Estimating and backtesting risk under heavy tails

Abstract.

While the estimation of risk is an important question in the daily business of banking and insurance, many existing plug-in estimation procedures suffer from an unnecessary bias. This often leads to the underestimation of risk and negatively impacts backtesting results, especially in small sample cases. In this article we show that the link between estimation bias and backtesting can be traced back to the dual relationship between risk measures and the corresponding performance measures, and discuss this in reference to value-at-risk, expected shortfall and expectile value-at-risk.

Motivated by the consistent underestimation of risk by plug-in procedures, we propose a new algorithm for bias correction and show how to apply it for generalized Pareto distributions to the i.i.d. setting and to a GARCH(1,1) time series. In particular, we show that the application of our algorithm leads to gain in efficiency when heavy tails or heteroscedasticity exists in the data.

Key words and phrases:

Keywords: value-at-risk, expected shortfall, estimation of risk capital, bias, risk estimation, backtesting, unbiased estimation of risk measures, generalized Pareto distribution.1. Introduction

Risk measures are a central tool in capital reserve evaluation and quantitative risk management, see McNeil et al. (2015) and references therein. Since efficient statistical estimation procedures for risk are highly important in practice, this aspect of risk measurement recently raised a lot of attention. Already Cont et al. (2010) observed that sensitivities of risk estimations with respect to the underlying data set pose a challenging problem when robustness is considered. Krätschmer et al. (2014) showed that a certain notion of statistical robustness for law-invariant convex risk measures always holds. The backtesting aspect and its relation to elicitability has been discussed in Acerbi and Székely (2014), Davis (2016), and Ziegel (2016), for example. Risk estimation statistical properties are also discussed in Bartl and Tangpi (2020) and Lauer and Zähle (2016, 2017). The latter work also considers the statistical bias of estimators, not to be confused with the risk bias we consider below in Equation (2.2) following Pitera and Schmidt (2018), see also Frank (2016) and Francioni and Herzog (2012) for the necessity to account for the risk bias. Moreover, Yuen et al. (2020) considered extreme value-at-risk in the context of distributionally robust inference.

When the estimation of risk is considered, the majority of the literature focuses on the plug-in approach combined with standard estimation techniques like maximum-likelihood estimation, see Embrechts and Hofert (2014), Krätschmer and Zähle (2017) and references therein. In this context, topics like predictive statistical inference analysis and bias quantification are typically studied in reference to the fit of the whole estimated distribution. Still, for risk measurement purposes, it is also important to measure adequacy and conservativeness of the capital projections directly, e.g. via backtesting. We refer to Nolde and Ziegel (2017) where the importance of such studies is shown in reference to elicitability and backtesting. The aim of this article is to consider this topic in reference to common distributional assumptions including the ones with heavy tails.

In particular, the risk of underestimating the required regulatory capital, which is embedded into the risk estimation process, and theoretical links between risk estimation and backtesting performance should be further studied; see e.g. Bignozzi and Tsanakas (2016) or Gerrard and Tsanakas (2011). To justify this point, let us mention that it was only recently pointed out in Moldenhauer and Pitera (2019) that the standard value-at-risk (VaR) backtesting breach count statistic is in fact a performance measure dual to the VaR family of risk measures as introduced in Cherny and Madan (2009). This shows that the VaR breach count statistic is bound to the VaR family in the same manner like the Sharpe ratio is bound to risk aversion specification in mean-variance portfolio optimization or acceptability indices are bound to coherent risk measures, see Bielecki et al. (2016). This indicates that there should be a direct statistical connection between the way how risk measure estimators are designed and how they perform in backtesting.

In this article, we study this connection by discussing estimation bias in the context of estimating risk and its connection to backtesting performance. We focus on an economic notion of unbiasedness for risk measures which turns out to be important whenever the underlying model needs to be estimated. Unbiasedness in the context of risk measures is the generalization of the well-known statistical unbiasedness to the risk landscape, see Pitera and Schmidt (2018). Also, we refer to Bignozzi and Tsanakas (2016) where a similar approach has been applied to residual risk quantification.

Here, we link the concept of unbiasedness for risk estimators to backtesting and compare the performance of existing estimators to the proposed unbiased counterparts in Gaussian and generalized Pareto distribution (GPD) frameworks. The results presented for value-at-risk and expected shortfall show that plug-in estimators suffer from a systematic underestimation of risk capital which results in deteriorated backtesting performance. While this is true even in an i.i.d. and light-tailed setting, it is more pronounced for heavy tails, small sample sizes, in the presence of heteroscedasticity, and with high confidence levels. Also, we propose a new bias reduction technique that increases the efficiency of value-at-risk and expected shortfall plug-in estimators.

This article is organized as follows. In Section 2 we introduce the theoretical background, while in Section 3 we comment on the relation between risk bias and backtesting. In Section 4 and Section 5 we illustrate this relation for value-at-risk and expected shortfall. Next, in Section 6 we study backtesting in a more general context. In Section 7, we introduce a bootstrapping algorithm for bias reduction. Section 8 illustrates the performance on simulated examples under GPD distribution and shows that the risk bias correction leads to better estimator performance. Concluding remarks are provided in Section 9.

2. The estimation of risk and the associated bias

Consider the risk of a financial position measured by a monetary risk measure . The position’s future P&L is denoted by . The estimation relies on a sample corresponding to historic realizations of the P&L. An estimator of the risk is a measurable function of the historical data, which we denote by . The position is secured by adding the estimated risk to the position and we denote the secured position by

| (2.1) |

Note that is a random variable since both and are random.

Assuming the monetary risk measure is law-invariant, the risk of depends on the underlying distribution of . Let denote the parameter space and let each identify a certain distribution choice; could be infinite-dimensional when linked to a non-parametric framework. For each we denote by the risk measure quantifying the underlying risk (e.g. of ) under . In particular, , where is the true but unknown parameter.

Following Pitera and Schmidt (2018), we call an estimator unbiased if

| (2.2) |

if we want to emphasize the difference to statistical notion of unbiasedness, we use the term risk unbiased instead of unbiased.

The definition of unbiasedness in (2.2) has a direct economic interpretation: the secured position has to be acceptable under all . This quantifies the estimation error arising from and contains the information on the actual risk the holder of the position faces when using the estimator to secure the future financial position . Note this is aligned with the predictive inference paradigm as we quantify the actual risk of the secured future position when using estimated risk for securitization.

We also refer to Bignozzi and Tsanakas (2016), where a concept of residual risk measuring the size of is introduced, and to Francioni and Herzog (2012) where so called probability unbiasedness is introduced – those concepts are consistent with risk unbiasedness in the VaR case.

Remark 2.1 (Relation to statistical bias).

When the risk measure is linear, unbiasedness coincides with statistical bias (up to the sign): indeed, if , then (2.2) is equivalent to

where is the expectation under the parameter . In the i.i.d. case, the arithmetic mean multiplied by turns out to be unbiased, just as in the statistical case. Also the estimator is unbiased, but certainly not an optimal choice. This highlights why additional properties besides unbiasedness are important.

