Continuous–time incentives in hierarchies††thanks: Research supported by the ANR project PACMAN ANR–16–CE05–0027, the FACE Foundation – Thomas Jefferson Fund & the Mobility Grant of Université Gustave Eiffel.

Abstract

This paper studies continuous–time optimal contracting in a hierarchy problem which generalises the model of Sung (2015) [78]. The hierarchy is modeled by a series of interlinked principal–agent problems, leading to a sequence of Stackelberg equilibria. More precisely, the principal can contract with the managers to incentivise them to act in her best interest, despite only observing the net benefits of the total hierarchy. Managers in turn subcontract with the agents below them. Both agents and managers independently control in continuous time a stochastic process representing their outcome. First, we show through a continuous–time adaptation of Sung’s model that, even if the agents only control the drift of their outcome, their manager controls the volatility of their continuation utility. This first simple example justifies the use of recent results on optimal contracting for drift and volatility control, and therefore the theory of second–order backward stochastic differential equations, developed in the theoretical part of this paper, dedicated to a more general model. The comprehensive approach we outline highlights the benefits of considering a continuous–time model and opens the way to obtain comparative statics. We also explain how the model can be extended to a large–scale principal–agent hierarchy. Since the principal’s problem can be reduced to only an –dimensional state space and a –dimensional control set, where is the number of managers immediately below her, and is therefore independent of the size of the hierarchy below these managers, the dimension of the problem does not explode.

Keywords. principal–agent problems, moral hazard, hierarchical contracting, 2BSDEs.

AMS 2020 subject classifications. Primary: 91A65; Secondary: 91B41, 60H30, 93E20.

JEL subject classifications. C61, C73, D82, D86.

1 Introduction

A little bit of history. The desire to optimise the organisation of work, in a scientific manner, has its origins in the early th century, through the work of Frederick Winslow Taylor, pioneer of the theory of scientific management. The main objective of this theory is to improve economic efficiency, especially labor productivity, and was one of the earliest attempts to apply science to the engineering of management processes. The main objective of Taylor’s model, developed in his monograph entitled The principles of scientific management, could be summarised as: How to make workers perform in the employer’s interest, i.e., in the most cost–efficient way and with the least possible resistance? To answer this question, Taylor promotes the supervision of workers, in opposition to

the management of initiative and incentive (Taylor (1911) [79, pp. 34]).

Nevertheless, during the course of the 20th century, management has noticeably evolved. This shift of paradigm is primarily due to the fact that the very nature of work has changed. Indeed, with the introduction of new technologies at all levels of production, the predominance of indirect labour requires forms of management that break with the classical model of Taylorian organisation of work. Furthermore, the recognition of the importance of the psychological climate, and in particular the idea that the recognition of workers stimulates their productivity, also represents an important advance compared to the Taylorian approach. Both the progressive elimination of simple jobs and the desire to empower the employee have made the supervision of workers difficult and even counterproductive. These two transformations imply that management nowadays relies more on employee initiative, and on the development of incentives to bring the interests of the employee and the employer together, than on the supervision of workers. However, the hierarchical organisation of work à la Taylor is still considered as the standard structure in companies, and only a few dare to adopt a different organisation.

A little bit of context. In an organisation, a hierarchy usually consists of a power entity at the top with subsequent levels of power underneath. This structure is the dominant mode in our contemporary society. Indeed, most companies, governments, and even criminal organisations have a hierarchical structure, with different levels of management or authority. This particular structure of organisations raises many questions: on its efficiency, its cost, its optimal size… To answer these questions, an abundant literature has emerged in the last century in a wide variety of fields, from philosophy to mathematics, through social and management sciences. The first mathematical model for the study of the optimal structure of a hierarchy seems to be the work of Williamson (1967) [84], but, as he mentioned, this question, which presents a serious dilemma for business theory, was originally introduced by Knight in 1921 (see Knight (2012) [45] for a recent edition). Many authors have followed this trend, including the models of Calvo and Wellisz (1978, 1979) [14, 15] and Keren and Levhari (1979) [44], as well as a generalisation by Qian (1994) [70] to take into account the notion of incentives.

The first attempt to define a mathematical framework for incentives in management is attributed to Barnard (1938) [6]. In particular, he advocates the need to create hierarchical relationships within organisations. Although he highlighted the serious issues associated with moral hazard, this very concept was introduced into the literature on management control almost thirty years later by Arrow (1963) [3]. Mathematical models on incentive theories then became more widespread in the 1970s, especially through the work of Mirrlees (1971) [60], and were applied a few years later to hierarchical organisations by Stiglitz (1975) [74] and Mirrlees (1976) [61]. Incentive theory is strongly related to contract theory and principal–agent problems, and is associated with a vast literature that cannot be mentioned here for the sake of conciseness.111We refer the interested reader to the seminal books by Bolton and Dewatripont (2005) [12], Salanié (2005) [71], or Laffont and Martimort (2009) [50] for more references. In the case of a hierarchy, we are dealing with a succession of interlinked principal–agent problems, or in other words, a sequence of nested Stackelberg equilibria. The interest of this mathematical formalism lies in the modelling of information asymmetries within a hierarchy, whether they are ex–ante (adverse selection) or ex–post (moral hazard) the signing of contracts between the entities constituting the hierarchy. Works in this direction include, among others, Tirole (1986) [80], Demski and Sappington (1987) [25], Baiman, Evans, and Noel (1987) [4] and Kofman and Lawarree (1993) [46] on collusion and auditing within a hierarchy, as well as Melumad, Mookherjee, and Reichelstein (1995) [57], McAfee and McMillan (1995) [56], Laffont and Martimort (1997) [49], Mookherjee (2006) [63] on adverse selection. In our framework, we will focus on moral hazard within a hierarchy, as in the work of Laffont (1990) [48], Yang (1995) [85], Macho–Stadler and Pérez–Castrillo (1998) [54], Itoh (2001) [40] and Jost and Lammers (2010) [42].222The essay by Miller and Whitford (2006) [59] presents, however, some limitations to the use of incentives within a hierarchy, through a simple principal–agent model. However, it should be noted that the above–mentioned models are discrete–time models, mostly consisting of a single period.

Moving to continuous–time. In the late 1980s, the literature on contract theory expanded to include continuous–time models. The first, and seminal, paper on continuous–time principal–agent problems is by Holmström and Milgrom (1987) [36]. This work was then extended, and main contributors in these regards are Schättler and Sung (1993) [73], Sannikov (2008) [72], Biais, Mariotti, Rochet, and Villeneuve (2010) [10] as well as Cvitanić and Zhang (2012) [18].333We can also mention in a non–exhaustive way the works of Sung (1995, 1997) [76, 77], Müller (1998, 2000) [64, 65], Hellwig and Schmidt (2002) [33] and Hellwig (2007) [34], that are based on an extension of the first–order approach, popular in static cases. More recently, Williams (2009, 2011, 2015) [81, 82, 83] and Cvitanić, Wan, and Zhang (2006, 2008, 2009) [19, 20, 21] characterise the optimal compensation for more general utility functions by using the stochastic maximum principle and forward–backward stochastic differential equations. More recently, Cvitanić, Possamaï, and Touzi (2018) [23] have developed a general theory that allows to address a wide spectrum of principal–agent problems. The basic idea is to identify a sub–class of contracts offered by the principal, which are revealing in the sense that the best–reaction function of the agent, and his optimal control, can be computed straightforwardly, and then proving that restricting one’s attention to this class is without loss of generality. With this approach, the problem faced by the principal becomes a standard optimal control problem. More importantly, this method allows one to address volatility control problems. It has subsequently been extended and applied in many different situations. We can mention in a non–exhaustive way the applications to finance by Cvitanić, Possamaï, and Touzi (2017) [22] and Cvitanić and Xing (2018) [17]; the works of Aïd, Possamaï, and Touzi (2019) [1] and Alasseur, Farhat, and Saguan (2019) [2] for applications related to the energy sector; as well as other various extensions, e.g., the works of Hernández Santibáñez and Mastrolia (2019) [35] and Hu, Ren, and Touzi (2019a) [37].

