capbtabboxtable[][\FBwidth]

Comparison of Bayesian Nonparametric Density Estimation Methods

Adel Bedouia111Corresponding author: Adel Bedoui. Email: bedoui.adel1@gmail.com and Ori Rosenb

aDepartment of Statistics, University of Georgia, Athens, Georgia 30602

bDepartment of Mathematical Sciences, University of Texas at El Paso, El Paso, Texas 79968

Key Words: Bayesian inference; asymptotic distribution; density estimation; Hamiltonian Monte Carlo; MCMC; penalized Gaussian mixtures.

ABSTRACT

In this paper, we propose a nonparametric Bayesian approach for Lindsey and penalized Gaussian mixtures methods. We compare these methods with the Dirichlet process mixture model. Our approach is a Bayesian nonparametric method not based solely on a parametric family of probability distributions. Thus, the fitted models are more robust to model misspecification. Also, with the Bayesian approach, we have the entire posterior distribution of our parameter of interest; it can be summarized through credible intervals, mean, median, standard deviation, quantiles, etc. The Lindsey, penalized Gaussian mixtures, and Dirichlet process mixture methods are reviewed. The estimations are performed via Markov chain Monte Carlo (MCMC) methods. The penalized Gaussian mixtures method is implemented via Hamiltonian Monte Carlo (HMC). We show that under certain regularity conditions, and as n increases, the posterior distribution of the weights converges to a Normal distribution. Simulation results and data analysis are reported.

1 Introduction

A hallmark of many modern data problems is to find the characteristics and the distribution of data. For instance, the objectives could be the extraction of information about skewness and multimodality in the data that are not available at first glance. As a result density estimation has become increasingly popular. In finance, density estimation plays an important role in detecting heavy tails and patterns in a market stock. A common classical approach is the histogram (Pearson, 1895). Several approaches to nonparametric density estimation are available, the most common of which is kernel estimation (Rosenblatt, 1956; Parzen, 1962; Nadaraya, 1964; Watson, 1964; Wand and Jones, 1995). In this paper, we consider three less traditional approaches to nonparametric density estimation: Lindsey’s method (Lindsey, 1974), Penalized Gaussian Mixtures (PGM) (Ghidey et al., 2004) and Dirichlet Process Mixture Models (DPMM) (Ferguson, 1973). Schellhase and Kauermann (2012) estimate densities using penalized mixtures of -spline densities and compare it via simulation to other estimation methods, including kernel estimation and classical finite mixtures. Schellhase and Kauermann (2012) discuss penalized mixtures in detail, and refer to R packages that implement the methods to which penalized mixtures are compared. Unlike their approach, ours is Bayesian. Moreover, we implement the HMC to estimate weights in the PGM method and show that, under certain regularity, the posterior distribution of the coefficients converges to a Normal distribution. In addition, we derive a Bayesian version for Lindsey’s method, which converts density estimation to a regression problem. To estimate the regression function, we applied the cubic smoothing spline as it is a flexible approach to fitting data such that it produces a smooth function. The use of the Bayesian nonparametric method has various advantages. For example, the resulting method is more robust to the data distribution, as it is partially based on the parameterized families of prior probabilities distributions. Moreover, we have the entire posterior distribution of our parameter of interest, which can be summarized through credible intervals, mean, median, standard deviation, quantiles, range, etc. That is, probability comes into play in a Bayesian credible interval after collecting the data. For example, based on the data, we think there is a 95% probability that the true parameter value is in the interval. However, the probability comes into play in a frequentist confidence interval before collecting the data. For instance, we think there is a 95% probability that we will collect data that produces an interval that contains the true parameter value.

2 Lindsey’s Method

Lindsey’s method (LM) (Lindsey, 1974) recasts density estimation as a regression problem. Wasserman (2006) describes it as follows. Suppose a random sample from a density on [a,b] is available. Divide the interval [a,b] into equal width bins and denote by and the number of observations and the abscissa of the center of the th bin, respectively. Let , then

| (1) |

where , and . The regression model (1) follows from the assumption that has an approximate Poisson distribution with mean and from applying the delta method. More specifically, using and applying the delta method show that and . To estimate , one applies their favorite nonparametric regression procedure to the data , , to obtain . An estimate is then given by

where . In this paper, we use the cubic smoothing splines to obtain . Lindsey’s method is described in many other references, for example Brown et al. (2010) and Efron (2010).

