On the correlation analysis of illiquid stocks

Abstract

The serial correlations of illiquid stock’s price changes are studied, allowing for unconditional heteroscedasticity and time-varying zero returns probability. Depending on the set up, we investigate how the usual autocorrelations can be accommodated, to deliver an accurate representation of the price changes serial correlations. We shed some light on the properties of the different serial correlations measures, by mean of Monte Carlo experiments. The theoretical arguments are illustrated considering shares from the Chilean stock market.

Keywords:

Illiquid stocks; Serial correlation; Weak dependence; Unconditional heteroscedasticity; Time-varying zero returns probability.

JEL Classification: C13; C22; C58.

1 Introduction

In quantitative finance, it is common to examine the serial correlations of financial assets. For a daily stock return , the correlations ) (), can be used for the momentum trading strategy. On the other hand, there is a huge literature considering the serial correlations to test if financial variables are efficient (see e.g. Harris and Kew (2014), Köchling, Müller and Posch (2019), Hurn, Martin, Phillips and Yu (2021,p41) and references therein). The autocorrelations can be investigated to specify the so-called ARMA-GARCH models (see Francq and Zakoïan (2019) Section 5.2, or McNeil, Frey and Embrechts (2015) Section 4.2.3). Several tools for investigating the serial correlations, taking into account for nonlinearities and/or heteroscedasticity, are available in the literature (see e.g. Romano and Thombs (1996), Lobato, Nankervis and Savin (2002), Patilea and Raïssi (2013) or Dalla, Giraitis and Phillips (2019)). Such kind of tools are widely used nowadays for many tasks. However, at the best of our knowledge, the presence of unconditional changes for the zeros returns probability is not taken into account in the correlations analysis of returns.

The main message conveyed by this study, is that the non-standard effects of the zero returns scheme, may lead to a misleading estimation of the financial variables serial correlations. First, let us underline that it is advisable to concentrate on the non zero returns. To see this through simple considerations, let us suppose for instance that (), with . Hence, it can be expected that observing is likely to be followed by , and vice et versa. Nevertheless, there is obviously no reason to think that a negative correlation, makes informative with regard to predicting or . In short, the zero returns are useless, if we are interested in price movements. As a consequence, we aim to investigate how past price changes can be possibly correlated with present price changes, correcting the effect induced by (i.e. use rather than . We have

assuming and provided that , , which shows that considering the standard for our task, can be quite misleading if . However, let us clarify that we are not claiming that zero returns are not informative at all (see Boudoukh, Richardson and Whitelaw (1994), Section 3.1 and references therein on this subject). For instance, it is well known that could be a piece of information for expecting whether or not (see Truquet (2019)). Actually, we shall use the possible non constant structure of the zero returns, to improve the estimation of the non zero returns correlations. Finally, let us clarify that is useful for specifying the ARMA part of the dynamics, while the , for some , is analyzed for the specifying the stylized financial effects, using for instance some GARCH model. The reader is referred to Patilea and Raïssi (2021) for more details on the analysis.

We aim to solve our issue following the approach introduced by Dunsmuir and Robinson (1981), Section 2, to take into account for missing values in time series. This consists in considering an imputation process , such that if the series is observed at date , and if it is missing. This process, originally introduced by Parzen (1963), is called the "amplitude modulated" sequence in the literature. Then, for some partially observed process , the empirical serial correlations are computed using (i.e. replacing the missing observations by zeros). Note that classically is assumed constant (see e.g. Stoffer and Toloi (1992) or Bondon and Bahamonde (2012) among others). Such procedure implies to correct adequately the empirical correlations, in order to retrieve a standard normal asymptotic distribution (see Dunsmuir and Robinson (1981)). In our context, as zero returns means irregularly observed price changes, it will be mathematically convenient to express our problem in a similar way. More precisely, we define if at date , and otherwise (see Hurn, Martin, Phillips and Yu (2021,p33) for intraday data). This makes our problem close to that of the missing value case, although is not formally missing when it is equal to zero. Nevertheless, the process is possibly non-stationary in our case. In addition, the presence of unconditional heteroscedasticity may also induce additional distortions in the autocorrelations measure. For these reasons, a corrected tool will be necessary to depict the correlation structure of the data adequately. Noting that we can reasonably assume that in general, then the corrections introduced in the paper are multiplicative. Hence, the main goal of the paper is to solve the adequate estimation of for eventual linear specification. On the other hand, let us underline that since , then the analysis of lead to correct the testing of the presence of the persistence of shocks or some long memory effects in the volatility, see Patilea and Raïssi (2021). Now let us examine the following examples illustrating that non-standard features for can be commonly observed for individual stocks.

