Distributionally Robust Parametric

Maximum Likelihood Estimation

Abstract

We consider the parameter estimation problem of a probabilistic generative model prescribed using a natural exponential family of distributions. For this problem, the typical maximum likelihood estimator usually overfits under limited training sample size, is sensitive to noise and may perform poorly on downstream predictive tasks. To mitigate these issues, we propose a distributionally robust maximum likelihood estimator that minimizes the worst-case expected log-loss uniformly over a parametric Kullback-Leibler ball around a parametric nominal distribution. Leveraging the analytical expression of the Kullback-Leibler divergence between two distributions in the same natural exponential family, we show that the min-max estimation problem is tractable in a broad setting, including the robust training of generalized linear models. Our novel robust estimator also enjoys statistical consistency and delivers promising empirical results in both regression and classification tasks.

1 Introduction

We are interested in the relationship between a response variable and a covariate governed by the generative model

| (1) |

where is a pre-determined function that maps the weight and the covariate to the parameter of the conditional distribution of given . The weight is unknown and is the main quantity of interest to be estimated. Throughout this paper, we assume that the distribution belongs to the exponential family of distributions. Given a ground measure on , the exponential family is characterized by the density function

with respect to , where denotes the inner product, is the natural parameters, is the log-partition function and is the sufficient statistics. The space of natural parameters is denoted by . We assume that the exponential family of distributions is regular, hence is an open set, and are affinely independent [5, Chapter 8].

The generative setting (1) encapsulates numerous models which are suitable for regression and classification [17]. It ranges from logistic regression for classification [26], Poisson counting regression [25], log-linear models [15] to numerous other generalized linear models [17].

Given data which are assumed to be independently and identically distributed (i.i.d.) following the generative model (1), we want to estimate the true value of that dictates (1). If we use to denote the empirical distribution supported on the training data, and define as the log-loss function with the parameter mapping

| (2) |

then the maximum likelihood estimation (MLE) produces an estimate by solving the following two equivalent optimization problems

| (3a) | ||||

| (3b) | ||||

The popularity of MLE can be attributed to its consistency, asymptotic normality and efficiency [45, Section 5]. Unfortunately, this estimator exhibits several drawbacks in the finite sample regime, or when the data carry high noise and may be corrupted. For example, the ML estimator for the Gaussian model recovers the sample mean, which is notoriously susceptible to outliers [38]. The MLE for multinomial logistic regression yields over-fitted models for small and medium sized data [16].

Various strategies can be utilized to counter these adverse effects of the MLE in the limited data regime. The most common approach is to add a convex penalty term such as a 1-norm or 2-norm of into the objective function of problem (3a) to obtain different regularization effects, see [35, 30] for regularized logistic regression. However, this approach relies on strong prior assumptions, such as the sparsity of for the 1-norm regularization, which may rarely hold in reality. Recently, dropout training has been used to prevent overfit and improve the generalization of the MLE [43, 46, 47]. Specific instances of dropout have been shown to be equivalent to a 2-norm regularization upon a suitable transformation of the inputs [46, Section 4]. Another popular strategy to regularize problem (3a) is by reweighting the samples instead of using a constant weight when calculating the loss. This approach is most popular in the name of weighted least-squares, which is a special instance of MLE problem under the Gaussian assumption with heteroscedastic noises.

Distributionally robust optimization (DRO) is an emerging scheme aiming to improve the out-of-sample performance of the statistical estimator, whereby the objective function of problem (3b) is minimized with respect to the most adverse distribution in some ambiguity set. The DRO framework has produced many interesting regularization effects. If the ambiguity set is defined using the Kullback-Leibler (KL) divergence, then we can recover an adversarial reweighting scheme [31, 10], a variance regularization [33, 20], and adaptive gradient boosting [12]. DRO models using KL divergence is also gaining recent attraction in many machine learning learning tasks [21, 41]. Another popular choice is the Wasserstein distance function which has been shown to have strong connections to regularization [40, 29], and has been used in training robust logistic regression classifiers [39, 11]. Alternatively, the robust statistics literature also consider the robustification of the MLE problem, for example, to estimate a robust location parameter [28]

Existing efforts using DRO typically ignore, or have serious difficulties in exploiting, the available information regarding the generative model (1). While existing approaches using the Kullback-Leibler ball around the empirical distribution completely ignore the possibility of perturbing the conditional distribution, the Wasserstein approach faces the challenge of elicitating a sensible ground metric on the response variables. For a concrete example, if we consider the Poisson regression application, then admits values in the space of natural numbers , and deriving a global metric on that carries meaningful local information is nearly impossible because one unit of perturbation of an observation with does not carry the same amount of information as perturbing . The drawbacks of the existing methods behoove us to investigate a novel DRO approach that can incorporate the available information on the generative model in a systematic way.

Contributions. We propose the following distributionally robust MLE problem

| (4) |

which is a robustification of the MLE problem (3b) for generative models governed by an exponential family of distributions. The novelty in our approach can be summarized as follows.

-

•

We advocate a new nominal distribution which is calibrated to reflect the available parametric information, and introduce a Kullback-Leibler ambiguity set that allows perturbations on both the marginal distribution of the covariate and the conditional distributions of the response.

-

•

We show that the min-max estimation problem (4) can be reformulated as a single finite-dimensional minimization problem. Moreover, this reformulation is a convex optimization problem in broadly applicable settings, including the training of many generalized linear models.

-

•

We demonstrate that our approach can recover the adversarial reweighting scheme as a special case, and it is connected to the variance regularization surrogate. Further, we prove that our estimator is consistent and provide insights on the practical tuning of the parameters of the ambiguity set. We also shed light on the most adverse distribution in the ambiguity set that incurs the extremal loss for any estimate of the statistician.

Technical notations. The variables admit values in , and is a finite-dimensional set. The mapping is jointly continuous, and denotes the inner product in . For any set , is the space of all probability measures with support on . We use to denote convergence in probability, and to denote convergence in distribution. All proofs are relegated to the appendix.

