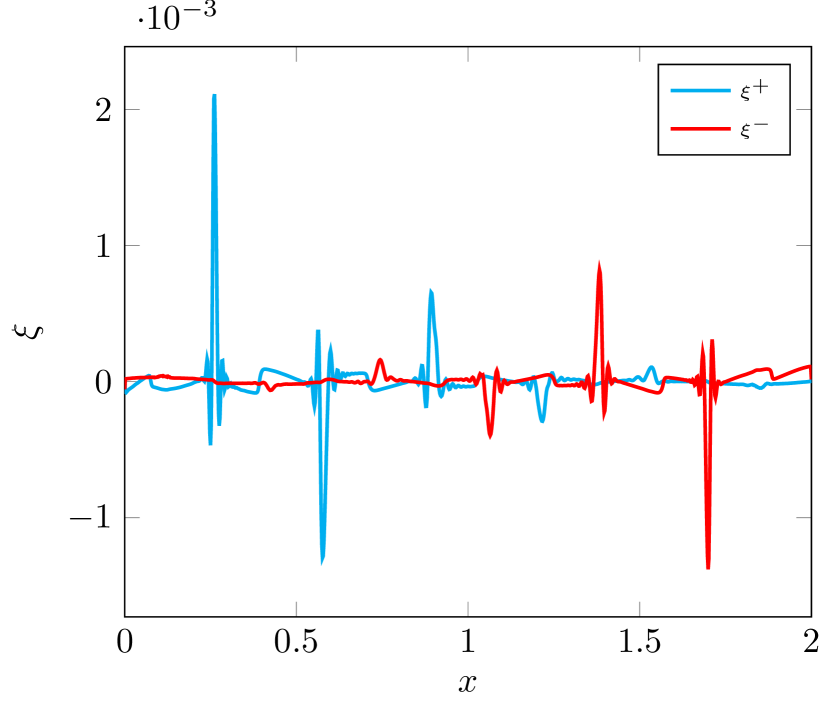

A second example is given by the network shown in Figure 2, where the node in the middle is a current supplying node where all transmission lines start. The line parameters and coupling conditions are given in table 2(b). The network is also integrated with a spatial stepsize of and again a CFL number of . For this network we also examine the order of convergence. Therefore, we solve the problem with stepsizes for and compute the corresponding maximal errors (see (24)) as well as the th estimate of the convergence order by

In Table 3 we see that the order of convergence approaches with the pure Lax-Wendroff scheme and stays below for the minmod-scheme as can be expected due to the order reduction at extrema.

| line | |||

|---|---|---|---|

| 2.0 | 3.0 | 1.0 | |

| 6.0 | 6.0 | 9.0 | |

| 2.0 | 1.0 | 2.0 | |

| 1.0 | 1.0 | 1.0 | |

| 2.0 | 2.0 | 2.0 |

| node | type | coupling condition |

|---|---|---|

| N1 | current | 10.0+3.0j |

| N2 | voltage | 4.0+4.0j |

| N3 | voltage | 2.0+5.0j |

| N4 | voltage | 3.0+6.0j |

| Lax Wendroff | Minmod | |

|---|---|---|

Plots of the line solutions and errors are similar to those of the single line and can be found in 3(a) and 3(b). Different parameters do not change the pictures much, which is why we do not show further images.

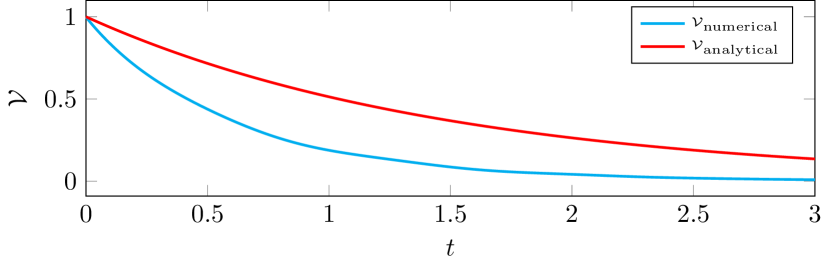

Lastly we compare the numerical (18) and analytical Lyapunov functions . The analytical Lyapunov function is given by

For the comparison we use the same network and the same initial data, but choose and for load and generator nodes respectively. With the numerical scheme we compute a solution and evaluate its Lyapunov function. The analytical Lyapunov function in this case is given by .

In Figure 4 we observe the estimate and the actually computed Lyapunov function.

