Average-Reward Off-Policy Policy Evaluation with Function Approximation

Abstract

We consider off-policy policy evaluation with function approximation (FA) in average-reward MDPs, where the goal is to estimate both the reward rate and the differential value function. For this problem, bootstrapping is necessary and, along with off-policy learning and FA, results in the deadly triad (Sutton & Barto, 2018). To address the deadly triad, we propose two novel algorithms, reproducing the celebrated success of Gradient TD algorithms in the average-reward setting. In terms of estimating the differential value function, the algorithms are the first convergent off-policy linear function approximation algorithms. In terms of estimating the reward rate, the algorithms are the first convergent off-policy linear function approximation algorithms that do not require estimating the density ratio. We demonstrate empirically the advantage of the proposed algorithms, as well as their nonlinear variants, over a competitive density-ratio-based approach, in a simple domain as well as challenging robot simulation tasks.

shangtong

1 Introduction

A fundamental problem in average-reward Markov Decision Processes (MDPs, see, e.g., Puterman (1994)) is policy evaluation, that is, estimating, for a given policy, the reward rate and the differential value function. The reward rate of a policy is the average reward per step and thus measures the policy’s long term performance. The differential value function summarizes the expected cumulative future excess rewards, which are the differences between received rewards and the reward rate. The solution of the policy evaluation problem is interesting in itself because it provides a useful performance metric, the reward rate, for a given policy. In addition, it is an essential part of many control algorithms, which aim to generate a policy that maximizes the reward rate by iteratively improving the policy using its estimated differential value function (see, e.g., Howard (1960); Konda (2002); Abbasi-Yadkori et al. (2019)).

One typical approach in policy evaluation is to learn from real experience directly, without knowing or learning a model. If the policy followed to generate experience (behavior policy) is the same as the policy of interest (target policy), then this approach yields an on-policy method; otherwise, it is off-policy. Off-policy methods are usually more practical in settings in which following bad policies incurs prohibitively high cost (Dulac-Arnold et al., 2019). For policy evaluation, we can use either tabular methods, which maintain a look-up table to store quantities of interest (e.g., the differential values for all states) separately, or use function approximation, which represents these quantities collectively, possibly in a more efficient way (e.g., using a neural network). Function approximation methods are necessary for MDPs with large state and/or action spaces because they are scalable in the size of these spaces and also generalize to states and actions that are not in the data (Mnih et al., 2015; Silver et al., 2016). Finally, for the policy evaluation problem in average reward MDPs, the agent’s stream of experience never terminates and thus actual returns cannot be obtained. Because of this, learning algorithms have to bootstrap, that is, the estimated values must be updated towards targets that include existing estimated values instead of actual returns.

In this paper, we consider methods for solving the average-reward policy evaluation problem with all the above three elements (off-policy learning, function approximation and bootstrapping), which comprise the deadly triad (see Chapter 11 of Sutton & Barto (2018) and Section 3). The main contributions of this paper are two newly proposed methods to break this deadly triad in the average-reward setting, both of which are inspired by the celebrated success of the Gradient TD family of algorithms (Sutton et al., 2009b, a) in breaking the deadly triad in the discounted setting.

Few methods exist for learning differential value functions. These are either on-policy linear function approximation methods (Tsitsiklis & Van Roy, 1999; Konda, 2002; Yu & Bertsekas, 2009; Abbasi-Yadkori et al., 2019) or off-policy tabular methods (Wan et al., 2020). The on-policy methods use the empirical average of received rewards as an estimate for the reward rate. Thus they are not straightforward to extend to the off-policy case. And, as we show later with a counterexample, the naive extension of the off-policy tabular method by Wan et al. (2020) to the linear function approximation setting can diverge, exemplifying the deadly triad. By contrast, the two algorithms we propose are the first provably convergent methods for learning the differential value function via off-policy linear function approximation.

All existing methods for estimating reward rate in off-policy function approximation setting require learning the density ratio, i.e., the ratio between the stationary distribution of the target policy and the sampling distribution (Liu et al., 2018a; Zhang et al., 2020a, b; Mousavi et al., 2020; Lazic et al., 2020). Interestingly, while density-ratio-based methods dominate off-policy policy evaluation with function approximation in average-reward MDPs, in the discounted MDPs, both density-ratio-based (Hallak & Mannor, 2017; Liu et al., 2018a; Gelada & Bellemare, 2019; Nachum et al., 2019a; Uehara & Jiang, 2019; Xie et al., 2019; Tang et al., 2019; Zhang et al., 2020a, b) and value-based (Baird, 1995; Sutton et al., 2009b, a, 2016; Thomas et al., 2015; Jiang & Li, 2015) methods have succeeded. It thus remains unknown whether a convergent value-based method could be found for such a problem and if it exists, how it performs compared with density-ratio-based methods. The two algorithms we propose are the first provably convergent differential-value-based methods for reward rate estimation via off-policy linear function approximation, which answer the question affirmatively. Furthermore, our empirical study shows that our value-based methods consistently outperform a competitive density-ratio-based approach, GradientDICE (Zhang et al., 2020b), in the tested domains, including both a simple Markov chain and challenging robot simulation tasks.

2 Background

In this paper, we use to denote the vector norm induced by a positive definite matrix , i.e., . We also use to denote the corresponding induced matrix norm. When , we ignore the subscript and write for simplicity. All vectors are column vectors. 0 denotes an all-zero vector whose dimension can be deduced from the context. 1 is similarly defined. When it does not confuse, we use a function and a vector interchangeably. For example, if is a function from to , we also use to denote the corresponding vector in .

We consider an infinite horizon MDP with a finite state space , a finite action space , a reward function , and a transition kernel . When an agent follows a policy in the MDP, at time step , the agent observes a state , takes an action , receives a reward , proceeds to the next time step and observes the next state . The reward rate of policy is defined as

| (1) |

where is the Cesaro limit. The Cesaro limit in (1) is assumed to exist and is independent of . The most general assumption that guarantees these is the following one:

Assumption 2.1.

Policy induces a unichain.

The action-value function in the average-reward setting is known as the differential action-value function and is defined as . Note that if a stronger ergodic chain assumption is used instead, the Cesaro limit in defining and is equivalent to the normal limit. The action-value Bellman equation is

| (2) |

where and are free variables and is the transition matrix, that is, . It is well-known (Puterman, 1994) that is the unique solution for and all the solutions for form a set .

In this paper, we consider a special off-policy learning setting, where the agent learns from i.i.d. samples drawn from a given sampling distribution. In particular, at the -th iteration, the agent draws a sample from a given sampling distribution . Distribution can be any distribution satisfying

Assumption 2.2.

