79 \affiliation\institutionTechnical University of Munich \affiliation\institutionTechnical University of Munich \affiliation\institutionTechnical University of Munich \affiliation\institutionTechnical University of Munich \affiliation\institutionTechnical University of Munich

Equilibrium Learning in Combinatorial Auctions:

Computing Approximate Bayesian Nash Equilibria via Pseudogradient Dynamics

Abstract.

Applications of combinatorial auctions (CA) as market mechanisms are prevalent in practice, yet their Bayesian Nash equilibria (BNE) remain poorly understood. Analytical solutions are known only for a few cases where the problem can be reformulated as a tractable partial differential equation (PDE). In the general case, finding BNE is known to be computationally hard. Previous work on numerical computation of BNE in auctions has relied either on solving such PDEs explicitly, calculating pointwise best-responses in strategy space, or iteratively solving restricted subgames. In this study, we present a generic yet scalable alternative multi-agent equilibrium learning method that represents strategies as neural networks and applies policy iteration based on gradient dynamics in self-play. Most auctions are ex-post nondifferentiable, so gradients may be unavailable or misleading, and we rely on suitable pseudogradient estimates instead. Although it is well-known that gradient dynamics cannot guarantee convergence to NE in general, we observe fast and robust convergence to approximate BNE in a wide variety of auctions and present a sufficient condition for convergence.

Key words and phrases:

Bayesian Games, Equilibrium Learning, Combinatorial Auctions1. Introduction

Auctions are widely used in advertising, procurement, or for spectrum sales (Bichler and Goeree, 2017; Milgrom, 2017; Ashlagi et al., 2011). Auction markets inherently involve incomplete information about competitors and strategic behavior of market participants. Understanding decision making in such markets has long been an important line of research in game theory. Auctions are typically modeled as Bayesian games and one is particularly interested in the equilibria of such games.

It is well-known that equilibrium computation is hard: Finding Nash equilibria is known to be PPAD-complete even for normal-form games, which assume complete information and finite action spaces, and where a Nash equilibrium is guaranteed to exist (Daskalakis et al., 2009). In auction games modeled as Bayesian games with continuous type and action spaces, agents’ values are drawn from some continuous prior value distribution and their strategies are described as continuous bid functions on these valuations. For markets of a single item, the landmark results by Vickrey (1961) have enabled a deep understanding of common auction formats. For multi-item auctions and more specifically combinatorial auctions, in which players bid on bundles of multiple items simultaneously, there has been little progress. While the complexity of computing Bayes-Nash equilibria (BNE) is not well understood, Cai and Papadimitriou (2014) show that BNE computation for a specific combinatorial auction is already (at least) PP-hard. Furthermore, finding an -approximation to a BNE is still NP-hard. Explicit solutions exist for very few specific environments, but in general, we neither know whether a BNE exists nor do we have a solution theory. Combinatorial auctions have become a pivotal research problem in algorithmic game theory (Roughgarden, 2016) and they are widely used in the field (Bichler and Goeree, 2017; Cramton et al., 2004). Thus, understanding their equilibria is paramount, and access to scalable numerical methods for computing or approximating BNE can have a significant impact.

Equilibrium learning in games differs from most learning tasks in that it suffers from the nonstationarity problem: Each player’s objective depends on other agents’ actions. Prior literature on equilibrium learning primarily focuses on complete-information games. In contrast, we focus on Bayes-Nash equilibria in games with continuous action space and continuous prior type distributions. The literature on equilibrium computation for these games is in its infancy and largely relies on best-response computations.

In this paper, we propose Neural Pseudogradient Ascent (NPGA) as a equilibrium learning method that follows gradient dynamics. While learning based on gradient dynamics has been used in complete-information games, this is not the case for Bayesian auction games: First, the underlying problem is equivalent to an infinite-dimensional variational inequality, for which we do not know an exact solution method. Second, the ex-post payoff function of auction games is non-differentiable. Finally, multi-agent gradient dynamics are known to converge to Nash equilibria only in restricted classes of games, even under complete information.

NPGA relies on self-play with neural networks, uses evolutionary strategies to compute gradients, and can exploit GPU hardware acceleration to massively parallelize the computations. In contrast to some previous work on numerical BNE computation, NPGA does not require any setting-specific subprocedures or information beyond evaluating auction outcomes themselves, and it can thus be applied to arbitrary Bayesian games. We discuss a sufficient condition for convergence of NPGA to a unique Bayes-Nash equilibrium and provide extensive experimental results on single-item and combinatorial auctions, which pose a benchmark problem in algorithmic game theory. Interestingly, we observe convergence of NPGA to approximate BNE in a wide range of small- and medium-sized combinatorial auction environments and recover the analytical Bayes-Nash equilibrium whenever it is known.

The remainder of this paper is structured as follows: In Section 2, we formally introduce the model and the problem. Section 3 examines related work, both in the problem domain of combinatorial auctions and related to our methodology. Next, we introduce and discuss NPGA in Section 4, before applying it to a suite of previously studied combinatorial auctions in Section 5. Finally, we summarize our findings and outline future research directions.

2. Problem statement

Bayesian Games and Combinatorial Auctions.

A Bayesian game or incomplete information game is a quintuple . describes the set of agents participating in the game. is the set of possible action profiles, with being the set of actions available to agent . is the set of type profiles. defines a joint prior probability distribution over type profiles that is assumed to be common knowledge among all agents. For any dependent random variable , we denote its cumulative distribution function by and its probability density function by . For example, denotes the marginal distribution of ’s type. At the beginning of the game, nature draws a type profile and each agent is informed of their own type only, thus the type constitutes private information based on which each agent chooses their action . Each agent’s ex-post utility function is then determined by , i.e. the agent’s utility depends on all agents’ actions but only on their own type. Agents aim to maximize their individual utility or payoff . Throughout this paper, we denote by the index a profile of types, actions or strategies for all agents but agent .

