Induced optimal partition invariancy in linear optimization: constraints perturbation

Abstract

In this paper, we study uni-parametric linear optimization problems, in which simultaneously the right-hand-side and the left-hand-side of constraints are linearly perturbed with identical parameter. In addition to the concept of change point, the induced optimal partition is introduced, and its relation to the well-known optimal partition is investigated. Further, the concept of free variables in each invariancy intervals is described. A modified generalized computational method is provided with the capability of identifying the intervals for the parameter value where induced optimal partitions are invariant. The behavior of the optimal value function is described in its domain. Some concrete examples depict the results. We further implement the methodology on some test problems to observe its behavior on large scale problems.

Keyword: Uni-parameter linear optimization; Change point; Induced partition invariancy analysis; Moore-Penrose inverse; Realization theory

MSC 2000: 90c05,90c31

1 Introduction

Existence of inaccuracy and variation in parameters of an optimization problem are indispensable, and investigation of their effects has attracted the primary concern of many researchers. Deviation from a predetermined optimal solution would be an implication of such variation. Consequently, the current solution fails to be optimal or feasible, and additional burden of problem-solving for other values of parameters is imposed. Parametric programming has denoted its competence in this situation which economically identifies the exact mapping of the optimal solution in the space of parameters; unnecessary many problems solving is avoided, and the optimal solution can be accordingly adjusted.

To be specific, consider the primal linear program

and its dual as

where , and are fixed data; and and are unknown vectors. Usually, vectors and are referred to as rim data. Assume that these problems are feasible, and denote their feasible solution sets by and , respectively. A primal feasible solution and a dual feasible solution are optimal solutions if they satisfy the well-known complementary condition . Optimal solution sets of these problems are denoted by and , correspondingly.

Consider the index set Let be a set of indices in this identifying a nonsingular submatrix from the columns of , and . The vector is called a primal basic feasible solution where , and . A dual basic feasible solution is identified as and . Recall that a basic optimal solution specifies a partition of the index set, known as basic optimal partition.

A primal-dual optimal solution is strictly complementary when By the Goldman-Tucker’s theorem [10], the existence of a strictly complementary solution is guaranteed if both Problems and are feasible. Interior point methods start from a solution and terminate at a strictly complementary optimal solution [15]. Having a primal-dual strictly complementary optimal solution, the index set is partitioned as

| ^* }. |

This partition is denoted by , and known as optimal partition. It is identical with the basic optimal partition only if the primal and dual optimal solutions are nondegenerate.

We consider the following uni-parametric linear optimization problem

where is a parameter, and are perturbing directions with no specific restriction on and .

In uni-parametric programming, it is assumed that the data are perturbed along a direction according to the parameter. The aim is to identify the region for the parameter value, where specific properties of the current optimal solution do not alter. For example, if the current optimal solution is basic, one might be interested in identifying the region at which the known optimal basis is invariant for every parameter values in this region. On the other hand, when the solution is strictly complementary, the aim could be the specifying of a region at which the known optimal partition is invariant for every parameter value in this region. We characterize conditions that guarantee the convexity of these regions. Recall that degeneracy of a primal or dual basic solution leads to having multiple dual or primal optimal solutions. Therefore, the basic optimal partition may not be unique in general. In spite, the convexity of optimal solution sets implies the uniqueness of the optimal partition.

We recall that the Problem has been studied when the basic optimal partition is known. The case when either or is zero, also studied. In this paper, we investigate the behavior of Problem when the optimal partition is known, and identify the regions where the given optimal partition is invariant. To do this end, we have to define the notion of induced optimal partition. Despite the optimal partition, which defines transition points, induced optimal partition suggests other points; here, we refer to as change points. These two types of points lead to determine the regions as intervals.

A computational algorithm is provided for finding all potential such intervals. Furthermore, the representation of the optimal value function is presented, and the results are clarified using some concrete examples. The methodology is also implemented on some test problems to investigate the efficiency of the algorithm and to observe computational challenges.

The rest of paper is organized as follows. Section 2 is devoted to reviewing the so-far-existing results of linear parametric programming in a nutshell. In Section 3, in addition to expression the admissibility of a direction of we review some other necessary concepts as optimal partition invariancy on Problem pseudo-inverse, and realization theory. In Section 4, the concept of optimal partition invariancy on principal problem is generalized to the Problem . The notion of change point is defined and distinguished from the transition point. Its economical interpretation is highlighted via a simple example. In Section 5, a generalized explicit formula is presented that identifies a closed form of the optimal value function on each invariancy interval. The process of finding all transition points, change points, and invariancy intervals are provided in Section 6. Some concrete examples illustrate the results in Section 7, and the methodology is also implemented on some test problems. The final section contains some concluding remarks.

