Acceptability Maximization

| Abstract: | The aim of this paper is to study the optimal investment problem by using coherent acceptability indices (CAIs) as a tool to measure the portfolio performance. We call this problem the acceptability maximization. First, we study the one-period (static) case, and propose a numerical algorithm that approximates the original problem by a sequence of risk minimization problems. The results are applied to several important CAIs, such as the gain-to-loss ratio, the risk-adjusted return on capital and the tail-value-at-risk based CAI. In the second part of the paper we investigate the acceptability maximization in a discrete time dynamic setup. Using robust representations of CAIs in terms of a family of dynamic coherent risk measures (DCRMs), we establish an intriguing dichotomy: if the corresponding family of DCRMs is recursive (i.e. strongly time consistent) and assuming some recursive structure of the market model, then the acceptability maximization problem reduces to just a one period problem and the maximal acceptability is constant across all states and times. On the other hand, if the family of DCRMs is not recursive, which is often the case, then the acceptability maximization problem ordinarily is a time-inconsistent stochastic control problem, similar to the classical mean-variance criteria. To overcome this form of time-inconsistency, we adapt to our setup the set-valued Bellman’s principle recently proposed in [KR19] applied to two particular dynamic CAIs - the dynamic risk-adjusted return on capital and the dynamic gain-to-loss ratio. The obtained theoretical results are illustrated via numerical examples that include, in particular, the computation of the intermediate mean-risk efficient frontiers. |

|---|---|

| Keywords: | acceptability index, acceptability maximization, optimal portfolio, gain-to-loss ratio, dynamic performance measures, tail-value-at-risk, set-valued Bellman principle |

| MSC2010: | 91G10, 93E20, 93E35, 90C35, 91B30, 49L20 |

1 Introduction

The renowned Sharpe ratio, introduced in [Sha64], besides being one of the best known tools in measuring the performance of financial portfolios, also played an important role in developing the portfolio optimization theory. It is well-known that one of the major shortcomings of the Sharpe ratio, as a performance measure, is its lack of monotonicity, i.e. a portfolio with strictly larger future gains may have a smaller Sharpe ratio. Over the years, in particular to overcome this drawback, a number of performance measures were introduced such as the Gini ratio [SY84], the MAD ratio [KY91], the minimax ratio [You98], the gain-to-loss ratio [BL00], the Sortino-Satchell ratio [SS01], among many others; see [CK13, OBS+05] for a comprehensive survey of ratio type performance measures. This naturally raises the question which properties – and, consequently, which performance measures – are desirable. Cherny and Madan [CM09] took an axiomatic approach to performance measurement, in line with the classical axiomatic approach to risk measurement by Artzner et al. [ADEH99]. In [CM09] the authors introduce the concept of a coherent acceptability index (CAI) as a measure of performance that satisfies a set of desirable properties – monotonicity, quasi-concavity, scale invariance and the Fatou property. It was proved that an unbounded CAI admits a robust representation in terms of a family of coherent risk measures (CRMs) given by

| (1.1) |

Equivalently, the representation (1.1) can be stated in terms of a family of acceptance cones, or in terms of a family of sets of probability measures. The concept of a coherent acceptability index in a dynamic setup was first studied in [BCZ14], and consequently in [BCDK16, BCC15, RGS13, BBN14].

The main goal of this paper is to study the optimization problem of the form

| (1.2) |

where is a static or dynamic CAI and is a set of feasible positions. We refer to this problem as acceptability maximization. The obtained results contribute to the rich literature on optimal portfolio selection or optimization of performance, such as classical mean-variance portfolio analysis or Sharpe ratio maximization (cf. [AN04, GISW02]). Clearly, acceptability maximization is a practically important and natural problem to study. Closest to the spirit of our study is [EM14], where the authors solve an acceptability maximization problem for some specific choices of static CAIs (AIMIN, AIMAX, AIMINMAX and AIMAXMIN) which are represented through families of distortion functions (or Choquet integrals). To the best of our knowledge, this is the only work that considers optimal control problems with CAI criteria. The proposed solution in [EM14] fundamentally relies on the representation of CAIs in terms of distortion functions.

In contrast to [EM14], in this work we mostly exploit the representation (1.1), and we consider both the static and the dynamic case. We start by considering the one-period (static) setup, presented in Section 2. First, we recall some key definitions and relevant results on CAIs (Section 2.1), and then we propose a numerical algorithm for solving (1.2) that approximates the maximal acceptability by a sequence of risk minimization problems (Section 2.2). In Section 2.3 we apply this algorithm to several important CAIs, such as the gain-to-loss ratio, the risk-adjusted return on capital and the tail-value-at-risk based CAI.

Undoubtedly, for many practical purposes, acceptability or performance needs to be measured in a multi-period setting where the investor dynamically rebalances her portfolio. We study this in Section 3. As was noted in [BCC15] and later systemically addressed in [BCP17, BCP18], the time consistency property stays at the heart of the matter when studying dynamic coherent acceptability indices (DCAIs) and their robust representations of the form (1.1) in terms of families of dynamic coherent risk measures (DCRMs) . We prove that if for every the DCRM is recursive (or strongly time consistent as a DCRM), and assuming some recursive structure of the underlying market model, then the maximal acceptability is constant across all times and states. Thus, in this case, it is enough to solve the corresponding optimization problem only once, at one state and one period of time; see Section 3.2.1 for details. However, in many relevant examples of DCAIs, are not strongly time consistent, and, similar to the classical control problems with mean-variance criteria, problem (1.2) is time-inconsistent in the sense that the (naive) dynamic programming principles does not hold true. To overcome this challenge, we adapt to our setup the set-valued Bellman’s principle recently proposed in [KR19]. This approach also provides the intermediate mean-risk efficient frontiers, in the spirit of the mean-variance efficient frontier. Within this approach, we consider two specific performance measures - the dynamic risk-adjusted return on capital (Section 3.2.2) and the dynamic gain-to-loss ratio (Section 3.2.3). The majority of the proofs are deferred to the appendices.

As mentioned above, this is the first attempt to study stochastic control problems with dynamic CAI criteria. While the static case is now relatively well understood, the acceptability maximization problem in a dynamic setup appears to be an interesting research area, with many open problems, primarily due to the time-inconsistent nature of such problems, as argued in this manuscript. In particular, it would be far-reaching to develop a Bellman’s principle of optimality for a class of DCAIs, beyond particular examples. In addition, from a practical point of view, it would be important to study the acceptability maximization problem for a larger classes of indices, for example not necessarily coherent ones. The authors plan to treat these problems in future works.

2 Acceptability Maximization in the Static Setting

In this section, we consider the static setting, before moving to the dynamic one in Section 3. First, we recall the definition of a coherent acceptability index and its connection to coherent risk measures. This serves as our framework for studying the maximization of performance, i.e., acceptability maximization. In Subsection 2.2 we provide a way to solve the acceptability maximization problem through a sequence of risk minimizations. At the end of the section, we provide examples of this approach. Proofs can be found in Appendix A.

2.1 Static Coherent Acceptability Indices and Risk Measures

We start by briefly reviewing the notion of a (static) coherent acceptability index (CAI) and its connection to (static) coherent risk measures (CRMs), following [CM09]. The concept of acceptability was developed as a methodology to define axiomatically minimal desirable properties of a functional that is meant to measure or assess the performance of a financial position or trading portfolio. As usual, we consider an underlying probability space , and we denote by the space of essentially bounded random variables on this space. In what follows, all equalities and inequalities between random variables will be understood in a almost surely sense. In this section, an element can be viewed as a discounted terminal cash flow of a zero-cost self-financed portfolio, or the terminal profit and loss (P&L) of a financial position. The mapping assigns to the portfolio the degree of its acceptability, with higher values corresponding to more desirable positions.

Definition 2.1.

A coherent acceptability index (CAI) is a function satisfying for all positions and any level

-

(A1)

Monotonicity: if , then ,

-

(A2)

Scale invariance: for all ,

-

(A3)

Quasi-concavity: if and , then for all ,

-

(A4)

Fatou property: if for all , and , then .

