Poisson QMLE for change-point detection in general integer-valued time series models

Mamadou Lamine DIOP 111Supported by the MME-DII center of excellence (ANR-11-LABEX-0023-01) and William KENGNE 222Developed within the ANR BREAKRISK: ANR-17-CE26-0001-01

THEMA, CY Cergy Paris Université, 33 Boulevard du Port, 95011 Cergy-Pontoise Cedex, France

E-mail: mamadou-lamine.diop@u-cergy.fr ; william.kengne@u-cergy.fr

Abstract: We consider together the retrospective and the sequential change-point detection in a general class of integer-valued time series. The conditional mean of the process depends on a parameter which may change over time. We propose procedures which are based on the Poisson quasi-maximum likelihood estimator of the parameter, and where the updated estimator is computed without the historical observations in the sequential framework. For both the retrospective and the sequential detection, the test statistics converge to some distributions obtained from the standard Brownian motion under the null hypothesis of no change and diverge to infinity under the alternative; that is, these procedures are consistent. Some results of simulations as well as real data application are provided.

Keywords: Change-point, retrospective detection, sequential detection, integer-valued time series, Poisson quasi-maximum likelihood.

1 Introduction

We consider a class of integer-valued time series in a semiparametric framework. Let be a fixed compact subset of () and . For any , define the class of observation-driven models given by

Class : A -valued () process belongs to if it satisfies:

| (1.1) |

where is the -field generated by the whole past at time , and is a measurable non-negative function, assumed to be known up to the parameter . This class includes numerous classical integer-valued time series, which can be written as a model : for instance, Poisson, negative binomial, binary INGARCH or Poisson exponential autoregressive model (proposed by Fokianos et al. (2009)). The class has been studied by Ahmad and Francq (2016). Under certain regularity conditions, they have established the consistency and asymptotic normality of the Poisson quasi-maximum likelihood estimator (PQMLE) of the model’s parameter.

In this work, our main focus of interest is the structural change-point problem in the model (1.1). By relying on the PQMLE, we will address this issue in two different frameworks: the retrospective (or off-line) and sequential (or on-line) detection. The retrospective detection is performed when all the data are available, whereas the on-line approach focus on sequential change detection as long as new data arrive. For surveys on these approaches, we refer readers to Basseville and Nikiforov (1993) and Csörgö and Horváth (1997).

The change-point problem in time series of count has been addressed in several studies; see among others, Franke et al. (2012), Hudecová (2013), Fokianos et al. (2014), Kang and Lee (2014), Kirch and Tadjuidje Kamgaing (2014), Doukhan and Kengne (2015), Cleynen and Lebarbier (2017), Diop and Kengne (2017, 2021) for some papers in the retrospective setting; and Kengne (2015), Kirch and Tajduidje Kamgaing (2015), Kirch and Weber (2018), Kengne and Ngongo (2020) for some recent papers in the sequential framework. Most of these works are developed in the parametric setting by assuming that the conditional distribution of the observation given the whole past is known; which is quite restrictive in practice. Diop and Kengne (2021) have considered the semiparametric framework, but they focussed on the model selection approach. Kirch and Tajduidje Kamgaing (2015) and Kirch and Weber (2018) developed a general setup based on estimating functions for sequential change-point detection in continuous and integer valued time series. As pointed out by Kengne and Ngongo (2020), the optimal estimating function in several classical parametric model is based on the score function and in the case of infinite memory process considered here, a more complex class of estimating functions is needed; which can lead some difficulties in the application of such sequential procedure.

In this contribution, we consider a process satisfying (1.1) depending on a parameter which may change over time.

-

(i)

In the retrospective detection, we construct a statistics based on the PQMLE and establish that it converges to a well-known distribution under the null hypothesis (no change) and diverges to infinity under the alternative.

-

(ii)

In the sequential detection, we construct a detector, based on the PQMLE, which converges (to some distribution) under the null hypothesis and diverges to infinity under the alternative. In order to perform a procedure with a more efficient detection delay (see Theorem 4.3), the updated estimator is computed without the historical observations.

