Unveiling the directional network behind financial statements data using volatility constraint correlation

Abstract

Financial data, such as financial statements, contain valuable and critical information that may assist stakeholders and investors in optimizing their capital to maximize overall economic growth. Since there are many variables in financial statements, it is crucial to determine the causal relationships, that is, the directional influence between them in a structural way, as well as to understand the associated accounting mechanisms. However, the analysis of variable-to-variable relationships in financial information using standard correlation functions is not sufficient to unveil directionality. Here, we use the volatility constrained correlation (VC correlation) method to predict the directional relationship between two arbitrary variables. We apply the VC correlation method to five significant financial information variables (revenue, net income, operating income, own capital, and market capitalization) of 2321 firms listed on the Tokyo Stock Exchange over 28 years from 1990 to 2018. This study identifies which accounting variables are influential and which are susceptible. Our findings show that operating income is the most influential variable while market capitalization and revenue are the most susceptible variables. Surprisingly, the results differ from the existing intuitive understanding suggested by widely used investment strategy indicators, the price–earnings ratio and the price-to-book ratio, which report that net income and own capital are the most influential variables affecting market capitalization. This analysis may assist managers, stakeholders, and investors to improve financial management performance and optimize firms’ financial strategies in future operations.

1 Introduction

The advent of information technology has made it possible to store and classify a large amount of financial data in real time on an unprecedented scale [1]. Financial information can be represented by a vast variety of data types. However, one of the most abundant types of data is multivariate time-series data, in which correlations among different assets are often used to perform risk management analysis, determine investment strategies, and improve financial management.

The correlation structure in financial markets has been investigated in many studies at different scales. Preis et al. analyzed 72 years of daily closing prices of the 30 stocks of the Dow Jones Industrial Average and found that the average correlation among the stocks is linearly scaled with market stress at various time scales [2]. Laloux et al. applied random matrix theory to understand the statistical structure of the correlation matrix of price changes and showed that there is a significant agreement between theoretical predictions and real data related to the density of eigenvalues [3]. This study raises serious questions about Markowitz’s naive use of empirical correlation matrices for portfolio risk management. Plerou et al. also applied random matrix theory to analyze the cross-correlation matrix of price changes of the largest 1000 US stocks [4]. Their findings showed that randomness cannot explain the universal and non-universal properties that enable the identification of cross-correlations between stocks. Jiang and Zheng uncovered the positive and negative subsector structures of Chinese, US, and global stock markets by applying a random matrix theory analysis and taking into account the sign of the components in the eigenvectors of the cross-correlation matrix [5]. Cross-correlations between volume change and price change of financial indexes were studied by [6]. Long-range magnitude cross-correlations in real-world data from various fields, such as finance, have also been studied intensively, using time-lag random matrix theory [7]. The integration of random matrix theory and network methods was also used to unveil correlation and network properties of 20 financial indexes [8]. The importance and novelty of physical methods applied to the study of financial cross-correlation analysis have been highlighted by Kwapien and Drozdz in their extensive review [9]. In particular, the application of random matrix theory to financial multivariate time series data deserved special attention. In this regard, several works have extended and further applied this statistical mechanics approach to the field of finance, namely [10, 11, 12, 13, 14, 15].

However, there are many examples of datasets in finance in which standard correlation metrics cannot detect the directionality of the correlation (i.e., causality). To solve this directionality problem, Ochiai and Nacher [16, 17, 18] introduced the volatility constrained correlation (VC correlation) method, which enables us to determine the directionality of influence, a critical feature that cannot be determined by applying only standard correlation analysis techniques. The directionality of influence between the Japanese Nikkei 225 stock index and other financial markets is determined [16]. VC correlation was applied to daytime and overnight returns, confirming the amplification of the negative correlation between them and consistency with the time causality [17]. Moreover, VC correlation was also used to analyze biological data and to predict gene regulatory interactions with high accuracy [18].

Meanwhile, financial statements are essential for decision making, such as investment and mergers and acquisitions, by shareholders, investors, and managers. Financial statements help improve the optimal allocation of capital and promote whole economies. The VC correlation approach has not been applied to financial statement analysis, despite its importance in fraud analysis as well as profitability. Handayani et al. identified the absence of correlation of financial statement components as red flags for detecting financial statement fraud [19]. Qualitative textual content in annual reports has been studied to predict fraud [20]. Ozdagoglu et al. classified financially correct and false statements corresponding to Turkish firms listed on Borsa Istanbul using a decision tree, logistic regression, and artificial neural networks [21]. Spathis developed a model for detecting the factors associated with false financial statements using univariate and multivariate statistical techniques, such as logistic regression [22]. Sorkun and Toraman detected fraud in e-ledgers through financial statements, using data-mining methods, such as support vector machines, decision stump, M5P tree, J48 tree, random forest, and decision tables [23].