2 Distributionally Robust Estimation with a Parametric Ambiguity Set

We delineate in this section the ingredients of our distributionally robust MLE using parametric ambiguity set. Since the log-loss function is pre-determined, we focus solely on eliciting a nominal probability measure and the neighborhood surrounding it, which will serve as the ambiguity set.

While the typical empirical measure may appear at first as an attractive option for the nominal measure, does not reflect the parametric nature of the conditional measure of given . Consequently, to robustify the MLE model, we need a novel construction of the nominal distribution .

Before proceeding, we assume w.l.o.g. that the dataset consists of distinct observations of , each value is denoted by for , and the number of observations with the same covariate value is denoted by . This regrouping of the data by typically enhances the statistical power of estimating the distribution conditional on the event .

We posit the following parametric nominal distribution . This distribution is fully characterized by parameters: a probability vector whose elements sum up to 1 and a vector of nominal natural parameters . Mathematically, satisfies

| (5) |

The first equation indicates that the nominal measure can be decomposed into a marginal distribution of the covariates and a collection of conditional measures of given using the definition of the conditional probability measure [44, Theorem 9.2.2]. The second line stipulates that the nominal marginal distribution of the covariates is a discrete distribution supported on , . Moreover, for each , the nominal conditional distribution of given is a distribution in the exponential family with parameter . Notice that the form of in (5) is chosen to facilitate the injection of parametric information into the nominal distribution, and it is also necessary to tie to the MLE problem using the following notion of MLE-compatibility.

Definition 2.1 (MLE-compatible nominal distribution).

Definition 2.1 indicates that is compatible for the MLE problem if the MLE solution is recovered by solving problem (3b) where the expectation is now taken under . Therefore, MLE-compatibility implies that and are equivalent in the MLE problem.

The next examples suggest two possible ways of calibrating an MLE-compatible of the form (5).

Example 2.2 (Compatible nominal distribution I).

If is chosen of the form (5) with and for all , then is MLE-compatible.

Example 2.3 (Compatible nominal distribution II).

We now detail the choice of the dissimilarity measure which is used to construct the neighborhood surrounding the nominal measure . For this, we will use the Kullback-Leiber divergence.

Definition 2.4 (Kullback-Leibler divergence).

Suppose that is absolutely continuous with respect to , the Kullback-Leibler (KL) divergence from to is defined as , where is the Radon-Nikodym derivative of with respect to .

The KL divergence is an ideal choice in our setting for numerous reasons. Previously, DRO problems with a KL ambiguity set often result in tractable finite-dimensional reformulations [7, 27, 10]. More importantly, the manifold of exponential family of distributions equipped with the KL divergence inherits a natural geometry endowed by a dually flat and invariant Riemannian structure [2, Chapter 2]. Furthermore, the KL divergence between two distributions in the same exponential family admits a closed form expression [4, 2].

Lemma 2.5 (KL divergence between distributions from exponential family).

The KL divergence from to amounts to

Using the above components, we are now ready to introduce our ambiguity set as

| (6) |

parametrized by a marginal radius and a collection of the conditional radii . Any distribution can be decomposed into a marginal distribution of the covariate and an ensemble of parametric conditional distributions at every event . The first inequality in (6) restricts the parametric conditional distribution to be in the -neighborhood from the nominal prescribed using the KL divergence, while the second inequality imposes a similar restriction for the marginal distribution . One can show that for any conditional radii satisfying , is non-empty with . Moreover, if all and are zero, then becomes the singleton set that contains only the nominal distribution.

The set is a parametric ambiguity set: all conditional distributions belong to the same parametric exponential family, and at the same time, the marginal distribution is absolutely continuous with respect to a discrete distribution and hence can be parametrized using a -dimensional probability vector.

At first glance, the ambiguity set looks intricate and one may wonder whether the complexity of is necessary. In fact, it is appealing to consider the ambiguity set

| (7) |

which still preserves the parametric conditional structure and entails only one KL divergence constraint on the joint distribution space. Unfortunately, the ambiguity set may be overly conservative as pointed out in the following result.

Proposition 2.6.

Proposition 2.6 suggests that the ambiguity set can be significantly bigger than , and that the solution of the distributionally robust MLE problem (4) with being replaced by is potentially too conservative and may lead to undesirable or uninformative results.

The ambiguity set requires parameters, including one marginal radius and conditional radii , , which may be cumbersome to tune in the implementation. Fortunately, by the asymptotic result in Lemma 4.4, the set of radii can be tuned simultaneously using the same scaling rate, which will significantly reduce the computational efforts for parameter tuning.

3 Tractable Reformulation

We devote this section to study the solution method for the min-max problem (4) by transforming it into a finite dimensional minimization problem. To facilitate the exposition, we denote the ambiguity set for the conditional distribution of given as

| (8) |

As a starting point, we first show the following decomposition of the worst-case expected loss under the ambiguity set for any measurable loss function.

Proposition 3.1 (Worst-case expected loss).

Suppose that is defined as in (6) for some and such that . For any function measurable, we have

Proposition 3.1 leverages the decomposition structure of the ambiguity set to reformulate the worst-case expected loss into an infimum problem that involves constraints, where each constraint is a hypergraph reformulation of a worst-case conditional expected loss under the ambiguity set . Proposition 3.1 suggests that to reformulate the min-max estimation problem (4), it suffices now to reformulate the worst-case conditional expected log-loss

| (9) |

for each value of into a dual infimum problem. Using Lemma 2.5, one can rewrite in (8) using the natural parameter representation as

Since is convex [4, Lemma 1], it is possible that is represented by a non-convex set of natural parameters and hence reformulating (9) is non-trivial. Surprisingly, the next proposition asserts that problem (9) always admits a convex reformulation.

Proposition 3.2 (Worst-case conditional expected log-loss).

