High-dimensional Model-assisted Inference for Local Average Treatment Effects with Instrumental Variables

Baoluo Sun111Baoluo Sun is Assistant Professor, Department of Statistics and Applied Probability, National University of Singapore, Singapore, SG 117546 (Email: stasb@nus.edu.sg), and Zhiqiang Tan is Professor, Department of Statistics, Rutgers University, Piscataway, NJ 08854, USA (Email: ztan@stat.rutgers.edu). & Zhiqiang Tan111Baoluo Sun is Assistant Professor, Department of Statistics and Applied Probability, National University of Singapore, Singapore, SG 117546 (Email: stasb@nus.edu.sg), and Zhiqiang Tan is Professor, Department of Statistics, Rutgers University, Piscataway, NJ 08854, USA (Email: ztan@stat.rutgers.edu).

Abstract.

Consider the problem of estimating the local average treatment effect with an instrument variable, where the instrument unconfoundedness holds after adjusting for a set of measured covariates. Several unknown functions of the covariates need to be estimated through regression models, such as instrument propensity score and treatment and outcome regression models. We develop a computationally tractable method in high-dimensional settings where the numbers of regression terms are close to or larger than the sample size. Our method exploits regularized calibrated estimation, which involves Lasso penalties but carefully chosen loss functions for estimating coefficient vectors in these regression models, and then employs a doubly robust estimator for the treatment parameter through augmented inverse probability weighting. We provide rigorous theoretical analysis to show that the resulting Wald confidence intervals are valid for the treatment parameter under suitable sparsity conditions if the instrument propensity score model is correctly specified, but the treatment and outcome regression models may be misspecified. For existing high-dimensional methods, valid confidence intervals are obtained for the treatment parameter if all three models are correctly specified. We evaluate the proposed methods via extensive simulation studies and an empirical application to estimate the returns to education.

Key words and phrases.

Calibrated estimation; Causal inference; Complier average causal effect; Doubly robust estimation; Instrumental variable; Lasso penalty; Model misspecification; Propensity score; Regularized M-estimation.

1 Introduction

A major difficulty in drawing causal inference from observational studies is the possible existence of unobserved background variables that are related to both the treatment status and outcome of interest, which is usually referred to as unmeasured confounding. In such settings, biased estimates of the causal effects may be obtained by comparing observed outcomes between treated and untreated individuals, even after adjusting for measured covariates. To tackle unmeasured confounding, instrumental variable (IV) methods have been widely used for estimating causal effects. While conventional IV methods are rooted in econometrics (Wright 1928), there are modern IV approaches which formulate structural assumptions required to be satisfied by IVs and provide nonparametric identification results for certain causal contrasts in terms of potential outcomes (Angrist et al. 1996; Robins 1994). Two basic IV assumptions are called instrument unconfoundedness and exclusion restriction. Intuitively, a valid IV serves as an exogenous experimental handle, the turning of which may change each individual’s treatment status and, through and only through this effect, also change observed outcome. Then under a monotonicity assumption and other technical conditions, the local average treatment effect (LATE), defined as the average treatment effect among individuals whose treatment status would be manipulated through the change of the IV, is identified from observed data nonparametrically (Angrist et al. 1996).

We consider the problem of estimating population LATEs provided that the IV assumptions hold after conditioning on a set of measured covariates. While a completely randomized IV is conceptually easy to interpret, the conditional version of instrument unconfoundedness is more plausible in allowing an IV to be randomized within different values of measured covariates. In general, it is helpful to think of estimation of LATEs in two stages. First, regression models are built and fitted for certain unknown functions of the covariates, such as the instrument propensity score and the treatment and outcome regression functions in Tan (2006a) or regression functions in Frolich (2007), Uysal (2011), and Ogburn et al. (2015). In the second stage, the fitted functions are substituted into various estimators, related to the identification formulas of LATEs. For the regression tasks in the first stage, a conventional approach involves an iterative process of model diagnosis, modification, and refitting until some criterion is satisfied, for example, by inspection of residual plots for outcome regression or covariate balance for propensity score models. This approach depends on ad hoc choices of how regression terms are added or dropped in model building. Moreover, uncertainty in the iterative process is complicated and often ignored in subsequent inference (i.e., confidence intervals or hypothesis testing) about LATEs.

In this article, we develop a new method, extending the doubly robust method in Tan (2006a) for estimating population LATEs to high-dimensional settings where the numbers of regression terms are close to or larger than the sample size in the first-stage estimation described above. The instrument and treatment are assumed to be binary. Three regression models are involved: an instrument propensity score model for the conditional probability of the instrument being 1 given the covariates, a treatment regression model for the conditional probability of the treatment being 1 given the instrument and covariates, and an outcome regression model for the conditional mean of the observed outcome given the treatment, instrument and covariates. The regression terms in all three models are pre-specified, for example, as main effects from a large number of covariates or additional interaction or nonlinear terms from even a moderate number of covariates.

Our method uses the doubly robust estimator of the LATE in Tan (2006a), in the form of a ratio of two augmented inverse probability weighted (AIPW) estimators. To tackle high-dimensional data, however, our method employs regularized calibrated estimation for estimating coefficients sequentially in the instrument propensity score and treatment and outcome regression models. The Lasso penalties (Tibshirani 1996) are introduced to achieve adequate estimation with a large number of regression terms under sparsity conditions where only a small but unknown subset of regression terms are associated with nonzero coefficients. The loss functions are carefully chosen for regularized estimation, different from least squares or maximum likelihood, by leveraging regularized calibrated estimation in Tan (2020b) for estimating average treatment effects (ATEs) under treatment uncounfoundedness in high-dimensional data. In fact, our estimators for the coefficient vectors in the instrument propensity score and treatment regression models are directly transferred from Tan (2020b). Moreover, our estimator for the coefficient vector in the outcome regression model is new as a regularized weighted likelihood estimator, with a pseudo-response depending on both treatment status and observed outcome. This differs sharply from maximum quasi-likelihood estimation where the response depends on observed outcome only.

We provide rigorous high-dimensional analysis of the regularized calibrated estimators and the resulting AIPW estimator for the LATE. We establish sufficiently fast convergence rates for the regularized calibrated estimators, in spite of their sequential construction with data-dependent weights and mean functions. Moreover, we show that under suitable sparsity conditions, the proposed estimator of LATE achieves a desired asymptotic expansion in the usual order with a sample size and then valid Wald confidence intervals can be obtained, provided that the instrument propensity score model is correctly specified, but the treatment and outcome regression models may be misspecified. Following the survey literature (Sarndal et al. 2003), our confidence intervals for the LATE are said to be instrument propensity score model based, and treatment and outcome regression models assisted. It should be stressed that our method is aimed to be computationally tractable for practical use, with the sequential construction of the regularized calibrated estimators. In principle, doubly robust confidence intervals for LATEs can also be obtained, which remain valid if either the instrument propensity score model or the treatment and outcome regression models are correctly specified. But there are several analytical and computational issues which need to be properly addressed in this direction (see Remarks 6 and 7).

Related work. There is an extensive literature on IV and related methods for causal inference (e.g., Baiocchi et al. 2014; Imbens 2014). For space limitation, we discuss closely related work only. Under the IV monotonicity assumption, parametric and semiparametric methods for estimating conditional LATEs given the full vector of covariates include Little & Yau (1998), Hirano et al. (2000), and Abadie (2003). For estimating population or subpopulation LATEs, doubly robust methods are proposed in Tan (2006a), Uysal (2011), and Ogburn et al. (2015), whereas nonparametric smoothing based methods are studied in Frolich (2007). Alternatively, there are various methods using IVs based on homogeneity assumptions for estimating certain average treatment effects on the treated (Robins 1994; Vansteelandt & Goetghebeur 2003; Tan 2010a). Doubly robust estimation of ATEs using IVs is studied in Okui et al. (2012) under a partially linear model and in Wang & Tchetgen Tchetgen (2018) under suitable identification assumptions.

The foregoing IV methods are developed in low-dimensional settings without regularized estimation. With high-dimensional data, Chernozhukov et al. (2018) proposed debiased methods for estimating various treatment parameters, using regularized likelihood-based estimation. In particular, for estimating population LATEs under the monotonicity assumption, their method exploits the doubly robust estimating function in Tan (2006a) similarly as our method, but employs regularized likelihood estimation for fitting three regression models as in Uysal (2011). The Wald confidence intervals for LATEs are shown to be valid under similar sparsity conditions as ours, provided that all the three regression models are correctly specified (or with negligible biases). Our main contribution is therefore to provide model-assisted confidence intervals for LATEs using differently configured regularized estimation. See Remark 4 for further discussion.

Similar methods to non-regularized calibrated estimation are proposed in Kim & Haziza (2014) for estimating ATEs under treatment unconfoundedness and in Vermeulen & Vansteelandt (2015) for general doubly robust estimation. In low-dimensional settings, such methods lead to computationally simpler variance estimation and confidence intervals than likelihood-based estimation for nuisance parameters, where valid confidence intervals can still be derived using usual influence functions (see Remark 5). Similarly as in Tan (2020b), we exploit these ideas in high-dimensional settings to obtain model-assisted confidence intervals for LATEs, which would not be feasible if using regularized likelihood-based estimation as in Chernozhukov et al. (2018).

