Equilibrium Oil Market Share under the COVID-19 Pandemic

Abstract

Equilibrium models for energy markets under uncertain demand and supply have attracted considerable attentions. This paper focuses on modelling crude oil market share under the COVID-19 pandemic using two-stage stochastic equilibrium. We describe the uncertainties in the demand and supply by random variables and provide two types of production decisions (here-and-now and wait-and-see). The here-and-now decision in the first stage does not depend on the outcome of random events to be revealed in the future and the wait-and-see decision in the second stage is allowed to depend on the random events in the future and adjust the feasibility of the here-and-now decision in rare unexpected scenarios such as those observed during the COVID-19 pandemic. We develop a fast algorithm to find a solution of the two-stage stochastic equilibrium. We show the robustness of the two-stage stochastic equilibrium model for forecasting the oil market share using the real market data from January 2019 to May 2020.

keywords:

Two-stage stochastic equilibrium , oil market share , COVID-19 pandemic, uncertain demand and supply.1 Introduction

In this paper, we consider the two-stage stochastic equilibrium model under uncertain demand and supply for forecasting the market share in an oligopoly market. This model is developed based on noncooperative game theory which allows us to investigate how the market share of one product (oil, electricity, steel, etc.) depends on the strategies of a few agents whose decisions against and affect each other. A Nash-equilibrium for oligopolies is expected, in which costs and benefits are balanced so that no agent can gain by changing only their own strategies. The uncertainties in the future events are represented by random variables in the model. The COVID-19 pandemic has significant impact on the global energy industry and arouse great challenging in maintaining market stability. Whether we can expect a Nash-equilibrium for crude oil market share during the COVID-19 pandemic is an interesting question.

In traditional oil industry, each producer has normally two strategies for maximizing its profits. One is to limit supply which leads to high oil price and this approach allows high-cost producers to remain profitable. The other is to drive up production and squeeze out high-cost producers, e.g., US shale oil, under expected low price market environment. It has been shown that under certain conditions, one strategy can be more appropriate than the other [2]. However, the change in production had inconsistent market responses due to the complex and uncertain nature of oil market [24, 34]. Furthermore, it has been observed that even during the periods of violently volatile in oil market, the relative market share remained stable. See Tables 3-4 for monthly oil market share from January 2019 to May 2020.

The industry of oil is no stranger to volatilities in price, supply and demand [26, 45]. Economic growth can be largely affected by oil volatility, and certain countries may be more sensitive than the others [30, 33, 42]. Most of these changes, the so-called oil shocks, were caused by the occurrence of major events of global economics and dramatic trends shifting that affects supply or/and demand sides in the crude oil market, and the situation was no different in the latest oil shock during COVID-19 pandemic. Events of the crude oil market are capable of delivering significant impact on energy markets as well as non-energy markets [23, 27, 32]. It is believed, however, despite different causes of oil shock, their consequences for economy are very similar [22]. The most apparent observation on oil uncertainty is its price, and it is naturally assumed as of certain importance to market participants. However, being an oligopoly market implies that the price is largely manipulated by major producers. In particular, these producers may choose to sell greater quantity of oil at a lower price over the strategies of limiting supply to boost price, because the former can be more profitable in long run. There are many attempts on predicting crude oil price recently using tools of machine learning and artificial intelligence [1, 3, 43].

To analyze the oil market share under uncertain supply and demand, we model the production decisions as a solution of a two-stage stochastic game. The two-stage stochastic game is suitable to reflect the complexity of the trading process while market demand needs to be predicted/estimated at the second stage to guide the production at the first stage for a certain period of time in the future. In the two-stage stochastic game, we have two types of decisions: “here-and-now” and “wait-and-see” for each agent. Endowed with market data of production, supply, demand, cost and price of the commodity, each agent chooses its here-and-now decision and wait-and-see decision with and without observation of uncertainties in the future events, respectively. For each agent, the objective of the first stage is to maximize its expected utilities under capacity constraints, and the objective of the second stage is to maximize its utilities subject to constraints endowed with its here-and-now decision and recourse term for almost every realization. The structure of the two-stage stochastic game is a natural way to represent the equilibrium state under uncertain environment. Each agent must make a here-and-now decision for a production plan before knowing the future events. The here-and-now decision will affect future revenues, cost and feasibilities over the decision horizon. The wait-and-see decision is made by taking the uncertain demand, supply and price in the future market into account. Assuming that the utility functions at both stages are concave and continuously differentiable, we can derive the equivalent two-stage stochastic equilibrium model by the first-order optimality condition, which is a special case of the two-stage stochastic variational inequalities (SVI).

Variational inequalities play a central role in operations research and optimization, which model equilibrium problems in engineering and economics [16] and represent the optimality conditions of the optimization problems [39]. Stochastic variational inequalities (also called one-stage SVI ) [4, 15, 17, 20, 21, 28, 29, 37] consider a here-and-now solution in an uncertain environment using expectation of random functions. Compared with the one-stage SVI, the two-stage SVI consider a pair of a here-and-now solution and a wait-and-see solution, which have inherently dynamic components that involve uncertain information and whose solutions depend on the outcome of random events to be revealed in the future. In the last few years, the two-stage SVI and multi-stage SVI have attracted considerable attention [5, 7, 6, 9, 10, 25, 35, 40, 41]. Chen, Pong and Wets [5], and Rockafellar and Wets [40] introduced the the two-stage SVI and multi-stage SVI with examples including the first-order optimality conditions for stochastic programs, Walras equilibrium problems with an incomplete financial market and stochastic Wardrop traffic flow equilibrium problems. The existence and uniqueness of solutions of the two-stage SVI, and convergence of its sample average approximation have been investigated in [6, 7]. The Progressive Hedging Algorithm (PHA) [38] for scenarios and policy aggregation in optimization under uncertainty has been extended to solve monotone two-stage SVI in [41].