For any and , the worst-case conditional expected log-loss (9) is equivalent to the univariate convex optimization problem

| (10) |

A reformulation for the worst-case conditional expected log-loss was proposed in [27]. Nevertheless, the results in [27, Section 5.3] requires that the sufficient statistics is a linear function of . The reformulation (10), on the other hand, is applicable when is a nonlinear function of . Examples of exponential family of distributions with nonlinear are (multivariate) Gaussian, Gamma and Beta distributions. The results from Propositions 3.1 and 3.2 lead to the reformulation of the distributionally robust estimation problem (4), which is the main result of this section.

Theorem 3.3 (Distributionally robust MLE reformulation).

Below we show how the Poisson and logistic regression models fit within this framework.

Example 3.4 (Poisson counting model).

The Poisson counting model with the ground measure being a counting measure on , the sufficient statistic , the natural parameter space and the log-partition function . If , we have

The distributionally robust MLE is equivalent to the following convex optimization problem

| (12) |

Example 3.5 (Logistic regression).

The logistic regression model is specified with being a counting measure on , the sufficient statistic , the natural parameter space and the log-partition function . If , we have

The distributionally robust MLE is equivalent to the following convex optimization problem

| (13) |

4 Theoretical Analysis

In this section, we provide an in-depth theoretical analysis of our estimator. We first show that our proposed estimator is tightly connected to several existing regularization schemes.

Proposition 4.1 (Connection to the adversarial reweighting scheme).

Proposition 4.1 asserts that by setting the conditional radii to zero, we can recover the robust estimation problem where the ambiguity set is a KL ball around the empirical distribution , which has been shown to produce the adversarial reweighting effects [31, 10]. Recently, it has been shown that distributionally robust optimization using -divergences is statistically related to the variance regularization of the empirical risk minimization problem [34]. Our proposed estimator also admits a variance regularization surrogate, as asserted by the following proposition.

Proposition 4.2 (Variance regularization surrogate).

Suppose that has locally Lipschitz continuous gradients. For any fixed , , there exists a constant that depends only on and , , such that for any and , we have

where and .

One can further show that for sufficiently small , the value of is proportional to the inverse of the local Lipschitz constant of at , in which case admits an explicit expression (see Appendix D). Next, we show that our robust estimator is also consistent, which is a highly desirable statistical property.

Theorem 4.3 (Consistency).

Assume that is the unique solution of the problem , where denotes the true distribution. Assume that has finite cardinality, , has locally Lipschitz continuous gradients, and is convex in for each and . If for each , and with probability going to , then the distributionally robust estimator that solves (4) exists with probability going to , and .

One can verify that choosing using Examples 2.2 and 2.3 will satisfy the condition , and as a direct consequence, choosing following these two examples will result in a consistent estimator under the conditions of Theorem 4.3.

We now consider the asymptotic scaling rate of as the number of samples with the same covariate tends to infinity. Lemma 4.4 below asserts that should scale at the rate . Based on this result, we can set for all , where is a tuning parameter. This reduces significantly the burden of tuning down to tuning a single parameter .

Lemma 4.4 (Joint asymptotic convergence).

Suppose that with . Let and be defined as in Example 2.2. Let , where and denotes the Jacobian operator. Then the following joint convergence holds

| (14) |

where with , are independent and .

Assuming that solves (3a) is asymptotically normal with square-root convergence rate, we remark that the asymptotic joint convergence (14) also holds for in Example 2.3, though in this case the limiting distribution takes a more complex form that can be obtained by the delta method.

Finally, we study the structure of the worst-case distribution for any value of input . This result explicitly quantifies how the adversary will generate the adversarial distribution adapted to any estimate provided by the statistician.

Theorem 4.5 (Worst-case joint distribution).

Given and such that . For any and , let with , where is the solution of the nonlinear equation

and let . Let and be the solution of the following system of nonlinear equations

| then the worst-case distribution is . | ||||

Notice that is decomposed into a worst-case marginal distribution of supported on and a collection of worst-case conditional distributions .

5 Numerical Experiments

| 100(DRO-MLE)/MLE | ||||

|---|---|---|---|---|

| MLE | 0.4906 | 0.1651 | 0.0246 | |

| 0.0967 | 0.0742 | 0.0195 | ||

| 0.0894 | 0.0692 | 0.0176 | ||

| DRO | 0.0547 | 0.0518 | 0.0172 |

We now showcase the abilities of the proposed framework in the distributionally robust Poisson and logistic regression settings using a combination of simulated and empirical experiments. All optimization problems are modeled in MATLAB using CVX [23] and solved by the exponential conic solver MOSEK [32] on an Intel i7 CPU (1.90GHz) computer. Optimization problems (12) and (13) are solved in under 3 seconds for all instances both in the simulated and empirical experiments. The MATLAB code is available at https://github.com/angelosgeorghiou/DR-Parametric-MLE.

5.1 Poisson Regression

We will use simulated experiments to demonstrate the behavior of the tuning parameters and to compare the performance of our estimator with regard to other established methods. We assume that the true distribution is discrete, the -dimensional covariate is supported on points and their locations are generated i.i.d. using a standard normal distribution. We then generate a -dimensional vector whose components are i.i.d. uniform over , then normalize it to get the probability vector of the true marginal distribution of . The value that determines the true conditional distribution via the generative model (1) is assigned to , where is drawn randomly from a 10-dimensional standard normal distribution.

