Life insurance policies with cash flows subject to random interest rate changes

Abstract.

The main purpose of this work is to derive a partial differential equation for the reserves of life insurance liabilities subject to stochastic interest rates where the benefits and premiums depend directly on changes in the interest rate curve. In particular, we allow the payment streams to depend on the performance of an overnight technical interest rate, making them stochastic as well. This opens up for considering new types of contracts based on the performance of the insurer’s returns on their own investments. We provide explicit solutions for the reserves when the premiums and benefits vary according to interest rate levels or averages under the Vasicek model and conduct some simulations computing reserve surfaces numerically. We also give an example of a reinsurance treaty taking over pension payments when the insurer’s average returns fall under some specified threshold.

Key words and phrases: Reserve, stochastic reserve, interest rate, stochastic interest rate, Thiele’s equation, Thiele’s PDE, regime switching interest rate.

MSC2010: 60H30, 91G20, 91G30, 91G60, 35Q91.

1. Introduction

In actuarial science, a reserve is a liability equal to the present value of future cash flows that the insurance company promises to pay out to the insured under certain conditions. In easier terms, a reserve is an estimate of how much the insurance company should charge today in order to meet future payments owed to the insured. This quantity is the basis to ensure solvency of the company and the standard way of computing premiums. The literature sometimes distinguishes between the terms present value of future obligations and actuarial reserve. The former is the cost of the insurance itself, while the latter is obtained by subtracting the premiums provided by the insured, which are used to pay back to the insured. In this sense, the paid-in premiums should match, in average, the future obligations in such a way that the reserve at the entry of the contract is null.

In life insurance, the main sources of risk of a policy are the state of the insured which triggers the payments, and the future development of the return on the financial investments or technical interest rate. In this note, we focus on the latter and model its risk via a continuous time stochastic process of Itô-diffusion type and Markovian. We suggest a way to make cash flows interest rate dependent and provide some new examples to show how this may relax the burden of low interest rate regimes.

Life insurance claims in the context of stochastic interest rates has been studied before. We mention [1, 2] for some specific interest rate models and [3, 7, 9] for more general models in the framework of Heath-Jarrow-Morton. A model for the interest rate of diffusion type was considered by Norberg and Møller in [10] and by the authors in [4] where they look at unit-linked insurances with variance risk, as well.

A classical way of computing reserves in the continuous time setting is by solving the so-called Thiele’s differential equation, which, in the case of deterministic interest rate is an ordinary differential equation and, in the case of stochastic interest rate, a partial differential equation (PDE). The corresponding Thiele’s equation for the case of stochastic rates was derived by Norberg and Møller in [10] and later risk adjusted by Persson in [11]. In the present manuscript we use the no arbitrage approach as in [11] to price insurance claims. A justification of why this is the right pricing approach can be found there. In addition, a complete and thourough discussion of the no arbitrage approach to Thiele’s equation is creditted to Steffensen in [12]. While interest rate there was taken to be deterministic, the reader may benefit from a precise and excellent discussion on the topic.

Although the above-mentioned works do consider stochastic rates, their models assume that payments are deterministic given the state of the policyholders stipulated by contract. In this note we want to generalize the type of contracts to those looking at interest rate behaviour both at punctual times and path-dependent past averages. In the spirit of [11] we generalize Thiele’s partial differential equation (Thiele’s PDE) to incorporate interest rate dependent cash flows. The motivation to do so comes from the fact that insurance policies have historically considered fixed returns for their policyholders. This has proven to carry the risk of low returns in the bond market and as a consequence, limitations in order to cover the agreed future liabilities. In this regard, we propose new policies that take into account the behaviour of the returns and how to price them. We also propose a reinsurance treaty which covers a percentage of the pension policies in case of low returns.

The paper is organized as follows: In Section 2 we introduce our modelling framekwork for the insurance and the interest rate models in two independent probability spaces coupled together. In Section 3 we review the classical pricing of financial derivatives and adapt the Feynman-Kac formula to both European and Asian-type options, where the latter are options whose contingent claim is a function of the integral of the underlying. Then we derive a Thiele partial differential equation for insurance contracts whose cash flows depend on the performance of the interest rate. We look at specific regime switching contracts in Section 4. The examples are given in general terms, but the simulations and analysis of concrete results are provided under the Vasicek interest rate model using a rather simplified model for Norwegian mortality. More specifically we look at: a pure endowment with reduction on premiums under high interest rate levels, pension plans with pension rise under high interest rate regimes, interest rate caps and floors insurances, a binary endowment associated to two average interest rate levels and finally a reinsurance treaty taking over part of the pensions if the average returns during the premium phase are below some threshold.

2. Framework

Our modelling framework will consist of two independent probability spaces. On the one hand, the states of the insured at any given time, which will be modelled by a Markov chain and on the other hand, the value of an overnight technical interest rate.

2.1. The insurance model

Let be a complete probability space where is the set of outcomes, is a suitable -algebra and is a probability measure on and we denote by the expectation under . This space carries a stochastic process where is a time horizon, possibly infinite. We will consider the (-augmented) filtration generated by and denote it by . Since we consider no further information on this space, it is natural to take . We assume that is a regular continuous time Markov chain taking values in a finite state space with transition probabilities

By regular here, we mean that the transition rates

and

exist for every , are finite and the functions , are continuous. Hence, we can recover from via Kolmogorov’s equations.

On this space we inherently have the following processes

Here, denotes the counting measure and the left a.s.-limit of at the point . The random variable tells us whether the insured is in state at time and tells us the number of transitions from to in the whole period .

Definition 2.1 (Stochastic cash flow).

A stochastic cash flow is a stochastic process with almost all sample paths with bounded variation.

More concretely, we will consider cash flows described by an insurance policy entirely determined by its policy functions. We denote by , , the sum of payments from the insurer to the insured up to time , given that we know that the insured has always been in state . Moreover, we will denote by , , , denotes the payments which are due when the insured switches state from to at time . We always assume that these functions are of bounded variation (almost surely in the case of random payments). The cash flows we will consider are entirely described by the policy functions defined by an insurance policy.

Definition 2.2 (Policy cash flow).

We consider payout functions , and , , for of bounded variation. The (stochastic) cash flow associated to this insurance is defined by

where

The quantity corresponds to the accumulated liabilities while the insured is in state and for the case when the insured switches from to .

The value of a stochastic cash flow at time will be denoted by and is defined as

where is a suitable discount factor (e.g. can be today’s value of one monetary unit at time with respect to a technical interest rate, see Definition 2.4).