2.1 Applying Cubic Smoothing Splines to Estimate the Regression Function

We now estimate the function in Equation (1) by the cubic smoothing splines method using Wahba (1990)’s approach. Precisely, we implement a Bayesian framework to estimate . We let:

where is a zero-mean Gaussian process with variance covariance matrix , with the element of given by

To facilitate the computation, we write where is obtained as follows. The matrix is expressed as , where is the matrix of eigenvectors of and is a diagonal matrix containing the eigenvalues of . Letting and setting the prior on to be N() means that . The parameter is a smoothing parameter controlling the smoothness of .

2.1.1 Prior Distributions

The following priors are placed on the parameters:

-

1.

, is a large fixed number.

-

2.

-

3.

, .

-

4.

, .

The model can thus be written as:

where

X= .

To properly model , One should be careful in selecting the choice of and in the uniform priors used for and . The eventual choice plays a critical role in the amount of smoothing of the data. One good choice is to let and . The number of columns of is reduced from to by retaining only the columns, corresponding to the largest eigenvalues of without affecting the fit.

2.1.2 Gibbs Sampling

To sample from the posterior we draw from the following conditional distributions

-

1.

Sample from

where , i.e., where and are concatenated columnwise, and

-

2.

Sample from

(2) i.e., a truncated distribution. , i.e., where and are concatenated columnwise

-

3.

Sample

(3)

3 Penalized Gaussian Mixtures

Ghidey et al. (2004) proposed a density estimation method based on a mixture of Gaussians with fixed parameters. In particular, the interval is first divided into a grid of equally spaced points, , , which are used as the means of the Gaussian densities in the following mixture model

| (4) |

where . This choice of is based on equating the width of the support of a cubic -spline consisting of four equal intervals of width , each, to . As an alternative to Gaussian densities, -spline densities can be used as the basis functions, see for example Staudenmayer et al. (2008). As for the value of , Schellhase and Kauermann (2012) recommend that it be large enough but usually small compared to the sample size, which is the rule of thumb advocated by Ruppert (2002). The weights in (4) are given by

such that , and is set to zero for identifiability.

Let . To obtain a smooth fit, the corresponding to neighboring Gaussian densities must be close to one another (Eilers and Marx, 1996). This can be achieved by constraining the corresponding to be close to one another. By analogy to Eilers and Marx (1996)’s idea, Lang and Brezger (2004) require the to satisfy , where , and , . However, this results in an improper prior distribution on similar to the intrinsic Gaussian Markov random field prior used in spatial statistics. Chib and Jeliazkov (2006) place a joint normal prior on and which fixes the impropriety of the prior on . For example, if , where is a fixed constant, the prior on becomes

| (5) |

where is a vector consisting of the first two entries of . The summation in the exponent on the right-hand side of (5) can be expressed as , where and is the matrix

Equation (5) can now be re-expressed as

where , for .

The parameter determines how smooth the estimated density will be. We place a Half- (Gelman, 2006) distribution on , whose pdf is , , where the hyperparameters and are assumed known. The larger the value of , the less informative the prior is. In addition, the weights, , are not sensitive to the value of A (see Appendix A3). Computationally, it is convenient to utilize the following scale mixture representation (Wand et al., 2012): , , where , is the inverse Gamma distribution with pdf , .

3.1 Estimation

Given a sample , it is convenient to augment the data with indicators taking values in . The augmented likelihood is then given by

| (6) |

Equation (6) in combination with the priors give rise to the following sampling scheme.

-

1.

Sample from

(7) where . A Hamiltonian Monte Carlo (HMC) algorithm is used to sample from this distribution. More details are given in the Appendix.

-

2.

Sample from .

-

3.

Sample from .

-

4.

Sample the indicators one at a time from multinomial distributions , where , , .

3.2 Asymptotic Distribution of

First, assume that we place a normal prior on with mean and covariance matrix . We assume that is known and is positive definite. Under certain regularity conditions, and as , the posterior distribution of converges to normal, with mean and covariance , where

and is the maximum likelihood estimate of , is the prior mean, and is the negative second derivative of the log likelihood evaluated at . A proof is presented in the Appendix. By placing a normal prior on 01τ2β^’P^*ββm_nJ_n

4 Dirichlet Process Mixture Models

Unlike the mixture of Section 3, in this section, mixtures with a countably infinite number of components are used by placing a Dirichlet process prior on the mixing proportions (Neal, 2000). Dirichlet process mixture models (DPMM) were originally proposed by Ferguson (1973), Antoniak (1974) and Ferguson (1983) and were first used in practice by Escobar (1994). Given data independently drawn from some unknown distribution, a direct formulation of the DPMM is as follows (Neal, 2000).

