State Space Vasicek Model of a Longevity Bond

Abstract

Life expectancy have been increasing over the past years due to better health care, feeding and conducive environment. To manage future uncertainty related to life expectancy, various insurance institutions have resolved to come up with financial instruments that are indexed-linked to the longevity of the population. These new instrument is known as longevity bonds . In this article, we present a novel classical Vasicek one factor affine model in modelling zero coupon longevity bond price (ZCLBP) with financial and mortality risk. The interest rate and the stochastic mortality of the constructed model are dependent but with uncorrelated driving noises. The model is presented in a linear state-space representation of the contiuous-time infinite horizon and used Kalman filter for its estimation. The appropriate state equation and measurement equation derived from our model is used as a method of pricing a longevity bond in a financial market. The empirical analysis results show that the unobserved instantaneous interest rate shows a mean reverting behaviour in the U.S. term structure. The zero-coupon bonds yields are used as inputs for the estimation process. The results of the analysis are gotten from the monthly observations of U.S. Treasury zero coupon bonds from December, 1992 to January, 1993. The empirical evidence indicates that to model properly the historical mortality trends at different ages, both the survival rate and the yield data are needed to achieve a satisfactory empirical fit over the zero coupon longevity bond term structure. The dynamics of the resulting model allowed us to perform simulation on the survival rates, which enables us to model longevity risk.

keywords:

Zero coupon Longevity bond, Kalman filter, Survival rate, Term structure, Stochastic mortality, Interest rate.1 Introduction

Human life expectancy has been increasing significantly for the last few decades, especially in the developed countries (example United Kingdom) where changes in lifestyle, medical advancement, genetic new discoveries , etc have been playing a good role. These life expectancy have proved to have an important effect at higher ages and have caused life offices (for example Pension funds, annuity providers, the government and Defined Benefits (DB) pension schemes) to incur losses on their annuity life business. The insurance industry is therefore taking the responsibility of the cost of the unanticipated higher longevity by issuing longevity bonds.

Longevity bonds can be defined as annuity bonds whose coupons are not fixed over time but fall in line with a given survivor index. Longevity bonds were first proposed by [4], with its first operational mortality-linked in 2003. In November 2004, BNP Paribas (in its role as structurer and manager) announced that the European Investment Bank (EIB) would issue a longevity bond with a maturity of twenty-five years. According to UK Office for National Statistics (ONS), the coupon payments were to be linked to a survivor index that is based on the realized mortality experience of a population of males from England and Wales aged 65 in 2003. Although the UK life offices and pension funds were the main intended investors, but then, this issue was unsuccessful at last. Different authors, for example [37] have modeled the mortality intensity as a stochastic process which allowed them to capture two important features of the mortality intensity: time dependency and uncertaintity of the future development. [38] proposed a new model for stochastic mortality. The model was based on affine term structure model that satisfies three important requirements for application in practice: analytical tractibility, clear interpretation of the factors and compatibility with financial option pricing models. They tested the model fit using data on Dutch mortality rates and it shows that despite its shortcomings, in general it fits the data well and it is easily applicable to the pricing of well known embedded option. [39] focus on mortality at pensionable ages and showed how the risk of longevity can be taken into account. However, longevity improvement is in an unpredicted way since longevity bond serves as an instrument to hedge against longer longevity risks faced by life offices and pension plans.

In recent years, different authors have studied longevity bond pricing. [41] discussed another approach of longevity pricing model using the parametric boot strap. [47] used three popular methods - first neutral method, sharp ratio rule and the wang transform and [45] proposed a Bayesian approach. [42] proposed a simple Partial internal model for longevity risk inside the framework of Solvency II. Their model tend to have connection with the Danish longevity benchmark mechanisms and it comprises of a component, which is based on the size of a given portfolio. This component can measure for each insurance portfolio the unsystematic longevity risk . In other to tackle the challange of measuring and modeling the longevity risk, many studies made use of the affine structure with mortality models application. For example [39] suggested for a cohort live an affine mortality structure with the same ages [38] introduced an affine mortality intensity model specially for Thiele and Makeham mortality laws and examines all ages in same time. Furthermore, [43] gave a variable method to modelling longevity risk while [44] proposed a mortality model with an age shift by using a principal component analysis PCA. [46] used the Principal Component Approach to model longevity risk and compared his approach with the existing stochastic mortality models. They went further using their model to examine the ratio of annuity price both for the deferred life annuity and life annuity products and then try to forecast the future mortality rates. They were able to prove that their model can resolve the Lee Carter Model’s problem by using the PCA approach.[48] used the famous [30] approach to develop a stochastic modeling of financing longevity risk in pension insurance and then used the Bayesian MCMC methods and prove that the LC model is not completely adaptable with mortality data.

