Some Theoretical Results Concerning Time-varying Nonparametric Regression with Local Stationary Regressors and Error

Abstract

With regard to a three-step estimation procedure, proposed without theoretical discussion by Li and You in Journal of Applied Statistics and Management, for a nonparametric regression model with time-varying regression function, local stationary regressors and time-varying AR(p) (tvAR(p)) error process , we established all necessary asymptotic properties for each of estimator. We derive the convergence rate and asymptotic normality of the preliminary estimation of nonparametric regression function, establish the asymptotic distribution of time-varying coefficient functions in the error term, and present the asymptotic property of the refined estimation of nonparametric regression function. In addition, with regard to the ULASSO method for variable selection and constant coefficient detection for error term structure, we show that the ULASSO estimator can identify the true error term structure consistently. We conduct two simulation studies to illustrate the finite sample performance of the estimators and validate our theoretical discussion on the properties of the estimators.

Keywords: time-varying autoregressive, locally stationary, local linear regression, ULASSO, BIC

1 Introduction

The nonparametric regression model has played a prominent role in finance and economics analysis due to its capability of capturing the nonlinear relationships between time series, which are commonly encountered in practice. In some scenario, the factors omitted from the regression model, like those included, are correlated across periods in an unknown way, which will bring errors with autocorrelation. This leads to the regression model

where the error process is autocorrelated but satisfies .

By modeling as some autocorrelated process, the autocorrelation in the data can be removed so that the regression function can be estimated more efficient. For instance, Xiao et al., (2003) considered the case in which is assumed to be an invertible linear process, with the finite-order ARMA() process as the special case, and showed that the autocorrelation function of the error process can improve the estimation of the regression function. Su and Ullah, (2006) modeled as a finite order nonparametric AR process. Liu et al., (2010) discussed the estimation of regression function based on the models with following both AR() and ARMA() process.

All aforementioned literatures share the same assumption that and are strictly stationary. In practice, this assumption sometimes is hard to justify since the time series are often observed with trends. One typical approach for applying the time series analysis is to remove the deterministic trend and seasonality components. Various nonparametric detrending procedures have been developed for the time series that contains the smooth trend and ARMA or AR error term, including those of Qiu et al., (2013); Shao and Yang, (2017); Schröder and Fryzlewicz, (2013); Truong, (1991), among others. For more detrending methods, the reader is referred to Brockwell and Davis, (2016). As a result of detrending, the model used is hard to reveal the evolutionary nature of the original data. In recent, an alternative approach for modeling nonstationary time series, viz, the locally stationary time series models come into researchers’ view. Locally stationary process is introduced by Dahlhaus, (1996), which can be used to model the nonstationary time series directly. Intuitively speaking, a process is locally stationary if over short periods of time (i.e., locally in time) it behaves in an approximately stationary way. Compared to the methods with the (weak) stationary assumption, locally stationary time series model seems more attractive since it can better describe the nonstationary behavior. Due to this fact, several models for locally stationary processes have been proposed in the recent literature. Bellegem and Dahlhaus, (2006) discussed the time-varying AR() models with the selection of order . Vogt, (2012) studied nonparametric regression, which includes a wide range of interesting nonlinear time series such as nonparametric autoregressive models. Pei et al., (2018) developed methods for inference in nonparametric time-varying fixed effects panel data models that allow for locally stationary regressors.

In this paper, we focus on a class of nonparametric regression models with time-varying regression function, local stationary regressors and time-varying AR() (tvAR()) error process, which is studied by Li and You, (2020). The model is given by

| (1.1) |

where and are unknown functions and allowed to change smoothly over time. The dimension covariates are assumed to be locally stationary. Without loss of generality, set in this paper. The error process satisfies . The white noise is independent and identically distributed (i.i.d.) with mean zero and variance , and . As discussed by Vogt, (2012), the tvAR() error process , under some mild conditions, is locally stationary.

Obviously, model (1.1) is a quite general form. If and are time-invariant, model (1.1) is specialized as

| (1.2) |

which are discussed in Su and Ullah, (2006); Liu et al., (2010). Liu et al., (2010) proposed an iterative estimation procedure for model (1.2) and showed that the iterative estimator is more efficient than the estimator by incorporating the correlation information of the error into the local linear regression. Motivated by this, Li and You Li and You, (2020) defined a three-step estimation procedure for model (1.1) and presented its applications in finance through two real data. They first obtained a preliminary estimation for by local linear regression, ignoring the time-varying autoregressive structure of the error term. Then the local linear methods was employed on the residuals from the first step to obtain the estimation of the time-varying autoregressive coefficient functions . At last, the autocorrelated error term was eliminated by plugging in the estimations obtained from the first two step and a refined estimation of was obtained by using local linear methods again. Intuitively, the refined estimation should be more efficient than the preliminary estimation, which is verified by the real data in Li and You, (2020), since the autocorrelated error term was estimated and eliminated. Unfortunately, no any theoretically results on the estimation was provided by Li and You, (2020). Due to its valuable application, it is worthy to discuss the estimation theoretically. In this paper, we present the asymptotical properties of preliminary estimation of , the estimation of , and the refined estimation of . Moreover, the fact that the refined estimation of is more efficient than the preliminary estimation is proved. This is also illustrated by the simulation studies. For the real data application, the readers are referred to Li and You, (2020).

The rest of the paper is organized as follows. Section 2 introduces some notations and presents the estimation method given by Li and You, (2020). Section 3 is the main part of the paper, in which all asymptotical properties of the estimations are provided. At last, the simulation studies are conducted in Section 4.