1.1 An example from the Chilean stock market

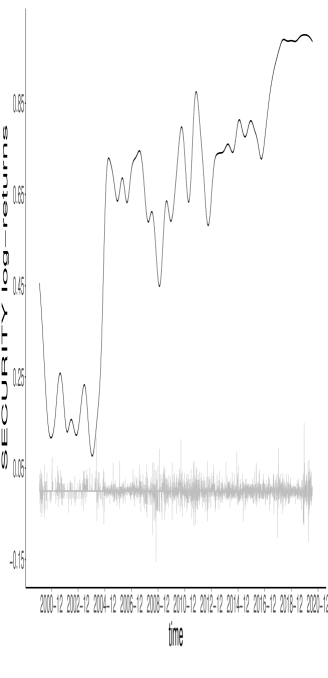

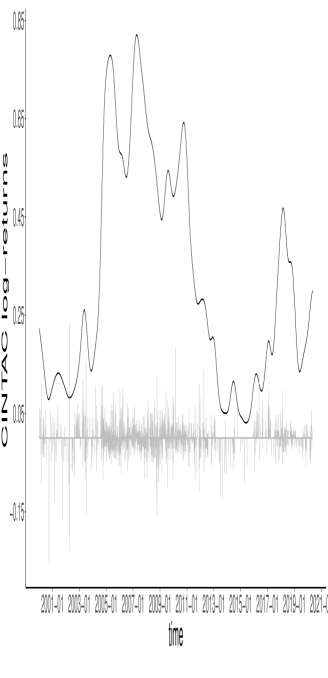

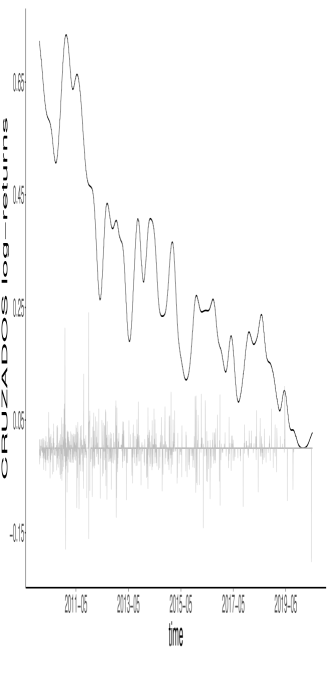

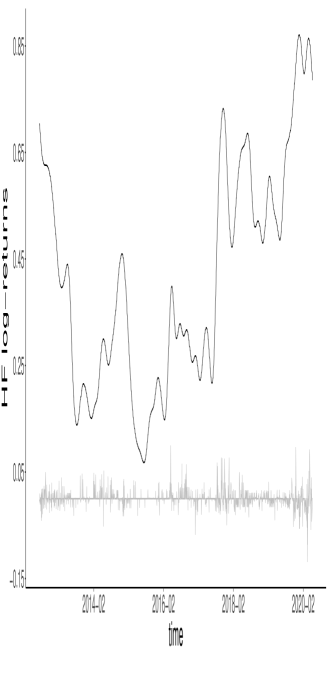

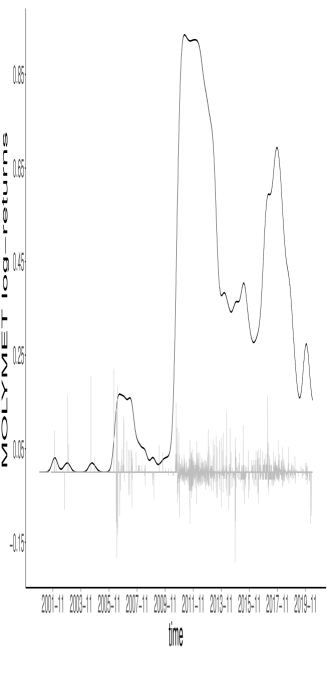

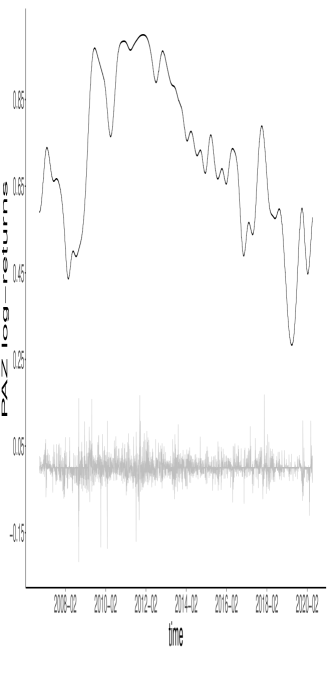

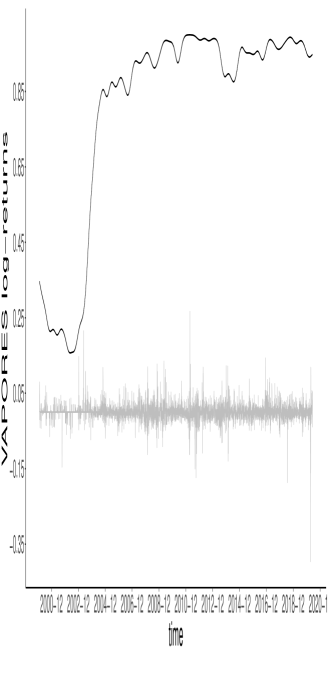

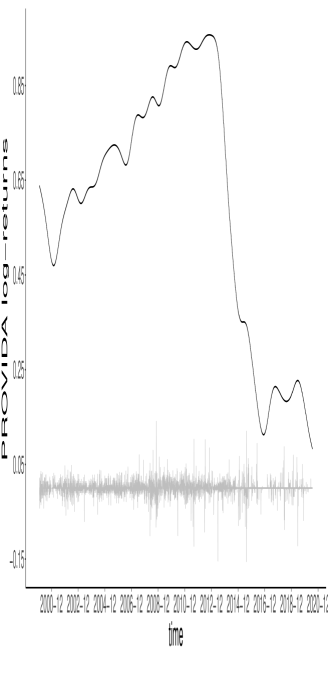

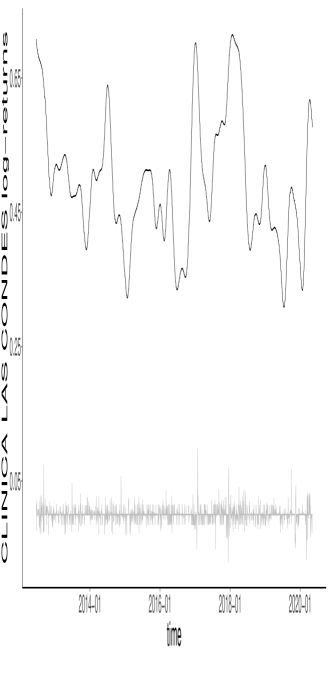

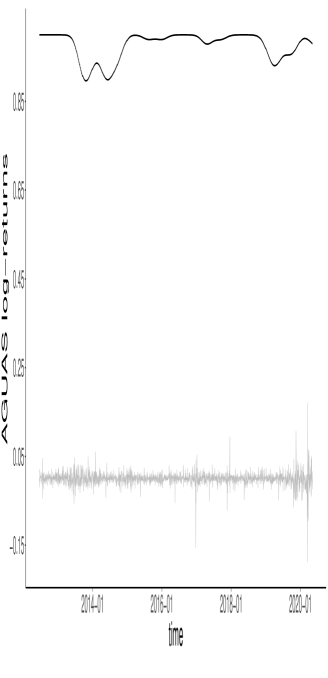

It is important to note that stocks with a large amount of zero returns, are quite common in all financial markets. In particular, it is well known that such a feature is especially observed for emerging markets (see e.g. Lesmond (2005,p424-426)). For the sake of illustration of the arguments presented above, we considered the closing prices of some firms taken from the Chilean stock market.222The author is grateful to Andres Celedon for research assistance. The data can be downloaded from the Yahoo Finance website. In Figure 1, we plotted the daily log-returns of stocks, that seem to exhibit non-constant zero returns probabilities. For several stocks, we can observe a large amount of years where the probability of observing a price change has a given level, and then, a quick shift can be noticed. Examining the Molymet stock in detail, we can observe a quick increase of the probability of observing a daily price change in the end of 2010. This could be explained by a capital increase of more than 216 million US Dollars, announced during the extraordinary shareholders meeting by August 13th, 2010. Note that more than 12.7 million new stocks have been issued in the end of October/early November 2010 on that occasion. Since then, it appears that the probability of a daily price change has never declined to its previous level. The quick increase of the daily price change probability for the Security bank stock, may be explained by the merger by absorption of the Dresdner Bank Lateinamerika in September 2004. In addition, the Security Bank issued more than 32.8 million new stocks after the capital increase announced during the extraordinary shareholders meeting by December 29th, 2004. Abrupt decreases of the liquidity levels can be also observed. For instance, the quick decrease of the daily trade probability for the Provida stock seems to be a consequence of the take-over bid of Metlife on Provida during September 2013. Other stocks seem to display long-run trending behaviors with regard to the non zero returns probability, as the Paz, HF or Cruzados stocks. The increase of for the Vapores stock during the 2000’s can be observed in a similar way for many stocks of the Chilean Stock market. Such a behavior is certainly the consequence of the fast development of the Chilean economy during this period. The consequences of such non-standard behaviors on the serial correlation estimation are further investigated in Section 5.2.

The structure of this study is as follows. In section 2, the theoretical framework is outlined. The main setting for the analysis of is also defined. In Section 3, the relevant serial correlation we may need to estimate the correlation structure of illiquid stocks is first highlighted. Subsequently, corrections for the autocorrelations in the stationary and non stationary cases are presented in Section 3.1 and Section 3.2. Thereafter, Monte Carlo experiments are conducted to assess the finite sample properties of the serial correlations estimators in Section 5. We also make additional comments on the autocorrelations of the Chilean stock market data presented above. Some concluding remarks are given in Section 6.

Throughout the paper the following notation is used. Let us consider a one-period profit-and-loss random variable . We assume that are observed, with the sample size. We denote by the -field generated by the past values of . Recall that if and if not. The almost sure convergence is denoted by , and the convergence in distribution is signified by . The convergence in probability is denoted by .