There are two sources of mortality risk that affect a portfolio of pensions or annuities: the unsystematic (idiosyncratic) and systematic (longevity) risk. In the case of the systematic mortality-related, there are different possible numbers of risks faced by annuity providers and life insurers. In this paper, the term mortality risk will be taken to include uncertainty of all forms in future mortality rates, increases and decreases in the rate mortality inclusive. Most of the times, longevity risk is normally taken to mean the risk that survival rates are higher than anticipated. But in this paper, is taken to mean uncertainty in either direction. In academic literature, several supporting instruments such as survivor bonds or longevity (cf.[4]) or survivor swaps (cf. [40]) have been proposed (see [29] for an overview).

Different approaches for the modelling of aggregate randomness in mortality rates over time have been proposed . A key earlier work is that of [30]. In their work, they focused on the practical application of stochastic mortality and its statistical analysis. Because aggregate mortality rates are better of measured annually, [30] and other authors (for example[31]; [32]; [33]) have adopted a similar approach and worked in discrete time model. Models following the approach of [30] typically adapt discrete-time series models. This is to capture the random element in the stochastic development of mortality rates. Similarly, different authors (see, for example, [34]; [39]; [35]; [36]; [37];[38]) have developed models in a continuous-time framework. This is because discrete model parameters can be calibrated to historical mortality experience while continuous-time model has more benefit in areas such as valuation and hedging of life insurance liabilities especially when we combine the mortality model with some financial analysis. Hence, continuous-time models have a key role to play when it comes to understanding how the prices of mortality-linked securities develops over time.

In this article, we addressed how to construct a market- consistent-valuation framework for long-term risky investment in the insurance and financial market. And also how interest rate models can be constructed to obtain analytically tractable and accurate pricing formulae for long-term assets. To achieve this we formulate a linear state-space representation of the continuous- time infinite horizon short rate models and use Kalman filter to jointly estimate the current term structure and its dynamics for markets with illiquid long-term bond. Analytical tractability is the most important of what we intend to achieve.This is because we want to take into consideration the parameter uncertainty and show how our result can be used to price new zero coupon longevity bond. Consequently, we choose to develop a model in continuous-time and adopt an approach that is similar to that of [10]. We propose a zero coupon longevity bond price model that is used to fit U.S. Treasury bond maturity data and show how the calibrated model can be used to price financial and mortality risk in longevity bond. To estimate our model , we use a state space formulation which contains the measurement and the transition equations. The model involves two stochastic factors - the interest rate and mortality risk. While former takes into account the yield data, the later takes into account the real survival rate. We present empirical evidence that indicates that to model sufficiently historical mortality longevity at different ages, these factors (the interest rate and mortality risk) are necessary in other to achieve a reasonable empirical fit over the zero coupon longevity bond term structure. Unlike the Econometrics models as that of the famous [30], our transition equations which are the time-series dynamics are presented in the model like a stochastic factor which allow us to simulate survival rates, thereby enabling us to model longevity risk. The measurement equation represents the yields observed data which is exponentially affine in the factors.

For pricing the zero coupon longevity bond, we adopt the risk-adjusted (or “risk-neutral”) approach of pricing adopted by, for example,[49]. We suggest a simple method for making the adjustment between risk-adjusted and real probabilities, which involves a constant market price both for the longevity and parameter risk. This is because of the current lack of market data.

The remaining of this paper is organized as follows. In section 2, we discuss the relationship between financial and motality longevity; present the formular for the mortality rate and interest rate equation; discuss the meaning of longevity bond as a financial product; present asymptotic yield for the infinite horizon and give the zero coupon longevity bond price for the constant parameter case.The state space formulation of the model and parameters estimation is discuss in section 3. In section 4, the emperical and data analysis were presented. In section 5, some conclusions are offered.

2 Financial and Mortality Longevity Rate Model

Longevity bonds are the first financial products to offer longevity protection by hedging the trend in longevity. Longevity bonds are needed because life expectancy has been constantly increasing as a result of medical improvements, better life standards, etc. As pointed out by [19] that life expectancy for men aged 60 is more than 5 years’ longer in 2005 than anticipated to be in mortality projections made in the 1980 and as such, this has brought about uncertainty of longevity projections.

In other to meet up with this demand, the Capital markets offer longevity bonds with coupons depending on the survival rate of a given population which can be used to hedge a big portion of the longevity risk. Longevity bonds can take a large variety of forms which can vary enormously in their sensitivities to longevity shocks. Hence, longevity bonds is ideal asset for hedging the longevity risk of a pension fund.