The stochastic integral is a well-defined pathwise Riemann-Stieltjes integral since is of bounded variation with probability one. Since we wish to have the best forecast for the reserve at a given time , it is natural to project on to the available information of the insurance company which, at this point, is given by . Hence, the present value of the cash flow given information is given by

| (2.1) |

In the above expression one can use any type of information in the conditional expectation to obtain proper reserves. In this case however, we may use the Markovianity of in order to compute as an actual value, that is by the Markov property of ,

for some Borel-measurable function , and hence

which corresponds to (2.1) and denotes the present value of given that we know that the insured is in state at time . An often abuse of notation is to simply write

Having established our insurance model, we will next introduce our market model with stochastic interest rate in an independent probability space.

2.2. The technical interest rate model

Let be a complete probability space where is the set of outcomes, is a suitable -algebra and is a probability measure on and we denote by the expectation under . This space carries a stochastic process: modelling the value of an overnight technical interest rate. On this space we consider the (-augmented) filtration generated by this process, denoted by and since no further information is considered we take . A natural modeling assumption at this point is to assume that and are independent.

More concretely, will be governed by the following stochastic differential equation of Itô type.

| (2.2) |

Here, is a standard Wiener process. Moreover, are measurable functions such that a pathwise unique global strong solution exists, and all moments are finite. For instance, if they satisfy the Lipschitz property uniformly in time, have at most linear growth and is away from , we have such result.

Moreover, from (2.2) is a strong Markov process admitting a stochastic flow of homeomorphisms satisfying the flow property, i.e , where

| (2.3) |

Remark 2.3.

Conditions for the existence of unique global strong solutions admitting a stochastic flow of homeomorphisms can be relaxed considerably. Low regularity can be considered if one wishes to, but since this is not the purpose of this work, we impose the classical Itô assumptions.

Definition 2.4 (Discount factor).

We define the (stochastic) discount factor as the process

which models the current value of one monetary unit at time .

Hence, a liability which is due at time has a present value today of , and value at time , .

2.3. The model

From now on we work on the probability space where , and and denote by the expectation under . The overall information considered by the insurer is , and we have for an -measurable random variable on that

for all .

We will simultaneously work on or restricted to , when necessary, without really distinguishing notations whenever the context is clear. For example, if and only depends on then is implicitly both under and since since we are working with probability measures.

2.4. Present value of a policy when , and are deterministic

We assume for a moment that is known and , , are deterministic. In particular, the only information available for the insurer is the state of the insured. Then [6, Theorem 4.6.10] states that the present value of a cash flow given by an insurance policy entirely described by the functions and is given by

| (2.4) |

The proof of the above formula is a consequence of [6, Theorem 4.6.3] which corresponds to (2.1) using the Markov property on the process . The formula itself is quite intuitive. The (future) value of the policy is the sum over all states of discounted accumulated payment streams coming from the insured being or changing state.

If we assume that are a.e. differentiable with derivative and with possibly countable discontinuities at say, points , then we can recast (2.4) as

| (2.5) | ||||

where for all and .

This is like saying that we assume that the functions admit a density (in the generalised sense) of the form

| (2.6) |

where is a (generalised) function called the Dirac delta function which has the property that

for all locally integrable functions . It can, for instance, be shown that

converges in as to .

Formula (2.5) in the case of stochastic interest rates has been studied by [11] and the corresponding Thiele’s partial defferential equation was derived. Here, in addition, we are interested in the case where and also are stochastic and subject to the performance of . Hence, the measure in (2.6) (or rather its density) is also stochastic.

3. Pricing and reserving life insurance subject to cash flows with stochastic interest rate

As we can see in (2.5), if we assume that , are adapted to , then we need to price claims of the form

for possibly varying maturities . Here, denotes the whole trajectory of up to time , and are suitable functionals on the space of continuous functions.

We will focus on claims that are functions of European and Asian type options on . For convenience introduce the following notation

| (3.1) |

and .

We will consider payoff functions of the form

for fixed and some suitable function . The risk neutral pricing approach tells us that if the market is free of arbitrage, there will be a martingale measure such that the price at time of an option with payoff is given by

| (3.2) |

By the Markov property of and the fact that we may express as a function of the states of and at time . That is,

| (3.3) |

where

and denotes the process given in (2.3).

The pricing measure is given by

where

and where for an Itô process and is an adapted process in .

Girsanov’s theorem implies that the process defined by

is a -Wiener processes.

More concretely, assuming that we have that the -dynamics of are given by

The following result is the celebrated Feynman-Kac formula which can be used to find the value of (3.3) using the theory of partial differential equations. The classical formula is often offered for European type options. Here, we provide a version for path-dependent options adapted to our purposes.

Theorem 3.1 (Feynman-Kac formula).

Let be an Itô diffusion given by

where , satisfy classical Itô assumptions for existence and uniqueness and is a standard Wiener process.

Let be two continuous functions. Consider the function solving the following PDE

| (3.4) |

with terminal condition .

Then

for all .

Proof.

Define the process

| (3.5) |

We denote by , and the partial derivaties of with respect to , and , respectively. Itô’s formula yields

The finite variation part is since satisfies PDE (3.4). Hence,

Taking expectations and using the martingale property of the Itô integral we have

| (3.6) |

Due to (3.5) we have

Hence, by (3.6) and the fact that we conclude that

∎

Applying the above result to the case , we have

Denote the differential operator

| (3.8) | ||||

We will denote by the solution to the PDE (3.7) with payoff function and maturity time . That is

| (3.9) |

From now on, we will assume that the policy functions are -a.s. a.e. differentiable with (stochastic) Lebesgue-Stieltjes measure given by

| (3.10) |

with

| (3.11) |

and that

| (3.12) |

for some functions , , , where we recall that is the notation in (3.1). These functions describe the stream of payments for each state of the insured and for the transitions between states subject to interest rate instantaneous and average changes.

In general, the cash flows coming from a policy are stochastic due to the fact that the states of the insured are stochastic, while the payments are deterministic, given that the state is known. Here, the payments are also stochastic per se, since they also depend on the interest rate curve.

Using the notation from (3.10) and (3.12) in connection with (3.3) and (2.5) we have that the prospective reserve is given by,

’ In particular, we see that the prospective reserve of interest-rate-linked policies with stochastic interest rate can be expressed as a function of , and . This is due to the fact that the process is -adapted and is Markovian. We can characterize the function , by deriving the so-called Thiele’s (partial) differential equation.

From now on, and without loss of generality, we assume and . Thus

| (3.13) | ||||

where above satisfies the PDE (3.7) with the corresponding maturity times and terminal conditions.

In the above expression the first term corresponds to the benefits associated to being in state at the end of the contract, the second term corresponds to inflow and outflow of benefits and premiums and the last term are benefits from transitions between to . We see that at the end of the contract we have indeed . The following theorem is the corresponding Thiele’s parial differential equation for (3.13), that is policies with payment streams subject to both sudden and average changes in the interest rate curve.

Theorem 3.2 (Thiele’s partial differential equation).

Let be the payout function determined by the policy functions , , and , , as defined in (3.11) and (3.12). Denote by , the value of an insurance contract at time given that the insured is in state at time and given the information . Then

where the function is the solution to the following partial differential equation

| (3.14) | ||||

with being the differential operator defined as

| (3.15) |

The boundary condition is given by .

