On Simultaneous Long-Short Stock Trading Controllers with Cross-Coupling

Abstract

The Simultaneous Long-Short (SLS) controller for trading a single stock is known to guarantee positive expected value of the resulting gain-loss function with respect to a large class of stock price dynamics. In the literature, this is known as the Robust Positive Expectation (RPE) property. An obvious way to extend this theory to the trading of two stocks is to trade each one of them using its own independent SLS controller. Motivated by the fact that such a scheme does not exploit any correlation between the two stocks, we study the case when the relative sign between the drifts of the two stocks is known. The main contributions of this paper are three-fold: First, we put forward a novel architecture in which we cross-couple two SLS controllers for the two-stock case. Second, we derive a closed-form expression for the expected value of the gain-loss function. Third, we use this closed-form expression to prove that the RPE property is guaranteed with respect to a large class of stock-price dynamics. When more information over and above the relative sign is assumed, additional benefits of the new architecture are seen. For example, when bounds or precise values for the means and covariances of the stock returns are included in the model, numerical simulations suggest that our new controller can achieve lower trading risk than a pair of decoupled SLS controllers for the same level of expected trading gain.

keywords:

Finance, Robustness, Stochastic Control, Uncertain Dynamic Systems.1. Introduction

The starting point for this paper is the fact that the so-called Simultaneous Long-Short (SLS) stock trading controller, see Barmish (2011); Barmish and Primbs (2016, 2011); Baumann and Grüne (2017); Malekpour and Barmish (2016); Deshpande and Barmish (2018), guarantees satisfaction of the Robust Positive Expectation (RPE) property, which means the following: The trading gain-loss function is guaranteed to have positive expected value for a broad class of stock-price processes.

In this paper, we go beyond the single-stock results cited above and pursue this theme in a more general two-stock trading scenario. To this end, we introduce Cross-Coupled SLS controllers to exploit a “correlation” between the stocks. For this new controller, we prove an RPE theorem which holds when the sign of the cross-coupling coefficient is chosen appropriately.

When additional information about the price processes is assumed, our numerical examples suggest that cross-coupled SLS controllers can achieve lower trading risk than a pair of decoupled SLS controllers for the same target value of the expected trading gain.

For an SLS controller trading a single stock, the key idea in existing literature involves generating the investment level in the stock from calculations based on hypothetically holding both long and short positions at the same time. This is accomplished using two complementary controllers.

The associated RPE results, obtained using linear feedback, differ from earlier work which is based on sample paths such as Dokuchaev and Savkin (2002); Dokuchaev (2002); Dokuchaev and Savkin (2004), and model-specific trading strategies such as Markowitz (1952); Zhang (2001); Song and Zhang (2013); Deshpande and Barmish (2016).

In addition to the work in Barmish (2011); Barmish and Primbs (2016, 2011); Baumann and Grüne (2017); Malekpour and Barmish (2016); Deshpande and Barmish (2018), other contributions to the SLS theory involve robustness results with respect to stock prices having time-varying drift and volatility Primbs and Barmish (2017), prices generated from Merton’s diffusion model Baumann (2017), generalization to the case of PI controllers Malekpour et al. (2018), and discrete-time systems with delays Malekpour and Barmish (2016).

More recently, in O’Brien et al. (2018), the authors generalize the RPE Theorem to the case of an SLS controller which can have different parameters for the long and short sides of the trade and suggest procedures for controller parameter selection to minimize trading risk based on historical data.

In Maroni et al. (2019), the authors start with a problem formulation which treats prices as if they are disturbances, as in Barmish (2008), and obtain the SLS controller parameters as the solution of an appropriately constructed optimization problem.

A noticeable attribute of the SLS literature is that it addresses single-stock trading scenarios.

For the multi-stock case, the obvious approach for using existing results would be to independently trade each stock using its own SLS controller, without exploiting any information about their price correlation.

Influenced by these considerations, the innovation in Deshpande and Barmish (2018) is to trade one stock with a long-only linear feedback and the other with a short-only linear feedback instead of using two separate SLS controllers.

Additionally, a strong assumption on the price relationships between the two stocks is made.

In contrast to the aforementioned, in this paper we impose a much weaker assumption.

Specifically, we assume that only the relative sign between the underlying drifts of the two stock prices is known.