There is a growing literature on confidence intervals and hypothesis testing in high-dimensional settings. Examples include debiased Lasso in generalized linear models (Zhang & Zhang 2014; van de Geer et al. 2014), and double robustness related methods (Belloni et al. 2014; Farrell 2015; Avagyan & Vansteelandt 2017; Smucler et al. 2019; Bradic et al. 2019; Ning et al. 2020), in addition to Chernozhukov et al. (2018) and Tan (2020b). Sample splitting and cross fitting are used in some of these methods, but not pursued here.

2 Background

Suppose that are independent and identically distributed observations of , where is an outcome variable, is a binary, treatment variable encoding the presence or absence of treatment , is a binary, instrument variable, and is a vector of measured covariates. We use the potential outcomes notation (Neyman 1990; Rubin 1974) to define quantities of causal interest. For , let denote the potential treatment status that would be observed if were set to level , and let denote the potential outcome that would be observed if the treatment and instrument and were set to the levels and respectively. Following Angrist et al. (1996), the population can be divided into four strata: the compliers with , the always-takers with , the never-takers with , and the defiers with .

2.1 Structural assumptions and LATE

Angrist et al. (1996) formalized an IV approach with a set of structural assumptions for identification of the local average treatment effect (LATE), also known as the average treatment effect among the compliers. Throughout, we make the following conditional versions of the IV assumptions (Abadie 2003; Tan 2006a; Frolich 2007):

-

(a)

Instrument unconfoundedness: for , where denotes independence.

-

(b)

Exclusion restriction: , henceforth denoted as , for .

-

(c)

Monotonicity: with probability 1.

-

(d)

Instrument overlap: with probability 1, where is called the instrument propensity score (Tan 2006a).

-

(e)

Instrumentation: .

-

(f)

Consistency: and .

Assumption (a) states that the instrument is essentially randomized within levels of the covariate . Assumptions (a) and (b) together imply an independence condition, for , which can be technically used in place of Assumptions (a) and (b). Assumption (c) excludes the existence of defiers in the population. Vytlacil (2002) and Tan (2006a) showed that the independence and monotonicity assumptions are equivalent to the assumptions of a nonparametric latent index model:

-

(i)

for a function and a random variable , where is the indicator function.

-

(ii)

and .

As a result, can be transformed to be uniformly distributed on and hence equals the treatment propensity score . The preceding representation is helpful for understanding the data-generating process, which is used in our simulation studies.

Assumption (d) ensures that every unit within levels of has a positive probability of receiving each instrument level . Assumption (e) requires a non-null causal effect of on , in accordance with the concept of being an experimental handle; turning of the handle needs to change treatment status . Assumption (f) relates the potential outcomes and treatments to the observed data, under no interference and well-defined intervention conditions.

Under Assumptions (a)–(f), the LATE conditionally on , defined as , can be identified as (Angrist et al. 1996)

For high-dimensional , LATE is difficult to interpret, depending on all covariates in . Moreover, estimation of LATE can be sensitive to modeling assumptions on the conditional expectations above. Hence it is of interest to consider the population LATE (or in short LATE), defined as . As shown by Tan (2006a) and Frolich (2007), LATE can be identified under Assumptions (a)–(f) in two distinct ways:

| (1) |

depending on the regression functions and for , or

| (2) |

depending on the instrument propensity score . Both (1) and (2) are in the form of a ratio of the difference in outcome over that in treatment .

A further identification exploited later in our approach is that the individual expectations for , not just the difference LATE , can also be identified. In fact, is identified under Assumptions (a)–(f) as

| (3) |

or equivalently as

| (4) |

Similarly, is identified as (3) or (4) with replaced by . The difference of the corresponding identification equations for and leads back to (1) or (2). As shown in Tan (2006a), both (3) and (4) can be derived from the following expression of :

| (5) |

which is a ratio of two differences, depending on potential outcomes and treatments. Because is an experimental handle with as “outcomes” under Assumption (a) (instrument unconfoundedness), each expectation in the numerator and denominator of (5) can be identified through outcome regression averaging or inverse probability weighting, so that (3) or (4) are obtained. These results are parallel to related identification results under the assumption of treatment unconfoundedness. See Tan (2006b, 2010b) and references therein.

2.2 Modeling assumptions and existing estimators

For estimating and LATE from sample data, additional modeling assumptions are required to estimate unknown functions in the identification equations (1)–(2) or (3)–(4). There are at least two distinct approaches, depending on models for the instrument propensity score or treatment and outcome regression functions and for (Tan 2006a). For simplicity, estimation of is discussed, whereas that of can be similarly handled. Throughout, denotes a sample average such that for a function .

Remark 1 (On modeling choices).

Consideration of models for and is conveniently aligned with our interest in estimating both and LATE, through identification equations (3)–(4). As illustrated in Tan (2006a, Section 5), separate estimates of and can be informative in applications. The conditional expectation in (3) is decomposed as . Both models for and can be specified using appropriate links functions, as in (9)–(10) below. If estimation of LATE is solely of interest through identification equations (1)–(2), then modeling assumptions can be introduced on and (Froelich 2007; Uysal 2011). In this case, our methods and theory developed later can be similarly extended.

First, consider an instrument propensity score model

| (6) |

where is an inverse link function, is a vector of known functions such as and is a vector of unknown parameters. For concreteness, assume that logistic regression is used such that . By (4), the inverse probability weighted (IPW) estimator of is

| (7) |

where is a fitted instrument propensity score. For low-dimensional , is customarily the maximum likelihood estimator of . In high-dimensional settings, can be a Lasso penalized maximum likelihood estimator , defined as a minimizer of , where denotes the norm, , is a tuning parameter, and is the average negative log-likelihood

| (8) |

Alternatively, for , consider treatment and outcome regression models, which can both be called “outcome regression” with as “outcomes”:

| (9) | ||||

| (10) |

where and are inverse link functions, assumed to be increasing with and , and are two vectors of known functions, and and are two vectors of unknown parameters of dimensions and respectively. By (3), the outcome-regression based estimator of is

| (11) |

where , , and, for , is a fitted treatment regression function and is a fitted outcome regression function. For low-dimensional , and are customarily maximum quasi-likelihood estimators of and or their variants. In high-dimensional settings, and can be regularized estimators. For concreteness, let be a Lasso penalized quasi-likelihood estimator of which is a minimizer of , where is excluding the intercept, is a tuning parameter, and

| (12) |

where . Let be a Lasso penalized quasi-likelihood estimator of which is a minimizer of , where is excluding the intercept, is a tuning parameter, and

| (13) |

where . The loss function (12) or (13) is the average negative log-quasi-likelihood in the case where model (9) or (10) corresponds to a generalized linear model with a canonical link (McCullagh and Nelder 1989).

Remark 2 (On outcome regression).

We comment on specification of outcome regression model (10). By the IV assumptions, depends on only through and . On one hand, this relationship can be incorporated in model (10), by including in various functions of and , as well as their interactions, for example, . On the other hand, such specification of , depending on an estimator , introduces additional variation which needs to be taken account of in theoretical analysis. For simplicity, this complication is not addressed in our theoretical results later. In fact, our method is shown to yield valid inference when model (10) may be misspecified, and hence can be chosen independently of . See Remarks 6 and 7 for related discussions on choices of model-assisted inference.

Consistency of the estimator relies on correct specification of model (6), whereas consistency of relies on correct specification of models (9)–(10). The weighting and regression approaches can be combined to obtain doubly robust estimators through augmented IPW estimation (Tan 2006a), in a similar manner as in the setting of treatment unconfoundedness (Robins et al. 1994; Tan 2007). The expectations and in (5) can be estimated by and respectively, where

| (14) | |||

| (15) |

The expectations and in (5) can be estimated by and respectively, where

| (16) | |||

| (17) |

By (5), the resulting doubly robust estimator of is

| (18) |

where and . Consistency of can be achieved if either model model (6) or models (9)–(10) are correctly specified.

There is potentially a further advantage of doubly robust estimators in high-dimensional settings. In this case, the estimator or in general converges at a slower rate than to the true value under correctly specified model (6) or models (9)–(10) respectively. Denote , , and , obtained from Lasso penalized likelihood estimation. By related results in Chernozhukov et al. (2018, Section 5.2), it can be shown that if both models (6) and (9)–(10) are correctly specified, then under suitable sparsity conditions, converges to at rate and admits the asymptotic expansion

| (19) |

where , , and , with the true values in models (6) and (9)–(10). From this expansion, valid Wald confidence intervals based on can be obtained for .

3 Methods and theory

3.1 Regularized calibrated estimation

To focus on main ideas, we describe our new method for estimating . Estimation of and LATE is discussed later in this section. Similarly as in Section 2.2, consider logistic regression model (6), for estimating the instrument propensity score , and models (9)–(10) for estimating treatment and outcome regression functions and respectively for . For technical reasons (see Section 3.2), we require that the “regressor” vector in model (6) is a subvector of and in models (9)–(10) (hence and ). This condition can be satisfied possibly after enlarging models (9)–(10) to accommodate .

A class of doubly robust estimators of , slightly more flexible than (18), is

where with and two possibly different versions of fitted values for , and with fitted values for respectively for , and, with and defined as (14)–(17),

Our point estimator of is , where, for , , , and are fitted values, and are estimators of defined as follows.