| (8) |

In (8), (possibly a vector) is the parameter of the mixture component to which belongs, and is the distribution of the mixture components. For example, if is , then . Two data points and , belonging to the same component, share the same component parameters, i.e., . The distribution is an infinite discrete distribution drawn from the Dirichlet process with concentration parameter and base distribution . For the th data point, an atom is drawn from , which may be equal to corresponding to , due to the discreteness of . The Dirichlet process can be represented by the Stick Breaking scheme (Sethuraman, 1994), the Chinese Restaurant Process (Aldous, 1985), and the Pólya Urn Scheme (Blackwell and MacQueen, 1973). In this work, we use the Stick Breaking representation. The stick breaking prior directly generates according to

| (9) |

where the random variables are iid . Having generated the , can now be expressed as , where are the distinct component parameters.

4.1 Infinite Mixture Models

Consider the finite mixture model

where the are component indicators, , and . Neal (2000) shows that the limit of , as , implies the conditional probabilities for the , which in turn shows the equivalence of the infinite mixture model and the DPMM.

4.2 Implementation

In this paper, we use the DPMM with Gaussian components, i.e., model (8), where is . More specifically, using the stick-breaking prior, , given in (9), the model can be written as

We implement the MCMC scheme of Ishwaran and Lancelot (2002), who truncate by , where is pre-specified. The priors on and on are as follows.

-

1.

, is fixed.

-

2.

, , are fixed.

-

3.

, , are fixed.

-

4.

, is fixed.

For the sampling scheme, see Ishwaran and Lancelot (2002).

5 Simulation and Example

5.1 Simulations

This section presents a comparison of the three density estimation methods described in sections 2-4, along with the kernel and log-spline densities. For the kernel density, we use two different bandwidths, which are UCV and SJ. UCV implements unbiased cross-validation, whereas SJ implements the methods of Sheather and Jones (1991) to select the bandwidth using pilot estimation of derivatives. We simulate data from five different distributions taken from Schellhase and Kauermann (2012) (Table 1). As in Schellhase and Kauermann (2012), we use two different sample sizes: and . For our PGM approach, we use three different values of : 20, 30, and 50. For the DPPM method, we set the number of mixture components equal to 35.

| Distribution | ||

|---|---|---|

To sample in PGM, we use a block of HMC and Gibbs sampler. The HMC technique requires fewer iterations to explore the parameter space and converges rapidly to the target distribution (Hartmann and Ehlers, 2017). Therefore, we implement the HMC and Gibbs sampler with 5000 iterations and 1000 burn-in. HMC has two tuning parameters: the step size and the number of leapfrog steps . We use trial and error to set their values. In particular, we select and . For Lindsey and DPPM methods, we implement the Gibbs sampler. We measure the performance of the estimates using the integrated mean squared error (IMSE). The IMSE is obtained by

where is the number of samples drawn from each distribution, which in our simulation study is set to 100. The MSE measures the difference between the true density and its estimate and is given by

where and are the true density and its estimate evaluated at , and is the sample size. The logspline and the kernel density estimates are estimated using the logspline package (Charles Kooperberg, Cleve Moler, Jack Dongarra, 2020) and stats package (R Core Team and contributors worldwide, 2013), respectively.