For the both retrospective and sequential detection, the proposed procedure is consistent.

The paper is structured as follows. Section 2 contains some classical assumptions as well as the definition of the PQMLE. In Section 3, we derive the procedure for the retrospective change-point detection and provide the main results. Section 4 focuses on the sequential change-point detection. Some results of simulations and real data example are displayed in Section 5 whereas Section 6 is devoted to a concluding remarks. Section 7 provides the proofs of the main results.

2 Assumptions and Poisson QMLE

Throughout the sequel, the following notations will be used:

-

•

, for any ;

-

•

for any function , where denotes the set of matrices of dimension with coefficients in ;

-

•

, where is a random vector with finite order moments;

-

•

for any such as .

We set the following classical Lipschitz-type condition on the function .

Assumption A (): For any , the function is times continuously differentiable on with ; and there exists a sequence of non-negative real numbers satisfying (or for ); such that for any ,

where denotes any vector, matrix norm.

In the whole paper, it is assumed that any belonging to is a stationary and ergodic process satisfying:

| (2.1) |

Let and . If , then for any subset , the conditional Poisson (quasi)log-likelihood computed on is given (up to a constant) by

where . We approximate this conditional (quasi)log-likelihood (see Ahmad and Francq (2016), for more details) by

| (2.2) |

where . According to (2.2), the PQMLE of computed on is defined by

| (2.3) |

If is an observed trajectory of a process belonging to , then we set the following regularity assumptions to obtain the asymptotic results (consistency and asymptotic normality) of the PQMLE (see Ahmad and Francq (2016)):

-

(A0):

for all , ; moreover, such that , for all ;

-

(A1):

is an interior point of ;

-

(A2):

and as , where ;

-

(A3):

The matrices and exist;

-

(A4):

for all , a.s ;

-

(A5):

there exists a neighborhood of such that: for all ,

-

(A6):

, and are of order for some , where

Remark 2.1

The aforementioned assumptions have been imposed by Ahmad and Francq (2016) to study the asymptotic behavior of the PQMLE; in their works, they proved that all assumptions hold for many classical models. But, many of these assumptions (more precisely, (A2), (A3), (A5) and (A6)) can be easily obtained from the Lipschitz-type condition A with .

Under (A0)-(A6), Ahmad and Francq (2016) have established that the estimator is strongly consistent and asymptotically normal; that is,

| (2.4) |

where and are defined in the assumption (A3). According to (A4), one can show that the matrices and are symmetric and positive definite. Throughout the sequel, we set for any with ,

Under the previous assumptions, and converge almost surely to and respectively. Hence, the matrix can be consistently estimated by .

3 Poisson QMLE for retrospective change-point detection

Assume that a trajectory of the process is observed and consider the following test problem:

-

H0:

is a trajectory the process with .

-

H1:

There exists (with ) such that is a trajectory of a process and a trajectory of a process .

By using the PQLME of the parameter, we construct a semi-parametric test statistic from the basic idea that, under the null hypothesis (i.e., no change), for , and are close to ; that is, the distances and are expected to not be too large.

Let and be two integer valued sequences satisfying: and as . For all , define the matrix by

| (3.1) |

Now, consider the test statistic:

with

where is a weight function non-decreasing in a neighborhood of zero, non-increasing in a neighborhood of one and satisfying

Its behavior can be controlled at the neighborhood of zero and one by the integral (see Csörgö et al. (1986))

The weight function allows to increase the power of the test procedure based on the statistic .

The proprieties of the matrix is very important to prove of the consistency of the proposed procedure. Indeed, when the parameter is constant over the observations (under H0), according to the assumptions of Section 2, we can show that is also a consistent estimator of the covariance matrix .

Under the alternative, the model depends on two parameters and the consistency of is not ensured.

But, under the classical Assumption (see below), one can show that the first matrix on the right hand side of (3.1)

converges to the covariance matrix of the stationary model of the first regime which is positive definite and the second matrix is positive semi-definite. This will play a key role in the proof of the consistency under the alternative.