In this paper, we consider sealed-bid combinatorial auctions (CA) on items. In such an auction, each agent, or bidder, is allocated a bundle of items (possibly ). Each agent’s types are given by a vector of private valuations over bundles, i.e. . Bidders then submit actions, called bids , according to some bid-language: In the general case, where bidders might be interested in any combination of items, bids are in , i.e. each player must submit bids. In practice this is prohibitive, and one commonly studies settings where valuations exhibit some structure that allows reducing the dimensionality of both the type and strategy spaces. The settings we study in Section 5 have type and action spaces or .

After observing their own type , bidders submit bids chosen according to some strategy or bid function that maps individual valuations to a probability distribution over possible actions.111Mixed strategies that randomize over actions would also be possible, but we restrict ourselves to pure or deterministic strategies that choose a specific action with certainty, as most work in auction theory focuses on pure-strategy Bayesian Nash equilibria. We denote by the resulting strategy space of bidder and by the space of possible joint strategies. Note that even for deterministic strategies, the spaces are infinite-dimensional unless are finite. The auctioneer collects these bids, applies some auction mechanism that determines (a) an allocation ; each bidder receives a (possibly empty) bundle , s.t. the union of these bundles is disjoint, , i.e. each item is allocated to at most one bidder, and (b) payments that the agents have to pay to the auctioneer. For brevity, we will restrict ourselves to bidders with quasi-linear utility functions given by ,

| (1) |

i.e. the utility of each player is given by how much she values the goods that she is allocated minus the price she has to pay for them.222Quasi-linear utilities correspond to risk-neutral bidders, but our method is also applicable to bidders with risk-averse utility functions, e.g. . Throughout this paper, we will differentiate between the ex-ante state of the game, where players know only the priors , the ex-interim state, where players additionally know their own valuation , and the ex-post state, where all actions have been played and can be observed.

Equilibria in Bayesian games.

In non-cooperative game theory, Nash equilibria (NE) are the central equilibrium solution concept. A set of bids is a pure-strategy NE of the complete-information game if for all and all . In a NE no agent has an incentive to deviate unilaterally, given the equilibrium strategy of all other agents. Bayesian-Nash equilibria (BNE) extend this notion to incomplete-information games, calculating the expected utility over the conditional distribution of opponent valuations . For a valuation , action and fixed opponent strategies , we denote the ex-interim utility of bidder by

| (2) |

We also denote the ex-interim utility loss of action incurred by not playing the best response action, given and , by

| (3) |

Note that can generally not be observed in online-settings because it requires knowledge of a best-response.

An ex-interim -Bayes Nash Equilibrium (-BNE) is a strategy profile such that no agent can improve her own ex-interim expected utility by more than by deviating from the common strategy profile. Thus, in an -BNE, we have:

| (4) |

A -BNE is simply called BNE. Thus, in a BNE, every bidder’s strategy maximizes her expected ex-interim utility given opponent strategies everywhere on her type space . While BNE are often defined at the ex-interim stage of the game, we also consider ex-ante Bayesian equilibria as strategy profiles that concurrently maximize each player’s ex-ante expected utility . We analogously define and the ex-ante utility losses of a strategy profile by

| (5) | ||||

| (6) |

and

| (7) |

Then, an ex-ante BNE can be characterized by the equations for all Clearly, every ex-interim BNE also constitutes an ex-ante equilibrium. The reverse holds almost surely, i.e. any ex-ante equilibrium fulfills Equation 4, except possibly on a nullset , i.e. with . To see this, one may consider the equation and the fact that by definition. In this paper, we concern ourselves with finding ex-ante equilibria of auction games.

3. Related work

Gradient dynamics in games have been studied in evolutionary game theory and multiagent learning. While earlier work considered mixed strategies over normal-form games (Zinkevich, 2003; Bowling and

Veloso, 2002; Bowling, 2005; Busoniu

et al., 2008), more recently, motivated by the emergence of GANs, there has been a focus on (complete-information) games with continuous action spaces and smooth utility functions (Mertikopoulos and

Zhou, 2019; Letcher et al., 2019; Balduzzi et al., 2018; Schaefer and

Anandkumar, 2019). A common result for many settings and algorithms is that gradient-based learning rules do not necessarily converge to Nash equilibria and may exhibit cycling behavior, but often achieve no-regret properties and thus converge to weaker Coarse Correlated equilibria (CCE). An analogous result exists for finite-type Bayesian games, where no-regret learners are guaranteed to converge to a Bayesian CCE (Hartline

et al., 2015). In the present paper, we study equilibrium learning via gradient dynamics in continuous-type Bayesian games, specifically auctions, where they have not been investigated previously to our knowledge.

Equilibrium computation in auctions. Earlier approaches to find equilibria in auctions were usually setting specific and relied on reformulating Equation 4 as a differential equation (where possible), then solving this equation analytically or numerically (Vickrey, 1961; Krishna, 2009; Ausubel and Baranov, 2019). Armantier et al. (2008) introduced a BNE-computation method that is based on expressing the Bayesian game as the limit of a sequence complete-information games. They show that the sequence of Nash equilibria in the restricted games converges to a BNE of the original game. While this result holds for any Bayesian game, setting-specific information is required to generate and solve the restricted games. Rabinovich et al. (2013) study best-response dynamics on mixed strategies in auctions with finite action spaces. Most recently, Bosshard et al. (2017, 2020) proposed a method to find BNE in combinatorial auctions that relies on smoothed best-response dynamics and is applicable to any Bayesian game. The method explicitly computes point-wise best-responses in a fine-grained linearization of the strategy space via sophisticated Monte-Carlo integration. Our method, NPGA does likewise not require setting-specific information while also avoiding costly explicit best-response computations.

Some recent work has explored other topics at the intersection of deep learning and game theory. Schuurmans and Zinkevich (2016) reformulate supervised NN training into finding NE in a corresponding game. Dütting et al. (2017) use deep learning to design revenue-optimal and truthful auction mechanisms from the auctioneer’s perspective. In contrast, we explore how to bid optimally from the perspective of an auction participant.