Proof.

The PDE given in (3.14) is a second order parabolic linear PDE. It is therefore well-posed and admits a unique solution under the assumption that the coefficients are continuous. See e.g. [5].

Observe that if and are two final conditions for the PDE given in Theorem 3.1 and and denote their solutions then solves the PDE corresponding to the final condition . This is a trivial consequence of the uniqueness of the PDE and the fact that appearing in (3.2) is linear in .

Define the function

where

and

| (3.16) |

where

Then the (stochastic) reserve with payout function determined by the policy functions , and as defined in (3.11) and (3.12) is given by

Our arguments will be for fixed and being maturity times. Hence and are well-defined.

First, observe that by Kolmogorov’s backward equation we have

| (3.17) |

Further, we can find a straightforward relation between the derivatives of and those of ,

where we used relation (3.17) first and (3.16) thereafter. Moreover, if is the differential operator of (3.15), then

since is linear.

For easier readability we drop the point in the notation. Now, we compute the Itô differential of under the risk neutral measure in two ways: first, by direct defition, i.e.

| (3.18) |

and now we compute using the relation (3.16) in connection with the identity (3.17),

Now, we use the fact that is a solution to . Hence,

| (3.19) |

Equating (3.18) and (3.19) we obtain the following PDE in time and space for the function for fixed :

| (3.20) |

On the other hand, recall that and

Therefore,

where we used Lebesgue’s dominated convergence theorem and the fundamental theorem of calculus. Observe that

Altogether,

In particular, evaluating at we have

| (3.21) | ||||

Integrating (3.20) with respect to on the region , interchanging integration and differentiability, using (3.21) and we obtain

All the terms involving will cancel each other. Indeed, observe that

Also,

where we used that .

As a result, we obtain and

and the result follows by grouping together the sums over , . ∎

The following result is a direct consequence of Thiele’s PDE obtained in Theorem 3.2 showing that one can aggregate reserves from policies of equal ages and expiration dates.

Corollary 3.3.

Assume we have policies with the same maturities and all policyholders enter the contract at the same age. Then the present value of all reserves

where corresponds to the reserve of policy at time and interest rate state , given that the policy holder is in state , satisfies the PDE

with terminal condition where

Here, , and denote the policy functions for the th policyholder.

4. Life insurance policies with stochastic policy functions

Henceforward, we assume that . Since there are only two states and one of them is absorbing, we drop the notations and . That is to say, we simply write to denote the force of mortality, , and the policy functions and the mathematical reserve given that the insured is alive, since otherwise .

For simulations purposes, we will assume the Gompertz-Makeham law of mortality on given by

This law of mortality describes the age dynamics of human mortality rather accurately in the age window from about to years of age, which is good enough for our analysis. For this reason, we excluded the very first and last age groups from the data. We obtain , and which are the least squares estimates obtained by fitting Norwegian mortality from 2019 (both genders together). See Statistics Norway, table: 05381 for the employed data. Our examples will assume that the age of the insured at the beginning of the contract is fixed to years old.

We will introduce the following notations

| (4.1) |

and

| (4.2) |

which appear naturally in many common policy specifications with regimes, such as endowment, term insurance, pensions, etc.

For simulation purposes we consider the dynamics of the Vasicek short-rate model, which are given by

| (4.3) |

where , are model parameters. In this case the market price of risk is an additional constant parameter. Since the Vasicek model has the property that it is invariant under change of measure, we simply take and the reader may adjust the interest market price of risk by a modification of and .

Under the model in (4.3), one can find fairly explicit expressions. For example, PDE (3.9) can be solved in closed form for some specific terminal conditions .

Introduce the notations

and the covariance

which gives the correlation function

It holds that

From the above, one can deduce that

where denotes the distribution function of a standard normally distributed random variable. Similarly, one can show that

Observe that when then we obtain the classical price of a zero-coupon bond at time with maturity and when both expectations are null.

