Robust Validation: Confident Predictions

Even When Distributions Shift111

Research supported by the NSF under CAREER Award CCF-1553086

and HDR 1934578 (the Stanford Data Science Collaboratory),

Office of Naval Research YIP Award N00014-19-2288,

and the Stanford DAWN Consortium.

Abstract

While the traditional viewpoint in machine learning and statistics assumes training and testing samples come from the same population, practice belies this fiction. One strategy—coming from robust statistics and optimization—is thus to build a model robust to distributional perturbations. In this paper, we take a different approach to describe procedures for robust predictive inference, where a model provides uncertainty estimates on its predictions rather than point predictions. We present a method that produces prediction sets (almost exactly) giving the right coverage level for any test distribution in an -divergence ball around the training population. The method, based on conformal inference, achieves (nearly) valid coverage in finite samples, under only the condition that the training data be exchangeable. An essential component of our methodology is to estimate the amount of expected future data shift and build robustness to it; we develop estimators and prove their consistency for protection and validity of uncertainty estimates under shifts. By experimenting on several large-scale benchmark datasets, including Recht et al.’s CIFAR-v4 and ImageNet-V2 datasets, we provide complementary empirical results that highlight the importance of robust predictive validity.

1 Introduction

The central conceit of statistical machine learning is that data comes from a population, and that a model fit on a training set and validated on a held-out validation set will generalize to future data. Yet this conceit is at best debatable: indeed, Recht, Roelofs, Schmidt, and Shankar [35] create new test sets for the central image recognition CIFAR-10 and ImageNet benchmarks, and they observe that published accuracies drop by between 3–15% on CIFAR and more than 11% on ImageNet (increases in error rate of 50–100%), even though the authors follow the original dataset creation processes. Given this drop in accuracy—even in carefully reproduced experiments—shift in the data generating distribution is inevitable, and should be an essential focus, given the growing applications of machine learning.

To address such distribution shifts and related challenges, a growing literature advocates fitting predictive models that adapt to changes in the data generating distribution. For example, researchers suggest reweighting data to match new test distributions when covariates shift [46, 18], while work on distributional robustness [5, 17, 15, 14, 7, 6, 38] considers fitting models that optimize losses under worst-case distribution changes. Yet the resulting models often are conservative, appear to sacrifice accuracy for robustness, and even more, they may not be robust to natural distribution shifts [47]. The models also come with few tools for validating their performance on new data.

Instead of seeking robust models, we instead advocate focusing on models that provide validity in their predictions: a model should be able to provide some calibrated notion of its confidence, even in the face of distribution shift. Consequently, in this paper we revisit cross validation, validity, and conformal inference [51] from the perspective of robustness, advocating for more robust approaches to cross validation and equipping predictors with valid confidence sets. We present a method for robust predictive inference under distributional shifts, borrowing tools both from conformal inference [51] and distributional robustness. Our method can allow valid inferences even when training and test distributions are distinct, and we provide a (in our view well-motivated, but still heuristic) methodology to estimate plausible amounts of shift to which we should be robust.

To formalize, consider a supervised learning problem of predicting labels from data , where we assume we have a putative predictive model that outputs scores measuring error (so that means that the model assigns higher likelihood to than given ). For example, for a probabilistic model , a typical choice is the negative log likelihood . For a distribution on ,222We always write for a probability on and for the induced distribution on for . we observe . Future data may come from or a distribution near—in some appropriate sense, deriving from distribution shift—to , and we wish to output valid predictions for future instances , where is unknown. The goal of this paper is twofold: first, given a level and an uncertainty set of plausible shifted distributions, we wish to construct uniformly valid confidence set mappings of the form for a threshold , which provide coverage, satisfying

| (1) |

Second, we propose a methodology for finding a collection of plausible shifts, providing convergence theory and a concomitant empirical validiation on real distribution shift problems.

1.1 Background: split conformal inference under exchangeability

To set the stage, we review conformal predictive inference [51, 27, 28, 29, 2]. The setting here is a supervised learning problem where we have exchangeable data , and for a given confidence level we wish to provide a confidence set such that . Standard properties of quantiles make such a construction possible. Indeed, assume that are exchangeable random variables; then, the rank of any among —its position if we sort the values of the —is evidently uniform on , assuming ties are broken randomly. Thus, for probability distributions on , defining the familiar quantile

| (2) |

and to be the corresponding empirical quantile on , we have

Using this idea to provide confidence sets is now straightforward [51, 29]. Let be a validation set—we assume here and throughout that we have already fit a model on training data independent of the validation set —and assume we have a scoring function , where a large value of indicates that the point is non-conforming. In typical supervised learning tasks, such a function is easy to construct. Indeed, assume we have a predictor function (fit on an independent training set); in the case of regression, predicts , while for a multiclass classification problem , and is large when the model predicts class to be likely given . Then natural nonconformity scores are for regression and for classification. As long as are exchangeable, if we define , the confidence set

| (3) |

immediately satisfies

| (4) |

whatever the scoring function and distribution on [51, 29]. The coverage statement (4) depends critically (as we shall see) on the exchangeability of the samples, failing if even the marginal distribution over changes, and it does not imply conditional coverage: we have no guarantee that .

1.2 Related work

The machine learning community has long identified distribution shift as a challenge, with domain adaptation strategies and covariate shift two major foci [46, 34, 3, 53, 31], though much of this work focuses on model estimation and selection strategies, and one often assumes access to data (or at least likelihood ratios) of data from the new distribution. We argue that a model should instead provide robust and valid estimates of its confidence rather than simply predictions that may or may not be robust. There is a growing body of work on distributionally robust optimization (DRO), which considers worst-case dataset shifts in neighborhoods of the training distribution; these have been important in finance and operations research, where one wishes to guard against catastrophic losses [36, 4, 5]. In DRO in statistical learning [39, 6, 15, 17, 42], the focus has also been on improving estimators rather than inferential predictive tasks. We extend this distributional robustness to apply in predictive inference.

Vovk et al. [51]’s conformal inference provides an important tool for valid predictions. The growing applications of machine learning and predictive analytics have renewed interest in predictive validity, and recent papers attempt to move beyond the standard exchangeability assumptions upon which conformalization reposes [49, 10], though this typically requires some additional assumptions for strict validity. Of particular relevance to our setting is Tibshirani et al.’s work [49], which considers conformal inference under covariate shift, where the marginal over changes while remains fixed. Validity in this setting requires knowing a likelihood ratio of the shift, which in high dimensions is challenging. In addition, as Jordan [24] argues, in typical practice covariate shifts are no more plausible than other (more general) shifts, especially in situations with unobserved confounders. For this reason, we take a more general approach and do not restrict to specific structured shifts.

1.3 A few motivating examples

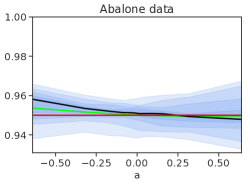

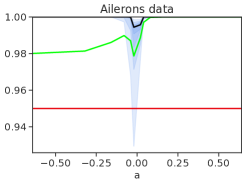

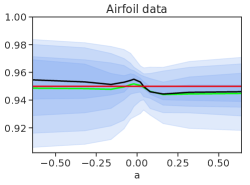

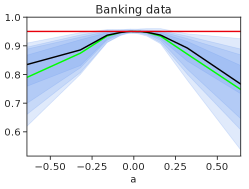

Standard validation methodology randomly splits data into train/validation/test sets, artificially enforcing exchangeabilty). Thus, to motivate the challenges in predictive validity even under simple covariate shifts—we only modify the distribution of , returning later to more sophisticated real-world scenarios—we experiment on nine regression datasets from the UCI repository [13]. We repeat the following 50 times. We randomly partition each dataset into disjoint sets , each consisting of of the data. We fit a random forest predictor using and construct conformal intervals of the form (3) with , so that for a threshold achieving coverage at nominal level on , as is standard in split-conformal prediction [51, 29]. We evaluate coverage on tiltings of varying strength on : letting be the top eigenvector of the test -covariance and be the mean of over , we reweight by probabilities proportional to for tilting parameters . Essentially, this shift asks the following question: why would we not expect a shift along the principal directions of variation in on future data?

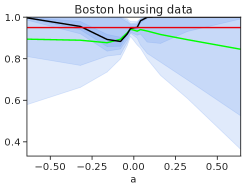

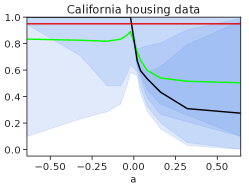

Figure 1 presents the results: even when the covariate shifts are small, which corresponds to tilting parameters with small magnitude, prediction intervals from the standard conformal methodology frequently fail to cover (sometimes grossly) the true response values. While this is but a simple motivation, if we expect some shift in future data—say along the directions of principal variation in , as the data itself is already variable along that axis—it seems that standard validation approaches [44, 20] provide too rosy of a picture of future validity [35], as they enforce exchangeability by randomly splitting data.

2 Robust predictive inference

Of course, standard cross validation and conformalization methodology makes no claims of validity without exchangeability [51, 2, 44], so their potential failure even under simple covariate shifts is not completely surprising. The coverage (4) relies on the exchangeability assumption between the training and test data and can quickly collapse when the test distribution violates that assumption, as Section 1.3 shows. These observations thus call for a notion of confidence more robust to potential future shifts.