In [CM09] four further properties – law invariance, consistency with the second order stochastic dominance, arbitrage consistency and expectation consistency – are discussed. These are not required for the coherent acceptability index, but, as the authors argue, they are desirable. Additionaly, coherent acceptability indices are closely related to coherent risk measures, a concept introduced in [ADEH99].

Definition 2.2.

A coherent risk measure (CRM) is a function satisfying for any

-

(R1)

Monotonicity: if , then ,

-

(R2)

Positive homogeneity: for all ,

-

(R3)

Translation invariance: for all ,

-

(R4)

Subadditivity: ,

-

(R5)

Fatou property: if , for all , and , then .

A family of coherent risk measures is called increasing if implies for any .

As was proved in [CM09], there is a strong connection between CAIs and increasing families of CRMs. Namely, the following robust representation type result holds true: A map , unbounded from above, is a coherent acceptability index if and only if there exists an increasing family of coherent risk measures such that

| (2.1) |

with the convention . Equivalently, the representation (2.1) can be formulated in terms of a family of acceptance sets, or an increasing family of sets of probability measures associated with dual representations of CRMs (see also Section 2.3). For various degrees of generalization of (2.1) see, for instance, [MS16, BCDK16, BCC15, RGS13, BBN14].

2.2 Algorithm for Acceptability Maximization: the Static Case

We fix a set of available or feasible positions. For example, could be the P&Ls of portfolios that satisfy certain trading or other constraints. Our aim is to identify among the available positions the ones with the highest degree of acceptability. Namely, we wish to solve the following optimization problem,

| () |

We denote the maximal acceptability by

| (2.2) |

and the set of maximally acceptable (optimal) portfolios by Generally speaking, a maximally acceptable portfolio may not exist, i.e. the set is empty if is not attained as a maximum. For we define the set of -optimal positions

The following Lemma summarizes the properties of these sets.

Lemma 2.3.

-

1.

If the feasible set is convex, then the sets and are convex, for any .

-

2.

The sets and are nested: , for any .

-

3.

.

Proof.

The proof is deferred to Appendix A. ∎

To solve the maximization problem (), we will use the robust representation (2.1), with denoting the corresponding increasing family of CRMs. For a given level we consider the problem of minimizing risk over the feasible set ,

| () |

We denote the optimal value of the risk minimization problem () by , and its optimal solution by assuming that the infimum is attained. In what follows we make the following standing assumption:

Assumption 2.4.

The unboundness from above of is usually satisfied in all practically important cases, while attainability of the min in () can be guaranteed, for example, by assuming that is compact. With this at hand, and in view of (2.1), we note that:

- •

- •

The next result summarizes the above observations, which are used in developing Algorithm 1 that solves the acceptability maximization problem ().

Lemma 2.5.

Let Assumption 2.4 hold and let .

-

1.

If , then

-

2.

If , then

-

3.

If , then for all

-

4.

If , then for all

Proof.

The proof is given in Appendix A. ∎

The main idea of the proposed numerical solution of () is to approximate the maximal acceptability by a sequence of risk minimization problems () for some appropriately chosen levels - a variation of the bisection method that will find a pair maximizing the level while satisfying . First, find two levels with opposite signs of the minimal risk , namely find a lower and upper bound on the maximal acceptability . Then, iteratively decrease the distance between the two bounds. This replaces one acceptability maximization problem () with a sequence of risk minimization problems (). This becomes particularly useful if the acceptability maximization is complicated and the risk minimization is easier to solve. Note that if the feasible set is convex, then the risk minimization becomes a convex optimization problem.

The next result summarizes the key features of Algorithm 1.

Lemma 2.6.

Suppose that Assumption 2.4 holds, and let be the initial (seed) value, be the maximal number of iterations (of Step 1) and be the tolerance level. Denote

Proof.

The proof is postponed to Appendix A. ∎

Remark 2.7.

Several comments are in order:

-

(i)

In Step 1, instead of the halving (), respectively the doubling (), one could select any respectively Similarly, in Step 2 one could replace the bisection with any choice of The results of Lemma 2.6 would differ in the interval on which is identified and the number of iterations.

- (ii)

-

(iii)

Assumption 2.4 allows us to merge the case with the case . Without it, we would need to distinguish between attained and not attained infimum for . If the infimum is attained for some portfolio , then and is a lower bound on . If the infimum is not attained, then for all positions we have so is an upper bound on This distinction would need to be built into Algorithm 1. Alternatively, if , this level could be discarded and the iteration repeated with some other choice of level in the appropriate interval. However, it is not clear how many such repetitions might be needed.

-

(iv)

Instead of specifying the maximal number of iterations and the initial value we could directly specify the interval in which the optimal would be searched. Then, Step 1 of the algorithm would need to check the signs of and and terminate immediately if lies in the interval or Step 2 would require iterations to terminate, assuming bisection steps. This might be of interest especially if the risk measure is well defined also for the limiting cases and see Section 2.3 for an example.

Algorithm 1 with tolerance outputs an -solution to the acceptability maximization problem, an element of the set We also know that the sets of -solutions are nested and intersect in the set of optimal solutions. Therefore, it is natural to ask about the convergence of the algorithm output as the tolerance vanishes. As the next result shows, such convergence holds true if the feasible set is compact. Generally speaking, for a non-compact it is possible to construct counter-examples, where the -solutions converge to an (infeasible) element outside of a (non-empty) optimal set or diverge.

Lemma 2.8.

Let and suppose that the feasible set is a compact set w.r.t. the topology of convergence in probability. Let be a sequence of solutions outputed from Algorithm 1 for a sequence of tolerances with . Then has an -a.s. convergent subsequence whose limit belongs to the set of optimal solutions

Proof.

The proof is given in Appendix A. ∎

2.3 Numerical Examples

We will illustrate the proposed algorithm with three examples of CAIs: the acceptability index corresponding to the tail-value-at-risk (), the gain-to-loss ratio () and the risk-adjusted return on capital (). First, we define these CAIs as well as identify the families of risk measures from the robust representation (2.1).

-

1.

The at level is defined as

where is the value-at-risk at level . It is well known that is not a coherent risk measure, while is a coherent risk measure. Moreover, using as a family of CRMs, we define the the acceptability index

It is easy to show that indeed is a CAI that is also law invariant, consistent with second order stochastic dominance, and arbitrage and expectation consistent; for more details see [CM09, Section 3.5]. However, one notable drawback of is that it ignores the gains and only takes into account the tail corresponding to losses.

-

2.

The gain-to-loss ratio is a CAI, popular among practitioners, and defined as the ratio of the mean and the expectation of the negative tail, namely

where and the convention for all is used. For additional properties of see, for instance, [CM09, Section 3.2]. We recall several representations of GLR, useful for our purposes. The representation of the form (2.1) is given in terms of expectiles. We recall that the expectile of a random variable at level is defined by a first-order condition

or as a minimizer of an asymmetric quadratic loss, see [BDB15] for more details. The expectile-,

for , is an increasing family of CRMs. One can show, for example by using that is the acceptance set of , that the representation (2.1) for has the form

Alternatively, one can use the system of supporting kernels corresponding to , as well as the explicit form of the extreme measures, cf. [CM09, Proposition 2]. It is also clear that for , if, and only if, , which can be conveniently used for computation purposes. This is not linked to the robust representation (2.1) since the mappings are not CRMs (for instance they are not translation invariant). Finally, we remark that there is another popular version of GLR, defined as . This version of is also monotone, scale invariant and has the Fatou property, but lacks quasi-concavity, and thus is not coherent. The two are connected via .

-

3.

The risk-adjusted return on capital, similar to , is a reward-risk type ratio, formally defined as

(2.3) where is a fixed CRM. The corresponding family of CRMs is given by

For risk measures satisfying this simplifies to . For more details see [CM09, Section 3.4]. In our numerical examples we will use with , also known as the stable tail-adjusted return ratio (see, for instance, [MRS03]).