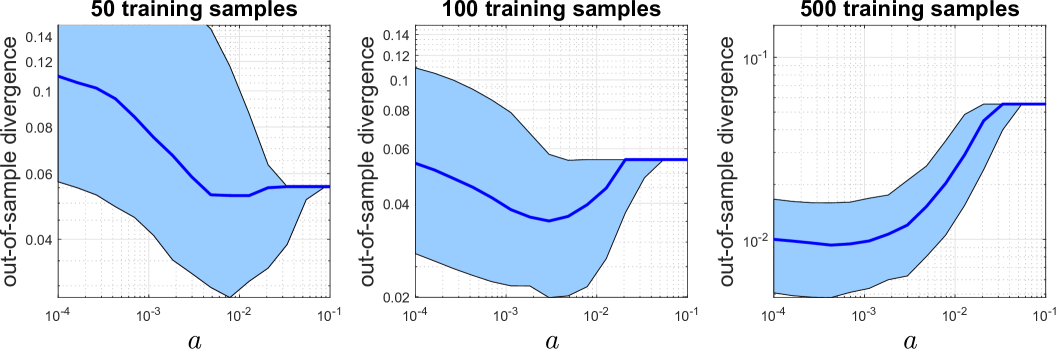

Our experiment comprises 100 simulation runs. In each run we generate training samples i.i.d. from and use the MLE-compatible nominal distribution of the form (5) as in Example 2.3. We calibrate the regression model (12) by tuning with and , both using a logarithmic scale with 20 discrete points. The quality of an estimate with respect to the true distribution is evaluated by the out-of-sample divergence loss

In the first numerical experiment, we fix the marginal radius and examine how tuning the conditional radii can improve the quality of the estimator. Figure 1 shows the 10th, 50th and 90th percentile of the out-of-sample divergence for different samples sizes. If the constant is chosen judiciously, incorporating the uncertainty in the conditional distribution can reduce the out-of-sample divergence loss by , and for and , respectively.

Next, we compare the performance of our proposed estimator to the that solves (3a) and the 1-norm () and 2-norm () MLE regularization, where the regularization weight takes values in on the logarithmic scale with 20 discrete points. In each run, we choose the optimal parameters that give the lowest of out-of-sample divergence for each method, and construct the empirical distribution of the out-of-sample divergence collected from 100 runs. Table 1 reports the 95% confidence intervals of , and , as well as the 5% Conditional Value-at-Risk (CVaR). Our approach delivers lower out-of-sample divergence loss compared to the other methods, and additionally ensures a lower value of CVaR for all sample sizes. This improvement is particularly evident in small sample sizes.

| AUC | CCR | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Dataset | DRO | KL | MLE | DRO | KL | MLE | ||||

| australian () | 92.74 | 92.62 | 92.73 | 92.71 | 92.61 | 85.75 | 85.72 | 85.52 | 85.60 | 85.72 |

| banknote () | 98.46 | 98.46 | 98.43 | 98.45 | 98.45 | 94.31 | 94.32 | 94.16 | 94.35 | 94.32 |

| climate () | 94.30 | 82.77 | 94.85 | 94.13 | 82.76 | 95.04 | 93.89 | 94.85 | 94.83 | 93.89 |

| german () | 75.75 | 75.68 | 75.74 | 75.74 | 75.67 | 73.86 | 74.05 | 73.82 | 73.70 | 74.05 |

| haberman () | 66.86 | 67.21 | 69.19 | 68.17 | 67.20 | 73.83 | 73.80 | 73.20 | 73.18 | 73.80 |

| housing () | 76.24 | 75.73 | 75.37 | 75.57 | 75.73 | 91.65 | 91.70 | 92.68 | 92.65 | 91.70 |

| ILPD () | 74.01 | 73.66 | 73.56 | 73.77 | 73.66 | 71.11 | 71.07 | 71.68 | 71.79 | 71.07 |

| mammo. () | 87.73 | 87.72 | 87.70 | 87.68 | 87.71 | 81.00 | 81.20 | 80.99 | 80.94 | 81.20 |

5.2 Logistic Regression

We now study the performance of our proposed estimation in a classification setting using data sets from the UCI repository [19]. We compare four different models: our proposed DRO estimator (13), the that solves (3a), the 1-norm () and 2-norm () MLE regularization. In each independent trial, we randomly split the data into train-validation-test set with proportion 50%-25%-25%. For our estimator, we calibrate the regression model (13) by tuning with using a logarithmic scale with 10 discrete points and setting . Similarly, for the and regularization, we calibrate the regularization weight from on the logarithmic scale with 10 discrete points. Leveraging Proposition 4.1, we also compare our approach versus the DRO nonparametric Kullback-Leibler (KL) MLE by setting and tune only with with 10 logarithmic scale points. The performance of the methods was evaluated on the testing data using two popular metrics: the correct classification rate (CCR) with a threshold level of 0.5, and the area under the receiver operating characteristics curve (AUC). Table 2 reports the performance of each method averaged over 100 runs. One can observe that our estimator performs reasonably well compared to other regularization techniques in both performance metrics.

Remark 5.1 (Uncertainty in ).

The absolute continuity condition of the KL divergence implies that our proposed model cannot hedge against the error in the covariate . It is natural to ask which model can effectively cover this covariate error. Unfortunately, answering this question needs to overcome to technical difficulties: first, the log-partition function is convex; second, the there are multiplicative terms between and in the objective function. Maximizing over the space to find the worst-case covariate is thus difficult. Alternatively, one can think of perturbing each in a finite set but this approach will lead to trivial modifications of the constraints of problem (11).

Acknowledgments.

Material in this paper is based upon work supported by the Air Force Office of Scientific Research under award number FA9550-20-1-0397. Additional support is gratefully acknowledged from NSF grants 1915967, 1820942, 1838676 and from the China Merchant Bank.

Appendix A Proofs of Section 2

Proof of Example 2.2.

We note that

If , then we have

where we used . Therefore solves . ∎

Proof of Example 2.3.

We find

where the first equality follows from the definition of the log-loss function , the inequality follows because , and the last equality follows because of the convex conjugate relationship that implies the optimal solution should satisfy

This implies that solves and completes the proof. ∎

Proof of Proposition 2.6.

Fix any set of conditional radii . If is empty then it is trivial that . Suppose that is non-empty and pick any . By definition of the set , can be decomposed into a marginal and a collection of conditional measures . Furthermore, because is finite, the marginal should be absolutely continuous with respect to . We have

where the equality is from the chain rule of the conditional relative entropy [24, Lemma 7.9]. The first inequality follows from the fact that for every . The second inequality follows from the last constraint defining the set . This implies that , and because was chosen arbitrarily, we have . As a consequence, .

Regarding the reverse relation, pick an arbitrary which admits the decomposition into a marginal and conditional measures . By setting the conditional radii with for every , one can verify using the chain rule of the conditional relative entropy that . This implies that .