Financial statements are closely linked to profitability and earnings prediction capability. This important subject has been analyzed in many works using different techniques. For example, Carstina et al. studied the correlation analysis of asset management and profitability indicators [24]. Ou and Penman studied the connection of a large set of financial statement variables with the direction of 1-year-ahead earnings changes [25]. Ishibashi et al. verified the applicability of variable selection using data-mining techniques for financial statement data [26]. Lokanan et al. evaluated the possibility of rating the creditworthiness of a firm’s quarterly financial report using a dynamic anomaly detection method in the case of Vietnamese listed firms [27]. Andres et al. applied machine-learning algorithms to study business profitability by preference learning [28]. Wimmer and Rada applied information technology, such as decision trees and genetic algorithms, to fundamental financial statement data to predict the direction of market capitalization [29]. Yan and Zheng constructed fundamental signals from financial statements and used a bootstrap approach to evaluate the impact of data mining on fundamental-based anomalies, finding that they are better explained by mispricing [30].

Although standard data analyses may reveal positive correlation tendencies among most of these accounting values, the causality between them has not been sufficiently investigated and clarified from a data science viewpoint. The causality or directionality of influence between them is difficult to determine using standard methods, such as standard correlation coefficients. In this work, we determine the direction of influence among the five primary financial accounting data (revenue, operating income, net income, own capital, and market capitalization) using the data-driven VC correlation technique and accounting data of 2321 firms listed from 1990 to 2018 on the Tokyo Stock Exchange, a standardized equities market in Japan. The observed directionality network of accounting variables enables us to observe the direct influence between accounting variables for the first time, suggesting future investment strategies and financial operations management. Our findings reveal not only that operating income is the most influential variable but also that market capitalization and revenue are the most susceptible variables. Interestingly, these predictions differ from the conventional understanding suggested by widely used investment strategy indicators, the price-earnings ratio and price-to-book ratio, which posit net income and own capital as the most influential variables on market capitalization. Therefore, our novel analysis may assist managers, stakeholders, and investors to improve financial strategies in future operations, and also may be useful in related financial engineering areas, such as fraud predictions and profitability forecasts.

2 Data

The Tokyo Stock Exchange in Japan is the world’s third largest exchange by market capitalization after the New York Stock Exchange and The Nasdaq Stock Market. Although there are many research works on the US market, there is also a necessity to investigate the Asian market which is emerging in the globe. In this study, we used the financial data of the Tokyo Stock Exchange, the largest exchange market in Asia, to study the directionality between financial data.

We use the five primary annual accounting data (revenue, operating income, net income, own capital, market capitalization) of 2321 firms listed on the Tokyo Stock Exchange over 28 years from 1990 to 2018. We exclude accounting data of banks, securities, non-life insurance, and life insurance companies, whose accounting data structure differs from that of general business companies.

3 Methods

3.1 Metrics

Let , , , , and be revenue, net income, operating income, own capital, and market capitalization, respectively, of company in year .

We define the rate of change of the five accounting variables (revenue, income, operating income, own capital, and market capitalization). The rate of change of revenue, own capital, and market capitalization are defined as follows:

| (1) | |||||

| (2) | |||||

| (3) |

respectively. Similarly, the rate of change of net income and operating income are defined by

| (4) | |||||

| (5) |

respectively. Here, for the definition of and , we use revenue as the denominator instead of and in order to normalize the rate of change properly. The reason is as follows. If we use net income or operating income as the denominator, they could have a negative value or an exceedingly small value. In such a case, the rate of change of income and operating income could take an extreme value, which would be difficult to handle.

3.2 Standard correlation

Let be the change rate of accounting variable in year for company defined in the previous subsection. Here, represents , , , , or (revenue, net income, operating income, own capital, or market capitalization, respectively).