Our contributions in this paper are twofold. We develop new optimization theory and algorithms for the two-stage SVI arising from an oligopoly market. Furthermore, we apply the new optimization results to show the existence of a Nash-equilibrium for oil production game in an uncertain environment. In particular, we model the game of crude oil production with a few agents as the two-stage SVI, and show the existence and uniqueness of solutions of the two-stage SVI. Moreover, we develop a fast algorithm to find a solution of the two-stage SVI, which is used to analyze and forecast oil market share under the CODVI-19 pandemic.

This paper is organized as follows. In section 2, we present the two-stage SVI arising from two-stage stochastic games. In section 3, we show the existence and uniqueness of the solution of the two-stage SVI and provide perturbation error bounds for the solution. In section 4, we develop a fast algorithm called Alternation Block Algorithm (ABA) to find a solution of the two-stage stochastic equilibrium. The computational cost of the ABA is much less than the popular PHA. We show outperformance of the ABA over the PHA using large-scale numerical examples. In section 5, we apply the two-stage SVI, our new theory and algorithm to study the impact and the production responses of oil producers during COVID-19 on oil market share. Our numerical results with real market data from January 2019 to May 2020 show the efficiency of our methods for modelling oil market share.

2 Two-stage stochastic quadratic games

We consider an oligopolistic market where agents compete to supply a homogeneous product noncooperatively in the future. Each agent needs to make a decision on the quantity of production based on the anticipated future market demand and supply and other agents’ decision in an uncertain environment. The uncertainties are represented by a random variable defined in the probability space with a support set and the space of measurable functions from to .

We define the variables and functions for each agent , .

, the production quantity

, the cost function of the production

, the supply quantity

, the cost function for supplying a quantity

The uncertain market supply and demand are characterized by a random total supply to the market and a random inverse demand function . Here can be regarded as the spot price of trading in the future.

Each agent aims to maximize its profit and make its decision in two stages. The first stage is to make optimal decision on production quantity based on the average of random demand, and the second stage is to make optimal decision on supply quantity based on the observation of the uncertainty in the future. The first stage decision is called “here-and-now” and the second stage decision is called “wait-and-see”.

For each realization of random variable and a nonnegative vector , agent wants to find an optimal decision by solving the following problem

| (3) |

Moreover, agent has to make an optimal decision before knowing the future events by solving

| (6) |

Here and are decision variables of the agents other than the agent .

Problem (6) is the first stage, and problem (3) is the second stage of the two-stage stochastic games [6, 7, 25, 36]. We call an optimal solution of the two-stage stochastic games, if for , is the optimal solution of the two-stage optimization problem

| (9) |

| (12) |

In this paper, we consider the case where the objective functions in (3)-(6) are quadratic concave in the following forms

| (13) |

| (14) |

| (15) |

where , , , and are real given numbers. In such setting, the function

is continuously differentiable with respect to (w.r.t.) for and

where are Lagrange multipliers for the constraints . If , then the optimal solution of the optimization problem (12) is for any , and the subdifferential of is

The Karush-Kuhn-Tucker (KKT) conditions of problems (3)-(6) with the functions defined in (13)-(15) derive the following two-stage stochastic linear complementarity problem (LCP)

| (16) |

for almost every , where

and is the vector with all elements being 1.

When the matrix is positive definite, problems (3)-(6) with the functions defined in (13)-(15) are equivalent to problem (16) in the sense that if is a solution of problems (3)-(6), then there is such that is a solution of (16); conversely, if is a solution of (16), then is a solution of problems (3)-(6). A sufficient condition for the matrix being positive definite is

| (17) |

Condition (17) implies that is a symmetric diagonally dominate matrix with positive diagonally elements and thus a positive definite matrix.

Let

| (18) |

It is easy to see that for any

| (19) |

where and

Note that we cannot apply [7, Proposition 2] for the existence of solutions of the two-stage stochastic LCP (16), since the condition that there exists a positive continuous function with such that

| (20) |

fails for any , and .

In the next section, we will establish the existence of solutions of the two-stage stochastic LCP (16) with a finite number of realizations of the random variable.

3 Existence, uniqueness and robustness of solutions

The matrix is positive semi-definite, but not positive definite, since

and if and .

Note that the matrix is not a -matrix. Thus the existence and uniqueness of the solution of the LCP and the error bound in [11, 12, 14] cannot be guaranteed for any . For example, if there is such that , then the LCP does not have a solution; if , then any with and is a solution of the LCP.

Let SOL be the solution set of the LCP. Since is a positive semi-definite matrix, SOL is a convex set [14]. A vector is called a least norm solution of the LCP if it is the solution of the optimization problem

where is the Euclidean norm.

The following lemma gives the form of the least norm solution of the LCP and shows that it is the unique solution of the LCP when .

Lemma 3.1.

For any and , the LCP has the least norm solution with

| (21) |

| (22) |

where is the projection from to the set . Moreover, the least norm solution is the unique solution of the LCP if .

Lemma 3.1 shows that for a fixed vector , the least norm solution of the LCP is uniquely defined by , and . In real applications, noise may be presented in the data set and we consider the perturbation bound of the solution regarding noise in , and .

Let us consider the following LCP with

From Lemma 3.1, the LCP with has the least norm solution in the following form

The following theorem provides the distance regarding the noise in data

Theorem 3.1.

Suppose that and let such that . Then the least norm solution of the LCP is continuous with respect to , and . Moreover, we have the following perturbation error bound

| (23) |

4 A new Alternating Block Algorithm (ABA)

In this section, we consider how to efficiently solve problem (16) with a finite number of realizations of the random variable. For , the probability for each realization is . For simplicity, we set , , and

In such setting, problem (16) is the standard LCP, and the progressive hedging algorithm for the LCP, is as follows.

Algorithm 1: Progressive Hedging Algorithm (PHA) [41]

Step 0. Given an initial point , let and , for , such that Set the initial point . Choose a step size Set

Step 1. For , find that solves the LCP

| (24) |

Let , and for update

to get point .

Step 2. Set go back to Step 1.

Theorem 4.1.

The LCP, has at least one solution , and has at most one solution with . Moreover, the sequence generated by the PHA converges to a solution of the LCP,.

