Growth, development, and structural change at the firm-level: The example of the PR China

Abstract

Understanding the microeconomic details of technological catch-up processes offers great potential for informing both innovation economics and development policy. We study the economic transition of the PR China from an agrarian country to a high-tech economy as one example for such a case. It is clear from past literature that rapidly rising productivity levels played a crucial role. However, the distribution of labor productivity in Chinese firms has not been comprehensively investigated and it remains an open question if this can be used to guide economic development. We analyze labor productivity and the dynamic change of labor productivity in firm-level data for the years 1998-2013 from the Chinese Industrial Enterprise Database. We demonstrate that both variables are conveniently modeled as Lévy alpha-stable distributions, provide parameter estimates and analyze dynamic changes to this distribution. We find that the productivity gains were not due to super-star firms, but due to a systematic shift of the entire distribution with otherwise mostly unchanged characteristics. We also found an emerging right-skew in the distribution of labor productivity change. While there are significant differences between the 31 provinces and autonomous regions of the P.R. China, we also show that there are systematic relations between micro-level and province-level variables. We conclude with some implications of these findings for development policy.

1 Introduction

For almost three decades, the PR China has been one of the fastest-growing economies. During this time, it made the transition from a largely agricultural developing country to the world’s second-largest industrial economy. Where state-owned enterprises (SOEs) ran the show in the 1980s, the country today is home to a multitude of private corporations of international importance. The PR China used to be a poor country and years behind in technological terms, but today, its development trajectory is of growing importance for the world in science and innovation, in CO2 emissions, and in technological impact on privacy, surveillance, and personal freedom. While the development is moderately well-understood in macro-economic terms, many open questions remain with regard to the development of the microstructure of the Chinese economy over the last decades. Which firms were the most productive ones, which were central to the transition process? How was productivity distributed among firms? How did this change over time? Can these processes be observed in all regions? In all sectors? Is it mirrored in profitability and investment rates? Can other developing economies achieve the same level of growth and development?

For developed countries, the distributions of firm-level data have been widely investigated and discussed in the literature. Many stylized facts are known although some questions remain contested. Ijiri and Simon (1964, 1977) proposed that firm sizes are highly skewed and follow Pareto distributions, essentially with a process following Gibrat’s law111Gibrat’s law with lower bound produces Pareto distributions; without such bound, it generates lognormal distributions (Mitzenmacher, 2004). as the root cause of this. The observation was later confirmed with more detailed data sets (Axtell, 2001; Gaffeo et al., 2003), although some of the literature prefers to model the distribution as a lognormal (Cabral and Mata, 2003) and other generating algorithms have been proposed ((Heinrich and Dai, 2016) offer an overview). It is clear that this has important policy implications for competition law, innovation policy, labor market governance, and the effectiveness of policy interventions in industrial organization. Connections to firm growth, innovation, and technological change (Yu et al., 2015; Li and Rama, 2015) further add to the importance of this distributional approach, as do the later, but equally important investigations of the distributions of firm growth rates (Bottazzi and Secchi, 2006) and productivities (Yang et al., 2019).

An important characteristic of firm-level distributions in developed countries is that no significant changes are observed with either time (Yang et al., 2019) or firm age (Cabral and Mata, 2003). Developing countries, however, may be very different. They are subject to substantial and rapid changes in sectoral structure, technology, economic policy, and social organization. Investigating such distributional changes for developing economies may shed light on the mechanisms driving that development, the effectiveness of policy measures, the microstructural impact of technological change, as well as potentially the history of developed countries. Studying similar historical processes for developed countries would require older data that is almost certainly not available in high resolution.

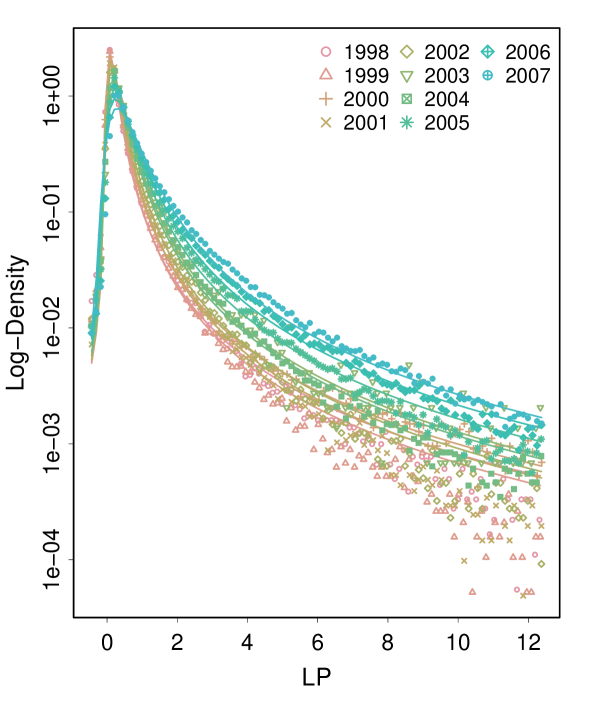

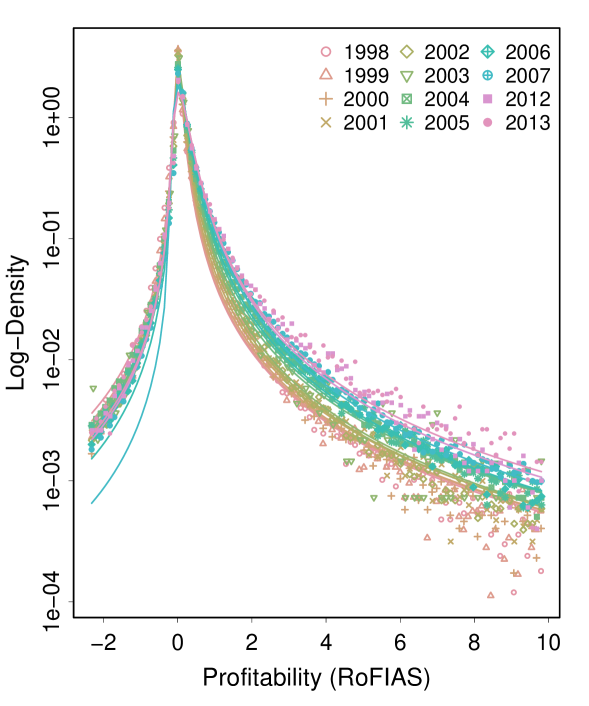

For the PR China a look at the data immediately suggests that a systematic shift is underway: Figure 1 shows the distribution (density) function of the labor productivity at the firm-level by year in a semi-log plot (horizontal axis linear, vertical axis logarithmic); the shape of the distribution remains constant, but the right side (positive tail) moves outward and the peak becomes less pronounced. We will discuss other systematic shifts, interpretations, and implications below (see Section 5); for now, we emphasize that there are systematic changes in the distributional model during this development phase of the Chinese economy.

We use a firm-level data set for the PR China for the years 1998-2013 to investigate changes in the economic microstructure during the years of China’s most rapid growth from a distributional model perspective. We will focus on the distribution of labor productivity and of labor productivity change; these are arguably the quantities that are most closely related to economic development. While other distributional models have been suggested for labor productivity (Yu et al. (2015) consider Asymmetric Exponential Power (AEP) distributions and Gaussian normal distributions), the mounting evidence for heavy tails in both labor productivity and labor productivity change (Yang et al., 2019) suggests the Lévy alpha-stable distribution (Nolan, 1998, 2019) as a distributional model. Lévy alpha-stable distributions generalize Gaussian normal distributions,222For one particular parameter setting, the Lévy alpha-stable converges to a Gaussian normal distribution. but have heavy tails for almost all parameter values.

Important consequences include that the apparent dispersion of labor productivity (Berlingieri et al., 2017) depends on how dispersion is measured. If such dispersion exists, it may be an indicator for misallocation of labor, capital, or other resources, a question of considerable relevance for the economy of the PR China (Hsieh and Klenow, 2009). It also relates to the debate on granular origins of aggregate fluctuations (Gabaix, 2011; Schwarzkopf et al., 2010) and the question of how characteristics of labor productivity distributions in firm populations should be quantified and interpreted. The characteristics of labor productivity dispersion measures and the consequences for these economic questions are studied comprehensively in Yang et al. (2019).

We demonstrate that labor productivity as well as labor productivity change and various other firm-level characteristics in the PR China are indeed fat-tailed with infinite variance. Further, we show that the Lévy alpha-stable distribution is an excellent fit and discuss how the characteristics of the distribution can be specified and tracked using the parameters of the Lévy alpha-stable fit. We discuss the emerging temporal and regional patterns as well as the behavior in other subsamples. Finally, we demonstrate connections between the distributions of labor productivity, labor productivity change, profitability, investment rate at the firm-level, as well as between these firm-level patterns and aggregated level data.

The paper is organized as follows: The literature on the development of productivity in the PR China during its period of rapid growth is reviewed in Section 2. Section 3 describes the data and the variables of interest. Section 4 discusses the distributional models that are tested, the Lévy alpha-stable and the Asymmetric Exponential Power, as well as the fitting procedure, and goodness of fit measures employed. Section 5 presents the findings and corresponding interpretations. Section 6 concludes.

2 Literature

The present paper aims to contribute to the study of distributional models of firm-level data, the investigation of the role of firm productivity in economic development, and, more specifically, the analysis of the rapid growth and development of the P.R. China in recent decades. We, therefore, give brief overviews of the literature in these three fields.

2.1 Distributional models of firm-level data

For developed countries, it has been established that the distributions of firm sizes, sales, etc. are heavily skewed (Ijiri and Simon, 1964; Axtell, 2001), with the Pareto (Axtell, 2001) and the lognormal distribution being proposed as distributional models (Cabral and Mata, 2003). The two-sided distributions of growth rates and productivities equally have much heavier tails than normal distributions; proposed distributional models include Asymmetric Exponential Power distributions for growth rates (Bottazzi and Secchi, 2006; Bottazzi et al., 2007; Bottazzi and Secchi, 2011) and Lévy alpha-stable distributions for productivities (Yang et al., 2019).

However, developed economies are relatively static. Very little change has been observed in these distributions over the recent decades for which good data is available (see e.g. (Yang et al., 2019)), and little change would be expected. To understand the development of firm-level distributions, scholars have instead focussed on firms of different age groups, their survival, and their shifts over time (Cabral and Mata, 2003). Important findings include that the form of the distribution does not change over time (Yang et al., 2019) or with age (Cabral and Mata, 2003; Angelini and Generale, 2008), that surviving firms are slightly larger (Cabral and Mata, 2003), and that they increase their productivity (making within-firm productivity gains important at the aggregate level) (Bartelsman et al., 2013; Li and Rama, 2015). Cabral and Mata (2003) report that surviving firms in a Portuguese data set have less long tails and lower skew; however, if the statistical process which the firm size follows in reality is heavy-tailed with low exponents333This is indeed indicated by empirical studies (Gaffeo et al., 2003; Fujimoto et al., 2011; Heinrich and Dai, 2016) that find tail exponents around or between and for firm size depending on how firm size is measured., these moments may not exist and Cabral and Mata’s findings may be statistical artifacts (Yang et al., 2019). The hypothesis that small firms are more dynamic and account for significant shares of productivity gains and newly created jobs has frequently been proposed, but remains controversial (Li and Rama, 2015).

2.2 Economic development and firm-level productivity

Comprehensive firm-level data is often not available for developing countries. In turn, many studies have to work with small and potentially biased sample sizes. Notable exceptions are studies of firms in the P.R. China - using the Chinese Industrial Enterprise Database that we also work with - and in India - using government census data. While the general distributional forms found for developed countries are confirmed (Hsieh and Klenow, 2009; Ma et al., 2008; Zhang et al., 2009; Coad and Tamvada, 2012; Sun and Zhang, 2012; Yu et al., 2015; Ding et al., 2016; Heinrich and Dai, 2016), wider dispersions for productivities are reported for India and China specifically (Hsieh and Klenow, 2009).

In a general equilibrium interpretation, productivities should equalize, as investors should prefer high productivities while low productivity firms should be frozen out. This should be especially true for firms in the same sector and region, since portfolio diversification should not constitute a reason to invest in low productivity establishments. Of course, there may be structural reasons why investment in low productivity firms persists; and it might not be easily observable to investors. However, implications could still be drawn in comparative analyses, if different dispersions are observed. Hsieh and Klenow (2009) choose to follow this equilibrium interpretation; their contribution has led to the influential interpretation that resources are more misallocated in developing countries (Hsieh and Klenow, 2009; Song et al., 2011; Bartelsman et al., 2013; Li and Rama, 2015; Goyette and Gallipoli, 2015) as well as occasionally strongly worded policy recommendations (Adamopoulos and Restuccia, 2014; Poschke, 2018). This has been explained with both structural factors, such as constraints on credit availability (Bloom et al., 2010; Cabral and Mata, 2003), and also internal factors of the firm population of developing countries, such as bad management and reluctance to delegate decision-making (Bloom et al., 2010; Chaffai et al., 2012). More recently, it has been found that productivities (both labor productivity and total factor productivity, TFP) are heavy-tailed with tail exponents below such that most dispersion measures, including the ones used in this line of research, are not meaningful (Yang et al., 2019).

The source of productivity gains is an important question in the study of economic development. Three main causes are (1) within-firm improvements, (2) selection pressure (unproductive firms do not survive), and (3) changes from distributional differences between entrants and exiting firms. Within-firm improvements were particularly important in developing countries (Li and Rama, 2015) and in successful developing economies such as China (Yu et al., 2015, 2017). While developed countries show some component from selection (2) and entry/exit (3) (Fariñas and Ruano, 2004; Li and Rama, 2015)444Studies also found a counter-cyclical contribution of entry and exit in developed economies (Spain): In phases of economic growth, when credit is readily available, less productive firms enter, resulting in a negative contribution to productivity growth (Fariñas and Ruano, 2004)., in some developing countries (Sub-Saharan Africa specifically) the entry-exit-process may come down to churning without any improvements, and firms may survive because they are born larger, not because they learn or improve (Van Biesebroeck, 2005; Li and Rama, 2015; Goyette and Gallipoli, 2015), resulting in heteroskedastic ”missing middle“ distributions (Van Biesebroeck, 2005).

Success and growth at the firm-level has been linked to innovation for Argentina (Chudnovsky et al., 2006), to innovation and technological competence for Indian firms (Coad and Tamvada, 2012), and export participation for Chilean, Chinese, and European firms (Volpe Martincus and Carballo, 2010; di Giovanni et al., 2011; Sun and Zhang, 2012).

Finally, systematic shifts in distributions have been shown for those developing countries that undergo rapid growth: Both Yu et al. (2015, 2017) and Ding et al. (2016) find a location shift in the productivity distributions (labor productivity and TFP respectively) for China in the 1990s and 2000s, indicating higher productivities across the entire firm population, while the functional form did not change. Nguyen (2019) finds a similar location shift in firm-level distributions for Vietnam. Heinrich and Dai (2016), studying the firm size distribution in Chinese provinces, find higher tail exponents in regions with high GDP per capita or high growth.

2.3 Firm-level productivity and growth in the PR China

Chinese firm-level distributions follow the same general patterns found elsewhere (Ma et al., 2008; Yu et al., 2015; Heinrich and Dai, 2016; Heinrich et al., 2020). While firm sizes seem to follow power laws (Ma et al., 2008; Heinrich and Dai, 2016), for labor productivities and growth rates, two distributions have been suggested: Asymmetric Exponential Power distributions from the exponential distribution family (Yu et al., 2015) were found to be a much better fit than Gaussians. Lévy alpha-stable distributions, which have power-law tails on both sides, have been suggested as an alternative since the data seems to be heavy-tailed (Heinrich et al., 2020). The distinction has important consequences.

The impressive economic growth of the PR China is reflected in the distributions as a location shift in productivity levels (Yu et al., 2015, 2017; Ding et al., 2016); the shift remains present in the gross industrial output per worker (labor productivity per wage), indicating that productivity has grown at a faster pace than labor inputs (Zhang and Liu, 2013). It is important to note that this is not a changing average, but a shift of the entire distribution which otherwise remains intact in spite of continuing entry and exit processes. The changes in the distribution’s parameters have so far not been comprehensively studied.

We give a brief overview over the contributing factors to China’s rapid growth from a historical perspective in Appendix C.

It this worthwhile to note that state-owned enterprises (SOEs) have been found to be in general less productive than privately owned firms, both in terms of average labor productivity and average TFP (Song et al., 2011; Yu et al., 2015; Hsieh and Song, 2015). While productivities of firms of all types vary widely and follow similar distributional forms as the economy as a whole (see Section 5), the mean difference is significant. SOE productivity did improve and has converged towards the productivity levels of private firms until at least 2007, but a gap in average productivity remains (Song et al., 2011; Yu et al., 2015). Boeing et al. (2016) find that compared to private firms, SOEs are less successful in converting patents into productivity improvements, although a generally positive relationship of productivity and R&D efforts does exist (Hu and Jefferson, 2004; Boeing et al., 2016). SOEs are often seen as a source of misallocation, thereby explaining their lower average productivity and tying the finding to the misallocation hypothesis (Hsieh and Klenow, 2009; Song et al., 2011). However, on the one hand, a closer look at the distributions reveals that the variation is still present within ownership type groups. On the other, firm-level dispersion may not be larger in China than in other countries if the measures employed in achieving these results were misleading for heavy-tailed data (Yang et al., 2019). The reason why SOEs are catching up and the mean difference between private firms and SOEs is converging is typically seen in the structural transformation of the state sector (Hsieh and Song, 2015; Jefferson et al., 2000). Greater flexibility of managers and delegation of decision-making capabilities as well as and the effects of rising incomes and autonomy on employee motivation have also been linked to the productivity improvements in SOEs (Groves et al., 1994).

Finally, regional disparities in productivity and other variables are well-known and expected for a country of the size of the PR China. Coastal provinces like Shanghai and Guangdong have a better TFP comparing with central and western provinces (Ding et al., 2016; Chen et al., 2009). High productivity firms prefer to concentrate their activities on regions with developed infrastructure, good universities, and related industrial clusters; Zhu et al. (2019) finds evidence for both sorting and adverse sorting effects. Meanwhile, officials in undeveloped regions are eager to attract investment by providing subsidies. However, government subsidies may attract low-productivity firms, since they have low opportunity costs (Zhu et al., 2019). Marshall and Jacobs externalities of spatial industrial agglomerations (Beaudry and Schiffauerova, 2009) likely also play a role in creating and maintaining regional disparities, as may the openness of regions towards outside influences, foreign trade, and flexible economic policy (Jiang, 2011).

3 Data

3.1 Sources

We use firm-level data from the Chinese Industrial Enterprise Database (CIEDB), which records several hundreds of thousands of firms each year for the time period between 1998 and 2013 and is commonly used by researchers working on firm-level data in China (Brandt et al., 2012; Hsieh and Song, 2015; Ding et al., 2016; Yu et al., 2015, 2017). The data ultimately derive from data recorded by the PR China’s National Bureau of Statistics. Similar to data provided by the Bureau van Dijk for Europe (ORBIS Europe), the CIEDB records data at the firm-level, not at the level of physical entities (plants). This facilitates investigating structural characteristics such as productivity and profitability at the firm-level, the level at which decision making and management take place. Different from other databases like COMPUSTAT or Bloomberg, but similar to ORBIS Europe, the CIEDB also includes small and medium-sized firms and thus provides better coverage of different types of enterprises. The data set also records the ownership type (state-owned, foreign-owned, private, etc.)555The database does not include firms from Hong Kong, Macau, and Taiwan, we, therefore, will not cover these three regions in the analysis..

There are some notable difficulties with the data, especially for the period after 2008. These difficulties are well-known and recognized in the literature (Brandt et al., 2014). Brandt et al. (2014) qualify the samples after 2008 as unreliable and recommend working with the more reliable date up to 2008 only. We largely follow this strategy. We complement this with later data from the period 2009-2013, where possible, to shed light on some developments after 2008.

Up to 2008, the database includes industrial firms with revenues above million Yuan. From 2009, only firms with revenues beyond million Yuan are present in the data set. The set of recorded variables also changes significantly over this time period. For instance, we are unable to compute value-added and productivities for the time period after 2008, as the measures required for their computation are only reported up until 2007.

In addition, we use industry level deflators from and macroeconomic data at province level from China Compendium of Statistics (1949-2008).

3.2 Data processing

We extract variables on identity666Ownership reforms led to continuous legal and structural changes, making it difficult to consistently identify the same firm (Jefferson et al., 2000). Using not just the firm ID but also phone number and ZIP code for identification is a typical way to address this (Brandt et al., 2014). (ID, phone number, ZIP code), characteristics (founding year, primary sector, ownership type), and structural and financial condition (output, assets, profits, wages, employment, intermediate input). These variables are present in the database throughout the years 1998-2007.777For 2003, the number of complete observations is very small. Progressively more variables either missing or reported in substantially different form starting in 2008. (See Table 1.) The monetary variables are deflated using industry level deflators.

We remove duplicates in terms of ID and Year before commencing with the data analysis.

In order to observe productivity changes, we attempt to identify firms that are present over multiple years both directly (using the unique ID) and indirectly, using phone numbers and address details as suggested in Brandt et al. (2014).

For the analysis of regional variation, the firms are assigned to the region of their postal address. As the region name is not typically part of the postal address, the ZIP codes were used to identify those regions.

| Year | Labor productivity | Labor productivity change | Labor productivity growth | Labor productivity (imputed) | Profitability | Investment rate |

| 1998 | 141,790 | - | - | 141,787 | 149,270 | - |

| 1999 | 148,982 | 113,684 | 112,996 | 148,973 | 147,636 | 121,091 |

| 2000 | 147,196 | 121,977 | 120,882 | 147,188 | 148,088 | 123,492 |

| 2001 | 158,671 | 116,674 | 116,001 | 158,664 | 157,453 | 119,211 |

| 2002 | 169,419 | 139,020 | 138,351 | 169,417 | 168,072 | 137,724 |

| 2003 | 11,404 | 9,503 | 9,490 | 11,404 | 11,369 | 9,461 |

| 2004 | 267,898 | 120,595 | 120,174 | 267,898 | 263,060 | 118,202 |

| 2005 | 262,830 | 227,569 | 227,032 | 262,830 | 261,369 | 223,671 |

| 2006 | 290,762 | 244,918 | 244,406 | 290,762 | 289,566 | 243,448 |

| 2007 | 324,638 | 268,614 | 268,376 | 324,638 | 323,131 | 267,151 |

| 2008 | - | - | - | - | 198,945 | 158,114 |

| 2009 | - | - | - | - | - | 130,155 |

| 2010 | - | - | - | - | - | 152,979 |

| 2011 | - | - | - | - | - | - |

| 2012 | - | - | - | 42,301 | - | 36,139 |

| 2013 | - | - | - | 41,625 | 216,817 | 180,634 |

3.3 Variables

In order to investigate structural change at the firm-level, we analyze labor productivity and its dispersion and dynamical change. Labor productivity has been conjectured to hold information about the firm’s capabilities, economic potential, and growth prospects. Its dynamical change facilitates investigating to what extent this potential is persistent in time. The dispersion of both variables holds information on the structural composition of the firm population of the country, the region, or the industry.

Labor productivity is defined as value-added per employee.

where indicates the firms and is the time. As the value-added is not part of the database, it has to be computed as the difference between output and intermediate input.

where is output and stands for intermediate input of firm at time . Alternatively, can be imputed as the sum of paid wages and profits

Imputed value-added differs from the direct computation in that reinvestments cannot be distinguished from negative profits and remain part of the resulting quantity. Reinvestments can be substantial and may occur in systematic patterns across the firm population.

To observe the dynamic development of labor productivities, we compute the labor productivity change by firm

An alternative choice would be labor productivity growth

However, as this is a growth rate, it has a singularity at . Changes in labor productivity in the vicinity of the singularity get grotesquely exaggerated. What is more, may be zero (in 1% of the observations) or negative (3% of the observations) since stocks and price changes are allowed.888Typically, output should be larger than intermediate inputs, . However, both are measured in monetary units, so whether is subject to price changes. Further, the firm may maintain, built up, or reduce stocks intertemporarily. For this reason, we refrain from using the growth rate and rely on the absolute change as our main indicator of the dynamical change of labor productivities.

The distributional models for these variables will be investigated in Section 5.1. It will be shown that this has important consequences for the selection and interpretation of quantitative measures for productivity dispersion. We complement the analysis of labor productivity with the study of the behavior of and dispersion of two more variables: Return on capital will serve as an indicator for the firms’ profitability from the perspective of investors. The investment rate is studied to assess investment patterns and growth. These variables are computed as

where are the profits and is the capital stock (fixed assets) of firm at time .

The number of observations for all variables by year is given in Table 1.

Additional analyses also use capital intensity, defined as:

4 Methods

4.1 Distributional models

Most studies of labor productivity and of firm-level data, in general, are based on generative models. They define, which effects on the measure under investigation are considered under the model; they fix their functional forms; and they establish the resulting distribution. Typically, the approximate form of the distribution to be explained is known, which constrains the variety of candidate models.

The advantages of the generative approach include that it is illustrative and verifiable by considering other quantities represented in the model. However, specific distributions can frequently be generated by large numbers of different generative models, and matching the correct distribution reveals little information about the correct generating process.

Instead, and in line with much of the modern literature (Frank, 2009; Bottazzi and Secchi, 2006; Yang, 2018; Yang et al., 2019), we consider a different approach: The attractor distribution to which the result of aggregations of (identical, independent) distributions converges. We remain agnostic with regard to the interpretation of the component distributions being aggregated, though temporal aggregation of shocks or aggregation across jobs, processes, or tasks within a firm are natural component separations that suggest themselves. If it is indeed the correct representation of the data, the distribution could be expected to remain stable under a number of changes to the system, as the aggregation continues to converge to this functional form.

In particular, following Yang et al. (2019), we use the Lévy alpha-stable distribution (Nolan, 2019, 1998) as our main distributional model, although we provide fits to the 4-parameter Asymmetric Exponential Power distribution suggested elsewhere in the literature (Bottazzi and Secchi, 2006; Bottazzi et al., 2007; Bottazzi and Secchi, 2011; Yu et al., 2015) as a point of comparison. In the following, we provide a non-technical explanation and some intuition why the Lévy alpha-stable distribution may be a good distributional model. A technical description is given in the Appendix A.

Random variables distributions can be aggregated in convolutions (i.e. summation of the variables), which yields a different distribution of the results (for technical details, see Appendix A.1). Aggregation leads to a loss of information; it washes out less strong signals and only a dominant pattern remains. As the convoluted distributions are independent, this pattern is the one that carries the least information (highest entropy), the one that is the most likely one without additional information, the one that constitutes the maximum entropy distribution under constraints that depend on the component distributions .