Recently, principal–agent problems in continuous time have been extended to models with several principals, through the works of Mastrolia and Ren (2018) [55] and Hu, Ren, and Yang (2019b) [38] for example. In our context, we are particularly interested in the extension to several agents, as by Koo, Shim, and Sung (2008) [47], Élie and Possamaï (2019) [28] and Baldacci, Possamaï, and Rosenbaum (2019) [5], and possibly to a continuum of agents with mean–field interactions by Élie, Mastrolia, and Possamaï (2018) [29], Carmona and Wang (2018) [16] and Élie, Hubert, Mastrolia, and Possamaï (2019) [30]. This latter extension to a large number of agents is a significant step towards the application of continuous–time contract theory to hierarchies. Nevertheless, this type of model seems for the moment to be countable on the fingers of a single hand. First, Miller and Yang (2015) [58] consider a hierarchy of players, each with a principal–agent relationship. Using the approach of Evans, Miller, and Yang (2015) [31], they identify conditions under which a dynamic programming construction of an optimal contract can be reduced to only a one–dimensional state space and one–dimensional control set, independent of the size of the hierarchy. However, the approach in [31] to characterise optimal contracts in continuous time is less general than the one in [23], on which we will rely in this present paper. In particular, it does not allow for volatility control, which seems inescapable in our framework. Then, Li and Yu (2018) [51] develop a method using forward–backward stochastic differential equations to characterise the equilibrium of a generalised Stackelberg game with multi–level hierarchy in a linear–quadratic setting. Finally, Keppo, Touzi, and Zuo (2020) [43] model the relationships between an investor, a partner, and a fund manager as a hierarchical principal–agent problem. More precisely in their model, the manager is an agent for the partner, the partner is a principal for the manager and an agent for the investor, and the investor is a principal for the partner. The framework is similar to the two aforementioned models, but the approach is different and related to Cvitanić, Possamaï, and Touzi (2017) [22] (and thus to [23]), to take into account the fact that the partner controls the volatility of the output. Nevertheless, in these three hierarchical models in continuous time, it is assumed that the entities of the hierarchy control and observe the same output process, while moral hazard prevents them from directly observing the controls.

Sung’s model. The present work is inspired by the model developed by Sung (2015) [78]. In this model, a top manager is hired by a principal to subcontract with middle managers (agents). Each worker (top and middle managers) controls his own output process, and all outputs are assumed to be independent. His model includes a bi–level moral hazard. First, the (top) manager does not observe the effort of the agents, but only the resulting outputs. Second, the principal observes only the total benefit of the hierarchy, i.e., the difference between the sum of the outputs of all workers and the sum of the contracts paid to the agents. Instead of studying a continuous–time version of the model, Sung considers that the one–period model is simpler and without loss of generality:

[f]or ease of exposition and without loss of generality, we formulate a discrete–time model which is analogous to its continuous–time counterpart (Sung (2015) [78, pp. 2]).

Extending the reasoning of Holmström and Milgrom (1987) [36], he therefore restricts the study to linear contracts, in the sense that they are linear with respect to the outcome, and states that

[t]his assumption is without loss of generality, as long as our results are interpreted in the context of continuous–time models (Sung (2015) [78, pp. 3]).

However, while the restriction to linear contracts can be justified in Sung’s framework for the first Stackelberg equilibrium, this is no longer the case for the contract offered by the principal to the (top) manager. More precisely, even if the workers are only controlling the drift of their outcomes, the manager controls both the drift and the volatility of the net benefit. Therefore, according to the work of Cvitanić, Possamaï, and Touzi (2018) [23], it appears that the type of contracts considered by Sung is sub–optimal. Indeed, in continuous time, it is not sufficient to limit oneself to linear contracts (in the sense of Holmström and Milgrom (1987) [36]) when the volatility of the state variable is controlled. More precisely, the optimal form of contracts should contain an additional part indexed on the quadratic variation of the net benefit. However, in the one–period model of Sung, this controlled quadratic variation cannot be estimated (unlike in continuous time), which leads to a fundamental gap between these two frameworks. From our point of view, this gap motivates a full study of Sung’s model in continuous time.

Main contributions. In this paper, we provide a systematic method to solve any hierarchy problems of this sort, including those in which workers can also control the volatility of the output process, and not just the drift. The main result is that optimal contracts in continuous time for the manager are not those expected by Sung (2015) [78], since they have to be indexed on the quadratic variation of the state variable, in the spirit of [23]. The search for the optimal contract therefore requires the application of the theory of second order backward stochastic differential equations (2BSDEs for short), subject to a slight extension to take into account the plurality of agents in the hierarchy. Furthermore, we show that, in a general way, the contract offered by the manager to one of his subordinate agents must be indexed not only on the performance of this particular agent, but also on the performance of other workers. However, several hypotheses are necessary to complete our study, notably on the shape of the dynamics of the state variables. Nevertheless, we will see that these assumptions are satisfied in the most common examples.

The theoretical model we develop allows us to determine the optimal form of incentives for a particular hierarchical structure, which can be extended in a straightforward way to a larger scale hierarchy. Although theoretical, the results we obtain give intuitions based on solid theoretical considerations to know which levers could be activated to incentivise workers within a hierarchy. In particular, the indexation of the contract on the quadratic variation of net profits for the managers argues in favour of remunerating them through stock options. These results can be applied to problems of incentives within a firm with a hierarchical structure, but also and above all as soon as work is delegated to an external entity. For example, these multi–layered incentive problems can be used to model the relationships between a firm and its subsidiaries or subcontractors, or the relationships between an investor, an investment company, and a fund manager, as in the model by Keppo, Touzi, and Zuo (2020) [43].

An overview of the paper. This work consists of two parts. In the first part, we study Sung’s model and some extensions. More precisely, the continuous–time version of Sung’s model is introduced and solved in Section 2. This opening example highlights the differences between the discrete–time model and its continuous–time equivalent, concerning the volatility control and the form of the contracts. In particular, this example leads to the conclusion that in order to rigorously study a continuous–time hierarchy problem, it is not possible to consider the associated discrete–time model with linear contracts. In our opinion, these conclusions justify the use of the theory of 2BSDEs to tackle problems of moral hazard within a hierarchy. In Section 3, we consider some extensions, by adding an ability parameter for the manager to justify his position in the hierarchy, by looking at different types of reporting from the manager to the principal (other than the reporting of the net profit), by extending to a more general hierarchy structure. The details and proofs of the main results in this first part can be found in Appendix A.

The second part of this paper is devoted to the study of the most general model possible. In particular, the workers (middle and top managers) can also control the volatility of their output, in addition to the drift. Moreover, we consider general utilities, allowing us to recover the exponential utility functions (CARA) of Sung’s model [78], but also other cases such as the one of risk–neutral workers. Finally, we consider a more general hierarchy since the principal contracts with managers, who in turns subcontract with the agents in their teams. The model is described in Section 4, and then solved in Section 5, going up the hierarchy. More precisely, we first solve the problem of agents (see Section 5.1), then the problem of their supervisors, i.e., the managers (see Section 5.2), and finally, we end with the principal’s problem (see Section 5.3). As previously mentioned, although some intuitions are presented in Appendix B, the resolution of this model is based on the theory of 2BSDE, whose presentation and theoretical results are postponed to Appendix C. Finally, Section 6 concludes and provides some extensions.