2 Notations and estimation procedure

In this section, some notations are introduced and the estimation method given by Li and You, (2020) are presented briefly for the readers’ convenience. The readers are referred to Li and You, (2020) for more details.

For model (1.1), we assume, without loss of generality, that the covariate is 1-dimensional.

step 1. The preliminary estimator of . Ignoring the time-varying autoregressive structure of the error term, and by applying local linear fitting method (Fan and Gijbels, (1996)) and locally weighted least square estimation method, the preliminary estimator of is derived as:

| (2.1) |

where , , , , . , and is a zero-symmetric kernel function with compact support. It should be noted that the product kernel is applied here and the bandwidths for both time and covariate are assumed to be same. Following the similar procedures in Ruppert and Wand, (1994) and Pei et al., (2018), the results can be easily modified to allow for non-product kernel and different bandwidths.

step 2. The estimator of . Let be the estimate of the unobservable error term . For the model with the assumption that is known, by minimizing

| (2.2) |

the estimation of can be obtained as

| (2.3) |

where is identity matrix, is zero matrix. Let . , and with for , and . Let , where .

In Section 3, we show that is efficient with the same convergence rate and has the same asymptotic distribution as the estimator when is observable, which is given by Kim, (2001).

Moreover, Li and You, (2020) presented the solution to the problem that the order of the error series is unknown in the real study. Denote the true value of as . Without loss of generality, it is assumed with that the first component of are nonzero smooth functions, while the next components are nonzero constant, and the final components are zeros. Define . It is obvious that identifying the coefficient functions and the constant coefficients simultaneously is equivalent to identifying these two sets together. Applying the uniform adaptive LASSO (ULASSO) method proposed by Wang and Kulasekera, (2012), the ULASSO estimator for each is defined as the minimizer of the convex function

| (2.4) |

where are defined in (2.2), are the tuning parameters, and are the uniform adaptive weights for all . Let , and denote , as the index set of the relative variables and the coefficient functions identified by . The two sets and are taken as the estimators of and respectively.

To determine the tuning parameters, Li and You, (2020) proposed a BIC selector:

| (2.5) |

where is the total number of nonzero elements in both and , and

Define to be the minimizer of (2.5). Thus, and are taken as the estimators of and respectively.

Once again, there is no any discussions on the property of and in Li and You, (2020), which is worthwhile and necessary to study. In Section 3, we show that can identify the true model consistently.

step 3. The refined estimator of . By minimizing the locally weighted least square loss function

where is a new bandwidth, the refined estimator of is derived (seeLi and You, (2020)).

where with . , , . . Li and You Li and You, (2020) explain the reason that the refined estimator is more efficient than the preliminary estimator intuitively. In Section 3, we present the asymptotic property of the refined estimator and show that the refined estimator is more efficient than the preliminary estimator theoretically.

3 Main results

Li and You, (2020) presented the whole procedure of the estimation and the application to the finance without any discussion on the property of the estimation. Due to its wide range of applications, it is worthwhile and necessary to discuss the statistical property of the estimation. In this article, we present the asymptotic properties of all estimators in Li and You, (2020). In this section, denotes a generic constant that may vary from line to line.

3.1 Asymptotic results on the preliminary estimator of

For the preliminary estimator of , , we present its uniform convergence rate and asymptotic normality. To do so, we need the following assumptions.

-

(C1)

Both and are locally stationary, i.e., for each re-scaled time point , there exist two strictly stationary processes and such that almost surely, and almost surely, where is a process of positive variables satisfying for some and , and is a process of positive variables satisfying for some and .

-

(C2)

is -mixing, and the mixing coefficients satisfies that for some and with the same in (C6).

-

(C3)

The density of the variable is smooth in and bounded away from zero. In particular, is continuously differentiable.

-

(C4)

is twice continuously partially differentiable and Lipschitz-continuous.

-

(C5)

has compact support and is Lipschitz-continuous, , and .

-

(C6)

For some , .

-

(C7)

With , with the same in (C6), and , it holds that

Remark 3.1.

(C1) is the basic assumption for a locally stationary process defined as in Vogt, (2012), which is reasonable in modeling economic and financial data. (C2) is the mixing condition for each time series, which is reasonable and allows the notation in the proofs as simple as possible. (C3)-(C5) are the regularity conditions commonly used in locally stationary fields and nonparametric settings. (C6) together with (C2) are useful conditions proposed by Hansen, (2008) to obtain the order of the stochastic part and the variance part. (C7) involves the conditions to satisfy the optimal convergence rate.

Remark 3.2.

The constant can be regarded as a measure of how well is approximated by : the larger can be chosen, the less mass is contained in the tails of the distribution of . So the approximation of by is getting better for larger . This is also true for with regard to .

Remark 3.3.

In general, it is not indispensable for the kernel function to have a bounded support as long as its tails are thin (e.g., a density function that has a second moment). However, as said in Fan and Yao, (2008), ’when the kernel function has a bounded support, the integration above takes place only around a neighborhood of . Hence, it suffices to assume that the density has a th continuous derivative at the point .’ For the sake of simplicity, it is assumed in this article that the kernel function has a bounded support. This assumption can be removed at the cost of lengthier arguments.

The uniform convergence rate and the asymptotic normality of the preliminary estimator are given by Theorem 3.1 and 3.2. The following lemma is needed to prove the theorems.

