sebrgb0.8,1,0.8

Optimization of the Model Predictive Control Update Interval Using Reinforcement Learning

Abstract

In control applications there is often a compromise that needs to be made with regards to the complexity and performance of the controller and the computational resources that are available. For instance, the typical hardware platform in embedded control applications is a microcontroller with limited memory and processing power, and for battery powered applications the control system can account for a significant portion of the energy consumption. We propose a controller architecture in which the computational cost is explicitly optimized along with the control objective. This is achieved by a three-part architecture where a high-level, computationally expensive controller generates plans, which a computationally simpler controller executes by compensating for prediction errors, while a recomputation policy decides when the plan should be recomputed. In this paper, we employ model predictive control (MPC) as the high-level plan-generating controller, a linear state feedback controller as the simpler compensating controller, and reinforcement learning (RL) to learn the recomputation policy. Simulation results for two examples showcase the architecture’s ability to improve upon the MPC approach and find reasonable compromises weighing the performance on the control objective and the computational resources expended.

keywords:

model predictive control, reinforcement learning, event-driven control1 Introduction

Reinforcement learning (RL) is a class of machine learning algorithms that discover optimal policies in the sense of maximizing some notion of utility through interacting with the dynamic system to be controlled (Sutton and Barto, 2018). It therefore offers an interesting complementary approach to developing control systems for problems unsuited to traditional control approaches based purely on first principles modeling. RL has already proven to be the state-of-the-art approach to classes of problems requiring complex decision-making over large time frames such as game playing (Mnih et al., 2015; Schrittwieser et al., 2019; Berner et al., 2019). However there are some major limitations to the RL framework that inhibits its applicability to control applications, notably the lack of guarantees for safe operation and ability to specify constraints. Some of these limitations can be addressed by combining RL with trusted control approaches such as model predictive control (MPC), thereby allow for learning of various aspects of the control problem while having a trusted controller oversee the process and ensure safe operation (Zanon and Gros, 2020; Gros et al., 2020).

On the other hand, the MPC approach has a few major drawbacks of its own, notably its reliance on having a reasonably accurate model of the system. Unfortunately, obtaining such a model can be both difficult and costly. Moreover, the MPC approach has a heavy online computational cost, as it involves solving an optimal control problem (OCP) at every time step over a selected horizon. MPC is therefore in many cases unsuited for low-powered or battery-driven applications, and employing MPC in these scenarios often necessitates some form of compromise, see e.g. Feng et al. (2012) and Gondhalekar et al. (2015). While we in this paper address this problem from an energy perspective of reducing the frequency of computations, one can also look at reducing the complexity of the MPC computation itself. The two main tunable parameters in this regard is the optimization horizon length, which when lowered can lead to myopic behaviour, and the step size which when too large impacts control performance as the controller is unable to properly respond to high frequency dynamics and transient disturbances. The main techniques to reduce computational complexity are early termination (suboptimal) MPC (Scokaert et al., 1999), explicit MPC (Bemporad et al., 2002), semi-explicit MPC (Goebel and Allgöwer, 2015) and move-blocking (Cagienard et al., 2004).

As an alternative to the normal digital control system approach of measuring system state and calculating control signal at equidistant points in time, one can instead select these points by some other criteria, yielding a control system that consists of a control law and a triggering policy. This event-triggered control paradigm could be used to increased control performance or reduce frequency of computations based on how the triggering policy is designed (Åström and Bernhardsson, 2002; Heemels et al., 2008). Event-triggered MPC has been suggested in the literature to reduce resource usage particularly in networked communication systems and multi-agent systems (Iino et al., 2009; Berglind et al., 2012; Li and Shi, 2014; Chakrabarty et al., 2018). In these works the triggering policy is a predetermined hand-crafted policy based on domain knowledge about the system and the controller, a learned policy on the other hand can be derived without requiring system knowledge and be adaptive to changing dynamics and uncertain disturbances. In Yoo and Johansson (2019) the authors use a learned empirical risk minimization model to predict the unknown system noise in \pgls*mpc framework and use its output to determine the triggering thresholds. For a recent review of machine learning applied to event-triggered networked control systems, see Sedghi et al. (2020).