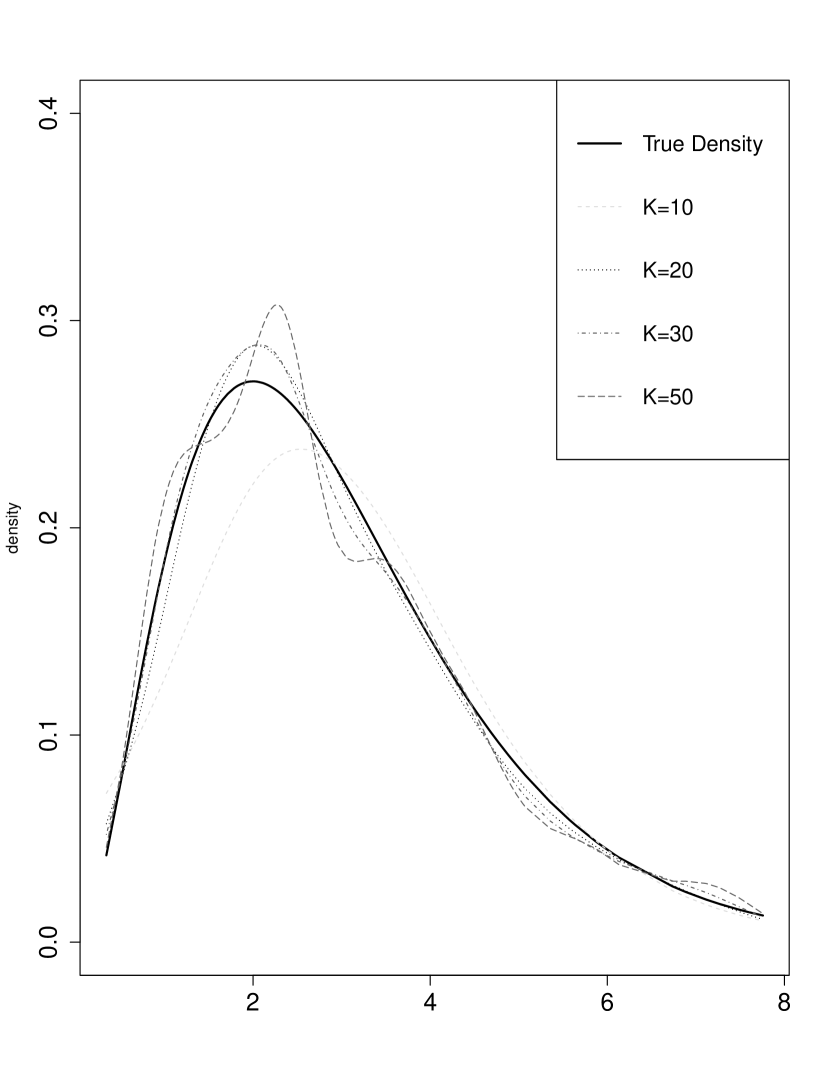

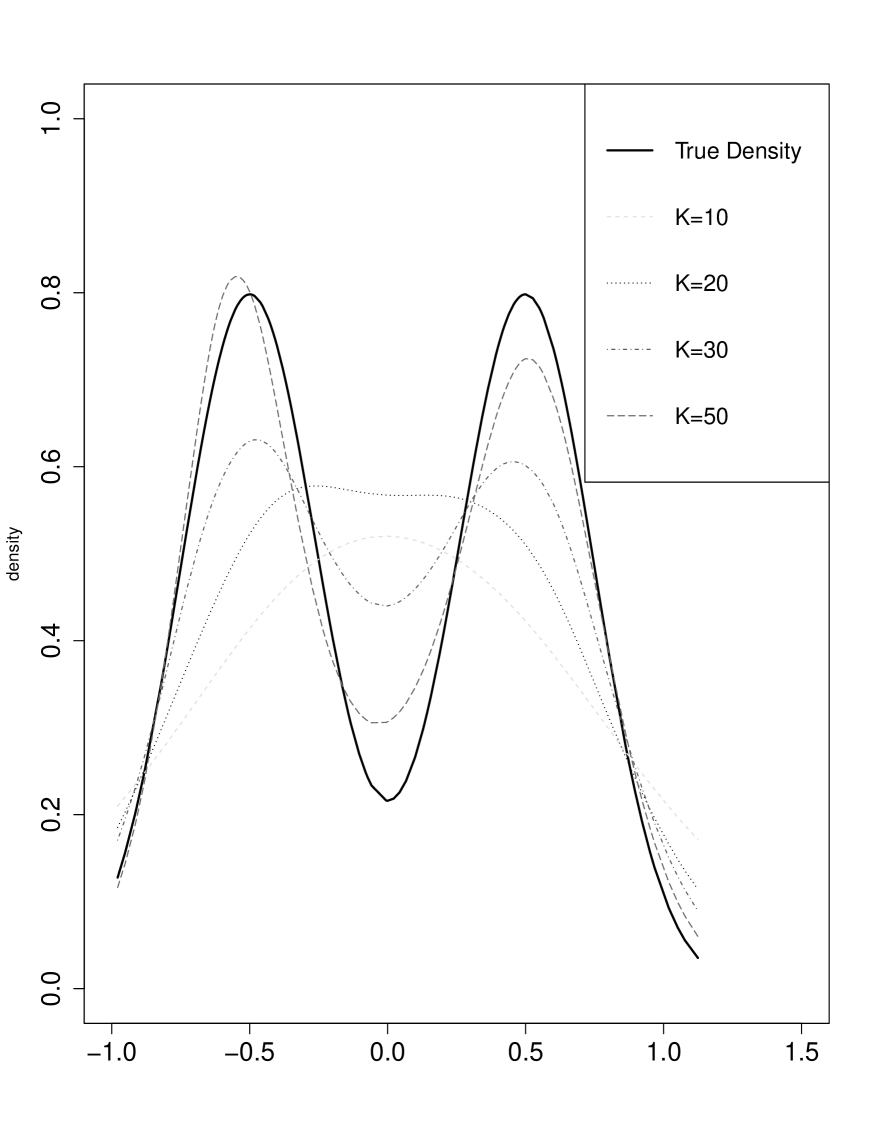

Table 2 presents the results of the simulations for the PGM, LM, DPPM, Kernel densities, and log-spline methods. Our Bayesian implementation of PGM and Lindsey methods appear to perform promisingly well in comparison with the DPMM, Kernel, log-spline methods, and the results from Schellhase and Kauermann (2012) and in some cases even better than its frequentist counterpart. Figure 1 displays the PGM estimates, based on a single sample from and , respectively. is the Gamma distribution with shape 3 and scale 1, and is the mixture of two components. Increasing the value of improves the fit.

| Sample size | PGM | LM | DPMM | Kernel | Log-spline | ||||

|---|---|---|---|---|---|---|---|---|---|

| K=20 | K=30 | K=50 | bw=UCV | bw=SJ | |||||

| 1.106 | 1.841 | 2.952 | 1.393 | 0.791 | 1.486 | 1.015 | 6.462 | ||

| 0.306 | 0.535 | 0.910 | 0.275 | 0.157 | 0.369 | 0.303 | 1.224 | ||

| 50.974 | 25.824 | 6.838 | 45.711 | 7.326 | 7.702 | 6.015 | 25.357 | ||

| 42.178 | 15.642 | 2.365 | 38.100 | 1.591 | 2.990 | 2.468 | 6.687 | ||

| 0.532 | 0.534 | 0.913 | 0.805 | 1.278 | 0.475 | 0.557 | 1.777 | ||

| 0.220 | 0.196 | 0.320 | 0.286 | 0.288 | 0.203 | 0.226 | 0.485 | ||

