Generalized distance to a simplex and a new geometrical method for portfolio optimization

Abstract

Risk aversion plays a significant and central role in investors’ decisions in the process of developing a portfolio. In this framework of portfolio optimization we determine the portfolio that possesses the minimal risk by using a new geometrical method. For this purpose, we elaborate an algorithm that enables us to compute any generalized Euclidean distance to a standard simplex. With this new approach, we are able to treat the case of portfolio optimization without short-selling in its entirety, and we also recover in geometrical terms the well-known results on portfolio optimization with allowed short-selling.

Then, we apply our results in order to determine which convex combination of the CAC 40 stocks possesses the lowest risk: not only we get a very low risk compared to the index, but we also get a return rate that is almost three times better than the one of the index.

Keywords: Portfolio optimization without short-selling, generalized distance to a standard simplex, geometrical approach of portfolio optimization, geometrical algorithm.

JEL Classification: G11, C61, C63.

1 Introduction and aims of the article

1.1 Framework

The paper [M52] published by Harry Markowitz in 1952 completely changed the methods of portfolio management and gave birth to the so-called “Modern Portfolio Theory”, thanks to which its author earned the Nobel Prize in Economics in 1990. Since his works and the paper [S63] of Sharpe, this theme centralizes a lot of interest and many developments have been written in this domain. Let us recall some recent and important works to which our article is linked.

In [DJDY08], Jón Daníelsson, Bjørn N. Jorgensen, Casper G. de Vries and Xiaoguang Yang study the portfolio allocation under the probabilistic VaR constraint and obtain remarkable topological results: the set of feasible portfolios is not always connected nor convex, and the number of local optima increases in an exponential way with

the number of states. They propose a solution to reduce computational complexity due to this exponential increase.

In [FS12], Claudio Fontana and Martin Schweizer give a simple approach to mean-variance portfolio problems: they change the problems’ parametrisation from trading strategies to final positions. In this way they are able to solve many quadratic optimisation problems by using orthogonality techniques in Hilbert spaces and providing explicit formulas.

In their important article [BCGD18], Hanene Ben Salah, Mohamed Chaouch, Ali Gannoun and Christian De Peretti (see also the thesis [B15]) define a new portfolio optimization model in which the risks are measured thanks to conditional variance or semivariance. They use returns prediction obtained by nonparametric

univariate methods to make a dynamical portfolio selection and get better performance.

In [PR19], Sarah Perrin and Thierry Roncalli show how four algorithms of optimization (the coordinate descent, the alternating direction method of multipliers, the proximal gradient method and the Dykstra’s algorithm) can be used to solve problems of portfolio allocation.

In [BIPS20], Taras Bodnar, Dmytro Ivasiuk, Nestor Parolya and Wolfgang Schmid make an interesting work about the portfolio choice problem for power and logarithmic utilities: they compute the portfolio weights for these utility functions assuming that the portfolio returns follow an approximate log-normal distribution, as suggested in [B00]. It is also noticeable that their optimal portfolios belong to the set of mean-variance feasible portfolios.

1.2 Aims and organization of the paper

The three aims of this article are the following:

— give a new geometrical algorithm (Algorithm 1) to compute any generalized distance to a simplex,

— determine, by making use of this algorithm, a portfolio with minimal variance,

— apply this technique to the CAC 40 stocks, and get a portfolio with return rate that is almost three times better than the one of the index.

After having briefly explained the notations in Section 1, we expose in Section 2 the portfolio optimization problem and prove by compactness and convexity arguments that it possesses a unique solution.

Then, in Section 3, we solve the problem in the case where short-selling is allowed. For this, we recall the classical method, and we give our very simple geometrical method.

Section 4 is the heart of the article: in this section, we solve the portfolio optimization problem in the case where short-selling is not allowed. For this purpose, we give a new geometrical algorithm to compute the distance from a point to a standard simplex, which can be used for every Euclidean distance.

We can eventually apply this algorithm to the example of the CAC 40 stocks and determine the portfolio with the lowest risk. This portfolio also has the property of being almost three times more efficient than the underlying index. This is done in Section 5.

1.3 Notations

We consider stocks and denote by the random variables that represent their return rate (for example, daily, monthly or yearly). For every , we set (mean of ) and (variance of ). We set

Matrix is the covariance matrix of , and is a random vector.

Definition 1.

We call portfolio (with allowed short-selling) every linear combination , where and .

The return rate of the portfolio is the linear combination .

If we don’t allow short-selling, then every must be nonnegative, and in that case the linear combination is a convex combination.