For logistic regression model (6), the estimator is a regularized calibrated estimator of (Tan 2020a), defined as a minimizer of the Lasso penalized objective function

| (20) |

with the calibration loss functions

| (21) | |||||

| (22) |

Minimization of (20) can be implemented using R package RCAL (Tan 2020a). For treatment regression model (9), is a regularized weighted likelihood estimator of , defined as a minimizer of the Lasso penalized objective function

| (23) |

with the weighted (quasi-)likelihood loss function

| (24) |

where the weight function is for . For outcome regression model (10), is a regularized calibrated estimator of , defined as a minimizer of the Lasso penalized objective function

| (25) |

with the loss function

| (26) |

where the weight function is the same as above. Interestingly, (26) can be equivalently expressed as a weighted (quasi-)likelihood loss

| (27) |

with the pseudo-response and weight . Hence existing software for Lasso penalized weighted estimation such as glmnet (Friedman et al. 2010) and RCAL can be employed to minimize (25) as well as (23). The loss (26) or (27) differs sharply from that of the likelihood loss (13), in terms of the residuals implied.

Compared with regularized likelihood estimation in Section 2.2, our method involves using a different set of estimators , which are called regularized calibrated estimators. Similarly as in Tan (2020b), these estimators are derived to allow model-assisted, asymptotic confidence intervals for based on . See Proposition 1 for a summary and Section 3.2 for further discussion. We also point out several interesting properties algebraically associated with our estimators. First, by the Karush–Kuhn–Tucker (KKT) condition for minimizing (20), the fitted instrument propensity score satisfies

| (28) | |||

| (29) |

where equality holds in (29) for any such that the th estimate is nonzero. These equations also hold with replaced by and replaced by . Eq. (28) shows that the inverse probability weights, with , sum to the sample size , whereas Eq. (29) implies that the weighted average of each covariate over the instrument group may differ from the overall average of by no more than . Such differences are of interest in showing how a weighted instrument group resembles the overall sample. In contrast, similar results are not available when using the regularized likelihood estimator . Moreover, Tan (2020a) studied a comparison between calibrated and maximum likelihood estimation in logistic regression. Minimization of the calibration loss (21) or (22) achieves a stronger control of relative errors of fitted propensity scores than that of the likelihood loss (8).

By the KKT condition associated with the intercept in for minimizing (23), the fitted treatment regression function satisfies

| (30) |

A similar equation holds with replaced by , by , and by . As a result of (30), our augmented IPW estimator for , defined as , can be simplified to

Hence always falls within the range of the binary treatment values and the predicted values , which are by definition in the interval . This boundedness property is not satisfied by the usual estimator , but is desirable for stabilizing the behavior of augmented IPW estimators, especially when used in the denominator of (18).

By the KKT condition associated with the intercept in for minimizing (25), the fitted functions and jointly satisfy

| (31) |

A similar equation holds with replaced by , by , and by . By (31), our augmented IPW estimator for , defined as , can be simplified to

where . As a consequence, always falls within the range of the observed values and the predicted values .

We present a high-dimensional analysis of the proposed estimator in Section 3.2 provided that instrument propensity score model (6) is correctly specified but treatment and outcome models (9)–(10) may be misspecified. Our main result shows that under suitable conditions, is consistent for and admits the asymptotic expansion

| (32) |

where , , , and, for , , , and , with defined as follows. The target value is defined as a minimizer of the expected loss

Because model (6) is correctly specified, the target values and are identical to the true value , so that (Tan 2020a). With possible misspecification of model (9), the target value is defined as a minimizer of the expected loss

| (33) |

If model (9) is correctly specified, then coincides with the true value such that . Otherwise, may differ from . Similarly, with possible misspecification of model (10), the target value is defined as a minimizer of the expected loss

| (34) |

If model (10) is correctly specified, then coincides with the true value such that . But may in general differ from . Suppose that the Lasso tuning parameters are specified as for in (20), for in (23), and for in (25), where are sufficiently large constants for . For a vector , denote and the size of the set as .

Proposition 1.

Suppose that Assumptions 1–3 hold as in Section 3.2, their corresponding versions with replaced by and replaced by , and , If model (6) is correctly specified, then satisfies the asymptotic expansion (32). Furthermore, the following results hold.

-

(i)

, where ;

-

(ii)

a consistent estimator of is

where ;

-

(iii)

an asymptotic confidence interval for is , where is the quantile of .

Finally, we describe how our method can be applied to estimate and LATE, denoted as . In addition to models (6) and (9)–(10), consider the following outcome regression model in the untreated population for ,

| (35) |

where is a vector of known functions as in model (10) and is a vector of unknown parameters of dimension . For augmented IPW estimation of and , define

where be a fitted regression function. Then a doubly robust estimator of , similar to that of in (18) is

| (36) |

where , is as in (18), and

Our point estimator of is , and that of LATE, , is , where and remain the same as before, and with defined as follows. For , let be a minimizer of the Lasso penalized objective function

with the weighted (quasi-)likelihood loss

where and . Under similar conditions as in Proposition 1, admits an asymptotic expansion in the form of (32), and Wald confidence intervals for and LATE can be derived accordingly. In particular, an asymptotic confidence interval for LATE is , where

where .

Remark 3 (On completely randomized instruments).

Our method is directly applicable in the special case where the instrument is assumed to be completely randomized, independently of observed covariates. The instrument propensity score model (6) with an intercept is valid, because is a constant. With flexible treatment and outcome models (9)–(10), the proposed estimator based on augmented IPW estimation is expected to achieve smaller variances than the simple Wald estimator. Such efficiency gains are analogous to related results on regression adjustment in completely randomized experiments (with full compliance) in low- and high-dimensional settings (e.g., Davidian et al. 2005; Bloniarz et al. 2016; Wager et al. 2016).

3.2 Theoretical analysis

We develop theoretical analysis which leads to Proposition 1 for the proposed estimator in high-dimensional settings, provided model (6) is correctly specified but models (9)–(10) may be misspecified. Similar analysis can be obtained for and . Before formal results are presented, we discuss heuristically how the asymptotic expansion (32) can be achieved, due to use of the regularized calibrated estimators for . For notational brevity, these estimators are denoted as unless otherwise noted.

There are two main steps in our analysis. First, the estimators can be shown to converge in probability to with the -norm error bounds:

| (37) | |||

| (38) | |||

| (39) |

where are the target values defined as minimizers of the corresponding expected loss functions in Section 3.1. For simplicity, we do not discuss prediction -norm error bounds for , which are also involved in our rigorous analysis later. While these results are built on existing high-dimensional, sparse analysis of Lasso penalized M-estimators (Buhlmann & van de Geer 2011; Huang & Zhang 2012; Tan 2020a), additional arguments are needed to carefully handle the dependency of on and that of on , hence the presence of in the bound for and and in that for .

Second, for , the augmented IPW estimators of and involved in can be shown to admit the following asymptotic expansions,

| (40) | ||||

| (41) |

where are defined as in Section 3.1. From (40)–(41), the expansion (32) for then follows by the delta method. To show (40) for , consider a Taylor expansion

| (42) |

where the remainder is taken to be under suitable conditions, and

Here and denotes the derivative of . A crucial point is that the expectations of the gradients and reduce to 0,

| (43) | ||||

| (44) |

provided that model (6) is correctly specified but model (9) may be misspecified. In fact, under correctly specified model (6), coincides with (Tan 2020a) and hence condition (44) holds. Moreover, condition (43) follows from the gradient equation for as a minimizer of the expected loss (33) for , because is a subvector of and the gradient of (33) at matches the expectation of in (43) with replaced by :

From conditions (43)–(44), the sum of the two terms and can be shown to be of order , which becomes and hence (42) leads to (40) for provided that .

Similarly, to show (41) for , consider a Taylor expansion

| (45) |

where the remainder is taken to be under suitable conditions, and

Here and denotes the derivative of . Under correctly specified model (6), coincides with (Tan 2020a) and hence the expectations of the gradients and reduce to 0,

| (46) |

Moreover, whether model (10) is correctly specified or not, the expectation of the gradient reduces to 0,

| (47) |

because is a subvector of , and is defined as a minimizer of the expected loss (34) for such that the following gradient is 0 at :

From these mean-zero conditions on the gradients, the sum of three terms . , and can be shown to be of order , which becomes and hence (45) leads to (41) for provided that , where .

Remark 4 (On likelihood vs calibrated estimation).

We compare calibrated estimation with usual likelihood-based estimation. From the preceding discussion, the mean-zero conditions (43)–(44) and (46)–(47) are crucial for the desired expansions (40)–(41) to hold. For example, if the expectations of and were nonzero, then the two terms and in (42) would be of order and in high-dimensional settings, as seen from (37)–(38). These mean-zero conditions can be satisfied in different manners. If models (6) and (9)–(10) are correctly specified, then (43)–(44) and (46)–(47) directly hold, with the target values identical to the true values . This reasoning is applicable with replaced by the regularized likelihood estimators , and would lead to asymptotic expansion (19) for , as studied in Chernozhukov et al. (2018). In contrast, for our method, while conditions (44) and (47) are satisfied by relying on model (6) being correctly specified, conditions (43) and (46) are achieved with possible misspecification of models (9)–(10), by carefully choosing (“calibrating”) the loss functions for the estimators and . Effectively, the loss function (24) and (26) for and are derived by integrating with respect to and respectively the gradients of and in , in the case of . See Tan (2020b, Section 3.2) for a related discussion.

Remark 5 (On low- vs high-dimensional estimation).

Our preceding discussion is mainly concerned with high-dimensional settings where the numbers of regressors , , and are close to or larger than the sample size . The asymptotic expansions (40)–(41) from calibrated estimation are desirable in facilitating construction of confidence intervals, because the first-order terms such as and are made to be negligible up to order . Otherwise, these first-order terms would be at least of order and difficult to quantify. For completeness, it should also be noted that for previous methods studied in low-dimensional settings (Tan 2006a, Ogburn et al. 2015), valid confidence intervals can be obtained from the more general asymptotic expansions (42) and (45) along with usual influence functions for likelihood-based or similar estimators ), where the first-order terms are of order .