Assume as usual that we have a score function , and observe data such that , so that is the push-forward of under . For a set of potential future score distributions on , our goal is to achieve coverage (1) for all distributions on pairs that induce a distribution on such that , that is,

Our focus is exclusively on validating our predictive model, not changing it, so we follow standard practice [51, 2] and use confidence sets to be of the form for a threshold . For such confidence sets, the choice is the smallest such that for every distribution of the scores. Our general problem to achieve coverage (1) with uncertainty set thus reduces to the optimization problem

| (5) |

In the next section, we characterize solutions to this problem, showing in Section 2.2 how to use the characterizations to achieve coverage on future data.

2.1 Characterizing and computing quantiles over -divergence balls

It remains to specify a set of distributions that makes problem (5) computationally tractable and statistically meaningful. We thus consider various restrictions on the likelihood ratio for . Following the distributionally robust optimization literature (DRO) [4, 39, 6, 15, 17, 42], we consider -divergence balls. Given a closed convex function satisfying and for , the -divergence [12] between probability distributions and on a set is

Jensen’s inequality guarantees that always, and familiar examples include , which induces the KL-divergence, and , which gives the -divergence. We study problem (5) in the case where is an -divergence ball of radius around :

| (6) |

Unlike most work in the DRO literature, instead of trying to build a model minimizing a DRO-type loss, we assume we already have a model and wish to robustly validate it: to provide predictive confidence sets that are valid and robust to distribution shifts no matter the model’s form. By the data processing inequality, all distributions on satisfying induce a distribution on satisfying , so solving problem (5) with provides coverage for all sufficiently small shifts on .

We show how to solve problem (5) for fixed and defining the constraint (6) by characterizing worst-case quantiles, essentially reducing the problem to a one-parameter (Bernoulli) problem. The choice of and determine plausible amounts of shift—appropriate choices are a longstanding problem [15]—and we defer approaches for selecting them to the sequel. For and any distribution on the real line, we define the -worst-case quantile

| (7) |

Key to our results both and on valid coverage in Section 2.2 is that this worst-case quantile is a standard quantile of at a level that depends only on , and , but not on .

Proposition 1.

Define the function by

Then the inverse

guarantees that for all distributions on and ,

See Appendix A.1 for a proof of the proposition.

Proposition 1 shows that it is easy to compute and , as they are both solutions to one-dimensional convex optimization problems and therefore admit efficient binary search procedures. In some cases, we have closed forms; for example gives , while yields . Another example:

Example 1 (Total variation distances): The total variation distance corresponds to the choice via the identity . For this case, we see immediately that , and then . Letting for shorthand, we sketch how to compute efficiently in more generality. Computing the inverse is equivalent to solving the optimization problem

We seek the largest feasible for this problem (as is feasible); because is convex and minimized at any with , for it is evident that . Thus may equivalently write

which a binary search over feasible solves to accuracy in time .

2.2 Achieving coverage with empirical estimates

With the characterization of , we can define the corresponding prediction set

| (8) |

As we observe only a sample , we use the empirical plug-in to develop confidence sets (8) (and therefore in problem (5)), considering . By doing this, Proposition 1 allows us to derive guarantees for the prediction set (8) from standard quantile statistics. In particular, the next proposition, whose proof we give in Appendix A.2, lower bounds future coverage conditionally on the validation set and relates future test coverage to the amount of shift.

Proposition 2.

Let be independent of , and let . Let be the c.d.f. of . Then the confidence set satisfies

With the two preceding propositions, we turn to the main coverage theorem and a few corollaries, which provide the validity of coverage as long as the true shift between and is no more than our guess. We provide the proof of the theorem in Appendix A.3.

Theorem 1.

Assume that is independent of , and let . Then

The theorem as stated is a bit unwieldy, so we develop a few corollaries, whose proofs we provide in Appendix A.4. In each, we assume that the we use to construct the confidence sets (8) satisfies , which guarantees validity.

Corollary 2.1.

Let the conditions of Theorem 1 hold, but additionally assume that . Then for , we have

If instead we replace in the definition (8) of the confidence set with

we can construct the corrected empirical confidence set

We then have the correct level coverage:

Corollary 2.2.

Let the conditions of Corollary 2.1 hold. Then

An easier corollary is immediate via Example 1, which shows that when the data distribution changes in variation distance by at most , we have (nearly) correct coverage by an identical increase in the choice of quantile level:

Corollary 2.3.

Let . Then

and if , then

Summarizing, the empirical prediction sets and achieve nearly or better than coverage if the -divergence between the new distribution and the current distribution remains below . When this fails, Theorem 1 shows graceful degradation in coverage as long as the divergence between and the validation population is not too large.

2.3 Towards more general uncertainty sets

We now provide an alternative characterization of that also adapts to other types of uncertainty sets. Our jumping off point is the quantile definition (7): for any continuous distribution , observe that

| (9) |

where equality follows from the fact that for all , if and only if , i.e. if and only if .

Efficient computation for Wasserstein balls. This simple duality result (9) gives us an avenue for computing the worst-case quantile w.r.t. different uncertainty sets. For example, if we replace the -divergence ball appearing in our derivations above with the -Wasserstein distance ball , then we need only replace the above inner maximization problem in (9) with

| (10) |

and we can then still perform the outer maximization via bisection. Problem (10) aims to transport as much mass as possible to for some infinitesimal , and hence is equivalent to the maximization program

Letting and solve the equation

we see that the solution is for and .

3 Procedures for estimating future distribution shift

While the results in the previous section apply for a fixed shift amount , a fundamental challenge is—given a validation data set—to determine the amount of shift against which to protect. We suggest a methodology to identify shifts motivated by two (somewhat oppositional) perspectives: first, the variability in predictions in current data is suggestive of the amount of variability we might expect in the future; second, from the perspective of protection against future shifts, that there is no reason future data would not shift as much as we can observe in a given validation set. As a motivating thought experiment, consider the case that the data is a mixture of distinct sub-populations. Should we provide valid coverage for each of these sub-populations, we expect our coverage to remain valid if the future (test) distribution remains any mixture of the same sub-populations. In empirical risk minimization (ERM)-based models, we expect rarer sub-populations to have higher non-conformity scores than average, and building on this intuition, our procedures look for regions in validation data with high non-conformity scores, choosing to give valid coverage in these regions.

We adopt a two-step procedure to describe the set of shifts we consider. Abstractly, let be a (potentially infinite) set indexing “directions” of possible shifts, and to each associate a collection of subsets of . (Typically, we either take when , or a subset of functions of , with each then a collection of level sets). For each , we consider the shifted distribution

| (11) |

which restricts to a smaller subset of the feature space without changing the conditional distribution of . The intuition behind the approach is twofold: first, conditionally valid predictors remain valid under covariate shifts of only (so that we hope to identify failures of validity under such shifts), and second, there may exist privileged directions of shift in the -space (e.g. time in temporal data or protected attributes in data with sensitive features) for which we wish to provide appropriate coverage.

Example 2 (Slabs and Euclidean balls): Our prototypical example is slabs (hyperplanes) and Euclidean balls, where we take , both of which have VC-dimension . In the slab case, for we define the collection of slabs orthogonal to ,

In the Euclidean ball case, we consider , the collection of -balls centered at .

Example 3 (Upper-level functional sets): A more general example takes be a collection of real-valued functions, for instance, a reproducing kernel Hilbert space (RKHS). For each , is then the collection of upper level-sets

Were all measurable functions, this would guarantee coverage under any covariate shift; practically, is a (much) smaller collection.

Given , we define the worst coverage for a confidence set mapping over -sets of size by

| (12) |

Our goal is to find a (tight) confidence set such that , which, in the setting of Section 2, corresponds to choosing such that

That is, we seek coverage over all large enough subsets of -space.

Barber et al. [2] show that one can theoretically construct such a confidence set when the collection of sets is not too large, e.g. if it has finite VC-dimension. Unfortunately, the computation of the worst coverage (12) is usually challenging when the dimension of the problem grows (as in Example 3), as it typically involves minimizing a non-convex function over a -dimensional domain. This makes the estimation of quantity (12) intractable for large and hints that requiring such coverage to hold uniformly over all directions may be too stringent for practical purposes. However, for a fixed , both sets in Example 3 admit -time algorithms for computing for any empirical distribution with support on points, which in the slab case is the maximum density segment problem [32]. Thus instead of the full worst coverage (12), we typically resort to a slightly weaker notion of robust coverage, where we require coverage to hold for “most” distributions of the form (11). In the next two sections, we therefore consider two approaches: one that samples directions , seeking good coverage with high probability, and the other that proposes surrogate convex optimization problems to find the worst direction , which we can show under (strong) distributional assumptions is optimal.

3.1 High-probability coverage over specific classes of shifts

Our first approach is to let be a distribution on that models plausible future shifts. A natural desiderata here is to provide coverage with high probability, that is, conditional on , to guarantee that for a hyperparameter and for ,

| (13) |

Thus with -probability over the direction of shift, the confidence set provides coverage over all satisfying . The coverage (13) becomes more conservative as decreases to , reducing to condition (12) when .