2.1 Zero Coupn Longevity Bond: The term structure equation

Given a probabilty space , which satisfies the usual hypothesis that the filtration is right continuous with left limits where is the joint process of interest rate, then the mortality rate is given by

| (2.1) |

for and in

Let and , equation 2.1 becomes

| (2.2) |

| (2.9) |

Let the dynamics of be given as

| (2.10) |

where is the drift, is the diffusion, and is two dimensional vector. From equation 2.10

| (2.11) |

where is two dimensional vector and are independent and is scaler. The dynamics of the process is given by the following stochastic differential equation.

| (2.12) |

is the mean reversion rate while is the diffusion term. We also assume that a market exist for bonds of every available maturity and that the market is abitrage free.

2.2 Affine Form of Longevity Bond Price

There are several ways of solving a longevity problem and one of it is classical Affine term structure model. Generally, affine term structure models are useful in modelling mortality intensity in the literature. [8] described the mortality intensity by affine models and calibrated the intensity processes by using observed and projected UK mortality tables. They claimed that affine processes with deterministic part increases exponentially which could describe the evolution of mortality intensity properly. [12] calibrated three affine stochastic mortality models using term assurance premiums of three Italian insurance companies and proposed that those affine models can be used for pricing mortality-linked securities.

The theory of Affine model rank among the most popular model both in theory and practice, and as such many examples have been investigated. The first term structure model-Vasicek model is an affine model. Others are Cox, Ingersol, Ross (CIR), Hull and White or Longstaff and Schwartz which are also Affine model.

In the bid of the expansion of the Affine model,[9] investigated the model and developed a general theory while [6] provided the classification and thereafter established most of the general representative of each class of Affine model.

The tractability and flexibilty of Affine model makes its popularity to be known and aslo there are often explicit solution for the bond price and bond option price. In this work, we will be considering another form of classical Vasicek one-factor model of a longevity bond price whose zero coupon longevity bond (ZCLB) is given as:

Theorem 2.1.

(Babbs, S. H., and M. J. P. Selby 1993) The price of a zero coupon longevity bond with maturity at time is given as

| (2.13) |

where norm,

| (2.14) | ||||

| (2.15) | ||||

| (2.16) | ||||

| (2.17) |

The price at time of a zero coupon longevity bond under the vasicek factor model with maturity can be written as:

| (2.18) |

where is a martingale measure.

Corollary 2.2.

The continuously compounded zero coupon longevity yield is given by

| (2.19) |

where

Proof.

This is a direct consequence of theorem 2.1 ∎

2.3 Asymptotic yield for Infinite horizon

Given the maturity of a zero coupon longevity bond is infinite and all the parameters remain constant, then the folowing proposition holds true.

Proposition 2.3.

Let represent the yield on a zero coupon longevity bond with infinite maturity. Since for then implies . Consequently

| (2.20) |

On constant parameters equation2.19 becomes

| (2.21) |

with

| (2.22a) | ||||

| (2.22b) | ||||

Proof.

where

is a function of , and is a dummy variable.

2.3.1 On Constant Parameter Zero Coupon Longevity Bond Price

Under constant parameters assumption of the vasicek longevity model 2.13, the price of a zero coupon longevity bond of any maturity of equation 2.13 is given as in Lemma 2.4

Lemma 2.4.

In the case where all the parameters (the long run average rate , the market price of risk process the mean reversion and diffusion coefficents) are all constant, the longevity bond price can be defined as

| (2.37) |

with

| (2.38a) | ||||

| (2.38b) | ||||

3 Application of Kalman Filter Technique for Longevity Bond Price

The application of the Kalman filter to longevity bond price model is considered in this section. More especially, the application to one-factor longevity bond price model is considered as presented in the previous section. The Kalman filter equations are employed so that the unobservable variables and parameters of the longevity bond price model can be estimated. To achieve this, the term structure of the models are represented in a linear state space form. This is to allow for measurement errors.

3.1 State Space Formulation

A state space model consists of a measurement equation relating the observed data and a Markovian transition equation that discribes the evolution of state vector over time. Here, state space model of the longevity bond price model of one-factor Vasicek model is developed. After the state space form of the model has been written, the selection of is chosen by construction because it is generally not unique. That is, one the major aims of state space formulation is to set up such that it will contain the necessary information on the system at time . The basic criterion for a good state space representation is a minimal realisation.This is situation where the length of the state vector of the state space is minimised.

3.1.1 State Equation

The state equation is represented by the exact discrete-time distribution of the state variable gotten from equation 2.10.By solving the linear differential equation of the state variable, the exact discrete-time distribution is obtained.

Thus

| (3.1) |

3.1.2 Measurement Equation

The measurement equation describes the relation between the yields observed and mortality rates as measured with errors and the possible unobserved states.The measured errors are additive and normally distributed. Recall from equation 2.21 for yield of a zero coupon longevity bond with infinite maturity

| (3.2) | ||||

| (3.7) | ||||

| (3.8) |

where the transpose is denoted by the superscript,

and

is a scalar and are functions of the term to maturity , then is a

and

where are parameters of the model.