2 The theoretical framework

In time series econometrics, there is a significant body of works dealing with long-run phenomena. For example, reference can be made to the huge cointegration literature. In the field of financial returns, Mikosch and Stărică (2004) and Stărică and Granger (2005), have documented the presence of a long-run unconditional time-varying variance. This pattern can be noted especially when the period under study is relatively large. In order to take into account for such a behavior, Engle and Rangel (2008) have proposed the spline GARCH model. This model combines stochastic effects in order to capture the short run GARCH effects, and a deterministic specification to describe the long-run unconditional changes of the variance. The reader is also referred to Hafner and Linton (2010) for the multivariate case. In this paper, we rely on such an approach to describe the returns non-stationary behavior:

| (1) |

where is a random process specified below, and is non-constant deterministic, fulfilling the following assumption.

Assumption 1 (Unconditional time-varying variance).

The ’s are given by , where is a measurable deterministic and strictly positive function on the interval , such that , and satisfies a piecewise Lipschitz condition on .333The piecewise Lipschitz condition means: there exists a positive integer and some mutually disjoint intervals with such that where are Lipschitz smooth functions on respectively.

Let us underline that the Dahlhaus (1997) rescaling device is often used in order to describe long-run effects (see e.g. Phillips and Xu (2006), Xu and Phillips (2008), Cavaliere and Taylor (2007,2008), Patilea and Raïssi (2012,2013) or Wang, Zhao and Li (2019)). A triangular notation should be adopted in view of Assumption 1. However, the double subscript is suppressed for notational simplicity. In view of the above, can be non-constant, but we also possibly allow to be stochastic, as exposed below. Let us mention that Patilea and Raïssi (2014) have proposed tests, for determining if a purely deterministic specification of the variance is sufficient, or additional GARCH effects must be taken into account.

In a similar way to the above literature, we suppose that the unconditional probability of observing a daily price change is time-varying. More precisely, it is assumed that the probabilities , , are equal to deterministic non constant functions . Note that we do not exclude the presence of stochastic short time effects (i.e. the is stochastic), so is possibly dependent.

Assumption 2 (Non constant unconditional probabilities).

Assumption 1 and 2 are quite general, and allow for a wide type of specifications, as trending behaviors or abrupt breaks for instance. If the functions or are non-constant, then the returns process is not stationary. In view of Assumption 2, we have , at least for some subperiod in the sample. Concerning the non-constant variance, the studies mentioned above provide evidence of unconditional heteroscedasticity for financial variables with . Then, it is likely that the same holds when . In Figure 1, we can observe abrupt breaks as well as trending behaviors, for the probabilities of observing a daily price change. It is reasonable to think that such structural changes may happen for both the non zero returns probability and the variance. In addition, let us mention that, using the above mentioned rescaling device, Truquet (2019) studied the pointwise estimation of the time-varying transition probabilities

| (2) |

with application to capture non-constant features for South African stock returns. In our case, (2) suggests that , , are non constant. Finally, let us make the following comment on Assumption 1 and 2 jointly.