The PHA has been widely used for solving stochastic optimization problems and stochastic variational inequalities. Due to the special structure of the , we propose a new algorithm for solving the LCP,, which is called Alternating Block Algorithm (ABA). At each iteration of the PHA, we need to solve linear complementarity problems in dimension. At each iteration of the ABA, we only need to solve strongly convex quadratic programs with a simple constraint in dimension and one linear complementarity problem in dimension. Hence the computation cost of the ABA is much less than that of the PHA.

Algorithm 2: Alternating Block Algorithm (ABA)

Step 0. Given an initial point with . Set

Step 1. For , find that solves quadratic program

| (25) |

Set

| (26) |

Step 2. Find that solves the LCP problem

Set go back to Step 1.

Let be the symmetric positive definite matrix such that Let

where is the nonsingular principal submatrix of whose entries of are indexed by the set

Theorem 4.2.

Suppose and the first component of the solution of the LCP, is positive. Then there is neighborhood of such that for any initial point in the neighborhood, the sequence generated by the ABA converges to the solution of the LCP,.

Now we use randomly generated problems to compare the performance of the PHA and ABA. With uniform distribution, we randomly generate each element of vectors on , on , and numbers on and on . Let and We generate sample from uniform distribution on and set

Then, we let

We terminate the two algorithms when one of the following three stop criteria is met: The number of iterations reaches 400, or , or

The initial points for PHA and ABA are and , respectively. The step size in the PHA is set to .

We choose , and increase the sample size from 5 to 1000. The dimension of the corresponding ranges from 55 to 30015. For each , we randomly generate 10 problems following the description above. The ABA and PHA methods are used to solve these 10 problems. The results reported in Table 1 are the average of iterations, cpu times(seconds), residuals and initial residuals. Table 1 shows that the ABA can solve the with all and efficiently. Another advantage of the ABA is that the iteration numbers remain almost the same when and increase, and the cpu time is roughly linearly increasing as increases. Moreover Table 1 shows that although the PHA can solve the problems with small and , it fails to solve the problems with large or within 400 iterations.

| ABA | PHA | ||||||

| iter | CPU | Res | iter | CPU | Res | Initial Res | |

| 5 5 55 | 15.60 | 0.02 | 6.40e-7 | 294.10 | 0.09 | 9.76e-7 | 5.37e+1 |

| 5 50 505 | 18.40 | 0.06 | 7.62e-7 | 342.90 | 0.58 | 9.91e-7 | 1.69e+2 |

| 5 100 1005 | 21.70 | 0.11 | 6.13e-7 | 371.20 | 1.18 | 1.23e-6 | 2.68e+2 |

| 5 500 5005 | 22.30 | 0.55 | 6.82e-7 | 379.00 | 5.92 | 2.25e-6 | 5.80e+2 |

| 5 1000 10005 | 22.00 | 1.11 | 6.37e-7 | 387.20 | 12.06 | 2.16e-6 | 8.38e+2 |

| 10 5 110 | 20.10 | 0.05 | 8.03e-7 | 383.10 | 0.22 | 5.36e-6 | 7.29e+1 |

| 10 50 1010 | 20.60 | 0.21 | 7.18e-7 | 399.20 | 1.66 | 1.64e-5 | 2.42e+2 |

| 10 100 2010 | 25.20 | 0.67 | 7.12e-7 | 400.00 | 3.63 | 4.22e-5 | 3.18e+2 |

| 10 500 10010 | 25.10 | 2.34 | 5.88e-7 | 400.00 | 17.75 | 9.66e-5 | 8.13e+2 |

| 10 1000 20010 | 23.00 | 6.31 | 5.95e-7 | 400.00 | 34.80 | 9.27e-5 | 1.01e+3 |

| 15 5 165 | 14.50 | 0.04 | 6.85e-7 | 400.00 | 0.40 | 1.21e-5 | 9.31e+1 |

| 15 50 1515 | 20.70 | 0.69 | 6.76e-7 | 400.00 | 3.66 | 1.74e-4 | 2.69e+2 |

| 15 100 3015 | 20.10 | 1.26 | 5.69e-7 | 400.00 | 9.97 | 1.62e-4 | 3.78e+2 |

| 15 500 15015 | 17.80 | 3.91 | 5.56e-7 | 400.00 | 48.55 | 3.11e-4 | 9.02e+2 |

| 15 1000 30015 | 21.60 | 11.31 | 1.02e-6 | 400.00 | 100.23 | 7.26e-4 | 1.41e+3 |

5 Impact of COVID-19 on oil market share

In this section, we use the real data of oil price, demand and the market share of 14 major oil producers in the last 17 months to demonstrate the predicability of the two-stage stochastic LCP model with adaptive parameters in the cost functions. Moreover, the model and the simulation results rationalize decisions made by major producers during COVID-19 pandemic.

Since its first identification, COVID-19 has become a pandemic across all continents of the globe. To fight back the disease, large portions of social and commercial activities have been restricted if not suspended entirely. It seemed, during the worst of the outbreak, the whole world had come to a halt, so did the consumption of oil.

This far reaching global event contributed to an already fragile market of oil. As a result of the pandemic, demand in transportation and factory output fell, which leads to decrease in overall demand for oil. Consequently, it caused oil prices to fall deeply. The last straw happened on 6 March 2020, when Russia rejected the demand of OPEC on further production cuts in response to the demand shrinkage. The oil price fell following the Russian announcement.

5.1 Modelling oil market share as a two-stage stochastic game

We treat the oligopoly market of oil as a two-stage stochastic game where oil producers compete for profit by deciding the optimal production at the first stage of the game.

In particular, we consider 15 oil producers in the following list as 15 agents in the game.