Before presenting the procedure, we index the confidence sets by the threshold for the score function , providing a complementary condition via the robust prediction set (8).

Definition 3.1.

For , the prediction set at level is

For a distribution on , the value provides sufficient divergence for threshold if

By the definition (8) of and Proposition 1, we see that gives sufficient divergence for threshold if and only if

To output a confidence set satisfying the high probability worst-coverage (13), we wish to find such that . Notably, any choice of satisfying yields a prediction set that both provides coverage for covariate shifts of the form (11) across most directions , in agreement with (13), and enjoys the protection against distribution shift we establish in Section 2 for the given value (including against more than covariate shifts). Algorithm 1 performs this using plug-in empirical estimators for , and .

| (14) |

We can show that procedure 1 approaches uniform coverage if the subsets in have finite VC-dimension.

Assumption A1 (Score continuity).

The distribution of the scores under is continuous.

Theorem 2.

See Appendix B for a proof of the theorem.

Theorem 2 shows that Procedure 1 approaches uniform coverage if the subsets in have finite VC-dimension. More precisely, the estimate almost achieves the randomized worst-case coverage (13): with probability nearly over the direction , provides coverage at level for all shifts (as in Eq. (11)) satisfying and . The second statement in the theorem is an insurance against drastic overcoverage: while we cannot guarantee that the worst coverage is always no more than , we can guarantee that—if the scores are continuous—then the empirical set has worst coverage no more than for at least a fraction of directions . In a sense, this is unimprovable: if the worst coverage is continuous in , the best we could expect is that while .

As a last remark, we note that when the scores are distinct, there is a complete equivalence between thresholds and divergence levels in Algorithm 1; see Appendix B.1 for a proof.

Lemma 3.1.

Assume that the scores are all distinct. Define and let . Then .

3.2 Finding directions of maximal shift

In this section, we revisit worst potential shifts, designing a methodology to estimate the worst direction and protect against it, additionally providing sufficient conditions for consistency. For a confidence set mapping , we define the worst shift direction

| (15) |

which evidently satisfies

If we could identify such a worst direction, and it is consistent across thresholds in our typical definition (a strong condition), then the procedures in the preceding sections allow us to choose thresholds to guarantee coverage. The intuition here is that there may exist a direction with higher variance in predictions, for example, time in a temporal system. A more explicit example comes from heteroskedastic regression:

Example 4 (Heteroskedastic regression): Let the data follow the model

where is non-decreasing, independent of , which generalizes the standard regression model to have heteroskedastic noise, with the noise increasing in the direction . Evidently the oracle (smallest length) conditional confidence set for is the interval where is the standard normal quantile. The standard split conformal methodology (Section 1.1) will undercover for those such that is large: shifts of in the direction may decrease coverage.

With this example as motivation, we propose identifying challenging directions for dataset shift by separating those datapoints with large nonconformity scores from those with lower scores. In principle, one can use any M-estimator find such a discriminator, and we suggest a potential approach in Section 3.2.1. To enable our coming analysis, we elaborate slightly and modify notation to reflect that the scoring function may change with sample size . We also refine Definition 3.1 of the confidence sets to explicitly depend on both the threshold and score function .

Definition 3.2.

For and a score , the -prediction set at level is

| (16) |

We assume in this section that is an RKHS, or a subset thereof, with associated Hilbert norm , and each collection is as in Example 3. The case where is the collection of all half-spaces corresponds to . Additionally, for every we let be the cumulative distribution function of when and its left-continuous version.

| (17) |

The intuition behind Algorithm 2 is simple: we seek a direction in which shifts in make the given nonconformity score large, then guarantee coverage for shifts in that direction and, via the distributionally robust confidence set the procedure returns, any future distributional shift for which the distribution of scores satisfies . Because we need only solve a single M-estimation problem—rather than sample a large number of directions as in Alg. 1—the estimation methodology is more computationally efficient.

3.2.1 Population-level consistency of the worst direction

The consistency of Algorithm 2 with the adequate worst-direction estimation procedure still requires strong assumptions, somewhat oppositional to the distribution-free coverage we seek (though again we still have the distributionally robust protections). Yet it is still of interest to understand conditions under which Alg. 2 is consistent; as we show here, in examples such as heteroskedastic regression (Ex. 3.2), this holds. We turn to our assumptions.

A challenge is that the worst direction may vary substantially in . One condition sufficient to ameliorate this reposes on stochastic orders, where for random variables and on , we say stochastically dominates in the upper orthant order , written , if for all (see [40, Ch. 6], where this is called the usual stochastic order). Letting denote the law of a random variable, we write if .

Assumption A2.

There is a direction such that has a continuous distribution and, for all ,

The intuition is that covariate shifts in direction not only increase nonconformity, but that is the worst such direction. Assumption A2 focuses on the dependence (copula) between and , when ranges over all potential directions of shift in , and states that and are more likely to take on larger values together. It only characterizes up to an increasing transformation, which is desirable as any such transformation leaves the collection of upper-level sets invariant.

Under Assumption A2, confidence sets share the same worst shift :

Lemma 3.2.

We present the (nearly immediate) proof of Lemma 3.2 in Appendix C.1.1. While Assumption A2 is admittedly strong, the next lemma (whose proof we provide in Appendix C.1.2) shows that it holds for linear shifts in the heteroskedastic regression case of Example 3.2.

Lemma 3.3.

We also suggest potential procedures for identifying the worst direction of shift under limited computational and statistical power. Ideally, a worst shift direction should allow ranking examples by difficulty, with larger values of corresponding to larger values of . The following lemma, whose proof we provide in Appendix C.1.3, formalizes this intuition, stating that the function maximizes the correspondence of the ranks of samples and . For ease of notation, we denote when appropriate.

Lemma 3.4.

Let Assumption A2 hold. Given three i.i.d. samples , and , the worst direction satisfies

| (18) |

While the natural empirical (finite-sample and non-convex) approximation of the problem (18) enjoys -consistency, and Sherman [41] characterizes its asymptotic distribution, such statistical consistency often comes at the cost of computational tractability, necessitating alternative approaches [11, 16]. Thus, we reframe our problem as a binary classification problem with label and feature vector , and consider the following least squares problem:

| (19) |

The following lemma, whose proof we provide in Appendix C.1.4, shows that the minimization problem (19) amounts to projecting the function

where and are independent, onto .

Lemma 3.5.

The minimization problem (19) is equivalent to

Additionally, if has a continuous distribution, and if , and are i.i.d. and , then

The function quantifies the “hardness” of an instance by comparing the score to an independent sample : if is the c.d.f. of , then . At the same time, it is the nonparametric analogue of the the maximizers in definition (18).

Moving to the finite-sample case, with a sample , we solve the following convex minimization problem, with a penalty :

| (20) |

Under appropriate conditions on the RKHS , this method is provably consistent, in the sense that converges towards as . This also entails that, if Assumption A2 holds for a vector space sufficiently large, then must be a non-decreasing function of . We summarize these results in the next proposition, which essentially states that we can asymptotically recover the worst direction up to a non-decreasing function, and whose proof we provide in Appendix C.1.5.

Proposition 3.

Assume that is a closed measurable space, and that is a dense, separable RKHS with a bounded measurable kernel. For any sequence such that , we have

Additionally, let Assumption A2 hold and have continuous distribution. Then there exists a non-decreasing function such that almost surely.

In our subsequent experiments, with a high-dimensional feature space, we use simpler least-squares and SVM estimators of the scores as a fitting procedure for the worst direction of shift, considering linear shifts only. This parametric approach is admittedly more restrictive, and obtaining consistency requires even stronger distributional assumptions, but we can still show that various M-estimators can identify the direction when Assumption A2 holds. We present one such plausible result here, assuming (i) Assumption A2 holds for consisting of linear shifts indexed by unit-norm vectors, (ii) that for some , is rotationally invariant and has finite second moments, and (iii) that is nonnegative and satisfies , and .

Proposition 4.

Let conditions (i)–(iii) above hold. Then is proportional to the least-squares solution

| (21) |

See Appendix C.1.6 for a proof.

3.2.2 Asymptotic estimation of the worst direction

With the population level recovery guarantees we establish in Propositions 3 and 4, it is now of interest to understand when we may recover the optimal worst direction and corresponding confidence set using Algorithm 2, which has access only to samples from the population . An immediate corollary of Theorem 2 ensures that, under the same conditions, Algorithm 2 returns a confidence set mapping that satisfies, conditionally on and and with probability over the second half of the validation data,

| (22) |

Recalling the definition (12), it remains to understand how close we can expect the uniform quantity to be to . By the bounds (22), if the worst coverage is continuous in and and are appropriately consistent, we should expect a uniform coverage guarantee in the limit as .

To present such a consistency result, we require a few additional assumptions.

Assumption A3 (Consistency of scores and directions).

As , we have

Assumption A4 (Continuous distributions).

For , the random variables and have continuous distributions. Additionally, has a continuous distribution with probability tending to as .

Assumption A5 (Distinct scores).

The scores are asymptotically distinct in probability,

Assumption A5 is a technical assumption that will typically hold whenever Assumption A4 holds, for example, if belongs to a parametric family.

Under these assumptions, Theorem 3 proves that we asymptotically provide uniform coverage at level over all shifts , . See Appendix C.2 for a proof.