The measurement equation is then given as:

| (3.9) |

where is made up the unknown parameters of the model which includes the distribution of the measurement error. is an matrix whose row is given by and is an matrix whose row is given as .

The elements and that of are then given by

and

where

Thus

and

3.2 Kalman Filter for Longevity Bond Price

The major purpose of the Kalman filter equations is to help in obtaining information about from the observed interest rates in the measurement equation. It also helps to estimate the unknown parameters of the models in such a way that it includes all the relevant information on the equation at time . The basic criterion for a good state space representation is a minimal realisation. That is, a situation where the length of the state vector of the state space is minimised. The filter consists of two sets of equation

-

1.

Prediction equations and

-

2.

Updating equations

3.2.1 Prediction Equations

In the prediction equation, the information comes from the observed variables. it involves estimation of the unobserved state variables at a particular time based on the available information up to the time before that particular time. However, in this case, the unobserved variables are the observed interest rates which implies that the information comes from the observed interest rates.

As the available information is given till time , the conditional expectation of the unknown vector space be denoted by . Also given the observed interest rates up to ,let the optimal estimator of be denoted by . Hence based on the observed interest rates up to time , the optimal estimator of is the conditional expectation of given the available information up to time . Thus we have

| (3.10) | ||||

where and . From the observed longevity bond up to time , the prediction error is connected with estimating . Let represent the covariance marix of the estimator error.that is

| (3.11) | ||||

where is the covariance matrix of .

3.2.2 Updating Equations

The update procedure entails additional information on the longevity bond yield at time . This is to obtain more accurate and updated estimator of . The new and present estimate of is called the filtered estimate. The moment new observed interest rates becomes available, can then be updated to .

While denotes the optimal estimator of based on the available information from the observed interest rates up to time and be the covariance matrix of the estimation error. Then the updating equations are given by

| (3.12) | ||||

and

| (3.13) | ||||

where

| (3.14) | ||||

| (3.15) |

The log-likelihood function given by

where is the correction term called measurement residual as given in equation 3.14. The logarithm price is used to suit the Kalman filter’s linear structure.

Using the updating equations, the optimal estimator at the next time step based on all the available information up to the current time step can be obtained.

| (3.16) |

substituting equation3.10 and the value for into equation3.16 we have

| (3.17) | ||||

from equation 3.17, the Kalman gain matrix given by

| (3.18) |

Eliminating from and then substituting the value for in 3.13

Recall, and , we have

Hence

Note: The generalised inverse formular for the sum of invertible matrices as seen in [16] is given as

| (3.19) |

which gives

| (3.20) |

| (3.21) |

Thus the Kalman Filter equation for the longevity bond price is given as follows

-

1.

State Prediction

-

2.

Error Covariance Prediction

-

3.

Kalman Gain

-

4.

State Update

-

5.

Error Covariance Update

4 Numerical Implementation

In this section, we we put into application all the preceding theoretical discussion of our estimation technique to our model. The exact discrete-time distribution of the state variable obtained from equation 2.10

By solving the linear differential equation of the state variable, the exact discrete-time distribution is obtained,

The measurement equation is then given as:

where is made up the unknown parameters of the model which includes the distribution of the measurement error. is an matrix whose row is given by and is an matrix whose row is given as .

The elements and that of are then given by

and

where

Thus

and

The predicted equation is obtained by given the available information up to time . As the available information is given till time , the conditional expectation of the unknown vector space be denoted by . Also given the observed interest rates up to ,let the optimal estimator of be denoted by . Hence based on the observed interest rates up to time , the optimal estimator of is the conditional expectation of given the available information up to time . That is

where and . Considering the error involved in estimating during the prediction step will be the next thing. From the observed longevity bond up to time , the prediction error is connected with estimating . Thus the estimator error is given as

where is the covariance matrix of and is the covariance matrix of the estimated error.

The updating equation is given as

and

where

Thus the log-likelihood function given by

where is the correction term called measurement residual as given in equation 3.14. The logarithm price is used to suit the Kalman filter’s linear structure.

The next optimal estimator will be based on all the available information up to the current time step which is gotten using the updating equation

and

| Results | ||

|---|---|---|

| Parameters | True | Estimated |

| 0.1 | 0.97 | |

| 1 | 2.06 | |

| 3 | 3.1 | |

Measurement Noise Covariance

The kalman filter tends to identify very closely the mean-reversion, long-term mean and volatility parameters and also offers a good approximation of the true parameters from a relatively small sampling space using the generated observed prices.