Remark 2.1.

If is time-varying, then it is easy to see that will be heteroscedastic whether is constant or not. However, in the sequel we will refer to the case where is time-varying (resp. constant), as heteroscedastic (resp. homoscedastic) in the sense that the prices changes (i.e. eliminating the zero returns) are heteroscedastic (resp. homoscedastic). When is constant and is time-varying, we will simply say that is not stationary, or have a time-varying zero returns probability to avoid confusion, although it is heteroscedastic. In short, is constant if and only if is constant, in view of Assumption 3 below.

The identifiability of (1) is ensured by considering the following assumption.

Assumption 3 (Identifiability).

We assume that and .

Note that the above condition is expressed conditional to , as we concentrate on the price changes. Usually in models such as (1) we set . However, allowing for a possible time-varying , then is in general non-constant in our case. The condition implies that , which is realistic since the stocks returns means are not significant in general.

If the sources of non stationarity are removed in (1), that is the unconditional heteroscedasticity and the time-varying probability, it can be expected that the remainder is stationary. The following assumption formalizes this idea.

Assumption 4 (Strict stationarity in the time-varying framework).

Given , the vectors and have the same joint distribution for any and any .

Now we turn to the dependence set-up used for . In the literature, a wide variety of models are available to capture the financial assets dynamics. Among many others, reference can be made to the large class of GARCH models first introduced by Engle (1982) (see the Bollerslev (2008) glossary). Hence, we consider a weak dependence concept, that allow for a wide range of specifications. In the sequel, we denote by

the mixing coefficients of . The reader is referred

to Davidson (1994) for details about the -mixing coefficients. Let us also introduce

, where denotes the

Euclidean norm.

Assumption 5 (Weak dependence condition for strong consistency).

There exist , , and , such that and .

Assumption 6 (Martingale difference condition for asymptotic normality).

(a) We assume that , and . (b) There exists such that .

Note that is allowed to be correlated under our mixing assumption. In Assumption 5, we make the usual trade-off between moment and mixing conditions (see Phillips (1987) and references therein). The Assumption 6(a) is consistent with an efficient market null hypothesis. Other dependence, prediction assumptions can be used to state the convergence and the asymptotic normality results below, as soon as convergence results are available. For instance, the reader is referred to Davidson (1994), Chapters 16 and 17, for the mixingale (asymptotic unpredictability) or the Near Epoch Dependence (NED) concepts.

3 Serial correlations in presence of zero returns

In this part, the serial correlations analysis of illiquid stocks is discussed in the light of the assumptions made above. For mathematical ease, the following notations are adopted. The correlations of the process are given by

As usual, we consider vectors of these autocorrelations: , for a given , fixed by the practitioner. The subscript zero means that the zero returns are included in the autocorrelations. Under Assumption 1-4, some basic computations show that

| (3) |

is constant. In the sequel, we consider . It is clear that the correlations of are not constant, due to the time-varying probabilities of observing a price change. As a consequence, these non-constant linear dynamics may be viewed as spurious. On the other hand, the unconditional heteroscedasticity does not play any role in the theoretical relation (3). Now, if in addition and are assumed constant, then does not depend on time:

| (4) |

In such a case, the notations can be simplified into , , and . It is interesting to note that the dependence effects in should be carefully taken into account to correctly measure the correlation structure. This last case is similar to the classical treatment of missing values in time series (see e.g. Stoffer and Toloi (1992)).

In view of Figure 1, non-stationary effects can be often assumed for . In addition, for computational reasons some bias could be introduced in the estimation step from the non-constant time-varying variance. These combined non-stationary behaviors can lead to erroneous conclusions. For instance, suppose that we are interested to measure the eventual non-zero correlations of a stock at different periods. In the case of the Molymet stock, using (3) may spuriously lead to conclude that the potential linear link between the returns is affected by the 2010 increase of capital. We can conclude therefore that if we are interested in analyzing the correlation structure of the price changes, then should be considered rather than . The methodology to handle the non-standard behaviors described above, will consist in applying a scale correction to the classical autocorrelation estimator

in order to obtain a consistent estimator of .

3.1 The stationary case

In this part, we suppose that , and are constant. In view of (4), let us introduce the autocorrelations estimator

| (5) |

and

see e.g. Stoffer and Toloi (1992) for this kind of correction. The subscript "pr" means that we remain with corrections based on probabilities. Introduce

The following proposition ensures that delivers a correct picture of the price changes autocorrelations. Recall that .

Proposition 3.1.

Suppose that is strictly stationary ergodic, such that and . Then, we have as .

Before moving forward to the case where is dependent, let us mention that the autocorrelations are often displayed with the confidence bounds under the hypothesis . For instance, it may serve to identify an horizon where the autocorrelations seem to vanish.

Proposition 3.2.

3.2 The non stationary case

Now both unconditional heteroscedasticity and time-varying zero returns probability are allowed. The cases where we have only unconditional heteroscedasticity, or only non-constant zero returns probability are briefly discussed in Remarks 3.1 and 3.2 below. From (3), the unconditional heteroscedasticity does not play any role in . However, in practice the numerator and denominator are computed separately on the whole sample. As a consequence, some heteroscedasticity effects are produced that must be taken into account for the estimation of . To this end, let us introduce the following estimator:

| (9) |

where

The kernel estimators of and are given by555If , then the corresponding term in the sum defining is set equal to zero. Note that in such a case, is often equal to zero.

where , and

The kernel function on the real line , and the bandwidth fulfill the following conditions.

