The Athena Class of Risk-Limiting Ballot Polling Audits††thanks: This material is based upon work supported in part by NSF Awards 2015253 and 1421373

Abstract

The main risk-limiting ballot polling audit in use today, Bravo, is designed for use when single ballots are drawn at random and a decision regarding whether to stop the audit or draw another ballot is taken after each ballot draw (ballot-by-ballot (B2) audits). On the other hand, real ballot polling audits draw many ballots in a single round before determining whether to stop (round-by-round (R2) audits). We show that Bravo results in significant inefficiency when directly applied to real R2 audits. We present the Athena class of R2 stopping rules, which we show are risk-limiting if the round schedule is pre-determined (before the audit begins). We prove that each rule is at least as efficient as the corresponding Bravo stopping rule applied at the end of the round. We have open-source software libraries implementing most of our results.

We show that Athena halves the number of ballots required, for all state margins in the 2016 US Presidential election and a first round with stopping probability, when compared to Bravo (stopping rule applied at the end of the round). We present simulation results supporting the stopping probability claims and our claims for the risk accrued in the first round. Further, Athena reduces the number of ballots by more than a quarter for low margins, when compared to the Bravo stopping rule applied on ballots in selection order. This implies that keeping track of the order when drawing ballots R2 is not beneficial, because Athena is more efficient even without information on selection order. These results are significant because current approaches to real ballot polling election audits use the B2 Bravo rules, requiring about twice as much work on the part of election officials. Applying the rules in selection order requires fewer ballots, but keeping track of the order, and entering it into audit software, adds to the effort.

All our contributions are for audits with zero error of the second kind. Our approach relies on analytical expressions we derive for stopping probabilities. The results of these analytical expressions are verified by comparison with the percentiles Lindeman et al. previously obtained using B2 Bravo simulations [5].

We believe our results may be applied in a straightforward fashion to other SPRTs with if the stopping condition is monotonic increasing with the number of winner ballots (Bayesian audits are an example) but proofs in this paper apply only to Bravo.

1 Introduction

The most popular examples of election tabulation ballot polling audits include Bravo [5] and Bayesian audits [10]; these audits may be viewed as special cases/extensions of the sequential probability ratio test (SPRT), see [14, 7]. When the decisions of whether to stop the audit or draw more ballots are taken after each ballot draw, and the stopping condition is satisfied exactly when the audit is stopped, these audits—as SPRTs—are most efficient audits. The term most efficient refers here, as elsewhere, to an audit requiring the smallest expected number of ballots given either hypothesis: a correct election outcome or an incorrect one, if the election is drawn from the assumed prior. The expectation is taken over the randomness of the ballot draws, and, in the case of Bayesian audits, also the randomness of the true tally (Bayesian audits treat the true tally as an unknown random variable).

In real election audits, multiple ballots are drawn in a round before a decision is taken. This paper shows that Bravo is not a most efficient test in this case, and proposes the Athena class of more efficient tests, demonstrating significant decreases in first-round sizes, and proving that the tests are risk-limited if the round schedule is pre-determined (before the audit begins). This could be of consequence for election audits of the 2020 US Presidential election.

1.1 Problem

We refer to audits where decisions are taken after each ballot draw as ballot-by-ballot or B2 audits. The general audit, however, is a round-by-round or R2 audit where, in the round, some ballots are drawn, after which a decision is taken regarding whether to (a) stop the audit and declare the election outcome correct, (b) stop the audit and go to a manual recount, or (c) draw the round. A B2 audit is a special case of the R2 audit, when a single ballot is drawn in each round.

There are two ways to apply B2 audit rules to an R2 audit. Consider a total of ballots drawn after the round, of which are for the reported winner.

-

•

End-of-round: In this application, the B2 stopping rule for winner ballots in a sample of ballots determines whether the audit will stop.

-

•

Selection-ordered-ballots: In this application, ballot order is recorded and the B2 stopping condition is tested . The audit stops if the B2 condition is satisfied for any value of .

Selection-ordered-ballots is generally more efficient than end-of-round as a means of applying B2 rules to R2 audits, but requires the significant additional effort of preserving enough information to be able to recreate the subtotals of winner ballots in selection order. End-of-round relies only on the tallies and does not require selection order. As our paper shows, neither is a most efficient R2 stopping rule.

One may view the problem we address as lying somewhere between (a) the problem solved by Neyman-Pearson [12]: derive a single-use binary hypothesis testing rule satisfying certain error criteria, and (b) the problem solved by Wald [15]: derive a stopping condition for sequential sampling, satisfying certain error criteria, where the condition is tested draw-by-draw. We address the problem of sequential sampling in rounds, where the condition is tested after multiple draws.

1.2 Our Contributions

Our contributions are as follows:

-

1.

We derive analytical expressions for the risk and probability of stopping, given the history of rounds and the margin for the Bravo audit. Treating the B2 Bravo audit as an R2 audit with , we verify that the expressions we derive predict the stopping percentiles originally obtained by Lindeman et al. using Bravo simulations [5, Table 1]. The average of the absolute value of the fractional difference between our results and those of [5] is 0.13%. The largest difference has value ballots, corresponding to a fractional difference of 0.41 %, in the estimate of the expected number of ballots drawn for a margin of 1%. This difference could be due to small inaccuracies in our computational approach (such as rounding off errors or the finiteness of summations involved in the computations) or the finiteness of the number of simulations used to generate the results of [5]. Our approach is easily extended to audits with stopping conditions that are monotone increasing in the number of ballots for the announced winner, such as Bayesian audits. The code for computing these expressions is available as a MATLAB library, released as open-source under the MIT License [13].

-

2.

We present the Athena class of R2 stopping rules for audits Minerva and Athena and prove that, if the round schedule is pre-determined (before the audit begins), Minerva and Athena are both risk-limiting and at least as efficient as the corresponding end-of-round Bravo stopping rule. Another audit from the Athena class, Metis, is out of scope for this draft.

-

3.

We provide experimental results and software to support the use of the proposed audits:

-

•

To illustrate the efficiency improvements, we compute (without simulations, using the derived analytical expressions), for each state in the 2016 US Presidential election, risk limit and a stopping probability of 0.9, first round sizes for end-of-round Bravo and Athena. We find that Athena requires about half the number of ballots, across all margins.

-

•

We compute first round sizes for selection-ordered-ballots Bravo and find that Athena requires about fewer ballots for the data of the 2016 US Presidential election, with the improvement being better for smaller margins. Thus Athena is more efficient than selection-ordered-ballots Bravo and does not require the additional book-keeping of recording selection ballot order.

-

•

We present the results of simulations supporting our predictions of first round stopping probabilities and the risk-limiting properties of Athena.

- •

This contribution is important because a number of states have undertaken ballot polling pilots in the last year and plan to use ballot polling audits in November 2020. We hope that our results and code can help developers of auditing software. We also note that, in many scenarios, ballot comparison or batch comparison audits could be more feasible. One may also consider combinations of ballot comparison and ballot polling audits, such as described in [8].

-

•

-

4.

The Athena class of R2 stopping rules is a class of B2 rules when round size is one. Of theoretical interest, we prove that B2 Minerva (round size one) has the same stopping rule as B2 Bravo, as does B2 Athena for some values of its parameters.

We do not claim that the audits of the Athena class are the most efficient R2 audits with zero error of the second kind (). The problem of finding the most efficient R2 audits is open.

Unlike the SPRT and other Martingale-based approaches, the stopping rules for audits of the Athena class use information about the history of round sizes. For this reason the stopping condition for rounds other than the first one does not depend only on the cumulative sample size and number of winner ballots drawn, but also on the history of individual round sizes.

We do not address some simple extensions of our work in this paper. For example, we do not consider audits with a limit on the total number of ballots drawn in the polling audit (if the audit fails to stop, a full sequential hand count would follow). Were we to do so, we could provide audits with larger stopping probabilities given the same risk limit.

This paper focuses exclusively on Bravo. However, we expect that our results extend to other risk-limiting SPRTs with and a stopping condition that is monotonic in the number of winner ballots drawn; examples include Bayesian audits.

1.3 Organization

Section 2 presents the model and related work. Section 3 motivates the problem with an example demonstrating that the application of B2 rules to an R2 audit results in inefficiencies. Section 4 introduces the Athena class of audits with examples and provides insight into why the audits are risk-limiting and more efficient than either R2 application of B2 Bravo. Section 5 describes the analytical approaches for computing probabilities for multiple-round audits. Section 6 presents the Minerva and Athena audits, and Section 7 presents rigorous claims of their risk-limiting and efficiency properties in the form of Theorems and Lemmas. Section 8 presents experimental results. Section 9 concludes. Proofs are in the Appendix.

1.4 Acknowledgements

We gratefully acknowledge comments on an early draft by: Matthew Bernhard, Amanda Glazer, Mark Lindeman, Jake Spertus, Mayuri Sridhar, Philip B. Stark, Damjan Vukcevic.

This version is updated from the previous one to reflect only a couple, and not all, of their valuable suggestions. Importantly, this draft notes that the risk-limiting property is proven only when round sizes are pre-determined. We have also made some of the changes, including some improvements to our notation, and the inclusion of the number of distinct ballots in tables listing the number of ballots required for a first round with 90% stopping probability for 2016 tallies. We plan to soon further update the manuscript to include estimated first round sizes for the 2021 tallies and address all other suggestions made by the reviewers.

This research was sponsored in part by NSF Awards 2015253 and 1421373.

2 The Model

We consider a plurality contest and assume ballots are drawn with replacement. We assume all ballots have a vote for either the winner or the loser; because ballots are sampled with replacement, our argument is easily extended to contests with multiple candidates and invalid ballots (as for Bravo, for example, see [4]). We denote by the true winner, the announced winner, the announced loser and the announced fractional tally for (typically based on preliminary, uncertified results).

A polling audit will estimate whether is the true winner. We denote by the total number of ballots drawn at the end of the round, and by the corresponding total number of ballots for the winner. Hence the number of new ballots drawn in round is , and the number of new votes for the winner drawn in round is . If necessary, one may assume that . We often refer to as the round schedule. A B2 audit is an R2 audit with round size . That is, the round schedule of a B2 audit is .

The total number of ballots drawn at any time during the audit is denoted (if the number of rounds drawn so far is , ). The random variable representing the number of ballots drawn so far for the winner is represented by (and to represent the number of ballots drawn for the winner up to the round). We use , and to represent specific numbers of winner ballots as well.

The entire sample drawn up to the round, in sequence, forms the signal or the observation; the corresponding random variable is denoted , the specific value . The entire sample drawn so far is denoted , its specific value . We do not a priori assume a last round for the audit. The audit stops when it satisfies the stopping condition.

2.1 The Model

We model the audit as a binary hypothesis test:

-

Null hypothesis : The election outcome is the closest possible incorrect outcome: and the fractional vote count for is . In particular, if the total number of valid votes is even, the election is a tie. If the total number of valid votes is odd, the margin is one in favor of . In this case, we assume that the number of valid votes is large enough that the fractional vote count is sufficiently close to . Henceforth, we will refer to both cases as being represented by a fractional vote count of .

-

Alternate hypothesis : The election outcome is correct: and the fractional vote count is as announced.

After each round the test takes as input and outputs one of the following:

-

•

Correct: The test estimates that and the audit should stop.

-

•

Incorrect: The test estimates that . We stop drawing votes and proceed to perform a complete hand count to determine .

-

•

Undetermined (draw more samples): We need to draw more ballots to improve the estimate.

When the audit stops, it can make one of two kinds of errors:

-

1.

Miss: A miss occurs when but the audit misses this, and outputs Correct. We denote by the probability of a miss:

is the risk in risk limiting audits and the Type I error of the test.

-

2.

Unnecessary Hand Count: Similarly, if , but the audit estimates that a hand count must follow, the hand count is unnecessary. We denote the probability of an unnecessary hand count by :

is the Type II error.

Like the Bravo audit, this paper focuses on tests with . The risk, on the other hand, is an important (generally) non-zero value characterizing the quality of the audit.

2.2 Related Work

A risk-limiting audit (RLA) with risk limit —as described by, for example, Lindeman and Stark [4]—is one for which the risk is smaller than for all possible (unknown) true tallies in the election. For convenience when we compare audits, we refer to this audit as an -RLA.

Definition 1 (Risk Limiting Audit (-RLA)).

An audit is a Risk Limiting Audit with risk limit iff for sample

There are many audits that would satisfy the -RLA criterion, and not all would be desirable. For example, the constant audit which always outputs Incorrect always requires a hand count and is risk-limiting with , , . However, , and the audit examines all votes each time; this is undesirable.

An example of an -RLA with and drawing fewer ballots is the B2 Bravo audit [5] which specifies round size increments of one.

Definition 2 (Bravo).

An audit is the B2 -Bravo audit iff the following stopping condition is tested at each ballot draw. If the sample is of size and has ballots for the winner,

| (1) |

Its p-value is .

is the likelihood ratio of the drawn sequence . The B2 -Bravo audit is an SPRT [15] with:

-

, the null hypothesis: the election is a tie

-

, the alternate hypothesis: the fractional tally for the winner is .

Implicit in Definition 2 is the point that a sequence is tested only if it has not previously satisfied the test. If for some sequence , all extensions of are defined as having passed the test. Determining the stopping condition by evaluating does not satisfy the assumptions of the test, and the properties of the test do not necessarily apply. As we shall see in Section 3, this is relevant to end-of-round Bravo. In fact, it is relevant to end-of-round applications of any B2 audit that is an SPRT.

B2 Bravo is a most efficient test given the hypotheses (if the stopping condition is satisfied exactly every time). Vora shows [14] that B2 -Bravo is an -RLA because it assumes a tie for , which is the wrong election outcome that is hardest to distinguish from the announced one, and hence defines the worst-case risk [14].

Other approaches, such as Rivest’s CLIP Audit [9], improve on B2 Bravo’s efficiency subject to certain constraints (namely, of as defined in [9]).