Lemma 3.1.

Let be a compact set of , and the bandwidth in (2.1) satisfies that

with , , and with the same in condition (C6). Then it holds under the conditions (C1)-(C7) that

Proof.

Theorem 3.1.

Assume that conditions (C1)-(C7) hold. , where is defined in condition (C1). Then we have

Proof.

By (2.1), we have

where

By Lemma 3.1, we have

Applying the arguments for Lemma 3.1 to , we have

We also claim that

| (3.1) |

where . Note that is irrelative with , thus (3.1) can be proved by following the idea of Vogt, (2012).

Note that

Firstly, using standard results from density estimation, we have

| (3.2) |

where denotes the kronecker product. Then we consider the term . Denote as a Lipschitz-continuous function with support for some . Assume that for all . Let , then it holds that

with

and

We firstly consider . Since the kernel function is bounded, we can find a constant such that for . By the definition of and the smoothness of , can be bounded by . Thus, it follows with conditions (C1) and (C5) that

uniformly in and . Using similarly arguments, we can find that and . Finally, applying Lemma 3.1 and conditions (C3) and (C4), we obtain that

Thus (3.1) holds by combining the results of and (3.2). Then we have

∎

Theorem 3.2.

Under the conditions (C1)-(C7), let , which guarantees that the bandwidth can be selected to obtain the optimal convergence rate. Then for any ,

where , and

| (3.3) |

To prove Theorem 3.2, we define the following notations. , , , . Let and be the -th row of and , respectively. Denote the Hessian matrix of at , and a -dimensional vector whose -th element is . Define

| (3.4) |

where is the -th order auto-covariance function of the approximate stationary process for the rescaled time point .

Proof.

With and as in the proof of Theorem 3.1, we have

where

Henceforth, we refer to and as the bias part and the variance part, respectively.

By conditions (C1) and (C4), we have

Hence, . By Taylor Theorem, we have

Thus the bias part can be written as

| (3.5) |

Note that

where

With the similar arguments as in Ruppert and Wand, (1994), we have

| (3.6) |

and

| (3.7) |

It follows from (3.5), (3.6), and (3.7) that the asymptotic bias

| (3.8) |

Next we consider the variance part. The following proof is completed by a classical blocking technique Cai et al., 2000b . Partition into subsets with small-block of size and large-block of size . Let , . For any non-zero vector , let

where . Thus

| (3.9) |

Let . It’s easy to show that and

| (3.10) | ||||

| (3.11) |

As shown in Kim, (2001),

| (3.12) |

Hence, it follows from that (3.11) and (3.12) that

Since is -mixing, it follows from Lemma (1) of Cai et al., 2000b that , which implies that the second term of (3.9) is negligible. Hence,

For , define

Then

With the similar arguments of Theorem 2 in Cai et al., 2000b , it can be shown that small block and the remainder are asymptotically negligible in probability, and each in large block is asymptotically independent under condition (C2). Thus the asymptotic normality of is derived by Lindeberg Theorem, and it holds that

It together with (3.6) follows that

| (3.13) |

where

Combining the results of (3.8) and (3.13), the theorem is proved. ∎

Theorem 3.1 and 3.2 show that the preliminary estimator is consistent and asymptotic normal. However, it’s not efficient due to the fact that the error structure is not taken into account for estimation. On the other side, Li and You, (2020) use it to estimate the error structure and then refine the estimator of with the fitted error structure.

3.2 Asymptotic results on the estimator of the error term

In this section, we discuss the asymptotic property for the estimator of the error term, , which is given by Li and You, (2020). To do so, we need some additional conditions except for conditions (C1)-(C7).

-

(C8)

The function is twice continuously differentiable in with uniformly bounded second ordered derivative, and the root of are bounded away from the unit circle for each .

-

(C9)

As , .

-

(C10)

.

-

(C11)

Remark 3.4.

Condition (C8) guarantees that the approximate stationary time series of around the neighborhood of is causal and satisfies , where , defined in (3.4), is the -th ordered auto-covariance function of . (C9) is the condition to obtain the optimal convergence for the estimator of . Conditions (C10) and (C11) are the same as the ones in Kim, (2001) for the asymptotic normality of time-varying autoregressive coefficient functions.

Theorem 3.3 presents that the asymptotic normality of . To prove it, we first show a proposition for the asymptotic normality of , where is the estimate of with in (2.3) replaced by its true value . Note that this proposition is the same as the i.i.d case in Cai et al., 2000a . Its proof is similar to Theorem 5 of Kim, (2001) and therefore omitted here.

Proposition 3.1.

Theorem 3.3.

Assume that conditions (C1)-(C11) are satisfied, , for any , it holds that

where , is given by (3.4), and

| (3.14) |

Proof.

With Slutsky Theorem, the asymptotic normality can be obtained immediately from (3.15) and Proposition 3.1. Therefore we just prove that

| (3.15) |

Define a matrix and a -dimensional vector as follows,

| (3.16) | ||||

| (3.17) |

where

| (3.18) | ||||

| (3.19) |

So (2.3) can be represented as .

By (3.18), the -th element of is

where is the -th element of and

Similarly, the -th element of is , where is the -th element of and

With the decomposition of and , (3.15) is immediately obtained from the fact that and the two statements below:

-

(i)

-

(ii)

Since the proof for (i) is similar as (ii), here we only demonstrate (ii).

Note that on the compact support of , thus we only present the proof for the case .

Next we prove that .