The average and standard deviation of for a given period are given by

| (6) | |||

| (7) |

For a paired data set , the standard correlation coefficient (Pearson correlation coefficient) is given by

| (8) |

Let be the average of the correlation coefficient for all firms, and be the standard deviation of correlation as follows:

| (9) | |||

where is the total number of firms.

3.3 Volatility constrained correlation

In this subsection, we introduce VC correlation following [16]. This metric enables us to amplify the correlation and identify the directionality of the influence.

Let be a subset of all time points . We define the expectation value, standard deviation, and correlation coefficient, where the data points are constrained to the subset as follows:

| (11) | |||

| (12) | |||

where denotes the number of elements of .

As a special case of , we set

| (14) |

where is the cutoff threshold, and in the following, we set so that we have enough data points to calculate the VC correlation. Later in Section 4.3, we will discuss how the results change by varying the threshold . For a pair of two accounting variables and , we define the VC correlation between them as follows:

| (15) | |||

| (16) |

Here, we call and the VC correlation between the accounting variables and of company . If is greater than , then the accounting variable has more influence on the accounting variable than in the opposite direction (i.e., accounting variable is more susceptible to accounting variable ).

We define the difference in VC correlations for the accounting variables and in company as follows:

| (17) |

On the one hand, if is positive, then the directionality of influence goes from to . On the other hand, if is negative, then the directionality of influence is from to .

The expectation value and standard deviation of the difference in VC correlations are given by

| (18) | |||

respectively.

Here,

| (20) |

where and denote the number of elements of and respectively, and indicates the number of elements of .

We examine the statistical significance of the directionality between the two accounting variables by computing the p-value when the null hypothesis is that the mean value of is zero. The threshold for statistical significance is that the p-value is less than . Here, we evaluate the p-value from the Z-score computed by . The results are shown in detail in the next section.

4 Results

4.1 VC correlation analysis predictions

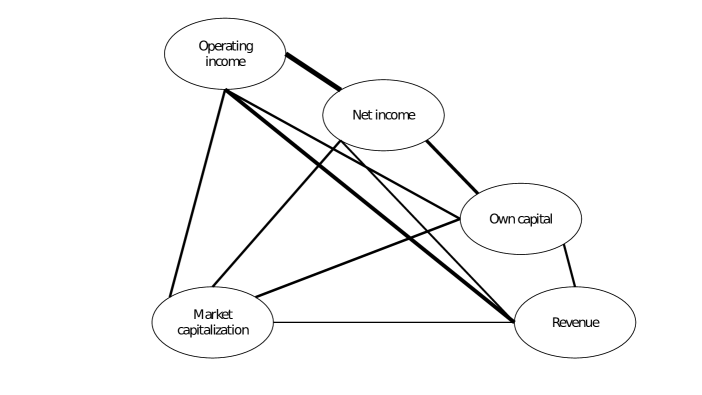

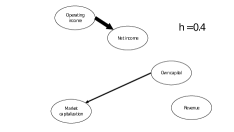

In Table 1, we show the results for the average of correlation , the standard deviation of correlation , and the number of firms for VC correlation computation for each paired accounting variable . Table 1 shows that all the averages of the correlation coefficient are positive, indicating that all five significant accounting variables are positively correlated. From these results, we plot the undirected network for the correlation relationship between the five accounting variables, as shown in Fig. 1.

The standard correlation analysis shown in Fig. 1 provides no information about the directionality between the accounting variables. By contrast, the VC correlation analysis enables us to observe the directionality between accounting variable pairs. In Table 2, we show the expectation values of the difference of VC correlation , the standard deviations of the difference of VC correlation , the directionality from one variable to another shown by arrow symbols (i.e., “” or “”), and p-values as the statistical significance of the predicted directionality.

From the expectation value and the standard deviation of the difference of the VC correlation shown in Table 2, we can determine the directionality (i.e., “” or “” in Table 2) as follows. If is positive (resp. negative) and the p-value is less than , then the directionality is from the first item to the second item (resp. from to ) with statistical significance. If the p-value is more than , there is no statistical significance, and we cannot say anything about directionality. In other words, when there is statistical significance, is an indicator of the directionality between the accounting variables and . We show the directionality in the right-most column in Table 2.

As an example, we explain the first row of Table 2. This row shows the result for the pair of net income(i) and market capitalization(m). The first variable is net income(i), and the second variable is market capitalization(m). Because of this pair is positive (), the directionality of the pair is from net income(i) to market capitalization(m) with very high statistical significance (p-value is . This directionality is indicated by the right arrow in the last column of the first row of Table 2.