The maximum entropy perspective may be helpful in that it allows computing the resulting distribution and understanding the type of its constraints in a concise way. The resulting distributional form is determined by the constraints in the maximum entropy perspective, or equivalently by the type of convolution and the characteristics of the component distributions in the convolution perspective. For instance, a single constraint on the mean of the distribution will yield an exponential or Laplacian (two-sided exponential) maximum entropy distribution. The Asymmetric Exponential Power distributions that are often used for the distributional models for firm growth (Bottazzi and Secchi, 2006; Bottazzi et al., 2007; Bottazzi and Secchi, 2011) or productivity (Yu et al., 2015), belong to this family, albeit with a modification that allows for asymmetry999The maximum entropy constraint includes a sign function under this modification to distinguish the two tails and account for different shapes of both sides. (for technical details, see Appendix A.5). A single constraint on the mean of the distribution under logarithmic transformation will yield a Pareto maximum entropy distribution, typically considered for distributional models of firm size distributions. A constraint on the variance of a distribution (implying a second constraint on the mean) will yield a Gaussian normal maximum entropy distribution.

Almost all maximum entropy distributions do not constitute attractors under further aggregation. If the resulting distribution is further convoluted, it continues to change. Those that do constitute attractors, i.e. those that yield an identical distribution under convolution are known as Lévy alpha-stable distributions (for technical details, see Appendix A.4). The Lévy alpha-stable is a generalization of several families of distributions, including Gaussian normal distributions, Cauchy, distributions and Lévy distributions. The generalized central limit theorem (GCLT) states that any sum of independent, identical distributions will converge to a Lévy alpha-stable distribution. Specifically, if the convoluted distributions have a finite variance, the sum will converge to a Gaussian normal, a member of the family of Lévy alpha-stable distributions (for technical details, see Appendix A.2). If not, it will yield a different member of this family with a heavy tail and a tail parameter .

Lévy alpha-stable distributions do not have a closed-form representation as a function in the frequency domain, except for special parameter sets.101010For it yields a Gaussian normal distribution, for , it yields a Cauchy distribution, and for it yields a Lévy distribution. The functional form in the Fourier domain (the characteristic function, for technical details, see Appendix A.3) is

| (1) |

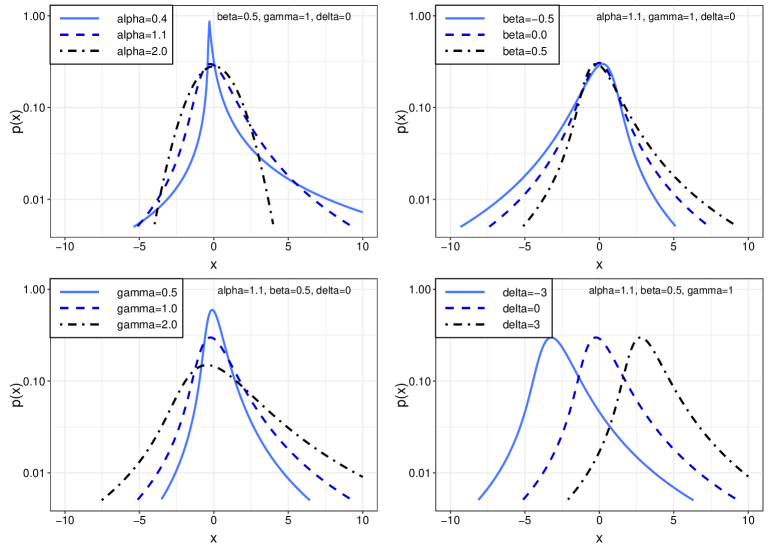

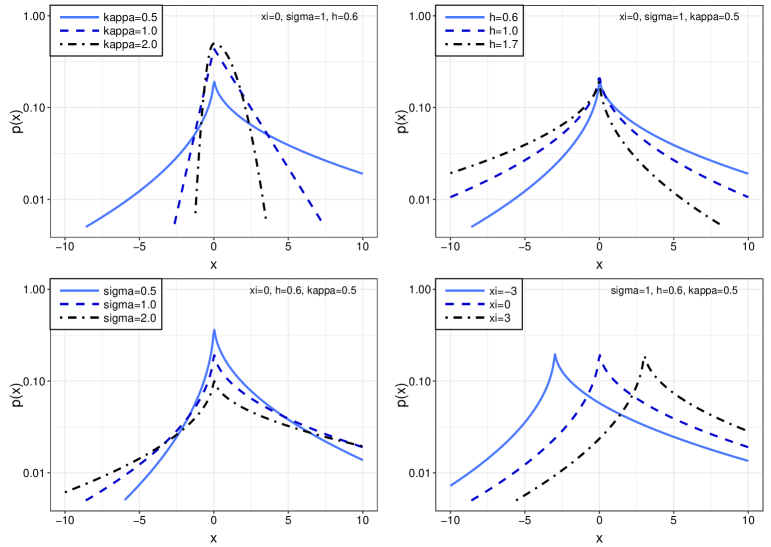

Figure 2 shows the bahaviour of the four parameters of the Lévy alpha-stable distribution in semi-log scale (y-axis logarithmic). The upper left panel contrasts the Gaussian case (black curve) with skewed fat-tailed cases for different tail indices . Note that the curve bends outward for the two fat-tailed cases, indicating that the tails are heavier than in an exponential distribution, which would be linear in a semi-log scale. This is a tell-tale sign of fat-tailedness. The lower left panel shows variations of the scale or width of the distribution. The scale, is another measure of dispersion besides the tail index and is independent from it. In the Gaussian case (), the scale is simply the standard deviation. For fat-tailed variants () such as the ones depicted in this panel, this is not the case, as the standard deviation is infinite. The right panels demonstrate different skew values and a location shift respectively.

4.2 Fitting

4.2.1 Lévy alpha-stable distributions

We use Nolan’s (Nolan, 1998, 2019) parametrization for the Lévy alpha-stable distribution as given in equation 1. Common methods to fit the distribution include maximum likelihood, the general method of moments (GMM), and McCulloch’s (McCulloch, 1986) quantile based estimation. Maximum likelihood is generally considered the most reliable, but requires much more computation power than the alternatives and is, for the data sizes considered here, not practical. A direct comparison of McCulloch’s method with GMM111111For this comparison, we used Hansen’s (1982) two-step algorithm with Carrasco et al.’s (2007) spectral cut-off regularization. showed that for the relevant data sizes of at least , , and (depending on the type of the subsample, see Section 3) observations each as considered here, McCulloch’s quantile-based estimation is more accurate and gives generally better Soofi ID scores (see Section4.3.1).

We use the R package StableEstim (Kharrat and Boshnakov, 2016).

4.2.2 Asymmetric exponential power (AEP) distributions

Contrasting our distributional model to AEP distributions is expedient not only because it has been suggested as a distributional model in the literature (Bottazzi and Secchi, 2006; Bottazzi et al., 2007; Bottazzi and Secchi, 2011; Yu et al., 2015), but also because AEP distributions show radically different tail behavior compared to Lévy alpha-stable distributions, which are heavy-tailed and have infinite variance for . While finite samples always have a finite variance, it will diverge in the sample size if the underlying distribution of the sample is heavy-tailed. As a result, measuring the variance of a sample from a heavy-tailed distribution will yield misleading results (Nolan, 2019; Emberchts et al., 1997; Yang et al., 2019), as they are tainted by other quantities such as the sample size. Similar problems exist for other dispersion measures (Yang et al., 2019). Performing OLS correlations on variables with hevy tails will likely also fail, since the error distribution will likely inherit the heavy tails and OLS requires errors with finite variance. For technical details, see Appendix A.6.

4.3 Goodness of fit

Two measures for model selection and validation are used, both based on information theory considerations. Additional techniques, such as the Kolmogorov-Smirnov test121212The KS test is known to have low precision and to lead to many false negatives. or cross-validation are possible, but were not applied in the present study.

4.3.1 Soofi ID index

Our main goodness-of-fit metric is based on Soofi et al.’s (Soofi et al., 1995) information distinguishability () concept, which gives the distinguishability of two distributions based on their information content. We can use this measure to assess to what extent a fitted model with parameters is distinguishable from the entropy maximizing distribution given a set of observations .

Formally, is based on the Kullback-Leibler divergence between the two distributions

where is the divergence operator.131313I.e., for any concept of divergence, is the divergence of and ; is the divergence of and given . Information distinguishability is defined as

| (2) |

and has support . indicates that the distributions are indistinguishable, while the differences are more pronounced the higher . For convenience, we construct a Soofi ID score as previously used by Yang (2018); Yang et al. (2019) by rescaling

| (3) |

with support such that indicates a perfect match while low values indicate that the distributional model under investigation is probably not correct for the sample in question.

4.3.2 Akaike information criterion (AIC)

Akaike’s (Akaike, 1973) information criterion (AIC) is based on the likelihood of a distributional model fit while accounting for the number of parameters. Formally,

| (4) |

where is the likelihood function of parameters given data and is the number of estimated parameters .

The AIC relies on the same concepts as the , namely minimizing Kullback-Leibler divergence, but rescales differently and applies a correction for . It offers a measure for model comparison, but is difficult to interpret in illustrative terms. , on the other hand, has a straight forward interpretation as the extent of similarity with an entropy maximizing model given the data.

| Year | Obs. | Lévy alpha-stable fit | AEP fit | |||||||

| LP | 1998 | 140,372 | 1.00 | 0.95 | 0.11 | 0.11 | 0.47 | 0.40 | 0.01 | 0.06 |

| 1999 | 147,492 | 1.06 | 0.95 | 0.12 | 0.13 | 0.45 | 0.46 | 0.02 | 0.07 | |

| 2000 | 145,724 | 0.97 | 0.95 | 0.14 | 0.14 | 0.42 | 0.27 | 0.00 | 0.10 | |

| 2001 | 157,083 | 1.08 | 0.95 | 0.15 | 0.18 | 0.42 | 0.48 | 0.02 | 0.10 | |

| 2002 | 167,723 | 1.08 | 0.95 | 0.17 | 0.20 | 0.44 | 0.48 | 0.03 | 0.12 | |

| 2003 | 11,288 | 1.04 | 0.95 | 0.21 | 0.28 | 0.43 | 0.40 | 0.02 | 0.18 | |

| 2004 | 265,218 | 1.06 | 0.95 | 0.20 | 0.25 | 0.42 | 0.45 | 0.03 | 0.15 | |

| 2005 | 260,200 | 1.03 | 0.95 | 0.25 | 0.30 | 0.40 | 0.45 | 0.03 | 0.17 | |

| 2006 | 287,854 | 1.00 | 0.95 | 0.30 | 0.36 | 0.37 | 0.43 | 0.03 | 0.21 | |

| 2007 | 321,390 | 0.99 | 0.95 | 0.36 | 0.43 | 0.36 | 0.43 | 0.03 | 0.24 | |

| 1999 | 112,546 | 0.96 | -0.05 | 0.08 | 0.01 | 1.07 | 0.34 | 0.00 | 0.02 | |

| 2000 | 120,757 | 0.90 | 0.25 | 0.09 | -0.00 | 0.72 | 0.22 | 0.00 | -0.04 | |

| 2001 | 115,506 | 0.93 | -0.11 | 0.10 | 0.01 | 1.28 | 0.24 | 0.00 | 0.07 | |

| 2002 | 137,628 | 0.99 | 0.12 | 0.11 | 0.01 | 0.92 | 0.41 | 0.02 | 0.01 | |

| 2003 | 9,407 | 0.97 | 0.14 | 0.13 | 0.01 | 0.90 | 0.38 | 0.01 | 0.00 | |

| 2004 | 119,389 | 1.03 | 0.20 | 0.18 | 0.02 | 0.86 | 0.42 | 0.03 | 0.00 | |

| 2005 | 225,293 | 1.01 | 0.26 | 0.19 | 0.04 | 0.84 | 0.42 | 0.03 | 0.02 | |

| 2006 | 242,468 | 0.99 | 0.29 | 0.20 | 0.05 | 0.81 | 0.40 | 0.03 | 0.02 | |

| 2007 | 265,926 | 0.99 | 0.25 | 0.25 | 0.06 | 0.84 | 0.40 | 0.03 | 0.04 | |

| 1998 | 136,435 | 0.91 | 0.37 | 0.08 | 0.00 | 0.73 | 0.34 | 0.00 | -0.01 | |

| 1999 | 145,513 | 0.91 | 0.44 | 0.07 | 0.00 | 0.69 | 0.34 | 0.00 | -0.01 | |

| 2000 | 141,570 | 0.93 | 0.51 | 0.08 | 0.01 | 0.67 | 0.34 | 0.00 | -0.00 | |

| 2001 | 155,527 | 0.93 | 0.55 | 0.09 | 0.02 | 0.65 | 0.32 | 0.00 | 0.00 | |

| 2002 | 166,246 | 0.98 | 0.61 | 0.10 | 0.03 | 0.64 | 0.34 | 0.00 | 0.01 | |

| 2003 | 11,250 | 1.01 | 0.59 | 0.11 | 0.05 | 0.65 | 0.36 | 0.01 | 0.03 | |

| 2004 | 260,311 | 0.96 | 0.61 | 0.12 | 0.05 | 0.63 | 0.31 | 0.00 | 0.02 | |

| 2005 | 258,741 | 1.00 | 0.69 | 0.14 | 0.06 | 0.59 | 0.35 | 0.01 | 0.02 | |

| 2006 | 286,602 | 1.01 | 0.78 | 0.14 | 0.06 | 0.56 | 0.35 | 0.01 | 0.03 | |

| 2007 | 319,847 | 1.02 | 0.92 | 0.15 | 0.07 | 0.52 | 0.35 | 0.01 | 0.03 | |

| 2012 | 40,840 | 1.00 | 0.75 | 0.18 | 0.09 | 0.55 | 0.36 | 0.01 | 0.03 | |

| 2013 | 40,090 | 0.96 | 0.74 | 0.18 | 0.09 | 0.55 | 0.33 | 0.01 | 0.04 | |

| 1999 | 119,401 | 0.86 | 0.40 | 0.09 | -0.04 | 0.61 | 0.24 | 0.00 | -0.09 | |

| 2000 | 118,108 | 0.86 | 0.40 | 0.09 | -0.06 | 0.61 | 0.25 | 0.00 | -0.12 | |

| 2001 | 117,732 | 0.86 | 0.41 | 0.10 | -0.02 | 0.60 | 0.25 | 0.00 | -0.09 | |

| 2002 | 136,224 | 0.84 | 0.46 | 0.11 | -0.02 | 0.57 | 0.24 | 0.00 | -0.08 | |

| 2003 | 9,362 | 0.93 | 0.58 | 0.13 | -0.05 | 0.53 | 0.23 | 0.00 | -0.10 | |

| 2004 | 116,966 | 0.92 | 0.66 | 0.24 | -0.12 | 0.49 | 0.26 | 0.00 | -0.22 | |

| 2005 | 221,420 | 0.82 | 0.60 | 0.15 | -0.02 | 0.49 | 0.23 | 0.00 | -0.09 | |

| 2006 | 240,962 | 0.87 | 0.58 | 0.14 | -0.03 | 0.53 | 0.25 | 0.00 | -0.09 | |

| 2007 | 264,428 | 0.86 | 0.59 | 0.14 | -0.04 | 0.52 | 0.25 | 0.00 | -0.11 | |

| 2008 | 156,516 | 0.78 | 0.59 | 0.15 | -0.07 | 0.48 | 0.22 | 0.00 | -0.16 | |

| 2009 | 128,846 | 0.87 | 0.56 | 0.18 | 0.02 | 0.53 | 0.25 | 0.00 | -0.07 | |

| 2010 | 151,441 | 0.63 | 0.20 | 0.03 | -0.03 | 0.51 | 0.10 | 0.00 | -0.10 | |

| 2012 | 8,746 | 0.88 | 0.95 | 0.58 | -0.03 | 0.36 | 0.25 | 0.00 | -0.22 | |

| 2013 | 35,452 | 0.86 | 0.55 | 0.11 | -0.05 | 0.54 | 0.22 | 0.00 | -0.10 | |

| Year | Lévy alpha-stable | AEP | Preferred model | |||||

| 1998 | 98.78 | 880.11 | 88.71 | 913.49 | 10.07 | -33.38 | Lévy -s. | |

| 1999 | 98.10 | 803.04 | 93.86 | 845.21 | 4.24 | -42.17 | Lévy -s. | |

| 2000 | 99.76 | 1,249.25 | 99.14 | 1,320.87 | 0.62 | -71.61 | Lévy -s. | |

| 2001 | 98.26 | 797.22 | 94.86 | 843.04 | 3.40 | -45.82 | Lévy -s. | |

| 2002 | 98.43 | 826.50 | 94.88 | 859.14 | 3.55 | -32.64 | Lévy -s. | |

| 2003 | 98.78 | 979.66 | 83.90 | 1,023.38 | 14.88 | -43.72 | Lévy -s. | |

| 2004 | 98.45 | 884.45 | 95.01 | 927.27 | 3.44 | -42.82 | Lévy -s. | |

| 2005 | 97.88 | 923.83 | 94.10 | 975.49 | 3.78 | -51.66 | Lévy -s. | |

| 2006 | 97.49 | 972.51 | 93.41 | 1,025.50 | 4.08 | -52.99 | Lévy -s. | |

| 2007 | 96.75 | 1,012.76 | 95.21 | 1,071.37 | 1.54 | -58.61 | Lévy -s. | |

| 1999 | 99.35 | 914.08 | 95.89 | 937.44 | 3.46 | -23.36 | Lévy -s. | |

| 2000 | 94.48 | 1,322.04 | 94.48 | 1,357.34 | 0.00 | -35.30 | - | |

| 2001 | 97.92 | 1,301.04 | 84.58 | 1,337.90 | 13.34 | -36.87 | Lévy -s. | |

| 2002 | 99.22 | 824.87 | 98.95 | 852.95 | 0.27 | -28.09 | Lévy -s. | |

| 2003 | 98.96 | 901.36 | 98.85 | 931.11 | 0.11 | -29.75 | Lévy -s. | |

| 2004 | 99.12 | 908.20 | 96.55 | 929.40 | 2.57 | -21.20 | Lévy -s. | |

| 2005 | 99.22 | 925.94 | 99.56 | 948.58 | -0.34 | -22.64 | Lévy -s. | |

| 2006 | 99.14 | 965.16 | 99.53 | 989.38 | -0.39 | -24.22 | Lévy -s. | |

| 2007 | 99.24 | 1,003.31 | 99.33 | 1,024.51 | -0.09 | -21.20 | Lévy -s. | |

| 1998 | 92.99 | 919.04 | 96.53 | 960.82 | -3.54 | -41.78 | AEP | |

| 1999 | 98.53 | 899.66 | 91.12 | 934.49 | 7.41 | -34.83 | Lévy -s. | |

| 2000 | 98.86 | 920.60 | 99.79 | 961.19 | -0.93 | -40.60 | even | |

| 2001 | 98.38 | 978.17 | 96.66 | 1,018.65 | 1.72 | -40.48 | Lévy -s. | |

| 2002 | 99.06 | 973.09 | 99.11 | 1,017.00 | -0.05 | -43.92 | even | |

| 2003 | 98.85 | 911.05 | 96.70 | 939.00 | 2.15 | -27.95 | Lévy -s. | |

| 2004 | 99.55 | 1,067.32 | 97.29 | 1,110.23 | 2.26 | -42.91 | Lévy -s. | |

| 2005 | 98.16 | 1,003.81 | 99.50 | 1,038.32 | -1.34 | -34.52 | even | |

| 2006 | 97.26 | 1,016.92 | 99.15 | 1,047.34 | -1.89 | -30.41 | even | |

| 2007 | 95.28 | 1,062.73 | 97.86 | 1,072.13 | -2.58 | -9.41 | even | |

| 2012 | 95.20 | 1,031.04 | 97.74 | 1,060.46 | -2.54 | -29.43 | even | |

| 2013 | 96.63 | 1,063.87 | 94.74 | 1,095.59 | 1.89 | -31.72 | Lévy -s. | |

| 1999 | 98.54 | 1,230.72 | 94.70 | 1,277.72 | 3.84 | -47.00 | Lévy -s. | |

| 2000 | 98.27 | 1,221.62 | 94.69 | 1,283.48 | 3.58 | -61.86 | Lévy -s. | |

| 2001 | 95.30 | 1,243.37 | 90.81 | 1,293.24 | 4.49 | -49.88 | Lévy -s. | |

| 2002 | 96.57 | 1,243.78 | 96.28 | 1,296.99 | 0.29 | -53.21 | Lévy -s. | |

| 2003 | 96.10 | 1,419.75 | 96.05 | 1,481.73 | 0.05 | -61.98 | Lévy -s. | |

| 2004 | 95.63 | 1,408.22 | 93.21 | 1,475.98 | 2.42 | -67.76 | Lévy -s. | |

| 2005 | 94.48 | 1,350.69 | 85.73 | 1,408.57 | 8.75 | -57.88 | - | |

| 2006 | 97.43 | 1,263.57 | 90.15 | 1,308.09 | 7.28 | -44.52 | Lévy -s. | |

| 2007 | 97.06 | 1,239.16 | 79.77 | 1,283.18 | 17.29 | -44.02 | Lévy -s. | |

| 2008 | 96.17 | 1,373.84 | 92.12 | 1,428.20 | 4.05 | -54.35 | Lévy -s. | |

| 2009 | 97.73 | 1,302.20 | 94.31 | 1,351.16 | 3.42 | -48.96 | Lévy -s. | |

| 2010 | 88.00 | 1,786.06 | 77.35 | 1,810.14 | 10.65 | -24.09 | - | |

| 2012 | 98.39 | 1,508.08 | 81.76 | 1,565.72 | 16.63 | -57.64 | Lévy -s. | |

| 2013 | 95.42 | 1,297.17 | 90.06 | 1,342.75 | 5.36 | -45.57 | Lévy -s. | |

5 Results

In this section, we investigate questions that are of importance for understanding developing economies in general and the Chinese case during the decade of rapid catch-up (1999-2013, the period for which we have data) in particular.

-

1.

What distributional model should be used for productivity microdata for developing countries (here, the P.R. China)? Do they differ from developed countries? (Section 5.1)

-

2.

Do the parameters of these distributions change with advancing development level? (Section 5.2)

-

3.

Are there persistent differences between regions (or countries)? (Section 5.3)

-

4.

If there are any systematic differences or developments, how do they relate to other characteristics at the micro- or macro-level (firm age, GDP growth, capital intensity, employment)? (Section 5.4)

Although our analysis is limited to the P.R. China, we can draw comparisons to the distributions of firm-level productivity data for developed economies (Yang et al., 2019) and conjecture that other developing economies may show similar patterns in phases of rapid economic catch-up. We also leverage the considerable diversity between Chinese provinces to assess regional differences, which may be an indicator of how different developing countries should be expected to be from one another in this regard.

5.1 Fitting productivity distributions

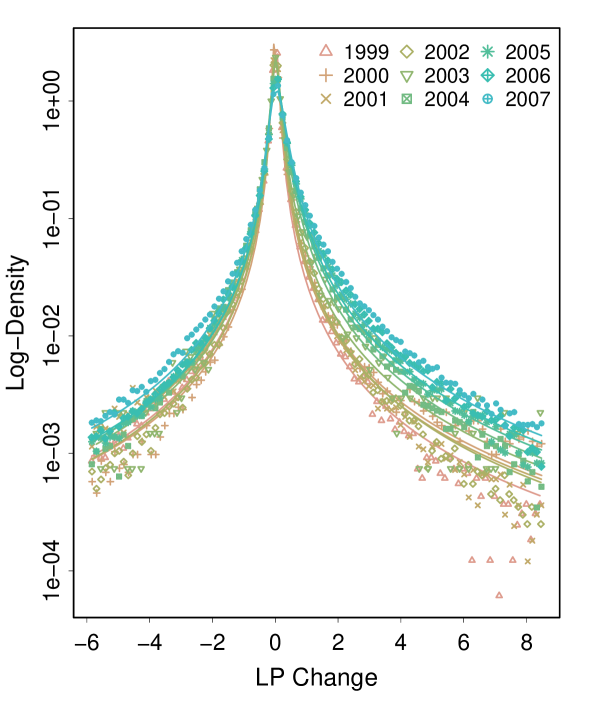

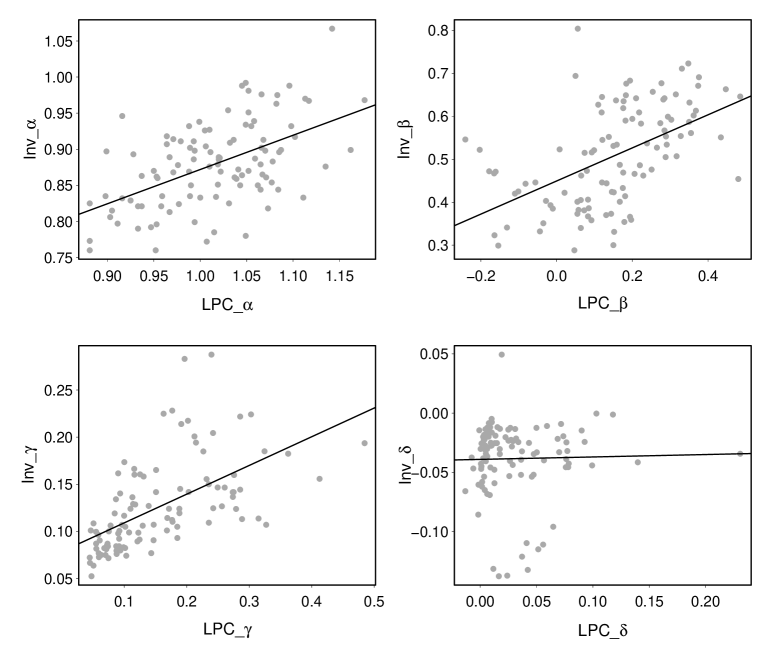

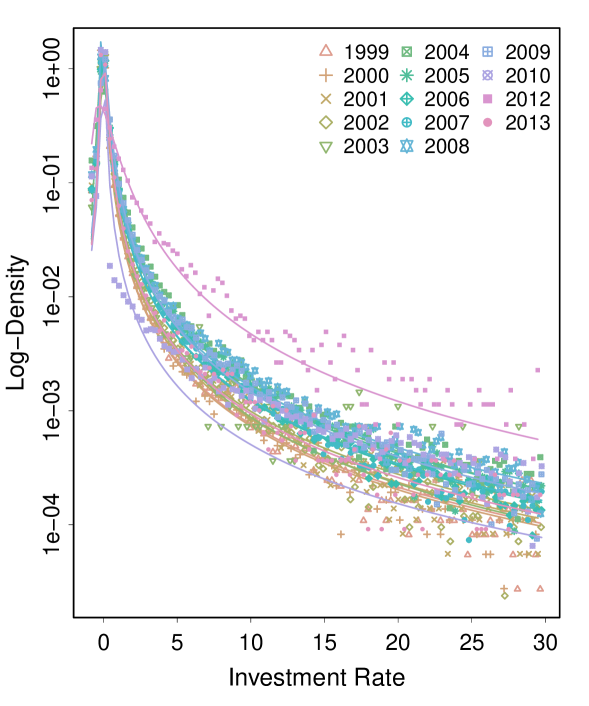

We performed parameter fits with the Lévy alpha-stable model and, as a point of comparison, for the AEP model for all variables listed in section 3.3. However, we concentrate our analysis on the labor productivity , and the labor productivity change , while the other variables (, ) serve as a point of comparison and to show that the functional forms of the distributions are connected. Lévy alpha-stable fit lines as well as empirical density by year are shown in Figures 1 () and 3 (). The parameter values for the fits are given in the upper two sections of Table 2, while the goodness of fit measures are listed in Table 3.