The concept of unbiasedness we study here might be considered as a generalization of the statistical bias to non-linear measures. Moreover, it turns out to be important to require additional properties. For example, consistency or other economic-driven properties such as minimization of the average mean capital reserve could be asked for. We refer to Example 7.3 in Pitera and Schmidt (2018) for further details.

Example 2.2 (Value-at-risk under normality).

Value-at-risk is the most recognised risk measure in both the financial and the insurance industry. For an arbitrary real-valued random variable its value-at-risk at level is given by

| (2.3) |

For the moment consider the simplest case, where are i.i.d. and . Then the true parameter is an element of the parameter space . The true value-at-risk at level of the position given is

| (2.4) |

where is the cumulative standard normal distribution function. We obtain that the value-at-risk of the secured position vanishes, as it should be.

However, since is not known, it needs to be estimated and the picture changes. If we denote by and the maximum-likelihood estimators based on the sample and plug them into Equation (2.4), we obtain the plug-in estimator

| (2.5) |

In comparison to the estimation of a confidence interval in the Gaussian case, where a -distribution arises, it is quite intuitive that the normal quantile should be replaced by a -quantile to capture the uncertainty remaining in the parameter estimates and . Indeed, it is not difficult to see that the unbiased estimator is given by

| (2.6) |

where refers to Student -distribution function with degrees of freedom, see Pitera and Schmidt (2018). Hence, unbiasedness requires that the risk of the position secured by the unbiased estimator vanishes for all , as stated in Equation (2.2). We refer to Section 4.2 for a discussion on how this impacts backtesting results.

As already mentioned, unbiasedness requires that the risk of the secured position is zero in all scenarios, which turns out to be too demanding in some cases. Alternatively we consider also the case where the estimated risk capital is sufficient to insure the risks (but is possibly not the smallest capital choice).

In this regard, we call sufficient if

| (2.7) |

As previously, if we want to emphasize the difference to statistical notion of sufficiency, we will use the term risk sufficient.

2.1. The law-invariant case

The family of risk measures is called law-invariant if we find a function from the convex space of cumulative distribution functions (cdfs) to , such that

for all and all ; here denotes the cdf of under the probability measure associated to . Value-at-risk and expected shortsall are prominent examples. In particular, we get for law-invariant families of risk measures.

Consequently, the law-invariant estimator is unbiased if

| (2.8) |

and sufficient if for all . In the i.i.d. case can be obtained from the convolution of the distribution of with the distribution of the estimator . In the Gaussian case considered in Example 2.2, this representation allowed us to quickly obtain the unbiased estimator in Equation (2.6).

Remark 2.3 (Plug-in estimators).

A common way to estimate risk measures is to use the plug-in procedure (see Example 2.2). In the case of a law-invariant risk measure this can be described as follows: first, estimate the unknown parameter by . Second, plug this estimator into the formula for , i.e. compute

Since the function is typically highly non-linear, finite-sample properties of the estimators are often not inherited by . This provides further motivation for studying unbiasedness of estimators of risk measures.

3. Relation between Backtesting and Bias

The notions of unbiasedness and sufficiency have an intrinsic connection to backtesting. In particular, the backtesting framework representation from Moldenhauer and Pitera (2019) can be placed into the context of risk unbiasedness which we illustrate in the following.

3.1. Backtesting

Backtesting is a well-established procedure of checking the performance of estimations on available data. More precisely, assume we have a sample of observations at hand. We aim at backtestings, each based on a sample of length : first, we compute risk estimators where each risk estimator is based on a historical sample of size , starting at and ending at . The corresponding realization of the associated P&L is given by and the associated secured position (see Equation (2.1)) is given by

| (3.1) |

Furthermore, we denote by the sample for the backtestings. Sometimes, if we want to underline the dependence of on the underlying estimator , we write instead of .

Remark 3.1 (Properties of ).

Even if the initial sample satisfies the i.i.d. assumption, the associated secured position will no longer be i.i.d. Indeed, if we write Equation (3.1) in full detail, i.e.

| (3.2) |

it becomes obvious that depends on to , such that and depend on an overlapping sample and, hence, independence is lost in general. Still, the majority of the backtesting statistics ignore this fact and assume that is equal to the true (but unknown) risk. In this case would be constant, hence would only depend on and so would be independent of .

The typical approach to backtesting is the so called traffic light approach and we refer to Section 4 where this is discussed in reference to regulatory VaR backtesting.

The key to the targeted duality is the observation that value-at-risk and expected shortfall are risk measures indexed by the confidence level . More generally, consider a family of monetary risk measures indexed by a parameter , such that the family is monotone and law-invariant: that is, every member of the family is given by a distribution-based risk measure and for any distribution and such that , we have

The typical task is to provide the (daily) risk estimations for some pre-defined reference risk level , e.g. or . The goal of backtesting is to validate the estimation methodology by quantifying the performance of the estimates using the sample of secured positions .

A natural choice for the objective function in the validation procedure is the performance measure that is dual to the family in the sense of Cherny and Madan (2009). Here, we concentrate on the empirical counterpart of the dual performance measure which is obtained by replacing the unknown distribution by its empirical counterpart. More precisely, we introduce a dual empirical performance measure of the secured position in reference to the family given by

| (3.3) |

where is the empirical plug-in risk estimator based on the empirical distribution for sample of length . Intuitively speaking, in (3.3) we look for the smallest value of that makes the secured sample acceptable in terms of the empirical estimators .

Remark 3.2 (Types of backtests).

In the literature, there is no unanimous definition of backtesting and there exist multiple performance evaluation frameworks. In this article, we follow the regulatory backtesting framework whose main aim is to assess secured position conservativeness, see e.g. BCBS (1996). Note that this is essentially different from comparative backtesting based on elicitability, when the overall fit is assessed, see Gneiting (2011). In other words, regulatory backtests are focused on risk underestimation, while comparative backtests penalize both underestimation and overestimation. Also, we focus on the unconditional coverage backtesting as the size and independence of breaches are typically assessed visually, see McNeil (1999) for conditional coverage tests including Christoffersen’s test.

3.2. The relation to bias

Next, we analyze the connection between the backtesting function introduced in (3.3) and bias. First, the inner part of Equation (3.3), , is the empirical counterpart of (risk) sufficiency. Consequently, if the risk estimator is sufficient, one expects not to exceed the reference level which should in turn indicate good performance of the secured position. Second, the minimum in (3.3) is achieved for for which the empirical equivalent of risk unbiasedness is satisfied. Thus, for an unbiased estimator, the value of should be close to the reference threshold value . Consequently, one would expect that unbiased estimators perform well in backtesting.

These two observations show that there is a direct relationship between backtesting performance and unbiasedness. For the computation of the empirical bias of one could simply compute the value , where is the reference risk level. Nevertheless, this quantity is difficult to interpret as the net size of bias could vary. For instance, the net bias is not scale invariant and it is proportional to the (current) underlying position size or the current market volatility.