Concerning the last statement, notice that the condition implies that and thus is non-empty. The proof is complete. ∎

Appendix B Proofs of Section 3

The proof of Proposition 3.1 relies on the following preliminary result.

Lemma B.1.

Let be a probability vector summing up to one. For any and satisfying , the finite dimensional set

| (16) |

is compact and convex. Moreover, the support function of satisfies

Proof of Lemma B.1.

The function is continuous and convex, hence, the set is closed and convex. Consequentially, can be written as the intersection between a simplex (thus compact and convex) and a closed, convex set, so is compact and convex.

The proof of the support function of proceeds in 2 steps. First, we prove the support function for the -inflated set

with the right-hand side of the last constraint being inflated with . In the second step, we use a limit argument to show that the support function of is attained as the limit of the support function of as tends to 0.

Reminding that is the -dimensional simplex. For any and any , by the definition of the support function, we have for every

| (17c) | ||||

| (17d) | ||||

where the interchange of the sup-inf operators in (B) is justified by strong duality [9, Proposition 5.3.1] because constitutes a Slater point of the set . By Berge’s maximum theorem [8], the optimal value of the inner supremum problem is a continuous function in because the simplex is compact and the objective function is continuous in the decision variable . As a consequence, we can restrict without any loss of optimality. Because is prescribed using linear constraints, strong duality implies that

where the last equality holds because the supremum problem is separable in each decision variable . It now follows from the first-order optimality condition that the maximizer is

and by substituting this maximizer into the objective function, the value of the support function is then equal to the optimal value of the below optimization problem

We now proceed to the second step. Denote temporarily the objective function of the above problem as , where combines both dual variables and . Define the function

Because is continuous, [36, Lemma 2.7] implies that is upper-semicontinuous at 0. Furthermore, is calm from below at because , thus [36, Lemma 2.7] implies that is lower-semicontinuous at 0. These two facts lead to the continuity of at . From the first part of the proof, we have for any . Moreover, by applying Berge’s maximum theorem [8] to (17c), is a continuous function of over . Thus we find

where the chain of equalities follows from the definition of , the continuity of in , the fact that for , and the continuity of at 0 established previously. The proof is now completed. ∎

Proof of Proposition 3.1.

To facilitate the proof, we define the following ambiguity set over the marginal distribution of the covariate as

Given a nominal marginal distribution supported on a finite set , the absolute continuity requirement suggests that is finite if and only if is absolutely continuous with respect to . Thus, any of interest should be supported on the same set , and and be finitely parametrized by a -dimensional vector . Let denote the convex compact feasible set in , that is,

and the ambiguity set can now be finitely parametrized as

By coupling with the conditional ambiguity sets , can be re-written as

The worst-case expected loss becomes

where the first equality follows from the law of total expectation, and the second equality follows from the finite reparametrization of . If we denote by the epigraph reformulation of the worst-case conditional expectations

then the worst-case expected loss can be further re-expressed as

| (18a) | ||||

| (18b) | ||||

| (18e) | ||||

where the sup-inf formulation (18a) is justified because is non-negative and we can resort to the epigraph formulations of the worst-case conditional expected loss. In (18b) we applied Sion’s minimax theorem [42], which is valid because the sup-inf program (18a) is a concave-convex saddle problem, and is convex and compact and is convex. In (18e) we have used Lemma B.1 to reformulate the supremum over . The claim then follows. ∎

Instead of solving the problem in the natural parameters coupled with its log-partition function , we will use the reparametrization to the mean parameters using the conjugate function of . More specifically, let be the convex conjugate of , that is,

Before proceeding to the technical proofs, the below lemma collects from the existing literature the necessary background knowledge about the log-partition function and its conjugate , along with the relationship between the natural parameter and its corresponding expectation parameter .

Lemma B.2 (Relevant facts).

The following assertions hold for regular exponential family.

-

(i)

The function is closed, convex and proper on .

-

(ii)

and are convex functions of Legendre type, and they are Legendre duals of each other.

-

(iii)

The gradient function is a one-to-one function from the open convex set onto the open convex set .

-

(iv)

The gradient functions and are continuous, and .

-

(v)

The function is essentially smooth over .

Proof of Lemma B.2.

Assertion (i) holds since is convex and closed for each , thus taking supremum, is convex and closed. is proper since is non-empty. Assertions (ii) to (iv) follows from [4, Lemma 1] and [4, Theorem 2]. Assertion (v) follows from [4, Lemma 1] and [37, Theorem 26.3], and the fact that and is a convex conjugate pair. ∎

From Assertion (ii), we have the mappings between the dual spaces and are given by the Legendre transformation

For any , the conjugate function can be expressed as

Lemma B.3 (KL divergence between distributions from exponential family).

Suppose that and belong to the exponential family of distributions with the same log-partition function and with natural parameters and respectively. The KL divergence from to amounts to

where is the convex conjugate of , and for any .

The result of Lemma B.3 can be found in [4, Appendix A], but the explicit proof is included here for completeness.

Proof of Lemma B.3.

Recall that the conditional ambiguity set defined in (8) is

for a parametric, nominal conditional measure , and a radius . The uncertainty set of expectation parameters induced by the ambiguity set is defined as

Lemma B.4 (Compactness of expectation parameter uncertainty set).

The set is compact, and it has an interior point whenever .

Proof of Lemma B.4.

By Lemma B.3 and the definition of the set , we can write as

Because is closed, convex, proper, and that , the function is coercive by [37, Corollary 14.2.2] and [6, Fact 2.11]. As a consequence, is bounded.

Because is essentially strictly convex on , is essentially smooth on by [37, Theorem 26.3]. [6, Theorem 3.8] now implies that if is a boundary point of then as then . Moreover, because is continuous over , the set is closed. This implies that , being a closed and bounded set of finite dimension, is compact.

The continuity of leads a straightforward manner to the non-empty interior of when . This observation completes the proof. ∎

Proof of Proposition 3.2.