A prototype of Athena mirrored the explicit risk allocation found in Stark’s Conservative Statistical Post-Election Audits [11] before ballots are examined for the audit, a list of increasing rounds , and a list of corresponding risks are generated. Dispensing with auditor flexibility in favor of a predetermined list of rounds and corresponding risks facilitated the investigation of the convolution procedure that underlies a fundamental improvement of Athena over Bravo.

3 The Problem

In this section we use an example to illustrate the problems of using B2 rules for an R2 audit.

The B2 -Bravo audit, Definition 2, is the following ratio test (inequality (1)) performed after each draw:

Because and the denominator above does not depend on , is monotone increasing with . There is hence a minimum value of for which the B2 -Bravo stopping condition is satisfied. That is, such that the stopping condition of Definition 2, inequality (1), is:

In fact it is easy to see that is a discretized straight line as a function of , with slope and intercept determined by and (see, for example, [15]).

| (2) |

where

We drop one or more arguments of , or when they are obvious.

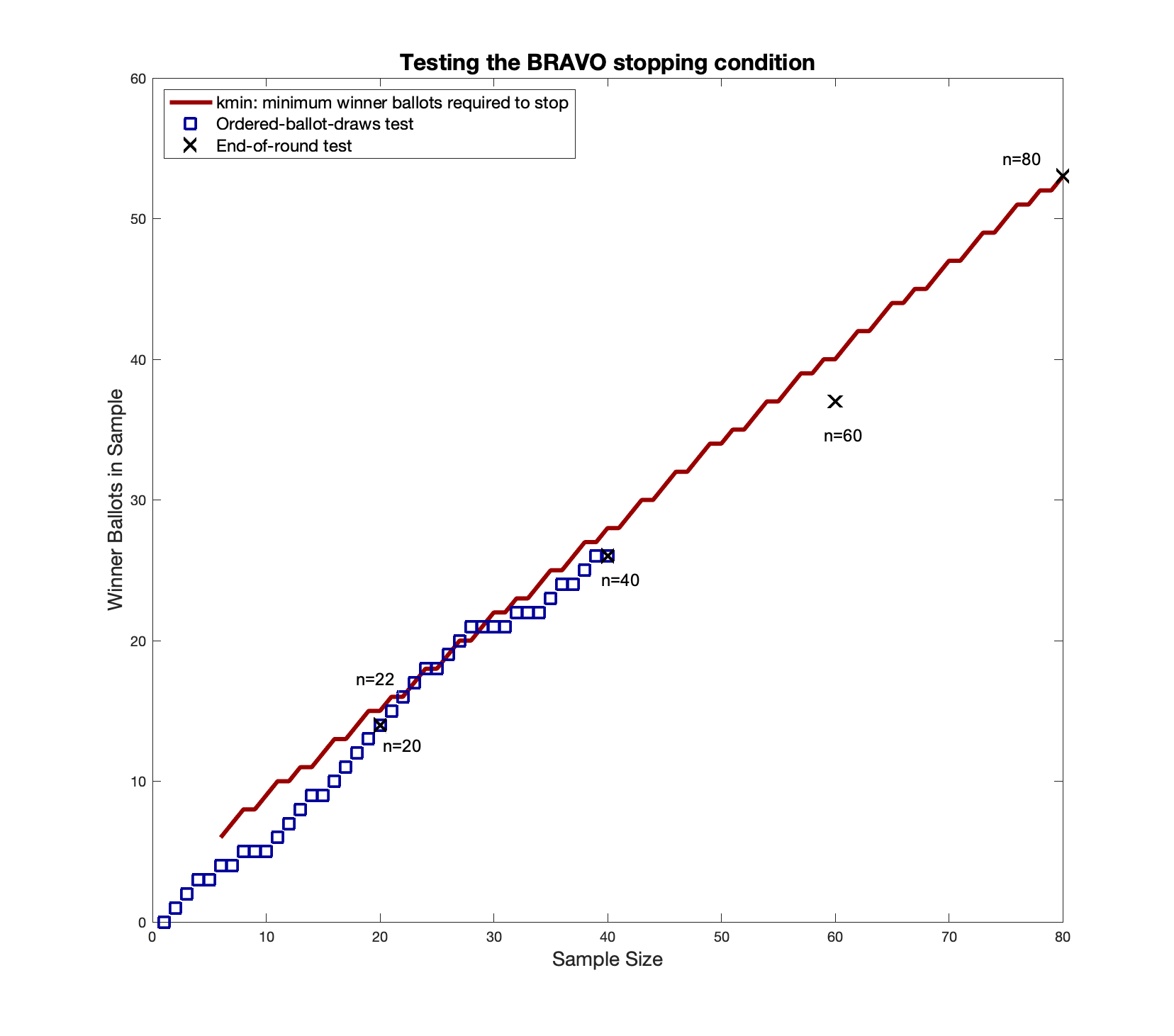

Example 1 (B2 Bravo vs R2 Bravo).

Let and , we get, from equation (2):

Consider ballots drawn in rounds of size and the Bravo condition being tested:

-

•

End-of-Round, which requires a record simply of the tally of the sample polled.

-

•

Selection-ordered-ballots, requires a record of the vote on each ballot polled, in selection order.

Note that the stopping condition is always the Bravo stopping condition; the variation is in when it is checked.

Figure 1 is a plot of as a function of round size. It also shows the results of the tests above, performed on an example sequence.

-

•

For a hypothetical sequence, selection-ordered-ballots Bravo checks the stopping condition at the blue squares till the stopping condition is satisfied, and the audit stops. It has information about the number of ballots for the winner and the total number of ballots drawn at each ballot draw.

-

•

If the same sequence were to go through an end-of-round Bravo audit, the stopping condition would be checked only at the end of the round, denoted in the figure by black crosses. The audit only has information on vote tallies at the end of the round.

We see that the stopping condition is satisfied during the second round, at , but that it is no longer satisfied when it is tested at the end of that round, at , or the following round, . It is satisfied at the end of the fourth round, , which is the number of ballots drawn in an end-of-round Bravo audit.

Thus:

-

•

B2 Bravo ends at , and ballots are drawn.

-

•

End-of-round Bravo ends at and ballots are drawn.

-

•

Selection-ordered-ballots Bravo ends at , and ballots are drawn.

The instance of selection-ordered-ballots Bravo in our example would stop at the end of the second round after ballots are drawn. Such an audit is risk-limiting even though the condition is not satisfied at the draw. This is because every time a sequence satisfies the stopping condition, all extensions of it are defined as having passed the audit as well. In the event that the election outcome is incorrect, any sequence that passes the audit contributes to the risk. A risk-limiting audit ensures that the total risk contribution of all sequences that satisfy the audit is bounded above by the risk limit, whatever the underlying election. This accounting naturally includes risk contributions of all extensions of sequences that pass the audit as well.

Note, however, that selection-ordered-ballots discards the extra information contained in the ballots drawn following the -ballot draw. It ought to be possible to include this information, obtained at some cost, to better estimate the correctness of the election outcome. (Imagine telling election officials and the public that the p-value of the draw was small enough earlier, that it is not any more, and the math allows us to use the earlier value because if the election outcome is incorrect, it is accounted for in the risk limit). We need not be limited by the B2 Bravo rules which begin with a large disadvantage when used for R2 audits, as they do not take into account that the ballots are drawn in rounds.

4 An Introduction to the Athena Class of Audits

In this section, we use an example to illustrate the workings of a proposed new R2 audit Minerva. In later sections, we provide more rigorous descriptions of the Athena class of R2 audits which we prove are risk-limiting and at least as efficient as end-of-round Bravo. As we mentioned in section 1, our proof requires that the the round schedule be pre-determined (before the audit begins). For example, one may choose a factor such that .

Example 2 (End-of-Round -Bravo).

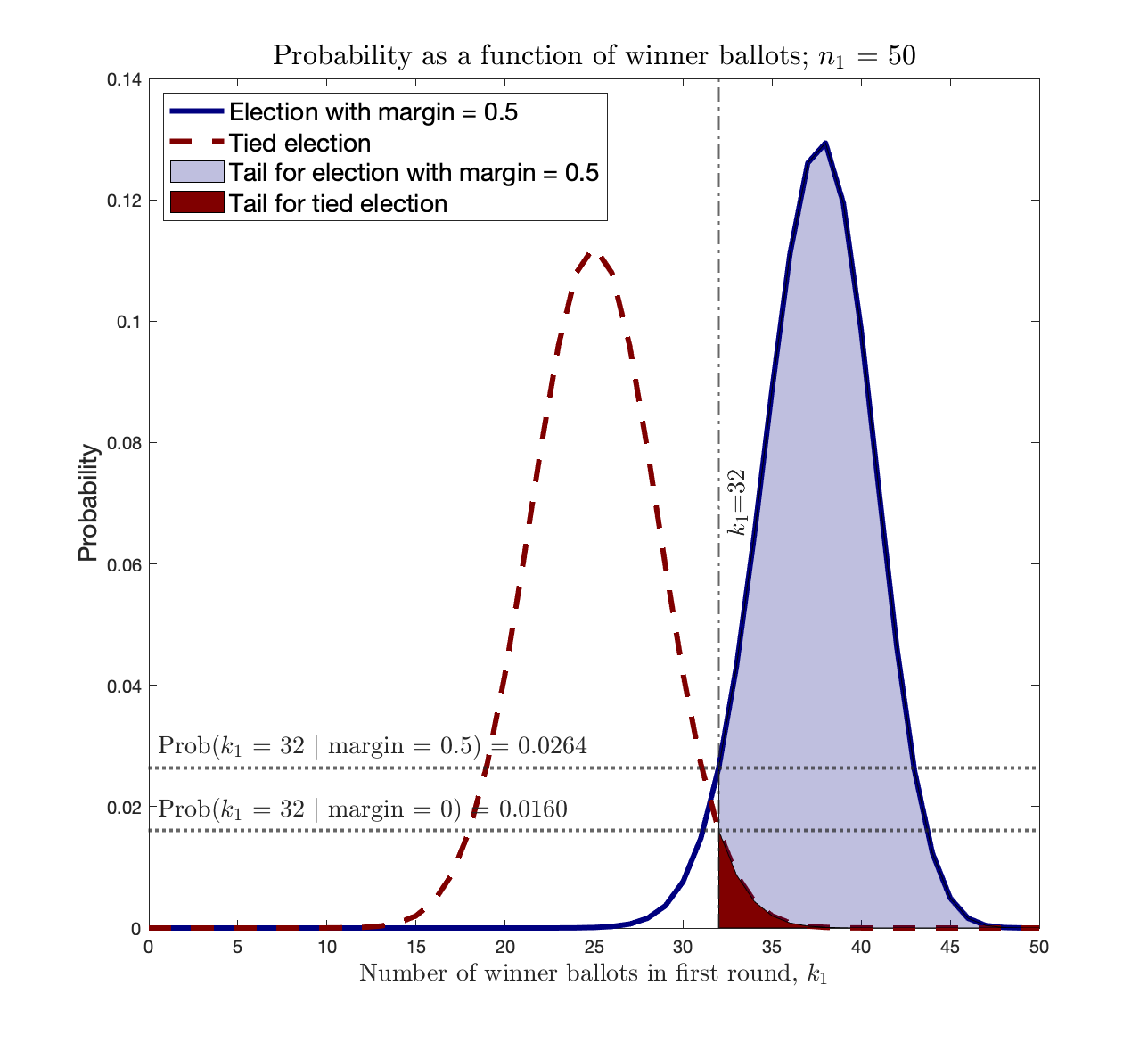

We consider the end-of-round -Bravo audit as in the previous section. Denote by the number of ballots drawn in the first round, and by those for the winner.

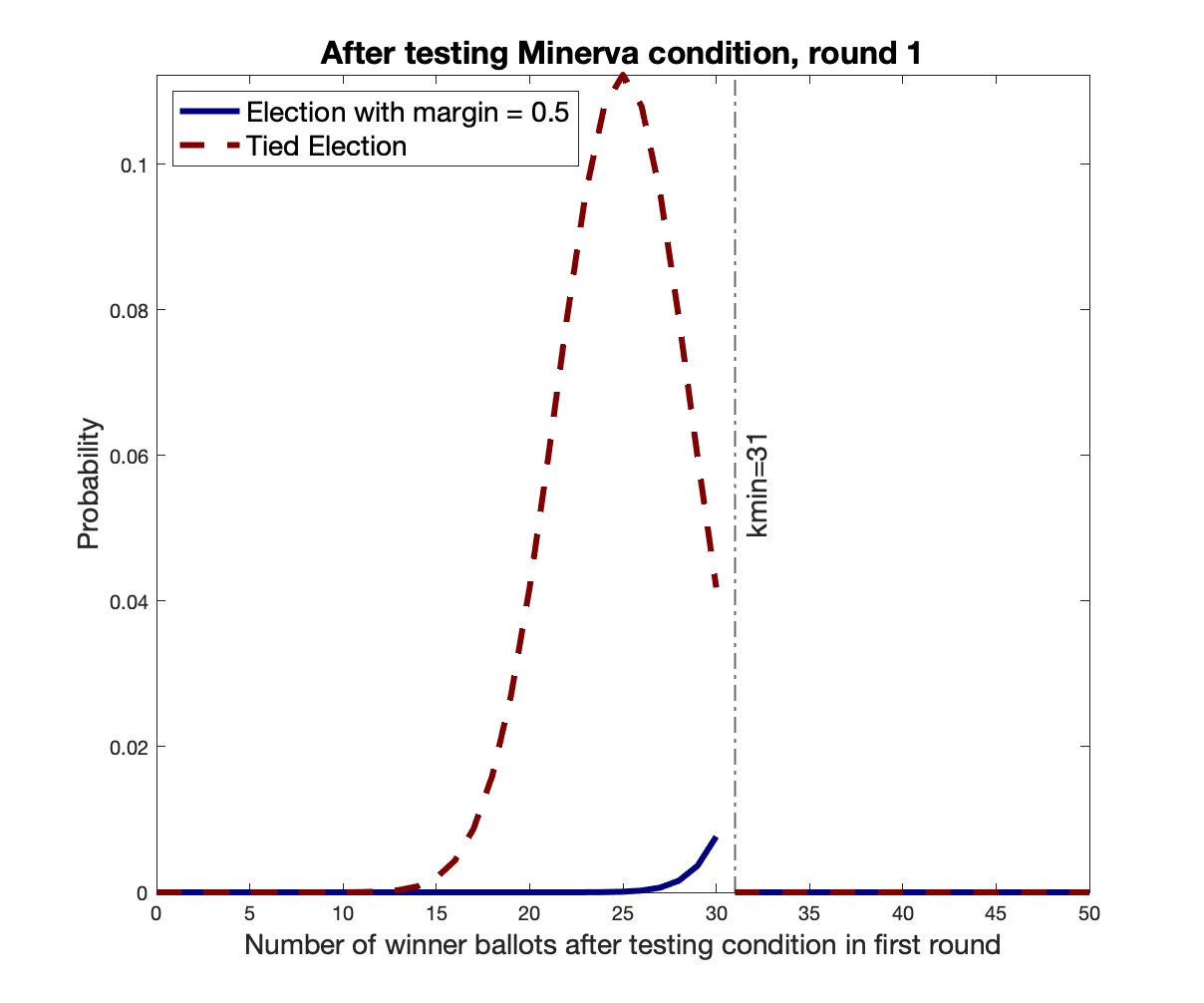

Suppose . Figure 2 shows the probability distributions of for the two hypotheses:

-

: the election is as announced, with (blue solid curve), and

-

: the election is a tie (red dashed curve).