By (C1), it’s easy to show that

On the other hand, notice that , we only need to show for . We have

Thus Similarly it holds that . Then argument (ii) holds. The proof is completed. ∎

Proposition 3.1 and Theorem 3.3 show that the estimator has the same convergence rate and the asymptotic distribution as the estimator when is observable as shown in Kim, (2001). Moreover, for the case that the order of error series is unknown, Li and You, (2020) proposed the estimate of and , viz., and respectively, which are used to identify the coefficient functions and the constant coefficients. Theorem 3.4 shows that and can identify the true model consistently. To prove it, we first present some lemmas.

Lemma 3.2.

Assume that conditions (C1)-(C11) are satisfied. defined in (3.4) is nonsingular for all and has uniformly bounded second derivatives. When , and as , we have

where and is the norm.

Proof.

The result of Lemma 3.2 can be directly derived from

| (3.20) |

To prove (3.20), we firstly define a ball . By Fan and Li, (2001), we only need to show that for any , there exists which doesn’t depend on such that

| (3.21) |

Let . For any , by definition of , we have

By some simple calculation, we have

Note that by Theorem 3.1, it holds that , which follows that

| (3.22) | ||||

| (3.23) |

Then we have

Let and , where denotes the minimal eigenvalue of matrix , and

Then

where

Similar with (3.2), we can show that

| (3.24) |

Note that is nonsingular, it holds that . Hence, by the definition of and and (3.24), .

On the other side, it follows from condition (C1) and Lemma 6.1 of Fan and Yao, (2008) that

| (3.25) |

Note that and converge in probability to a positive constant respectively, which implies that

| (3.26) |

So it follows from (3.25) and (3.26) that . Therefore, as long as the constant is large enough, the value of is positive, which implies that . Thus (3.21) holds, which means that there exists a minimum in the ball for any with probability . Therefore the minimizer of must satisfy that . The proof is completed.

∎

Lemma 3.3.

Assume that conditions (C1)-(C11) are satisfied. defined in (3.4) is nonsingular for all and has uniformly bounded second derivatives. When , , , and as , we have

-

(i)

;

-

(ii)

.

Proof.

The proof for (i) is similar to Theorem 2 in Wang and Kulasekera, (2012). One difference is that the equations contain can be easily handled by using equation (3.22) and (3.23), another is that Theorem 1 of Wang and Kulasekera, (2012) are replaced by Lemma 3.2 in our case.

The consistency of and in (ii) is implied from (i). ∎

Theorem 3.4.

Assume conditions (C1)-(C11) are satisfied. defined in (3.4) is nonsingular for all and has uniformly bounded second derivatives, then it holds that

Proof.

The proof is similar with the i.i.d. case in Wang and Kulasekera, (2012), we show the procedure briefly and omit the details. Denote as the th component of . Let and . Then Theorem 3.4 is equivalent to . By (ii) of Lemma 3.3, we know that as , satisfies that .

Then, we can divide into three sets, i.e., , , and , corresponding to overfitted case, underfitted case, and correctly fitted case, respectively. The rest of the proof can be finished by mimicking the proof of Theorem 4 in Wang and Kulasekera, (2012), where Theorem 3 of in Wang and Kulasekera, (2012) are replaced by Lemma 3.3 in our case. ∎

In practice some data driven methods like grid search can be used to determine the tuning parameters . Actually, is also allowed and it can save much computation cost according to the condition of Lemma 3.3. Moreover, we can set in (2.4) if we only focus on the purpose of identifying the nonzero coefficients.

3.3 Asymptotic results on the refined estimator of

With the estimator of the error structure, , Li and You Li and You, (2020) derived a refined estimator of , which is denoted as . Theorem 3.5 presents the asymptotic property of and show that is more efficient than the preliminary estimator .

Theorem 3.5.

Proof.

(i) Following the same way as the proof of Theorem 3.2, we can easily show that

(iv) Condition (C8) implies that there exist some constant such that for all , then

By the standard results from density estimation, it holds that .

Combining the results of (i)-(iv), we have that

∎

Remark 3.5.

There are two bandwidths and in the procedure of estimating . Theorem 3.5 shows that the bandwidth in the refined estimator should be of the standard order of estimating a binary nonparametric function. However, the bandwidth for the preliminary estimator should be of smaller order to control the bias in the first step of the estimation. Specially, to ensure the optimal convergence rate of the estimators of the error autoregressive structure as shown in Theorem 3.3, the order of should be even smaller than the bandwidth , i.e., . In practice, standard bandwidth selection methods can be utilized for and . Then can be multiplied by a constant like 0.5 to obtain as suggested by Liu et al., (2010).

4 Numerical studies

Li and You, (2020) conducted two real data studies for their proposed method. In order to give an overall evaluation on the finite sample performance of their proposed method, two simulation studies are conducted in this section. The Epanechnikov kernel is used throughout this section. In each study, the leave-one-out cross-validation is applied to select the optimal bandwidth for and , and is for the preliminary estimator. Since the results are not very sensitive to the bandwidth, only the case of the optimal bandwidth is reported here.

The first study is designed to compare the performance of the preliminary estimator and the refined estimator of the time-varying nonparametric function.

Example 1.

Assume that the order of the error autoregressive structure is known. is generated by the model

where , and the explanatory variable is generated from a time-varying AR(1) process that is locally stationary, i.e.,

where . The error term is generated by the time-varying autoregressive process , where follows normal distribution , and the time-varying autoregressive coefficient function are specified as follows.