2 Minimisation of the variance of a portfolio

2.1 The standard simplex of dimension

Let us recall some classical results that we will use in the following.

Proposition 1.

We have and .

Proof.

We immediately have .

Moreover,

hence

∎

The following proposition is immediate.

Proposition 2.

The matrix has the two following properties.

- (i)

-

It is symmetric positive,

- (ii)

-

It is symmetric definite positive if and only if are almost surely affinely independent.

In all the following, we assume that is symmetric definite positive: this is always true in practise.

Let us denote by the affine hyperplane of with equation , and by the standard simplex (also called standard simplex of dimension ), i.e.

The simplex is a Haussdorff compact subset of that is contained in the hyperplane .

For example, if , is the line of equation in the usual plane, and the standard simplex is the segment of this line.

2.2 Existence and uniqueness of the solution

Minimizing the variance of the portfolio is equivalent to finding the minimum on of the quadratic form

Let us consider the scalar product

and the Euclidean norm

The aim is to determine the point of that realizes the minimal distance to from the origin point in the sense of .

As is a Haussdorff compact subset, and as is continuous, we know that this minimum does exist. We will prove that it is also unique. For this, the convexity plays a central role (see for example [R17]).

Proposition 3.

The map is strictly convex.

Proof.

For every and for every , we have

hence

which is nonnegative, as is positive.

Moreover, if , this quantity is positive as is definite positive.

∎

Proposition 4.

Let be a convex domain and a convex map. Then,

- (i)

-

every local minimum of is global,

- (ii)

-

if is strictly convex, then possesses at most one minimum.

Proof.

(i) Let be a local minimum of in . Let us assume by contradiction that it is not global: there exists such that . For every , let us set . Then belongs to , and for small enough, is close enough to , i.e. is close enough to . Thus . As is convex, we have , hence , i.e. , which is a contradiction.

(ii) Let us assume by contradiction that possesses a least two distinct minima and with . Then, as is strictly convex, , which is a contradiction to the fact that is a minimum.

∎

As a consequence of Proposition 4, the quadratic form possesses exactly one minimum on , and his minimum is global.

3 Minimisation of on

In this section, we give two methods to compute the portfolio that possesses the lowest risk: the classical one, and our geometrical approach.

Let us denote by the canonical basis of . A basis of the vector hyperplane that directs is . Moreover, for every , belongs to if and only if .

Let is denote by the vector , which is orthogonal to the hyperplane , and let us set

3.1 Minimisation of on by the classical method

Here we briefly recall the classical method to compute the portfolio that possesses the lowest risk. Several sources, such as [N09], [M10] and [PP14], provide a clear presentation of these well-known tools.

Proposition 5.

The unique solution that minimises the map on is the vector .

Proof.

According to Lagrange’s multipliers theorem, there exists such that . Here we have and , thus , i.e. . As , we get

hence and . ∎

Example 1.

For , the formula is very simple: by setting

we have

and

hence

3.2 Minimisation of on by the geometrical approach

Here we recover the classical results on the portfolio with minimal variance with allowed short-selling by making use of an Euclidean interpretation.

This portfolio is , where is the orthogonal projection onto of the origin point.

Let us define the matrix

Proposition 6.

The unique solution that minimises on is the vector whose coordinates in are given by the last column of the inverse of matrix .

Proof.

For every in , is the orthogonal projection onto of the origin point if and only if is orthogonal to , that is to say, for every , .

Since , we deduce that is the solution if and only if , i.e. , which means that the coordinates in of are given by the last column of .

∎

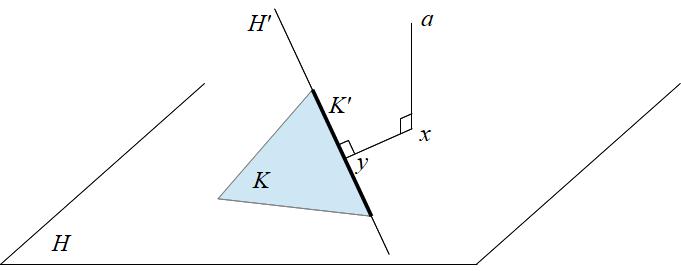

4 Distance to from a point of

In this section, we will solve the problem of portfolio optimization without short-selling, by giving an explicit and calculable solution that doesn’t seem to appear in the literature.

4.1 Projections onto affine hyperplanes of

Let us now consider a subset of and the vector subspace of , identified with , where . Let be the affine hyperplane of defined by the equation . Let us fix and define by , and let us denote by the complementary of in . Then, a basis of the vector hyperplane of parallel to is .