4. Pseudogradient dynamics in auction games

Next, we present our method for equilibrium computation in auctions, which we call Neural Pseudogradient Ascent (NPGA). On a high level, we propose following the gradient dynamics of the game via simultaneous gradient ascent of all bidders. As we will see, however, computing the gradients themselves is not straightforward in the auction setting and we will need some modifications to established gradient dynamics methods such as Zinkevich (2003); Silver et al. (2014). For now, assume that players observe a gradient-oracle with respect to the current strategy profile in each iteration. Then the rule proposes that players perform a projected gradient update:

| (8) |

where is the projection onto the set of feasible strategies for agent . Several things must be noted about Equation 8: First, we consider the gradient dynamics of the ex-ante utility , rather than ex-interim or ex-post utilities. The goal of an individual update step is thus to marginally improve the expected utility of player across all possible joint valuations . This perspective ultimately considers low-probability events less important than high-probability events, which is in contrast to some other methods, which explicitly aim to optimize all ex-interim states (Bosshard et al., 2017). Second, to compute the gradient oracle in self-play, we rely on access to other players strategies, but evaluating each player’s policy relies only on their own valuation. We thus follow the centralized-training, decentralized-execution framework common in multi-agent learning. Third, are functions in an infinite-dimensional function space, so the gradient is itself a functional derivative. In our ex-ante perspective, we thus consider this to be the Gateaux derivative over the Hilbert space , equipped with the inner product (which, in turn, defines the projection in Equation 8 as ).

Policy networks.

To implement this derivative in practice, we represent each bidder’s strategy by a policy network specified by a neural network architecture and a corresponding parameter vector . Importantly, given a suitable network architecture, one can ensure that all always yield feasible bids, thus making the projection in the update step obsolete. In the empirical part of this study, we restrict ourselves to fully-connected feed-forward neural networks with ReLU activations in the output layer, which ensure nonnegative bids—the only feasibility constraint in the auctions we study. In any case, is finite and we thus transform the problem of choosing an infinite-dimensional strategy into choosing a finite-dimensional parameter vector .

Policy pseudogradients.

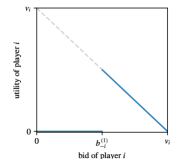

The deterministic policy gradient theorem (Silver et al., 2014) gives an established, canonical way to compute the payoff gradient with respect to the parameters : . However, the regularity conditions required by the theorem are commonly violated in combinatorial auctions. In particular, due to the discrete nature of the allocations , the ex-post utilities are usually discontinuous—and thus not (sub)differentiable in . While this nondifferentiability does not extend to , it nevertheless renders the policy gradient formula above inapplicable: Although the set of discontinuities is a -nullset in practice, its true gradient provides systematically misleading signals, even on the differentiable intervals of : Consider a first-price sealed-bid auction in which winning bidders pay their bid amount . The utility graph is separated into two sections (see Figure 1): (a) Bidding lower than the highest opposing bid leads to zero payoff and thus no learning feedback, , and (b) winning with a the highest bid must yields feedback to decrease the bid, . Back-propagation will thus lead to a steady decrease of bids, until all players bid constant zero at any valuation.

To alleviate this, we instead estimate the policy gradient using a finite difference approach based on evolutionary strategies (ES) Salimans et al. (2017). To calculate , we perturb the parameter vector times, , using zero-mean Gaussian noise for , where are hyperparameters. We then calculate each perturbation’s fitness, , via Monte-Carlo integration, and estimate the gradients as the fitness-weighted perturbation noise . Salimans et al. (2017) motivated their application of this ES gradient estimate to reinforcement learning because it’s applicable to parallelization across large-scale CPU-clusters, but here we instead exploit its property that it gives an asymptotically unbiased estimator of even when itself is not well-defined. To summarize, NPGA “implements” Equation (8) via ES-pseudogradients and a neural network parametrization of strategy functions which renders the projection step unnecessary:

| (9) |

Vectorizing auction evaluations.

The only information about the game needed in the computation of this learning rule is the evaluation of for a given strategy profile. Given a vectorized implementation of the joint ex-post utility , estimating via Monte-Carlo integration over is suitable to parallel execution on hardware accelerators such as GPUs. To this end, we built custom vectorized implementations of many common auction mechanisms using the PyTorch framework (Paszke et al., 2017), enabling Monte-Carlo estimation multiple orders of magnitude faster compared to previous numerical work on auctions. For moderately sized auction games commonly studied in the literature, allocations can be computed in a vectorized fashion via full enumeration of feasible allocations.333We stress that, with current hardware, this approach remains intractable for larger auctions that are applied in the real world, e.g. spectrum auctions. Common payment rules either have inherently vectorizable closed-form formulation (e.g. first-price auctions) or can be reformulated as the solution of a constrained quadratic program (e.g. the Vickrey-Clarke-Groves (VCG) mechanism or core-selecting pricing rules Day and Cramton (2012)). To solve a large batch of the latter in parallel, we leverage a custom vectorized implementation of interior-point methods. (A similar approach has previously been used by Amos and Kolter (2019).)

A convergence criterion.

As discussed in Section 3, gradient dynamics do not converge to Nash equilibria in general. For differentiable, finite-dimensional, complete-information games (auctions are neither!), Mertikopoulos and Zhou (2019) show that strict monotonicity of the payoff gradients is a sufficient condition for almost-sure convergence of gradient dynamics to a unique Nash equilibrium as it leads to strict concavity of the game. Ui (2016) shows an analogous result for ex-post differentiable Bayesian games, in which payoff-monotonicity guarantees the existence of a unique BNE. However, the result likewise does not directly apply to auctions due to their ex-post nondifferentiability. Instead, we give a slightly less restrictive criterion based on ex-interim payoff monotonicity that ensures convergence of gradient dynamics and whose formulation is compatible with auction games.

Definition 0 (Strict Ex-interim Payoff Monotonicity).