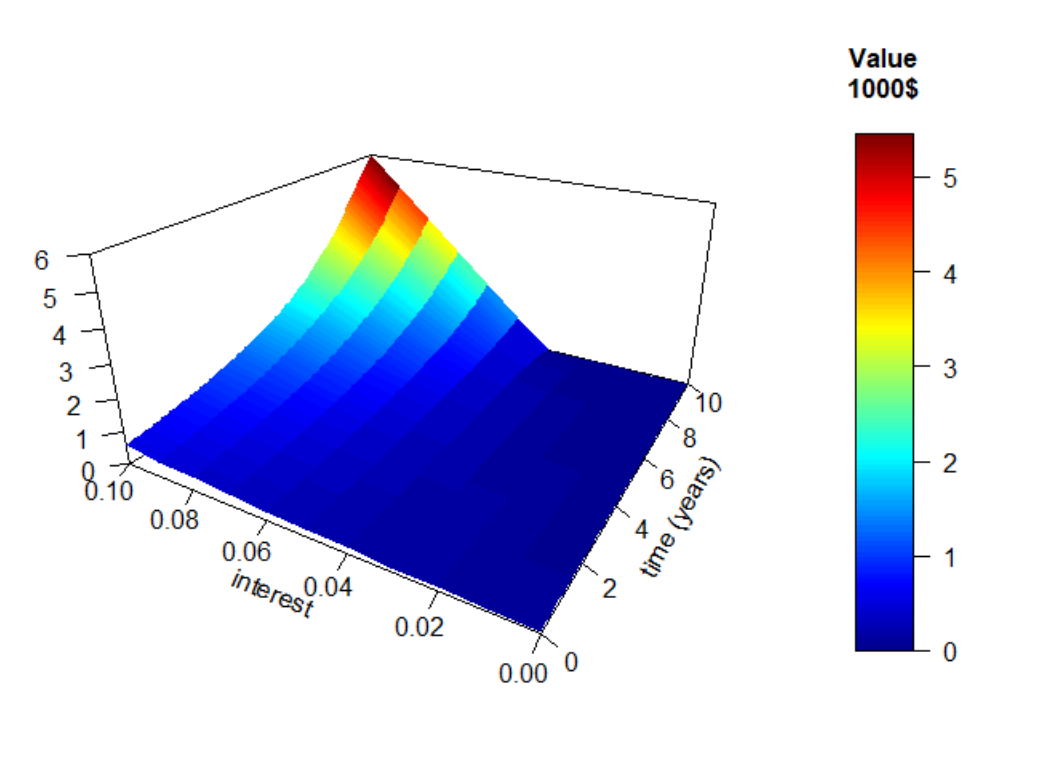

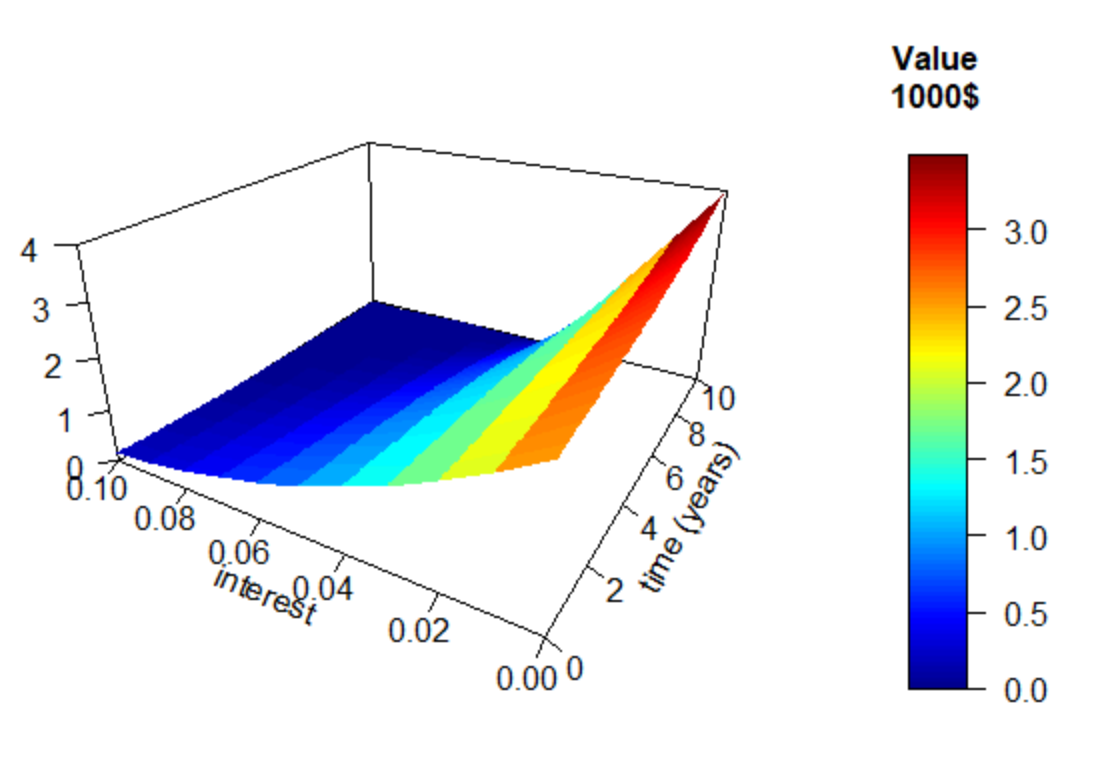

4.1. Pure endowment with premium reduction on high interest rate levels

Let be the guaranteed endowment to be paid at the end of the contract upon survival. Let be a reduction factor and an interest rate level above which premiums are reduced by a factor of . Then the value of this contract, premiums taken into account is given by

where is the function given in (4.1).

We choose in such a way that . In this case, the expected difference between reserves is given by