Because is a mapping onto the space of natural parameters, we use the shorthand . Moreover, let . The worst-case conditional expectation of the log-loss function becomes

where the first equality is from the definition of and the second equality follows from the linearity of the expectation operator. The last equality follows from the definition of the ambiguity set using the function by Lemma B.3. Because the term does not involve the decision variable , it suffices now to consider the optimization problem

| (22) |

Suppose at this moment that and . When , the feasible set of (22) satisfies the Slater condition because is a continuous function. Hence, by a strong duality argument, the convex optimization problem (22) is equivalent to

where and the interchange of the supremum and the infimum operators is justified thanks to [9, Proposition 5.3.1]. Consider now the infimum problem on the right hand side of the above equation. If , then the inner supremum subproblem on the right hand side is unbounded because , thus is never an optimal solution to the infimum problem. By utilizing the definition of the conjugate function, one thus deduce that problem (22) is equivalent to

| (23) |

where the equality exploits the fact that for any [13, Table 3.2].

We now show that the reformulation problem (23) is valid when . Indeed, when , problem (22) has a unique feasible solution , thus its optimal value is . Moreover, in this case, problem (23) becomes

Notice that the term in the square bracket of the optimization problem on the right hand side is non-negative by the definition of the conjugate function. Thus, the infimum problem over admits the optimal value of 0 as tends to . As a consequence, when , both problem (22) and (23) have the same optimal value and they are equivalent.

Consider now the situation where . In this case, problem (23) becomes

By definition of the conjugate function, we have , and thus, by combining with the fact that , this infimum problem will admit the optimal value of 0. Notice that when , the optimal value of problem (22) is also 0. This shows that (23) is equivalent to (22) for any possible value of . Replacing in (23) by its equivalence and substituting by its equivalence complete the reformulation (10). ∎

Appendix C Proofs of Section 4

Proof of Proposition 4.1.

Let denote the dimensional vector of all ’s. Let , we have

On the other hand, we note

Therefore the objective functions are the same and the two problems are equivalent. ∎

The proof of Proposition 4.2 relies on the following result.

Lemma C.1.

Let be a simplex and be a probability vector. For any two vectors , any vector and any scalar , we have

where .

Proof of Lemma C.1.

Let denote the dimensional vector of ’s, we have

where the first inequality follows from Pinsker’s inequality [14, Theorem 4.19] and the fact that , the second inequality follows from the fact that and dropping the constraint , and the last inequality is from Cauchy-Schwarz.

In the last step, we have

which completes the proof. ∎

We now ready to prove Proposition 4.2.

Proof of Proposition 4.2.

Let and be two -dimensional vectors whose elements are defined as

By Lemma C.1, we find

where . In the last step, notice that

It now remains to provide the bounds for . For any , let , we have

Because has locally Lipschitz continuous gradients, is locally strongly convex [22, Theorem 4.1]. Moreover, the feasible set of the above problem is compact by Lemma B.4, hence there exists a constant such that

Notice that the constants depends only on and . Thus, we find

By setting , we have

Combining terms leads to the postulated results. ∎

For any , , let denote the value of the worst-case expected log-loss

Lemma C.2.

Suppose that the log-partition function has locally Lipschitz continuous gradients, that and that is a compact set. For any fixed , there exist constants that depend only on , and such that for any value and any radius

Proof of Lemma C.2.

Consider the set

and its -inflated set

Because is compact and is a continuous function, is compact [1, Theorem 2.34]. Note that we can rewrite as

Let be temporarily the set

We have that . Recall the definition of :

Therefore is closed, convex and proper. Therefore by [6, Proposition 2.16], implies that is super-coercive, i.e., . Thus

Therefore is bounded, which implies that is also bounded.

Since is compact, there exists a subsequence such that as . Since is bounded, it suffices to show that is closed. Choose any sequence such that as , we want to show that . For each , since , there exists and such that . Since and are compact, there exists a subsequence such that and for some and . Since , by continuity we have . Note that

by continuity of , we have

Therefore and hence is closed.

The finite dimensional set is closed and bounded, thus it is compact, and moreover . The convex hull of is also compact [1, Corollary 5.33]. Because has locally Lipschitz continuous gradients, is locally strongly convex [22, Theorem 4.1]. Moreover, is also essentially smooth by Lemma B.2(v). Thus over the set , there exist constants such that

Notice that the constants and depend only on , and thus on , and

Denote temporarily the shorthand . We have , and so

Because and are both in , we have

We now have

A similar argument leads to the lower bound. This observation completes the proof. ∎

Proof of Theorem 4.3.

Without loss of generality consider . For notational simplicity, denote

Since with probability going to , following the same argument as in the proof of Proposition 4.2, we have that with probability going to , for any ,

where

For each , since in probability, we have . Therefore there exists compact set for each such that is contained in with probability going to . Choose , since , we have eventually. Therefore, by Lemma C.2, for each with probability going to

where the above constant can be chosen independent of due to the finite cardinality assumption of . Since the function is continuous in for any , we have is bounded for all ranging over a compact set . Thus for each with probability going to , we have

Since , we have for each

Thus . On the other hand, since is , we have . Therefore as ,

for any compact set . Next, since in probability, we have by continuous mapping theorem

Besides, by the strong law of large number,

Recall that

Therefore, for each , we have

where

Since for each ,

Therefore solves . If admits an unique solution, then clearly is such a solution. Since is convex, by [3, Theorem II.1],

for any compact set . Thus by triangle inequality

for any compact set . Let denote the unit closed ball in , then is compact for any . Thus uniformly over . Since is convex and is its unique optimal solution, we have

Therefore, with probability going to ,

Thus by convexity of , also

Thus the solution that solves satisfies

Since is chosen arbitrarily, we conclude that in probability. ∎

Proof of Lemma 4.4.