Notations

Let be the set of positive integers. For every –dimensional (column) vector with , we denote by its coordinates and for , we denote by the usual inner product, with associated norm , which we simplify to when is equal to . Let and be the vectors of size whose coordinates are all equal to respectively and . The zero element in is denoted by . For any , will denote the space of matrices with real entries. The transpose of will be denoted by and the zero element in is denoted by . When , we let . We also identify and . The identity matrix in will be denoted by . We also denote by (resp. ) the set of symmetric positive (resp. symmetric definite positive) matrices in . The trace of a matrix will be denoted by . For any vector , we denote by the diagonal matrix in whose entries are the elements of the vector .

Throughout this paper, denotes some maturity fixed in the contract. For any positive integer , let denote the set of continuous functions from to . On , define the evaluation mappings by and the truncated supremum norms by , for . Unless otherwise stated, is endowed with the norm .

2 An opening example: Sung’s model in continuous time

In order to justify the motivation of this work, we present in this section a simple hierarchical contracting problem, similar to the one considered by Sung (2015) [78]. In this model, the principal contracts one manager who in turn subcontracts with many agents. The hierarchy is illustrated in Figure 1. Despite its simplicity, this illuminating example shows the need to take volatility control into account, and therefore justifies the use of the 2BSDEs theory in the rest of this paper. The reasoning will remain informal throughout Sections 2 and 3, the reader is referred to the theoretical part of this paper, from Section 4 onwards, for a rigorous model setting in continuous time.

The only difference with Sung’s model is that we consider here a continuous–time model: between and some time , denoting the maturity fixed in the contract, the firm has tasks which have to be carried out by workers. The outputs of the tasks are represented by stochastic processes, denoted by , with dynamic

| (2.1) |

for . More precisely, the –th worker carries out the task with outcome by choosing a costly effort with values in , where is the set of control processes444The set of admissible control processes will be rigorously defined, in weak formulation, in the theoretical part of this paper, more precisely in Section 4.1.. For simplicity, we assume that for are independent Brownian motions and that the efforts of a worker only impact his own project, which means that all projects are independent and no workers collude. Again for the sake of simplicity in this part, we will consider the following quadratic cost of effort:

| (2.2) |

Still following Sung’s framework in [78], we also assume that the benefit of each worker is represented by a CARA utility function with risk aversion coefficient . The holder of the firm (the principal) is risk–neutral and seeks to maximise the expected difference between the sum of the outcomes and the sum of the compensations paid to the workers. The minimum level of utility that must be guaranteed by a contract to make it acceptable to a worker, i.e., his reservation utility, is defined by his utility without contract.

We define the direct contracting case (DC case) as the case where the principal can directly contract with the agents, without the help of a manager. In this setting, the optimal efforts of the workers are deterministic constant processes given by the result of Holmström and Milgrom (1987) [36], and summarised in Lemma A.1. This case is also discussed by Sung, but the main point of his paper [78], and thus of ours, is to study the case where the principal contracts with a manager, who in turn subcontracts with the agents.

In the hierarchical contracting case (HC case) considered by Sung, the principal cannot directly contract with the workers. She hires a manager (the worker indexed by ) who:

-

carries out his own task by choosing an effort process ;

-

hires agents to carry out the remaining tasks: each agent handles the outcome , by choosing his effort level , for ;

-

reports to the principal the total benefit, that is the difference between the sum of the outcomes and the sum of the compensations to be paid to the agents.

We will show that, in the continuous–time framework, we can improve Sung’s results in [78] by considering a more general form of contracts.

2.1 A continuous–time principal–manager–agents problem

As already mentioned, we are faced with a bi–level principal–agent problem, in the sense that a principal contracts with a manager who in turn subcontracts with many agents. In this section we define the continuous–time equivalent formulation of the value functions considered in [78], as well as the admissible set of contracts.

Agent’s problem. Consider first to focus on the –th agent’s problem. He controls his own output with dynamic (2.1) by choosing an effort . Given a contract offered by his supervisor, namely the manager, the –th agent’s value function is simply defined by:

| (2.3) |

where is the probability associated to the effort . We assume that the manager cannot directly observe the efforts of the agents, which implies a first level of moral hazard in our framework. The manager only observes the outcome processes for . In order to follow Sung’s model as closely as possible, we also assume that the compensation for the –th agent can only be indexed on his performance, i.e., his outcome process , and denote the set of admissible contracts by .555It is worth noticing that this restriction is not admissible in a more general model, as we will see in Remark 2.3. Note that since the reservation utility of the –th agent is defined as his utility without contract, it is given by .

Manager’s problem. The manager controls his own output with dynamic (2.1) by choosing an effort . He also designs the compensations for the agents, namely a collection of contracts

Although we consider that the manager designs the contracts for the agents, all compensations, whether for the agents or the manager, are paid by the principal. Given a contract designed by his supervisor (the principal), the manager’s value function is defined by

| (2.4) |

where, informally, is the probability associated to both the effort and the choice of the contracts , under the optimal efforts of the agents. As in [78], the second level of moral hazard in our framework is linked to the fact that the manager only reports (in continuous time) to the principal the total benefit , i.e., the difference between the sum of the outcomes and the sum of the compensations to be paid:

| (2.5) |

More precisely, in this setting, the principal cannot independently observe the agents’ outcomes or the certainty equivalent of their continuation utility, . Nor does she observe the manager’s outcome , nor his effort . Therefore, she can only index the contract for the manager on the total benefit, i.e., the variable . The contract is thus a measurable function of , and the corresponding set of admissible contract is denoted by .

Principal’s problem. Finally, we consider a risk–neutral principal whose problem is to maximise the sum of the outcomes minus the sum of the compensations to be paid to each worker, by choosing the optimal contract for the manager. Mathematically speaking, we define her value function as follows:

| (2.6) |

where is the probability associated to the choice of the contract , under optimal efforts of the workers.

Remark 2.1.

It should be noted that the three value functions defined above by (2.3–2.4–2.6) should be rigorously written in weak formulation. However, for the sake of simplicity in this section, we avoid this technical side for the moment and refer the reader to the theoretical part of this paper (from Section 4 onwards) for a more correct writing of these three value functions.

2.2 Solving the sequence of Stackelberg equilibria

In order to solve this principal–manager–agents problem, we follow the general theory developed by Cvitanić, Possamaï, and Touzi (2018) [23] and the application in [22] to a framework with CARA utility functions. More precisely, for each Stackelberg equilibrium, starting with the manager–agent problem, we have to:

-

identify a sub–class of contracts, offered to a considered worker by his supervisor, which are revealing in the sense that the best–reaction function of the worker and his optimal control can be computed straightforwardly;

-

prove that the restriction to revealing contracts is without loss of generality;

-

solve the supervisor’s problem, which boils down to a standard optimal control problem.

Revealing contract for an agent. Consider to focus on the contract for the –th agent. Recall that his contract is assumed to be a measurable function of his output . By applying classical results of contract theory for drift control only (see, e.g., the work by Sannikov (2008) [72]), the optimal form of contracts is the terminal value of the certainty equivalent of the continuation utility, which is defined for all as follows:

| (2.7) |

where is a payment rate chosen by the manager, and for all is the Hamiltonian of the –th agent. This form of contract is exactly the continuous–time equivalent of the linear contract considered by Sung in [78, Equation (7)]. Note that this form of compensation includes in particular a fixed part , which is chosen so as to satisfy the –th agent’s participation constraint. Assuming for simplicity that is a standard quadratic cost function defined by (2.2), we can establish the following result, whose proof is straightforward666As the proof of this result is very similar to that of Proposition 2.5 below, providing a similar result for the manager, we have chosen not to detail it here. The reader is thus referred to Section A.1 for a sketch of the proof. in the light of the choice of contract’s form (2.7).