4. The Backtesting of Value-at-risk

The classical regulatory backtest for a value-at-risk (VaR) estimator (recall the definition in Equation (2.3)) counts the empirical number of overshoots and compares it to the expected number of overshoots. More precisely, given the positions secured by the estimator , an overshoot or a breach occurs at time when the position is not sufficiently secured, i.e. when . Hence, it is natural to consider the average breach count measured by the exception rate

| (4.1) |

This measure, or equivalently the non-standardized breach count , is the standard statistic used in regulatory backtesting, see BCBS (2009). Now, it is relatively easy to show that

where corresponds to the empirical VaR at level , the value is the -th order statistic of the data, and the value denotes the integer part of . In other words, (4.1) is a direct application of (3.3) in the VaR context which indicates direct relation between risk bias and backtesting in the VaR framework. See also Equation (6) in Bignozzi and Tsanakas (2016) where the link between risk bias and backtesting in the VaR context is outlined.

4.1. Regulatory backtesting

For regulatory backtesting we consider the traffic-light approach: namely, we use yearly time series ( historical observations) and the estimator is said to be in the green zone, if , in the yellow zone, if , and in the red zone, if . This corresponds to less than five, between five and nine, and ten or more breaches, respectively; we refer to BCBS (1996) for more details.

To show that bias is indeed directly reflected in backtesting we consider two examples in Section 4.2 and Section 4.3, see Gerrard and Tsanakas (2011) for more examples. The presented results will illustrate that the usage of biased risk estimators leads to a systematic underestimation of risk. This important defect becomes more pronounced with heavier tails of the underlying distribution, increased confidence level (i.e. decreasing ), or reduced sample size. Also, it turns out that an existing bias negatively effects the predictive accuracy as defined in Gneiting (2011). For example, it was shown in Section 8.3 in Pitera and Schmidt (2018) that the consistent VaR score of the Gaussian unbiased estimator is better than the score of the standard Gaussian plug-in estimator.

4.2. Backtesting under normality

In this section we show that in the Gaussian setting, many popular VaR risk estimators are biased, even in an asymptotic sense. Assume that the observed sample is an i.i.d realization from a normal distribution with unknown parameters. For simplicity, we fix , , i.e. backtesting on a yearly basis and consider the following four quantities: first, recall from Example 2.2, that the true risk (i.e. the VaR of the underlying distribution) is given by

Of course, the true parameter is only known in simulated scenarios, which we use later for testing the performance of competitive approaches. Note that having identically distributed random variables implies that true risk does not depend on .

Second, if we denote the parameter estimates in backtesting period by , and , we obtain the common plug-in-estimator of the value-at-risk,

| (4.2) |

Third, as stated in Example 2.2, the unbiased estimator of value-at-risk can be computed (see Pitera and Schmidt (2018) for details) and is given by

| (4.3) |

Fourth, it is natural to consider an empirical quantile as the estimator for value-at-risk. We call this estimator the empirical estimator and recall that111To estimate empirical VaR we used the standard quantile function built into R software with default (type 9) setting.

| (4.4) |

We are now ready to perform the backtesting and to illustrate the impact of an existing bias on the estimator’s performance. To this end, we consider a large Gaussian sample, and construct backtests according to Equation (4.1): for the estimators specified by , the average number of exceptions up to time is given by

| (4.5) |

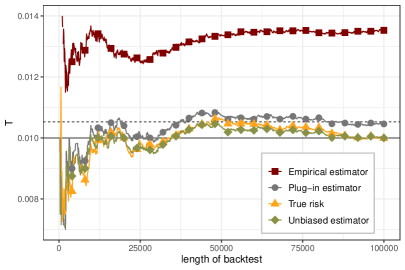

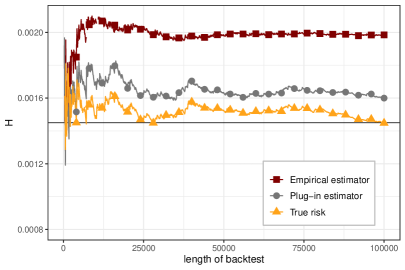

For a numerical illustration we keep the window length of historical data, , fixed and consider . For the case of standard normal random variables (i.e. , ), we plot the results in Figure 1.

Ideally, the value should converge to theoretical reference value when . At first sight a bit surprising, Figure 1 shows that this is neither the case for the plug-in estimator nor the empirical estimator.

However, for the unbiased estimator, and – of course – for the true risk, convergence to the theoretical reference value holds. In fact, the asymptotic exception rate for the plug-in estimator can be directly computed: for , the strong law of large numbers in combination with the continuous mapping theorem implies that

| (4.6) |

where is normally distributed, and the above introduced estimators of mean and standard deviation, both based on a sample of fixed size .

The simulations also show that the asymptotic exception rate of the empirical estimator is surprisingly large and oscillates around 1.35%. This implies serious monitoring consequences: under the correct model setting for VaR at level , the breach probability in the backtest should also be 1%. Then, the probability of reaching the yellow or the red zone (having five or more exceptions in the annual backtest, see Section 4.1) is equal to approximately . On the other hand, if the individual breach probability is equal to 1.35%, the probability of reaching the yellow or the red zone is equal to approximately 25%.222We get and , where is the Bernoulli distribution with trials and probability of success equal to and , respectively. Hence, monitoring the performance by this measure will announce problems with the model two and a half times more often as it should. Intuitively, this is due to a severe underestimation of the risk by the empirical estimator - insufficient capital leads to significantly more overshoots.

If, on the other hand, the length of the estimation window is increased, formally referring to the case , the exception rate converges to also for the empirical and the plug-in estimator, as expected.

Remark 4.1 (Link to predictive inference methods).

The proposed approach leading to the unbiasedness of risk estimators detailed in Equation (2.2) follows the principle of predictive inference propagated amongst others in Billheimer (2019). Instead of focusing on the estimation of parameters, the goal is to predict future observations, or, more precisely, their inherent risk. As in the case of the predictive confidence interval, see (Geisser, 1993, Example 2.2), this implies the change from the Gaussian distribution to the -distribution, which can be spotted in Equations (4.2) and (4.3).

In other words, the unbiased estimator is taking into account the fact that estimated capital will be used to secure a future and risky position and requires that the estimation procedure acknowledges parameter uncertainty.

It seems interesting to note that predictive inference methods can be applied to get unbiased estimators in other settings, i.e. for other distributional families and related estimation techniques. For example, under the Pareto distribution, one can show that while the standard VaR plug-in estimator is (risk) biased, the adjusted estimator , with

is unbiased. For more details, we refer to Gerrard and Tsanakas (2011), where the link between failure probability and uncertainty embedded into parameter estimation is discussed.

4.3. Backtesting under generalized Pareto distributions (GPD)

In the context of heavy tails, a closed-form expression for the unbiased estimator is no longer available and one has to rely on numerical procedures. We introduce such an approach in the following section. We begin by describing the currently existing estimators for generalized Pareto distributions and illustrate their performance.

Consider the i.i.d. setting from Section 3 and assume that follows a GPD (in the left tail) with threshold , shape , and scale ; we also set . In practical applications, the threshold is often considered as known while the parameters and have to be estimated.