| 10.061 | 24.875 | 31.106 | 22.358 | 35.321 | 2.808 | 2.240 | 9.962 | ||

| 1.474 | 2.322 | 5.440 | 19.815 | 30.593 | 0.829 | 0.699 | 2.344 | ||

| 1.004 | 1.081 | 1.440 | 1.676 | 1.634 | 1.658 | 1.484 | 2.870 | ||

| 0.536 | 0.336 | 0.407 | 0.205 | 0.627 | 0.209 | 0.58 | 0.706 | ||

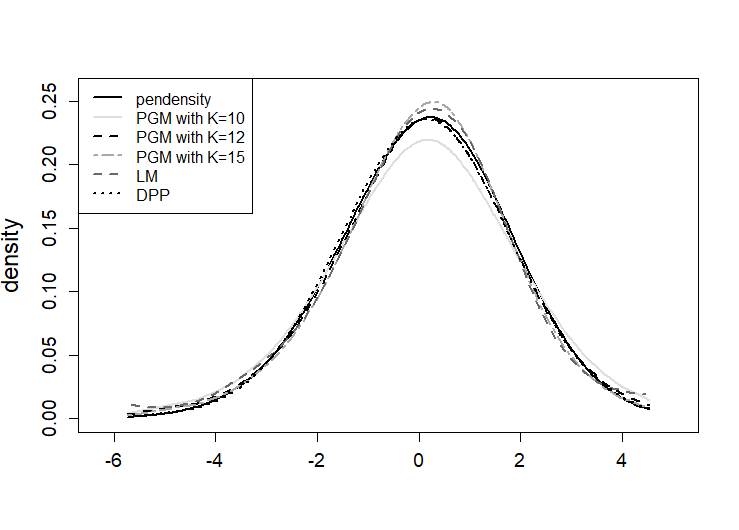

5.2 Example: Daily Returns.

We use the daily return data set from Schellhase and Kauermann (2012) presented in Section 3.2 of their paper, which represents the return of the two German stocks Deutsche Bank AG and Allianz AG in 2006. The corresponding density estimates of the Bayesian penalized mixture approach is given in Figure 2. We show the PGM estimate along with 3 competitors, which are Lindsey’s method, Dirichlet process mixture model, and penalized mixture approach (pendensity) (Schellhase and Kauermann, 2012). For the Bayesian PGM method, we used three different values for : 10, 12, and 15. We implement the MCMC scheme with 5000 iterations, the first 1000 of which are used as burn-in. The corresponding estimates are displayed in Figure 2. The PGM with and the DPPM approaches provide almost identical density estimates compared to the pendensity method.