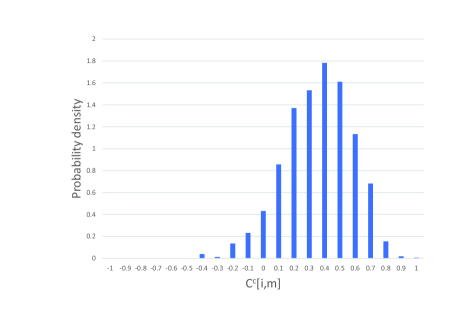

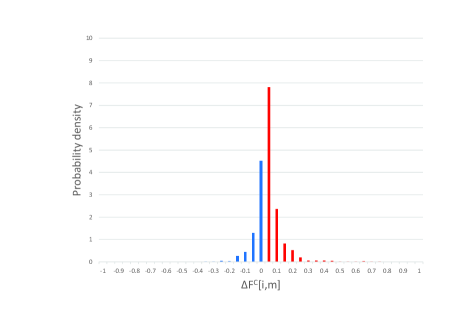

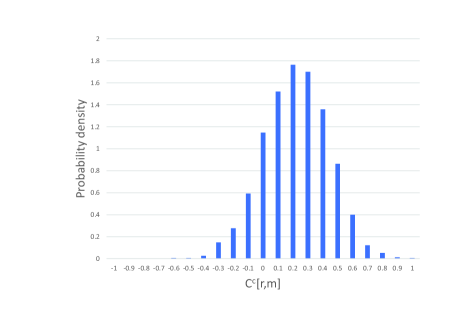

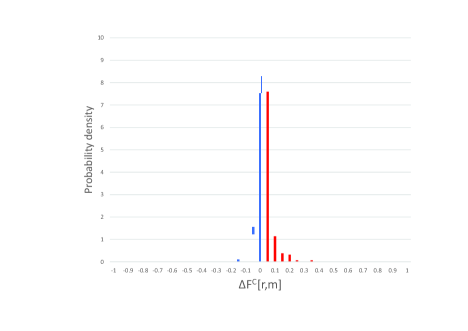

As complementary information, Fig. 2(a) shows the distribution of the correlation coefficients between net income(i) and market capitalization(m). Fig. 2(b) shows the distribution of the difference of VC correlations . Meanwhile, Fig. 3(a) shows the distribution of the correlation coefficient between revenue(r) and market capitalization(m). Fig. 3(b) shows the distribution of the difference of VC correlation .

We can observe that the distribution of the difference in VC correlations in Fig. 2(b) is asymmetric compared to Fig. 3(b). This implies that there is directionality from net income to market capitalization. Although the asymmetry appears to be small in Fig. 2(b), the large sample size makes the p-value very small, as shown in the first row of Table 2 (p-value is ). This indicates that there is sufficient statistical significance for the suggested directionality.

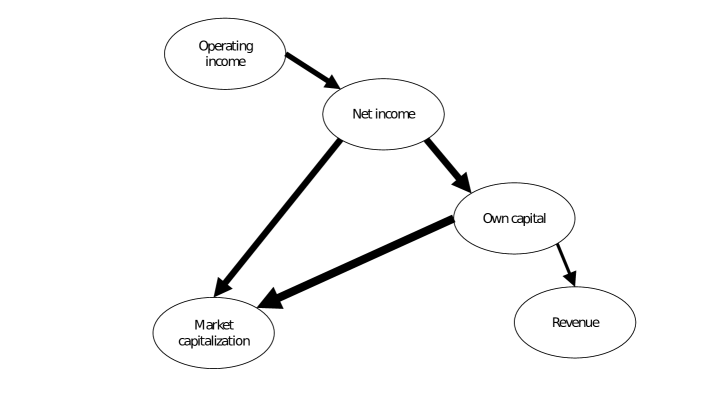

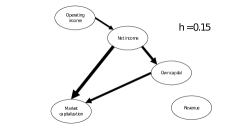

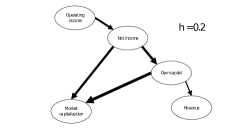

As shown in Table 1 and Fig. 1, all the correlations between the accounting variables are positively correlated. However, some pairs of accounting variables have not only positive correlations but also directionality of influence with statistical significance, as shown in Table 2. From the directionality of the VC correlations presented in Table 2, we show the directionality network in Fig. 4. The five pairs of accounting variables have directionality of influence with statistical significance, and we show them as five oriented links in Fig. 4. A comparison of Fig. 4 with Fig. 1 clearly shows the directionality between the accounting variables.