Let us note that the sequence is also very important for the statistic ;

it is used to assure that the length of and are not too small, which allows to obtain the convergence of the numerical algorithm used to compute these estimators.

Such approach to construct the statistic for change-point detection in a retrospective setting has already been used by Doukhan and Kengne (2015) and Diop and Kengne (2017).

Theorems 3.1 and 3.2 give the asymptotic behavior of the statistic under the null and alternative hypothesis.

Theorem 3.1

Under H0 with an interior point of , assume that (A0)-(A6), A () and (2.1) (with ) hold with

| (3.2) |

If there exists such that , then

where is a -dimensional Brownian bridge.

According to the results of Theorem 3.1, at a nominal level , the critical region of the test is , where is the -quantile of the distribution of . This assures that the test procedure has correct size asymptotically. In the empirical studies, we will consider the cases where , and we will use the values of provided in Lee et al. (2003).

Under the alternative, we assume

Assumption B: there exist such that (where is the integer part of ).

Theorem 3.2

This theorem establishes that the proposed procedure is consistent in power. Under H1, a classical estimator of the breakpoint is

4 Sequential change-point detection

Assume that we observed an available historical trajectory generated from (1.1) according to a parameter . New data will arrive and we would like to monitor these data from the time in order to test whether any structural change occurs. More precisely, for each new observation, we want to know if a change occurs in the parameter . To address this problem, consider the following classical hypothesis testing:

-

H:

is constant over the observations ; that is, .

-

H:

There exists , (with ), such that and .

Let be a monitoring instant. As in Bardet and Kengne (2014), we derive a test procedure based on a statistic (called the detector) which evaluates the difference between and for any . Since the matrix and are symmetric and non-singular (see Ahmad and Francq (2016)), from the central limit given in (2.4), we deduce

where is the identity matrix. Hence, define the detector

To assure the convergence of and avoid some excessive distortion in the procedure, we introduce a sequence of integer numbers with and define the set . Therefore, the detector will be computed for . In the sequel, we assume that the sequence satisfies:

Let ( can be equal to infinity). The sequential monitoring scheme rejects H at the first time satisfying such that for a suitably chosen constant , where denote the integer part of . The procedure is called closed-end method when and open-end method when . The set is called the monitoring period, and its length depends on the time that we when to monitor the data. To obtain a procedure that is able to detect change that occurs at the beginning of the monitoring and that occurs a long time after the beginning of the monitoring, we will use a function , called a boundary function satisfying:

Assumption B∗: is a non-increasing and continuous function such as .

The monitoring scheme rejects H at the first time (with ) such as there exists satisfying . Hence, we define the stopping time as follows:

with the convention that . Therefore, we have

| (4.1) |

So, one would like to correctly calibrate a suitable boundary function such that the probability of false alarm is close to a fixed level and the probability of true alarm is close to , at least for large enough; that is, for some given ,

| (4.6) |

In the case where with a positive constant, the first condition of (4.6) leads to compute the critical value depending on . Moreover, if a change-point is detected under H; i.e., and , then the detection delay is defined by

| (4.7) |

For the open and closed-end procedure, the following theorem gives the main result obtained under H

Theorem 4.1

In the empirical studies, we will use the boundary function with a positive constant. Since this function satisfies Assumption , the following corollary can be immediately deduced from Theorem 4.1.

Corollary 4.2

Assume that , for all . Under the assumptions of Theorem 4.1, and with or ,

where, using the notation if ,

At a nominal level , we take , where is the -quantile of the distribution of . The values of can be computed through Monte-Carlo simulations as described in Bardet and Kengne (2014).

For the open-end and closed-end procedure, the following theorem shows that the detector tends to infinity when the parameter changes from to (under H).

Theorem 4.3

The following corollary can be immediately deduced from the relation (4).