, , , and for all ,

where denotes the marginal distribution of . The last part of Assumption 2.2 means that every state-action pair is possible to be sampled. This is a necessary condition for learning the differential value function accurately for all state-action pairs. In the rest of the paper, the expectation is taken w.r.t. .

If no sampling distribution is given, one could instead draw samples in the following way. First randomly sample from a batch of transitions collected by one or multiple agents, with all agents following possibly different unknown policies in the same MDP. Then sample . Assuming that the number of all state-action pairs in the batch grows to infinity as the batch size grows to infinity then sampling from the batch is approximately equivalent to sampling from some distribution satisfying Assumption 2.2.

Our goal is to approximate, using the data generated from , both the reward rate and the differential value function. The reward rate is approximated by a learnable scalar . The differential value function is only approximated up to a constant. That is, we are only interested in approximating for some . This is sufficient if the approximated value function is only used for policy improvement in a control algorithm. However, when the state and/or action spaces are large, function approximation may be necessary to represent . This paper mainly considers linear function approximation, where the agent is given a feature mapping that generates a -dimensional vector given a state-action pair . The agent further maintains a learnable weight vector and adjusts it to approximate, for all , using . Let be the feature matrix whose row is . For the uniqueness of the solution for , it is common to make the following assumption:

Assumption 2.3.

has linearly independent columns.

3 Differential Semi-Gradient Evaluation

We first present Differential Semi-gradient Evaluation (Diff-SGQ), which is a straightforward extension of the tabular off-policy Differential TD-learning algorithm (Wan et al., 2020) to linear function approximation.

At the -th iteration, the algorithm draws a sample from and updates and as

| (3) | ||||

| (4) |

where is the stepsize used at -th iteration, , , and is the temporal difference error. From (2), it is easy to see holds for any probability distribution ; in particular, it holds for , which is the intuition behind the update (4).Diff-SGQ iteratively solves

| (5) |

whose solutions, if they exist, are TD fixed points. A TD fixed point is an approximate solution to (2) using linear function approximation. We consider the quality of the approximation in the next section. All the proposed algorithms in this paper aim to find a TD fixed point up to some regularization bias if necessary.

In general, there could be no TD fixed point, one TD fixed point, or infinitely many TD fixed points, as in the discounted setting. To see this, let , , and . Then combining (3) and (4) gives

| (6) |

where . Writing (6) in vector form, we have , where

| (7) | |||

| (8) | |||

| (9) |

If and only if is invertible, there exists a unique TD fixed point

| (10) |

Otherwise, there is either no TD fixed point or there are infinitely many.

Unfortunately, even if there exists a unique TD fixed point, Diff-SGQ can still diverge, which exemplifies the deadly triad (Sutton & Barto, 2018) in the average-reward setting. The following example confirms this point.

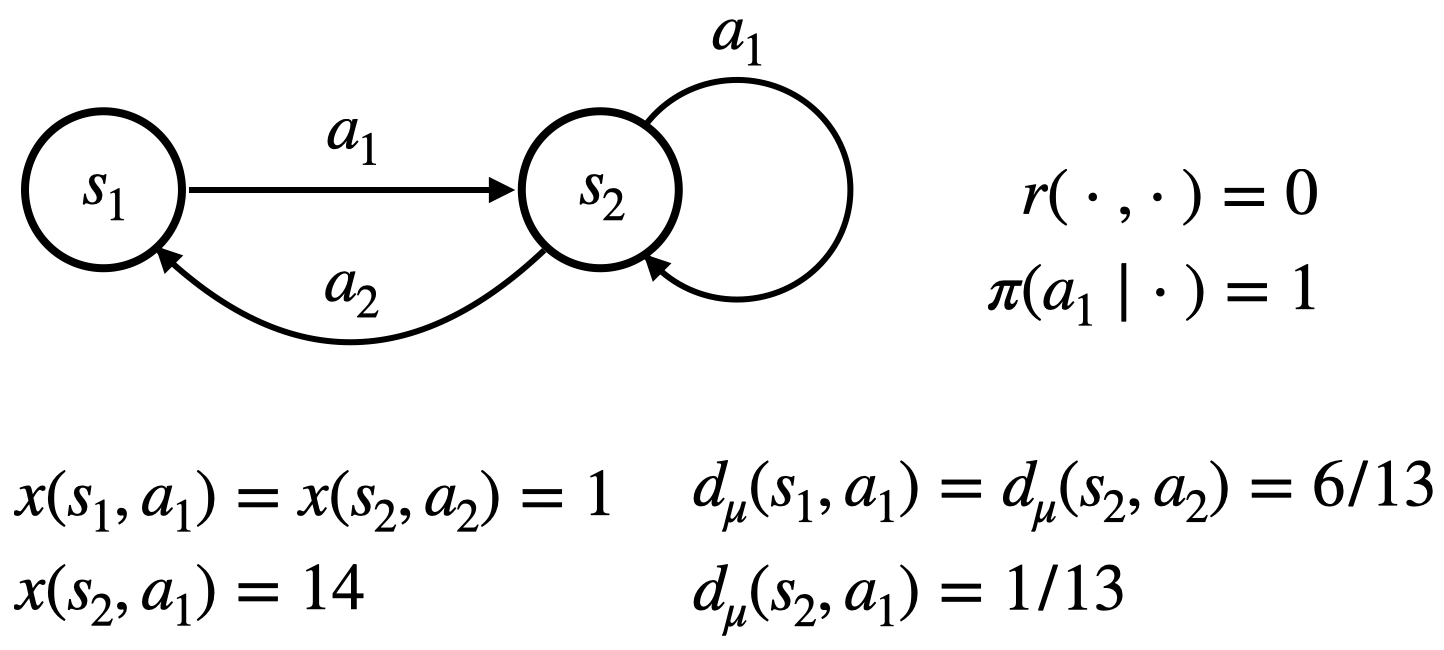

Example 1 (The divergence of Diff-SGQ).

Consider a two-state MDP (Figure 1). The expected Diff-SGQ update per step can be written as Here, we consider a constant stepsize. The eigenvalues of are both positive. Hence, no matter what positive stepsize is picked, the expected update diverges. The sample updates (3) and (4) using standard stochastic approximation stepsizes, therefore, also diverge. Furthermore, because both eigenvalues are positive, A is an invertible matrix, implying the unique existence of the TD fixed-point.