4.2 Statistical validation analysis

To further validate these results, we perform two statistical tests. The first validation requires splitting the data into two groups and validating the results for each group independently. For the second test (randomization), we reshuffle the data to check whether the results can be verified.

For the first statistical test, we split the data of all companies into two groups of equal numbers (each part has half). Specifically, we arrange the data in order of decreasing security codes and divide them into an odd-numbered group and an even-numbered group. We then compute the VC correlation for these two groups in the same way as for the full dataset.

The statistical analysis results are presented in Table 3. All the results with statistical significance in the splitting data are consistent with the directionality result of the original non-splitting result. Note that when the sample size decreases, the statistical significance tends to decrease. However, the test results indicate that the directionality signal was sufficiently robust and consistent with the original results (directionality) with a raised threshold of 0.2. Therefore, we conclude that the splitting data analysis validated the original directionality.

Second, we randomize the data by randomly swapping the accounting variables for each company to calculate the VC correlation. We show the results in Table 4. We compute all pairs whose directionality is confirmed in the original data. As expected, the statistical significance of directionality completely disappears for all pairs. This means that even when the threshold is raised to 0.2, the statistical signal of directionality vanishes, as expected. This indicates that the directional statistical signal of the original calculation is reliable.

In summary, we have validated the results using two methods, which significantly support the robustness and reliability of the original predictions.

4.3 Determination of threshold

The present analysis has been done with the threshold set up as 0.2. In what follows, we will discuss how the results change when we vary the threshold .

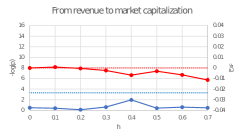

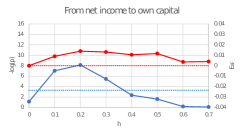

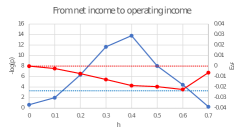

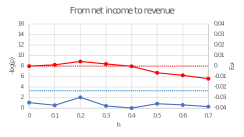

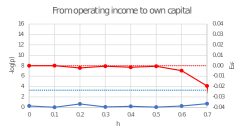

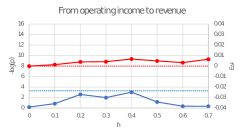

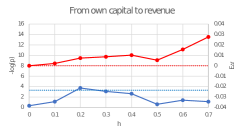

In Fig. 5, for each accounting variable pair , we have displayed and p-value as a function of the threshold . (That is, the horizontal axis is the threshold , and the vertical axis is for directionality and for statistical significance.) The blue dotted line indicates the threshold value of . The red dotted line indicates . If the blue line exceeds the blue dotted line, there is a statistical significance. Furthermore, in that case, if (red line) is positive (above the red dotted line), then a directionality is predicted from to . Conversely, if it is negative, a directionality is predicted from to .

The relation between the statistical significance of directionality predictions and the effect of the threshold parameter is shown in Fig. 5. As a first example, in Fig. 5(a), when and , there is a statistical significance (blue line is above the blue dotted line) and (red line) is positive. This indicates that there is a directionality from net income to market capitalization. Next, in the case of Fig. 5(f), there is statistical significance when and . In that case, is negative, so the direction is from operating income to net income. In the case of Fig. 5(c), the blue line never exceeds the blue dotted line, so there is no statistical significance for any threshold . Therefore, there is no directional relationship between revenue and market capitalization. All results in Fig. 5 show that the directionality does not change when the threshold is shifted to some extent, indicating that the results are robust to these changes.

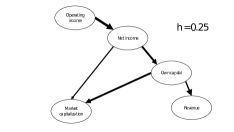

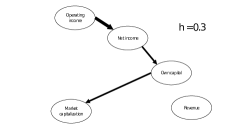

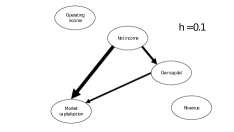

Fig. 6 shows how the structure of the directional network changes when the threshold is varied. The thickness of the oriented links is proportional to , and the greater the thickness, the greater the statistical significance. As shown in Fig. 6, as the threshold increases, the number of links increases, reaching the maximum number of links and link thickness at . Moreover, when increases further, all the links vanish progressively. Since we have the number of links as well as the link strength (thickness) reach a maximum when the threshold is 0.2, we selected the threshold for the computation as shown in Section 4.1. It is worth noting that as the threshold increases, the directional network structure is progressively unveiled starting from zero number of links (), and reaches its maximum at . From this point, the links start vanishing, driven by a decreasing of the statistical significance ().