Corollary 4.4

Under the assumptions of Theorem 4.3,

Hence, it follows from Theorem 4.3 that the change is detected with probability tending to one, both for open-end and closed-end (when ) procedures and the detection delay can be bounded by for any (or even by with using the same arguments).

5 Some numerical results

In this section, we evaluate the performance of the proposed test procedures through an empirical study. For each procedure (the retrospective and the sequential detection), we present some simulation results for change-point detection in a model that belongs to the class (1.1). Applications to the number of transactions per minute for the stock Ericsson B are also provided. The nominal level considered in the sequel is .

5.1 Simulation for the retrospective change-point detection

The results of this subsection have been obtained by computing the test statistic with and equals to (with ).

Consider the negative binomial INGARCH model (NB-INGARCH) given by

| (5.1) |

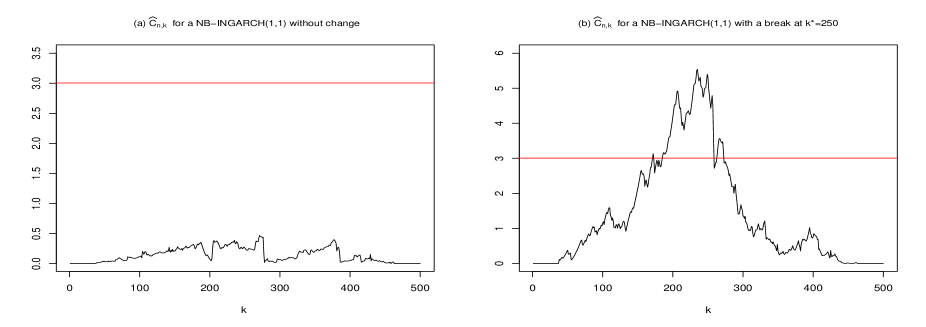

where , and denotes the negative binomial distribution with parameters and . We denote by the parameter of the model. We first generate two trajectories from (5.1): a scenario under H0 when the parameter is constant and a scenario under H1 when the parameter changes at . The statistic is displayed in Figure 1. From this figure, one can see that, in the scenario without change, the statistic is less than the limit of the critical region that is represented by the horizontal line (see Figure 1(a)). Under the alternative (of change in the model), is greater than the critical value of the test and the statistic is large around the point where the change occurs (see Figure 1(b)).

For and , Table 1 indicates the empirical levels computed when the parameter is (under H0) and the empirical powers computed when changes to at (under H1); these results are based on replications. The scenario ; considered in the simulations is close to the fitted model obtained from the number of transactions per minute for the stock Ericsson B (see below). From the findings of Table 1, one can see that even if the procedure exhibits some size distortion when , the empirical levels are close to the nominal one when . Also, the empirical powers displayed increases with the sample size. These results are consistent with Theorem 3.1, 3.2 and are overall satisfactory.

| Empirical levels: | ||||

| Empirical powers: | ||||

5.2 Simulation for the sequential change-point detection

We consider the NB-INGARCH model and focus on the closed-end procedure with ; i.e, the historical available data are and the monitoring period is . The detector is computed with for . In the sequel, we denote , for any .

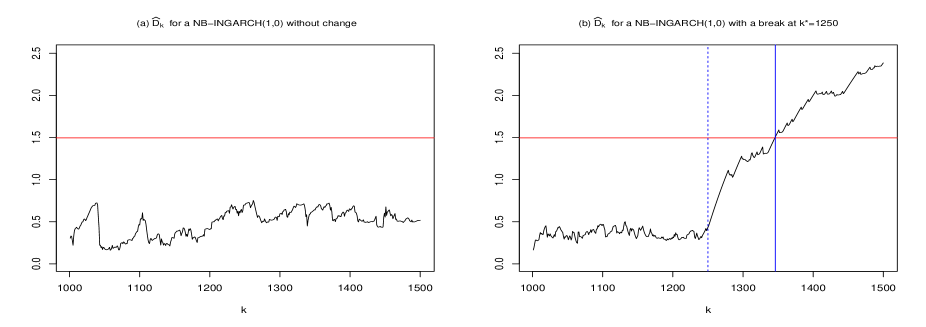

For , Figure 2 displays a typical realization of the statistic from the model (5.1) in a scenario without change and a scenario with a change-point at . As can be seen in Figure 2(a), in the scenario without change, the detector is under the horizontal line which represents the limit of the critical region. Figure 2(b) shows that before change occurs, is less than the the limit of the critical region. But, after the break, the detector increases with a high speed until exceed the critical value; such growth over a long period indicates that something (structural change) is happening in the model.