2 Literature Review

Let us first review some findings in parametric linear programming. In a parametric linear optimization when right-hand-side is perturbed, it is proved that the invariancy regions are open intervals if they are not a singleton. Moreover, the optimal value function is a continuous piecewise linear over these intervals [15], and therefore, these intervals may be referred to as linearity intervals. Singleton regions are referred to as break points since optimal value function does not have a continuous derivative at these points.

Perturbation at the left-hand-side alongside a direction with arbitrary rank has been studied to find basic invariancy intervals[7]. The author studied properties of the optimal value function and the associated optimal basic feasible solution in a neighborhood about a fixed parameter value. Computable formulas for the Taylor series’ (and hence all derivatives) of the optimal value function were provided, as well as for the primal and dual optimal basic solutions as functions of the parameter. It also identifies the parameter values where the optimal value function is differentiable in the case of degeneracy.

In another study, the author considered the same problem and could present a closed form of the optimal value function as a fractional function of the parameter in the optimal basic invariancy interval [16]. It was denoted that the optimal value function is piecewise fractional in terms of the parameter. In another study, a solution algorithm has presented for a linear program with inequality constraints and a single parameter at their left-hand-side [14]. This algorithm includes inversion techniques of perturbed matrices, which accompanies with some computational complexities. The case when the problem is in the canonical form, a primal-dual strictly complementary optimal solution is in hand, and perturbing direction is of rank one, has been studied in [11].

Recently an algorithm has been introduced for the exact solution of multi-parametric linear programming problems with inequality constraints [6]. The perturbation occurs simultaneously on the objective function’s coefficients, the right-hand-side, and the left-hand-side of the constraints. This algorithm is based on the principles of symbolic manipulation and semi-algebraic geometry, and critical regions are identified by semi-algebraic geometry. From the critical region, the authors meant the region where active constraint sets are invariant. , It is shown that these regions are neither necessarily convex nor connected. The entire parametric space is explored implicitly within the algorithm, while there is no necessity for determining the inverse of parametric matrices. It was shown that the objective function is fractional on critical regions. Though their considered problem can be reduced to their assumption on the invariancy of the active set of constraints necessitate having an optimal basic solution. Moreover, their approach is highly dependent on mathematical software, which may increase the complexity of computation. As the author acknowledged, their methodology is not efficient for large-scale problems.

In another study, the case when is of arbitrary rank, and the problem is in standard form with known optimal partition, has been investigated [8]. Their method was an adaptation of the proposed approach in [16]. The authors presented a computational procedure for finding all intervals, and the representation of the optimal value function on these intervals. They further investigated some properties of the optimal value function. Let us call the considered problem in [8] as the principal parametric linear program which, in our notation, is

Its dual is

Let and denote the optimal solution sets of and , respectively.

The main results deserve to mention are as follows. Despite the case when only rim data is perturbed, that the domain of the optimal value function is closed [9, 15], this domain might be open when is perturbed. Further, there is no clear relation between optimal partitions at a breakpoint and at its potential neighboring intervals despite the perturbation at rim data [13]. Moreover, the invariancy region might not be convex unless with some conditions[11]. The last, unlike rim variation, the set of admissible changes (See page 3.1) corresponding to Problem is not a convex set [11].

3 Preliminaries

In this section, some necessary preliminary concepts and assumptions for the convexity of the invariancy region are posed, and optimal partition invariancy is reviewed in our literature. It follows by the concept of Moore-Penrose inverse and finalizes with some facts from realization theory.

3.1 Convexity of the invariancy region

In the following subsection, we consider some assumptions that guarantee the convexity of the invariancy region for the problem Observe that the dual of this problem is

Here runs throughout a nonempty subset , where Problem has an optimal solution for every parameter value . This set is nonempty since it is assumed that Problems and are feasible at . In general, is not a convex set, and to guarantee its convexity, we have to make some assumptions. First, let denote a perturbing direction referred to as change direction. For a , is said an admissible change if Problem has an optimal solution, or equivalently

There are some instances at which, is not an admissible change for all , just because is an admissible change. A change direction is an admissible direction if there exists , such that is an admissible change for all Let us denote the set of all admissible directions by . For an admissible direction , let and Analogous to [11], it can be proved that if , and each is a polyhedron containing the origin, then is simply an interval. In this study, we assume that these conditions are fulfilled.

