Skjernvej 4A, 9220, Aalborg, Denmark

Estimating the Copula of a class of Time-Changed Brownian Motions: A non-parametric Approach

Abstract

Within a high-frequency framework, we propose a non-parametric approach to estimate a family of copulas associated to a time-changed Brownian motion. We show that our estimator is consistent and asymptotically mixed-Gaussian. Furthermore, we test its finite-sample accuracy via Monte Carlo.

1 Introduction

One of the most fundamental results in probability theory is the so-called Sklar’s Theorem. It states that for every random vector there exists a copula (see Section 2) such that

where is the cumulative distribution function (cdf for short) of and

| (1.1) |

and is the cdf of , for in .

Since then, copulas have been applied in a large number of sciences, for instance in hydrology ([11]), engineering ([15]), and, perhaps most noticeably, in finance. In finance, their primary use is in risk management and portfolio allocation. Specifically, copulas are used to model the joint distribution of financial assets. For a detailed account see [3] and [5]. Note that this way of using copulas can be considered as a spatial way of modeling dependence, i.e. describing the dependence between two or several stochastic processes at distinct times. Copulas have also found their use in temporal modelling as well. [4] characterized Markov processes by means of their copulas. [14] also define so-called copula processes. Furthermore, [4] derived the copula of the bivariate distributions of a Brownian motion. In addition, [13], argued that the copula of a Brownian motion could be uses to construct similar processes with arbitrary marginal distributions.

In the spatial set-up, parametrical and non-parametrical inference for copulas is well documented. See for instance [12] and [6]. However, in the temporal case very little statistical analysis has been done, see for instance [2]. This paper aims at developing some results in that direction.

In the present work, we concentrate on the statistical inference for a family of copulas associated with the finite-dimensional distributions of a class of time-changed Brownian motions. More precisely, we propose a non-parametric estimator for a family of conditional copulas linked to a time-changed Brownian motion. We show consistency and asymptotic (mixed) normality under the assumption that the process is observed in a high-frequency set-up.

The paper is structured as follows. Section 2 introduces the notations used through the paper and discusses some essential preliminaries. In Section 3 we present our results and we show the performance of the estimator in finite-samples. In the last section the proofs of our main results are presented.

2 Background

In this section we recall several definitions and properties required to present our main results. Throughout this paper will denote a filtered probability space satisfying the usual assumptions of right-continuity and completeness. If is a set, then we will denote the -fold cartesian product of with itself as . Similarly, if is a metric space, then the product metric defined on is denoted .

2.1 Copulas of Time-Changed Brownian motion

For we write () if () for every . Whenever with , we define . Recall that a copula is a function satisfying the following:

| (2.1) | ||||

In this paper we focus on the time-changed Brownian motion

| (2.2) |

where is a continuous random time change independent of , that is, it is a non-decreasing process taking values in such that is a -stopping time for all . Within this framework, for all the copula associated to , is completely determined by the law of and the random fields

| (2.3) |

where

| (2.4) |

in which denotes the cdf of the standard normal distribution. For more details on the previous statements we refer the reader to [3] and [4]. It is not difficult to see that the mapping satisfies (2.1) almost surely for all . Moreover, it holds that

| (2.5) |

where denotes the cdf of given . Motivated by (2.5) and the terminology used in [9], we will refer to as the conditional copula associated to .

2.2 Limit Theorems and Convergence

The notations and stand, respectively, for convergence in probability and in distribution of random vectors. As usual the space of cádlág fields will be denoted by . If and are two cádlág processes we write , whenever

A sequence of random vectors on is said to converges stably in law towards (in symbols ), which is defined on an extension of , say , if for every continuous and bounded function and any bounded random variable it holds that

where denoted expectation w.r.t. . For a concise exposition of stable convergence see [7]. Given a stochastic process , we will use the notation , . The realized variation of a process is defined and denoted as the process

where denotes the integer part of . It is well known that if is a continuous semimartingale, then

3 Estimating the conditional copula of

As discussed in Section 2, the copula associated to , for , is completely determined by the law of as well as the family of conditional copulas , where as in (2.3). For the rest of this section, we propose a non-parametric approach for estimating the later. Our sample scheme is as follows: The process is observed on a fixed interval , , at times , for . Thus, motivated by (2.3) and the fact that , as , we propose to estimate via

Our first result shows that is indeed a consistent estimator for .