1 Saudi Arabia, 2 Russia, 3 USA,

4 Iraq,

5 China,

6 Canada,

7 United Arab Emirates (UAE), 8 Iran,

9 Kuwait, 10 Nigeria, 11 Mexico, 12 UK, 13 Venezuela,

14 Indonesia, 15 other.

Producer makes a decision on its oil production quantity , based on its predicted further characteristics of the oil market at a later time, where the trading actually occurs. We suppose the trading occurs at the second stage where producer supplies part if not all of its produced quantity in the first stage to generate revenue. The spot price of the trading is uncertain at the time of production decision, and is mainly depended on the demand supply relation at the second stage. To be more precise, supply quantity of producer is uncertain being further event at the time of production decision.

To simulate the effect of excessive supply on price, we adapt a simple supply and demand relation and express the inverse demand function as:

where is the benchmark price and represents the negative effect on price if there is excessive supply of oil with respect to the observed demand at the second stage.

Traditionally, for the production of every barrel of crude oil, producers need to explore oil fields before building the extraction site, even after the oil is extracted refinement and shipment require both time and labour not to mention the cost that involves. The nature of the oil production has been evolving with the technological advance which enables, e.g., extraction from oil sands. There exist fundamental differences in energy infrastructures between traditional producers and oil sands producers, e.g., US, Canada [31], and it is expected to be reflected at the first stage in choosing production strategies.

In this paper, we assume that the costs in both stages are quadratic as expressed in (13) and (14) where the parameters are to be learned from market data. We also include an extra term in the first stage to represent the strategic concern of producer in response to global production quantity . Note that we have no restriction on the sign of and when it is positive it represents the fact that producer is willing to decrease its production when the global production is high. Typical of such agents are often price setters, since the action would give a boost to the oil price and may be more profitable despite the production cuts. In reality, Russia’s refusal to production cuts agreement triggered huge volatility of the market during the COVID-19 pandemic. To express it with our model, it means that Russia adapted its value of to be negative given the market prediction back in March 2020. That is to say, Russia made a “squeeze” strategy and decided that if the price drop caused by over supplying is under control, the maintained market share is potentially more important for long term profitability. Other notable decisions of producers during the COVID-19 pandemic include that Russia refused to production cut on 6th March 2020; Saudi Arabia offered price discount on 8th March and increased production; U.S. demanded production cuts on 2nd April 2020; OPEC and Russia cut production on 9th April 2020.

We will use our model to show that most decisions of producers were reasonable from the prospective of the producers, since they had different tolerance on low oil prices, and they all attempted the best action for their own benefits.

5.2 Numerical simulation and parameter setting

The market data used in our study are obtained from the following sources.

-

(i) Statistical Review of World Energy111https://www.bp.com/en/global/corporate/energy-economics/statistical-review-of-world-energy.html, latest publish in June 2020 by bp. Inc;

This data set provides average daily production quantities of major oil-producing countries, and the percentage of their production of the total production is regarded as their market shares respectively.

-

(ii) Oil Price Dynamics Report222https://www.newyorkfed.org/research/policy/oil_price_dynamics_report, weekly by Federal Reserve Bank of New York;

This data set reports the crude oil price change and the supply/demand relation contributing to the change. It shows supply contribution, demand contribution and other contribution called residual contribution.

-

(iii) U.S. Energy Information Administration333https://www.eia.gov, weekly and daily spot price of Brent.

For the model (3)-(6) with (13)-(15), parameters in the first stage are taken as follows:

-

1.

: This parameter represents the quadratic production cost of producer . For the traditional producers, this contributes to the cost of exploration, site building and equipment setting up, etc. For oil sand producers, the financial cost can also be regarded as non-linear with respect to production quantity. However, all major producers should have similar scale of values to maintain profitable. In our simulation of in-sample and out-of-sample, we took

respectively, where and are market share of producer in the current month and previous month for simulation of 2019, and market shares of January 2020 and December 2019 for simulation of 2020. The data of market share are given in Tables 3-4.

-

2.

: This parameter represents the linear production cost of producer . It is widely agreed that traditional producers have very low unit cost of oil production. As for the oil sand producers, the unit cost is much higher. In our simulation,

-

3.

: This parameter represents producer ’s response to the total of production by all producers. Before the pandemic, it was widely agreed that supply should be kept in accordance to the demand but little preference was taken till Russia’s refusal to further production cuts. In our simulation, for all producers in 2019, and were given in Table 2 for different producers in 2020.

| 2020 | Jan | Feb | Mar | Apr | May |

|---|---|---|---|---|---|

| Saudi Arabia | 0 | 0.01 | 0 | -0.022 | 0 |

| Russia | -0.01 | 0 | 0 | -0.008 | 0.01 |

| USA | -0.01 | 0 | -0.02 | -0.04 | 0 |

| Iraq | 0 | 0 | 0 | -0.01 | 0 |

| China | 0 | 0 | 0.01 | -0.01 | 0 |

| Canada | 0 | 0 | -0.02 | -0.03 | 0 |

| UAE | 0 | 0 | -0.02 | -0.05 | 0 |

| Iran | 0 | 0 | -0.02 | -0.045 | 0 |

| Kuwait | 0 | 0 | -0.01 | -0.045 | 0 |

| Nigeria | 0 | 0 | -0.01 | -0.08 | -0.06 |

| Mexico | 0 | 0 | 0 | -0.065 | -0.045 |

| UK | 0 | 0 | -0.1 | -0.16 | -0.08 |

| Venezuela | 0 | 0 | -0.1 | -0.23 | -0.13 |

| Indonesia | 0 | 0 | -0.1 | -0.23 | -0.13 |

| other | -0.01 | 0 | 0.005 | 0.005 | -0.005 |

These are basic production cost parameters restricted by technological advance and complicated operations, and we do not expect them to change over short periods of time for all producers. For the purpose of forecasting current year production, these parameters are revised monthly taken based on the market share of the month before.

The stochastic parameters are the risk-adjusted spot price and , where is benchmark price, is stochastic supply discount, and are the supply cost coefficients.