In this work we look at the single agent setting and suggest to learn the triggering policy with RL. Several other works such as Baumann et al. (2018) and Yang et al. (2019) have proposed RL for learning the triggering policy, however these works simultaneously learn the control law as opposed to our work which employs MPC for this purpose. The contribution of this paper lies in proposing a novel architecture involving a dual mode MPC and linear quadratic regulator (LQR) control law and \pgls*rl based triggering policy, and in deriving how the event-triggered MPC problem can be framed as \pgls*mdp. The MPC solves the OCP, providing a plan in the form of an input sequence and the predicted state trajectory from executing the input sequence, while the LQR provides an additive compensatory input based on the state trajectory prediction errors extending the viability of MPC solution. Finally, the RL triggering policy, henceforth referred to as the recomputation policy, selects time instants when the improved control performance from recomputing the MPC solution outweigh the computational costs. We empirically demonstrate the effectiveness of the proposed architecture through two simulated use cases.

The rest of the paper is organized as follows. First, Section 2 presents the requisite theoretical background of the proposed architecture, while Section 3 presents the implementation details. Section 4 describes the two case studies illustrating the proposed system, and Section 5 presents the results of these case studies and discusses their significance. Finally, Section 6 presents our closing thoughts on the paper.

2 Preliminaries and Problem Formulation

2.1 Model Predictive Control

MPC is a control technique where the current control action is obtained by solving at each time step an open loop finite horizon OCP (1), where the initial state is given as the current state of the plant. The MPC solution consists of an input sequence minimizing the objective function over the optimization horizon, of which only the first input is applied to the plant, and the OCP is then computed again at the subsequent time step. We consider in this paper discrete time direct state feedback MPC, meaning the MPC gets exact measurements of the state of the plant at discrete time intervals, and the optimization variables are assumed constant between sampling instances.

| (1a) | ||||

| s.t. | (1b) | |||

| (1c) | ||||

| (1d) | ||||

Here, is the plant state vector at time and is the measurement of these states, is the control input vector and , are time-varying parameters whose value is forecasted over the optimization horizon, is the MPC model dynamics which may differ from the plant system dynamics due to unmodeled effects such as process noise , is the constraint vector and is the optimization horizon length. The objective function consists of the stage cost , which — in addition to the input-change term discouraging bang-bang control — is summed over every step of the optimization horizon except the last, and the end of horizon cost . The state and control inputs are subject to constraints, which must hold over the whole optimization horizon for the MPC solution to be considered feasible.

We propose in this paper to modify the traditional MPC approach by not statically recomputing the MPC solution at every time step, but instead to utilize a recomputation policy to select at each time step whether or not to recompute the MPC solution. This means that of the MPC input sequence computed at time , not only the first input is applied but rather a variable number of inputs are applied sequentially to the plant at the corresponding time instance , until the recomputation policy triggers the recomputation of the MPC solution at time . We detail this recomputation policy next.

2.2 Event-triggered MPC

The recomputation policy is a stochastic policy parameterized by , defining a probability distribution over a binary output action, , where corresponds to recomputing the MPC solution at step and corresponds to not recomputing it. The recomputation policy receives a state that is not simply the real system state because depends on the state of the system when the MPC was last recomputed. For classical RL theory to apply for the state must be a Markov state. We will therefore define next an augmented state space that does have this property.

Assume that the MPC solution delivers an input sequence associated to a measured state , at time instant and that the sequence is applied to the system. The inputs received by the plant in the time interval are then a function of state at time . Since is not known a priori, one ought to generally view the control system stemming from the triggering policy and the MPC scheme as being a control law from an augmented state space, , containing 1. the current state of the system, 2. the state of the system when the last optimization took place, and 3. the number of time samples from which the last optimization took place. Labelling the current time of the system as and the last time when the optimization occurred as , that augmented state reads as:

| (5) |

where , and where has the real system dynamics, and where the deterministic state transition occurs when is drawn from the stochastic policy . The MPC control law actually deployed on the system then reads as:

| (6) |

where is the element of the MPC solution solved for the initial state .

The recomputation policy, and the MPC and LQR control laws together form a control system defining the inputs actually applied to the plant in a closed loop system. The control system and the plant dynamics together define the state transition dynamics in the augmented state space , where states does have the Markov property. The event-triggered MPC problem is therefore an Markov decision process (MDP) in the augmented state space , such that classic RL can be applied on . In that context external parameters (forecasts) can be seen as being part of the states , .

