New Mixed Portmanteau Tests for Time Series Models

Esam Mahdi

School of Mathematics and Statistics, Carleton University, Ottawa, ON, Canada

esammahdi@cunet.carleton.ca

Highlights

-

•

We propose omnibus portmanteau statistics that can be used as a goodness-of-fit and test for the presence of (possibly nonlinear) dependence structure in the residuals of time series models.

-

•

The test statistics are based on combining the autocorrelations of the residuals at different powers.

-

•

The asymptotic distribution is derived under the general class of time series models, including ARMA and GARCH, and other nonlinear structures.

-

•

Extensive simulations are conducted to demonstrate the good performance of the proposed tests.

-

•

The proposed tests are implemented in R.

-

•

Real time series data are employed to show the practical use of the proposed tests.

Abstract

This article proposes omnibus portmanteau tests for contrasting adequacy of time series models. The test statistics are based on combining the autocorrelation function of the conditional residuals, the autocorrelation function of the conditional squared residuals, and the cross-correlation function between these residuals and their squares. The maximum likelihood estimator is used to derive the asymptotic distribution of the proposed test statistics under a general class of time series models, including ARMA, GARCH, and other nonlinear structures. An extensive Monte Carlo simulation study shows that the proposed tests successfully control the type I error probability and tend to have more power than other competitor tests in many scenarios. Two applications to a set of weekly stock returns for companies from the S&P 500 demonstrate the practical use of the proposed tests.

Keywords: ARMA and GARCH models; Autocorrelation; Cross-correlation; Nonlinearity test; Mixed portmanteau tests; Quasi-maximum likelihood estimation; Stock returns.

1 Introduction

Time series models often consist of two components: (i) the conditional mean part; and (ii) the conditional variance part. Traditionally, the autoregressive and moving average (ARMA) models are classified as linear and specify the mean part, whereas the generalized autoregressive conditional heteroscedasticity (GARCH) models are nonlinear and describe the variance part. During the past four decades, time series analysis was dominated by the ARMA models, where a good model should be able to specify the dependence structure of the series adequately (Box and Jenkins, 1970). Dependency, in ARMA models, is often measured by using the residual autocorrelation function (ACF). To test the adequacy of an ARMA model, a portmanteau statistic was proposed by Box and Pierce (1970) based on the distribution of the residual ACF. Since then, several authors have improved the portmanteau tests (see, for example, Fisher and Gallagher, 2012; Ljung and Box, 1978; Peña and Rodríguez, 2002, 2006; Mahdi, 2017).

In the last two decades, the analysis of nonlinear time series models has attracted a great deal of interest in business, economics, finance, and other fields. Box and Jenkins (1970), Granger and Andersen (1978) and Tong and Lim (1980) noticed that the squared residuals of time series models are significantly autocorrelated even though the residuals are not autocorrelated. This indicates that the error term of these models might be uncorrelated but not independent. The authors suggested using the ACF of the squared values of the series to detect nonlinearity. In this respect, Engle (1982) showed that the classical portmanteau tests proposed by Box and Pierce (1970) and Ljung and Box (1978) fail to detect the presence of the autoregressive conditional heteroscedasticity (ARCH) in many financial time series models. To test for the presence of an ARCH process, Engle (1982) introduced a Lagrange multiplier statistic based on the autocorrelations of the squared residuals.

Several authors have developed portmanteau test statistics employing the ACF of the squared residuals to detect nonlinear structures and ARCH effect in time series models (see, for example, Fisher and Gallagher, 2012; McLeod and Li, 1983; Peña and Rodríguez, 2002, 2006; Rodríguez and Ruiz, 2005). All the above test statistics were derived under the assumptions of ARMA models and were not proposed for nonlinear time series models.

A portmanteau test was developed by Li and Mak (1994) to check the adequacy of nonlinear time series models, including ARMA-ARCH, and other conditional heteroscedastic structures. Under a general class of time series models, two mixed portmanteau tests, to detect the linear and nonlinear dependency in time series models, were considered by Wong and Ling (2005) summing the statistics derived by Box and Pierce (1970) and Li and Mak (1994) for the first one, and summing the statistics proposed by Ljung and Box (1978) and McLeod and Li (1983) for the second one. Wong and Ling (2005) showed that their mixed tests are, in many situations, more powerful than the tests proposed by Ljung and Box (1978) and McLeod and Li (1983), when the fitted model has a disparity in its first and second moments. Zhu (2013) proposed another mixed portmanteau test for ARMA-GARCH models with parameters estimated by a quasi-maximum exponential likelihood estimator. Li et al. (2018) proposed a first-order zero-drift GARCH (ZD-GARCH(1, 1)) model to study conditional heteroscedasticity and heteroscedasticity together, for which the authors constructed a portmanteau test for model checking. Their test statistic was derived based on the lag- autocorrelation function of the th power of the absolute residuals, where is a positive integer and .

For the test statistics presented by Wong and Ling (2005); Zhu (2013) and Li et al. (2018), the authors did not consider the cross-correlation between the residuals at different powers. The idea of using the cross-correlation between the residuals at different powers to test for linearity was considered by Welsh and Jernigan (1983); Lawrance and Lewis (1985, 1987); Psaradakis and Vávra (2019).

In this article, we propose four mixed portmanteau statistics for time series models. The proposed test statistics are composed by three components: The first of them utilizes the autocorrelations of the residuals, which is designed to capture the linear dependency in the mean part of time series models. Then, the second component of these statistics utilizes the autocorrelation of the squared residuals, which can be used to test for conditional heteroscedastic effects. The third component of these statistics is related to the cross-correlations between the residuals and their squared values, which may be helpful to test for other types of nonlinear models in which the residuals and their squared values are cross-correlated. The cross-correlations between the residuals and their squared values allow us to propose two different tests. One of these tests is based on the positive lags and the other one uses the negative lags. Therefore, the tests proposed in the present study combine the statistics presented in Wong and Ling (2005) and Psaradakis and Vávra (2019).

The remainder of this article is organized as follows. Section 2 defines some popular time series models with their assumptions. In Section 3, we propose new auto-and-cross-correlated test statistics for contrasting the adequacy of fitted time series models and derive their asymptotic distributions. In Section 4, a Monte Carlo simulation study is conducted to compare the performance of the proposed statistics with some tests commonly used in the literature. We show that the empirical size of the proposed tests successfully controls the type I error probability and tends to have higher power than other tests in many cases. Section 5 presents illustrative applications to demonstrate the usefulness of the proposed tests for real-world data. We finish this article in Section 6 by providing concluding remarks.