Assumption 7 (Kernel and bandwidth).

-

(a)

is a continuous kernel function defined on the real line with compact support, such that for some finite real number , and .

-

(b)

As , .

Of course different bandwidths can be used for and . Nevertheless, for ease of exposition, the kernel estimators are presented with the same bandwidth. Define

where

We are now ready to state the following asymptotic results, in our non standard framework.

Proposition 3.4.

Now we shall compare the stationary case and the non-stationary case. If we suppose that the conditions of Proposition 3.1 hold (the variance and the zero return probability are constant), then we can write:

As a consequence, the correction (9) can be applied to the stationary case as well. The reverse is not true in general, as the combined effects of the heteroscedasticity and non-constant liquidity levels must be specifically taken into account. On the other hand, the "vpr" needs to estimate the probability structure, on the contrary to the "pr" correction. In the real data analysis below, a tool for identifying the "pr" and "vpr" cases is provided.

Let us end this section, by considering briefly the case where we have unconditional heteroscedasticity, and constant probability on one hand; and the case where the time-varying probability is the unique source of non-stationarity.

Remark 3.1 (Unconditional heteroscedasticity, constant zero returns probabilities).

Let us consider the assumptions of Proposition 3.3, strengthened by the assumption that is strictly stationary (i.e. , , are constant). In such a case, we have

and

for any . Therefore, the non-constant variance effect vanishes, as we can write . Hence, in view of (16), it is easy to see that

in the case of a time-varying variance, and a constant zero returns probability.

Remark 3.2 (Constant variance, time-varying zero returns probabilities).

Now, we assume that the conditions of Proposition 3.3 hold true, strengthened by the assumption that is constant. In a similar way as above we write

and

for any . Again, we readily have

in the case of constant variance, and time varying zero returns probability.

4 An index for deciding between and

In this part, we provide a tool to determine whether or should be used. From the above section, is suitable if we have , with

| (10) |

The use of , corresponds to the situation where there exists at least some , such that . The above alternatives can be viewed, in some sense, as a diagnostic for . If we decide that , then this is equivalent to assert that the following statements are not true:

-

(a)

and are constant for all ,

-

(b)

is non-constant, but has a constant zero returns probability,

-

(c)

, but has a time-varying zero returns probability.

If decide that all the ’s are equal to zero, then we can conjecture that (a), (b) or (c) holds true. This last assertion can only be conjectured, as we may have for some specific non-constant and functions, .

Now, let us introduce the index , where

5 Numerical illustrations

In this part, the different tools introduced in the previous sections, are first investigated by mean of Monte Carlo experiments. Then, the autocorrelation structures of the above presented Chilean market’s stocks are analyzed more deeply.

5.1 Monte Carlo experiments

The pointwise estimation of the correlation is studied (). Some comments are also made on the index for . In all the experiments, the following Data Generating Process (DGP) is considered

| (11) | |||||

where and are parameters given below. Note that and are only rescales of and according to Assumption 3. We set . In our simulation experiments, the sequence is defined in two ways. Firstly, to illustrate possible bias of correlated non-zero returns, we consider

| (12) |

if and are both different from zero, and if not. The innovations process is not correlated but dependent and defined as follows. Let us consider the process given in Romano and Thombs (1996): , where is standard Gaussian iid. Introducing the sequence which is equal to 1 if and , and if not, we set . As is strictly stationary, it is clear that is constant. From the specification of a dependence is allowed for (i.e., we have higher expectation to obtain if ). From a simulation of of length given in (12), we computed . Secondly, to illustrate the asymptotic normality results obtained under the no correlation hypothesis, we set with if , and if not. Using again a simulation of length , we computed . In all the cases, we have as and are taken independent. The possible non-stationary effects for will be handled by with

The parameters , and and give the cases of interest for our Monte Carlo experiments:

-

(i)

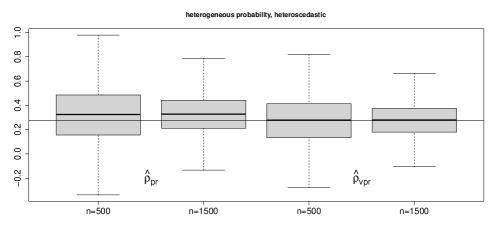

Heterogeneous probability, heteroscedastic: Both and are time-varying. We set , and , .

-

(ii)

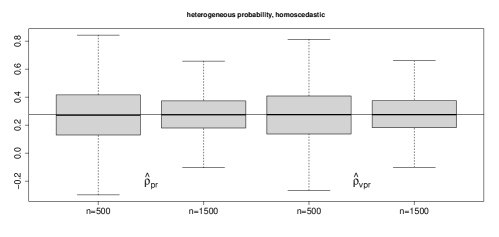

Heterogeneous probability, homoscedastic: is time-varying and is constant. We set and , .

-

(iii)

Homogeneous probability, heteroscedastic: is constant and is time-varying. We set , and .

-

(iv)

Homogeneous probability, homoscedastic: and are constant. We set and .

In all the experiments, independent trajectories of (11) are simulated, with lengths . Such sample sizes roughly correspond to 2 and 6 years of daily returns. All the settings are inspired from the real data study below. The outputs of our simulations are provided in box-plots in Figures 3-6 for the studied autocorrelations, and in Figures 9-10 for the index introduced in Section 4. In Table 2, the relative frequencies of "pr" and "vpr" autocorrelations outside their 5% level asymptotic confidence bounds are given. The bandwidths minimize the leave-one-out cross validation criterion (LOOCV) for the estimation of the probability structures , :

where is the estimator of using , and obtained by omitting .