2.3 Reinforcement Learning

The closed loop system MDP as described above is defined by the tuple , , R, , , . is the set of states , and is the set of actions. is the discrete-time transition function describing the probabilistic transitions between states as a function of time and actions, and is a distribution of initial states. is the cost function which assigns a scalar value to the states of the problem. Lastly, is the discount factor weighing the relative importance of immediate and future costs.

We consider the episodic setting, where an episode consists of a sequence of states and actions of length , denoted by . We further define the return as the total cost of the episode, where is a terminal state cost. RL encompasses a set of algorithms to generate policies with the goal of finding the optimal policy that optimizes the RL objective which in this setting can be formulated as (7a).

| (7a) | |||

| (7b) | |||

The expectation in (7a) is taken over the initial state distribution, the probabilistic transition function, and the possibly stochastic policy .

2.3.1 Policy Gradients

Policy gradient algorithms is a family of RL methods that directly optimize the parameters of parameterized policies by estimating the gradient of the policy performance index with respect to , and using a gradient descent scheme to minimize the objective (7a). The policy gradient is given by (Sutton and Barto, 2018):

| (8a) | ||||

| (8b) | ||||

Where is the advantage function describing the relative value of states with respect to the costs obtained over the future trajectory generated by from the state in question. is often replaced by other functions of the costs depending on the algorithm, e.g. by for “vanilla” policy gradient. Policy gradient algorithms can therefore intuitively be interpreted as adjusting the log likelihood of actions such that actions that lead to lower costs are more likely to be chosen. This gradient relies on access to the costs for the states and actions in the trajectory, which is obtained by sampling trajectories from the plant. Policy gradient methods have good convergence guarantees in theory, but since it is a sampling based approach it suffers from high variance in the gradient estimates in practice (Peters and Schaal, 2008).

2.3.2 Policy Representation

As the action space of the policy in our method is binary we represent the policy as a logistic regression model. In the logistic model, the logarithm of the odds of a binary dependent variable taking on a given value is modeled as a linear combination of the input variables (9):

| (9) |

3 Proposed Control System Architecture

The proposed architecture is described in Algorithm 3.1. The MPC solution is computed at the first time step, generating an optimal predicted state trajectory and a sequence of optimal inputs that produces this trajectory . The first input is then applied to the system as usual, but instead of discarding the rest of the MPC solution, we allow a learned policy to decide based on an observation of the current recomputation state, , whether the last MPC solution is still of acceptable quality, or if it should be recomputed. If the recomputation policy decides not to recompute, a tracking LQR is applied to the state prediction error to correct the state trajectory to match the plan generated by the MPC. Algorithm 3.1 describes the operation of the control system with a fixed recomputation policy, e.g. after the RL policy is done learning, as how and when the learning is performed would depend on the chosen learning algorithm.

In this paper we use the GPOMDP algorithm (Baxter and Bartlett, 2001) to train the RL recomputation policy, and implement the MPC with the CasADi framework (Andersson et al., 2019), the Ipopt optimizer (Wächter and Biegler, 2006) and the do-mpc python library (Lucia et al., 2017).

Remark 3.1.

In our experiments computing the LQR input and evaluating the RL policy takes on the order of less time than computing the MPC solution, lending credence to this architecture saving significant computational resources.

[htbp] \SetAlgoLinedControl System Architecture

Initialize state and parameters: \For Compute MPC solution: Execute MPC control input: \Fori = k, …, k + N - 1 Wait for next sampling instant and measure system state: Compute prediction errors: \eIfRecomputation policy draws Break loop Compute additive LQR input: Apply input constraints: Execute control input: Update MPC model, state and parameters:

4 Case Studies

4.1 Systems

4.1.1 Cart Pendulum

We first look at a nonlinear system where the quality of the MPC control input is considerably better than that of the LQR. For this purpose we use the well studied classical control task of balancing an inverted pendulum mounted on a small cart. This system represents the problem of embedded control of battery powered systems where the MPC is needed for sufficient control performance but its computation accounts for a substantial part of the total battery resources available.