2 The general time series model and its assumptions

Assume that is a time series that is generated by the strictly stationary and ergodic model defined by

| (2.1) |

where represents the information set (-algebra) generated by , and denotes the vector of unknown parameters and its true value is . and are the conditional mean and conditional variance of , respectively. Both are assumed to have continuous second order derivative almost surely (a.s.). The process is a sequence of independent and identically distributed (i.i.d.) random variables with mean zero, variance one, and finite fourth moment.

The usual ARMA-GARCH model can be seen as a special case of this model that can be written as

| (2.2) |

where is a sequence of i.i.d. random variables with mean zero, variance one, and , with , , , for , and .

Ignoring the constant term, the Gaussian log-likelihood function of given the initial values can be written as

| (2.3) |

where

where . Assuming the parameter space is , where is an interior vector in , and and for convenience, let’s denote , , and . The first derivative of the log-likelihood function is given by

By taking the conditional expectations of the iterative second derivatives with respect to , we have

Assume that is a martingale difference in terms of and let be the quasi-maximum likelihood estimator of , that is, , where denotes a.s. convergence. Then, it follows that

| (2.4) |

where and in probability as . Furthermore, it has been shown that the asymptotic distribution of is normal with zero mean vector and variance-covariance matrix (see Hall and Heyde, 1980; Higgins and Bera, 1992; Ling and McAleer, 2010).

3 The proposed test statistics

Let be the lag of the series with , where is the largest value considered for the auto-and-cross-correlations and define

as the lag- theoretical autocorrelation of the error process where is the true but unknown parameter vector. Let

and

with

We derive the asymptotic distribution of the proposed test statistics under the null hypothesis that the time series model in (2.1) takes the correct functional forms given by . The alternative hypothesis is . Equivalently, the null and alternative hypotheses can be used for testing the lag residual auto-and-cross-correlation so that and , for all . For simplicity, we dropped the symbol so that and .

Given a sample time series of length observations , under the assumptions of and (2.4), we fit the model defined in (2.1). Subsequently, we calculate the standardized residuals (conditional residuals) raised to powers using the following expressions:

where , and denote the sample residuals, squared-residuals, conditional volatility, and conditional variance of , respectively.

The corresponding sample correlation coefficient between the standardized residuals may be written as

| (3.5) |

where , for , , for , is the autocovariance (cross-covariance), at lag-, between the standardized residuals to th power and the standardized residuals to th power, and , for .

Under the regular assumptions, it can be shown that , , and , where converges to the value two (see Li and Mak, 1994; Wong and Ling, 2005) and (Theorem Ling and McAleer, 2003). Hence, at lag-, if we define and as the counterparts of and , respectively, with the replacement of the fitted residual and conditional variance by and , respectively, we obtain:

We employ these autocorrelation coefficients to propose new portmanteau goodness-of-fit tests, as later defined in (3.12), to check for linear and nonlinear dependencies within the residual series.

Theorem 3.1.

Proof.

The proof is given in the Appendix (7).

By the results of Theorem 3.1, we propose the portmanteau statistic, namely, and its modified version, namely, to test that the model stated in (2.1) is correctly specified. Thus, we have that

| (3.12) |

where are defined in (3.6), and are obtained after replacing the autocorrelation coefficients in (3.5) by their standardized values formulated as

| (3.13) |

From the theorem on quadratic forms given in Box (1954), it is straightforward to show that and are asymptotically chi-square distributed with degrees of freedom.

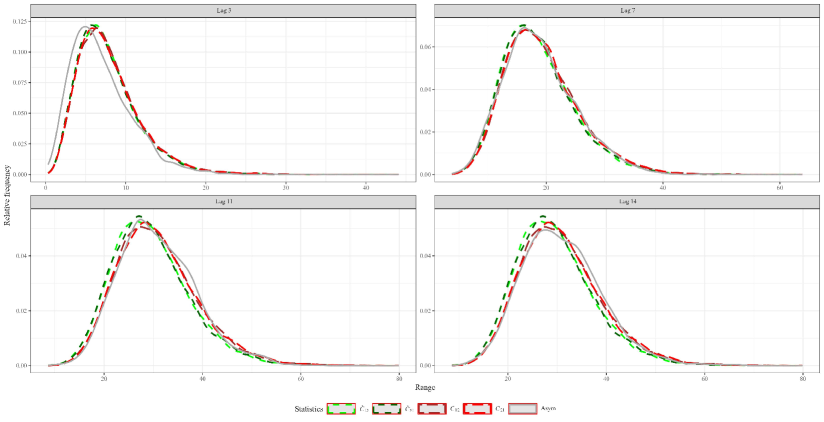

Figure 1 illustrates the accuracy of the approximation of the empirical distribution of and , for to the chi-square distribution employing replicates when an ARMA(1,1) model fits to a sample of size generated from an ARMA(1,1) process defined as

| (3.14) |

The parameters of the ARMA model stated in (3.14) are selected to be very close to non-stationarity and non-invertibility case, whereas the coefficient of the MA model is near to cancellation with the coefficient of the AR model to demonstrate the usefulness of the proposed tests, even with extreme cases.

We found similar results for small and large samples and our preliminary analysis indicates that the portmanteau tests based on the statistics control the type I error probability more successfully than the tests that consider the statistics . Hence, we recommend the use of .

Remark 3.1.

As mentioned, the proposed test statistics in (3.12) can be seen as combinations of the statistics presented by Wong and Ling (2005) and Psaradakis and Vávra (2019). Thus, each test statistic may be seen as a linear combination of three existent test statistic proposed by Ljung and Box (1978), McLeod and Li (1983), and Psaradakis and Vávra (2019), modifying the corresponding statistic , which are linear combinations of three statistics given by Box and Pierce (1970), Li and Mak (1994), and Psaradakis and Vávra (2019).

4 Simulation studies

We carry out Monte Carlo simulations to examine statistical properties of the proposed tests. For comparative purposes, we also consider three test statistics given by

| (4.15) |

where and represent the statistics presented in Psaradakis and Vávra (2019) and denotes the statistic proposed by McLeod and Li (1983). In addition, we consider two statistics introduced by Li and Mak (1994) and Wong and Ling (2005), which are denoted by and , respectively, given by

| (4.16) | |||||

| (4.23) |

First, we examined six statistics, , and namely, assuming the following five linear models studied by Psaradakis and Vávra (2019):

- A1. AR(1) model:

-

;

- A2. AR(2) model:

-

;

- A3. MA(1) model:

-

;

- A4. ARMA(2,1) model:

-

;

- A5. ARMA(1,1) model:

-

.