4 One-Stage Differential Gradient Evaluation

We now present an algorithm that is guaranteed to converge to the TD fixed point if it uniquely exists. Motivated by the Mean Squared Projected Bellman Error (MSPBE) defined in the discounted setting and used by Gradient TD algorithms, we define the MSPBE in the average-reward setting as

| (11) |

where is the projection matrix and is the vector of TD errors for all state-action pairs. The vector is the projection of the vector of TD errors on the column space of . The existence of the matrix inverse in , , is guaranteed by Assumption 2.2 and

Assumption 4.1.

For any such that and for any , .

The above assumption guarantees that if is a solution for in (5), then no other solution’s approximated action-value function would be identical to up to a constant. This assumption is also used by Tsitsiklis & Van Roy (1999) in their on-policy policy evaluation algorithms in average-reward MDPs. Apparently the assumption does not hold in the tabular setting (i.e., when ). However, with function approximation, we usually have many more states than features (i.e., ), in which case the above assumption would not be restrictive.

Let , we have , with which we give a different form for (11):

| (12) | ||||

| (13) |

It can be seen that if (6) has a solution, then that solution also minimizes (12), in which case solving (6) can be converted to minimizing (12). However, when (6) does not have a unique solution, the set of minimizers of (12) could be unbounded and thus algorithms minimizing risk generating unbounded updates. To ensure the stability of our algorithm when (6) does not have a unique solution, we use a regularized as our objective:

| (14) |

where , is a positive scalar, and is a ridge regularization term on .

To minimize , one could proceed with techniques used in TDC (Sutton et al., 2009a), which we leave for future work. In this paper, we proceed with the saddle-point formulation of GTD2 introduced by Liu et al. (2015), which exploits Fenchel’s duality:

| (15) |

for any positive definite , yielding

| (16) | ||||

| (17) |

So , where

| (18) |

As is convex in and concave in , we have now reduced the problem into a convex-concave saddle point problem. Applying primal-dual methods to this problem, that is, performing gradient ascent for following and gradient descent for following , we arrive at our first new algorithm, One-Stage Differential Gradient Evaluation, or Diff-GQ1. At the -th iteration, with a sample from , Diff-GQ1 updates and as

| (19) | ||||

| (20) | ||||

| (21) |

where is the sequence of learning rates satisfying the following standard assumption:

Assumption 4.2.

is a positive deterministic nonincreasing sequence s.t. and .

The algorithm is one-stage because, while there are two weight vectors updated in every iteration, both converge simultaneously.

Theorem 1.

We defer the full proof to Section A.1.

Proof.

(Sketch) With , we rewrite (19) as

| (22) |

where

| (23) |

The asymptotic behavior of is governed by

The convergence of to a unique point can be guaranteed if is a Hurwitz matrix, or equivalently, if the real part of any eigenvalue of is strictly negative. Therefore, it is important to first ensure that is nonsingular. If was nonsingular, we can show being nonsingular easily even with . However, in general, may not be nonsingular and therefore, we require to ensure being nonsingular. We can easily show that the real part of any eigenvalue of is strictly negative and thus is Hurwitz. Standard stochastic approximation results (Borkar, 2009) then show Define as the lower half of , we have It is easy to verify (e.g., using the first order optimality condition of ) that is the unique minimizer of . ∎

Quality of TD Fixed Points. We now analyze the quality of TD fixed points. For our analysis, we make the following assumption.

Assumption 4.3.

There exists at least one TD fixed point.

Let be one fixed point (a solution of (6)). We are interested in the upper bound of the absolute value of the difference between the estimated reward rate and the true reward rate and also the upper bound of the minimum distance between the estimated differential value function to the set . In general, as long as there is representation error, the TD fixed point can be arbitrarily poor in terms of approximating the value function, even in the discounted case (see Kolter (2011) for more discussion). In light of this, we study the bounds only when is close to , the stationary state-action distribution of , in the sense of the following assumption. Let be a constant,

Assumption 4.4.

is positive semidefinite, where

A similar assumption about is also used by Kolter (2011) in the analysis of the performance of the MSPBE minimizer in the discounted setting. Kolter (2011) uses while we use to account for the lack of discounting. In Section D.1, we show with simulation that this assumption holds with reasonable probability in our randomly generated MDPs. Furthermore, we consider the bounds when all the features have zero mean under the distribution .

Assumption 4.5.

.

This can easily be done by subtracting each feature vector sampled in our learning algorithm by some estimated mean feature vector, which is the empirical average of all the feature vectors sampled from . Note without this mean-centered feature assumption, a looser bound can also be obtained. Our intention here is to show that bounds of our algorithms are on par with their counterparts in the discounted setting and thus one does not lose these bounds when one moves from the discounted setting to the average-reward setting.

We defer the proof to Section A.2. As a special case, there exists a unique TD fixed point in the on-policy case (i.e., ) under Assumptions 2.1, 2.3, and 4.1. Then as and a tighter bound for the estimated differential value function can be obtained. See Tsitsiklis & Van Roy (1999) for details.

Finite Sample Analysis. We now provide finite sample analysis for a variant of Diff-GQ1, Projected Diff-GQ1, which is detailed in Section A.3 in the appendix. Projected Diff-GQ1 is different from Diff-GQ1 in three ways: 1) for each iteration, Projected Diff-GQ1 projects the two updated weight vectors to two bounded closed sets to ensure that the weight vectors do not become too large, 2) Projected Diff-GQ1 uses a constant stepsize, and 3) Projected Diff-GQ1 does not impose ridge regularization, that is, it considers the objective directly.

Proposition 2.

(Informal) Under standard assumptions, if Assumption 4.4 holds and is nonsingular, with proper stepsizes, with high probability, the iterates generated by Projected Diff-GQ1 satisfy

| (27) | ||||

| (28) |

where .

We defer the precise statement and its proof to Section A.3.

5 Two-Stage Differential Gradient Evaluation

While Assumption 4.1 is not restrictive, we present in this section a new algorithm that does not require it but can still converge to the TD fixed point if it uniquely exists. The algorithm achieves this by drawing one more sample from for each iteration, and performing two learning stages, where converges only when has converged. We call this algorithm Two-Stage Differential Gradient Evaluation, or Diff-GQ2, and derive it as follows.

Consider the TD fixed point (5). Writing in vector form, we have

| (29) |

Replacing in with (29), we have:

| (30) | |||

| (31) |

or equivalently

| (32) |

where , . The combination of (29) and (32) is an alternative definition for TD fixed points. When is invertible, the unique TD fixed points are

| (33) | ||||

| (34) |

It is easy to verify that , where is defined in (10).

Denote , then (32) can be written as , from which we define a new MSPBE objective:

| (35) |

where in is invertible under Assumption 2.2. is different from defined in (12) in that is a function of only while is a function of both and . However, the solutions of MSPBE = 0 are exactly the solutions of in = 0, if both solutions exist.