Let be a Bayesian game, such that the individual ex-interim utilities are continuously differentiable in with gradients bounded by a constant via . is called strictly (ex-interim) payoff-monotone, if for all , , and almost everywhere the following holds:

| (10) |

While analytical verification of this criterion is elusive, except in special settings, it can (approximately) be checked numerically by sampling pairs of action profiles for all players and using finite-difference gradient-estimators. Doing so, we observe consistency with the criterion in all settings studied in Section 5. In the following, we provide a convergence result for NPGA under ex-interim monotonicity. For our convergence analysis, we will rely on certain properties of “appropriate” neural network architectures:

Definition 0 (Regular Convex Policy Network).

A Regular Convex Policy Network is a neural network with and the following properties:

-

(1)

is a convex neural network in its parameters: For any convex function , the map is convex.

-

(2)

universally approximates : There exists a , s.t. for all there is a parameter vector with .

-

(3)

Regularity: is Lipschitz-continuous in its parameters in the sense that there’s some such that for all we have .

Neural networks that are employed in practice (and in our empirical analysis) generally do not comply with Definition 4, but such networks have been shown to exist, see e.g. Bach (2017), who studies wide single-hidden-layer networks with ReLU activations, in which only the output-layer weights are being trained. We’ll state our main proposition before discussing this difference further:

Proposition 0.

Let be a Bayesian game such that the ex-post utilities exist, and such that the ex-interim payoff-gradients exist and fulfill strict ex-interim payoff monotonicity. Then, with an NN architecture as in Definition 4 and appropriate update step sizes, NPGA converges to an ex-ante -BNE of , where .

While existence and uniqueness of BNE in infinite-dimensional games are unknown in the general case, Proposition 4 guarantees efficient computability in a wide range of settings, some of which we explore in the next section. Still, it’s important to note that there may be auctions for which payoff-monotonicity does not hold.

A proof outline Proposition 4 is given at the end of this article in Appendix A, for additional technical derivations, see the supplementary material. As demonstrated in the proof, the use of Regular Convex Policy Networks transforms the training process into a problem of finding a Nash Equilibrium in a concave, finite-dimensional, complete-information game. Crucially, concavity of this game ensures existence of, and convergence to, a unique global equilibrium. Just as neural networks are known to find “good” solutions to nonconvex optimization problems in practice despite a lack of theoretical guarantees, we will see below that we observe convergence to BNE when using standard neural network architectures that don’t meet Definition 4: As such, we see Regular Convex Policy Networks as a helpful tool for theoretical analysis, but their implementation is generally neither practical nor desirable while common architectures achieve similar results.

5. Empirical Results

We evaluate NPGA on three suites of auction theoretic settings: First, in Section 5.1 we validate our method on a suite of the most commonly studied auctions, i.e. single-item auctions with symmetric priors, before considering two suites of combinatorial auctions, the LLG (Section 5.2.1) and LLLLGG (Section 5.2.2) environments. In total, we study 21 different auction settings with different numbers of players, pricing rules, risk-profiles, and prior distributions of the valuations. In 18 of these settings, the (unique) BNE is known analytically, in three settings, no BNE is known.

Evaluation Metrics

To evaluate the quality of strategy-profiles learned by NPGA, we will provide four metrics, whenever available: When we have access to the analytical solution BNE , we can simply check whether . To do so, we report each agent’s

-

(1)

utility loss that results from unilaterally deviating from the BNE strategy profile by playing the learned strategy instead: , compare Equation 7,

-

(2)

and the distance in strategy space.

Both of these can be estimated via Monte-Carlo integration over the valuations , i.e. given a batch of size of valuations , we approximate by the sample mean of and by the RMSE of and in action-space.

However, to make NPGA applicable in practice, we are also interested in judging the quality of when no BNE is known. To do so, we also estimate the potential gains of deviating from the current strategy profile as well as an estimator to the “true” epsilon of (smallest s.t. forms an ex-interim -BNE). In the absence of analytical solutions, one may periodically calculate these estimators and use them as a termination criterion once the desired precision is reached. As we will see, these additional metrics are expensive: To calculate the estimators and we introduce a grid of equidistant points per bidder, covering the action spaces . Now, given a valuation and a bid , we approximate the ex-interim utility loss of at via

| (11) |

Note that the batch only runs across opponent valuations . To evaluate at a single , we thus need auction evaluations. We can then estimate the

-

(3)

worst-case ex-interim loss: ,

-

(4)

and the ex-ante loss: .

Estimations of can be shared for both computations, nevertheless we need auction evaluations to calculate these metrics (in contrast, an iteration of NPGA requires only evaluations, with ). As the metrics are expensive to compute with dense grids, we use smaller batch sizes and than in evaluating , and calculate these metrics only once every 100 iterations of the algorithm.

Hyperparameters

We use common hyperparameters across almost all settings (except where noted otherwise): Fully connected neural networks with two hidden layers of 10 nodes each with SeLU (Klambauer et al., 2017) activations. ES-parameters , . We use Adam optimizer steps with default hyperparameters as suggested in Kingma and Ba (2017). To avoid degenerate initializations of (e.g. where one or more bidders bid constant zero due to dead ReLUs in the output layer), we perform supervised pre-training to the truthful strategy . All experiments were performed on a single Nvidia GeForce 2080Ti and batch sizes in Monte-Carlo sampling were chosen to maximize GPU-RAM utilization: A learning batch size of ; primary evaluation batch size (for ) of ; and secondary evaluation batch size and grid size (for ). Each experiment is repeated ten times over 5,000 iterations each.