We will continue to refer to Figure 2 in the following sections, when we will address the shaded areas.

Suppose . The B2 -Bravo stopping condition (see inequality(1)) tested end-of-round is:

| (3) |

For our particular example, Figure 2, the likelihood ratio above is:

And the sample does not pass the end-of-round Bravo audit. Recall that the B2 Bravo p-value is the reciprocal of the above probability ratio. In this example, it is .

| (4) |

4.1 The Minerva Audit

We propose the Athena class of audits, which use the tails of the probability distribution functions to define the stopping condition. Here we provide an informal description of the simplest of the Athena class, the Minerva audit.

Example 3 (The Minerva Audit).

For the parameters of Example 2, , , and , we describe the Minerva stopping condition, a comparison test of the ratio of the tails of the distributions:

| (5) |

Compare this to the stopping condition for Bravo, inequality (3).

Note that is the stopping probability for round (the probability that the audit will stop in round given ) associated with deciding to stop at —and not at smaller values. It is the tail of the solid blue curve, the translucent blue area in Figure 2. Similarly, is the associated risk. It is the tail of the red dashed curve denoting the tied election, and shaded red.

For our example, the ratio of the tails of the two curves of Figure 2 is (the values are not denoted in the figure):

And the sample passes the Minerva audit.

4.2 The Minerva audit is risk-limiting

We will prove in Section 7 that the Minerva stopping condition is monotonic increasing as a function of ; one may understand this informally as follows. As explained in Section 3, is monotone increasing with . The Minerva ratio is a weighted average of the values of for and is also, hence, monotone increasing with . If a sample with winner ballots of a total of ballots were to satisfy the stopping condition, so would all samples with .

Smaller values of are associated with larger tails in both curves of Figure 2; and the tails denote the stopping probability (given , the translucent blue tail of the solid blue curve) and the risk (given , the solid red tail of the dashed red curve). The smaller the value of , hence, the larger the associated stopping probability and risk. We could simply choose the smallest acceptable (denoted as ) so that the associated risk is , but then we could not plan to ever go to another round because we would have exhausted the risk budget in the first round. For the Minerva audit, we choose so that the risk is no larger than times the stopping probability. This allows us to go on to an indefinite number of rounds.

Let and be informally defined as follows (more formal definitions follow in Sections 6 and 5):

and

We define and more carefully in section 7 and describe how to compute these values in section 5. Loosely speaking, they denote the risk associated with the round () and the stopping probability of the round () respectively.

The Minerva stopping condition is:

If is the risk of the audit and its stopping probability,

because , the stopping probability of the audit, is no larger than .

In other words, the total risk of the audit is the sum of the risks of each individual round. The stopping condition ensures that each of these risks is no larger than times the corresponding stopping probability. Adding all the risks gives us the total risk, which is no larger than times the total stopping probability. Because the total stopping probability cannot be larger than one, the total risk cannot be larger than , and Minerva is risk-limiting.

4.3 Minerva is at least as efficient as end-of-round Bravo

In this section, we further examine the audit of our previous examples to understand the behavior of the ratios of Bravo and Minerva, and respectively.

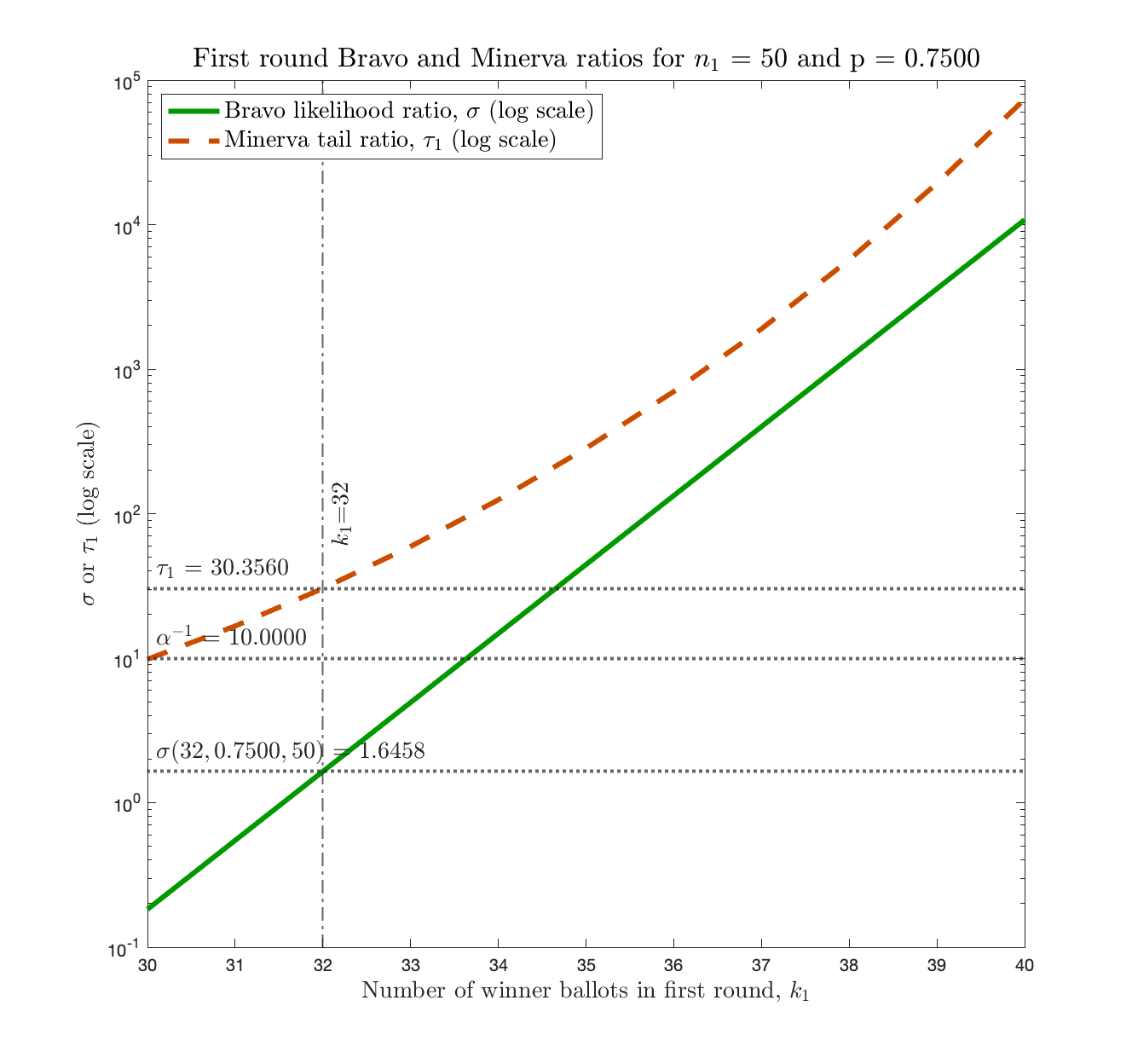

Example 4 (Bravo vs. Minerva Ratios).

For the parameters of Examples 2 and 3: , and , Figure 3 presents the likelihood ratio for end-of-round Bravo (green solid line), , and the tail ratio for Minerva (orange dashed line), , on a log scale. An audit satisfies the stopping condition when its ratio equals or exceeds .

We see that

This means that any sample satisfying end-of-round Bravo will also satisfy Minerva. In fact, it will often be the case that the Minerva condition will be satisfied and the end-of-round Bravo one will not.

The reason for Minerva stopping at smaller values of is as follows. Consider . While

can be much larger for larger values of . The Minerva ratio, , at is a weighted average of all the values of for , allowing the larger values of to “make up” for the smaller ones; in fact, for .

In other words, because the end-of-round Bravo ratio increases as increases, the weighted average, the Minerva ratio, will always be larger than the end-of-round Bravo ratio except if is the largest possible number of winner votes, in which case the two ratios will be equal. Equivalently, the Minerva p-value will always be smaller except when is the largest possible number of winner votes, and the p-values are equal. Thus, Minerva is at least as efficient.

4.4 The Athena audit

In this section we present an example introducing the Athena audit.

Example 5.

We can see from Figure 3 that the Minerva tail ratio at is larger than . However, the end-of-round Bravo ratio is smaller than :

which means that the observation is more likely given (the election is a tie) than it is given (the election is as announced)!

This is technically not an issue; it simply means that Minerva can stop in such a situation and be risk-limiting. We could also choose to enforce an additional stopping condition of a lower bound on the likelihood ratio of the sample. If the sample satisfies the Minerva condition and is of size with votes for the winner, the additional stopping condition would be:

for some . We term this combination of two stopping conditions the Athena audit.

A reasonable choice is (the observation is at least as likely given as it is given ). We would, of course, not desire , because we would then be requiring the satisfaction of the Bravo condition with risk limit .

We can see from Figure 3 that the Athena condition for is satisfied for and no smaller values of . Recall that Minerva stops for . Thus, Minerva would stop for and Athena would not.

In our experiments we have observed samples satisfying Minerva but not Athena when the election margin is wide, as in our example. Hence, clearly, Athena is not as efficient as Minerva, because it imposes an additional condition. One may think of Minerva as determining whether the election outcome is correct, and Athena determining, in addition, if the election tally is close enough to the announced tally.

5 Computing Risks and Stopping Probabilities for Multiple-Round Audits

In this section we describe how probability distributions may be computed in multiple round audits with monotone stopping conditions; that is, audits where the stopping condition is represented through the use of . We use examples to demonstrate how the probability distributions may be computed for rounds and above.

Example 6 (Testing the Stopping Condition).

Consider an election with and a risk limit of . Suppose the first round size is and the draw results in ballots for the announced winner. Recall that (see equation (4), Example 2)

Thus the sample passes neither the Minerva nor the end-of-round Bravo audit.

Now suppose we draw more ballots to get ballots in all, of which are for the winner. We will need to compute the probability distribution on to determine the ratio of the tails for the Minerva stopping condition.

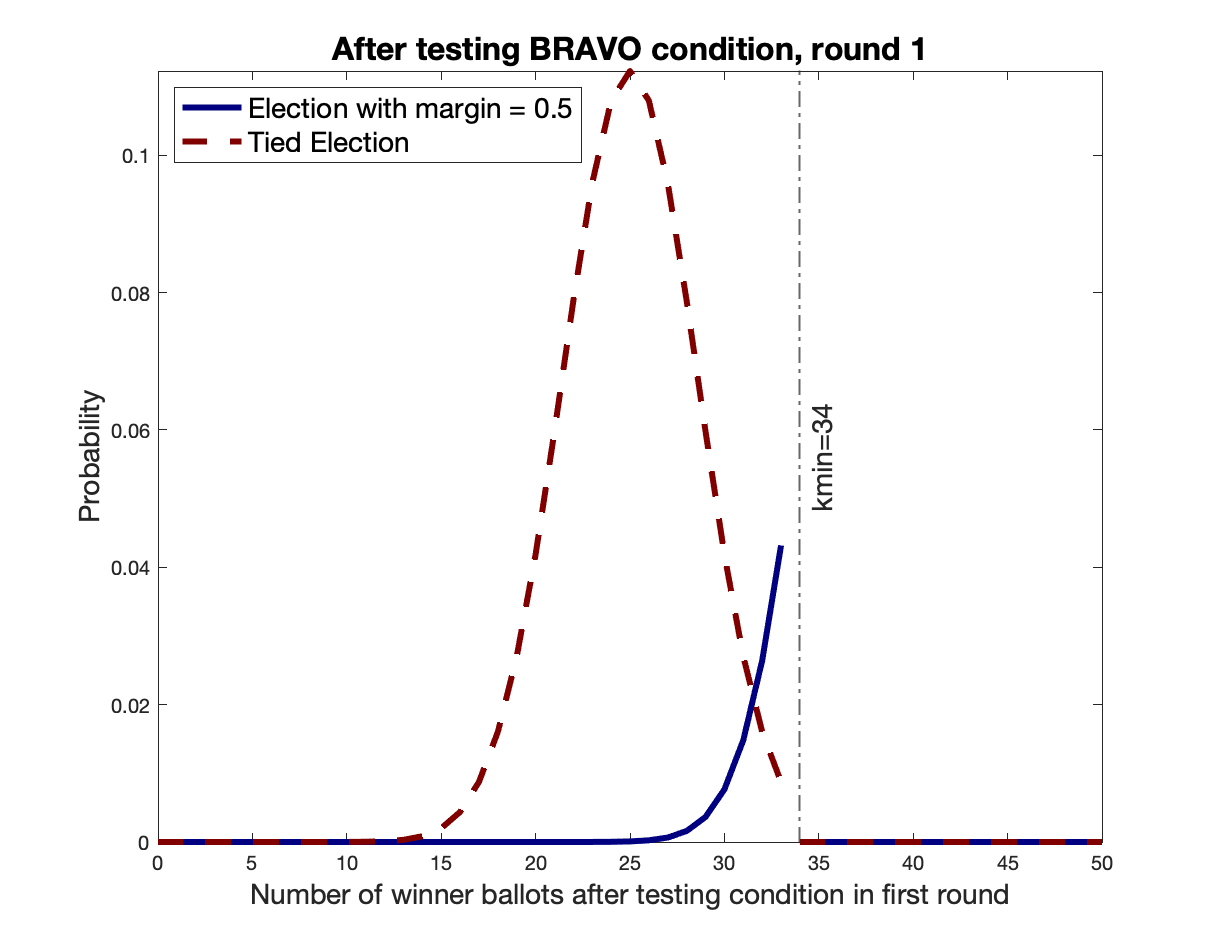

Note that the probability distribution of is not the binomial distribution for a sample size of . In fact, if the audit did not stop in the first round, for Minerva, which means that can be no larger than , even if all ballots in the second round are for the announced winner. Similarly, for the end-of-round Bravo audit can be no larger than .