In our numerical examples below, we maximize the acceptability index over the set of profits and losses that are possible to attain by investing in the market with (risky) assets. Without loss of generality, thanks to scale invariance of CAIs, we fix the initial investment to . For numerical tractability, we assume that is finite. The (gross or total) returns , of these assets are modeled as a matrix . Then, the sets of available profits and losses, with or without short-selling, become

where . So, corresponds to the trading strategy (the amount invested in each asset) and to the corresponding terminal P&L.

To illustrate the main features of the proposed algorithm, we first consider a toy market model, consisting of assets and with returns given in Table 1(b), Panel A. Generally speaking, it is reasonable to select the input parameters such that that . Panel B of Table 1(b) summarizes the iterations of the algorithm with the following input parameters: the starting (seed) acceptability level set to , the tolerance and the maximal number of iterations of Step 1. The algorithm outputs bounds on the maximal acceptability and an -optimal solution ; see the last two rows of Table 1(b), Panel B. For each of the three acceptability indices, the optimal portfolio puts more weight on the first asset, with being the most balanced and being the most extreme. This is because the first asset carries (in some sense) less risk, although at the cost of lower mean return than the second one. All three considered CAIs are loss based measures, but each in a different way. The measures how far and how deep into the tail the losses can go. The optimal position for balances the return in the second and the third state of the world. The treats loss directly through the expectation of effective losses (the negative part of the P&L). Thus, the corresponding optimal position is in the range where the portfolio return is negative in only one state of the world. Since we are using in defining the , only the worst-case scenario (state of the world) is considered, which is the reason why the corresponding optimal position relies heavily on the first asset, for which the worst-case loss is lower. We also remark that in this market model, the short-selling constraints do not change the results.

For the sake of completeness, we also show the iteration of the modified algorithm outlined in Remark 2.7(iv). We use the fact that for each of the three indices – – the corresponding risk measures are well-defined for the limiting parameter values and Since the bisection cannot be done on an interval of infinite length, we index the families of risk measures by a parameter on a bounded interval or, respectively by on Then, the bisection is performed with respect to the parameter . The iterations for are presented in Table 2, see the modified algorithm. This modification avoids the risk of failing to find a lower or upper bound for a badly chosen starting point (compare to Table 3(c)). Moreover, zero and infinite acceptability are often determined after solving two risk minimization problems, instead of On the other hand, one needs to treat the tolerance parameter carefully: although the bisection is performed on the parameter , the termination criterion needs to be set on in order for the error not to be distorted (see Table 2). A mixed version of the algorithm is also provided – it switches to a bisection on the original parameter , as soon as a finite upper bound is found. The iterations for are also given in Table 2, see the mixed algorithm. In addition, we also make the following slight modification to the algorithm: at each iteration a risk minimization problem is solved, finding its optimal solution . If the considered level is found to be a lower bound then the maximal acceptability, then the position is used for updating the optimal solution of the acceptability maximization. Otherwise, it is not used at all. One can easily see that given a fixed position , all levels satisfying are lower bounds on the maximal acceptability. Hence, if it is relatively easy to find a level such that , then it can be used to update the lower bound. For the CAIs used in this example such level can be found without any further optimization. We refer to this modification of the original algorithm as zero-level version.

We also run the proposed algorithm on a more realistic market model, consisting of stocks and states of the world. The return matrix is obtained as draws from a multivariate Student’s -distribution. In Table 3(c) we report the results for various input parameters and . The results are intuitively clear, and expected: the distance of the initial guess from the true affects the number of iterations needed to find the upper and lower bound (Step 1). The tolerance determines the number of iterations in Step 2. We also note that for a badly chosen starting point the algorithm can fail to find a lower or an upper bound unless is increased. We also note that the maximal acceptability differs in a market with and without short-selling, but the impact of the parameters is the same. Similar to the toy model, we list in Table 4(c) the results for different versions of the algorithm – original one, modified, mixed and zero-level. We also present the results both with and without short-selling constraints. These results show that neither of the versions of the algorithm is performing strictly better than the others. Similar conclusions were observed for various other sets of parameters.

3 Acceptability Maximization in the Dynamic Setting

In this section, we consider the acceptability maximization problem in a dynamic setting. We use the theory of dynamic coherent acceptability indices introduced in [BCZ14] and their link to dynamic coherent risk measures. We briefly recall the key definitions and results from [BCZ14], and then focus on acceptability maximization in the context of optimal investment in a multi-period market model. It turns out that the maximal acceptability is constant in a setting when the determining family of dynamic coherent risk measures is recursive and when the underlying market has a recursive structure. We conclude by considering the non-recursive case by focusing on two specific performance measures – the dynamic risk-adjusted return on capital and the dynamic gain-to-loss ratio – where we use the specific structure of the problem to introduce a solution scheme tailored to these performance measures.

3.1 Dynamic CAIs and dynamic CRMs

The concept of a coherent acceptability index was first extended to a dynamic setting in [BCZ14] and consequently studied in [BCDK16, BCC15, RGS13, BBN14]. A dynamic coherent acceptability index (DCAI) is meant to measure the performance of financial positions or instruments over time, accounting for the incoming flow of information. We start by briefly recalling the setup of [BCZ14], where DCAIs are designed to measure the performance of (discounted) cash flows or dividend streams or unrealized P&Ls. Most of the properties from the static setup are naturally transferred to the dynamic case. An addition is the time consistency property, which stays at the core of financial interpretations of DCAIs, but is also fundamentally used in establishing the dual representations. We refer to [BCP17, BCP18] for an in-depth discussion of various forms of time-consistency in decision making, in particular those arising in the theory of dynamic risk and performance measures. Following [BCZ14], we take a discrete and finite state setting by denoting for some fixed , and letting be a filtered probability space, with having full support. We will write instead of the conditional expectation given . Without loss of generality, we will assume that is trivial. The dividend streams or unrealized P&Ls will be modeled as -adapted real-valued stochastic process . We will denote by the set of all such processes, and by the -measurable random variables. As usual, for will denote the indicator function which is equal to one for and zero otherwise. Without loss of generality, we assume a zero interest rate, or, view as discounted cash flows. Operations between random variables, such as minimum, maximum, product, or sum will be understood -wise.

Definition 3.1.

A dynamic coherent acceptability index (DCAI) is a function satisfying for all times all cash flows all events , and all random variables

-

(A1)

Adaptiveness: is -measurable,

-

(A2)

Independence of the past: if for all , then ,

-

(A3)

Monotonicity: if for all , then ,

-

(A4)

Scale invariance: for all ,

-

(A5)

Quasi-concavity: for

-

(A6)

Translation invariance: for any and ,

-

(A7)

Dynamic consistency: if and there exists an such that , then .

A DCAI is normalized if for all , there exist such that and . It is right-continuous if for any .

As in the static case, DCAIs are closely related to dynamic coherent risk measures (DCRMs).

Definition 3.2.

A dynamic coherent risk measure (DCRM) is a function satisfying for all times all cash flows all states , all events , and all random variables

-

(R1)

Adaptiveness: is -measurable,

-

(R2)

Independence of the past: if for all , then ,

-

(R3)

Monotonicity: if for all , then ,

-

(R4)

Homogeneity: for all ,

-

(R5)

Subadditivity:

-

(R6)

Translation invariance: for any and ,

-

(R7)

Dynamic consistency:

A family of dynamic coherent risk measures is called increasing if implies for any . It is left-continuous at if for any .

Originally, DCRMs were introduced in [Rie04], although with a different (stronger) notion of time-consistency, which will be discussed in Section 3.2.1. As proved in [BCZ14], there is a one-to-one relationship between a DCAI and an increasing family of DCRMs, similar to (2.1). Namely, the following assertions hold true:

-

1.

For a normalized dynamic coherent acceptability index the functions defined as

(3.1) form an increasing, left-continuous family of dynamic coherent risk measures.

-

2.

For an increasing family of dynamic coherent risk measures a function defined as

(3.2) is a normalized, right-continuous dynamic coherent acceptability index. Moreover, there exists an increasing sequence of sets of probability measures such that

(3.3) The converse implication is also true, under an additional technical property of time consistency of ,

-

3.