Theorem 3.

To conclude, we see that the M-estimation-based Procedure 2 to find the worst shift direction can be consistent. Yet even without the (strong) assumptions Theorem 3 requires, we contend the methodology in Algorithm 2 (and Alg. 1) is valuable: it is important to look for variation in coverage within a dataset and to protect against possible future dataset shifts. In particular, Assumption A2 only ensures that the function is the worst shift independently of the threshold , i.e that for all , but in general, the function remains a reasonable estimation target in itself: one can view it as the “average” worst direction over a random choice of threshold .

4 Coverage sensitivity under covariate shifts

To this point in the paper, the approaches we take for robustness to distribution shifts may often be conservative. Here, we take a complementary and exploratory viewpoint to identify ways in which a predictor may be sensitive. While coverage guarantees of standard predictive inference methods may fail when new data comes from a shifted distribution (recall Section 1.3), protecting against all possible shifts can lead to conservative predictive sets. It is thus of practical interest to identify the particular directions in which a predictive model is indeed distributionally unstable. We therefore propose a measure that evaluates coverage sensitivity under distribution shifts of interest, and we study this measure’s convergence properties by building on a recent line of work distribution shift sensitivity [23, 45, 19].

For a choice of threshold , we wish to understand the sensitivity of (mis)-coverage of the predictive set (as in Eq. (16)) under covariate specific distribution shifts. In distinction from Section 2, where we consider general shifts on the score distribution, we now focus on covariate shift. For an index set , this consists of allowing only the distribution of to vary while the conditional distribution of given remains invariant. Thus, if we let be the distribution of when , we consider shifts of measures on belonging to

Assuming (as we will show is possible) that we can accurately evaluate coverage under such shifts, if a given scoring function is insensitive, then we gain confidence in the performance of , while scoring functions sensitive to such covariate shifts should give us pause.

4.1 Covariate-specific sensitivity analysis

Our goal here is to estimate scoring model’s sensitivity, which we take to be the mis-coverage of the predictive set function as the distribution of varies within . For shift amounts and probability distributions (indexed by ) on , we therefore define the covariate specific sensitivity function

Define the conditional miscoverage function on by

| (23) |

so we can express the sensitivity function as

| (24) |

as the covariate shift only affects the marginal distribution of by assumption.

The goal is to leverage equation (24) to build a consistent estimator of the sensitivity function. Given a sample , a natural approach is to follow a two step procedure, by first computing an estimate of the miscoverage function using the first points, and then approximating the sensitivity function with the remaining data points, forming the naive estimate

where is the empirical distribution of .

Unfortunately, if converges to at a slower rate than , we expect the same behavior from , so we take a different tack. In the next section, we show instead how, given an additional (large) sample of unlabeled data , we can achieve a -consistent asymptotically normal estimate of using a debiasing correction [9, 23, 45].333 Notably, Jeong and Namkoong [23] and Subbaswamy et al. [45] perform sensitivity analyses to distribution shift for various semiparametric functionals related to that here. We present alternative results and proofs as their results appear to have incorrect proofs. Subbaswamy et al. [45, Thm. 1] builds off of Jeong and Namkoong [23, Lemma 14], whose proof [23, Appendix C.3] appears to have a mistake: in the final line of the proof, they use that their functionals of interest have densities uniformly bounded away from 0, but nowhere do they assume this or argue that it must hold. A trade-off is that our debiasing typically leads to a loss of monotonicity of the estimate in the parameter . For clarity we focus on a particular limiting divergence, the Rényi -divergence

A quick calculation shows this corresponds to distribution balls of the form

which offers a simpler dual representation for the sensitivity function (24):

Lemma 4.1 (Example 3, Duchi and Namkoong [15]).

Let be defined via the Rényi divergence . Then the sensitivity function satisfies

4.2 Cross-fit dual estimation of the sensitivity function

We develop a debiased cross-fit estimator of using the representation in Lemma 4.1 and an additional unlabeled sample of covariates , which helps to estimate expectations of the form . To build intuition, consider an (abstract) functional of the form in Lemma 4.1, so that for a function and we wish to estimate

Consider a first-order expansion of around , where (recall Eq. (23)) and minimizes (as in Lemma 4.1) and is thus the quantile of . Then using that the subdifferential , we heuristically (ignoring interchanges of differentiation and integration) write

and rearranging,

where we used that by construction. For “near enough” to , we have . In short, we have sketched that

| (25) |

for appropriately near to the population quantities . Our idea, then, is to use the first-order term in Eq. (25) to correct an empirical calculation of .

Using the expansion (25) as motivation, for any pair of functions and , define the augmentation function by

Let be the quantile of under . For shorthand, omit the subscript on the miscoverage (23) to write , define , and choose . Then , so for all , Lemma 4.1 shows that

| (26) |

Algorithm 3 proceeds by first estimating , and successively, before leveraging equation (26) to form a “debiased” cross-fit estimator of . As mentioned above, it assumes access to a set of unlabeled examples where , which we use to estimate from . Intuitively, this allows us to accurately estimate properties of -measurable variables, and it is reasonable in semi-supervised regimes where unsupervised examples are cheaper than labeled data.

We first split the data into batches of size . For each batch , we form an estimate of using all samples from . Using the pool of unlabeled samples, we then compute an estimate of the quantile (see step (27)), which then gives the th augmented estimator (28). Average over all batches gives the final estimator . (The augmentation term makes potentially non-monotonic in .)

| (27) |

| (28) |

| (29) |

4.2.1 Consistency and convergence rate of the augmented estimator

We study the consistency and rate of covergence of the sensitivity estimator (29) as a path function of , for which we require a few assumptions below. Assumption A6 states that the fitted estimator needs to be appropriately consistent for , while Assumption A7 basically ensures the pool of unlabeled samples is large enough to provide a good estimate of the quantiles of . Assumption A8 is technical and prevents the random variable from being too concentrated, thus allowing quantile estimation.

Assumption A6 (Miscoverage estimation).

For each batch , we have

Assumption A7 (Quantile estimation).

For each and every compact , the quantile estimator satisfies

Assumption A8.

The random variable has a bounded density on .

Under these assumptions, we have the following theorem, which shows that for every compact set , the sequence of processes converges in distribution in to a tight Gaussian process, whose covariance is tedious to specify though we characterize it in the proof of the theorem in Appendix D.

Theorem 4.

A few consequences of Theorem 4 are immediate. First, we have -consistency:

as the supremum mapping is continuous in , and so . As another immediate consequence, we see that under the assumptions of Theorem 4, for every , there exists such that

(This is similar to the result [45, Thm. 1], but as we note in footnote 3, the papers [45, 23] may have technical mistakes.)

5 Empirical analysis

Given the challenges arising in the practice of machine learning and statistics, this paper argues that methodology equipping models with a notion of validity in their predictions—e.g., conformalization procedures as in this paper—is essential to any modern prediction pipeline. Section 1.3 illustrates the need for these sorts of procedures, showing that the standard conformal methodology is sensitive to even small shifts in the data, through (semi-synthetic) experiments on data from the UCI repository. In Section 2, we propose methods for robust predictive inference, giving methodology that estimates the amount of shift to which we should be robust. Fuller justification requires a more careful empirical study that highlights both the failures of non-robust prediction sets on real data as well as the potential to handle such shifts using the methodology here. To that end, we turn to experimental work:

- •

-

•

Section 5.2 shows evaluation centered around the new MNIST, CIFAR-10, and ImageNet test sets. These datasets exhibit real-world distributional shifts, and we test whether our methodology of estimating plausible shifts is sufficient to provide coverage in these real-world shifts.

-

•

In Section 5.3, we consider a time series where the goal is to predict the fraction of people testing positive for COVID-19 throughout the United States.