Now, we consider scenarios under H and H with break at in the model (5.1).

For and , Table 2 indicates the empirical levels and the empirical powers based on replications. The case where is related and close to the real data example.

Some elementary statistics of the empirical detection delays are summarized in Table 3.

The results of Table 2 show some distortion in terms of the empirical level for moderate sample sizes (see for instance, ). However, one can see that the empirical levels of the procedure approaching the nominal level when increases. In addition, for all scenarios considered, the empirical powers increases with and tends to approach one as increases; which is in accordance with the asymptotic results of Theorem 4.3 and Corollary 4.4.

In Table 3, let us recall that the detection delay (defined in (4.7)) is the random distance between the break instant and the stopping time of the procedure. For example, when with a change-point occurred at the time ; from Table3, this change-point is detected on average after a delay of 20, 23, 23 and 20 respectively for these scenarios.

Also, one can see that, for two historical sample sizes and with , the sequence decreases when and increases.

This is in accordance with Theorem 4.3 where can be bounded by for any .

| Empirical levels: | |||||

| Empirical powers: | |||||

| Mean | SD | Min | Med | Max | ||||||

| NB-INGARCH: | ||||||||||

| NB-INGARCH: | ||||||||||

5.3 Real data application

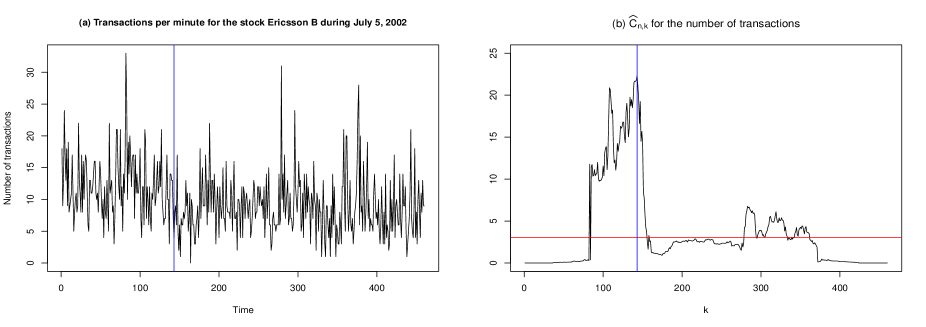

Consider the series of the number of transactions per minute for the stock Ericsson B during July 5, 2002 (see Figure 3(a)). There are available observations that represent the transaction from through . The empirical mean is while the empirical variance is , which indicates that the data are overdispersed. See for instance, Fokianos et al. (2009), Fokianos and Neumann (2013), Davis and Liu (2016), Doukhan and Kengne (2015), Diop and Kengne (2017) for some works that carried out an application to such data. This series has been already analyzed by Diop and Kengne (2017) with a retrospective change point procedure based on the maximum likelihood estimator of the model’s parameter, under the assumption that, the conditional distribution of the data is negative binomial. We carry out an application without this assumption.

Firstly, we apply the off-line change-point detection procedure with a INGARCH representation. The realizations of the statistic with , and are displayed in Figure 3(b). A change point is found at , which exactly corresponds to the break that has been detected by Diop and Kengne (2017) (under the negative binomial assumption). With the PQMLE, the estimated model on each regime yields:

where in parentheses are the standard errors of the estimators obtained from the robust sandwich matrix.