Remark 6 (On choices of model-assisted inference).

Our method allows model-assisted inference, relying on correct specification of instrument propensity score model (6) but not treatment and outcome regression models (9)–(10). Similar ideas can be employed to develop model-assisted inference relying on correct specification of models (9)–(10) but not model (6), or doubly robust inference relying on correct specification of either model (6) or models (9)–(10). In each case, additional modifications would be needed with increasing analytical and computational complexity. For example, model (6) needs to be properly expanded such that regularized estimation of could be designed to satisfy all three mean-zero conditions in (43) and (46). In contrast, by handling model-assisted inference based on model (6), our method is developed in a practically convenient manner, involving sequential estimation in the three models (6), (9), and (10).

Remark 7 (On asymmetry between propensity score and outcome regression).

Our choice of inference based on instrument propensity score model (6) is also related to a fundamental asymmetry between propensity score and outcome regression approaches (Tan 2007). As reflected by the estimator (11), fitted treatment and outcome regression functions and are desired to be valid for all observed covariates , but such functions for those values of with close to 0 are effectively determined by extrapolation according to models (9)–(10), which can be built and checked from only the truncated data . In contrast, model (6) can be readily learned from without data truncation.

Remark 8 (On calibrated estimation for propensity scores).

By a careful examination of the outline above, our theoretical analysis also remains valid with replaced by the regularized likelihood estimator . In particular, the mean-zero conditions (44) and (47) would still be satisfied under correctly specified model (6). Nevertheless, we prefer the regularized likelihood estimator for two additional reasons. One is the informative form of the KKT condition (29). The other is an advantage of calibrated estimation in controlling relative errors of propensity scores for inverse probability weighting, regardless of outcome regression, as studied in Tan (2020a).

In the remainder of this section, we present formal results underlying Proposition 1. While convergence of the regularized calibrated estimators and the AIPW estimator for can be obtained directly from Tan (2020b), our analysis needs to carefully tackle convergence of and the AIPW estimator for . The situation is more complicated than in Tan (2020b), as well as the earlier literature on Lasso penalized -estimation (Buhlmann & van de Geer 2011; Huang & Zhang 2012), mainly because the loss function for , i.e., from (26), involves not only data-dependent weight but also data-dependent mean function . We extend a technical strategy in Tan (2020b) to control such dependency and establish the desired convergence of under similar conditions as required in unweighted Lasso penalized -estimation in high-dimensional settings. The error bounds obtained, however, depend on the sparsity sizes of the target values and , in addition to that of .

First, we summarize the results which can be deduced directly from Tan (2020b) about and the AIPW estimator for . Suppose that the Lasso tuning parameters are specified as for in (20) and for in (23), where and . For a matrix with row indices , a compatibility condition (Buhlmann & van de Geer 2011) is said to hold with a subset and constants and if for any vector satisfying .

Assumption 1.

Suppose that the following conditions are satisfied.

-

(i)

almost surely for a constant .

-

(ii)

is bounded below by a constant almost surely.

-

(iii)

A compatibility condition holds for with the subset and some constants and , where .

-

(iv)

is sufficiently small.

Assumption 2.

Suppose that the following conditions are satisfied.

-

(i)

almost surely for a constant .

-

(ii)

is bounded in absolute values by almost surely.

-

(iii)

for any , where is a constant.

-

(iv)

A compatibility condition holds for with the subset , and some constants and , where .

-

(v)

is sufficiently small.

Theorem 1 (Tan 2020b).

Suppose that Assumptions 1–2 hold and . For sufficiently large constants and , we have probability ,

| (48) | |||

| (49) |

where , , and are positive constants and and are sample versions of and . i.e., and . Moreover, if model (6) is correctly specified, then we also have with probability ,

| (50) | |||

| (51) |

where and are positive constants.

Inequalities (48)–(49) lead directly to the desired convergence (37)–(38) for . Moreover, inequality (50) yields the asymptotic expansion (40) for the AIPW estimator provided . Inequality (51) can be used to show that the sample variance is a consistent estimator for , provided , which is satisfied under . While consistent variance estimation is sufficient for justifying Wald confidence intervals for by the Slutsky theorem, the convergence rate in (51) can be improved under additional conditions. See Tan (2020b, Theorem 4).

Next, we discuss theoretical analysis of , with the Lasso tuning parameter in (25), where . As the loss is convex in , the corresponding Bregman divergence is defined as

The symmetrized Bregman divergence is easily shown to be

| (52) |

After statement of the assumptions required, Theorem 2 establishes the convergence of to the target value in the both norm and the symmetrized Bregman divergence.

Assumption 3.

Suppose that the following conditions are satisfied.

-

(i)

almost surely for a constant .

-

(ii)

is uniformly sub-gaussian given with parameters .

-

(iii)

is bounded in absolute values by almost surely.

-

(iv)

for any , where is a constant.

-

(v)

A compatibility condition holds for with the subset , and some constants and , where .

- (vi)

Theorem 2.

From the proof, an upper bound can also be obtained with probability on the weighted prediction norm (in the scale of linear predictors),

| (54) |

where is the sample version of , i.e., . For notational simplicity of subsequent discussion, let be a constant such that the right-hand side of (53) is upper bounded by . Then we have with probability ,

which lead to the desired convergence (39). With the preceding results for , Theorem 3 provides an error bound for the AIPW estimator for .

Theorem 3.

Inequality (55) yields the asymptotic expansion (41) for the AIPW estimator provided . Inequality (56) can be used to show that the sample variance is a consistent estimator for , provided , which is satisfied under .

Our theoretical analysis above deals with convergence of and the asymptotic expansions of the AIPW estimators for and , i.e., (40) and (41) with . Similar results can be obtained as Theorems 1–3 with replaced by and replaced by , provided that Assumptions 1–3 are modified accordingly. Combining both results for and leads to Proposition 1 by standard arguments.

4 Simulation studies

We present simulation studies to compare pointwise properties of based on regularized likelihood estimation without or with post-Lasso refitting and based on regularized calibrated estimation and coverage properties of the associated confidence intervals. In addition, motivated by Remark 3, we compare these methods with the IPW (i.e. Wald) estimator , with , in the setting where the instrument is assumed to be completely randomized.

4.1 Implementation details

Both the regularized likelihood and calibrated methods are implemented using the R package RCAL (Tan 2020a). The penalized versions of loss functions (8), (12) and (13) for computing , and , or penalized loss functions (20), (23) and (25) for computing , and , are minimized for fixed tuning parameters using algorithms similar to those in Friedman et al. (2010), but with the coordinate descent method replaced by an active set method as in Osborne et al. (2000) for solving each Lasso penalized least squares problem. All variables in , and are standardized to have sample means 0 and variances 1.

We determine the value of the Lasso tuning parameter using 5-fold cross validation based on the corresponding loss function. Let be a -fold random partition of the observation indices . For a loss function , either the average negative log-likelihood in (8), or the calibration loss in (21)–(22) for , denote by the loss function obtained when the sample average is computed over only the subsample indexed by . The 5-fold cross-validation criterion is defined as , where is a minimizer of the penalized loss over the subsample of size indexed by , the complement of . Then is selected by minimizing over the discrete set , where for , the value is computed as either when the likelihood loss (8) is used, or or when calibration loss (21) or (22) is used respectively. It can be shown that in each case, the penalized loss over the original sample of size has a minimum at for all .

The computation of or proceeds similarly as above. In the latter case, cross-validation based on is performed with held at the fixed value obtained in the prior step, and cross-validation based on is performed with held at the fixed values in the prior steps.

4.2 Conditionally randomized instrument

Let be independent variables where each is truncated to the interval , and then standardized to have mean 0 and variance 1. Consider the transformed variables , , and . Let , where for , and for . This setup follows that in the preprint of Tan (2020b) and ensures strict one-to-one mapping between and . Figure S1 in the Supplement shows the scatter plots from a simulated data sample of the variables , which are correlated with each other as would be found in real data. Consider the following data-generating configurations:

-

(C1)

Generate given from a Bernoulli distribution with . Then, independently, generate from a standard Logistic distribution, and from a Normal distribution with variance 1 and mean .

-

(C2)

Generate as in (C1), but generate and from a Normal distribution with variance 1 and mean .

-

(C3)

Generate given from a Bernoulli distribution with , then generate as in (C1).

Set if . The observed data consist of independent and identically distributed copies . Consider the following model specifications:

-

(M1)

Logistic instrument propensity score model (6), logistic -outcome model (9) and linear -outcome model (10) with for .

-

(M2)

Logistic instrument propensity score model (6) and logistic -outcome model (9) with for , and linear -outcome model (10) with , , , , , and , , where is the quartile of the fitted values and .