If is a normalized, right-continuous dynamic coherent acceptability index, then there exists an increasing, left-continuous family of dynamic coherent risk measures , such that representation (3.2) holds. Vice versa, for an increasing, left-continuous family of dynamic coherent risk measures there exists a normalized, right-continuous dynamic coherent acceptability index , such that (3.1) holds.

Similar to the static case, we are interested in finding the position with highest degree of acceptability. Given a set of available, or feasible, cash flows , the problem of interest is

| (3.4) |

It is straightforward to adapt Algorithm 1 to the dynamic setup to solve the corresponding version of (3.4) for a given and . However, this approach, generally speaking, is computationally not feasible. Usually one would aim to establish a recursive set of equations in the form of a dynamic programming principle or Bellman’s principle of optimality that would solve (3.4), which will be provided in the next section for the optimal investment problem.

3.2 Optimal portfolio selection problem

In this section, we consider the acceptability maximization problem in the context of optimal portfolio selection in a market model with available assets. We denote by the vector of assets (total or gross) returns between time and time , namely, if denotes the price of the -th asset at time , then . We assume that are independent and identically distributed on a probability space , and denote by the natural filtration generated by the process . In addition, we assume that all one step asset returns are strictly positive. Note that we implicitly assume that these assets do not pay dividends.

We assume that the investor starts with a positive initial wealth , and invests it in the available assets by following a self-financing trading strategy, possibly with some additional trading constraints. A trading strategy is an adapted stochastic process with , where is the monetary amount invested in asset between time and . The portfolio value at time arising from the trading strategy is given by for any . We consider two feasible sets in particular, one with no trading constraints and one with short-selling constraints. The set of all self-financing trading strategies with initial value is

Correspondingly, the set of feasible trading strategies with short-selling constraints is

The time feasible sets and are defined analogously. The next result shows that the feasible sets are positive homogeneous and recursive.

Lemma 3.3.

-

1.

For a positive -measurable wealth the feasible sets scale as follows

-

2.

The feasible sets are recursive,

where and .

Proof.

The proof is deferred to Appendix B. ∎

Our aim is to find the optimal trading strategy among the feasible ones by maximizing the portfolio’s acceptability as measured by a given DCAI . We recall that the dynamic setup of [BCZ14] and [Rie04] assumes that the inputs to a DCAI are (discounted) dividend processes, a setup usually convenient for pricing purposes or assessing the performance or riskiness of some dividend paying securities, or random future cash-flows (cf. [AFP12, AP11, BCIR13, BCC15] and references therein). When dealing with optimal investment (i.e. an optimal portfolio selection problem), traditionally and also more conveniently, one works with the value process or the (discounted) cumulative dividend process. Given a portfolio with value process , the corresponding dividend stream is defined as

and . Thus, the cumulative P&L up to time becomes . We refer the reader to [AP11, BCDK16] for a detailed discussion on use of dividend streams and cumulative dividend streams within the general theory of assessment indices.

We denote by the wealth process generated by the trading strategy and will stand for the corresponding dividend stream. In addition, for a given dividend stream we define the time tail dividend stream as , and we also put .

The optimization problem we wish to solve at initial time is

| () |

or the variant thereof, if short-selling is allowed, in which case the feasible set is . By property (A2), independence of the past of DCAIs, we have that . This would suggest that in order to solve we should consider the problems

| () |

One certainly can study (), and try to establish a dynamic programming principle for this stochastic control problem, although, generally speaking, this problem is not time consistent. More importantly, from a practical point of view, including the change in portfolio value from time to , namely the term , in the optimization criteria at time is less desirable. In particular, using (3.3), one would optimize at time a function that depends on , rather than a function depending on total future return . With this in mind, we introduce and focus our attention on a family of auxiliary acceptability maximization problems

| () |

which are more in line with the setup from the optimal portfolio selection problem. Note that for any trading strategy the cash flows and coincide, and hence at the initial time the auxiliary problem is the same as the original problem . Therefore, solving the auxiliary family of problems, which we will address next, will lead to the solution of the original acceptability maximization problem.

3.2.1 The Case of Recursive Risk Measures

As we already mentioned, the form of the time consistency property (R7) for DCRMs is tailored for the robust representation (3.2) of DCAIs with the time consistency property (A7). This form of time consistency is weaker than the so-called strong time consistency of risk measures:

-

(R7’)

Strong time consistency: for any and , if and then .

Strong time consistency (R7’) is the one usually associated with dynamic risk measures (cf. [Rie04, BCP17]), due to its natural financial interpretation, but also because of its equivalence to:

-

(R7”)

Recursiveness: , for any and .

One major benefit of having the recursive property is its direct applicability to stochastic control problems. This very property makes many stochastic control problems with risk as the terminal criteria to be time consistent. Note that such recursive property in principle can not be satisfied by any DCAI, cf. [BCP18, BCP17].

In this section, we study the acceptability maximization problem () assuming that the corresponding family of risk measures is strongly time consistent. We work under the market setup of Section 3.2 with short-selling constraints and with an initial value .

The one-step risk measures generated by are defined as

for any -measurable random variable , here denotes the zero process. In what follows we assume that the one-step risk measures are identical across all nodes of the multinomial model. Namely, with denoting the partition of that generates , we assume that for any , and any and

| (3.5) |

for all , all and all satisfying and zero otherwise. As previously, we denote the maximal acceptability attainable at the market as

Under the above, what may appear, natural assumptions, we obtain a somehow surprising result: the maximal acceptability is constant across wealth level, time and states of the world.

Theorem 3.4.

Let be a normalized right-continuous DCAI and be the corresponding family of DCRMs. Assume that for each the DCRM is strongly time consistent, and all the one step risk measures satisfy (3.5). Then, under the market model assumption of this section, the maximal acceptability is independent of the wealth, time and state, that is,

for all , and positive .

Proof.

The proof is given in Appendix B. ∎

In view of Theorem 3.4 the auxiliary acceptability maximization has a constant optimal objective value in time, and since at the initial time the auxiliary and the original problem coincide, we obtain that it suffices to solve for some instead of . The next result shows how to construct the corresponding optimal trading strategy.

Theorem 3.5.

Assume that for some the supremum is attained and denote by the corresponding optimal position (given ),

where was defined in Lemma 3.3(2). Let be the trading strategy defined as

Then, the trading strategy is an optimal solution of , i.e. .

Proof.

The proof is given in Appendix B. ∎

The results of this subsection rely on the properties of the family of risk measures corresponding to the DCAI under consideration. Similar to the static case, one may be interested in the risk minimization problem corresponding to a fixed level . As may be expected, the recursive setting of this section has direct implications on the minimal achievable risk (infimum of the risk minimization problem). It can be proved that the minimal risk is positively homogeneous and it also has a recursive form. Unlike the maximal acceptability it is not constant, but it maintains the same sign over all times and states. Furthermore, if an optimal solution (optimal trading strategy) exists, it can be constructed recursively in the spirit of Theorem 3.5.

3.2.2 The Case of Dynamic RAROC

Using the definition of the static RAROC, the identity (2.3), as well as the representation (3.3), one naturally defines the dynamic risk adjusted return on capital (dRAROC) as follows:

with the convention , where is a given dynamic coherent risk measure (not to be confused with the family of DCRMs corresponding to an acceptability index).

As was shown in [BCZ14, Section 6], dRAROC fulfills the properties (A1)-(A6), but it, in general, fails to satisfy the dynamic consistency property (A7), and therefore, it is not a DCAI. Nevertheless, for some choices of , dRAROC satisfies some weaker forms of time consistency. In particular, if is the dynamic version of , then the corresponding dRAROC is so-called semi-weakly acceptance time consistent, but not semi-weakly rejection time consistent; for more details see [BCP17, BCP18]. This will be the example we consider in our numerical experiment below. With this in mind, we are interested in identifying an investment with the highest performance measured by dRAROC, i.e. the maximization of the dRAROC-performance in the framework of self-financing portfolios introduced in Section 3.2. Furthermore, we focus our attention only on the case of a feasible set with short-selling constraints , but most of the results can be extended to the case with no trading constraints. Hence, we wish to solve the following optimization problem:

| (3.6) |

As already mentioned, this problem is time-inconsistent (in the sense of optimal control), and in view of the above it does not fit the framework of Section 3.2.1.