Let be a point of .

Let us set

then

Proposition 7.

The orthogonal projection of onto is the vector whose nonzero coordinates in are given by , which means that and .

Proof.

For every , is the orthogonal projection of onto if and only if the three following conditions hold

-

(i)

for every , ,

-

(ii)

,

-

(iii)

for every , is orthogonal to .

Since

we have if and only if

i.e. . ∎

4.2 The algorithm for computing the generalized distance to from a point of

We now propose a recursive algorithm to compute the point realizing the distance to from a point . In his article [C16], L. Condat gave a new and fast algorithm to project a vector onto a simplex. However, his algorithm was made only for the usual Euclidean distance. Our algorithm can be used for every Euclidean distance. The reader can also have a look at the paper [CY11] about the projection onto a simplex.

Algorithm 1.

Entry: (,)

Compute the orthogonal projection of onto

If belongs to

Return

Else

If is a simplex (i.e. has exactly vertices)

Return the vertex that is the closest to

Else

Determine the hyperface of that is the closest to

Compute the orthogonal projection of onto (the affine

subspace defined by )

Apply recursively the algorithm to (,)

Proposition 8.

Algorithm 1 ends.

Proof.

This is straightforward since at each step of the algorithm the dimension of the simplex decreases of one unit. ∎

Lemma 1.

If belongs to , then the distance from to is realized in a point of the frontier of .

Proof.

Let us proceed by contradiction by assuming that the distance from to is realized in a point in . Let us denote by the intersection of the line with an hyperface of crossed by this line. Then, by Minkowski, we get , which is absurd since realizes the minimal distance from to . ∎

As a consequence, if belongs to , then the distance from to is the distance from to the hyperface of that is the closest to .

Proposition 9.

Algorithm 1 is correct.

Proof.

Let us prove by induction on the dimension of that the algorithm provides us such that .

If has dimension , the result is clear.

Now assume that the algorithm is correct for every simplex. Let us consider a simplex (with ), and prove that the algorithm is correct for . Let be the orthogonal projection of onto .

— If belongs to , then is the solution, and the algorithm is correct.

— If does not belong to , as , we consider the simplex defined above, the affine subspace and the orthogonal projection of onto . By induction hypothesis applied to and the simplex , the algorithm provides us such that . In particular, belongs to . Let us now prove that . According to the Pythagorean theorem, as is orthogonal to , we have

thanks to Lemma 1.

Moreover, as is orthogonal to , we have

since is orthogonal to .

Finally, as is orthogonal to , hence and the algorithm is correct for .

∎

Remark 1.

Let be in . Then the hyperface of that is the closest to is not necessarily the hyperface of obtained by suppressing the (or one) vertex of that is the furthest of .

Proof.

Let us consider the following example: let be the simplex in the hyperplane of . Let us set

Then the distances from to the vertices , , are respectively , , .

Now, the projections of onto the edges defined by , , are respectively

and the distances from to these edges are , , .

So we have but . Here, the vertex of that is the furthest of is , but the distance from to is realized in a point of the edge defined by .

∎

4.3 Minimisation of on

Now that we have the algorithm to compute the generalized distance to a standard simplex, it is easy to find the solution that minimises on : the portfolio that possesses the lowest risk is , where is the point of that realizes the distance from the origin point to , i.e. .

5 Application to portfolio optimization

Here we determine the portfolio with lowest risk: we determine the convex combination of CAC 40 stocks222We use the following abbreviations.

AC : Accor SA

ACA : Credit Agricole S.A.

AI : L’Air Liquide S.A.

AIR : Airbus SE

ATO : Atos SE

BN : Danone S.A.

BNP : BNP Paribas SA

CA : Carrefour SA

CAP : Capgemini SE

CS : AXA SA

DG : VINCI SA

DSY : Dassault Systemes SE

EL : EssilorLuxottica Societe anonyme

EN : Bouygues SA

ENGI : ENGIE SA

FP : TOTAL S.A.

GLE : Societe Generale Societe anonyme

HO : Thales S.A.

KER : Kering SA

LR : Legrand SA

MC : LVMH Moet Hennessy - Louis Vuitton

ML : Cie Gle des Et. Michelin

MT : ArcelorMittal

OR : L’Oreal S.A.

ORA : Orange S.A.

PUB : Publicis Groupe S.A.