Theorem 1.

Let , such that . Then for all , , and , it holds

Now we proceed to derive second-order asymptotics for . In order to do this, we require stronger assumptions on the structure of . Specifically, we are going to assume that there is a -Brownian motion such that

| (3.1) |

where is a cádlág process. Observe that by Knight’s Theorem, admits the representation

| (3.2) |

where . Thus, if is assumed to be independent of , we can further choose to be independent of . This can be seen easily in the case when . Indeed, in that situation it is well known (see for instance [1]) that (3.2) holds with

where , which easily implies that is independent of . The general case can be analysed in a similar way. Assuming that admits the representation (3.1) we obtain the following Central Limit Theorem for

Theorem 2.

Let be given by (3.1) and assume that for all . Fix and denote by . Then for , as

where is a standard normal random variable independent of and

in which ,

A simple way to estimate is by using power variations: If is càdlàg (see for instance [8]), then as

Thus, a feasible estimator for is

Thus, we have an easy consequence of the previous theorem:

Corollary 1.

Under the assumptions of the previous theorem we have that

3.1 Simulation study

In this part we study the finite-sample behavior of our proposed estimator. We use here Monte Carlo simulations to investigate the sensitivity of to the variation of as well as the sample size. Our set-up is as follows: The volatility term is simulated according to the so-called Cox-Ingersoll-Ross process, i.e. satisfies the stochastic differential equation

The parameters are set in such a way that the Feller condition is satisfied. Based on this, we sample over the interval equidistant discretizations , where is given as in (3.2).

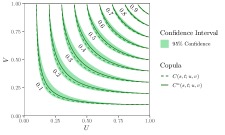

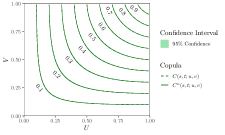

In Figure 1 we have plotted the level sets of and together with the confidence contours provided by Theorem 2. The confidence countours behave as we would imagine; near the line we see that that they allow for the largest deviations. As approach the boundary of , the intervals diminish as expected: and coincide on the boundary. Furthermore, as increases we see that the confidence contours become increasingly narrow as expected.

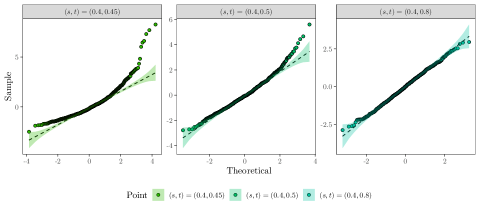

In Figure 2 we report the finite-sample distribution of our standardized error against the standard normal distribution. We can see that the accuracy of our statistic is sensitive to the boundary points where and are close. Again, this behaviour is not unexpected; the temporal gradient , as in Theorem 2, is given by

Here, is the density function of a standard Gaussian. We see, that terms proportional to appear. However, recall that as for the copula reduces to . Furthermore, it is also very likely that numerical errors influence the result here, due to terms such as .

We conclude this section by investigating whether the convergence in Theorem 1 can be extended to uniform convergence over . Specifically, we investigate, via Monte Carlo simulations, the asymptotic behavior of the statistic

as the sample size increases.

Figure 3 shows the density estimates, obtained via a Gaussian kernel density estimate, for on a logarithmic scale focusing on the peaks. Observe that the mean is located in the lower tail, due to a substantial number of simulations resulting in being very close . Similarly, is also added to the plot, showing that the shift in the distribution is, relatively, proportional to on a logarithmic scale. Based on Figure 3, these simulations indicate that Theorem 1 may be extended to include the supremum over .

4 Proofs

The following lemmas are key for the proof of our main results.

Lemma 1.

Let be as in (2.4). For all , the mapping is continuous in and continuously differentiable in .

Proof.