We then put forward a new architecture that cross-couples two SLS controllers to take advantage of this relative-sign information.

In comparison to existing SLS literature, our new control architecture includes an extra degree of freedom: a cross-coupling feedback parameter , which forces interactions between the two SLS controllers.

In addition to the introduction of this novel trading architecture, the main theoretical contributions in this paper are results related to the expected value of the trading gain-loss function.

First, we provide a closed-form expression for the expected value of the trading gain-loss function.

Subsequently, we prove that for a range of , satisfaction of the RPE property is guaranteed with respect to a large class of stochastic processes for the stock prices. We also establish a recursive formula to calculate the variance of the gain-loss function.

Under strengthened assumptions that additional information about the stock prices is known over and above the relative sign between the mean returns,

we demonstrate via a numerical simulation example that there can be performance benefits due to the use of cross-coupling.

In our example, using an assumed price model with known means and variances of the stock-price returns, an optimized cross-coupled architecture achieves lower risk than two similarly optimized independent SLS controllers.

The methodology used in the numerical example can be easily adapted to evaluate performance benefits when the price model assumed is not precise.

For example, when the drifts and volatilities of the price processes are characterized with bounds instead of precise values, minimax optimization of the controller design is still possible.

Additionally, in our numerical example, we consider the account leverage resulting from the use of the cross-coupled controller.

For the specific case of Geometric Brownian Motion prices, along most sample paths, trading with the optimal cross-coupled controller results in lower account leverage than that obtained with optimal independent SLS controllers. For scenarios with a limit on the trading account leverage, we see that a “saturated” implementation of our cross-coupled controller still results in trading gains with a positive sample mean.

2. Two-Stock Trading Scenario

In this section, we describe our two-stock trading setup, including the assumptions which are in force.

Stock Price Dynamics

We consider two stocks with stochastically varying prices and having associated returns

at stages , with the assumption that the return vectors are independent and identically distributed. The mean values of the returns and are unknown to the trader. Only the relative sign between the two means, namely , is assumed to be known. For instance, if the two stocks are from the same sector, it is often the case that they tend to move in the same direction; i.e., , over the medium to long term; e.g., see King (1966). Similarly, when assets in a portfolio are negatively correlated; e.g., see Irwin and Landa (1987), we assume .

Idealized Market Assumptions

In the theory to follow, consistent with existing SLS literature, an idealized market is assumed. That is, transaction costs such as brokerage, commissions, taxes, or fees levied by the stock exchange, are not incurred. In addition, we assume perfect liquidity so that there is no gap between the bid and ask prices, and the trader can buy or sell any number of shares, including fractions, at the market price. These assumptions are similar to those made in the context of “frictionless markets” in finance literature; e.g., see Merton (1990).

Leverage and Interest

In practice, the broker usually imposes limits on the trading account leverage. For our theoretical analysis, however, we assume that leverage limits are not in play. That is, the trader has sufficient account resources to hold any desired position in the stocks. In Section 8, when we provide a numerical example, we study the practical implications of a leverage constraint and suggest further research on this issue in Section 9. We also assume that the margin interest and the risk-free rates of return are zero; we defer consideration of nonzero rates to future research.

3. Two Independent SLS Controllers

To provide context for the analysis and main results to follow, we first elaborate on the obvious way that existing single-stock SLS theory might be applied to the two-stock case. As discussed in Section 1, one can simply design two decoupled SLS controllers: one for the first stock and another for the second. Proceeding in this manner, the net investment levels and in the stocks at stage are obtained as sums

where and for are the nominally long and short positions in the -th stock, each obtained using a linear feedback controller. That is, with initial investment levels and and feedback parameters and , the long and short investment functions are given respectively as

for , where the cumulative gain-loss functions resulting from individual long and short positions in each stock are obtained using the gain-loss update equations

for ,

with .

In the sequel, we refer to the above as the 2-SLS controller.

Now, the overall trading gain-loss function for this setup is given by

Applying existing results as in Deshpande and Barmish (2018) to each of the two stocks individually, we arrive at

which is positive for , and , not both zero.

4. Cross-Coupling and State Equations

In this section, we describe the main technical novelty of this paper: a new architecture for trading which involves cross-coupling between two single-stock SLS controllers. This is achieved by augmenting each of the four linear investment functions of Section 3 with a coupling term having feedback gain to obtain

for ; .