Proposition 2.2.

Fix . Let , be an –valued process, predictable with respect to the filtration generated by , satisfying appropriate integrability conditions777We have to require minimal integrability on the process so that the stochastic integral with is well–defined. Nevertheless, since this section is informal, the conditions of integrability are ignored for the time being. The reader can refer to the general model for a rigorous definition of the admissible process ., and consider the associated contract defined through (2.7). Given this contract, the optimal effort of the –th agent is given for by

Moreover, under the probability associated to the optimal effort , the dynamics of and satisfy

Simplification of the manager’s problem. Recall that the manager, in addition to controlling his own output with dynamic (2.1) by choosing an effort , also designs the collection of contracts for the agents. As mentioned above, instead of studying all possible contracts for the –th agent, it has been proved by Sannikov (2008) [72] that it is sufficient to restrict the study to contracts of the form (2.7). Therefore, the manager’s problem boils down to a standard optimal control problem: to design the compensation for the –th agent, the manager only have to choose the payment rate . We thus define by the collection of all processes , where each is predictable with respect to the filtration generated by , and satisfies appropriate integrability conditions. We can now rewrite the manager’s problem defined by (2.4) in a more standard way:

Recall that we consider that the manager designs the contracts for the agents, but he does not pay them. All compensations, whether for the agents or the manager, are paid by the principal. For this reason, we assume that the principal chooses, for all , the constant in the –th agent’s contract, noticing that this constant must be chosen in order to ensure that his participation constraint is satisfied.

Since the manager only reports to the principal the total benefit in continuous time, his compensation offered by the principal can only be a measurable function of . Then, given the form of the manager’s utility and the dynamic of the output for , is the only state variable of his control problem. Therefore, his optimal control, namely , will naturally be adapted to the filtration generated by .

Remark 2.3.

In fact, the set of admissible control processes for the manager cannot be properly defined in this framework. Indeed, recall that we choose to restrict the contract for an agent to his own . Therefore, the payment rate should not depend on anything other than . In particular, it cannot be predictable with respect to the filtration generated by , since it contains information generated by the outputs of other workers. However, under this assumption, the optimal control of the manager on the –th agent’s contract, which will be denoted by , should be a function of , and thus cannot be computed by the principal, since she only observes . Moreover, we will generically have , , where and are two processes chosen by the principal, assumed to be predictable with respect to what she observes, i.e., with respect to the filtration generated by . Indeed, the manager’s contract is restricted to a measurable function of , therefore the payment rates and indexing the contract on should also be functions of . We thus obtain a contradiction. Nevertheless, in this particular example, every optimal efforts and controls controls turn out to be be deterministic (and even constant), and we can thus index the contract for the –th agent only on his own output . This model has been chosen in this section to easily compare our results with those of Sung (2015) [78]. However, in a more general case, we will not be able to restrict the study to such contracts. More precisely, we will be forced to consider that each agent knows the output of other workers, and that his contract can be indexed on it. The controls of the manager will thus be predictable with respect to the filtration generated by , and can then be computed at the optimum by the principal.

Towards volatility control. Let us set aside for the moment the previous remark, it will be dealt with in the general model (from Section 4 onwards). The most important thing to notice at this stage is that, even if the agents are only controlling the drift of their outcomes, the manager controls both the drift and the volatility of , as we can see from its dynamic under optimal efforts of the agents, which is as follows:

| (2.8) |

recalling that for all . Indeed, by choosing optimally the payment rate in each agent’s contract ( for all ), the manager controls in a way the volatility of the certainty equivalent of agents’ continuation utilities (through the term ), and thus the volatility of . Therefore, we must consider a more extensive class of contracts than the one used by Sung in [78]. Indeed, in continuous time, it is not sufficient to limit oneself to linear contracts (in the sense of Holmström and Milgrom (1987) [36]) when the volatility of the state variable is controlled, as demonstrated by Cvitanić, Possamaï, and Touzi (2018) [23]. This is where our model and Sung’s will diverge. Instead of studying the model in continuous time, Sung considers that the one–period model is simpler and without loss of generality. He therefore continues to restrict the study to contracts that are linear with respect to the outcome, insisting that this restriction is

without loss of generality, as long as our results are interpreted in the context of continuous–time models. (Sung (2015) [78]).

According to our study in continuous time, it appears that the type of contracts considered by Sung is sub–optimal (see Section 2.3.1 for the analysis of the results).

Revealing contract for the manager. Let be the set of all such that for all . We define by the collection of all processes , predictable with respect to the filtration generated by , satisfying appropriate888Similarly as noticed in Footnote 7, we have to require minimal integrability on the process so that the stochastic integral with is well–defined. The reader can refer to the general model for a rigorous definition of the set of admissible control processes . integrability conditions. The set represents the admissible control processes for the principal, when she only observes the variable . Taking into account the previous discussion, it is necessary to use recent results on optimal contracting for drift and volatility control, and therefore the theory of 2BSDEs, to state the following result. We refer to the previously mentioned works of Cvitanić, Possamaï, and Touzi (2018) [23] for the general result, [22] for an application with exponential utilities, as well as Lin, Ren, Touzi, and Yang (2020) [53] for an extension to random time horizon or Élie, Hubert, Mastrolia, and Possamaï (2019) [30] for a model with a continuum of agents with mean–field interaction.

Proposition 2.4.

Assuming that the principal only observes , the optimal form of contracts offered by the principal to the manager is given by

| (2.9) |

where is the manager’s Hamiltonian, and is a pair of processes optimally chosen by the principal. In addition, similar to the agent’s contract form (2.7), represents a fixed part of the compensation, which is chosen so as to satisfy the manager’s participation constraint.

Given the dynamic of the state variable and its quadratic variation, the manager’s Hamiltonian is defined, for any , as follows:

| (2.10) |

Considering any contracts of the form (2.9), we can easily solve the manager’s problem, mainly by maximising the previous Hamiltonian. The proof of the following proposition is therefore a direct consequence of the considered form of contracts, and is detailed in Section A.1.

Proposition 2.5.

Let . The optimal effort on the drift and the optimal control on the –th agent’s compensation chosen by the manager are respectively given by and for all , where, for all ,

| (2.11) |

Under the optimal probability associated to the optimal efforts of both the agents and the manager, the dynamics of and are respectively given, for all , by:

Solving the principal’s problem. Proposition 2.4 states that it is sufficient to restrict the space of contracts to those of the form (2.9), and thus simplifies the principal’s problem. Recall that we assume that the principal chooses all the constants in each agent’s contract, as well as the constant in the manager’s contract. Informally, these constants have to be chosen such that each contract satisfies the participation constraint of the corresponding worker. Given the form of the manager’s and agents’ utility, and in particular since the manager does not pay the compensation for his agents, he is indifferent to the value of , for , as long as the agents accept the contracts. This is why we consider that the principal chooses it, and we denote by the collection of and , for . Moreover, recall that we have assumed as in [78] that the reservation utility level of each worker is given by his utility without any contract, thus equal to , and that the initial outcomes are equal to zero.

Proposition 2.6.

The principal’s problem defined by (2.6) is reduced to . By solving standard control problem, we determine her optimal controls, the optimal contracts and her utility.

-

The optimal payment rates for the manager are given by the constant processes and , where is solution of the following maximisation problem

(2.12) where and, for all and any ,

(2.13) -

The optimal contract offered by the principal to the manager is given by:

where is the manager’s Hamiltonian defined by (2.10). In particular, the optimal choice of the fixed part of the compensation is the one that saturates the manager’s participation constraint, i.e., such that he obtains exactly his reservation utility. In this case, since his utility reservation is equal to , the optimal is .