6 Summary

In this paper, we have derived a nonparametric Bayesian approach for Lindsey (Lindsey, 1974) and penalized Gaussian mixtures method (Ghidey et al., 2004). Lindsey’s method recasts density estimation as a regression problem where we implement the cubic smoothing spline to estimate the regression function. For the PGM method, we used the HMC algorithm to estimate the weights mixtures. Moreover, we showed, under certain regularity, that the posterior distribution of the estimates in PGM converges to a Normal distribution. We ran simulations and compared our approaches to DPPM, Kernel, and log-splines methods. In general, it appeared from simulations that our approaches performed promisingly well when compared to the competitors, and in some cases even better than its frequentist counterpart. Among the Bayesian methods, the Lindsey approach is computationally less expensive.

Acknowledgement

The authors were supported in part by the National Security Agency under Grant Number H98230-12-1-0246. The United States Government is authorized to reproduce and distribute reprints not-withstanding any copyright notation herein.

Appendices

Appendix A1. Sampling from of Section 3

To draw from the conditional posterior density (7), we use the HMC algorithm (Neal, 2011). We first give an overview of HMC and then apply it to (7). HMC, also known as Hybrid Monte Carlo, is an MCMC method to generate posterior samples for which direct sampling is difficult. It uses the gradient of the posterior density and the Hamiltonian system to sample successive states for the Metropolis-Hastings algorithm with a large acceptance probability. The underlying logic of the HMC sampling is as follows. To sample from a posterior distribution , we treat the parameter as a particle and denote its value at its current position. We define the potential energy and the kinetic energy, respectively, as

where is the momentum vector, and is the mass matrix, also known as the dispersion matrix. The kinetic energy arises from the Gaussian distribution , where is a symmetric positive definite matrix. We set equal to the identity matrix. The Hamiltonian system is defined as

The position of and the momentum of the particle change over time and are determined by the partial derivatives of the Hamiltonian system. These partial derivatives give rise to the so-called Hamiltonian equations of motion

| (10) |

Neal (2011) showed that these Hamiltonian equations are reversible, invariant, and volume-preserving, which makes the Hamiltonian system suitable for MCMC sampling schemes. When lacks a closed form, equations (10) have no analytic solutions. Thus, the solution is approximated at discrete time steps. Following Neal (2011), we apply the leapfrog integration method to approximate the solution of the Hamiltonian equations. First, a small step size is selected, and the starting value of is the maximizer of . Then, given the current value of and at time , the position and momentum at time are updated as follows.

Sometimes the approximation introduces errors, and an accept-reject algorithm is required to conserve the invariant property of HMC (Neal, 2011). The procedure works as follows. In the first step, new values for the momentum vector are randomly drawn from a Gaussian distribution , independently of the current values of . In the second step, starting with the current state, , a Hamiltonian system is simulated for steps using the leapfrog method, with a step size of . At the end of this -step trajectory, the proposed state is accepted with probability

where and . If the proposed state is rejected, the next state is the same as the current one. To apply HMC to the sampling of in our case, we need to obtain and its gradient.

Appendix A2. Proof of the asymptotic Distribution of Section 3.2

The posterior distribution of is

where

Similar to Bernardo and Smith (1994), we expand the logarithm term about its maximum , obtained by setting the first derivatives of the logarithm to zero

where is the remainder, which is small for large .

In addition, we have: , where

If we assume is large and ignore constants of proportionality, we have:

Setting and , we have:

We complete the square above by adding and subtracting . Therefore,

is the kernel of , with and defined above.