For (M2), linear spline bases are included as additional functions in . As discussed in Remark 2, the dependence of on is in general unknown. A simple strategy is then to incorporate splines bases in to enlarge -outcome model.

| (C1) cor IPS, more cor OR | (C2) cor IPS, less cor OR | (C3) mis IPS, more cor OR | |||||||

| RCAL | RML | RML2 | RCAL | RML | RML2 | RCAL | RML | RML2 | |

| (M1) | |||||||||

| Bias | |||||||||

| .433 | .435 | .896 | .518 | .521 | 1.231 | .429 | .434 | .804 | |

| .418 | .400 | 2.533 | .510 | .486 | 11.410 | .418 | .422 | .957 | |

| Cov90 | .854 | .811 | .868 | .889 | .830 | .848 | .886 | .876 | .885 |

| Cov95 | .908 | .889 | .930 | .935 | .897 | .898 | .932 | .933 | .939 |

| (M2) | |||||||||

| Bias | |||||||||

| .432 | .438 | .752 | .522 | .521 | 1.301 | .427 | .433 | .784 | |

| .415 | .401 | 1.290 | .509 | .486 | 11.804 | .415 | .422 | .790 | |

| Cov90 | .848 | .803 | .872 | .884 | .832 | .851 | .884 | .877 | .883 |

| Cov95 | .909 | .882 | .928 | .933 | .895 | .894 | .937 | .929 | .941 |

| (M1) | |||||||||

| Bias | |||||||||

| .428 | .424 | .632 | .518 | .521 | .749 | .438 | .451 | .961 | |

| .411 | .393 | .600 | .493 | .477 | .742 | .411 | .413 | .816 | |

| Cov90 | .837 | .808 | .832 | .879 | .831 | .833 | .882 | .864 | .857 |

| Cov95 | .900 | .869 | .901 | .933 | .888 | .899 | .945 | .924 | .920 |

| (M2) | |||||||||

| Bias | |||||||||

| .430 | .424 | .632 | .515 | .520 | .759 | .441 | .450 | .714 | |

| .407 | .393 | .605 | .491 | .476 | .744 | .407 | .412 | .677 | |

| Cov90 | .820 | .803 | .831 | .874 | .824 | .828 | .875 | .862 | .858 |

| Cov95 | .880 | .868 | .900 | .929 | .888 | .894 | .939 | .928 | .917 |

Note: RCAL denotes , RML denotes and RML2 denotes the variant where the nuisance parameters are estimated by refitting models with only the variables selected from the corresponding Lasso estimation. Bias and are the Monte Carlo bias and standard deviation of the points estimates, is the square root of the mean of the variance estimates, and Cov90 or Cov95 is the coverage proportion of the 90% or 95% confidence intervals, based on 1000 repeated simulations. The true values of under (C1)–(C3) are calculated using Monte Carlo integration with 100 repeated samples each of size .

The instrument propensity score (IPS) model is correct in configurations (C1) and (C2) but misspecified in (C3). The outcome regression (OR) -model is correct in configurations (C1) and (C3), but misspecified in (C2), while the -model in either (M1) or (M2) is misspecified in all configurations (C1)–(C3), but it can be regarded as being “closer” to the truth in (C1) and (C3) than in (C2) due to using instead of as regressors. Therefore the models in both (M1) and (M2) can be classified as follows in configurations (C1)–(C3):

-

(C1)

IPS model correctly specified, OR models “more correctly” specified;

-

(C2)

IPS model correctly specified, OR models “less correctly” specified;

-

(C3)

IPS model misspecified, OR models “more correctly” specified.

Similarly as in Kang & Schafer (2007) for , the OR - and -models in case (C2) and IPS model in (C3) appear adequate by standard diagnosis techniques. See Figures S2–S4 in the Supplement for scatterplots of against within , boxplots of within and as well as boxplots of within and for .

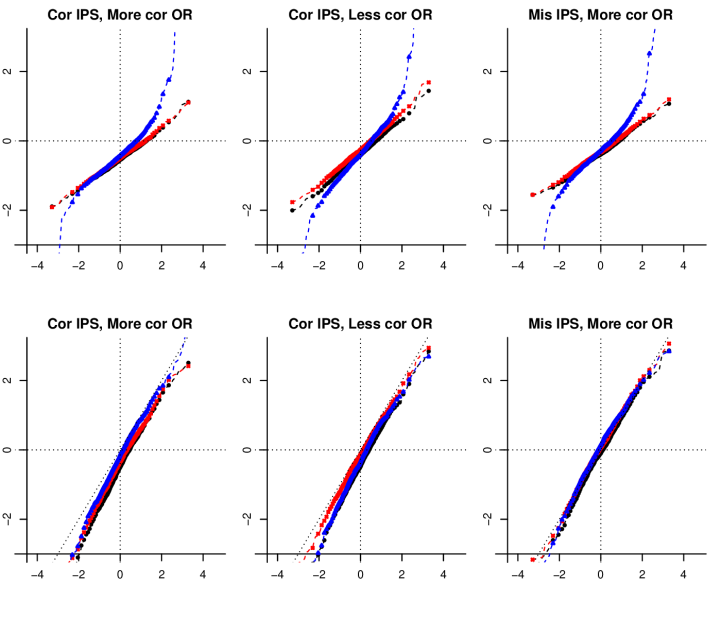

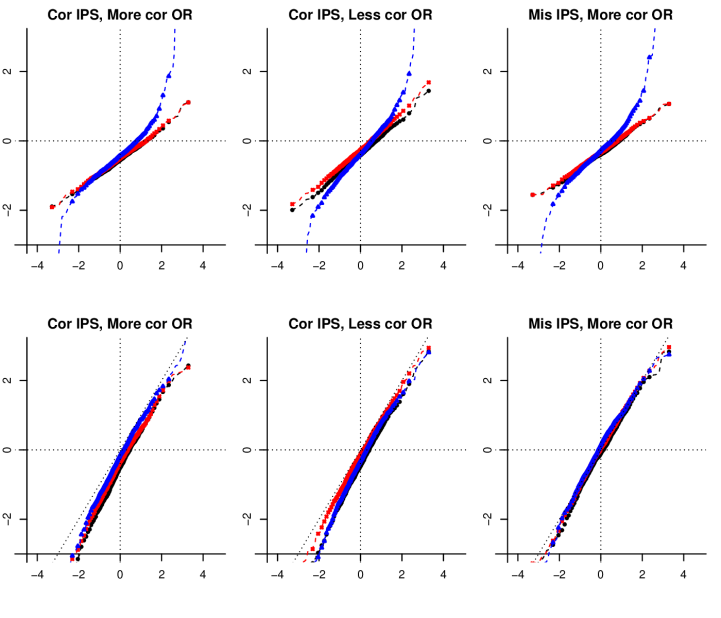

For and or , Table 1 summarizes the results based on 1000 repeated simulations. The methods RCAL and RML perform similarly to each other in terms of absolute bias, variance and coverage in (C1) and (C3), but RCAL yields noticeably smaller absolute biases and better coverage than RML and RML2 in (C2). The post-Lasso refitting method RML2 appears to achieve coverages closer to the nominal probabilities in (C1), but yield substantially higher variances in all three cases (C1)–(C3). These properties can also be seen from the QQ-plots of the estimates and t-statistics in Figures S5–S8 in the Supplement. The performances of each of the three methods are similar with models (M1) or (M2) specified. Hence in the settings studied, there is little benefit in adding the spline terms in the outcome -model.

4.3 Completely randomized instrument

We generate data under the following configurations with a completely randomized instrument:

-

(C4)

Generate from a Bernoulli distribution with , and, independently, generate from a standard Logistic distribution. Then, generate and from a Normal distribution with variance 1 and mean .

-

(C5)

Generate as in (C4), but generate and from a Normal distribution with variance 1 and mean .

For and , Table 2 summarizes the results based on 1000 repeated simulations. See the Supplement for results. The methods RCAL, RML and IPW yield small bias and adequate coverage proportions in (C4) and (C5). The refitting method RML2 also yields small bias, but coverage proportions noticeably below the nominal probabilities. The average interval lengths, , from RCAL and RML are comparable, and are shorter than those of IPW in (C4), and shorter in (C5). Such efficiency gains are comparable to those reported in previous simulation studies dealing with the average treatment effect, e.g. the interval lengths of Lasso-adjusted methods are shorter than those of the unadjusted difference-of-means estimator in Bloniarz et al. (2016). In instrumental variable analysis, such variance reduction is particularly helpful because the Wald estimator usually suffers from large standard errors.

| (C4) cor IPS, more cor OR | (C5) cor IPS, less cor OR | |||||||

| IPW | RCAL | RML | RML2 | IPW | RCAL | RML | RML2 | |

| (M1) | ||||||||

| Bias | .019 | .046 | .015 | .020 | ||||

| .439 | .409 | .406 | .424 | .544 | .521 | .522 | .545 | |

| .444 | .410 | .401 | .378 | .529 | .501 | .498 | .473 | |

| Cov90 | .903 | .904 | .902 | .843 | 890 | .889 | .886 | .829 |

| Cov95 | .952 | .956 | .951 | .925 | 937 | .942 | .937 | .908 |

| (M2) | ||||||||

| Bias | .021 | |||||||

| .411 | .405 | .424 | .520 | .521 | .545 | |||

| — | .407 | .401 | .379 | — | .500 | .498 | .474 | |

| Cov90 | .903 | .907 | .843 | .889 | .890 | .836 | ||

| Cov95 | .949 | .948 | .922 | .942 | .939 | .901 | ||

Note: See the footnote of Table 1. IPW denotes , with asymptotic variance estimated by accounting for variation of .

5 Effect of education on earnings

The causal relationship between education and earnings has been of considerable interest in economics. Card (1995) proposed proximity to college as an instrument for completed education. The argument is that proximity to college could be taken as being randomized conditionally on observed covariates, and its influence on earnings could be only through that on schooling decision. Consider the analytic sample in Card (1995) from National Longitudinal Survey (NLS) of Young men, which comprises 3,010 men with valid education and wage responses in the 1976 interview. Similarly as in Tan (2006a), we define the treatment as education after high school, i.e. , the instrument a binary indicator for proximity to a 4-year college, and the outcome a surrogate outcome constructed for the log of hourly earnings at age 30. The raw vector of covariates include a race indicator, indicators for nine regions of residence and for residence in SMSA in 1966, mother’s and father’s years of schooling (momed and daded respectively) and indicators for missing values, indicators for living with both natural parents, with one natural parent and one step parent, and with mother only at age 14, and the Knowledge of World of Work score (kww) in 1966 and a missing indicator. We use mean imputation for the missing values, and standardize all continuous variables with sample means 0 and variances 1.