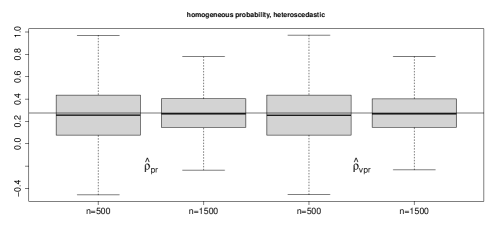

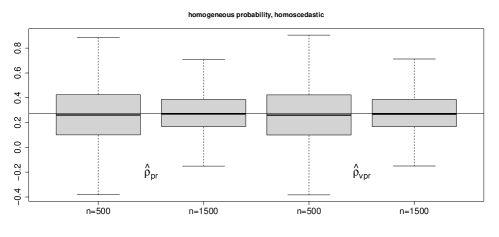

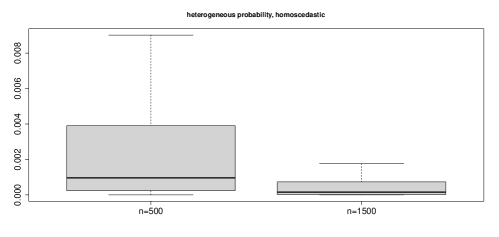

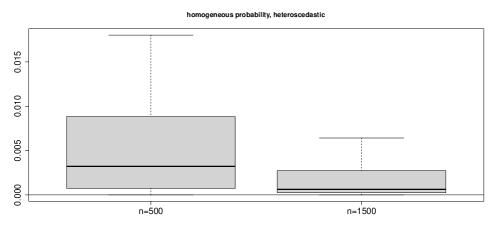

We begin with the situations where the "pr" and "vpr" corrections are both valid (i.e., the (ii), (iii) and (iv) cases, see Figure 10). Its turns out that the "pr" and "vpr" corrections seem unbiased and similar. Indeed, in such cases the and are asymptotically valid for estimating . At first sight there is no loss of efficiency for the more sophisticated "vpr" correction. Naturally, if there is some evidence that either or is constant, then it is better to use the simpler "pr" correction. Since is relevant in the (ii), (iii) and (iv) cases, it can be seen that the converges to zero as the samples are increased (see Figure 9).

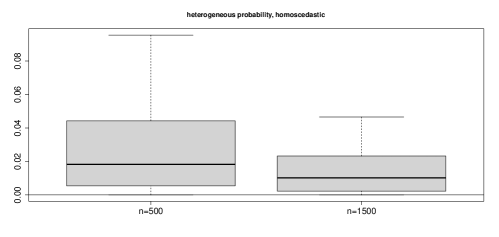

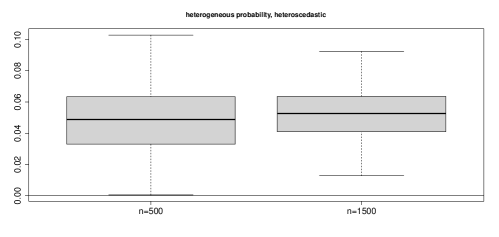

Now, case (i) is examined (i.e., the presence of both heterogeneous variance and non-zero returns probability, see Figure 9). It can be observed that only the "vpr" correction, seems to handle adequately the double source of non-stationarity. This is in accordance with the fact, that the numerator and the denominator of the serial correlations are computed separately, which induces some undesirable combined non-stationary effects for the estimator. Such effects cannot be taken into account, when only probabilities are considered for correcting the serial correlations. Moreover, the seems to benefit from the additional piece of information brought from the non-constant , on the contrary to the . Indeed, it is found that the is more accurate than the . Noting that only is valid for estimating , we can observe that does not converges to zero.

In this part, some comments on the confidence intervals for the studied autocorrelations are made. From Table 2, we can see that the results are the same for the "vpr" and "pr" corrections. This is not surprising as the corrected serial correlations are scale transformation of the correlations that include the zero returns. In addition, we note some finite sample distortions. This is a consequence of the Heteroscedastic Consistent (HC) covariance matrix estimation used to take into account for the non-linearities in the data. Such finite sample shortcomings for the HC estimator is well known in the literature (see e.g. Vilasuso (2001) or Raïssi (2011)). Simulations for the "pr" correction, not displayed here, show that the relative frequencies of the serial correlations outside their confidence bounds become close to the asymptotic nominal level 5% for large samples.

From our simulation results, we can conclude that if the stock features are incompletely taken into account, then the analysis of the serial correlation between non-zero returns can be misleading. The combined effects of a non-constant zero returns probability and an unconditional heteroscedasticity may produce important bias and a lack of accuracy. However, it is also important to identify each case properly to avoid a correction that is too sophisticated. For these reasons, we recommend consider the index of the studied stocks and any event in the company history that can cause a structural change in both the variance and the degree of liquidity.

5.2 Real data analysis

The correlation structures of the non-zero returns of the Chilean stocks presented in the Introduction are studied in detail. The main stocks indexes of the Santiago Stock Exchange (SSE), are the IPSA (the 30 most liquid stocks) and the IGPA (comprising the 30 stocks of the IPSA, plus 48 other stocks according to some criteria). Note that most of the stocks that are part of the IGPA, but not of the IPSA have zero returns. The studied stocks are representative examples of such illiquid assets. The sample sizes are given in Table 1.

We first determine the adequate correction for each stock. Recall that the stocks returns, together with the Nadaraya-Watson estimators of are displayed in Figures 1 and 2. In addition, as underlined in the Introduction, events in some companies history strongly suggest that at least is not constant. On the other hand, is provided in Table 1. It emerges that seems to be time-varying for most of the stocks, and in particular, the "vpr" correction is advisable for the Cintac and Molymet stocks. We conjecture that in many cases the long-run or abrupt changes in the liquidity degree is not accompanied by a change of the unconditional variance. In particular, it seems that the take-over bid of Metlife on Provida on one hand, and the merger by absorption and capital increase of the Security bank on the other hand, only led to a change in the degree of liquidity. However, it appears that the capital increase of 2010 in the Molymet case resulted in an increase of both the unconditional variance and the probability of a daily price change.