5.1. Single-Item Auctions

| valuations | n | time sec/it | ||||

|---|---|---|---|---|---|---|

| Uniform risk-neutral | 2 | 0.0000 | 0.0072 | 0.0011 | 0.0059 | 0.31 |

| 3 | 0.0001 | 0.0104 | 0.0007 | 0.0051 | 0.40 | |

| 5 | 0.0001 | 0.0194 | 0.0005 | 0.0053 | 0.46 | |

| 10 | 0.0001 | 0.0303 | 0.0003 | 0.0047 | 0.73 | |

| Uniform risk-averse | 2 | 0.0003 | 0.0057 | 0.0012 | 0.0065 | 0.46 |

| 3 | 0.0001 | 0.0069 | 0.0008 | 0.0048 | 0.52 | |

| 5 | 0.0001 | 0.0161 | 0.0006 | 0.0066 | 0.63 | |

| 10 | 0.0002 | 0.0383 | 0.0005 | 0.0085 | 0.93 | |

| Gaussian risk-neutral | 2 | 0.0079 | 0.3684 | 0.0443 | 0.4394 | 0.31 |

| 3 | 0.0103 | 0.4478 | 0.0225 | 0.9723 | 0.39 | |

| 5 | 0.0172 | 0.8819 | 0.0176 | 1.7324 | 0.45 | |

| 10 | 0.0169 | 1.8801 | 0.0118 | 2.1660 | 0.68 |

First-price sealed-bid (FPSB) auctions on a single item, in which the highest-bidding player wins the item and pays her own bid as price, are the best-known auctions and for many configurations their BNE are known analytically Krishna (2009). We apply NPGA to 12 such FPSB settings with 2, 3, 5 and 10 bidders with uniform- and normal-distributed valuations and risk-neutral and risk-averse utility functions. The results are given in Table 1.

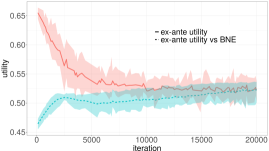

In all settings, we observe convergence of NPGA to a close approximation of the analytical BNE in terms of ex-ante payoff, both when evaluated in self-play and against opponents playing the BNE. However, we also see that sometimes there’s no full norm-convergence in the strategy space: This indicates that NPGA learns ex-ante BNE as the algorithm is designed to do, but may bid suboptimally in “unimportant” regions of the valuation space, e.g. when there are many players and ’s valuation is low (see Gaussian-10p setting): Learning a highly-nuanced signal in these regions would require a larger sample-size. Similarly, the estimator tends to be pessimistic, as expected. Nevertheless, we see that the strategy-space distance is low in most settings, and even when it is not, the learned strategy becomes indistinguishable from the BNE in terms of ex-ante utility: Figure 2 shows the learning curve for the Gaussian-10p setting where the norm has not converged. Additionally, we observe that the exploitability-estimate , while not exactly equal to , is consistent in order of magnitude and may thus serve as a suitable proxy for convergence in the absence of known BNE.

For a complete treatment of the single-item setting, we also implemented Vickrey/Second Price auctions, where NPGA consistently found the BNE (all metrics ), as well as learning using the canonical policy gradient theorem instead of pseudogradients, which, as expected (see Section 4), consistently failed to learn the BNE and instead lead to all players bidding 0 everywhere.

5.2. Combinatorial Auctions

Local-global combinatorial auctions will serve as our main benchmark for BNE compuation. In such auctions, there are two groups of bidders, locals and globals: Globals are interested in larger bundles of items while their priors allow them to draw higher valuations, so local bidders need to coordinate to outbid the globals. We consider settings where locals have either independent or correlated uniform priors with (for each bundle ). The 3-player LLG setting (Section 5.2.1) is a standard setting in auction theory and one of the smallest CAs that requires strategic cooperation between bidders; the larger 6-player LLLLGG setting (Section 5.2.2) was proposed by (Bosshard et al., 2017) and, to our knowledge, is the most complex environment in which approximate BNE have been computed to date.

| priors | payment | bidder | time sec/it | ||||

|---|---|---|---|---|---|---|---|

| independent | n.-VCG | locals | 0.0001 | 0.0050 | 0.0002 | 0.0009 | 0.84 |

| global | 0.0000 | 0.0269 | 0.0000 | 0.0001 | |||

| n.-bid | locals | -0.0002 | 0.0073 | 0.0003 | 0.0013 | 0.79 | |

| global | 0.0000 | 0.0424 | 0.0000 | 0.0001 | |||

| n.-zero | locals | -0.0001 | 0.0078 | 0.0002 | 0.0019 | 0.79 | |

| global | 0.0000 | 0.0088 | 0.0000 | 0.0001 | |||

| FPSB | locals | – | – | 0.0009 | 0.0031 | 0.65 | |

| global | – | – | 0.0016 | 0.0064 | |||

| correlated | n.-VCG | locals | -0.0001 | 0.0042 | – | – | 0.80 |

| global | 0.0000 | 0.0305 | – | – | |||

| n.-bid | locals | 0.0003 | 0.0064 | – | – | 0.83 | |

| global | 0.0000 | 0.0498 | – | – | |||

| n.-zero | locals | 0.0001 | 0.0059 | – | – | 0.81 | |

| global | 0.0000 | 0.0072 | – | – |

5.2.1. The LLG setting

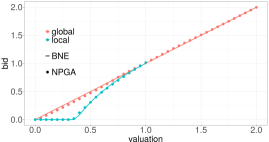

The LLG setting includes two local bidders and one global bidder that bid on items. Local bidders are each interested in the bundle , while the global bidder wants the package of both items. Each bidder submits a bid for their respective bundle. The setting has been extensively studied in the context of different core-selecting pricing rules as commonly used in real-world spectrum auctions (Day and Cramton, 2012; Goeree and Lien, 2016). Closed-form solutions of the unique, symmetric BNE under three such rules are known in the LLG setting for both independent and correlated priors: the nearest-VCG rule, the nearest-zero (or proxy) rule, and the nearest-bid rule. The interested reader is referred to Ausubel and Baranov (2019) for details. In these rules, it has been shown that the global bidder is bidding truthfully in the BNE. The local bidders’ BNE strategies differ in each payment rule and depending on the correlation between locals’ priors. We evaluate NPGA on the three core payment rules with independent and correlated priors (correlation coefficient of local bidders: ) as well as the first-price payment rule with independent priors, for which no exact BNE is known. Numerical results for all rules are presented in Table 2. We again observe that NPGA converges to the BNE in all six-settings where it is known. In fact, after low hundreds of iterations, we can no longer detect a difference in utility to the true BNE with available measurement precision, while still observing slight differences in strategy-space distance: Figure 3 depicts the strategy learned by NPGA after 5,000 iterations in comparison to the analytical BNE strategy for the nearest-zero payment rule, and shows an almost perfect fit. In the FPSB auction, no BNE is known, but values of (while the global (local) bidders achieve an ex-ante utility of ()) indicate that exploitability of is minuscule.