The state space consists of which is position and velocity of cart along horizontal axis, and angle of pendulum to the vertical axis and angular velocity of the pendulum, respectively. We discretize the system equations in (10a-10c) with step time , and add unmeasured process disturbance , which means that feedback control from the LQR is a necessary addition to the MPC plan to stabilize the pendulum. We sample initial states according to , where is the uniform distribution, and put constraints on the input , which is a force applied to the cart along the horizontal axis. Finally, the physical parameters are the pendulum length and weight, , the total weight of the cart and the pendulum, , and the gravitational acceleration, .

The MPC is configured with . This objective function promotes stabilization of the pendulum, while the RL policy cost function has an additional objective to minimize computation. The LQR is based on a fixed linearized model (10c) obtained by using the small angle approximation, while its cost matrices are .

| (10a) | ||||

| (10b) | ||||

| (10c) | ||||

4.1.2 Battery Storage

The battery storage system models the trading of electricity from a battery storage that is subject to quickly changing electricity prices as well as uncertain production and consumption from the electricity grid it is connected to (11a). Here, is the state of charge, i.e. the fraction of available battery capacity, kWh is the total battery capacity, is the trading of power from the battery on the market where represents selling and is buying. is the sum of production and consumption on the power grid, and is the time-varying price of electricity.

This is an economic problem where the objective is to maximize the profit of the battery storage through the sum of trading and the potential of the storage , where is the average price of electricity. The MPC has an optimization horizon of 20 time steps, . In this problem we look at fast trading, i.e. , which is dominated by the balance market. Spot prices are evaluated every hour and fixed for the duration, while the prices are highly stochastic and vary around the spot prices on the balance market due to e.g. unforeseen errors on the grid. The control system receives forecast for the future production and consumption as well as the expected price of electricity. It then needs to plan whether to save up electricity for better times ahead or sell surplus charge for a good price. We assume that when the MPC solution is computed it runs for the whole sampling interval on a computer consuming W from the battery, modeled through the term in (11a). Lastly, only 10% of the battery capacity can be traded in a single window (11b), with no cost for changing amount between windows, . The LQR accounts for errors in the forecasted production and consumption, as well as the consumption from the MPC computation itself which is not part of the MPC model (11c), .

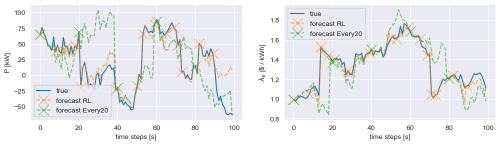

fig:forecasts

The uncertainty in this problem lies in the forecasts of the time-varying parameters, and . These grow more unreliable the further ahead in time we forecast, and as such the plan generated by the MPC becomes less and less optimal. The true values of the time-varying parameters are generated by sampling a base value with varying duration, representing the changing power demands due to events as described above, with an additive Ornstein–Uhlenbeck (OU) process. Further, forecasts are generated by assuming the base value is constant over the forecast length and adding a second OU noise process whose strength is linearly scaled with forecast length, see figure LABEL:fig:forecasts.

Remark 4.1.

and are not based on real historical data, and are generated with the aim of emulating the market as described above and to produce a non-trivial test problem.

| (11a) | ||||

| (11b) | ||||

| (11c) | ||||

4.2 Baseline Policies

To assess the quality of the RL policy we compare the learned policy to the fixed baseline policies: standard MPC (, never recomputing until end of horizon (), and recomputing on a fixed static schedule every time steps (.

Remark 4.2.

We experimented with early termination MPC based on maximum allowed iterations as well as optimality tolerance, but its performance was considerably worse than the other approaches and as such it is not included. Early termination would likely perform better with a sequential quadratic programming (SQP) based optimizer that exploits warm start more efficiently than Ipopt.

4.3 Training and Evaluation

We train and evaluate the policies in an episodic setting, where an episode consists of 100 time steps with randomly generated initial conditions, process-noise, time-varying parameters etc. as discussed above for each system. The RL state is augmented with a squared version of each component, and the whole state vector is normalized before being fed to the policy. To evaluate the policies and minimize the effects of the random variables on the results, we construct a test set for each system consisting of 100 episodes where all random variables are drawn in advance such that the episode is consistent across policy evaluations. To account for the inherent stochasticity of the RL policy, we evaluate the policy five times over the test set and report mean results. We use the undiscounted return as the objective value to compare policies on the episode and average these returns over the test set.