Under the assumption of a fixed and known (left tail) distribution it is well-known how to compute the value-at-risk under GPD, we refer to McNeil et al. (2015) for details. Indeed, basic calculations yield the true risk value

where is threshold-adjusted confidence level. Denoting by and (with additional referring to the estimation period) the probability weighted moments (PWM) estimators for and we readily obtain the plug-in estimator for value-at-risk in the GPD case333One could alternatively use different estimation technique to obtain the plug-in estimator, based e.g. on the Maximum Likelihood framework; for most plug-in procedures (that do not take into account predictive inference), the conclusions from this section should apply.,

When the threshold needs to be estimated, we would additionally replace by . Moreover, to numerically asses an existing bias in the estimation, we also consider the empirical estimator , already introduced previously in Equation (4.4).

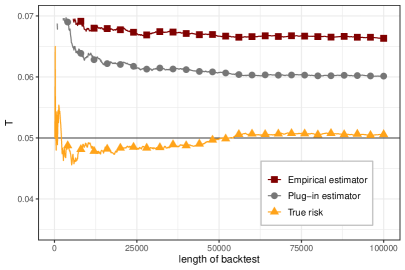

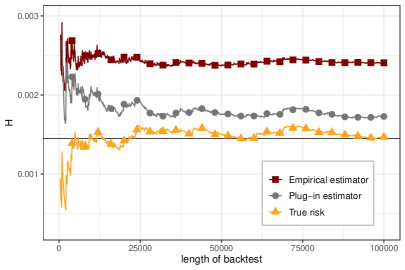

For simplicity, we consider a fixed parameter set , , , and assume conditional sampling. Since only 20% of the data lie beyond the threshold and the observed sample consists only of the data below the threshold, the corresponding periods have to be adjusted accordingly. We consider a learning period of length and adjusted reference level . For , we construct the secured position and perform the backtest according to Equation (4.5). Again, note that for simplicity we have assumed that we are given a consistent set of rolling left-tail observations and ignored non left-tail (above the threshold) inputs. The results are shown in Figure 2.

The figure considers a fixed window size, , together with increasing sample size, i.e. . We observe that the bias vanishes for the true value-at-risk – as expected there is no bias once the true distribution is known. On the contrary, both the plug-in estimator and the empirical estimator show a clear bias. The asymptotic risk level reached by is around 6% (instead of 5%), while for it is even close to 7%. The latter means that in 7% of the observed cases the estimated risk capital is not sufficient to cover the occurred losses which corresponds to a significant underestimation of the present risk.

5. Expected Shortfall backtesting

In this section we show that our observations on bad performance of biased estimators for VaR also hold true for expected shortfall (ES). ES is a well-recognised measure in both the financial and the insurance industry. For a financial position with value-at-risk the expected shortfall at level is given by

| (5.1) |

Since value-at-risk is law-invariant, so is expected shortfall and the associated representation can immediately be obtained from (2.3).

Next, we illustrate the backtesting performance in case of expected shortfall by mimicking the framework introduced in Section 4. The duality-based performance metric based on (3.3) can also be used for ES backtesting. For the sample secured by ES, the empirical mean of the overshooting samples is given by

| (5.2) |

where denotes the th order statistic of . The performance statistic (5.2) simply measures the cumulative breach count and answers a simple question: how many (worst-case) scenarios do we need to consider to know that the aggregated loss does not exceed the aggregated capital reserve, see Moldenhauer and Pitera (2019) for details. As expected, (5.2) is the empirical counterpart of (3.3), i.e. we have

where denotes the empirical expected shortfall at level estimator. As in Section 4.2 and Section 4.3, we show backtesting results for Gaussian and GPD distributions. In both cases, we replace average exception rate statistic with (5.2). Hence, for every estimator in scope, we consider

| (5.3) |

where, for each , the order statistic corresponds to the th order statistic of the associated secured position

and where denotes the -th day estimated expected shortfall risk using estimator .

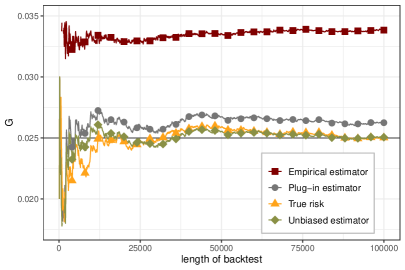

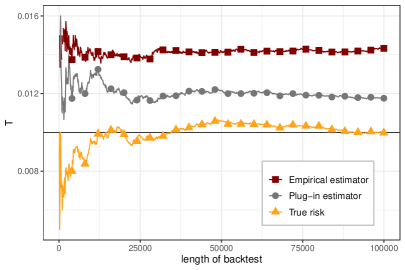

5.1. The Gaussian setting

Under the Gaussian i.i.d. setting introduced in Section 4.2, we consider the same set of estimators, now defined for reference level , with the same learning sample size as before, i.e. . In this setting, we consider true risk, Gaussian plug-in, Gaussian unbiased, and empirical estimators given by

where the constant is obtained using approximation scheme introduced in Example 5.4 in Pitera and Schmidt (2018).

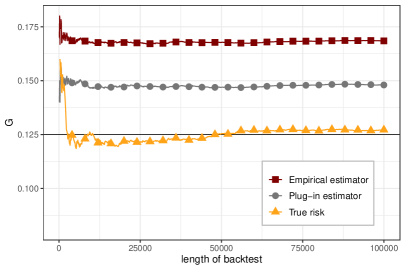

5.2. The GPD setting

Similarly, in the GPD i.i.d. setting introduced in Section 4.3, we consider the empirical estimator as well as the true risk and the plug-in estimators given by

for conditional reference risk level , and conditioned sample size , see McNeil et al. (2015) for details. Note that we need to assume for expected shortfall to be finite.

In both cases we consider the same set of parameters that was used in Section 4.2 and Section 4.3, respectively, and plot values of backtesting statistic . The aggregated results for both normal case and GPD case are presented in Figure 3. As in the value-at-risk case, only the estimator who knows the underlying distribution (true risk) and the Gaussian unbiased estimator show no bias. In all other cases, a significant bias is visible.

6. Backtesting in a general context

While up to now we focussed mainly on value-at-risk and expected shortfall, the link between estimation procedure and backtesting results turns out to be fairly general and can be established for a large class of risk measures. We illustrate this by considering risk measures based on expectiles, see Section 6.1, a family of risk measures which recently gained a lot of attraction due to the fact that it combines coherence with elicitability, see Nolde and Ziegel (2017) for details.

In addition we consider backtesting beyond the i.i.d. case, i.e. extend the considered framework to the heteroscedastic case. For heteroscedastic data, the link between estimation and backtesting performance becomes even more pronounced, especially when the estimation technique is not linked directly to the underlying process dynamics. We provide a high-level illustration in Section 6.2 using a GARCH(1,1) setting.