As noted above, estimating and is computationally expensive, and is not needed to run NPGA itself. The average total computation time over 5,000 iterations is below 70 minutes in any LLG setting.444The computation of estimated utility loss is not straightforward for correlated priors because it requires sampling from the conditional distributions which (1) may not be available in general and (2) adds additional computational complexity. While we do not report the estimated utility loss in these setting, the more relevant utility loss (playing against BNE) is so low that we assume convergence.

| payment | bidder | time sec/iter | ||

|---|---|---|---|---|

| first-price | locals | 0.0015 (0.0003) | 0.0109 (0.0025) | 0.97 (0.005) |

| globals | 0.0010 (0.0002) | 0.0077 (0.0016) | ||

| near.-VCG | locals | 0.0013 (0.0003) | 0.0052 (0.0012) | 275.22 (0.670) |

| globals | 0.0011 (0.0006) | 0.0098 (0.0059) |

5.2.2. The LLLLGG setting

In the LLLLGG setting, four local and two global bidders compete for six items, where each bidder is interested in two (partly overlapping) bundles (containing 2 (local) or 4 (global) items each), with actions being represented as . No analytical BNE are known in this setting (except for the trivial VCG pricing rule, where bidding truthfully constitutes a BNE). We apply NPGA to LLLLGG with first-price and nearest-vcg rules.

In LLLLGG, computing the clearing prices is nontrivial and computationally expensive and forms our computational bottleneck, particularly at large batch-sizes: Nearest-VCG prices require solving a linear- and a subsequent quadratic optimization problem for each auction (Day and Cramton, 2012). Because NPGA evaluates many thousand auctions in each iteration, we implemented a custom interior-point solver that can solve batches of quadratic optimization problems on the GPU. Nonetheless we make the following hyperparameter adjustments to reduce complexity in the nearest-VCG setting: ; ; and on two experiments of 1,000 iterations each.

For both pricing rules, NPGA learns strategy profiles with an estimated ex-ante utility loss for both local and global bidders. Global (local) bidders achieve stable average utilities of 0.238 (0.18) in first-price and 0.181 (0.201) in nearest-vcg, thus the estimated loss indicates that players can be exploited for less than 1% of their achieved utility. Figure 4 shows the NPGA learning-curve for both groups of bidders in the first-price setting. We see that both utility and the loss converge fast, the latter reaching a value of after just 700 iterations.

BNE-computation in the LLLLGG setting has previously been studied by Bosshard et al. (2017, 2020).Their method, based on point-wise best-response dynamics, has limited comparability to NPGA, as they differ both in goals and evaluation, but one may summarize that NPGA has somewhat lower precision, being an ex-ante method and due to memory-constraints, while being significantly faster: In Bosshard et al. (2017), Bosshard et al. report finding an estimated ex-interim -BNE for the LLLLGG first-price setting in CPU-core hours; NPGA finds an estimated ex-ante -BNE (ex-interim ) in 81 minutes on a single GPU (5,800 CUDA-core-hours).555In a recent follow-up paper Bosshard et al. (2020), Bosshard et al. further improve the sample-efficiency of Bosshard et al. (2017) using sophisticated Monte-Carlo estimation methods. Much of this optimization is equally applicable to NPGA and will be part of future work.

6. Conclusion and future work

This paper explores equilibrium learning in Bayesian games, one of the large unsolved problems in algorithmic game theory. Gradient dynamics are challenging in Bayesian auction games for several reasons: these games are not differentiable, and the continuous type- and action spaces make efficient representation difficult or expensive. We propose Neural Pseudogradient Ascent as a numerical method for equilibrium learning that relies on pseudogradients on parameter spaces of policy networks. We hope that our approach will make possible the study of gradient dynamics in game-theoretical and microeconomic settings where they have previously been considered inapplicable. In experiments, we validate NPGA on standard single-item and combinatorial auctions, which constitute a pivotal problem in algorithmic game theory with many practical applications. We find that NPGA converges to approximate BNE for central benchmark problems in this field, and we prove a sufficient criterion under which almost sure convergence to equilibria is guaranteed. In summary, the method can provide an effective numerical tool to compute approximate BNE not only for combinatorial auctions but also for other Bayesian games, without setting-specific customization, all while running on consumer hardware and leveraging GPU-parallelization for performance.

Appendix A Proof of Proposition 4

Proof.

We will approximate the infinite-dimensional Bayesian-game by a finite-dimensional (but continuous action), complete-information “proxy game”. Under strict monotonicity, the regularity conditions above, and with Regular Convex Policy Networks, we argue that NPGA almost surely finds an approximation of the unique NE in this proxy game. We then give a bound on the ex-ante loss in the original game for this proxy-NE, thus certifying an -BNE.

First, existence of the ex-interim gradients (Definition 4) implies that the ex-ante utilities are Gâteaux-differentiable in the Hilbert spaces with Gâteaux-gradients (Follows from 2.54, 2.55, 17.10 of Bauschke and Combettes (2011) and direct calculations.) With ex-interim payoff-monotonicity, we then have

| (12) | ||||

I.e. the ex-ante gradients are strictly monotone operators on . It follows that are strictly concave in (Bauschke and Combettes, 2011, Thm 17.10). With a neural network as in Definition 4, the functions are then also strictly concave in for any opponent strategies . We can then construct a finite-dimensional, complete-information Parameter Game , in which all players approximate their strategies in using policy networks and we interpret the parameters of the networks as the action of the new game: . As this game is finite-dimensional and concave, Mertikopoulos and Zhou (2019) establish that (1) it has a unique Nash equilibrium and (2) the dual averaging algorithm converges almost surely to given an unbiased and finite-variance oracle of the gradients . Next, we argue that induces an approximate BNE in the original Bayesian Game before analyzing how NPGA implements dual averaging in with noisy feedback, thus finding a good approximation of . Let thus be the Nash equilibrium of . Then for any player , is a best response (BR) to and is an ex-ante BR to in the Bayesian Game with restricted strategy space of functions expressible by the network. As we assumed universal approximation properties of , however, any BR in the unrestricted game must be close in function space to , and the ex-ante utility loss incurred by not playing instead of is bounded: In fact, with the Lipschitz-regularity conditions on the ex-interim gradients and universal approximability of , we observe the following for arbitrary : If and are BRs to in and , respectively, then

| (13) | ||||

where . In the NE, all are BRs, so we have .