Now, we turn to the analysis of the first order linear dynamics for the studied stocks. The autocorrelations that seem relevant are in bold type in Table 1. The non-standard "vpr" statistics are close to the "pr" correction when is close to zero. Surprisingly, and are similar for the Cintac stock, although is elevated. For the non-stationary Molymet stock, the "vpr" correction deliver a higher first order correction than the "pr" correction. Below, some concluding remarks are provided in the light of the Monte Carlo experiments results and the outputs in Table 1.

6 Conclusion

At first glance, for estimating the linear relationship between present and lagged non-zero returns, it makes sense to consider a lack of a daily price movement as missing, without any further processing. In the stationary case, this can be done by applying a scale correction to the usual autocorrelations, using only the probabilities related to observing non-zero returns, as advocated in the classical literature. It turns out that such treatment of the data, is still valid when a structural change can be observed in either the daily non-zero returns probability, or the unconditional variance. However, when both unconditional heteroscedasticity and non-constant liquidity levels are present, the above correction for the serial autocorrelations is possibly distorted in two ways. Firstly, a bias can be observed. Secondly, a relatively high variability can be noticed. This spurious picture of the serial correlations, can be the consequence of neglected structural changes in the variance and in the liquidity degree. These shortcomings could result in an erroneous analysis of the stock’s properties. We propose to solve such issues through a simple scale correction, that takes into account the presence of such a non-stationary behavior in the stock’s history. This more realistic correction can lead to accurate assessment of the serial correlations of illiquid assets.

References

-

Bolerslev, T. (2008) Glossary to ARCH (GARCH). CREATES Research Paper 2008-49.

-

Bondon, P., and Bahamonde, N. (2012) Least squares estimation of ARCH models with missing observations. Journal of Time Series Analysis 33, 880-891.

-

Boudoukh, J., Richardson, M., and Whitelaw, R. (1994) A tale of three schools: insights on autocorrelations of short-horizon returns. Review of Financial Studies 7, 539-573.

-

Brockwell, P.J., and Davis, R.A. (2006) Times Series: Theory and Methods. 2nd edition, Springer, New York.

-

Cavaliere, G., and Taylor, A.M.R. (2007) Time-transformed unit-root tests for models with non-stationary volatility. Journal of Time Series Analysis 29, 300-330.

-

Cavaliere, G., and Taylor, A.M.R. (2008) Bootstrap Unit Root Tests for Time Series with Nonstationary Volatility. Econometric Theory 24, 43-71.

-

Dahlhaus, R. (1997) Fitting time series models to nonstationary processes. Annals of Statistics 25, 1-37.

-

Dalla, V., Giraitis, L., and Phillips, P.C.B. (2020) Robust tests for white noise and cross-correlation. Econometric Theory 1-29.

-

Davidson, J. (1994) Stochastic limit theory. Oxford University Press. New York.

-

Davydov, Y. A. (1968) Convergence of distributions generated by stationary stochastic process. Theory of Probability and its Applications 13, 691-696.

-

Dunsmuir, W., and Robinson, P. M. (1981) Estimation of time series models in the presence of missing data. Journal of the American Statistical Association 76, 560-568.

-

Engle, R.F. (1982) Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica 50, 987-1007.

-

Engle, R.F., and Rangel, J.G. (2008) The spline GARCH model for unconditional volatility and its global macroeconomic causes. Review of Financial Studies 21, 1187-1222.

-

Francq, C., and Zakoïan, J-M. (2019) GARCH models : structure, statistical inference, and financial applications. Wiley.

-

Hafner, C.M., and Linton, O. (2010) Efficient estimation of a multivariate multiplicative volatility model. Journal of Econometrics 159, 55-73.

-

Hansen, B.E. (1991) Strong laws for dependent heterogeneous processes. Econometric Theory 7, 213-221.

-

Harris, D., and Kew, H. (2014) Portmanteau autocorrelation tests under Q-dependence and heteroscedasticity. Journal of Time Series Analysis 35, 203-217.

-

Hurn, S., Martin, V.L., Phillips, P.C.B. and Yu, J. (2021) Financial Econometric Modeling Oxford University Press.

-

Köchling, G., Müller, J., and Posch, P.N. (2019) Does the introduction of futures improve the efficiency of Bitcoin? Finance Research Letters 30, 367-370.

-

Lesmond, D.A. (2005) Liquidity of emerging markets. Journal of Financial Economics 77, 411-452.

-

Lobato, I.N., Nankervis, J.C., and Savin, N.E. (2002) Testing for zero autocorrelation in the presence of statistical dependence. Econometric Theory 18, 730-743.

-

McNeil, A., Frey, R., and Embrechts, P. (2015) Quantitative Risk Management: Concepts, Techniques and Tools. Princeton University Press. New Jersey.

-

Mikosch, T., and Stărică, C. (2004) Nonstationarities in financial time series, the long-range dependence, and the IGARCH effects. Review of Economics and Statistics 86, 378-390.

-

Parzen, E. (1963) On spectral analysis with missing observations and amplitude modulation. Sankhya Series A 25, 383-392.

-

Patilea, V., and Raïssi, H. (2012) Adaptive estimation of vector autoregressive models with time-varying variance: application to testing linear causality in mean. Journal of Statistical Planning and Inference 142, 2891-2912.

-

Patilea, V., and Raïssi, H. (2013) Corrected portmanteau tests for VAR models with time-varying variance. Journal of Multivariate Analysis 116, 190-207.

-

Patilea, V., and Raïssi, H. (2014) Testing second order dynamics for autoregressive processes in presence of time-varying variance. Journal of the American Statistical Association 109, 1099-1111.

-

Patilea, V., and Raïssi, H. (2021) Powers correlation analysis of returns with a nonstationary zero-process. Arxiv Working document https:arxiv.orgpdf2104.04472.pdf.