For model A1, the parameter used by Psaradakis and Vávra (2019) was . However, we considered here a value negative of the parameter close to non-stationarity case to assess the behavior of the test statistics associated with positive and negative values of the parameters. We also analyzed for this model the cases where whose results showed very minor changes in the behavior of the proposed tests. For model A3, we also explored the cases where and obtained good results.

Second, we investigated four statistics, , and namely, according to the following three nonlinear models studied by Velasco and Wang (2015) and Han and Ling (2017):

- A6. GARCH(1,1) model:

-

;

- A7. AR(1)-ARCH(1) model:

-

;

- A8. AR(1)-GARCH(1,1) model:

-

;

where or Student- distribution with 10 degrees of freedom.

In all experiments, we use the R software (www.R-project.org, R Core Team, 2020) to simulate 1000 replicates of artificial series of size with . However, only the last data points are used to carry out portmanteau tests with the residuals of some fitted models.

The empirical size and power of the tests are calculated based on a nominal level 5%. Simulation results for nominal levels 1% and 10% are not reported, due to space conservation, but they are available upon request.

First, we calculate the type I error probability, at lags , based on six statistics, , and namely, when a true model is fitted to a series generated according to models A1-A5. Second, we investigated the accuracy of estimating type I error probability using four statistics, , and namely, when a true model is fitted to a series generated according to models A6-A8.

| Model | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Gaussian distribution | |||||||||||||||

| A1 | 5.7 | 5.8 | 4.4 | 4.4 | 4.4 | 3.6 | 5.7 | 5.9 | 4.7 | 4.7 | 4.7 | 4.4 | |||

| 5.6 | 5.4 | 4.9 | 4.9 | 5.0 | 3.7 | 5.6 | 5.5 | 4.9 | 4.9 | 5.1 | 4.3 | ||||

| A2 | 5.2 | 4.8 | 4.2 | 4.2 | 4.1 | 3.1 | 5.4 | 4.9 | 4.3 | 4.3 | 4.6 | 3.6 | |||

| 5.2 | 5.5 | 5.0 | 5.0 | 5.0 | 3.5 | 5.4 | 5.3 | 4.8 | 4.8 | 5.2 | 4.0 | ||||

| A3 | 6.0 | 5.8 | 4.4 | 4.4 | 4.3 | 3.7 | 6.0 | 6.0 | 4.6 | 4.6 | 4.8 | 4.4 | |||

| 5.5 | 5.8 | 5.1 | 5.1 | 5.0 | 3.7 | 5.8 | 5.8 | 5.0 | 5.0 | 5.1 | 4.3 | ||||

| A4 | 6.6 | 6.2 | 4.3 | 4.3 | 3.9 | 4.1 | 6.2 | 5.9 | 4.3 | 4.4 | 4.5 | 4.2 | |||

| 6.5 | 6.4 | 4.5 | 4.7 | 4.6 | 4.5 | 5.6 | 5.2 | 5.4 | 4.2 | 4.8 | 4.3 | ||||

| A5 | 5.5 | 5.3 | 4.3 | 4.4 | 4.0 | 2.9 | 5.6 | 5.4 | 4.3 | 4.3 | 5.2 | 4.0 | |||

| 5.3 | 5.6 | 4.8 | 4.8 | 5.0 | 3.6 | 5.5 | 5.6 | 4.8 | 4.8 | 5.1 | 4.0 | ||||

| Student- distribution with 10 degrees of freedom | |||||||||||||||

| A1 | 5.8 | 5.4 | 4.1 | 4.1 | 4.3 | 3.4 | 5.6 | 5.1 | 4.0 | 4.0 | 4.3 | 3.9 | |||

| 6.2 | 6.3 | 4.5 | 4.5 | 5.3 | 4.2 | 6.1 | 6.3 | 5.0 | 5.0 | 5.3 | 4.6 | ||||

| A2 | 4.5 | 4.6 | 3.9 | 3.9 | 3.9 | 2.9 | 4.6 | 4.5 | 3.6 | 3.6 | 3.9 | 3.3 | |||

| 5.7 | 5.7 | 4.3 | 4.3 | 5.2 | 3.5 | 5.8 | 5.8 | 4.7 | 4.7 | 5.5 | 4.0 | ||||

| A3 | 5.6 | 5.2 | 4.4 | 4.4 | 4.3 | 3.4 | 5.4 | 5.3 | 4.1 | 4.1 | 4.3 | 3.8 | |||

| 5.9 | 6.0 | 4.5 | 4.5 | 5.2 | 4.0 | 6.0 | 6.4 | 5.0 | 5.0 | 5.5 | 4.4 | ||||

| A4 | 7.2 | 7.4 | 4.9 | 5.1 | 4.2 | 4.0 | 5.8 | 6.0 | 4.8 | 5.0 | 4.7 | 4.2 | |||

| 6.2 | 6.0 | 4.6 | 4.8 | 5.0 | 4.4 | 5.8 | 5.6 | 4.8 | 5.0 | 5.2 | 4.4 | ||||

| A5 | 5.0 | 4.7 | 4.2 | 4.2 | 4.1 | 2.9 | 4.9 | 4.8 | 3.9 | 3.9 | 4.1 | 3.6 | |||

| 5.6 | 5.9 | 4.3 | 4.3 | 5.1 | 3.8 | 5.7 | 5.8 | 4.7 | 4.7 | 5.5 | 4.1 | ||||

The empirical sizes of the test corresponding to the nominal size over 1000 independent simulations belong to the 95% confidence interval and to the 99% confidence interval . From Tables 1 and 2, note that tests based on the statistics and can distort the test size, whereas the tests using the statistics and the proposed statistics exhibit no substantial size distortion and, generally, have empirical levels that improve as increases. Also, we found similar results for the cases where the error terms have either skew-normal distribution with asymmetry parameter or Student- distribution with degrees of freedom . These results are omitted here due to space conservation, but they are available upon request.