3.2 Optimal partition invariancy

Let us quote the notion of optimal partition from [8], and clarify its relationship with the optimal partition defined in Page 1. Let

| (2) |

be injective and strictly increasing functions, where , and . Further, let

be a map where and . Let such that is a strictly complementary optimal solution of Problems and with the optimal partition , where

Moreover, let be a set of parameters such that for each , the principal Problem has an optimal solution with the optimal partition . Clearly, any strictly complementary optimal solution corresponding to an arbitrary implies and . Furthermore, when the following three properties hold for

- Property 1.

-

has a pseudo-inverse,

- Property 2.

-

,

- Property 3.

-

(or equivalently ),

then is a strictly complementary optimal solution of Problems and with optimal partition . Recall that the aim of optimal partition invariancy is to find the region , where for every , optimal partition of the associated problem is . This is equivalent to establishment of Properties 1-3 for such a parameter .

3.3 Moore-Penrose inverse

There exists a unique matrix for a real matrix , is known as Moore-Penrose inverse (or simply pseudo-inverse) and denoted by , that satisfies the following equations.

| (3) | |||||

| (4) | |||||

| (5) | |||||

| (6) |

where denotes the conjugate transpose of matrix . In general, is not necessarily an identity matrix, while it maps all column vectors of to themselves, and . A matrix satisfying (3) and (4) is known as a generalized inverse. It always exists but is not usually unique unless Conditions (5) and (6) hold, too. Observe that if a matrix is nonsingular, the pseudo-inverse and the inverse coincide. For more details, one can refer to [3].

Let be an index set of nonsingular submatrices of with . It was proved [2] that the pseudo-inverse is a convex combination of ordinary inverses , as

where denotes that padded with the right number of zeros in the right places, and

The volume of , denoted by , is defined as 0 if and

otherwise [2]. Let be a subvector of with indices in . The Euclidean norm least squares solution of the linear system is a convex combination of basic solutions , i.e.,

| (7) |

The representation (7) follows easily for of full column rank [4]. When is a matrix of full row rank, a solution is in the row space of i.e., .

3.4 Realization theory

Here, the realization theory for scalar rational functions is reviewed. More details for matrix-valued and operator-valued functions can be found in [1]. A fundamental observation in realization is that, when and then is a rational function and can be described completely in terms of eigenvalues of two matrices and as

where is an identity matrix. More explicitly, let be eigenvalues of and be eigenvalues of , counted according to their multiplicities. Then

| (8) |

The number , i.e., the factors in numerator and denominator, on the right-hand-side of (8) is minimal when and do not have common eigenvalues.

4 New concepts and main results

In this section, we present our approach for finding the invariancy interval of Problem The first step is to convert this problem to the one with only perturbation in the left-hand-side of the constraints.

Recall that two problems are equivalent if they contribute similar features, and a solution of one can be immediately identified by the other’s, while they may have different numbers of variables and constraints [5]. Let us rewrite as

Considering as a constraint, leads to a problem in which only the coefficient matrix is perturbed with as

with

where is an identity matrix, zeros are matrices of appropriate sizes, , and . The optimal value function of this problem is denoted by . The dual of is

Suppose and , respectively denote optimal solution sets of and Further, let as the support set of an arbitrary vector . Let where zero is a row vector with dimension and . We define the partition as with

and with

It can be easily understood that in this partition is the same as in the optimal partition extracted from a strictly complementary optimal solution of Problems and at . Moreover, considering the equivalence of two Problems and an optimal solution can be induced by an optimal solution of Problem and vice versa. Therefore, we refer to such an optimal solution for as induced optimal solution, and the corresponding partition as induced optimal partition. Note that, an induced optimal solution is an induced strictly complementary solution when for all and for and are not simultaneously zero.

In the sequel, we assume that is the known optimal partition of Problems and at , and is the induced optimal partition of Problems and Let and Obviously, and . Let us adapt the notations and concepts of the principal Problem to the Problem . Let

be injective and strictly increasing functions with . Analogously, define

It can be easily observed that and Moreover, when is empty then i.e., In this case,

On the other hand, for ,

Further, for the induced optimal solution of Problem , it holds

The following theorem states necessary and sufficient conditions for an optimal solution of being an induced optimal solution.

Theorem 1.

Let and Then, is an induced strictly complementary optimal solution of and if and only if

-

Cond. 1. has pseudo-inverse,

-

Cond. 2. For , is positive when , negative when , and zero otherwise,

-

Cond. 3. and zero otherwise.