4.1 Model Simulation Results

The results of the actual longevity bond market data is presensented in this section. The U.S. Treasury Bonds data as used in this work was downloaded from the website Yahoo finance. The raw data includes the Date, Open, High, Low, Close, Adjusted (Adj) Close and Volume. The data is a daily quotes ranging from of December 1992 to the of November 2017 with 10 years maturity.

| U.S Treasury Bond | |||||||

|---|---|---|---|---|---|---|---|

| Date | Open | High | Low | Close | Adj Close | Volume | |

| 0 | 1992-12-31 | 6.70 | 6.70 | 6.70 | 6.70 | 6.70 | 0.0 |

| 1 | 1993-01-04 | 6.60 | 6.60 | 6.60 | 6.60 | 6.60 | 0.0 |

| 2 | 1993-01-05 | 6.61 | 6.61 | 6.61 | 6.61 | 6.61 | 0.0 |

| 3 | 1993-01-06 | 6.63 | 6.63 | 6.63 | 6.63 | 6.63 | 0.0 |

| 4 | 1993-01-07 | 6.76 | 6.76 | 6.76 | 6.76 | 6.76 | 0.0 |

| 5 | 1993-01-08 | 6.75 | 6.75 | 6.75 | 6.75 | 6.75 | 0.0 |

| 6 | 1993-01-11 | 6.71 | 6.71 | 6.71 | 6.71 | 6.71 | 0.0 |

| 7 | 1993-01-12 | 6.72 | 6.72 | 6.72 | 6.72 | 6.72 | 0.0 |

| 8 | 1993-01-13 | 6.71 | 6.71 | 6.71 | 6.71 | 6.71 | 0.0 |

| 9 | 1993-01-14 | 6.65 | 6.65 | 6.65 | 6.65 | 6.65 | 0.0 |

| 10 | 1993-01-15 | 6.60 | 6.60 | 6.60 | 6.60 | 6.60 | 0.0 |

| 11 | 1993-01-18 | NaN | NaN | NaN | NaN | NaN | NaN |

| 12 | 1993-01-19 | 6.59 | 6.59 | 6.59 | 6.59 | 6.59 | 0.0 |

| 13 | 1993-01-20 | 6.61 | 6.61 | 6.61 | 6.61 | 6.61 | 0.0 |

| 14 | 1993-01-21 | 6.60 | 6.60 | 6.60 | 6.60 | 6.60 | 0.0 |

| 15 | 1993-01-22 | 6.57 | 6.57 | 6.57 | 6.57 | 6.57 | 0.0 |

| 16 | 1993-01-25 | 6.48 | 6.48 | 6.48 | 6.48 | 6.48 | 0.0 |

| 17 | 1993-01-26 | 6.50 | 6.50 | 6.50 | 6.50 | 6.50 | 0.0 |

| 18 | 1993-01-27 | 6.48 | 6.48 | 6.48 | 6.48 | 6.48 | 0.0 |

| 19 | 1993-01-28 | 6.44 | 6.44 | 6.44 | 6.44 | 6.44 | 0.0 |

Adj Close price is used in adjusting the closing price of a stock in order to correctly reflect the value of that stock after accounting for any corporate shares. The estimated parameter set are then given in the table 3 below.