After introducing a ridge term with for the same reason as Diff-GQ1, we arrive at the objective that Diff-GQ2 minimizes:

| (36) |

Applying Fenchel’s duality on yields , where

| (37) | ||||

| (38) |

is convex in and concave in . To apply primal-dual methods for finding the saddle point of , we need to obtain unbiased samples of . As this term includes two nested expectations (i.e., and ), Diff-GQ2 requires two i.i.d. samples and from at the -th iteration for a single gradient update. This is not the notorious double sampling issue in minimizing the Mean Square Bellman Error (see, e.g., Baird (1995) and Section 11.5 by Sutton & Barto (2018)), where two successor states and from a single state action pair are required, which is not possible in the function approximation setting. Sampling two i.i.d. tuples from is completely feasible.

At the -th iteration, Diff-GQ2 updates and as

| (39) | ||||

| (40) | ||||

| (41) | ||||

| (42) |

where , again, satisfies Assumption 4.2. Additionally, following (29), Diff-GQ2 updates as

| (43) | ||||

| (44) |

where satisfies the same assumption as .

Assumption 5.1.

is a positive deterministic nonincreasing sequence s.t. and .

Theorem 2.

If Assumptions 2.1, 2.2, 2.3, 4.2, & 5.1 hold, then almost surely, the iterates generated by Diff-GQ2 (39) & (44) satisfy

| (45) |

where is the unique minimizer of . Define , we have

| (46) |

for some constant . Further, if Assumption 4.3 holds, then , and if is invertible, then for , and converge almost surely to and defined in (33).

We defer the full proof to Section A.4. Similar to Projected Diff-GQ1, we provide a finite sample analysis for a variant of Diff-GQ2, Projected Diff-GQ2, in Section A.5.

6 Experiments

In light of the reproducibility challenge in RL research (Henderson et al., 2017), we perform a grid search with 30 independent runs for hyperparameter tuning in all our experiments. Each curve corresponds to the best hyperparameters minimizing the error of the reward rate prediction at the end of training and is averaged over 30 independent runs with the shaded region indicating one standard deviation. To the best of our knowledge, GradientDICE is the only density-ratio-based approach for off-policy policy evaluation in average-reward MDPs that is provably convergent with general linear function approximation and has computational complexity per step. We, therefore, use GradientDICE as a baseline. See Section B.1 for more details about GradientDICE. All the implementations are publicly available. 111https://github.com/ShangtongZhang/DeepRL

Linear Function Approximation. We benchmark Diff-SGQ, Diff-GQ1, Diff-GQ2, and GradientDICE in a variant of Boyan’s chain (Boyan, 1999), which is the same as the chain used in Zhang et al. (2020b) except that we introduce a nonzero reward for each action for the purpose of policy evaluation. The chain is illustrated in Figure 3. We consider target policies of the form for all , where is some constant. The sampling distribution we consider has the form and for all , where is some constant. Even if , the problem is still off-policy. We consider linear function approximation and use the same state features as Boyan (1999), which are detailed in Section C. We use an one-hot encoding for actions. Concatenating the state feature and the one-hot action feature yields the state-action feature we use in the experiments.

We use constant learning rates for all compared algorithms, which is tuned in . For Diff-GQ1 and Diff-GQ2, besides tuning in the same way as Diff-SGQ, we tune in . For GradientDICE, besides tuning in the same way as Diff-GQ1, we tune , the weight for a normalizing term, in .

We run each algorithm for steps. Diff-GQ2 updates are applied every two steps as one Diff-GQ2 update requires two samples. The results in Figure 2 suggest that the three differential-value-based algorithms proposed in this paper consistently outperform the density-ratio-based algorithm GradientDICE in the tested domain.

Nonlinear Function Approximation. The value-based off-policy policy evaluation algorithms proposed in this paper can be easily combined with neural network function approximators. For Diff-SGQ, we use a target network (Mnih et al., 2015) to stabilize the training of neural networks. For Diff-GQ1 and Diff-GQ2, we introduce neural network function approximators in the saddle-point objectives (i.e., and ) directly, similar to Zhang et al. (2020b) in GradientDICE. The details are provided Sections B.2, B.3, and B.4.

We benchmark Diff-SGQ, Diff-GQ1, Diff-GQ2, and GradientDICE in several MuJoCo domains. To this end, we first train a deterministic target policy with TD3 (Fujimoto et al., 2018). The behavior policy is composed by introducing Gaussian noise to , i.e., . The ground truth reward rate of is computed with Monte Carlo methods by running for steps. We vary from . More details are provided in Section C. For Differential FQE, Diff-GQ1, and Diff-GQ2, we tune the learning rate from . For GradientDICE, we additionally tune from . The results with are reported in Figure 4, where Diff-GQ1 consistently performs the best. The results with and are deferred to Section D.2, where Diff-GQ1 consistently performs the best as well.

7 Related Work and Discussion

In this paper, we addressed the policy evaluation problem with function approximation in the model-free setting. If the model is given or learned by the agent, such a problem could be solved by, for example, classic approximate dynamic programming approaches (Powell, 2007), search algorithms (Russell & Norvig, 2002), and other optimal control algorithms (Kirk, 2004). For more discussion about learning a model, see, for example, Sutton (1990); Sutton et al. (2012); Liu et al. (2018b); Chua et al. (2018); Wan et al. (2019); Gottesman et al. (2019); Yu et al. (2020); Kidambi et al. (2020).

The on-policy average-reward policy evaluation problem was studied by Tsitsiklis & Van Roy (1999), which proposed and solved a Projected Bellman Equation (PBE). The reward rate in PBE is a known quantity, which is trivial to estimate in the on-policy case. The reward rate, however, cannot be obtained easily in the off-policy case and needs to be estimated cleverly. Such a challenge is resolved in our work by optimizing a novel objective, , which has the reward rate estimate as a free variable to optimize. Moreover, by proposing the other novel objective , we showed that the reward rate or its direct estimate does not even have to appear in an objective. In fact, for the uniqueness of the solution, our algorithms did not optimize and MSPBE2, but optimized a regularized version of these objectives, where the weight of the regularization term can be arbitrarily small. Introducing a regularization term in MSPBE-like objectives is not new though; see, for example, Mahadevan et al. (2014); Yu (2017); Du et al. (2017); Zhang et al. (2020d, b). One could, of course, apply regularization to Diff-SGQ directly, similar to Diddigi et al. (2019) in the discounted off-policy linear TD. Unfortunately, the weight for their regularization term has to be sufficiently large to ensure convergence.