We reanalyze the NLS data to estimate LATE of education beyond high school on log hourly earnings, using more flexible, higher dimensional models than previously allowed. We apply based on regularized calibrated estimation (RCAL) and based on regularized likelihood estimation (RML) as well as the post-Lasso variant (RML2). The specification for consists of all the indicator variables mentioned above, momed, daded, linear spline bases in kww as well as interactions between the spline terms with all the indicator variables. The vector augments and by adding linear spline terms for each fitted treatment regression , . We vary the model complexity by considering the number of knots in the set , with knots at the -quantiles for . The tuning parameter is determined using -fold cross validation based on the corresponding penalized loss functions, as described in Section 4. As an anchor specification, we also consider main-effect models with and , whereby the nuisance parameters are estimated using non-penalized likelihood or calibration estimation.

| RCAL | RML | RML2 | |

|---|---|---|---|

| Non-penalized main effects | |||

| — | |||

| LATE | |||

| Linear spline with 3 knots | |||

| LATE | |||

| Linear spline with 9 knots | |||

| LATE | |||

| Linear spline with 15 knots | |||

| LATE | |||

Note: Estimate standard error. As defined in Section 2.2, , , or is the number of regressors in IPS, outcome -model, or outcome -model.

Table 3 shows the estimates of and LATE of education beyond high school on log hourly earnings. Regularized estimation from RCAL, RML and RML2 yield similar point estimates; the differences are small compared with the standard errors. The RCAL and RML estimates have noticeably smaller standard errors than RML2. Interestingly, for splines with 15 knots, the LATE is estimated from RCAL with 95% confidence interval , which excludes 0, whereas those from RML and RML2 include 0.