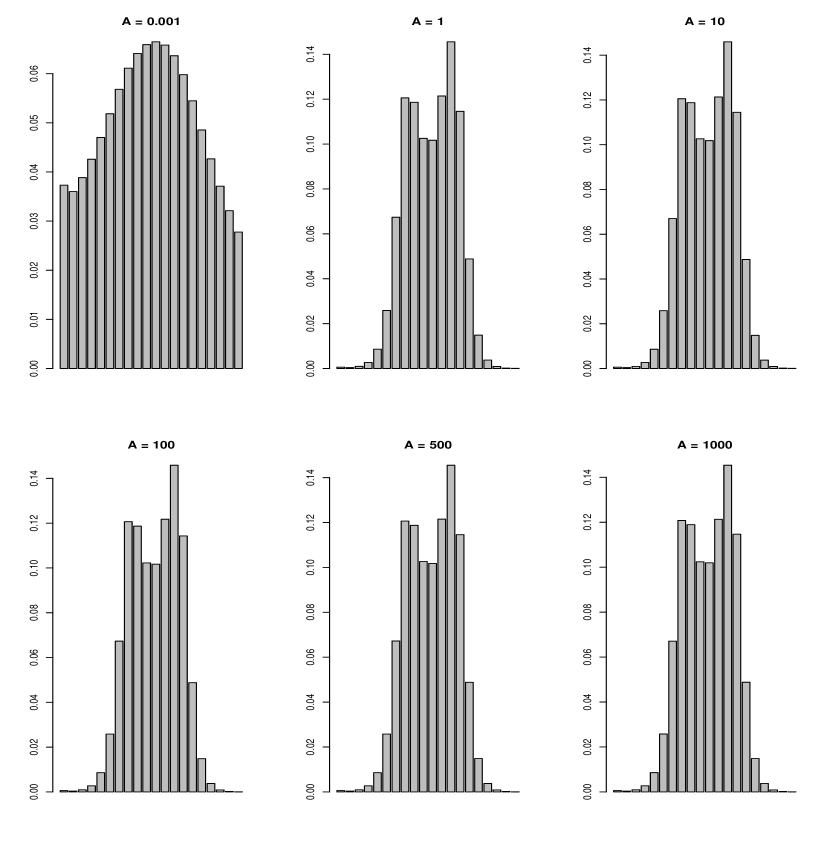

Appendix A3. The effect of the value A on the weights

In this example, we study the effect of the value A on the weights, , that use the logistic transformation such that and . We simulate datasets with from the following model: We set and . Similarly, we use a block of HMC and Gibbs sampler with 5000 iterations and 1000 burn-in. Figure 3 depicts the bar plots of the weights ’s based on different values of . We can see the absence of the effect of the prior on the weights after the logistic transformation; except when is near to zero where the weights take values near to .

References

- Aldous (1985) Aldous, D. (1985), “Exchangeability and related topics,” in École d’Été de Probabilités de Saint-Flour XIII-1983, ed. Hennequin, P., Berlin Heidelberg: Springer, vol. 1117 of Lecture Notes in Mathematics.

- Antoniak (1974) Antoniak, C. (1974), “Mixtures of Dirichlet processes with applications to Bayesian nonparametric problems,” The Annals of Statistics, 2, 1065–1358.

- Bernardo and Smith (1994) Bernardo, J. M. and Smith, A. F. M. (1994), Bayesian Theory, John Wiley & Sons, Chichester, New York, USA.

- Blackwell and MacQueen (1973) Blackwell, D. and MacQueen, J. (1973), “Ferguson distributions via Pólya urn schemes,” The Annals of Statistics, 1, 353–355.

- Brown et al. (2010) Brown, L., Cai, T., Zhang, R., Zhao, L., and Zhou, H. (2010), “The root-unroot algorithm for density estimation as implemented via wavelet block thresholding,” Probabability Theory and Related Fields, 146, 401–433.

- Charles Kooperberg, Cleve Moler, Jack Dongarra (2020) Charles Kooperberg, Cleve Moler, Jack Dongarra (2020), logspline: Routines for Logspline Density Estimation, R Foundation for Statistical Computing.

- Chib and Jeliazkov (2006) Chib, S. and Jeliazkov, I. (2006), “Inference in semiparametric dynamic models for binary longitudinal data,” Journal of the American Statistical Association, 101, 685–700.

- Efron (2010) Efron, B. (2010), Large-Scale Inference: Empirical Bayes Methods for Estimation, Testing, and Prediction, Cambridge University Press, New York.

- Eilers and Marx (1996) Eilers, P. and Marx, B. (1996), “Flexible estimation with -splines and penalties,” Statistical Science, 11, 89–121.

- Escobar (1994) Escobar, M. (1994), “Estimating normal means with a Dirichlet process prior,” Journal of the American Statisticial Association, 89, 268–277.

- Ferguson (1973) Ferguson, T. (1973), “A Bayesian analysis of some nonparametric problems,” The Annals of Statistics, 1, 209–230.