Finally, we show that NPGA finds a good approximation of . As deliberated above, we choose the NN architecture in such a way that becomes unconstrained, i.e. any parameter is feasible, where is the dimension of the network for player . On an unconstrained action set , however, dual averaging (with Euclidean regularization) is equivalent to Online Gradient Ascent on Zinkevich (2003); Mertikopoulos and Zhou (2019). Therefore, NPGA implements Dual Averaging on using the gradient oracle .

To use the convergence result of Mertikopoulos and Zhou (2019) of NPGA to , it would remain to show that the Neural Pseudogradients are finite-variance and unbiased estimators of the true gradients . This is unfortunately violated for strictly positive ES-noise variance used in NPGA (but asymptotically true for ). However, for we can set and introduce yet another finite-dimensional game . Now, one can show (see supplement) that (1) is, again, concave, that (2) the ES-gradients are finite-variance, unbiased estimators of , and (3) that the loss in of any is bounded by that in via

| (14) |

Due to (1), again admits a unique NE (Mertikopoulos and Zhou, 2019, Thm 2.2), and with (2) and Definition 4, NPGA converges to almost surely for appropriate step sizes (Mertikopoulos and Zhou, 2019, Cor 4.8).

To summarize, we showed that NPGA finds a parameter profile that forms a NE of and which retains an-ex ante loss in of

| (15) |

Thus, setting where , NPGA converges almost surely to an ex-ante -BNE of . ∎

We’re grateful for funding by the Deutsche Forschungsgemeinschaft (DFG, German Research Foundation) - BI 1057/1-8. We thank Vitor Bosshard, Ben Lubin, Panayotis Mertikopoulos, Sven Seuken, Takashi Ui, and Felipe Maldonado for valuable feedback, and two former students in our group: Kevin Falkenstein, for a separate implementation of initial algorithms, and Anne Christopher, for developing the custom batched QP solver. All errors are ours.

References

- (1)

- Amos and Kolter (2019) Brandon Amos and J. Zico Kolter. 2019. OptNet: Differentiable Optimization as a Layer in Neural Networks. arXiv:1703.00443 [cs, math, stat] (Oct. 2019). arXiv:1703.00443 [cs, math, stat]

- Armantier et al. (2008) Olivier Armantier, Jean-Pierre Florens, and Jean-Francois Richard. 2008. Approximation of Nash Equilibria in Bayesian Games. Journal of Applied Econometrics 23, 7 (Nov. 2008), 965–981. https://doi.org/10.1002/jae.1040

- Ashlagi et al. (2011) Itai Ashlagi, Dov Monderer, and Moshe Tennenholtz. 2011. Simultaneous Ad Auctions. Mathematics of Operations Research 36, 1 (2011), 1–13.

- Ausubel and Baranov (2019) Lawrence M. Ausubel and Oleg Baranov. 2019. Core-Selecting Auctions with Incomplete Information. International Journal of Game Theory (July 2019). https://doi.org/10.1007/s00182-019-00691-3

- Bach (2017) Francis Bach. 2017. Breaking the Curse of Dimensionality with Convex Neural Networks. Journal of Machine Learning Research 18, 19 (2017), 1–53.

- Balduzzi et al. (2018) David Balduzzi, Sebastien Racaniere, James Martens, Jakob Foerster, Karl Tuyls, and Thore Graepel. 2018. The Mechanics of N-Player Differentiable Games. arXiv:1802.05642 [cs]; ICML (Feb. 2018). arXiv:1802.05642

- Bauschke and Combettes (2011) Heinz H. Bauschke and Patrick L. Combettes. 2011. Lower Semicontinuous Convex Functions. In Convex Analysis and Monotone Operator Theory in Hilbert Spaces, Heinz H. Bauschke and Patrick L. Combettes (Eds.). Springer, New York, NY, 129–141.

- Bichler and Goeree (2017) Martin Bichler and Jacob K Goeree. 2017. Handbook of Spectrum Auction Design. Cambridge University Press.

- Bosshard et al. (2017) Vitor Bosshard, Benedikt Bünz, Benjamin Lubin, and Sven Seuken. 2017. Computing Bayes-Nash Equilibria in Combinatorial Auctions with Continuous Value and Action Spaces. In Proceedings of the Twenty-Sixth International Joint Conference on Artificial Intelligence. 119–127.

- Bosshard et al. (2020) Vitor Bosshard, Benedikt Bünz, Benjamin Lubin, and Sven Seuken. 2020. Computing Bayes-Nash Equilibria in Combinatorial Auctions with Verification. Journal of Artificial Inelligence Research (2020). arXiv:1812.01955

- Bowling (2005) Michael Bowling. 2005. Convergence and No-Regret in Multiagent Learning. In Advances in Neural Information Processing Systems 17, L. K. Saul, Y. Weiss, and L. Bottou (Eds.). MIT Press, 209–216.

- Bowling and Veloso (2002) Michael Bowling and Manuela Veloso. 2002. Multiagent Learning Using a Variable Learning Rate. Artificial Intelligence 136, 2 (April 2002), 215–250. https://doi.org/10.1016/S0004-3702(02)00121-2

- Busoniu et al. (2008) Lucien Busoniu, Robert Babuska, and B. De Schutter. 2008. A Comprehensive Survey of Multiagent Reinforcement Learning. IEEE Transactions on Systems, Man, and Cybernetics, Part C (Applications and Reviews) 38, 2 (March 2008), 156–172. https://doi.org/10.1109/TSMCC.2007.913919

- Cai and Papadimitriou (2014) Yang Cai and Christos Papadimitriou. 2014. Simultaneous Bayesian Auctions and Computational Complexity. In Proceedings of the Fifteenth ACM Conference on Economics and Computation - EC ’14. ACM Press, Palo Alto, California, USA, 895–910.