The distributions of both variables (, ) have striking and regular characteristics. They are (i) unimodal (one pronounced peak), (ii) heavy-tailed (bent outwards in semi-log), (iii) have wide support over both negative and positive numbers, and (iv) are highly stable over time. The Lévy alpha-stable model is an excellent fit of the distribution and the data, better than the alternative AEP in all cases.141414This is confirmed by both goodness of fit measures employed here, the Soofi ID score () and the Akaike information criterion (). Table 3 explicitly lists which model provides a better fit for which sample in either criterion ( or ). AEP performs systematically worse than Lévy alpha-stable in the labor productivity, the labor productivity change, and the investment rate. Both models appear to be good fits for the profitability (). Only in the case of the labor productivity change in 1999, both models resulted in a Soofi ID score which indicates a less perfect fit. It is, however, a marginal case with for both Lévy alpha-stable and AEP. This is confirmed both in the goodness of fit measures in Table 3 and in the fit lines in Figures 1 and 3.

5.2 Economic development and systematic changes to productivity distributions

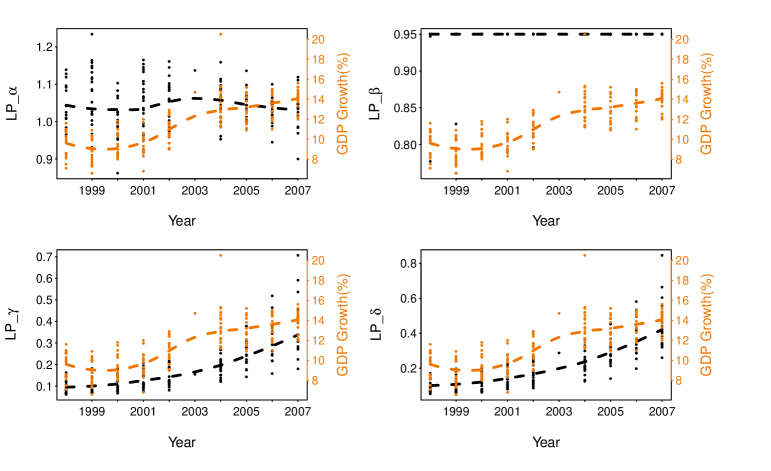

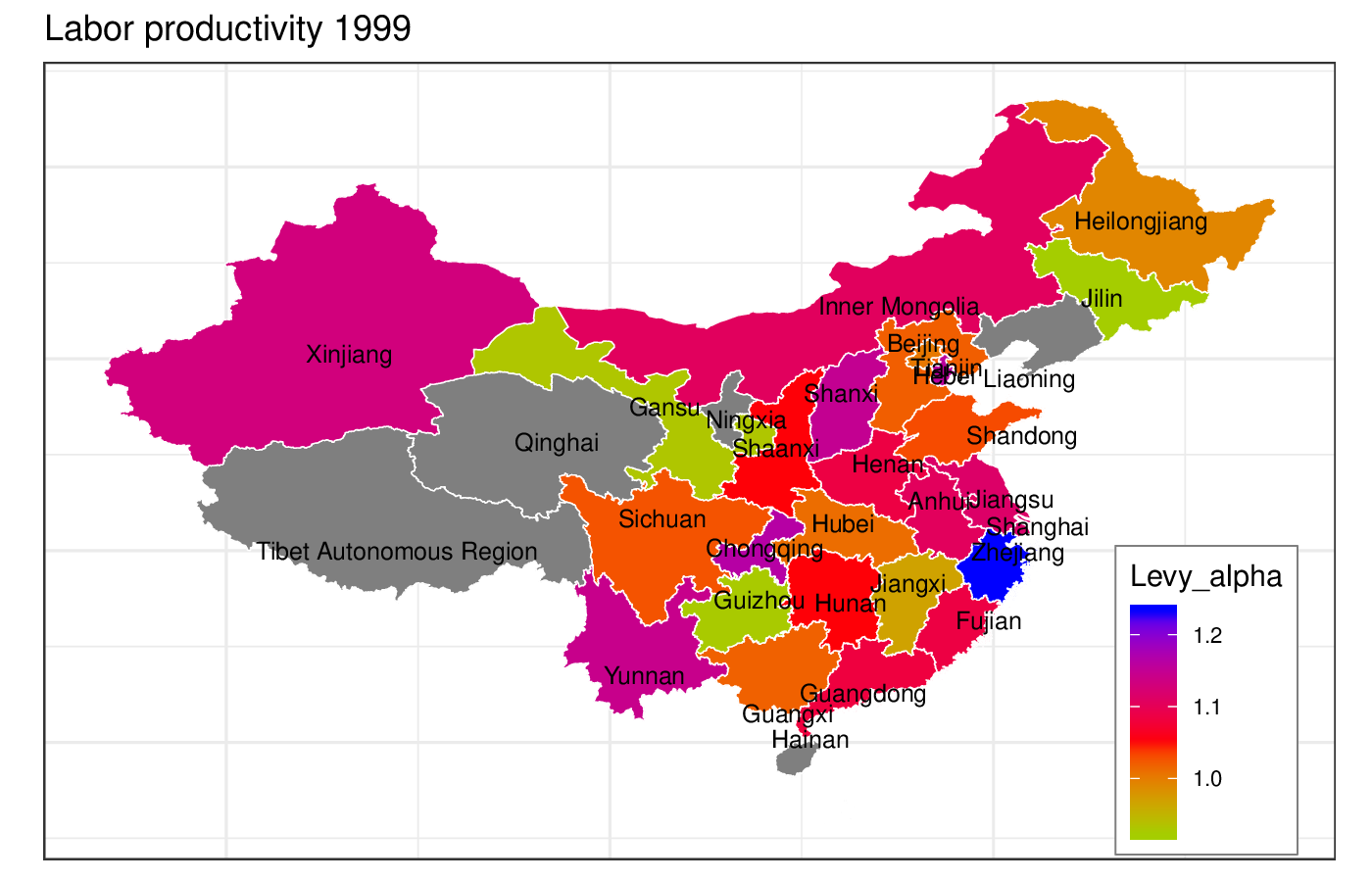

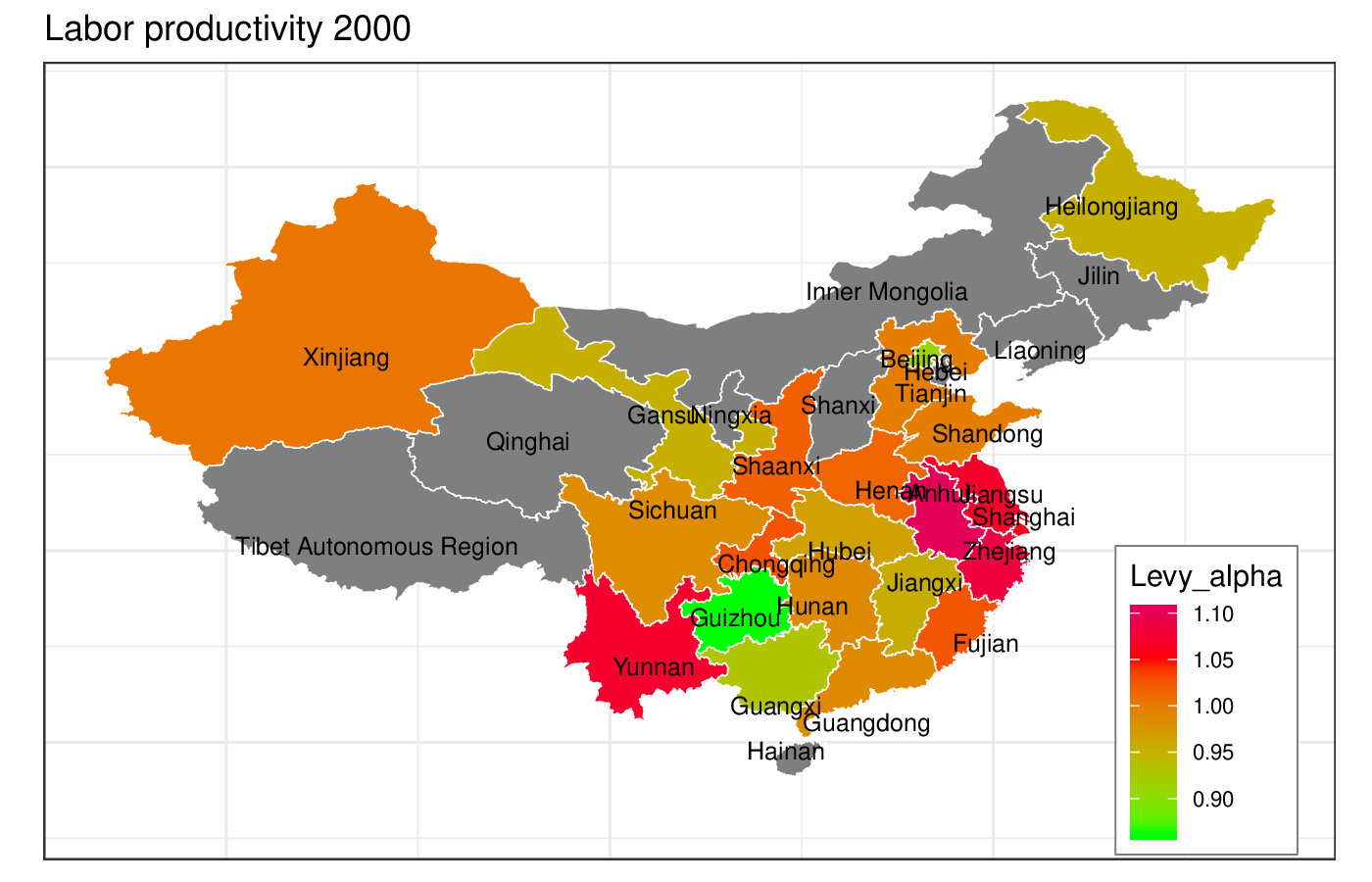

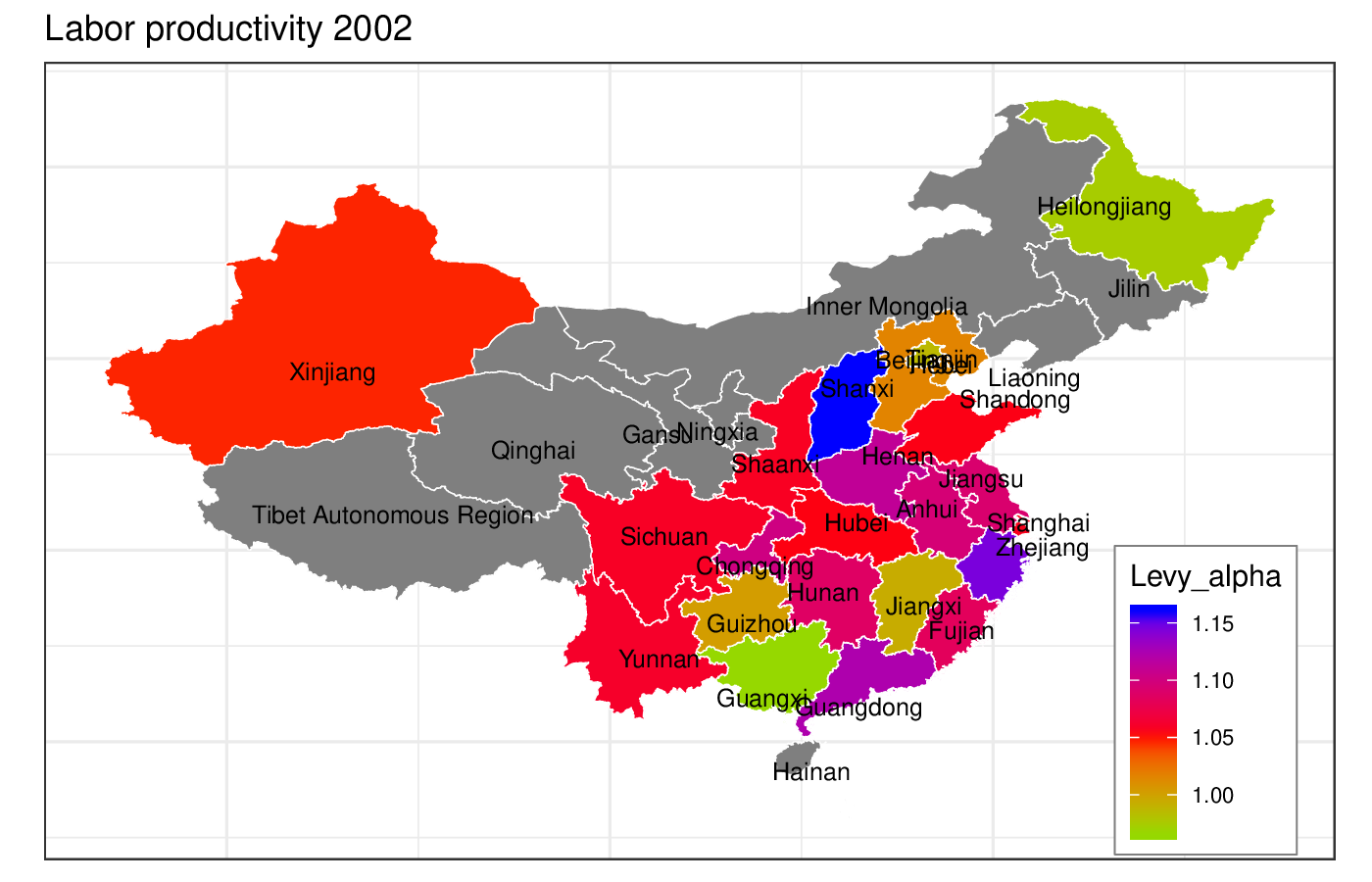

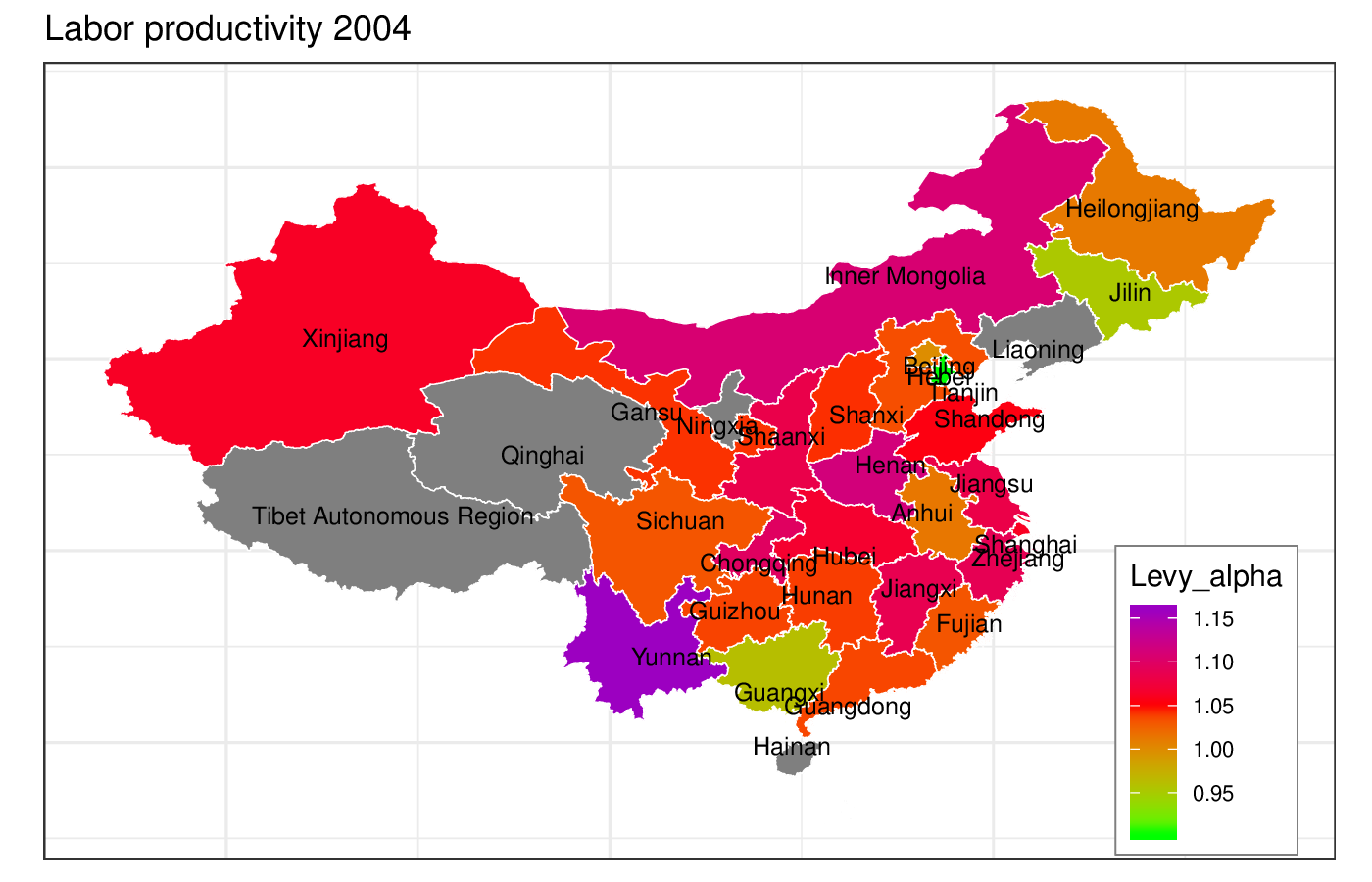

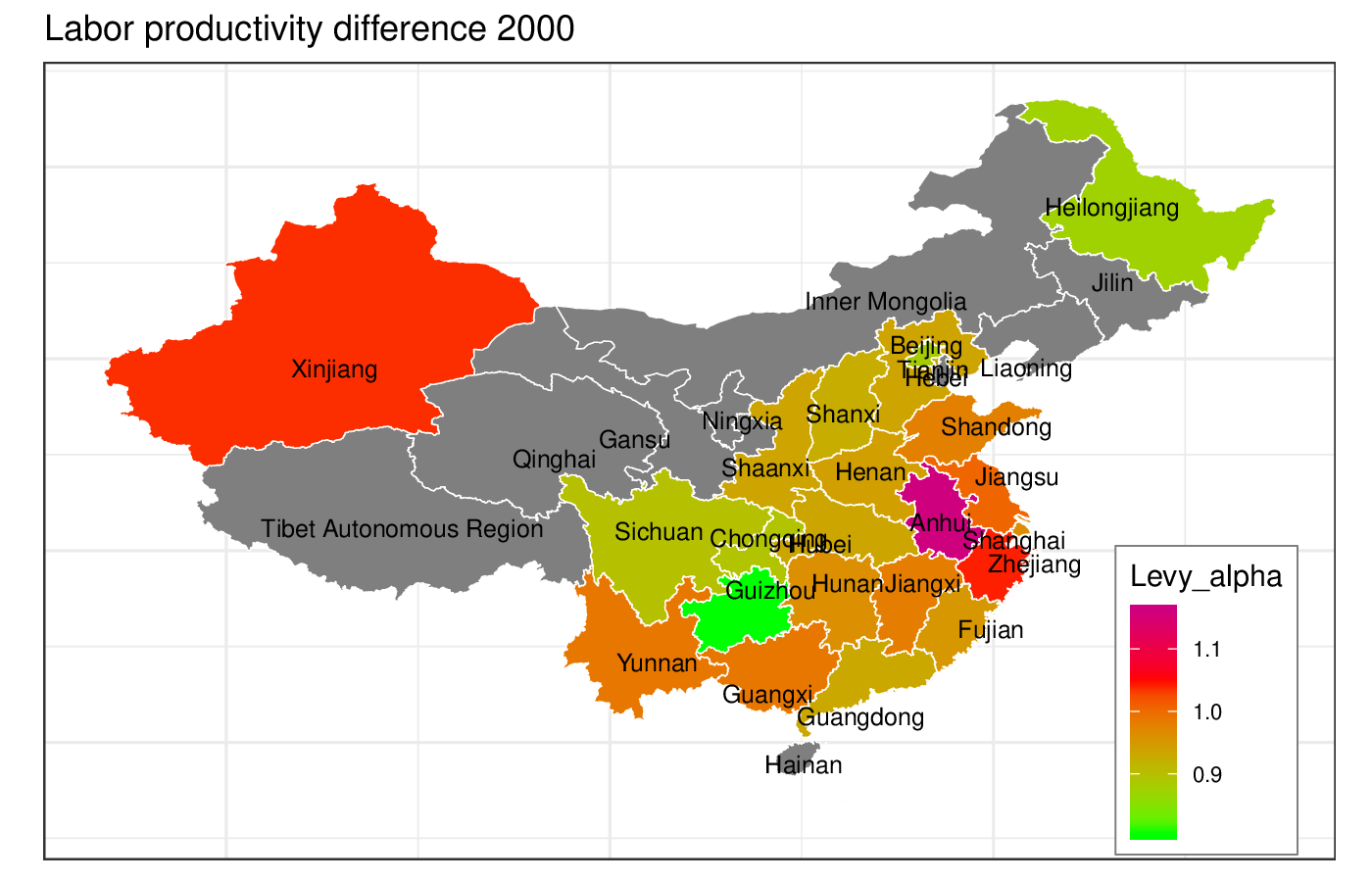

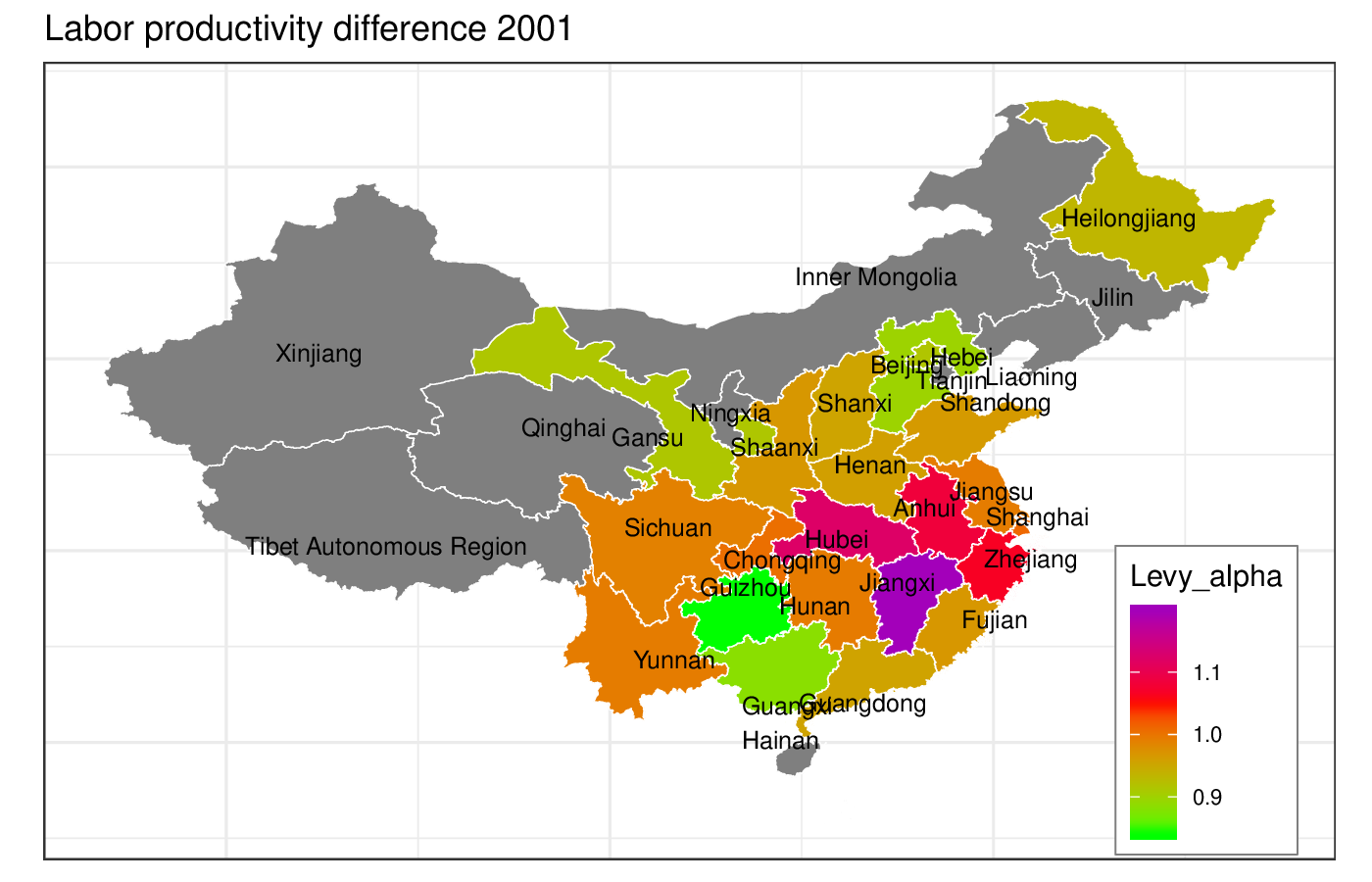

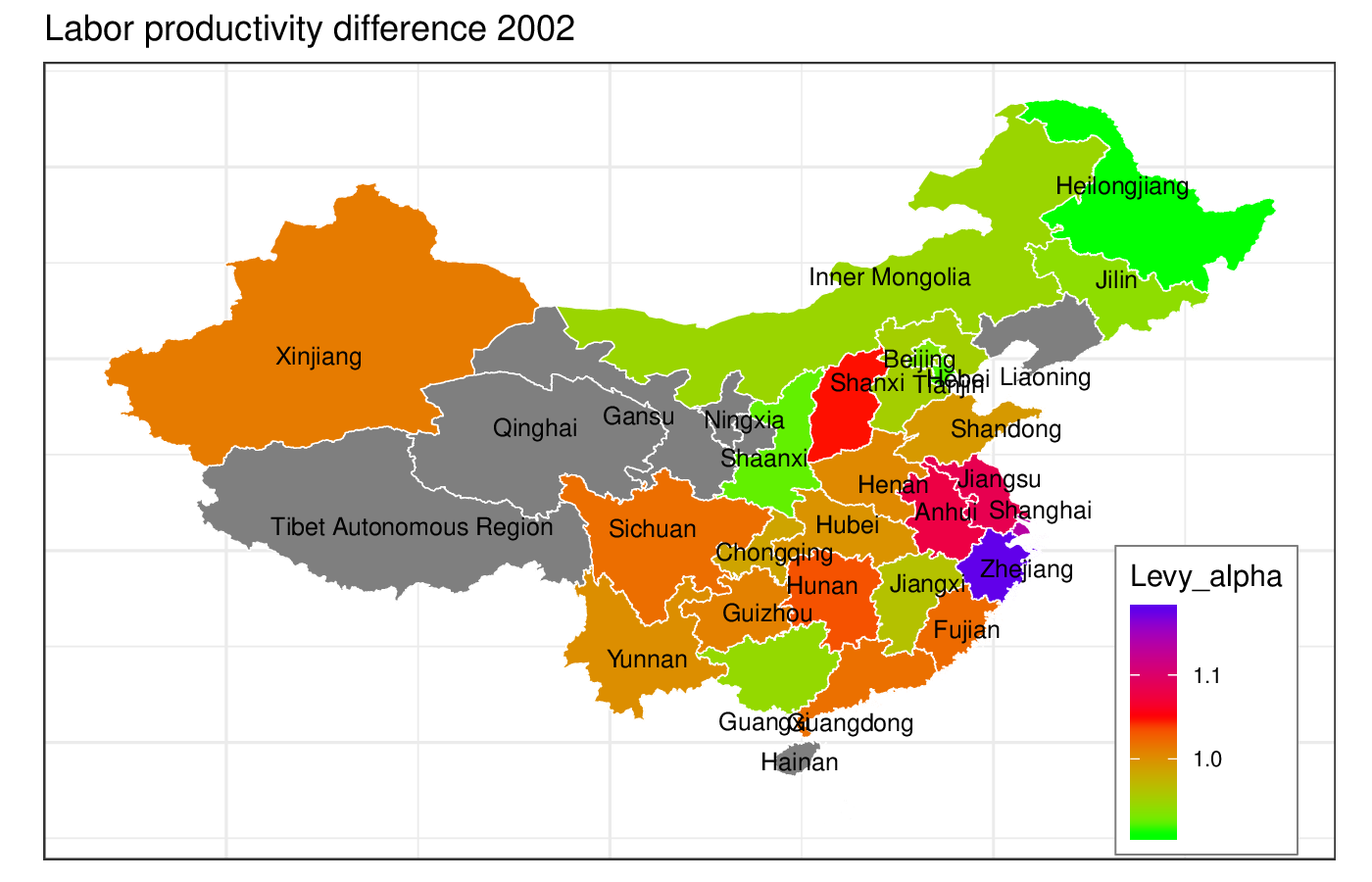

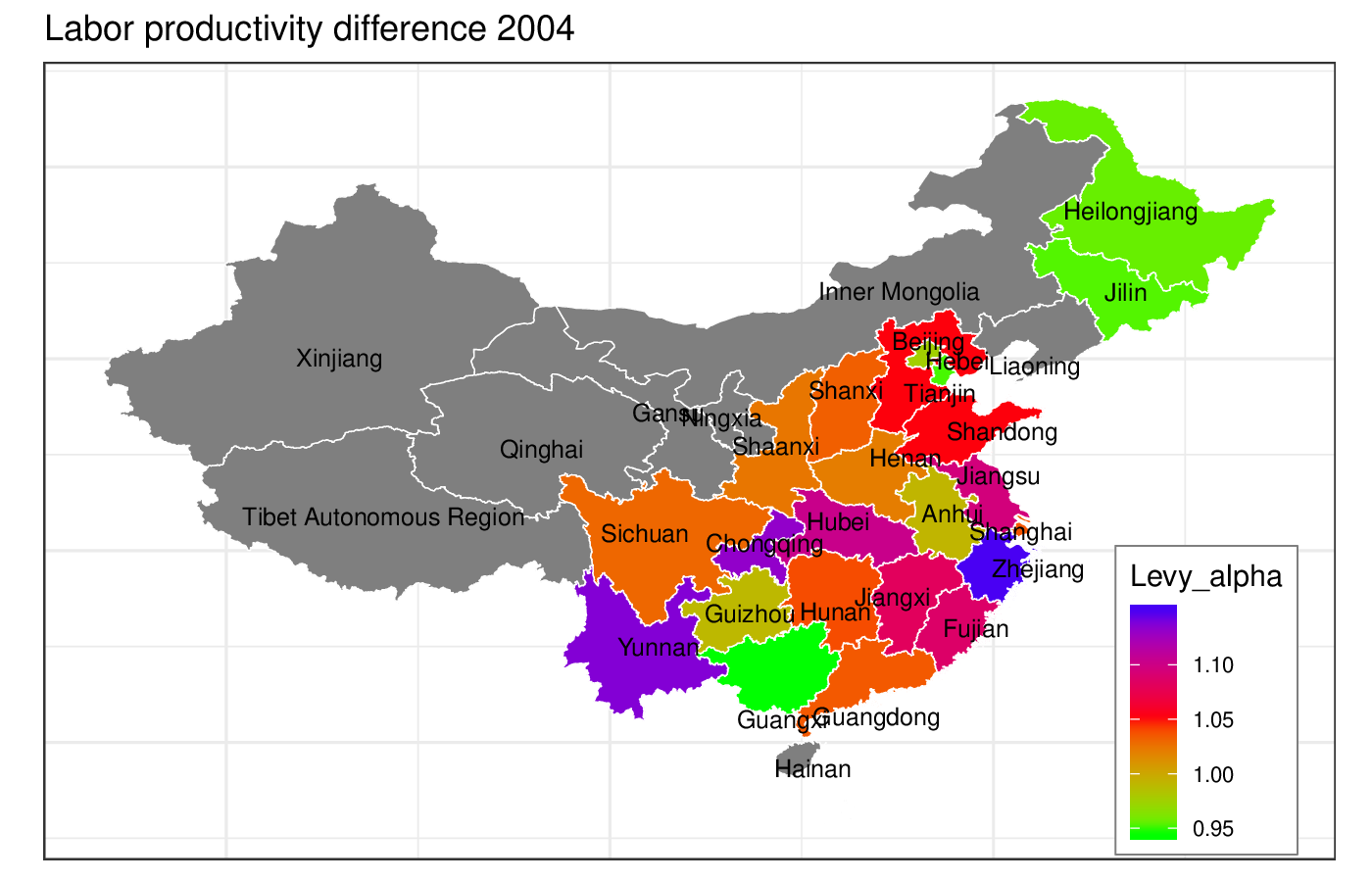

The fundings in Section 5.1 show that the productivity distribution is found for the P.R. China is consistent with those identified for a wide range of developed economies (Yang et al., 2019). However, while Yang et al. (2019) find that there is no systematic change for developed economies over a period of 10 years (2006-2015), there is a persistent shift in several parameters in the case of China. This is evidenced by the densities and fit lines in Figures 1 () and 3 () not overlaying each other but being neatly aligned next to one another in the exact order of years. The parameter values for the complete sample are given in Table 2; further, the black line in Figures 4 and 5 illustrate the development of the average of these parameter fits for each of the P.R. China’s 31 provinces and autonomous regions.151515This does not include the Special Administrative Regions Hong Kong and Macao, which are not represented in the database.

For both distributions, the modal value became less pronounced, while the wings (not necessarily the tails) were pushed out, especially the one to the positive side (higher labor productivity, higher intertemporal gains in labor productivity). For both and , the location parameter increases substantially from 1998 to 2008 and the scale parameter increases in concert. This reflects the increase in labor productivity over the period of study with yearly changes and variation growing proportionally. While tail index and the skew remain almost unchanged for , they increase systematically for . This has several implications:

-

•

Super-star firms do not become more prevalent with China’s development push. The tail index of remains approximately the same. Not even the skew of the distribution changes. Instead the entire distribution shifts.

-

•

The tails of the labor productivity change () distribution grow shorter (higher , indicating that large productivity changes in one and the same firm become less common. Instead, the productivity change remains in the body of the distribution, therefore becoming more uniform across the economy.

-

•

A right-skew emerges in the labor productivity change () distribution. The body of the distribution stretches to the right (higher positive, but not excessively large productivity gains).