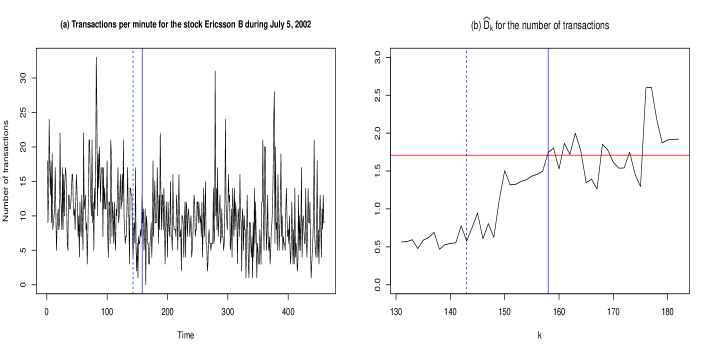

Secondly, we apply the sequential procedure to this series by considering the closed-end setting with and the observations from to as the historical data. Therefore, the monitoring starts at the time and may continue until the time if no break is detected before this instant; i.e, the monitoring period is . Figure 4 displays the realizations of the detector for . From this figure, one can see that the sequential procedure stops at time ; that is, minutes after the break time detected from the retrospective procedure, which is reasonably good.

6 Concluding remarks

This contribution addresses together the retrospective and the sequential change-point detection in a general class of integer-valued time series. Numerous works have been done on these directions by assuming that the conditional distribution of the process is known; which is quite restrictive for practical issues. To overcome this drawback, we tackle these questions in a semiparametric framework with procedures based on the Poisson QMLE. For both the retrospective and the sequential detection, we propose test statistics that converge to some distributions obtained from the standard Brownian motion under the null hypothesis of no change and diverge to infinity under the alternative; that is, these procedures are consistent. In the sequential detection, the updated estimator which is computed without the historical observations leads to a procedure with a reasonably good detection delay that can be bounded by for any . Empirical studies show that these procedures overall work well for simulated and real data example. A good extension of this work is to carry out these procedures with the estimator that are based on the negative binomial QMLE (see Aknouche et al. (2018)).

7 Proofs of the main results

Let and be sequences of random variables or vectors. Throughout this section, we use the notation to mean: for all . Write to mean: for all , there exists such that for large enough. In the sequel, denotes a positive constant whose the value may differ from one inequality to another.

7.1 Results of the retrospective change-point detection

The following lemma is obtained from the Lemma A.1 and A.4 of Diop et Kengne (2021) (for (i.) see also the proof of Theorem 2.1 of Ahmad and Francq (2016)); the proof is then omitted.

Lemma 7.1

Assume that the assumptions of Theorem 3.1 hold. Then,

7.1.1 Proof of Theorem 3.1

Define the statistic

with

where is defined at (2.4) and computed at . Let , and . The Taylor expansion to the function implies that there exists between and such that

It is equivalent to

| (7.1) |

where

| (7.2) |

The following lemma will be useful in the sequel.

Lemma 7.2

Suppose that the assumptions of Theorem 3.1 hold. Then,

-

1.

;

-

2.

is a stationary ergodic, square integrable martingale difference sequence with covariance matrix (computed at );

-

3.

(computed at );

-

4.

.

Proof.

-

1.

See the proofs of Lemma A.1 of Diop and Kengne (2017) and Lemma 7.3. of Doukhan and Kengne (2015); by using the same arguments, one can go along similar lines as in these proofs.

-

2.

Under H0, is a stationary and ergodic process, the same properties hold for . Moreover,

(7.3) Since and are -measurable for any , it holds that .

Also, - 3.

-

4.

By applying with , it holds that

where belongs between and . Since , from the proof of Theorem 2.2 of [1], we get

Now, let us use Lemma 7.2 to show that

Let . By applying (7.1) with and , we get

| (7.5) |

With and , (7.1) becomes

| (7.6) |

As , we have

According to (7.5), for large enough, we get

It is equivalent to

| (7.7) |

For large enough, is an interior point of and we have . Hence, for large enough, we get from (7.7)

| (7.8) |

Similarly, we can use (7.6) to obtain

| (7.9) |

The subtraction of the two above equalities gives

i.e.,

According the above equation, we have

| (7.10) |

Recall that for any ,

The process is a stationary ergodic square integrable martingale difference process with covariance matrix (see Lemma 7.2). By applying the central limit theorem for the martingale difference sequence (see Billingsley (1968)), we have

where is a Gaussian process with covariance matrix .