Fenchel’s duality, which we used in the derivation of our algorithms, is not new in RL research. For example, it has been applied to cope with the double sampling problem (see, e.g., Liu et al. (2015); Macua et al. (2014); Dai et al. (2017); Xie et al. (2018); Nachum et al. (2019a, b); Zhang et al. (2020a, b)) or to construct novel policy iteration frameworks (Zhang et al., 2020c).

8 Conclusion

In this paper, we provided the first study of the off-policy policy evaluation problem (estimating both reward rate and differential value function) in the function approximation, average-reward setting. Such a problem encapsules the existing off-policy evaluation problem (estimating only the reward rate; see, e.g., Li (2019)). To this end, we proposed two novel MSPBE objectives and derived two algorithms optimizing regularized versions of these objectives. The proposed algorithms are the first provably convergent algorithms for estimating the differential value function and are also the first provably convergent algorithms for estimating the reward rate without estimating density ratio in this setting. In terms of estimating the reward rate, though our goal is not to achieve new state of the art, our empirical results confirmed that the proposed value-based methods consistently outperform a competitive density-ratio-based method in tested domains. We conjecture that this performance advantage results from the flexibility of value-based methods, that is, for any , is a feasible learning target. By contrast, the density ratio is unique. Overall, our empirical study suggests that value-based methods deserve more attention in future research on off-policy evaluation in average-reward MDPs.

Acknowledgments

SZ is generously funded by the Engineering and Physical Sciences Research Council (EPSRC). This project has received funding from the European Research Council under the European Union’s Horizon 2020 research and innovation programme (grant agreement number 637713). The experiments were made possible by a generous equipment grant from NVIDIA.

References

- Abbasi-Yadkori et al. (2019) Abbasi-Yadkori, Y., Bartlett, P., Bhatia, K., Lazic, N., Szepesvari, C., and Weisz, G. Politex: Regret bounds for policy iteration using expert prediction. In International Conference on Machine Learning, 2019.

- Baird (1995) Baird, L. Residual algorithms: Reinforcement learning with function approximation. Machine Learning, 1995.

- Borkar (2009) Borkar, V. S. Stochastic approximation: a dynamical systems viewpoint. Springer, 2009.

- Boyan (1999) Boyan, J. A. Least-squares temporal difference learning. In Proceedings of the 16th International Conference on Machine Learning, 1999.

- Chua et al. (2018) Chua, K., Calandra, R., McAllister, R., and Levine, S. Deep reinforcement learning in a handful of trials using probabilistic dynamics models. In Advances in Neural Information Processing Systems, 2018.

- Dai et al. (2017) Dai, B., Shaw, A., Li, L., Xiao, L., He, N., Liu, Z., Chen, J., and Song, L. Sbeed: Convergent reinforcement learning with nonlinear function approximation. arXiv preprint arXiv:1712.10285, 2017.

- Diddigi et al. (2019) Diddigi, R. B., Kamanchi, C., and Bhatnagar, S. A convergent off-policy temporal difference algorithm. arXiv preprint arXiv:1911.05697, 2019.

- Du et al. (2017) Du, S. S., Chen, J., Li, L., Xiao, L., and Zhou, D. Stochastic variance reduction methods for policy evaluation. In Proceedings of the 34th International Conference on Machine Learning, 2017.

- Dulac-Arnold et al. (2019) Dulac-Arnold, G., Mankowitz, D., and Hester, T. Challenges of real-world reinforcement learning. arXiv preprint arXiv:1904.12901, 2019.

- Fujimoto et al. (2018) Fujimoto, S., van Hoof, H., and Meger, D. Addressing function approximation error in actor-critic methods. arXiv preprint arXiv:1802.09477, 2018.

- Gelada & Bellemare (2019) Gelada, C. and Bellemare, M. G. Off-policy deep reinforcement learning by bootstrapping the covariate shift. In Proceedings of the 33rd AAAI Conference on Artificial Intelligence, 2019.

- Gottesman et al. (2019) Gottesman, O., Liu, Y., Sussex, S., Brunskill, E., and Doshi-Velez, F. Combining parametric and nonparametric models for off-policy evaluation. arXiv preprint arXiv:1905.05787, 2019.

- Hallak & Mannor (2017) Hallak, A. and Mannor, S. Consistent on-line off-policy evaluation. In Proceedings of the 34th International Conference on Machine Learning, 2017.

- Henderson et al. (2017) Henderson, P., Islam, R., Bachman, P., Pineau, J., Precup, D., and Meger, D. Deep reinforcement learning that matters. arXiv preprint arXiv:1709.06560, 2017.

- Howard (1960) Howard, R. A. Dynamic programming and markov processes. 1960.

- Jiang & Li (2015) Jiang, N. and Li, L. Doubly robust off-policy value evaluation for reinforcement learning. arXiv preprint arXiv:1511.03722, 2015.

- Kidambi et al. (2020) Kidambi, R., Rajeswaran, A., Netrapalli, P., and Joachims, T. Morel: Model-based offline reinforcement learning. arXiv preprint arXiv:2005.05951, 2020.

- Kirk (2004) Kirk, D. E. Optimal control theory: an introduction. Courier Corporation, 2004.

- Kolter (2011) Kolter, J. Z. The fixed points of off-policy td. In Advances in Neural Information Processing Systems, 2011.

- Konda (2002) Konda, V. R. Actor-critic algorithms. PhD thesis, Massachusetts Institute of Technology, 2002.

- Lazic et al. (2020) Lazic, N., Yin, D., Farajtabar, M., Levine, N., Gorur, D., Harris, C., and Schuurmans, D. A maximum-entropy approach to off-policy evaluation in average-reward mdps. Advances in Neural Information Processing Systems, 2020.

- Li (2019) Li, L. A perspective on off-policy evaluation in reinforcement learning. Frontiers of Computer Science, 2019.

- Liu et al. (2015) Liu, B., Liu, J., Ghavamzadeh, M., Mahadevan, S., and Petrik, M. Finite-sample analysis of proximal gradient td algorithms. In Proceedings of the 31st Conference on Uncertainty in Artificial Intelligence, 2015.

- Liu et al. (2018a) Liu, Q., Li, L., Tang, Z., and Zhou, D. Breaking the curse of horizon: Infinite-horizon off-policy estimation. In Advances in Neural Information Processing Systems, 2018a.

- Liu et al. (2018b) Liu, Y., Gottesman, O., Raghu, A., Komorowski, M., Faisal, A. A., Doshi-Velez, F., and Brunskill, E. Representation balancing mdps for off-policy policy evaluation. Advances in Neural Information Processing Systems, 2018b.