6.1. Backtesting Expectile Value-at-Risk

For a financial position , its expectile value-at-risk (EVaR) at level is given by

Following Bellini and Di Bernardino (2017), we set the reference threshold to . For EVaR backtesting, given a secured position , we use the distorted Gain-Loss empirical ratio

where is the distortion function and refers to the expectation under the empirical distribution, which immediately implies the right hand side. Note that while the non-distorted gain-loss ratio was suggested in (Bellini and Di Bernardino, 2017, Section 4) as the expectile performance evaluation metric, we decided to apply a distortion to be consistent with the framework introduced in (3.3).

In particular, it is natural to invert the initial ratio as it might be non-stable due to a small population of negative values in . More explicitly, we set

so is looking for a minimal threshold for which is falling into the empirical acceptance set of measure , cf. Equation 4 in Bellini and Di Bernardino (2017) where acceptance sets for EVaR are discussed.

Hence, is a special example of empirical performance measure introduced in (3.3). To illustrate the link between estimation bias and backtesting for EVaR let us mimic the framework introduced in Section 4 for simulated Gaussian and Student data444For simplicity, we decided to use the Student- distribution instead of the GPD distribution used in the previous paragraph. The reason for this is that since EVaR is not a conditional left tail risk measure, one would need to consider also the distribution above the threshold in the GPD setting..

To this end, we pick a large sample of i.i.d. normally distributed random variables and a sample of Student- distributed ones with 5 degrees of freedom , set the learning period to and perform the backtest for true risks, plug-in estimators, and empirical expectile estimators. The values for true risks, , were obtained using the R functions enorm and from expectreg. The plug-in estimator values, , were obtained as in the VaR case, i.e. we estimated underlying parameters (mean, scale, shape) and plugged them in into true risk parametric formulas. The empirical estimator values, , were obtained using the R function expectile from expectreg; the estimation is based on LAWS procedure.

Again, for every estimator in scope, we considered

| (6.1) |

The results for both normal and Student- data are presented in Figure 4. Again, we see a behaviour consistent with the one observed for VaR and ES. No systemic bias is observed only for the true risk estimator, which suggests that the bias presence is in fact linked to estimation procedure framework rather than specific risk measure choice.

6.2. Backtesting in the GARCH(1,1) setting

In this section we adopt the framework introduced in Section 4 to the heteroscedastic case. In this regard, assume that the observed sample of observations denoted by is a realisation from a GARCH(1,1) process following the dynamic

| (6.2) |

where is Gaussian white noise, , , , and . For simplicity, we assume we are given a fixed initial (conditional) standard deviation that is equal to .

The true conditional value-at-risk is obtained by assuming full knowledge of the underlying parameters. Assume we have observed the process until time , the true (conditional) value-at-risk for is given by

| (6.3) |

since . Note that here, , such that the true value-at-risk indeed depends on the parameter and the history of the process.

On the other hand, the associated plug-in estimator is obtained in two steps: first, the parameters are estimated by the quasi-least squares estimators ; see Section II.4.2 in Alexander (2009). Next, is obtained recursively via (6.2) applied to past observations with the estimated parameters and is the estimated process mean. The plug-in estimator then has the form

| (6.4) |

For reference purposes, we also calculate the standard empirical VaR estimator, and report its values. To the best of our knowledge, an unbiased estimator is not available in the GARCH(1,1) context which motivates a numerical procedure for bias reduction which we introduce in the following section.

The values of for are presented in Figure 5. As expected, a positive bias could be identified for both empirical and the plug-in estimator. It should be noted that due to the non-i.i.d. nature of the data, the asymptotic exception rate for the empirical estimator increases in comparison to the Gaussian setting from around 1.35% to around 1.45%. Also, note that the asymptotic exception rate for the plug-in estimator (1.2%) is bigger in comparison to the rate for the Gaussian plug-in estimator (1.05%). Hence, we conclude that for the heteroscedastic setting considered here, the (risk) bias increases due to additional uncertainty encoded in the dependency structure.

7. Bias reduction for plug-in estimators

Our previous findings show that plug-in estimators typically come with a bias implying a negative impact on their backtesting performance. However, in many situations they are the natural starting point for more elaborate estimators, which we will detail now.

For a law-invariant risk measure, the plug-in procedure can be formalized as follows: assume that the distribution of lies in the parametric family and consider a distribution-based risk measure , see Section 2. Then, the plug-in estimator is obtained using the following two steps: first, we estimate the parameter . Second, we plug the estimator into the formula for the risk measure and obtain

Since we expect this estimator to be biased, we introduce a general scheme for improving the efficiency of an existing parametric plug-in estimator. As a motivation, let us revisit the Gaussian case: from Equations (4.3) and (4.2) it may be observed that the unbiased estimator is obtained from the plug-in estimator by changing the parameters according to the mapping

| (7.1) |

where is the underlying sample size. In particular, only a rescaling with respect to the underlying variance takes place and no rescaling with respect to the mean.

This inspires the following procedure for bias-reduction: denote the -dimensional estimated parameter by . We search for a transformation , such that minimizes the bias. In most cases a linear mapping will suffice, and - as noted above - it may also be optimal to change only a few parameters and not all.

In other words, assuming that we aim at finding for which the tweaked plug-in estimator

has the smallest bias; here denotes component-wise multiplication. While a global minimizer might cease to exist, we aim at a local minimization which we introduce now.

7.1. Local bias minimization

In the local bias minimization we consider only a subset which is chosen dependent on the data at hand. For the distribution-based risk measure and some vector we define the maximal risk bias of the estimator on by

| (7.2) |

In particular, if , then is risk sufficient. Indeed, under this condition

for all and hence satisfies (2.7).

The local bias minimizer is the parameter which satisfies

| (7.3) |

and the estimator

| (7.4) |

is the locally risk minimizing estimator. In practice, it will of course not be easy to obtain this estimator and we detail in the following a bootstrap procedure to compute an approximation of .

For completeness, we refer to Bignozzi and Tsanakas (2016), where a similar approach based on absolute risk bias adjustment has been proposed. However, note that the approach proposed in the aforementioned paper is different from ours as it aims to estimate the bias value directly using the bootstrap method; the estimated value is later added to estimated risk to reduce the bias. That saying, for simplified scale-location families those two approaches could produce consistent results. In particular, we note that while in Bignozzi and Tsanakas (2016) the GPD case is not studied, the authors consider the Student -distribution framework and show how to minimize bias in this setting. While the numerical analysis in the cited paper is not directly linked to backtesting or predictive accuracy analysis as in our case (see Section 8), absolute bias reduction oriented studies also indicate improved performance when imposing control on the underlying risk bias (called residual risk therein) e.g. by considering residual add-on or shifting risk measure reference risk level.

7.2. The bootstrapping bias reduction

The most likely parameter after estimation is and we will consider in the following. For simplicity we write and similar for .

We focus on the i.i.d. situation here, where

since will be independent of the past data, and where denotes the convolution of two distributions.

The estimation of will be done on simulated data according to the distribution , which is called bootstrap. The obtained optimal parameter is denoted by and the associated estimator is denoted by

The proposed algorithm is summarized in details in Figure 6.