As the objective of the policy is to learn when it is viable to not recompute the MPC solution, we initialize the RL policy to (with high probability) mimic the standard MPC approach and always elect to recompute. For both systems we train with and a learning rate of .

5 Results and Discussion

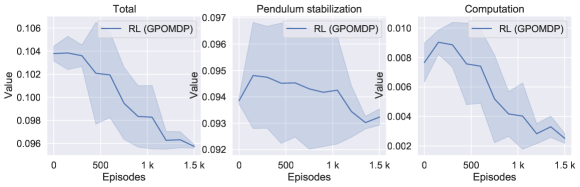

fig:training\subfigure[Cart pendulum system] \subfigure[Battery storage system]

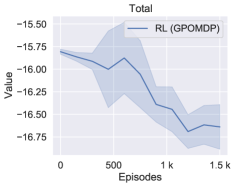

\subfigure[Battery storage system]

Figure LABEL:fig:training shows the evolution of the learning process of the RL recomputation policy evaluated every 150 episodes on the test set. It starts out emulating the MPC strategy achieving similar objective value scores, and from there identifies instances where similar control performance can be achieved without recomputing the MPC solution. It converges after around 1500 episodes corresponding to about 4 hours of real world training time for the cart pendulum system and 400 hours for the battery storage systems. While this is considerable training time, in our experiments the policy generally monotonically improves on the objective and the system could be designed such that even the maximum recomputation interval guarantees safe operation.

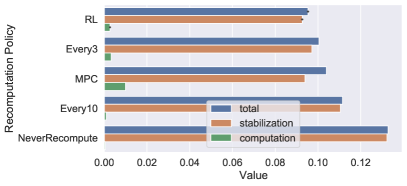

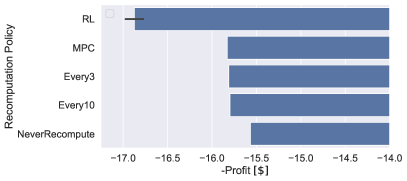

fig:eval\subfigure[Cart pendulum system] \subfigure[Battery storage system]

\subfigure[Battery storage system]

The trained RL policy is compared to the baseline controllers in Figure LABEL:fig:eval. It is the best performing policy for both systems, outperforming the second best policy by around 5% and 7% for the cart pendulum and battery storage systems, respectively. While this might seem like a minuscule improvement we would argue that the optimization landscape in the recomputation optimization problem is very noisy — involving complex interactions between the MPC and LQR control laws as well as the plant dynamics — and the ability to consistently estimate a gradient even with such little room for improvement speaks to the potential of the proposed architecture. For the cart pendulum problem the RL policy is able to have virtually the same control performance as the standard MPC approach with less than one fourth of the computational cost. A noteworthy result is that for the battery system the computational cost is negligible, meaning the performance improvements of the RL policy mainly stem from it recognizing situations where carrying out larger parts of a single MPC solution is more optimal than individual parts of separate solutions. These situations arises due to the battery storage system having considerable stochasticity which is not modeled by the MPC, meaning its solutions are generally suboptimal.

One major effect we do not account for in this work is the time it takes to obtain the MPC solution, which is often significant compared to the sampling time. The recomputation policy could therefore instead by trained as a self-triggering policy predicting the number of time steps the current solution is viable for. The MPC could then be scheduled so that a new solution is ready when needed, while also giving the MPC more optimization time resulting in a higher quality solution.

6 Conclusion

In this paper we have presented a novel control system architecture which promises to deliver the performance of MPC with reduced computational frequency and energy usage, opening up new applications particularly for battery driven systems and other applications where energy is a limiting factor. It is important to note that we did not spend significant time tuning the parameters of the MPC and LQR controllers, being satisfied with establishing the MPC as the superior controller, and employed a basic classical RL algorithm with a simple function approximator containing only a handful of learned parameters. All this is to say that the architecture seems to be fairly robust towards tuning and suboptimality of the individual components, and larger improvements could likely be obtained with more effort put into hyperparameter optimization. Moreover it is not clear how one would even tune the LQR when its objective is to extend the viability of the MPC solution, aside from trial-and-error. One could therefore extend the role of RL in this architecture to also optimize and tune the other controllers, or even have it act as the simpler controller itself. This is left for future work. \acksThis work was financed by grants from the Research Council of Norway (PhD Scholarships at SINTEF grant no. 272402, and NTNU AMOS grant no. 223254).