Lastly we want to illustrate the severe restriction, the CFL number places on utilizing an explicit scheme for realistic power networks. Therefore we take some sample line parameters from [Bra04, Table 3 on page 26], namely parameters for an aerial transmission line for a voltage of :

| (25) | ||||

and compute the wave speed given in (4) from them,

which is nearly the speed of light. The wave speed for a buried cable still fulfills . Therefore for a rather coarse spatial step size of we get a restriction on the time step of

so that time steps per second have to be taken. For any realistic power network, computing so many time steps is at least difficult to implement and probably either too slow or too expensive to be practical. On the other hand, the mean lifetime of the exponential decay of the Lyapunov function computed from (25) is about and this is a worst-case estimate as illustrated by 4. Therefore for all practical purposes using the powerflow equations as is done in energy system simulation is a valid choice.

6 Summary and future work

We have shown that the powerflow equations used in engineering applications can be thought of as special solutions to the Telegrapher’s equations on the transmission lines between the nodes of the power network. We also provided a second-order numerical scheme to compute these PDE solutions. The scheme — with possible exclusion of the coupling points— is furthermore Lyapunov stable, which mimics the analytical solution. The Lyapunov stability including the coupling conditions will be investigated in future research using ideas presented in [GKS72].

Our numerical methods are extendable to higher order as there are splitting schemes at least up to order 666see https://www.asc.tuwien.ac.at/~winfried/splitting/index.php and there are entropy-stable ENO schemes of arbitrary order [FMT12] so that the Telegrapher’s equation could be solved with much higher accuracy. However, comparing the computational costs, actually computing PDE solutions for realistic physical parameters can be only done for small instances and with high implementation effort.

Acknowledgments

The authors gratefully thank the BMBF project ENets (05M18VMA) and the DFG project GO1920/10-1 for the financial support.

References

- [And15] G. Andersson “Lecture Notes on Power System Analysis, Power Flow Analysis, Fault Analysis, Power System Dynamics and Stability” ETH Zürich, 2015

- [BC16] G. Bastin and J.M. Coron “Stability and Boundary Stabilization of 1-D Hyperbolic Systems”, Progress in Nonlinear Differential Equations and Their Applications Springer International Publishing, 2016 DOI: 10.1007/978-3-319-32062-5

- [Bez+17] Jeff Bezanson, Alan Edelman, Stefan Karpinski and Viral B Shah “Julia: A fresh approach to numerical computing” In SIAM review 59.1 SIAM, 2017, pp. 65–98 URL: https://doi.org/10.1137/141000671

- [BHH16] Mapundi K. Banda, Axel-Stefan Häck and Michael Herty “Numerical Discretization of Coupling Conditions by High-Order Schemes” In Journal of Scientific Computing 69.1 Springer ScienceBusiness Media LLC, 2016, pp. 122–145 DOI: 10.1007/s10915-016-0185-x

- [Bie15] D. Bienstock “Electrical Transmission System Cascades and Vulnerability” Philadelphia, PA: Society for IndustrialApplied Mathematics, 2015 DOI: 10.1137/1.9781611974164

- [BK14] Raul Borsche and Jochen Kall “ADER schemes and high order coupling on networks of hyperbolic conservation laws” In Journal of Computational Physics 273 Elsevier BV, 2014, pp. 658–670 DOI: 10.1016/j.jcp.2014.05.042

- [BMZ15] Antonio Baeza, Pep Mulet and David Zorío “High Order Boundary Extrapolation Technique for Finite Difference Methods on Complex Domains with Cartesian Meshes” In Journal of Scientific Computing 66, 2015 DOI: 10.1007/s10915-015-0043-2

- [Bra04] Heinrich Brakelmann “Netzverstärkungs-Trassen zur Übertragung von Windenergie: Freileitung oder Kabel?” Bundesverband Windenergie e.V., 2004

- [EK17] H. Egger and T. Kugler “Damped wave systems on networks: exponential stability and uniform approximations” In Numerische Mathematik 138.4 Springer ScienceBusiness Media LLC, 2017, pp. 839–867 DOI: 10.1007/s00211-017-0924-4

- [EN01] Klaus-Jochen Engel and Rainer Nagel “One-Parameter Semigroups for Linear Evolution Equations” In Semigroup Forum 63, 2001, pp. 278–280 DOI: 10.1007/s002330010042

- [FMT12] Ulrik S. Fjordholm, Siddhartha. Mishra and Eitan. Tadmor “Arbitrarily High-order Accurate Entropy Stable Essentially Nonoscillatory Schemes for Systems of Conservation Laws” In SIAM Journal on Numerical Analysis 50.2, 2012, pp. 544–573 DOI: 10.1137/110836961