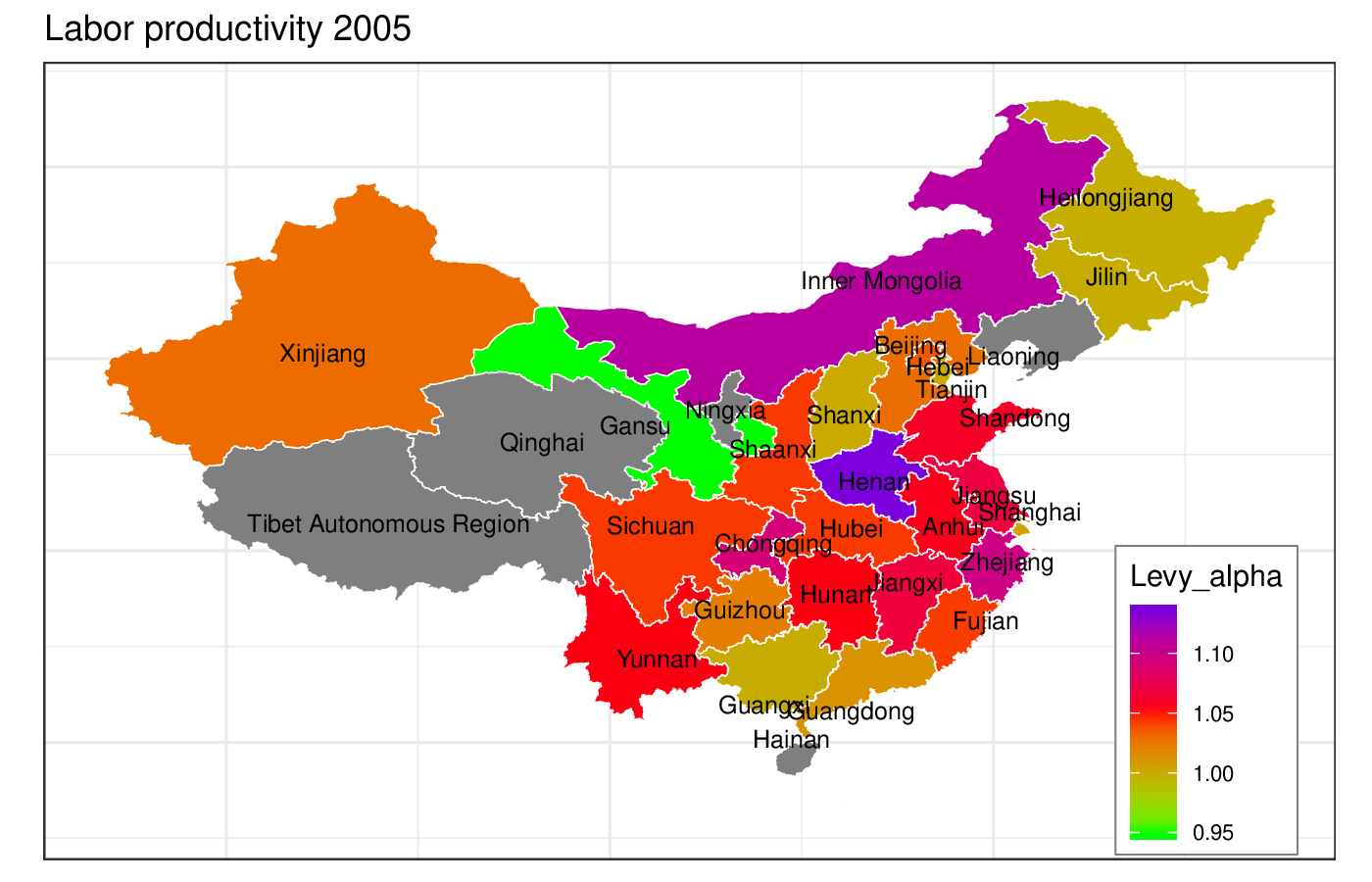

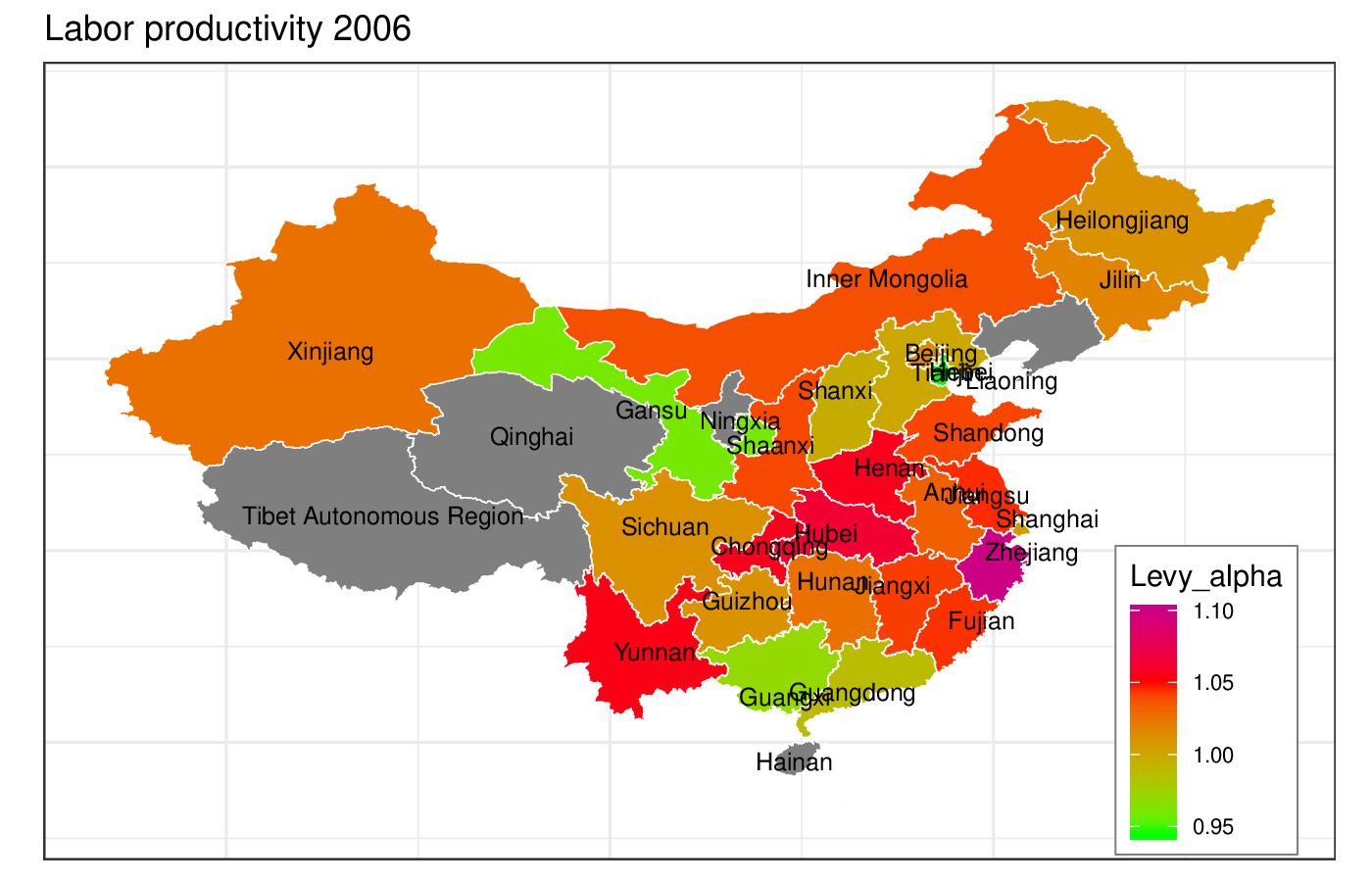

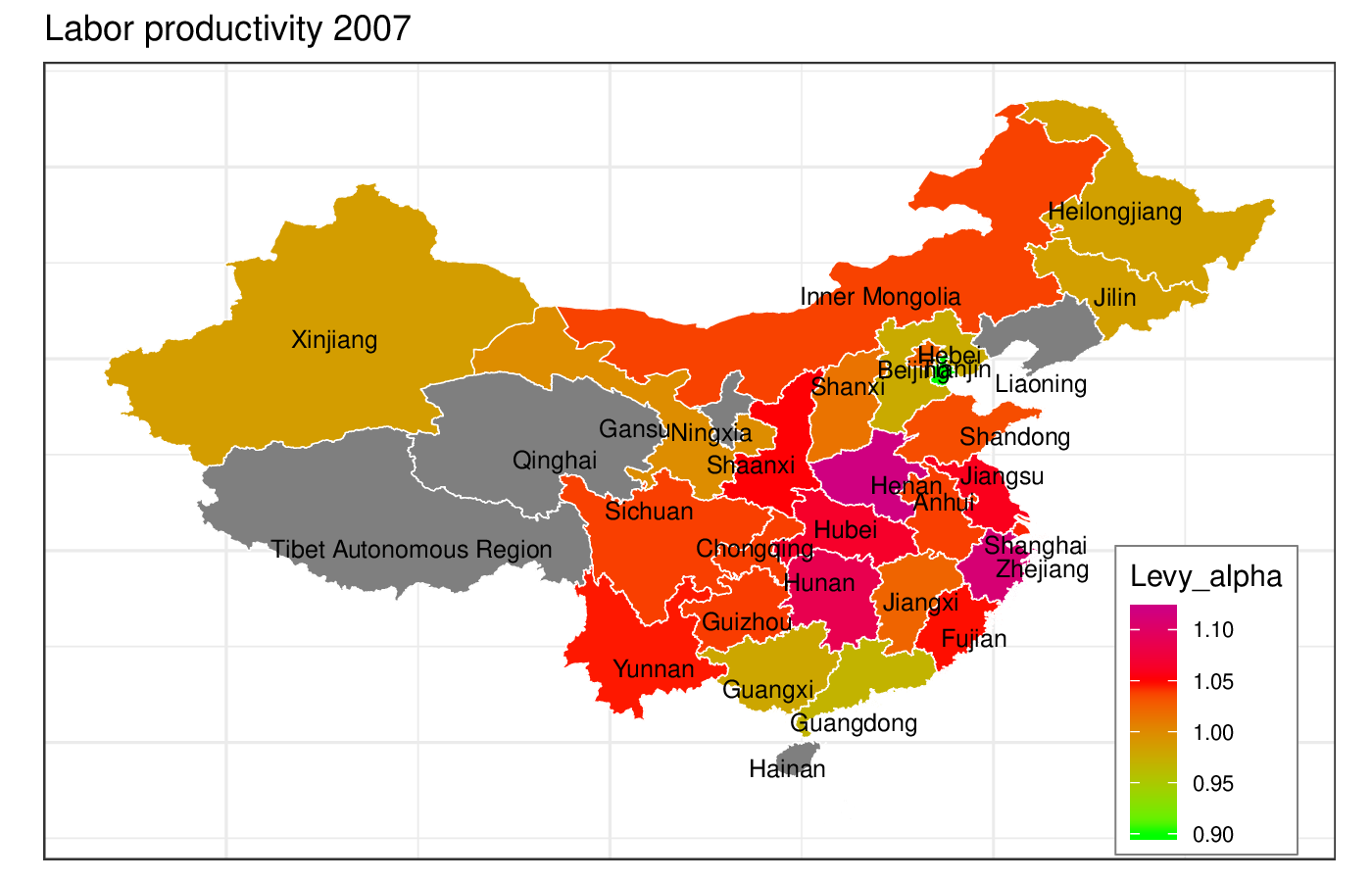

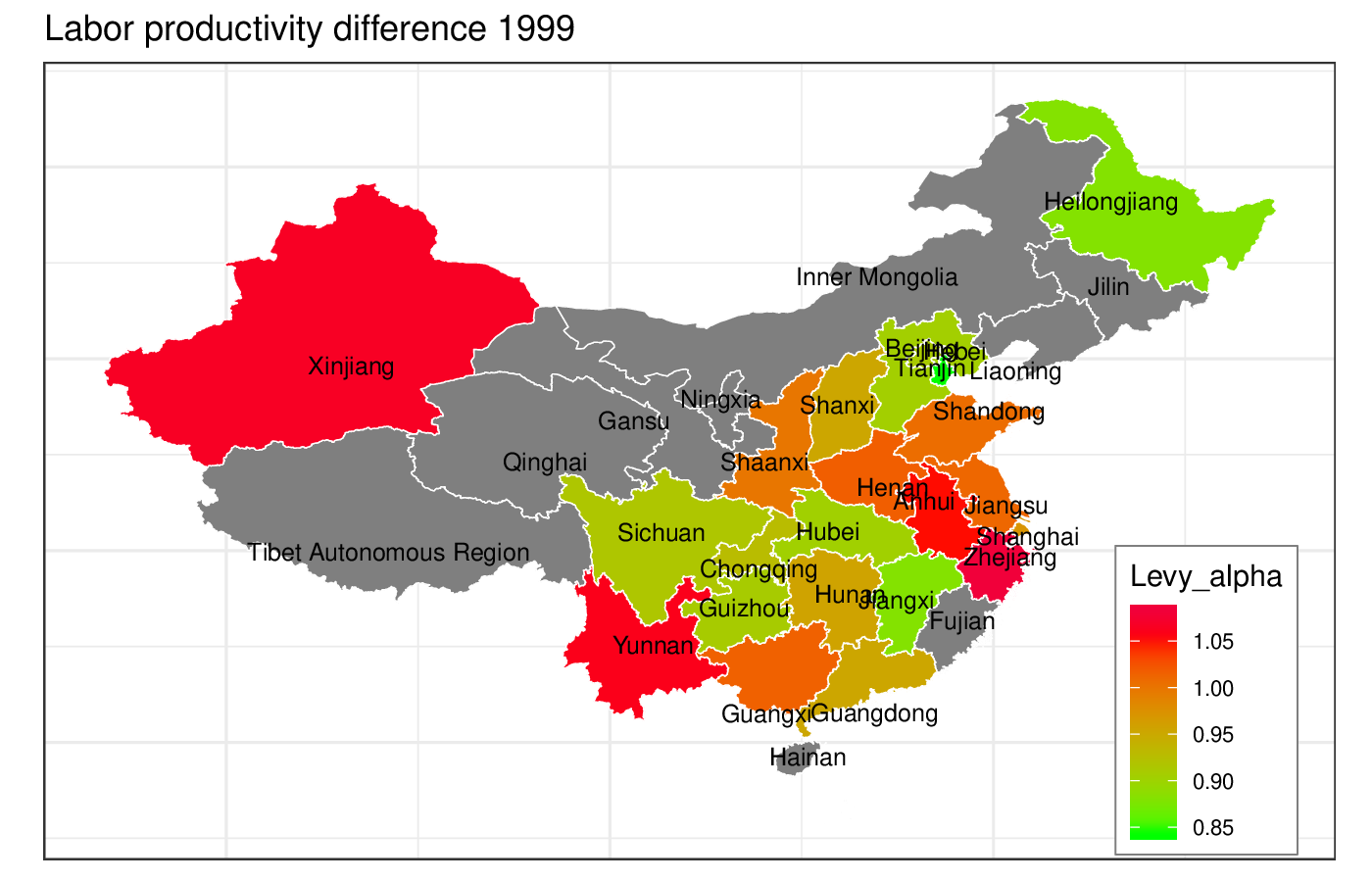

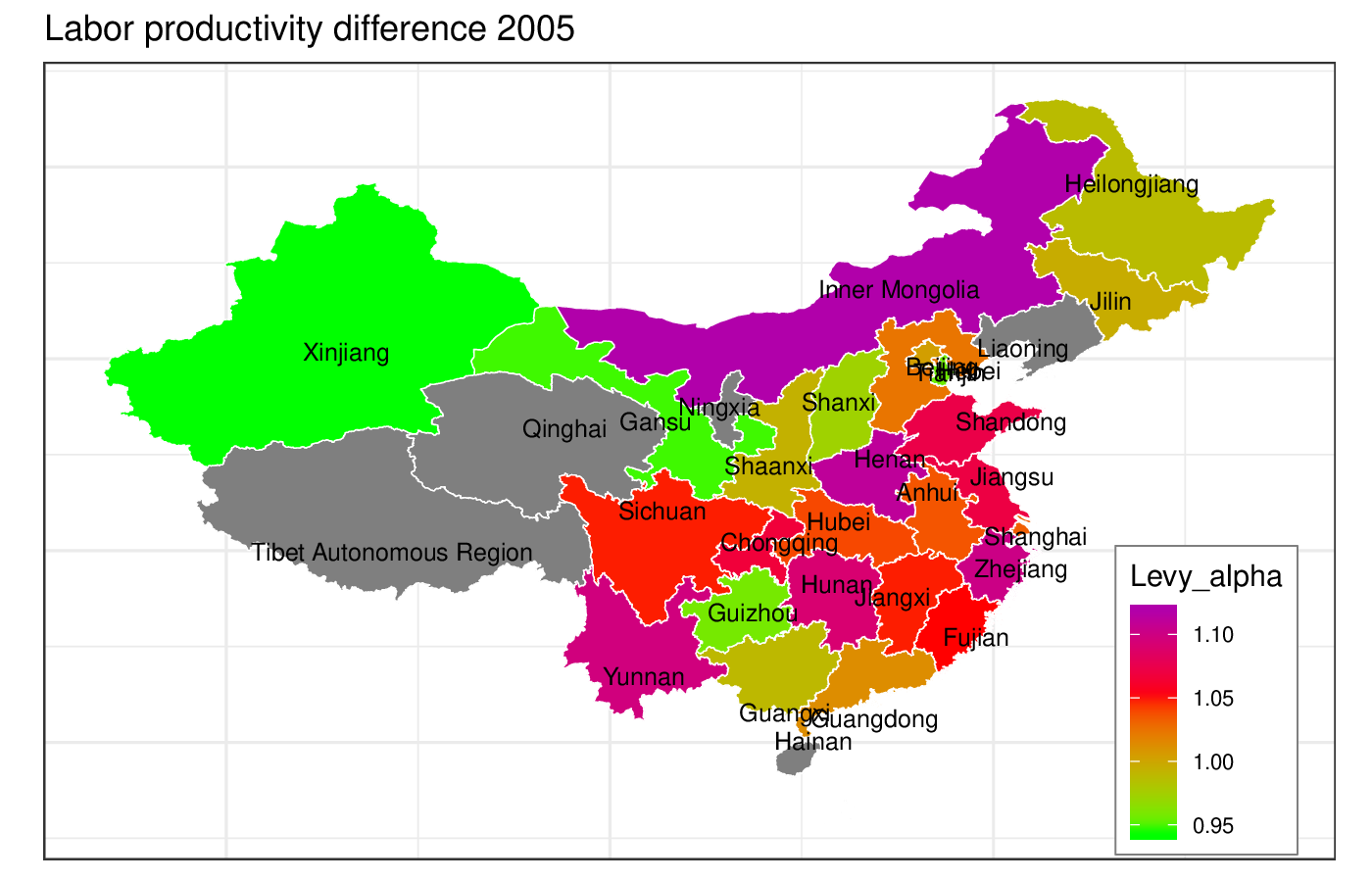

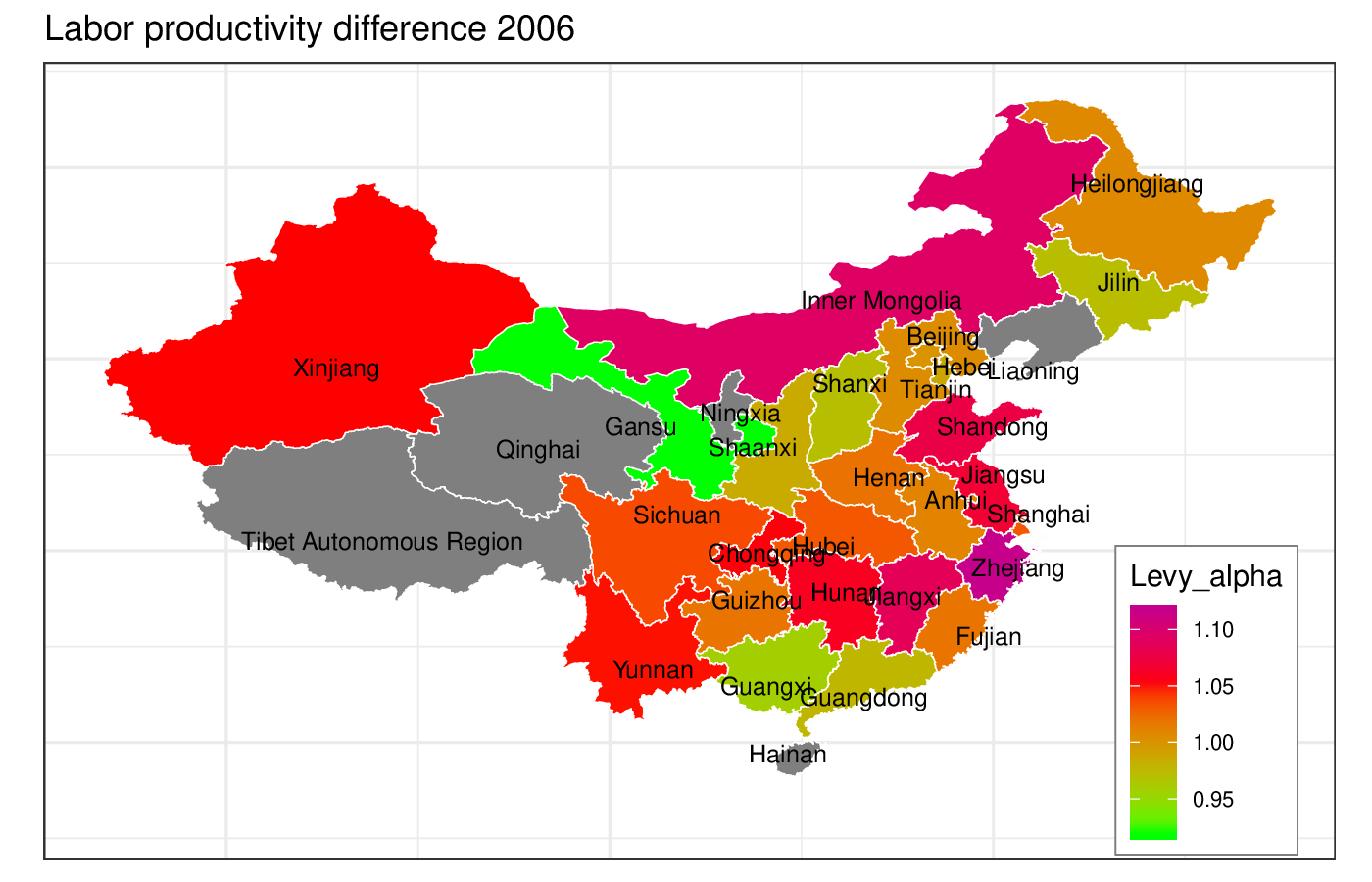

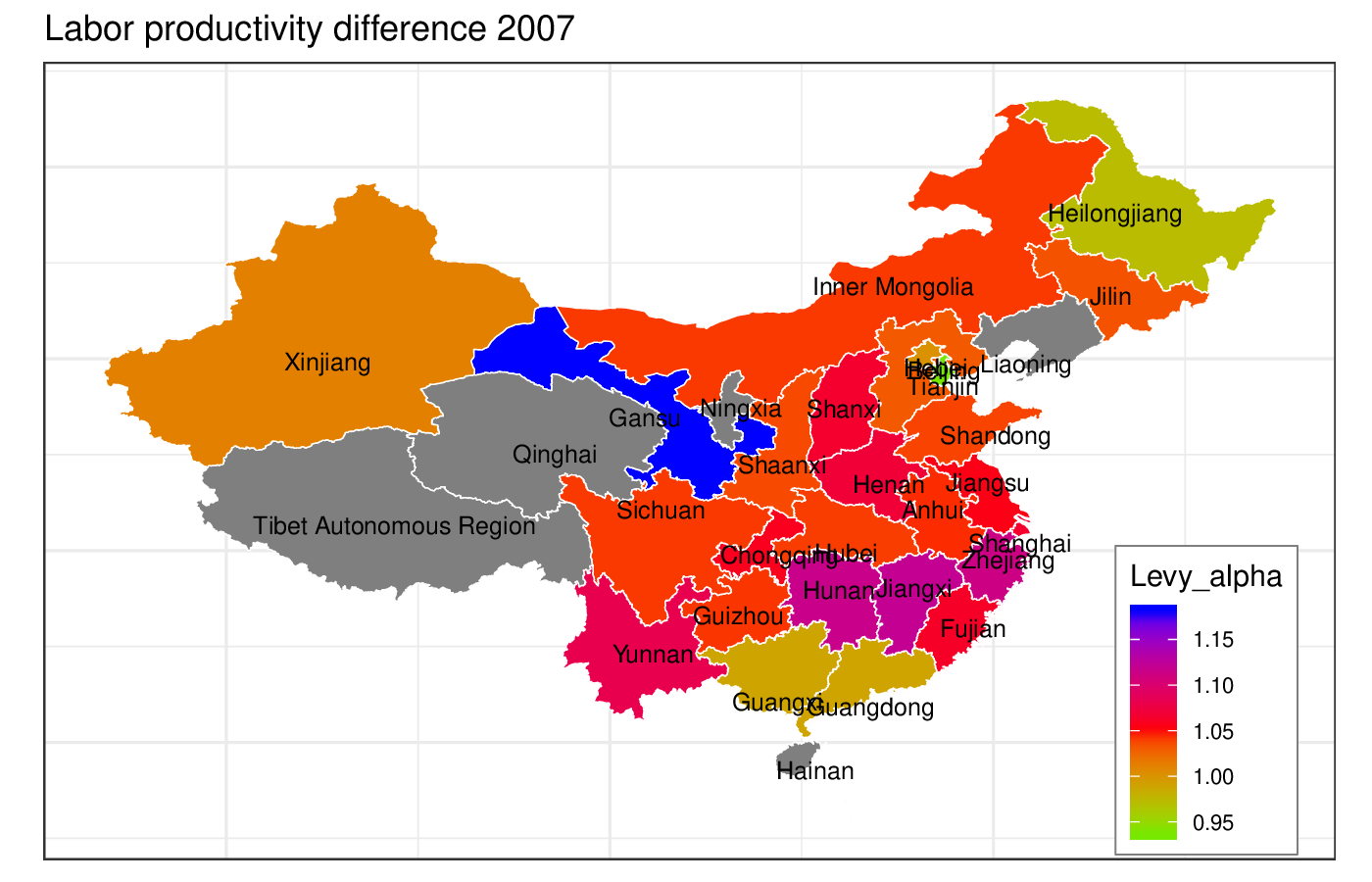

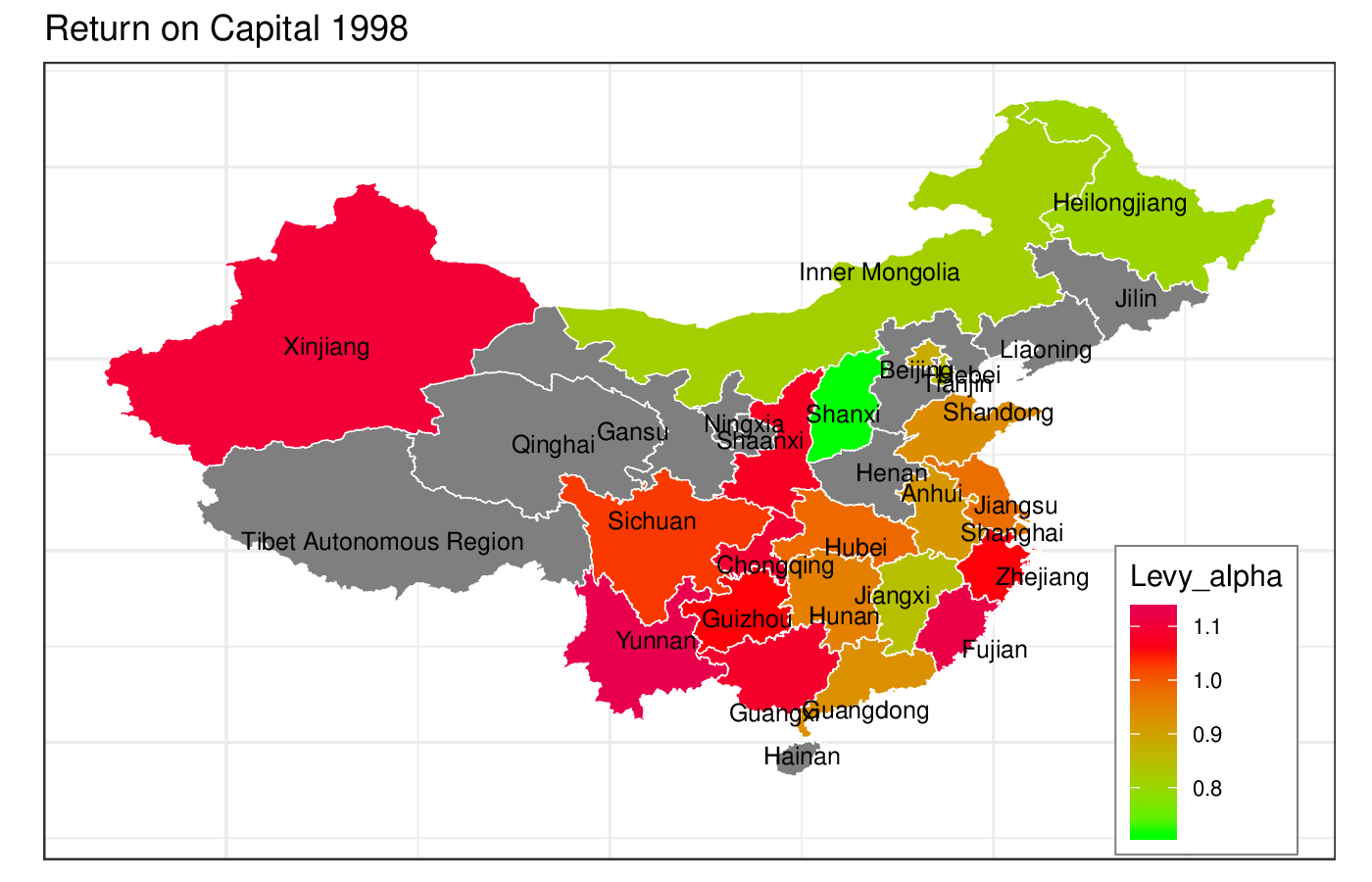

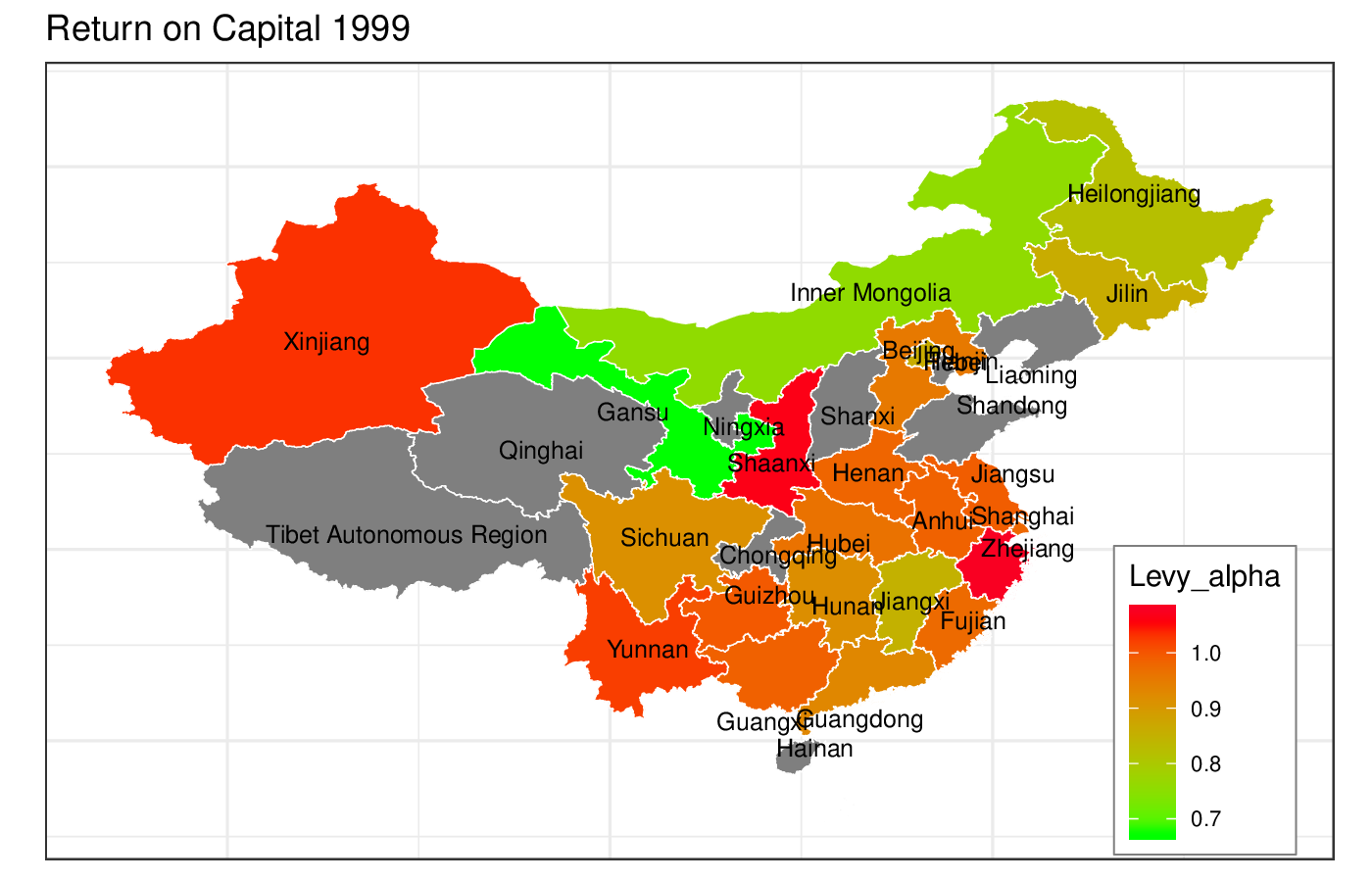