-

Model (a)

;

-

Model (b)

;

-

Model (c)

.

Moreover, the square root of average squared error (RASE) criterion is used to evaluate the performance of the estimators. For an estimator , its RASE is defined as

With , , and being model (a)-(c), the empirical mean values and standard deviations (SD) of RASE based on 500 replications are presented in Table 1. For the comparison purpose, the oracle estimator , which is the local linear estimator of when the time-varying autoregressive error structure is completely known, is also calculated and presented in Table 1.

| Mean | SD | Mean | SD | Mean | SD | |||

|---|---|---|---|---|---|---|---|---|

| Model (a) | 0.5 | 200 | 0.253 | 0.029 | 0.166 | 0.027 | 0.161 | 0.024 |

| 300 | 0.208 | 0.024 | 0.145 | 0.022 | 0.142 | 0.021 | ||

| 400 | 0.182 | 0.020 | 0.136 | 0.019 | 0.135 | 0.018 | ||

| 1.0 | 200 | 0.505 | 0.058 | 0.302 | 0.052 | 0.290 | 0.046 | |

| 300 | 0.415 | 0.047 | 0.248 | 0.042 | 0.242 | 0.037 | ||

| 400 | 0.362 | 0.040 | 0.222 | 0.035 | 0.219 | 0.031 | ||

| Model (b) | 0.5 | 200 | 0.312 | 0.048 | 0.189 | 0.040 | 0.161 | 0.024 |

| 300 | 0.260 | 0.041 | 0.165 | 0.035 | 0.142 | 0.021 | ||

| 400 | 0.231 | 0.031 | 0.154 | 0.027 | 0.135 | 0.018 | ||

| 1.0 | 200 | 0.624 | 0.096 | 0.351 | 0.080 | 0.290 | 0.046 | |

| 300 | 0.519 | 0.081 | 0.292 | 0.070 | 0.242 | 0.037 | ||

| 400 | 0.459 | 0.062 | 0.262 | 0.055 | 0.219 | 0.032 | ||

| Model (c) | 0.5 | 200 | 0.366 | 0.079 | 0.193 | 0.047 | 0.161 | 0.024 |

| 300 | 0.322 | 0.074 | 0.162 | 0.035 | 0.142 | 0.021 | ||

| 400 | 0.298 | 0.070 | 0.149 | 0.029 | 0.135 | 0.018 | ||

| 1.0 | 200 | 0.732 | 0.159 | 0.359 | 0.098 | 0.290 | 0.046 | |

| 300 | 0.643 | 0.148 | 0.286 | 0.073 | 0.242 | 0.037 | ||

| 400 | 0.593 | 0.141 | 0.251 | 0.061 | 0.219 | 0.032 | ||

From Table 1, we can draw the following conclusions:

-

•

Under all of three error term models, the refined estimator has both smaller mean values and standard deviations of RASE than the preliminary estimator . The improvement of is getting more significant as the complexity of the error term increases.

-

•

An increase in results in a decrease in the mean values and standard deviations of RASE for all estimators. An increase in results in an increase in the mean values and standard deviations of RASE for all estimators.

-

•

The performance of the refined estimator is very close to , which is also consistent with the theoretical results.