| Estimated Parameter Set | ||

|---|---|---|

| Parameters | True | Estimated |

| 3 | 3.19 | |

| 0.5 | 0.4 | |

| 1 | 1.4 | |

Measurement Noise Covariance

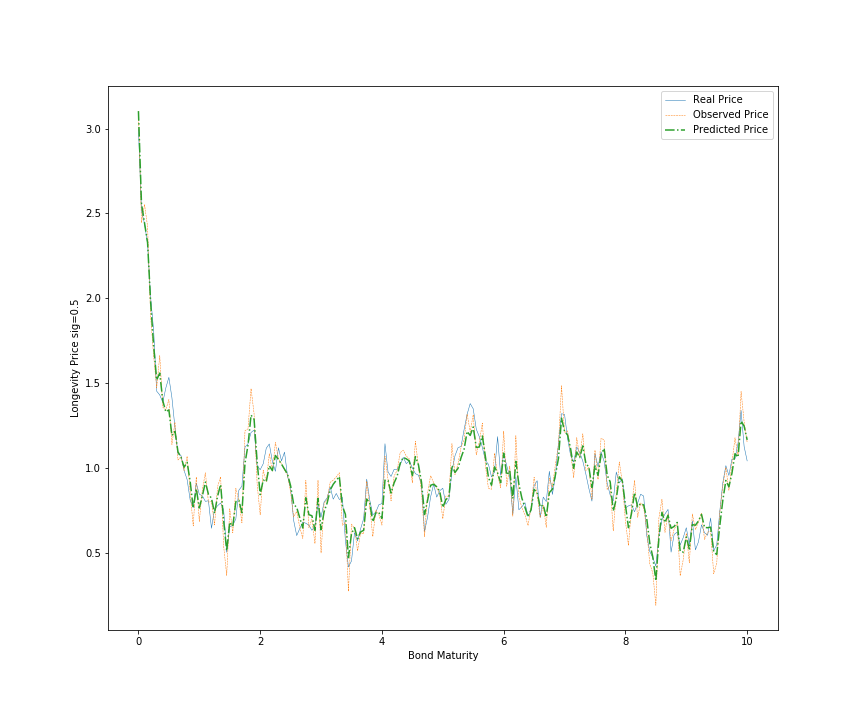

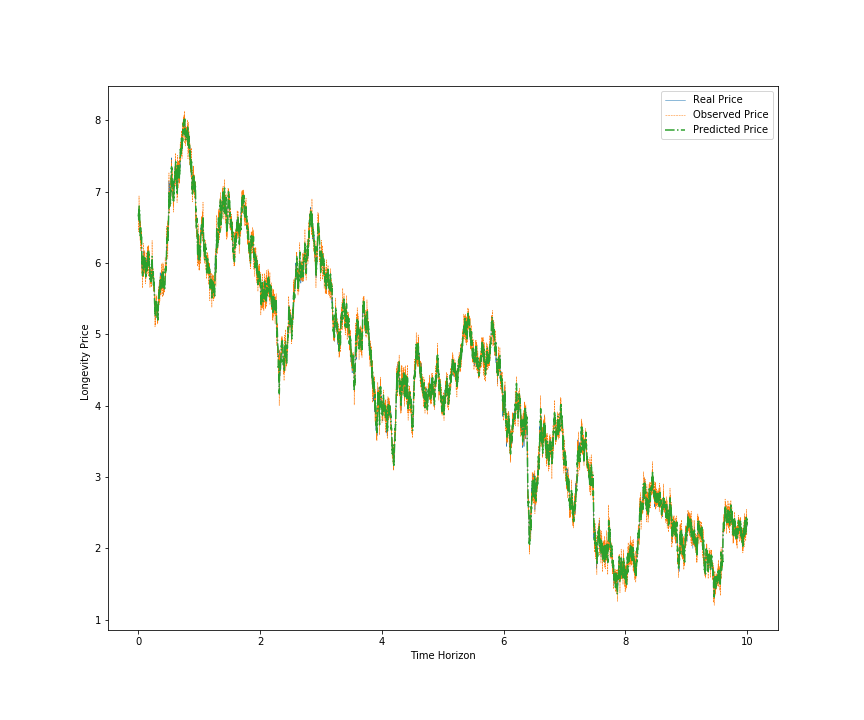

Figure 1 and Figure 2, shows that a mean reversion cycle matches the real price (solid line).An increase in the measurement noise which is usually distributed to the real price gives the observed value system (thin line). The predicted price is calculated using the Kalman filter (dot-dashed line) which is real close to the observed price. The Kalman filter with Gaussian distributions is quite robust and adaptable to univariating and multivariating economic system variables.

The application of a Kalman filter in this instance to match price information basically replicates a linear fitting routine.Also the application of Kalman filter to estimate the parameter set using maximum likehood to optimize our parameter set proves to be almost realistic. Although there are some errors in our estimate parameters, however, our predicted price looks more likely like the real prices which shows that Kalman filter is a good method to estimate unobservable parameter set. To observe the action of mean reversion, we simulated the stochastic behaviour of bond price with a mean reversion speed equal to to observe the weak mean reversion.

5 Conclusion

In this paper a one-factor Vasicek model was estimated for the U.S. Treasury term structure from December, 1992 to January, 1993. We modeled a linear state-space continuous time term structure model. Firstly, we specified a time series process for the instantaneous spot interest rate where the zero coupon longevity bond price formula is a function of the model’s parameters and the unobserved instantaneous spot rate. The parameters of the model are the long-run mean rate, the mean reversion towards the long-run mean, diffusion coefficients of the short-term interest rate and the market price of risk. The model is estimated using a maximum likelihood approach which is based on the Kalman filter. The Kalman filter recursive algorithm uses observable data on bonds to extract values for the unobserved state variables which combines the cross section and time series information in the term structure.

The observed yields on zero-coupon longevity bonds is modelled as a linear function of one-factor state variable. Result of the empirical analysis is based on monthly observations of U.S. Treasury zero coupon bonds from December, 1992 to January, 1993. Ten maturities have been chosen which spans across the yield curve from 1 year to 20 years. The yield curve is expected to include influences on the short, medium and infinite horizon of the term structure. The model parameters and their standard errors are estimated.