-

For all , the optimal contract offered by the manager to the –th agent is given by:

where is the –th agent’s Hamiltonian, and recalling that is defined in Proposition 2.5. In particular, as for the manager, the optimal choice of the fixed part of the compensation is .

-

Finally, the value function of the principal is given by:

The proof of this proposition is detailed in Section A.1.

2.3 The benefits of continuous time

2.3.1 Non–optimality of linear contracts in continuous time

Propositions 2.4 and 2.6 require that the optimal contracts for the manager must be indexed on the quadratic variation of the net profit through the parameter . However, in [78], Sung restricts the analysis to linear contracts: although he remarks that decisions on middle managerial contracts are affecting the volatility of the net profit of the firm, he chooses to view them as a case similar to unobservable project choice decisions, modelled by Sung (1995) [76]. More precisely, he states the following:

As shall be seen in our hierarchical contracting problem, the top manager turns out to choose not only the mean of the outcome of his own effort but, in effect, the volatility of the total profit of the firm as he chooses middle managerial contracts. Thus, our problem turns out to be similar to the unobservable project choice problem in Sung [21]. (Sung (2015) [78, pp. 3])

In the aforementioned article [76], Sung studies a principal–agent problem in continuous time where the volatility can be controlled. He distinguishes two cases.

-

One where the variance is observed, but since the Brownian motion is only one dimensional, there is no moral hazard on the volatility’s effort anymore. Indeed, in this case, the variance is equal to the square of the volatility effort, and since the variance is observed, the effort is easily computable by the principal. Therefore, the principal directly controls the volatility’s effort of the agent and the model degenerates to the first–best case (no moral hazard) for the volatility.

-

One where the variance is not observed by the principal, and therefore she cannot index the contract on the quadratic variation of the outcomes, which obviously leads to consider only linear contracts.

In [78], as Sung considers that the variance is not observed, the principal cannot offer a contract to the manager indexed on it, which is equivalent to forcing in our extended class of contracts defined by (2.9). Therefore, he does not optimise the utility of the principal with respect to , since he forces .

Nevertheless, in continuous time, it seems natural to consider that the principal observes the quadratic variation of the total benefit, , and can therefore contract on it. Indeed, she observes in continuous time and can therefore estimate the quadratic variation through the sum of the squared increments. Moreover, a result of Bichteler (1981) [11] (see Neufeld and Nutz (2014) [66, Proposition 6.6] for a modern presentation) states that this quadratic variation, even controlled, can be defined independently of the probability associated to the effort. Therefore, contrary to above, the contract can be indexed on the quadratic variation. Moreover, since the process is naturally driven by independent Brownian motions, the principal does not perfectly observe the controls of the manager, but only a functional of . This prevents the volatility control case from degenerating into the first–best case, contrary to what is mentioned in above.

Therefore, Sung’s argument in [78] to justify restricting the study to linear contracts, namely that his model has to be understood as a continuous–time model in which linear contracts are supposedly optimal, seems not to be valid. One way to fix this problem in the one–period model would be to propose contracts indexed on the variance of . However, as this variance is controlled, it depends on the probability chosen by the manager, which is unknown to the principal when the efforts are not optimal. Indeed, unlike in continuous time, where the quadratic variation, even controlled, can be defined independently of the effort probability, this is not the case for the variance in the one–period model. Therefore, it is not easy to find an equivalent to the contract indexed on the quadratic variation for the one–period model.999It is worth noticing that in a discrete–time framework, but with multiple periods, one could also approximate the variance. However, in any case, it is a well–known result that it is not possible to find an optimal contract in the one–period model, even without volatility control, as soon as the monotone likelihood ratio101010The monotone likelihood ratio is defined in this case by the ratio between the derivative of the considered process density with respect to the effort and the density itself. is not bounded from below, which is the case in [78] since the output processes are Gaussian. Indeed, Mirrlees (1999) [62] shows that, in this case, there is a sequence of contracts, called forcing contracts, that allows to obtain the results of the first–best case (when there is no moral hazard) at the limit, but that there is no optimal contract. Restricting oneself to linear contracts in the case of drift control only in the one–period model is justified because these are the optimal contracts in continuous time, but, unfortunately, this reasoning is no longer valid in the case of volatility control.

In conclusion, unlike the case of drift control only, in the case of volatility control it is not possible to consider the one–period model by limiting the study to linear contracts, and expect to obtain the same results as in continuous time. This result therefore justifies the full study of continuous–time models and the use of the recent theory of 2BSDEs, from a theoretical point of view. In the following, we will see through numerical results that it is obviously beneficial in a practical way for the principal to consider the problem in continuous time.

2.3.2 Numerical results

In [78, Theorem 2], Sung presents some interesting facts such as the decrease in the efforts of the manager and agents when the total number of workers increases, as well as their limits for an infinitely large company. These facts seem also be true in our framework, but we do not believe it is necessary to dwell on proving the same results. We find it more interesting to focus on the differences between the two models, and of course on the benefits of the approach being considered in this paper. In our opinion, the simplest way to achieve this goal is to present in this subsection some numerical simulations.

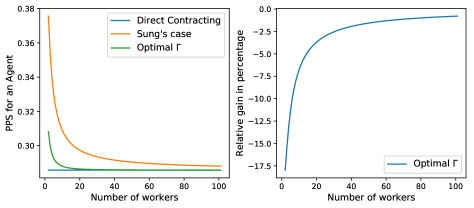

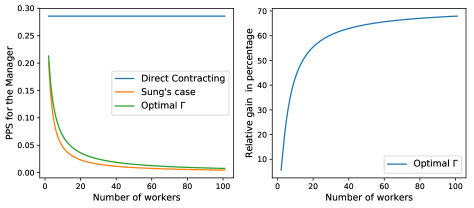

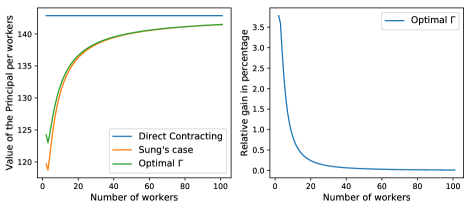

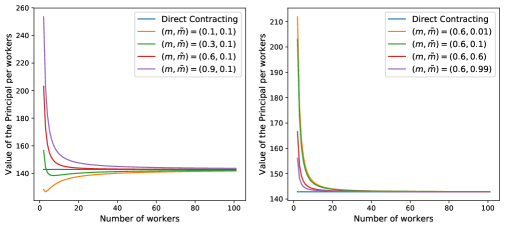

Therefore, to illustrate the benefits induced by considering contracts with the quadratic variation term, we decide to perform some numerical simulations based on the parameters chosen in [78, Section 5], in particular in the case of identical workers. More precisely, we let for all , , and , where . We thus represent in the left graphs of Figures 2, 3, LABEL: and 4, respectively the optimal pay–for–performance sensitivities for the agents, for the manager, as well as the value per workers for the principal, in three cases:

-

in the DC case (blue line), i.e., without any manager (see Lemma A.1 for theoretical results);

-

in the case of Sung’s (orange curve), i.e., when the manager’s contract is linear;

-

in our framework (green curve), i.e., when his contract is more sophisticated with an indexation on the quadratic variation.

All curves are represented with respect to the number of workers, starting from (i.e. ), to consider at least two agents in the DC case or one agent and one manager in the HC case. Pay–for–performance sensitivity (PPS for short) is a common proxy for the strength of incentives (see Gryglewicz, Hartman–Glaser, and Zheng (2020) [32]). In our framework, this sensitivity is directly related to the efforts of the workers. Indeed, for all , the –th agent’s optimal effort is given by , where is precisely the PPS for the –th agent’s contract. A similar relation stands for the manager. We could have similarly represented workers’ efforts, but we decide to use this indicator to simplify the comparison with the results of Sung given in [78, Table 1], although they have been recalculated in our case for different numbers of agents. On the right graphs of the three figures below, we represent the relative gain induced by considering sophisticated contracts versus linear ones.