- •

5.1 UCI datasets

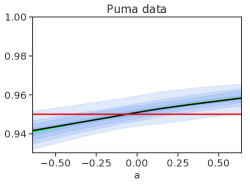

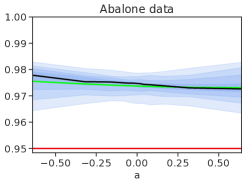

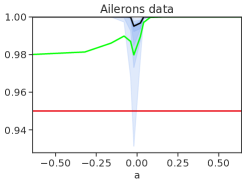

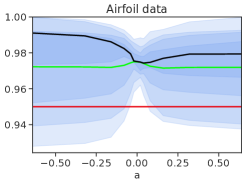

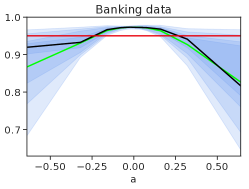

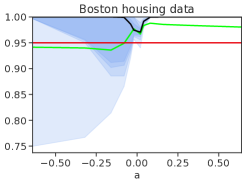

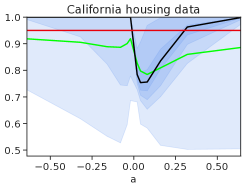

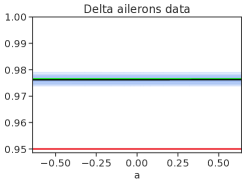

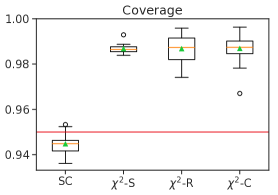

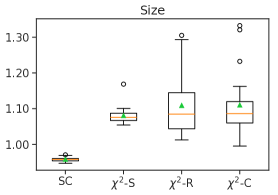

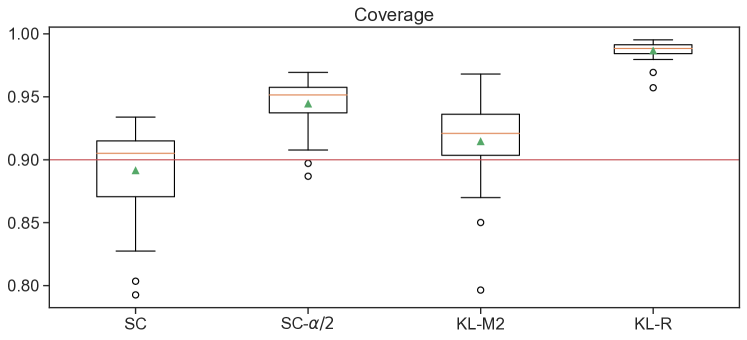

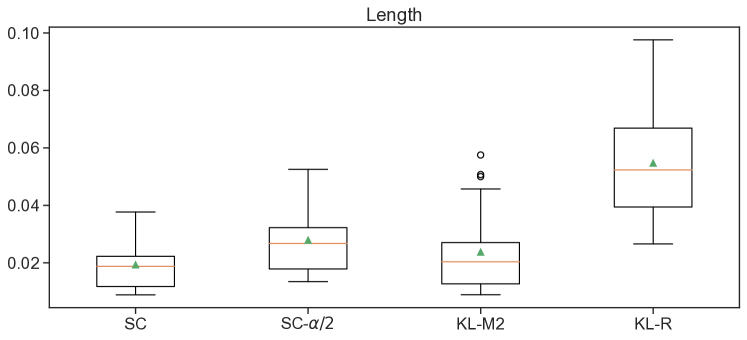

We revisit the experiments in Section 1.3, focusing on evaluating our methodology for robust predictive inference. Our goal here is to show that when our estimate of the amount of shift is comparable to the actual amount of shift, our methodology delivers coverage without inflating prediction sets too much. Accordingly, throughout these experiments, we fix the desired robustness level , corresponding (approximately) to the median chi-squared divergence between the natural and tilted empirical distributions across the nine data sets and values of the tilting parameter . We therefore expect Algorithm 1, which emphasizes robustness to worst-case shifts, to restore the coverage level for the tiltings from Section 1.3 that possess (roughly) this level of shift.

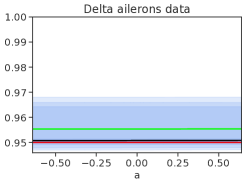

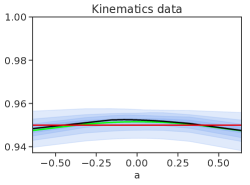

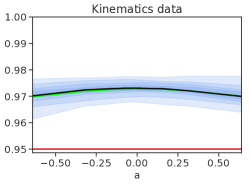

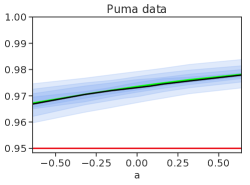

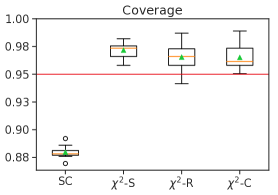

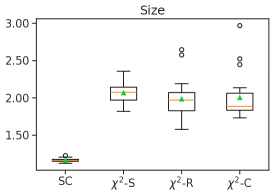

Figure 2 presents the results for the chi-squared divergence (the results for the Kullback-Leibler divergence are similar). Although not perfect, we see that the methodology often restores validity for the shifts from Section 1.3. We see clearly improved performance over the standard conformal methodology on the abalone, delta ailerons, kinematics, puma, and airfoil datasets (compare to Figure 1). On all of these datasets, the robust methodology consistently yields average coverage above the nominal level, while standard conformal fails to cover on each of the datasets. Treating the test sample as truth, we evaluate the median chi-squared divergence between these natural and shifted distributions across values of the tilting parameter ; the divergence values are .03, .02, .04, .05, and 3.65, respectively, while the level of divergence for the remaining datasets (ailerons—which still covers—banking, and Boston and California housing) is roughly twice as large, which explains the loss in coverage. We note in passing that in other experiments we omit for brevity, the trends above hold for other types of shifts.

5.2 CIFAR-10, MNIST, and ImageNet datasets

We evaluate our procedures on the CIFAR-10, ImageNet, and MNIST datasets [25, 37, 26], which continue to play a central role in the evaluation of machine learning methodology. Concerns about overfitting to these benchmarks motivate Recht, Roelofs, Schmidt, and Shankar [35] to create new test sets for both CIFAR-10 and ImageNet by carefully following the original dataset creation protocol. Though these new test sets strongly resemble the original datasets, as Recht et al. observe, the natural variation arising in the creation of the new test sets yield evidently significant differences, giving organic dataset shifts on which to evaluate our procedures. Our goal here is to show that even when we do not know the actual amount of shift, our methodology from Section 3.1 can still give reasonable estimates of it that translate into marginal coverage on these datasets.

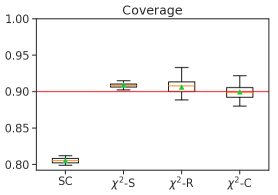

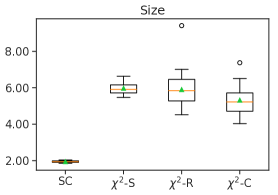

We evaluate on the three datasets as follows. We use 70% of the original CIFAR-10, MNIST, and ImageNet datasets for training, and treat the remaining 30% as a validation set. We fit a standard ResNet-50 [21] to the training data, and use the negative log-likelihood , where is the output of the (top) sigmoid layer of the network, as the scoring function on the validation data for our conformalization procedures. We compare our procedures to the split conformal methodology on three new datasets nominally generated identically to the initial datasets: the CIFAR-10.1 v4 dataset [35], which consists of 2,000 3232 images from 10 different classes; the QMNIST50K data, which extends MNIST to consist of 50,000 2828 images from 10 classes [54]; and the ImageNetV2 Threshold0.7 data [35], consisting of 10,000 images from 200 classes. In each test of robust predictive inference, we set the level of robustness to achieve the nominal coverage for the CIFAR-10 and MNIST datasets and for the ImageNet dataset, by using the data-driven strategies that we detail in Section 3: sampling directions of shift from the uniform distribution on the unit sphere (Alg. 1), estimating the shift direction via regression (Alg. 2) or via classification, which replaces the regression step in Alg. 2 with a support vector machine (SVM) to separate the largest 50% of scores from the smallest. In contrast to our experiments from Section 5.1 with semi-synthetic data, we cannot compute the exact level of shift here; the question is whether the provided methodology provides marginal coverage.

Figures 3, 4, and 5 present the results for each setup over 20 random splits of the data. As is apparent from the figures, we see that the standard conformal methodology fails to correctly cover. As both the new CIFAR-10 and ImageNet test sets exhibit larger degradations in classifier performance (increased error) than does the MNIST test set [35], we expect the failure of standard conformal to be pronounced on these two datasets. Indeed, the split conformal method (Sec. 1.1) provides especially poor coverage on these datasets, where it yields average coverage .88 (instead of the nominal .95) and .8 (instead of the nominal .9) on the new CIFAR-10 and ImageNet test sets, respectively. On the other hand, our inferential methodology consistently gives more coverage regardless of the strategy used to estimate the amount of divergence , with the sampling strategy notably consistently delivering marginal coverage without over-covering. The uniformity in coverage across the three strategies is notable, as our procedures for estimating the amount of shift assume some structure for the underlying shift, which is unlikely to be consistent with the provenance of the new test sets.

In our experiments, estimating the direction of shift using either regression or classification (Alg. 2) is faster than sampling directions (Alg. 1); the former takes time and the latter , where is the number of sampled directions , using a linear-time implementation for computing the worst coverage (maximum density segment) along a direction [32]. The difference of course depends on the desired sampling frequency .

Finally, the aforementioned validity does not (apparently) come with a significant loss in statistical efficiency: Figures 3, 4, and 5 show that our confidence sets are not substantially larger than those coming from standard conformal inference—which may be somewhat surprising, given the relatively large number of classes present in the ImageNet dataset.

5.3 COVID-19 forecasting

Our final evaluation of prediction accuracy under shifts is to predict test positivity rates for COVID-19, in each of United States counties in a time series over weeks from January through the beginning of August 2021, using demographic features. As a non-stationary time series, robustness is essential here as a fixed model of course cannot adapt to the underlying distributional changes.

Our prediction task is as follows. For each of weeks, and at each of locations (counties), we observe a real-valued response , , , measuring the fraction of people with COVID-19. We use data from the DELPHI group at Carnegie Mellon University [1, 48] and consider a similar featurization, using the following trailing average features within each county: (1) the number of COVID-19 cases per 100,000 people; (2) the number of doctor visits for COVID-like symptoms; and (3) the number of responses to a Facebook survey indicating respondents have COVID-like symptoms. We standardize both the features and responses so that they lie in ], and collect the features into vectors , , .