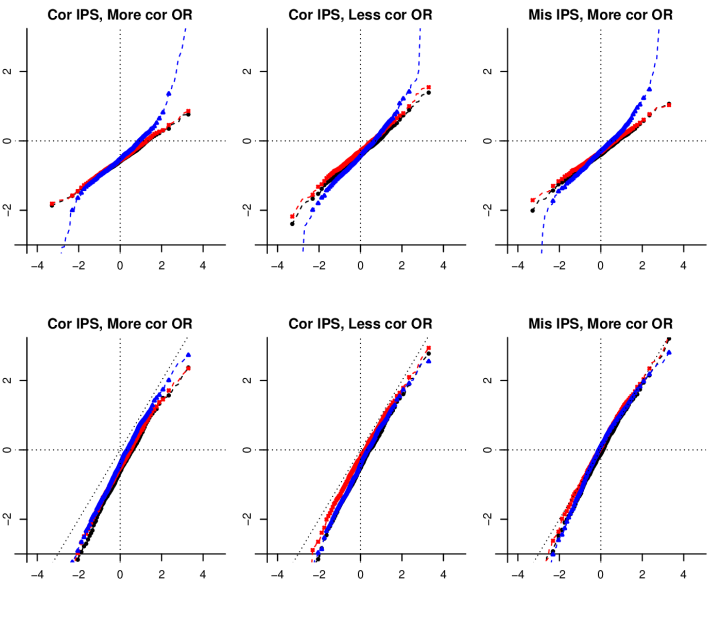

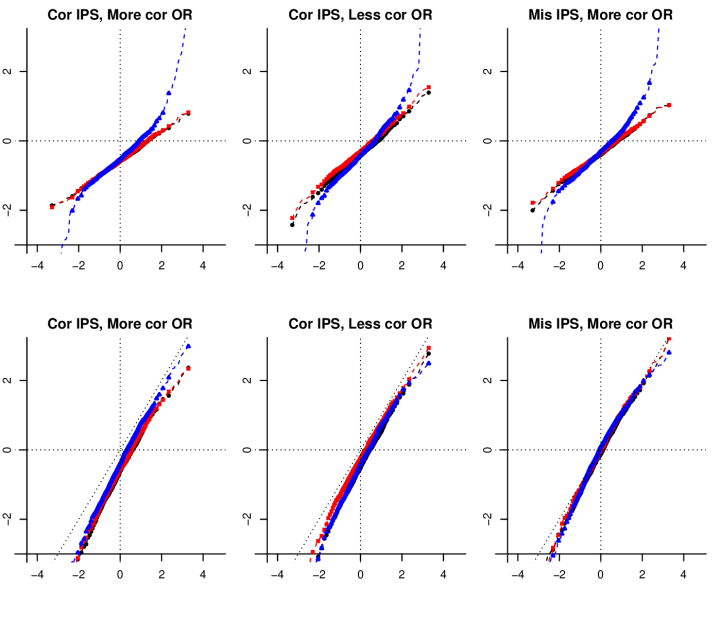

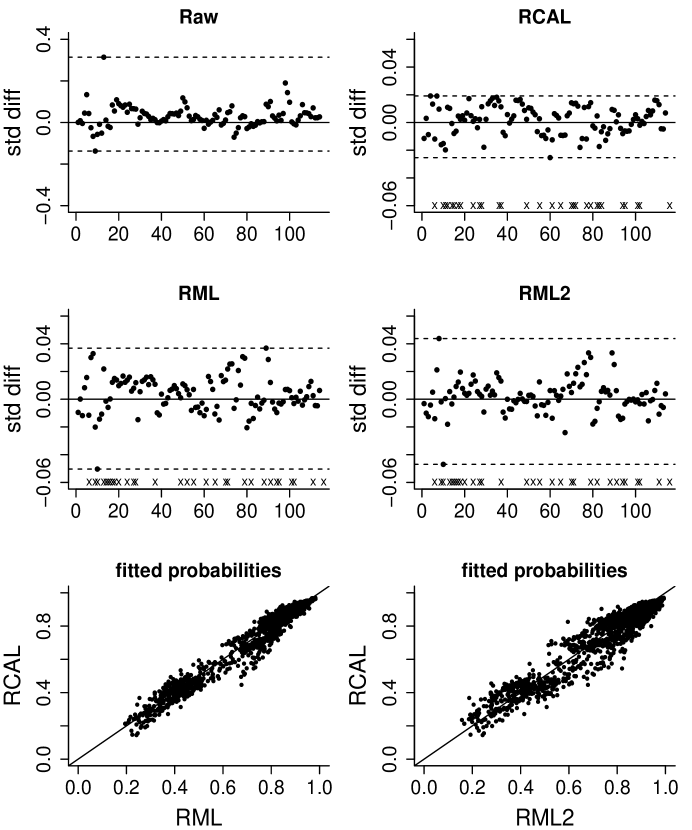

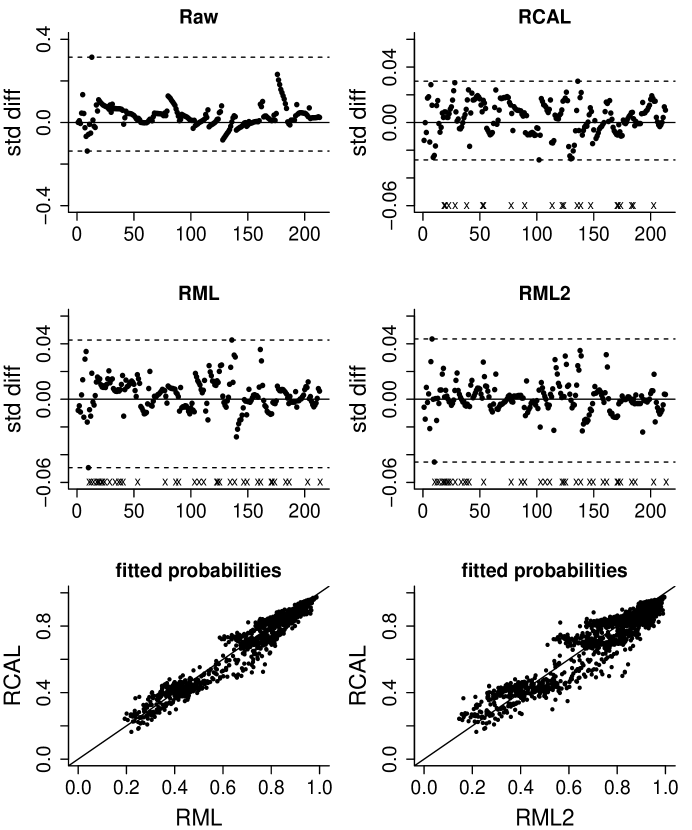

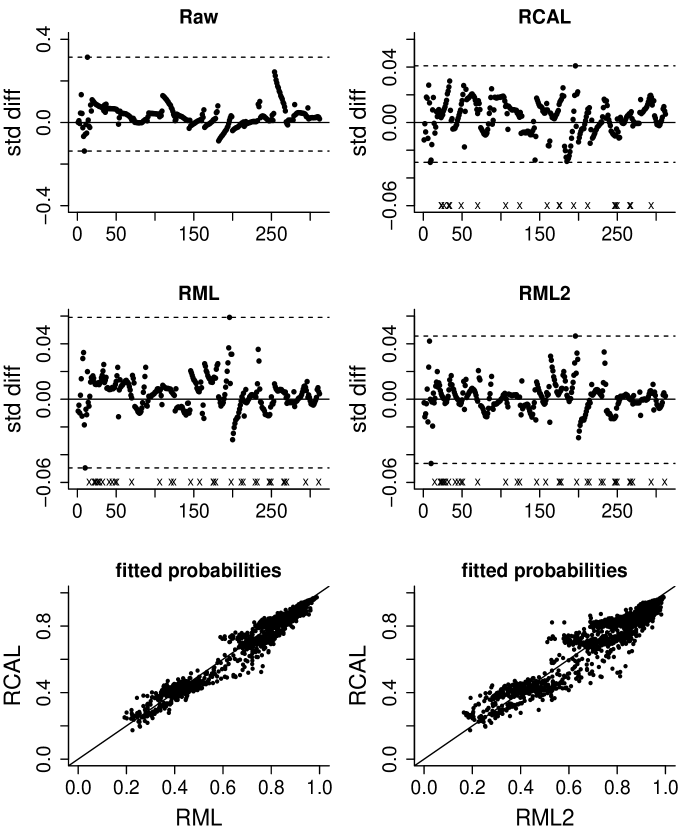

While the validity of confidence intervals is difficult to assess using real data, Figure S9 in the Supplement shows that the standardized sample influence functions for estimation of LATE. The curves from RCAL appear to be more normally distributed than RML or RML2, especially in the tails. In addition, Figures S10–S12 in the Supplement present the standardized calibration differences for all the variables , , similarly as in Tan (2020a). Compared with RML and RML2, our method RCAL consistently yields smaller maximum absolute standardized differences and involves fewer nonzero estimates of in IPS models.

6 Conclusion

We develop a computationally tractable method and appropriate theoretical analysis, to obtain model-assisted confidence intervals for population LATEs in high-dimensional settings. There are various interesting topics which warrant further investigation. Both the instrument and treatment are assumed to be binary here. It is desirable to extend our method to handle multi-valued instruments and treatments and to estimate treatment effects under other identification assumptions. Another methodological question is whether doubly robust confidence intervals can be derived in a computationally and theoretically satisfactory manner for practical use.

References

-

Abadie, A. (2003) Semiparametric instrumental variable estimation of treatment response models, Journal of Econometrics, 113, 231–263.

-

Angrist, J.D., Imbens, G.W. and Rubin, D.B. (1996) Identification of causal effects using instrumental variables, Journal of the American Statistical Association, 91, 444–455.

-

Avagyan, V. and Vansteelandt, S. (2017) Honest data-adaptive inference for the average treatment effect under model misspecification using penalised bias-reduced double-robust estimation, arXiv preprint, arXiv:1708.03787.

-

Bloniarz, A., Liu, H., Zhang, C., Sekhon, J.S. and Yu, B. (2016) Lasso adjustments of treatment effect estimates in randomized experiments, Proceedings of the National Academy of Sciences, 113, 7383–7390.

-

Baiocchi, M., Cheng, J., and Small, D.S. (2014). Instrumental variable methods for causal inference, Statistics in Medicine, 33, 2297–2340.

-

Belloni, A., Chernozhukov, V. and Hansen, C. (2014) Inference on treatment effects after selection among high-dimensional controls, The Review of Economic Studies, 81, 608–650.

-

Bradic, J., Wager, S. and Zhu, Y. (2019) Sparsity double robust inference of average treatment effects, arXiv preprint, arXiv:1905.00744.

-

Buhlmann, P. and van de Geer, S. (2011) Statistics for High-Dimensional Data: Methods, Theory and Applications, New York: Springer.

-

Card, D. (1995) Using geographic variation in college proximity to estimate the return to schooling, in Aspects of Labour Market Behaviour: Essays in Honour of John Vanderkamp, 201–222, Toronto: University of Toronto Press.

-

Chernozhukov, V., Chetverikov, D., Demirer, M., Duflo, E., Hansen, C., Newey, W. and Robins, J.M. (2018) Double/debiased machine learning for treatment and structural parameters, The Econometrics Journal, 21, C1–C68.

-

Davidian, M., Tsiatis, A.A. and Leon, S. (2005) Semiparametric estimation of treatment effect in a pretest–posttest study with missing data, Statistical Science, 20, 261–301.

-

Farrell, M. (2015) Robust inference on average treatment effects with possibly more covariates than observations, Journal of Econometrics, 189, 1–23.

-

Friedman, J., Hastie, T. and Tibshirani, R. (2010). Regularization paths for generalized linear models via coordinate descent, Journal of Statistical Software, 33, 1–22.

-

Frölich, M. (2007) Nonparametric IV estimation of local average treatment effects with covariates, Journal of Econometrics, 139, 35–75.

-

Hirano, K., Imbens, G.W., Rubin, D.B. and Zhou, X.-H. (2000), Assessing the effect of an influenza vaccine in an encouragement design, Biostatistics, 1, 69–88.

-

Huang, J. and Zhang, C.-H. (2012) Estimation and selection via absolute penalized convex minimization and its multistage adaptive applications, Journal of Machine Learning Research, 13, 1839–-1864.

-

Imbens, G.W. (2014) Instrumental variables: An econometrician’s perspective, Statistical Science, 29, 323–358.

-

Kang, J.D.Y. and Schafer, J.L. (2007) Demystifying double robustness: A comparison of alternative strategies for estimating a population mean from incomplete data, Statistical Science, 4, 523–539.

-

Kim, J.K. and Haziza, D. (2014) Doubly robust inference with missing data in survey sampling, Statistica Sinica, 24, 375–394.

-

Little, R.J.A. and Yau, L. (1998). Statistical techniques for analyzing data from prevention trials: Treatment of no-shows using Rubin’s causal model, Psychological Methods, 3, 147–159.

-

McCullagh, P. and Nelder, J. (1989) Generalized Linear Models (2nd edition), New York: Chapman & Hall.

-

Neyman, J. (1990) On the application of probability theory to agricultural experiments. Essay on principles. Section 9, Statistical Science, 5, 465–472.

-

Ning, Y., Peng, S. and Imai, K. (2020) Robust estimation of causal effects via high-dimensional covariate balancing propensity score, Biometrika, to appear.

-

Ogburn, E.L., Rotnitzky, A. and Robins, J.M. (2015) Doubly robust estimation of the local average treatment effect curve, Journal of the Royal Statistical Society, Ser. B, 77, 373–396.

-

Okui, R., Small, D.S., Tan, Z. and Robins, J.M. (2012) Doubly robust instrumental variable regression, Statistica Sinica, 22, 173–205.

-

Osborne, M., Presnell, B., and Turlach, B. (2000) A new approach to variable selection in least squares problems, IMA Journal of Numerical Analysis, 20, 389-–404.

-

Robins, J.M. (1994) Correcting for non-compliance in randomized trials using structural nested mean models, Communications in Statistics-Theory and methods, 23, 2379–2412.

-

Robins, J.M., Rotnitzky, A. and Zhao, L.P. (1994) Estimation of regression coefficients when some regressors are not always observed, Journal of the American Statistical Association, 89, 846–866.

-

Rubin, D.B. (1974) Estimating causal effects of treatments in randomized and nonrandomized studies, Journal of educational Psychology, 66, 688–701.

-

Särndal, C.E., Swensson, B. and Wretman, J. (2003) Model Assisted Survey Sampling, Springer Science & Business Media.

-

Smucler, E., Rotnitzky, A. and Robins, James M. (2019) A unifying approach for doubly-robust regularized estimation of causal contrasts, arXiv preprint, arXiv:1904.03737.

-

Tan, Z. (2006a) Regression and weighting methods for causal inference using instrumental variables, Journal of the American Statistical Association, 101, 1607–1618.

-

Tan, Z. (2006b) A distributional approach for causal inference using propensity scores, Journal of the American Statistical Association, 101, 1619–1637.

-

Tan, Z. (2007) Comment: Understanding OR, PS and DR, Statistical Science, 22, 560–568.

-

Tan, Z. (2010a) Marginal and nested structural models using instrumental variables, Journal of the American Statistical Association, 105, 157–169.

-

Tan, Z. (2010b) Bounded, efficient, and doubly robust estimation with inverse weighting, Biometrika, 97, 661–682.

-

Tan, Z. (2020a) Regularized calibrated estimation of propensity scores with model misspecification and high-dimensional data, Biometrika, 107, 137–158.

-

Tan, Z. (2020b) Model-assisted inference for treatment effects using regularized calibrated estimation with high-dimensional data, Annals of Statistics, 48, 811–837.

-

Tibshirani, R. (1996) Regression shrinkage and selection via the lasso, Journal of the Royal Statistical Society, Ser. B, 58, 267–288.

-

Uysal, S.D. (2011) Doubly robust IV estimation of the local average treatment effects, Unpublished manuscript.

-

van de Geer, S., Buhlmann, P., Ritov, Y. and Dezeure, R. (2014) On asymptotically optimal confidence regions and tests for high-dimensional models, Annals of Statistics, 42, 1166–1202.

-

Vansteelandt, S.and Goetghebeur, E. (2003) Causal inference with generalized structural mean models, Journal of the Royal Statistical Society, Ser. B, 65, 817–835.

-

Vermeulen, K. and Vansteelandt, S. (2015) Bias-reduced doubly robust estimation, Journal of the American Statistical Association, 110,1024–1036.

-

Vytlacil, E. (2002) Independence, monotonicity, and latent index models: An equivalence result, Econometrica, 70, 331–341.