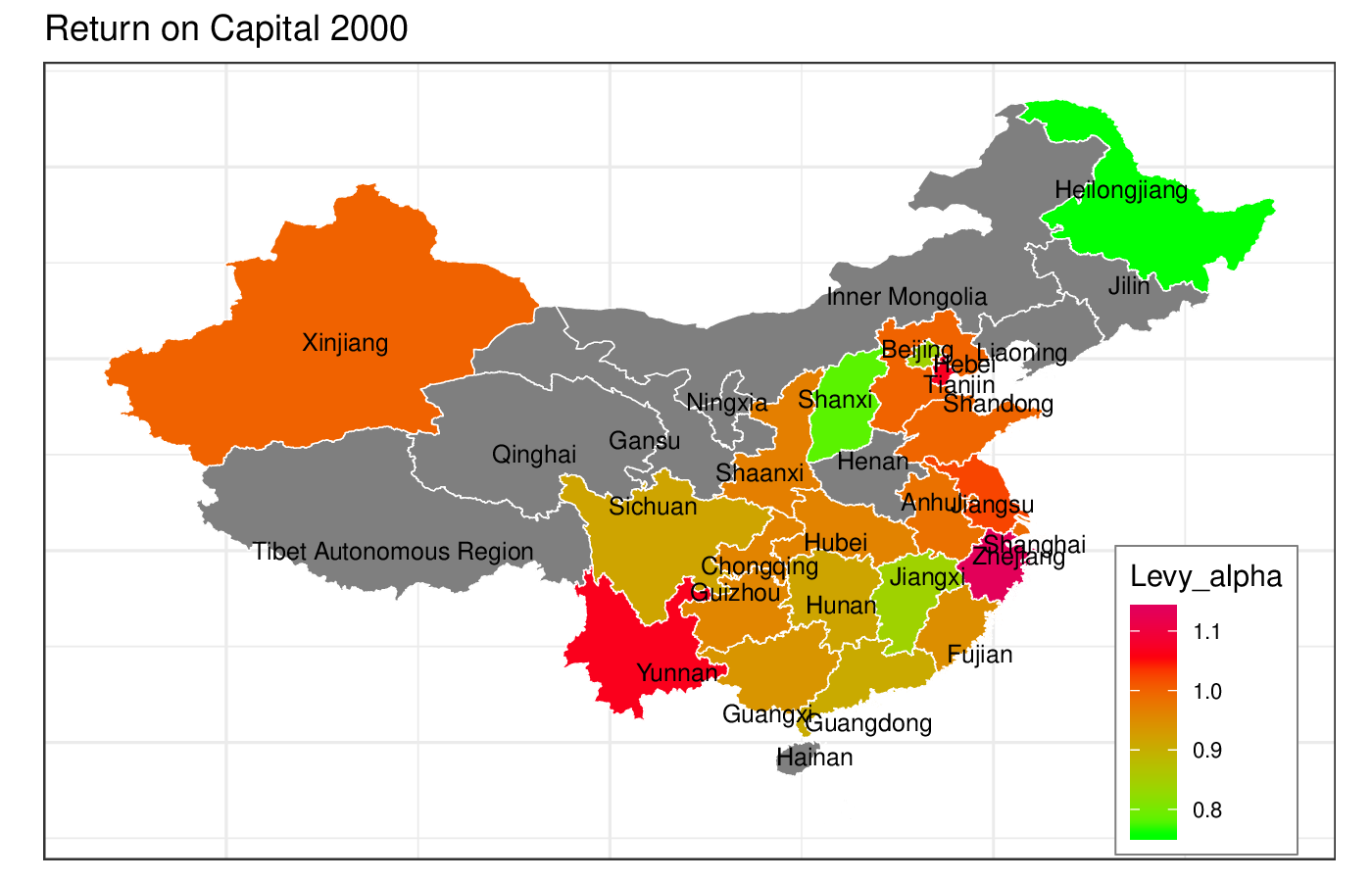

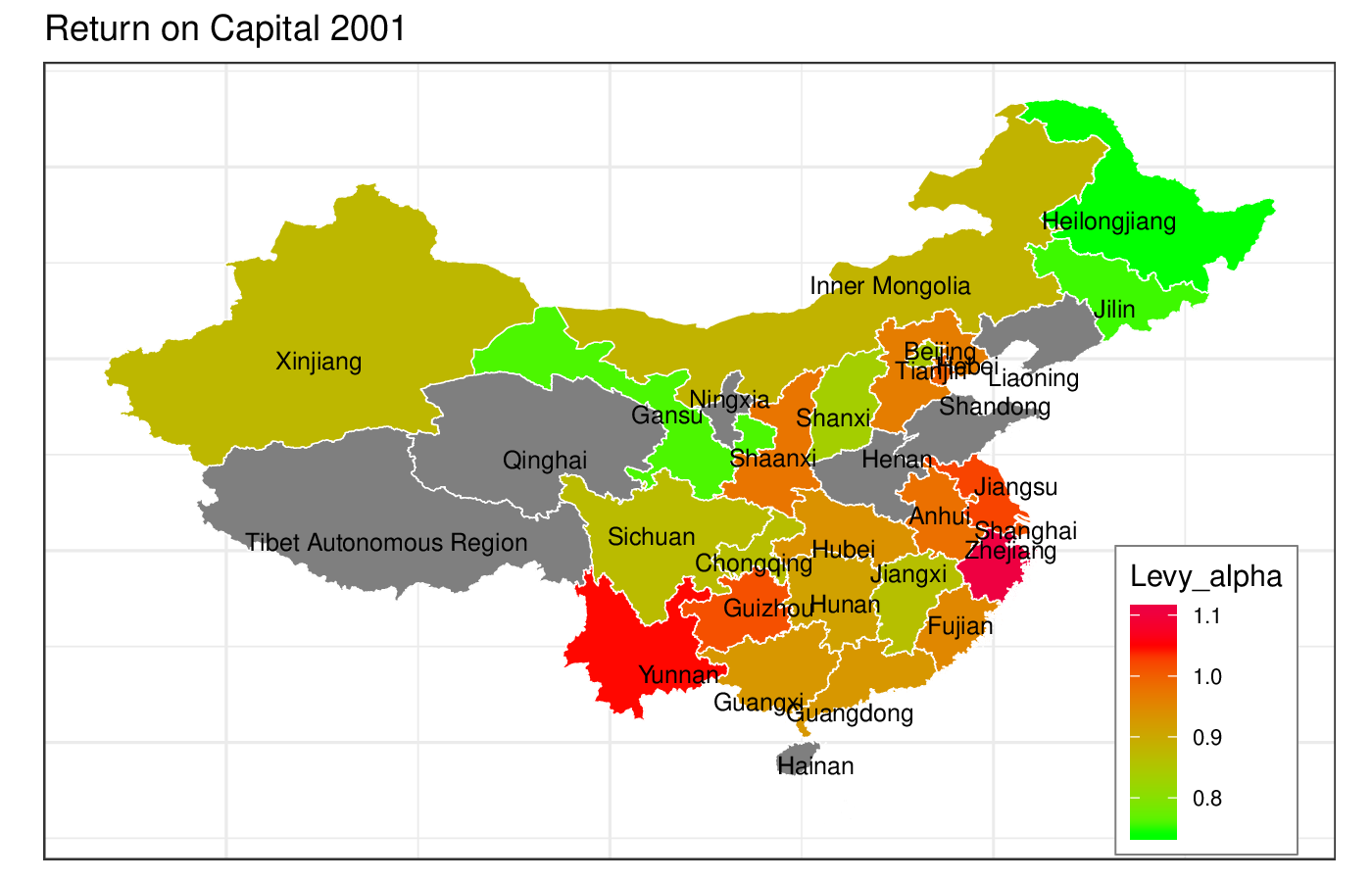

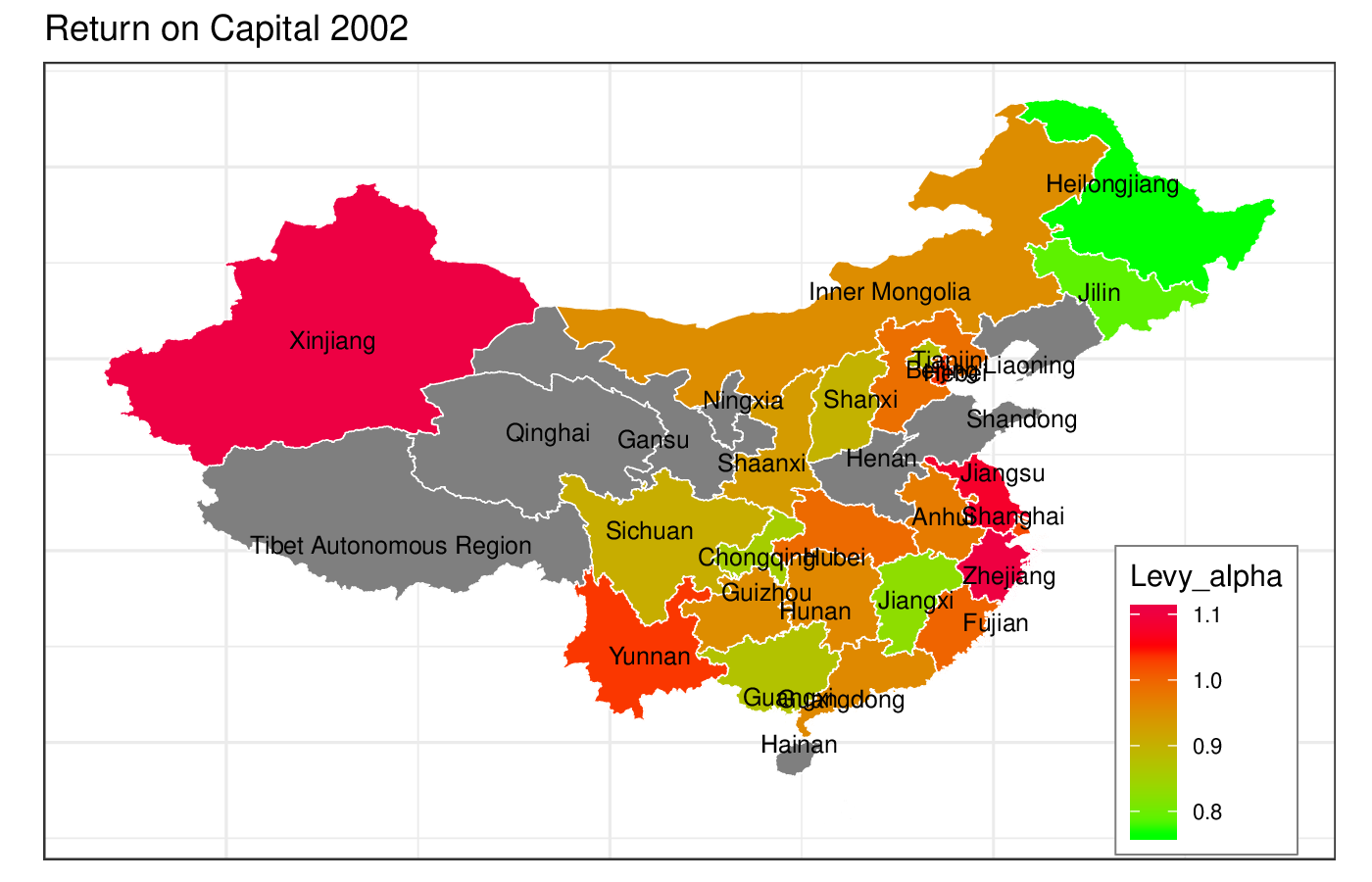

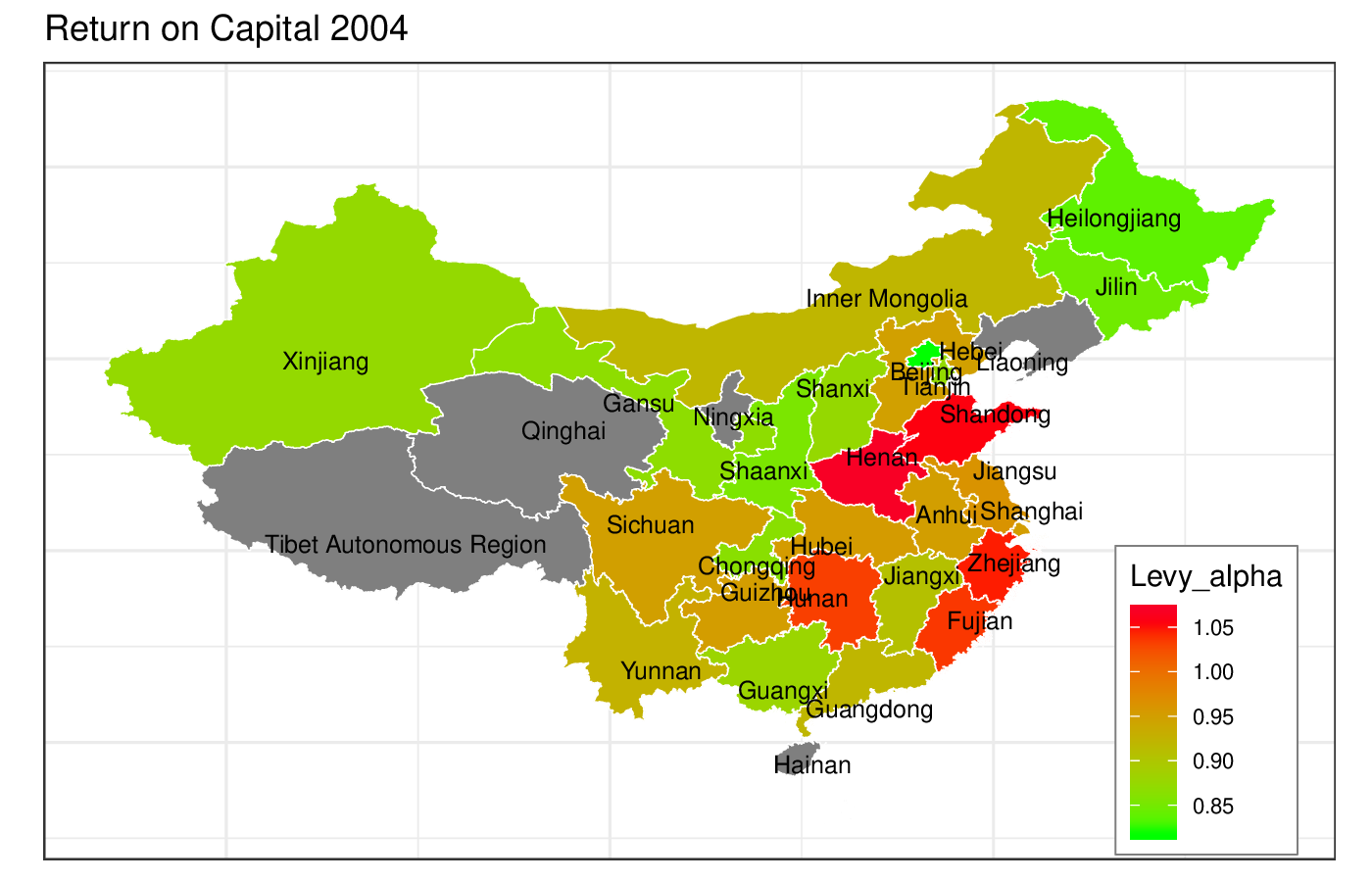

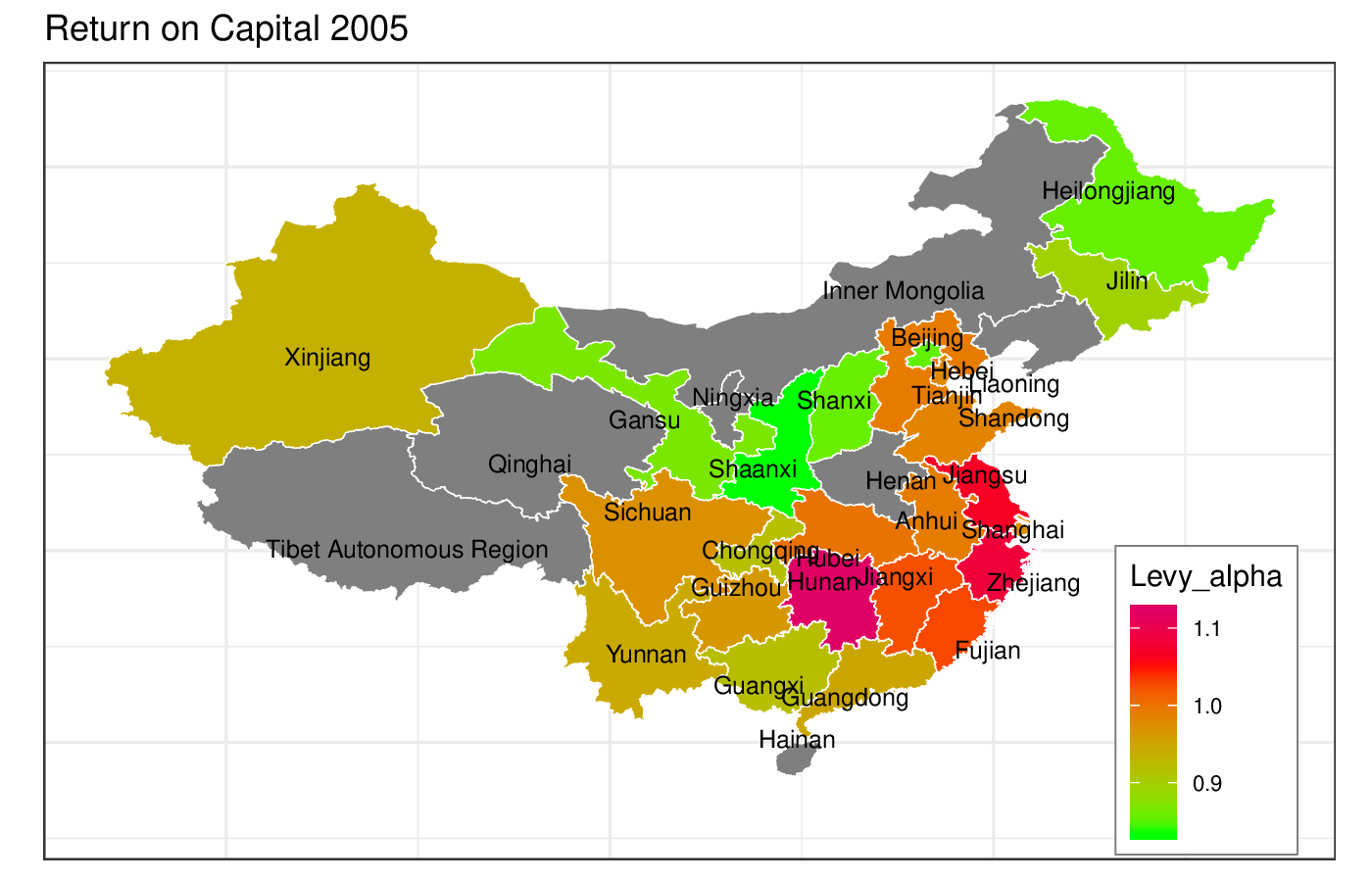

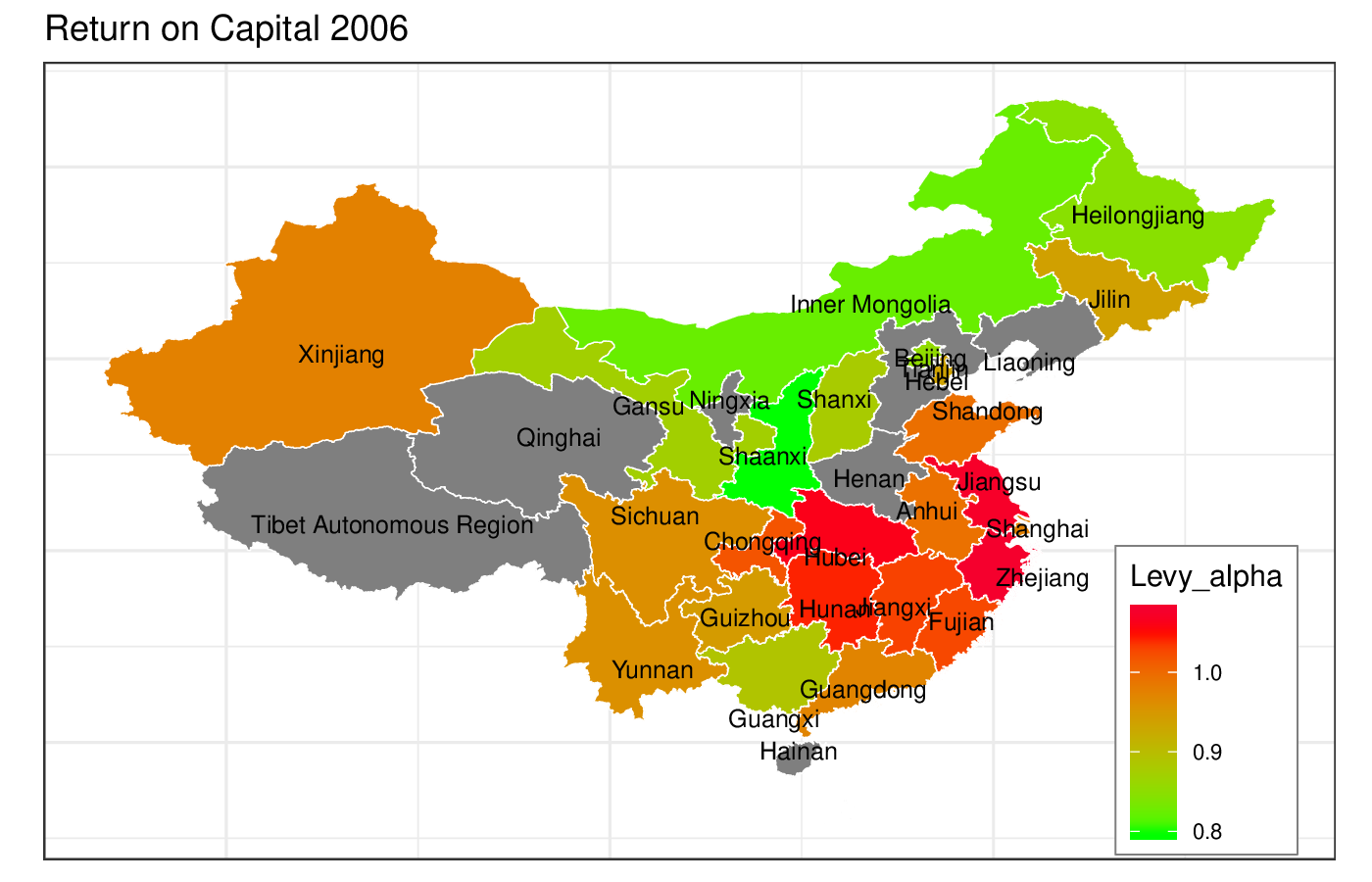

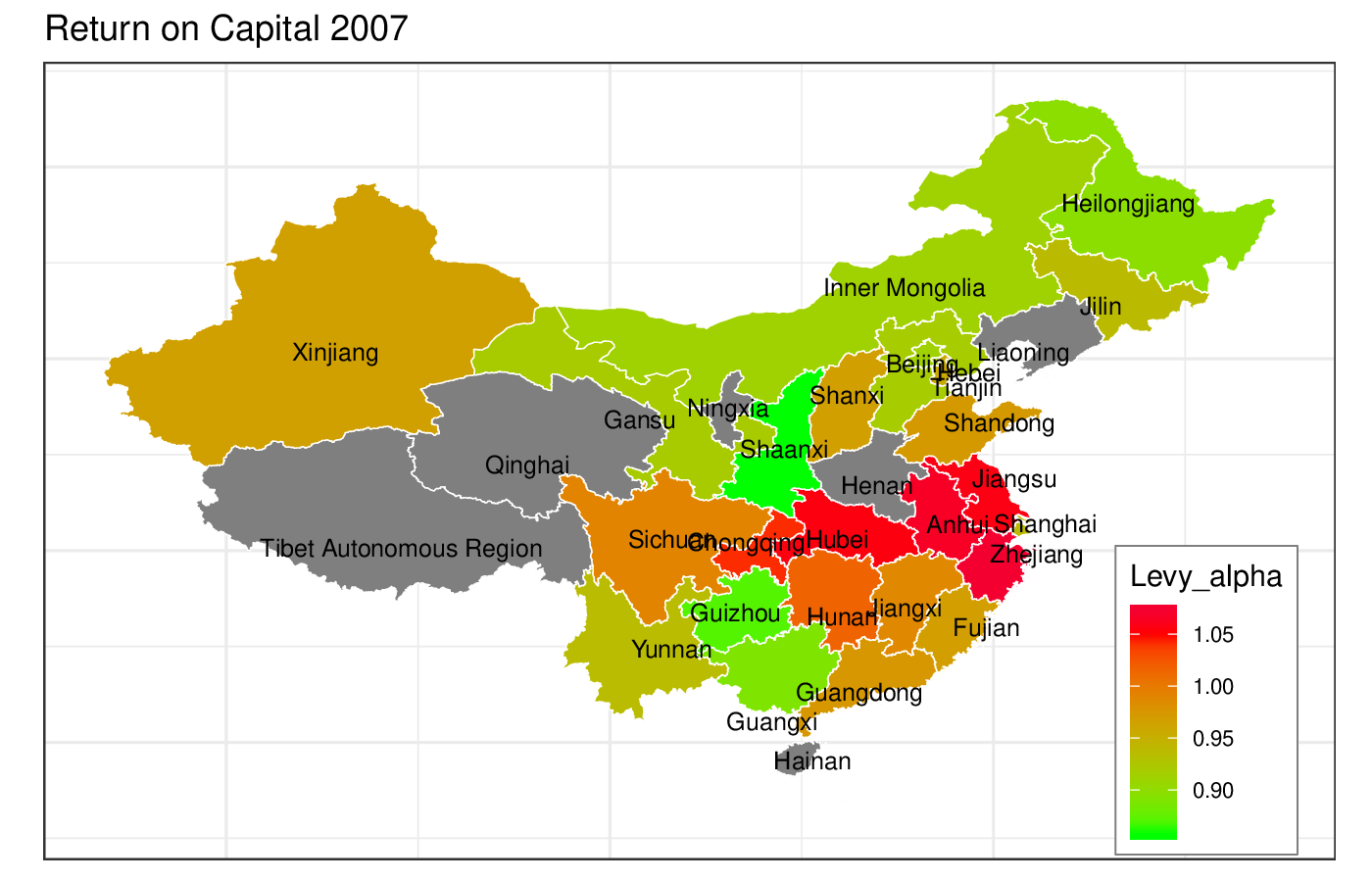

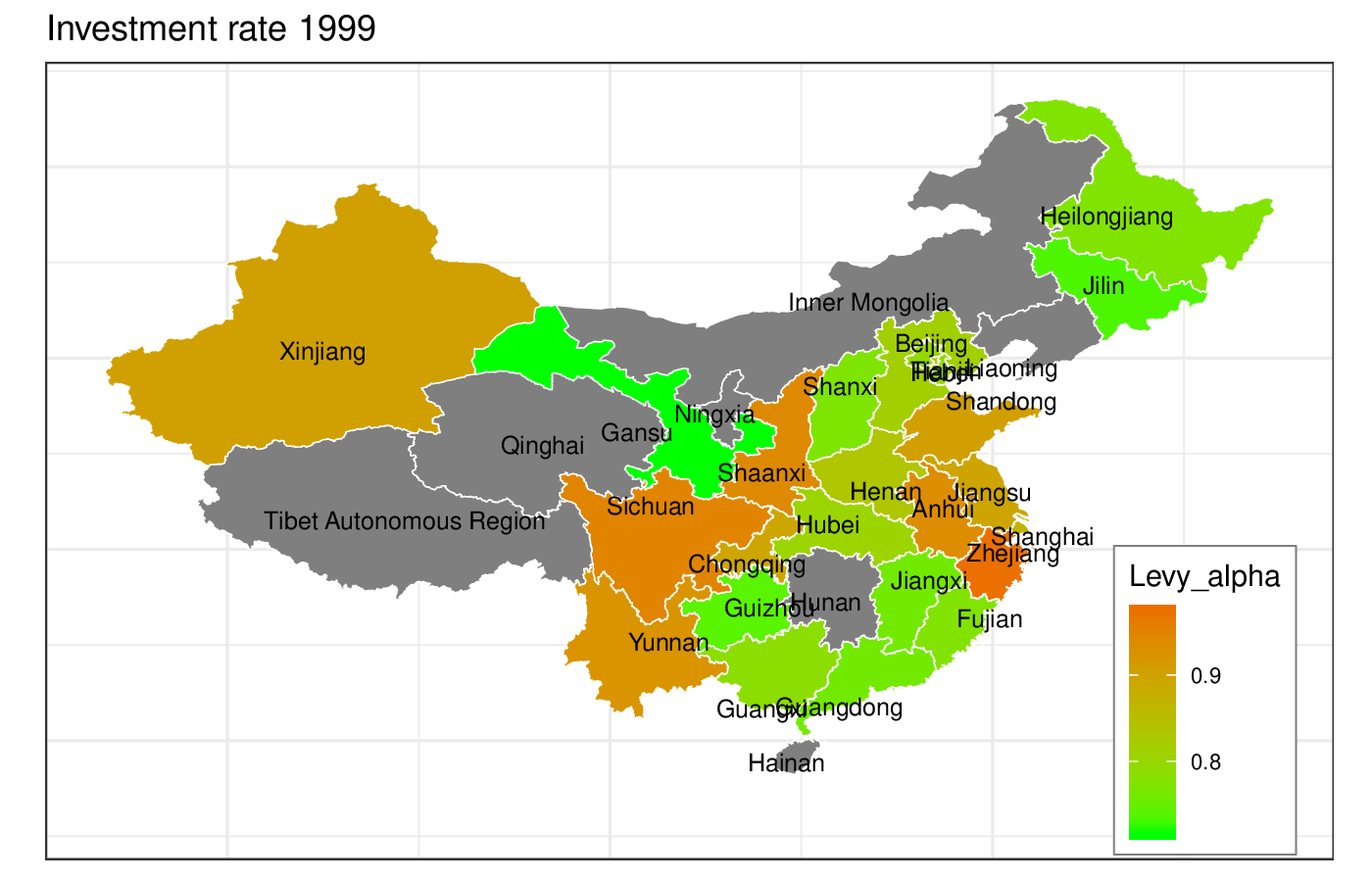

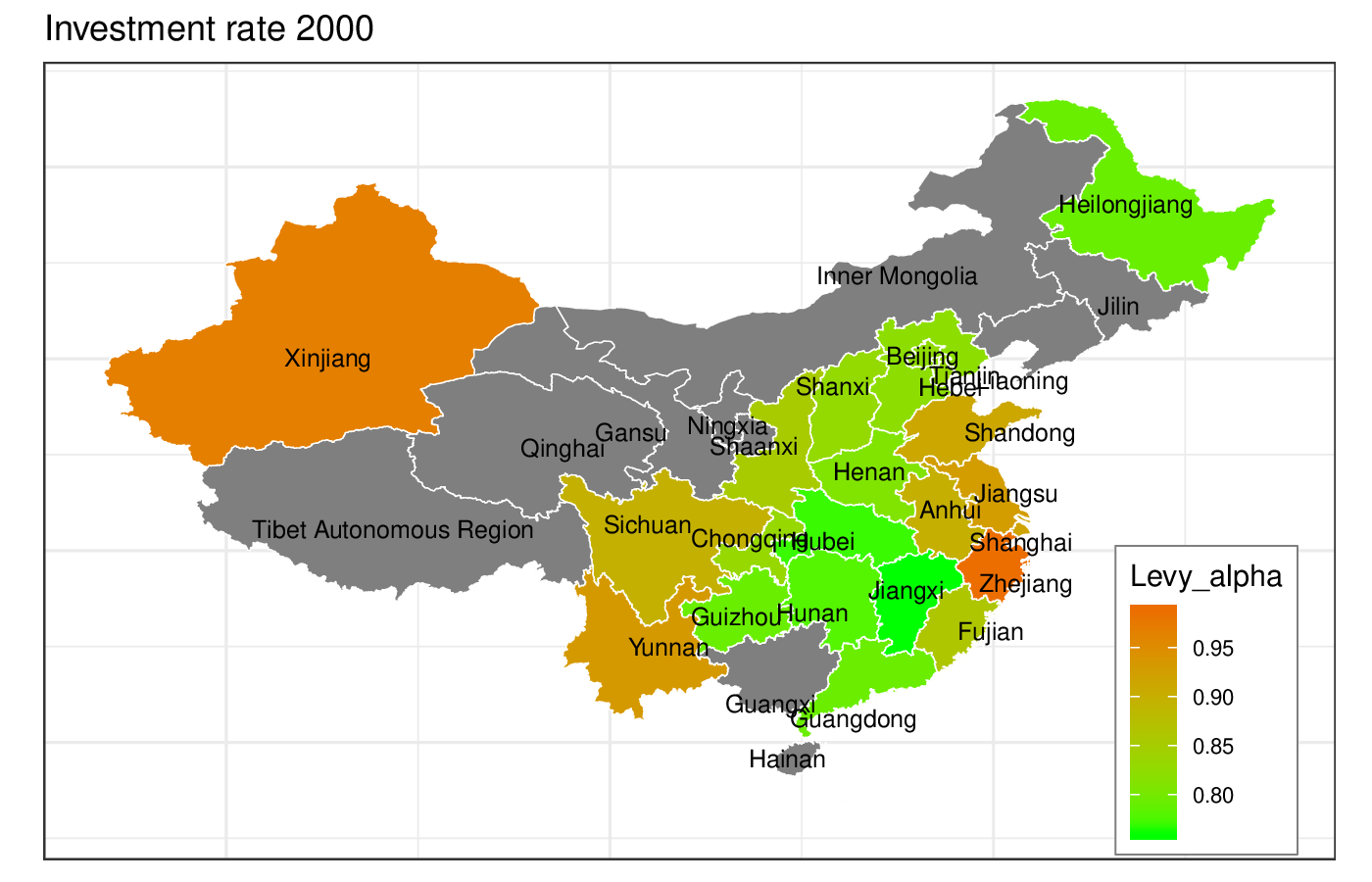

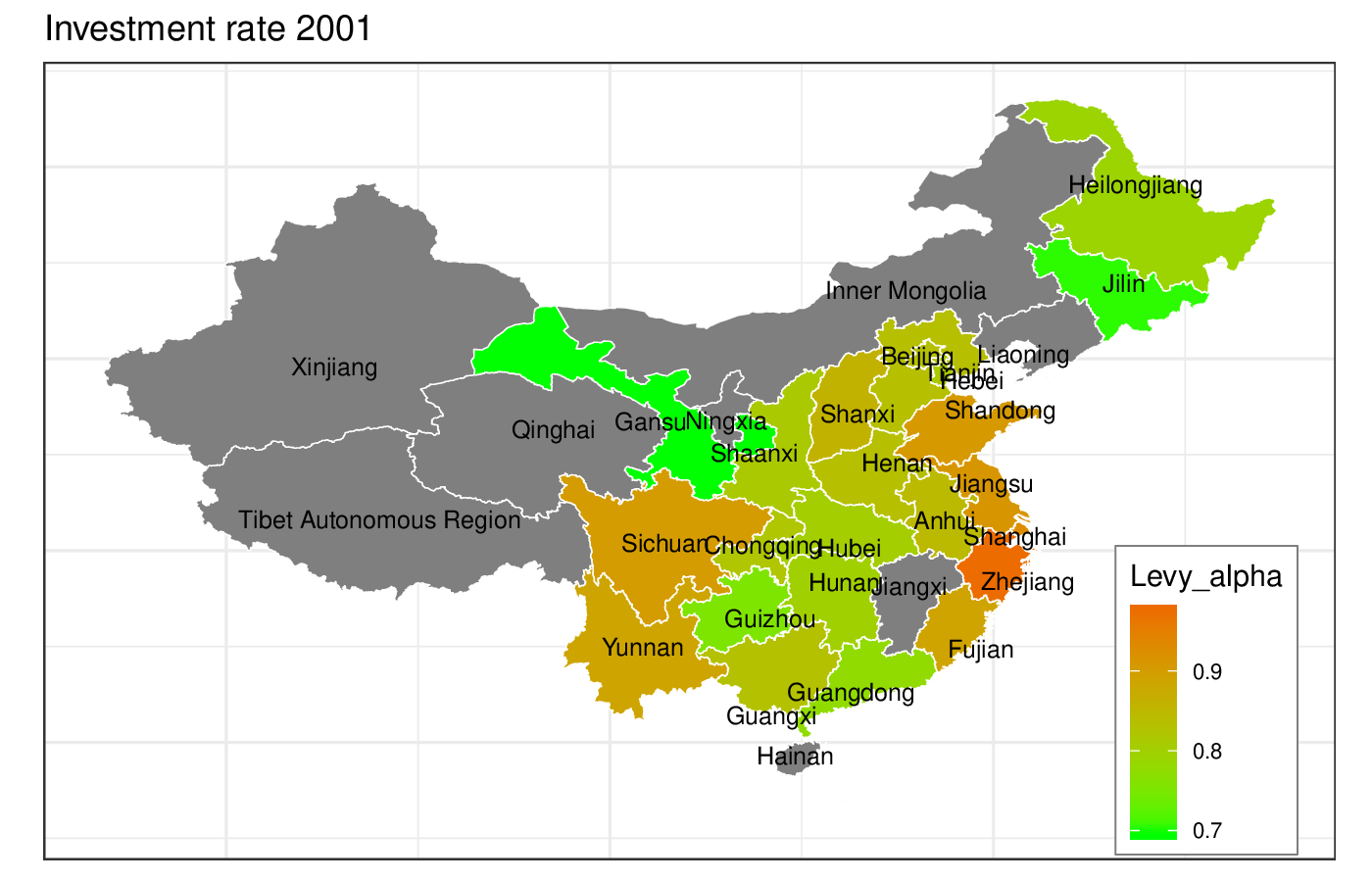

5.3 Regional variation

While we only have data for one country, the P.R. China, we can investigate regional variation by considering subsamples of the data set for the 31 Chinese provinces and autonomous regions. In cross-country studies, where the cases are not subject to the same policy decision and idiosyncratic influences, any systematic differences should be more pronounced.