- Liu et al. (2019) Liu, Y., Swaminathan, A., Agarwal, A., and Brunskill, E. Off-policy policy gradient with state distribution correction. arXiv preprint arXiv:1904.08473, 2019.

- Macua et al. (2014) Macua, S. V., Chen, J., Zazo, S., and Sayed, A. H. Distributed policy evaluation under multiple behavior strategies. IEEE Transactions on Automatic Control, 2014.

- Mahadevan et al. (2014) Mahadevan, S., Liu, B., Thomas, P., Dabney, W., Giguere, S., Jacek, N., Gemp, I., and Liu, J. Proximal reinforcement learning: A new theory of sequential decision making in primal-dual spaces. arXiv preprint arXiv:1405.6757, 2014.

- Mnih et al. (2015) Mnih, V., Kavukcuoglu, K., Silver, D., Rusu, A. A., Veness, J., Bellemare, M. G., Graves, A., Riedmiller, M., Fidjeland, A. K., Ostrovski, G., et al. Human-level control through deep reinforcement learning. Nature, 2015.

- Mousavi et al. (2020) Mousavi, A., Li, L., Liu, Q., and Zhou, D. Black-box off-policy estimation for infinite-horizon reinforcement learning. In International Conference on Learning Representations, 2020.

- Nachum et al. (2019a) Nachum, O., Chow, Y., Dai, B., and Li, L. Dualdice: Behavior-agnostic estimation of discounted stationary distribution corrections. arXiv preprint arXiv:1906.04733, 2019a.

- Nachum et al. (2019b) Nachum, O., Dai, B., Kostrikov, I., Chow, Y., Li, L., and Schuurmans, D. Algaedice: Policy gradient from arbitrary experience. arXiv preprint arXiv:1912.02074, 2019b.

- Nair & Hinton (2010) Nair, V. and Hinton, G. E. Rectified linear units improve restricted boltzmann machines. In Proceedings of the 27th International Conference on Machine Learning, 2010.

- Powell (2007) Powell, W. B. Approximate Dynamic Programming: Solving the curses of dimensionality, volume 703. John Wiley & Sons, 2007.

- Puterman (1994) Puterman, M. L. Markov decision processes: discrete stochastic dynamic programming. John Wiley & Sons, 1994.

- Russell & Norvig (2002) Russell, S. and Norvig, P. Artificial intelligence: a modern approach. 2002.

- Silver et al. (2016) Silver, D., Huang, A., Maddison, C. J., Guez, A., Sifre, L., Van Den Driessche, G., Schrittwieser, J., Antonoglou, I., Panneershelvam, V., Lanctot, M., et al. Mastering the game of go with deep neural networks and tree search. Nature, 2016.

- Sutton (1990) Sutton, R. S. Integrated architectures for learning, planning, and reacting based on approximating dynamic programming. In Proceedings of the 7th International Conference on Machine Learning, 1990.

- Sutton & Barto (2018) Sutton, R. S. and Barto, A. G. Reinforcement Learning: An Introduction (2nd Edition). MIT press, 2018.

- Sutton et al. (2009a) Sutton, R. S., Maei, H. R., Precup, D., Bhatnagar, S., Silver, D., Szepesvári, C., and Wiewiora, E. Fast gradient-descent methods for temporal-difference learning with linear function approximation. In Proceedings of the 26th International Conference on Machine Learning, 2009a.

- Sutton et al. (2009b) Sutton, R. S., Maei, H. R., and Szepesvári, C. A convergent temporal-difference algorithm for off-policy learning with linear function approximation. In Advances in Neural Information Processing Systems, 2009b.

- Sutton et al. (2012) Sutton, R. S., Szepesvári, C., Geramifard, A., and Bowling, M. P. Dyna-style planning with linear function approximation and prioritized sweeping. arXiv preprint arXiv:1206.3285, 2012.

- Sutton et al. (2016) Sutton, R. S., Mahmood, A. R., and White, M. An emphatic approach to the problem of off-policy temporal-difference learning. The Journal of Machine Learning Research, 2016.

- Tang et al. (2019) Tang, Z., Feng, Y., Li, L., Zhou, D., and Liu, Q. Doubly robust bias reduction in infinite horizon off-policy estimation. arXiv preprint arXiv:1910.07186, 2019.

- Thomas et al. (2015) Thomas, P. S., Theocharous, G., and Ghavamzadeh, M. High-confidence off-policy evaluation. In Twenty-Ninth AAAI Conference on Artificial Intelligence, 2015.

- Tsitsiklis & Van Roy (1999) Tsitsiklis, J. N. and Van Roy, B. Average cost temporal-difference learning. Automatica, 35(11):1799–1808, 1999.

- Uehara & Jiang (2019) Uehara, M. and Jiang, N. Minimax weight and q-function learning for off-policy evaluation. arXiv preprint arXiv:1910.12809, 2019.

- Wan et al. (2019) Wan, Y., Zaheer, M., White, A., White, M., and Sutton, R. S. Planning with expectation models. arXiv preprint arXiv:1904.01191, 2019.

- Wan et al. (2020) Wan, Y., Naik, A., and Sutton, R. S. Learning and planning in average-reward markov decision processes. arXiv preprint arXiv:2006.16318, 2020.

- Xie et al. (2018) Xie, T., Liu, B., Xu, Y., Ghavamzadeh, M., Chow, Y., Lyu, D., and Yoon, D. A block coordinate ascent algorithm for mean-variance optimization. In Advances in Neural Information Processing Systems, 2018.

- Xie et al. (2019) Xie, T., Ma, Y., and Wang, Y.-X. Towards optimal off-policy evaluation for reinforcement learning with marginalized importance sampling. In Advances in Neural Information Processing Systems, 2019.

- Yu (2017) Yu, H. On convergence of some gradient-based temporal-differences algorithms for off-policy learning. arXiv preprint arXiv:1712.09652, 2017.

- Yu & Bertsekas (2009) Yu, H. and Bertsekas, D. P. Convergence results for some temporal difference methods based on least squares. IEEE Transactions on Automatic Control, 2009.

- Yu et al. (2020) Yu, T., Thomas, G., Yu, L., Ermon, S., Zou, J., Levine, S., Finn, C., and Ma, T. Mopo: Model-based offline policy optimization. arXiv preprint arXiv:2005.13239, 2020.

- Zhang et al. (2020a) Zhang, R., Dai, B., Li, L., and Schuurmans, D. Gendice: Generalized offline estimation of stationary values. In International Conference on Learning Representations, 2020a.