| Model | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Gaussian distribution | |||||||||||

| A6 | 3.7 | 3.8 | 2.3 | 2.8 | 4.1 | 4.0 | 2.7 | 2.3 | |||

| 3.5 | 3.4 | 1.8 | 3.2 | 3.5 | 3.6 | 2.5 | 2.5 | ||||

| A7 | 3.9 | 3.9 | 2.3 | 3.5 | 4.5 | 45 | 3.2 | 3.1 | |||

| 3.8 | 3.7 | 2.1 | 3.6 | 4.5 | 4.4 | 3.2 | 4.1 | ||||

| A8 | 4.0 | 3.8 | 2.3 | 2.8 | 4.0 | 3.8 | 2.7 | 2.4 | |||

| 3.4 | 3.3 | 1.8 | 3.0 | 3.3 | 3.4 | 2.3 | 2.3 | ||||

| Student- distribution with 10 degrees of freedom | |||||||||||

| A6 | 4.4 | 4.0 | 2.4 | 2.8 | 4.2 | 3.7 | 2.6 | 2.1 | |||

| 4.4 | 4.1 | 2.9 | 4.1 | 4.2 | 4.2 | 2.9 | 3.0 | ||||

| A7 | 4.4 | 4.3 | 2.6 | 3.0 | 4.8 | 4.7 | 3.4 | 2.0 | |||

| 5.1 | 5.0 | 3.3 | 4.8 | 5.1 | 5.2 | 3.7 | 3.3 | ||||

| A8 | 4.8 | 4.3 | 2.7 | 2.7 | 4.3 | 4.0 | 2.9 | 1.4 | |||

| 4.7 | 4.8 | 2.9 | 3.6 | 4.1 | 4.4 | 2.9 | 2.7 | ||||

4.1 Testing linearity in linear time series models

Now, we investigate the efficiency to distinguish power for the mean term of the test statistics , and 111We also test the form of the GARCH-type models by examining the GARCH(1,1) model versus the MA(1)-GARCH(1,1) and AR(1)-GARCH(1,1) models based on the test statistics , and . The results are available upon request. For expositional simplicity, we define as the highest test power attained by the statistics and , whereas as the highest test power attained by and , that is,

| (4.24) |

The power of the tests are calculated under the null hypothesis that satisfies the ARMA model

which can be seen as an AR() model, where .

We followed the approach presented by Ng and Perron (2005) who used the Bayesian information criterion (BIC) to select the order , where denotes the floor function (integer part) of the number , when an AR() model erroneously fits to series generated from the following models studied by Li and Mak (1994), Wong and Ling (2005), Han and Ling (2017), and Psaradakis and

Vávra (2019):

- B1. Bilinear (BL) model:

-

, where , with parameter values of being selected in the range ;

- B2. Random coefficient AR (RCAR) model:

-

, where and are two sequences of i.i.d. random variables, which are independent from each other variable; note that the RCAR model is a special case of the AR(1) and ARCH(1) models as observed in , which is the conditional variance over time. We select parameter values of from the range ;

- B3. TAR model:

-

, where ;

- B4. AR(1)-ARCH(2) model:

-

, where .

Note that we found similar results based on the Akaike information criterion –AIC– (Akaike, 1974).

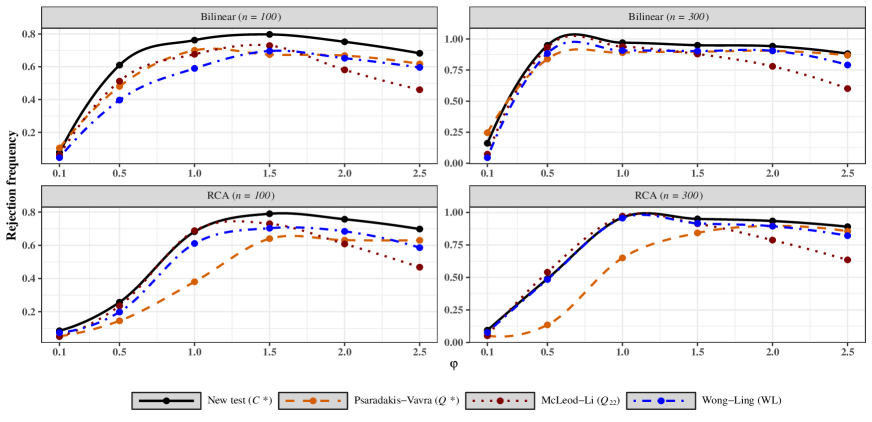

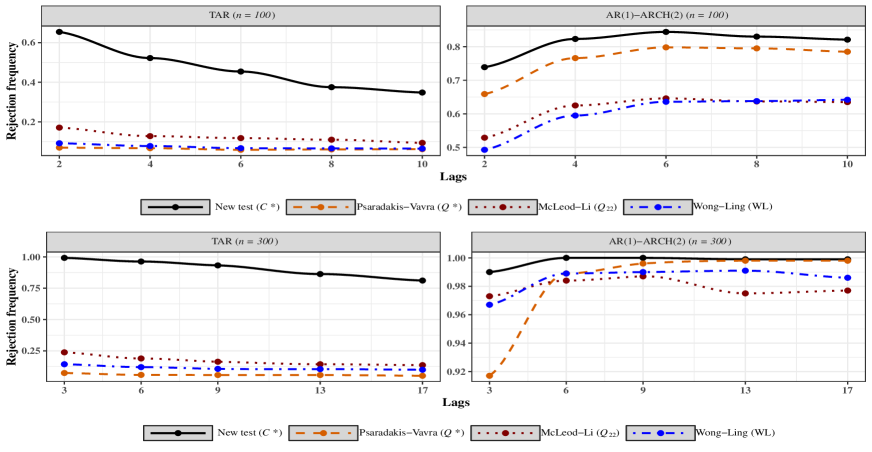

Figure 2 displays the rejection frequencies considering a 5% nominal level of the statistics , and when an AR() model erroneously fits data of size from BL (B1) and RCAR (B2) models at lag value . The results for both models are based on parameter values varying from 0 to 2.5, as mentioned. In addition, Figure 3 shows the rejection probability of the aforementioned tests (of nominal level ) employing the nonlinear TAR (B3) and AR(1)-ARCH(2) (B4) models. For , the tests are calculated at lags and , respectively. From Figures 2 and 3, note that the performance of the proposed statistic is, in general, the best, especially for small sample sizes. Thus, we conclude that the proposed statistics are helpful for testing for linearity of stationary time series.