The empirical results of the analysis show that the unobserved instantaneous interest rate tends to exhibit a mean reverting behaviour in the U.S. term structure. The empirical evidence also indicates that to model adequately historical mortality trends at different ages, both the survival rate and the yield data are necessary for an optimal satisfactory for the empirical fit over the zero coupon longevity bond term structure. The result from the model dynamics allowed us to simulate the survival rates, which enabled us to model longevity risk. The affine form of longevity bond price models is able to be used not only for pricing and hedging longevity risk for pension funds and insurers but also for evaluating capital requirements for risk management.

Acknowlegment

My sincre gratitude to University of South Africa for giving me Bursary funding thereby making the financial burden lessened for this research. Also to AIMS South Africa for allowing me use their research facilities during the period of this research.

References

- [1] Simon H. Babbs and K. Ben Nowman, An application of generalized Vasicek term structure models to the UK gilt-edged market: a Kalman filtering analysis, Applied Financial Economics,8 (1998), 637-644.

- [2] Simon H. Babbs and K. Ben Nowman, Kalman filtering of generalized Vasicek term structure models, Journal of Financial and Quantitative Analysis, 34 (1999), 115-130.

- [3] Tomas Bjork, Arbitrage Theory in Continous time, Oxford University Press, 1998.

- [4] Blake, D., Burrows, W., 2001. Survivor Bonds: Helping to Hedge Mortality Risk.The Journal of Risk and Insurance,, 68: 339–348.

- [5] Bolder, David Jamieson.2001. Affine Term-Structure Models: Theory and Implementation, Bank of Canada Working Paper 2001–1015. Ottawa : Bank of Canada. October.

- [6] Dai, Qiang and Kenneth Singleton (2000). Specification analysis of affine term structure models. Journal of Finance 55, 1943–1978. Boston: ICER.

- [7] Yang Chang and Michael Sherris, Longevity Risk Management and the Development of a Value-Based Longevity IndexSchool of Risk and Actuarial Studies and CEPAR, UNSW Business School, Sydney Australia,2018.

- [8] Luciano, Elisa, and Elena Vigna. 2005. Mortality risk via affine stochastic intensities: Calibration and empirical relevance. Mortality risk via affine stochastic intensities: Calibration and empirical relevance.

- [9] Duffie, Darrell, and Rui Kan. 1996, A yield-factor model of interet rates. Mathematical Finance 6: 379–406.

- [10] Vasicek, Oldrich. 1977, An equilibrium characterization of the term structure, Journal of Financial Economics 5: 177–88.

- [11] Monika Piazzesi, Affine Term Structure Models, Department of Economics, Stanford University, Stanford, CA.

- [12] Russo, Vincenzo, Rosella Giacometti, Sergio Ortobelli, Svetlozar Rachev, and Frank J Fabozzi.2011 Calibrating affine stochastic mortality models using term assurance premiums, n- surance: mathematics and economics 49 (1): 53–60.

- [13] Menoncin, Francesco. 2008,The role of longevity bonds in optimal portfolios Insurance: Mathematics and Economics 42 (1): 343–358. doi:10.1186/1687-2770-2013-53.

- [14] Ankush Agarwal, Christian-Oliver Ewald and Yongjie Wang Hedging longevity risk in defined contribution pension schemes.Adam Smith Business School, University of Glasgow, G12 8QQ Glasgow, UK

- [15] Harvey, A. C., Forecasting, structural time series models and the Kalman filter. Cambridge university press, 1990.

- [16] H. V. Henderson and S. R. Searle, On Deriving the Inverse of a Sum of Matrices. Society for Industrial and Applied Mathematics 23(1981),0036-1445 press, 1990.

- [17] Ibhagui, O. Application of teh kalman filter to interest rate modelling. 2010. http://archive.aims.ac. za/postgraduate-diploma-essays/2009-10/wallace.pdf.

- [18] Loeys, J., Panigirtzoglou, N. and Ribeiro, R. 2007, Longevity: a market in the making, Technical report, J.P. Moragn Securities Ltd.

- [19] M. Hardy. A matter of life and death. Financial Engineering News ,46(3..):17-20, February.. 2005.

- [20] First International Conference on Longevity Risk and Capital Markets Solutions.The longevity bond February 2005.

- [21] Babbs, S. H., and M. J. P. Selby. Pricing by Arbitrage in Incomplete Markets. Unpubl. Paper, London 1993.

- [22] Francesco Menoncin The Role of Longevity Bonds in Optimal Portfolios. Discussion Paper n.0601. December 28, 2005.

- [23] European Community, 2009. Directive 2009/138/EC of the European Parliament and of the Council of 25 November 2009 on the taking-up and pursuit of the business of Insurance and Reinsurance (Solvency II). December.

- [24] IFRS Foundation, 2010. Insurance Contracts. Exposure Draft ED/2010/8.