Hence,

where is a -dimensional standard motion, and is a -dimensional Brownian bridge.

From (7.10), as , we have

According to the properties of , we have for any

Hence, we have shown that as ,

and for all ,

In addition, since for some , one can show that (see also [5])

Hence, for large enough, we have

7.1.2 Proof of Theorem 3.2

Assume that the trajectory satisfies

| (7.11) |

where with and () is a stationary solution of the model (1.1) depending on with .

We have

| and | |||

Then, to prove the Theorem 3.2, it suffices to show that .

Recall that the matrix used to construct the test statistic is given by

According to the asymptotic proprieties of the PQMLE, we have

where

Moreover, the asymptotic proprieties of the PQMLE implies

.

Recall that, by definition, the two matrices in the formula of are positive semi-definite and the first one converges a.s. to which is positive definite.

Then, for large enough, we can write

Therefore, since

we deduce that, . This completes the proof of the theorem.

7.2 Results of the sequential change-point detection

For any and , denote

where and are computed under H and depend on . The following lemma will be useful.

Lemma 7.3

Under the assumptions of Theorem 4.1,

Proof.

Let and . As , from Ahmad and Francq (2016), it holds that , and for , .

Hence,

7.2.1 Proof of Theorem 4.1

According to (4), it is enough to show that

According to Lemma 7.3, to obtain the above convergence, it suffices to show that

| (7.12) |

Let and . As , we can proceed similarly as in (7.8) and (7.9) to show that

The subtraction of the two above equalities gives

This implies

Hence,

Thus, to prove (7.12), we will show that

| (7.13) |

Now, let us consider the following two cases.

(1.) Closed-end procedure.

Let . Define the set .

According to Lemma 7.2, is a stationary ergodic martingale difference sequence with covariance matrix .

Then, by Cramér-Wold device (see Billingsley (1968)), it holds that

where means the weak convergence on the Skorohod space and is a -dimensional Gaussian centered process such as . Therefore,

| and | ||

Hence,

Thus, (7.13) follows; which ends the proof in the case of the closed-end procedure.

(2.) Open-end procedure.

According to (7.13) and (1.), it suffices to show that the limit distribution (as ) of

exists and is equal to the limit distribution (as ) of

Let . For some , we have

From the Hájek-Rényi-Chow inequality (see Chow (1960)), we can get

| (7.14) |

Moreover, since the function is non-increasing, for any , we have

| (7.17) |

by using again the Cramèr-Wold device and the central limit theorem applied to the martingale difference sequence . It comes from (7.14) and (7.2.1) that

| (7.18) |

Furthermore, from the proof of Lemma 6.3 of Bardet and Kengne (2014), we get

Therefore,

| (7.19) |

The relations (7.18) and (7.19) complete the proof in the case of the open-end procedure.

7.2.2 Proof of Theorem 4.3

Denote for . For large enough, we have and thus . Moreover since for some , for large enough and for both the open-end and closed-end procedures, . Hence, is between and and for large enough. Therefore, according to Assumption , we can find a constant such that

| (7.20) |

Moreover, from [1] , we get

Thus, since and are symmetric positive definite, and , it comes from (7.2.2) that

References

- [1] Ahmad, A. and Francq, C. Poisson QMLE of count time series models. Journal of Time Series Analysis 37, (2016), 291-314.

- [2] Aknouche, Abdelhakim and Bendjeddou, Sara and Touche, Nassim Negative Binomial Quasi-Likelihood Inference for General Integer-Valued Time Series Models. Journal of Time Series Analysis 39, (2018), 192-211.