For our experiments, we randomly choose , and let representing to 10% of the unit production cost. The data (ii) gives the crude oil price change due to different factors of contributions, namely contribution of demand , supply and the residual contribution . Then, price change is computed as follows:

These contributions and over certain period of time are uncertain. We assume that it can be described by random variable with unknown distribution, written as , and . For the purpose of our numerical tests, we formulate empirical distributions of historical data and use them as an approximation to the unknown distributions of different factors of contribution respectively. Recall that in our model the price is given by

in which the demand is ignored as it would be a constant term and has no effect on solution. Then, for any realization of of -th day, it corresponds to

where is the known price of prior day given in (iii), and are random scenarios taken from empirical distributions of and , respectively.

It follows that, we can generate a set of data of stochastic supply discount

where absolute value ensures that increase in quantity has a negative influence on price, is uniformly distributed and is the total supply obtained from data (i). We chose sample size of random variable for both in-sample and out-of-sample in the numerical simulation.

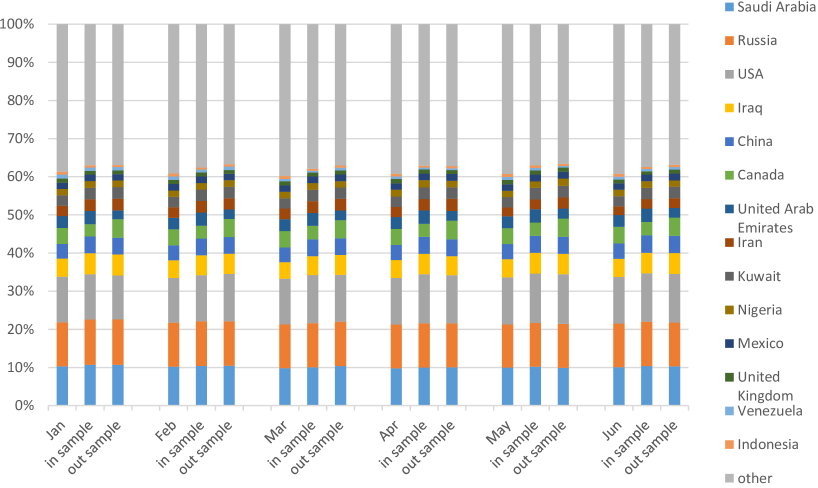

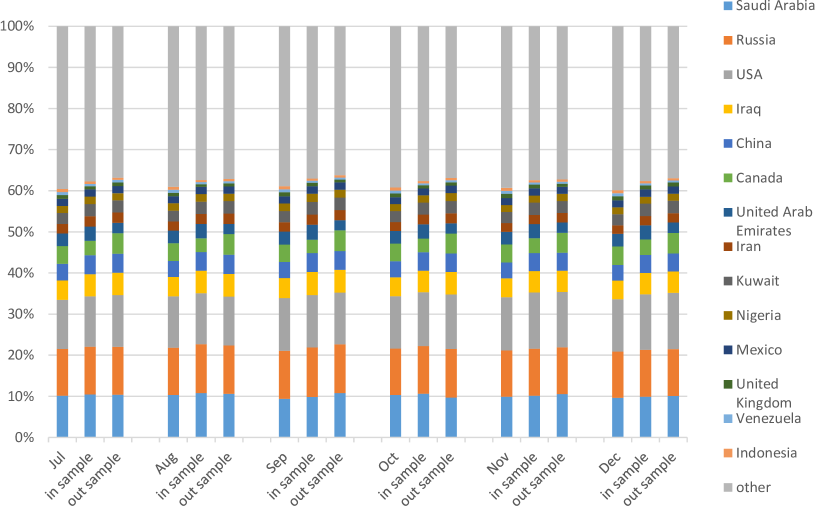

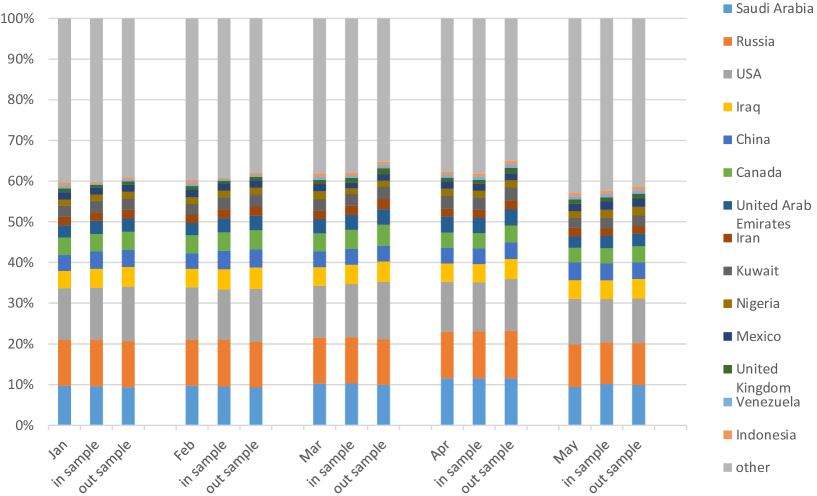

For long-term prediction (yearly market shares prediction), we refer interested readers to [25] for more details. Here, we focus on short-term prediction, namely the monthly in-sample and out-of-sample market shares. Table 3 gives average of daily market shares of producers in each month of 2019. Figures 2 and 2 display results for the recovered monthly market shares in 2019. For each month, the first column is the real market share, while the second and third column are the in sample and out sample recovered results, respectively. They show that our two-stage stochastic LCP model recovers and predicts the short-term real market shares from January 2019 to May 2020 very well. Although global oil demand has been hit hard by COVID-19 and oil price has fell to historically low, our results show that a Nash-equilibrium for the global oil market share during the COVID-19 pandemic can be expected.

| Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Saudi Arabia | 10.31 | 10.22 | 9.82 | 9.77 | 10.00 | 10.10 | 10.12 | 10.34 | 9.39 | 10.36 | 9.91 | 9.64 |

| Russia | 11.54 | 11.52 | 11.46 | 11.45 | 11.31 | 11.42 | 11.38 | 11.47 | 11.67 | 11.29 | 11.26 | 11.23 |

| USA | 11.95 | 11.75 | 11.96 | 12.27 | 12.33 | 12.25 | 11.98 | 12.49 | 12.83 | 12.74 | 12.93 | 12.76 |

| Iraq | 4.72 | 4.61 | 4.37 | 4.68 | 4.75 | 4.72 | 4.70 | 4.73 | 4.84 | 4.59 | 4.58 | 4.50 |

| China | 3.86 | 3.91 | 3.88 | 3.93 | 3.95 | 4.04 | 4.05 | 3.90 | 3.94 | 3.90 | 3.89 | 3.85 |

| Canada | 4.20 | 4.19 | 4.29 | 4.21 | 4.18 | 4.33 | 4.31 | 4.30 | 4.26 | 4.27 | 4.39 | 4.49 |

| UAE | 3.09 | 3.08 | 3.06 | 3.09 | 3.11 | 3.09 | 3.11 | 3.09 | 3.16 | 3.09 | 3.07 | 3.04 |

| Iran | 2.71 | 2.77 | 2.80 | 2.68 | 2.34 | 2.29 | 2.28 | 2.22 | 2.24 | 2.17 | 2.11 | 2.11 |

| Kuwait | 2.73 | 2.73 | 2.73 | 2.72 | 2.75 | 2.68 | 2.68 | 2.63 | 2.73 | 2.65 | 2.71 | 2.71 |

| Nigeria | 1.70 | 1.62 | 1.66 | 1.80 | 1.60 | 1.65 | 1.71 | 1.81 | 1.86 | 1.70 | 1.68 | 1.64 |

| Mexico | 1.63 | 1.72 | 1.70 | 1.70 | 1.69 | 1.70 | 1.69 | 1.70 | 1.75 | 1.66 | 1.71 | 1.70 |

| UK | 1.08 | 1.13 | 1.12 | 1.13 | 1.13 | 0.97 | 0.91 | 0.83 | 0.97 | 0.93 | 1.03 | 1.04 |

| Venezuela | 1.04 | 0.86 | 0.60 | 0.66 | 0.82 | 0.79 | 0.76 | 0.74 | 0.73 | 0.70 | 0.70 | 0.71 |

| Indonesia | 0.77 | 0.76 | 0.76 | 0.71 | 0.77 | 0.73 | 0.75 | 0.74 | 0.75 | 0.74 | 0.73 | 0.73 |

| other | 38.65 | 39.15 | 39.79 | 39.19 | 39.27 | 39.24 | 39.56 | 39.03 | 38.89 | 39.21 | 39.29 | 39.87 |

| Jan | Feb | Mar | Apr | May | |

|---|---|---|---|---|---|

| Saudi Arabia | 9.72 | 9.75 | 10.23 | 11.57 | 9.44 |

| Russia | 11.26 | 11.30 | 11.33 | 11.42 | 10.44 |

| USA | 12.72 | 12.85 | 12.76 | 12.28 | 11.23 |

| Iraq | 4.25 | 4.53 | 4.54 | 4.49 | 4.59 |

| China | 3.88 | 3.87 | 3.92 | 3.90 | 4.32 |

| Canada | 4.36 | 4.41 | 4.42 | 3.74 | 3.66 |

| UAE | 2.98 | 2.99 | 3.54 | 3.88 | 2.72 |

| Iran | 2.10 | 2.05 | 2.01 | 1.96 | 2.17 |

| Kuwait | 2.66 | 2.66 | 2.90 | 3.13 | 2.42 |

| Nigeria | 1.61 | 1.67 | 1.88 | 1.75 | 1.65 |

| Mexico | 1.72 | 1.75 | 1.77 | 1.75 | 1.83 |

| UK | 0.97 | 0.95 | 1.02 | 1.00 | 1.05 |

| Venezuela | 0.73 | 0.75 | 0.73 | 0.71 | 0.76 |

| Indonesia | 0.73 | 0.72 | 0.72 | 0.72 | 0.79 |

| other | 40.32 | 39.75 | 38.24 | 37.68 | 42.93 |

Of particular interests are what had happened in March and April among Russia, Saudi Arabia and U.S.A. In particular, the Brent spot price fell from around $70 per barrel to about $50 since the identification of the pandemic and was believed to decrease further. If no actions of change were taken by the major producers, what could have happened is that the high-cost producers would be forced to cut production because they are more vulnerable in low price environment. On one hand, if the production cut is significant, the price will boost and the non-limited producers can be more profitable. On the other hand, if the oil price continues to fall, the optimal production decision has little to change for the traditional producers with low unit cost, e.g., Russian, Saudi Arabia. In indeed, with our model of two-stage stochastic game, the estimated market share given no strategic changes can be seen in accordance with the description above. It is, given the estimated market share, the most rational decision for Russia is to refuse the production cut agreement. Saudi Arabia, who believed to have the lowest unit production cost, followed the strategy of Russia immediately by offering price discount and increased its production. For both countries, the low price environment has little effects in the sense of maintaining their market share respectively. The same cannot be said for U.S.A., who has high cost in unit oil production, and is estimated to loss its market share if not to change its production strategy, presented by choosing non-zero in our model. It is most apparent from Table 2, that all the major producers responded in choosing their strategies to increase production quantities. The reality was counter intuitive at first glance, but those were in fact all rational decisions and can be forecasted by our model

6 Conclusion

In this paper, we model the oil market share using the two-stage stochastic LCP (16) via the two-stage stochastic games (3)-(6) with quadratic concave utility functions (13)-(15).

We show the existence and uniqueness of a Nash-equilibrium for the oil market share by the solution of the two-stage stochastic LCP (16). Moreover, we propose the Alternating Block Algorithm (ABA) to find a solution of the

two-stage stochastic LCP (16) with finite realizations. We derive the convergence theorems of the ABA and the PHA for

solving (16) with finite realizations and show the ABA is much faster than the PHA by randomly generated problems. We apply the new theoretical results and the ABA to

the analysis of the oil market share from January 2019 to May 2020. Simulation results show that our model is effective for forecasting the oil market share under an uncertain environment of COVID-19 pandemic.