Proof.

Observe that satisfaction of Cond. 1 is necessary to others, since the pseudo-inverse of appears in them. Moreover, Cond.s 2 and 3, respectively, are the strictly feasibility conditions of the solution for Problems and Since for , the dual feasibility condition of only associates to those variables with indices in , , it suffices to consider the indices of instead of . Recall that corresponds to the positive variables in Problem where . Respecting the concept of induced optimal solution and strictly feasibility of primal and dual problems, validity of the statement is immediate. ∎

Now, having the induced optimal partition , for a given the aim of induced optimal partition invariancy is to find the region , where for all , the induced optimal partition of the associated problem is identical with . Recall that this invariancy region contains all such ’s at which Cond.s 1-3 in Theorem 1 hold.

Let us define the notion of change point to distinguish it from the transition point. Due to the assumption that is an admissible direction (See page 3.1), the induced optimal partition invariancy region, is an interval. At the endpoints of this interval, induced optimal partitions are changed provided that the Problem is feasible and has optimal solutions at these points. Otherwise, there is no induced optimal partition at these points. Variation of induced partition means that some indices interchange between and when the parameter is replaced by one of the endpoints of the interval. More clearly, this transition may happen between and , or between , and In the first case, the point is referred to as a transition point, and in the second case, it is called a change point . Note that when a parameter value is a change point only, indices of free variable interchange between their index sets only. Since they are absent in the objective function , this variation does not affect its representation. Therefore, at a transition point, the representation of the optimal value function changes, and it fails to have the first derivative. The representation of the optimal value function on the neighborhoods of the change point does not change when it is not a transition point, simultaneously.

Let us illustrate the importance of a change point in practice via a simple example. Consider manufacturing of products, using sources, and denotes the amount of available value of source A unit of product needs amount of the source For instance, let is the available machine time in this production plan, and is the time necessary to produce one unit of item . Therefore, the corresponding constraint could be as

where is the production level of . Without loss of generality, one may assume that variation in production time affects its quality. Thus, positive as the increase in the production time of increases the quality of this product and vice versa. This variation may necessitate a change on , but this is not the only reason. Consequently, the corresponding parametric form of this constraint is

where is an slack variable. Equivalently,

where could be considered as the degree of quality. Without loss of generality, let be a change point of the corresponding linear optimization problem. This means that for Further, let for some and for some This means that increasing (decreasing) of the quality degree implies in growth (decline) of Here, is the difference between the available variation in corresponding total production time and the necessary time to change the quality of products. More clearly, the amount of variation in total production time for the current quality, equals to the variation of production time of every product at an optimal production plan. Increasing of the quality implies in slack in total considered extra time versus the necessary time in an optimal solution at (i.e. ). On the other hand, decreasing the quality leaves some spare time from that is more than the reduced available time (i.e. ). This information would guide the manager to adjust the production plan efficiency.

4.1 Identifying an induced invariancy interval

Note that Cond.s 1-3 in Theorem 1 quids us to derive some computational tools that lead to identifying an induced invariancy interval. Realization theory helps us to translate Property 1-3 for Problem to computational forms in terms of eigenvalues of some matrices. In the sequel, these conditions are translated in terms of eigenvalues of specific matrices.

Consider Properties 1-3 (See Page 3.2). For the principal Problem with optimal partition at the approach in [8] needs to calculate To determine this matrix, we consider three possibilities. First let with as defined in (2). In this case then

| (9) |

When then and therefore

| (10) |

Finally for has full row and full column ranks and Moore-Penrose inverse is reduced to the standard inverse, i.e., then

| (11) |

Note that applying (9) or (10) leads to identical nonzero eigenvalues of some matrices we need in our procedure. More clearly, using (9) leads to identify eigenvalues of multiplication of two matrices, say while using (10) needs to do the same for Observe that for two matrices and with appropriate sizes, nonzero eigenvalues of and are identical, and the extra ones are zero.Therefore, depending on the size of and more-cost-effective calculation suggests to apply the one with less dimension. In our problem in question, in the principal problem is replaced by and by Thus without loss or generality, we assume that and construct our methodology based on (9).

The following theorem provides an inequality, which is identical to Cond. 1, the existence of the pseudo-inverse of .

Theorem 2.

For a given , let correspond to the induced optimal partition of Problem Then, for all with , has pseudo-inverse if and only if

| (12) |

where the nonzero values of are nonzero eigenvalues of

Proof.