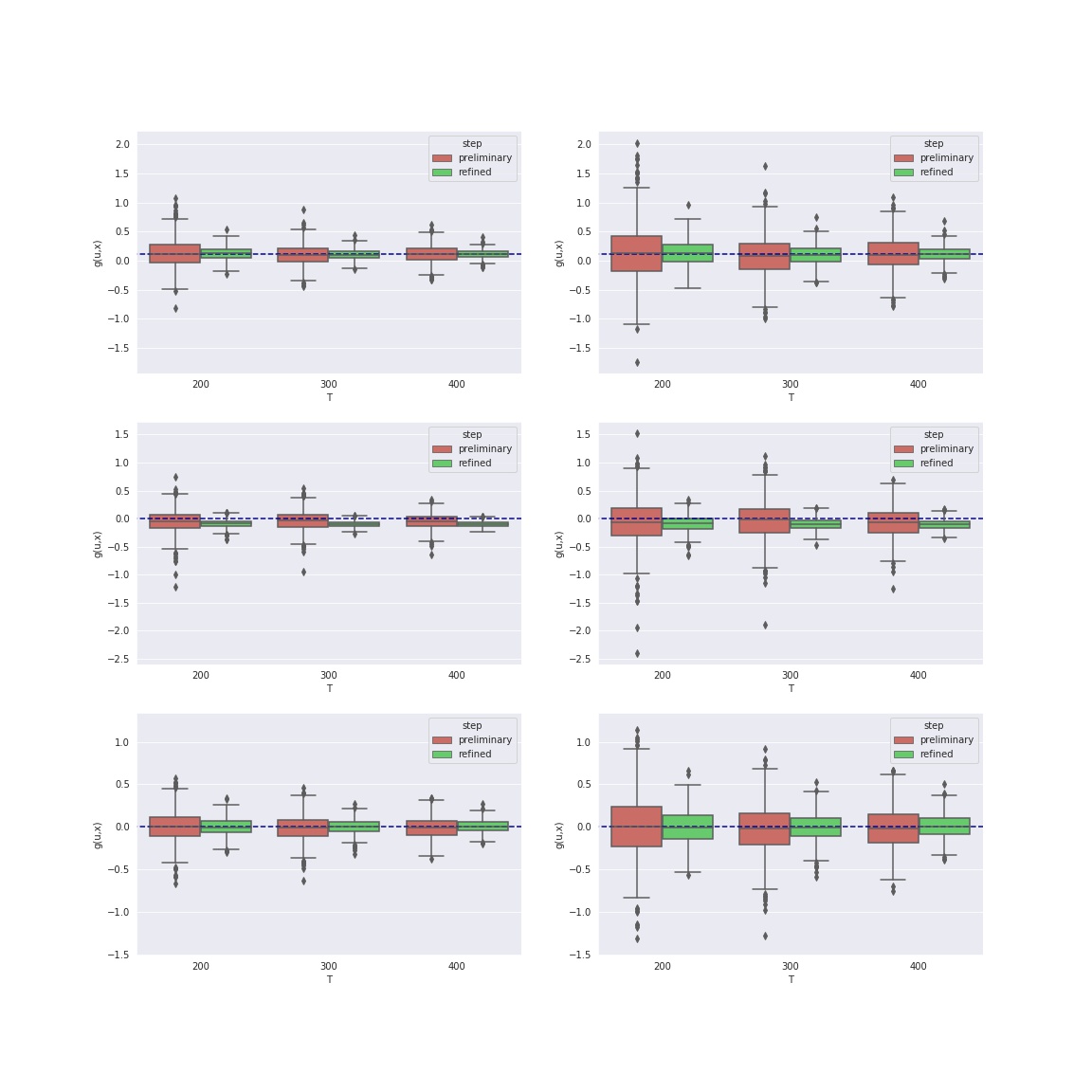

Figure 1 depicts the boxplots of and at points under Model (b). It shows that the standard error is decreasing with the increase of , and the bias is negligible when is large, which is claimed by Theorem 3.5.

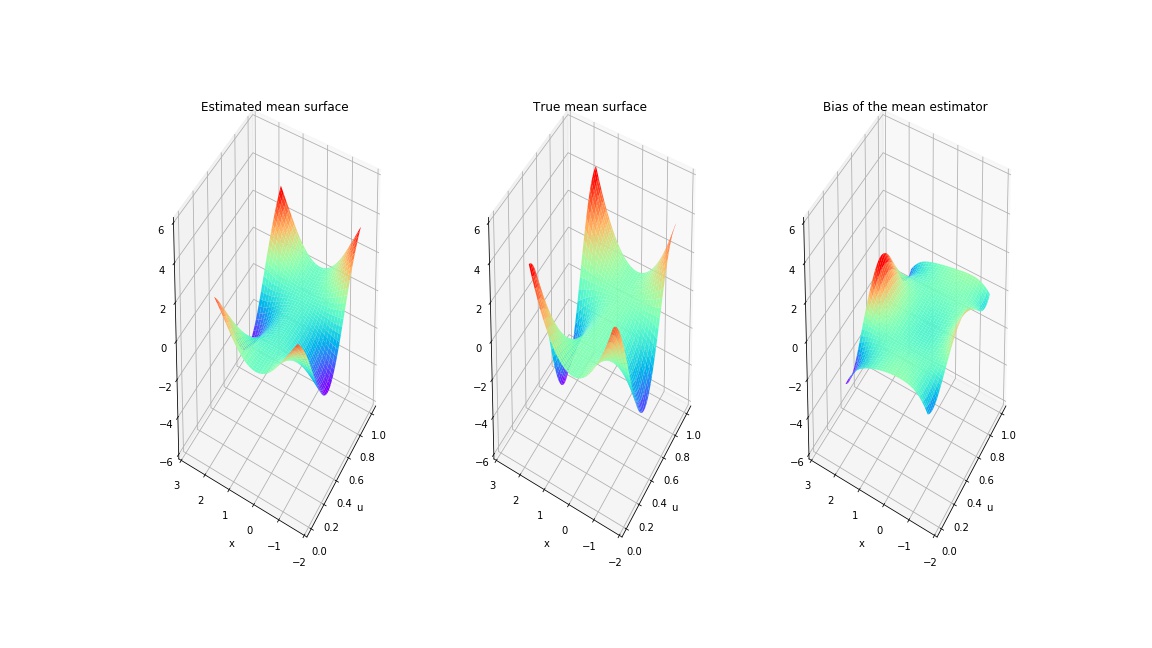

To further illustrate the performance of the refined estimator, we plot the average refined estimated function, the true function, and the bias of the average estimated function in Figure 2 for case (a) with and . The estimated surface is consistent with the true surface, which validate the theoretical results. We omit the results for other cases, which are similar.

Example 2.

In this example, we aim to show the performance of the ULASSO estimator. The model settings and simulation settings are the same as in Example 1 except that the order of the error autoregressive structure is unknown. It’s obvious that Model (a) is a tvAR(1) with ; Model (b) is a tvAR(2) with and ; Model (c) is a tvAR(2) with .

Under the assumption that the order of the error autoregressive structure is unknown, the ULASSO estimator is adopted to estimate the autoregressive structure. is denoted as the optimal ULASSO estimate of which the shrinkage parameters are determined by the BIC criterion (2.5). To evaluate the performance of ULASSO estimate, the result of variable selection (VS, i.e. nonzero coefficient selection) is classified as Wang and Kulasekera, (2012): 1. underfitted (at least one true nonzero variable is missing); 2. correctly fitted; 3. overfitted (all the significant variables are identified while at least one spurious variable is included). The percentages in each category are presented under the heading ‘VS’ in Table 2. Similarly, we can partition the results for detecting the true coefficient functions and constant coefficient into these categories. Therefore, a correct selection means that the procedure identified both types correctly, an underfitted indicating missing at least one true function or a coefficient etc. These percentages are given under the heading ‘VS & CI’ in Table 2.