- Zhang et al. (2020b) Zhang, S., Liu, B., and Whiteson, S. GradientDICE: Rethinking generalized offline estimation of stationary values. In Proceedings of the 37th International Conference on Machine Learning, 2020b.

- Zhang et al. (2020c) Zhang, S., Liu, B., and Whiteson, S. Mean-variance policy iteration for risk-averse reinforcement learning. In Proceedings of the 35th AAAI Conference on Artificial Intelligence, 2020c.

- Zhang et al. (2020d) Zhang, S., Liu, B., Yao, H., and Whiteson, S. Provably convergent two-timescale off-policy actor-critic with function approximation. In Proceedings of the 37th International Conference on Machine Learning, 2020d.

Appendix A Proofs

We first state a general result from Borkar (2009) which will be repeatedly used. Consider updating as

| (47) |

where , and denotes some bounded random or deterministic noise that converges to 0 as . Assuming

Assumption A.1.

is a positive deterministic nonincreasing sequence satisfying

Assumption A.2.

There exist and such that

| (48) |

satisfies

-

1.

a.s..

-

2.

for some constant a.s..

Here

| (49) |

where denotes the -field.

Assumption A.3.

The real part of every eigenvalue of is strictly negative.

Theorem 3 combines the third extension of Theorem 2 in Chapter 2.2 and Theorem 7 in Chapter 3 of Borkar (2009).

A.1 Proof of Theorem 1

Proof.

The proof mimics the convergence proof of GTD2 in Sutton et al. (2009a). We proceed by verifying Assumptions A.1- A.3 thus invoking Theorem 3. With , we rewrite (19) as

| (51) |

where

The asymptotic behavior of is governed by

| (52) |

where

| (53) | |||

| (54) |

Assumption A.1 is satisfied by our requirement on . For Assumption A.2, we define

| (55) |

It is easy to see

| (56) | ||||

| (57) |

Because our samples are generated in an i.i.d fashion, Assumption A.2 is guaranteed to hold.

To verify Assumption A.3, we first show . Using the rule of block matrix determinant, we have

| (58) |

Assumption 4.1 ensures is positive definite and is positive semidefinite, implying is positive semidefinite. For any , if and only if has the form for some , implying , i.e., . So as long as , , implying is positive definite. It follows easily that . Let be an eigenvalue of . implies . Let be the corresponding normalized eigenvector of , i.e., , where is the conjugate transpose of . Let , we have

| (59) |

As , we have , where denotes the real part. So

| (60) |

Because , we have . Assumption A.3 then holds. Invoking Theorem 3 yields

| (61) |

Let be the lower half of , we have

| (62) |

From (16), we can rewrite as

| (63) |

It is easy to verify (e.g., using the first order optimality condition of ) that is the unique minimizer of .

It can also be seen that if and is invertible, as well and . ∎

A.2 Proof of Proposition 1

Proof.

is a TD fixed point implies

| (64) |

which implies

| (65) |

expanding which yields

| (66) | ||||

| (67) |

So we have

| (68) |

implying

| (69) |

Using the Schur complement, Assumption 4.4 implies (see Kolter (2011) for more details)

| (70) |

holds for any . We have

| (71) | ||||

| (72) | ||||

| (73) | ||||

| (74) | ||||

| (75) | ||||

| (76) | ||||

| (77) | ||||

| (78) | ||||

| (79) |

From the above derivation we have

| (80) |

Take the infimum

| (81) |

For the reward rate at the fixed point, we have, for all ,

| (82) | ||||

| (83) | ||||

| (84) |

where the inequality is due to the Cauchy-Schwarz inequality.

∎

A.3 Projected Diff-GQ1

The Projected Diff-GQ1 optimizes the MSPBE1 objective:

| (85) |

where

| (86) |

Similar to the Revised GTD Algorithms in Liu et al. (2015), the Projected Diff-GQ1 update and as

| (87) | ||||

| (88) |

where is a constant learning rate, is a compact subset in and is projection into w.r.t. . If is nonsingular, has a unique saddle point, which we refer to as . It is easy to see is the unique minimizer of . We have

Proposition 3.

Proof.

We first state a lemma.

Lemma 1.

With at least probability ,

| (91) |

where are constants.

Proof.

A.4 Proof of Theorem 2

Proof.

With , we rewrite (39) as

| (94) |

where

| (95) |

The asymptotic behavior of is governed by

| (96) |

where . Similar to the proof of Theorem 1 in Section A.1, up to change of notations, we can get

| (97) |

where

| (98) |

is the unique minimizer of . We then rewrite (44) as

| (99) |

Similar to the convergence proof of , we can obtain

| (100) |

Assumption 4.3 implies there exists such that,

| (101) |

or equivalently,

| (102) |

has unique or infinite manly solutions. From standard results of system of linear equations, this is equivalent to

| (103) |

where denotes the Moore-Penrose pseudoinverse, which always exists for any matrix. By the property of the Moore-Penrose pseudoinverse, it is easy to see

| (104) |

Consequently, we have

| (105) |

implying

| (106) |

It can also be seen that if is invertible, and . Applying SVD to and using to denote its minimum nonzero singular value, it is easy to see

| (107) |

∎

A.5 Projected Diff-GQ2

The Projected Diff-GQ2 objective is

| (108) |

where

| (109) |

The Projected Diff-GQ2 update , and as

| (110) | ||||

| (111) | ||||

| (112) | ||||

| (113) |

where and are constant learning rates, is a compact subset in and is projection into w.r.t. . If is nonsingular, has a unique saddle point, which we refer to as . It is easy to see is the unique minimizer of . We have

Proposition 4.

Proof.

We first state a lemma.

Lemma 2.

With at least probability ,

| (116) |

where is a constant.

Proof.