4.4 Interpretation of the results

The accounting variables in our analysis belong to several categories of financial accounting. Revenue, operating income, and net income are the main accounting variables in the income statement. In accounting terms, revenue is calculated first, then operating income, and finally, net income. Own capital is an accounting variable found in the balance sheet and is equivalent to total assets minus liabilities. Market capitalization (or market cap) is the total market value of publicly traded shares and is equivalent to the share price multiplied by the number of shares. By bearing these key concepts in mind, we can derive the following findings from our data-driven analysis.

First, Fig. 4 shows that operating income is a source node, while market capitalization and revenue are sinking nodes. In other words, operating income is the most influential accounting variable, while market capitalization and revenue are the most susceptible variables. Market capitalization is determined by the balance of supply and demand of market participants and the shareholders’ strategy, which are mainly affected by the results of firms’ operational management. Therefore, it is reasonable to assume that market capitalization is the most susceptible variable of the five variables.

Second, and more importantly, Fig. 4 shows that net income and own capital influence market capitalization. This can be understood as follows. Market participants often evaluate the share price by the price–earnings ratio and price-to-book ratio computed from net income and own capital. Therefore, net income and own capital are thought to be the most influential items for market capitalization, as most investors often use these ratios as indicators. However, Fig. 4 reveals that operating income has more influence on all accounting variables than net income and own capital, which are the only middle of influence flow in the directed network. This novel finding suggests that the usage of operating income rather than net income and own capital, which have been traditionally used to calculate the price–earnings ratio and the price-to-book ratio investment indicators, could lead to notably improved investment strategies.

Third, Fig. 4 shows that operating income is the most influential item, affecting net income, which finally affects revenue. Revenue is the most susceptible item, which is against the calculation order of the statement of operation. Operatively, net income is calculated from operating income, which is calculated from revenue. Therefore, the order of influence in the context of income statement calculation is supposed to be in the order of revenue to operating income, and finally to net income. However, from our data-driven analysis, the influence order is different, which implies that operating income rather than revenue should be the focus of management strategy, which is our third main finding.

Since corporate finance and the structure of capital markets are common throughout the world, it is expected that we can observe a similar directionality network structure in other markets around the world. Indeed, it would be very interesting to extend this research methodology to the study of markets in other countries. In our view, the analysis could unveil not only the similarities but also the genuine differences of each market, providing a global understanding of the financial statement data and their interdependencies.

5 Conclusion

Previous studies of correlation coefficients in finance data have found out about the correlation between two variables but not their direction [2, 4, 5, 6, 7, 8]. However, we were able to capture the directionality between variables in financial statement data that cannot be captured by ordinary correlation coefficients.

In this study, the VC correlation approach unveiled the directionality between five major accounting variables, which is difficult to obtain using standard correlation methods. Our data-driven computations yielded new insights on major accounting variables, which can be translated into novel recommendations for investment strategies. We summarize our findings as follows.

First, from the directionality network, we observed that operating income is the origin of influence on the other four accounting variables (net income, own capital, market capitalization, and revenue). Market capitalization and revenue are the most susceptible accounting variables. Second and more importantly, although market participants often focus on net income and own capitalization to evaluate the share price for investment strategy, operating income may be a better accounting variable on which to focus. Third, the influence order of revenue, operating income, and net income differs from the order of accounting calculation of income statements.

In summary, we believe that these results may lead to improved performance of financial management and application of optimal financial strategies for firms in future operations. Financial engineering-related areas, such as fraud detection and profitability analysis, could also benefit from our findings. In future work, we aim to expand the number of accounting variables to obtain a large-scale map of the directional interactions that governs global financial flows.

6 Acknowledgments

T.O. was partially supported by a JSPS Grant-in-Aid for Scientific Research (Grant Number 15K01200).

References

- [1] R.N.Mantenga, H.E.Stanley, An Introduction to Econophysics, Cambridge University Press, Cambridge,UK, 2000.