4.2 Testing the AR-ARCH models

In order to examine the ability for discriminating power for the mean and conditional variance parts of a time series model, we consider the AR-GARCH model versus nonlinear models with GARCH errors. The process satisfies the null hypothesis of heteroskedasticity given by

The alternative models are:

- D1. AR(1)-ARCH(2) model:

-

;

- D2. AR(1)-GARCH(1,1) model:

-

;

- D3. AR(2)-ARCH(2) model:

-

;

- D4. TAR model with GJR-GARCH(1,1) error:

-

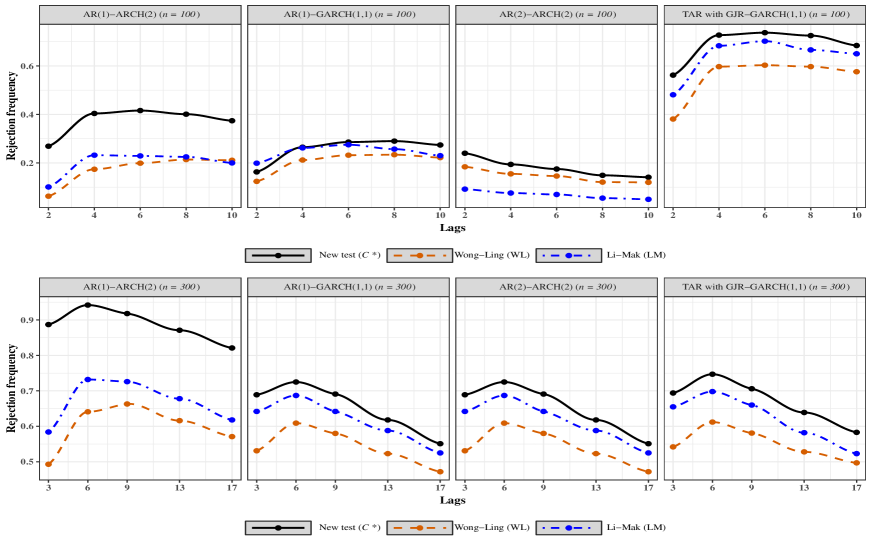

For each model, the power of the test for the statistics , and are calculated at lags and associated with . The results are shown in Figure 4. Note that the performance of the proposed test is in general better when compared with the other two tests.

Worth noting that, in general, as the lag order increases, the power of the portmanteau tests decreases, especially under models like the TAR model, for several reasons including the following:

-

•

When the lag is large compared to the overall sample size, we usually get less reliable estimates of autocorrelation and, consequently, less power in the portmanteau test.

-

•

As we increase the lag order, we are including more lags in the test, which means we are estimating more parameters. This results in a loss of degrees of freedom in the test statistics. With fewer degrees of freedom, the test becomes less sensitive to detecting the absence of autocorrelation.

-

•

TAR models have different nonlinear thresholds which complicate the estimation of the autocorrelation function at higher lag orders, making it more challenging to detect the absence of autocorrelation.

5 Empirical applications

5.1 Test for nonlinearity in AR models using stock returns

We demonstrate the usefulness of the proposed tests for detecting nonlinearity in AR models for a set of weekly stock returns. We select 92 companies studied by Kapetanios (2009) and Psaradakis and Vávra (2019). These companies are a subset of the Standard & Poor 500 composite index (S&P 500), spanning over the period from 18 June 1993 to 31 December 2007 ( observations).

Following the procedure presented by Psaradakis and Vávra (2019), we fit an AR() model for each series, where the order of was selected by minimizing the BIC according to the algorithm explained in Section 4.1 (Ng and Perron, 2005). The asymptotic p-values (at 5% significance level) for tests based on the statistics , and , with , are reported in Table 3. Since the conditional heteroskedasticity is often considered as a main characteristic of asset returns, we expect that the AR model will not capture the nonlinear features in most of the stock returns considered in our analysis and the null hypothesis of linearity should be rejected.

| Company | p-value | Company | p-value | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Alcoa Inc | 0.00 | 0.00 | 0.00 | 0.00 | Deere and Co. | 0.00 | 0.03 | 0.00 | 0.01 |

| Apple Inc. | 0.00 | 0.01 | 0.41 | 0.19 | D.R. Horton | 0.06 | 0.21 | 0.02 | 0.11 |

| Adobe Systems Inc | 0.00 | 0.15 | 0.00 | 0.00 | Danaher Corp. | 0.00 | 0.01 | 0.00 | 0.00 |

| Analog Devices Inc | 0.00 | 0.00 | 0.00 | 0.00 | Walt Disney Co. | 0.00 | 0.10 | 0.00 | 0.01 |

| Archer-Daniels-Midland | 0.07 | 0.52 | 0.01 | 0.05 | Duke Energy | 0.00 | 0.00 | 0.00 | 0.00 |

| Autodesk Inc | 0.00 | 0.06 | 0.01 | 0.02 | Ecolab Inc. | 0.00 | 0.00 | 0.00 | 0.00 |

| American Electric Power | 0.00 | 0.00 | 0.00 | 0.00 | Equifax Inc. | 0.96 | 0.55 | 0.99 | 0.99 |

| AES Corp | 0.00 | 0.00 | 0.00 | 0.00 | Edison Int’l | 0.00 | 0.00 | 0.00 | 0.00 |

| AFLAC Inc | 0.00 | 0.00 | 0.00 | 0.00 | EMC Corp. | 0.01 | 0.02 | 0.03 | 0.12 |

| Allergan Inc | 0.95 | 0.46 | 0.92 | 0.99 | Emerson Electric | 0.00 | 0.03 | 0.00 | 0.00 |

| American Intl Group Inc | 0.00 | 0.00 | 0.00 | 0.00 | Equity Residential | 0.00 | 0.41 | 0.00 | 0.00 |

| Aon plc | 0.00 | 0.00 | 0.00 | 0.00 | EQT Corporation | 0.00 | 0.03 | 0.00 | 0.00 |

| Apache Corporation | 0.00 | 0.02 | 0.00 | 0.00 | Eaton Corp. | 0.04 | 0.21 | 0.51 | 0.54 |

| Anadarko Petroleum | 0.00 | 0.15 | 0.00 | 0.00 | Entergy Corp. | 0.00 | 0.03 | 0.00 | 0.00 |

| Avon Products | 0.00 | 0.17 | 0.09 | 0.01 | Exelon Corp. | 0.22 | 0.33 | 0.06 | 0.29 |

| Avery Dennison Corp | 0.00 | 0.00 | 0.00 | 0.00 | Ford Motor | 0.00 | 0.04 | 0.00 | 0.01 |

| American Express Co | 0.00 | 0.00 | 0.00 | 0.01 | Fastenal Co | 0.09 | 0.14 | 0.04 | 0.22 |

| Bank of America Corp | 0.00 | 0.00 | 0.00 | 0.00 | FedEx Corporation | 0.00 | 0.03 | 0.00 | 0.00 |

| Baxter International Inc. | 0.00 | 0.00 | 0.33 | 0.20 | Fiserv Inc | 0.00 | 0.00 | 0.00 | 0.00 |