The proof is the same as the proof of Lemma 1. We, therefore, omit the proof to avoid verbatim repetition. ∎

We have

| (117) |

Taking infimum both sides and invoking Lemma 2 and Proposition 1 to bound RHS completes the proof of the first half. Let we rewrite the update as

| (118) |

where

| (119) |

in other words, is updated following a noisy stochastic gradient . Let denote the expectation w.r.t. for . As does not depend on the samples at the -th iteration, we have

| (120) | ||||

| (121) | ||||

| (122) | ||||

| (123) |

where and are some constants and depends on the variance of and . Using Lemma 2 to bound and invoking Theorem 4 in the appendix of Liu et al. (2019) yields

| (124) |

in other words,

| (125) |

combining which and Proposition 1 yields

| (126) |

which completes the proof. ∎

Appendix B Algorithm Details

B.1 GradientDICE with Linear and Nonlinear Function Approximation

Let be the stationary state action distribution under the target policy (assuming it exists), GradientDICE aims to learn the density ratio . Let , parameterized by , be the function to approximate the density ratio, GradientDICE considers the following problem to optimize :

| (127) | |||

| (128) |

Here , parameterized by , is an auxiliary function and is an auxiliary variable. GradientDICE uses primal-dual algorithms to optimize . Let be a learning rate, GradientDICE updates are

| (129) | ||||

| (130) | ||||

| (131) |

We could then use as an estimate of the reward rate, which is, however, computationally expensive. To obtain the average-reward estimate in an efficiently way, we additionally maintain a scalar estimate directly, which is updated as

| (132) |

B.2 Diff-SGQ with Nonlinear Function Approximation

Let be the function to estimate the differential action-value function parameterized by and be the scalar estimate for the average-reward, Diff-SGQ updates and as

| (133) | ||||

| (134) |

where and are parameters of the target network, which are synchronized with and periodically.

B.3 Diff-GQ1 with Nonlinear Function Approximation

Let be our estimates for the differential action-value function and the average-reward, we have

| (135) | ||||

| (136) | ||||

| (137) | ||||

| (138) |

When using function approximation, we assume is parameterized by and consider the following problem:

| (139) | |||

| (140) |

Here the auxiliary function is parameterized by . Diff-GQ1 updates are then

| (141) | ||||

| (142) | ||||

| (143) |

If both and are linear, the above updates are the same as (19) with .

B.4 Diff-GQ2 with Nonlinear Function Approximation

Let be our estimates for the differential action-value function, we have

| (144) | ||||

| (145) | ||||

| (146) | ||||

| (147) |

When using function approximation, we assume is parameterized by and consider the following problem:

| (148) | |||

| (149) | |||

| (150) |

Here the auxiliary function is parameterized by . Diff-GQ2 updates are then

| (151) | ||||

| (152) | ||||

| (153) |

where is a scalar estimate for the reward rate. If both and are linear, the above updates are the same as (19) with .

Appendix C Implementation Details

C.1 Boyan’s Chain

The state features we use are provided in Section C.1 of Zhang et al. (2020b).

C.2 MuJoCo

The dataset is composed by running the behavior policy for steps. For GradientDICE, we use neural networks to parameterize and . For Diff-SGQ, we use neural networks to parameterize . For Diff-GQ1 and Diff-GQ2, we use neural networks to parameterize and . All the networks have the standard architecture, which are exactly the same as Zhang et al. (2020b). They are two-hidden-layer networks with each hidden layer consisting of 64 hidden units and ReLU (Nair & Hinton, 2010) activation function. The output layer does not have nonlinear activation function. The for all algorithms is always a global scalar parameter. For GradientDICE, we find using an additional parameter for reward rate prediction performs better and is much more computationally efficient than using , where is the number of transitions in the dataset. As recommended by Zhang et al. (2020b), we use SGD to train all algorithms and do not use ridge regularization. We sample transitions each step to form a minibatch for training. Diff-GQ2 performs one gradient update every two steps. For Diff-SGQ, we update the target network every 100 steps.

Appendix D Other Experimental Results

D.1 Simulation of Assumption 4.4

We provide simulation results investigating when Assumption 4.4 is likely to hold. For each trial, we first generate a random , each row of which is randomly sampled from a simplex. We then compute its stationary distribution analytically. The sampling distribution is composed by adding Gaussian noise to , i.e., . We then normalize by . If the normalized still does not lie in a simplex, we then apply softmax to . We use and generate the feature matrix randomly, each element of which is sampled from and is uniformly randomly sampled from . We then analytically compute if in Assumption 4.4 is positive semidefinite or not. We conduct trials for each and report the probability that is positive semidefinite in Tables 1 and 2.

| 0.70 | 0.69 | 0.70 | 0.65 | 0.52 | |

| 0.64 | 0.65 | 0.63 | 0.56 | 0.42 | |

| 0.55 | 0.50 | 0.44 | 0.41 | 0.36 | |

| 0.52 | 0.42 | 0.43 | 0.38 | 0.35 |

| 0.92 | 0.92 | 0.91 | 0.77 | 0.58 | |

| 0.92 | 0.92 | 0.84 | 0.68 | 0.50 | |

| 0.93 | 0.68 | 0.53 | 0.48 | 0.42 | |

| 0.93 | 0.51 | 0.49 | 0.45 | 0.42 |

D.2 Additional Results on MuJoCo

The results on MuJoCo tasks with and are reported in Figure 5.

Appendix E Other Differential Gradient Evaluation Algorithms

In this section, we briefly discuss two other variants of Differential Gradient Evaluation algorithms, Diff-GQ3 and Diff-GQ4. Diff-GQ1 uses as the feature matrix for both the primal variable and the dual variable . Consequently, to ensure the objective is strictly concave in , has to be positive definite, i.e., Assumption 4.1 is assumed. Diff-GQ2 uses as the feature matrix for both the primal variable and the dual variable . Consequently, to obtain an estimate of the reward rate from , two i.i.d. samples are required. To combine the advantages of both Diff-GQ1 and Diff-GQ2, Diff-GQ3 uses as the feature matrix for the primal variable but as the feature matrix for the dual variable . Diff-GQ3 considers the following MSPBE:

| (164) |

Similar to the derivation of Diff-GQ1, we arrive at the Diff-GQ3 update:

| (165) | ||||

| (166) | ||||

| (167) |

Theorem 4.

The proof is the same as the proof of Theorem 1 up to change of notations and thus omitted. If and is nonsingular, it is easy to see that

| (169) |

and is the unique minimizer of MSPBE. Though in the tabular setting (i.e., ), this is the TD fixed point , in general they are not the same. Moreover, in Diff-GQ3, we apply ridge regularization to . If ridge is applied to only like Diff-GQ1 and Diff-GQ2, the current proof of Theorem 4 will not hold. We leave more analysis of Diff-GQ3 for future work.

We now briefly describe Diff-GQ4. Given a reward rate estimate , we define

| (170) |

Importantly, in MSPBE4, is fixed and is not a learnable parameter of this MSPBE. By contrast, in MSPBE3, both and are learnable parameters of the MSPBE. Diff-GQ4 updates in the same way as Diff-SGQ but updates following under the current , i.e.,

| (171) | ||||

| (172) | ||||

| (173) |

Our preliminary work confirms the convergence of Diff-GQ4 when is sufficiently large. We leave the analysis of Diff-GQ4 with a general and its fixed point for future work.