Denote

W.l.o.g. we can assume that . We first show the joint convergence

where is a block-diagonal matrix with diagonal blocks given by . Note that

For convenience denote . We let

Let be the sum of the first samples of such that . If , we add additional independent copies of where to the sum , and denote it by as well. Denote

Note that are independent, by i.i.d central limit theorem

where is a block-diagonal matrix with . We next show that

Note that

By Chebyshev inequality

Since almost surely, by dominated convergence theorem

Thus

which means that . Thus by Slutsky’s lemma

Finally, since , by Slutsky’s lemma,

Now note that

and

Also note that the vector-valued function is continuously differentiable at , therefore, by the delta method

where is a block-diagonal matrix with diagonal elements given by

the Jacobian matrix of evaluated at . Thus

Note that by Lemma B.3, we find

Note that is infinitely-many differentiable, we have the follow Taylor expansion

where is a random variable with values between and . Therefore

Because , and is continuous, we have

Moreover, since we have the joint convergence

by continuous mapping theorem

where with , and are independent for . ∎

Before proving the result on the worst-case distribution in Theorem 4.5, we first prove the worst-case conditional measure that maximize problem (9).

Proposition C.3 (Worst-case conditional distribution).

For any and , then the supremum problem (9) is attained by with , where is the solution of the nonlinear algebraic equation

| (24) |

Proof of Proposition C.3.

Reminding that problem (9) is written as

In the first step, we show that is feasible in problem (9), which means that . Indeed, we find that

where the first equality exploits the expression of the KL divergence between two distributions from the same family in Lemma B.3, and the second equality follows from the fact that solves (24).

Proposition 3.2 asserts that the worst-case conditional expected log-loss problem (9) is equivalent to the convex program (10). Noticing that (24) is the first-order optimality condition of problem (10), thus, by definition, is the minimizer of (10). The objective value of in (9) amounts to

where the first equality follows by substituting the expression of and the linearity of the expectation operator, the second equality follows from the convex conjugate relationship between the expectation parameters and the log-partition function , and the last equality follows from the fact that solves (24). Notice that the last expression coincide with the objective value of (10) evaluated at the optimal solution . This observation implies that attains the optimal value in (9). ∎

Next, we establish the following result on the optimal solution of the support function of the set defined as in Lemma B.1.

Lemma C.4 (Support point of ).

Let be defined as in (16). For any , if there exist and that solve the following system of nonlinear algebraic equation

| (25a) | ||||

| (25b) | ||||

| then the optimal solution that attains is | ||||

| (25c) | ||||

Proof of Lemma C.4.

By definition of in (25c), one can verify that and that , where the equality follows from (25a). Moreover,

where the equalities follow from the definition of in (25c), and the equations (25a) and (25b), respectively. This implies that .

It now remains to show that . By Lemma B.1, we have

If is the solution of (25a)-(25b), then satisfy the Karush-Kuhn-Tucker condition of the above infimum optimization problem, and thus we have

Moreover, we find

where the first equality follows from the definition of , the second equality follows from (25b) and the third equality follows from (25a). This observation completes the proof. ∎

Proof of Theorem 4.5.

It is easy to verify that is a probability measure because each and is a probability measure, and since solves

| (26) | ||||

| (27) |

If we set , then we have

Moreover, because is constructed using Proposition C.3, we have for all . Furthermore, we also have

where the equalities follow from the construction of and the equations (26) and (27), respectively. This implies that .

It now remains to show that is optimal. For any weight , by the definition of , we have

We thus find

| (28) | ||||

| (29) | ||||

| (30) | ||||

where the set in (28) is defined as in (16). Equality (29) follows from Lemma C.4 and from the definition of and that solve (26)-(27). Equality (30) follows from the definition of . The proof is completed. ∎

Appendix D Auxiliary Results

Lemma D.1 (Locally strongly convex parameter).

If is locally strongly smooth, and at , the smoothness parameter is , then is locally strongly convex at with strongly convex parameter in a sufficiently small neighbourhood of .

Proof of Lemma D.1.

The proof follows directly from the proof of [22, Theorem 4.1]. By the definition of locally strongly smooth, for some neighborhood of , we have for

Since and , we have

In the last step, note that . Taking where . if is sufficiently small. We have

Therefore is locally strongly convex at with strongly convex parameter . ∎

In Proposition 4.2, since is locally Lipschitz continuous, we have that is locally strongly smooth with smoothness parameter at , where can be chosen as the local Lipschitz constant for a neighborhood around . By Lemma D.1 and the proof of Proposition 4.2, for sufficiently small , we can choose explicitly as , thus .

References

- [1] C. D. Aliprantis and K. C. Border, Infinite Dimensional Analysis: A Hitchhiker’s Guide, Springer, 2006.

- [2] S. Amari, Information Geometry and Its Applications, Springer, 2016.

- [3] P. K. Andersen and R. D. Gill, Cox’s regression model for counting processes: A large sample study, Annals of Statistics, 10 (1982), pp. 1100–1120.

- [4] A. Banerjee, S. Merugu, I. Dhillon, and J. Ghosh, Clustering with Bregman divergences, Journal of Machine Learning Research, 6 (2005), pp. 1705–1749.

- [5] O. Barndorff-Nielsen, Information and Exponential Families, John Wiley & Sons, 2014.

- [6] H. Bauschke and J. Borwein, Legendre functions and the method or random Bregman projections, Journal of Convex Analysis, 4 (1997), pp. 27–67.

- [7] A. Ben-Tal, D. den Hertog, A. De Waegenaere, B. Melenberg, and G. Rennen, Robust solutions of optimization problems affected by uncertain probabilities, Management Science, 59 (2013), pp. 341–357.

- [8] C. Berge, Topological Spaces: Including a Treatment of Multi-Valued Functions, Vector Spaces, and Convexity, Courier Corporation, 1963.

- [9] D. Bertsekas, Convex Optimization Theory, Athena Scientific, 2009.

- [10] D. Bertsimas, V. Gupta, and N. Kallus, Data-driven robust optimization, Mathematical Programming, 167 (2018), p. 235–292.

- [11] J. Blanchet, K. Murthy, and F. Zhang, Optimal transport based distributionally robust optimization: Structural properties and iterative schemes, arXiv preprint arXiv:1810.02403, (2018).