- [3] Basseville, M. and Nikiforov, I. Detection of Abrupt Changes: Theory and Application. Prentice Hall, Englewood Cliffs, NJ, 1993.

- [4] Csörgö, M. and Horváth, L. Limit theorems in change-point analysis. John Wiley & Sons Inc , (1997).

- [5] Csörgo M, Csörgo S, Horváth L, Mason D.M. Weighted empirical and quantile processes. The Annals of Probability 14, (1986), 31-85.

- [6] Bardet, J.M. and Kengne, W. Monitoring procedure for parameter change in causal time series. Journal of Multivariate Analysis 125, (2014), 204-221.

- [7] Billingsley, P. Convergence of Probability Measures. John Wiley & Sons Inc., New York, 1968.

- [8] Chow, Y. A martingale inequality and the law of large numbers. Proceedings of the American Mathematical Society 11(1), (1960), 107-111.

- [9] Cleynen, A. and Lebarbier, E. Model selection for the segmentation of multiparameter exponential family distributions. Electronic Journal of Statistics 11, (2017), 800-842.

- [10] Davis, R.A. and Liu, H. Theory and Inference for a Class of Observation-Driven Models with Application to Time Series of Counts. Statistica Sinica 26, (2016), 1673-1707.

- [11] Diop, M.L. and Kengne, W. Testing parameter change in general integer-valued time series. J. Time Ser. Anal. 38, (2017), 880-894.

- [12] Diop, M.L. and Kengne, W. Piecewise autoregression for general integer-valued time series. Journal of Statistical Planning and Inference 211, (2021), 271-286.

- [13] Diop, M.L. and Kengne, W. Density power divergence for general integer-valued time series with multivariate exogenous covariate. Preprint, arXiv:2006.11948v1, 2020.

- [14] Doukhan, P. and Kengne, W. Inference and testing for structural change in general poisson autoregressive models. Electronic Journal of Statistics 9, (2015), 1267-1314.

- [15] Franke, J., Kirch, C. and Tadjuidje Kamgaing, J. Changepoints in times series of counts. J. Time Ser. Anal. 33, (2012) 757-770.

- [16] Fokianos, K., Rahbek, A. and Tjøstheim, D. Poisson autoregression. Journal of the American Statistical Association 104, (2009), 1430-1439.

- [17] Fokianos, K., Gombay, E. and Hussein, A. Retrospective change detection for binary time series models. Journal of Statistical Planning and Inference 145, (2014) 102-112.

- [18] Fokianos, K. and Neumann, M. A goodness-of-fit test for Poisson count processes. Electronic Journal of Statistics 7, (2013), 793-819.

- [19] Hudecová, Š. Structural changes in autoregressive models for binary time series. Journal of Statistical Planning and Inference 143, (2013) 1744-1752.

- [20] Lee, S. , Ha, J. , and Na, O. The Cusum Test for Parameter Change in Time Series Models. Scand. J. Statist. 30, (2003), 781-796.

- [21] Kang, J. and Lee, S. Parameter change test for Poisson autoregressive models. Scandinavian Journal of Statistics 41, (2014), 1136-1152.

- [22] Kengne, W. Sequential change-point detection in poisson autoregressive models. Journal de la Société Française de Statistique 156, 4 (2015), 98-112.

- [23] Kengne, W. and Ngongo, I. S. Inference for nonstationary time series of counts with application to change-point problems. Preprint arXiv:2005.00934, 2020.

- [24] Kirch, C. and Tajduidje Kamgaing, J. Detection of change points in discrete valued time series. Handbook of discrete valued time series. In: Davis RA, Holan SA, Lund RB, Ravishanker N, (2014).

- [25] Kirch, C., and Tajduidje Kamgaing, J. On the use of estimating functions in monitoring time series for change points. Journal of Statistical Planning and Inference 161 (2015), 25-49.

- [26] Kirch, C. and Weber, S. Modified sequential change point procedures based on estimating functions. Electronic Journal of Statistics 12, 1 (2018), 1579-1613.