For and considering (9), we have

Since exists, then exists if and only if

| (13) |

where for a square matrix , denotes the resolvent set of consisting of those complex numbers for which is invertible [8]. Thus, (13) is identical to (12) where the nonzero values of are nonzero eigenvalues of The proof is complete. ∎

Remark 1.

Recall that for the size of is greater than the size of Thus, it is more cost-effective to consider as the eigenvalues of

Corollary 1.

The following theorem translates Cond. 2 in terms of eigenvalues of some further specific matrices.

Theorem 3.

Let correspond to the induced optimal partition of Problems and Then, for , and is identical with

| (14) |

When is identical with

| (15) |

where nonzero values of are nonzero eigenvalues of the matrix and are nonzero eigenvalues of

Proof.

We prove (14), the proof of (15) goes similarly, and we omit it. For and the inequality holds if and only if when and when Using (9), we have

| (16) |

Based on the realization theory and considering

Eq. (16) can be converted to

where the nonzero values of are nonzero eigenvalues of and are nonzero eigenvalues of This completes the proof. ∎

Remark 2.

In addition to Remark 1, observe that for the size of is greater than the size of Thus, one has better to consider as the eigenvalues of .

Analogous to Theorem 3, next theorem translates Cond. 3 in terms of eigenvalues of some other specific matrices. Recall that in this theorem functions and are defined as (2) for Problem .

Theorem 4.

Let be the induced optimal partition of Problems and . For the inequality is translated as

where the nonzero values of and are nonzero eigenvalues of the matrices and respectively.

Proof.

Consider the dual constraints of as

Observe that the vector in is of dimension and Thus, is identical with Further, is the feasibility of which is identical with the optimality of Thus, one can replace with in Cond. 3. On the other hand, and denote the sets of indices in respectively corresponding to positive and zero variables of . Thus, can be rewritten as

for . Equivalently, as

| (17) |

Considering (9) and realization theory, (17) can be reworded as

where and are as stated. The proof is complete. ∎

Remark 3.

For , one has better to consider and as the eigenvalues of and , respectively.

5 Closed form of the optimal value function

Without loss of generality, let In the sequel, the representation of the optimal value function is derived.

Theorem 5.

Let Cond.s 1-3 satisfy for a fixed . The representation of the optimal value function is

| (18) |

where the nonzero values are nonzero eigenvalues of the matrix and nonzero values of are nonzero eigenvalues of the matrix .

Proof.

Corollary 2.

In the spacial case , the closed form of the optimal value function is

where are eigenvalues of and are eigenvalues of

6 Finding all transition and change points

The following computational algorithm is devised to find all transition and change points of Problem in . All induced invariancy intervals are identified by these points. The inputs of this algorithm is the perturbing direction in addition to the fixed data and After finding a transition point or a change point, the algorithm needs to select a point in the next immediate right invariancy interval as close as possible to the aforementioned identified point. This selection could be carried out by adding to the identified transition or change point. The output of this algorithm is the point and while it is expected that These points are transition or change points when the associated problems in these points have optimal solutions. Distinguishing between transition points and change points can be carried out using the induced optimal partitions at their immediate adjacent intervals. The algorithm consists of the following steps.

- Step 0:

-

Let .

- Step 1:

-

Solve Problems and and identify and , respectively. If is infeasible or unbounded then stop. is a transition or change point

- Step 2:

-

If then is a transition or change point.Let let

- Step 3:

- Step 4:

-

If stop, otherwise solve If this problem is unbounded or infeasible, stop. Otherwise, identify Set

- Step 5:

-

Solve Problem . If this problem is infeasible or unbounded, then stop. Otherwise, identify and go to Step 3.

Remark 5.

To find the induced optimal invariancy intervals and transition or change points to the left of , one can replace and substitutes with in Steps 2 and 4 of the algorithm. This algorithm terminates in a finite number of iterations since the number of induced optimal partitions is finite.

7 Illustrative Examples

In this section, two concrete examples are designed to clarify the approach. In these examples, we set . The first example is an instance that includes a point which is both transition and change point.

Example 1.