Acknowledgements

Xiaojun Chen would like to thank Hong Kong Research Grant Council for grant PolyU153001/18P.

References

References

- [1] Barunḱ, J, Malinská, B. Forecasting the term structure of crude oil futures prices with neural networks. Applied energy, 2016; 164: 366-379. https://doi.org/10.1016/j.apenergy.2015.11.051

- [2] Behar A, Ritz R. OPEC vs US shale oil: Analyzing the shift to a market-share strategy. Enegy Econ 2017;63:185-98. https://doi.org/10.1016/j.eneco.2016.12.021.

- [3] Chiroma, H, Abdulkareem, S, Herawan, T. Evolutionary Neural Network model for West Texas Intermediate crude oil price prediction. Applied Energy, 2015; 142; 266-273. https://doi.org/10.1016/j.apenergy.2014.12.045

- [4] Chen X, Fukushima M. Expected residual minimization method for stochastic linear complementarity problems. Math Oper Res 2005;30:1022–38. https://doi.org/10.1287/moor.1050.0160.

- [5] Chen X., Pong TK, Wets RJB. Two-stage stochastic variational inequalities: an ERM-solution procedure. Math Program 2017;165:71-111. https://doi.org/10.1007/s10107-017-1132-9.

- [6] Chen X, Shapiro A, Sun H. Convergence analysis of sample average approximation of two-stage stochastic generalized equations. SIAM J Optim 2019;29:135-61. https://doi.org/10.1137/17M1162822.

- [7] Chen X, Sun H, Xu H. Discrete approximation of two-stage stochastic and distributionally robust linear complementarity problems. Math Program 2019;177:255-89. https://doi.org/10.1007/s10107-018-1266-4.

- [8] Chen X, Wang Z. Computational error bounds for differential linear variational inequality. IMA J Numer Anal 2012;32:957-82. https://doi.org/10.1093/imanum/drr009.

- [9] Chen X, Wets RJB. eds, Stochastic Equilibrium and Variational Inequalities. Math Program 2017;165.

- [10] Chen X, Wets RJB, Zhang Y. Stochastic variational inequalities: Residual minimization smoothing sample average approximations. SIAM J Optim 2012;22:649–73. https://doi.org/10.1137/110825248.

- [11] Chen X, Xiang S. Computation of error bounds for P-matrix linearcomplementarity problem. Math Program 2006;106:513-25. https://doi.org/10.1007/s10107-005-0645-9.

- [12] Chen X, Xiang S. Perturbation bounds of P-matrix linear complementarity problems. SIAM J Optim 2007;18:1250-65. https://doi.org/10.1137/060653019.

- [13] Chen X, Xiang S. Newton iterations in implicit time-stepping scheme for differential linear complementarity systems. Math Program 2013;138:579-606. https://doi.org/10.1007/s10107-012-0527-x.

- [14] Cottle RW, Pang JS, Stone RE. The Linear Complementarity Problem. New York: Academic Press; 1992.

- [15] Ehrenmann A, Smeers Y. Generation capacity expansion in a risky environment: a stochastic equilibrium analysis. Oper Res 2011;59:1332–46. https://doi.org/10.1287/opre.1110.0992.

- [16] Ferris M, Pang JS. Engineering and economic applications of complementarity problems. SIAM Rev 1997;39:669–713. https://doi.org/10.1137/S0036144595285963.

- [17] Gürkan G, Özge AY, Robinson SM. Sample-path solution of stochastic variational inequalities. Math Program 1999;84:313–33. https://doi.org/10.1007/s10107980038a.

- [18] Gürkan G, Ozdemir O, Smeers Y. Generation capacity investments in electricity markets: perfect competition. CentER Discussion Paper; Tilburg: Econometrics 2013;045. http://dx.doi.org/10.2139/ssrn.2314862.

- [19] Gürkan G, Pang JS. Approximations of Nash equilibria. Math Program 2009;117:223–53. https://doi.org/10.1007/s10107-007-0156-y.

- [20] Genc TS, Reynolds SS, Sen S. Dynamic oligopolistic games under uncertainty: a stochastic programming approach. J Econ Dyn Control 2007;31:55–80. https://doi.org/10.1016/j.jedc.2005.09.011.

- [21] Gabriel SA, Fuller JD. A Benders decomposition method for solving stochastic complementarity problems with an application in energy. Comput Econ 2010;35:301–29. https://doi.org/10.1007/s10614-010-9200-8.

- [22] Hamilton JD. Causes and Consequences of the Oil Shock of 2007-08. Brookings Papers on Economic Activity, Economic Studies Program, The Brookings Institution 2009;40:215-83. https://doi.org/10.3386/w15002.

- [23] Ji Q, Fan Y. How does oil price volatility affect non-energy commodity markets?. Applied Energy 2012;89:273-80. https://doi.org/10.1016/j.apenergy.2011.07.038.

- [24] Ji Q, Guo JF. Oil price volatility and oil-related events: An Internet concern study perspective. Applied Energy 2015;137:256-64. https://doi.org/10.1016/j.apenergy.2014.10.002.

- [25] Jiang J, Shi Y, Wang X, Chen X. Regularized two-stage stochastic variational inequalities for Cournot-Nash equilibrium under uncertainty. J Comp Math 2019;37:813-42. https://doi.org/10.4208/jcm.1906-m2019-0025.

- [26] Juvenal L, Petrella I. Speculation in the oil market. J Appl Econ 2015;30:621-49. https://doi.org/10.1002/jae.2388.

- [27] Kan S, Chen B, Chen G. Worldwide energy use across global supply chains: Decoupled from economic growth?. Appl Energy 2019;250:1235-45. https://doi.org/10.1016/j.apenergy.2019.05.104.

- [28] Kannan A, Shanbhag UV, Kim HM. Strategic behavior in power markets under uncertainty. Energy Syst 2011;2:115–41. https://doi.org/10.1007/s12667-011-0032-y.

- [29] Kannan A, Shanbhag UV, Kim HM. Addressing supply-side risk in uncertain power markets: stochastic Nash models, scalable algorithms and error analysis. Optim Methods Softw 2013;28:1095–138. https://doi.org/10.1080/10556788.2012.676756.