| BBT Corporation | 0.00 | 0.01 | 0.00 | 0.00 | Fifth Third Bancorp | 0.00 | 0.00 | 0.00 | 0.00 |

| Best Buy Co. Inc. | 0.00 | 0.01 | 0.00 | 0.00 | Fluor Corp. | 0.01 | 0.03 | 0.01 | 0.05 |

| Becton Dickinson | 0.00 | 0.10 | 0.00 | 0.00 | Frontier Commun. | 0.00 | 0.00 | 0.00 | 0.00 |

| Franklin Resources | 0.00 | 0.00 | 0.00 | 0.00 | Gannett Co. | 0.00 | 0.09 | 0.02 | 0.02 |

| Brown-Forman Corp | 0.00 | 0.00 | 0.02 | 0.00 | General Dynamics | 0.00 | 0.06 | 0.00 | 0.02 |

| Baker Hughes Inc | 0.00 | 0.00 | 0.00 | 0.00 | General Electric | 0.00 | 0.00 | 0.00 | 0.00 |

| The Bank of NY Mellon | 0.00 | 0.00 | 0.00 | 0.00 | General Mills | 0.54 | 0.77 | 0.81 | 0.41 |

| Ball Corp | 0.00 | 0.00 | 0.00 | 0.00 | Genuine Parts | 0.00 | 0.01 | 0.00 | 0.00 |

| Boston Scientific | 0.01 | 0.04 | 0.01 | 0.12 | Gap (The) | 0.00 | 0.00 | 0.00 | 0.00 |

| Cardinal Health Inc. | 0.01 | 0.03 | 0.01 | 0.07 | Grainger Inc. | 0.00 | 0.03 | 0.00 | 0.00 |

| Caterpillar Inc. | 0.01 | 0.06 | 0.08 | 0.13 | Halliburton Co. | 0.00 | 0.00 | 0.00 | 0.00 |

| Chubb Corp. | 0.00 | 0.00 | 0.00 | 0.00 | Hasbro Inc. | 0.05 | 0.08 | 0.28 | 0.18 |

| Coca-Cola Enterprises | 0.00 | 0.00 | 0.00 | 0.00 | Health Care REIT | 0.00 | 0.00 | 0.00 | 0.00 |

| Carnival Corp. | 0.00 | 0.00 | 0.00 | 0.00 | Home Depot | 0.00 | 0.07 | 0.00 | 0.01 |

| CIGNA Corp. | 0.04 | 0.00 | 0.66 | 0.93 | Hess Corporation | 0.83 | 0.33 | 0.92 | 0.97 |

| Cincinnati Financial | 0.00 | 0.00 | 0.00 | 0.00 | Harley-Davidson | 0.02 | 0.00 | 0.58 | 0.92 |

| Clorox Co. | 0.00 | 0.00 | 0.00 | 0.00 | Hewlett-Packard | 0.00 | 0.04 | 0.00 | 0.00 |

| Comerica Inc. | 0.00 | 0.00 | 0.00 | 0.04 | Block H and R | 0.00 | 0.01 | 0.00 | 0.00 |

| CMS Energy | 0.00 | 0.00 | 0.00 | 0.00 | Hormel Foods Corp. | 0.01 | 0.06 | 0.00 | 0.04 |

| CenterPoint Energy | 0.00 | 0.00 | 0.00 | 0.00 | The Hershey Company | 0.13 | 0.27 | 0.56 | 0.20 |

| Cabot Oil and Gas | 0.00 | 0.01 | 0.00 | 0.00 | Intel Corp. | 0.00 | 0.10 | 0.00 | 0.00 |

| ConocoPhillips | 0.23 | 0.19 | 0.42 | 0.44 | International Paper | 0.00 | 0.29 | 0.00 | 0.00 |

| Campbell Soup | 0.00 | 0.00 | 0.00 | 0.00 | Interpublic Group | 0.00 | 0.03 | 0.00 | 0.00 |

| CSX Corp. | 0.02 | 0.15 | 0.03 | 0.03 | Ingersoll-Rand PLC | 0.02 | 0.10 | 0.50 | 0.44 |

| Cablevision Corp. | 0.00 | 0.00 | 0.00 | 0.00 | Johnson Controls | 0.00 | 0.01 | 0.33 | 0.01 |

| Chevron Corp. | 0.00 | 0.03 | 0.01 | 0.01 | Jacobs Eng. Group | 0.22 | 0.07 | 0.35 | 0.68 |

| Dominion Resources | 0.00 | 0.00 | 0.00 | 0.00 | Johnson and Johnson | 0.00 | 0.00 | 0.00 | 0.00 |

From the results in Table 3, we found that the linearity assumption is rejected by the proposed tests in cases compared with , and cases on the basis of the test statistics , and , respectively. This arguably suggests that the proposed tests are preferable to test the presence of nonlinearity in AR models for asset returns.

5.2 Goodness-of-fit-tests for nonlinear time series models

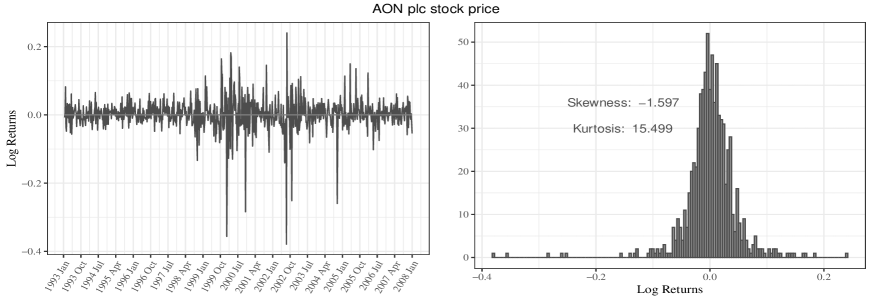

We examine the ability of the portmanteau tests to distinguish an unsuitable model for weekly stock returns of Aon plc company studied in Section 5.1. We find a strong evidence against linearity in the AR model for the returns of this company by using portmanteau tests. The Aon plc returns are displayed in Figure 5 which shows that the log-return series have high persistence in volatility with negative skewness and excess kurtosis. We conclude, therefore, that these returns might exhibit conditional heteroskedasticity effects, and a model that belongs to the ARCH family with a Student- distribution of the error process might better explain the leptokurtic distribution of the returns. Thus, we fit ARCH(1), AR(1)-ARCH(1), ARCH(2), and GARCH(1,1) models and apply the test statistics , and at lag value . The asymptotic p-values for testing the model adequacy based on these proposed statistics are reported in Table 4. From this table, the test statistic fails to detect the inadequacy in all of the fitted models, whereas the test statistic suggests that the ARCH(1), ARCH(2) and GARCH(1,1) models might be suitable to describe for the Aon plc returns. Only the proposed test statistics suggest a clear indication of inadequacy of the ARCH(1), AR(1)-ARCH(1), and ARCH(2) models, while the GARCH(1,1) model might be an adequate model for the Aon plc returns according to the proposed test statistics.