If the audit continues, the maximum number of ballots before new ones are drawn is for Bravo and for Minerva. The probability distributions before the new sample is drawn are as shown in Figures 4 and 5, and may be denoted as:

and

where and denote the end-of-round Bravo and Minerva audits for the given parameters.

The “discarded” tails, in both cases, represent the probabilities that the audit stops. When this is conditional on , we refer to it as the stopping probability of the round (), large values are good. When it is conditional on , it is the worst-case risk corresponding to the round (), large values are bad. Recall that our stopping condition bounds the worst-case risk for the round to be no larger than a fraction of the stopping probability.

Using the above probability distributions, we can now compute the distribution of ballots for the announced winner in the sample of size , which we obtain after drawing more ballots.

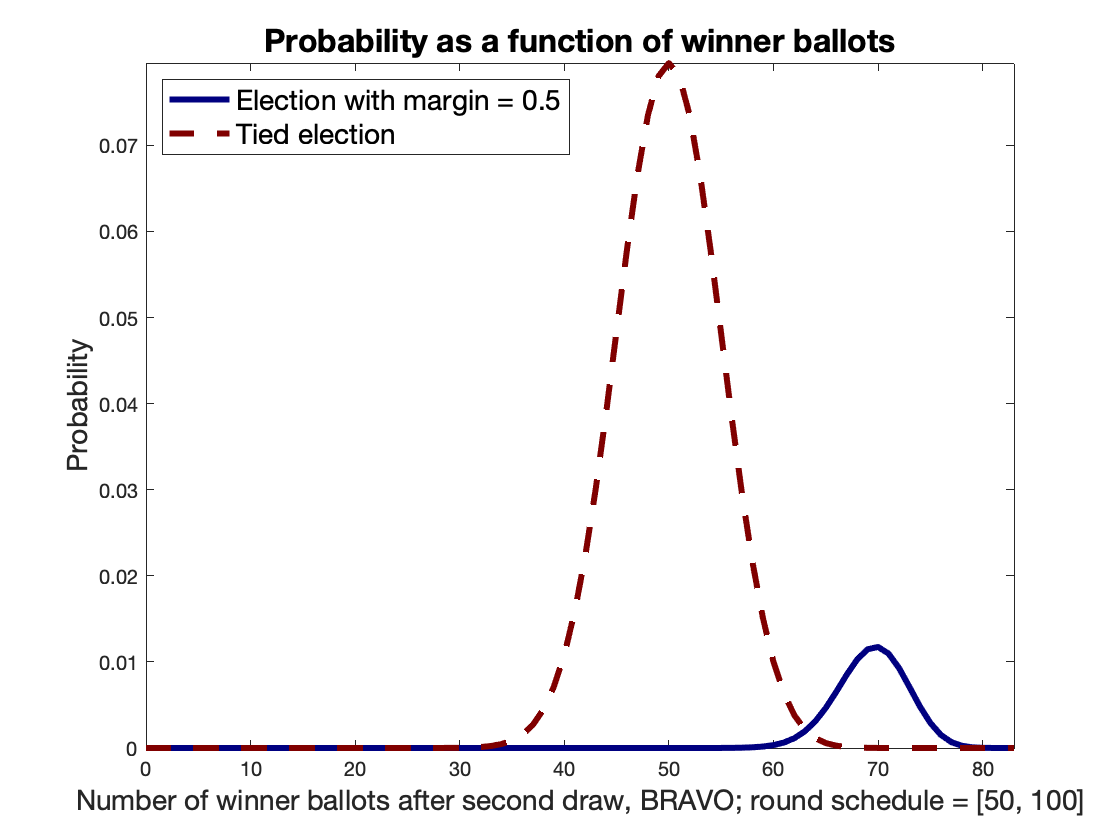

Example 7 (Second Round Distribution).

Continuing with Example 6, we consider an election with , risk limit and round sizes . We wish to compute the probability distribution for , the number of votes for the announced winner after drawing the second round of ballots. Recall that (see equation (4), Example 2)

First consider the end-of-round Bravo audit. After the first round stopping condition is tested, and the audit stopped if the condition is satisfied, the number of votes for the winner is at most . Let be the number of votes for the winner. Then lies between and . It is distributed as in Figure 4, and we denote the distribution by for the null hypothesis (tied election, represented by the red dashed line) and for the alternate hypothesis (election is as announced, represented by the blue solid line).

There would be a total of winner ballots in the sample after the second draw if winner ballots were drawn among the new ballots drawn in round 2. is a random variable, and its distribution is the binomial distribution for the draw of size .

If we denote the distribution of as , it is:

where is the probability of drawing votes for the announced winner in a sample of size , when the fractional vote for the announced winner is for and for .

The above expression is known as the convolution of the two functions, and is denoted:

where represents the convolution operator and the hypothesis. The convolution of two functions can be computed efficiently using Fourier Transforms; this result is the convolution theorem.

After drawing the second sample, the probability distributions for Bravo are as in Figure 6.

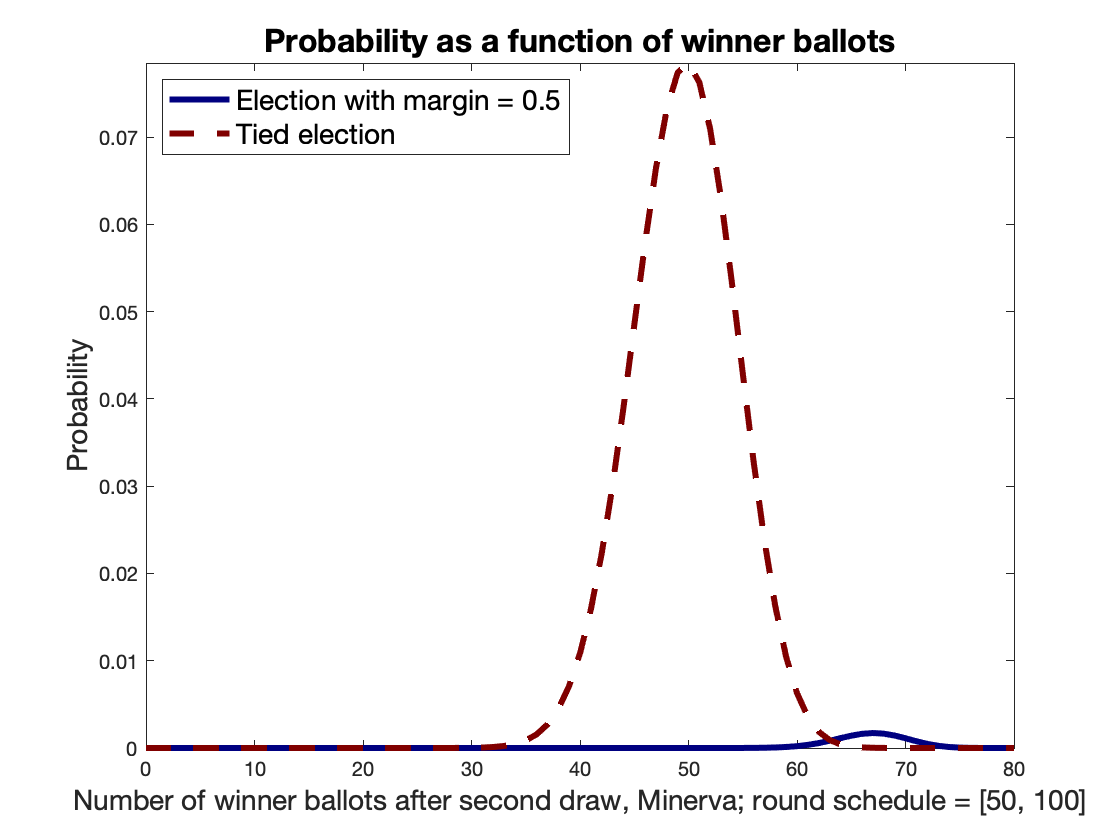

Similarly, for Minerva, lies between and . is similarly the convolution of the function(s) represented in Figure 5 and the binomial distribution corresponding to a draw of ballots for the respective hypotheses. After drawing the second sample, the probability distributions for Minerva are as in Figure 7.

In order to compute probability distributions for the next round, we would first compute the value of for this round using the tail ratio, then zero the probability distributions for the value of and above, and then perform a convolution with the binomial distribution corresponding to the size of the next draw. And so on.

Probability distributions for B2 audits may be computed similarly, with the round schedule: . We used this approach to compute percentiles for the Bravo stopping probabilities; see Section 8 for the results.

6 The Athena Class of Audits

In this section we rigorously describe Minerva and Athena, two audits from the new Athena class of risk-limiting audits. The stopping condition for Bravo is a comparison test for the ratio of probabilities of the number of winner ballots. On the other hand, the stopping conditions for the Athena class are comparison tests for the ratio of the complementary cumulative distribution functions (cdfs). For the Athena class of audits, the stopping condition for a given round does depend on previous round sizes, which are required to compute the complementary cdfs, but not on future round sizes.

6.1 The Minerva audit

Given the B2 -Bravo test we define the corresponding R2 Minerva test by its stopping condition, which is a comparison test of the ratio of the complementary cdfs of samples that did not satisfy the stopping condition for any previous round. We expect that similar R2 Minerva tests can be defined for other SPRTs with zero error of the second kind whose probability ratio is a monotonic increasing function of , such as Bayesian audits, but do not address these in this paper. Note that the round schedule is predetermined before the audit begins.

Definition 3 (-Minerva).

Given B2 -Bravo and round sizes , the corresponding R2 Minerva stopping rule for the round is:

| (6) |

where is the complementary cumulative distribution ratio for the round:

| (7) |

and, as with B2 -Bravo, , the alternate hypothesis, is that the fractional tally for the winner is .

Clearly, for and the first round,

6.2 The Athena audit

In addition to comparing the ratio of complementary cumulative distribution functions as in Minerva, the Athena audit also enforces a lower bound on the probability ratio, , of the B2 -Bravo test.

Definition 4 (-Athena).

Given B2 -Bravo, round sizes and parameter , the corresponding Athena stopping rule for the round is:

| (8) |

where is the complementary cumulative distribution ratio for the round:

| (9) |

and, as with B2 -Bravo, , the alternate hypothesis, is that the fractional tally for the winner is .

Clearly, for and the first round,

We further define the risk and stopping probability associated with each round.

Definition 5 ().

The probability of stopping in the round for audit is defined as:

Definition 6 ().

The risk of the round of audit is defined as:

7 Risk-Limiting Properties of the Athena Class of Audits

In this section we present the risk-limiting and efficiency properties of Minerva and Athena. We begin with an outline of our approach. Rigorous statements follow and proofs are in the Appendix.

7.1 An outline of the proofs

In this section we provide an outline of the claims and proofs.

Using induction on the number of rounds, we prove a couple of interesting properties, including, at the core, that the likelihood ratio of (total number of winner ballots) in the round is

That is, for winner ballots in round , when sequences are restricted to those that did not satisfy stopping conditions in previous rounds, the likelihood ratio is simply , independent of any additional constraints on sequence order and the past or future round schedule. This property leads to the result that the test in the round is a comparison test for .

For the base case, it is easily shown that the likelihood ratio in the first round is , as there is no previous round:

is easily seen to be monotone increasing with because .

The induction step proceeds as follows. Suppose the likelihood ratio for the number of winner ballots in round is . The ratios used for the stopping conditions of the round in Minerva and Athena

and

respectively, are weighted sums of for . Because is monotone increasing with , the respective stopping conditions are monotone increasing with , and can be expressed as comparison tests for .

Athena has two conditions. The second one is a comparison test for the likelihood ratio, and hence also equivalent to a comparison test for the number of winner ballots. The overall comparison test is the stricter of the two, and is also a comparison test. Thus the stopping condition for round is a test of the form for a that depends on the audit, its parameters including previous round sizes, the election parameters and the risk limit. As described in section 4, one can use convolution to compute the probability distributions for .

To determine the nature of the likelihood ratio for round , we proceed as follows. The likelihood ratio for in round is assumed to be . Hence, the distribution of in round given is a multiple of , and that given is the same multiple of . The multiplying factor itself is a function of , current and previous round sizes, and , as it captures the previous comparison tests on the number of winner ballots. On convolution, when one obtains the distributions for round , the multiplying factors change, but the one for the distribution given is the same as that for the distribution given . Loosely speaking, the number of ways of obtaining a sequence with winner ballots in a round of size , given previous round sizes (and hence previous comparison tests for winner ballots), is independent of the hypothesis. Thus the likelihood ratio of in round remains .