At each week , we fit a simple logistic model where for a fixed , we compute

| (30) |

We treat the data at the weeks as the validation set, the data at the remaining weeks as the test set, so that at each time we fit the single most recent time period’s data. We make predictions on a new example at time via the logistic link

For our robust conformalization procedures, we consider the Kullback-Leibler divergence and estimate the divergence between weeks and via regression (Alg. 2), as well as with a nonparametric divergence estimator [33]; given this we then make robust predictions at the test times . We compare to the standard split conformal methodology—which is of course not robust to departures from the validation distribution—but also consider the standard conformal methodology with the more conservative miscoverage level to attain robustness to a variation distance shift of (recall Corollary 2.3). We set throughout these experiments.

Figures 6–9 present the results. From Figure 6, we can see that the standard conformal methodology (once again) fails to cover, whereas our (two) robust conformalization procedures retain validity. These results are in line with our expectations: we expect the standard methodology to undercover as it is not robust to distributional changes, and we expect both Alg. 2 as well as the nonparametric divergence estimator of Nguyen et al. [33] to deliver reasonably accurate estimates of the divergence level given the low ambient dimension of the feature space (recall that ), translating into generally good coverage here. We can also see that the standard conformal methodology with the conservative miscoverage level gives coverage at roughly the right level, though it is does not adapt the miscoverage level to the problem at hand (as estimating an appropriate level of divergence is an important component). Along these lines, Figure 7 reveals a more complete picture: the heuristic also gives rise to (slightly) longer confidence intervals than most of the other methods—which is intuitive as again we have no guarantee that corresponds to the true amount of divergence between the validation and test distributions. Overall, our robust conformalization procedure combined with Nguyen et al.’s nonparametric divergence estimator [33] appears to strike the best balance between coverage and confidence interval length in this instance.

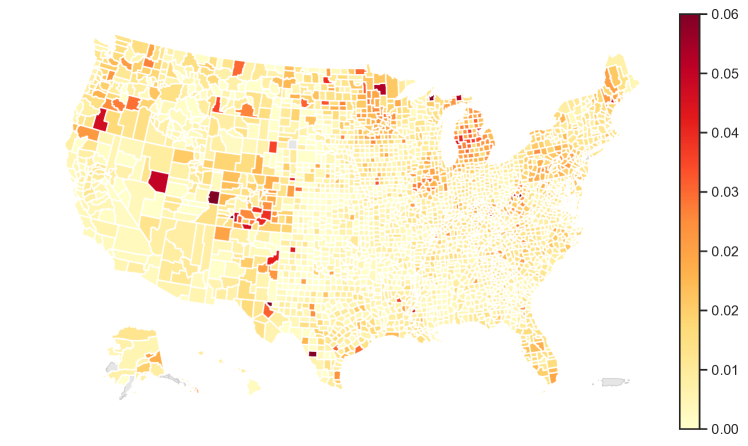

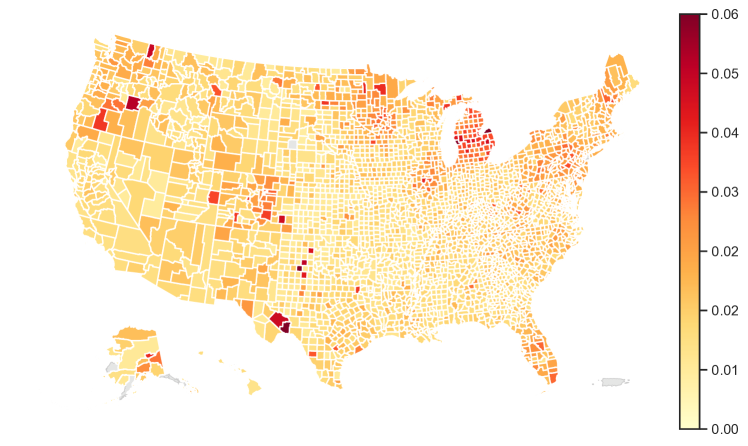

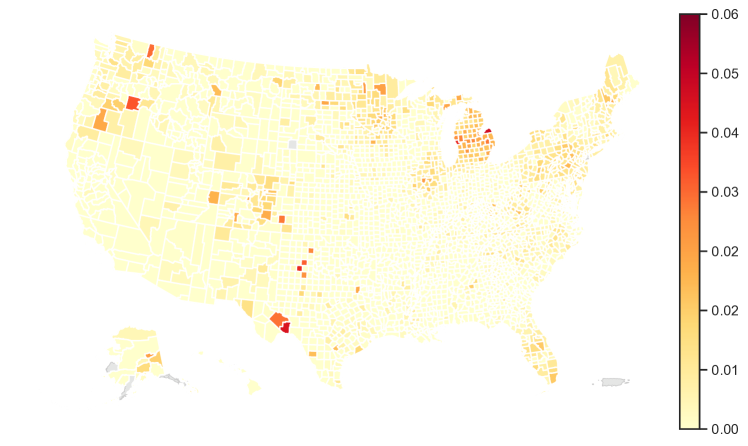

We view these results from a more qualitative perspective in Figures 8 and 9. In Figure 8, we show the actual number of COVID-19 cases on April 16, 2021, when the state of Michigan saw a sudden spike in the incidence of COVID-19 after several weeks of implementing precautionary measures. As an especially pronounced example of distributional shift, it is natural to ask whether our procedures might offer any kind of protection in this instance. Figure 9 shows the upper and lower endpoints of the confidence intervals that our robust conformalization procedure generates at this point in time. By comparing the colors in the figures, we can see that our robust prediction intervals generally contain the true response value both across the United States as well as in Michigan, in particular—despite the presence of such a severe distributional shift.

5.4 Experiments on covariate sensitivity

Our final experiment is to evaluate our sensitivity predictions for covariate shift, as in Sec. 4. The point is twofold: we (i) identify covariates for which covarage may be sensitive, then (ii) test whether these putative sensitivities are indeed present in data. To do so, we consider three datasets from the UCI repository [13]: real-estate data, weather history data, and wine quality data.

We repeat the following experiment 25 times: we randomly partition each dataset into disjoint sets each containing respectively of the data, then fit a linear regression model using and construct conformal intervals of the form (3) with , so that , setting the threshold so that we achieve coverage at nominal level on . We estimate the sensitivity function using as in Algorithm 3 for each singleton covariate (i.e. the covariate set for each of ), where we estimate the conditional probabilities of miscoverage using default tuning parameeters in R’s version of random forests.

Figure 10 shows the results. The plot is somewhat complex: for each of the three datasets, we estimate sensitivity (as a function of shift ) for each covariate in the dataset (e.g. House age in the real estate data). Then for an individual covariate, we plot (estimated) maximum miscoverage as a function of the radius of potential shift in that covariate (the estimated sensitivity function (24), where is the covariate of interest); this is the red solid line in each plot. As we are curious about coverage losses under covariate shifts, we plot miscoverage (dashed lines) on the subset of the test data containing examples either from the upper or lower quantiles of each covariate, which corresponds to Rényi -divergence , as in Lemma 4.1. We expect that these miscoverages to fall below the maximum miscoverage line, which we observe across all three datasets. Specifically, we see that for real estate data, coverage of the corresponding confidence sets drops most when the marginal distribution of the covariate “House age” shifts while that for weather history data, the coverage drops most for shifts in the “Pressure” covariate. For the wine quality dataset, coverage seems almost equally sensitive to all covariates. An interesting question for future work is to identify those directions which are sensitive—as opposed to the approach here, which identifies potentially sensitive covariates.

6 Discussion and conclusions

We have presented methods and motivation for robust predicitve inference, seeking protection against distribution shift. Our arguments and perspective are somewhat different from the typical approach in distributional robustness [5, 17, 15, 7, 38], as we wish to maintain validity in prediction. A number of future directions and questions remain unanswered. Perhaps the most glaring is to fully understand the “right” level of robustness. While this is a longstanding problem [15], we present approaches to leverage the available validation data. Alternatives might be compare new covariates and test data to the available validation data. Tibshirani et al. [49] suggest an importance-sampling approach for this, reweighting data based on likelihood ratios, which may sometimes be feasible but is likely impossible in high-dimensional scenarios. It would be interesting, for example, to use projections of the data to match -statistics on new test data, using this to generate appropriate distributional robustness sets. We hope that the perspective here inspires renewed consideration of predictive validity.

References

- Arnold et al. [2021] T. Arnold, J. Bien, L. Brooks, S. Colquhoun, D. Farrow, J. Grabman, P. Maynard-Zhang, A. Reinhart, and R. Tibshirani. covidcast: Client for Delphi’s COVIDcast Epidata API, 2021. URL https://cmu-delphi.github.io/covidcast/covidcastR/. R package version 0.4.2.

- Barber et al. [2021] R. F. Barber, E. J. Candès, A. Ramdas, and R. J. Tibshirani. The limits of distribution-free conditional predictive inference. Information and Inference, 10(2):455–482, 2021.

- Ben-David et al. [2010] S. Ben-David, J. Blitzer, K. Crammer, A. Kulesza, F. Pereira, and J. Vaughan. A theory of learning from different domains. Machine Learning, 79:151–175, 2010.