To illustrate how Algorithm 1 works, let us calculate the value of for two reference VaR cases that were already considered before, i.e. for plug-in normal and plug-in GPD estimators. Inspired by the Gaussian case, (7.1), we apply rescaling only to the scale parameters. We fix the rolling window length to , use i.i.d. samples, and consider VaR at level . In the normal case, we compute univariate and get the adjusted plug-in estimator

for various choices of true and . In the GPD case we consider an exogenous threshold which we set to and consider univariate for the adjusted plug-in estimator

for various exemplary choices of underlying true parameters and . Note that while a linear adjustment is applied in the GPD case, it effectively takes into account values of parameter as the size of is computed locally for each and effectively depends on .

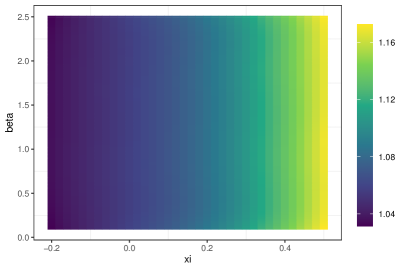

Also, in the GPD case we are using conditioned samples, i.e. 5% denotes the conditioned VaR level. For example, assuming that initial sample size was 250 and 50 observations were negative, this setting would effectively correspond to unconditional threshold . In both cases, we set for bootstrap sampling, and apply the algorithm detailed in Figure 6 on an exemplary representative parameter grid. The results are presented in Figure 7.

Two main conclusions can be made at this stage. First, the local bias adjustment for the normal case does not depend on the underlying parameters and is close to the value presented in (7.1), i.e. we have

Second, in the GPD case, it could be observed that the bias value adjustment looks like an increasing function of . This is in line with intuition as the parameter is used for linear scaling which should not impact (relative) bias adjustment due to positive homogeneity of VaR.

8. Performance of the local bias minimization

In this section we present two examples of the local bias minimization procedures when the underlying returns follow a GPD distribution. For the first case we consider value-at-risk, while for the second we consider expected shortfall.

To asses the performance of the bias reduction, we simulate samples from the GPD families with different parameter settings and compare the performance of the plug-in estimators with its locally unbiased equivalent constructed via a variant of Algorithm 1. For completeness, in both cases we also show the results for true risk and empirical estimators.

The parameter sets we consider are

| (8.1) | ||||||

while the confidence thresholds are equal to , 7.5%, and , respectively. In first two cases the learning period is set equal to , while in the last case it is equal to .

The first setting corresponds to the Student -distribution with 3 degrees of freedom and 20% percentage threshold; the second setting corresponds to parameters calibrated to market data from the S&P500 index – see Table 5 in Gilli and Kellezi (2006); the third setting comes from Table 5 in Moscadelli (2004) and is related to an operational risk framework. Note that in the third set we have which implies that the first moment is infinite. Moreover, in the third case corresponds to the Corporate Finance data set from Gilli and Kellezi (2006), where peaks over the chosen threshold were observed.

For simplicity, in all cases, we fix , estimate and , and rescale only when Algorithm 1 is used. The bootstrap sample size was chosen to be , see Step (2) of Algorithm 1.

Already at this point it is visible that the peaks-over-threshold setting implies a very small number of observations: we have typically around 50 (or even only 42) data points at hand. Given that the underlying distribution has heavy tails (and in the third case additionally a non-existing first moment), a high variance of the parameter estimates and the presence of outliers can be expected. While in theory this could be remedied by increasing , we propose to adjust the bootstrapping algorithm to account for this difficulties and present the adjusted procedure in the following. If the sample size is larger and the underlying distribution has light tails, one may safely proceed as in Pitera and Schmidt (2018), or rely directly on the bootstrapping algorithm presented in Figure 7.2.

To measure the performance of both VaR and ES estimators, we introduce a number of performance metrics. Recall that our inputs are risk estimators , realised P&Ls , and the corresponding secured positions .

8.1. Performance metrics for value-at-risk

For measuring the performance of estimators in the context of value at risk we consider the following five metrics: first, the exception rate defined in (4.1), i.e.

Intuitively, here one would expect that should be close to the reference risk level chosen for the value-at-risk to be estimated.

Second, we consider the mean score statistic based on the quantile strictly consistent scoring function , where corresponds to the risk estimator, denotes the realised P&L, and is the underlying risk level. In our language, the secured position equals such that and we obtain the mean score

The mean score is a common elicitable backtesting statistic used for the comparison of estimator performance, see Gneiting (2011) and Fissler et al. (2015).

Third, we consider the rolling window traffic-light non-green zone backtest statistic NGZ as already mentioned. We fix the length of an additional rolling window to . The number of overshoots in the interval equals and the average Non-Green Zone (NGZ) classifier is defined as

where the exception number is the 95% confidence threshold. Namely, under the correct model, the sequence is i.i.d. Bernoulli distributed with probability of success equal to . Consequently, should be linked to a Bernoulli trial of length with success probability . For example, for and , we get

which would lead to 95% confidence threshold equal to . Hence, in a perfect setting, NGZ should be close to for the first dataset. Using similar reasoning, for the second and the third datasets settings, we get NGZ values equal to approximately 8% and 5%, respectively.

Fourth, we introduce Diebold-Mariano comparative (-)test statistic with unbiased estimator being the reference one. The test statistic is given by

where is the time series of comparative errors between two estimators, is the sample mean comparative error, and is the sample standard deviation of the comparative error, respectively; see Osband and Reichelstein (1985) for details. In the VaR case, the -th day comparative error is given by

where and denote the considered estimators (such as plug-in estimator, empirical estimator, or true risk) and is the consistent scoring function already introduced above.

Finally, we consider the mean and the standard deviation of the estimated regulatory capital. When all other criteria are satisfied, these additional criteria allows to identify the estimator which requires minimal regulatory capital and/or has the smallest statistical bias. We define the mean of risk estimator (MR) and standard deviation of risk estimator (SD) by

| (8.2) |

Note that smaller values of MR indicate that (on average) smaller capital reserves are required. Ideally, this metric should be close to the true risk. Since parameters need to be estimated we expect that this model uncertainty is reflected by an increase in MR.

8.2. Performance metric for expected shortfall

For simplicity, we decided to focus only on the backtesting performance; other conclusions should be similar to VaR. In this regard, we consider the averaged cumulative exception rate defined in (5.2), i.e.

For completeness, we also include results of MR and SD in the ES case.

8.3. Bias reduction for value-at-risk in the GPD framework

For the following data experiment, we consider the three different sets of GPD parameters and estimate VaR using three different (conditional) reference levels. We follow a backtesting rolling window approach with total number of simulations equal to . We consider five different VaR estimators: the empirical estimator (emp), the plug-in GPD estimator (plug-in), the true risk (true), and two bootstrap-based estimators which will be described below.

First, to obtain a suitable reference benchmark for the bootstrapping procedure, we adjust the GPD plug-in estimator by a fixed multiplier that is computed based on true values of and . In this regard, set

| (8.3) |

where is computed using true values of and in the first step of Algorithm 1; note that adjusting by results in (8.3).