RI : Pernod Ricard SA

RMS : Hermes International

RNO : Renault SA

SAF : Safran SA

SAN : Sanofi

SGO : Compagnie de Saint-Gobain S.A.

STM : STMicroelectronics N.V.

SU : Schneider Electric

SW : Sodexo S.A.

UG : Peugeot S.A.

URW : Unibail-Rodamco-Westfield

VIE : Veolia Environnement S.A.

VIV : Vivendi

WLN : Worldline

for which the variance is minimal333For this computation, we do not consider EL, GLE and WLN, for which we don’t have enough data..

We use the mean and the standard deviation of monthly444The French stock market month (that ends the third Friday in the month) is used. variation.

5.1 Portfolio optimization from 2007-04-23 to 2020-07-21

Here we consider the period from 2007-04-23 to 2020-07-21, that is to say we start from the highest point of CAC 40 index. Table 1 gives the mean and the standard deviation of stocks’ return rates that appear in the results.

| Stock | AI | BN | CA | DSY | ENGI |

|---|---|---|---|---|---|

| Mean | 0.73% | 0.18% | -0.559% | 1.53% | -0.43% |

| Std. Dev. | 5.73% | 5.55% | 8.02% | 6.58% | 7.06% |

| Stock | HO | ORA | RMS | SAN | VIV |

| Mean | 0.53% | -0.18% | 1.6% | 0.4% | 0.08% |

| Std. Dev. | 6.57% | 6.74% | 8.63% | 6.25% | 6.75% |

By using Algorithm 1, we determine the portfolio with allowed short-selling that possesses the lowest risk: this linear combination is given by Table 2. The mean of its monthly variation is and its standard-deviation .

| Stock | AI | BN | CA | DSY | ENGI |

|---|---|---|---|---|---|

| 7.28% | 22.69% | 3.90% | 12.63% | 2.41% | |

| Stock | HO | ORA | RMS | SAN | VIV |

| 3.81% | 21.05% | 8.96% | 16.57% | 0.70% |

We observe here that the linear combination obtained is a convex combination, which means that this portfolio is also the portfolio without short-selling that possesses the lowest risk. In geometrical terms, this means that the orthogonal projection of the origin point onto the hyperplane already belongs to the simplex .

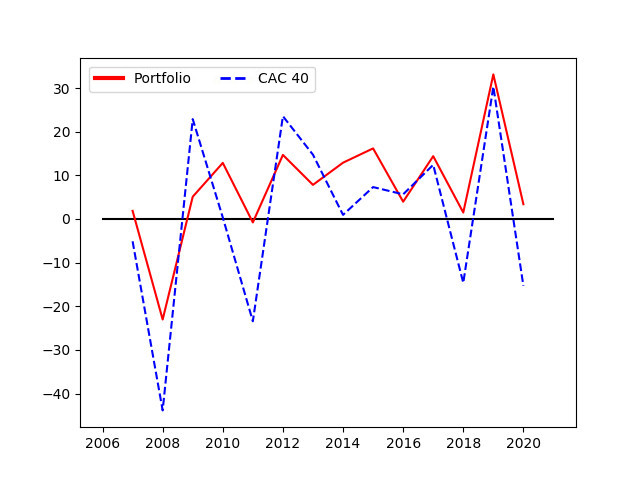

| Year | 2007 | 2008 | 2008 | 2010 | 2011 | 2012 | 2013 |

|---|---|---|---|---|---|---|---|

| Porfolio’s r. r. | 1.85% | -23.04% | 5.09% | 12.84% | -0.80% | 14.67% | 7.81% |

| CAC 40’s r. r. | -5.12% | -43.87% | 22.87% | 0.34% | -23.45% | 23.54% | 14.72% |

| Year | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

| Porfolio’s r. r. | 12.89% | 16.16% | 3.95% | 14.38% | 1.47% | 33.12% | 3.37% |

| CAC 40’s r. r. | 0.93% | 7.30% | 5.64% | 12.40% | -14.65% | 30.33% | -15.34% |

Table 3 and Figure 2 give the yearly return rate of this portfolio. We notice that the portfolio is more profitable and more regular than the index: indeed, its mean is and its standard deviation , whereas for the index, the mean is and the standard deviation . Moreover, the return rate of the portfolio is almost never negative.