- Ben-Tal et al. [2013] A. Ben-Tal, D. den Hertog, A. D. Waegenaere, B. Melenberg, and G. Rennen. Robust solutions of optimization problems affected by uncertain probabilities. Management Science, 59(2):341–357, 2013.

- Bertsimas et al. [2018] D. Bertsimas, V. Gupta, and N. Kallus. Data-driven robust optimization. Mathematical Programming, Series A, 167(2):235–292, 2018.

- Blanchet and Murthy [2019] J. Blanchet and K. Murthy. Quantifying distributional model risk via optimal transport. Mathematics of Operations Research, 44(2):565–600, 2019.

- Blanchet et al. [2019] J. Blanchet, Y. Kang, and K. Murthy. Robust Wasserstein profile inference and applications to machine learning. Journal of Applied Probability, 56(3):830–857, 2019.

- Cauchois et al. [2021] M. Cauchois, S. Gupta, and J. Duchi. Knowing what you know: valid and validated confidence sets in multiclass and multilabel prediction. Journal of Machine Learning Research, 22(81):1–42, 2021.

- Chernozhukov et al. [2018a] V. Chernozhukov, D. Chetverikov, M. Demirer, E. Duflo, C. Hansen, W. Newey, and J. Robins. Double/debiased machine learning for treatment and structural parameters. The Econometrics Journal, 21(1):C1–C68, 2018a.

- Chernozhukov et al. [2018b] V. Chernozhukov, K. Wuthrich, and Y. Zhu. Exact and robust conformal inference methods for predictive machine learning with dependent data. arXiv:1802.06300 [stat.ML], 2018b.

- Clémençon et al. [2008] S. Clémençon, G. Lugosi, and N. Vayatis. Ranking and empirical minimization of -statistics. Annals of Statistics, 36(2):844–874, 2008.

- Csiszár [1967] I. Csiszár. Information-type measures of difference of probability distributions and indirect observation. Studia Scientifica Mathematica Hungary, 2:299–318, 1967.

- Dua and Graff [2017] D. Dua and C. Graff. UCI machine learning repository, 2017. URL http://archive.ics.uci.edu/ml.

- Duchi and Namkoong [2019] J. C. Duchi and H. Namkoong. Variance-based regularization with convex objectives. Journal of Machine Learning Research, 20(68):1–55, 2019.

- Duchi and Namkoong [2021] J. C. Duchi and H. Namkoong. Learning models with uniform performance via distributionally robust optimization. Annals of Statistics, 49(3):1378–1406, 2021. URL https://arXiv.org/abs/1810.08750.

- Duchi et al. [2013] J. C. Duchi, L. Mackey, and M. I. Jordan. The asymptotics of ranking algorithms. Annals of Statistics, 41(5):2292–2323, 2013.

- Esfahani and Kuhn [2018] P. M. Esfahani and D. Kuhn. Data-driven distributionally robust optimization using the Wasserstein metric: Performance guarantees and tractable reformulations. Mathematical Programming, Series A, 171(1–2):115–166, 2018.

- Gretton et al. [2009] A. Gretton, A. Smola, J. Huang, M. Schmittfull, K. Borgwardt, and B. Schölkopf. Covariate shift by kernel mean matching. In J. Q. nonero Candela, M. Sugiyama, A. Schwaighofer, and N. D. Lawrence, editors, Dataset Shift in Machine Learning, chapter 8, pages 131–160. MIT Press, 2009.

- Gupta and Rothenhäusler [2021] S. Gupta and D. Rothenhäusler. The s-value: evaluating stability with respect to distributional shifts. arXiv:2105.03067 [stat.ME], 2021.

- Hastie et al. [2009] T. Hastie, R. Tibshirani, and J. Friedman. The Elements of Statistical Learning. Springer, second edition, 2009.

- He et al. [2016] K. He, X. Zhang, S. Ren, and J. Sun. Deep residual learning for image recognition. In Proceedings of the IEEE Conference on Computer Vision and Pattern Recognition, pages 770–778, 2016.

- Hiriart-Urruty and Lemaréchal [1993] J. Hiriart-Urruty and C. Lemaréchal. Convex Analysis and Minimization Algorithms I. Springer, New York, 1993.

- Jeong and Namkoong [2020] S. Jeong and H. Namkoong. Robust causal inference under covariate shift via worst-case subpopulation treatment effects. arXiv:2007.02411 [stat.ML], 2020. URL https://arxiv.org/abs/2007.02411.

- Jordan [2019] M. I. Jordan. Artificial intelligence—the revolution hasn’t happened yet. Harvard Data Science Review, 1(1), 2019.

- Krizhevsky and Hinton [2009] A. Krizhevsky and G. Hinton. Learning multiple layers of features from tiny images. Technical report, University of Toronto, 2009.

- LeCun et al. [1998] Y. LeCun, C. Cortes, and C. Burges. MNIST handwritten digit database, 1998. URL http://yann.lecun.com/exdb/mnist. ATT Labs [Online].

- Lei [2014] J. Lei. Classification with confidence. Biometrika, 101(4):755–769, 2014.

- Lei and Wasserman [2014] J. Lei and L. Wasserman. Distribution-free prediction bands for non-parametric regression. Journal of the Royal Statistical Society, Series B, 76(1):71–96, 2014.

- Lei et al. [2018] J. Lei, M. G’Sell, A. Rinaldo, R. J. Tibshirani, and L. Wasserman. Distribution-free predictive inference for regression. Journal of the American Statistical Association, 113(523):1094–1111, 2018.

- Liese and Vajda [2006] F. Liese and I. Vajda. On divergences and informations in statistics and information theory. IEEE Transactions on Information Theory, 52(10):4394–4412, 2006.

- Lipton et al. [2018] Z. C. Lipton, Y.-X. Wang, and A. Smola. Detecting and correcting for label shift with black box predictors. In Proceedings of the 35th International Conference on Machine Learning, 2018.

- min Chung and Lu [2003] K. min Chung and H.-I. Lu. An optimal algorithm for the maximum-density segment problem. In Proceedings of the 11th Annual European Symposium on Algorithms, 2003.

- Nguyen et al. [2010] X. Nguyen, M. J. Wainwright, and M. I. Jordan. Estimating divergence functionals and the likelihood ratio by convex risk minimization. IEEE Transactions on Information Theory, 56(11):5847–5861, 2010.

- Quionero-Candela et al. [2009] J. Quionero-Candela, M. Sugiyama, A. Schwaighofer, and N. D. Lawrence. Dataset Shift in Machine Learning. The MIT Press, 2009.

- Recht et al. [2019] B. Recht, R. Roelofs, L. Schmidt, and V. Shankar. Do ImageNet classifiers generalize to ImageNet? In Proceedings of the 36th International Conference on Machine Learning, 2019.

- Rockafellar and Uryasev [2000] R. T. Rockafellar and S. Uryasev. Optimization of conditional value-at-risk. Journal of Risk, 2:21–42, 2000.

- Russakovsky et al. [2015] O. Russakovsky, J. Deng, H. Su, J. Krause, S. Satheesh, S. Ma, Z. Huang, A. Karpathy, A. Khosla, M. Bernstein, A. C. Berg, and L. Fei-Fei. ImageNet large scale visual recognition challenge. International Journal of Computer Vision, 115(3):211–252, 2015.

- Sagawa et al. [2020] S. Sagawa, P. W. Koh, T. B. Hashimoto, and P. Liang. Distributionally robust neural networks for group shifts: On the importance of regularization for worst-case generalization. In Proceedings of the Eighth International Conference on Learning Representations, 2020.

- Shafieezadeh-Abadeh et al. [2015] S. Shafieezadeh-Abadeh, P. M. Esfahani, and D. Kuhn. Distributionally robust logistic regression. In Advances in Neural Information Processing Systems 28, pages 1576–1584, 2015.

- Shaked and Shanthikumar [2007] M. Shaked and J. G. Shanthikumar. Stochastic Orders. Springer Series in Statistics. Springer, 2007.

- Sherman [1994] R. P. Sherman. Maximal Inequalities for Degenerate -Processes with Applications to Optimization Estimators. Annals of Statistics, 22(1):439–459, 1994.

- Sinha et al. [2018] A. Sinha, H. Namkoong, and J. Duchi. Certifying some distributional robustness with principled adversarial training. In Proceedings of the Sixth International Conference on Learning Representations, 2018.

- Steinwart and Christmann [2008] I. Steinwart and A. Christmann. Support Vector Machines. Springer Publishing Company, Incorporated, 1st edition, 2008.

- Stone [1974] M. Stone. Cross-validatory choice and assessment of statistical predictions. Journal of the Royal Statistical Society, Series B, 36(2):111–147, 1974.

- Subbaswamy et al. [2021] A. Subbaswamy, R. Adams, and S. Saria. Evaluating model robustness to dataset shift. In Proceedings of the 24th International Conference on Artificial Intelligence and Statistics, 2021.

- Sugiyama et al. [2007] M. Sugiyama, M. Krauledat, and K.-R. Müller. Covariate shift adaptation by importance weighted cross validation. Journal of Machine Learning Research, 8:985–1005, 2007.