- [25] Cox J.C.,J.E. Intersoll and S.A. Ross 1985A Theory of the Term Structure of Interest Rates.Econometrica, 53 pp. 385 - 407.

- [26] Longstaff, F. A. and E.S. Schwartz 1992aInterest Rate Volatility and the Term Structure: A Two Factor General Equilibrium. Journal of Finance,XLVII, 1259 - 1282.

- [27] Cowley, A., and J. D Cummins, 2005Securitization of Life Insurance Asset and Liabilities,Journal of Risk and Insurance, 72:193-226.

- [28] Cairns, A. J. G., D. Blake, P. Dawson and K. Dowd, 2005Pricing the Risk on Longevity Bonds, Life and Pension, October 4: 1-44.

- [29] Blake, D., A.J.G Cairns, and K. Dowd, (2006)Living with Mortality: Longevity Bonds and Other Mortality - Linked securities, British Actuarial Journal in Press.

- [30] Lee, R. D., and L. R. Carter, (1992) Modeling and Forecasting U.S. mortality,Journal of American Statistical Association 87: 659-675.

- [31] Brouhns, N., M. Denuit, and J. k. Vermunt, (2002)A Poission Log-Bilinear Regression Approach to the Construction of Projected Life Tables, Insurance: Mathematics and Economics, 31:373-393.

- [32] Renshew, A. E., and S. Haberman, (2003) Lee-Carter Mortality Forcasting with age Specific Enhancement, Insurance: Mathematics and Economics, 33:255-275.

- [33] Currie I. D., M. Durban and P. H. C. Eilers (2004)Smoothing and Forecasting Mortality Rates, Statistical Modelling, 4:279-298

- [34] Milevsky, M. A., and S.D. Promislow (2001)Mortality Derivatives and the Option to Annuitise, insurance: Mathematics and Economics, 29:299-318.

- [35] Dehl, M., and T. Moller Valuation and Hedging of Life Insurance Liabilities with Systematic Mortality Risk In the proceedings of the 5th International AFIR coloquium, Zurich, Avaliable online at ¡http://www.afir 2005.ch¿

- [36] Miltersen, K. R., and S. A. Perrson, 2005.Is Mortality Dead? Stochastic Forward Force of Mortality Determined by No Arbitrage,Working Paper University of Bergen.

- [37] Biffis, E., (2005). Affine Processes for Dynamic Mortality and Actuarial Valuation Insurance: mathematics and Economics, 68:339-348.

- [38] Schrager, D. F., (2006)Affine Stochastic Mortality,Insurance: Mathematics and Economics, 38:81-97.

- [39] , Dehl, M. (2004) Stochastic Mortality in Life Insurance:Market Reserves and Mortality-Linked Insurance Contracts,Insurance: Mathematics and Economics, 35: 113-136.

- [40] Dowd, K., D. Blake, A. Cairns, and P. Dawson, (2006), Survivor Swaps, Journal of Risk and Insurance, 73:1-17.

- [41] Johnny Siu-Hang Li 2010,Pricing longevity risk with the parametric bootstrap: A maximum entropy approach.Insurance: Mathematics and Economics 47, Issue 2,176 186.

- [42] Søren Fiig Jarner and Thomas Møller 2013,A partial internal model for longevity risk.Scandinavian Actuarial Journal Volume 2015, Issue 4.

- [43] Tzuling Lin, Larry Y. Tzeng 2010,An additive stochastic model of mortality rates: An application to longevity risk in reserve evaluation.Insurance: Mathematics and Economics 46, Issue 2,423 435.

- [44] Andrew J.G. Cairns 2011,Modelling and management of longevity risk: Approximations to survivor functions and dynamic hedging.Insurance: Mathematics and Economics 49, Issue 3, 438 453.

- [45] Atsuyuki Kogurea, Yoshiyuki Kurachib 2010,A Bayesian approach to pricing longevity risk based on risk-neutral predictive distributions.Insurance: Mathematics and Economics V 46,162 172.

- [46] Sharon S. Yanga , Jack C. Yueb, Hong-Chih Huangc 2010,Modeling longevity risks using a principal component approach: A comparison with existing stochastic mortality models.Insurance: Mathematics and Economics 46, Issue 1,254 270.

- [47] Bingzheng Chena, Lihong Zhangb , Lin Zhaoa 2010,On the robustness of longevity risk pricing.Insurance: Mathematics and Economics Volume 47, Issue 3.358 373.

- [48] Vesa Ronkainen 2012, Stochastic modelling of financing longevity risk in pension insurance. Economics: Mathematics nad Economics.

- [49] Musiela, M. and Rutkowski, M. (1998). Martingale Methods in Financial Engineering, volume 36 of Applications of Mathematics. Springer-Verlag.