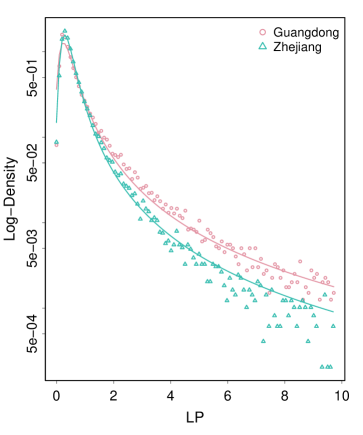

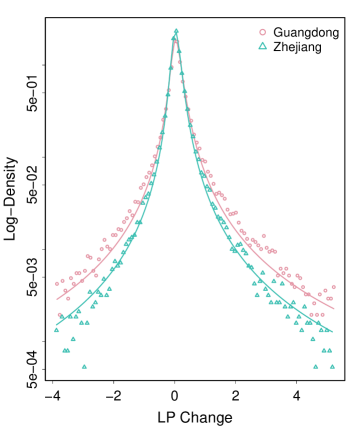

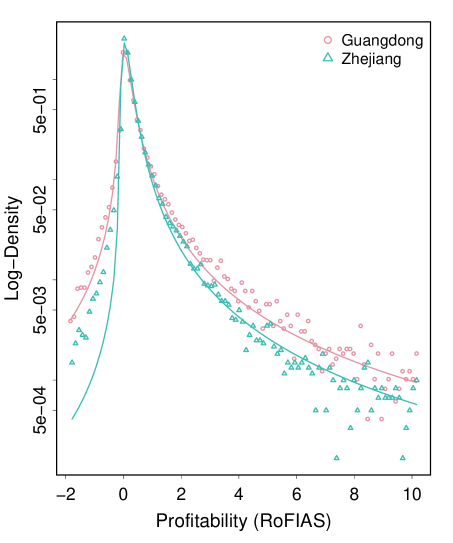

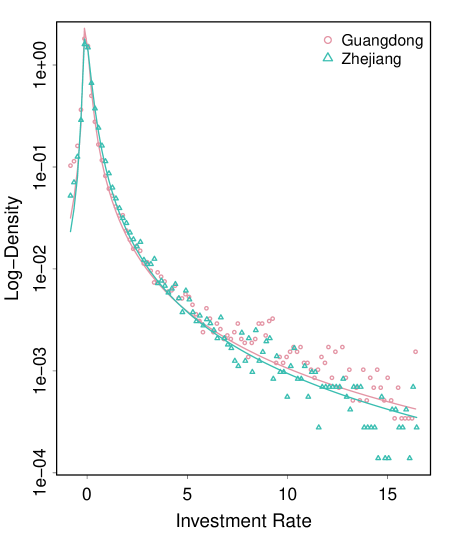

Two of the most dynamic and economically strongest regions of the PR China are Guangdong and Zhejiang. While Zhejiang is one of the most active regions supporting private economic sectors, and has benefited from the early economic boom in Yangtze River Delta, Guangdong is in South China, north of Hong Kong, and driven significantly by the opening-up endeavors. Both are coastal provinces and have the potential to develop the same industries. Yet, the regional distributions of and differ sharply and persistently. Guangdong maintains one of the lowest tail indices among all provinces, i.e. a very high probability weight in the tails ( to ). Zhejiang is at the other end of the provincial dispersion, with a moderately high tail index between and . Figure 6 shows the density of labor productivity and labor productivity change in both regions.

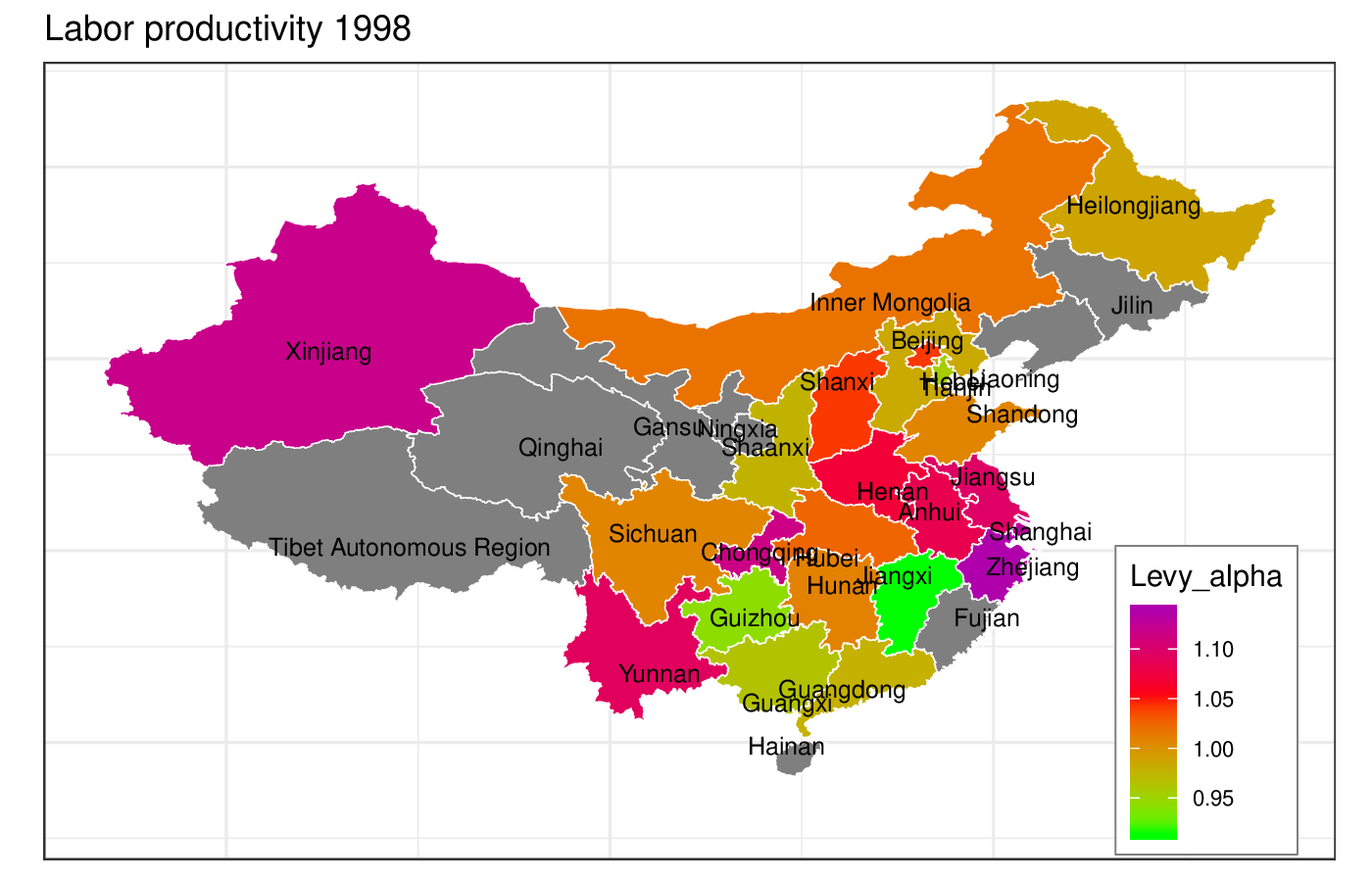

Figures 7 and 8 show the development of the tail index parameter of the Lévy alpha-stable fit of labor productivity and labor productivity change at the region level. Indeed it can be seen that Guangdong and neighboring regions (Guangxi, Jiangxi) and Zhejiang and its neighbors (Shanghai, Anhui) persistently find themselves at opposing ends of the variation. The Guangdong area tends to have longer tails (lower exponents) than the Shanghai/Zhejiang area.

Other regions with longer tails include the Northeast (Heilongjiang), the Beijing region, Inner Mongolia and, in the earlier years of the period of study, the central region. As pointed out in Heinrich and Dai (2016), this subtle change over time may reflect the transition of various regions to a standard market economy system that occurred at different time periods (see details in Heinrich and Dai (2016)). Some regions, such as Inner Mongolia, likely stand out because of regional specificities; in Inner Mongolia a domination of the mining sector with rather large firms and certain volatility of empirical labor productivity depending on world market prices for metals etc. Some regions with a smaller population of firms (Xinjiang, Guangsu) are more volatile with less confidence being warranted for these fits.

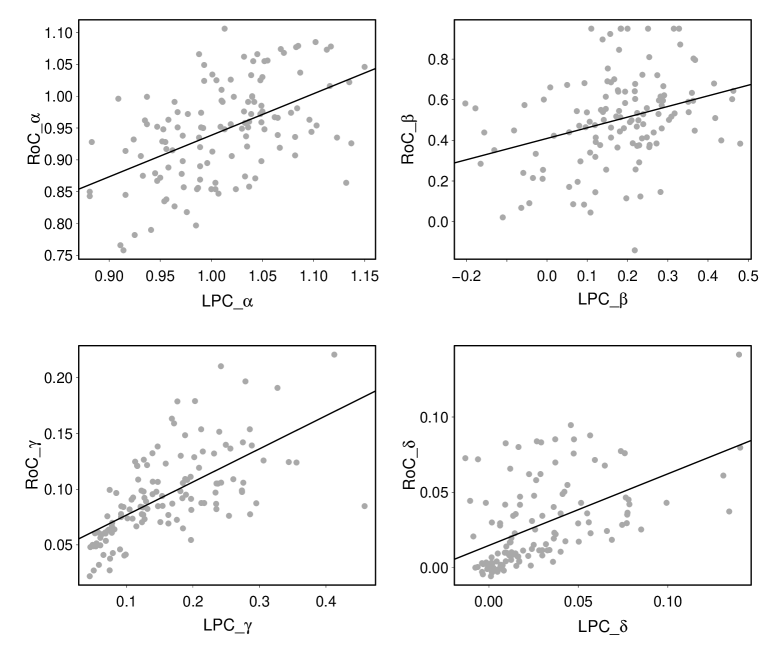

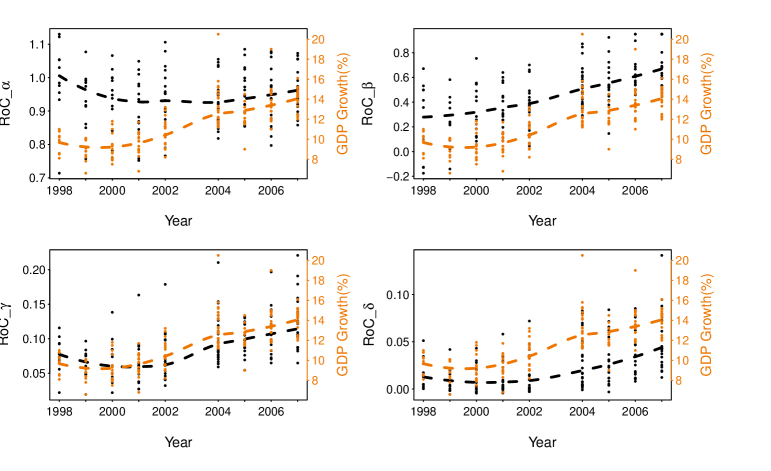

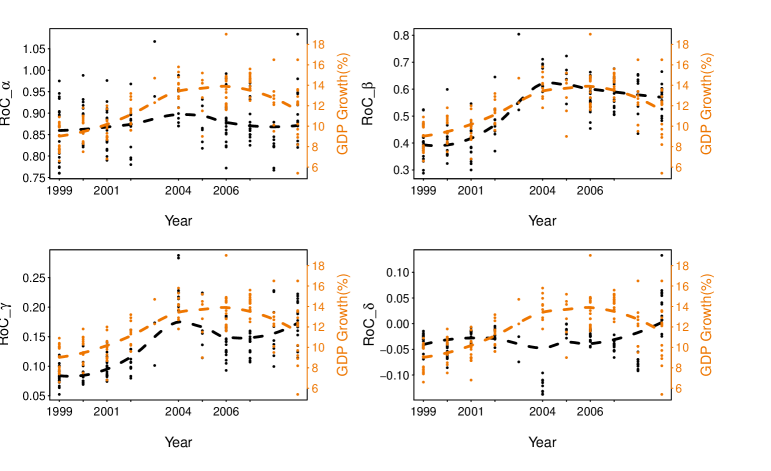

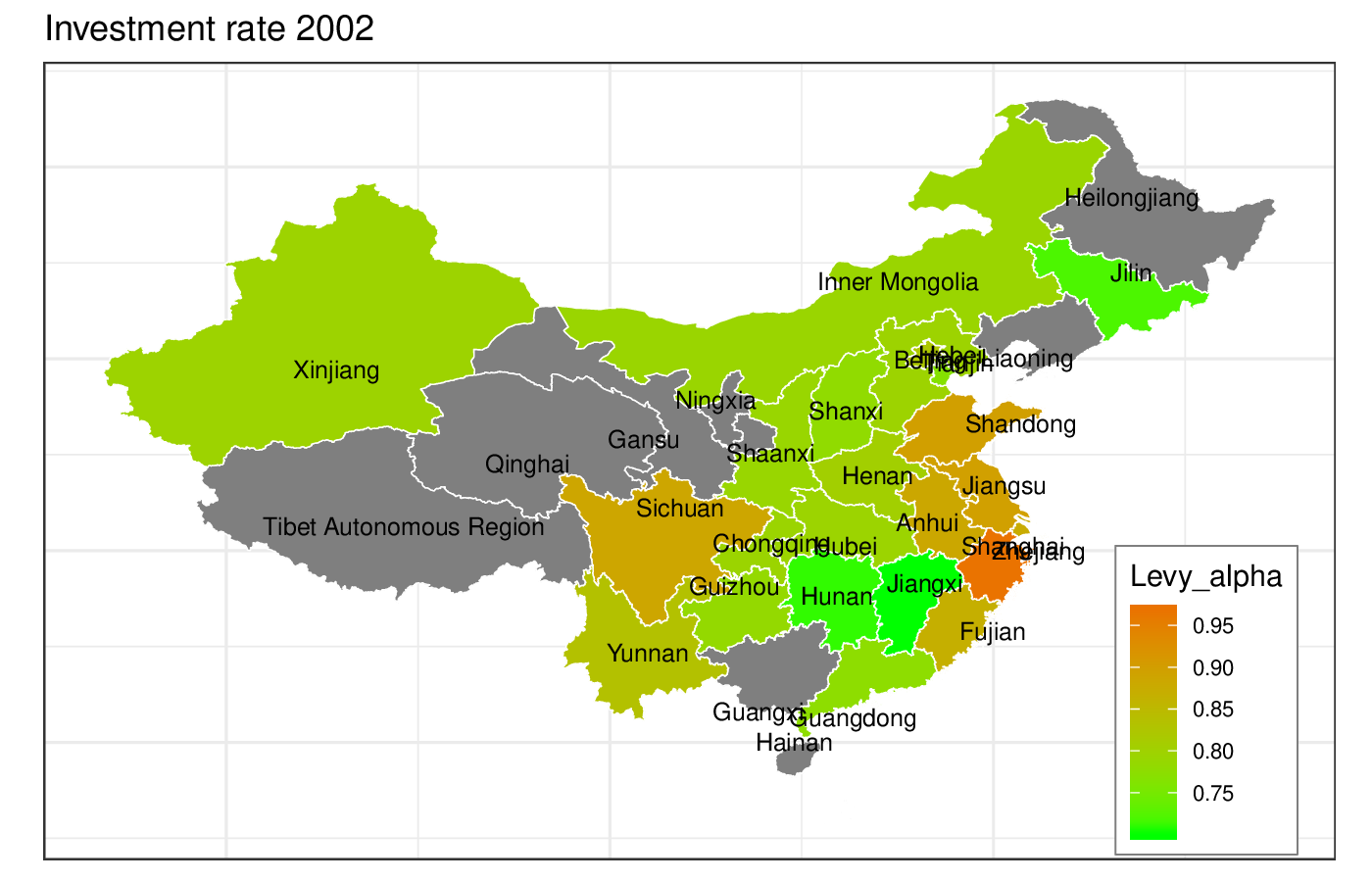

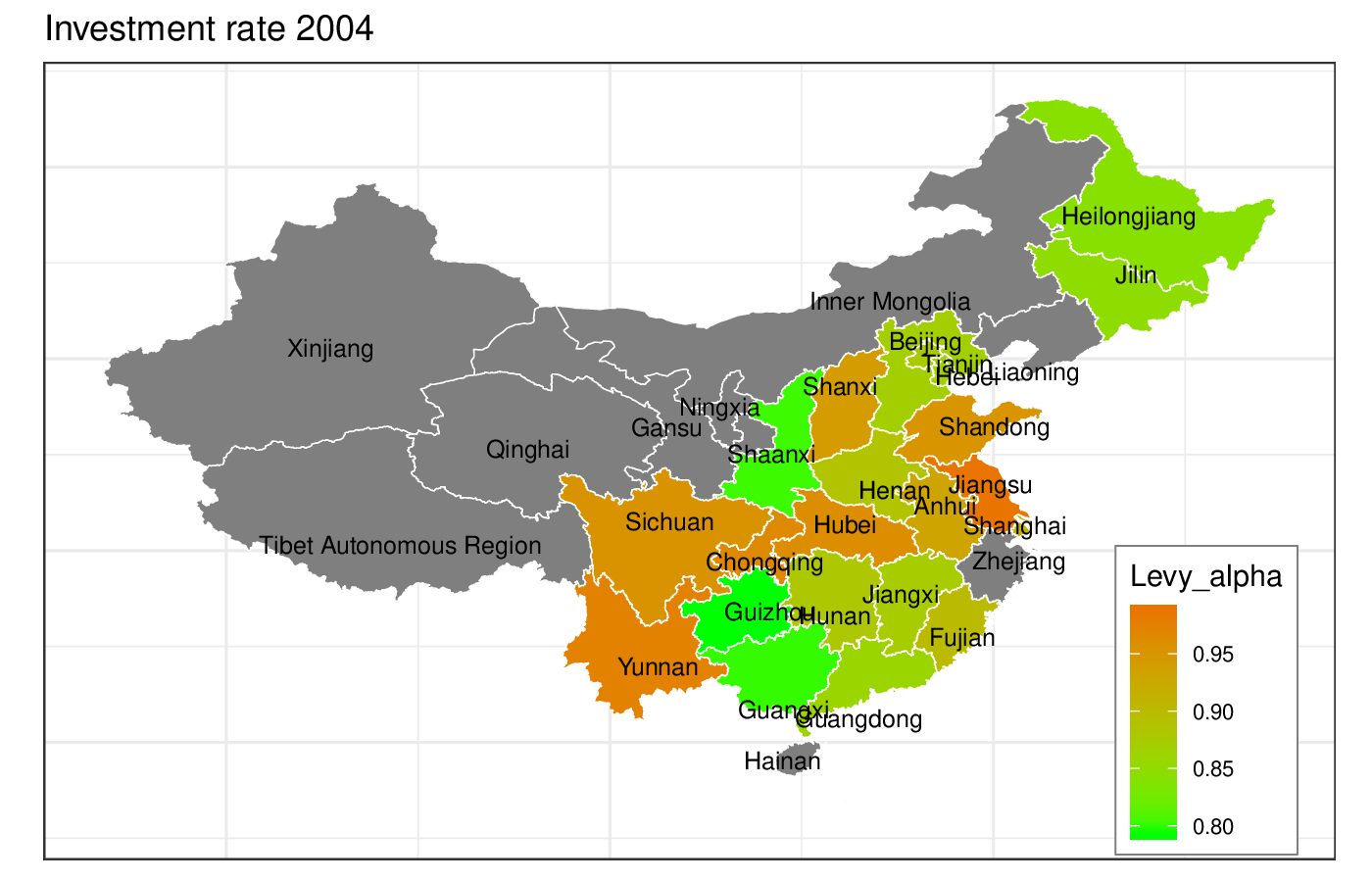

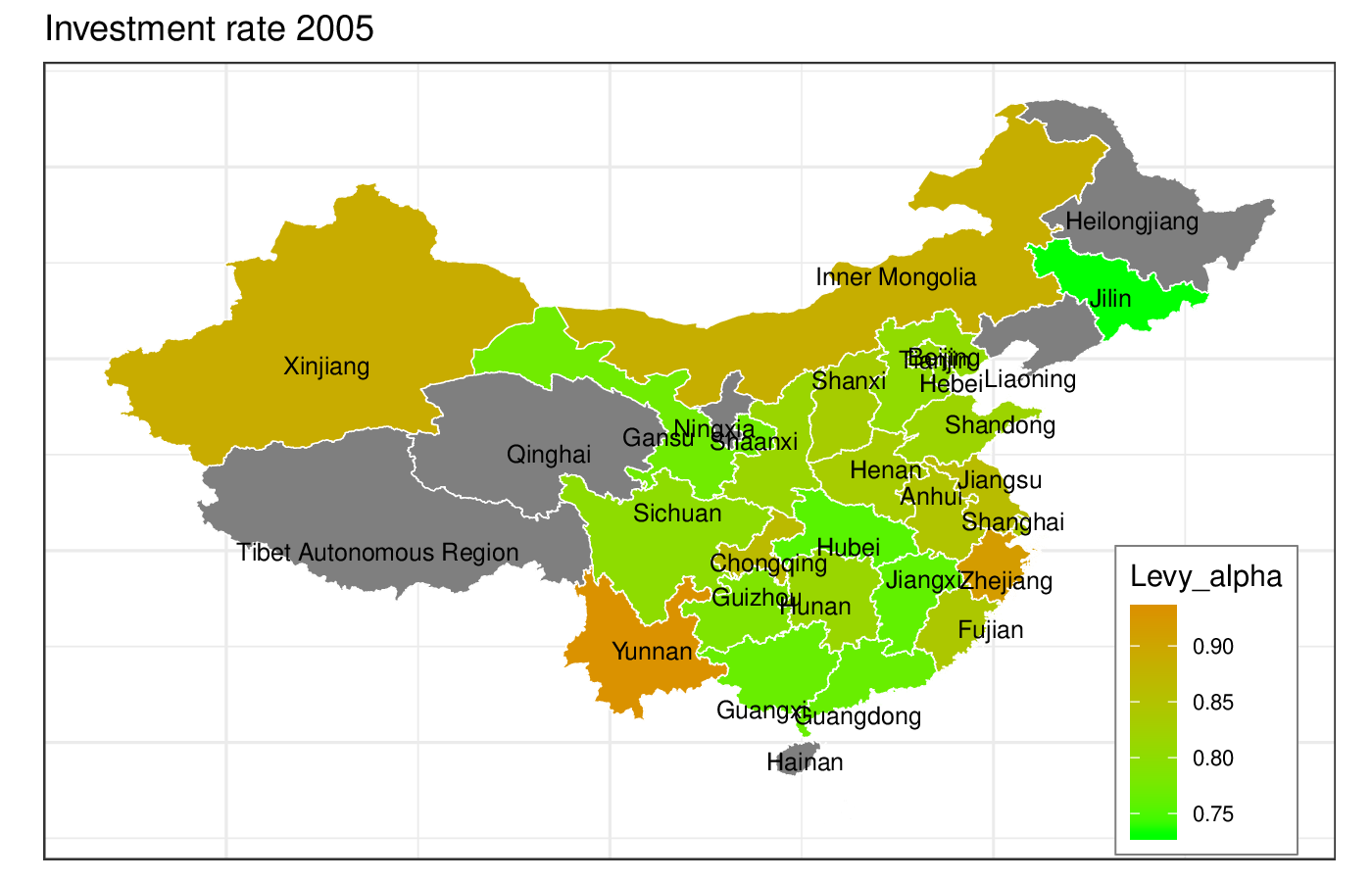

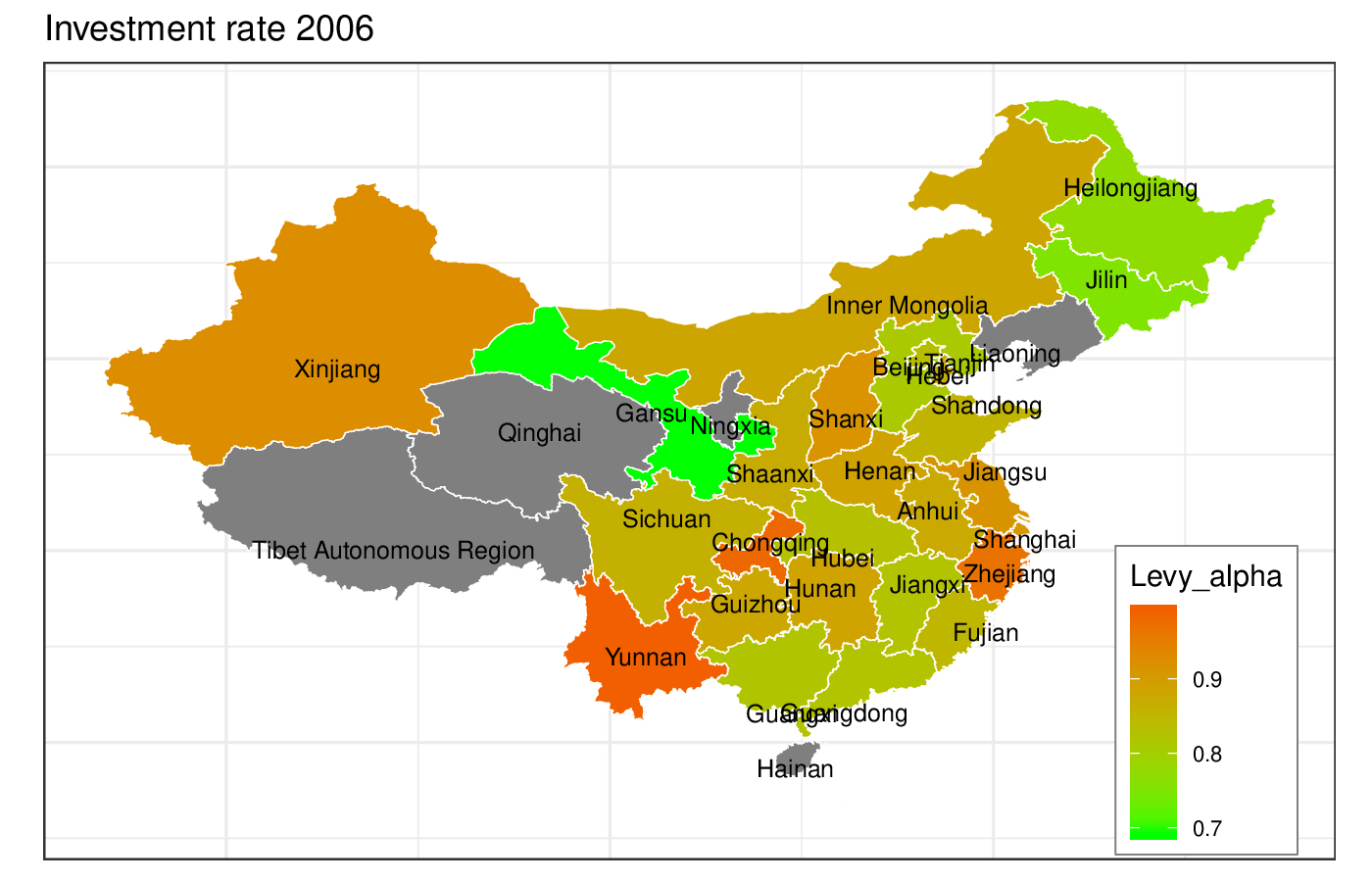

So far, we have shown that there are strong and persistent differences in the characteristics of the productivity distributions among the regions of China. This indicates that this would very likely also hold between countries. Beyond that, we can show in the Chinese case that micro-level variables are strongly interconnected: For instance, there is a cluster of regions with a shorter tail (higher tail index ) around Shanghai and Zhejiang in both (Figure 7) and (Figure 8). This regional pattern is also present in the figures for profitability and the investment rate shown in the Appendix D (Figures 21 and 22). Indeed, it can be shown that at the regional level, the distributions of the key firm-level variables are interconnected. The correlations of parameters fitted for the labor productivity change () distribution and investment rate () distribution are shown in Figure 9; those of the parameters for () and the profitability () are plotted in Figure 10. For each pair of distributions, the same parameters are highly correlated. I.e. a high tail index for the labor productivity change distribution is associated with a high tail index for the distributions of profitability and investment rate. The same is true for the skew () and the scale () of all distributions and the location of the modal value () of and distributions.161616The only exception is the parameter of the distribution of the investment rate, which is not associated with any of the other fits and appears to fall into clusters. The reason is that there is a strong time signal in this variable (Lévy parameter of ) with left shifts in the investment rate distribution in 2004 and in 2008, which may be caused by idiosyncratic shocks (such as the financial crisis hitting in 2008), by tax policy or by accounting intricacies.