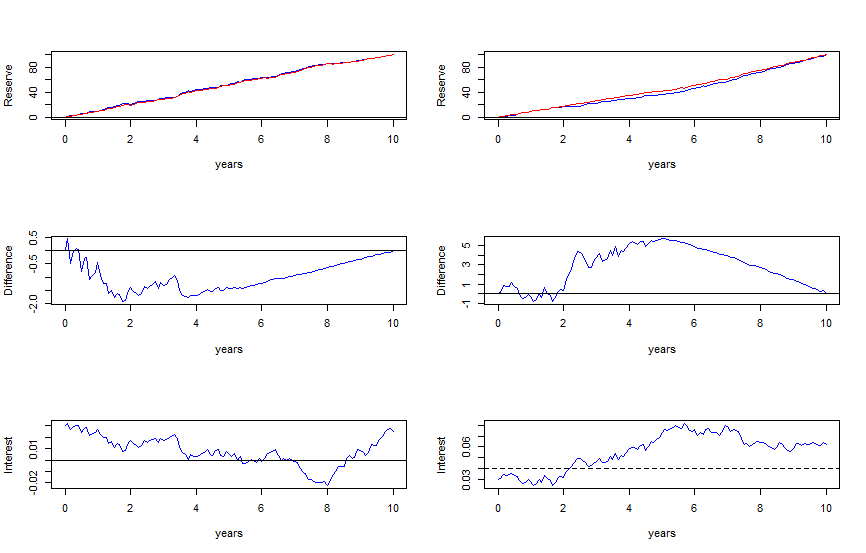

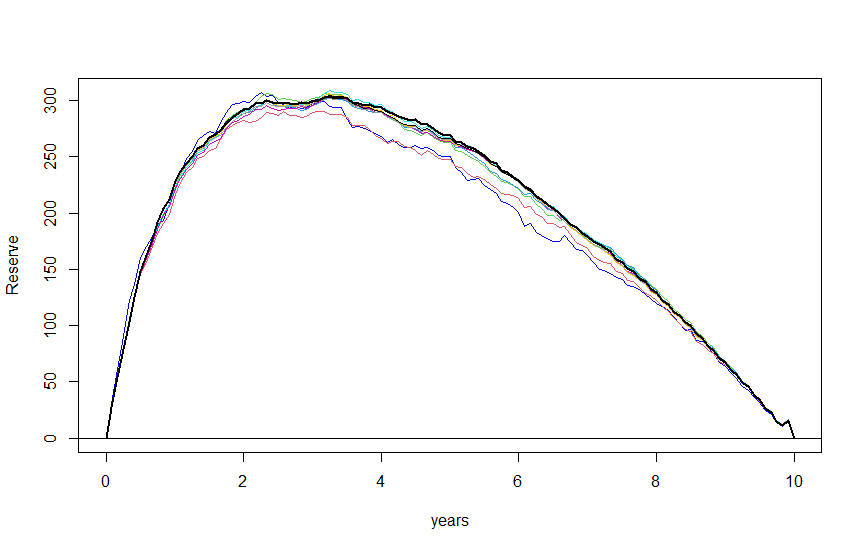

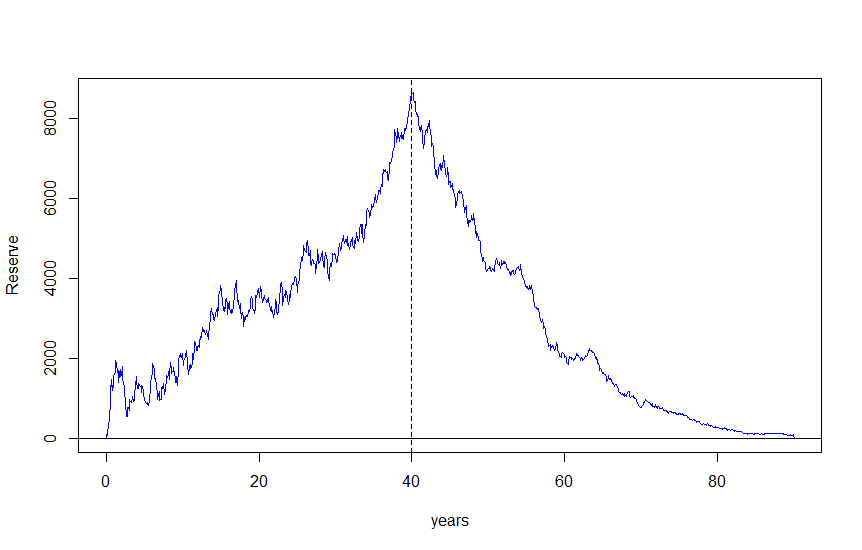

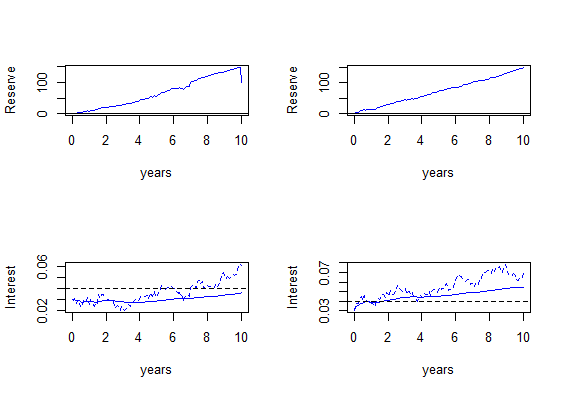

In Figure 1 we show an example of two random interest rate curves and the corresponding reserves for a contract () with and without reduction and the difference between such reserves. The parameters for the interest rate model are , , , , . The contract pays an endowment of in years for a person who is years old today. For the reduction case we take a threshold of and a premium reduction of .

One may argue that is a rather high premium for an endowment of , but the insured could have potentially profited from long high interest regimes as, for instance, the outcome on the right. There, the insured has to pay approximately for eight years of high interest rate and for the two first years of the contract. Thus, a total amount of . Under the same outcome, an insured with no reduction would have paid . In any case, to overcome the potential issue of paying too high premiums, one can add a premium refund at the end of the contract if the rates are low, or as we will see later, define a policy based on average rates rather than current rates.

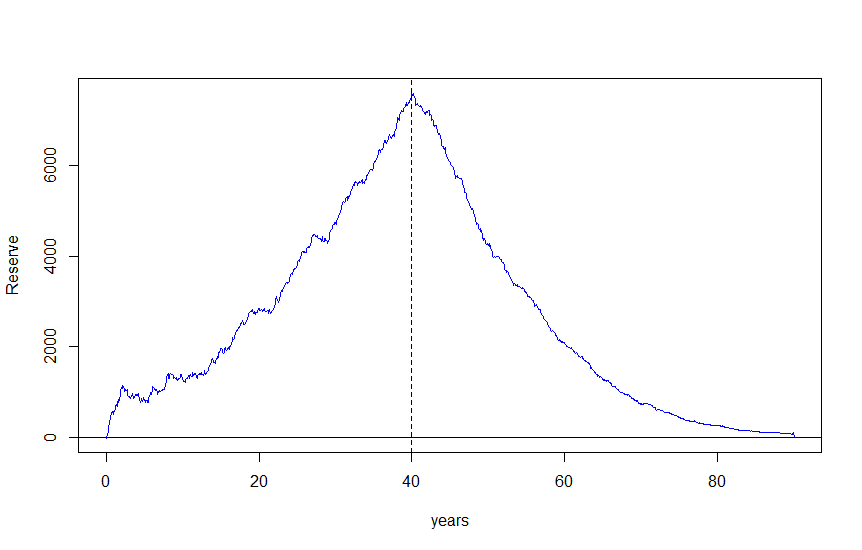

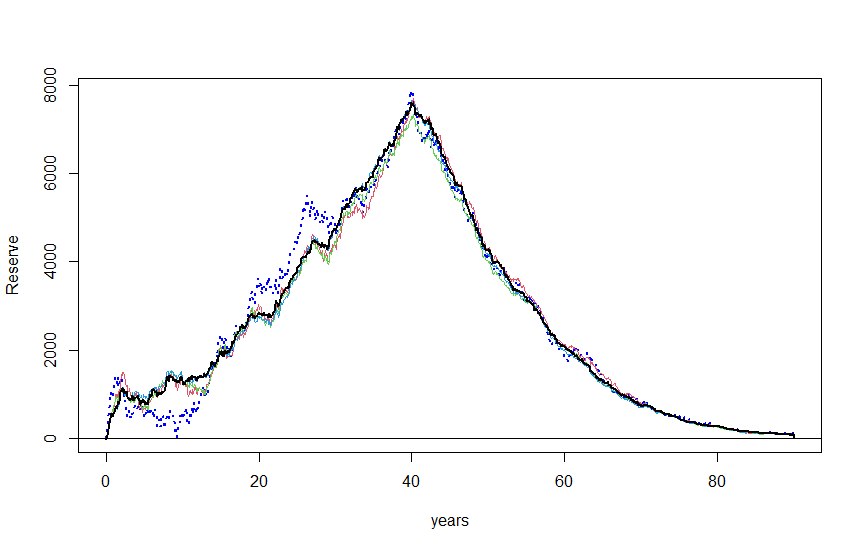

We can see in Figure 1 the reserves and their differences for two (random) interest rate regimes; one with regime mostly under (right), and another with regime crossing (left). Both outcomes shows that the reserves for the case of a policy with premium reduction requires slightly higher reserves. In Figure 2, we show the mean difference in the long-run.