We refer to this as the Cross-Coupled SLS (CC-SLS) controller.

When , we recover the decoupled 2-SLS controller and the corresponding results stated in Section 3.

To provide some insight into the operation of the CC-SLS controller, we consider the case when the drifts and as well as are positive. For this case, we expect and to both be positive, with and both negative.

This leads to and being greater than would be the case if ; i.e., greater than the long-investment levels in the 2-SLS counterpart.

Another case which can be similarly analyzed is encountered when the first stock follows a sample path with a positive trend, but the second stock does not, so that is positive; resulting in a smaller than would be the case without coupling. More generally, the CC-SLS controller invests more aggressively or less aggressively than its 2-SLS counterpart, depending on the extent to which the stock behaviors are consistent with their drifts.

Gain-Loss Update Equations

Substituting the formulae for the relevant CC-SLS investment functions into each of the four gain-loss update equations in Section 3, we obtain the closed-loop equations

for ; , with overall trading gain-loss function

State-Space Representation

We work with a state-space representation of the CC-SLS controller to derive our main results on robust positivity of . With state

and , the output of interest is

Then, the gain-loss update equations become

where

and constant input Since , the standard solution for is

where the state transition matrix from stage to is given by

Taking expectations, we obtain

where

and

5. Main Results

In this section, we provide two theorems related to the expected value of the overall gain-loss function at stage .

The first theorem gives us the formula for . Following this, the second theorem gives us conditions under which .

For simplicity of the proofs, we assume that both and are nonzero. However, by separately considering the case when one of these two drifts vanish, it is easy to see that in this situation, except for the break-even case when both and are zero.

To obtain a formula for , we use the following notation. For , , and , we define

and the function

which is positive for all and .

Expected Value Theorem

Suppose two stocks with stochastically varying prices and with mean returns and are traded using the Cross-Coupled SLS controller with , , and coupling coefficient satisfying . Then, for and nonzero, the expected value of the gain-loss function is given by

Proof

For and coupling coefficient , we diagonalize the block-diagonal matrix defined in Section 4 to obtain

where

is composed of the eigenvectors of as its columns, and

is the diagonal matrix with the corresponding eigenvalues of .

Note that the standing assumptions assure that and are nonzero.

Rewriting the expression for in terms of and , we obtain

where the diagonal matrix is given by

Since is a scalar, we write

where is the trace operator, and its cyclic property Strang (2009) gives us

where and denote the diagonal entries of the respective matrices. For as given above, we need only find the values of , which we collect in the vector

Further simplification using yields

Then the summation above for simplifies to the claimed closed-form expression. ∎

Remarks

We observe that the expected value of the gain-loss function is of the form

where and are independent of . This is similar in form to the result given for two independent SLS controllers in Section 3, that is,

In the theorem to follow, we use the closed-form expression for to prove that if the RPE property of the CC-SLS controller is guaranteed.

Robust Positive Expectation Theorem

Suppose two stocks with stochastically varying prices and with nonzero mean returns and are traded using the Cross-Coupled SLS controller with coupling coefficient satisfying and . Then, for any , robust satisfaction of the condition

is guaranteed.

| Scenario | Bounds on | ||||

|---|---|---|---|---|---|

Proof

Beginning with the formula obtained for and rearranging, it suffices to show that the following three inequalities hold:

For arbitrary admissible pair and , we verify the satisfaction of the first two inequalities above for the cases enumerated in Table 1. In each row of the table, we consider a possible combination of the signs of and . Each combination determines the range of possible values can take, which in turn dictates the signs of and . Using these in conjunction with the positivity of for establishes the first two inequalities.

To prove the third inequality holds, given that

we readily see that Thus, to complete the proof, it suffices to show that

To this end, we consider the following two cases:

Case 1: If , we see from Table 1 that and . Combined with the fact that the function for all , it follows that and . Hence,

Case 2: If , we see from Table 1 that . Without loss of generality, assuming , we obtain with and we use this condition to arrive at

Since , it is easily shown that

This completes the proof of the theorem. ∎

6. Variance of the Gain-Loss Function

Assuming that the mean vector

and covariance matrix

of the returns of the two stocks are known, we now derive a recursion to calculate . Recalling the state-update equation from Section 4, we first rewrite the state matrix as

where , is the identity matrix ,

and we rewrite as

where

With this notation, the state update equation becomes

with initial value . It follows that

To calculate the variance of the gain-loss function, we first define , and subsequently

We now obtain the recursion

Substituting the various quantities into the recursion above for and denoting the ()-th element of the matrix as , it follows that

Starting with initial value , we use the above recursion for to obtain . Recalling that the gain-loss function for , we now calculate

and subsequently,

From this, we calculate the standard deviation of , which is used in the numerical example in Section 8.