From Table 2, we can see that for every model, the percentage of correctly fitted models is satisfying and it increases steadily with the sample size. Furthermore, the percentage of correct selection (VS & CI) is also acceptable, especially when the sample size is moderate or large. On the other hand the percentage of VS & CI is slightly less than that of VS. This is not surprising since the convergence speed of the derivative is a little slower than that of the coefficient function.

| VS | VS CI | |||||||

|---|---|---|---|---|---|---|---|---|

| Under | Correct | Over | Under | Correct | Over | |||

| Model (a) | 0.5 | 200 | 0.050 | 0.872 | 0.078 | 0.182 | 0.734 | 0.084 |

| 300 | 0.006 | 0.916 | 0.078 | 0.030 | 0.888 | 0.082 | ||

| 400 | 0.000 | 0.962 | 0.038 | 0.008 | 0.952 | 0.040 | ||

| 1.0 | 200 | 0.206 | 0.724 | 0.070 | 0.294 | 0.626 | 0.080 | |

| 300 | 0.048 | 0.880 | 0.072 | 0.064 | 0.856 | 0.080 | ||

| 400 | 0.000 | 0.938 | 0.062 | 0.004 | 0.928 | 0.068 | ||

| Model (b) | 0.5 | 200 | 0.088 | 0.712 | 0.200 | 0.274 | 0.496 | 0.230 |

| 300 | 0.024 | 0.802 | 0.174 | 0.092 | 0.692 | 0.216 | ||

| 400 | 0.000 | 0.890 | 0.110 | 0.020 | 0.846 | 0.134 | ||

| 1.0 | 200 | 0.114 | 0.672 | 0.214 | 0.314 | 0.454 | 0.232 | |

| 300 | 0.028 | 0.790 | 0.182 | 0.100 | 0.688 | 0.212 | ||

| 400 | 0.000 | 0.870 | 0.130 | 0.026 | 0.820 | 0.154 | ||

| Model (c) | 0.5 | 200 | 0.172 | 0.480 | 0.348 | 0.208 | 0.404 | 0.388 |

| 300 | 0.006 | 0.608 | 0.386 | 0.006 | 0.554 | 0.440 | ||

| 400 | 0.002 | 0.694 | 0.304 | 0.004 | 0.650 | 0.346 | ||

| 1.0 | 200 | 0.192 | 0.450 | 0.358 | 0.234 | 0.382 | 0.384 | |

| 300 | 0.006 | 0.570 | 0.424 | 0.008 | 0.528 | 0.464 | ||

| 400 | 0.004 | 0.664 | 0.332 | 0.006 | 0.602 | 0.392 | ||

To further evaluate the ULASSO estimate, the mean values and standard deviations of RASE of are calculated and presented in Table 3. Moreover, the performance of constant coefficient estimation for in Model (b) is also evaluated. If it is identified as the constant, i.e., , the estimate of is taken as the mean of estimate at each time point, i.e.,

The bias and the standard error (SE) of are included in the last two columns of Table 3. It shows from Table 3 that under all of three error term models, an increase in results in a decrease in the mean values and standard deviations of RASE for all estimates. An increase in results in an increase in the mean values and standard deviations of RASE. Moreover, for the constant coefficient estimation for Model (b), the bias and the standard error of also decreases with the increase of . From Table 3, we can conclude that the performance of the estimates for both time-varying coefficient function and the non-zero constant coefficient are satisfying.

| RASE | estimate | |||||||

| mean | SD | mean | SD | bias | SE | |||

| Model (a) | 0.5 | 200 | 0.260 | 0.066 | ||||

| 300 | 0.223 | 0.047 | ||||||

| 400 | 0.189 | 0.038 | ||||||

| 1.0 | 200 | 0.279 | 0.089 | |||||

| 300 | 0.228 | 0.060 | ||||||

| 400 | 0.205 | 0.034 | ||||||

| Model (b) | 0.5 | 200 | 0.200 | 0.047 | 0.136 | 0.075 | 0.094 | 0.107 |

| 300 | 0.173 | 0.038 | 0.102 | 0.061 | 0.057 | 0.088 | ||

| 400 | 0.158 | 0.031 | 0.075 | 0.042 | 0.028 | 0.066 | ||

| 1.0 | 200 | 0.206 | 0.056 | 0.149 | 0.078 | 0.116 | 0.108 | |

| 300 | 0.173 | 0.040 | 0.109 | 0.064 | 0.071 | 0.088 | ||

| 400 | 0.162 | 0.032 | 0.081 | 0.045 | 0.040 | 0.068 | ||

| Model (c) | 0.5 | 200 | 0.275 | 0.082 | 0.226 | 0.101 | ||

| 300 | 0.211 | 0.054 | 0.155 | 0.049 | ||||

| 400 | 0.179 | 0.052 | 0.125 | 0.040 | ||||

| 1.0 | 200 | 0.280 | 0.084 | 0.240 | 0.110 | |||

| 300 | 0.223 | 0.055 | 0.155 | 0.052 | ||||

| 400 | 0.194 | 0.054 | 0.127 | 0.041 | ||||

5 Conclusion

In this paper, we focus on the theoretical results of statistical inference for a class nonparametric regression models with time-varying regression function, local stationary regressors and time-varying AR(p) (tvAR(p)) error process (1.1), for which the estimation procedure is studied by Li and You, (2020) with no theoretical discussion. With regard to their estimators, we establish the convergence rate and asymptotic normality of the preliminary estimation of nonparametric regression function, show that their estimator of error term has the same convergence rate and the asymptotic distribution as the estimator when is observable, present the asymptotic property of the refined estimation of nonparametric regression function, and show that is more efficient than the preliminary estimator . In addition, with regard to the ULASSO method for variable selection and constant coefficient detection for error term structure, we show that the ULASSO estimator can identify the true error term structure consistently. Simulation results have been provided to illustrate the finite sample performance of the estimators and validate our theoretical discussion on the properties of the estimators.