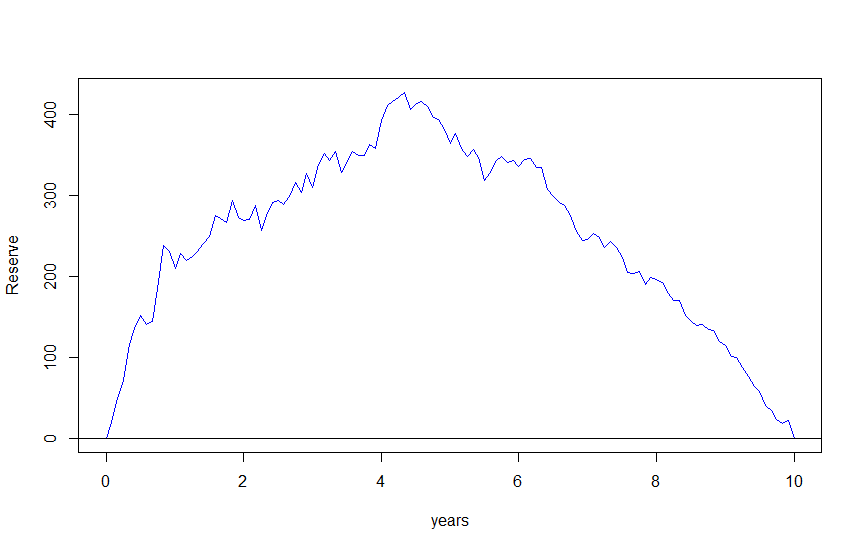

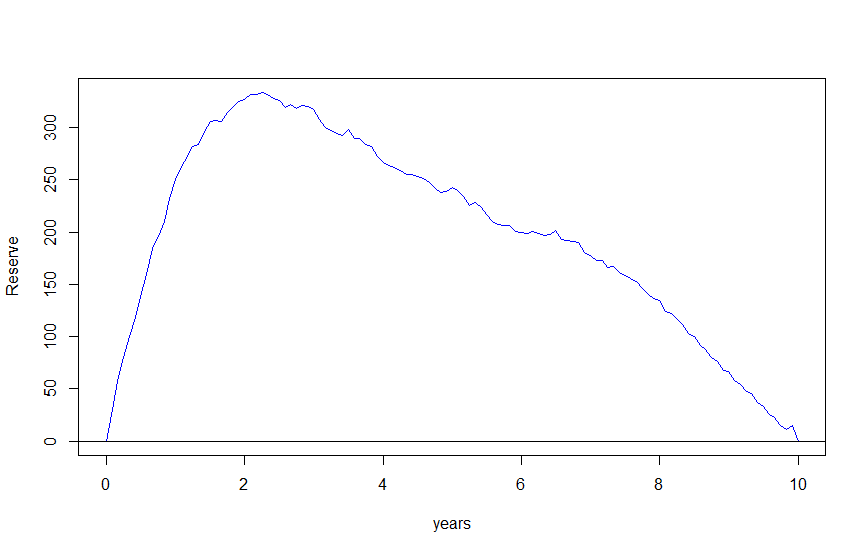

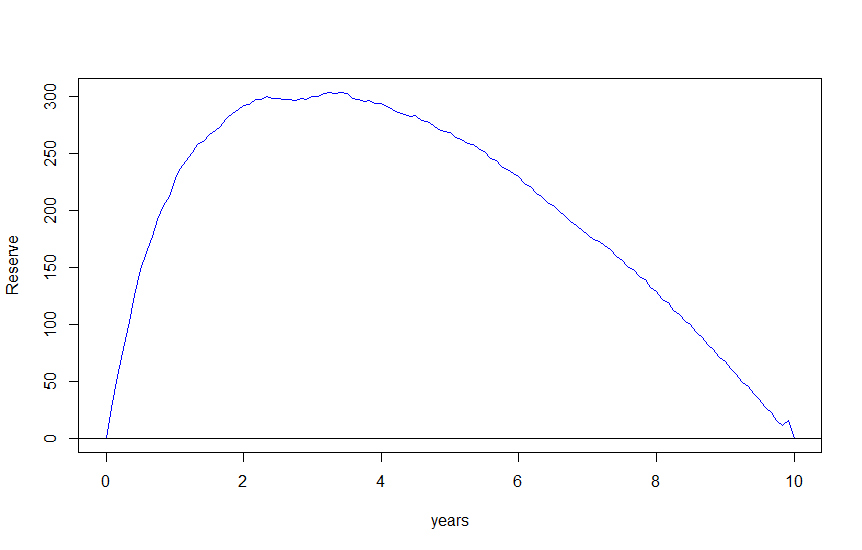

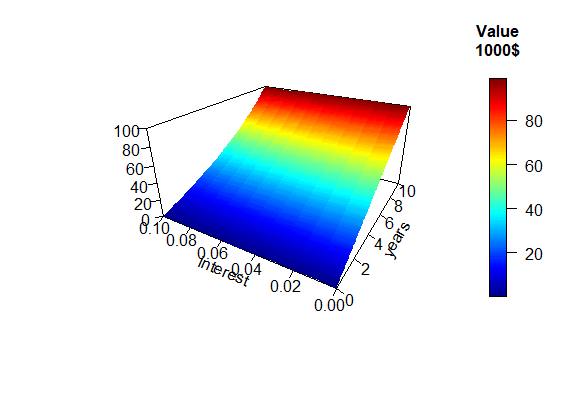

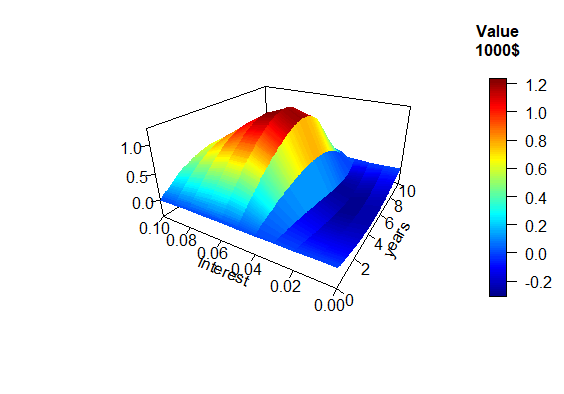

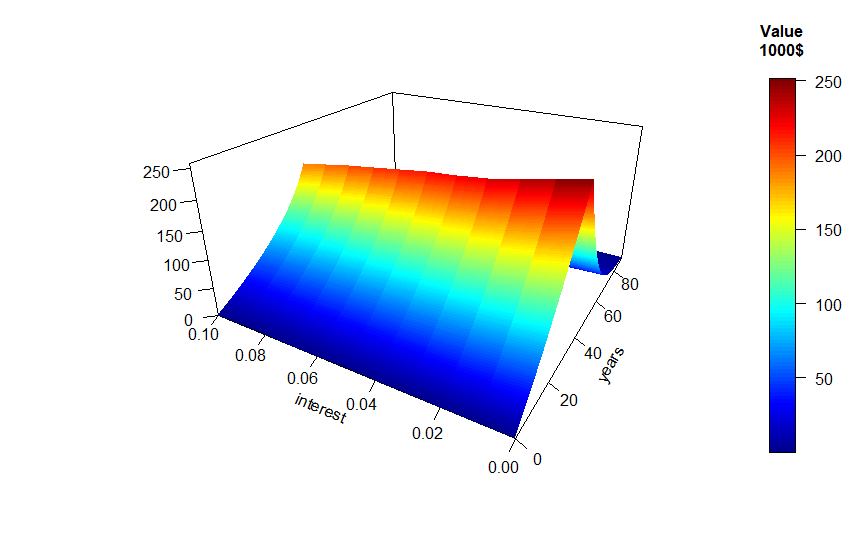

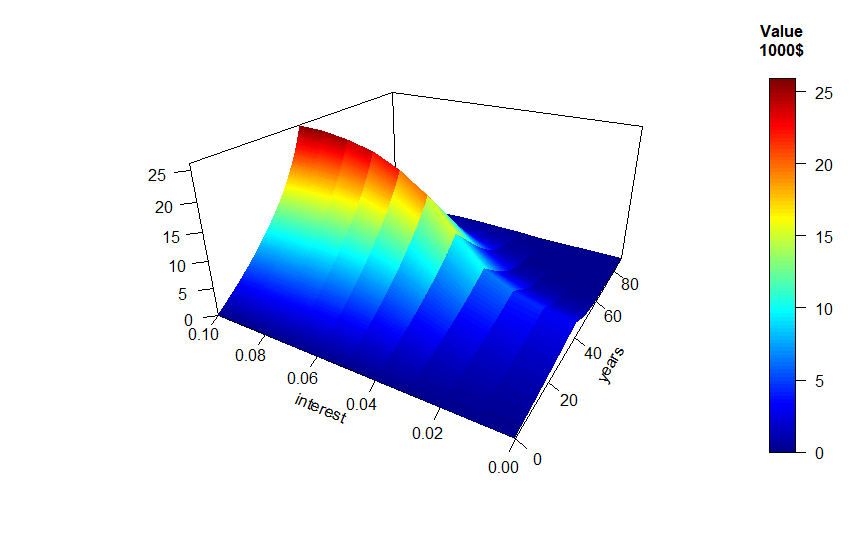

To finish this example we show the reserve surface, i.e. the function for and the surface of the difference between the reserves with reduction and without.

4.2. Pension insurance with pension bonus during high interest rate regimes

In the case of a pension insurance, the present value of a policy with periodical premiums paying a periodical pension of if interest is low and if interest is high, from time until end of life is given by

The PDE associated to in this case is given by

where

with boundary condition .

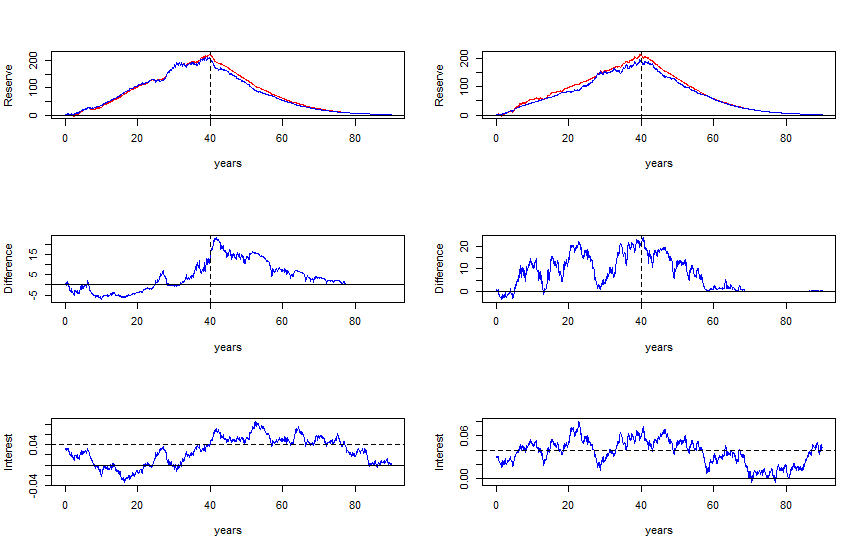

Insurance companies usually set the end of the contract at an age of or similar. Hence, a computationally more friendly boundary condition for the case that the insured is years old would be being the maximum length of the contract years.