Our results obviously present the same features as those outlined in [78]. Since the manager can subcontract with the agents, he can benefit, to some extent, from the results of agents’ efforts and transfers his own compensation risk to them. As a consequence, agents are induced to work harder than implied in the direct contracting case (see Figure 2, left). To counterbalance this undesirable risk–shifting motivation of the risk–averse manager, the principal set his contract sensitivity to a level lower than that of the contract in the DC case. Consequently, the manager makes less effort than what would be required in the direct contracting situation (see Figure 3, left). In addition, the larger the size of the company, the more motivated the manager is to shift the risk onto the agents. Consequently, the larger the number of workers, the lower–powered the managerial incentive contract. Sung concludes that the results obtained with this model on the low managerial effort can serve as an explanation of the empirical finding of Jensen and Murphy (1990) [41] that the average CEO contract sensitivity of large firms is lower than that of small firms.

Nevertheless, our sophisticated contracts allow an improvement of the results. More specifically, the PPSs we obtain, both for the manager and for the agents, are closer to the PPS in the DC case, compared to those obtained by Sung. More precisely, using a contract with the quadratic variation for the manager allows the principal to better monitor his own performance. This results in a higher PPS for the manager (see Figure 3, left), and therefore forces him to make more effort. The relative gain (Figure 3, right) is increasing with respect to the number of workers and reaches for example % for workers in the company ( agents in addition to the manager). The new contracts we consider therefore mitigates the undesirable risk–shifting motivation of the risk–averse manager. The manager still benefits from the results of agents’ efforts and transfers a part of his own compensation risk to them, but less than with linear contracts. Consequently, agents are still induced to work harder than implied in the DC case (see Figure 2, left), but less than in Sung’s framework.

Figure 4 (left) represents the value function of the principal per workers. With the sophisticated contracts, this value is obviously higher than with linear contracts, which confirms the interest of our study. Even if the relative gain seems small (see Figure 4, right), this result motivates a full study with even more sophisticated contracts, in the theoretical part of this paper (from Section 4 onwards). Indeed, even if this only leads to a small increase in the principal’s value per worker when the number of workers is large, the gain has to be multiplied by the number of workers. Moreover, when the number of workers is small, the gain is significant nonetheless, but above all it allows to reduce the effort gaps between the agents and the manager. It is interesting to consider the benefit of these contracts not only from the principal’s point of view, but also from a global managerial perspective. Indeed, by developing this type of contracts, the principal better monitors the manager’s efforts, and therefore regulates his risk–shifting motivation, which results in improved conditions for the agents and a better division of work and risk between the agents and the manager.

Remark 2.7.

One can notice that the principal’s profit per worker is not monotonous when the number of workers is small. In particular, her profit is higher when there are two workers instead of three, while it is then increasing with the number of workers. This is actually explained by the fact that when there is only one agent supervised by the manager, there is less loss of information when going up the hierarchy. Indeed, since the principal can estimate the quadratic variation of , given in this case by:

she has access (up to a sign) to the volatility control of the manager, i.e., the indexation parameter . Therefore, in this particular case, there is ’less’ moral hazard on volatility control, and we could expect that the model degenerates towards the first–best case regarding volatility control. This fact should at least partially explain the higher profit of the principal.

3 Explicit extensions of Sung’s model

In this section, we propose some basic extensions of Sung’s model developed in Section 2. The first possible extension is to add a coefficient of ability for the manager, allowing to highlight the interest for the principal to delegate the management of the agents. Indeed, a good manager should have a positive impact on the work of the agents below him, and improve the efficiency of the hierarchical organisation to the point that above a certain number of workers, it becomes more profitable to group them in a working team led by a manager. The second extension we propose is to consider a different reporting: the manager will report the sum of the cost and the sum of the outcomes, instead of only reporting the difference between the two sums (the benefits). We will see that more precise reporting will lead to a degeneracy of the model towards the direct contracting case. The last extension considers a more complicated hierarchy, with a top manager in–between the principal and the managers. In this case, we show that, although it is more complicated to obtain analytical results, the resolution tools remain the same and it is thus theoretically very simple to add a level in the hierarchy using our approach.

3.1 On the positive impact of hierarchical organisations

As we have seen in the previous numerical results, the hierarchical organisation considered in Sung’s model is not recommended compared to the direct contracting case. Indeed, the utility obtained by the principal, when she hires a manager, is smaller compared to the case when he contracts directly with all the workers. This decrease in utility is linked to the fact that the ’severity’ of moral hazard increases with the number of levels in the hierarchy, but, above all, because we do not model any specific ability of the manager. In reality, hierarchical structures appear for logistical reasons, since it would be complicated for a principal to supervise a large number of workers, but also because a manager should have more ability to manage a small group of workers than the owner (or the investors) of the firm. We therefore provide a simple extension to take into account the manager’s ability to improve the productivity of his workers.

We can say that the manager’s skills are defined by a pair where measures the help he provides to the agents under his supervision, and is a penalty suffered because of his management activities. Indeed, it seems natural to consider that, by helping the agents, the manager has less time for his own work. We consider that the manager’s skill and respectively affect the cost functions of the agents and the manager as follows

In the one hand, this means that the manager’s ability decreases the cost of effort of each agent under his supervision. However, the more agents he is responsible for, the weaker the effect is. On the other hand, the parameter increases its own cost, representing the fact that helping agents leaves him less time for his own work. In other words, devoting time to helping the agents penalises his own result. We obtain the same form of solutions as in the previous section, more precisely by replacing and respectively by

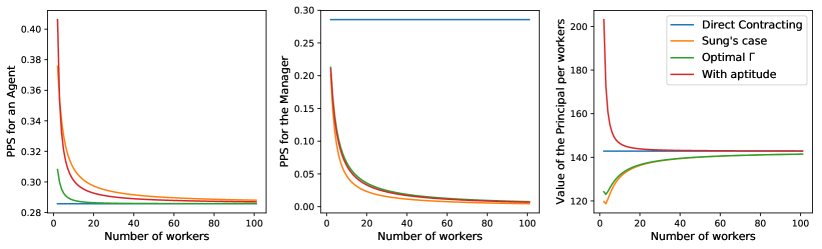

In order to evaluate the effects of the manager’s ability parameters, we present some numerical results, with identical workers and the same set of parameters as in the previous simulations (see parameters in Section 2.3.2).

In Figure 5, we represent, in addition to the previous results, the PPS for an agent (on the left), for the manager (in the middle), as well as the value of the principal (on the right) when we take into account the skills of the manager (red curves). Specifically, we set . We can see that the agents are incentivised to work more than without the help of their manager, but still less than in Sung’s framework. The results are the opposite for the manager. The key point to observe here is that the value of the principal is higher than in the DC case, which means that a hierarchical structure can be beneficial for the principal when the manager has an ability to supervise the agents.

Therefore, this modeling highlights the interest for the principal to delegate the management of the agents. As can be seen in Figure 6, if the manager has good management skills, i.e., large enough, it becomes more cost–effective for the principal to form a working team headed by a manager. The right graph of Figure 6 shows that the influence of the parameter is negligible, in the sense that if is large enough, then the value of the principal is higher than in the DC case regardless of the value of . This is in line with the previous results. Indeed, since under a hierarchical contracting, the manager works less than in the DC case, the fact that its cost is higher matters less, as long as his ability is sufficiently beneficent to the agents.

Remark 3.1.