- Cramton et al. (2004) Peter Cramton, Yoav Shoham, and Richard Steinberg. 2004. Combinatorial Auctions. Technical Report 04mit. University of Maryland, Department of Economics - Peter Cramton.

- Daskalakis et al. (2009) C. Daskalakis, P. Goldberg, and C. Papadimitriou. 2009. The Complexity of Computing a Nash Equilibrium. SIAM J. Comput. 39, 1 (Jan. 2009), 195–259. https://doi.org/10.1137/070699652

- Day and Cramton (2012) Robert W. Day and Peter Cramton. 2012. Quadratic Core-Selecting Payment Rules for Combinatorial Auctions. Operations Research 60, 3 (June 2012), 588–603.

- Dütting et al. (2017) Paul Dütting, Zhe Feng, Harikrishna Narasimhan, and David C. Parkes. 2017. Optimal Auctions through Deep Learning. arXiv:1706.03459 [cs] (June 2017). arXiv:1706.03459 [cs] http://arxiv.org/abs/1706.03459

- Goeree and Lien (2016) Jacob K. Goeree and Yuanchuan Lien. 2016. On the Impossibility of Core-Selecting Auctions. Theoretical Economics 11, 1 (2016), 41–52. https://doi.org/10.3982/TE1198

- Hartline et al. (2015) Jason Hartline, Vasilis Syrgkanis, and Eva Tardos. 2015. No-Regret Learning in Bayesian Games. In Advances in Neural Information Processing Systems 28, C. Cortes, N. D. Lawrence, D. D. Lee, M. Sugiyama, and R. Garnett (Eds.). Curran Associates, Inc., 3061–3069.

- Kingma and Ba (2017) Diederik P. Kingma and Jimmy Ba. 2017. Adam: A Method for Stochastic Optimization. arXiv:1412.6980 [cs] (Jan. 2017). arXiv:1412.6980 [cs] http://arxiv.org/abs/1412.6980

- Klambauer et al. (2017) Günter Klambauer, Thomas Unterthiner, Andreas Mayr, and Sepp Hochreiter. 2017. Self-Normalizing Neural Networks. arXiv:1706.02515 [cs, stat] (June 2017). arXiv:1706.02515 [cs, stat]

- Krishna (2009) Vijay Krishna. 2009. Auction Theory. Academic press.

- Letcher et al. (2019) Alistair Letcher, David Balduzzi, Sebastien Racaniere, James Martens, Jakob Foerster, Karl Tuyls, and Thore Graepel. 2019. Differentiable Game Mechanics. arXiv:1905.04926 [cs, stat] (May 2019). arXiv:1905.04926 [cs, stat]

- Mertikopoulos and Zhou (2019) Panayotis Mertikopoulos and Zhengyuan Zhou. 2019. Learning in Games with Continuous Action Sets and Unknown Payoff Functions. Mathematical Programming 173, 1 (Jan. 2019), 465–507.

- Milgrom (2017) Paul Milgrom. 2017. Discovering Prices: Auction Design in Markets with Complex Constraints. Columbia University Press.

- Paszke et al. (2017) Adam Paszke, Sam Gross, Soumith Chintala, Gregory Chanan, Edward Yang, Zachary DeVito, Zeming Lin, Alban Desmaison, Luca Antiga, and Adam Lerer. 2017. Automatic Differentiation in PyTorch. In NIPS-W.

- Rabinovich et al. (2013) Zinovi Rabinovich, Victor Naroditskiy, Enrico H. Gerding, and Nicholas R. Jennings. 2013. Computing Pure Bayesian-Nash Equilibria in Games with Finite Actions and Continuous Types. Artificial Intelligence 195 (Feb. 2013), 106–139. https://doi.org/10.1016/j.artint.2012.09.007

- Roughgarden (2016) Tim Roughgarden. 2016. Twenty Lectures on Algorithmic Game Theory — Algorithmics, Complexity, Computer Algebra and Computational Geometry.

- Salimans et al. (2017) Tim Salimans, Jonathan Ho, Xi Chen, Szymon Sidor, and Ilya Sutskever. 2017. Evolution Strategies as a Scalable Alternative to Reinforcement Learning. arXiv:1703.03864 [cs, stat] (March 2017). arXiv:1703.03864 [cs, stat]

- Schaefer and Anandkumar (2019) Florian Schaefer and Anima Anandkumar. 2019. Competitive Gradient Descent. Advances in Neural Information Processing Systems 32 (2019), 7625–7635.

- Schuurmans and Zinkevich (2016) Dale Schuurmans and Martin A Zinkevich. 2016. Deep Learning Games. In Advances in Neural Information Processing Systems 29, D. D. Lee, M. Sugiyama, U. V. Luxburg, I. Guyon, and R. Garnett (Eds.). Curran Associates, Inc., 1678–1686. http://papers.nips.cc/paper/6315-deep-learning-games.pdf

- Silver et al. (2014) David Silver, Guy Lever, Nicolas Heess, Thomas Degris, Daan Wierstra, and Martin Riedmiller. 2014. Deterministic Policy Gradient Algorithms. In International Conference on Machine Learning. 387–395.

- Ui (2016) Takashi Ui. 2016. Bayesian Nash Equilibrium and Variational Inequalities. Journal of Mathematical Economics 63 (March 2016), 139–146. https://doi.org/10.1016/j.jmateco.2016.02.004

- Vickrey (1961) William Vickrey. 1961. Counterspeculation, Auctions, and Competitive Sealed Tenders. The Journal of finance 16, 1 (1961), 8–37.

- Zinkevich (2003) Martin Zinkevich. 2003. Online Convex Programming and Generalized Infinitesimal Gradient Ascent. In Proceedings of the Twentieth International Conference on International Conference on Machine Learning. AAAI Press, Washington, DC, USA, 928–935.