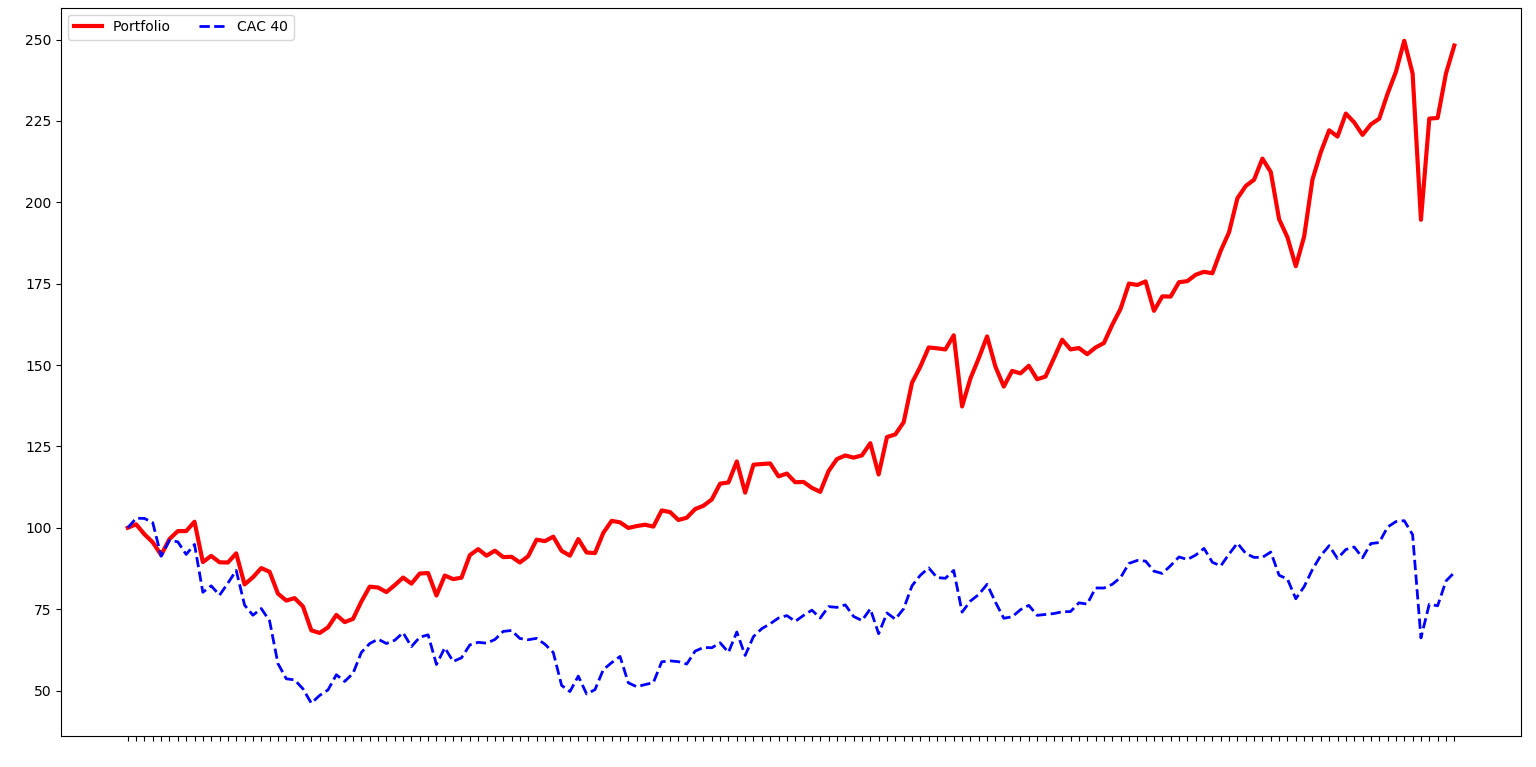

Finally, Table 4 and Figure 3 give the final value of the portfolio compared with the CAC 40 index and show the monthly variations of their value.

| Date | 2009-01-19 | 2020-07-21 |

|---|---|---|

| Portfolio | 100 | 248.16 |

| CAC 40 | 100 | 86.26 |

5.2 Portfolio optimization from 2009-01-19 to 2020-07-21

Here we consider the period from 2009-01-19 to 2020-07-21, that is to say we start from the lowest point of CAC 40 index. As in previous section, Table 5 gives the mean and the standard deviation of stocks’ return rates that appear in the results.