- [30] Engemann KM, Owyang MT, Wall HJ. Where is an oil shock?. Journal of Regional Science 2014;54:169 C185. https://doi.org/10.1111/jors.12071.

- [31] Lazzaroni EF, Elsholkami M, Arbiv I, Martelli E, Elkamel A, Fowler M. Energy infrastructure modeling for the oil sands industry: Current situation. Appl Energy 2016;181:435-45. https://doi.org/10.1016/j.apenergy.2016.08.072

- [32] Narayan PK, Narayan S, Zheng X. Gold and oil futures markets: Are markets efficient?. Appl energy 2010;87:3299-303. https://doi.org/10.1016/j.apenergy.2010.03.020.

- [33] Nordhaus WD. Who’s afraid of a big bad oil shock?. Brookings Papers on Economic Activity 2007;2007:219-38. https://doi.org/10.1353/eca.2008.0013.

- [34] Panda D, Ramteke M. Preventive crude oil scheduling under demand uncertainty using structure adapted genetic algorithm. Appl Energy 2019;235:68-82. https://doi.org/10.1016/j.apenergy.2018.10.121.

- [35] Pang JS, Sen S, Shanbhag UV. Two-stage non-cooperative games with risk-averse players. Math Program 2017;165:119–47. https://doi.org/10.1007/s10107-017-1148-1.

- [36] Ralph D, Xu H. Convergence of stationary points of sample average two stage stochastic programs: a generalized equation approach. Math Oper Res 2011;36:568-92. https://doi.org/10.1287/moor.1110.0506.

- [37] Ravat U, Shanbhag UV. On the characterization of solution sets of smooth and nonsmooth convex stochastic Nash games. SIAM J Optim 2011;21:1168–99. https://doi.org/10.1137/100792644.

- [38] Rockafellar RT, Wets RJB. Scenarios and policy aggregation in optimization under uncertainty. Math Oper Res 1991;16:235–90. https://doi.org/10.1287/moor.16.1.119.

- [39] Rockafellar RT, Wets RJB. Variational Analysis. Springer-Verlag Berlin Heidelberg; 1998.

- [40] Rockafellar RT, Wets RJB. Stochastic variational inequalities: single-stage to multistage. Math Program 2017;165:331–60. https://doi.org/10.1007/s10107-016-0995-5.

- [41] Rockafellar RT, Sun J. Solving monotone stochastic variational inequalities and complementarity problems by progressive hedging. Math Program 2018;174:453–71. https://doi.org/10.1007/s10107-018-1251-y.

- [42] Eyden RV, Difeto M, Gupta R, Wohar ME. Oil price volatility and economic growth: Evidence from advanced economies using more than a century s data. Appl Energy 2019;233 C234:612-21. https://doi.org/10.1016/j.apenergy.2018.10.049.

- [43] Wang M, Zhao L, Du R, Wang C, Chen L, Tian L, Stanley, HE. intelligence algorithms. Applied Energy, 2018; 220: 480-495. https://doi.org/10.1016/j.apenergy.2018.03.148

- [44] Yao J, Adler I, Oren SS. Modeling and computing two-settlement oligopolistic equilibrium in a congested electricity network. Oper Res 2008;56:34–47. https://doi.org/10.1287/opre.1070.0416.

- [45] Yao T, Zhang YJ, Ma CQ. How does investor attention affect international crude oil prices?. Appl Energy 2017;205:336-44. https://doi.org/10.1016/j.apenergy.2017.07.131.

Appendix, Proofs of Lemma 3.1, Theorems 3.1, 4.1, 4.2 Proof of Lemma 3.1

Proof.

It is easy to see that and , that is, is a feasible solution of the LCP. Hence from the feasibility and the positive semi-definiteness of , the LCP has at least one solution [14, Theorem 3.1.2].

The LCP is the first order optimality condition of the strongly convex quadratic program

Because of the strong convexity, the first order optimality condition is necessary and sufficient for the unique optimal solution of problem (A.1), which is a fixed point of the fixed point problem

Hence, has the form of (21).

Proof of Theorem 3.1

Proof.

We first prove (23). Let

Then we have

which implies

where “mid” is the componentwise median operator. Following the proof of Lemma 2.1 in [8], there is a diagonal matrix diag with such that

Hence we obtain

Since is symmetric positive definite, by Theorem 2.7 in [12], we have

Therefore, using , , and we obtain (23) from (A.2).

Next we show the continuity of the last -components of the least norm solution of the LCP. Without loss of generality, assume that From (23), for any , there is such that if , then This implies for , Hence, we have .

For that, is, , we have . If , then , otherwise . Hence, using (23), we have

where Hence, the solution of the LCP is continuous with respect to , and . We complete the proof.

∎

Proof of Theorem 4.1

Proof.

Let diag(. It is ease to verify that is a solution of the LCP, if and only if is a solution of the LCP,.

Since for any , the matrix is positive semi-definite. Moreover, with , is a feasible solution of the LCP,. Hence the feasibility implies that LCP, has at least one solution [14]. If has the component , then by Lemma 3.1, the component of is uniquely dependent on . Moreover, we have

where is a diagonal matrix with diagonal elements being 0 or 1. Since and are positive definite, is the unique solution of this system of equations. Hence, the LCP, has at most one solution with .

For any , we can easily find

where for . Moreover, the matrix is positive semi-definite for any . Hence from [41], the sequence generated by Algorithm 1 converges to a solution of the LCP,. We complete the proof. ∎

Proof of Theorem 4.2

Proof.

From Step 2 of Algorithm 2 and the definition of a solution, we have

which imply

Let such that . By Theorem 2.1 in [13] and Lemma 3.1, for any , the LCP has a unique solution , which is a Lipschitz continuous function with the Lipschitz constant of . Hence, from , we have

and

Since , we obtain , and the convergence of to . Using Lemma 3.1 again, the sequence generated by the ABA converges to the solution of the LCP,. ∎