We will take the approach of [KR19] to deal with time-inconsistency of (3.6). First we note that for a positive level

Using this, one could apply the idea of Algorithm 1 to the family of functions for . In the nutshell, the procedure would consist of the following: First, minimize the risk among the feasible positions, i.e. solve the mean-risk problem with an infinite risk aversion. If the optimal value were negative, an infinite performance measured by would be implied. Second, repeatedly minimize among the feasible positions for various levels – that is, solve the mean-risk problem for the risk aversion at various levels . Therefore, the algorithm would be iteratively computing elements of the mean-risk efficient frontier. If the (full) efficient frontier, i.e. the set of all portfolios that are not dominated in terms of their mean and risk, was available instead, the optimal solution of (3.6) could be found simply as the element of the frontier with the highest ratio of the mean to the risk. Of course, applying Algorithm 1 is not computationally efficient in the dynamic setup, but it motivates us to compute the efficient frontier, i.e. to consider the bi-objective mean-risk problem

| (3.7) |

where we used the fact that . This will also overcome the problem of time-inconsistency of (3.6) and thus lead to an efficient way to solve (3.6). As it turns out, problem (3.7) is time consistent in the set-valued sense, i.e., the set-valued Bellman’s principle of optimality recently proposed in [KR19] provides a way to solve the mean-risk problem (3.7) recursively, assuming that the dynamic risk measure is recursive, i.e. strongly time consistent. We emphasis that the recursiveness of does not imply the recursiveness of the members of the family and is a separate property from the dynamic consistency of the performance measure dRAROC. The set-valued Bellman’s principle of optimality of [KR19] also provides the intermediate mean-risk efficient frontiers, namely it solves the sequence of mean-risk problems

for each time point . Note that since is equal to the ratio of the mean to the risk, the element of the frontier of the time-consistent problem (3.7) with the highest ratio is the optimal solution of the time-inconsistent problem (3.6). The same can be said about the intermediate mean-risk efficient frontiers and (auxiliary) problems .

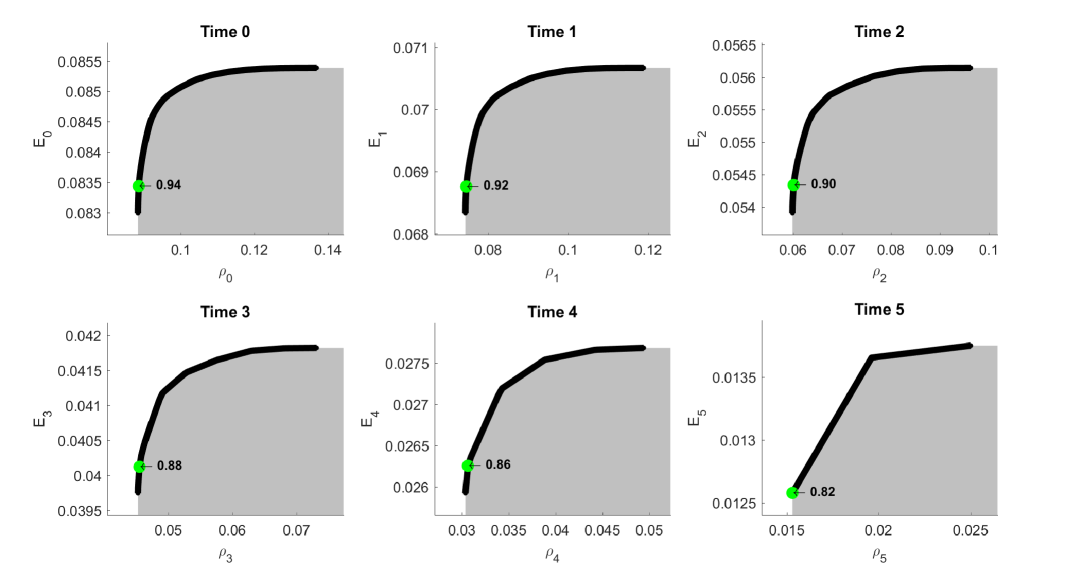

We illustrate this on a dynamic version of the example from Section 2.3. We consider the market model with two assets, and with one-time-step asset returns , having the probability law given in Panel A of Table 1(b), and we take . We take the DCRM to be the recursive dynamic at significance level . We recall that the dynamic is defined analogously to the static by replacing with the conditional , which in turn is defined as a conditional quantile.

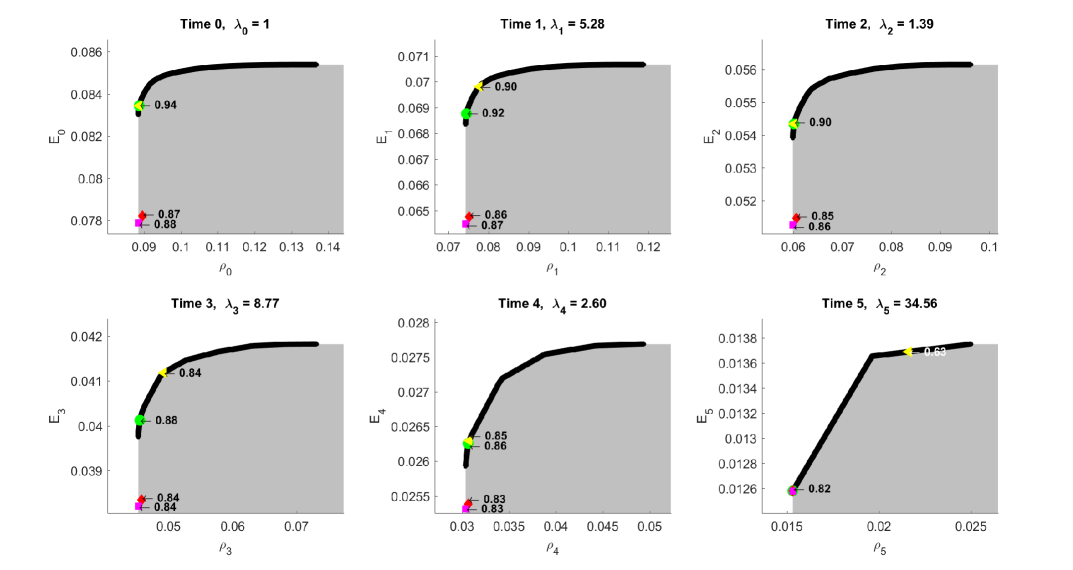

In Figure 1 we display the mean-risk efficient frontier of problem (3.7), as well as the intermediate frontiers. The bright green points correspond to the elements with the highest dRAROC.

The trading strategy corresponding to the highest- element of the time frontier can be recovered from the solution of the mean-risk problem, see [KR19] for details. The mean-risk profiles, and the corresponding values of dRAROC, of this portfolio in the subsequent time points are determined by the strategy itself and vary over times and states of the world. They are depicted as yellow triangles for a selected state of the world in Figure 2. All of them lie on the efficient frontiers (yellow triangles), but, in general, do not coincide with the highest- element (bright green points). This confirms the time-inconsistency of dRAROC – the strategy optimal from the viewpoint of time is not dRAROC-maximal at the subsequent time instances.

For comparison, we include also a myopic (magenta square) and an inconsistent switching (red diamond) approach. In the myopic case, the investor at each time solves a one step optimization problem, hence looking always only one period ahead and chooses the position that maximizes the RAROC over this one-period horizon. The switching strategy represents a time inconsistent behavior in the sense that at time the dRAROC-maximal element of the (time consistent) frontier is selected, the trading strategy corresponding to it is found, and the position is taken. At the next time the previously found trading strategy is discarded and a new one, corresponding to the dRAROC-maximal element of the frontier, is selected. Since each (efficient) trading strategy is discarded after one time period, none of the corresponding (dRAROC-optimal) mean-risk profiles are ever realized. Figure 2 shows the actual means, risks and values of dRAROC that these behaviors yield. Clearly, neither the myopic nor the switching give at any time (except at ) the maximal performance. They even lead to portfolios, which are not mean-risk efficient at all, i.e. they do not lie on the frontier.