- Taori et al. [2020] R. Taori, A. Dave, V. Shankar, N. Carlini, B. Recht, and L. Schmidt. When robustness doesn’t promote robustness: Synthetic vs. natural distribution shifts on ImageNet. under review, 2020. URL https://openreview.net/forum?id=HyxPIyrFvH.

- Tibshirani [2020] R. J. Tibshirani. Can symptoms surveys improve COVID-19 forecasts?, 2020. URL https://delphi.cmu.edu/blog/2020/09/21/can-symptoms-surveys-improve-covid-19-forecasts/.

- Tibshirani et al. [2019] R. J. Tibshirani, R. F. Barber, E. J. Candès, and A. Ramdas. Conformal prediction under covariate shift. In Advances in Neural Information Processing Systems 32, 2019.

- van der Vaart [1998] A. W. van der Vaart. Asymptotic Statistics. Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, 1998.

- Vovk et al. [2005] V. Vovk, A. Grammerman, and G. Shafer. Algorithmic Learning in a Random World. Springer, 2005.

- Wainwright [2019] M. J. Wainwright. High-Dimensional Statistics: A Non-Asymptotic Viewpoint. Cambridge University Press, 2019.

- Wen et al. [2014] J. Wen, C.-N. Yu, and R. Greiner. Robust learning under uncertain test distributions: Relating covariate shift to model misspecification. In Proceedings of the 31st International Conference on Machine Learning, pages 631–639, 2014.

- Yadav and Bottou [2019] C. Yadav and L. Bottou. Cold case: The lost MNIST digits. In Advances in Neural Information Processing Systems 32, 2019.

Appendix A Proofs of results on robust inference

A.1 Proof of Proposition 1

We provide several properties of , deferring their proof to Sec. A.1.1.

Lemma A.1 (Properties of ).

Let be a closed convex function such that and for all . Then the function satisfies the following.

-

(a)

is a convex function.

-

(b)

is non-increasing in and non-decreasing in . Moreover, for all , there exists , and is strictly increasing for .

-

(c)

is continuous for and .

-

(d)

For and , . For , equality holds for , strict inequality holds for and , and if and only if .

-

(e)

Let as in the statement of Proposition 1. Then for , if and only if .

We now define the worst-case cumulative distribution function, which generalizes the c.d.f. of a distribution in the same way the worst-case quantile generalizes standard quantiles.

Definition A.1 (-worst-case c.d.f.).

Let and consider any distribution on the real line. The -worst-case cumulative distribution function is

| (31) |

Proposition 1 will then follow from the coming lemma.

Lemma A.2.

Let be a distribution on with c.d.f. . Then

| (32) |

Deferring the proof of this lemma as well (see Sec. A.1.2), let us see how it implies Proposition 1. Observe that for all , and any real distribution with c.d.f. , we have

where equality uses Lemma A.2 and follows because by Lemma A.1, as if and only if .

A.1.1 Proof of Lemma A.1

It is no loss of generality to assume that and , as replacing by generates the same -divergence and evidently .

-

(a)

Let be the perspective transform of , which is convex, with the understanding that

-

•

for ,

-

•

,

-

•

for all , where .

Then is the partial minimization of the convex function and hence convex, where is the convex indicator function, if its argument is false and otherwise. (See [22, Ch. IV] for proofs of each of these claims and that the limits indeed exist.)

-

•

-

(b)

That is non-increasing is evident. As is nonnegative, convex, and , it must therefore be non-decreasing. That is strictly increasing in is again immediate by convexity as .

-

(c)

Any convex function is continuous on the interior of its domain, thus is continuous on . To see that is continuous from the left at , first observe that is non-decreasing by (b) (which only uses convexity and the fact that ), so we only need to prove that

where the last equality follows from the fact that is decreasing on . However, for any such that , the continuity of in and the fact that ensure the existence of such that . Since is non-increasing on , this implies that , hence that , which concludes the proof.

That is right continuous at is immediate because is non-decreasing and convex.

-

(d)

The non-strict inequality is immediate by considering and using that . The strict inequality is immediate because is continuous near , the equality for is trivial since , and equals if and only if .

-

(e)

Let for shorthand. Suppose that . Then as is strictly increasing when it is positive, we have for all , so that for any , or .

A.1.2 Proof of Lemma A.2

Recall that is a real distribution with c.d.f. . We treat the cases , and separately.

-

•

If , the result is immediate, since we have .

-

•

Suppose now that . The inequality is immediate:

The reverse inequality is a consequence of the data processing inequality [30]. Fix . Let be a distribution satisfying . We show how to construct with and . Indeed, define the Markov kernel by

Then , while satisfies

by the data processing inequality. Now we observe that

By construction, , and it is immediate that

Matching the expression of to the definition of gives . Taking the infimum over all possible distributions concludes the proof.

-

•

Finally, if , we have since for any , the distribution satisfies and . The proof of the other inequality is similar to the case where , except a valid Markov kernel is now

to account for the fact that .

A.2 Proof of Proposition 2

A.3 Proof of Theorem 1

We require the following lemma to prove the theorem.

Lemma A.3 (Quantile coverage [51, 29, 2]).

Assume that with c.d.f. , and let be their empirical distribution. Then for all ,

We include the brief proof of Lemma A.3 below for completeness, giving the proof of Theorem 1 here. By Proposition 2, for , we have

Marginalizing over , this implies that

where inequality is a consequence of Jensen’s inequality applied to (recall Lemma A.1(a)), while inequality uses Lemma A.3 and that is non-decreasing.

Proof of Lemma A.3 Let independent of . Then

where we break ties uniformly at random to define the rank of in , ensuring by exchangeability that it is uniform on . ∎

A.4 Proof of Corollaries 2.1 and 2.2

When , Lemma A.1 guarantees that , so Theorem 1 gives

| (33) |

To prove Corollary 2.1, note that as in convex, it has (at least) a left derivative , which satisfies

This gives the first corollary.

For the second corollary, replacing in Eq. (33) with gives

Appendix B Proof of Theorem 2

Throughout the proof, we will typically not assume that the scores are distinct, and thus will not make Assumption A1. Some inequalities will require the assumption, which implies the distinctness of the scores, and we will highlight those.

Recall that and , that for all

and that we use as shorthand for the law of for . We also use and for the empirical distributions f and , respectively. Observe that for all and , if and only if

By a VC-covering argument (cf. [8, Sec. A.4] or [2, Thm. 5]), there exists a universal constant such that the following holds. For , define . Then with probability at least over , the following equations hold simultaneously for all :

| (34) |

and

| (35) |

We assume for the remainder of the proof that inequalities (34) and (35) hold.

Define the empirical quantile

We first give a lemma on its coverage.

Lemma B.1.

Proof Applying the bounds (34), we can bound the worst-case quantiles via

| (37) |

The inclusions

are an immediate consequence of inequality (35), and, in turn, imply that for all ,

Combining these inclusions with the inequalities (37), we thus obtain

| (38) | ||||

The infimum and supremum quantiles satisfy

where the inequality always holds and the equality requires Assumption A1.

We now observe that for any fixed , the function is non-decreasing, since the confidence sets increase as increases. Recalling inequalities (B), we conclude that

and

simultaneously for all , with the second inequality requiring Assumption A1.

∎

Recall that in Algorithm 1 is the -empirical quantile of . Then inequalities (36) in Lemmma B.1 and that is non-decreasing in imply

while under Assumption A1, we have the converse lower bound

using the second inequality of Lemma B.1.

For , define the functions for all . The set of functions is uniformly bounded (by ) and each is non-decreasing in so that its VC-dimension cannot exceed 1. Thus, there exists a universal constant such that, with probability [e.g. 52, Thm. 4.10, Ex. 5.24],

Similarly, if we define , then with probability at least , we have . Combining the statements, we see that with probability over the draw and , we have

and under Assumption A1,

B.1 Proof of Lemma 3.1

Let for shorthand, and assume w.l.o.g. that . We will show that if , then if

| (39) |

Evidently this implies that for all , giving the lemma, so for the remainder, we show the equivalence (39).

Recall the definition in the discussion following Proposition 1. Suppose that , where , which immediately implies that, for all , . By Proposition 1, we therefore see that if satisfies , then

In addition, as the scores are all distinct, if , making in this case equal to

The mapping is concave and nonnegative. As is -coercive by assumption, we also have that it is defined on , and it is continuous strictly increasing on . Its inverse (as a function of ) is therefore continuous, which implies in particular that , and hence equality (39) holds.

Appendix C Proofs related to finding worst shift directions

C.1 Proofs on worst direction recovery

C.1.1 Proof of Lemma 3.2

Fix , , and consider such that , i.e . We then have

where and comes from Assumption A2, and from the continuity of the distribution of , which guarantees that .

Since , this implies that

The result follows by taking the infimum over all such that .

C.1.2 Proof of Lemma 3.3

Let , and assume for simplicity that (the squared error case is similar). We then have for all ,

Inequality is simply a restatement of the elementary fact , while equality is due to the fact that, since every linear combination has a continuous distribution for all , has an uniform distribution on .

C.1.3 Proof of Lemma 3.4

Assumption A2 ensures the following upper orthant stochastic order:

Letting , we first observe by conditioning on that

We then have the following lemma on upper orthant ordering.

Lemma C.1.

Let . Then if and only if for all non-negative and non-decreasing functions ,

| (40) |