- [12] J. Blanchet, F. Zhang, Y. Kang, and Z. Hu, A distributionally robust boosting algorithm, in 2019 Winter Simulation Conference, 2019, pp. 3728–3739.

- [13] J. M. Borwein and A. S. Lewis, Convex Analysis and Nonlinear Optimization, Springer, 2006.

- [14] S. Boucheron, G. Lugosi, and P. Massart, Concentration Inequalities: A Nonasymptotic Theory of Independence, OUP Oxford, 2013.

- [15] R. Christensen, Log-Linear Models, Springer, 1990.

- [16] V. M. T. de Jong, M. J. C. Eijkemans, B. van Calster, D. Timmerman, K. G. M. Moons, E. W. Steyerberg, and M. van Smeden, Sample size considerations and predictive performance of multinomial logistic prediction models, Statistics in Medicine, 38 (2019), pp. 1601–1619.

- [17] A. J. Dobson and A. G. Barnett, An Introduction To Generalized Linear Models, CRC press, 2018.

- [18] A. Domahidi, E. Chu, and S. Boyd, ECOS: An SOCP solver for embedded systems, in 2013 European Control Conference (ECC), IEEE, 2013, pp. 3071–3076.

- [19] D. Dua and C. Graff, UCI machine learning repository, 2017.

- [20] J. C. Duchi, P. W. Glynn, and H. Namkoong, Statistics of robust optimization: A generalized empirical likelihood approach, arXiv preprint arXiv:1610.03425, (2016).

- [21] L. Faury, U. Tanielian, F. Vasile, E. Smirnova, and E. Dohmatob, Distributionally robust counterfactual risk minimization, in AAAI Conference on Artificial Intelligence, 2020.

- [22] R. Goebel and R. T. Rockafellar, Local strong convexity and local Lipschitz continuity of the gradient of convex functions, Journal of Convex Analysis, 15 (2008), p. 263–270.

- [23] M. Grant and S. Boyd, CVX: Matlab software for disciplined convex programming, version 2.1, Mar. 2014.

- [24] R. Gray, Entropy and Information Theory, Springer, 2011.

- [25] J. M. Hilbe, Modeling Count Data, Cambridge University Press, 2014.

- [26] D. W. Hosmer Jr, S. Lemeshow, and R. X. Sturdivant, Applied Logistic Regression, John Wiley & Sons, 2013.

- [27] Z. Hu and J. Hong, Kullback-Leibler divergence constrained distributionally robust optimization, Available on Optimization Online, (2013).

- [28] P. J. Huber, Robust estimation of a location parameter, Annals of Mathematical Statistics, 35 (1964), pp. 73–101.

- [29] D. Kuhn, P. M. Esfahani, V. A. Nguyen, and S. Shafieezadeh-Abadeh, Wasserstein distributionally robust optimization: Theory and applications in machine learning, in Operations Research & Management Science in the Age of Analytics, INFORMS, 2019, pp. 130–166.

- [30] S. Lee, H. Lee, P. Abbeel, and A. Y. Ng, Efficient L1 regularized logistic regression, in Proceedings of the Twenty-First National Conference on Artificial Intelligence and the Eighteenth Innovative Applications of Artificial Intelligence Conference, 2006, pp. 401–408.

- [31] M. Li and D. B. Dunson, Comparing and weighting imperfect models using D-probabilities, Journal of the American Statistical Association, (2019), pp. 1–26.

- [32] MOSEK ApS, The MOSEK optimization toolbox. Version 9.2., 2019.

- [33] H. Namkoong and J. C. Duchi, Stochastic gradient methods for distributionally robust optimization with f-divergences, in Advances in Neural Information Processing Systems 29, 2016, pp. 2208–2216.

- [34] , Variance-based regularization with convex objectives, in Advances in Neural Information Processing Systems 30, 2017, pp. 2971–2980.

- [35] A. Y. Ng, Feature selection, L1 vs. L2 regularization, and rotational invariance, in Proceedings of the 21st International Conference on Machine Learning, 2004, pp. 78–85.

- [36] V. Nguyen, D. Kuhn, and P. Mohajerin Esfahani, Distributionally robust inverse covariance estimation: The Wasserstein shrinkage estimator, arXiv preprint arXiv:1805.07194, (2018).

- [37] R. T. Rockafellar, Convex Analysis, Princeton University Press, 1970.

- [38] P. J. Rousseeuw and M. Hubert, Robust statistics for outlier detection, WIREs Data Mining and Knowledge Discovery, 1 (2011), pp. 73–79.

- [39] S. Shafieezadeh-Abadeh, P. M. Esfahani, and D. Kuhn, Distributionally robust logistic regression, in Advances in Neural Information Processing Systems 28, 2015, pp. 1576–1584.

- [40] S. Shafieezadeh-Abadeh, D. Kuhn, and P. M. Esfahani, Regularization via mass transportation, Journal of Machine Learning Research, 20 (2019), pp. 1–68.

- [41] N. Si, F. Zhang, Z. Zhou, and J. Blanchet, Distributionally robust policy evaluation and learning in offline contextual bandits, in Proceedings of the 37th International Conference on Machine Learning, 2020.

- [42] M. Sion, On general minimax theorems, Pacific Journal of Mathematics, 8 (1958), pp. 171–176.

- [43] N. Srivastava, G. Hinton, A. Krizhevsky, I. Sutskever, and R. Salakhutdinov, Dropout: A simple way to prevent neural networks from overfitting, Journal of Machine Learning Research, 15 (2014), pp. 1929–1958.

- [44] D. Stroock, Probability Theory: An Analytic View, Cambridge University Press, 2011.

- [45] A. W. van der Vaart, Asymptotic Statistics, Cambridge University Press, 2000.

- [46] S. Wager, S. Wang, and P. S. Liang, Dropout training as adaptive regularization, in Advances in Neural Information Processing Systems 26, 2013, pp. 351–359.

- [47] S. Wang and C. Manning, Fast dropout training, in Proceedings of the 30th International Conference on Machine Learning, 2013, pp. 118–126.