| Stock | AI | BN | CA | DSY | ENGI | HO |

|---|---|---|---|---|---|---|

| Mean | 1.03% | 0.44% | -0.13% | 1.93% | -0.470% | 0.79% |

| Std. Dev. | 5.36% | 5.34% | 7.9699% | 6.0% | 7.0900% | 6.4799% |

| Stock | OR | ORA | RI | RMS | SAN | VIV |

| Mean | 1.3599% | -0.18% | 1.0% | 1.8599% | 0.64% | 0.37% |

| Std. Dev. | 5.42% | 6.77% | 5.93% | 7.4399% | 6.03% | 6.77% |

The portfolio with allowed short-selling that possesses the lowest risk is given by the following linear combination in Table 6. The mean of its monthly variation is and its standard-deviation .

| Stock | AI | BN | CA | DSY | ENGI | HO |

|---|---|---|---|---|---|---|

| 10.70% | 28.25% | 5.42% | 20.91% | -2.34% | 1.88% | |

| Stock | OR | ORA | RI | RMS | SAN | VIV |

| -20.66% | 19.75% | -3.07% | 17.26% | 18.36% | 3.54% |

Now, according to Algorithm 1, the portfolio without short-selling that possesses the lowest risk is given by the following convex combination in Table 7. The mean of its monthly variation is and its standard-deviation .

| Stock | AI | BN | CA | DSY | HO |

|---|---|---|---|---|---|

| 6.17% | 19.22% | 3.43% | 17.37% | 2.96% | |

| Stock | ORA | RMS | SAN | VIV | |

| 17.15% | 15.60% | 16.73% | 1.37% |

Let us note that some stocks that were in the linear combination of the portfolio with allowed short-selling now disappear: the geometric explanation of this fact immediately comes from Lemma 1.

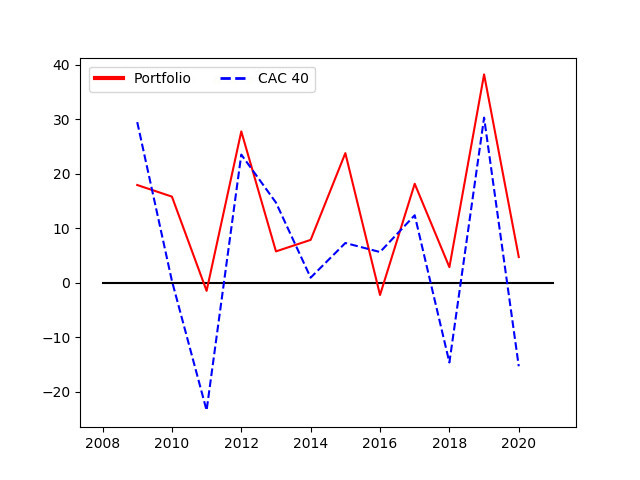

The yearly return rate is given by Table 8. Here again, as shown by Table 8 and Figure 4, the portfolio is more profitable and more regular than the index: its mean is and its standard deviation , whereas for the index, the mean is and the standard deviation . Moreover, the return rate of the portfolio is negative for only two years, and the absolute value of these negative return rates very small.