| Fitted model | LM | |||

|---|---|---|---|---|

| ARCH(1) | 0.003 | 0.049 | 0.137 | |

| AR(1)-ARCH(1) | 0.001 | 0.025 | 0.126 | |

| ARCH(2) | 0.008 | 0.076 | 0.125 | |

| GARCH(1,1) | 0.208 | 0.467 | 0.658 |

6 Conclusions

In this article, we have introduced four mixed portmanteau statistics for assessing the adequacy of time series models. The tests we propose are based on a linear combination of three auto-and-cross-correlation components. The first and second components are derived from the autocorrelations of residuals and their squared values, respectively. Meanwhile, the third component takes into account the cross-correlations between the residuals and their square values, considering both positive and negative lags. Two of these tests can be viewed as an extended version of the Ljung and Box test, while the others can be considered an extension of the Box and Pierce test. Based on our simulation study, it is recommended to use the proposed tests, which can be seen as an extended version of the Ljung and Box test. These tests demonstrate better control over the type I error probability compared to existing tests. Furthermore, they generally exhibit more statistical power than tests relying on the statistics introduced by Li and Mak (1994), McLeod and Li (1983), Psaradakis and Vávra (2019), and Wong and Ling (2005).

Simulation results indicate that combining and in a test statistic significantly reduces the test’s power. This can be justified by the lack of independence between these two distinct components, as they share a substantial amount of information about correlation. Consequently, they will add complex redundant correlation which leads to decrease the power in the proposed test.

Some of the test statistics that we have discussed have high computational burdens, so we have implemented them in an R package named portes (Mahdi and McLeod, 2020). The idea discussed in this article may be extended to formulate an omnibus portmanteau test that combines the cross-correlations between the residuals and their square values at both positive and negative lags with the autocorrelations of the residuals and their squared values. The framework we propose could be expanded to identify seasonality in time series and to detect various types of nonlinearity dependence in multivariate time series, as discussed by (Mahdi, 2016).

In this article, our focus has been on measures derived from second-order mixed moments. Nevertheless, there is potential for extending these measures to higher-order moments. Our simulation study revealed that severe skewness, such as in the case of a skewed -distribution, can distort the size of all portmanteau tests. When distributional assumptions are relaxed, the robustness of bootstrapping and Monte Carlo significance test approaches becomes evident (Efron and Tibshirani, 1994; Lin and McLeod, 2006; Mahdi and Ian McLeod, 2012). Therefore, a possible extension of this article could involve considering these approaches for calculating p-values.

7 Appendix

By Taylor’s theorem there exists a random vector on the line segment between and such that

| (7.25) |

where the second derivative depends on the second-order derivatives . By assumption, the second-order partial derivatives are dominated by a fixed integrable function for every in a ball around , so that the probability of the event tends to 1. Thus

| (7.26) |

As the sequence converges to 0 in probability when is consistent for , we can rewrite (7.26) by employing the first-order Taylor series approximation:

| (7.27) |

where

By the ergodic theorem, for large , and after taking the expectation with respect to , it is straightforward to show that

where

is a vector, which can be consistently estimated by

| (7.28) |

It follows that stated in (7.27) can be expressed as , where is the resultant matrix. Thus, by scaling each term by the variance of the standardized residual, we have

| (7.29) |

When is normally distributed, the random vector is asymptotically normal distributed with a mean of zero vector and a variance , where is the identity matrix.

For the case of and , Li and Mak (1994) and Ling and Li (1997) showed that

| (7.30) |

where is an matrix, and is given by

| (7.31) |

The authors proved that is asymptotically normal distributed with a mean of zero vector and a variance .

Now, we consider the case that and . Analogous to the reasoning in equations (7.25-7.27), we can express the first-order Taylor series approximation of as follows:

| (7.32) |

where

By the ergodic theorem, for large , note that

where

is a vector, which can be consistently estimated by

| (7.33) |

Thus, stated in (7.32) may be expressed as , and

| (7.34) |

where .

Similarly, for the case and , it is straightforward to show that

| (7.35) |

where , and is a vector given by

| (7.36) |

The assumptions on imply that the random vectors and are asymptotically normal distributed with mean zero and variance and , respectively.

By utilizing the results from (7), (7), (7), and (7) we can deduce the joint distribution of , for the cases and . Without loss of generality, we establish the proof for the case and . The proof for and readily ensues. Therefore, if the model defined in (2.1) is correctly specified, we obtain:

where

Note that so that the factors and can be replaced by and , respectively.

Let . By using a martingale difference approach in terms of and following the same arguments provided by Wong and Ling (2005, Theorem 1), one can easily show that ; hence, , where . The matrices , and can be consistently estimated by their sample values, denoted by , and , respectively. Under the assumptions of the model stated in (2.1), we get

Thus, we reach

For the ARMA models, we have , and , whereas for GARCH models, we have and . Furthermore, for large , when the model stated in (2.1) is correctly specified, the off-diagonal block matrices in the matrix are approximately zero. Therefore, in general, the matrix has the form stated as

| (7.38) |

with .

Acknowledgment

Our sincere thanks go to Dr. Ajay Jasra, the editor, Dr. Mathieu Gerber, the associate editor, the two anonymous reviewers, Dr. Jan G. De Gooijer, and Kazem Ghanbari for their valuable and insightful suggestions on the manuscript.

Disclosure statement

The author reports no conflict of interest regarding this paper.

References

- Akaike (1974) Akaike, H. (1974). A new look at the statistical model identification. IEEE Transactions on Automatic Control 19(6), 716–723.

- Box and Jenkins (1970) Box, G. and G. Jenkins (1970). Time Series Analysis: Forecasting and Control. San Francisco: Holden-Day.

- Box (1954) Box, G. E. P. (1954). Some theorems on quadratic forms applied in the study of analysis of variance problems, i. effect of inequality of variance in the one-way classification. The Annals of Mathematical Statistics 25(2), 290–302.

- Box and Pierce (1970) Box, G. E. P. and D. A. Pierce (1970). Distribution of residual autocorrelations in autoregressive-integrated moving average time series models. Journal of the American Statistical Association 65(332), 1509–1526.