It is now easy to show that the audits are risk-limiting. The tail (beginning at ) of the probability distribution of in the round conditional on hypothesis () is the stopping probability (risk) associated with the round. Both Minerva and Athena audits require that the tail corresponding to (the risk corresponding to round ) be no more than times the tail corresponding to (the stopping probability), thus ensuring that the sum of all the risk contributions of the rounds is no more than times the total stopping probability, and hence no more than .

Both Minerva and Athena are more efficient than end-of-round Bravo. This is because the ratios , and are all compared to the same value, . For winner ballots, the ratio for Bravo is , which is monotone increasing with . The ratios for Athena and Minerva, and respectively, are weighted sums of for and hence strictly larger, unless is the largest value with non-zero probability (it would be value of of for the previous round, plus the size of the current draw), when they are equal. Thus, if a sample satisfies the end-of-round Bravo condition, it also satisfies the conditions on and . The Athena audit includes a second test, which is a comparison test for . If , this too is satisfied if the end-of-round Bravo condition is satisfied.

We state the above claims more formally in the rest of this section, and prove them in the Appendix. We also prove that the Minerva and Athena () stopping conditions, when round increments are specified to be one, are equivalent to the B2 Bravo condition, though p-values are not the same except for samples where the audits stop.

7.2 Notation

We establish some shorthand notation which will be useful.

For ease of notation, when the audit and its parameters: round schedule , risk limit , fractional vote for the winner are fixed, we denote:

Thus is the ratio of the complementary cdfs in round when the number of winner ballots drawn is , and the sequence did not satisfy the stopping condition in a previous round.

Similarly,

and

and is the likelihood ratio of winner ballots in round when the sequence did not satisfy the stopping condition in a previous round.

Note also the following simple observation:

| (10) |

7.3 Properties of the Minerva and Athena complementary cdf ratios

In this section we prove interesting properties of the Minerva and Athena ratios that are necessary to prove that the audits are risk-limiting.

Note that the B2 -Bravo stopping condition is based on :

where the history of round size is completely captured in the total number of ballots drawn, .

We prove that is also the likelihood ratio of winner ballots in all rounds of the Minerva and Athena audits, even though round sizes are not constrained in any way. We additionally prove other interesting properties.

Theorem 1.

For the -Minerva test, if the round schedule is pre-determined (before the audit begins), the following are true for

-

1.

when and are defined and non-zero.

-

2.

is monotone increasing as a function of .

-

3.

such that

Similarly:

Theorem 2.

For the -Athena test, if the round schedule is pre-determined (before the audit begins), the following are true for :

-

1.

when and are defined and non-zero.

-

2.

is monotone increasing as a function of .

-

3.

such that

7.4 Minerva and Athena are risk-limiting

Now we may state the results on the risk limiting properties of the audits.

Theorem 3.

-Minerva is an -RLA if the round schedule is pre-determined (before the audit begins).

Exactly the same approach may be used to prove:

Theorem 4.

-Athena is an -RLA if the round schedule is pre-determined (before the audit begins).

7.5 Properties of B2 versions of Minerva and Athena

In this section we study the relationship between B2 Bravo and Minerva with each round consisting of a single ballot draw. We make the following observation: samples satisfying the stopping condition of -Bravo, performed ballot-by-ballot, are exactly those satisfying that of the -Minerva audit, where is the hypothesis that the winner’s fractional tally is . The p-values of the two audits, however, differ except at their values of .

Theorem 5.

The B2 -Bravo audit stops for a sample of size with ballots for the winner, if and only if the -Minerva audit stops.

Corollary 1.

Given such that , the B2 -Bravo audit stops for a sample of size with ballots for the winner, if and only if the -Athena audit stops.

7.6 Strong RLAs

We define a new audit property which characterizes the difference between Minerva and Athena.

Definition 7 (Strong Risk Limiting Audit ()-RLA).

An audit procedure is an ()-Strong Risk Limiting Audit if it is a Risk Limiting Audit with risk level and, if, for every accepted sample, the likelihood-ratio is bounded below by :

It is easy to see that:

Lemma 1.

B2 Bravo, end-of-round Bravo and selection-ordered-ballots Bravo are -strong RLAs.

7.7 Efficiency

In this section we present an efficiency result for Minerva and Athena (for .

Theorem 6.

Given sample of size with samples for the winner,

where denotes the -Bravo test and the -Minerva test or the

-Athena test for if the round schedule is pre-determined (before the audit begins).

From this it follows that Minerva and Athena (for is each at least as efficient as the corresponding end-of-round application of B2 rules. In section 8.2 we demonstrate that Athena and Minerva can be considerably more efficient.

8 Experimental Results

In this section we describe our experimental results. We first present our analytical results for percentiles of the Bravo stopping condition, and compare them with those reported by Lindeman et al. [5, Table 1]. We then describe our estimates of first round sizes, comparing Athena () to both end-of-round Bravo and selection-ordered-ballots Bravo. Finally, we present simulation results.

8.1 B2 BRAVO Percentile Verification

We used the approach described in Section 5 to generate the probability distributions for B2 Bravo using various election margins to see how our estimates compared to those obtained by Lindeman et al. [5, Table 1]. They used simulations.

Table 1 presents our values. Values in parentheses are from [5, Table 1], where they differ. Also listed in the table is Average Sample Number (ASN), which is computed using a standard theoretical estimate (and not using our analytical expressions, nor simulations). It provides a baseline to compare with the values for the Expected Ballots column. Some of the difference between our values and those of [5, Table 1] is likely due to rounding off. Further, we notice that both our values and those of [5, Table 1], when they differ from ASN, are lower than ASN. In our case, the difference is likely due to the fact that we compute our probability distributions for only up to 6ASN draws, using a finite summation to estimate the probability distributions, and we model the discrete character of the problem, which is not captured by ASN. The largest difference between our values and those of [5, Table 1] is ballots, corresponding to a fractional difference of 0.41 %, in the estimate of the expected number of ballots drawn for a margin of 1%. Our value is further from ASN. The average of the absolute value of the fractional difference between our results and those of [5] is 0.13%. The differences between our values and those obtained with simulations could be because simulations may not be sufficiently accurate at the lower margins, where most of the errors are. It could also be because our finite summation is not sufficient at low margin.

| Margin | Expected Ballots | ASN | |||||

|---|---|---|---|---|---|---|---|

| 0.4 | 12 | 22 | 38 | 60 | 131 | 29.47 | 30.03 |

| (30) | |||||||

| 0.3 | 23 | 38 | 66 | 108 | 236 | 52.83 | 53.25 |

| (53) | |||||||

| 0.2 | 49 | 84 | 149 | 244 | 538 | 118.00 | 118.88 |

| (119) | |||||||

| 0.18 | 77 | 131 | 231 | 381 | 842 | 183.60 | 184.89 |

| (840) | (184) | ||||||

| 0.1 | 193 | 332 | 587 | 974 | 2,155 | 466.47 | 469.26 |

| (2,157) | (469) | ||||||

| 0.08 | 301 | 518 | 916 | 1,520 | 3,366 | 726.95 | 730.80 |

| (730) | |||||||

| 0.06 | 531 | 914 | 1,621 | 2,698 | 5,976 | 1,287.60 | 1,294.62 |

| (1,619) | (2,700) | (5,980) | (1,294) | ||||

| 0.04 | 1,190 | 2,051 | 3,637 | 6,055 | 13,433 | 2,887.28 | 2,901.97 |

| (1,188) | (6,053) | (13,455) | (2,900) | ||||

| 0.02 | 4,727 | 8,161 | 14,493 | 24,155 | 53,646 | 11,506.45 | 11,561.66 |

| (4,725) | (8,157) | (14,486) | (24,149) | (53,640) | (11,556) | ||

| 0.01 | 18,845 | 32,566 | 57,856 | 96,469 | 214,385 | 45,935.85 | 46,150.44 |

| (18,839) | (32,547) | (57,838) | (96,411) | (214,491) | (46,126) |

8.2 First-round estimates

In this section we report the results of our estimates for first round sizes for 90% stopping probability for both end-of-round Bravo and Athena (), for the announced statewide results of the 2016 US Presidential election. Our results are presented in Table 2.

We constructed a table of stopping probability as a function of round size for a given margin, where the stopping probability of a round is the tail corresponding to the value for that round size. We observed that the stopping probability is not a monotone increasing function of round size. This is because, if increases with round size (it does not decrease, but it may remain the same), the stopping probability may decrease slightly. For our first-round-size computations reported in section 8, we use the more conservative estimates: given a desired stopping probability , we chose round sizes such that all larger rounds stopped with probability at least . For small margins, smaller than (except the states of Michigan and New Hampshire, which had the smallest margin), we did not construct the entire table, but began looking for the values by checking if the values of with the requisite tail size satisfied the stopping condition. Finally, for the states of Michigan and New Hampshire, we approximated round size by estimating the binomial as a gaussian.

We first examined the relationship between end-of-round Bravo and Athena () first-round sizes. We estimated the stopping probability and the first-round sizes for end-of-round Bravo as described above. We use the round size beyond which the stopping probability is at least for both end-of-round Bravo and Athena, thus our round-size estimates are conservative. We scaled these estimates by the ratio of total ballots cast to the number of valid ballots in the contest between the two leading candidates, Trump and Clinton. Better estimates would result from taking into consideration every possible margin for every round size. Our approach, however, is sufficient for the purposes of a rough comparison (we have developed software for the more accurate approach; it is being tested). Of course, some of these sizes are too large for consideration in a real audit; in particular, the round size for New Hampshire is more than the number of ballots cast in the election.