Consider the following problem

where is the parameter. This problem can be rewritten as

By considering this problem is equivalent with

| (19) |

in which only the coefficient matrix is perturbed. To be clear

In the first iteration of the algorithm, when and , implementation of Step 1 reveals the induced primal-dual optimal solution of Problem (19) as

Corresponding induced optimal partitions are

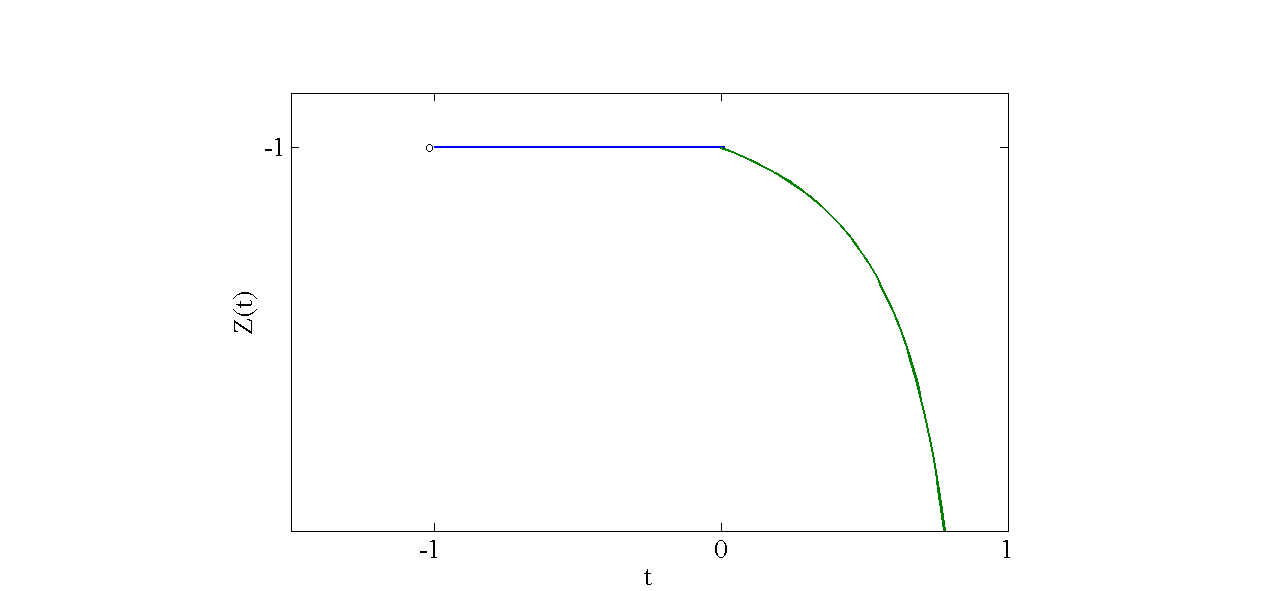

By Step 2, is as a transition or change point. From Step 3, the corresponding invariancy interval containing , is , and Since Problem (19) at this point is unbounded, the algorithm is terminated at step 4.

This algorithm can be applied to find the invariancy intervals to the left of . The immediate right invariancy interval is (-1,0), while Problem (19) at is unbounded.

The results are reported in Table 1 which includes the induced optimal partition invariancy intervals and corresponding induced optimal partitions. Representation of the optimal value function on these intervals are identified using (18) and appeared at the last column. Fig. 1 depicts the optimal value function on these intervals.

As reflected in Table 1, domain of the optimal value function is the open interval It is continuous at point , but fails to be continuous or even defined at the end points. Observe that when one passes from to each neighboring interval, an index from moves to Thus is a transition point. Further, moving from the interval to 0, not only and exchanges the index 2, but also and exchanges the index 4. Thus is a change point, too.

The following example contains a change point where in its neighborhoods, the representation of the optimal value function dose not change.

Example 2.

Assume the following problem

where is the parameter. One can rewrite this problem as

Substitution of and results to

To be clear

Table 2 has a summary of the results and Fig. 2 denotes the corresponding optimal value function. As this table shows, is simultaneously transition and change point, while and are only transition points. The optimal value function is continuous on them but not differentiable. The point is a change point, and the optimal value function is continuous and differentiable at this point. The domain of the optimal value function is the closed interval in this example. Here, explicitly, at the indices interchange between and and the index interchanges between and At the indices interchange only between and Approaching from the left to the index 5 moves from to and passing from this point it moves to As can be seen in the neighborhood of this point, the representation of the optimal value function does not alter. This is a visible display of the difference between a mere transition point and a mere change point.