- [FR16] S. Frank and S. Rebennack “An introduction to optimal power flow: Theory, formulation, and examples” In IIE Transactions 48.12 Taylor & Francis, 2016, pp. 1172–1197

- [GH19] Stephan Gerster and Michael Herty “Discretized feedback control for systems of linearized hyperbolic balance laws” In Math. Control Relat. Fields 9.3, 2019, pp. 517–539 DOI: 10.3934/mcrf.2019024

- [GHM21] S. Göttlich, M. Herty and A. Milde “Mathematical Modeling, Simulation and Optimization for Power Engineering and Management” Springer International Publishing, 2021 DOI: 10.1007/978-3-030-62732-4

- [GHS16] S. Göttlich, M. Herty and P. Schillen “Electric transmission lines: control and numerical discretization” In Optimal Control Applications & Methods 37.5, 2016, pp. 980–995 DOI: 10.1002/oca.2219

- [GKL19] Simone Göttlich, Ralf Korn and Kerstin Lux “Optimal control of electricity input given an uncertain demand” In Math. Methods Oper. Res. 90.3, 2019, pp. 301–328 DOI: 10.1007/s00186-019-00678-6

- [GKS72] Bertil Gustafsson, Heinz-Otto Kreiss and Arne Sundström “Stability Theory of Difference Approximations for Mixed Initial Boundary Value Problems. II” In Mathematics of Computation 26.119 American Mathematical Society, 1972, pp. 649–686 URL: http://www.jstor.org/stable/2005093

- [GPR18] Martin Gugat, Vincent Perrollaz and Lionel Rosier “Boundary stabilization of quasilinear hyperbolic systems of balance laws: exponential decay for small source terms” In Journal of Evolution Equations 18.3 Springer ScienceBusiness Media LLC, 2018, pp. 1471–1500 DOI: 10.1007/s00028-018-0449-z

- [GPT19] S. Göttlich, A. Potschka and C. Teuber “A partial outer convexification approach to control transmission lines” In Comput. Optim. Appl. 72.2, 2019, pp. 431–456 DOI: 10.1007/s10589-018-0047-6

- [GS17] Simone Goettlich and Peter Schillen “Numerical Discretization of Boundary Control Problems for Systems of Balance Laws: Feedback Stabilization” In European Journal of Control 35, 2017 DOI: 10.1016/j.ejcon.2017.02.002

- [GT18] S. Göttlich and C. Teuber “Space mapping techniques for the optimal inflow control of transmission lines” In Optim. Methods Softw. 33.1, 2018, pp. 120–139 DOI: 10.1080/10556788.2016.1278542

- [Gug14] Martin Gugat “Boundary feedback stabilization of the telegraph equation: decay rates for vanishing damping term” In Systems Control Lett. 66, 2014, pp. 72–84 DOI: 10.1016/j.sysconle.2014.01.007

- [Jer+20] M. Jereminov et al. “Evaluating Feasibility Within Power Flow” In IEEE Transactions on Smart Grid 11.4, 2020, pp. 3522–3534 DOI: 10.1109/TSG.2020.2966930

- [Jia05] Y.-L. Jiang “Mathematical modelling on RLCG transmission lines” In Nonlinear Anal. Model. Control 10.2, 2005, pp. 137–149

- [KMN03] Marjeta Kramar, Delio Mugnolo and Rainer Nagel “Semigroups for Initial-Boundary Value Problems” In Evolution Equations: Applications to Physics, Industry, Life Sciences and Economics Basel: Birkhäuser Basel, 2003, pp. 275–292

- [KP18] A. M. Kettner and M. Paolone “On the Properties of the Power Systems Nodal Admittance Matrix” In IEEE Transactions on Power Systems 33.1, 2018, pp. 1130–1131 DOI: 10.1109/TPWRS.2017.2719583

- [LeV02] R.J. LeVeque “Finite Volume Methods for Hyperbolic Problems”, Cambridge Texts in Applied Mathematics Cambridge University Press, 2002

- [MM01] Antonio Maffucci and Giovanni Miano “Transmission lines and lumped circuits”, 2001 DOI: 10.1016/B978-0-12-189710-9.X5000-1

- [Rud87] W. Rudin “Real and Complex Analysis”, Mathematics series McGraw-Hill, 1987

- [Tad87] E. Tadmor “The numerical viscosity of entropy stable schemes for systems of conservation laws” In Mathematics of Computation 49.179, 1987, pp. 91–103 DOI: 10.2307/2008251