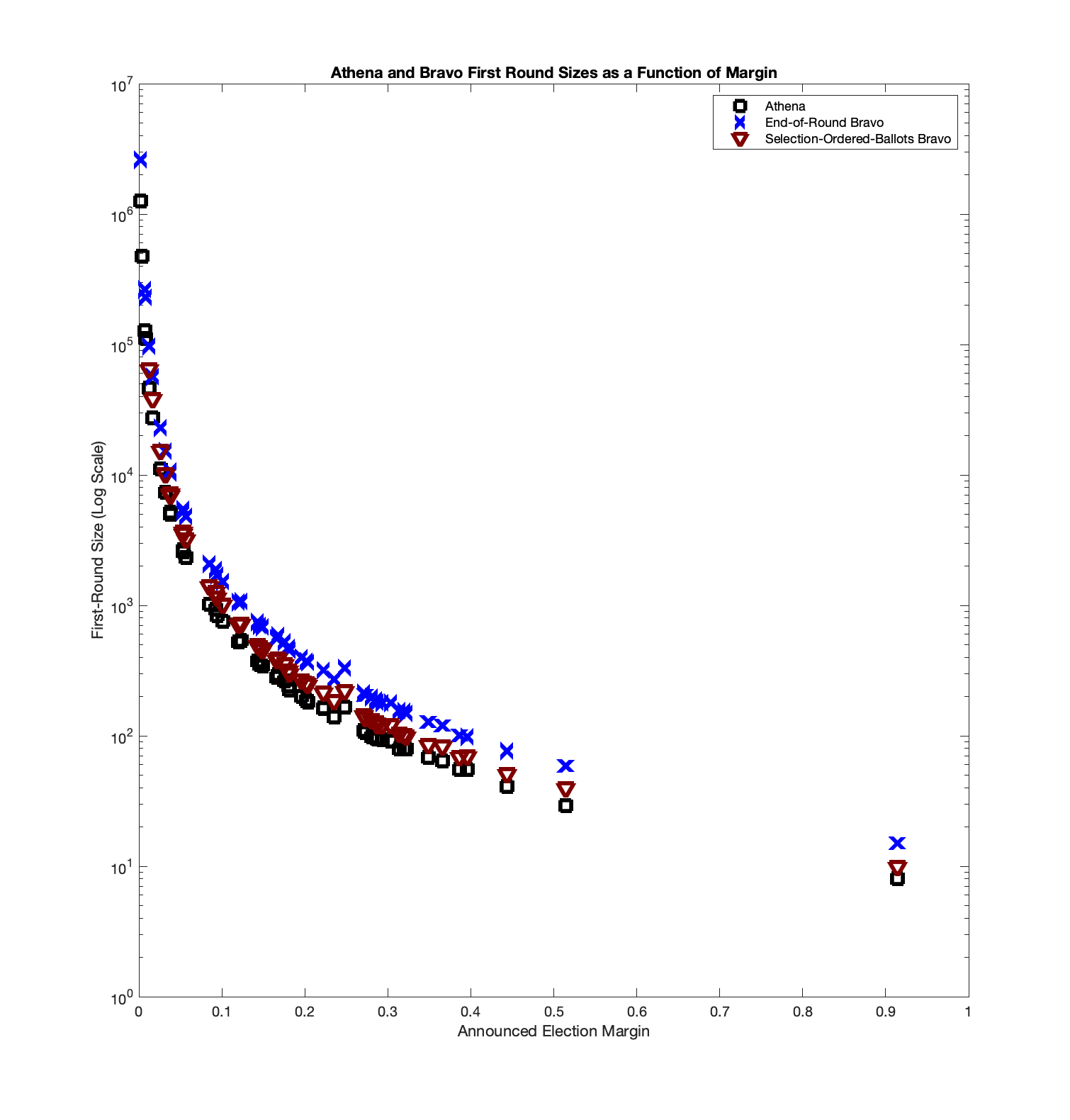

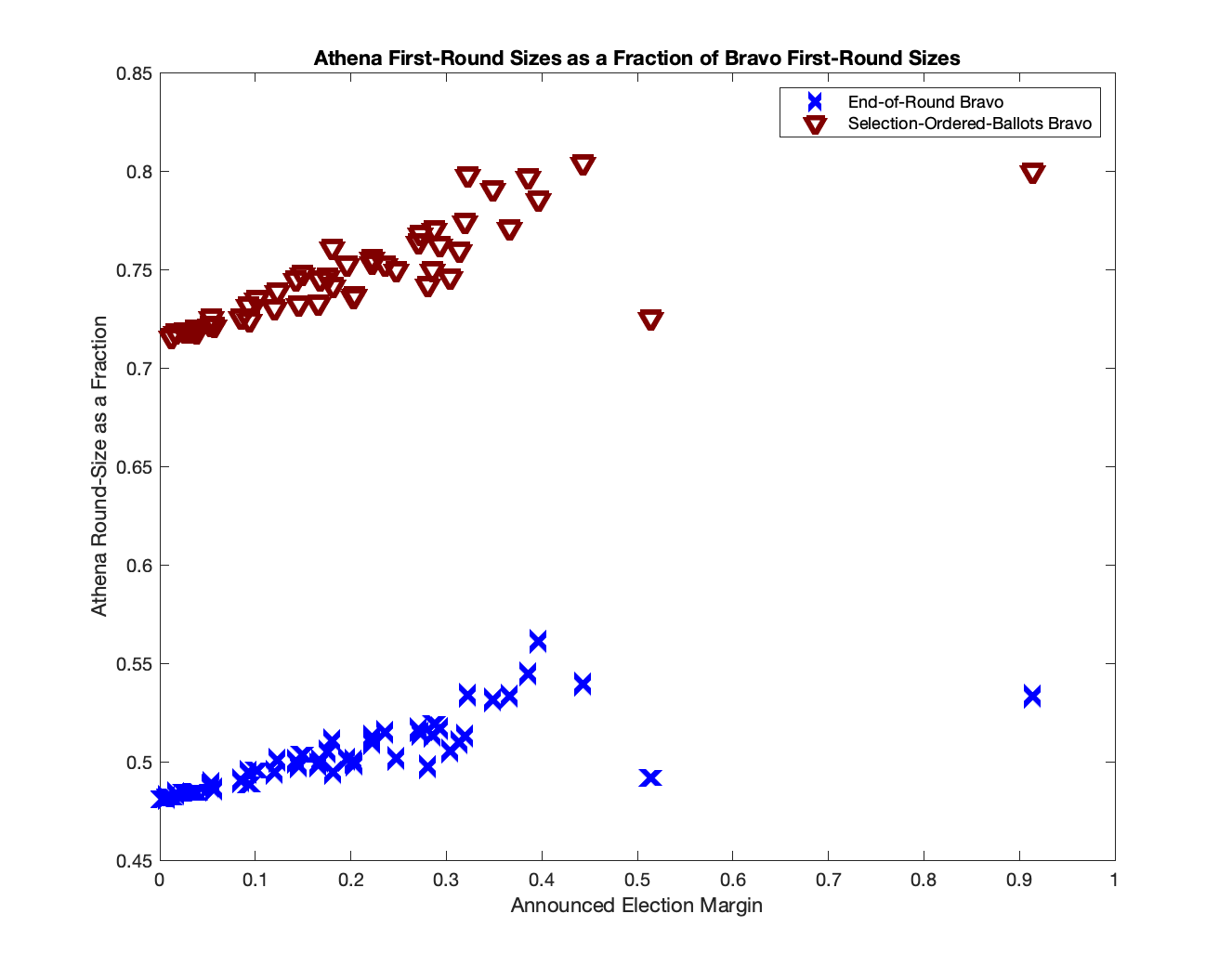

It is noteworthy that, across all margins, Athena first round sizes are about half those of end-of-round Bravo. We note that the number of distinct ballots drawn (thanks to Philip B. Stark for the suggestion) behaves similarly with margin, except for the smallest margins, when the number of ballots drawn is so large that the number of distinct ballots drawn differs from the number of ballot draws.

We also estimate first round sizes for stopping probability for selection-ordered-ballots Bravo by treating it as a multiple-round audit. We use the approach described in Section 5, for which our verification results were presented in Section 8.1. Our results are presented in Table 3. We currently omit estimates for states with margins smaller than . In the other states, we observe that the improvement on using Athena () is , with greater improvements for smaller margins. Recall that, unlike selection-ordered-ballots Bravo, Athena does not require that the ballots be noted in selection order; sample tallies are sufficient.

We present the same data (number of ballot draws, not number of distinct ballots) in the form of plots. Figure 8 plots the first round sizes of Athena, end-of-round Bravo and selection-ordered-ballots Bravo on a log scale as a function of margin. One can observe that the Athena round sizes are the smallest, and the end-of-round the largest. Figure 9 plots the Athena round size as a fraction of the corresponding end-of-round Bravo and selection-ordered-ballots Bravo round sizes. There is a small variation with margin, with the Athena round sizes being smaller fractions for smaller margins (that is, the improvement from using Athena is larger for smaller margins). Note that a couple of states with the largest margins do not have the largest ratios. This is likely because the round sizes are very small, and hence a difference of a single ballot changes the ratio considerably.

| State | Margin | EoR Bravo | Athena | Athena size as a fraction | |||

| of EoR Bravo size | |||||||

| Draws | Distinct Ballots | Draws | Distinct Ballots | Draws | Distinct Ballots | ||

| Alabama | 0.2875 | 181 | 181 | 94 | 94 | 0.5193 | 0.5193 |

| Alaska | 0.1677 | 590 | 590 | 295 | 295 | 0.5000 | 0.5000 |

| Arizona | 0.0378 | 10,732 | 10,710 | 5,204 | 5,199 | 0.4849 | 0.4854 |

| Arkansas | 0.2857 | 187 | 187 | 96 | 96 | 0.5134 | 0.5134 |

| California | 0.3226 | 148 | 148 | 79 | 79 | 0.5338 | 0.5338 |

| Colorado | 0.0537 | 5,475 | 5,470 | 2,676 | 2,675 | 0.4888 | 0.4890 |

| Connecticut | 0.1428 | 748 | 748 | 374 | 374 | 0.5000 | 0.5000 |

| Delaware | 0.1200 | 1,057 | 1,056 | 523 | 523 | 0.4948 | 0.4953 |

| DistrictOfColumbia | 0.9139 | 15 | 15 | 8 | 8 | 0.5333 | 0.5333 |

| Florida | 0.0124 | 96,608 | 96,115 | 46,563 | 46,449 | 0.4820 | 0.4833 |

| Georgia | 0.0532 | 5,266 | 5,263 | 2,567 | 2,567 | 0.4875 | 0.4877 |

| Hawaii | 0.3488 | 128 | 128 | 68 | 68 | 0.5312 | 0.5312 |

| Idaho | 0.3662 | 120 | 120 | 64 | 64 | 0.5333 | 0.5333 |

| Illinois | 0.1804 | 474 | 474 | 242 | 242 | 0.5105 | 0.5105 |

| Indiana | 0.2023 | 374 | 374 | 187 | 187 | 0.5000 | 0.5000 |

| Iowa | 0.1013 | 1,520 | 1,520 | 753 | 753 | 0.4954 | 0.4954 |

| Kansas | 0.2222 | 318 | 318 | 162 | 162 | 0.5094 | 0.5094 |

| Kentucky | 0.3134 | 155 | 155 | 79 | 79 | 0.5097 | 0.5097 |

| Louisiana | 0.2034 | 365 | 365 | 182 | 182 | 0.4986 | 0.4986 |

| Maine | 0.0319 | 15,202 | 15,049 | 7,358 | 7,322 | 0.4840 | 0.4865 |

| Maryland | 0.2803 | 197 | 197 | 98 | 98 | 0.4975 | 0.4975 |

| Massachusetts | 0.2930 | 180 | 180 | 93 | 93 | 0.5167 | 0.5167 |

| Michigan | 0.0024 | 2,618,926 | 2,018,381 | 1,259,688 | 1,107,933 | 0.4810 | 0.5489 |

| Minnesota | 0.0166 | 56,680 | 56,139 | 27,421 | 27,294 | 0.4838 | 0.4862 |

| Mississippi | 0.1818 | 453 | 453 | 224 | 224 | 0.4945 | 0.4945 |

| Missouri | 0.1964 | 401 | 401 | 201 | 201 | 0.5012 | 0.5012 |

| Montana | 0.2222 | 320 | 320 | 164 | 164 | 0.5125 | 0.5125 |

| Nebraska | 0.2710 | 213 | 213 | 110 | 110 | 0.5164 | 0.5164 |

| Nevada | 0.0259 | 22,943 | 22,711 | 11,110 | 11,056 | 0.4842 | 0.4868 |

| NewHampshire | 0.0039 | 1,007,590 | 552,067 | 475,357 | 351,311 | 0.4718 | 0.6364 |

| NewJersey | 0.1457 | 703 | 703 | 350 | 350 | 0.4979 | 0.4979 |

| NewMexico | 0.0930 | 1,888 | 1,886 | 934 | 934 | 0.4947 | 0.4952 |

| NewYork | 0.2354 | 272 | 272 | 140 | 140 | 0.5147 | 0.5147 |

| NorthCarolina | 0.0381 | 10,330 | 10,319 | 5,000 | 4,998 | 0.4840 | 0.4843 |

| NorthDakota | 0.3962 | 98 | 98 | 55 | 55 | 0.5612 | 0.5612 |

| Ohio | 0.0854 | 2,077 | 2,077 | 1,018 | 1,018 | 0.4901 | 0.4901 |

| Oklahoma | 0.3861 | 101 | 101 | 55 | 55 | 0.5446 | 0.5446 |

| Oregon | 0.1231 | 1,068 | 1,068 | 535 | 535 | 0.5009 | 0.5009 |

| Pennsylvania | 0.0075 | 265,245 | 259,621 | 127,792 | 126,477 | 0.4818 | 0.4872 |

| RhodeIsland | 0.1662 | 562 | 562 | 280 | 280 | 0.4982 | 0.4982 |

| SouthCarolina | 0.1492 | 683 | 683 | 344 | 344 | 0.5037 | 0.5037 |

| SouthDakota | 0.3194 | 154 | 154 | 79 | 79 | 0.5130 | 0.5130 |

| Tennessee | 0.2725 | 206 | 206 | 106 | 106 | 0.5146 | 0.5146 |

| Texas | 0.0943 | 1,706 | 1,706 | 833 | 833 | 0.4883 | 0.4883 |

| Utah | 0.2477 | 329 | 329 | 165 | 165 | 0.5015 | 0.5015 |

| Vermont | 0.3037 | 180 | 180 | 91 | 91 | 0.5056 | 0.5056 |

| Virginia | 0.0565 | 4,790 | 4,788 | 2,329 | 2,329 | 0.4862 | 0.4864 |

| Washington | 0.1757 | 525 | 525 | 265 | 265 | 0.5048 | 0.5048 |

| WestVirginia | 0.4432 | 76 | 76 | 41 | 41 | 0.5395 | 0.5395 |

| Wisconsin | 0.0082 | 229,503 | 220,878 | 110,622 | 108,592 | 0.4820 | 0.4916 |

| Wyoming | 0.5141 | 59 | 59 | 29 | 29 | 0.4915 | 0.4915 |

| State | Margin | EoR Bravo | Athena | Athena size as a fraction | |||

| of SB Bravo size | |||||||

| Draws | Distinct Ballots | Draws | Distinct Ballots | Draws | Distinct Ballots | ||