| Year | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 |

|---|---|---|---|---|---|---|

| Portfolio’s r. r. | 17.95% | 15.82% | -1.49% | 27.80% | 5.76% | 7.87% |

| CAC 40’s r. r. | 29.51% | 0.34% | -23.45% | 23.54% | 14.72% | 0.93% |

| Year | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

| Portfolio’s r. r. | 23.81% | -2.25% | 18.18% | 2.86% | 38.27% | 4.72% |

| CAC 40’s r. r. | 7.30% | 5.64% | 12.40% | -14.65% | 30.33% | -15.34% |

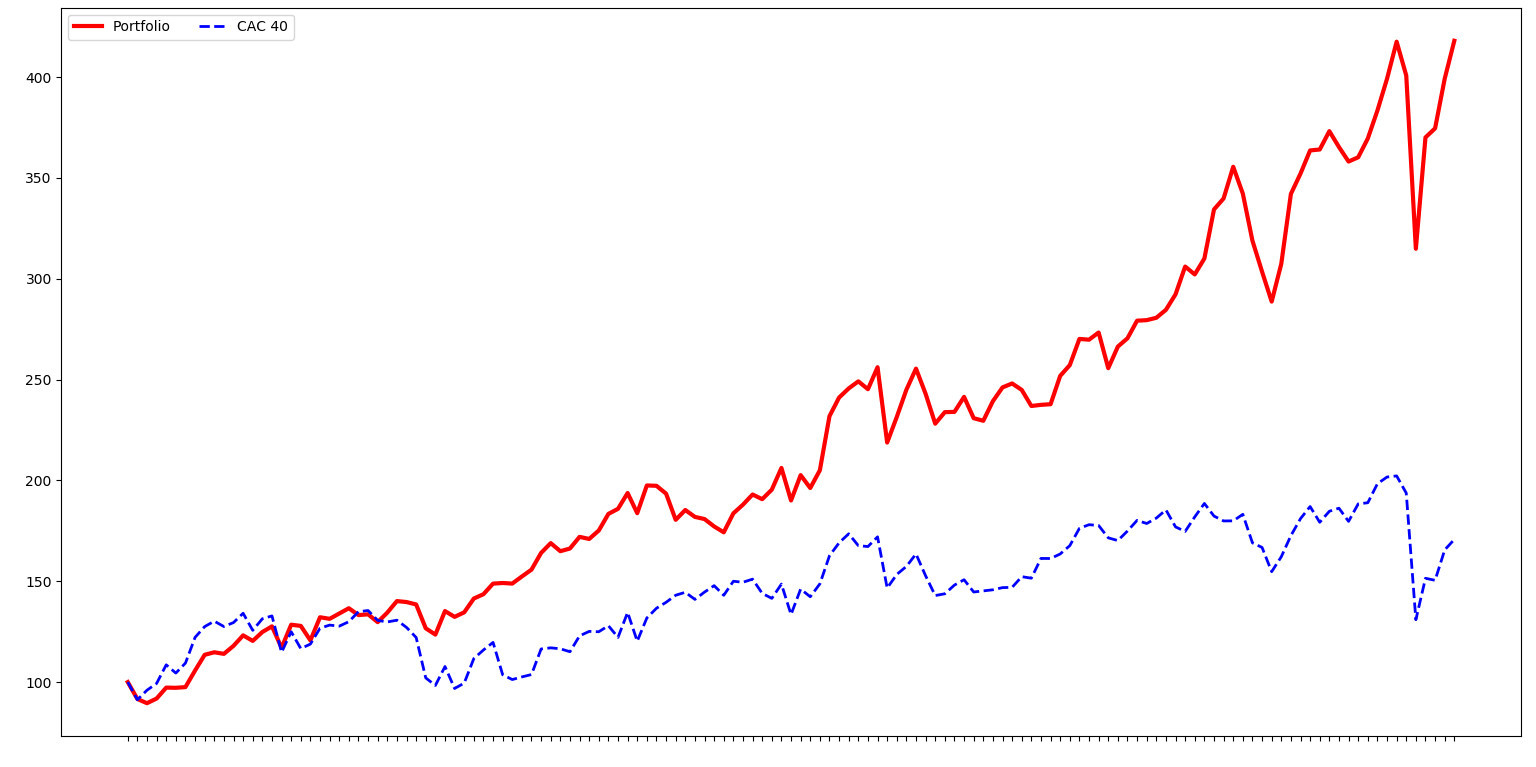

Finally, Table 9 and Figure 5 above give the final value of the portfolio compared with the CAC 40 index and show the monthly variations of their value.

| Date | 2009-01-19 | 2020-07-21 |

|---|---|---|

| Portfolio | 100 | 417.97 |

| CAC 40 | 100 | 170.73 |

Appendix — Python programs

Here we give a possible way to program Algorithm 1 in Python as well as the subroutine used to compute an orthogonal projection.

The function orth_proj(c,a,J) computes an orthogonal projection, where

— c is the covariance matrix,

— a is the point of which we want to compute the orthogonal projection,

— J is the list of indices of vectors of that define the affine subspace onto which we want to project a.

def orth_proj(c,a,J):

p=len(J); n=len(c); i0=J[0]; L=list(set(range(n))-set(J))

#L is the complementary of J

#Matrix of the system

Mpart1=np.array([[c[i,j]-c[i0,j] for j in J] for i in J[1:]])

Mpart2=np.ones((1,p))

M=np.concatenate((Mpart1,Mpart2),axis=0)

#Second part of the system

b=np.array([sum(a[j]*(c[i,j]-c[i0,j]) for j in range(n))

for i in J[1:]]+[1])

#Solving

sol=np.linalg.solve(M,b)

x=np.zeros(n); x[J]=sol

return x

The function mini_dist_fct(c,a) finds the point that realizes the minimal distance from to the standard simplex and also returns the square of this distance: it is a possible version of Algorithm 1.

def mini_dist_fct(c,a):

#Scalar product

def phi(x,y):

return np.dot(x,np.dot(c,y))