We could consider another case where the manager’s skills and respectively affect the outcomes’ drift of the agents and the manager in the following way:

This basic extension finally leads to the same problem and solution as Sung’s model, only the utility of the principal is increased by (is decreased if . However, this model is not necessarily very realistic, because if the agents do not make any effort, the manager’s ability is sufficient to increase the outcomes. The previous model therefore seems more interesting, both in terms of interpretations and results.

3.2 On other types of reporting

Throughout Section 2, we have assumed that the manager reports only the net benefit to his supervisor, the principal. The goal of this subsection is to provide some interesting results on other types of reporting.

3.2.1 Reporting of profits and costs

Within the same hierarchical structure as before, we consider here that the manager reports to the principal the sum of the profits and the sum of the costs (and not only the net profit , i.e., the difference between the two values). Therefore his contract will be indexed on the following –dimensional state variable

Since the agents’ problem remain unchanged, the dynamic of under their optimal efforts is given by

We consider the same criterion for the manager as before. Following the reasoning behind Proposition 2.4, we are led to consider contracts similar to (2.9), but now indexed on the –dimensional variable :

| (3.1) |

where is the manager’s Hamiltonian, and is a tuple of parameters optimally chosen by the principal. We thus denote by the set of admissible control processes for the principal, defined as the collection of all processes , predictable with respect to the filtration generated by and satisfying appropriate integrability conditions, where

Given the dynamic of the state variable and its quadratic variation, we can compute the manager’s Hamiltonian and thus establish a result similar to Proposition 2.5.

Proposition 3.2.

Let . The optimal drift effort and the optimal control on the –th agent’s compensation, chosen by the manager, are respectively given by and , where

Under the probability associated to the optimal effort and controls of the manager (and the agents), the dynamics of and are respectively given by:

where .

The principal’s problem remains essentially unchanged compared to (2.6), she still maximises the difference between the sum of the outcomes and sum of the compensations owed to the manager and the agents. The only difference is the contract space on which she optimises her criterion. In particular, given the optimal form (3.1) of the contracts, her problem becomes:

To solve the previous optimisation problem, it is in fact equivalent to consider the following maximisation problem:

| (3.2) |

where is defined for all and by

| (3.3) |

Remark 3.3.

In this setting, we could also consider the case where the manager directly pays the agents he manages (not only designs their contracts). His value function is thus defined by:

and the optimal form of contract for the manager is as follows:

Since the manager is directly paying the agents, the problem of the principal is only to maximise the difference between the sum of the outcomes and the compensation due to the manager:

which leads to the exact same maximisation as before. Indeed, in this case, the compensation for the manager is equal to the sum of the compensations for the agents and the contract of the previous case:

and thus the two frameworks are strictly equivalent, since

The supremum given by (3.2) is not easily computable in the general case, but if all agents have the same characteristics, we obtain the following result, whose proof is postponed to Section A.2.

3.2.2 Separate reporting of the manager’s performance

For now, we focused our study on two frameworks, one where the manager reports only net benefits (Section 2), the other where he reports the sum of the total profit (sum of outcomes) and the total cost (sum of payments) separately (Section 3.2.1). We could consider other scenarii where the manager reports more information to the principal, for example if he reports his personal outcome separately. However, with this reporting, the HC case degenerates towards the DC case, in the sense that optimal efforts of the agents and the manager, as well as the value of the principal, can be equal to those in the DC case, given by Lemma A.1. The proof of the following proposition is postponed to Section A.2.

Proposition 3.5.

If the manager reports to the principal his own outcome separately, the problem degenerates towards the DC case. More precisely:

-

if the manager reports , it is possible to find a sequence of contracts such that, at the limit, all workers apply the optimal efforts of the DC case, and the principal receives the maximum utility possible, i.e., ;

-

if the manager reports , the result of holds and moreover, if agents are identical, we can find a contract which allows to attain the DC case.

Since these reporting leads to a degeneration towards the DC case, they are less interesting mathematically speaking. However, from a managerial point of view, it is relevant to observe that reporting the manager’s output separately makes it possible to reduce the moral hazard within the hierarchy.

3.3 On a more complex hierarchy

We consider in this section a more complex hierarchy illustrated by Figure 7: the principal hires a top manager, who hires managers, and each manager hires agents. This new hierarchy requires small adjustments in notations, which will be reused in the general model. First, the top manager controls his own outcome and receives the compensation designed by the principal. Then, the managers, indexed by , each carry out their own outcome and receive the compensation designed by the top manager. For and , the –th agent is the –th agent of the –th manager. He controls the output and will receive the compensation designed by his manager. The dynamics of the output processes are given by

for all and , where and all are independent Brownian motions.

Agent’s problem. Apart from these notation changes, the problem for the agents remains the same. Therefore, for and , the optimal contract form for the –th agent is similar to (2.7):

where is an –valued process, predictable with respect to the filtration generated by , satisfying appropriate integrability conditions, chosen by the –th manager. This contract leads to the optimal effort .

Manager’s problem. Let . The problem of the –th manager is also equivalent to the manager’s problem in Sung’s model. In addition to choosing his effort , he designs the compensation for the –th agent under his supervision by choosing the payment rate , for , and receives the payment offered by his supervisor (the top manager). We assume that the –th manager only reports in continuous time to his supervisor the total benefit of his working team, i.e., the following variable

Under optimal efforts of the agents, and using the notation , the dynamic of is given by

We assume that the contract for each manager is indexed on the total benefit of his working team, i.e., each contract is a measurable function of only. Given the form of his value function, is the only state variable of the –th manager’s control problem. Since he controls both the drift and the volatility of , the optimal form of contract is given by:

| (3.4) |

where is his Hamiltonian and is a pair of parameters optimally chosen by the top manager. More precisely, we define by the collection of all processes , predictable with respect to the filtration generated by and satisfying appropriate integrability conditions, where

The set thus represents the admissible control processes for the top manager. By computing and maximising the –th manager’s Hamiltonian, we obtain the following proposition.

Proposition 3.6.

Let consider a contract of the form (3.4) indexed by a pair . Then, for all , the optimal effort on the drift of the –th manager’s outcome is , and for all , his optimal control on the –th agent’s compensation is where

Remark 3.7.

The problem highlighted in Remark 2.3 obviously also arises here. Indeed, to restrict the contract for the –th agent to a measurable function of , the payment process must be predictable with respect to the filtration generated by . Similarly, to restrict the contract for the –th manager to a measurable function of , the payment rate processes and must be predictable with respect to the filtration generated by . Since the optimal payment rate is a function of and , the model is consistent if and only if and are deterministic functions of time only, which is actually the case in this example (they are even constant).

Top manager’s problem. The top manager carries out his own output , by choosing his effort level , and designs the contracts for the managers. Like other managers, he has a CARA utility function with a risk–aversion parameter , and maximises the utility of the difference between the payment he receives from the principal, , and his cost of effort:

where is the probability associated to the effort and the choice of the process , under the optimal efforts of the managers and their agents. In this setting, the top manager observes in continuous time the net benefit of each working team led by a manager, that is the tuple . Moreover, like every managers, the top manager reports in continuous time to the principal the benefits of his team of workers composed of all managers and agents below him, namely the following variable:

Therefore the principal can only offer to the top manager a contract indexed on , and, since he controls the volatility of through his choice of contracts for the managers, the optimal form of his compensation is the same as (3.4) but indexed on the variable :

where is a pair of processes optimally chosen by the principal. More precisely, we define by the collection of all processes , predictable with respect to the filtration generated by and satisfying appropriate integrability conditions, where is the set of all such that the top manager’s Hamiltonian defined below by (3.3) is well defined.