| Alabama | 0.2875 | 122 | 122 | 94 | 94 | 0.7705 | 0.7705 |

| Alaska | 0.1677 | 396 | 396 | 295 | 295 | 0.7449 | 0.7449 |

| Arizona | 0.0378 | 7,227 | 7,217 | 5,204 | 5,199 | 0.7201 | 0.7204 |

| Arkansas | 0.2857 | 128 | 128 | 96 | 96 | 0.7500 | 0.7500 |

| California | 0.3226 | 99 | 99 | 79 | 79 | 0.7980 | 0.7980 |

| Colorado | 0.0537 | 3,687 | 3,685 | 2,676 | 2,675 | 0.7258 | 0.7259 |

| Connecticut | 0.1428 | 502 | 502 | 374 | 374 | 0.7450 | 0.7450 |

| Delaware | 0.1200 | 716 | 716 | 523 | 523 | 0.7304 | 0.7304 |

| DistrictOfColumbia | 0.9139 | 10 | 10 | 8 | 8 | 0.8000 | 0.8000 |

| Florida | 0.0124 | 65,051 | 64,827 | 46,563 | 46,449 | 0.7158 | 0.7165 |

| Georgia | 0.0532 | 3,555 | 3,554 | 2,567 | 2,567 | 0.7221 | 0.7223 |

| Hawaii | 0.3488 | 86 | 86 | 68 | 68 | 0.7907 | 0.7907 |

| Idaho | 0.3662 | 83 | 83 | 64 | 64 | 0.7711 | 0.7711 |

| Illinois | 0.1804 | 318 | 318 | 242 | 242 | 0.7610 | 0.7610 |

| Indiana | 0.2023 | 254 | 254 | 187 | 187 | 0.7362 | 0.7362 |

| Iowa | 0.1013 | 1,024 | 1,024 | 753 | 753 | 0.7354 | 0.7354 |

| Kansas | 0.2222 | 215 | 215 | 162 | 162 | 0.7535 | 0.7535 |

| Kentucky | 0.3134 | 104 | 104 | 79 | 79 | 0.7596 | 0.7596 |

| Louisiana | 0.2034 | 247 | 247 | 182 | 182 | 0.7368 | 0.7368 |

| Maine | 0.0319 | 10,238 | 10,169 | 7,358 | 7,322 | 0.7187 | 0.7200 |

| Maryland | 0.2803 | 132 | 132 | 98 | 98 | 0.7424 | 0.7424 |

| Massachusetts | 0.2930 | 122 | 122 | 93 | 93 | 0.7623 | 0.7623 |

| Michigan | 0.0024 | - | - | 1,259,688 | 1,107,933 | - | - |

| Minnesota | 0.0166 | 38,185 | 37,939 | 27,421 | 27,294 | 0.7181 | 0.7194 |

| Mississippi | 0.1818 | 302 | 302 | 224 | 224 | 0.7417 | 0.7417 |

| Missouri | 0.1964 | 267 | 267 | 201 | 201 | 0.7528 | 0.7528 |

| Montana | 0.2222 | 217 | 217 | 164 | 164 | 0.7558 | 0.7558 |

| Nebraska | 0.2710 | 144 | 144 | 110 | 110 | 0.7639 | 0.7639 |

| Nevada | 0.0259 | 15,462 | 15,357 | 11,110 | 11,056 | 0.7185 | 0.7199 |

| NewHampshire | 0.0039 | - | - | 475,357 | 351,311 | - | - |

| NewJersey | 0.1457 | 478 | 478 | 350 | 350 | 0.7322 | 0.7322 |

| NewMexico | 0.0930 | 1,276 | 1,275 | 934 | 934 | 0.7320 | 0.7325 |

| NewYork | 0.2354 | 186 | 186 | 140 | 140 | 0.7527 | 0.7527 |

| NorthCarolina | 0.0381 | 6,961 | 6,956 | 5,000 | 4,998 | 0.7183 | 0.7185 |

| NorthDakota | 0.3962 | 70 | 70 | 55 | 55 | 0.7857 | 0.7857 |

| Ohio | 0.0854 | 1,403 | 1,403 | 1,018 | 1,018 | 0.7256 | 0.7256 |

| Oklahoma | 0.3861 | 69 | 69 | 55 | 55 | 0.7971 | 0.7971 |

| Oregon | 0.1231 | 724 | 724 | 535 | 535 | 0.7390 | 0.7390 |

| Pennsylvania | 0.0075 | - | - | 127,792 | 126,477 | - | - |

| RhodeIsland | 0.1662 | 382 | 382 | 280 | 280 | 0.7330 | 0.7330 |

| SouthCarolina | 0.1492 | 460 | 460 | 344 | 344 | 0.7478 | 0.7478 |

| SouthDakota | 0.3194 | 102 | 102 | 79 | 79 | 0.7745 | 0.7745 |

| Tennessee | 0.2725 | 138 | 138 | 106 | 106 | 0.7681 | 0.7681 |

| Texas | 0.0943 | 1,150 | 1,150 | 833 | 833 | 0.7243 | 0.7243 |

| Utah | 0.2477 | 220 | 220 | 165 | 165 | 0.7500 | 0.7500 |

| Vermont | 0.3037 | 122 | 122 | 91 | 91 | 0.7459 | 0.7459 |

| Virginia | 0.0565 | 3,229 | 3,228 | 2,329 | 2,329 | 0.7213 | 0.7215 |

| Washington | 0.1757 | 355 | 355 | 265 | 265 | 0.7465 | 0.7465 |

| WestVirginia | 0.4432 | 51 | 51 | 41 | 41 | 0.8039 | 0.8039 |

| Wisconsin | 0.0082 | - | - | 110,622 | 108,592 | - | - |

| Wyoming | 0.5141 | 40 | 40 | 29 | 29 | 0.7250 | 0.7250 |

8.3 First-round Simulations

We observed that the stopping conditions ( values) for both Athena () and Minerva are identical for the Athena first round sizes presented in Table 2. This is because, for round sizes with large Minerva stopping probabilities, the value of is a very good representative of the underlying distribution, and the likelihood ratio for is larger than .

We performed simulations of Minerva for each of the round sizes and corresponding margins (except for a couple of the low margin states, Michigan and New Hampshire); the results are presented in Table 4. The simulations used the declared tallies, and hence included ballots that were not votes for the two main candidates.

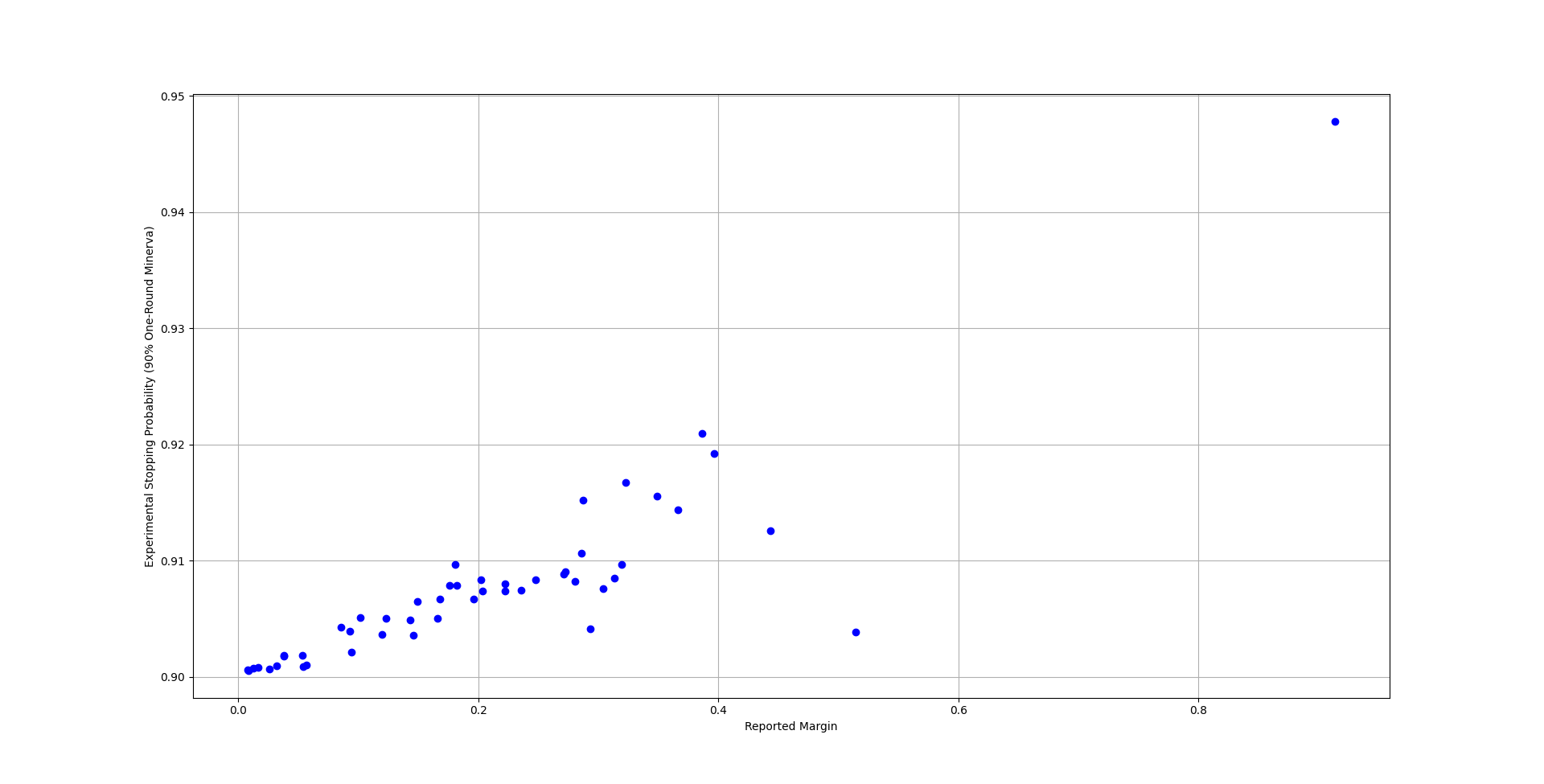

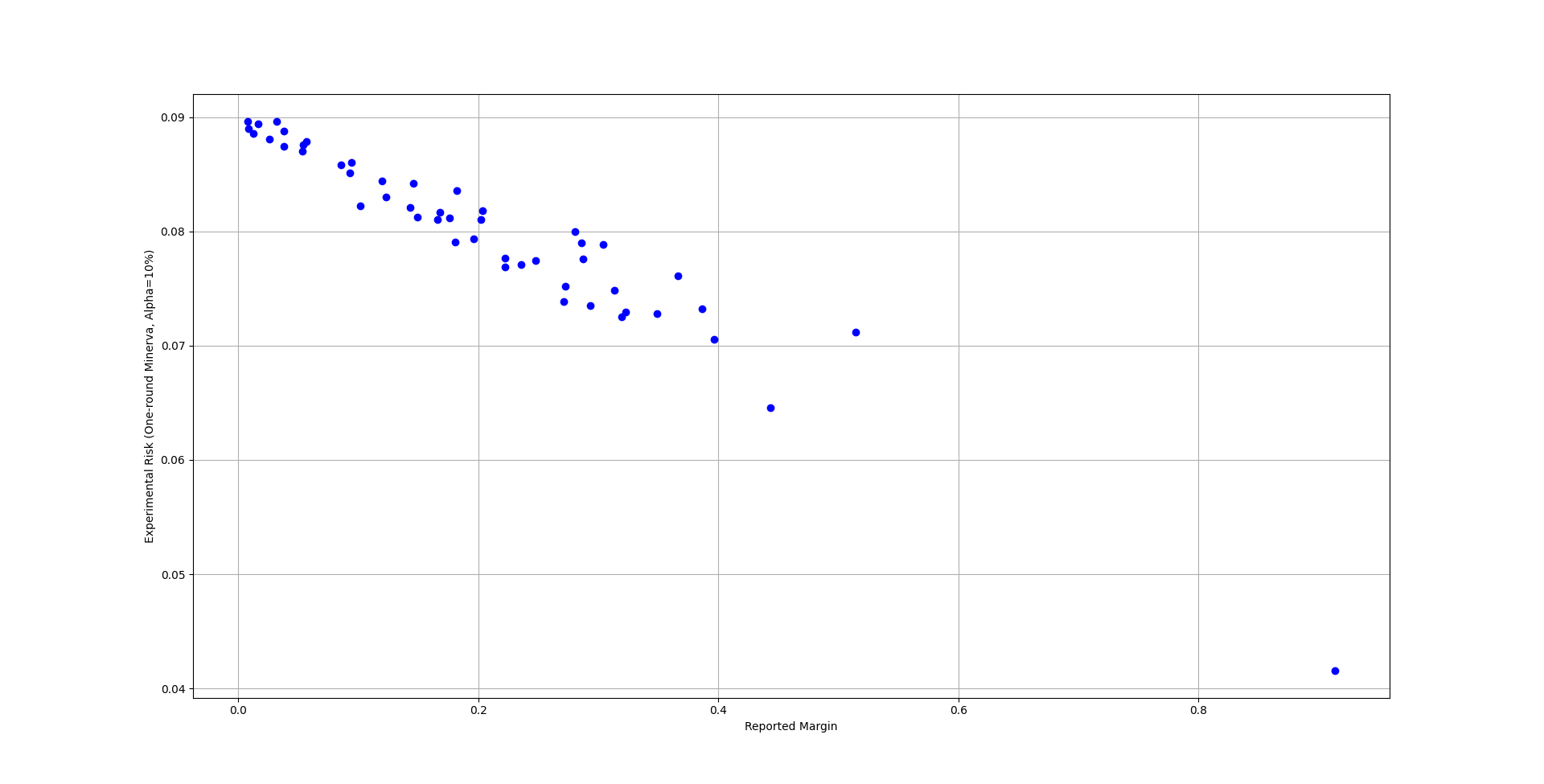

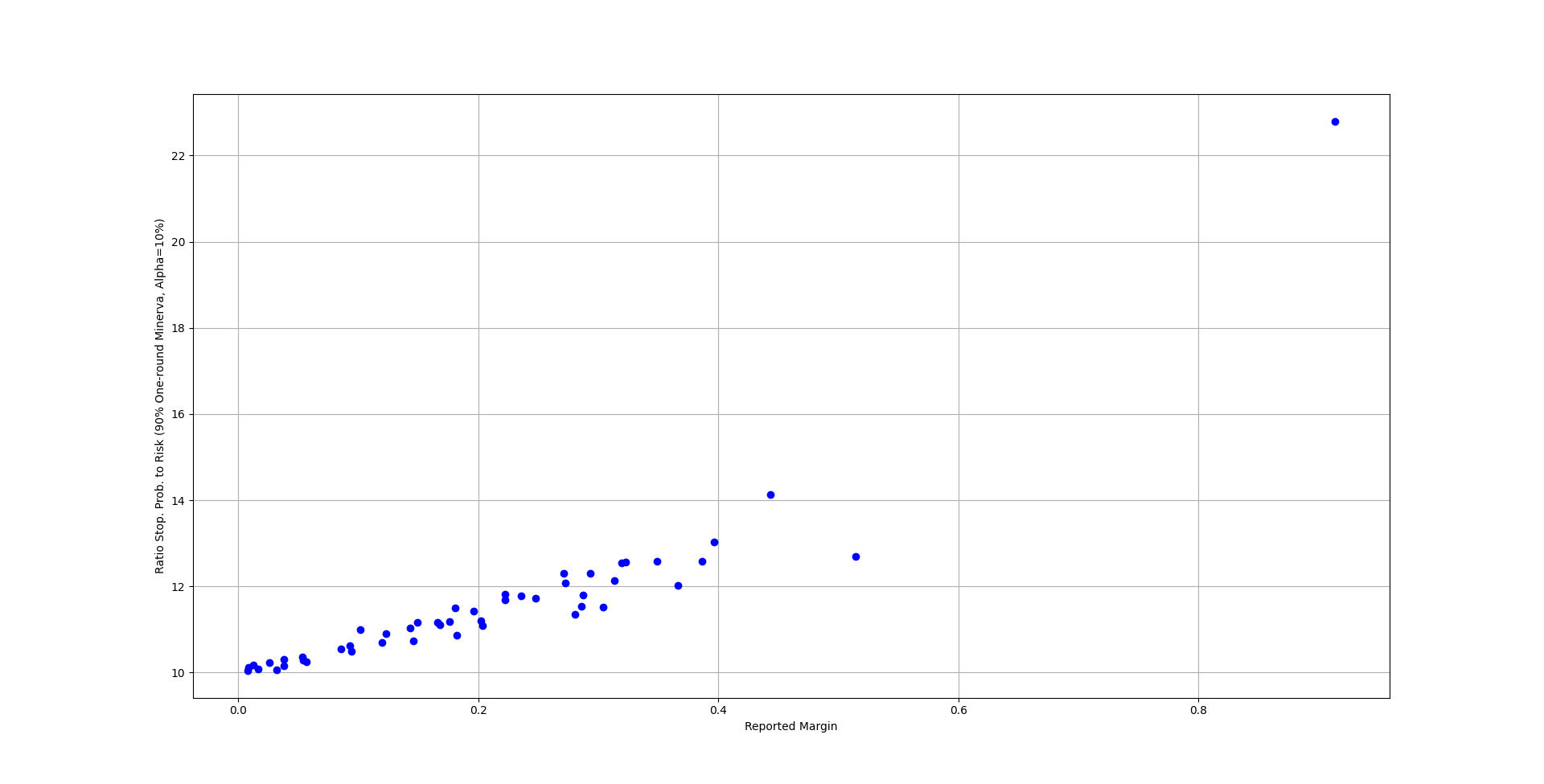

We observed that the empirical stopping probabilities for each state were slightly larger than . Additionally, we observed that the risk of the first round for each state was smaller than , and hence that the stopping probability to risk ratio was larger than , which is as required by the stopping condition for Minerva. Future work will include larger-scale and more complete simulations, as the risk-limited nature of the audit would need to be verified over multiple audit rounds.