- [2] T. Preis, D.Y. Kenett, H.E. Stanley, D. Helbing, E. Ben-Jacob, Quantifying the behavior of stock correlations under market stress, Sci. Rep. 2(2012) 752.

- [3] L. Laloux, P. Cizeau, J. Bouchaud, M. Potters, Noise dressing of financial correlation matrices, Phys. Rev. Lett. 83(1999) 1467.

- [4] V. Plerou, P. Gopikrishnan, B. Rosenow, L.A.N. Amaral, H.E. Stanley, Universal and nonuniversal properties of cross correlations in financial time series, Phys. Rev. Lett. 83(1999) 1471.

- [5] X.F. Jiang, B. Zheng, Anti-correlation and subsector structure in financial systems, EPL 97(2012) 48006.

- [6] B. Podobnik, D. Horvatic, A.M. Petersen, H.E. Stanley, Cross-correlations between volume change and price change, PNAS, 106(52)(2009) 22079.

- [7] B. Podobnik, D. Wang, D. Horvatic, I. Grosse, H.E. Stanley, Time-lag cross-correlations in collective phenomena, EPL, 90(2010) 68001.

- [8] S. Kumar, N. Deo, Correlation and network analysis of global financial indices, Phys. Rev. E 86(2012) 026101.

- [9] J. Kwapień, S. Drożdż, Physical approach to complex systems, Physics Reports, 515(3–4)(2012) 115.

- [10] V. Plerou, P. Gopikrishnan, B. Rosenow, L.A.N. Amaral, T. Gühr, H.E. Stanley, Random matrix approach to cross correlations in financial data, Phys. Rev. E 65 (2002) 066126.

- [11] A. Utsugi, K. Ino, M. Oshikawa, Random matrix theory analysis of cross correlations in financial markets, Phys.Rev. E 70 (2004) 026110.

- [12] J. Kwapień, S. Drożdż, P. Oświe¸ cimka, Statistical properties of stock market eigensignals, Acta Phys. Pol. B 36 (2005) 2423.

- [13] B. Tóth, J. Kertész, Increasing market efficiency: Evolution of cross-correlations of stock returns, Physica A 360 (2005) 505.

- [14] C. Biely, S. Thurner, Random matrix ensembles of time-lagged correlation matrices: derivation of eigenvalue spectra and analysis of financial time-series, Quant. Finance 8 (2008) 705.

- [15] J. Kwapień, S. Drożdż, A.Z. Górski, P. Oświe¸ cimka, Asymmetric matrices in an analysis of financial correlations, Acta Phys. Pol. B 37 (2006) 3039.

- [16] T. Ochiai, J.C. Nacher, Volatility-constrained correlation identifies the directionality of the influence between Japan’s Nikkei 225 and other financial markets, Physica A 393(2014) 364.

- [17] T. Ochiai, J.C. Nacher, Predicting link directionality in gene regulation from gene expression profiles using volatility-constrained correlation, Biosystems, 145(2016) 9.

- [18] T. Ochiai, J.C. Nacher, VC correlation analysis on the overnight and daytime return in Japanese stock market, Physica A 515(2019) 537.

- [19] H. Handayani, T. Tarjo, Y. Rimawati Correlation of financial statement components in detecting financial fraud, Asia Pac. Fraud J. 1(2)(2016) 275.

- [20] S. Goel, J. Gangolly, Beyond the numbers: Mining the annual reports for hidden cues indicative of financial statement fraud Intell. Sys. Acc. Fin. Mgmt. 19(2012) 75.

- [21] G. Ozdagoglu, A. Ozdagoglu, Y. Gumus, G. Kurt-Gumus, The application of data mining techniques in manipulated financial statement classification: The case of Turkey, J. AI Data Min. 5(1) (2017) 67.

- [22] C. T. Spathis, Detecting false financial statements using published data: Some evidence from Greece, Manag. Audit. J. 17(4)(2002) 179.

- [23] M. C. Sorkun, T. Toraman, Fraud detection on financial statements using data mining techniques, Int. J. Intell. Syst. Appl. Eng. 5(3)(2017) 132.

- [24] S. Carstina, M. Siminica, D. Circiumaru, A. Tanasie, Correlation analysis of the indicators of asset management and profitability, Int. J. Econ. Bus. Admin. 3(2)(2015) 3.

- [25] J.A. Ou, S.H. Penman, Financial statement analysis and the prediction of stock returns, J. Acc. Econ. 11(4)(1989) 295.