Finally, let us look again at the strategy depicted in yellow, namely the strategy that solves (3.6) at time zero. While this stochastic control problem is time-inconsistent, one can ask which objective does the optimal strategy maximize at the intermediate times. Note that the -maximal element of the time frontier corresponds to a nonlinear scalarization

Thus, we will concentrate on a class of non-linear scalarizations including the one above. Specifically, we consider scalarizations of the time frontier of the form

| (3.8) |

where the mapping is fully determined by the value , which can be interpreted as a non-linear risk aversion parameter. For any given efficient trading strategy, one can compute the value of , such that the strategy is an optimal solution of a scalar problem with the objective (3.8). This way, a sequence of can be computed for the –optimal strategy (represented on the frontiers by the yellow mean-risk pairs). Since the frontiers (and the mean-risk profiles) are adapted, also the corresponding scalarization coefficient will be adapted. We computed the corresponding in the given state of the world and depicted it also in Figure 2.

Thus, the sequence of scalar problems (3.8) is time consistent in the usual sense for the computed risk aversion parameters . As is by construction included, a time zero member of this time consistent family is the –maximization problem. Thus, an investor with a criteria at time zero and a like criteria, that differs only in a changed risk aversion parameter , where is changing in a certain manner according to the changes in the stock market, would behave time consistent in the classical sense. This is in line with the findings about the moving scalarization (a time and state dependent risk aversion parameter) that leads to a time consistent problem and a time consistent behaviour of the investor as also discussed in the mean-risk portfolio optimization problem in [KR19] and for other otherwise time inconsistent problems in [KMZ17].

3.2.3 The Case of Dynamic GLR

Similar to dRAROC, the dynamic gain-to-loss ratio (dGLR) is defined as

| (3.9) |

with the convention Unlike dRAROC, dGLR is a normalized and right-continuous DCAI (see [BCZ14, Section 6]). Our aim is to identify among all self-financing portfolios the ones with the highest dGLR, that is to solve the problem

| (3.10) |

Similar to the static GLR, the family of DCRM from the robust representation is identified by the conditional expectiles, and since the conditional expectiles are not strongly time consistent, the results of Subsection 3.2.1 do not apply here. As was also noted in the static case, instead of the corresponding family of risk measures one can consider the family for . Note that for any fixed time instance one can view the problem as a static one, and thus one can apply Algorithm 1, but this would be, as discussed before, computationally infeasible to do for all . Here, with the intention of obtaining a Bellman’s principle of optimality, we take an approach inspired by the previous subsection and in the spirit of [KR19]. Motivated by the numerator and denominator of (3.9), we consider the bi-objective mean-loss problem

| (3.11) |

By the same argument as in the dRAROC case, the element of the efficient frontier with the highest ratio corresponds to the portfolio with the highest value of . The recursive approach of [KR19], unfortunately, can not be applied directly here, due to the lack of translation invariance of the objective function which makes it impossible to express through . Nevertheless, to solve (3.11), we consider the following sequence of bi-objective problems

| (3.12) |

where is the fixed initial wealth. Problem (3.12) does not have a natural interpretation as a mean-loss problem, unless , however, it does give a recursive solution of (3.11) in terms of the set-valued Bellman’s principle of [KR19].

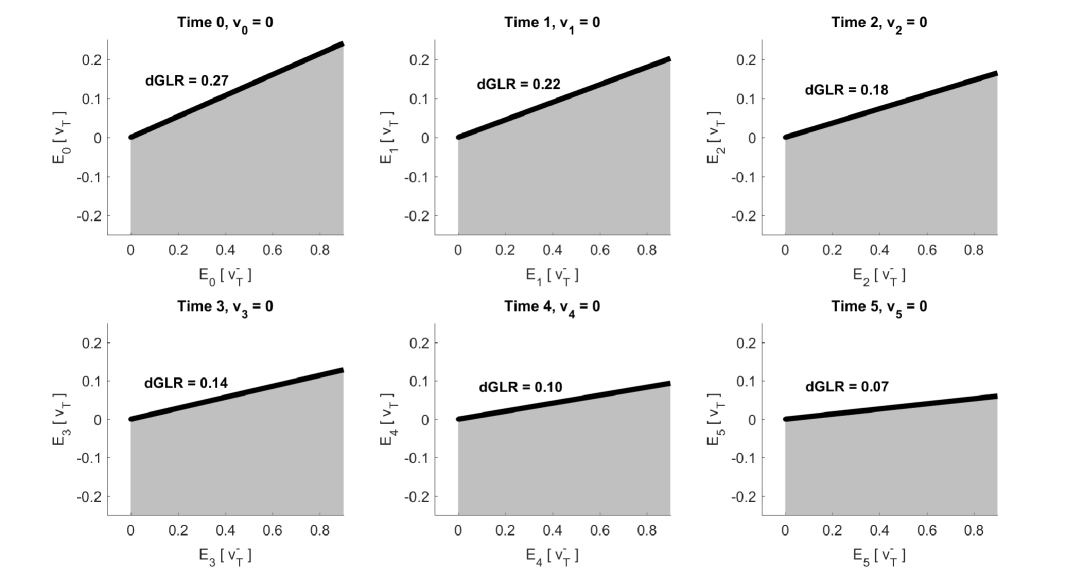

We also note that the computational approach from [KR19] based on scaling arguments is not applicable here either, and therefore one needs to solve (3.12) for any As the problems (3.12) can be rewritten as bi-objective linear optimization problems and differ only in the right-hand side of the constraints, they form a class of parametric bi-objective linear problems with the parameter We solved these parametric problems via polyhedral projection (cf. [LW16]).

We conclude this section by illustrating the solution to (3.10) in the same market model setup as in Section 3.2.2 and by taking the initial wealth . Figure 3 contains the efficient frontier at time and the highest value of problem (3.10) given by . As the intermediate frontiers are computed for all possible values of , we depict for illustration only those frontiers corresponding to for each time point . The case of the current wealth coinciding with the initial wealth would give problem (3.12) the interpretation as the mean-loss problem. Therefore the corresponding maximal value of can be obtained. Since the zero-cost trading strategy can be scaled, the frontier is naturally a half-line. The highest value of dGLR corresponds to the slope of the frontier. The optimal trading strategy of (3.10) can be deduced from the solution of (3.12). Thus, an auxiliary, but time-consistent bi-objective problem (3.12) (following a backward recursion by the set-valued Bellman’s principle of optimality) is used to compute the optimal solution of the time-inconsistent problem (3.10).

Acknowledgments

IC acknowledges partial support from the National Science Foundation (US) grant DMS-1907568. IC thanks the Vienna University of Economics and Business for the hospitality during a research visit related to the workshop on dynamic multivariate programming in March 2018, where this project has been initiated. The authors thank Christian Diem for helpful discussions in the early stages of the project.

Appendix A Proofs from Section 2

Proof of Lemma 2.3.

The first property follows from the quasi-concavity of , the second from the definition of the sets, for the third consider

∎

Proof of Lemma 2.5.

-

1.

The positive value of the risk minimization problem means that all portfolios have positive risk at level - that is for all . Therefore all portfolios have acceptability at most - that is for all Consequently, We do not obtain a strict inequality as we have no information about the continuity of the risk measure in the parameter

-

2.

The assumption of attainment of the infimum implies that there exists such that Then and

-

3.

The maximal acceptability above means that there exists some portfolio with From the monotonicity of the family of risk measures and (2.1) it follows that for all and therefore

-

4.

The maximal acceptability below means that for all Consequently, for all it holds Since by Assumption 2.4 the infimum of the risk minimization problem is attained, also The same follows for all as the family of risk measures is increasing.

∎

Proof of Lemma 2.6.

-

1.

Let . With the halving update rule, at iteration (counting from ) the tested value is and by Lemma 2.5 at each step Therefore after iterations the algorithm is terminated and no non-zero lower bound on the acceptability is found. The portfolio is never assigned, as no portfolio with a known lower bound on the acceptability is found.

-

2.