-

Wager, S., Du, W., Taylor, J. and Tibshirani, R.J. (2016) High-dimensional regression adjustments in randomized experiments, Proceedings of the National Academy of Sciences, 113, 12673–12678.

-

Wang, L., and Tchetgen Tchetgen, E. (2019) Bounded, efficient and multiply robust estimation of average treatment effects using instrumental variables, Journal of the Royal Statistical Society, Ser. B, 80, 531–550.

-

Wright, P.G. (1928) Tariff on Animal and Vegetable Oils, Macmillan Company, New York.

-

Zhang, C.-H. and Zhang, S.S. (2014) Confidence intervals for low-dimensional parameters with high-dimensional data, Journal of the Royal Statistical Society, Ser. B, 76, 217–242.

Supplementary Material for

“High-dimensional Model-assisted Inference for Local Average Treatment Effects with Instrumental Variables

Baoluo Sun & Zhiqiang Tan

I Additional results in simulation studies

|

| (C4) cor IPS, more cor OR | (C5) cor IPS, less cor OR | |||||||

| IPW | RCAL | RML | RML2 | IPW | RCAL | RML | RML2 | |

| (M1) | ||||||||

| Bias | .019 | .046 | .023 | .029 | .040 | |||

| .439 | .424 | .417 | .435 | .544 | .508 | .508 | .526 | |

| .444 | .408 | .400 | .378 | .529 | .504 | .500 | .529 | |

| Cov90 | .903 | .891 | .885 | .841 | .890 | .903 | .900 | .889 |

| Cov95 | .952 | .946 | .942 | .906 | .937 | .943 | .945 | .936 |

| (M2) | ||||||||

| Bias | .023 | .030 | .004 | |||||

| .423 | .416 | .432 | .506 | .508 | .514 | |||

| — | .407 | .400 | .378 | — | .504 | .500 | .476 | |

| Cov90 | .889 | .891 | .844 | .903 | .903 | .879 | ||

| Cov95 | .942 | .940 | .911 | .946 | .947 | .931 | ||

| (M1) | ||||||||

| Bias | .015 | .020 | ||||||

| .409 | .406 | .424 | .521 | .522 | .545 | |||

| — | .410 | .401 | .378 | — | .501 | .498 | .473 | |

| Cov90 | .904 | .902 | .843 | .889 | .886 | .829 | ||

| Cov95 | .956 | .951 | .925 | .942 | .937 | .908 | ||

| (M2) | ||||||||

| Bias | .021 | |||||||

| .411 | .405 | .424 | .520 | .521 | .545 | |||

| — | .407 | .401 | .379 | — | .500 | .498 | .474 | |

| Cov90 | .903 | .907 | .843 | .889 | .890 | .836 | ||

| Cov95 | .949 | .948 | .922 | .942 | .939 | .901 | ||

Note: See the footnote of Table 2. For completeness, the results with and are also included.

II Additional results in empirical application

|

The standardized calibration difference in the group for a function using an estimated is , where denotes the sample variance.

|

|

|

III Technical details

III.1 Probability lemmas

Denote by the event that (48)–(49) hold. Then under Theorem 1. The following Lemmas 1–4 are used in the proof of Theorem 2 (Section III.2).

Lemma 1.

Proof. This can be shown similarly as Lemma 2 in the Supplement of Tan (2020b).

Recall

Lemma 2.

Proof. This can be shown similarly as Lemma 1(ii) in the Supplement of Tan (2020b).

Recall

Lemma 3.

Under Assumptions 1(i)–(ii), there exists a positive constant , depending on , such that , where denotes the event

Proof. This is Lemma 1(ii) in the Supplement of Tan (2020b).

Denote

Lemma 4.

Proof. This can be shown similarly as Lemma 3 in the Supplement of Tan (2020b).

In the event , we have for any vector ,

By Assumption 3(ii), and hence

Combining the preceding three inequalities shows that in the event ,

| (S1) |

Lemma 5.

Proof. This can be shown similarly as Lemma 4 in the Supplement of Tan (2020b).

Similarly as (S1), we have in the event , for any vector ,

| (S2) |

Lemma 6.

Proof. Using (S7), this can be shown similarly as Lemma 13 in the Supplement of Tan (2020b).

Lemma 7.

Proof. Using (S20), this can be shown similarly as Lemma 13 in the Supplement of Tan (2020b).

III.2 Proof of Theorem 2

We split the proof of Theorem 2 into a series of lemmas. The first one is usually called a basic inequality for , but depending on the first-step estimators .

Lemma 8.

For any coefficient vector , we have

| (S3) |

Proof. This can be shown similarly as Lemma 6 in the Supplement of Tan (2020b).

The second lemma deals with the dependency on in the upper bound from the basic inequality (S3). Denote

Lemma 9.

In the event , we have

where and, with ,

Proof. Consider the following decomposition

where

To handle , we have by the mean value theorem and Assumption 1(i),

| (S4) |

By the Cauchy–Schwartz inequality, we have in the event ,

| (S5) |

where . The second step follows because

in the event by (48), (S1) with , and Assumption 3(vi). To handle , we have by the mean value theorem and Assumption 1(i). Moreover, by Assumptions 2(i)–(iii),

| (S6) | |||

| (S7) |

By the Cauchy–Schwartz inequality and Assumption 3(ii), we have in the event ,

| (S8) |

where and . The second step follows by (49) and Assumption 3(vi). Combining (S5)–(S8) yields the desired inequality.

The third lemma derives an implication of the basic inequality (S3) using the triangle inequality for the norm, while incorporating the bound from Lemma 9.

Lemma 10.

Denote . In the event , we have

| (S9) |

Proof. In the event , we have

From this bound and Lemmas 8–9, we have in the event ,

Using the identity for and the triangle inequality for and rearranging the result yields (S9).

The following lemma provides a desired bound relating the Bregman divergence with the quadratic function .

Lemma 11.

In the event , we have for any vector ,

where , , and . Throughout, set for .

Proof. Direct calculation yields

By the mean value theorem and Assumption 1(i), . By inequality (S6) and Assumptions 2(i)–(iii), we have

The first step follows because, with , and hence for any . Then by (48)–(49) and Assumption 3(vi), we obtain in the event ,

where , with . Furthermore, by Assumption 3(iii)–(iv), we have

where . The desired result follows because for .

The following lemma shows that Assumption 3(v), a theoretical compatibility condition for , implies an empirical compatibility condition for .

Lemma 12.

Proof. In the event , we have from Lemma 2. Then Assumption 3(v) implies that for any satisfying ,

where . The last inequality uses . The desired result follows because and by Assumption 3(vi).

The final lemma completes the proof of Theorem 2, because by probability Lemmas 1–4 in Section III.1.

Lemma 13.

For , inequality (53) holds in the event :

Proof. Denote , , , and

In the event , inequality (S9) from Lemma 10 leads to two possible cases: either

| (S10) |

or , that is,

| (S11) |

where because and . We deal with the two cases separately as follows.

If (S11) holds, then , which, by Lemma 12, implies

| (S12) |

By Lemma 11, we have

| (S13) |

Combining (S11), (S12), and (S13) and using yields

| (S14) |

But . Inequality (S14) along with Assumption 3(vi) implies that . As a result, and hence

| (S15) |

From this bound, inequality (S14) then leads to .

If (S10) holds, then simple manipulation using and (S13) together with gives

| (S16) |

Similarly as above, using and inequality (S16) along with Assumption 3(vi), we find . As a result, and hence

| (S17) |

From this bound, inequality (S16) then leads to . Therefore, (53) holds through (S10) and (S11) in the event .

III.3 Proof of Theorem 3

We split the proof into two lemmas. The first one deals with the convergence of the AIPW estimator in (55). Recall from (16) that

Lemma 14.

In the setting of Theorem 2, take and . Then we have in the event ,

where , , , depending on in the proof.

Proof. Consider the following decomposition

| (S18) |

where

Denote , , and . Then

We handle the three terms separately.

First, a Taylor expansion for yields for some ,

denoted as . Because is a subvector of , we have in the event ,

Moreover, we have in the event ,

where . The second step follows because by (48) and (S2) with ,

Combining the preceding inequalities yields

| (S19) |

Second, the term can be decomposed as

denoted as . Similarly as (S7) for , we have

| (S20) |

Combining this inequality with (S4) and (S7) and applying the Cauchy–Schwartz inequality shows that in the event ,

| (S21) |

and, with ,

| (S22) |

where and as in Lemma 9, and . From these two inequalities, we obtain

| (S23) |

Finally, the term can be decomposed as

denoted as . Recall that because model (6) is correctly specified. Take in Lemma 6. Then in the event , we have and hence

where . Take in Lemma 7. Then in the event , we have and hence

where . Hence

| (S24) |

The second lemma deals with the convergence of the mean squared difference between and in (56) for variance estimation.

Lemma 15.

Second, writing and using Assumption 1(i)–(ii), we have

Then we obtain similarly as in (S21)–(S22),

| (S26) |

where and are as in Lemma 14.

Finally, using Assumption 1(i)–(ii), we also have

Then we obtain similarly as in (S21)–(S22) but using the bounds and ,

| (S27) |

where and . Combining (S25)–(S27) yields the desired result.

References

-

Tan, Z. (2020a) Regularized calibrated estimation of propensity scores with model misspecification and high-dimensional data, Biometrika, 107, 137–158.

-

Tan, Z. (2020b) Model-assisted inference for treatment effects using regularized calibrated estimation with high-dimensional data, Annals of Statistics, 48, 811–837.