- [26] K. Ishibashi, T. Iwasaki, S. Otomasa, K. Yada, Model selection for financial statement analysis: Variable selection with data mining technique, Proc. Comput. Sci. 96(2016) 1681.

- [27] M. Lokanan, V. Tran, N.H. Vuong, Detecting anomalies in financial statements using machine learning algorithm: The case of Vietnamese listed firms, Asian J. Acc. Res. 4(2)(2019) 181.

- [28] J. de Andres, P. Lorca, A. Bahamonde, J.J. del Coz, The use of machine learning algorithms for the study of business profitability: A new approach based on preferences, Int. J. Digit. Acc. Res. 4(8)(2004) 99.

- [29] H. Wimmer, R. Rada, Applying information technology to financial statement analysis for market capitalization prediction, Open J. Acc. 2(2013) 1.

- [30] X. Yan, L. Zheng, Fundamental analysis and the cross-section of stock returns: A data-mining approach, Rev. Financ. Stud. 30(4)(2017) 1382.

| [net-income(i), market-cap(m)] | 0.308 | 0.219 | 1310 |

| [own-capital(o), market-cap(m)] | 0.337 | 0.232 | 1388 |

| [revenue(r), market-cap(m)] | 0.169 | 0.218 | 1184 |

| [operating-income(p), market-cap(m)] | 0.317 | 0.206 | 1419 |

| [net-income(i), own-capital(o)] | 0.427 | 0.216 | 1366 |

| [net-income(i), operating-income(p)] | 0.610 | 0.268 | 1408 |

| [net-income(i), revenue(r)] | 0.273 | 0.293 | 1149 |

| [operating-income(p), own-capital(o)] | 0.302 | 0.221 | 1376 |

| [operating-income(p), revenue(r)] | 0.505 | 0.278 | 1461 |

| [own-capital(o), revenue(r)] | 0.293 | 0.257 | 1301 |

| p-value | directionality | |||

|---|---|---|---|---|

| [net-income(i), market-cap(m)] | 0.0110 | 0.0687 | ||

| [own-capital(o), market-cap(m)] | 0.0129 | 0.0730 | ||

| [revenue(r), market-cap(m)] | -0.000422 | 0.0502 | ||

| [operating-income(p), market-cap(m)] | 0.00299 | 0.0613 | ||

| [net-income(i), own-capital(o)] | 0.0139 | 0.0892 | ||

| [net-income(i), operating-income(p)] | -0.00712 | 0.0529 | ||

| [net-income(i),revenue(r)] | 0.00441 | 0.0570 | ||

| [operating-income(p), own-capital(o)] | -0.00217 | 0.0664 | ||

| [operating-income(p), revenue(r)] | 0.00395 | 0.0499 | ||

| [own-capital(o), revenue(r)] | 0.00734 | 0.0709 |

| p-value | directionality | |||

|---|---|---|---|---|

| [net-income(i), market-cap(m)] (even) | 0.00964 | 0.0651 | ||

| [net-income(i), market-cap(m)] (odd) | 0.0123 | 0.0720 | ||

| [own-capital(o), market-cap(m)] (even) | 0.0136 | 0.0760 | ||

| [own-capital(o), market-cap(m)] (odd) | 0.0123 | 0.0699 | ||

| [net-income(i), own-capital(o)] (even) | 0.0111 | 0.0866 | ||

| [net-income(i), own-capital(o)] (odd) | 0.0167 | 0.0916 | ||

| [net-income(i), operating-income(p)] (even) | -0.00794 | 0.0568 | ||

| [net-income(i), operating-income(p)] (odd) | -0.00631 | 0.0488 | () | |

| [own-capital(o), revenue(r)] (even) | 0.0102 | 0.0672 | ||

| [own-capital(o), revenue(r)] (odd) | 0.00458 | 0.0741 | () |

| p-value | directionality | |||

|---|---|---|---|---|

| [net-income(i), market-cap(m)] (r) | 0.0695 | 0.564 | ||

| [own-capital(o), market-cap(m)] (r) | 0.0741 | 0.789 | ||

| [net-income(i), own-capital(o)] (r) | 0.0903 | 0.560 | ||

| [net-income(i), operating-income(p)] (r) | 0.0534 | 0.560 | ||

| [own-capital(o), revenue(r)] (r) | 0.0712 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|