References

- Andersson et al. (2019) Joel A E Andersson, Joris Gillis, Greg Horn, James B Rawlings, and Moritz Diehl. CasADi – A software framework for nonlinear optimization and optimal control. Mathematical Programming Computation, 11(1):1–36, 2019. 10.1007/s12532-018-0139-4.

- Baumann et al. (2018) Dominik Baumann, Jia-Jie Zhu, Georg Martius, and Sebastian Trimpe. Deep reinforcement learning for event-triggered control. In Proceedings of the 57th IEEE International Conference on Decision and Control (CDC), pages 943–950, December 2018.

- Baxter and Bartlett (2001) J. Baxter and P. L. Bartlett. Infinite-horizon policy-gradient estimation. Journal of Artificial Intelligence Research, 15:319–350, Nov 2001. ISSN 1076-9757. 10.1613/jair.806.

- Bemporad et al. (2002) Alberto Bemporad, Manfred Morari, Vivek Dua, and Efstratios N. Pistikopoulos. The explicit linear quadratic regulator for constrained systems. Automatica, 38(1):3 – 20, 2002. ISSN 0005-1098. https://doi.org/10.1016/S0005-1098(01)00174-1.

- Berglind et al. (2012) J.D.J. Barradas Berglind, T.M.P. Gommans, and W.P.M.H. Heemels. Self-triggered mpc for constrained linear systems and quadratic costs. IFAC Proceedings Volumes, 45(17):342 – 348, 2012. ISSN 1474-6670. https://doi.org/10.3182/20120823-5-NL-3013.00058. 4th IFAC Conference on Nonlinear Model Predictive Control.

- Berner et al. (2019) Christopher Berner, Greg Brockman, Brooke Chan, Vicki Cheung, Przemysław Debiak, Christy Dennison, David Farhi, Quirin Fischer, Shariq Hashme, Chris Hesse, et al. Dota 2 with large scale deep reinforcement learning. arXiv preprint arXiv:1912.06680, 2019.

- Cagienard et al. (2004) R. Cagienard, P. Grieder, E. C. Kerrigan, and M. Morari. Move blocking strategies in receding horizon control. In 2004 43rd IEEE Conference on Decision and Control (CDC) (IEEE Cat. No.04CH37601), volume 2, pages 2023–2028 Vol.2, 2004. 10.1109/CDC.2004.1430345.

- Chakrabarty et al. (2018) A. Chakrabarty, S. Zavitsanou, F. J. Doyle, and E. Dassau. Event-triggered model predictive control for embedded artificial pancreas systems. IEEE Transactions on Biomedical Engineering, 65(3):575–586, 2018. 10.1109/TBME.2017.2707344.

- Feng et al. (2012) Le Feng, Christian Gutvik, Tor Johansen, Dan Sui, and Alf Brubakk. Approximate explicit nonlinear receding horizon control for decompression of divers. Control Systems Technology, IEEE Transactions on, 20:1275–1284, 09 2012. 10.1109/TCST.2011.2162516.

- Goebel and Allgöwer (2015) Gregor Goebel and Frank Allgöwer. A simple semi-explicit mpc algorithm. IFAC-PapersOnLine, 48(23):489 – 494, 2015. ISSN 2405-8963. https://doi.org/10.1016/j.ifacol.2015.11.326. 5th IFAC Conference on Nonlinear Model Predictive Control NMPC 2015.

- Gondhalekar et al. (2015) Ravi Gondhalekar, Eyal Dassau, and Francis J. Doyle III. Tackling problem nonlinearities & delays via asymmetric, state-dependent objective costs in mpc of an artificial pancreas. IFAC-PapersOnLine, 48(23):154 – 159, 2015. ISSN 2405-8963. https://doi.org/10.1016/j.ifacol.2015.11.276. 5th IFAC Conference on Nonlinear Model Predictive Control NMPC 2015.

- Gros et al. (2020) Sebastien Gros, Mario Zanon, and Alberto Bemporad. Safe reinforcement learning via projection on a safe set: how to achieve optimality? In IFAC 2020, 02 2020.