7.1 Computational results

In the sequel, the results of executing the methodology on some test problems from Netlib are reported. They are in standard form, and their characteristics are reflected in Table 3.

| Name | Rows | Columns |

|---|---|---|

| Afiro | 27 | 51 |

| Blend | 74 | 114 |

| Stocfor1 | 117 | 165 |

| Scagr7 | 129 | 185 |

Computations are carried out on Asus FX570UD - FY213, Intel core i7-8550u with 12GB Ram with platform Windows 10 Enterprise. The algorithm has been implemented in MATLAB R2019b using some main standard commands as linprog with the option ’interior-point-legacy’, eig, pinv. We used standard commands as infsup, in0, intersect, of version 11 of the interval arithmetic toolbox, INTLAB, for interval computations.

In each parametric Problem , elements of are randomly selected and their values are produced by the pseduorandom normal codes of the Matlab. Further, each element of is produced by the uniform distribution from interval . Computational results with are reported in Table 4.

| Convex section | No. of detected Ind. | CPU time (Sec.) | |||||||

| Inv. | Trans. | Chang. | |||||||

| Problem | of | Int. | Points | Points | Both | Min | Mean | Max | Total |

| 0.013 | 0.016 | 0.021 | |||||||

| Afiro | (-3.136, 59.944) | 44 | 29 | 3 | 11 | 0.240 | 0.585 | 0.829 | 4151 |

| 37.205 | 64.131 | 92.316 | |||||||

| 18.762 | 29.608 | 36.888 | |||||||

| 0.351 | 0.376 | 0.545 | |||||||

| Blend | (-0.060,2.092] | 34 | 30 | 3 | 0 | 1.084 | 1.384 | 2.665 | 18935 |

| 287.569 | 428.632 | 552.295 | |||||||

| 94.105 | 126.503 | 166.173 | |||||||

| 2.379 | 2.600 | 7.238 | |||||||

| Scagr7 | [-0.466,0.668] | 35 | 31 | 0 | 3 | 1.795 | 2.263 | 5.988 | 70189 |

| 959.6 | 1648.3 | 2687.8 | |||||||

| 214.869 | 352.202 | 882.132 | |||||||

In this table, the first column is the name of problems, the second column is the corresponding convex section of the domain of the optimal value function containing The four consequent columns are the number of detected invariancy intervals, transition points, change points and those that are both transition and change points. The values in the last column (in CPU time) corresponds to the total times for determining all invarian???? The “min” is the minimum time spent in detection of one of the invariancy intervals. The “mean” is the average consumed time in detection of an invariancy interval.

The “min” (“max”) is the minimum (maximum) time spent in detection of all invariancy intervals. The “mean” is the average consumed time in detection of an invariancy interval. The first row is related to the required time to find the eigenvalues of the matrices (See Theorem 2), (See Theorem 3), and and (See Theorem 4). The second to fourth rows are the times consumed to determine the intervals satisfying Cond.s 1-3, respectively.

For example, in Afiro, induced invariancy intervals are 44 with 29 points as mere transition points, 3 points as mere change points, and 11 points as both transition and change points. In the last column, 4151 is the total time for determining all invariancy intervals. The values 0.013, 0.016, and 0.021 are respectively, related to min, mean, and max of the required time to find the eigenvalues of some specific matrices in Theorems 2, 3, and 4. The values (0.240 , 0.585 , 0.829), (37.205, 64.131, 92.316), and (18.762, 29.608, 36.888) are respectively, related to min, mean, and max of the times consumed to determine the intervals satisfying Cond.s 1-3, respectively.

As Tables 3 and 4 show, the computation time increases as the size of the problem increases. However, this is not a general rule. For example, the problem Stocfor1 only revealed one invariancy interval for several random selections of and ; and the total CPU time was almost less than 700 Sec.Furthermore, these results show that the time required to determine an interval satisfying Cond. 2, is as least as the two-thirds of the total time.