- Efron and Tibshirani (1994) Efron, B. and R. Tibshirani (1994). An Introduction to the Bootstrap. Chapman & Hall/CRC Monographs on Statistics & Applied Probability. Taylor & Francis.

- Engle (1982) Engle, R. (1982). Autoregressive conditional heteroscedasticity with estimates of the variance of united kingdom inflation. Econometrica 50(4), 987–1007.

- Fisher and Gallagher (2012) Fisher, T. J. and C. M. Gallagher (2012). New weighted portmanteau statistics for time series goodness of fit testing. Journal of the American Statistical Association 107(498), 777–787.

- Granger and Andersen (1978) Granger, C. W. J. and A. P. Andersen (1978). An introduction to bilinear time series models. Vandenhoeck and Ruprecht: Gottingen.

- Hall and Heyde (1980) Hall, P. and C. Heyde (1980). Estimation of parameters from stochastic processes. In Martingale Limit Theory and its Application, Probability and Mathematical Statistics: A Series of Monographs and Textbooks, New York, pp. 155–199. Academic Press.

- Han and Ling (2017) Han, N. S. and S. Ling (2017). Goodness-of-fit test for nonlinear time series models. Annals of Financial Economics 12(02), 1750006.

- Higgins and Bera (1992) Higgins, M. L. and A. K. Bera (1992). A class of nonlinear arch models. International Economic Review 33(1), 137–158.

- Kapetanios (2009) Kapetanios, G. (2009). Testing for strict stationarity in financial variables. Journal of Banking and Finance 33, 2346–2362.

- Lawrance and Lewis (1985) Lawrance, A. J. and P. A. W. Lewis (1985). Modelling and residual analysis of nonlinear autoregressive time series in exponential variables. Journal of the Royal Statistical Society. Series B (Methodological) 47(2), 165–202.

- Lawrance and Lewis (1987) Lawrance, A. J. and P. A. W. Lewis (1987). Higher-order residual analysis for nonlinear time series with autoregressive correlation structures. International Statistical Review / Revue Internationale de Statistique 55(1), 21–35.

- Li et al. (2018) Li, D., X. Zhang, K. Zhu, and S. Ling (2018). The zd-garch model: A new way to study heteroscedasticity. Journal of Econometrics 202(1), 1–17.

- Li and Mak (1994) Li, W. K. and T. K. Mak (1994). On the squared residual autocorrelations in non-linear time series with conditional heteroskedasticity. Journal of Time Series Analysis 15(6), 627–636.

- Lin and McLeod (2006) Lin, J.-W. and A. McLeod (2006). Improved peña-rodríguez portmanteau test. Computational Statistics and Data Analysis 51(3), 1731–1738.

- Ling and Li (1997) Ling, S. and W. K. Li (1997). Diagnostic checking of nonlinear multivariate time series with multivariate arch errors. Journal of Time Series Analysis 18(5), 447–464.

- Ling and McAleer (2003) Ling, S. and M. McAleer (2003). Asymptotic theory for a vector arma-garch model. Econometric Theory 19(2), 280–310.

- Ling and McAleer (2010) Ling, S. and M. McAleer (2010). A general asymptotic theory for time-series models. Statistica Neerlandica 64(1), 97–111.

- Ljung and Box (1978) Ljung, G. M. and G. E. P. Box (1978). On a measure of lack of fit in time series models. Biometrika 65(2), 297–303.

- Mahdi (2016) Mahdi, E. (2016). Portmanteau test statistics for seasonal serial correlation in time series models. SpringerPlus 5(1485).

- Mahdi (2017) Mahdi, E. (2017). Kernel-based portmanteau diagnostic test for arma time series models. Cogent Mathematics 4(1), 1296327.

- Mahdi and Ian McLeod (2012) Mahdi, E. and A. Ian McLeod (2012). Improved multivariate portmanteau test. Journal of Time Series Analysis 33(2), 211–222.

- Mahdi and McLeod (2020) Mahdi, E. and A. I. McLeod (2020). portes: Portmanteau tests for univariate and multivariate time series models. R package version 5.0.

- McLeod and Li (1983) McLeod, A. I. and W. K. Li (1983). Diagnostic checking arma time series models using squared-residual autocorrelations. Journal of Time Series Analysis 4(4), 269–273.

- Ng and Perron (2005) Ng, S. and P. Perron (2005). A note on the selection of time series models. Oxford Bulletin of Economics and Statistics 67(1), 115–134.

- Peña and Rodríguez (2002) Peña, D. and J. Rodríguez (2002). A powerful portmanteau test of lack of fit for time series. Journal of the American Statistical Association 97(458), 601–610.

- Peña and Rodríguez (2006) Peña, D. and J. Rodríguez (2006). The log of the determinant of the autocorrelation matrix for testing goodness of fit in time series. Journal of Statistical Planning and Inference 136(8), 2706–2718.

- Psaradakis and Vávra (2019) Psaradakis, Z. and M. Vávra (2019). Portmanteau tests for linearity of stationary time series. Econometric Reviews 38(2), 248–262.

- R Core Team (2020) R Core Team (2020). R: A Language and Environment for Statistical Computing. Vienna, Austria: R Foundation for Statistical Computing. ISBN 3-900051-07-0.

- Rodríguez and Ruiz (2005) Rodríguez, J. and E. Ruiz (2005). A powerful test for conditional heteroscedasticity for financial time series with highly persistent volatilities. Statistica Sinica 15(2), 505–525.

- Tong and Lim (1980) Tong, H. and K. S. Lim (1980). Threshold autoregression, limit cycles and cyclical data. Journal of the Royal Statistical Society: Series B (Methodological) 42(3), 245–268.

- Velasco and Wang (2015) Velasco, C. and X. Wang (2015). A joint portmanteau test for conditional mean and variance time-series models. Journal of Time Series Analysis 36(1), 39–60.

- Welsh and Jernigan (1983) Welsh, A. K. and R. W. Jernigan (1983). A statistic to identify asymmetric time series. In Proceedings of the Business and Economics Statistics Section, Alexandria, VA: American Statistical Association, pp. 390–395. American Statistical Association.

- Wong and Ling (2005) Wong, H. and S. Ling (2005). Mixed portmanteau tests for time-series models. Journal of Time Series Analysis 26(4), 569–579.

- Zhu (2013) Zhu, K. (2013). A mixed portmanteau test for arma-garch models by the quasi-maximum exponential likelihood estimation approach. Journal of Time Series Analysis 34(2), 230–237.