#Canonical basis

n=len(c)

e=[np.array(j*[0]+[1]+(n-j-1)*[0]) for j in range(n)]

dico={}

#Recursive function mini_dist(c,a,J)

def mini_dist(c,a,J):

#Orthogonal projection of a

x=orth_proj(c,a,J)

#Case 1: the orthogonal projection belongs to the simplex

if all(t>=0 for t in x):

return [x,phi(x-a,x-a)]

#Case 2: the orthogonal projection does not belong to the

#simplex and the simplex has dimension 1

elif len(J)==2:

d0=phi(x-e[J[0]],x-e[J[0]])

d1=phi(x-e[J[1]],x-e[J[1]])

if d0<=d1:

return [e[J[0]],phi(e[J[0]]-a,e[J[0]]-a)]

else:

return [e[J[1]],phi(e[J[1]]-a,e[J[1]]-a)]

#Case 3: the orthogonal projection does not belong to the

#simplex and the simplex has dimension greater than 1

else:

#Looking for the hyperface that is the closest to x

s=J[0]

if str(set(J)-{s})+str(x) in dico:

delta=dico[str(set(J)-{s})+str(x)]

else:

delta=mini_dist(c,x,list(set(J)-{s}))

dico[str(set(J)-{s})+str(x)]=delta

d=delta[1]

for j in J[1:]:

if str(set(J)-{j})+str(x) in dico:

delta0=dico[str(set(J)-{j})+str(x)]

else:

delta0=mini_dist(c,x,list(set(J)-{j}))

dico[str(set(J)-{j})+str(x)]=delta0

d0=delta0[1]

if d0<d:

s=j; d=d0

#Projection onto the simplex defined by the

#closest hyperface

J=list(set(J)-{s})

if str(set(J))+str(x) in dico:

delta=dico[str(set(J))+str(x)]

else:

delta=mini_dist(c,x,J)

dico[str(set(J))+str(x)]=delta

x=delta[0]

return [x,phi(x-a,x-a)]

#Computing the point realizing the minimal distance

return mini_dist(c,a,list(range(n)))

References

- [B00] Louis Bachelier, Théorie de la spéculation, Gauthier-Villars, Paris (1900).

- [B15] Hanene Ben Salah, Gestion des actifs financiers : de l’approche Classique à la modélisation non paramétrique en estimation du DownSide Risk pour la constitution d’un portefeuille efficient, thèse (2015).

- [BCGD18] Hanene Ben Salah, Mohamed Chaouch, Ali Gannoun, Christian De Peretti, Mean and median-based nonparametric estimation of returns in mean-downside risk portfolio frontier, Annals of Operations Research 262 (1), DOI: 10.1007/s10479-016-2235-z (2018).

- [BIPS20] Taras Bodnar, Dmytro Ivasiuk, Nestor Parolya, Wolfgang Schmid, Mean-variance efficiency of optimal power and logarithmic utility portfolios, Mathematics and Financial Economics 14, 675–698 (2020).

- [C16] Laurent Condat, Fast projection onto the simplex and the ball, Mathematical Programming 158, 575–585 (2016).

- [CY11] Yunmei Chen, Xiaojing Ye, Projection Onto A Simplex, arXiv:1101.6081v2 [math.OC] (2011).

- [DJDY08] Jón Daníelsson, Bjørn N. Jorgensen, Casper G. de Vries, Xiaoguang Yang, Optimal portfolio allocation under the probabilistic VaR constraint and incentives for financial innovation, Annals of Finance 4, 345–367 (2008).

- [FS12] Claudio Fontana, Martin Schweizer, Simplified mean-variance portfolio optimisation, Math Finan Econ 6, 125–152, DOI 10.1007/s11579-012-0067-4 (2012).

- [M52] Harry Markowitz, Portfolio Selection, The Journal of Finance 7 (No. 1), 77–91 (1952).

- [M10] Franck Moraux, Finance de marché, Pearson Education France (2010).

- [N09] Anna Nagurney, Portfolio Optimization, University of Massachusetts (2009).

- [PP14] Patrice Poncet, Roland Portait, Finance de marché, Dalloz, Paris, 4e édition (2014).

- [PR19] Sarah Perrin, Thierry Roncalli, Machine Learning Optimization Algorithms & Portfolio Allocation, Papers 1909.10233, arXiv.org (2011).

- [R17] Aude Rondepierre, Méthodes numériques pour l’optimisation non linéaire déterministe, INSA de Toulouse (2017).

- [S63] William Forsyth Sharpe, A Simplified Model for Portfolio Analysis, Management Science 9, 277–293 (1963).