| Convex section | No. of detected Ind. | Total CPU | ||||

|---|---|---|---|---|---|---|

| Inv. | Trans. | Chang. | ||||

| Precision | of | Int. | Points | Points | Both | Time (Sec.) |

| 0.005 | 56 | 36 | 7 | 12 | 5408 | |

| 0.010 | 48 | 31 | 5 | 11 | 5262 | |

| 0.015 | 44 | 29 | 3 | 11 | 4151 | |

| 0.020 | 41 | 27 | 3 | 10 | 3783 | |

| 0.025 | 42 | 28 | 2 | 11 | 3859 | |

| 0.030 | 40 | 25 | 2 | 12 | 3601 | |

| 0.035 | 40 | 25 | 2 | 12 | 3683 | |

| 0.040 | 34 | 22 | 1 | 10 | 3662 | |

| 0.045 | 32 | 20 | 1 | 10 | 3221 | |

| 0.050 | 29 | 17 | 1 | 11 | 2594 | |

In order to analyse the effect of on the number of detected invariancy intervals, the behavior of Afiro is investigated and the results are denoted in Table 5 for up to with step size . As it is depicted in this table, when increases, the total running time for computing the convex domain containing zero would decrease. For example, the total running time for computing the convex invariancy interval for and is equal to 4151 and 3783, respectively, with the exception at and . Analogously, as increases, the number of detected invariancy intervals might decrease. This means that some invariancy intervals might be divided into some subintervals by decreasing the value of . For example, the number of invariancy intervals of Problem Afiro for and are 44 and 41, respectively. The exception is for and that this number rises from 41 to 42.

Acknowledgment

We would like to thank Azarbaijan Shahid Madani University for its support.

8 Conclusion

In this paper, we considered a uni-parametric linear program when an identical parameter linearly perturbed the left and the right sides of constraints. The induced optimal partition was defined, and a methodology for identifying the corresponding invariancy interval was provided. It was proved that the optimal value function is fractional on each interval; it is continuous at internal jointing points. A computational algorithm was presented, enabling to find all invariancy intervals. In addition to the traditional concept of the transition point, the concept of change point was also introduced. Examples indicated the validity of the findings. As future work, this study could be conducted for more than one parameter or a uni-parametric linear program when left and right-hand-side of constraints in addition to the objective coefficients were linearly perturbed by an identical parameter, as well as for the case where the perturbation is not linear.

References

- [1] H. Bart, I. Gohberg, M. A. Kaashoek, Minimal Fractorization of matrix and operator functions, Operator Theory: Advances and Aplications 1, Birkhäser Verlag, Basel, (1979).

- [2] A. Ben-Israel, A volume associated with matrices, Linear Algebra and its Applications, 167 (1992), pp. 87-111.

- [3] A. Ben-Israel, and T.N. Greville, Generalized inverses: theory and applications, Springer Science & Business Media 15 (2003).

- [4] A. Ben-Tal and M. Teboulle, A geometric property of the least squares solution of linear equations, Linear Algebra and its Applications, 139 (1990), pp. 165-170.

- [5] S. Boyd and L. Vandenberghe, Convex optimization, Econometrica, Cambridge University Press, (2004).

- [6] V.M. Charitopoulos, L.G. Papageorgiou, and V. Dua, Multi-parametric linear programming under global uncertainty. AIChE Journal 63 (9), (2017a. ), pp. 3871-3895 .

- [7] R. M. Freund, Postoptimal analysis of a linear program under simultaneous changes in matrix coefficients, Mathematical Programming Study, 24 (1985), pp. 1-13.

- [8] A. Ghaffari Hadigheh and N. Mehanfar, Matrix perturbation and optimal partition invariancy in linear optimization, Asia-Pacific Journal of Operational Research, No. 03, 32 (2015), Pages 17.

- [9] A. Ghaffari-Hadigheh, O. Romankko, and T. Terlaky, Sensitivity analysis in convex quadratic optimization: Simultaneous perturbation of the objective and right-hand-side vectors, Algorithmic Operations Research 2 (2007), pp. 94-111.

- [10] A. Goldman, A. Tucker, Theory of linear programming, In H. Kuhn, A. Tucker(eds), Linear Inequalities and Related Systems, Annals of Mathematical Studies, Princeton University Press, Princeton, New Jersey, No. 38, (1956), pp. 53-97.

- [11] H. Greenberg, Matrix sensitivity analysis from an interior solution of a linear program, INFORMS Journal on Computing, No. 3, 11 (1999), pp. 316-327 .

- [12] H. Greenberg, Simultaneous primal-dual right-hand-side sensitivity analysis from a strictly complementary solution of a linear program, SIAM Journal of optimization 10(2000), pp. 427-442.

- [13] A. Holder, Parametric linear programming, (2010).

- [14] R. Khalilpour, I.A. Karimi, Parametric optimization with uncertainty on the left-hand-side of linear programs, Comput. Chem. Eng. 60 (2014), pp. 31-40.

- [15] C. Roos, T. Terlaky, and J. P. Vial, Interior point methods for linear optimization, Springer Science & Business Media, (2005).

- [16] R. A. Zuidwijk, Linear parametric sensitivity analysis of the constraint coefficient matrix in linear programs, ERIM report series research in management, (2005), pp. 1-10.