Second, we consider an estimator that is computed using the bootstrapping algorithm detailed in Figure 6 applied to each sample separately. We set

| (8.4) |

here is the local bias correction for the estimates and on day .

| Parameters | VaR | NGZ | DM (-value) | MR (SD) | ||||

|---|---|---|---|---|---|---|---|---|

| GPD | emp | 0.050 | 50 | 0.066 | 0.2475 | 0.20 | -11.8 (0.000) | 4.47 (0.92) |

| plug-in | 0.060 | 0.2426 | 0.15 | -0.4 (0.689) | 4.57 (0.78) | |||

| b-true | 0.052 | 0.2425 | 0.08 | — | 4.83 (0.83) | |||

| b | 0.052 | 0.2424 | 0.08 | 2.2 (0.028) | 4.83 (0.80) | |||

| true | 0.051 | 0.2331 | 0.11 | 18.7 (0.000) | 4.61 (0.00) | |||

| GPD | emp | 0.075 | 50 | 0.091 | 0.3140 | 0.13 | -10.7 (0.000) | 4.59 (0.71) |

| plug-in | 0.087 | 0.3101 | 0.12 | -0.5 (0.617) | 4.58 (0.57) | |||

| b-true | 0.078 | 0.3100 | 0.07 | — | 4.76 (0.61) | |||

| b | 0.077 | 0.3097 | 0.07 | 4.4 (0.000) | 4.76 (0.58) | |||

| true | 0.077 | 0.3017 | 0.08 | 18.2 (0.000) | 4.63 (0.00) | |||

| GPD | emp | 0.100 | 42 | 0.119 | 7.2509 | 0.08 | -13.3 (0.000) | 10.57 (7.16) |

| plug-in | 0.124 | 7.2003 | 0.12 | 0.0 (1.000) | 9.08 (4.51) | |||

| b-true | 0.111 | 7.2003 | 0.07 | — | 10.38 (5.19) | |||

| b | 0.111 | 7.1907 | 0.07 | 13.2 (0.000) | 10.30 (4.60) | |||

| true | 0.101 | 7.1175 | 0.05 | 12.0 (0.000) | 9.82 (0.00) |

As already mentioned, in the case with small sample size ( or ) and the presence of heavy tails it is necessary to adjust Algorithm 1 for this. In this regard, we proceed as follows:

-

(1)

To provide a challenging benchmark we realized that in the small sample context it turns out to be useful to allow a small positive bias of the estimator. In this regard, we modified objective function in step (4). Namely, in all cases we allowed a bias equal to 10% of the estimator standard error. For the first two datasets, this corresponds to approximately 1% of the true risk value, while for the third dataset this corresponds to 10% of the true risk value. Note that in the third case we have which increases the standard error significantly.

-

(2)

For the bootstrapping estimator we only took care of outliers: namely, we set (i.e. do not apply any adjustment) if the estimated value of seemed already very high. We chose the case where the estimated plug-in risk was above the 10% upper quantile of the aggregated estimated capital sample . This corresponds to situations, where the size of non-adjusted (above the threshold) estimated risk is already higher than the (above the threshold) true risk by approximately 28% for the first two datasets, and higher than 48% for the third dataset.

The results of the performance analysis are presented in Table 1 and we can make the following observations.

-

(1)

The bootstrapped estimator shows its unbiasedness by reaching an exception rate that is closest to the true risk exception rate. Its values of the mean score and the non-green zone NGZ are also closest to the true risk. Moreover, it outperforms other estimators in the Diebold-Mariano test.

-

(2)

The modification (2) above, applied to the bootstrapping estimator led to the outperformance over the estimator shown in the Diebold-Mariano test statistics (DM). This shows that in the heavy-tail- and small-sample-environment one needs to pay special attention to the bootstrapping bias correction. Intuitively, one needs to robustify the estimating procedure and in particular one should avoid adjusting estimates which already considerably overestimate the underlying risk.

-

(3)

The mean risk of the bootstrapped estimators is typically higher compared to the other estimators showing that biased estimators often underestimate risk.

-

(4)

In the third, extreme case we observe that the empirical estimator performs quite well in terms of the no-green-zone (but not in terms of the other measures). This results from a high capital requirement shown in the mean risk statistic MR.

Summarizing, the above results show that the suggested improved bootstrapping procedure performs very well even in the difficult context considered here with a very small sample size and in the presence of heavy tails. It also complements the asymptotic analysis presented in Section 4 showing that the plug-in procedure indeed underestimates risk in the setting considered here.

8.4. Bias reduction for expected shortfall in the GPD framework

| Parameters | ES | MR (SD) | |||

|---|---|---|---|---|---|

| GPD | emp | 0.050 | 50 | 0.100 | 6.14 (1.83) |

| plug-in | 0.078 | 6.73 (2.01) | |||

| b-true | 0.050 | 7.88 (2.41) | |||

| b | 0.057 | 7.66 (2.22) | |||

| true | 0.051 | 6.70 (0.00) | |||

| GPD | emp | 0.075 | 50 | 0.136 | 6.80 (2.40) |

| plug-in | 0.121 | 7.08 (2.44) | |||

| b-true | 0.079 | 8.35 (3.08) | |||

| b | 0.092 | 8.03 (2.65) | |||

| true | 0.077 | 7.07 (0.00) |

In this section we consider expected shortfall instead of value-at-risk. Expected shortfall is much more sensitive to heavy tails, such that a priori we can expect an even clearer picture.

To this end, we consider the first two parameter sets from Equation (8.1). Note that in the third dataset we have which implies an exploding first moment, such that expected shortfall is no longer finite. The results are presented in Table 2 and the following observations can be made:

-

(1)

The bias adjustment for expected shortfall is large in comparison to the adjustment in the value-at-risk case, computed for the same confidence threshold . This is visible through the increased mean risk MR.

-

(2)

The performance (measured in terms of ) for empirical and plug-in estimators is significantly worse in comparison to the bootstrapped estimator, since the former tend to underestimate the risk. This is in line with the results presented for the VaR case.

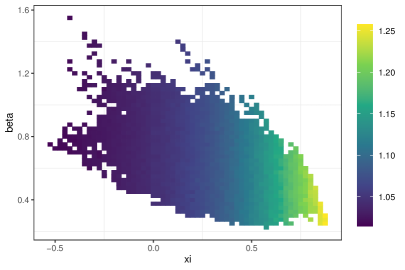

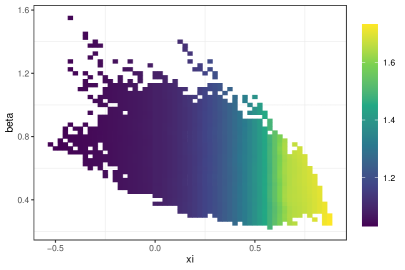

Additionally, we illustrate the effect from observation (1) with a plot showing value-at-risk and expected shortfall bias adjustments computed for all estimated parameter values for the second dataset, see Figure 8. Note that the these results are in perfect agreement with results in Figure 7, i.e. is the main bias determination driver.