Let . With the doubling update rule, at iteration (counting from ) the tested value is and by Lemma 2.5 at each step Therefore, after iterations the algorithm is terminated and no finite upper bound on the acceptability is found. The optimal solution of the risk minimization problem is outputted as . It has a degree of acceptability of at least .

-

3.

(a) According to Lemma 2.5 for it holds therefore Step 1 of Algorithm 1 identifies both lower and upper bound, and Lemma 2.5 also guarantees that the found values are true bounds, Step 2 continues until the length of the interval is sufficiently small.

(b) The optimal solution to the risk minimization problem is returned as . By Assumption 2.4 it holds so From part (a) it follows that so

(c) The worst-case scenario for the length of the interval after Step 1 is Since the bisection step decreases the length of the interval by half, after bisection iterations the length of the interval would be . To obtain a length below we need .

∎

Proof of Lemma 2.8.

By Lemma 2.6 the algorithm for the tolerance outputs Since is compact, there is a subsequence with a limit, denoted , in the feasible set. The compactness also implies there exists such that for all feasible positions . Then, since and scale invariance and the Fatou property of imply for any fixed

Letting go to zero, we obtain . Therefore, is an element of the set ∎

Appendix B Proofs from Section 3

Proof of Lemma 3.3.

For the first part, positive homogeneity follows from the self-financing property and the linearity of the portfolio value As for the second part, the recursiveness, we have

The result for the set is obtained similarly. ∎

Proof of Theorem 3.4.

First we note that is scale invariant, i.e. for any , which follows immediately from the scale invariance of the DCAI and Lemma 3.3(1). Thus, it is enough to prove that , for all and , which we will show next.

To prove the second claim we, use two types of sets of risks: the set of risks of one-step-ahead dividends,

and the set of risks of feasible portfolios,

The fact that the asset returns are iid and the assumption that the one-step risk measures are identical imply that at a given level the sets of one-step-ahead risks coincide across all times and all states,

| (B.1) |

At time the two types of sets of risks for a given level coincide, . The relationship between the acceptability index and the corresponding family of risk measures implies the following two equivalence:

| (B.2) | ||||

We prove the claim by a backward induction. Let be an arbitrary state of the world and set . In the first step of the induction we prove that for all states : Consider a level . According to (B.2) the set contains positive elements only. Then, (B.1) implies that the same is true for the set , which means . Now consider a level . According to (B.2) the set contains some non-positive element. By (B.1), the same is true for the set , so .

The induction hypothesis assumes that for all . For levels this means that the sets and the sets (via (B.1) and the first step of the induction) contain positive elements only. For levels this means that the sets and the sets (via (B.1) and the first step of the induction) contain some non-positive element. The adaptiveness (R1) and independence (R2) of the risk measure imply that there exists an element that is non-positive in all states of the world. The same is true also for the set .

Inductive step: The properties of the risk measure imply the following form of the set ,

Consider a level . According to the induction hypothesis all are positive. Then, by applying the monotonicity (R3), an arbitrary element of can be bounded by

The risk is an element of the set , so by the induction hypothesis it is positive in all states of the world. This shows .

Now consider a level . Consider the elements of of the form

where is a non-positive element of , whose existence is guaranteed by the induction hypothesis. Monotonicity of the risk measure bounds these risks by

The risks are elements of the set , and by the induction hypothesis at least one of them is non-positive. Therefore, the set contains at least one non-positive element and . ∎

Proof of Theorem 3.5.

Firstly, note that the construction of the trading strategy guarantees that it is adapted and feasible. We prove the claim via backward induction by showing that

This suffices to show that . Since is a supremum, equality follows.

Consider time . Optimality of the position and the positive homogeneity imply that

for all levels . The iid asset returns and the identical one-step risk measures together with the positive homogeneity give the same for all states .

The induction hypothesis assumes that the risk

For the inductive step we use the recursiveness of the risk measure to express the time risk as

At level the induction hypothesis and the monotonicity provide a bound

The inequality follows again from the iid asset returns, identical one-step risk measures, the positive homogeneity and the strategy corresponding to the scaled position . We conclude . ∎

| Asset 1 | ||||

|---|---|---|---|---|

| Asset 2 |

| AIT | GLR | RAROC | ||||||||||||||

| Iter | Iter | Iter | ||||||||||||||

| Step 1 | Step 1 | Step 1 | ||||||||||||||

| + | + | |||||||||||||||

| + | + | + | ||||||||||||||

| Step 2 | ||||||||||||||||

| Step 2 | Step 2 | |||||||||||||||

| + | ||||||||||||||||

| + | + | + | ||||||||||||||

| + | ||||||||||||||||

| + | + | + | ||||||||||||||

| + | + | + | ||||||||||||||

| + | + | |||||||||||||||

| + | + | |||||||||||||||

| + | + | |||||||||||||||

| + | + | + | ||||||||||||||

| + | + | |||||||||||||||

| + | ||||||||||||||||

| Modified algorithm for GLR | Mixed algorithm for GLR | Zero-level algorithm for GLR | |||||||||||||||||

| Iter | Iter | Iter | |||||||||||||||||

| Step 1 | Step 1 | Step 1 | |||||||||||||||||

| + | + | ||||||||||||||||||

| + | |||||||||||||||||||

| Step 2 | Step 2 | Step 2 | |||||||||||||||||

| + | |||||||||||||||||||

| + | + | + | |||||||||||||||||

| + | Iter | + | |||||||||||||||||

| + | + | ||||||||||||||||||

| + | |||||||||||||||||||

| + | + | ||||||||||||||||||

| + | + | + | |||||||||||||||||

| + | + | ||||||||||||||||||

| + | + | + | |||||||||||||||||

| + | + | ||||||||||||||||||

| + | |||||||||||||||||||

| + | + | ||||||||||||||||||

| + | + | + | |||||||||||||||||

| + | + | ||||||||||||||||||

| + | + | + | |||||||||||||||||

| + | |||||||||||||||||||

| + | |||||||||||||||||||

| + | |||||||||||||||||||

| 1.9e-06, 5.0e-05 | |||||||||||||||||||

| Step 1 | Step 2 | Run time | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Iter | Iter | (s) | |||||||

| 5 | 18 | 6.1e-05 | 3.78 | ||||||

| 2 | 18 | 7.6e-05 | 3.40 | ||||||

| 4 | 18 | 9.5e-05 | 3.56 | ||||||

| 5 | 31 | 7.5e-09 | 6.22 | ||||||

| 15 | no Step 2 | 1.88 | |||||||

| 17 | 18 | 6.1e-05 | 4.67 | ||||||

| 15 | no Step 2 | 4.61 | |||||||

| 16 | 18 | 6.1e-05 | 7.15 | ||||||

| Step 1 | Step 2 | Run time | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Iter | Iter | (s) | |||||||

| 9 | 22 | 6.1e-05 | 21.53 | ||||||

| 5 | 21 | 7.6e-05 | 17.27 | ||||||

| 2 | 21 | 9.5e-05 | 15.74 | ||||||

| 9 | 35 | 7.5e-09 | 30.40 | ||||||

| 15 | no Step 2 | 6.50 | |||||||

| 18 | 22 | 6.1e-05 | 23.91 | ||||||

| 15 | no Step 2 | 13.41 | |||||||

| 20 | 22 | 6.1e-05 | 30.27 | ||||||

| Step 1 | Step 2 | Run time | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Iter | Iter | (s) | |||||||