7. Risk Mitigation via Cross-Coupling

To augment the analysis of the CC-SLS controller in Section 4, we

now analyze a trading scenario where a cross-coupling can result in lower trading risk when compared to two independent SLS controllers.

This analysis is performed under the strengthened assumption that the mean returns and covariances of the two stock prices are known.

Then in the spirit of modern portfolio theory, for the classical case when the controller parameters and are optimized with respect to these assumed price models,

we compare the mean and standard deviation of obtained by the CC-SLS controller against the ones obtained by the 2-SLS controller.

We demonstrate how, for a given target return, the CC-SLS controller architecture can lead to lower trading risk than that of the 2-SLS controller. Namely, the standard deviation of resulting from the use of the CC-SLS is lower than that obtained using 2-SLS.

Associated with the two controllers described in Sections 3 and 4, whenever convenient,

we emphasize the dependence of various quantities on the controller parameter vector

by including it as an argument in mathematical functions of interest; e.g., we write instead of for the gain-loss function at stage . Thus, given initial trading account value , the account value at stage is given by

and depends on . Without loss of generality, we assume so that the cumulative return

is equal to , and the risk-return pair is

8. Numerical Example

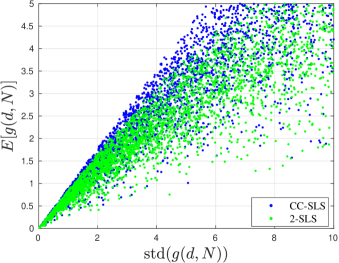

To illustrate the ideas in Section 7, we work with an assumed stochastic model of the stock-price processes with independent returns having respective mean values and and known variances and Then, for both the CC-SLS and the 2-SLS controllers, we consider 5000 candidate parameter vectors selected by using the uniform distribution to generate points

noting that is inadmissible in the RPE Theorem.

For each vector selected above for the CC-SLS controller, we force to get a corresponding 2-SLS parameter vector.

Then for each , and , we calculate the risk-return pair

for each of the two controllers. In Figure 1, for the CC-SLS controller, each such pair is denoted with a blue dot and for the 2-SLS controller, a green dot is used.

For each of the two architectures, for a given target return , we seek a parameter vector that solves

In terms of Figure 1, this means that the CC-SLS optimum parameter vector corresponds to the leftmost blue dot along the line with

Similarly for 2-SLS, the optimum parameter vector corresponds to the leftmost green dot along the same line.

From the figure, we see that for target return , the optimal CC-SLS controller appears to guarantee a lower level of the risk versus that obtained for the optimal 2-SLS controller.

To make the above more concrete, for , using the search sets for the controller parameters above, an optimal 2-SLS controller parameter vector is found to be

and results in

Similarly, an optimal CC-SLS parameter vector is found to be

and results in

Consistent with the discussion above, this CC-SLS controller leads to lower risk than its 2-SLS counterpart.

Account Leverage Considerations

As stated in Section 2, the broker typically imposes limits on the account leverage to ensure that investment levels are commensurate with the account value. Thus, to supplement the foregoing risk-return analysis, we study the leverage used by the two optimal controllers above. Given that one or both stocks may be sold short with the corresponding net investments , consistent with practice, we work with leverage ratio

and study using one million sample paths. For simulating these paths, however, we need to know the joint distribution of the returns, not just their means and covariances. To this end, we assume that the prices are obtained from two independent Geometric Brownian Motion models which are consistent with the used for the two controller optimization tasks above. Since the total returns are log-normally distributed, we generate these prices using the update equations

where and . Without loss of generality, we assume that the initial prices in the above update equations are . Subsequently, for , we estimate that for the CC-SLS controller, about 95% of the time, and that for the 2-SLS controller, using that same 95% figure of merit, we estimate Furthermore, out of the one million sample paths, the optimal CC-SLS controller results in a bankruptcy, characterized by account value , in only sample paths as compared to bankruptcies for the 2-SLS controller. For such sample paths, we record the maximum leverage to be To summarize, the optimal CC-SLS controller not only leads to lower risk than its optimal 2-SLS controller, but it also results in a much lower account leverage almost all the time and leads to a lower probability of account bankruptcy.