- Heemels et al. (2008) W. P. M. H. Heemels, J. H. Sandee, and P. P. J. Van Den Bosch. Analysis of event-driven controllers for linear systems. International Journal of Control, 81(4):571–590, 2008. 10.1080/00207170701506919.

- Iino et al. (2009) Y. Iino, T. Hatanaka, and M. Fujita. Event-predictive control for energy saving of wireless networked control system. In 2009 American Control Conference, pages 2236–2242, 2009. 10.1109/ACC.2009.5160732.

- Li and Shi (2014) Huiping Li and Yang Shi. Event-triggered robust model predictive control of continuous-time nonlinear systems. Automatica, 50(5):1507 – 1513, 2014. ISSN 0005-1098. https://doi.org/10.1016/j.automatica.2014.03.015.

- Lucia et al. (2017) Sergio Lucia, Alexandru Tătulea-Codrean, Christian Schoppmeyer, and Sebastian Engell. Rapid development of modular and sustainable nonlinear model predictive control solutions. Control Engineering Practice, 60:51–62, 2017.

- Mnih et al. (2015) Volodymyr Mnih, Koray Kavukcuoglu, David Silver, Andrei A Rusu, Joel Veness, Marc G Bellemare, Alex Graves, Martin Riedmiller, Andreas K Fidjeland, Georg Ostrovski, et al. Human-level control through deep reinforcement learning. nature, 518(7540):529–533, 2015.

- Peters and Schaal (2008) Jan Peters and Stefan Schaal. Reinforcement learning of motor skills with policy gradients. Neural Networks, 21(4):682 – 697, 2008. ISSN 0893-6080. https://doi.org/10.1016/j.neunet.2008.02.003. Robotics and Neuroscience.

- Schrittwieser et al. (2019) Julian Schrittwieser, Ioannis Antonoglou, T. Hubert, K. Simonyan, L. Sifre, S. Schmitt, A. Guez, Edward Lockhart, Demis Hassabis, T. Graepel, T. Lillicrap, and D. Silver. Mastering atari, go, chess and shogi by planning with a learned model. ArXiv, abs/1911.08265, 2019.

- Scokaert et al. (1999) P. O. M. Scokaert, D. Q. Mayne, and J. B. Rawlings. Suboptimal model predictive control (feasibility implies stability). IEEE Transactions on Automatic Control, 44(3):648–654, 1999. 10.1109/9.751369.

- Sedghi et al. (2020) Leila Sedghi, Zohaib Ijaz, Md. Noor-A-Rahim, Kritchai Witheephanich, and Dirk Pesch. Machine learning in event-triggered control: Recent advances and open issues, 2020.

- Sutton and Barto (2018) Richard S. Sutton and Andrew G. Barto. Reinforcement Learning: An Introduction. A Bradford Book, Cambridge, MA, USA, 2018. ISBN 0262039249. 10.5555/3312046.

- Wächter and Biegler (2006) Andreas Wächter and Lorenz Biegler. On the implementation of an interior-point filter line-search algorithm for large-scale nonlinear programming. Mathematical programming, 106:25–57, 03 2006. 10.1007/s10107-004-0559-y.

- Yang et al. (2019) X. Yang, H. He, and D. Liu. Event-triggered optimal neuro-controller design with reinforcement learning for unknown nonlinear systems. IEEE Transactions on Systems, Man, and Cybernetics: Systems, 49(9):1866–1878, 2019. 10.1109/TSMC.2017.2774602.

- Yoo and Johansson (2019) J. Yoo and K. H. Johansson. Event-triggered model predictive control with a statistical learning. IEEE Transactions on Systems, Man, and Cybernetics: Systems, pages 1–11, 2019. 10.1109/TSMC.2019.2916626.

- Zanon and Gros (2020) Mario Zanon and Sebastien Gros. Safe reinforcement learning using robust mpc. IEEE Transactions on Automatic Control, PP:1–1, 09 2020. 10.1109/TAC.2020.3024161.

- Åström and Bernhardsson (2002) K. J. Åström and B. M. Bernhardsson. Comparison of riemann and lebesgue sampling for first order stochastic systems. In Proceedings of the 41st IEEE Conference on Decision and Control, 2002., volume 2, pages 2011–2016 vol.2, 2002. 10.1109/CDC.2002.1184824.