| 2 | 15 | 6.1e-05 | 7.20 | ||||||

| 4 | 15 | 7.6e-05 | 9.41 | ||||||

| 8 | 14 | 9.4e-05 | 12.84 | ||||||

| 2 | 28 | 7.5e-09 | 11.07 | ||||||

| 15 | no Step 2 | 10.55 | |||||||

| 20 | 15 | 6.1e-05 | 19.59 | ||||||

| 15 | no Step 2 | 7.04 | |||||||

| 18 | 15 | 6.1e-05 | 13.41 | ||||||

| Algorithm | Step 1 | Bisection on | Bisection on | Run time | |||||

|---|---|---|---|---|---|---|---|---|---|

| Iter | Iter | Iter | (s) | ||||||

| Original | 5 | 18 | 6.1e-05 | 3.32 | |||||

| Modified | 2 | 23 | 8.3e-05 | 3.67 | |||||

| Mixed | 2 | 5 | 18 | 6.1e-05 | 3.90 | ||||

| Zero level | 3 | 18 | 5.9e-05 | 2.96 | |||||

| free | Original | 5 | 18 | 6.1e-05 | 4.89 | ||||

| Modified | 2 | 23 | 8.5e-05 | 5.11 | |||||

| Mixed | 2 | 5 | 18 | 6.1e-05 | 5.09 | ||||

| Zero level | 3 | 18 | 5.1e-05 | 4.36 | |||||

| Algorithm | Step 1 | Bisection on | Bisection on | Run time | |||||

|---|---|---|---|---|---|---|---|---|---|

| Iter | Iter | Iter | (s) | ||||||

| Original | 9 | 22 | 6.1e-05 | 19.45 | |||||

| Modified | 2 | 29 | 7.4e-05 | 18.42 | |||||

| Mixed | 2 | 8 | 22 | 6.1e-05 | 19.75 | ||||

| Zero level | 3 | 22 | 6.7e-05 | 14.54 | |||||

| free | Original | 9 | 22 | 6.1e-05 | 39.56 | ||||

| Modified | 2 | 29 | 7.9e-05 | 40.85 | |||||

| Mixed | 2 | 8 | 22 | 6.1e-05 | 41.66 | ||||

| Zero level | 3 | 22 | 6.8e-05 | 32.17 | |||||

| Algorithm | Step 1 | Bisection on | Bisection on | Run time | |||||

|---|---|---|---|---|---|---|---|---|---|

| Iter | Iter | Iter | (s) | ||||||

| Original | 2 | 15 | 6.1e-05 | 5.88 | |||||

| Modified | 2 | 18 | 6.0e-05 | 5.88 | |||||

| Mixed | 2 | 2 | 15 | 6.1e-05 | 5.62 | ||||

| Zero level | 2 | 15 | 9.1e-05 | 5.53 | |||||

| free | Original | 2 | 15 | 6.1e-05 | 6.91 | ||||

| Modified | 2 | 18 | 6.3e-05 | 8.00 | |||||

| Mixed | 2 | 3 | 18 | 6.1e-05 | 8.12 | ||||

| Zero level | 2 | 15 | 9.4e-05 | 7.04 | |||||

References

- [ADEH99] P. Artzner, F. Delbaen, J.-M. Eber, and D. Heath. Coherent measures of risk. Math. Finance, 9(3):203–228, 1999.

- [AFP12] B. Acciaio, H. Föllmer, and I. Penner. Risk assessment for uncertain cash flows: model ambiguity, discounting ambiguity, and the role of bubbles. Finance and Stochastics, 16:669–709, 2012.

- [AN04] V. Agarwal and N. Y. Naik. Risks and Portfolio Decisions Involving Hedge Funds. The Review of Financial Studies, 17(1):63–98, 01 2004.

- [AP11] B. Acciaio and I. Penner. Dynamic risk measures. In G. Di Nunno and B. Øksendal (Eds.), Advanced Mathematical Methods for Finance, Springer, pages 1–34, 2011.

- [BBN14] S. Biagini and J. Bion-Nadal. Dynamic quasi-concave performance measures. Journal of Mathematical Economics, 55:143–153, December 2014.

- [BCC15] T. R. Bielecki, I. Cialenco, and T. Chen. Dynamic conic finance via Backward Stochastic Difference Equations. SIAM J. Finan. Math., 6(1):1068–1122, 2015.

- [BCDK16] T. R. Bielecki, I. Cialenco, S. Drapeau, and M. Karliczek. Dynamic assessment indices. Stochastics: An International Journal of Probability and Stochastic Processes, 88(1):1–44, 2016.

- [BCIR13] T. R. Bielecki, I. Cialenco, I. Iyigunler, and R. Rodriguez. Dynamic Conic Finance: Pricing and hedging via dynamic coherent acceptability indices with transaction costs. International Journal of Theoretical and Applied Finance, 16(01):1350002, 2013.

- [BCP17] T. R. Bielecki, I. Cialenco, and M. Pitera. A survey of time consistency of dynamic risk measures and dynamic performance measures in discrete time: LM-measure perspective. Probability, Uncertainty and Quantitative Risk, 2(3):1–52, 2017.

- [BCP18] T. R. Bielecki, I. Cialenco, and M. Pitera. A unified approach to time consistency of dynamic risk measures and dynamic performance measures in discrete time. Mathematics of Operations Research, 43(1):204–221, 2018.

- [BCZ14] T. R. Bielecki, I. Cialenco, and Z. Zhang. Dynamic coherent acceptability indices and their applications to finance. Mathematical Finance, 24(3):411–441, 2014.

- [BDB15] F. Bellini and E. Di Bernardino. Risk management with expectiles. European Journal of Finance, 05 2015.

- [BL00] A. Bernardo and O. Ledoit. Gain, loss, and asset pricing. J. of Polit. Econ., 108:144–172, 2000.

- [CK13] P. Cheridito and E. Kromer. Reward-Risk Ratio. Journal of Investment Strategies, 3(1):1–16, 2013.

- [CM09] A. Cherny and D. B. Madan. New measures for performance evaluation. The Review of Financial Studies, 22(7):2571–2606, 2009.

- [EM14] E. Eberlein and D. B. Madan. Maximally acceptable portfolios. In Kabanov Y., Rutkowski M., Zariphopoulou T. (eds) Inspired by Finance. Springer, 2014.

- [GISW02] W. N. Goetzmann, J. E. Ingersoll, M. I. Spiegel, and I. Welch. Sharpening Sharpe ratios. NBER Working Paper No. 9116, page 51, 2002.

- [KMZ17] C. Karnam, J. Ma and J. Zhang. Dynamic approaches for some time-inconsistent optimization problems. Ann. Appl. Probab., 27(6):3435–3477, 2017.

- [KR19] G. Kováčová and B. Rudloff. Time consistency of the mean-risk problem. Preprint arXiv:1806.10981, 2019.

- [KY91] H. Konno and H. Yamazaki. Mean-absolute deviation portfolio optimization model and its applications to Tokyo stock market. Management science, 37(5):519–531, 1991.

- [LW16] A. Löhne and B. Weißing. Equivalence between polyhedral projection, multiple objective linear programming and vector linear programming. Mathematical Methods of Operations Research, 84(2):411–426, Oct 2016.

- [MRS03] R. D. Martin, S. Z. Rachev, and F. Siboulet. Phi-alpha optimal portfolios and extreme risk management. The Best of Wilmott 1: Incorporating the Quantitative Finance Review, 1:223, 2003.

- [MS16] D. B. Madan and W. Schoutens. Applied conic finance. Cambridge University Press, Cambridge, 2016.

- [OBS+05] S. Ortobelli, A. Biglova, S. Stoyanov, S. Z. Rachev, and F. Fabozzi. A comparison among performance measures in portfolio theory. IFAC Proceedings Volumes, 38(1):1 – 5, 2005. 16th IFAC World Congress.

- [RGS13] E. Rosazza Gianin and E. Sgarra. Acceptability indexes via -expectations: an application to liquidity risk. Mathematical Finance (2013) 7:457-475, 2013.

- [Rie04] F. Riedel. Dynamic coherent risk measures. Stochastic Process. Appl., 112(2):185–200, 2004.

- [Sha64] W. F. Sharpe. Capital asset prices: A theory of market equilibrium under conditions of risk. Journal of Finance, 19:425–442, 1964.

- [SS01] F. A. Sortino and S. Satchell. Managing downside risk in financial markets. Butterworth-Heinemann, 2001.

- [SY84] H. Shalit and S. Yitzhaki. Mean-Gini, portfolio theory, and the pricing of risky assets. J. of Finance, 39(5):1449–1468, 1984.

- [You98] M. R. Young. A minimax portfolio selection rule with linear programming solution. Management science, 44(5):673–683, 1998.