Under optimal efforts and controls of the managers and the agents (and associated probability ), the dynamic of is given for all by:

where, for all , and in addition for all ,

| (3.5) |

Therefore, the top manager’s Hamiltonian is defined as follows:

| (3.6) |

The first supremum is attained for the optimal effort for . In addition, the optimal control of the top manager for the managers’ contracts are given for all and all by and , for

where can be numerically computed as the maximiser of the previous Hamiltonian , for all . Abusing notations slightly for simplicity, we will denote in the following, for all ,

| (3.7) |

Remark 3.8.

In addition to the measurability issues of the manager’s control, mentioned in Remark 3.7, we also have, in this more complex model, a measurability problem for the top manager’s control. Indeed, since we restrict the space of the contracts for the –th manager to measurable contracts with respect to his own , the processes and defining the contract must be adapted to the filtration generated by . In fact, these processes, chosen by the top manager, are functions of and , the principal’s controls. Since the principal only observes , the processes and should be adapted to the filtration generated by , contradicting the fact that and are adapted to the filtration generated by . Again, this question of measurability is actually not a problem in this particular case since all optimal controls are deterministic or even constant, but will be in a more general framework.

Principal’s problem. We consider the same problem for the principal as before, namely that she maximises the difference between the sum of the outcomes and the sum of the costs at terminal time , which can be summarised by . Her problem is reduced to the optimal choice of the indexation parameters in the contract , the pair , and thus to the following maximisation problem:

where and using the notations defined by (3.7). Optimal parameters are constant over time, and their values can be obtained thanks to a simple numerical optimisation.

By comparing to the first example where there is no top manager and only one manager, we can see that the structure of the problem is the same. Adding a level in the hierarchy is no more complicated, all it takes is writing an additional control problem. With this in mind, and in order to avoid overloading the notations, we will consider only three levels in the hierarchy for the general model, i.e., one principal, managers, with a fixed number of agents each.

4 The general model: preliminaries

For the general model, we focus on the following hierarchy, represented in Figure 8: the principal contracts with managers, and each manager for in turn subcontracts with agents, indexed by for . The –th agent is therefore the –th agent of the –th manager. The term workers will refer to the actors in the hierarchy who are in charge of managing a project, i.e., both agents and managers. The total number of workers is given by . Fix throughout the general model a positive integer , which represents the dimension of the noise which affects each project.111111We assume here that does not depend on a specific agent. This is without loss of generality, as we can always add unused coordinates to a given project. The –th agent will manage the project with output , while the –th manager is in charge of the project with output . We assume here for simplicity that the outputs are one–dimensional121212We could consider that each output is –dimensional for . In this case, each coordinate of can be interpreted as the profit generated by a task managed by the –th worker. Nevertheless, at some point we would be led to consider the total profit generated by a worker, which will naturally corresponds to the sum of the coordinates of his output. Therefore, to simplify, we choose to directly consider each output as the total profit generated by the –th worker, and thus avoid increasing the notations by considering –dimensional vectors and finally taking their inner product with . and uncorrelated, meaning that tasks to be performed have been clearly separated. Moreover, each worker in the hierarchy can only impact directly his own project. This set up can be justified by the fact that each worker have a specific set of skills, implying that they are the only ones able to perform their tasks. In fact, we could let them interact, but this would make the Nash equilibrium hard to solve. In addition, interactions between workers will naturally occur at the level of managers, and therefore a way to handle this issue will be explained at that time. The most important aspect that we wish to address in this paper is the loss of information by moving up the hierarchy. To model this, we assume that each manager only reports the results of his team to the principal through a (possibly multidimensional) variable , as in Sung’s model detailed in the previous sections. Thus, the principal does not have a separate access to the results of each worker, which could lead to a degeneracy of the problem towards the DC case, as we have seen in particular in Section 3.2.2.

Additional notations

Recall that denotes some maturity fixed in the contract, and that for any positive integer , denotes the set of continuous functions from to . We will denote by the set of bounded twice continuously differentiable functions from to , whose first and second derivatives are also bounded. For a probability space of the form and an associated filtration , we will have to consider processes , taking values in some Polish space , which are –optional, i.e., –measurable where is the so-called optional –field generated by –adapted right–continuous processes. In particular, such a process is non–anticipative in the sense that , for all and .

For , and for some set , we will make use of the following notations for vectors:

| (4.1) |

and their corresponding sets:

| (4.2) |

In a similar way, we also define

-

•

, the vector obtained by suppressing the elements of ;

-

•

, the vector obtained by suppressing the element of ;

-

•

and .

We will also use the following notations for sums:

| (4.3) |

4.1 Theoretical formulation for the workers

Fix throughout this section and , to consider all the workers, i.e., both the agents and the managers. Each worker takes care of his own task by choosing a pair , where and are respectively – and –valued, for some subsets and of Polish spaces. More specifically, and represent the effort of the worker to impact respectively the expected value and the variability of his outcome.131313If the outcome represents the value added by the –th worker, then naturally represents an effort to increase the average and an effort to decrease the volatility. However, in more general terms, the outcome may represent different measures of a worker’s performance, and it is therefore possible that the worker may need to decrease the average of the outcome or increase its volatility. In addition, we will consider the following functions, assumed to be bounded:

More precisely, the scalar product between the two functions will represent the drift of the outcome of the –th worker, while will represent its volatility. We will denote for simplicity , as well as the Cartesian product of the sets , following the notations defined by (4.2). To easily write the dynamic of the column vector composed by the collection of all the , we define by and the functions that will correspond respectively to the drift and the volatility of the process . These functions and will be defined for all and respectively by:

| (4.4) |

in the sense that is a column vector composed by the collection of all the scalar product , meaning that , and

| (4.5) |

where symbolises direct sum141414The symbol denote for direct sum of matrices, which is defined for two matrix and by: of matrices (vectors in this case). To be consistent with the weak formulation of control problems, we need to define the canonical space for the workers. Nevertheless, before that, we should discuss about what should be observed by the agents and their managers.

4.1.1 Intuition

According to the intuitions developed in Remarks 2.3 and 3.8, we cannot assume that the –th agent only observes his own output , since his contract cannot be restricted to a measurable function of this output. Indeed, in the general case, the parameters and chosen by his manager and indexing the contract on his output would not be a priori deterministic functions of time. Moreover, if we restrict the payment rates and for the –th agent to be adapted only to the filtration generated by , the principal, who does not observe , will not be able to compute the –th manager’s Hamiltonian. In fact, to better understand this measurability problem, we have to approach it from the top of the hierarchy.

We want to study a case of loss of information by proceeding up the hierarchy, modelled by the fact that each manager reports only the variable to the principal, representing the performance of his work team. Indeed, if we consider for example that the principal represents the company’s shareholders as in [78], it is logical to assume that she is not aware of the precise results of each team led by a manager, and that she is probably only interested in the profits and costs, or even the net profits/benefit of each team, represented by the vector . This assumption is particularly relevant if we consider, for example, that each team is a department of the company (or a subsidiary of the parent company), and that shareholders can only compare the benefits of the different departments to optimise their investments and the importance given to each department.

Therefore, the principal only observes the collection of the , for . Under some restrictive conditions151515These conditions could be that the principal’s problem is separable in each , with independent and independently controlled by each manager. To illustrate a separable problem for the principal, one can consider Sung’s model developed in Section 2 and adding other working teams, led by managers, also reporting the net benefit of their working team to the principal. In this case, if each manager controls only his own and if all are independent, since the net benefit is just a difference of sums, and the principal is risk–neutral, her problem is completely separable in each ., she may offer a contract for the –th manager which only depends on the result of his working team. However, more generally, her controls would be adapted to any information available to her, i.e., the filtration generated by , and therefore it makes little sense to restrict the space of contracts for the –th manager to measurable functions of . We are thus led to study a more general space of contracts for the managers, measurable with respect to the filtration generated by .