-

Phillips, P.C.B. (1987) Time series regression with a unit root. Econometrica 55, 277-301.

-

Phillips, P.C.B., and Xu, K.L. (2006) Inference in autoregression under heteroskedasticity. Journal of Time Series Analysis 27, 289-308.

-

Raïssi, H. (2011) Testing linear causality in mean when the number of estimated parameters is high. Electronic Journal of Statistics 5, 507-533.

-

Romano, J. P., and Thombs, L. A. (1996) Inference for autocorrelations under weak assumptions. Journal of the American Statistical Association 91, 590-600.

-

Stărică, C., and Granger, C. (2005) Nonstationarities in stock returns. Review of Economics and Statistics 87, 503-522.

-

Stoffer, D.S., and Toloi, C.M.C. (1992) A note on the Ljung-Box-Pierce portmanteau statistic with missing data. Statistics and Probability Letters 13, 391-396.

-

Truquet, L. (2019) Local stationarity and time-inhomogeneous Markov chains. The Annals of Statistics 47, 2023-2050.

-

Vilasuso, J. (2001) Causality tests and conditional heteroscedasticity: Monte Carlo evidence. Journal of Econometrics 101, 25-35.

-

Wang, S., Zhao, Q., and Li, Y. (2019) Testing for no-cointegration under time-varying variance. Economics Letters 182, 45-49.

-

Xu, K.L., and Phillips, P.C.B. (2008) Adaptive estimation of autoregressive models with time-varying variances. Journal of Econometrics 142, 265-280.

Proofs

In the sequel, is a constant, possibly different from line to line.

Proof of Proposition 3.1.

Note that and are strictly stationary ergodic under the conditions of Proposition 3.1. Then, from the ergodic Theorem (see Francq and Zakoïan (2019) Theorem A.2), we have

| (13) |

for any . Hence, we clearly obtain

| (14) |

where we recall that . Using again the Ergodic Theorem, we write

| (15) |

for any . In view of (14), (15) and (4) the result follows. ∎

Proof of Proposition 3.2.

First note that , since is uncorrelated. In addition, we have for any . Then, noting that is a strictly stationary ergodic martingale increments sequence, we have

Proof of Proposition 3.3.

We begin with the numerator of . Denoting by the -mixing coefficients of , we have , setting , for . In view of the above argument, Assumption 6 implies that . In addition, by the Hölder inequality, we write . Then, using the Strong Law of Large Numbers (SLLN) of Hansen (1991), corollary 4, we obtain

for . From Assumption 4, we have

In view of Assumption 1 and 2, deduce that

| (16) |

where the remainder is non stochastic, such that . Then

Similarly, for the denominator we have

| (17) |

in view of Assumption 3. Deduce that

| (18) |

Now, the asymptotic behavior of the kernel estimators is established. Here, as a finite number of breaks is assumed, we consider a smooth function without a loss of generality. Also, we only consider , as the arguments are similar for . Let . From Lemma A(c) in Xu and Phillips (2008), we write

On the other hand, we have

in view of our mixing assumption. The last inequality is obtained from the inequality of Davydov (1968): there exists a constant such that

In view of the above, we obtain

Next, let us write

where the last equality is obtained for small enough , and since a compact support is assumed for . Hence, using the Lipschitz condition in Assumption 2, deduce that

In view of the above, we may write

| (19) |

Similarly, we also have

| (20) |

Considering the denominator of the serial correlations correcting term, we obtain

| (21) | |||||

From (19) and (20), and using the SLLN of Hansen (1991), the first term of the above equality converges to zero in probability. On the other hand, using again the SLLN of Hansen (1991), we have

Proof of Proposition 3.4.

Let . Using similar arguments as in the proof of Proposition 3.2, then the SLLN of Hansen (1991) can be used and we obtain

Now, let us write , where and . Then, introducing and , we write

as , and in view of Assumption 4. Then, from the CLT for martingale differences sequences in Francq and Zakoïan (2019), Theorem A.3, and using (17) and (22) the first statement follows. For the second statement, it is easy to see that the SLLN of Hansen (1991) can be applied using the same arguments as in the proof of Proposition 3.3. ∎

Proof of Proposition 4.1.

From (21) we have

| (23) |

where

Some computations give

The numerator of is equal to

Since it is supposed that , then we can write

Hence, using the usual convergence property of Riemann sums, and in view of the Lipschitz and the finite number of breaks conditions in Assumption 1 and 2, we obtain Gathering the above facts for , deduce that,

| (24) |

using the SLLN of Hansen (1991), and where

is a dimensional matrix, with

∎

Tables and Figures

| n | 1- | ||||

|---|---|---|---|---|---|

| Aguas | 1958 | 2.40 | -0.13 | 0.00 | |

| Clinica las Condes | 1958 | 50.82 | 0.02 | 0.01 | |

| Cintac | 5159 | 67.76 | 0.09 | 0.27 | |

| Cruzados | 2594 | 70.39 | -0.11 | 0.00 | |

| HF | 1941 | 58.84 | 0.37 | 0.02 | |

| Molymet | 4896 | 72.06 | 0.09 | 0.28 | |

| Paz | 3392 | 27.49 | 0.10 | 0.00 | |

| Vapores | 5162 | 19.96 | 0.13 | 0.00 | |

| Security | 5188 | 37.72 | -0.02 | 0.00 | |

| Provida | 5179 | 40.08 | -0.01 | 0.00 |

| 500 | 1500 | |||||

|---|---|---|---|---|---|---|

| prob. | var. | Case | pr | vpr | pr | vpr |

| homo. | homo. | (iv) | 2.9 | 2.9 | 2.8 | 2.8 |

| homo. | het. | (iii) | 2.6 | 2.6 | 2.9 | 2.9 |

| het. | homo. | (ii) | 3.0 | 3.0 | 3.9 | 3.9 |

| het. | het. | (i) | 3.3 | 3.3 | 3.7 | 3.7 |