The model introduced by Li and You, (2020) is with time-varying AR(p) (tvAR(p)) error process. Actually, it can be extended to the model with time-varying autoregressive moving average model (tvARMA(p,q)), which is also local stationary. The essential thought on this article can be also extended to the estimations under the model with tvARMA(p,q) error term.

Acknowledgements

We would like to express our gratitude to Dr. Jinhong You for his heuristic discussion on the article. Our thanks also go to the referees for their time and comments.

References

- Bellegem and Dahlhaus, (2006) Bellegem, S. V. and Dahlhaus, R. (2006). Semiparametric estimation by model selection for locally stationary processes. Journal of the Royal Statistical Society: Series B, 68:721–746.

- Brockwell and Davis, (2016) Brockwell, P. J. and Davis, R. A. (2016). Introduction to time series and forecasting. Springer-Verlag, New York, 3 edition.

- (3) Cai, Z., Fan, J., and Li, R. (2000a). Efficient estimation and inferences for varying-coefficient models. Journal of the American Statistical Association, 95(451):888–902.

- (4) Cai, Z., Fan, J., and Yao, Q. (2000b). Functional-coefficient regression models for nonlinear time series. Journal of the American Statistical Association, 95(451):941–956.

- Dahlhaus, (1996) Dahlhaus, R. (1996). Asymptotic statistical inference for nonstationary processes with evolutionary spectra. Lecture Notes in Statistics, 115:145–¨C159.

- Fan and Gijbels, (1996) Fan, J. and Gijbels, I. (1996). Local polynomial modelling and its applications. Monographs on Statistics and Applied Probability. Chapman & Hall/CRC.

- Fan and Li, (2001) Fan, J. and Li, R. (2001). Variable selection via nonconcave penalized likelihood and its oracle properties. Journal of the American statistical Association, 96(456):1348–1360.

- Fan and Yao, (2008) Fan, J. and Yao, Q. (2008). Nonlinear time series: nonparametric and parametric methods. Springer Science & Business Media.

- Hansen, (2008) Hansen, B. E. (2008). Uniform convergence rates for kernel estimation with dependent data. Econometric Theory, 24(3):726–748.

- Kim, (2001) Kim, W. (2001). Nonparametric kernel estimation of evolutionary autoregressive processes. Technical report, Discussion Papers, Interdisciplinary Research Project 373: Quantification and Simulation of Economic Processes.

- Li and You, (2020) Li, J. and You, J. (2020). Time-varying nonparametric regression models with the locally stationary error process and its applications in finance. Journal of Applied Statistics and Management, to appear.

- Liu et al., (2010) Liu, J. M., Chen, R., and Yao, Q. (2010). Nonparametric transfer function models. Journal of econometrics, 157(1):151–164.

- Pei et al., (2018) Pei, Y., Huang, T., and You, J. (2018). Nonparametric fixed effects model for panel data with locally stationary regressors. Journal of Econometrics, 202(2):286–305.

- Qiu et al., (2013) Qiu, D., Shao, Q., and Yang, L. (2013). Efficient inference for autoregressive coefficients in the presence of trends. Journal of Multivariate Analysis, 114:40–53.

- Ruppert and Wand, (1994) Ruppert, D. and Wand, M. P. (1994). Multivariate locally weighted least squares regression. The annals of statistics, pages 1346–1370.

- Schröder and Fryzlewicz, (2013) Schröder, A. L. and Fryzlewicz, P. (2013). Adaptive trend estimation in financial time series via multiscale change-point-induced basis recovery.

- Shao and Yang, (2017) Shao, Q. and Yang, L. (2017). Oracally efficient estimation and consistent model selection for auto-regressive moving average time series with trend. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 79(2):507–524.

- Su and Ullah, (2006) Su, L. and Ullah, A. (2006). More efficient estimation in nonparametric regression with nonparametricautocorrelated errors. Econometric Theory, 22:98–126.

- Truong, (1991) Truong, Y. K. (1991). Nonparametric curve estimation with time series errors. Journal of Statistical Planning and Inference, 28(2):167–183.

- Vogt, (2012) Vogt, M. (2012). Nonparametric regression for locally stationary time series. The Annals of Statistics, 40(5):2601–2633.

- Wang and Kulasekera, (2012) Wang, D. and Kulasekera, K. (2012). Parametric component detection and variable selection in varying-coefficient partially linear models. Journal of Multivariate Analysis, 112:117–129.

- Xiao et al., (2003) Xiao, Z., Linton, O. B., Carroll, R. J., and Mammen, E. (2003). More efficient local polynomial estimation in nonparametric regression with autocorrelated errors. Journal of the American Statistical Association, 98:980–992.