If is in the boundary of the result is trivial. Suppose that and put

and when . From Example 5.32 in [13], it follows that for almost all

| (4.1) |

The continuity then follows by the Lebesgue’s Dominated Convergence Theorem. On the other hand, for we have that for

where is density of a standard normal distribution. Since for any constants such that , it holds that as , we deduce that

| (4.2) |

Interchanging roles between and allow us to conclude that (4.2) is fulfilled for all . Another application of the Dominated Convergence Theorem concludes the proof.∎

For the next result we need the following subspace of :

Lemma 2.

Let , and . Then the mapping

is continuous, where denotes the supremum metric.

Proof.

We must show, that for every and there exists a such that

| (4.3) |

To this end, note first that for all , Now, let and consider the set . For we have

This implies . Now set . Then, for every . Let . By the Heine-Cantor Theorem, it follows that the restriction of to is uniformly continuous. This means that we can find such that for all . Now, put . We conclude from above that if and then for all , from which (4.3) follows. ∎

Proof of Theorem 1.

Let . From Lemma 1, the mapping is continuous in . Thus, we deduce that extends (as in Lemma 2) to a continuous function . Moreover

where denotes the shift operator, i.e.

In view that is a continuous operator from to and , as , we can now apply The Continuous Mapping Theorem (see for instance [3]) to conclude that

which is exactly the conclusion of the theorem.∎

Proof of Theorem 2.

First note that thanks to Lemma 5.3.12 in [8] we may and do assume that for some deterministic constant . Now, let

Since for all we can find large enough such that . Moreover, by Taylor’s Theorem

From Theorem 5.4.2 in [8], it follows that for any

where is a Brownian motion independent of . Therefore, it is enough to show that

| (4.4) |

In view that , every subsequence contains a further subsequence such that . Fix By using that , we can find an open ball with center and radius which is totally contained in . Moreover, for every there is such that

This in particular implies that for all and , is contained in an open ball with center and radius . Therefore, we can find a compact set such that for all and . Hence, by the continuity of on (see Lemma 1) and the Dominated Convergence Theorem, we deduce that as

References

- [1] O. E Barndorff-Nielsen and A. Shiryaev. Change of Time and Change of Measure. WORLD SCIENTIFIC, 2nd edition, 2015.

- [2] Xiaohong Chen and Yanqin Fan. Estimation of copula-based semiparametric time series models. Journal of Econometrics, 130(2):307–335, 2006.

- [3] U. Cherubini, F. Gobbi, S. Mulinacci, and S. Romagnoli. Introduction to empirical processes and semiparametric inference. John Wiley & Sons Ltd, 2012.

- [4] William F Darsow, Bao Nguyen, Elwood T Olsen, et al. Copulas and markov processes. Illinois journal of mathematics, 36(4):600–642, 1992.

- [5] Christian Genest, Michel Gendron, and Michaël Bourdeau-Brien. The advent of copulas in finance. The European Journal of Finance, 15(7-8):609–618, 2009.

- [6] Christian Genest, Kilani Ghoudi, and L-P Rivest. A semiparametric estimation procedure of dependence parameters in multivariate families of distributions. Biometrika, 82(3):543–552, 1995.

- [7] Erich Häusler and Harald Luschgy. Stable convergence and stable limit theorems, volume 74. Springer, 2015.

- [8] Jean Jacod and Philip Protter. Discretization of processes, volume 67. Springer Science & Business Media, 2011.

- [9] Andrew J Patton. Modelling asymmetric exchange rate dependence. International economic review, 47(2):527–556, 2006.

- [10] Sidney Resnick. A probability path. Springer, 2019.

- [11] G Salvadori and Carlo De Michele. On the use of copulas in hydrology: theory and practice. Journal of Hydrologic Engineering, 12(4):369–380, 2007.

- [12] Olivier Scaillet and Jean-David Fermanian. Nonparametric estimation of copulas for time series. FAME Research paper, (57), 2002.

- [13] Volker Schmitz. Copulas and stochastic processes. PhD thesis, Bibliothek der RWTH Aachen, 2003.

- [14] Andrew G Wilson and Zoubin Ghahramani. Copula processes. pages 2460–2468, 2010.

- [15] SC Yang, TJ Liu, and HP Hong. Reliability of tower and tower-line systems under spatiotemporally varying wind or earthquake loads. Journal of Structural Engineering, 143(10):04017137, 2017.