Saturated 2-SLS and CC-SLS Controllers

Noting that the account leverage for both controllers can far exceed the limits imposed by stock brokers, to illustrate how one might conform with common practice, we revisit our simulation with the added constraint , and “saturate” the investments of the 2-SLS and the CC-SLS controllers whenever this inequality is violated. More precisely, we take

and

Although such a scheme ensures that for all , the theoretical guarantee of robust positive expectation is no longer available. Nonetheless, from the one million sample paths of the GBM prices described above, we statistically estimate and , and encounter no bankruptcies using the saturated CC-SLS controller. In comparison, for the saturated 2-SLS controller, we estimate , with and face account bankruptcy in 12 sample paths. Thus, for this more practical scenario, the saturated CC-SLS and 2-SLS controllers yield positive average trading gains while conforming to the leverage constraints imposed on them.

9. Conclusion

In this paper, we introduced the notion of cross-coupled SLS controllers for trading two stocks.

We derived a closed-form expression for the expected trading gain-loss function resulting from this new architecture and, based on this formula, our new Robust Positive Expectation Theorem provides conditions under which positivity of the expected gain-loss function is guaranteed.

We also provided simulations which suggest, under strengthened hypotheses, that our new CC-SLS architecture enables controller designs that achieve lower trading risk than two independent SLS controllers for the same target expected gain.

Finally, in our numerical simulations, we found that the cross-coupled SLS controller results in lower trading account leverage than two decoupled SLS controllers. Similarly, we showed that using “saturated” implementations of both controller designs which guarantee compliance with a leverage limit imposed by the broker, the mean-variance performance of the cross-coupled SLS controller is better than that obtained with two decoupled SLS controllers.

Three directions for future research immediately present themselves:

The first involves the introduction of cross-coupling into different variants of the SLS controller found in the literature; e.g., in Malekpour and Barmish (2016), an SLS controller with delays is considered. A second direction involves extending the theory presented in this paper to trading scenarios involving more than two stocks.

Finally, the third possible direction for future research is motivated by the fact that the practitioner invariably faces leverage restrictions. Hence, it would be of interest to see if the CC-SLS controller still leads to a guarantee of robust positive expectation when a saturation scheme, along the lines studied in the previous section, is used. Results given in Barmish and Primbs (2016) for a standalone SLS controller provide motivation for further work.

References

- Barmish [2008] B. Ross Barmish. On Trading of Equities: A Robust Control Paradigm. IFAC Proceedings Volumes, 41(2):1621 – 1626, 2008. ISSN 1474-6670. https://doi.org/10.3182/20080706-5-KR-1001.00276. 17th IFAC World Congress.

- Barmish [2011] B. Ross Barmish. On Performance Limits of Feedback Control-Based Stock Trading Strategies. Proceedings of the American Control Conference, pages 3874–3879, San Fransisco, 2011. 10.1109/ACC.2011.5990879.

- Barmish and Primbs [2011] B. Ross Barmish and James A. Primbs. On Arbitrage Possibilities via Linear Feedback in an Idealized Brownian Motion Stock Market. Proceedings of IEEE Conference on Decision and Control, pages 2889–2894, Orlando, 2011. 10.1109/CDC.2011.6160731.

- Barmish and Primbs [2016] B. Ross Barmish and James A. Primbs. On a New Paradigm for Stock Trading Via a Model-Free Feedback Controller. IEEE Transactions on Automatic Control, 61(3):662–676, 2016. ISSN 0018-9286. 10.1109/TAC.2015.2444078.

- Baumann [2017] Michael Heinrich Baumann. On Stock Trading Via Feedback Control When Underlying Stock Returns Are Discontinuous. IEEE Transactions on Automatic Control, 62(6):2987–2992, 2017. ISSN 0018-9286. 10.1109/TAC.2016.2605743.

- Baumann and Grüne [2017] Michael Heinrich Baumann and Lars Grüne. Simultaneously Long Short Trading in Discrete and Continuous Time. Systems & Control Letters, 99:85–89, 2017. ISSN 0167-6911. 10.1016/J.SYSCONLE.2016.11.011.