- Ferguson (1983) — (1983), “Bayesian density estimation by mixtures of normal distributions,” in Recent Advances in Statistics, eds. Rizvi, H. and Rustagi, J., New York: Academic Press, pp. 287–303.

- Gelman (2006) Gelman, A. (2006), “Prior distributions for variance parameters (Comment on article by Browne and Draper),” Bayesian Analysis, 1, 515–534.

- Ghidey et al. (2004) Ghidey, W., Lesaffre, E., and Eilers, P. (2004), “Smooth random effects distribution in a linear mixed model,” Biometrics, 60, 945–953.

- Hartmann and Ehlers (2017) Hartmann, M. and Ehlers, R. (2017), “Bayesian inference for generalized extreme value distributions via Hamiltonian Monte Carlo,” Communications in Statistics: Simulation and Computation, 46, 5285–5302.

- Ishwaran and Lancelot (2002) Ishwaran, H. and Lancelot, F. (2002), “Approximate Dirichlet process computing in finite normal mixtures: smoothing and prior information,” Journal of Computational and Graphical Statistics, 11, 1–26.

- Lang and Brezger (2004) Lang, S. and Brezger, A. (2004), “Bayesian P-splines,” Journal of Computational and Graphical Statistics, 13, 183–212.

- Lindsey (1974) Lindsey, J. (1974), “Construction and comparison of statistical models,” Journal of the Royal Statistical Society Series B, 36, 418–425.

- Nadaraya (1964) Nadaraya, E. (1964), “On estimating regression,” Theory of Probability and Its Applications, 9, 141–142.

- Neal (2000) Neal, R. (2000), “Markov chain sampling methods for Dirichlet process mixture models,” Journal of Computational and Graphical Statistics, 9, 249–265.

- Neal (2011) — (2011), Handbook of Markov Chain Monte Carlo, chapter 5: MCMC using Hamiltonian dynamics, Chapman & Hall/CRC Handbooks of Modern Statistical Methods.

- Parzen (1962) Parzen, E. (1962), “On estimation of a probability density function and mode,” The Annals of Mathematical Statistics, 33, 1065–1076.

- Pearson (1895) Pearson, K. (1895), “Contributions to the Mathematical Theory of Evolution. II. Skew Variation in Homogeneous Material,” Philosophical Transactions of the Royal Society A: Mathematical, Physical and Engineering Sciences, 186, 343–414.

- R Core Team and contributors worldwide (2013) R Core Team and contributors worldwide (2013), stats: The R Stats Package, R Foundation for Statistical Computing, Vienna, Austria, ISBN 3-900051-07-0.

- Rosenblatt (1956) Rosenblatt, M. (1956), “Remarks on some nonparametric estimates of a density function,” Annals of Mathematical Statistics, 27, 832–837.

- Ruppert (2002) Ruppert, D. (2002), “Selecting the number of knots for prenalized splines,” Journal of Computational and Graphical Statistics, 11, 735–757.

- Schellhase and Kauermann (2012) Schellhase, C. and Kauermann, G. (2012), “Density estimation and comparison with a penalized mixture approach,” Computational Statistics, 27, 757–777.

- Sethuraman (1994) Sethuraman, J. (1994), “A constructive definition of Dirichlet priors,” Statistica Sinica, 4, 639–650.

- Sheather and Jones (1991) Sheather, S. J. and Jones, M. C. (1991), “A reliable data-based bandwidth selection method for kernel density estimation.” Journal of the Royal Statistical Society series B, 53.

- Staudenmayer et al. (2008) Staudenmayer, J., Ruppert, D., and Buonaccorsi, J. (2008), “Density estimation in the presence of heteroscedastic measurement error,” Journal of the American Statistical Association, 103, 726–736.

- Wahba (1990) Wahba, G. (1990), Spline Models for Observational Data, vol. 59 of CBMS-NSF Regional Conference Series in Applied Mathematics, Philadelphia: SIAM.

- Wand and Jones (1995) Wand, M. and Jones, M. (1995), Kernel Smoothing, New York: Chapman & Hall/CRC.

- Wand et al. (2012) Wand, M., Ormerod, J., Padoan, S., and Frühworth, R. (2012), “Mean field variational Bayes for elaborate distributions,” Bayesian Analysis, 7, 847–900.

- Wasserman (2006) Wasserman, L. (2006), All of Nonparametric Statistics, Springer-New York.

- Watson (1964) Watson, G. (1964), “Smooth regression analysis,” Sankhyā: The Indian Journal of Statistics, Series A, 26, 359–372.