| State | Margin | Round Risk | Round Stopping Probability |

|---|---|---|---|

| Alabama | 0.2875 | 0.0776 | 0.9152 |

| Alaska | 0.1677 | 0.0817 | 0.9067 |

| Arizona | 0.0378 | 0.0888 | 0.9019 |

| Arkansas | 0.2857 | 0.0790 | 0.9107 |

| California | 0.3226 | 0.0730 | 0.9167 |

| Colorado | 0.0537 | 0.0876 | 0.9009 |

| Connecticut | 0.1428 | 0.0821 | 0.9049 |

| Delaware | 0.1200 | 0.0844 | 0.9036 |

| District Of Columbia | 0.9139 | 0.0416 | 0.9478 |

| Florida | 0.0124 | 0.0886 | 0.9007 |

| Georgia | 0.0532 | 0.0870 | 0.9018 |

| Hawaii | 0.3488 | 0.0728 | 0.9156 |

| Idaho | 0.3662 | 0.0761 | 0.9144 |

| Illinois | 0.1804 | 0.0791 | 0.9097 |

| Indiana | 0.2023 | 0.0811 | 0.9083 |

| Iowa | 0.1013 | 0.0823 | 0.9051 |

| Kansas | 0.2222 | 0.0777 | 0.9074 |

| Kentucky | 0.3134 | 0.0748 | 0.9085 |

| Louisiana | 0.2034 | 0.0818 | 0.9074 |

| Maine | 0.0319 | 0.0896 | 0.9010 |

| Maryland | 0.2803 | 0.0800 | 0.9082 |

| Massachusetts | 0.2930 | 0.0736 | 0.9041 |

| Michigan | 0.0024 | - | - |

| Minnesota | 0.0166 | 0.0894 | 0.9008 |

| Mississippi | 0.1818 | 0.0836 | 0.9078 |

| Missouri | 0.1964 | 0.0793 | 0.9067 |

| Montana | 0.2222 | 0.0769 | 0.9080 |

| Nebraska | 0.2710 | 0.0739 | 0.9088 |

| Nevada | 0.0259 | 0.0881 | 0.9006 |

| New Hampshire | 0.0039 | - | - |

| New Jersey | 0.1457 | 0.0842 | 0.9034 |

| New Mexico | 0.0930 | 0.0852 | 0.9039 |

| New York | 0.2354 | 0.0771 | 0.9075 |

| North Carolina | 0.0381 | 0.0874 | 0.9018 |

| North Dakota | 0.3962 | 0.0705 | 0.9192 |

| Ohio | 0.0854 | 0.0858 | 0.9043 |

| Oklahoma | 0.3861 | 0.0732 | 0.9210 |

| Oregon | 0.1231 | 0.0830 | 0.9050 |

| Pennsylvania | 0.0075 | 0.0896 | 0.9006 |

| Rhode Island | 0.1662 | 0.0811 | 0.9050 |

| South Carolina | 0.1492 | 0.0813 | 0.9065 |

| South Dakota | 0.3194 | 0.0725 | 0.9097 |

| Tennessee | 0.2725 | 0.0752 | 0.9091 |

| Texas | 0.0943 | 0.0861 | 0.9021 |

| Utah | 0.2477 | 0.0774 | 0.9084 |

| Vermont | 0.3037 | 0.0788 | 0.9076 |

| Virginia | 0.0565 | 0.0879 | 0.901 |

| Washington | 0.1757 | 0.0812 | 0.9079 |

| West Virginia | 0.4432 | 0.0645 | 0.9126 |

| Wisconsin | 0.0082 | 0.089 | 0.9006 |

| Wyoming | 0.5141 | 0.0712 | 0.9039 |

Figures 10, 11 and 12 present the stopping probability, the risk and the ratio of stopping probability to risk as a function of margin for all states except DC, which has a very large margin. Larger margins have very small round sizes, and the difference of a few ballots makes greater impact. This explains the points at margins of 0.5141 (Wyoming) and 0.4432 (West Virginia).

9 Conclusion

We describe inefficiencies with the use of audits developed for ballot-by-ballot decisions in round-to-round procedures, such as are in use in real audits today. We propose new audits, Minerva and Athena, which we prove are risk-limiting and at least as efficient as audits that apply the ballot-by-ballot decision rules at the end of the round.

We describe an approach to computing stopping probabilities and risks of audits with stopping conditions that are monotone increasing with the number of ballots for the winner in the sample. We demonstrate its accuracy in reproducing the empirically-obtained percentile values from [5, Table 1], and find that the average fractional discrepancy is .

We predict first round sizes (for 90% stopping probability) for all states in the US Presidential election of 2016 for end-of-round Bravo and Athena (). We find that our proposed audits require half the ballots across all margins. We similarly compare first round sizes to ordered-ballot-draw Bravo as well, finding improvements, with the larger improvements corresponding to smaller margins. We thus see that the additional effort of retaining information on ballot order, required by selection-ordered-ballots Bravo, is not beneficial as the Athena class of audits does not require it.

We hope to present a third audit of the Athena class, Metis, which is more efficient for multiple-round audits, in a future draft of this manuscript.

Large first-round sizes for polling audits of low margin contests should not deter election officials from performing audits. Other options exist besides those reported in Section 8, which presents results for ballot polling audits only. Ballot comparison audits are far more efficient in terms of number of ballots needed for the audit; if cast vote records (CVRs) which can be efficiently matched with the corresponding paper ballot are easily available, or their creation requires less effort than the random sampling of a large number of ballots, they should be considered, especially for low margin contests. It might also be possible to perform a combination of ballot polling audits and ballot comparison audits—such as described by Ottoboni et al. in the paper on SUITE [8]—to reduce effort.

We provide open-source software for computing probability distributions and for the Minerva and Athena audits, hoping it can help developers of election auditing software. We also hope our work can help election officials planning audits.

References

- [1] L. D. Fisher. Self-designing clinical trials. Statistics in medicine, 17(14):1551–1562, 1998.

- [2] B. K. Ghosh and P. K. Sen. Handbook of sequential analysis. CRC Press, 1991.

- [3] N. A. Heard and P. Rubin-Delanchy. Choosing between methods of combining-values. Biometrika, 105(1):239–246, 2018.

- [4] M. Lindeman and P. B. Stark. A gentle introduction to risk-limiting audits. IEEE Security & Privacy, 10(5):42–49, 2012.

- [5] M. Lindeman, P. B. Stark, and V. S. Yates. BRAVO: Ballot-polling risk-limiting audits to verify outcomes. In EVT/WOTE, 2012.

- [6] S. Morin and G. McClearn. The R2B2 (Round-by-Round, Ballot-by-Ballot) library, https://github.com/gwexploratoryaudits/r2b2.

- [7] S. Morin, G. McClearn, N. McBurnett, P. Vora, and F. Zagorski. A note on risk-limiting Bayesian polling audits for two-candidate elections. In Voting, 2020.

- [8] K. Ottoboni, P. B. Stark, M. Lindeman, and N. McBurnett. Risk-limiting audits by stratified union-intersection tests of elections (SUITE). In E-Vote-ID 2018, pages 174–188, 2018.

- [9] R. L. Rivest. Clipaudit—a simple post-election risk-limiting audit. arXiv:1701.08312.

- [10] R. L. Rivest and E. Shen. A Bayesian method for auditing elections. In EVT/WOTE, 2012.

- [11] P. B. Stark. Conservative statistical post-election audits. Ann. Appl. Stat., 2(2):550–581, 06 2008.

- [12] H. L. Van Trees. Detection, Estimation and Modulation Theory, Part I. John Wiley and Sons, 1968.

- [13] P. L. Vora. brla_explore, https://github.com/gwexploratoryaudits/brla_explore.

- [14] P. L. Vora. Risk-limiting Bayesian polling audits for two candidate elections. CoRR, abs/1902.00999, 2019.

- [15] A. Wald. Sequential tests of statistical hypotheses. The Annals of Mathematical Statistics, 16(2):117–186, 1945.

- [16] G. Wassmer. Basic concepts of group sequential and adaptive group sequential test procedures. Statistical Papers, 41(3):253–279, 2000.

- [17] F. Zagórski. Athena - risk limiting audit (round-by-round), https://github.com/filipzz/athena.

Appendix A Proofs

A.1 Preliminaries

Before we prove the Theorems, we need the following general results from basic algebra.

Lemma 2.

Given a monotone increasing sequence: , for , the sequence:

is also monotone increasing.

Proof.

Note that is a weighted average of the values of for :

Observe that, because is monotone increasing,

with equality if and only if . Suppose . Then:

And is also monotone increasing. ∎

Lemma 3.

Given a strictly monotone increasing sequence: and some constant ,

Proof.

Let be the first index for which the sequence exceeds or equals . That is, let be such that

Because the sequence is monotone increasing,

If no elements in the sequence exceed or equal , let . ∎

Lemma 4.

Given , with , is strictly monotone increasing as a function of .

Proof.

Let . Then:

Hence

∎

A.2 Proofs of properties of the complementary cdf ratios

Theorem 1.

For the -Minerva test, if the round schedule is pre-determined (before the audit begins), the following are true for

-

1.

when and are defined and non-zero.

-

2.

is strictly monotone increasing as a function of .

-

3.

such that

Proof.

We show this by induction.

Consider .

-

1.

-

2.

where is the largest possible value for . Note that .

- 3.

Thus the theorem is true for .

Suppose the theorem is true for . We will show it is true for .

From property (3) of this theorem for , we observe that, after the stopping decision is made and before the next round is drawn, the number of winner ballots in the sample is strictly smaller than . The distribution on the winner votes may be modeled as and where:

and

When we draw the next round of ballots with replacement, the resulting distributions on the winner ballots are convolutions:

and

where represents the convolution operator and the probability of drawing ballots for the winner in a sample of size from a distribution with fractional tally for the winner. Using property (1) of this theorem for , we see that

and

for some , a function of , current and previous round sizes, and .

Some book keeping demonstrates that

where

And

which proves property (1) for . Properties (2) and (3) follow for by application of Lemmas 2-4.

Thus the theorem is true for all .

∎

Theorem 2.

For the -Athena test, if the round schedule is pre-determined (before the audit begins), the following are true for :

-

1.

when and are defined and non-zero.

-

2.

is strictly monotone increasing.

-

3.

such that

Proof.

The proof proceeds exactly as that for Theorem 1, except that there are two stopping conditions, which may be represented as:

and

Hence

∎

A.3 Proof of risk-limiting property of Minerva

Theorem 3.

-Minerva is an -RLA if the round schedule is pre-determined (before the audit begins).

A.4 Properties of B2 versions of Minerva and Athena

Theorem 5.

The B2 -Bravo audit stops for a sample of size with ballots for the winner, if and only if the -Minerva audit stops.

Proof.

Consider the round of the Minerva audit: the ballot draw. Suppose that, before the round is drawn, and after the stopping condition is tested for the round and the audit stopped if it is satisfied, is the largest value of winner ballots possible. It is strictly smaller than the corresponding , because the audit has stopped for all other values. Further, because at most one winner ballot will be drawn in the round, the largest possible number of winner ballots in the round is .

More formally, let the largest value of for which be , where is as defined in the proof of Theorem 1. Then

by the definition of , Theorem 1. Further, the largest value of for which is .

We now show that if the round stops at all, it will be for and no other values of .

We observe that the only way to obtain ballots in the round is if the existing number of winner ballots is and the new ballot drawn is for the winner. The probability is:

On the other hand, ballots arise in the round if the existing number is and a winner ballot is drawn, or the existing number is and the ballot drawn is not for the winner.

Similarly:

and

If the condition is satisfied by values other than , because is monotone increasing, it is satisfied by :

Thus is a weighted average of and and:

as . And hence, does not pass the stopping condition.

Thus, if and denote the B2 Minerva and B2 Bravo audits respectively,

Samples that do satisfy the stopping condition have the same Minerva and Bravo p-values, which are otherwise not the same. ∎

Corollary 1.

Given such that , the B2 -Bravo audit stops for a sample of size with ballots for the winner, if and only if the -Athena audit stops.

Proof.

As in Theorem 5, the audit round stops only for the largest possible number of winner votes if it does at all. Thus, it stops if and only if it satisfies the -Bravo stopping condition. Additionally, the second stopping condition for Athena is also a Bravo condition, and is always satisfied when the first one is satisfied because . ∎

A.5 Proof of efficiency property of Minerva and Athena

Theorem 6.

Given sample of size with samples for the winner,

where denotes the -Bravo test and the -Minerva test or the

-Athena test for if the round schedule is pre-determined (before the audit begins).

Proof.

Note that for a fixed election and fixed round sizes, each of and , the complementary cdf stopping conditions for Minerva and Athena respectively, is a weighted sum of , the monotone increasing Bravo stopping condition. Further, if is the number of winner ballots, the elements in the weighted sum are at least as large as . In fact, equality for occurs only when is the largest possible number of winner ballots in the round. Thus

Note that Athena has a second condition, which is also satisfied

∎