We still consider a person who is years old today and will retire at the age of , that is in years from now. In Figure 4 we show an example of two random interest rate curves and the corresponding reserves for a contract () with and without bonus on pensions and the difference between such reserves. The parameters for the interest rate model are , , , , . The contract pays a pension of yearly if and if . We take a pension bonus of .

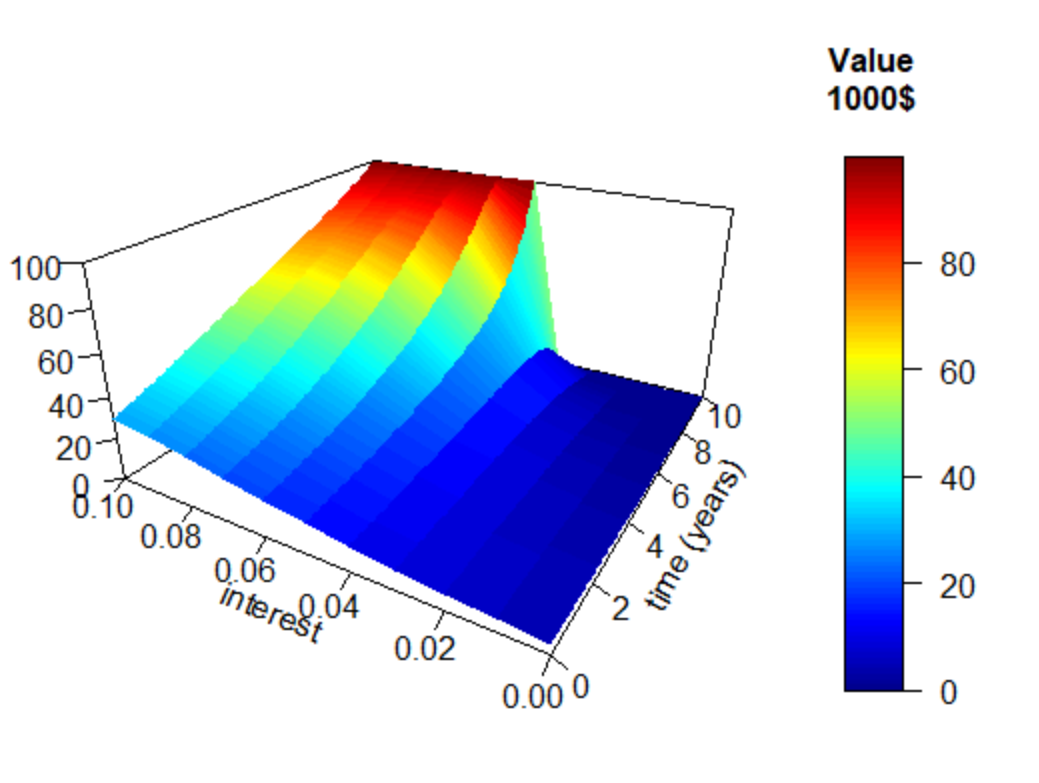

4.3. Interest rate caps and floors insurance

One can also look at four classical options on . Figure 7 shows the surfaces for the present value of an interest rate cap, an interest rate floor, a call and a put option with strike rate at the end of the contract. We obtain these present values by solving the PDE from Theorem 3.2 which in this case is given by

with terminal conditions , , and . We use an explicit finite difference method to obtain the solutions. The curve we see at corresponds to the fair premium of the contract.