- Deshpande and Barmish [2016] Atul Deshpande and B Ross Barmish. A General Framework for Pairs Trading with a Control-Theoretic Point of View. Proceedings of IEEE Conference on Control Applications, pages 761–766, Buenos Aires, 2016.

- Deshpande and Barmish [2018] Atul Deshpande and B. Ross Barmish. A Generalization of the Robust Positive Expectation Theorem for Stock Trading via Feedback Control. Proceedings of the European Control Conference, pages 514–520, Limassol, 2018. 10.23919/ECC.2018.8550535.

- Dokuchaev and Savkin [2004] N.G. Dokuchaev and Andrey V. Savkin. Universal Strategies for Diffusion Markets and Possibility of Asymptotic Arbitrage. Insurance: Mathematics and Economics, 34(3):409–419, 2004. ISSN 0167-6687. 10.1016/J.INSMATHECO.2004.01.004.

- Dokuchaev [2002] Nikolai Dokuchaev. Dynamic Portfolio Strategies: Quantitative Methods and Empirical Rules for Incomplete Information. International Series in Operations Research & Management Science. Springer US, Boston, MA, 2002. ISBN 978-0-7923-7648-4. 10.1007/978-1-4615-0921-9.

- Dokuchaev and Savkin [2002] Nikolai Dokuchaev and Andrey V. Savkin. A Bounded Risk Strategy for A Market with Non-Observable Parameters. SSRN Electronic Journal, 2002. ISSN 1556-5068. 10.2139/ssrn.321960.

- Irwin and Landa [1987] Scott H. Irwin and Diego Landa. Real Estate, Futures, and Gold as Portfolio Assets. Journal of Portfolio Management, 14(1):29–34, Fall 1987.

- King [1966] Benjamin F King. Market and Industry Factors in Stock Price Behavior. The Journal of Business, 39(1):139–190, 1966. ISSN 00219398, 15375374.

- Malekpour et al. [2018] S. Malekpour, J. A. Primbs, and B. R. Barmish. A Generalization of Simultaneous Long-Short Stock Trading to PI Controllers. IEEE Transactions on Automatic Control, 63(10):3531–3536, 2018. 10.1109/TAC.2018.2799484.

- Malekpour and Barmish [2016] Shirzad Malekpour and B. Ross Barmish. On Stock Trading Using a Controller with Delay: The Robust Positive Expectation Property. 2016 IEEE 55th Conference on Decision and Control, pages 2881–2887, Las Vegas, 2016. 10.1109/CDC.2016.7798698.

- Markowitz [1952] Harry Markowitz. Portfolio Selection. The Journal of Finance, 7(1):77–91, 1952. 10.1111/j.1540-6261.1952.tb01525.x.

- Maroni et al. [2019] G. Maroni, S. Formentin, and F. Previdi. A Robust Design Strategy for Stock Trading via Feedback Control. Proceedings of the European Control Conference, pages 447–452, Naples, 2019. 10.23919/ECC.2019.8795812.

- Merton [1990] Robert C. Merton. Continuous-time Finance. B. Blackwell, 1990. ISBN 9780631185086.

- O’Brien et al. [2018] Joseph D O’Brien, Mark Burke, and Kevin Burke. A Generalized Framework for Simultaneous Long-Short Feedback Trading. arXiv preprint, 2018.

- Primbs and Barmish [2017] James A. Primbs and B. Ross Barmish. On Robustness of Simultaneous Long-Short Stock Trading Control with Time-Varying Price Dynamics. Proceedings of the IFAC World Congress, 50(1):12267–12272, Toulouse, 2017. ISSN 2405-8963. 10.1016/J.IFACOL.2017.08.2045.

- Song and Zhang [2013] Qingshuo Song and Qing Zhang. An Optimal Pairs-Trading Rule. Automatica, 49(10):3007–3014, 2013.

- Strang [2009] Gilbert Strang. Introduction to Linear Algebra. Wellesley-Cambridge Press, Wellesley, MA, fourth edition, 2009. ISBN 9780980232714 0980232716 9780980232721 0980232724 9788175968110 8175968117.

- Zhang [2001] Qing Zhang. Stock Trading: An Optimal Selling Rule. SIAM Journal on Control and Optimization, 40(1):64–87, 2001.