9. Conclusion

Our experiments show that plug-in estimators of risk capital typically suffer from an underestimation of risk. We could show that this effect is more pronounced when heavy tails are present, the sample size is small or heteroscedasticity drives the underlying process. This underestimation is measurable by backtests, and we analyzed a number of backtests related to value-at-risk, expected shortfall or risk measures based on expectiles. Moreover, we suggest a new bias reduction technique based on a bootstrap procedure which increases the efficiency of plug-in estimators. Our findings highlight that predictive inference in reference to the estimation of risk and risk bias is an interesting topic that requires further studies, especially in non-i.i.d. settings.

Acknowledgements

The first author acknowledges support from the National Science Centre, Poland, via project 2016/23/B/ST1/00479. The second author acknowledges support from the Deutsche Forschungsgemeinschaft under the grant SCHM 2160/13-1.

References

- (1)

- Acerbi and Székely (2014) Acerbi, C. and Székely, B. (2014), ‘Back-testing expected shortfall’, Risk magazine (November).

- Alexander (2009) Alexander, C. (2009), Market Risk Analysis: Practical Financial Econometrics, Vol. 2, John Wiley & Sons.

- Bartl and Tangpi (2020) Bartl, D. and Tangpi, L. (2020), ‘Non-asymptotic rates for the estimation of risk measures’, preprint, arXiv:2003.10479 .

- BCBS (1996) BCBS (1996), Supervisory framework for the use of ’backtesting’ in conjunction with the internal models approach to market risk capital requirements, Technical report, Basel Committee on Banking Supervision, Bank for International Settlements.

- BCBS (2009) BCBS (2009), Fundamental review of the trading book: A revised market risk framework - Consultative document, Technical report, Bank for International Settlements, Basel Committee on Banking Supervision.

- Bellini and Di Bernardino (2017) Bellini, F. and Di Bernardino, E. (2017), ‘Risk management with expectiles’, The European Journal of Finance 23(6), 487–506.

- Bielecki et al. (2016) Bielecki, T. R., Cialenco, I., Drapeau, S. and Karliczek, M. (2016), ‘Dynamic assessment indices’, Stochastics 88(1), 1–44.

- Bignozzi and Tsanakas (2016) Bignozzi, V. and Tsanakas, A. (2016), ‘Parameter uncertainty and residual estimation risk’, Journal of Risk and Insurance 83(4), 949–978.

- Billheimer (2019) Billheimer, D. (2019), ‘Predictive inference and scientific reproducibility’, The American Statistician 73(sup1), 291–295.

- Cherny and Madan (2009) Cherny, A. S. and Madan, D. B. (2009), ‘New measures for performance evaluation’, The Review of Financial Studies 22(7), 2571–2606.

- Cont et al. (2010) Cont, R., Deguest, R. and Scandolo, G. (2010), ‘Robustness and sensitivity analysis of risk measurement procedures’, Quantitative Finance 10(6), 593–606.

- Davis (2016) Davis, M. (2016), ‘Verification of internal risk measure estimates’, Statistics & Risk Modeling 33, 67–93.

- Embrechts and Hofert (2014) Embrechts, P. and Hofert, M. (2014), ‘Statistics and quantitative risk management for banking and insurance’, Annual Review of Statistics and Its Application 1, 493–514.

- Fissler et al. (2015) Fissler, T., Ziegel, J. F. and Gneiting, T. (2015), ‘Expected shortfall is jointly elicitable with value at risk - implications for backtesting’, Risk magazine (December).

- Francioni and Herzog (2012) Francioni, I. and Herzog, F. (2012), ‘Probability-unbiased value-at-risk estimators’, Quantitative Finance 12(5), 755–768.

- Frank (2016) Frank, D. (2016), ‘Adjusting var to correct sample volatility bias’, Risk magazine (October).

- Geisser (1993) Geisser, S. (1993), ‘Predictive Inference: An Introduction’.

- Gerrard and Tsanakas (2011) Gerrard, R. and Tsanakas, A. (2011), ‘Failure probability under parameter uncertainty’, Risk Analysis: An International Journal 31(5), 727–744.

- Gilli and Kellezi (2006) Gilli, M. and Kellezi, E. (2006), ‘An application of extreme value theory for measuring financial risk’, Computational Economics 27(2-3), 207–228.

- Gneiting (2011) Gneiting, T. (2011), ‘Making and evaluating point forecasts’, Journal of the American Statistical Association 106(494), 746–762.

- Krätschmer et al. (2014) Krätschmer, V., Schied, A. and Zähle, H. (2014), ‘Comparative and qualitative robustness for law-invariant risk measures’, Finance and Stochastics 18(2), 271–295.

- Krätschmer and Zähle (2017) Krätschmer, V. and Zähle, H. (2017), ‘Statistical inference for expectile-based risk measures’, Scandinavian Journal of Statistics 44(2), 425–454.

- Lauer and Zähle (2016) Lauer, A. and Zähle, H. (2016), ‘Nonparametric estimation of risk measures of collective risks’, Statistics & Risk Modeling 32(2), 89–102.

- Lauer and Zähle (2017) Lauer, A. and Zähle, H. (2017), ‘Bootstrap consistency and bias correction in the nonparametric estimation of risk measures of collective risks’, Insurance: Mathematics and Economics 74, 99–108.

- McNeil (1999) McNeil, A. J. (1999), ‘Extreme value theory for risk managers’, Internal Modelling and CAD II published by RISK Books pp. 93–113.

- McNeil et al. (2015) McNeil, A. J., Frey, R. and Embrechts, P. (2015), Quantitative risk management: concepts, techniques and tools-revised edition, Princeton university press.

- Moldenhauer and Pitera (2019) Moldenhauer, F. and Pitera, M. (2019), ‘Backtesting expected shortfall: a simple recipe?’, Journal of Risk 22(1).

- Moscadelli (2004) Moscadelli, M. (2004), ‘The modelling of operational risk: experience with the analysis of the data collected by the basel committee’, Technical Report 517, Banca d’Italia .

- Nolde and Ziegel (2017) Nolde, N. and Ziegel, J. F. (2017), ‘Elicitability and backtesting: Perspectives for banking regulation’, The annals of applied statistics 11(4), 1833–1874.

- Osband and Reichelstein (1985) Osband, K. and Reichelstein, S. (1985), ‘Information-eliciting compensation schemes’, Journal of Public Economics 27(1), 107–115.

- Pitera and Schmidt (2018) Pitera, M. and Schmidt, T. (2018), ‘Unbiased estimation of risk’, Journal of Banking & Finance 91, 133–145.

- Yuen et al. (2020) Yuen, R., Stoev, S. and Cooley, D. (2020), ‘Distributionally robust inference for extreme value-at-risk’, Insurance: Mathematics and Economics 92, 70–89.

- Ziegel (2016) Ziegel, J. F. (2016), ‘Coherence and elicitability’, Mathematical Finance 26, 901–918.