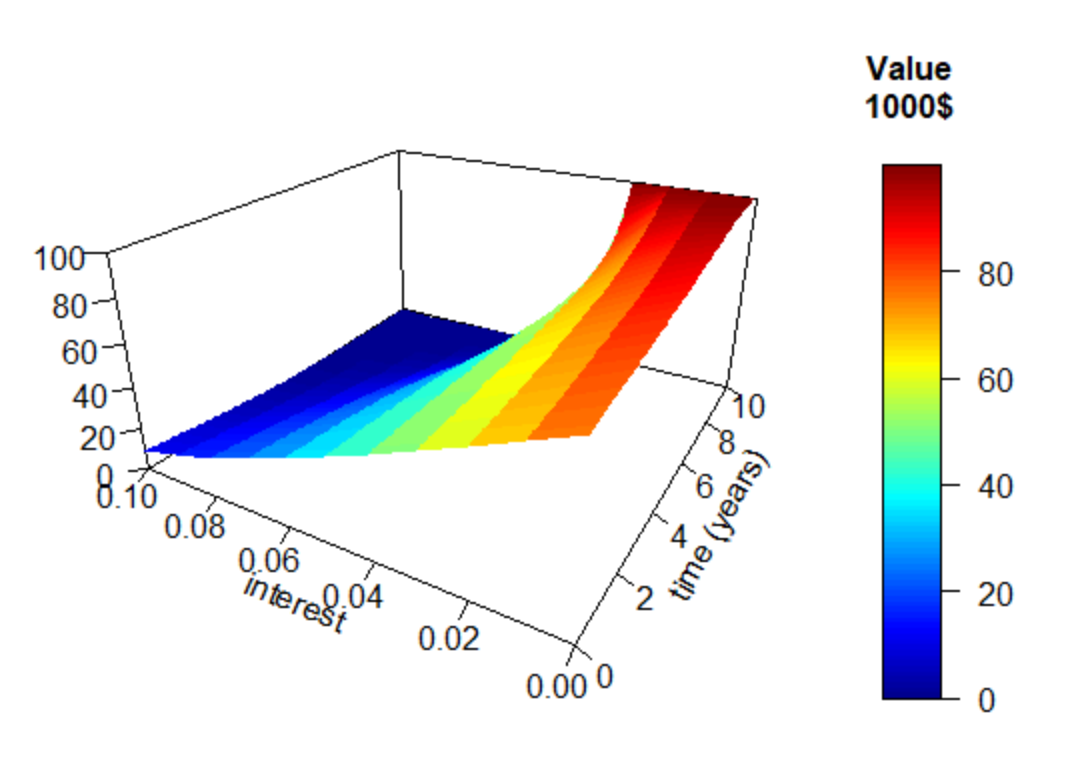

4.4. Binary endowment based on average interest rate

Let and be two endowments. The policy pays upon survival at expiry time if the average interest rate during the contract time is above and otherwise. Mathematically, the present value of this policy is given by

where here is the function defined in (4.2).

In Figure 8 we show the reserves for a binary endowment of if the average is above at the end of the contract and if the average is below under the same model as in the previous examples. The reserve is indeed stochastic.

4.5. A reinsurance treaty on pensions when insurer’s average return is low

Using the new model introduced in Section 3 we can consider reinsurance agreements between the insurer and the reinsurer. If we assume that models the return on investments for the insurer, then their liabilities depend on . If returns are low, then the pension liabilities increase, making it difficult to meet the requirements with their customers. One possibility to relax such risk could be to cede some of the risk (of low returns) to the reinsurer. In this example, we consider two polices; one for the insured and another one for the insurer (with the reinsurer). For a pension policy paying a yearly pension from upon death (or high enough ) we consider

giving rise to

the value of the policy at each time. On the other hand, we can look at the performance of from the contract start to the time pension payments start . If average returns are too low we can cede some of the liabilities to the reinsurer by purchasing a (stochastic) endowment (re)insurance in a similar fashion as in Section 4.4, which pays of the value of the pension at time , that is the following (stochastic) endowment

The value of this endowment (re)insurance is thus given by

The above conditional expectation is rather involved. This example shows why the PDE derived in Theorem 3.2 may be useful when looking at policies with stochastic payments where explicit expressions cannot directly be obtained. The reserve is a function of three variables: time , level of return and level of the average return . It satisfies the following PDE

where is the differential operator in (3.15). The terminal condition is given by

Here, is a function of two variables where again, is time, is the level of the return and it satisfies the following PDE

with terminal condition .

References

- [1] Bacinello, A.R., Ortu, F. (1993). Pricing Guaranteed Securities-linked Life Insurance under Interest Rate Risk. In proceedings from AFIR (Actuarial Approach for Financial Risks) 3rd International Colloquium, Rome, Italy, volume 1, pages 35–55.

- [2] Bacinello, A.R., Ortu, F. (1993). Single an Periodic Premiums for Guaranteed Equity-Linked Life Insurance under Interst Rate Risk: The "Lognormal + Vacisek" Case. In Peccati L. and M. Viren editors, Financial Modelling, pages 1–25. Physica-Verlag, Heidelberg, Germany.

- [3] Bacinello, A. R., Persson, S. A. (2000) Design and Pricing of Equity-Linked Life Insurance Under Stochastic Interest Rates. Available at SSRN: https://ssrn.com/abstract=276701 or http://dx.doi.org/10.2139/ssrn.276701

- [4] Baños, D. R., Lagunas-Merino, M., Ortiz-Latorre, S. (2020) Variance and Interest Rate Risk in Unit-Linked Insurance Policies. Risks 8(3), 84.

- [5] Evans, L. Partial Differential Equations. American Mathematical Society. 2nd edition. 2010.

- [6] Koller, M. Stochastic Models in Life Insurance. Springer-Verlag Berlin Heidelberg. Ed. 1. 2012.

- [7] Kurtz, A. (1996). Pricing of Equity-linked Life Insurance Policies with an Asset Value Guarantee and Periodic Premiums. In proceedings from AFIR (Actuarial Approach for Financial Risks) 6th International Colloquium, Nürnberg, Germany, volume 2, pages 1485–1496.

- [8] Nielsen, J.A., Sandmann, K., (1995). Equity-linked life insurance: a model with stochastic interest rates. Insurance: Mathematics and Economics 16, 225–253.

- [9] Nielsen, J.A., Sandmann, K., (1996). Uniqueness of the Fair Premium for Equity-Linked Life Insurance Contracts. The Geneva Risk and Insurance Review 21(1), 65–102.

- [10] Norberg, R., Møller, C. M. (1996). Thiele’s Differential Equation with Stochastic Interest Rate of Diffusion Type. Scand. Actuarial J. 1, 37–49.

- [11] Persson, S. A. (1998). Stochastic Interest Rate in Life Insurance: The Principle of Equivalence Revisited. Scand. Actuarial J. 2, 97–112.

- [12] Steffensen, M. (2000). A no arbitrage approach to Thiele’s differential equation. Insurance: Mathematics and Economics 27, 201–214.