These systematic regional differences evident in concert in a number of variables in the Chinese case indicate that such patterns should also be expected in cross-country comparisons. The following section will furthermore investigate relations between productivity distributions and various other macro- and micro-level variables using a Bayesian multi-level regression approach.

5.4 Relation of productivity distributions and their parameters to other economic measures

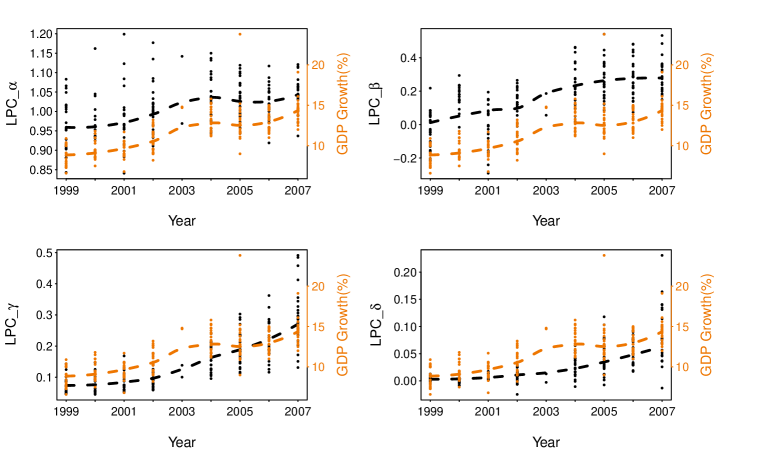

To understand how Lévy parameters of each variable are associated with the geographical predictors (in this case, Chinese regions), we run a simple mixed linear regression model. We use a Bayesian multi-level approach to properly account for group-level similarities and differences through a partial pooling. The likelihood function is written as follows:

| (5) |

where the subscript and indicate the year and province index which will be used as the main group effect variable. See Appendix B for a detailed discussion on prior specification. We assume that the outcome variable is distributed according to the Gaussian likelihood function around a mean and the standard deviation . The independent variables (predictors) include GDP growth (GDP_r), firm age, employment (Emp), as well as capital intensity () at the regional level. The firm-level variables among these (not the GDP growth) are computed using the regional averages in the data set. The intercept has two varying components by year and province along with the overall intercept.

-

•

: The overall intercept. The expected value of when all other explanatory variables are zero.

-

•

: The varying intercept effect coming from the year index. The deviation in the intercept for year from the overall intercept .

-

•

: The varying intercept effect coming from the province index. The deviation in the intercept for province from the overall intercept .

-

•

: The coefficient of GDP Growth. The expected change in across all and .

-

•

: The coefficient of Firm Age. The expected change in across all and .

-

•

: The coefficient of Employment. The expected change in across all and .

-

•

: The coefficient of Capital Intensity. The expected change in across all and .

We use the Hamiltonian Monte Carlo (HMC) to obtain a sequence of random samples from a posterior probability distribution. We use the Bayesian programming language Stan and the R-package brms that operationalize the HMC algorithm to efficiently compute posterior distributions (Stan Development

Team, 2015; Bürkner, 2017). For a more detailed discussion on HMC and Stan, see (Gelman et al., 2014; Carpenter et al., 2017).

Table 4 summarizes the estimation results for each variable and parameter. We only report the mean and standard deviation (in parenthesis) of the posterior distribution of each parameter. A full summary table can be found in the Appendix 22.

| Variable | Parameters | Intercept | GDP Growth | Firm Age | Employment | Capital Intensity |

| LP Change | 0.9841 (0.0462) | 0.0083 (0.0027) | -0.0012 (0.0006) | -0.0001 (0.0001) | -0.0001 (0.0001) | |

| -0.0564 (0.1025) | 0.0256 (0.0065) | -0.0035 (0.0014) | 0 (0.0001) | -0.0001 (0.0002) | ||

| 0.0555 (0.0466) | 0.0094 (0.0026) | 0 (0.0005) | -0.0002 (0.0001) | 0.0004 (0.0001) | ||

| -0.0105 (0.024) | 0.0054 (0.0014) | -0.0001 (0.0003) | -0.0001 (0) | 0 (0) | ||

| LP | 1.0823 (0.0509) | 0.0007 (0.0031) | -0.0001 (0.0002) | -0.0001 (0.0001) | -0.0001 (0.0001) | |

| 0.2304 (0.063) | 0.0054 (0.0032) | 0 (0.0002) | -0.0005 (0.0001) | 0.0004 (0.0001) | ||

| 0.2574 (0.0681) | 0.009 (0.0035) | 0 (0.0002) | -0.0005 (0.0001) | 0.0003 (0.0001) | ||

| RoC | 1.1235 (0.0564) | -0.0033 (0.0033) | -0.0008 (0.0002) | -0.0003 (0.0001) | -0.0001 (0.0001) | |

| 0.167 (0.1337) | 0.0333 (0.0081) | 0 (0.0004) | -0.0003 (0.0002) | -0.0001 (0.0002) | ||

| 0.0713 (0.0208) | 0.0034 (0.0012) | -0.0001 (0.0001) | 0 (0) | -0.0001 (0) | ||

| 0.0341 (0.0181) | 0.0018 (0.0011) | 0 (0.0001) | -0.0001 (0) | -0.0001 (0) | ||

| Inv Rate | 0.7954 (0.0486) | 0.0004 (0.0025) | -0.0014 (0.0008) | 0.0002 (0.0001) | 0.0002 (0.0001) | |

| 0.4201 (0.0955) | 0.0047 (0.0044) | 0.0005 (0.0015) | -0.0001 (0.0001) | 0.0001 (0.0002) | ||

| 0.122 (0.0286) | 0.0028 (0.0016) | -0.0007 (0.0005) | 0 (0) | 0 (0.0001) | ||

| -0.0687 (0.0191) | -0.0001 (0.0009) | -0.0001 (0.0003) | 0.0001 (0) | 0 (0) |

For each variable, we show the regression results for Lévy parameters. Note that we do not report on the regression of in the labor productivity variable since it is always very close to 1 (maximal skewness) and doesn’t have much variation.

GDP Growth

:

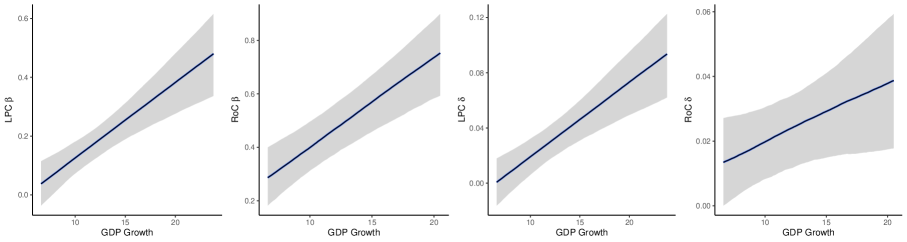

A higher regional economic growth tends to be associated with a higher , and in and profitability. The GDP coefficients in labor productivity and investment rate tend to be rather noisy except for . parameter is only informative in the case: the higher the provincial GDP growth the higher and thus the thinner the tails. in other variables has neither enough variation nor a clear pattern in relation to regional GDP growth. Figure 11 shows the marginal effects of GDP Growth on key parameters. From this, we can infer that the economic growth in China is characterized by four distinctive patterns. As the economy grows in China, 1) firms become more technologically dynamic and more profitable (a high in and profitability), 2) the economy has an increasing number of highly innovative and profitable firms (a high in and profitability), 3) firms become more diverse in their performance (a high in , , profitability and investment rate), and 4) the technological competition among firms gets more fierce over time (a high in ).

Firm Age

:

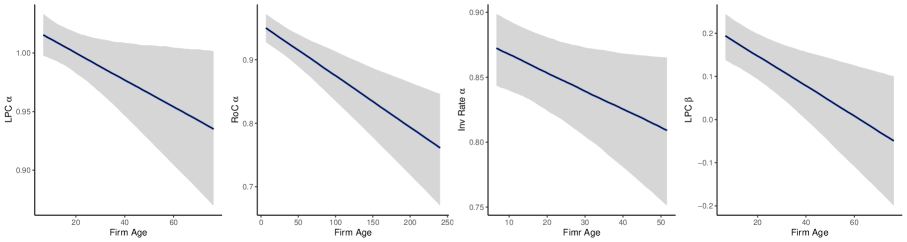

The higher the average firm age, the lower and thus heavier tails in , profitability, and Investment rate, and the lower in . and are very noisy in all parameters except for in profitability and investment rate. Figure 12 shows the marginal effects of firm age on key parameters. From this, we can infer that, when the province has a higher average firm age, 1) the market tends to be less competitive for technological change, profitability, and firm growth (a low in , profitability, and investment rate), 2) the economy has an increasing number of less innovative firms (a low in ), and 3) the firm performance in terms of profitability and investment tends to be diverse but with a relatively high degree of uncertainty.

Employment

:

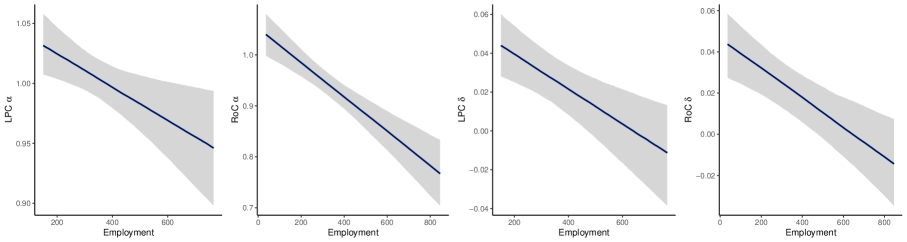

A larger average employment size is associated with a lower in , , profitability, a lower in profitability, a lower in , , and a lower in and Profitability. Investment Rate has a somewhat different pattern and has a positive relationship between employment size and and . Figure 13 shows the marginal effects of employment on key parameters. From this, we can infer that, when the province has larger size firms with a high number of employees, 1) the market tends to become less competitive overall (a low in , , profitability), 2) firms become less technologically dynamic and more profitable (a low in and profitability), and 3) firms become less diverse in their performance in technological change (a low in and ).

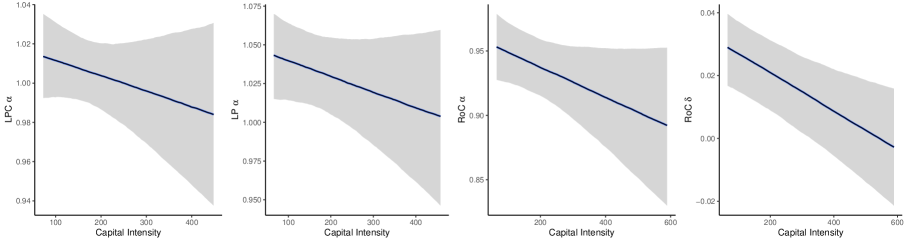

Capital Intensity

:

Higher average capital intensity is associated with a lower in , , and Profitability but a higher in the Investment rate, a higher in and , and a lower in profitability. Figure 14 shows the marginal effects of capital intensity on key parameters. From this, we can infer that, as the province has more firms with a higher capital intensity (a higher degree of mechanization), 1) the market tends to become less competitive overall (a low in , , profitability), 2) firms become more diverse in their performance in technological change (a high in and ), and 3) the firms tend to be less profitable overall (a low in profitability).

6 Conclusion

The distribution of productivity at the firm level has, like other economic quantities, been thoroughly investigated in recent years. For the developed economies, many stylized facts are known now: The distribution is unimodal, strongly right-skewed, has heavy tails, and is persistent in time. Yang et al. (2019), who also summarize the state of the art, report no systematic changes in their study covering millions of observations for European developed countries over a period of 10 years.

It is a fair question to ask if we might have systematic changes in developing countries, since these countries experience more rapid structural, demographic, and technological changes. Is the distribution the same? Do the parameter estimates show any trends? If so, what does that tell us about the development process and about development policy? Can and should productivity distributions be managed?

While we cannot provide direct evidence for the entire developing world, we did offer evidence for one country, the PR China as an example in this paper. Our study covers a crucial period of Chinese history, 1998-2007 (and further to 2013 with less reliable data), a period in which the country experienced the highest growth rates; when the economy and the technology sector took off; when the Chinese converged to the consumption and lifestyle habits of the developed world.

We demonstrated that the distributions of a wide range of quantities at the firm-level are heavy-tailed with a Lévy alpha-stable distribution being an excellent distributional model and clearly superior to the alternative AEP distribution that was also tested. This includes labor productivity () and labor productivity change (). Consistent with the developed economies, both the shape of the distribution and the parameter values were remarkably consistent over time.

However, we did find a systematic shift: The location parameter of both productivity and productivity change were steadily increasing over the period of the study. The scale parameter followed suit. Tail index () and skew () were stable for the productivity level, but for the productivity change, the tail grew shorter ( increasing) and the distribution developed a right skew ( increasing). What this means is that the productivity gains China experienced in the period of study do not come from super-star firms of exceptionally high productivity: The tail weight of remained unchanged and that of decreased. Instead, labor productivity increases became more consistent, concentrated, and uniform across the economy (decreasing tail weight of ) and the body of labor productivity change extended to the right (emerging right-skew).

Further, we showed that there are significant and systematic differences across the regions of China that persist in time over the period of the study. This is even the case for differences for superficially similar regions such as the technology centers of Guangdong and Zhejiang/Shanghai. If this can be shown for the regions of China, that are subject to similar policies, environmental factors, and idiosyncratic shocks, differences in cross-country studies with multiple developing countries would be expected to be more pronounced.

Nevertheless, there were systematic relations between the parameters of the productivity distribution, a range of other distributions of micro-level variables (profitability, capital intensity, firm age), as well as macro-level characteristics (GDP growth, employment) of the respective regions, as shown in our Bayesian multi-level regression in Section 5.4.

The tail indices of the distributions were found to be between and in most cases, implying infinite variance (since ) and very slow convergence to the theoretical mean, if the mean even exists (only for ). As a consequence, characteristics of the labor productivity distribution in the form of moments would be avoided. Such characteristics are, however, commonly given as variants of direct moments, the mean for the location, the variance, standard deviation, or Olley-Pakes gap for the dispersion. Hsieh and Klenow (2009) for instance, in his otherwise exemplary study of misallocation in China and India, uses sample variances.

What does this mean for development policy? First, concentration on super-star firms - be that domestic ones or branches of foreign groups - might be the wrong approach for successful technological catch-up. It would certainly be a different approach from that taken in China. Second, it instead seems important to ensure that productivity gains can also be realized by other firms. The most direct approach for this is encouraging technology transfer and providing incentives for sourcing intermediate products locally (which would also lead to cooperation and technology transfer). Technologies are arguably the most important factor in determining productivity at the firm level. Third, other factors such as instrumental institutions and a comprehensive education system could support this process. Fourth, significant differences would be expected between different countries. Direct comparisons of the parameters of productivity distributions in isolation are likely of only limited value. Instead, such comparisons should be done with a range of measures for the economic micro-structure at the firm level (productivity, age, capital intensity, etc.) while also taking the intertemporal development of these variables into account. Fifth, particular skepticism is advised with respect to measures that rely on moments of the productivity distribution (or similar quantities), as these may not exist. An example is the use of variance as a dispersion indicator, which will certainly fail.

While our findings are encouraging, more research is needed to confirm our findings for other developing countries. Do firm-level data in India, Vietnam, Nigeria, and other rapidly developing countries have the same characteristics? Can catch-up processes like the one showcased here be repeated in still other developing economies in the future? What impact might the Covid-19 pandemic have, that changed the face of the world economy by hitting many developed economies, but also some individual developing countries (like Tanzania) very hard?

Finally, can our example teach us something about the development history of European and other developed countries, the USA, Japan, South Korea? These countries’ catch-up phases were much longer ago in history, at a time, when economic microdata were not collected to the same extent as today. We may be unable to reconstruct the microdata, but it may still be possible to infer how the development process unfolded.

References

- Adamopoulos and Restuccia (2014) Adamopoulos, T. and Restuccia, D. (2014). The size distribution of farms and international productivity differences. American Economic Review, 104(6):1667–97.

- Akaike (1973) Akaike, H. (1973). Maximum likelihood identification of Gaussian autoregressive moving average models. Biometrika, 60(2):255–265.

- Angelini and Generale (2008) Angelini, P. and Generale, A. (2008). On the evolution of firm size distributions. American Economic Review, 98(1):426–38.

- Asquith (2018) Asquith, W. (2018). lmomco - L-moments, censored L-moments, trimmed L-moments, L-comoments, and many distributions. R package version 2.3.1.

- Asquith (2014) Asquith, W. H. (2014). Parameter estimation for the 4-parameter asymmetric exponential power distribution by the method of l-moments using r. Computational Statistics & Data Analysis, 71:955 – 970.

- Au and Henderson (2006) Au, C.-C. and Henderson, J. V. (2006). How migration restrictions limit agglomeration and productivity in China. Journal of Development Economics, 80(2):350–388.

- Axtell (2001) Axtell, R. L. (2001). Zipf distribution of U.S. firm sizes. Science, 293(5536):1818–1820.

- Bartelsman et al. (2013) Bartelsman, E., Haltiwanger, J., and Scarpetta, S. (2013). Cross-country differences in productivity: The role of allocation and selection. American Economic Review, 103(1):305–34.

- Beaudry and Schiffauerova (2009) Beaudry, C. and Schiffauerova, A. (2009). Who’s right, marshall or jacobs? the localization versus urbanization debate. Research Policy, 38(2):318 – 337.

- Berlingieri et al. (2017) Berlingieri, G., Blanchenay, P., and Criscuolo, C. (2017). The great divergence(s). OECD Science, Technology and Industry Policy Papers, 39.

- Bloom et al. (2010) Bloom, N., Mahajan, A., McKenzie, D., and Roberts, J. (2010). Why do firms in developing countries have low productivity? American Economic Review, 100(2):619–23.

- Boeing et al. (2016) Boeing, P., Mueller, E., and Sandner, P. (2016). China’s R&D explosion - analyzing productivity effects across ownership types and over time. Research policy, 45(1):159–176.

- Borensztein and Ostry (1996) Borensztein, E. and Ostry, J. D. (1996). Accounting for China’s growth performance. The American Economic Review, 86(2):224–228.

- Bosworth and Collins (2008) Bosworth, B. and Collins, S. M. (2008). Accounting for growth: comparing China and India. Journal of Economic Perspectives, 22(1):45–66.

- Bottazzi et al. (2007) Bottazzi, G., Cefis, E., Dosi, G., and Secchi, A. (2007). Invariances and diversities in the patterns of industrial evolution: Some evidence from italian manufacturing industries. Small Business Economics, 29(1-2):137–159.

- Bottazzi and Secchi (2006) Bottazzi, G. and Secchi, A. (2006). Explaining the distribution of firm growth rates. The RAND Journal of Economics, 37(2):235–256.

- Bottazzi and Secchi (2011) Bottazzi, G. and Secchi, A. (2011). A new class of asymmetric exponential power densities with applications to economics and finance. Industrial and corporate change, 20(4):991–1030.

- Brandt et al. (2008) Brandt, L., Hsieh, C.-T., and Zhu, X. (2008). Growth and structural transformation in China. In Brandt, L. and Rawski, T. G., editors, China’s Great Economic Transformation, page 683–728. Cambridge University Press.

- Brandt et al. (2017) Brandt, L., Van Biesebroeck, J., Wang, L., and Zhang, Y. (2017). Wto accession and performance of chinese manufacturing firms. American Economic Review, 107(9):2784–2820.

- Brandt et al. (2012) Brandt, L., Van Biesebroeck, J., and Zhang, Y. (2012). Creative accounting or creative destruction? firm-level productivity growth in chinese manufacturing. Journal of Development Economics, 97(2):339–351.

- Brandt et al. (2014) Brandt, L., Van Biesebroeck, J., and Zhang, Y. (2014). Challenges of working with the chinese nbs firm-level data. China Economic Review, 30:339–352.

- Bürkner (2017) Bürkner, P.-C. (2017). brms: An R package for Bayesian multilevel models using Stan. Journal of Statistical Software, 80(1):1–28.

- Cabral and Mata (2003) Cabral, L. M. B. and Mata, J. (2003). On the evolution of the firm size distribution: Facts and theory. American Economic Review, 93(4):1075–1090.

- Cao and Birchenall (2013) Cao, K. H. and Birchenall, J. A. (2013). Agricultural productivity, structural change, and economic growth in post-reform China. Journal of Development Economics, 104:165–180.

- Carpenter et al. (2017) Carpenter, B., Gelman, A., Hoffman, M. D., Lee, D., Goodrich, B., Betancourt, M., Brubaker, M., Guo, J., Li, P., and Riddell, A. (2017). Stan: A probabilistic programming language. Journal of statistical software, 76(1).

- Carrasco et al. (2007) Carrasco, M., Florens, J.-P., and Renault, E. (2007). Linear inverse problems in structural econometrics estimation based on spectral decomposition and regularization. Handbook of econometrics, 6:5633–5751.

- Chaffai et al. (2012) Chaffai, M., Kinda, T., and Plane, P. (2012). Textile manufacturing in eight developing countries: Does business environment matter for firm technical efficiency? The Journal of Development Studies, 48(10):1470–1488.

- Chen et al. (2009) Chen, K.-H., Huang, Y.-J., and Yang, C.-H. (2009). Analysis of regional productivity growth in China: A generalized metafrontier MPI approach. China Economic Review, 20(4):777–792.

- Chow and Li (2002) Chow, G. C. and Li, K.-W. (2002). China’s economic growth: 1952–2010. Economic Development and Cultural Change, 51(1):247–256.

- Chudnovsky et al. (2006) Chudnovsky, D., López, A., and Pupato, G. (2006). Innovation and productivity in developing countries: A study of argentine manufacturing firms’ behavior (1992–2001). Research Policy, 35(2):266 – 288.

- Coad and Tamvada (2012) Coad, A. and Tamvada, J. P. (2012). Firm growth and barriers to growth among small firms in india. Small Business Economics, 39(2):383–400.

- di Giovanni et al. (2011) di Giovanni, J., Levchenko, A. A., and Rancière, R. (2011). Power laws in firm size and openness to trade: Measurement and implications. Journal of International Economics, 85(1):42 – 52.

- Ding et al. (2016) Ding, S., Guariglia, A., and Harris, R. (2016). The determinants of productivity in chinese large and medium-sized industrial firms, 1998–2007. Journal of Productivity Analysis, 45(2):131–155.

- Emberchts et al. (1997) Emberchts, P., Kluppelberg, C., and Mikosch, T. (1997). Time series analysis for heavy-tailed processes. In Modelling Extremal Events,, pages 371–412. Springer, Berlin, Heidelberg.

- Fariñas and Ruano (2004) Fariñas, J. C. and Ruano, S. (2004). The dynamics of productivity: A decompostion approach using distribution functions. Small Business Economics, 22(3-4):237–251.

- Frank (2009) Frank, S. A. (2009). The common patterns of nature. Journal of Evolutionary Biology, 22(8):1563–1585.

- Fujimoto et al. (2011) Fujimoto, S., Ishikawa, A., Mizuno, T., and Watanabe, T. (2011). A new method for measuring tail exponents of firm size distributions. Economics: The Open-Access, Open-Assessment E-Journal, 5(1-20).

- Gabaix (2011) Gabaix, X. (2011). The granular origins of aggregate fluctuations. Econometrica, 79(3):733–772.

- Gaffeo et al. (2003) Gaffeo, E., Gallegati, M., and Palestrini, A. (2003). On the size distribution of firms: additional evidence from the G7 countries. Physica A: Statistical Mechanics and its Applications, 324(1-2):117 – 123. Proceedings of the International Econophysics Conference.

- Gelman et al. (2014) Gelman, A., Carlin, J. B., Stern, H. S., Dunson, D. B., Vehtari, A., and Rubin, D. B. (2014). Bayesian data analysis, volume 2. CRC press Boca Raton, FL.

- Gelman et al. (2017) Gelman, A., Simpson, D., and Betancourt, M. (2017). The prior can often only be understood in the context of the likelihood. Entropy, 19(10):555.

- Gong (2018) Gong, B. (2018). Agricultural reforms and production in China: Changes in provincial production function and productivity in 1978–2015. Journal of Development Economics, 132:18–31.